Embed Size (px)

Citation preview

INSU

RANC

E

187, Nazju Ellul Street, Gzira GZR 1629, Malta

t: +356 2133 1010 e: [email protected]

www.planit247.eu

Many people assume that their health insurance plan at home will also cover them whilst they’re abroad. In reality,

this is rarely the case. If you have no medical plan in place whilst travelling abroad, an exciting and enjoyable

experience could quickly turn in to a nightmare. This policy provides you with comprehensive medical coverage

worldwide*. With our network of over 20,000 medical providers and a 24-hour assistance helpline we will ensure you

are given the best possible medical care wherever you are in the world*. (Except the United States, its territories and

Possessions).

Unparalleled Medical Assistance.

Tangiers directly employs medical and administrative professionals in over 80 countries with fluency in fifty languages.

Our employees live and work beside our clients in onerous environments, because when they need healthcare the

most they should not have to wait.

Global Network, Local Presence

With our vast network of medical service and emergency care providers worldwide, Tangiers are able to move quickly

to analyze and satisfy immediate or emergency medical needs before they become bigger problems. Our agents speak

the local lingo, meaning they can translate to keep you and your doctor well informed; whether you need a knee guy

in Nairobi, a chopper in Chad, we’ll be able to help you. Even assistance companies that are generally experienced

and reliable can face scenarios that could be considered ‘assistance black holes’. By having our own employees on the

ground, the local knowledge and care we can provide can literally fill these black holes and save lives.

Cover for War and Terrorism is automatically Included*

*as long as insured is not actively participating in war or terrorism.

Terrorist activity has increased in frequency and severity over the last two decades. We have seen an increase in

attacks in more volatile territories, such as Iraq and Afghanistan, but also in countries where you might feel safe, such

as Paris, London or Madrid. Many other travel medical providers shy away from providing cover for travel to higher

risk areas. It might not be immediately obvious to you, but if you read the small print they will often include the

exclusion: “The Company will not pay if there is a travel advisory in effect on or within six months prior to the Insured

Person’s date of arrival in the Host Country.”

This exclusion hugely restricts coverage in a number of countries around the world. battleface™ provides coverage for

incidents resulting from passive war and terrorism where many other policies won’t.

You can buy battleface™ if you are aged 18 years or over and not yet 65 years of age (provided there is at least one

adult insured). You will need to ensure you have received all immunizations recommended by your Home Country

prior to entry in to the Host Country. Cover is not provided by battleface™ if you are in the military or intend to carry

a weapon.

Length of Coverage: The minimum length of coverage is 5 days, and you can buy any number up to 365 days.

Why do you need a travel medical expense plan?

Why battleface™?

Who can buy?

The coverage provided by this policy is not permanent health insurance or comprehensive health insurance,

or any other kind of primary health insurance or health plan. It shall only relate to accidental bodily injury

and/or illness as provided for below. Coverage for acts of war and/or terrorism is included in this policy,

subject to all restrictions and exclusions contained herein.

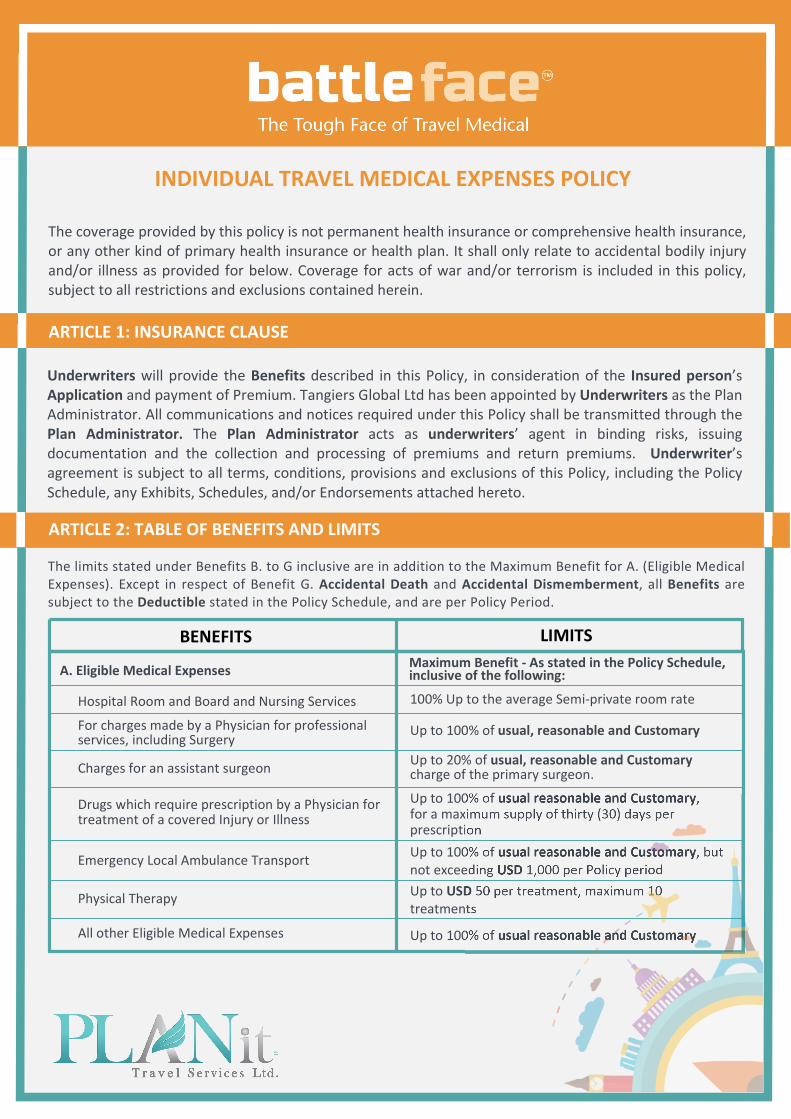

INDIVIDUAL TRAVEL MEDICAL EXPENSES POLICY

ARTICLE 1: INSURANCE CLAUSE

Underwriters will provide the Benefits described in this Policy, in consideration of the Insured person’s

Application and payment of Premium. Tangiers Global Ltd has been appointed by Underwriters as the Plan

Administrator. All communications and notices required under this Policy shall be transmitted through the

Plan Administrator. The Plan Administrator acts as underwriters’ agent in binding risks, issuing

documentation and the collection and processing of premiums and return premiums. Underwriter’s

agreement is subject to all terms, conditions, provisions and exclusions of this Policy, including the Policy

Schedule, any Exhibits, Schedules, and/or Endorsements attached hereto.

