Embed Size (px)

Citation preview

1 Public Public May 2015 X

1Q15 Earnings Presentation

May 15, 2015

Public

2

Forward Looking Statements

This presentation may contain certain statements that express the management’s expectations, beliefs and assumptions about future events or results. Such statements are not historical fact, being based on currently available competitive, financial and economic data, and on current projections about the industries BM&FBOVESPA works in.

The verbs “anticipate,” “believe,” “estimate,” “expect,” “forecast,” “plan,” “predict,” “project,” “target” and other similar verbs are intended to identify these forward-looking statements, which involve risks and uncertainties that could cause actual results to differ materially from those projected in this presentation and do not guarantee any future BM&FBOVESPA performance.

The factors that might affect performance include, but are not limited to: (i) market acceptance of BM&FBOVESPA services; (ii) volatility related to (a) the Brazilian economy and securities markets and (b) the highly-competitive industries BM&FBOVESPA operates in; (iii) changes in (a) domestic and foreign legislation and taxation and (b) government policies related to the financial and securities markets; (iv) increasing competition from new entrants to the Brazilian markets; (v) ability to keep up with rapid changes in technological environment, including the implementation of enhanced functionality demanded by BM&FBOVESPA customers; (vi) ability to maintain an ongoing process for introducing competitive new products and services, while maintaining the competitiveness of existing ones; (vii) ability to attract new customers in domestic and foreign jurisdictions; (viii) ability to expand the offer of BM&FBOVESPA products in foreign jurisdictions.

All forward-looking statements in this presentation are based on information and data available as of the date they were made, and BM&FBOVESPA undertakes no obligation to update them in light of new information or future development.

This presentation does not constitute an offer to sell or the solicitation of an offer to buy any securities, nor shall there be any sale of securities where such offer or sale would be unlawful prior to registration or qualification under the securities law. No offering shall be made except by means of a prospectus meeting the requirements of the Brazilian Securities Commission CVM Instruction 400 of 2003, as amended.

3

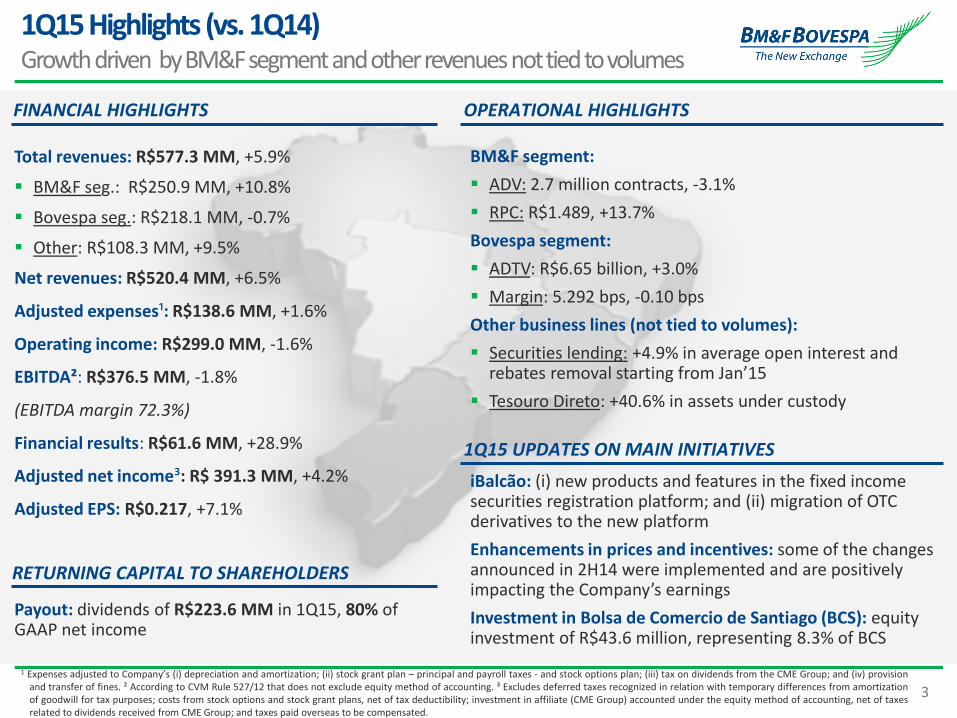

1Q15 Highlights (vs. 1Q14) Growth driven by BM&F segment and other revenues not tied to volumes

FINANCIAL HIGHLIGHTS OPERATIONAL HIGHLIGHTS

Total revenues: R$577.3 MM, +5.9%

BM&F seg.: R$250.9 MM, +10.8%

Bovespa seg.: R$218.1 MM, -0.7%

Other: R$108.3 MM, +9.5%

Net revenues: R$520.4 MM, +6.5%

Adjusted expenses¹: R$138.6 MM, +1.6%

Operating income: R$299.0 MM, -1.6%

EBITDA²: R$376.5 MM, -1.8%

(EBITDA margin 72.3%)

Financial results: R$61.6 MM, +28.9%

Adjusted net income³: R$ 391.3 MM, +4.2%

Adjusted EPS: R$0.217, +7.1%

Payout: dividends of R$223.6 MM in 1Q15, 80% of GAAP net income

RETURNING CAPITAL TO SHAREHOLDERS

BM&F segment:

ADV: 2.7 million contracts, -3.1%

RPC: R$1.489, +13.7%

Bovespa segment:

ADTV: R$6.65 billion, +3.0%

Margin: 5.292 bps, -0.10 bps

Other business lines (not tied to volumes):

Securities lending: +4.9% in average open interest and rebates removal starting from Jan’15

Tesouro Direto: +40.6% in assets under custody

1Q15 UPDATES ON MAIN INITIATIVES

iBalcão: (i) new products and features in the fixed income securities registration platform; and (ii) migration of OTC derivatives to the new platform

Enhancements in prices and incentives: some of the changes announced in 2H14 were implemented and are positively impacting the Company’s earnings

Investment in Bolsa de Comercio de Santiago (BCS): equity investment of R$43.6 million, representing 8.3% of BCS

1 Expenses adjusted to Company’s (i) depreciation and amortization; (ii) stock grant plan – principal and payroll taxes - and stock options plan; (iii) tax on dividends from the CME Group; and (iv) provision and transfer of fines. ² According to CVM Rule 527/12 that does not exclude equity method of accounting. ³ Excludes deferred taxes recognized in relation with temporary differences from amortization of goodwill for tax purposes; costs from stock options and stock grant plans, net of tax deductibility; investment in affiliate (CME Group) accounted under the equity method of accounting, net of taxes related to dividends received from CME Group; and taxes paid overseas to be compensated.

4

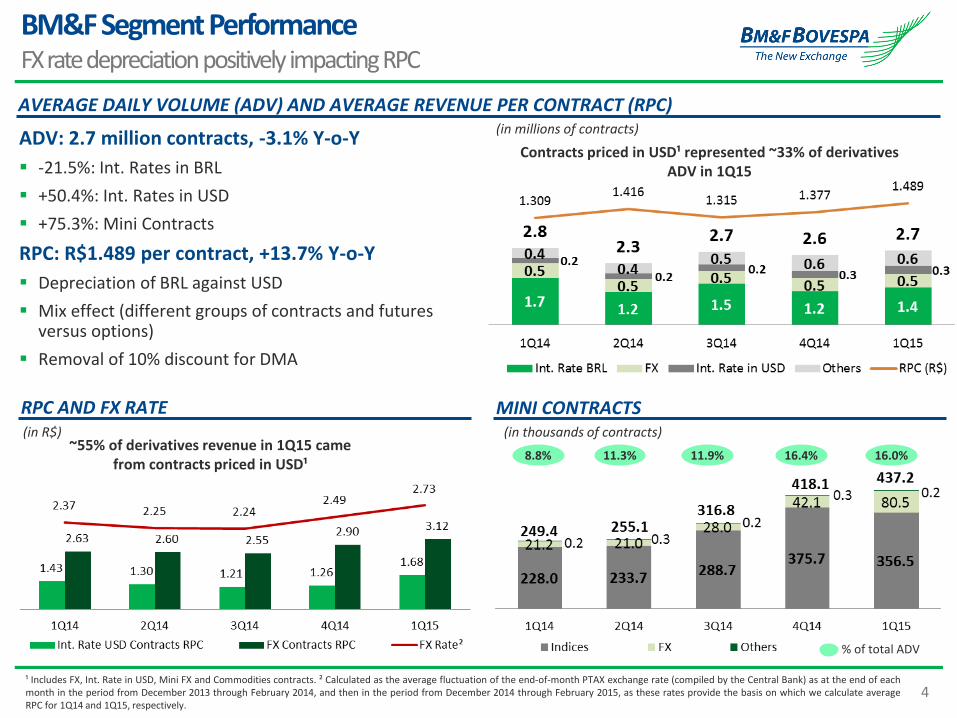

BM&F Segment Performance FX rate depreciation positively impacting RPC

ADV: 2.7 million contracts, -3.1% Y-o-Y

-21.5%: Int. Rates in BRL

+50.4%: Int. Rates in USD

+75.3%: Mini Contracts

RPC: R$1.489 per contract, +13.7% Y-o-Y

Depreciation of BRL against USD

Mix effect (different groups of contracts and futures versus options)

