Embed Size (px)

Citation preview

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent

DRAFT

E-Commerce and Amazon impact on packagingPresentation in RISI conferenceBarcelona, March 7, 2018

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 2

• Top management consulting firm, helping leaders in every industry make their most critical decisions on strategy, operations, organization, M&A and IT

• Founded in 1973, 7000 employees in 55 offices worldwide

• Worked with over 5000 companies, including 2/3 of the Global 500

• Consulted on 50% of the largest global private equity deals in the last decade

• 85% of business comes from companies with whom we’ve worked before

Introduction

ILKKA LEPPÄVUORI BAIN & COMPANY

• Partner, Helsinki

• 12 years with Bain

• Head of EMEA Forest Products, Paper & Packaging Practice

• Relevant experience:- Forestry, pulp, paper, packaging,

sawmilling, production machinery - Strategy, M&A, performance

improvement, commercial excellence, digitalisation

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 3

Key messages

Bricks & Mortar retail

growth is dead

Amazon and Alibaba are the

undisputed leaders in e-commerce

E-commerce will fundamentally

change the nature of packaging

Clear, bold strategies are needed in this era of potential

disruptions

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 4

Base case scenario: virtually all retail growth comes from e-commerce

CONSUMER ELECTRONICS CLOTHING/APPAREL FOOD/GROCERIES

Source: Forrester; Bain analysis

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 5

Labor costs in last mile delivery are still slowing down e-commerce growth – a number of drivers could dramatically reduce costs

0

2

4

6

8

10

Average last mile delivery costs (EUR)

US

6-10

Labor

Other4-5

~2

JP

~2

UK

~1.5

25-30% 15% 7% 7% 5%% of €30delivery

PARCELSURBAN

FOODURBAN

PARCELSRURAL

DRIVERS OF COST REDUCTION IN THE LAST MILE

• Volume growth

• Autonomous vehicles- Drones- Droids- Autonomous vehicles- Semi-autonomous vans

• Pick-up lockers

• Pick-up at store

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 6

Key messages

Bricks & Mortar retail growth is

dead

Amazon and Alibaba are

the undisputed

leaders in e-commerce

E-commerce will fundamentally

change the nature of packaging

Clear, bold strategies are needed in this era of potential

disruptions

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 7

0.01 0.02 0.05 0.1 0.2 0.5 1 2 5 10

Alibaba

AmazoneBayWalmart.com

Apple

eBay

Amazon

eBay

Softbank

Amazon

Otto Group

JD.com

Amazon

Amazon

AmazonRakuten

Flipkart

Tesco

AmazonGroupe Casino

U.S.

France

China

U.K.

Japan

Germany

India

Walmart.com

Alibaba

Amazon

eBay

$100B GMV 2016

Legend:

Amazon and Alibaba are the undisputed leaders in e-commerce

Note: Amazon investing heavily in India; Alibaba reflects both T-Mall and Taobao; retail value of sale before sales tax, excludes motor vehicles and click-and-collect when not paid for online; Apple includes Itunes and App Store; eBay GMV in UK & Germany adjusted to account for C2C GMVSource: Euromonitor; Companies websites; Analyst reports; Expert interviews (for India); Bain analysis

Relative market share (RMS)