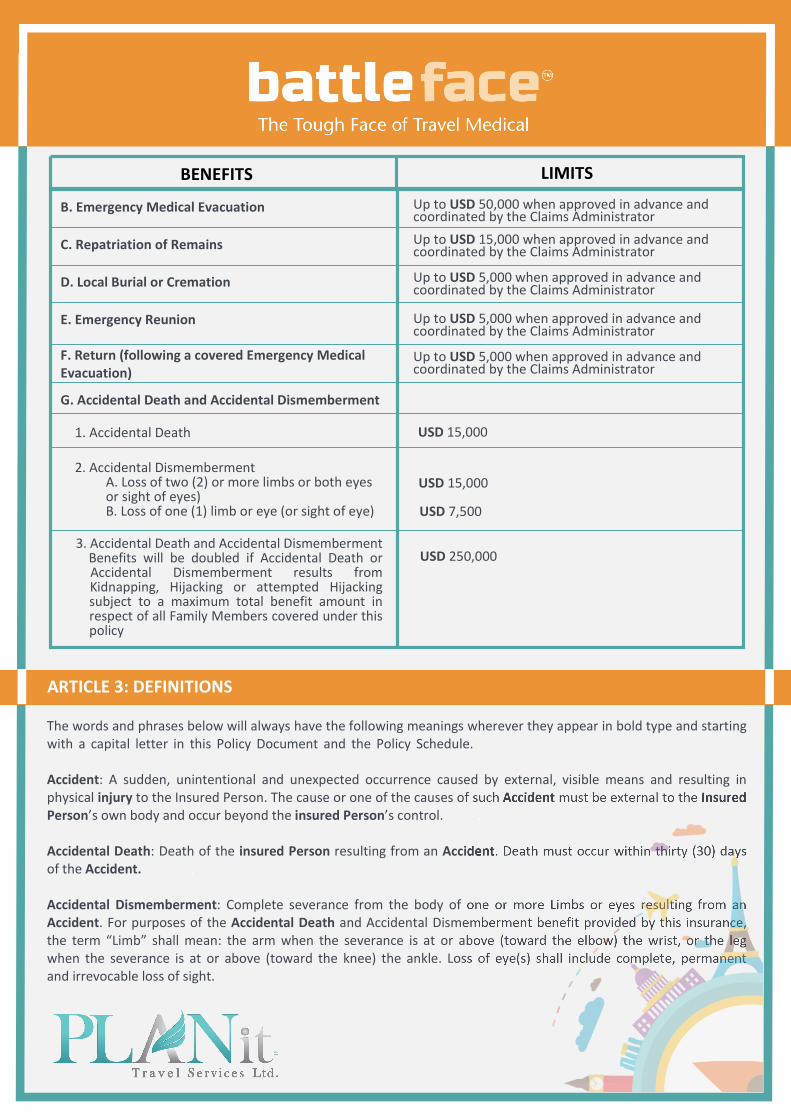

ARTICLE 2: TABLE OF BENEFITS AND LIMITS

The limits stated under Benefits B. to G inclusive are in addition to the Maximum Benefit for A. (Eligible Medical

Expenses). Except in respect of Benefit G. Accidental Death and Accidental Dismemberment, all Benefits are

subject to the Deductible stated in the Policy Schedule, and are per Policy Period.

BENEFITS LIMITS

A. Eligible Medical Expenses

Up to 100% of usual reasonable and Customary

Hospital Room and Board and Nursing Services

Maximum Benefit - As stated in the Policy Schedule, inclusive of the following:

100% Up to the average Semi-private room rate

Up to 100% of usual, reasonable and Customary

Up to 20% of usual, reasonable and Customary charge of the primary surgeon.

Up to 100% of usual reasonable and Customary, for a maximum supply of thirty (30) days perprescription

Up to 100% of usual reasonable and Customary, but

not exceeding USD 1,000 per Policy period

Up to USD 50 per treatment, maximum 10

treatments

All other Eligible Medical Expenses

Physical Therapy

Emergency Local Ambulance Transport

Drugs which require prescription by a Physician fortreatment of a covered Injury or Illness

Charges for an assistant surgeon

For charges made by a Physician for professionalservices, including Surgery

BENEFITS LIMITS

B. Emergency Medical Evacuation Up to USD 50,000 when approved in advance and coordinated by the Claims Administrator

C. Repatriation of Remains Up to USD 15,000 when approved in advance and coordinated by the Claims Administrator

D. Local Burial or Cremation Up to USD 5,000 when approved in advance and coordinated by the Claims Administrator

E. Emergency Reunion Up to USD 5,000 when approved in advance and coordinated by the Claims Administrator

F. Return (following a covered Emergency Medical

Evacuation)

Up to USD 5,000 when approved in advance and coordinated by the Claims Administrator

G. Accidental Death and Accidental Dismemberment

1. Accidental Death USD 15,000

2. Accidental DismembermentA. Loss of two (2) or more limbs or both eyes or sight of eyes)B. Loss of one (1) limb or eye (or sight of eye)

USD 15,000

USD 7,500

3. Accidental Death and Accidental Dismemberment Benefits will be doubled if Accidental Death or

Accidental Dismemberment results from Kidnapping, Hijacking or attempted Hijacking subject to a maximum total benefit amount in respect of all Family Members covered under thispolicy

USD 250,000

ARTICLE 3: DEFINITIONS

The words and phrases below will always have the following meanings wherever they appear in bold type and starting

with a capital letter in this Policy Document and the Policy Schedule. .

Accident: A sudden, unintentional and unexpected occurrence caused by external, visible means and resulting in

physical injury to the Insured Person. The cause or one of the causes of such Accident must be external to the Insured

Person’s own body and occur beyond the insured Person’s control. .

Accidental Death: Death of the insured Person resulting from an Accident. Death must occur within thirty (30) days

of the Accident. .

Accidental Dismemberment: Complete severance from the body of one or more Limbs or eyes resulting from an

Accident. For purposes of the Accidental Death and Accidental Dismemberment benefit provided by this insurance,

the term “Limb” shall mean: the arm when the severance is at or above (toward the elbow) the wrist, or the leg

when the severance is at or above (toward the knee) the ankle. Loss of eye(s) shall include complete, permanent

and irrevocable loss of sight.

Act of Terrorism: An act, including but not limited to the use of force or violence and/or the threat thereof, of any

person or group(s) of persons, whether acting alone or on behalf of or in connection with any organization(s) or

government(s) committed for political, religious, ideological or similar purposes including the intention to influence

any government and/or to put the public, or any section of the public, in fear. .

AiDs: Acquired Immune Deficiency Syndrome as that term is defined by the United States Centers for Disease Control.

ArC: AiDs Related Complex as that term is defined by the United States Centers for Disease Control. .

Amateur Athletics: A sport or other athletic activity that is organized and/or sanctioned, involving regular or

scheduled practices and/or regular or scheduled games. This definition does not include athletic activities that are

non-contact and engaged in by an insured Person solely for recreational, entertainment or fitness purposes and not

for wage, reward or profit. .

pplication: The fully answered Application that is completed by or on behalf of the insured Person, submitted to the

Plan Administrator, and maintained on file with the Plan Administrator. .

Benefits: The Eligible Expenses that will be paid under this Policy for covered costs incurred while coverage is in effect.

Benefit Period: Up to one hundred and eighty (180) consecutive days beginning on the first day of diagnosis or

treatment (whichever occurs first) of a covered injury or illness that occurs during the Policy Period.

Claims Administrator: Tangiers International Ltd 54, Melita Street, Valletta, VLT 1122.

Contact sports: A sport or other athletic activity that necessarily involves physical contact with opposing players as

part of normal play, including but not limited to, American football, boxing, ice hockey, rugby, soccer, and wrestling.

Custodial Care: That type of care or service, wherever furnished and by whatever name called, that is designed

primarily to assist an Insured Person in performing the activities of normal daily living, including but not limited to

eating, drinking and washing. This includes non-acute care for the comatose, semi-comatose, paralyzed or mentally

incompetent patients until they are fit to return to their Home Country. .

Deductible: The USD amount of eligible expenses, specified in the Policy Schedule that the Insured Person must pay

per Policy Period, before Benefits are paid hereunder. .

Delivery: Procedures concerning pregnancy or childbirth. .

Durable Medical Equipment: A standard basic hospital bed and/or a standard basic wheelchair. .

Educational or Rehabilitative Care: Care for restoration (by education or training) of the Insured Person’s ability to

function in a normal or near normal manner following an Illness or Injury. This type of care includes, but is not limited

to, vocational or occupational therapy and speech therapy. .

Effective Date: The Effective Date stated in the Policy Schedule at: :

a. 12:01am GMT; or

b. The moment the Plan Administrators receive the Application and correct premium; or

c. The moment the Insured Person departs from his or her Home Country whichever occurs last.

Emergency: A medical condition manifesting itself by acute signs or symptoms which could reasonably result in

placing the Insured Person’s life or limb in danger if medical attention is not provided within twenty four (24) hours.

Emergency Dental Treatment – The emergency dental treatment and dental Surgery necessary to restore or replace

sound natural teeth lost or damaged in an Accident which was covered under this insurance, provided that this shall

not include any form of routine dental examination, care or treatment.

