Embed Size (px)

Citation preview

18th-20th September , 2017 Granada (SPAIN)

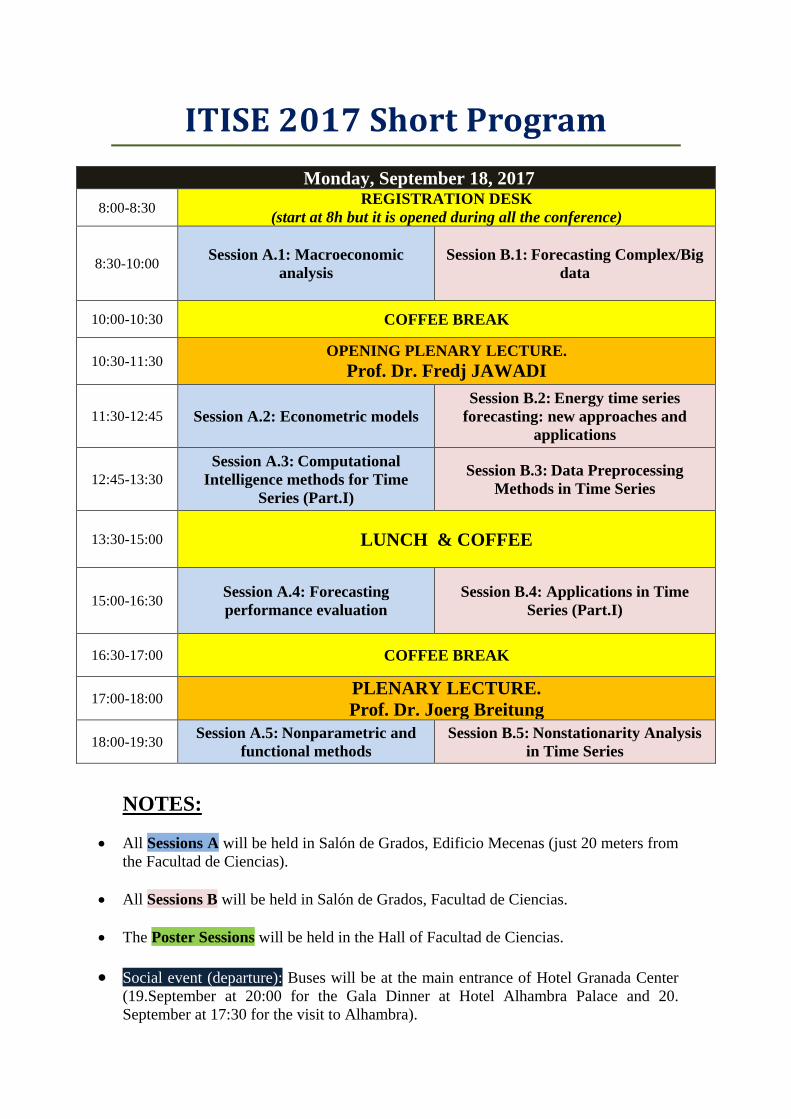

ITISE 2017 Short Program

Monday, September 18, 2017

8:00-8:30 REGISTRATION DESK

(start at 8h but it is opened during all the conference)

8:30-10:00 Session A.1: Macroeconomic

analysis

Session B.1: Forecasting Complex/Big

data

10:00-10:30 COFFEE BREAK

10:30-11:30 OPENING PLENARY LECTURE.

Prof. Dr. Fredj JAWADI

11:30-12:45 Session A.2: Econometric models

Session B.2: Energy time series

forecasting: new approaches and

applications

12:45-13:30

Session A.3: Computational

Intelligence methods for Time

Series (Part.I)

Session B.3: Data Preprocessing

Methods in Time Series

13:30-15:00 LUNCH & COFFEE

15:00-16:30 Session A.4: Forecasting

performance evaluation

Session B.4: Applications in Time

Series (Part.I)

16:30-17:00 COFFEE BREAK

17:00-18:00 PLENARY LECTURE.

Prof. Dr. Joerg Breitung

18:00-19:30 Session A.5: Nonparametric and

functional methods

Session B.5: Nonstationarity Analysis

in Time Series

NOTES:

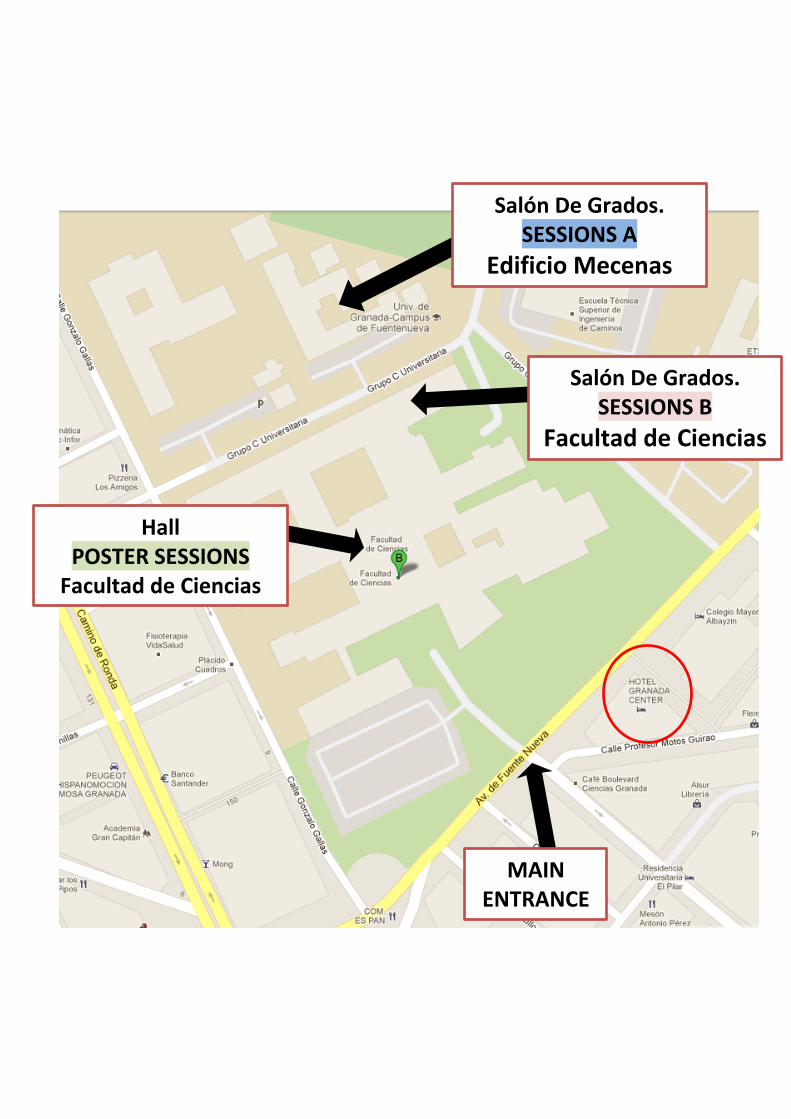

All Sessions A will be held in Salón de Grados, Edificio Mecenas (just 20 meters from

the Facultad de Ciencias).

All Sessions B will be held in Salón de Grados, Facultad de Ciencias.

The Poster Sessions will be held in the Hall of Facultad de Ciencias.

Social event (departure): Buses will be at the main entrance of Hotel Granada Center

(19.September at 20:00 for the Gala Dinner at Hotel Alhambra Palace and 20.

September at 17:30 for the visit to Alhambra).

Tuesday, September 19, 2017

8:00-8:30 REGISTRATION DESK

(start at 8h but it is opened during all the conference)

8:30-10:00

Session A.6: Computational

Intelligence methods for Time

Series (Part.II)

(8:30-9:15) Session B.6.A: Recent

Developments on Time-Series

Modelling for Financial Data

(9:15-10:00) Session B.6.B: Advanced

mathematical methodology in Time

Series (Part.I)

10:00-10:30 COFFEE BREAK

10:30-11:30 PLENARY LECTURE.

Dr. Travis Berge

11:30-12:45 Session A.7: Econometric

Forecasting

Session B.7: Applications in Time

Series (Part.II)

12:45-13:30 Session A.8: Deep Learning and

Time Series Analysis

Session B.8: Applications in Time

Series (Part.III)

13:30-15:00 LUNCH & COFFEE

15:00-16:30

Session A.9: Advanced

mathematical methodology in Time

Series (Part.II)

Session B.9: Energy Forecasting

16:30-17:00 COFFEE BREAK

17:00-18:00 PLENARY LECTURE.

Prof. Dr. Anna Korzeniewska

18:00-18:45

Session A.10: Future of

Mathematical and Logical

Structures behind Time Series

Analysis and History

Session B.10: Structural Time Series

Models

18:45-19:45 Session A.11/B.11: "Poster Session.

20:00 Gala Dinner at Hotel Alhambra Palace

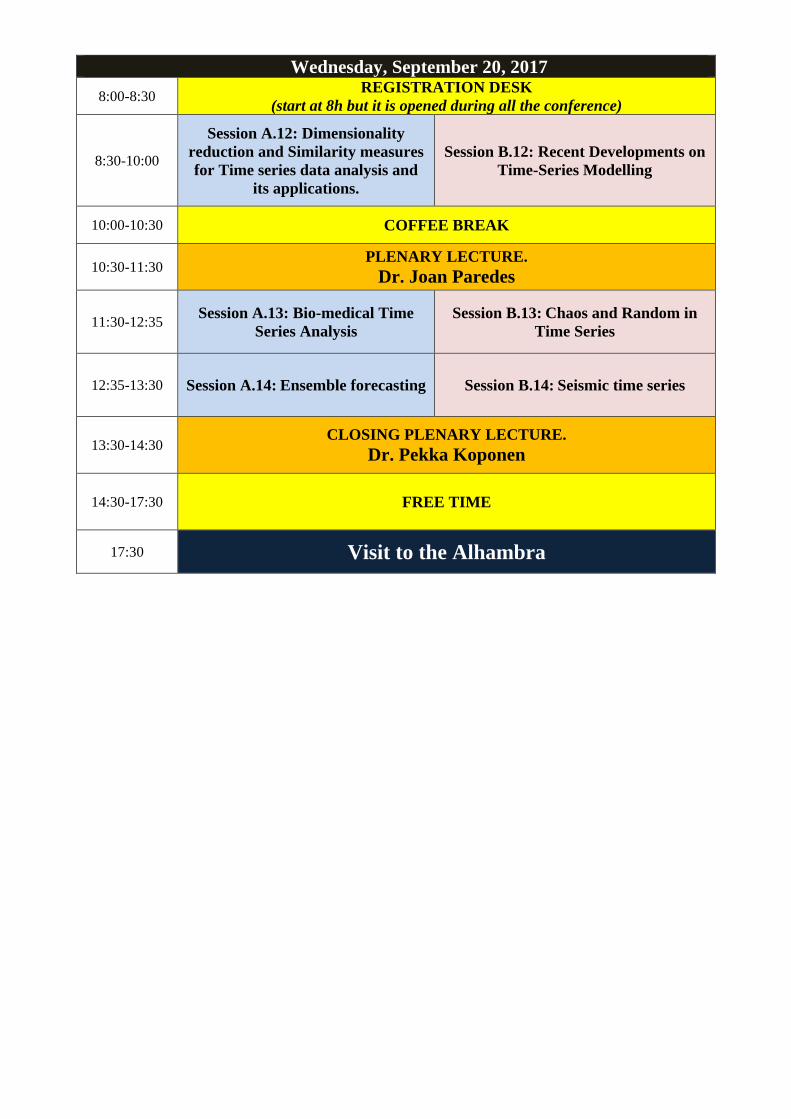

Wednesday, September 20, 2017

8:00-8:30 REGISTRATION DESK

(start at 8h but it is opened during all the conference)

8:30-10:00

Session A.12: Dimensionality

reduction and Similarity measures

for Time series data analysis and

its applications.