Removal of 10% discount for DMA

AVERAGE DAILY VOLUME (ADV) AND AVERAGE REVENUE PER CONTRACT (RPC)

MINI CONTRACTS

(in millions of contracts)

RPC AND FX RATE (in R$)

~55% of derivatives revenue in 1Q15 came from contracts priced in USD¹

¹ Includes FX, Int. Rate in USD, Mini FX and Commodities contracts. ² Calculated as the average fluctuation of the end-of-month PTAX exchange rate (compiled by the Central Bank) as at the end of each month in the period from December 2013 through February 2014, and then in the period from December 2014 through February 2015, as these rates provide the basis on which we calculate average RPC for 1Q14 and 1Q15, respectively.

Contracts priced in USD¹ represented ~33% of derivatives ADV in 1Q15

(in thousands of contracts)

% of total ADV

11.3% 11.9% 16.4% 16.0% 8.8%

5

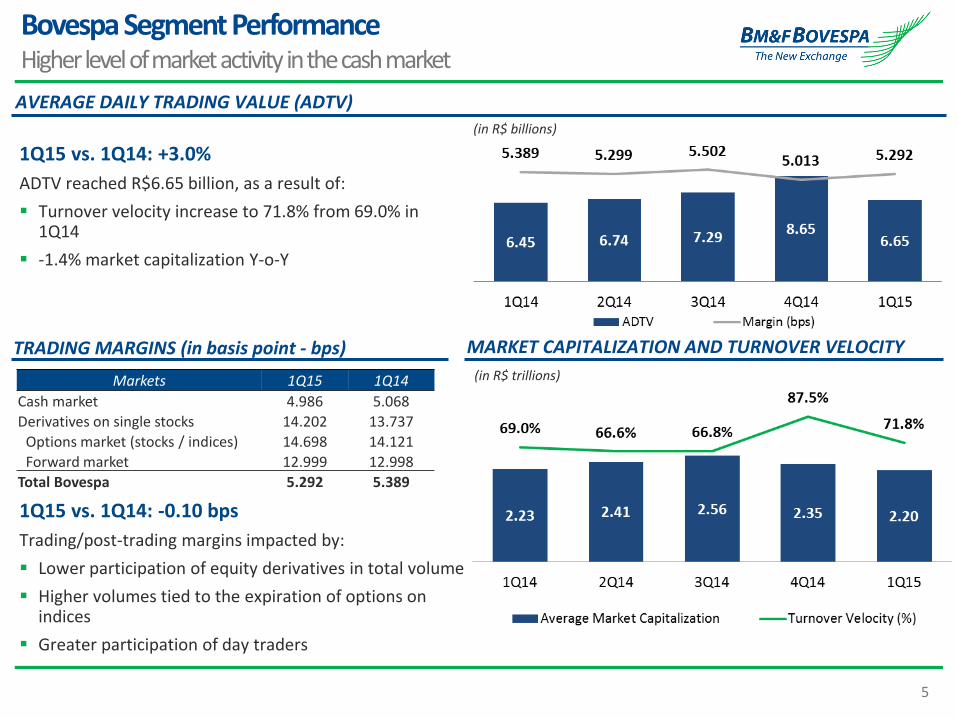

Bovespa Segment Performance Higher level of market activity in the cash market

1Q15 vs. 1Q14: +3.0%

ADTV reached R$6.65 billion, as a result of:

Turnover velocity increase to 71.8% from 69.0% in 1Q14

-1.4% market capitalization Y-o-Y

AVERAGE DAILY TRADING VALUE (ADTV)

MARKET CAPITALIZATION AND TURNOVER VELOCITY TRADING MARGINS (in basis point - bps)

Markets 1Q15 1Q14

Cash market 4.986 5.068

Derivatives on single stocks 14.202 13.737

Options market (stocks / indices) 14.698 14.121

Forward market 12.999 12.998

Total Bovespa 5.292 5.389

1Q15 vs. 1Q14: -0.10 bps

Trading/post-trading margins impacted by:

Lower participation of equity derivatives in total volume

Higher volumes tied to the expiration of options on indices

Greater participation of day traders

(in R$ billions)

(in R$ trillions)

6

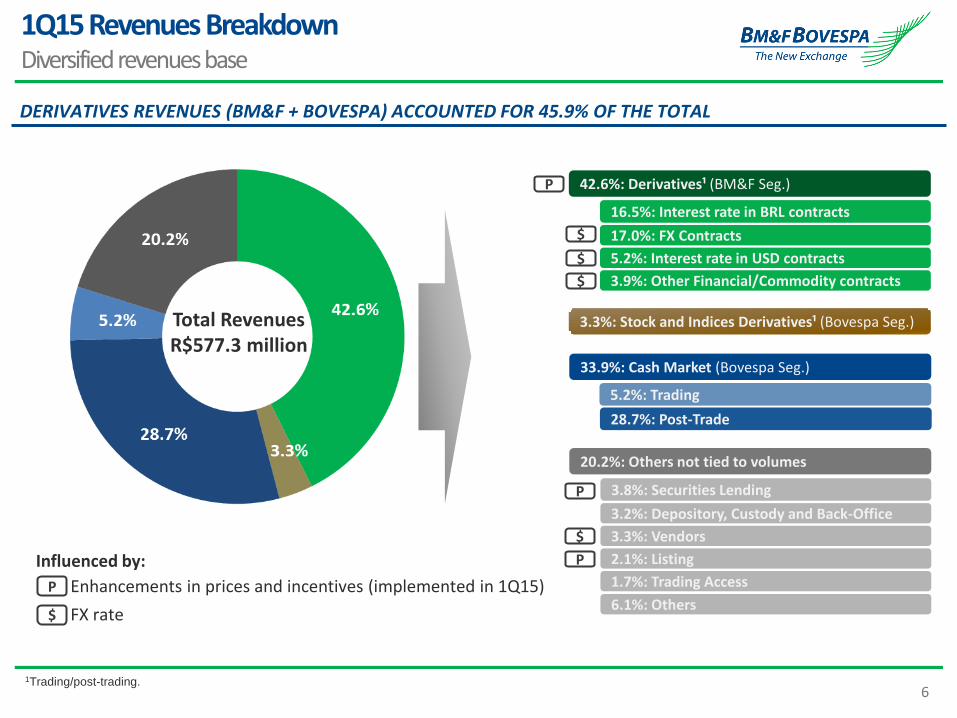

1Q15 Revenues Breakdown Diversified revenues base

42.6%: Derivatives¹ (BM&F Seg.)

Total Revenues R$577.3 million

3.8%: Securities Lending

3.2%: Depository, Custody and Back-Office

3.3%: Vendors

2.1%: Listing

1.7%: Trading Access

20.2%: Others not tied to volumes

DERIVATIVES REVENUES (BM&F + BOVESPA) ACCOUNTED FOR 45.9% OF THE TOTAL

16.5%: Interest rate in BRL contracts

17.0%: FX Contracts

5.2%: Interest rate in USD contracts

3.9%: Other Financial/Commodity contracts

1Trading/post-trading.

Enhancements in prices and incentives (implemented in 1Q15)

FX rate

P

$

$

P

P

$

P

$

$

Influenced by:

6.1%: Others

33.9%: Cash Market (Bovespa Seg.)

