Embed Size (px)

Citation preview

18th Cross Atlantic and European Tax Symposium

Mitch ThompsonSquire Patton Boggs (US) LLP21 November 2014

Hybrid Mismatch Arrangements:The Past, Present and Future

2squirepattonboggs.com 2squirepattonboggs.com

Hybrid Entities - Agenda

Background and history of hybrid entities

Typical hybrid entity structures and US tax objectives

Thoughts on the effects of BEPS Action 2

3squirepattonboggs.com 3squirepattonboggs.com

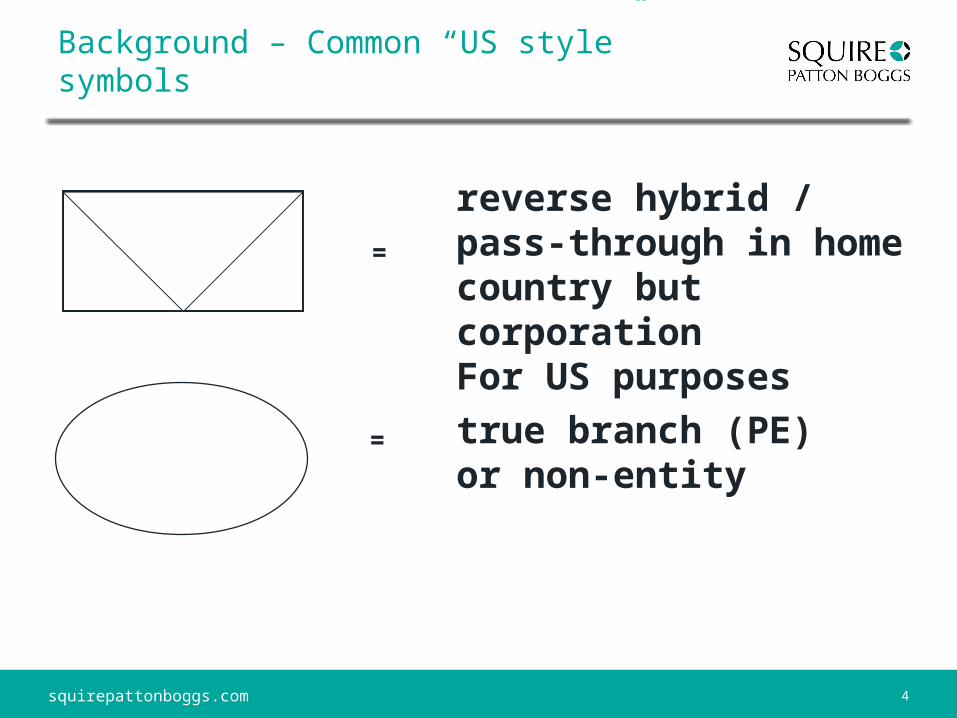

Background – Common “US style” symbols

=

=

corporation

single owner / disregarded

two or more owners / partnership

=

4squirepattonboggs.com 4squirepattonboggs.com

Background – Common “US style” symbols

=

reverse hybrid / pass-through in home country but corporationFor US purposes

true branch (PE) or non-entity

=

5squirepattonboggs.com 5squirepattonboggs.com

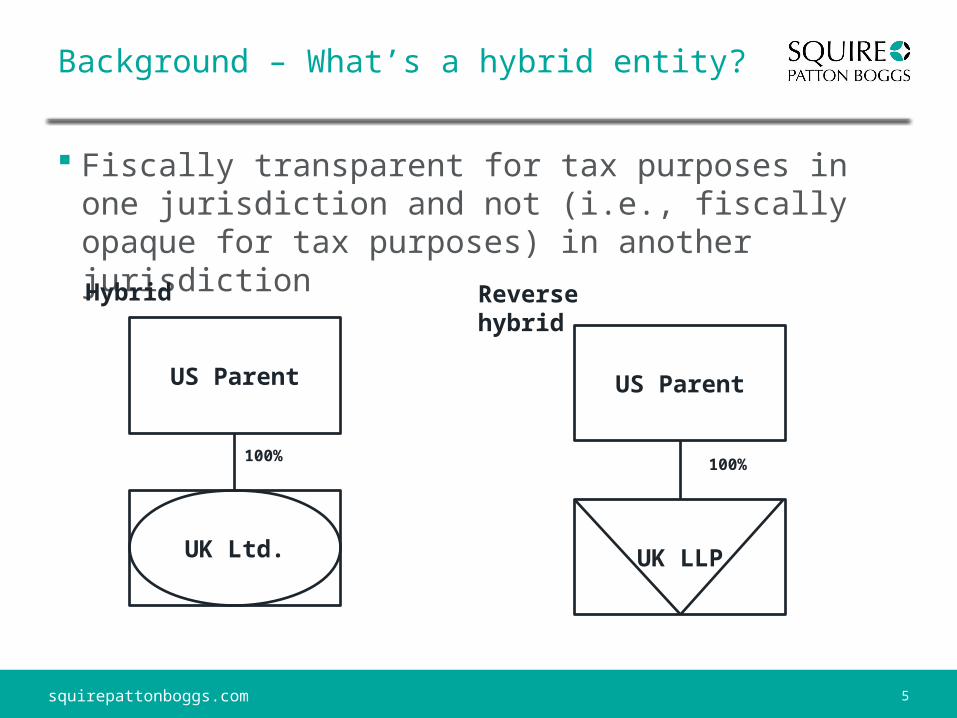

Background – What’s a hybrid entity?

