Embed Size (px)

Citation preview

19- 1

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Fundamentals of Corporate

Finance

Sixth Edition

Richard A. Brealey

Stewart C. Myers

Alan J. Marcus

Slides by

Matthew Will

Chapter 19

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Short-Term Financial Planning

19- 2

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Topics Covered

Links Between Long-Term and Short-Term Financing

Working Capital Tracing Changes in Cash and Working Capital Cash Budgeting A Short-Term Financing Plan Sources of Short-Term Financing The Cost of Bank Loans

19- 3

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Working Capital

Factors in establishing working capital levels

1.Matching maturities

2.Permanent working capital requirements

3.The advantages of liquidity

19- 4

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

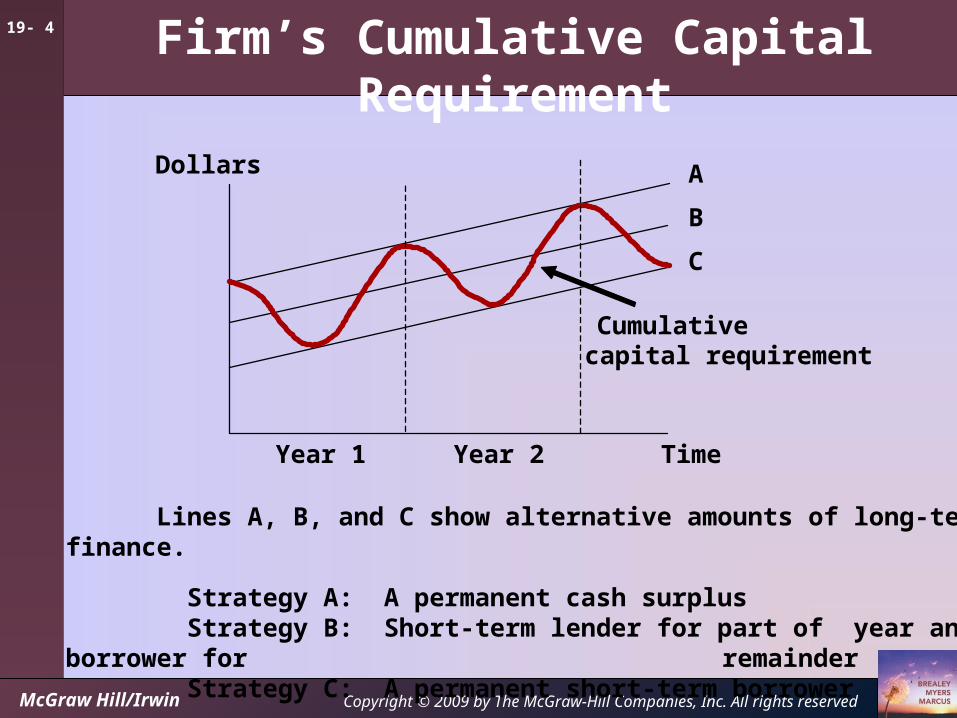

Firm’s Cumulative Capital Requirement

Lines A, B, and C show alternative amounts of long-term finance.

Strategy A: A permanent cash surplus Strategy B: Short-term lender for part of year and borrower for

remainder Strategy C: A permanent short-term borrower

A

B

C

Year 2Year 1

Dollars

Cumulativecapital requirement

Time

19- 5

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Working Capital

Net Working Capital - Current assets minus current liabilities. Often called working capital.

Cash Conversion Cycle - Period between firm’s payment for materials and collection on its sales.

Carrying Costs - Costs of maintaining current assets, including opportunity cost of capital.

Shortage Costs - Costs incurred from shortages in current assets.