5.2%: Trading

28.7%: Post-Trade

3.3%: Stock and Indices Derivatives¹ (Bovespa Seg.)

7

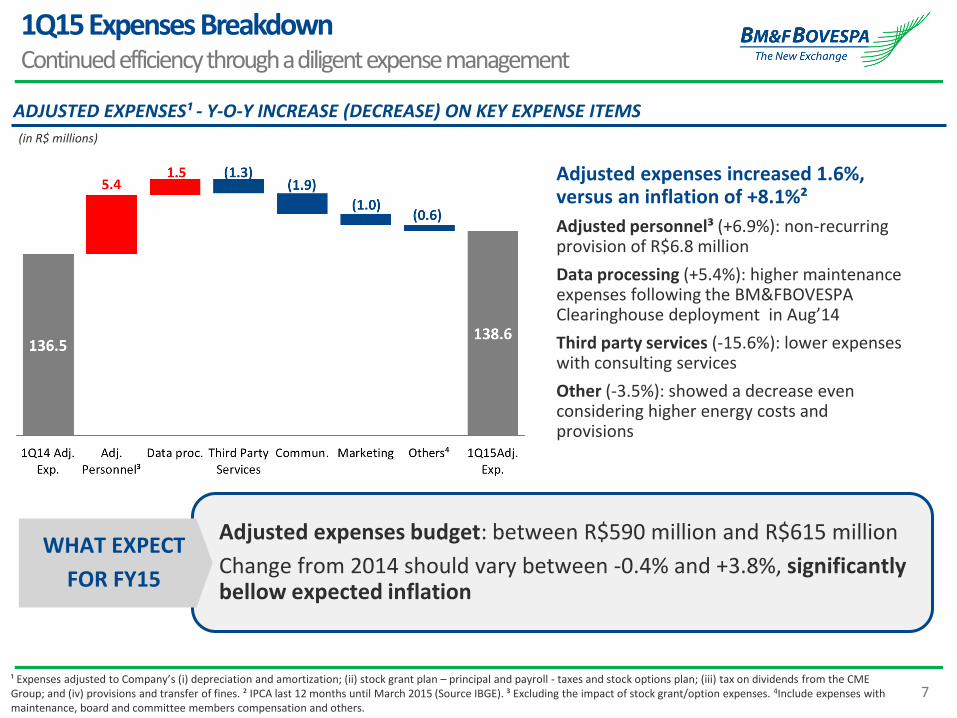

1Q15 Expenses Breakdown Continued efficiency through a diligent expense management

Adjusted expenses increased 1.6%, versus an inflation of +8.1%²

Adjusted personnel³ (+6.9%): non-recurring provision of R$6.8 million

Data processing (+5.4%): higher maintenance expenses following the BM&FBOVESPA Clearinghouse deployment in Aug’14

Third party services (-15.6%): lower expenses with consulting services

Other (-3.5%): showed a decrease even considering higher energy costs and provisions

ADJUSTED EXPENSES¹ - Y-O-Y INCREASE (DECREASE) ON KEY EXPENSE ITEMS

(in R$ millions)

¹ Expenses adjusted to Company’s (i) depreciation and amortization; (ii) stock grant plan – principal and payroll - taxes and stock options plan; (iii) tax on dividends from the CME Group; and (iv) provisions and transfer of fines. ² IPCA last 12 months until March 2015 (Source IBGE). ³ Excluding the impact of stock grant/option expenses. 4Include expenses with maintenance, board and committee members compensation and others.

Adjusted expenses budget: between R$590 million and R$615 million

Change from 2014 should vary between -0.4% and +3.8%, significantly bellow expected inflation

WHAT EXPECT

FOR FY15

8

Long-term Incentive Plan Based on Stock Grants Impacts of changes in the long-term incentive plans

Income Statement (consolidated) in R$ millions

Net revenues -

Expenses (18.3)

Personnel (18.3)

Stock grant – principal amount (9.9)

Stock grant – payroll taxes (8.4)

Operating income (18.3)

Equity on income of investees -

Financial results -

Earnings before taxes (18.3)

Income tax and social contribution 6.2

Net income (12.1)

Impacts on the income statement

Transition impacts (from stock options to stock grants)

R$25.0 million non-recurring expense related to payroll taxes from the transition (not considered on the table), as announced in the Notice to the Market released on February 4, 2015.

AS OF 1Q15 BM&FBOVESPA STARTED TO RECORD EXPENSES RELATED TO STOCK GRANTS¹

¹ There will be a small residual amount of stock options plans outstanding. In 1Q15, expenses related to that represented only 0.05% of the personnel line. ² For each stock grant program, a minimum total term of 3 years from the stock grant date and the last date for transfer shall be respected. Moreover, a minimum waiting period of 12 months shall be respected (i) between the stock grant date and the first transfer date and (ii) between each of the lots of shares, after the first transfer.

Principal amount Payroll taxes

Basis for calculation # of shares granted # of shares granted x 60.3%

Price reference Share price on the grant

date Share price on the transfer

date

Impacted by BVMF3 market price variation (volatility on expenses)

No Yes

Accounting accrual Pro-rata for vesting period Pro-rata for vesting period

Form of payment Shares Cash

Time of payment Share transfer date² Share transfer date²

Tax deductible Yes Yes

Impacts on the Income Statement Overview of the stock grant plan

9

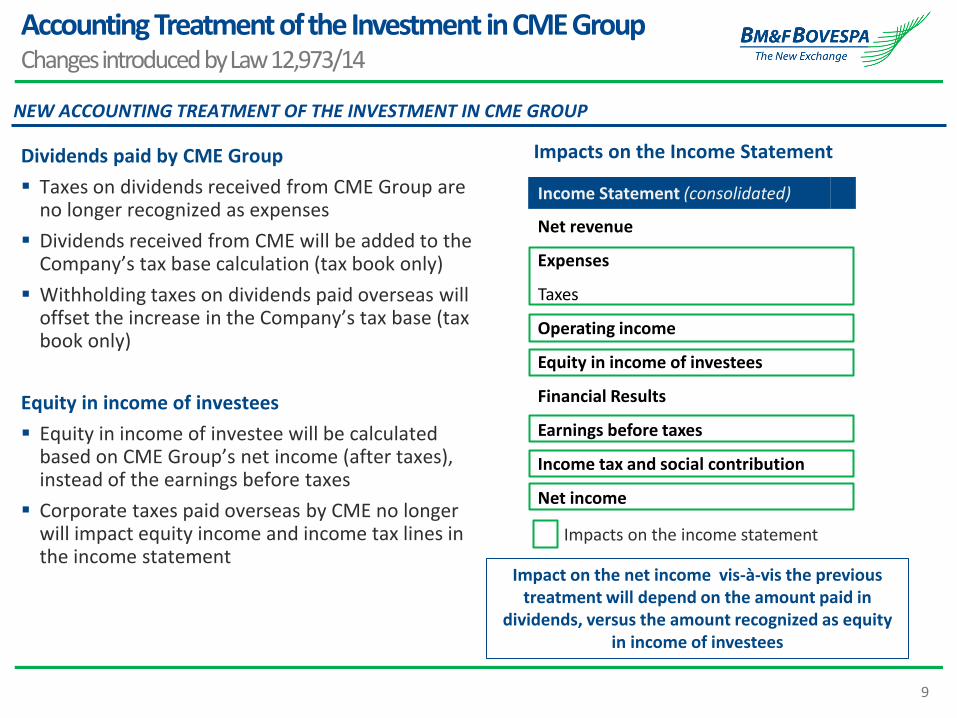

Accounting Treatment of the Investment in CME Group Changes introduced by Law 12,973/14

NEW ACCOUNTING TREATMENT OF THE INVESTMENT IN CME GROUP

Income Statement (consolidated)

Net revenue

Expenses

Taxes

Operating income

Equity in income of investees

Financial Results

Earnings before taxes

Income tax and social contribution

Net income

Impacts on the income statement

Dividends paid by CME Group

Taxes on dividends received from CME Group are no longer recognized as expenses

Dividends received from CME will be added to the Company’s tax base calculation (tax book only)

Withholding taxes on dividends paid overseas will offset the increase in the Company’s tax base (tax book only)

Equity in income of investees

Equity in income of investee will be calculated based on CME Group’s net income (after taxes), instead of the earnings before taxes