Session B.12: Recent Developments on

Time-Series Modelling

10:00-10:30 COFFEE BREAK

10:30-11:30 PLENARY LECTURE.

Dr. Joan Paredes

11:30-12:35 Session A.13: Bio-medical Time

Series Analysis

Session B.13: Chaos and Random in

Time Series

12:35-13:30 Session A.14: Ensemble forecasting Session B.14: Seismic time series

13:30-14:30 CLOSING PLENARY LECTURE.

Dr. Pekka Koponen

14:30-17:30 FREE TIME

17:30 Visit to the Alhambra

MAIN ENTRANCE

Hall POSTER SESSIONS

Facultad de Ciencias

Salón De Grados. SESSIONS B

Facultad de Ciencias

Salón De Grados. SESSIONS A

Edificio Mecenas

ITISE 2017 Conference Program

ITISE 2017 FULL PROGRAM

Monday, September 18, 2017

Session A.1: Macroeconomic analysis

Chairman: Dr. David Chernin and Dr. Nuno Ferreira

Determining macroeconomic indicators to implement a short-term forecasting model forVAT revenue.

Maria Del Camino Gonzalez Vasco and Cesar Perez Lopez

Fiscal Regime Shifts, and Household Expectations on Policy Dynamics

Diederik Kumps and Peter Claeys

Macroeconomic Forecasting in Small Open Economies Using Dynamic Factor Models

David Chernin and Markus Kirchner

An implied rating software system

Ventsislav Nikolov

Macroeconomic Forecasting using Approximate Factor Models with Outliers

Ray Yeutien Chou, Tso-Jung Yen and Yu-Min Yen

Testing Granger-causality on macroeconomic time series: a bootstrap approach

Matteo Farne and Angela Montanari

Session B.1: Forecasting Complex/Big data

Chairman: Dr. Luis Javier Herrera and Dr. Josefine Wilms

Filtering and prediction of Noisy and Unstable Signals: the Case of Google Trends Data

Livio Fenga

Sparse Granger-Causal Network Learning via the Depth Wise Group LASSO – AnApplication of ADMM for Large Vector Autoregressions

Ryan J. Kinnear and Ravi R. Mazumdar

Short-term Stream Flow Forecasting at Australian River Sites using Data-drivenRegression Techniques

Melise Steyn, Josefine Wilms, Willie Brink and Francois Smit

Hidden Markov Models for monitoring Circadian Rhythmicity in Telemetric Activity Data

Barbel Finkenstadt

An Implementation of HMM Classier in High Dimensions Based on MapReduce

Badreddine Benyacoub

1

ITISE 2017 Conference Program

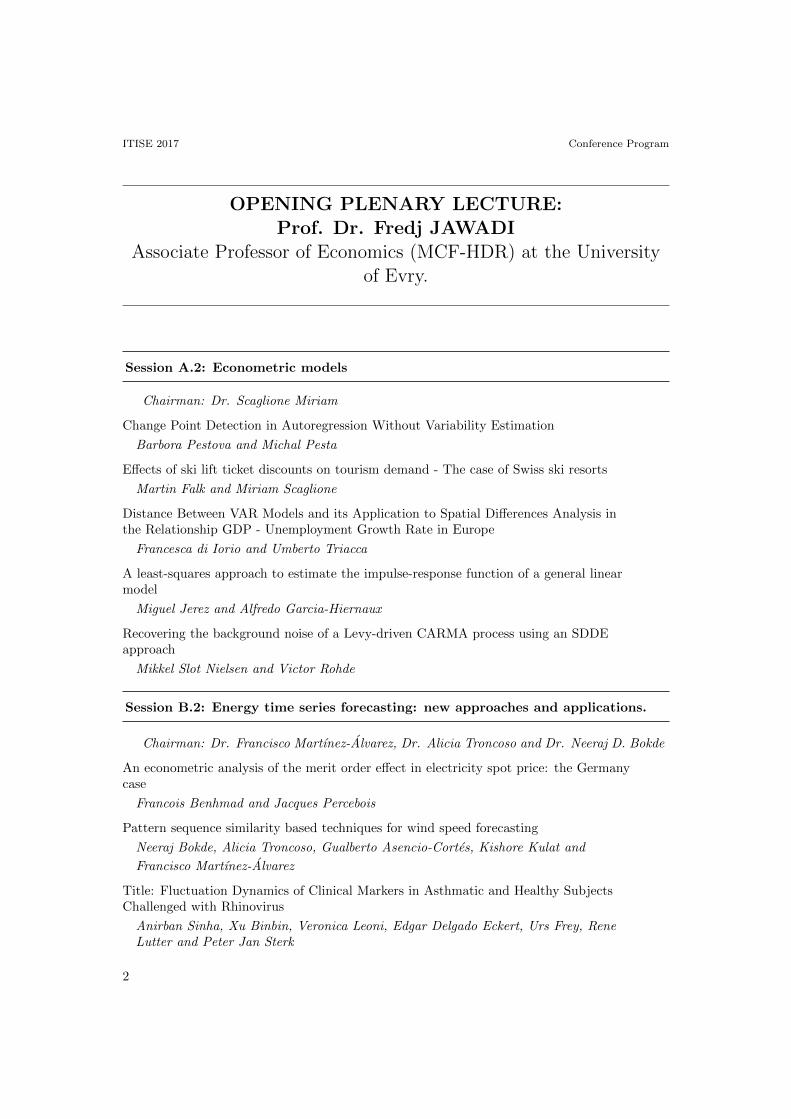

OPENING PLENARY LECTURE:Prof. Dr. Fredj JAWADI

Associate Professor of Economics (MCF-HDR) at the Universityof Evry.

Session A.2: Econometric models

Chairman: Dr. Scaglione Miriam

Change Point Detection in Autoregression Without Variability Estimation

Barbora Pestova and Michal Pesta

Effects of ski lift ticket discounts on tourism demand - The case of Swiss ski resorts

Martin Falk and Miriam Scaglione

Distance Between VAR Models and its Application to Spatial Differences Analysis inthe Relationship GDP - Unemployment Growth Rate in Europe

Francesca di Iorio and Umberto Triacca

A least-squares approach to estimate the impulse-response function of a general linearmodel

Miguel Jerez and Alfredo Garcia-Hiernaux

Recovering the background noise of a Levy-driven CARMA process using an SDDEapproach

Mikkel Slot Nielsen and Victor Rohde

Session B.2: Energy time series forecasting: new approaches and applications.