19- 6

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Working Capital

Simple Cycle of operations

Cash

Finished goodsinventory

ReceivablesRaw materials

inventory

19- 7

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

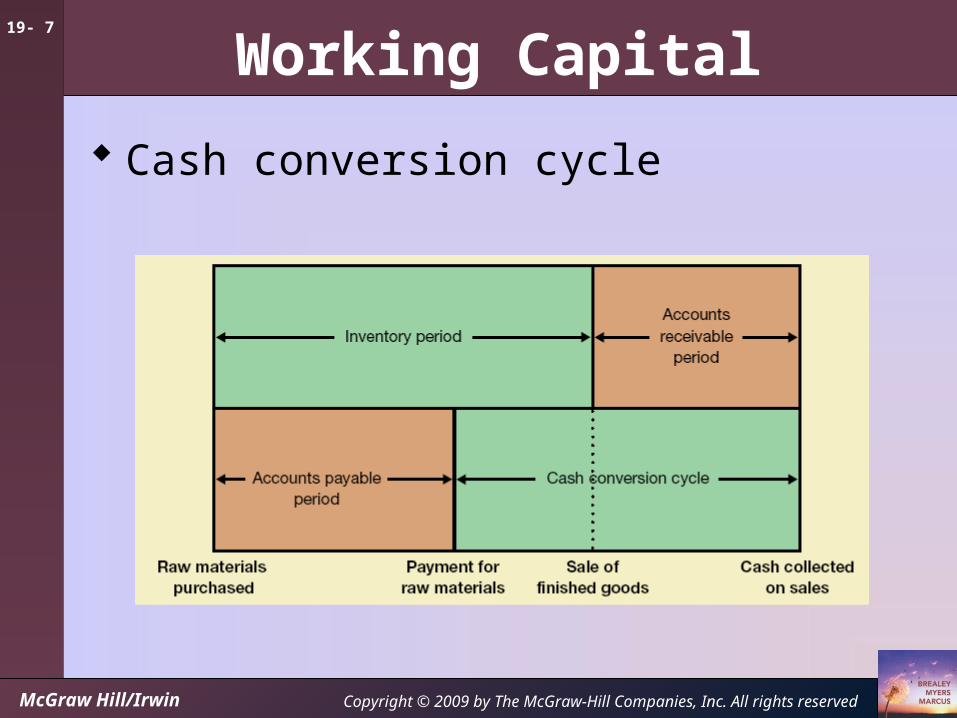

Working Capital

Cash conversion cycle

19- 8

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Working Capital

COGS/365 annual

payable accounts=period payable Accounts

sales/365 annual

receivable accounts=period sreceivable Accounts

COGS/365 annual

inventory=periodInventory

19- 9

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Working Capital

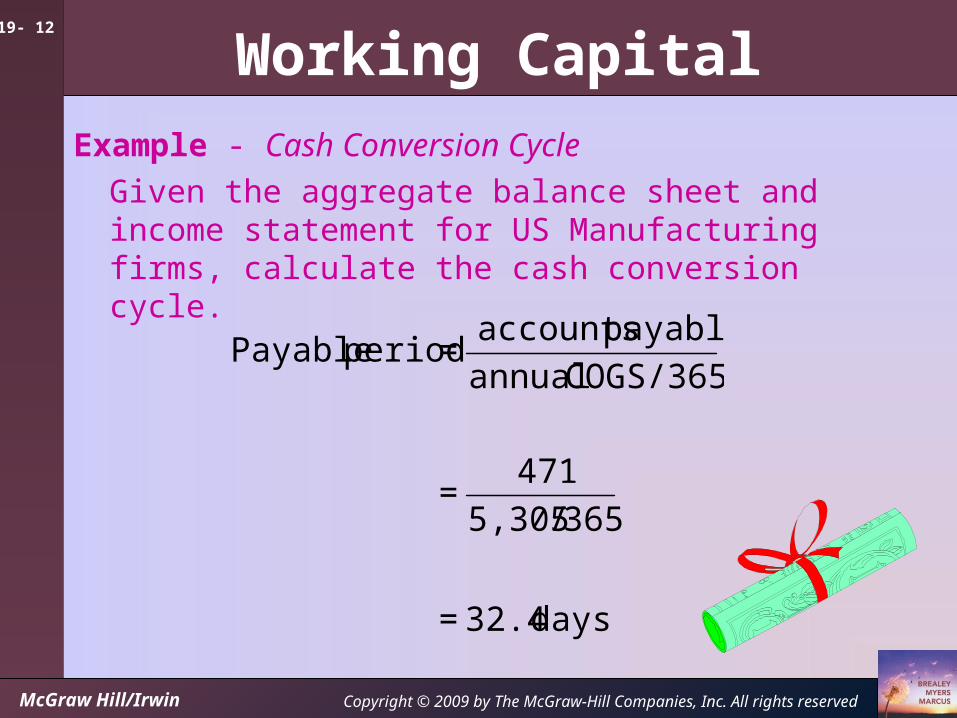

Example - Cash Conversion Cycle

Given the aggregate balance sheet and income statement for US Manufacturing firms, calculate the cash conversion cycle.

471A/P

703A/R5,305COGS

613Inventory5,887Sales

20072007

SheetBalanceStatementIncome

19- 10

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Working Capital

Example - Cash Conversion Cycle

Given the aggregate balance sheet and income statement for US Manufacturing firms, calculate the cash conversion cycle.

days 2.24

5,305/365

613=

COGS/365 annual

inventory =periodInventory

19- 11

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Working Capital

Example - Cash Conversion Cycle

Given the aggregate balance sheet and income statement for US Manufacturing firms, calculate the cash conversion cycle.

days 43.6=

5,887/365

703=

sales/365 annual

receivable accounts=period sReceivable

19- 12

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Working Capital

Example - Cash Conversion Cycle

Given the aggregate balance sheet and income statement for US Manufacturing firms, calculate the cash conversion cycle.

days 32.4=

365/5,305

471=

COGS/365 annual

payable accounts=period Payable

19- 13

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Working Capital

Example - Cash Conversion Cycle

Given the aggregate balance sheet and income statement for US Manufacturing firms, calculate the cash conversion cycle.