Corporate taxes paid overseas by CME no longer will impact equity income and income tax lines in the income statement

Impact on the net income vis-à-vis the previous treatment will depend on the amount paid in

dividends, versus the amount recognized as equity in income of investees

Impacts on the Income Statement

10

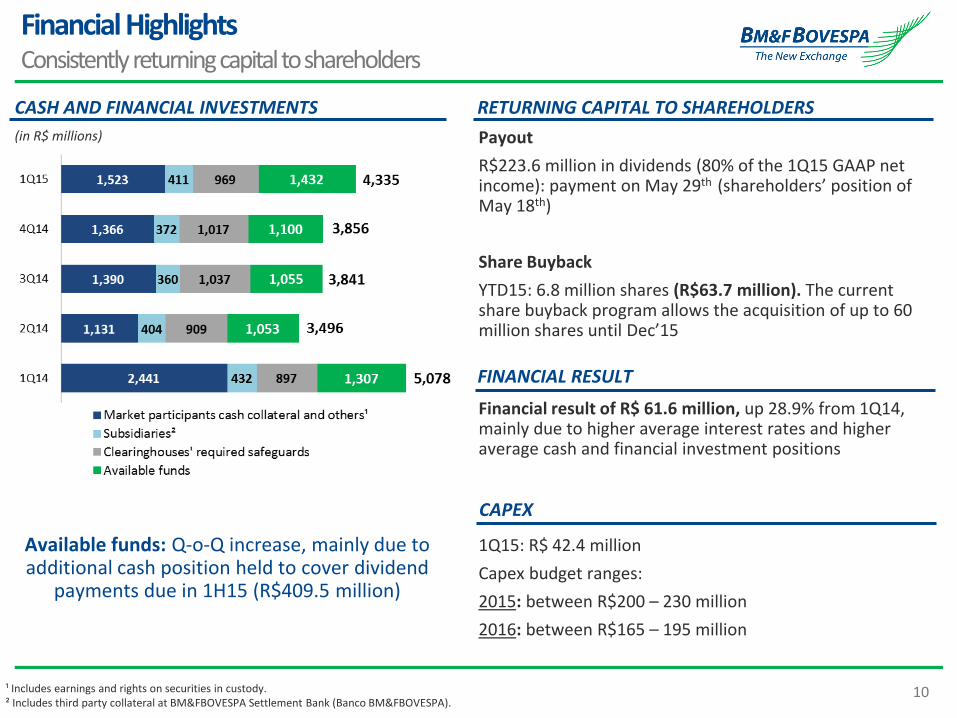

Financial Highlights Consistently returning capital to shareholders

1Q15: R$ 42.4 million

Capex budget ranges:

2015: between R$200 – 230 million

2016: between R$165 – 195 million

Payout

R$223.6 million in dividends (80% of the 1Q15 GAAP net income): payment on May 29th (shareholders’ position of May 18th)

Share Buyback

YTD15: 6.8 million shares (R$63.7 million). The current share buyback program allows the acquisition of up to 60 million shares until Dec’15

FINANCIAL RESULT

CAPEX

RETURNING CAPITAL TO SHAREHOLDERS

Financial result of R$ 61.6 million, up 28.9% from 1Q14, mainly due to higher average interest rates and higher average cash and financial investment positions

CASH AND FINANCIAL INVESTMENTS

Available funds: Q-o-Q increase, mainly due to additional cash position held to cover dividend

payments due in 1H15 (R$409.5 million)

¹ Includes earnings and rights on securities in custody. ² Includes third party collateral at BM&FBOVESPA Settlement Bank (Banco BM&FBOVESPA).

(in R$ millions)

11

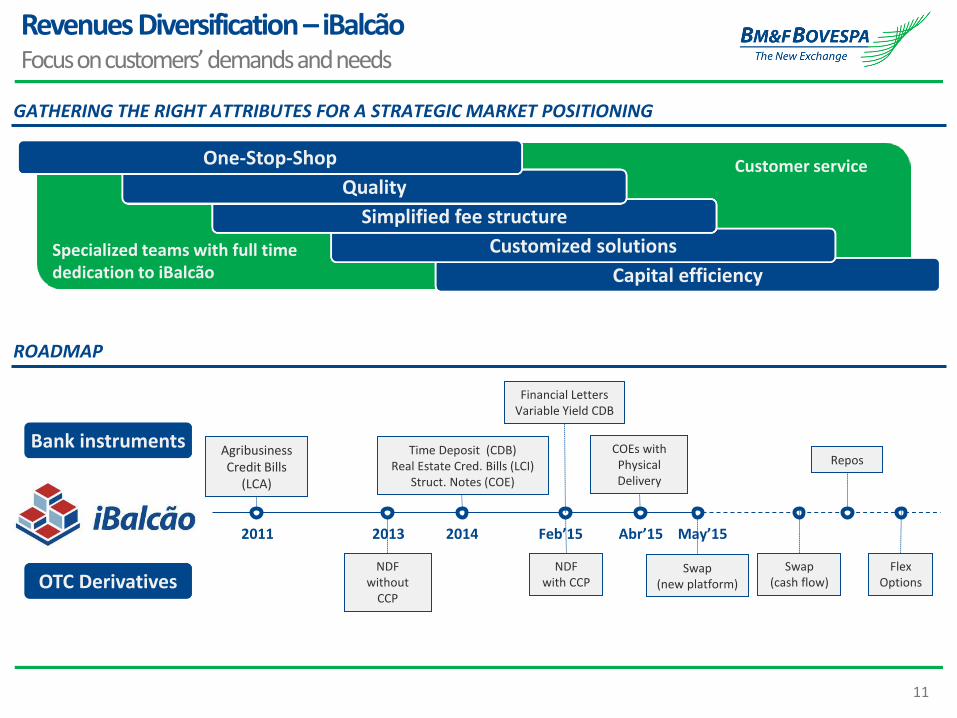

Revenues Diversification – iBalcão Focus on customers’ demands and needs

ROADMAP

Capital efficiency

Customized solutions

Simplified fee structure

Quality

One-Stop-Shop Customer service

Specialized teams with full time dedication to iBalcão

GATHERING THE RIGHT ATTRIBUTES FOR A STRATEGIC MARKET POSITIONING

Bank instruments

OTC Derivatives NDF

with CCP NDF

without CCP

Financial Letters Variable Yield CDB

Repos

Swap (new platform)

Swap (cash flow)

Flex Options

COEs with Physical Delivery

Agribusiness Credit Bills

(LCA)

2013 2014 Feb’15 Abr’15 2011

Time Deposit (CDB) Real Estate Cred. Bills (LCI)

Struct. Notes (COE)

May’15

12

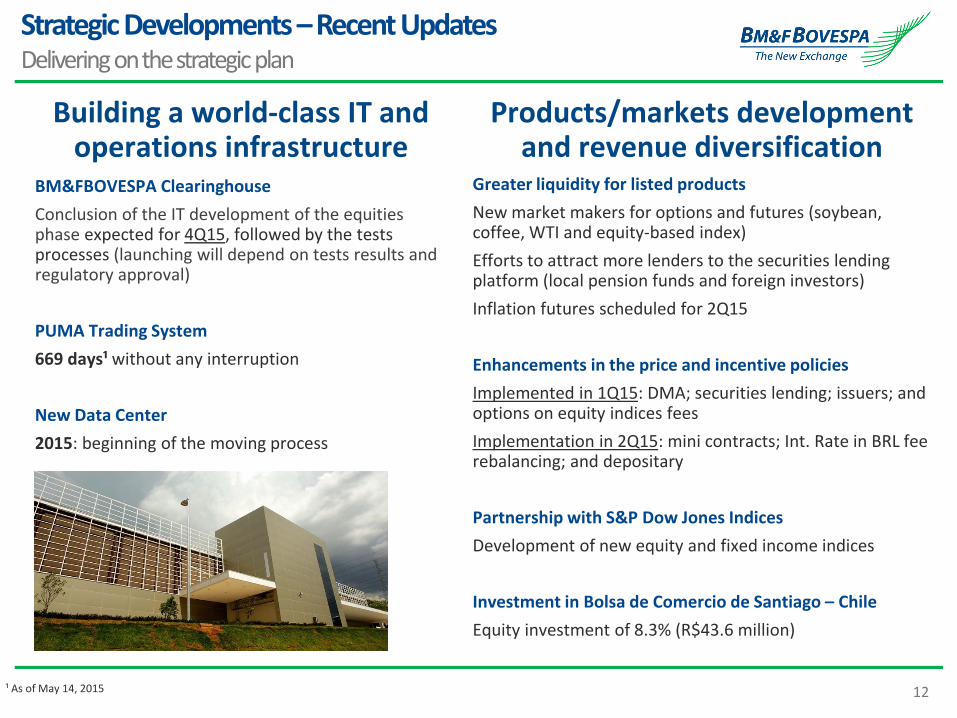

Strategic Developments – Recent Updates Delivering on the strategic plan

Building a world-class IT and operations infrastructure

BM&FBOVESPA Clearinghouse

Conclusion of the IT development of the equities phase expected for 4Q15, followed by the tests processes (launching will depend on tests results and regulatory approval)