Chairman: Dr. Francisco Martınez-Alvarez, Dr. Alicia Troncoso and Dr. Neeraj D. Bokde

An econometric analysis of the merit order effect in electricity spot price: the Germanycase

Francois Benhmad and Jacques Percebois

Pattern sequence similarity based techniques for wind speed forecasting

Neeraj Bokde, Alicia Troncoso, Gualberto Asencio-Cortes, Kishore Kulat and

Francisco Martınez-Alvarez

Title: Fluctuation Dynamics of Clinical Markers in Asthmatic and Healthy SubjectsChallenged with Rhinovirus

Anirban Sinha, Xu Binbin, Veronica Leoni, Edgar Delgado Eckert, Urs Frey, ReneLutter and Peter Jan Sterk

2

ITISE 2017 Conference Program

Data driven application for the detection of energy consumption anomalies and theirroot causes in commercial buildings

Gerard Mor, Jordi Cipriano, Eloi Gabaldon, Jordi Carbonell, Jaime Marti-Herreroand Daniel Chemisana

Multiple seasonal Holt-Winters improvement for the special events forecast usingDiscrete-Interval Multiple Seasonalities

Juan Carlos Garcıa-Dıaz and Oscar Trull

Session A.3: Computational Intelligence methods for Time Series (Part.I)

Chairman: Dr. Hector Pomares and Dr. German Gutierrez Sanchez

Signal Classification using Covariance Matrices: A Riemannian Geometry Framework

Shaelyn G. Divins, Joshua S. Beard, Nenad Mijatovic, Anthony O. Smith, Adrian M.Peter, Dean A. Clauter and Rana Haber

Combining Support Vector Regression with Scaling Methods for Highway TollgatesTravel Time and Volume Predictions

Amanda Yan Lin, Mengcheng Zhang and Selpi Selpi

Functional Data Classification by Discriminative Interpolation with Features

Rana Haber, Anand Rangarajan, Nenad Mijatovic, Anthony O. Smith and Adrian M.Peter

Session B.3: Data Preprocessing Methods in Time Series

Chairman: Dr. Barbel Finkenstadt

Telescope: A Hybrid Forecast Method for Univariate Time Series

Marwin Zufle, Andre Bauer, Nikolas Herbst, Valentin Curtef and Samuel Kounev

Rainfall Measurements from Commercial Cellular Networks

Reason L. Machete, Leonard A. Smith and Nnyaladzi Batisani

Understanding Instantaneous frequency detection: A discussion of Hilbert-HuangTransform versus Wavelet Transform

Maximiliano Bueno Lopez, Marta Molinas and Geir Kulia

Session A.4: Forecasting performance evaluation

Chairman: Dr. Jacek Leskow

Simplex combination and selection of forecasters

Antonio S. Martın Arroyo

Forecasting via Fokker-Planck using conditional probablilites

Chris Montagnon

Forecasting UK House Prices During Turbulent Periods

Alisa Yusupova and Efthymios Pavlidis

3

ITISE 2017 Conference Program

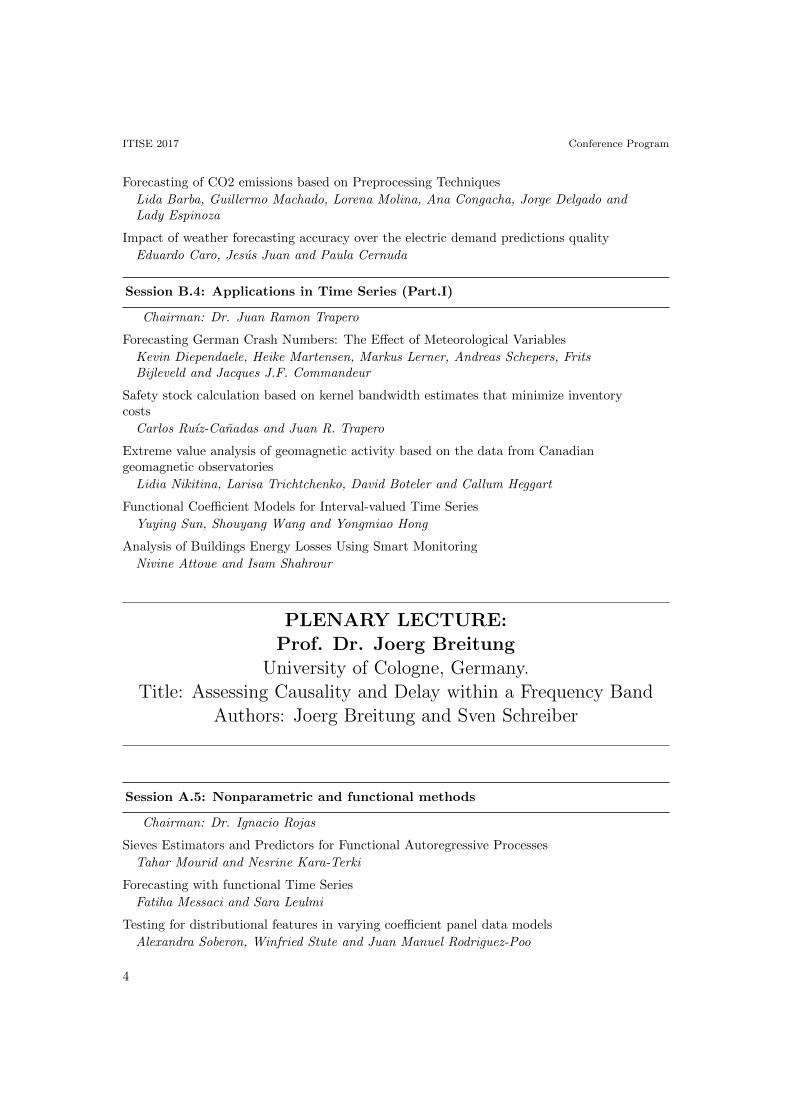

Forecasting of CO2 emissions based on Preprocessing Techniques

Lida Barba, Guillermo Machado, Lorena Molina, Ana Congacha, Jorge Delgado andLady Espinoza