days 6.39periodInventory

days 30.3=period Payable

days 39.7=period sReceivable

Cash conversion cycle = (42.2+43.6) – 32.4 = 53.4

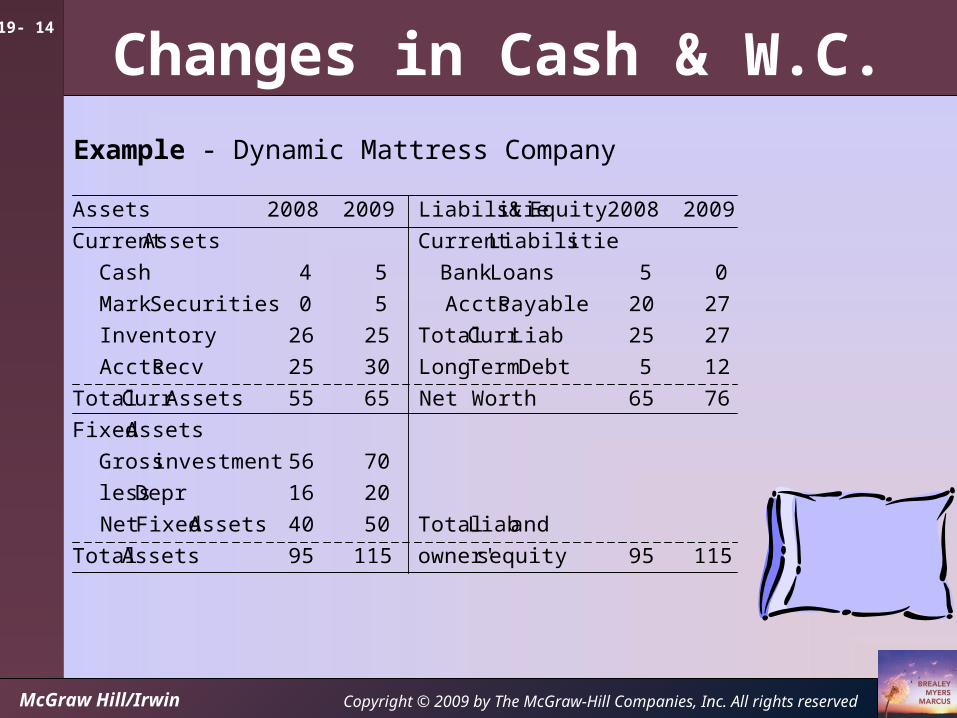

19- 14

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Changes in Cash & W.C.

Example - Dynamic Mattress Company

11595equity sowner'11595Assets Total

and Liab Total5040Assets FixedNet

2016Depr less

7056investment Gross

Assets Fixed

7665Net Worth6555AssetsCurr Total

125Debt Term Long3025Recv Accts

2725LiabCurr Total2526Inventory

2720Payable Accts 50SecuritiesMark

05LoansBank 54Cash

sLiabilitieCurrent AssetsCurrent

20092008Equity & sLiabilitie20092008Assets

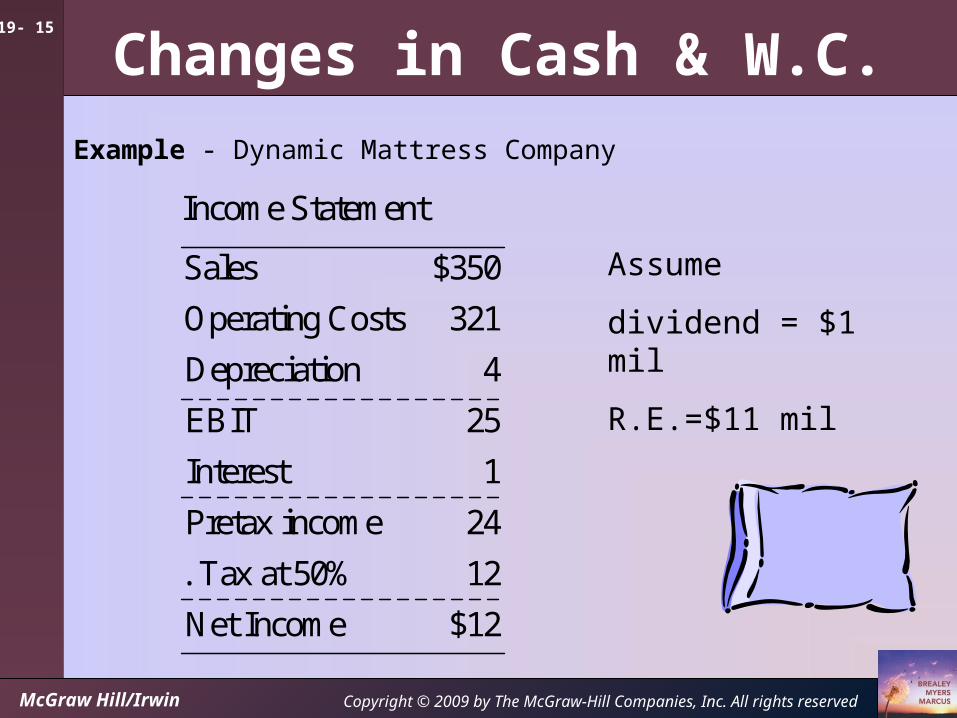

19- 15

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Changes in Cash & W.C.

Example - Dynamic Mattress CompanyIncome Statement

Sales $350

Operating Costs 321

Depreciation 4

EBIT 25

Interest 1

Pretax income 24

. Tax at 50% 12

Net Income $12

Assume

dividend = $1 mil

R.E.=$11 mil

19- 16

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Changes in Cash & W.C.Example -Dynamic Mattress Company

1 $balancecash in Increase

$30 UsesTotal

1Dividend

5receivable accounts Increased

5securities marketable Purchased

14assets fixedin Invested

5loanbank short term Repaid

Uses

$31Sources Total

4onDepreciati

12incomeNet

operations fromCash

7payable accounts Increased

1sinventorie Reduced

7debt termlong Issued

Sources

19- 17

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Changes in Cash & W.C.