PUMA Trading System

669 days¹ without any interruption

New Data Center

2015: beginning of the moving process

Greater liquidity for listed products

New market makers for options and futures (soybean, coffee, WTI and equity-based index)

Efforts to attract more lenders to the securities lending platform (local pension funds and foreign investors)

Inflation futures scheduled for 2Q15

Enhancements in the price and incentive policies

Implemented in 1Q15: DMA; securities lending; issuers; and options on equity indices fees

Implementation in 2Q15: mini contracts; Int. Rate in BRL fee rebalancing; and depositary

Partnership with S&P Dow Jones Indices

Development of new equity and fixed income indices

Investment in Bolsa de Comercio de Santiago – Chile

Equity investment of 8.3% (R$43.6 million)

Products/markets development and revenue diversification

¹ As of May 14, 2015

13

APPENDIX

14

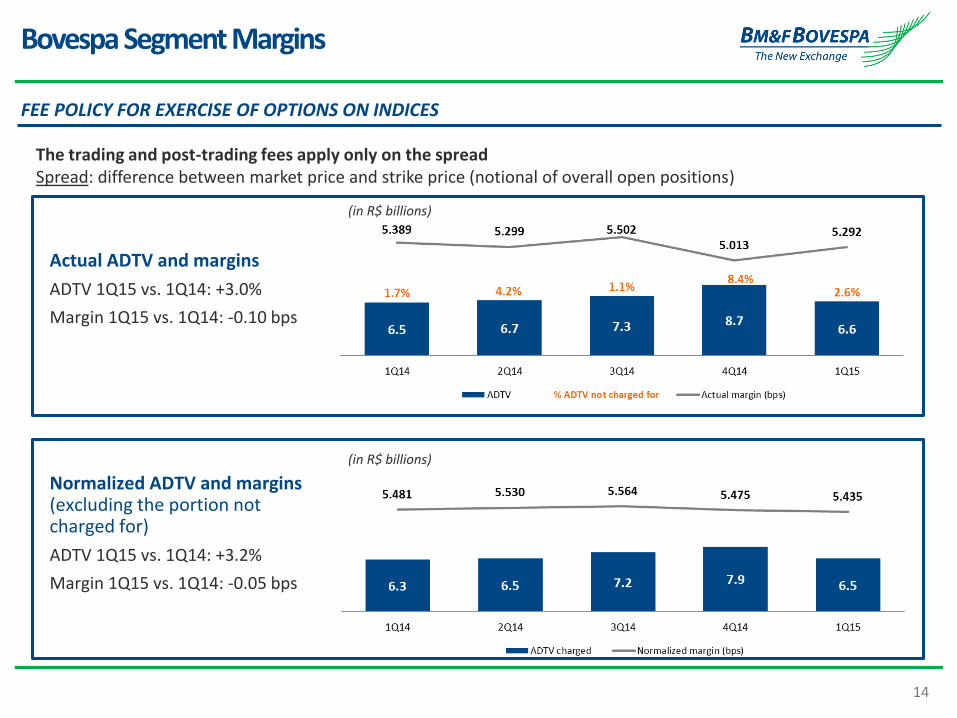

Bovespa Segment Margins

FEE POLICY FOR EXERCISE OF OPTIONS ON INDICES

Actual ADTV and margins

ADTV 1Q15 vs. 1Q14: +3.0%

Margin 1Q15 vs. 1Q14: -0.10 bps

Normalized ADTV and margins (excluding the portion not charged for)

ADTV 1Q15 vs. 1Q14: +3.2%

Margin 1Q15 vs. 1Q14: -0.05 bps

The trading and post-trading fees apply only on the spread Spread: difference between market price and strike price (notional of overall open positions)

(in R$ billions)

(in R$ billions)

15

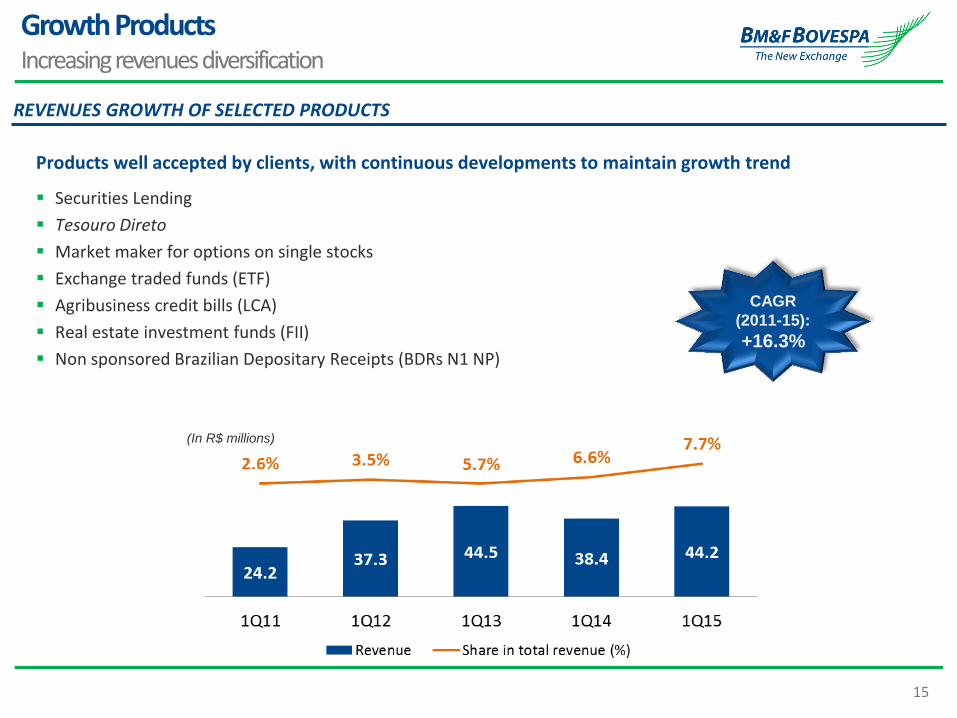

Growth Products Increasing revenues diversification

Products well accepted by clients, with continuous developments to maintain growth trend

Securities Lending

Tesouro Direto

Market maker for options on single stocks

Exchange traded funds (ETF)

Agribusiness credit bills (LCA)

Real estate investment funds (FII)

Non sponsored Brazilian Depositary Receipts (BDRs N1 NP)

CAGR

(2011-15):

+16.3%

(In R$ millions)