Impact of weather forecasting accuracy over the electric demand predictions quality

Eduardo Caro, Jesus Juan and Paula Cernuda

Session B.4: Applications in Time Series (Part.I)

Chairman: Dr. Juan Ramon Trapero

Forecasting German Crash Numbers: The Effect of Meteorological Variables

Kevin Diependaele, Heike Martensen, Markus Lerner, Andreas Schepers, FritsBijleveld and Jacques J.F. Commandeur

Safety stock calculation based on kernel bandwidth estimates that minimize inventorycosts

Carlos Ruız-Canadas and Juan R. Trapero

Extreme value analysis of geomagnetic activity based on the data from Canadiangeomagnetic observatories

Lidia Nikitina, Larisa Trichtchenko, David Boteler and Callum Heggart

Functional Coefficient Models for Interval-valued Time Series

Yuying Sun, Shouyang Wang and Yongmiao Hong

Analysis of Buildings Energy Losses Using Smart Monitoring

Nivine Attoue and Isam Shahrour

PLENARY LECTURE:Prof. Dr. Joerg Breitung

University of Cologne, Germany.Title: Assessing Causality and Delay within a Frequency Band

Authors: Joerg Breitung and Sven Schreiber

Session A.5: Nonparametric and functional methods

Chairman: Dr. Ignacio Rojas

Sieves Estimators and Predictors for Functional Autoregressive Processes

Tahar Mourid and Nesrine Kara-Terki

Forecasting with functional Time Series

Fatiha Messaci and Sara Leulmi

Testing for distributional features in varying coefficient panel data models

Alexandra Soberon, Winfried Stute and Juan Manuel Rodriguez-Poo

4

ITISE 2017 Conference Program

Time Series predictor based on deterministic and stochastic assumptions

Pedro Cadahia, Jose Manuel Bravo Caro, Manuel Emilio Gegundez-Arias andAntonio Golpe

Session B.5: Nonstationarity Analysis in Time Series

Chairman: Dr. Wolfgang Konen

Functional and fraction of time models in the analysis of periodically correlated time series

Jacek Leskow

A Modified EM Algorithm for Parameter Estimation in Linear Models withTime-Dependent Autoregressive and t-Distributed Errors

Boris Kargoll, Mohammad Omidalizarandi, Hamza Alkhatib and Wolf-Dieter Schuh

Copulas for Modeling the Relationship between the Inflation and the Exchange Rates

Laila Ait Hassou, Fadoua Badaoui, Cyrille Okou Guei, Amine Amar, Abdelhak Zoglatand Elhadj Ezzahid

Multitaper Spectral Estimation for the Continuous Wavelet Transform with the MorletMother Wavelet

Guillaume Lenoir

Fractal analysis applied to light curves of pulsating stars

Sebastiano de Franciscis, Javier Pascual Granado, Juan Carlos Suarez and RafaelGarrido Haba

5

ITISE 2017 Conference Program

Tuesday, September 19, 2017

Session A.6: Computational Intelligence methods for Time Series (Part.II)

Chairman: Dr. Hector Pomares and Dr. German Gutierrez Sanchez

Multiplicative Seasonal Neural Network Model Based on Robust Learning Algorithm

Ozge Gundogdu and Erol Egrioglu

Local selection of learning data for neural networks in prediction of PM10 pollution

Krzysztof Siwek and Stanislaw Osowski

An Incremental von Mises Mixture Framework for Modelling Human Activity StreamingData

Eris Chinellato, Kanti Mardia, David Hogg and Anthony G. Cohn

Simulation of Defect Prediction over Time in Building Facade

Woo-Ram Kim, Kichang Jeong, Yongdeok Jeon, Jinhong Park, Heeyoung Jeong andJae-Seob Lee

Session B.6.A: Recent Developments on Time-Series Modelling for FinancialData

Chairman: Dr. Fredj Jawadi

Multidimensional time-frequency analysis of the CAPM

Roman Mestre and Michel Terraza

Bank-Based Financial Development and Economic Growth In Sacu Economies

Joel Hinaunye Eita

Prediction of High-Dimensional Time-Series with Exogenous Variables Using ExtendedKoopman Operator Framework in Reproducing Kernel Hilbert Space

Jia-Chen Hua, Farzad Noorian, Philip H.W. Leong, Gemunu Gunaratne and JorgeGoncalves

Session B.6.B: Advanced mathematical methodology in Time Series (Part.I)

Chairman: Dr. Bernd Sussmuth

A New Estimation Technique for AR(1) Model with Long-tailed Symmetric Innovations

Aysen Dener Akkaya and Ozlem Turker Bayrak

Eigenvalues distribution limit of covariance matrices with AR processes entries

Zahira Khettab and Tahar Mourid

On methods to assess the significance of community structure in networks of financialtime series

Argimiro Arratia and Martı Renedo

6

ITISE 2017 Conference Program

PLENARY LECTURE:Dr. Travis Berge

Senior Economist. Board of Governors of the Federal ReserveSystem (USA)

Title: Understanding Survey-based Expectations

Session A.7: Econometric Forecasting

Chairman: Dr.Roger Hammersland and Dr.Argimiro Arratia

Untangling the inefficiency of hotel industry: the Portuguese Teixeira Duarte Hotelchain analysis

Nuno Ferreira and Manuela de Oliveira

Predicting the financial status of companies using data balancing and classificationmethods

Huthaifa Aljawazneh, Antonio Mora Garcıa and Pedro Castillo Valdivieso

Combining forecasts to capture realized volatility dynamics

Danilo Carita, Giovanni De Luca and Giampiero M. Gallo

Financial variables and the real economy: Evidence using a data based procedure ofSimultaneous Structural Model Design

Roger Hammersland

Session B.7: Applications in Time Series (Part.II)