Fiscally transparent for tax purposes in one jurisdiction and not (i.e., fiscally opaque for tax purposes) in another jurisdiction

US Parent

UK Ltd.

US Parent

UK LLP

100% 100%

Hybrid Reverse hybrid

6squirepattonboggs.com 6squirepattonboggs.com

Background – History of US “check the box”

Since the 1920s it was necessary to determine for US income tax purposes whether unincorporated entities are “associations” taxed as corporations

US rules in this area evolved over the years: Multi-factor “corporate resemblance test” based on case law; Followed by a similarly complex test under IRS regulations; Refined further by several administrative pronouncements

through the 1980s

7squirepattonboggs.com 7squirepattonboggs.com

Background – History of US “check the box”

Rapidly expanding use of US limited liability companies (“LLCs”) put further strain on this area of US tax practice

Certain legal changes in some US states added additional complexity

US policymakers realized the existing system was effectively “elective” for well advised taxpayers

So, beginning in 1995 the US IRS introduced by regulation the explicitly elective regime we know today as “check the box”

8squirepattonboggs.com 8squirepattonboggs.com

Background – History of US “check the box”

The policy goals of check-the-box were Simplicity, Administrability, and Certainty

Initial and primary focus of the CTB regime was US domestic tax The preamble to the regulations raised questions about the

international context and consequences The rules weren’t limited to US domestic tax, however, and

so the large-scale use of hybrids by US MNEs resulted

9squirepattonboggs.com 9squirepattonboggs.com

Background – History of US “check the box”

Check-the-box is an incredibly flexible planning tool Can create hybrid entities Can create hybrid instruments (at least for US purposes)

There have been numerous attempts to put the “genie back in the bottle,” entirely or to some extent CTB trimmed or limited in specific contexts, e.g.

• US foreign tax credit planning• Dual consolidated losses• Non-US acquisitions• Treaty availability

Obama administration’s ill-fated attempt to repeal international CTB

10squirepattonboggs.com 10squirepattonboggs.com

Typical structures - Interest

Third party debt

US Parent

Non-USDRE

CFC

100%

Double Deduction

ConsolidateOrGroup Taxation

Bank Debt

11squirepattonboggs.com 11squirepattonboggs.com

Typical structures - Interest

Related party debt

US Parent

non-USDRE

100%Parent Debt

Deduction / No Inclusion

12squirepattonboggs.com 12squirepattonboggs.com

Typical structures – US Foreign tax credit

US Parent

Non-USDRE

CFC

CFC

13squirepattonboggs.com 13squirepattonboggs.com

Typical structures – CFC Planning

US Parent

CV

BV 1

BV 2

Div/Roy/Int

Div/Roy/Int

14squirepattonboggs.com 14squirepattonboggs.com

Typical Structures - CFC Planning

Irish 1

BV

Irish 2

US Parent

CustomersAnd Affiliates

15squirepattonboggs.com 15squirepattonboggs.com

Typical structures – Acquisition / Step ups

Hybrid entity acquisition types

non-USSeller

Target

US Parent

US Parent

$

Shares

non-USSeller

Target

$

Partnership Interest

338(g)election

16squirepattonboggs.com 16squirepattonboggs.com

Outlook on changes and reforms

Action 2 deliverable September 2014 Really ready for immediate implementation? Commentary due from OECD by September 2015

US outlook As mentioned, plenty of prior US experience addressing hybrid

entities• Internal Revenue Code section 894(c)• Canada-US treaty• Certain non-US acquisitions / reorganizations• FTC splitters

US hybrid reform might come with larger-scale US tax reform

17squirepattonboggs.comsquirepattonboggs.com

Thank You!

Mitch Thompson, PartnerSquire Patton Boggs (US) [email protected]+ 1.216.479.8794 office

+ 1.216.407.8875 mobile

![[TITLE] - Squire Patton Boggs/media/files/insight… · Web view(employment law, pensions and immigration law); and . Built Environment (property, construction, planning, environmental)](https://img.pdfslide.us/doc/110x75/5f235c2c8b93ec76df104a66/title-squire-patton-boggs-mediafilesinsight-web-view-employment-law-pensions.jpg)