Emergency Room: That part of a Hospital designated for the immediate care of Emergency medical conditions.

Extended Care Facility: An institution, or a distinct part of an institution, which is licensed as a Hospital, Extended

Care Facility or rehabilitation facility by the jurisdiction in which it operates; and is regularly engaged in providing

twenty four (24) hour skilled nursing care under the regular supervision of a Physician and the direct supervision of a

Registered Nurse; and maintains a daily record on each patient; and provides each patient with a planned program

of observation prescribed by a Physician; and provides each patient with active treatment of an Illness or Injury. This

does not include a facility primarily for rest, the aged, Substance Abuse treatment, Custodial Care, nursing care or for

care of Mental Health Disorders or the mentally incompetent.

Family Member: the Insured Person’s fiancé(e) spouse or civil partner (or someone of either sex with whom the

Insured Person has been living as though they were their spouse or civil partner), or the grandchild, child, brother,

sister, parent, grandparent, grandchild, step-brother, step-sister, step-parent, parent-in-law, son-in-law, daughter-in

law, sister-in-law, brother-in-law, aunt, uncle, nephew, niece, of the Insured Person .

GMT: Greenwich Mean Time

Hijacking: Seizing control of a conveyance in transit by use of force.

HIV+: Laboratory evidence defined by the United States Centers for Disease Control as being positive for Human

Immunodeficiency Virus infection.

Home Country: The country where the Insured Person principally resides as declared on the Application and stated in

the Policy Schedule.

Home Health Care Agency: A public or private agency or one of its subdivisions, which operates pursuant to law and

is regularly engaged in providing Home Nursing Care under the supervision of a Registered Nurse, and maintains a

daily record on each patient, and provides each patient with a planned program of observation and treatment by a

Physician.

Home Nursing Care: Services provided by a Home Health Care Agency and supervised by a Registered Nurse, which

are directed toward the personal care of a patient, provided always that such care is provided in lieu of Medically

Necessary Inpatient care in a Hospital.

Hospital: An institution which operates as a hospital pursuant to law, and is licensed by the country or administrative

unit in which it operates; and operates primarily for the reception, care and treatment of sick or injured persons as

Inpatients; and provides twenty four (24) hour nursing service by Registered Nurses Nurses on duty or call; and has a

staff of one or more Physicians available at all times; and provides organized facilities and equipment for diagnosis

and treatment of acute medical conditions on its premises; and is not primarily a rehabilitation facility, long-term

care facility, Extended Care Facility, nursing, rest, Custodial care or convalescent home, a place for the aged, drug

addicts, alcoholics or runaways; or similar establishment.

Host Country: The country(ies) stated in the Policy Schedule under Destination(s), being visited by the Insured Person

or where the Insured Person resides temporarily. This excludes the Insured Person’s Home Country and the United

States.

Illness: A sickness, disorder, pathology, abnormality, ailment, disease or any other medical, physical or health

condition. This does not include learning disabilities, attitudinal disorders or disciplinary problems.

Injury: Identifiable physical harm to the body caused by an Accident that requires medical treatment.

Inpatient: A patient who occupies a Hospital bed for more than twenty four (24) hours for medical treatment and

whose admission was recommended by a Physician.

Insured Person: Each person for whom an Application has been completed and who has been accepted for coverage

hereunder and is named in the Policy Schedule as an Insured Person.

Intensive Care Unit: A Cardiac Care Unit or other unit or area of a Hospital that meets the required standards of the

Joint Commission on Accreditation of Hospitals for Special Care Units or where appropriate, the relevant local

government or local health authority standards.

Investigational, Experimental or for Research Purposes: Terms used to describe procedures, services or supplies that

are by nature or composition, or are used or applied, in a way which deviates from generally accepted standards of

current medical practice.

Kidnapping: The taking away of a person by force, threat or deceit with intent to cause him or her to be detained

against his or her will for ransom or political purposes. For purposes of this insurance Kidnapping does not include

Kidnapping perpetrated by any Family Member of the kidnapped Person.

Medical Provider: A Hospital, Physician or other person or organization which provides medical services and/or

Supplies.

Medically Necessary: A service or supply which is necessary and appropriate for the diagnosis or treatment of an

Illness or Injury based on generally accepted current medical practice as determined by Underwriters. A service or

supply will not be considered Medically Necessary if it is provided only as a convenience to the Insured Person or

Medical Provider, and/or is not appropriate for the insured Person’s diagnosis or symptoms, and/or exceeds in scope,

duration or intensity that level of care which is needed to provide safe, adequate and appropriate diagnosis or

treatment of an Illness or Injury.

Mental Health Disorder: A mental or emotional disease or disorder which generally denotes a disease of the brain

with predominant behavioral symptoms; or a disease of the mind or personality, evidenced by abnormal behavior; or

a disorder of conduct evidenced by socially deviant behavior. This includes but is not limited to: psychosis, those

psychiatric illnesses listed in the current edition of the diagnostic and Statistical Manual for Mental Disorders of the

American Psychiatric Association.

Physician: A doctor of Medicine (MD), doctor of Dental Surgery (DDS), doctor of Dental Medicine (DDM) or a licensed

Physical Therapist or Physiotherapist. Physician does not include a doctor of Chiropractic (DC), a doctor of Osteopathy

(DO), a doctor of Psychology (Ph.D), a doctor of Psychiatry (Psy.D) or any other degree or designation. A Physician

must be currently licensed by the jurisdiction in which the services are provided, and the services provided must be

within the scope of that license. A Physician must be a person other than the Insured Person, the Insured Person’s

Relative or Family member, or one who ordinarily resides with the Insured Person.

Plan Administrator: Tangiers Global Ltd., St. Clare House, 30-33 Minories. London EC3N 1PE. United Kingdom.

Policy Period: The period of time not exceeding twelve (12) consecutive months beginning on the Effective Date and

ending on the Termination Date specified in the Policy Schedule.

Pre-existing Condition: Any:

(1) condition for which medical advice, diagnosis, care, or treatment (includes receiving services and supplies,

consultations, diagnostic tests or prescription medicines) was recommended or received during the two (2) years

immediately preceding the Policy Effective Date;

(2) condition that had manifested itself in such a manner that would have caused a reasonably prudent person to

seek medical advice, diagnosis, care, or treatment (includes receiving services and supplies, consultations, diagnostic

tests or prescription medicines) within the two (2) years immediately preceding the Policy Effective Date;

(3) Injury, Illness, sickness, disease, or other physical, medical, mental, or nervous conditions, disorder or ailment

(whether known or unknown) that, with reasonable medical certainty, existed at the time of application or within the

two (2) years immediately preceding the Policy Effective Date.

Preferred Medical Provider: Medical Providers designated by the Claims Administrator as preferred.

Principal Residence: The location, indicated on the Insured Person’s Application, where the Insured Person ordinarily

resides, but not including locations in the Host Country or in the United States.

Professional Sports: A sporting activity undertaken for wage, reward or profit.

Proof of Claim: A completed and signed Claimant’s Statement and Authorization form, together with any/all required

attachments, original itemized bills from Physicians, Hospitals and other Medical Providers, original receipts for any

expenses which have already been paid by or on behalf of the Insured Person, and any other documentation that is

deemed necessary by the Underwriters and/or the Claims Administrator.

Registered Nurse:

(1) A graduate nurse who has been registered or licensed to practice by the local authority Board of Nurse Examiners

or other state authority, and who is legally entitled to place the letters “RN” after his or her name; or

(2) Where (1) above is not appropriate it shall mean a nurse that has achieved the minimum training standards

required to legally register to legally practice nursing in their Home Country.

Relative: Biological or step parent; biological or step child; current spouse; biological or step-siblings; or sibling in law,

fiancé(e) or betrothed individual.