Chairman: Dr. Eris Chinellato and Dr. Martin Hanel

Astronomical Time Delay Estimations

Mariko Kimura, Hyungsuk Tak and Taichi Kato

Advanced Symbolic Time Series Analysis in Cyber Physical Systems

Roland Ritt, Paul O’Leary, Christopher Josef Rothschedl and Matthew Harker

Period Analysis in Astronomy by using Lasso

Keisuke Isogai

A Non-stationary Index-flood Model With Local Likelihood Smoothing for DroughtAssessment

Filip Strnad, Martin Hanel, Vojtech Moravec and Adam Vizina

Advantage Analysis of Cross-Border Trade by Grey Model in Time Series

Qing Li

7

ITISE 2017 Conference Program

Session A.8: Deep Learning and Time Series Analysis

Chairman: Dr. Marijana Cosovic

Deep Learning for Detection of BGP Anomalies

Marijana Cosovic, Slobodan Obradovic and Emina Junuz

Abnormal State Prediction based on Deep Learning using Multiple Time SeriesProduction Process Data

Shigeru Fujimura and Wen Song

Session B.8: Applications in Time Series (Part.III)

Chairman: Dr. Minvydas Ragulskis

A multistep-ahead predictor of hourly potential evapotranspiration for irrigationtriggering in horticultural nurseries

Rousseau Tawegoum

Sequential Motor Unit Number estimation

Peter Ridall

Forecasting of Demand on Raw for Dairy Products

Marina Arkhipova, Viacheslav Sirotin and Kirill Arkhipov

Session A.9: Advanced mathematical methodology in Time Series (Part.II)

Chairman: Dr. Hitoaki Yoshida

A New Approach for Time Series Decomposition and Prediction

Yading Yue, Guangan Zhuang, Rong Zhang, Jianchun Zhao and Lichun Liu

Robust estimation of covariance and correlation functions of a stationary multivariateprocess

Higor Cotta, Valderio Reisen, Pascal Bondon and Wolfgang Stummer

Time Series Anomaly Detection with Discrete Wavelet Transforms and MaximumLikelihood Estimation

Markus Thill, Wolfgang Konen and Thomas Baeck

Kurtosis Computations and Black-Scholes Model with GARCH Volatility

Muhammad Sheraz

Short-term time series forecasting based on internal smoothing of Pade interpolants

Minvydas Ragulskis, Kristina Lukoseviciute, Tadas Telksnys and Zenonas Navickas

Global Linkages across Sectors and Frequency Bands: A band spectral panel regressionapproach

Bernd Sussmuth and Jingjing Lyu

8

ITISE 2017 Conference Program

Session B.9: Energy Forecasting

Chairman: Dr. Adam Vizina and Dr. Vanessa Haykal

Fuel Consumption Estimation for Climbing Phase

Jingjie Chen and Yongping Zhang

Energy Prediction of Access Points in Wi-Fi Networks Using Time Series Modeling

David Rodrıguez Lozano, Juan A. Gomez-Pulido and Arturo Duran Domınguez

A Combination of Variational Mode Decomposition with Neural Networks on HouseholdElectricity Consumption Forecast

Vanessa Haykal, Hubert Cardot and Nicolas Ragot

Nonparametric panel stationarity testing. An application to crude oil production

Manuel Landajo, Marıa Jose Presno and Paula Fernandez Gonzalez

Detection of temperature break point for gas storage

Andrzej Szczurek, Andrzej Kielbik and Monika Maciejewska

Dynamics of Memory in Investor Attention to Energy Market

Ravi Prakash Ranjan and Malay Bhattacharyya

PLENARY LECTURE:Dr. Anna Korzeniewska

Johns Hopkins University School of Medicine (USA)Title: Event Related Causality analysis of electrocorticographic

(ECoG) time series as diagnostic tool for epileptic surgeryAuthors: Anna Korzeniewska, Piotr Franaszczuk and Nathan

Crone

Session A.10: Future of Mathematical and Logical Structures behind TimeSeries Analysis and History

Chairman: Dr. Kalle Saastamoinen

The Dependence Structures of Non-Stationary Bivariate INAR(1) Processes: The Caseof the Bivariate Poisson Innovations

Naushad Mamode Khan, Yuvraj Sunecher and Vandna Jowaheer

Similarity Analysis of Time Interval Data Sets Regarding Time Shifts and Rescaling

Marc Haßler, Sabina Jeschke and Tobias Meisen

9

ITISE 2017 Conference Program

Logical Comparison Measures in Classification of Data

Kalle Saastamoinen

Session B.10: Structural Time Series Models

Chairman: Dr. Krzysztof Siwek

Nonlinear Dynamical Analysis of Twitter Time Series

Andrey V. Dmitriev, Vitaly Silchev, Victor Dmitriev and Svetlana Maltseva

Interpolation of ARMA processes with infinitely divisible white noise

Argimiro Arratia, Alejandra Cabana and Enrique Cabana

Forecasting Local Inflation with Global Inflation: When Economic Theory Meets the Facts

Enrique Martinez-Garcia and Roberto Duncan

Session A.11/B.11: Poster Session

Chairman: Dr. Fernando Rojas

An Estimating Parameter of Local Polynomial Regression on Economic Time Series Data

Autcha Araveeporn

Temporal Patterns Analysis of Paddy Production in Sri Lanka

Nanayakkarawasam Bataduwa Widanelage Imali Udeshika

Modeling and temporal patterns analysis of electricity demand in Sri Lanka

Nanayakkarawasam Bataduwa Widanelage Imali Udeshika

A Tunisian Economic Activity Index using Macroeconomic Data and Sovereign CreditRatings

Adel Karaa, Sofiene Amri and Azza Bejaoui

Volume, durations and jumps in SV models for the evolution of intraday financial volatility

Antonio Santos

A Comparative Study on Time Series Analysis for Forecasting Domestic Civil AviationPassenger Volume in India

Raghav Lakhotia and Harmeet Singh

Identification and Estimation issues in Exponential Smooth Transition AutoregressiveModels

Daniel Buncic

Research on RGB-D Action Recognition Based on Timing Sequence Analysis of GroupSparse Coding