REVENUES GROWTH OF SELECTED PRODUCTS

16

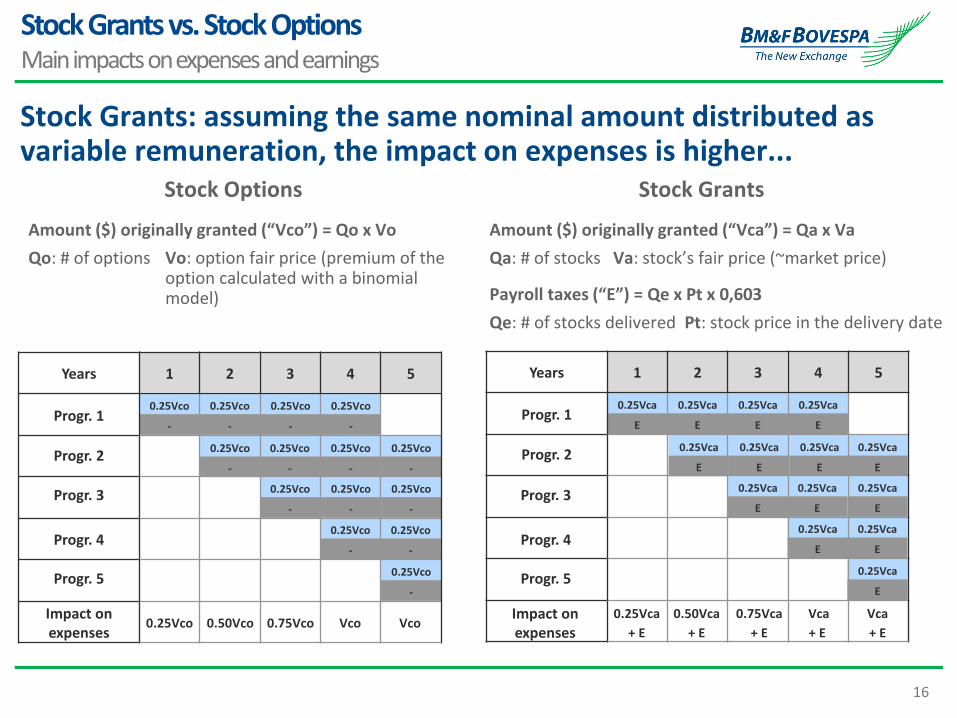

Stock Grants vs. Stock Options Main impacts on expenses and earnings

Amount ($) originally granted (“Vco”) = Qo x Vo

Qo: # of options

Stock Grants: assuming the same nominal amount distributed as variable remuneration, the impact on expenses is higher...

Stock Options Stock Grants

Amount ($) originally granted (“Vca”) = Qa x Va

Qa: # of stocks Va: stock’s fair price (~market price)

Payroll taxes (“E”) = Qe x Pt x 0,603

Qe: # of stocks delivered Pt: stock price in the delivery date

Progr. 1

Progr. 2

Progr. 3

Impact on expenses

0.25Vco 0.50Vco

Progr. 1

Progr. 2

0.25Vca

E

0.25Vca

E

0.25Vca

E

0.25Vca

E

0.25Vca

E

0.25Vca

E

0.25Vca

E

0.25Vca

+ E

0.50Vca

+ E

0.25Vca

E

Progr. 4

Progr. 5

0.75Vco Vco Vco

0.25Vca

E

0.25Vca

E

0.25Vca

E

0.25Vca

E

0.25Vca

E

0.25Vca

E

0.25Vco

-

0.25Vco

-

0.25Vco

-

0.25Vco

-

0.25Vco

-

0.25Vco

-

0.25Vco

-

0.25Vco

-

0.25Vco

-

0.25Vco

-

0.25Vco

-

0.25Vco

-

0.25Vco

-

0.25Vco

-

0.75Vca

+ E

Vca

+ E

Vca

+ E

Impact on expenses

Progr. 3

Progr. 4

Progr. 5

Vo: option fair price (premium of the option calculated with a binomial model)

Years 1 2 3 4 5 Years 1 2 3 4 5

17

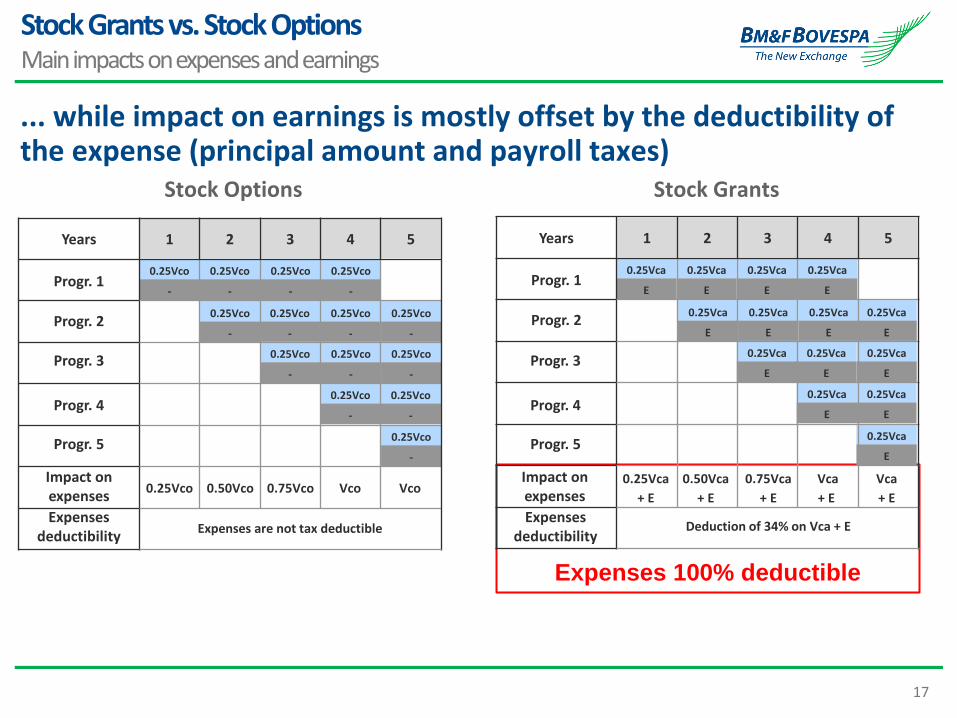

... while impact on earnings is mostly offset by the deductibility of the expense (principal amount and payroll taxes)

Stock Options Stock Grants

Progr. 1

Progr. 2

Progr. 3

Impact on expenses

Progr. 1

Progr. 2

Progr. 4

Progr. 5

Impact on expenses

Progr. 3

Progr. 4

Progr. 5

Expenses deductibility

Expenses deductibility

Expenses 100% deductible

Expenses are not tax deductible Deduction of 34% on Vca + E

Stock Grants vs. Stock Options Main impacts on expenses and earnings

0.25Vco 0.50Vco 0.75Vco Vco Vco

0.25Vco

-

0.25Vco

-

0.25Vco

-

0.25Vco

-

0.25Vco

-

0.25Vco

-

0.25Vco

-

0.25Vco

-

0.25Vco

-

0.25Vco

-

0.25Vco

-

0.25Vco

-

0.25Vco

-

0.25Vco

-

0.25Vca

E

0.25Vca

E

0.25Vca

E

0.25Vca

E

0.25Vca

E

0.25Vca

E

0.25Vca

E

0.25Vca

+ E

0.50Vca

+ E

0.25Vca

E

0.25Vca

E

0.25Vca

E

0.25Vca

E

0.25Vca

E

0.25Vca

E

0.25Vca

E

0.75Vca

+ E

Vca

+ E

Vca

+ E

Years 1 2 3 4 5 Years 1 2 3 4 5

18

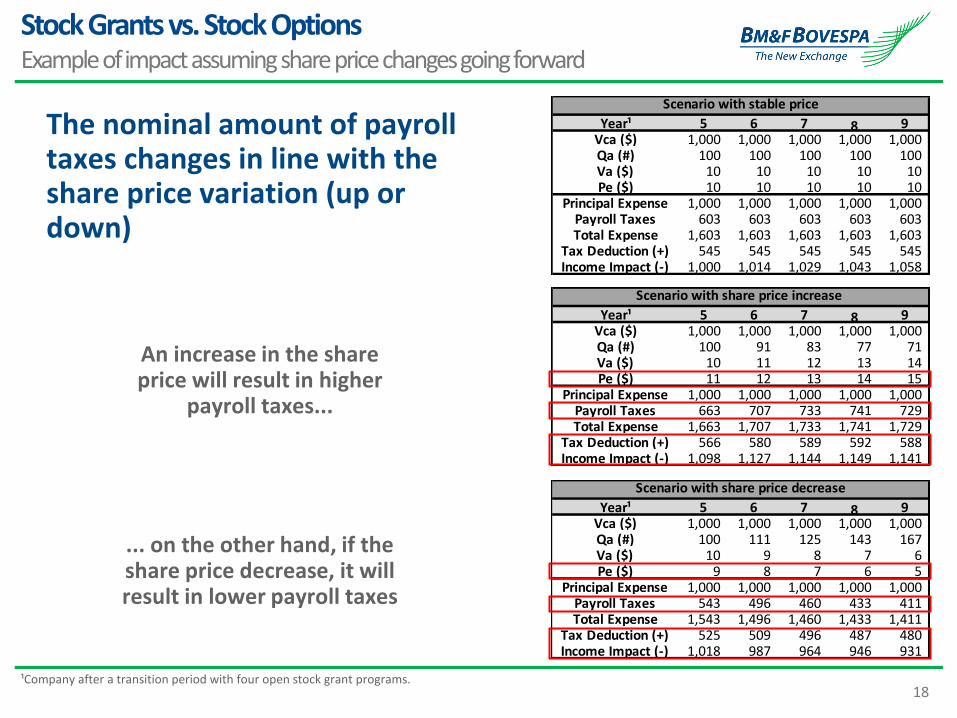

Year¹ 5 6 7 8 9Vca ($) 1,000 1,000 1,000 1,000 1,000 Qa (#) 100 111 125 143 167 Va ($) 10 9 8 7 6 Pe ($) 9 8 7 6 5