Example - Dynamic Mattress Company

Dynamic used cash as follows Paid $1 mil dividend. Repaid $5 mil short term bank loan Invested $14 mil Purchased $5 mil of marketable securities Accounts receivable expanded by $5 mil

19- 18

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Cash Budgeting

Steps to preparing a cash budgetStep 1 - Forecast the sources of cash.

Step 2 - Forecast uses of cash.

Step 3 - Calculate whether the firm is facing a cash shortage or surplus.

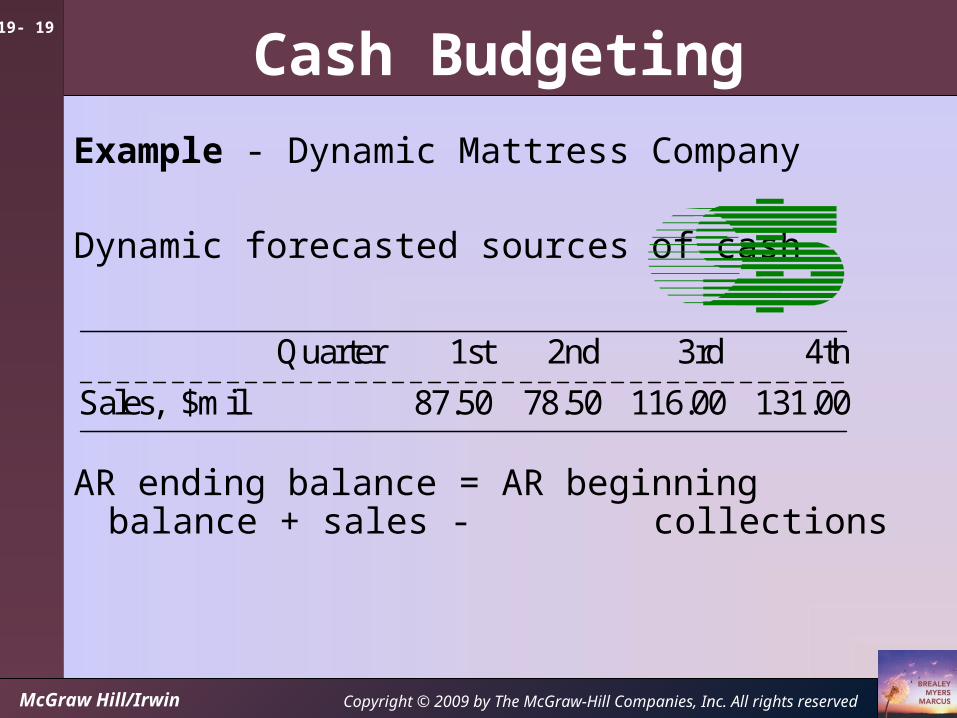

19- 19

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Cash Budgeting

Example - Dynamic Mattress Company

Dynamic forecasted sources of cash

AR ending balance = AR beginning balance + sales - collections

Quarter 1st 2nd 3rd 4th

Sales, $mil 87.50 78.50 116.00 131.00

19- 20

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Cash Budgeting

Example - Dynamic Mattress Company

Dynamic collections on ARQtr

1st 2nd 3rd 4th

1. Beginning receivables 30.0 32.5 30.7 38.2

2. Sales 87.5 78.5 116.0 131.0

3. Collections

. Sales in current Qtr (80%) 70 62.8 92.8 104.8

. Sales in previous Qtr (20%) 15.0 17.5 15.7 23.2

Total collections 85.0 80.3 108.5 128.0

4. Receivables at end of period

. (4 = 1 + 2 - 3) $32.5 $30.7 $38.2 $41.2

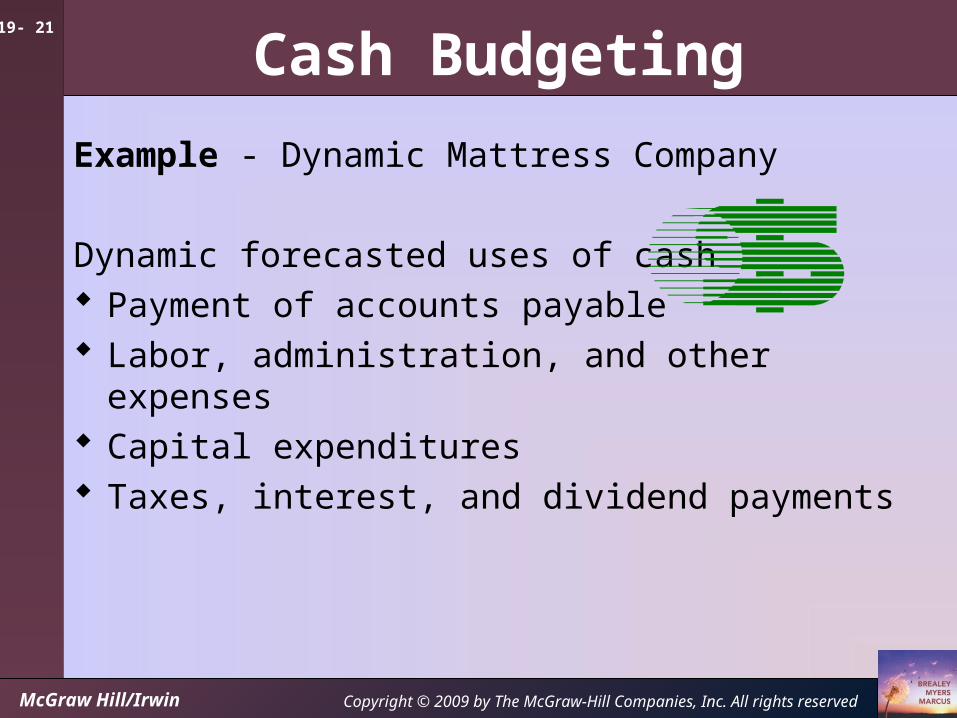

19- 21

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Cash Budgeting

Example - Dynamic Mattress Company