Yun Liu, Wei Chang, Hui Li and Chuanxu Wang

Modeling of p-order persistent time series by the modified Langevin equation

Zbigniew Czechowski

Development of a Routing Procedure to Assist an Earth Systems Model with LongTerm Coastal Discharge Predictions

Josefine Wilms and Marcus Thatcher

10

ITISE 2017 Conference Program

Estimation and tests with bivariate censored data

Nahima Nemouchi, Aboud Nemouchi and Mohamed Boukeloua

Bootstrap confidence intervals for conditional density function in Markov processes

Ines Barbeito Cal, Ricardo Cao and Dimitris Politis

Autoregressive model order determination

Ventsislav Nikolov

Measuring (Nonlinear) Granger Causality in Quantiles

Abderrahim Taamouti and Xiaojun Song

The analysis of variability of short data sets based on Mahalanobis distance calculationand surrogate time series testing

Teimuraz Matcharashvili, Natalia Zhukova, Tamaz Chelidze, Evgeni Baratashvili,Tamar Matcharashvili and Manana Janiashvili

Robust and Accurate Inference via a Mixture of Gaussian and Student’s t Errors forPulsar Timing Data Analysis

Hyungsuk Tak, Justin A. Ellis and Sujit K. Ghosh

Geomagnetic Storms, Earthquakes and their Influence on GNSS Coordinate Time Series

Inese Varna, Janis Balodis and Diana Haritonova

Time Series Model Selection by Rolling Windows

Elif Akca and Ceylan Yozgatligil

Risk function kernel estimators and Single Index Model.

Naouel Belkhir

On factor-augmented univariate forecasting

Niang Abdou-Aziz

Robust Multivariate Time Series Analysis in Nonlinear Models with Autoregressive andt-Distributed Errors

Hamza Alkhatib, Boris Kargoll and Jens-Andre Paffenholz

Electricity price forecasting using a hybrid time series model

Busra Tas and Ceylan Yozgatligil

The Demand and Supply Model of Housing: Evidence from the Turkish Housing Market

Yusuf Varli

Robust autocovariance estimation from the frequency domain

Higor Cotta, Valderio Reisen and Pascal Bondon

Inhomogeneous Point Process Intensity Dynamics Identification based on availablePrecedents

Viacheslav Antsiperov

Forecasting Intraday Risk Measures using Multiplicative Component GARCH Modeland Multimodal Distributions

Aymeric Thibault and Pascal Bondon

Alternative Solution for the Adjustment of Defect Liability Period in Construction

Kichang Jeong, Woo-Ram Kim and Jaeseob Lee

11

ITISE 2017 Conference Program

The role of probability in the positioning of gas stations

Milos Pavlovic

Penalized Latent Class Model for Clustering with Application to Variable Selection

Abdelghafour Talibi, Boujemaa Achchab, Ramon Gutierrez-Sanchez and Ahmed Nafidi

Modeling and analysis of the cosmic rays variations during periods of heliosphericdisturbances on the basis of wavelet transform and neural networks

Oksana Mandrikova and Timur Zalyaev

Exploring a century of Savoy history using hidden-Markov models with Beta-inflateddistributions

Julien Alerini and Madalina Olteanu

Minimizing the Number of Probes and Maximizing Classification Performance for P300BCI speller

Weilun Wang, Horie Shigeki and Goutam Chakraborty

Forecasts of electricity consumption in selected sectors of the Polish economy.

Marek Kott

Estimation of the crustal velocity field in Baza and Galera faults from GPS positiontime series in 2009-2012

Antonio J. Gil

12

ITISE 2017 Conference Program

Wednesday, September 20, 2017

Session A.12: Dimensionality reduction and Similarity measures for Timeseries data analysis and its applications.

Chairman: Dr. Goutam Chakraborty and Dr. Basabi Chakraborty

Linear Trend Filtering via Adaptive Lasso

Matus Maciak

A time series clustering technique to analyze the stock market movement after thebudget announcement

Arup Mitra, Saptarsi Goswami, Basabi Chakraborty, Arun Jalan and Amlan Chakrabarti

An Efficient Anomaly Detection in Quasi Periodic Time-series Data - A Case Studywith ECG

Goutam Chakraborty, Takuya Kamiyama, Hideyuki Takahashi and Tetsuo Kinoshita

A novel genetic algorithm based similarity measure for time series classification

Basabi Chakraborty and Sho Yoshida

New Hybrid Feature Selection Algorithm based on Consistency Measures and SimulatedAnnealing Search

Adrian Pino Angulo, Kilho Shin and Takako Hashimoto

Design Aircraft Engine Bivariate Data Phases using Change-Point Detection Methodand Self-Organizing Maps

Cynthia Faure, Jean-Marc Bardet, Jerome Lacaille and Madalina Olteanu

Human Gait Recognition by Deep Convolutional Activation Feature of Recurrence Plotfor Accelerometer Time Series

Yusuke Manabe

Session B.12: Recent Developments on Time-Series Modelling

Chairman: Dr. Madalina Olteanu

Method for modeling and analysis of natural time series

Oksana Mandrikova, Nadezhda Fetisova and Yury Polozov

Modeling and analysis of the cosmic rays variations during periods of heliosphericdisturbances on the basis of wavelet transform and neural networks

Oksana Mandrikova and Timur Zalyaev

Analyzing Spatial Dissimilarities via Effective-Time Series

Madalina Olteanu and Julien Randon-Furling

Educational Data Mining: A Case Study of Data Pre-Processing and Investigation ofStudents’ Academic Achievement for Artificial Intelligence Classifier

Usamah Mat and Norlida Buniyamin

Forecasting Diffusion Investments in FinTech Using Diffusion Models

Miriam Scaglione and Simone Dimitriou

13

ITISE 2017 Conference Program

PLENARY LECTURE:Prof. Dr. Joan Paredes

European Central Bank. Germany.Title: Fiscal targets. A guide to forecasters?