Sexually Transmitted Diseases: Syphilis, gonorrhea, lymphogranuloma venereum, chancroid, granuloma inguinale,

chlamydiosis, pelvic inflammatory disease, trichomoniasis, genital candidiasis, genital herpes, genital warts, amebiasis,

viral hepatitis, scabies, crab lice, cervical dysplasia, and bacterial vaginitis.

Substance Abuse: Alcohol, drug or chemical abuse, overuse or dependency.

Surgery: An invasive diagnostic procedure, or the treatment of Illness or Injury by manual or instrumental operations

performed by a Physician while the patient is under general or local anesthesia.

Termination Date: The date when all cover under this Policy ends for an Insured Person, being the earlier of:

a. midnight on the Termination Date stated in the Policy Schedule; or

b. The moment of the Insured Person’s arrival upon return to his or her Home Country (unless the Insured Person

has started a Benefit Period); or

c. The moment the Insured Person is naturalized as a United States citizen.

Underwriters: Certain underwriters at Lloyd’s of London participating in the contract number stated in the Policy

Schedule.

United States: The United States of America including all states, districts, territories and possessions.

USD: United States Dollar

Usual, Reasonable and Customary: The most common charge for similar services, medicines or supplies within the

area in which the charge is incurred, so long as those charges are reasonable. What is defined as Usual, Reasonable

and Customary charges will be determined by Underwriters. In determining whether a charge is Usual, Reasonable

and Customary, Underwriters may consider one or more of the following factors: the level of skill, extent of training,

and experience required to perform the procedure or service; the length of time required to perform the procedure

or services as compared to the length of time required to perform other similar services; the severity or nature of the

Illness or Injury being treated; the amount charged for the same or comparable services, medicines or supplies in the

locality; the amount charged for the same or comparable services, medicines or supplies in other parts of the country;

the cost to the Medical Provider of providing the service, medicine or supply; such other factors as Underwriters, in

the reasonable exercise of discretion, determine are appropriate.

A. Eligibility

Only individuals who meet all of the following requirements at the time of commencement of this insurance are eligible

for coverage hereunder:

1. At the Effective Date the Insured Person must:

a. not be a United States Citizen and not be a United States resident

b. be aged eighteen (18) years or over unless covered under the same policy as and travelling with their parent,

guardian or a legally responsible adult who resides at the same address, in which case the minimum age is

reduced to over one (1) month old, and not yet sixty five (65) years of age.

c. have received all immunizations recommended by their Home Country prior to entry into the Host Country;

and

2. At all times during the Policy Period the Insured Person

a. must not carry any firearm or any instrument or device designed or intended to cause injury or death to

another person; and

b. must not be a member of any military or para military force.

B. Effective Date and Termination Date

The cover provided under this Policy shall commence on the Effective Date and shall end on the Termination Date.

C. Benefit Period

Underwriters will pay Eligible Medical Expenses under ARTICLE 9. A of this Policy for the Benefit Period. The Benefit

Period applies only to Eligible Medical Expenses covered under ARTICLE 9. A. of this Policy.

D. Home Country Coverage

In the event that an Insured Person begins a Benefit Period during the Policy Period, and insurance terminates as a

result of the Insured Person returning to their Home Country, Underwriters will pay Eligible Medical Expenses under

ARTICLE 9. A of this Policy, which are incurred in the Insured Person's Home Country during the Benefit Period and

are not covered by any other insurance or government plan. Home Country coverage applies only to Eligible Medical

Expenses related to the Injury or Illness that began during the Policy Period.

ARTICLE 4: ELIGIBILITY, EFFECTIVE DATE, TERMINATION DATE, BENEFIT PERIOD AND HOME

COUNTRY COVERAGE

ARTICLE 5: GENERAL PROVISIONS

A. Entire Agreement

This Policy, including the Policy Schedule and any Exhibits, Declarations, Schedules, Endorsements and/ or Riders

attached hereto, constitutes the entire agreement between underwriters and the insured Person.

B. Currency

The monetary limits and Premiums stated in this Policy are in USD. Benefits may be paid in local currency equivalents.

C. Notice

Any notice to an insured Person shall be sent by registered mail, and addressed to the insured Person's mailing

address on file with the Plan Administrator on the date the notice is mailed. The insured Person is required to notify

the Plan Administrator promptly of any change in mailing address.

D. Data Protection

Information provided to Underwriters will be processed by them and their agents in compliance with the provisions of

the Data Protection Act 1998 of England and Wales, for the purpose of administering this insurance and handling claims,

if any. The information may also be sent for processing to other entities, including those located outside the European

Economic Area and others where there is a legal obligation to provide it. Under the Act some information, such as that

relating to health, is classed as ‘sensitive personal data’ and requires explicit consent for processing. Underwriters may

Require the provision of such consent so that they can deal with claims. The person effecting this insurance should

ensure that all persons covered are aware of this.

ARTICLE 6: CONDITIONS

A. Premium

1.The Premium for this insurance shall be as stated in the Policy Schedule.

2. Payment: Payment of the required Premium shall be remitted to the Plan Administrator on or before the

Insured Person's Effective Date.

B. Misrepresentation and Fraud

1. Application:

Underwriters rely on the statements made by the Insured Person on the Application in determining whether or

not the Insured Person meets the Eligibility requirements for insurance hereunder. The Application must be

completed with all reasonable care, honestly and to the best of the knowledge of the person completing it.

If Underwriters establish that the Insured Person deliberately or recklessly provided Underwriters with false or

misleading information, Underwriters shall be entitled to declare this insurance null and void, retain the premium

and decline all claims. If Underwriters establish that the Insured Person was careless, Underwriters shall be

entitled to declare this Insurance null and void and return the premium, vary the terms or reduce proportionately

the amount paid for claims.

If this Policy is wholly or mainly for purposes unrelated to the Insured Person‘s trade, business or profession

then the effect of any misrepresentation will depend on its nature.

If this Policy is wholly or mainly for purposes related to the Insured Person‘s trade, business or profession then

any misstatement, concealment or fraud in the Application, or in relation to any statement or warranty made

by the Insured Person or their authorized representative, whether in writing or otherwise, to Underwriters or

their representatives, on or in connection with the Application shall render this insurance null and void and all

claims hereunder shall be forfeited, in addition to any and all other remedies available to Underwriters.

2. Claims:

Underwriters rely on the statements made by the Insured Person on the Claimant’s Statement and in connection

with the submission of any claim hereunder in determining whether or not and to what extent Benefits under

this insurance may be payable.

If this Policy is wholly or mainly for purposes unrelated to the Insured Person‘s trade, business or profession then

the effect of any misrepresentation in connection with a claim will depend on the nature of the misrepresentation.

• If the representation was deliberate or reckless Underwriters shall be entitled to declare this insurance null and

void and decline the claim and any subsequent claims.

• If the representation was careless, depending on the circumstances, Underwriters shall be entitled to declare

this insurance null and void, return the premium and decline the claim or amend the terms or reduce

proportionately the amount paid for claims.

If this Policy is wholly or mainly for purposes related to the Insured Person‘s trade, business or profession then

any misstatement, concealment or fraud in the making of any claim hereunder shall render this insurance null

and void and all claims hereunder shall be forfeited, in addition to any and all other remedies available to

Underwriters.

C. Proof of Claim

When Underwriters receive notice of claim, they will provide the Insured Person with forms for filing Proof of Claim.

The Insured Person shall have sixty (60) days beginning on the last day of the Policy Period or, if applicable, the last

day of the Benefit Period, to submit Proof of Claim to Underwriters.

Subsequent to receipt of Proof of Claim, Underwriters may, at their sole discretion, request and require additional

information, including but not limited to medical records, necessary to confirm the validity of any claim prior to

payment thereof.