Dynamic forecasted uses of cash Payment of accounts payable Labor, administration, and other expenses Capital expenditures Taxes, interest, and dividend payments

19- 22

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Cash BudgetingExample - Dynamic Mattress Company

Dynamic

cash budget

$35.0$26.0$15.0-$45.0-

uses) minus (sources

inflowcash Net

93.095.095.3131.5cash of uses Total

5.04.54.04.0dividends & interest, , taxes

8.05.51.332.5esexpenditur capital

30.030.030.030.0expensesadmin andlabor

50.055.060.065.0AP ofpayment

cash of Uses

128.0121.080.386.5Sources Total

0.012.50.01.5other

128.0108.580.385.0ARon scollection

cash of Sources

4th3rd2nd1st

Qtr

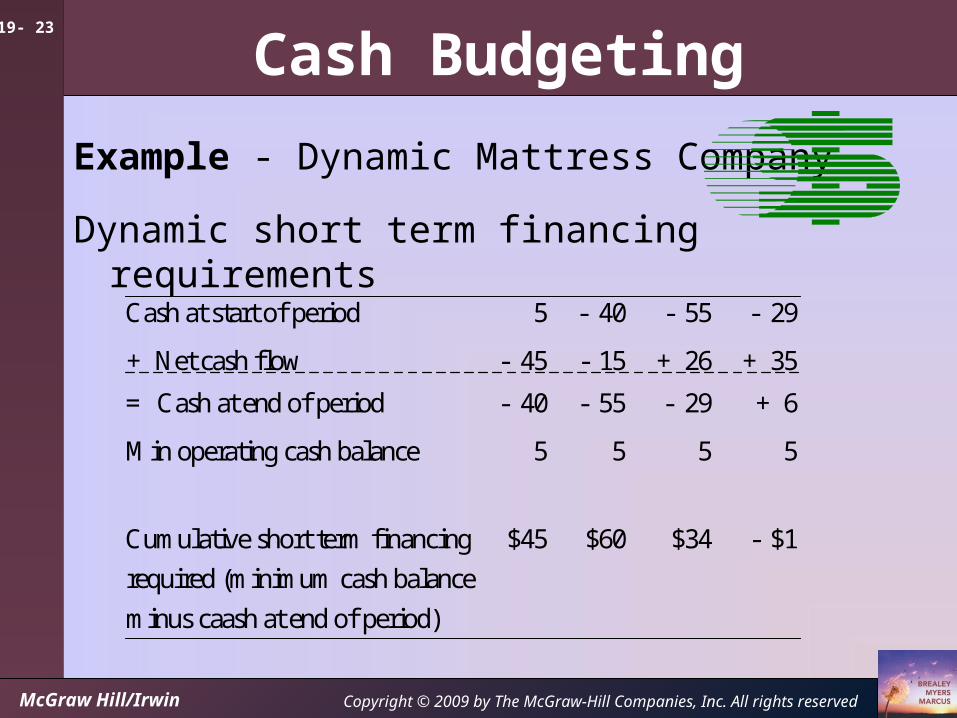

19- 23

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Cash Budgeting

Example - Dynamic Mattress Company

Dynamic short term financing requirements

Cash at start of period 5 - 40 - 55 - 29

+ Net cash flow - 45 - 15 + 26 + 35

= Cash at end of period - 40 - 55 - 29 + 6

Min operating cash balance 5 5 5 5

Cumulative short term financing

required (minimum cash balance

minus caash at end of period)

$45 $60 $34 - $1

19- 24

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Cash Budgeting

Forecast Uses of Cash

1.Payments of accounts payable.

2.Labor, administrative, and other expenses.

3.Capital expenditures.

4.Taxes, interest, and dividend payments.