Principal Expense 1,000 1,000 1,000 1,000 1,000 Payroll Taxes 543 496 460 433 411 Total Expense 1,543 1,496 1,460 1,433 1,411

Tax Deduction (+) 525 509 496 487 480 Income Impact (-) 1,018 987 964 946 931

Scenario with share price decrease

Year¹ 5 6 7 8 9Vca ($) 1,000 1,000 1,000 1,000 1,000 Qa (#) 100 91 83 77 71 Va ($) 10 11 12 13 14 Pe ($) 11 12 13 14 15

Principal Expense 1,000 1,000 1,000 1,000 1,000 Payroll Taxes 663 707 733 741 729 Total Expense 1,663 1,707 1,733 1,741 1,729

Tax Deduction (+) 566 580 589 592 588 Income Impact (-) 1,098 1,127 1,144 1,149 1,141

Scenario with share price increase

An increase in the share price will result in higher

payroll taxes...

... on the other hand, if the share price decrease, it will result in lower payroll taxes

The nominal amount of payroll taxes changes in line with the share price variation (up or down)

¹Company after a transition period with four open stock grant programs.

Stock Grants vs. Stock Options Example of impact assuming share price changes going forward

Year¹ 5 6 7 8 9Vca ($) 1,000 1,000 1,000 1,000 1,000 Qa (#) 100 100 100 100 100 Va ($) 10 10 10 10 10 Pe ($) 10 10 10 10 10

Principal Expense 1,000 1,000 1,000 1,000 1,000 Payroll Taxes 603 603 603 603 603 Total Expense 1,603 1,603 1,603 1,603 1,603

Tax Deduction (+) 545 545 545 545 545 Income Impact (-) 1,000 1,014 1,029 1,043 1,058

Scenario with stable price

19

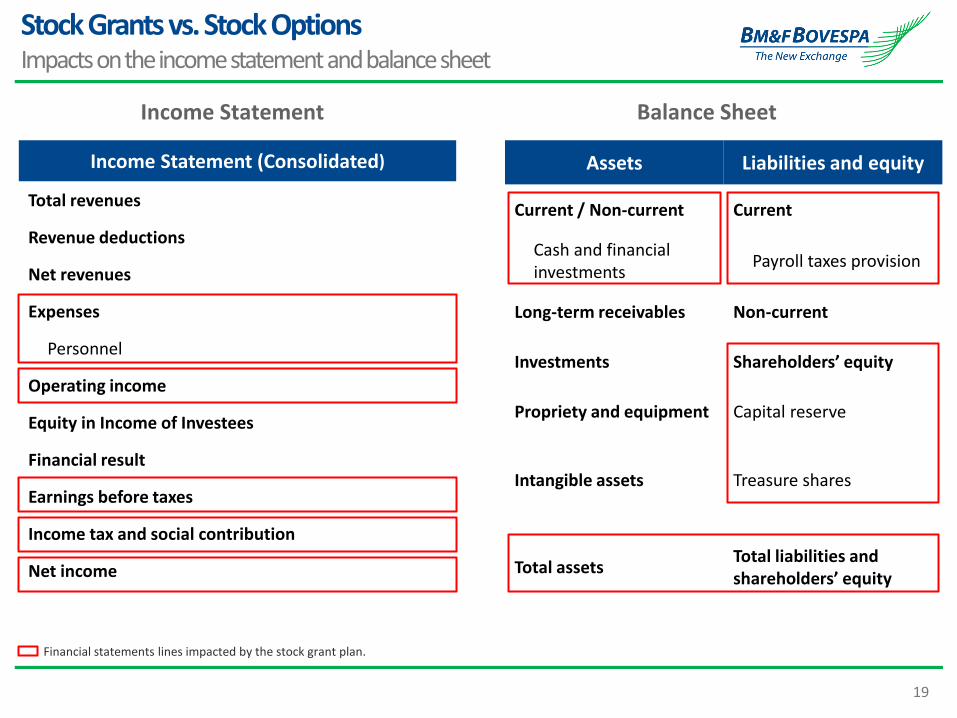

Income Statement Balance Sheet

Income Statement (Consolidated)

Total revenues

Revenue deductions

Net revenues

Expenses

Personnel

Operating income

Equity in Income of Investees

Financial result

Earnings before taxes

Income tax and social contribution

Net income

Assets Liabilities and equity

Current / Non-current Current

Cash and financial investments

Payroll taxes provision

Long-term receivables Non-current

Investments Shareholders’ equity

Propriety and equipment Capital reserve

Intangible assets Treasure shares

Total assets Total liabilities and shareholders’ equity

Financial statements lines impacted by the stock grant plan.

Stock Grants vs. Stock Options Impacts on the income statement and balance sheet

20

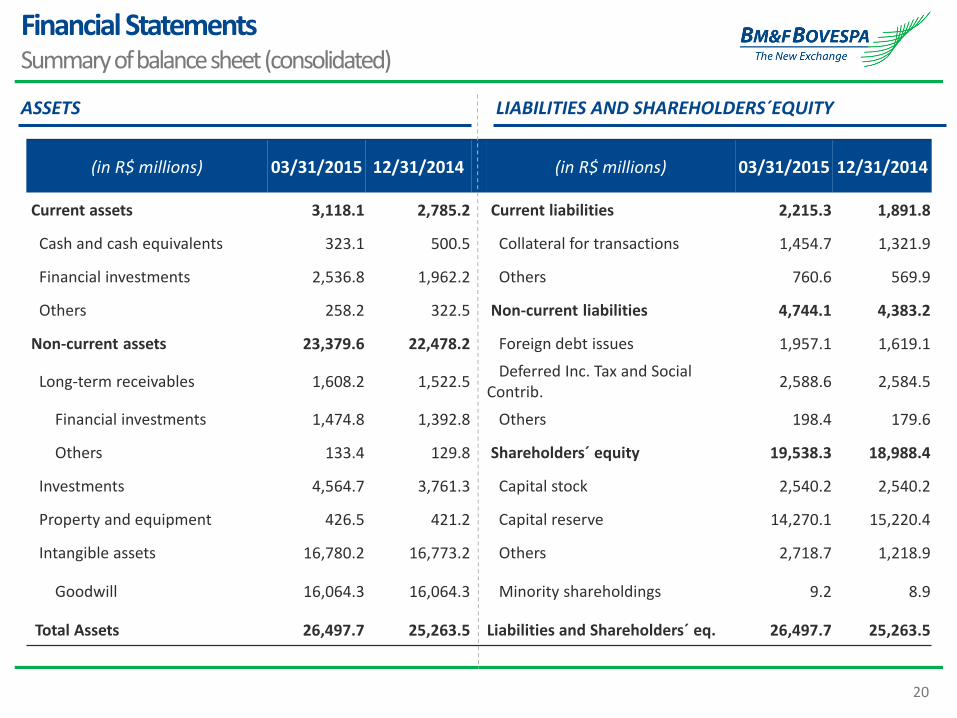

Financial Statements Summary of balance sheet (consolidated)

(in R$ millions) 03/31/2015 12/31/2014 (in R$ millions) 03/31/2015 12/31/2014

Current assets 3,118.1 2,785.2 Current liabilities 2,215.3 1,891.8

Cash and cash equivalents 323.1 500.5 Collateral for transactions 1,454.7 1,321.9

Financial investments 2,536.8 1,962.2 Others 760.6 569.9

Others 258.2 322.5 Non-current liabilities 4,744.1 4,383.2

Non-current assets 23,379.6 22,478.2 Foreign debt issues 1,957.1 1,619.1

Long-term receivables 1,608.2 1,522.5 Deferred Inc. Tax and Social Contrib.