Authors: Joan Paredes, Gabriel Perez-Quiros and Javier J. Perez

Session A.13: Bio-medical Time Series Analysis

Chairman: Dr. Ignacio Rojas

Quantitative characterization of intracellular calcium signals

Iker Malaina, Carlos Bringas, Alberto Perez-Samartın, Luis Martinez and IldefonsoMartınez de La Fuente

Correlation Dimension Estimation from EEG Time Series for Alzheimer DiseaseDiagnostics

Martin Dlask and Jaromir Kukal

An application of the GAM-PCA-VAR model to respiratory disease and air pollution data

Marton Ispany, Juliana Bottoni de Souza, Valderio A. Reisen, Glaura C. Franco,Pascal Bondon and Jane Meri Santos

Session B.13: Chaos and Random in Time Series

Chairman: Dr. Matus Maciak and Dr. Salih Ergun

Fixed, random effects and temperature trends

Azzouz Dermoune, Khalifa Es-Sebaiy, Mohammed Es.Sebaiy and Jabrane Moustaaid

Cryptanalysis of a Random Number Generator Based on a Chaotic Ring Oscillator

Salih Ergun

Factors Affecting Randomness in Pseudo-Random Number Series Extracted fromChaotic Time Series of Logistic Map and Chaos Neural Network

Hitoaki Yoshida, Masatomo Sasaki, Takeshi Murakami, Shogo Shimono and SatoshiKawamura

Chaos Neural Network for Ultra-Long Period Pseudo-Random Number Generator

Hitoaki Yoshida, Yukito Kon and Takeshi Murakami

Session A.14: Ensemble forecasting

Chairman: Dr. Julien Randon-Furling

A new approach to nowcast economic time series using ensembles of hidden Markov andArima models

Alvaro Gomez-Losada and Panayotis Christidis

14

ITISE 2017 Conference Program

Ensemble Learning Framework for Predicting Project Cost Overrun Levels inConstruction Procurement Auctions

Hyosoo Moon, Trefor P. Williams and Moonseo Park

Time Series Forecasting applying Data Transformation and Neural Networks Ensembles

German Gutierrez, M. Paz Sesmero Lorente and Araceli Sanchis

Session B.14: Seismic time series

Chairman: Dr. Lidia Nikitina

Dynamical evolution of the community structure of complex network inherent in seismictime series

Norikazu Suzuki

Real-Time Radioactive Precursor of the April 16, 2016 Mw 7.8 Earthquake in Ecuador

Theofilos Toulkeridis, Fernando Mato, Katerina Toulkeridis-Estrella, Juan CarlosPerez Salinas, Santiago Tapia and Walter Fuertes

Analysis of time series of earthquake occurrence in Caucasus

Teimuraz Matcharashvili, Zhukova Natalia, Ekaterine Mepharidze and AleksandreSborshchikovi

PLENARY LECTURE:Dr. Pekka Koponen

Senior Scientist, D.Sc.Tech VTT Technical Research Centre ofFinland, Energy Systems

Title: Improving the performance of machine learning models byintegrating partly physical control response models in short-term

forecasting of aggregated power system loadsAuthors: Pekka Koponen, Harri Niska and Reino Huusko

Session A.15: Virtual Presentations

Chairman: Dr. Ignacio Rojas

Intelligent approach to vehicle routes planning base on artificial neural networksprediction model

Daniel Kubek and Pawel Wiecek

Performance Analysis of Time Series Forecasting of Ebola Casualties Using MachineLearning Algorithms.

Manish Kumar Pandey and Karthikeyan Subbiah

15

ITISE 2017 Conference Program

On the relationship between GHGs and Global Temperature Anomalies: Multilevelrolling analysis and copula calibration

Elettra Agliardi, Christian Cech and Thomas Alexopoulos

Joint multifractal description of the influence of climatic variables on referenceevapotranspiration time series

Ana Belen Ariza Villaverde, Pablo Pavon Domınguez, Juan Marıa Gomez Lopez,Eduardo Gutierrez de Rave Aguera and Francisco Jose Jimenez Hornero

Forecasting Power Output of Photovoltaic Systems Using Linear, Non-Linear andEnhanced Models

Georgia Xanthopoulou, Athanasios Salamanis, Dionysios Kehagias, Ioannis Antoniou,Charalampos Bratsas and Dimitrios Tzovaras

Comparing Three Time Series Segmentation Methods via Novel Evaluation Criteria

Huynh Thi Thu Thuy, Vo Thi Ngoc Chau and Duong Tuan Anh

Comparative analysis of criteria for filtering time series of word usage frequencies

Inna Belashova and Vladimir Bochkarev

Recurrent Fuzzy Regression Functions Approach based on IID Innovations Bootstrapwith Rejection Sampling

Ali Zafer Dalar, Eren Bas, Erol Egrioglu, Ufuk Yolcu and Ozge Cagcag Yolcu

A New Fuzzy Time Series Method Based on Fuzzy c-means and Recurrent Pi-SigmaNeural Network

Cem Kocak, Erol Egrioglu, Ufuk Yolcu and Eren Bas

Attractor modelling effect in matter’s microstructure data analysis: a predictiveindicator of material scales

Fairouz Bettayeb

Spark and Solr: a powerful and ergonomic combination for online search in the BigData environment (case of the UAE)

Karim Aoulad Abdelouarit, Boubker Sbihi and Noura Aknin

Generalized nonparametric method for analyzing economic data inconsistent with themodel of single rational representative consumer

Nikolay Klemashev and Alexander Shananin

Time series and artificial intelligence with genetic algorithms hybrid approach for rareearths price prediction.

Fernando Sanchez Lasheras, Sergio Luis Suarez Gomez, Maria Victoria RiesgoGarcıa, Alicia Krzemien and Ana Suarez Sanchez

A GIS-based Model for Cholera Forecast

Dau Xuan Hoang and Thi Ngoc Anh Le

Nonparametric Time Series Analysis in a very, very small sample: an application in aclinical psychology context.

Samantha Bouwmeester and Gabriela Koppenol-Gonzalez Marin

16

Organized and supported by:

Sessions A.Salón de Grados Edificio Mecenas

Sessions B.Salón de Grados

Facultad de Ciencias