D. Payment of Claims

If the Insured Person is

1. aged eighteen (18) years old or over

a. Accidental Death - Underwriters will pay the Benefit Amount to the Insured Person’s estate

b. Accidental dismemberment - Underwriters will pay the Benefit Amount to the Insured Person

c. All Other Claims where the Claims Administrator has agreed in writing that payment or partial payment of

Benefits is due to the Insured Person - Underwriters will make such payment to the Insured Person whose receipt

shall be a full discharge of all liability by Underwriters in respect of the claim.

2. aged under eighteen (18) years

a. Accidental Death and Accidental dismemberment - Underwriters will pay the Benefit Amount to the Insured

Person’s spouse (if any) or otherwise to the Insured Person’s parent or legal guardian

b. All Other Claims where the Claims Administrator has agreed in writing that payment or partial payment of

Benefits is due to the Insured Person - Underwriters will make such payment to the Insured Person’s spouse

(if any) or otherwise to the Insured Person’s parent or legal guardian whose receipt shall be a full discharge

of all liability by Underwriters in respect of the claim.

E. Legal Actions

No action of law or equity may be brought to recover Benefits under this insurance until sixty (60) days after written

Proof of Claim has been provided to Underwriters. No such action may be brought after the end of two (2) years after

the time that written Proof of Claim is required to be furnished.

F. Waiver of Rights

In the event that Underwriters do not enforce or require compliance with any provision herein, this will not invalidate,

modify or render such provision unenforceable at any other time, whether or not the circumstances are the same.

G. Claims Cooperation

The Insured Person and their Physician(s), Hospital(s) and other Medical Provider(s) shall cooperate fully with

Underwriters including granting full right of access to all related medical documentation, reports and evidence.

Underwriters may deny coverage for any claim where there has been a refusal or material failure to so cooperate.

H. Patient Advocacy

Underwriters may determine that a particular claim or diagnosis occurring under this insurance may be placed under

the Patient Advocacy program to ensure that Medically Necessary services and supplies are provided in the most cost

effective manner. In the event Underwriters determine that a claim or diagnosis meets the Patient Advocacy program

requirements, they will notify the Insured Person, and a Patient Advocate will be assigned to the Insured Person.

Thereafter, the Patient Advocate may make recommendations of alternative treatment settings and/or procedures

and/or supplies, which may be more cost effective for the Underwriters and/or the Insured Person Such

ecommendations will be made with input from the Insured Person and the Insured Person’s Physician(s) and will be

made only when it can be reasonably demonstrated that the Medically Necessary services and supplies can be

provided in a more cost-effective manner to Underwriters and/or the Insured Person. Underwriters will use best

efforts to evaluate and recommend alternative treatment settings and/or procedures and/or supplies, which can

reasonably be expected to result in the same or better care of the Insured Person. The Insured Person, in accepting

The recommendations, agrees to hold Underwriters harmless and Underwriters shall not be held liable or otherwise

responsible for any treatment, service, supply, procedure or care provided to the Insured Person except for the

payment of Benefits under this insurance. After the Insured Person has been notified that the claim or diagnosis

meets the Patient Advocacy program requirements, Underwriters reserve the rights to:

1. make payment for treatments, services and/or supplies which are not covered under this insurance which

would be beneficial to the Insured Person and cost effective to Underwriters; and

2. deny payment for expenses which would otherwise be covered under this insurance which are over the

amount Underwriters would have paid had the Insured Person followed the recommendations of the Patient

Advocacy program.

I. Subrogation

The Insured Person undertakes to cooperate with Underwriters in the prosecution of any and all valid claims they

may have against third parties arising out of any occurrence which results or may result in a loss payment by

Underwriters and to account for any amounts recovered on the basis that Underwriters shall be entitled to recover

first in full any sums paid by them before the Insured Person shares in any amount so recovered. Should the Insured

Person fail to prosecute any valid claims against third parties and Underwriters thereupon become liable to make

payment under this insurance, then Underwriters shall be subrogated to all rights of the Insured Person. Any amount

recovered by Underwriters shall be used to pay the expenses of collection and reimbursement of Underwriters for

any amount that they may have paid or become liable to pay under this insurance. Any remaining amounts shall be

paid to the Insured Person.

J. Other Insurance

Underwriters shall not pay any claim if there is other insurance that would, or would but for the existence of this

insurance, pay such claim. Except, where benefit amounts insured elsewhere are less than the applicable benefit

amount insured by this Policy, this Policy insures for the difference between the benefit amounts insured elsewhere

and the applicable benefit amount of this Policy, subject always to the applicable Deductible stated in the Policy

Schedule. Underwriters shall not pay any claim in respect of care, treatment, services or supplies furnished by any

program or agency funded by any government.

K. Assignment

The Insured Person may assign Benefits under this insurance to a Hospital, Physician or other Medical Provider.

Any assignment shall not confer upon such Hospital, Physician or other Medical Provider, any right or privilege

granted to the Insured Person under this insurance except for the right to receive Benefits, if any, which are

determined to be due and payable hereunder. No Hospital, Physician or other Medical Provider shall have any direct

or indirect claim or right of action against Underwriters or the Plan Administrator.

L. Right of Recovery

In the event of overpayment of any claim hereunder because:

1. All or some of the expenses were not paid for by or on behalf of the Insured Person or were subsequently

recovered by or on behalf of the Insured Person; or

2. Any Relative of the Insured Person or Family Member, whether or not that person is or was an Insured Person,

is repaid for all or some of those expenses by a source other than Underwriters; or

3. All or some of the expenses were not Eligible Expenses; or

4. All or some of the expenses were paid or reimbursed based on incorrect benefit application,

Underwriters have the right to recover the amount of overpayment from the Insured Person and/or the Hospital,

Physician or other Medical Provider of services or supplies. The amount of the recovery is the difference between:

a. The amount of expenses actually paid by Underwriters; and

b. The amount of Benefits which should have been paid by Underwriters.

If the Insured Person or the Hospital, Physician or other Medical Provider of services or suppliers does not promptly

make any such refund to Underwriters, Underwriters may, in addition to any other remedies available to them,

either:

i. reduce the amount of any future claim that is otherwise eligible for payment hereunder, to the full extent of the

refund due Underwriters; or

ii. cancel the Policy issued to the Insured Person by giving thirty (30) days advance written notice by mail to the

Insured Person's last known address.

M. Claims Assistance

Every attempt will be made to help Insured Persons understand the Benefits provided by this insurance, however,

any statement made by an employee of Underwriters or the Plan Administrator will be deemed a representation

and not a warranty. Actual Benefit payment can only be determined at the time a claim is submitted and all facts are

presented in writing. If a definite answer to a specific question is required, the Insured Person can submit a written

request, including all pertinent information and a statement from the attending Physician (if applicable), and a written

reply will be sent to the Insured Person and kept on file.

N. Several Liability Notice

The subscribing Underwriters’ obligations under contracts of insurance to which they subscribe are several and not

joint and are limited solely to the extent of their individual subscriptions. The subscribing Underwriters are not

responsible for the subscription of any co- subscribing underwriter who for any reason does not satisfy all or part of

its obligations.

O. Sanction Limitation and Exclusion Clause

Underwriters shall not be deemed to provide cover and shall not be liable to pay any claim or provide any benefit

hereunder to the extent that the provision of such cover, payment or such claim or provision of such benefit would

expose Underwriters to any sanction, prohibition or restriction under United Nations resolutions or the trade or

economic sanction, laws or regulations of the European Union, United Kingdom or United States of America.

Underwriters hereon agree that all summonses, notices or processes requiring to be served upon them for the

purpose of instituting any legal proceedings against them in connection with this insurance shall be properly served

if addressed to them and delivered to them care of the party(ies) indicated.

Underwriters, by giving the above authority do not renounce their right to any special delays or periods of time to

which they may be entitled for the service of any such summonses, notices or processes by reason of their residence

of domicile in England.

Any service which is carried out in accordance with the above manner shall be without prejudice to any other

alternative method of service provided by law.