2,588.6 2,584.5

Financial investments 1,474.8 1,392.8 Others 198.4 179.6

Others 133.4 129.8 Shareholders´ equity 19,538.3 18,988.4

Investments 4,564.7 3,761.3 Capital stock 2,540.2 2,540.2

Property and equipment 426.5 421.2 Capital reserve 14,270.1 15,220.4

Intangible assets 16,780.2 16,773.2 Others 2,718.7 1,218.9

Goodwill 16,064.3 16,064.3 Minority shareholdings 9.2 8.9

Total Assets 26,497.7 25,263.5 Liabilities and Shareholders´ eq. 26,497.7 25,263.5

LIABILITIES AND SHAREHOLDERS´EQUITY ASSETS

21

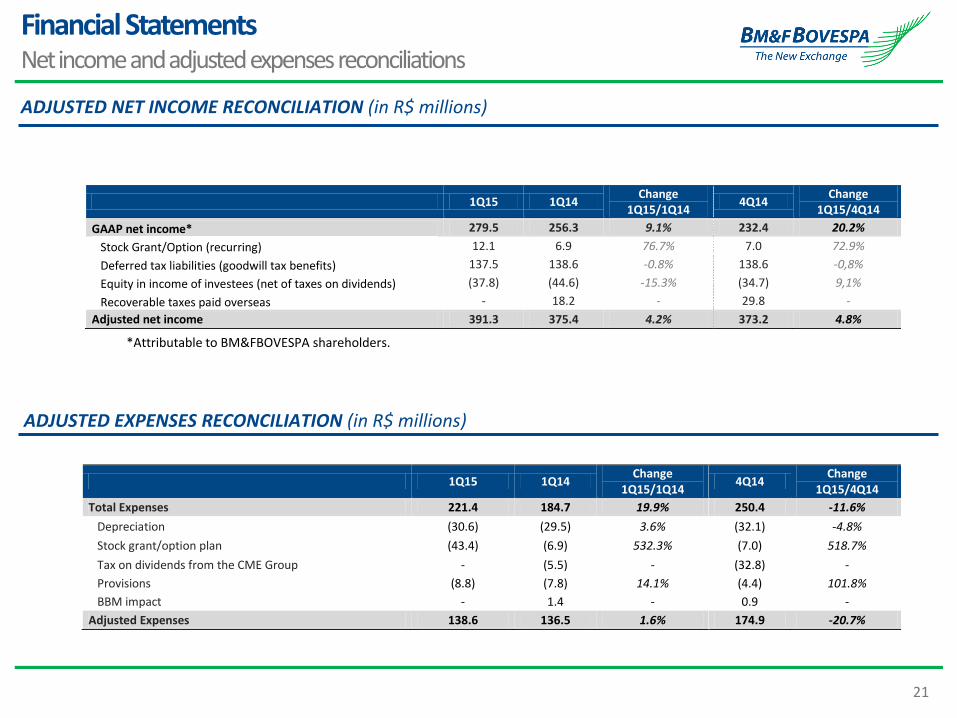

1Q15 1Q14 Change

1Q15/1Q14 4Q14

Change 1Q15/4Q14

Total Expenses 221.4 184.7 19.9% 250.4 -11.6%

Depreciation (30.6) (29.5) 3.6% (32.1) -4.8%

Stock grant/option plan (43.4) (6.9) 532.3% (7.0) 518.7%

Tax on dividends from the CME Group - (5.5) - (32.8) -

Provisions (8.8) (7.8) 14.1% (4.4) 101.8%

BBM impact - 1.4 - 0.9 -

Adjusted Expenses 138.6 136.5 1.6% 174.9 -20.7%

1Q15 1Q14 Change

1Q15/1Q14 4Q14

Change 1Q15/4Q14

GAAP net income* 279.5 256.3 9.1% 232.4 20.2%

Stock Grant/Option (recurring) 12.1 6.9 76.7% 7.0 72.9%

Deferred tax liabilities (goodwill tax benefits) 137.5 138.6 -0.8% 138.6 -0,8%

Equity in income of investees (net of taxes on dividends) (37.8) (44.6) -15.3% (34.7) 9,1%

Recoverable taxes paid overseas - 18.2 - 29.8 -

Adjusted net income 391.3 375.4 4.2% 373.2 4.8%

Financial Statements Net income and adjusted expenses reconciliations

*Attributable to BM&FBOVESPA shareholders.

ADJUSTED NET INCOME RECONCILIATION (in R$ millions)

ADJUSTED EXPENSES RECONCILIATION (in R$ millions)

22

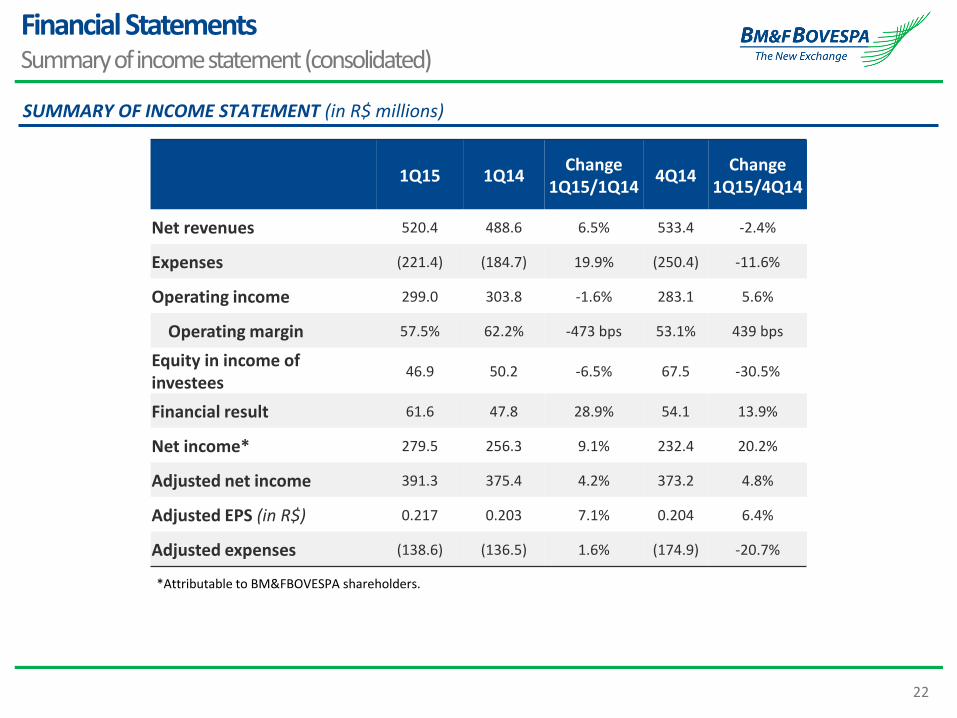

1Q15 1Q14 Change

1Q15/1Q14 4Q14

Change 1Q15/4Q14

Net revenues 520.4 488.6 6.5% 533.4 -2.4%

Expenses (221.4) (184.7) 19.9% (250.4) -11.6%

Operating income 299.0 303.8 -1.6% 283.1 5.6%

Operating margin 57.5% 62.2% -473 bps 53.1% 439 bps

Equity in income of investees

46.9 50.2 -6.5% 67.5 -30.5%

Financial result 61.6 47.8 28.9% 54.1 13.9%

Net income* 279.5 256.3 9.1% 232.4 20.2%

Adjusted net income 391.3 375.4 4.2% 373.2 4.8%

Adjusted EPS (in R$) 0.217 0.203 7.1% 0.204 6.4%

Adjusted expenses (138.6) (136.5) 1.6% (174.9) -20.7%

SUMMARY OF INCOME STATEMENT (in R$ millions)

*Attributable to BM&FBOVESPA shareholders.

Financial Statements Summary of income statement (consolidated)

23

Contact

Investor Relations Department

Phone: 55 11 2565-4729 / 4418 / 4207 / 4834 / 7938