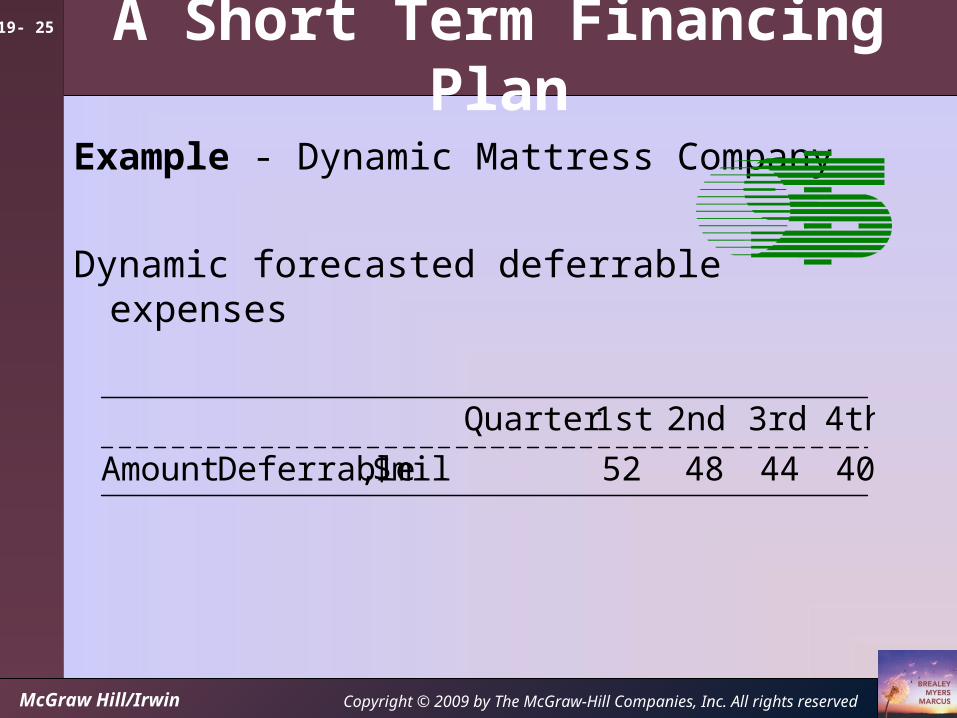

19- 25

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

A Short Term Financing Plan

Example - Dynamic Mattress Company

Dynamic forecasted deferrable expenses

40444852$mil ,DeferrableAmount

4th3rd2nd1stQuarter

19- 26

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

A Short Term Financing Plan

Example -

Dynamic

Mattress

Company-

Financing PlanFinancing Plan

031.3940.0040.00quarter of End 13.

31.3940.0040.000quarter of Beginning 12.

credit of Line

2.98000balancescash oAddition t 11.

balancescash in Increase

31.398.6100credit of line Of 10.

015.8000payables stretched Of 9.

Repayments

0015.8045.00raisedcash Total 8.

0005.00sold Securities 7.

0015.800payables Stretched 6.

00040.00loanBank 5.

RaisedCash

34.37-24.41-15.8045.00requiredcash Total 4.

0.7900payables stretechdon 3.Interest

.63.80.800loanbank on Interest 2.

35.00-26.00-15.0045.00operationsfor Cash 1.

tsRequiremenCash

4th3rd2nd1st

Qtr

19- 27

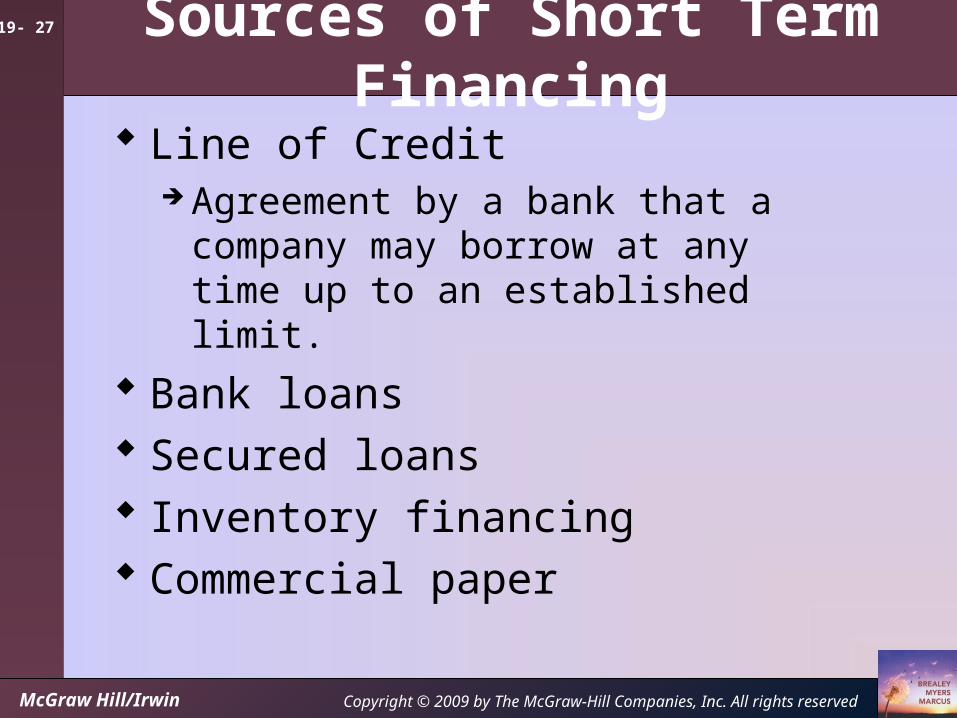

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Sources of Short Term Financing Line of Credit

Agreement by a bank that a company may borrow at any time up to an established limit.