ARTICLE 7: PRE-CERTIFICATION REQUIREMENTS

A. The following Medical expenses must always be Pre-certified:

1. Inpatient care; and

2. Any Surgery and

3. Care in an Extended Care Facility; and

4. Home Nursing Care; and

5. Durable Medical Equipment; and

6. Artificial limbs; and

7. Computerized Tomography (CAT Scan); and

8. Magnetic Resonance Imaging (MRI).

B. To comply with the Pre-certification requirements, the Insured Person must:

1. Contact the Claims Administrator at the telephone number contained in the Insured Person’s Policy as soon

as possible before the expense is to be incurred; and

2. Comply with the instructions of the Claims Administrator and submit any information or documents they

require; and

3. Notify all Physicians, Hospitals and other Medical Providers that this insurance contains Precertification

requirements and ask them to fully cooperate with the Claims Administrator.

ARTICLE 8: PREFERRED MEDICAL PROVIDER (PRO) REQUIREMENTS

C. If the Insured Person complies with the Pre-certification requirements, and the expenses are Pre certified,

Underwriters will pay Eligible Medical Expenses subject to all terms, conditions, provisions and exclusions herein. If

the Insured Person does not comply with the Pre-certification requirements or if the expenses are not Pre-certified:

1. Eligible Medical Expenses will be reduced by 50%; and

2. The Deductible will be subtracted from the remaining amount.

D. Emergency Pre-certification: In the event of an Emergency Hospital admission, Pre-certification must be made

within forty eight (48) hours after the admission, or as soon as is reasonably possible but no later than one week

thereafter.

E. Pre-certification Does Not Guarantee Benefits - The fact that expenses are Pre-certified does not guarantee either

payment of Benefits or the amount of Benefits. Eligibility for and payment of Benefits are subject to all the terms,

conditions, provisions and exclusions herein.

F. Concurrent Review - For Inpatient stays of any kind, the Claims Administrator will pre-certify a limited number of

days of confinement. Additional days of Inpatient confinement may later be pre-certified if the Insured Person

receives prior approval.

To comply with the Preferred Medical Provider requirements, the Insured Person must receive medical treatment

from Preferred Medical Providers as directed by the Claims Administrator. If the Insured Person chooses to seek

treatment from a Preferred Medical Provider, Underwriters will remit payment for eligible expenses directly to the

Medical Provider.

Nothing contained in this insurance restricts or interferes with the Insured Person's right to select the Hospital,

Physician or other Medical Provider of the Insured Person’s choice. Nothing contained in this insurance restricts or

interferes with the relationship between the Insured Person and the Hospital, Physician or other Medical Providers

with respect to treatment or care of any condition, or the right of any Insured Person to receive, at his or her own

expense, services and/or supplies that are not covered under this insurance.

ARTICLE 9: ELIGIBLE EXPENSES (AND PERSONAL ACCIDENT BENEFITS)

A. Eligible Expenses – Eligible Medical ExpensesSubject to the Deductible and the limits stated in ARTICLE 2, Underwriters will pay the following expenses incurred

while this insurance is in effect:

1. Charges made by a Hospital for:

a. daily room and board and nursing services not to exceed the average semi-private room rate; and

b. daily room and board and nursing services in Intensive Care Unit; and

c. use of operating, treatment or recovery room; and

d. services and supplies which are routinely provided by the Hospital to persons for use while Inpatients; and

e. Emergency Room treatment of an Injury; and

f. Emergency Room treatment of an Illness resulting in admission to the Hospital as Inpatient for further treatment

of that Illness; and

g. Emergency Room treatment of an Illness which does not result in admission to the Hospital as Inpatient, if non

Emergency Room care was not available due to the time or location of the Insured Person at the onset of symptoms.

No coverage is provided for non-emergency treatment of Illness in Emergency Room when or where alternative non-

emergency care facilities are available. Emergency medical expenses cease upon the Insured Person’s return to their

Home Country.

2. For Surgery at an outpatient surgical facility, including services and supplies.

3. For charges made by a Physician for professional services, including Surgery. Charges for an assistant surgeon are

covered up to 20% of the Usual, Reasonable and Customary charge of the primary surgeon, but standby availability

will not be deemed to be a professional service and therefore is not covered hereunder.

4. For dressings, sutures, casts or other supplies which are Medically Necessary and administered by or under the

supervision of a Physician, but excluding nebulizers, oxygen tanks, diabetic supplies, other supplies for use or

application at home, and all devices or supplies for repeat use at home, except Durable Medical Equipment as herein

Defined.

5. For diagnostic testing using radiology, ultrasonographic or laboratory services (psychometric, intelligence,

behavioral and educational testing are not included).

6. For artificial limbs, eyes or larynx, breast prosthesis or basic functional artificial limbs, but not the replacement or

repair thereof.

7. For reconstructive Surgery when the reconstructive Surgery is directly related to Surgery which is covered

hereunder.

8. For hemodialysis and the charges by the Hospital for processing and administration of blood or blood components

but not the cost of the actual blood or blood components.

ARTICLE 9: ELIGIBLE EXPENSES (AND PERSONAL ACCIDENT BENEFITS)

9. For oxygen and other gasses and their administration by or under the supervision of a Physician.

10. For anesthetics and their administration by a Physician or anesthetist.

11. For drugs which require prescription by a Physician for treatment of a covered Injury or Illness, but not for the

replacement of lost, stolen, damaged, expired or otherwise compromised drugs, and for a maximum supply of thirty

(30) days per prescription.

12. For care in a licensed Extended Care Facility upon direct transfer from an acute care Hospital.

13. Home Nursing Care in bed by a qualified licensed professional, provided by a Home Health Care Agency upon

direct transfer from an acute care Hospital and only in lieu of Medically Necessary Inpatient hospitalization.

14. Emergency Local Ambulance transport necessarily incurred in connection with Injury or Illness resulting in

Inpatient hospitalization.

15. Emergency Dental Treatment and dental Surgery necessary to restore or replace sound natural teeth lost or

damaged in an Accident which was covered under this insurance.

16. Medically Necessary rental of Durable Medical Equipment (consisting of a standard basic hospital bed and or a

standard basic wheelchair) up to the purchase prices.

17. Physical therapy by an authorised physiotherapist necessarily incurred to continue recovery from a covered Injury

or Illness, and subject to the maximum amounts specified in the ARTICLE 2. Such physical therapy must be prescribed

by a Physician who is not affiliated with the authorised physiotherapy practice performing the physical therapy.

B. Eligible Expenses - Emergency Medical Evacuation Subject to the Deductible and the Limits stated in ARTICLE 2, and subject to the Conditions and Restrictions contained

in this provision, Underwriters will pay the following expenses arising out of Emergency Medical Evacuation:

1. Emergency air transportation to a suitable airport nearest to the Hospital where the Insured Person will receive

treatment; and

2. Emergency ground transportation necessarily preceding Emergency air transportation; and from the destination

airport to the Hospital where the Insured Person will receive treatment.