Bank loans Secured loans Inventory financing Commercial paper

19- 28

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

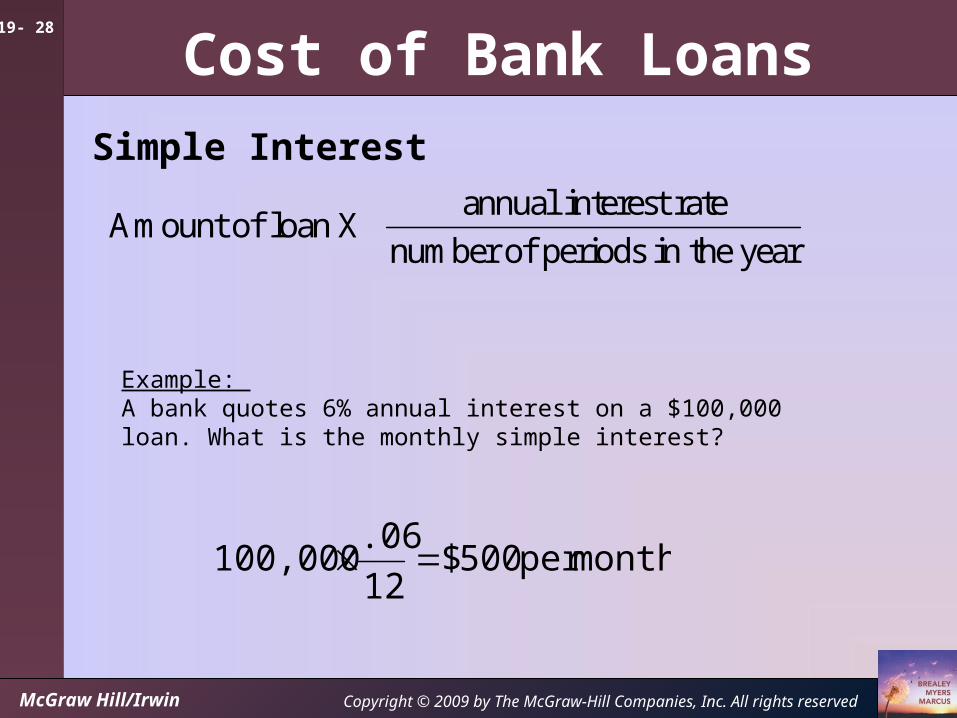

Cost of Bank Loans

Simple Interest

Amount of loan X annual interest rate

number of periods in the year

Example: A bank quotes 6% annual interest on a $100,000 loan. What is the monthly simple interest?

monthper 500$12

.06 100,000

19- 29

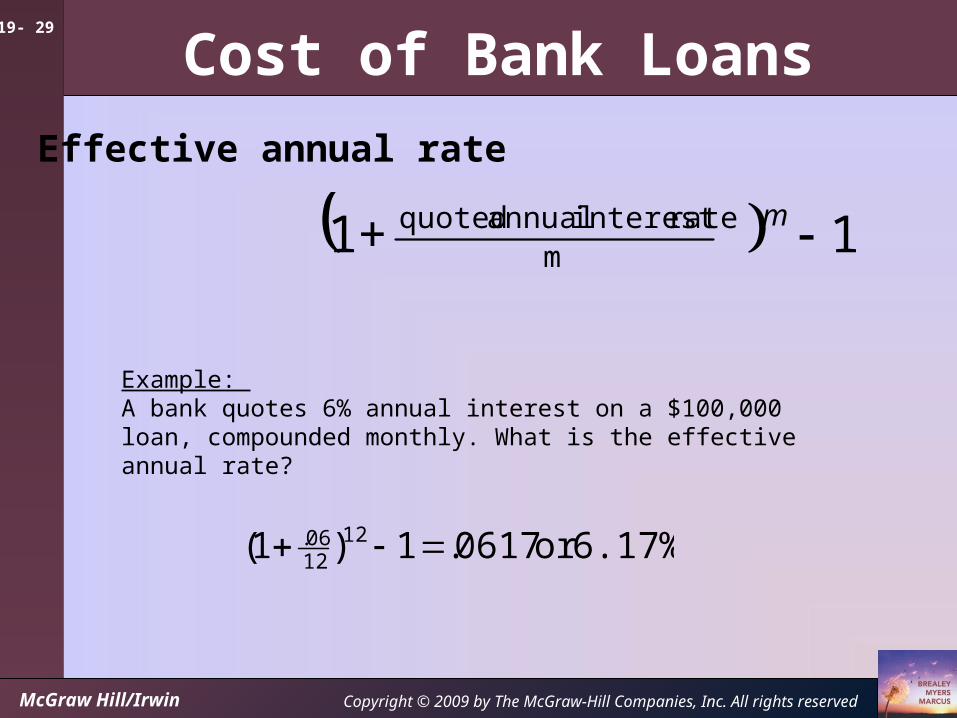

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Cost of Bank Loans

1+1 mrateinterest annual quoted m

Effective annual rate

Example: A bank quotes 6% annual interest on a $100,000 loan, compounded monthly. What is the effective annual rate?

6.17%or 0617.1)1( 121206.