Conditions and Restrictions:

a. The Insured Person must comply with all conditions and provisions of the insurance; and

b. Underwriters will provide Emergency Medical Evacuation Benefits only when the Illness or Injury giving rise to

the Emergency Medical Evacuation is covered under this Insurance; and

c. Underwriters will provide Emergency Medical Evacuation Benefits only when all of the following conditions are

met:

i. Medically Necessary treatment, services and supplies cannot be provided locally; and

ii. transportation by any other method would result in loss of Insured Person’s life or limb; and

iii. recommended by the attending Physician who certifies to the above; and

iv. agreed upon by the Insured Person or a Relative of the Insured Person; and

v. approved in advance and coordinated by the Claims Administrator; and

vi. the condition giving rise to the Emergency Medical Evacuation occurred spontaneously and without

advance warning, either in the form of recommendations received form a Physician or symptoms which

would have caused a prudent person to seek medical attention prior to the on set of the Emergency.

d. Underwriters will provide Emergency Medical Evacuation only to the nearest Hospital that is qualified to provide

the Medically Necessary treatment, services and supplies to prevent the Insured Person’s loss of life or limb.

e. The Claims Administrator will use their best efforts to arrange any Emergency Medical Evacuation within the

least amount of time possible. The Insured Person understands that the timeliness of Emergency Medical

evacuation can be affected by circumstances which are not within the control of the Claims Administrator such as:

availability of transportation equipment and staff, delays or restrictions on flights caused by mechanical problems,

government officials, telecommunications problems and weather. The Insured Person agrees to hold Underwriters

and the Claims Administrator harmless and Underwriters and the Claims Administrator shall not be held liable for

any delays that are not within their direct and immediate control. Notwithstanding the foregoing items c. i.-iii and

d, Underwriters will pay for expenses to return the Insured Person to their Home Country if the attending

Physician and Underwriters’ or their duly appointed medical consultant agree that transfer to the Home Country is

more appropriate than transfer to the nearest qualified Hospital.

C. Eligible Expenses - Repatriation of Remains Subject to the Deductible and the Limits stated in ARTICLE 2, and subject to the Conditions and Restrictions contained

in this provision, Underwriters will pay the following:

Repatriation of Remains expenses arising from the death of an Insured Person:

1. Air or ground transportation of bodily remains or ashes to the airport or ground transportation terminal nearest

to the Principal Residence of the deceased Insured Person; and

2. Reasonable costs of preparation of the remains necessary for transportation. Conditions and Restrictions:

a. The Insured Person must be in compliance with all conditions and provisions of this insurance; and

b. Repatriation of Remains must be approved in advance and coordinated by the Claims Administrator; and

c. Underwriters will provide Repatriation of Remains Benefits only when the death of the Insured Person occurs

i. as a result of an Injury or Illness that is covered under this insurance; and

ii. while this insurance is in effect; and

d. The Claims Administrator will use its best efforts to arrange any Repatriation of remains within the least amount

of time possible. The Insured Person understands that the timeliness of Repatriation can be affected by circumstances

which are not within the control of the Claims Administrator such as but not limited to: availability of transportation

equipment and staff, delays or restrictions on flights caused by mechanical problems, government officials,

telecommunications problems and weather. The Insured Person, and their heirs, agree to hold Underwriters and the

Claims Administrator harmless and neither Underwriters nor the Claims Administrator shall be held liable for any

delays which are not within their direct and immediate control. Further, Underwriters and the Claims Administrator

are held harmless and shall not be held liable for loss of or any damage or other impairment to bodily remains incurred

during the repatriation process or otherwise.

D. Eligible Expenses - Local Burial or Cremation Subject to the Deductible and the Limits stated in ARTICLE 2, and subject to the Conditions and Restrictions contained

in this provision, Underwriters will pay the following Local Burial or Cremation expenses arising from the death of an

Insured Person. Underwriters will pay for the Insured Person to be buried or cremated in the country of death in lieu

of Repatriation of Remains Benefits herein provided.

Conditions and Restrictions:

a. The Insured Person must be in compliance with all conditions and provisions of this insurance; and

b. Local Burial or Cremation must be approved in advance and coordinated by the Claims Administrator; and

c. Underwriters will provide Local Burial or Cremation Benefits only when the death of the Insured Person occurs

as a result of an Injury or Illness that is covered under this insurance; and

d. Underwriters will provide Local Burial or Cremation Benefits only when the death of the Insured Person occurs

while this insurance is in effect; and

e. The Claims Administrator will use their best efforts to arrange any local burial or cremation within the least

amount of time possible. The Insured Person understands that the timeliness of Burial or Cremation can be affected

by circumstances that are not within the control of the Claims Administrator such as, but not limited to government

officials, government rules, regulations or laws, telecommunications problems and weather. The Insured Person,

and their heirs, agrees to hold Underwriters and the Claims Administrator harmless and neither Underwriters nor

the Claims Administrator shall be held liable for any delays which are not within their direct and immediate control.

Further, Underwriters and the Claims Administrator are held harmless and shall not be held liable for loss of or any

damage or other impairment to bodily remains incurred during the Local Burial or Cremation process or otherwise

And;

f. Local Burial or Cremation Benefits cannot be used in conjunction with the Emergency Evacuation or Repatriation

of Remains benefit and excludes coverage for death in the Insured Person’s Home Country.

E. Eligible Expenses - Emergency Reunion

Subject to the Deductible and the Limits stated in ARTICLE 2, and subject to the Conditions and Restrictions contained

in this provision, Underwriters will pay the following Emergency Reunion expenses, following a covered Emergency

Medical Evacuation under this insurance:

1. The cost of an economy round-trip air or ground transportation ticket for one Relative of the Insured Person for

transportation to the terminal serving the area where the Insured Person is hospitalized or is to be hospitalized

following Emergency Medical Evacuation; and

2. Reasonable expenses at Underwriters’ discretion for lodging and meals for the Relative, which are incurred in the

area where the Insured Person is hospitalized for a period not to exceed fifteen (15) days.

Conditions and Restrictions:

a. The Insured Person must be in compliance with all conditions and provisions of this insurance; and

b. Emergency Reunion must be approved in advance and coordinated by the Claims Administrator; and

c. Underwriters will provide Emergency Reunion Benefits only following an Emergency Medical Evacuation of

An Insured Person that is covered hereunder.

F. Eligible Expenses - Return (following a covered Emergency Medical Evacuation)

Subject to the Deductible and the Limits stated in ARTICLE 2, and subject to the Conditions and Restrictions contained

in this provision, Underwriters will pay the following return expenses:

The cost of an economy one-way air and/or ground transportation ticket for the Insured Person from the area where

the Insured Person was hospitalized following an Emergency Medical Evacuation to the area where the Insured

Person was initially evacuated from, or to the terminal serving the area of the Insured Person’s Principal Residence,

subject to the following Conditions and Restrictions:

a. The Insured Person must be in compliance with all conditions and provisions of this insurance; and

b. Return Benefits must be approved in advance and coordinated by the Claims Administrator; and

c. Underwriters will provide Return Benefits only following a covered Emergency Medical Evacuation when

Evacuation when the attending Physician states that it is Medically Necessary for the Insured Person to return to

his or her Home Country or to the area from which he or she was initially evacuated for continued treatment,

recuperation and recovery.

G. Accidental Death and Accidental Dismemberment

Subject to the Benefit Amounts stated in ARTICLE 2, and subject to the Conditions and Restrictions contained in this

provision, Underwriters will pay Accidental Death and Accidental Dismemberment Benefits.

The Benefit Amount will be doubled if Accidental Death or Accidental Dismemberment results from Kidnapping,

attempted Kidnapping, Hijacking or attempted Hijacking, but subject to a maximum total Benefit amount in respect

of all Family Members covered under this Policy.

Conditions and Restrictions:

a. The Insured Person must comply with all conditions and provisions of this insurance; and

b. The Accident giving rise to the Accidental Death or Accidental Dismemberment must be covered under

this insurance and must not be an Accident occurring whilst the Insured Person is

i. travelling on a licensed form of public transport (Common Carrier); or

ii. within their Home Country.

c. Underwriters will not pay more than one Benefit Amount for Accidental Death and/or Accidental Dismemberment

resulting from the same Accident.

ARTICLE 10: EXCLUSIONS

This insurance excludes any treatment in the Insured Person’s Home Country, except as provided for in ARTICLE 4,

Item 4. Charges for the following treatments and/or services and/or supplies and/or conditions and/or items are

excluded from coverage hereunder:

1. Any expense of any nature incurred in the United States

2. All charges related to:

a. pregnancy or childbirth unless a qualified medical practitioner confirms that the charges arise from

complications of pregnancy or childbirth and that such complications could not reasonably have been foreseen by

the Insured Person at the date this Policy was purchased.

b. the care of children aged under one month old.