19- 30

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

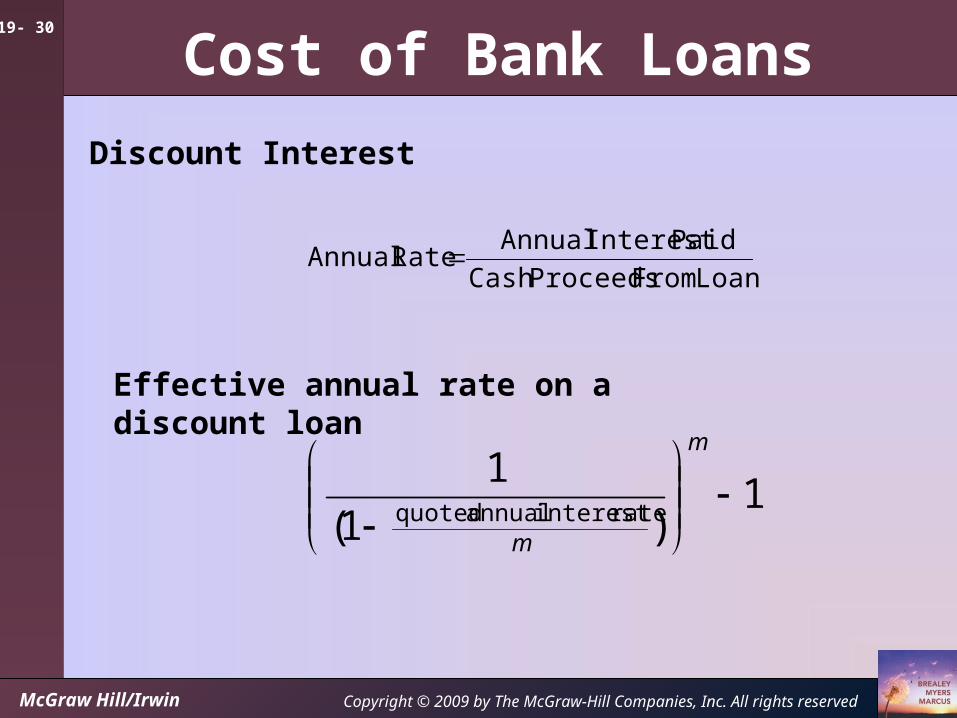

Cost of Bank Loans

Discount Interest

1)1(

1rateinterest annual quoted

m

m

Effective annual rate on a discount loan

Loan From ProceedsCash

PaidInterest Annual Rate Annual

19- 31

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Example:

A company can receive a 6% discount loan on $100,000.

What is the annual interest rate assuming annual payments?

What is the effective annual interest rate given monthly payments?

Cost of Bank Loans

6.38%or 0638.94,000

6,000 Rate Annual

6.20%or 062.1)1(

112

1206.

EAR

19- 32

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

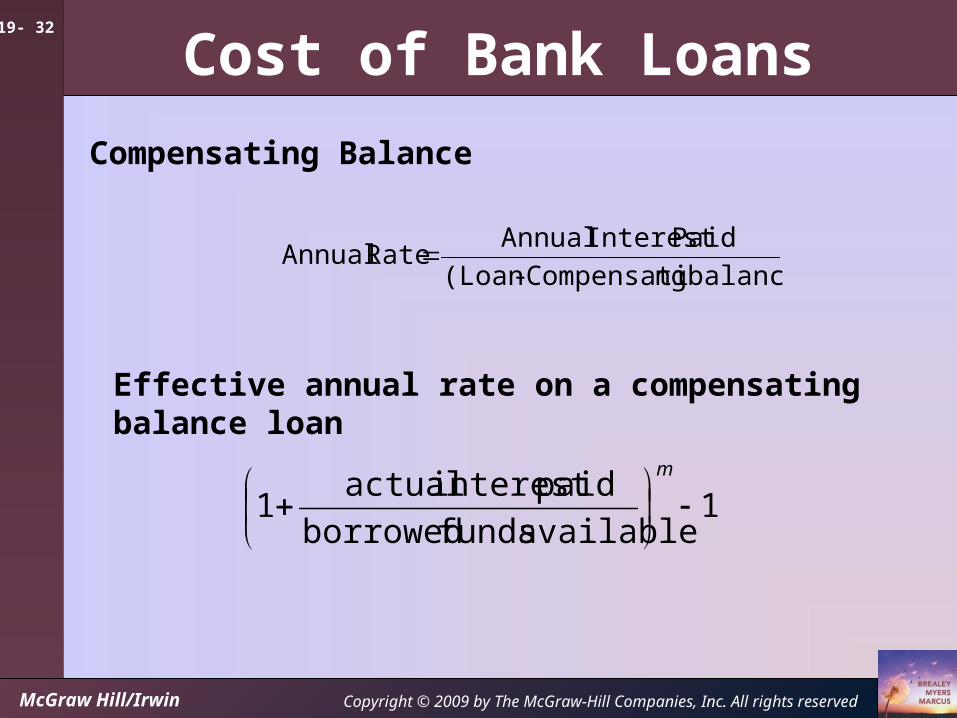

Cost of Bank Loans

Compensating Balance

1available funds borrowed

paidinterest actual1

m

Effective annual rate on a compensating balance loan

balance) ngCompensati -(Loan

PaidInterest Annual Rate Annual

19- 33

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Cost of Bank Loans

Example:

A company can receive a 6% discount loan on $100,000, but must maintain a $20,000 compensating balance.

What is the annual interest rate assuming annual payments?

What is the effective annual interest rate given monthly payments?

7.50%or 075.20,000)-(100,000

6,000 Rate Annual

7.76%or 0776.180,000

6,0001

12

EAR

19- 34

McGraw Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved

Web Resources