3. Treatment related to birth defects and congenital illnesses. Birth defects are deemed to include hereditary

conditions.

4. Charges for treatment of Mental Health Disorders.

5. Charges which are not incurred by an Insured Person during the Policy Period, or during a Benefit Period, if

applicable.

6. Charges for treatment of any condition(s) when the purpose of departing the Home Country was to obtain

treatment in the Host Country(ies).

7. Charges for any Benefits hereunder which are not presented to Underwriters for payment within sixty (60) days

beginning on the last day of the Policy Period, or Benefit Period if applicable.

8. Treatment, services or supplies that are not administered by or under the supervision of a Physician, and products

that can be purchased without a Physician’s prescription.

9. Treatment, services or supplies that are not Medically Necessary.

10. Treatment, services or supplies provided at no cost to the Insured Person.

11. Charges which exceed Usual, Reasonable and Customary.

12. Telephone consultations or failure to keep a scheduled appointment.

13. Surgery, treatments, services or supplies that are Investigational, Experimental or for Research purposes.

14. Charges Incurred while confined primarily to receive Custodial Care, Educational or Rehabilitative Care, or any

medical treatment in any establishment for the care of the aged.

15. Weight modification or surgical treatment of obesity, including but not limited to wiring of the teeth and all forms

of intestinal bypass Surgery.

16. Modifications of the physical body intended to improve the psychological, mental or emotional well-being of the

Insured Person, including but not limited to sex-change Surgery.

17. Surgery, treatments, services or supplies for cosmetic or aesthetic reasons, except for reconstructive Surgery

when such reconstructive Surgery is directly related to and follows Surgery which was covered hereunder.

18. Treatment of Insured Persons who are HIV+, have AIDS or ARC, and all diseases caused by and/or related to HIV.

19. Any drug, treatment or procedure that either promotes or prevents conception including but not limited to:

artificial insemination, treatment for infertility or impotency, sterilization or reversal of sterilization.

20. Any drug, treatment or procedure that either promotes, enhances or corrects impotency or sexual dysfunction.

21. Abortions, except to save the life of the mother.

22. Any dental treatment, including but not limited to routine dental examination, treatment, the care of teeth,

gums or bones supporting the teeth, dentures and preparation of dentures, except for Emergency Dental Treatment

necessary to replace sound natural teeth lost or damaged in an Accident covered hereunder.

23. Corrective devices and medical appliances, including eyeglasses, contact lenses, hearing aids, hearing implants,

eye refraction, visual therapy, and any examination or fitting related to these devices, dentures or dental appliances,

and all vision and hearing tests and examinations.

24. Eye Surgery, such as radial keratotomy, when the primary purpose is to correct nearsightedness, farsightedness

or astigmatism.

25. Treatment of the temporomandibular (jaw) joint.

26. Injury sustained while under the influence of or due wholly or partly to the effects of intoxicating liquor or drugs

other than drugs taken in accordance with treatment prescribed and directed by a Physician but not for the treatment

of Substance Abuse.

27. Costs resulting from self-inflicted Injury or Illness and/or suicide or attempted suicide whether sane or insane.

28. Diagnosis or treatment of venereal disease, including all Sexually Transmitted Diseases and conditions.

29. Routine medical examinations, including but not limited to vaccinations, immunizations, annual check-ups, the

issue of medical certificates and attestations, and examinations as to the suitability of employment or travel.

30. Treatment by a chiropractor.

31. Charges resulting from or occurring during the commission of a violation of law by the Insured Person, including

without limitation, the engaging in an illegal occupation or act, but excluding minor traffic violations.

32. Medical treatment for Substance Abuse or addiction or conditions that may be attributed to Substance Abuse or

addictions and direct consequences thereof.

33. Speech, vocational, occupational, biofeedback, acupuncture, recreational, sleep or music therapy, holistic care of

any nature, massage and kinestherapy.

34. Any services, supplies, or treatment performed or provided by a Relative of the Insured Person or any Family

Member or any person who ordinarily resides with the Insured Person.

35. Orthoptics and visual eye training.

36. Services, supplies, or treatment that are not included as Eligible Expenses as described herein.

37. The following care, treatment or supplies for the feet: orthopedic shoes, orthopedic prescription devices to be

attached to or placed in shoes, treatment of weak, strained, flat, unstable or unbalanced feet, metatarsalgia or

bunions, and treatment of corns, calluses or toenails.

38. Services, supplies, or treatment for hair loss including wigs, hair transplants or any drug that promises hair growth

whether or not prescribed by a Physician.

39. Treatment related directly or indirectly to any Pre-existing Condition.

40. Exercise programs, whether or not prescribed or recommended by a Physician.

41. Treatment required as a result of complications or consequences of a treatment or condition not covered

hereunder.

42. Charges for travel or accommodation, except as provided for in the Local Ambulance, Emergency Medical

Evacuation, Repatriation of Remains, Emergency Reunion, and Return sections of this insurance.

43. Treatment incurred as a result of exposure to non-medical nuclear radiation and/or radioactive material(s).

44. Organ or Tissue Transplants or related services.

45. Treatment for acne, moles, skin tags, diseases of sebaceous glands, seborrhea, sebaceous cyst, unspecified

disease of sebaceous glands, hypertrophic and atrophic conditions of skin, nevus.

46. All expenses of any cryogenic preservation and implantation or re-implantation of living cells.

47. Diagnosis or treatment of all forms of cancer / neoplasm.

48. All Emergency Medical Evacuation, Repatriation of Remains, or Local Burial or Cremation costs not approved or

arranged in advance by the Claims Administrator.

49. Coverage for Local Burial or Cremation is excluded from coverage if death occurs in the Insured Person’s Home

Country.

50. Claims payable under any government system, including the Australian Medicare system, are excluded from

Coverage.

51. The Accidental Death and Accidental Dismemberment and Eligible Medical Expense Benefits shall be excluded

with respect to Accidents occurring while the Insured Person is participating in any of the following:

a. Amateur Athletics, Contact Sports, intercollegiate, interscholastic, intramural, and club sports or athletic

activities and Professional Sports. Non-contact and non-organized/non-sanctioned amateur sports or athletic

activities engaged in by the Insured Person solely for leisure, recreational, entertainment or fitness purposes

are not excluded unless they are excluded by (b) through (j) of this provision; and

b. mountaineering where a reasonably prudent person would use ropes or guides at elevations of 4,500 meters

or higher; and

c. aviation; and

d. hang gliding, sky diving, parachuting or bungee jumping; and

e. racing by any animal or motorized vehicle; and

f. spelunking / potholing; and

g. Sub aqua pursuits involving underwater breathing apparatus unless PADI/NAUI certified, accompanied by a

Certified instructor, and at depths of less than then (10) metres; and

h. jet skiing; and

i. any other sport or activity which is undertaken for thrill seeking and exposes the Insured

Person to abnormal risk of Injury.

52. Any injury or illness resulting directly or indirectly from the use of any biological, chemical, radioactive or nuclear

agent, material, device or weapon.

53. Any injury or illness resulting from the insured Person’s direct or indirect involvement in any war, Act of Terrorism,

strike, riot or civil commotion. Provided that nothing contained in this exclusion shall exclude any claim for injury or

illness arising from the insured Person’s passive involvement in such situations; and

54. Any injury or illness sustained when the insured Person has unreasonably failed or refused to depart a country

within forty eight (48) hours of the time an evacuation order has been issued by the insured Person’s Home Country.

55. Any expenses (medical travel or any other costs) relating directly or indirectly to the Ebola virus.

ARTICLE 11: FILING A CLAIM

Notice of claim, claimant’s statement, and Proof of Claim must be mailed to the Claims Administrator:

Tangiers International, Ltd

54 Melita Street

Valletta VLT 1122, Malta

Tel: +356 2778 0016

Fax: +356 2720 5500

e-mail: [email protected]