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 8

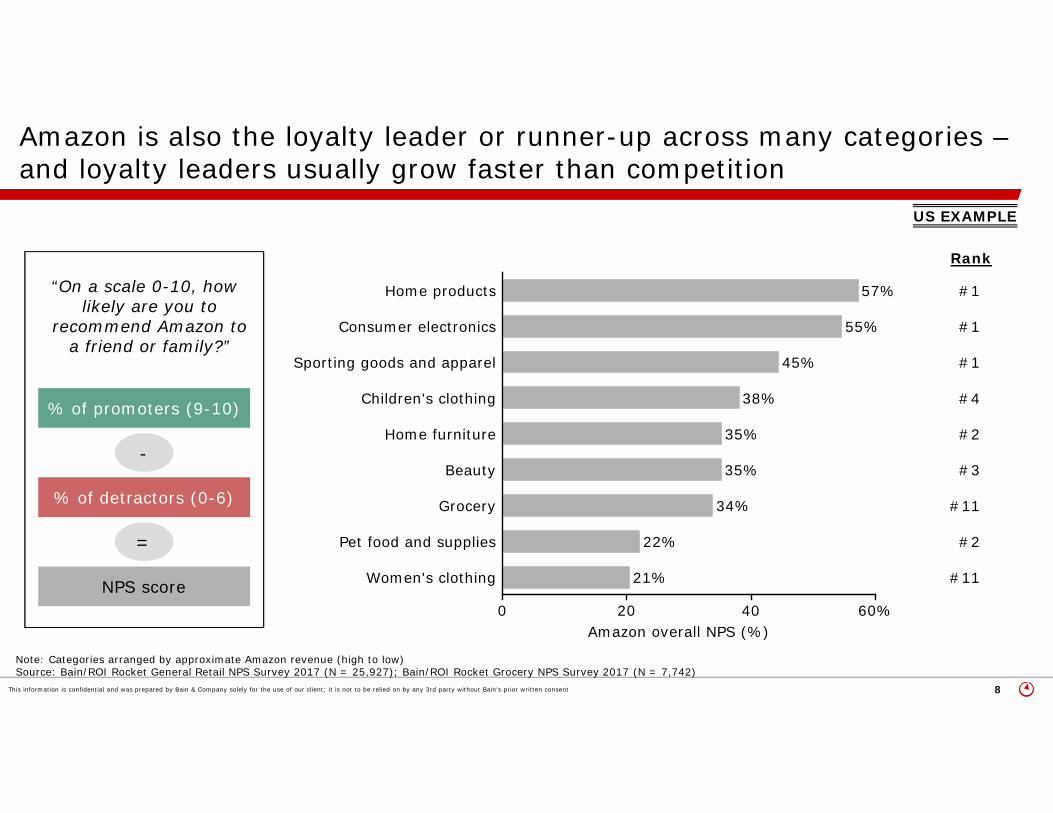

Amazon is also the loyalty leader or runner-up across many categories –and loyalty leaders usually grow faster than competition

0 20 40 60%

Women's clothing 21%

Pet food and supplies 22%

Grocery 34%

Beauty 35%

Home furniture 35%

Children's clothing 38%

Sporting goods and apparel 45%

Consumer electronics 55%

Home products 57%

#1

#11

#4

#2

#11

#1

#3

#1

#2

Amazon overall NPS (%)

US EXAMPLE

Note: Categories arranged by approximate Amazon revenue (high to low)Source: Bain/ROI Rocket General Retail NPS Survey 2017 (N = 25,927); Bain/ROI Rocket Grocery NPS Survey 2017 (N = 7,742)

“On a scale 0-10, how likely are you to

recommend Amazon to a friend or family?”

% of promoters (9-10)

% of detractors (0-6)

NPS score

=

-

Rank

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 9

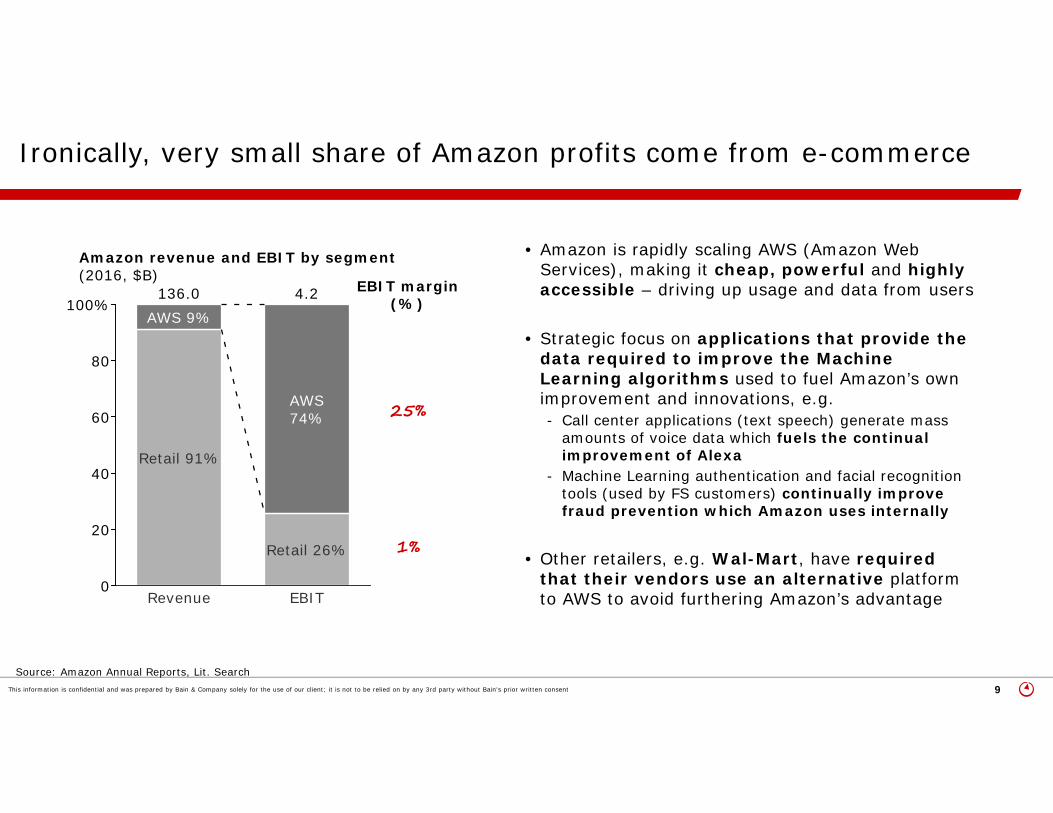

Ironically, very small share of Amazon profits come from e-commerce

0

20

40

60

80

100%

Revenue

Retail 91%

AWS 9%136.0

EBIT

Retail 26%

AWS74%

4.2

Amazon revenue and EBIT by segment(2016, $B)

EBIT margin(%)

25%

1%

• Amazon is rapidly scaling AWS (Amazon Web Services), making it cheap, powerful and highly accessible – driving up usage and data from users

• Strategic focus on applications that provide the data required to improve the Machine Learning algorithms used to fuel Amazon’s own improvement and innovations, e.g.- Call center applications (text speech) generate mass

amounts of voice data which fuels the continual improvement of Alexa

- Machine Learning authentication and facial recognition tools (used by FS customers) continually improve fraud prevention which Amazon uses internally

• Other retailers, e.g. Wal-Mart, have required that their vendors use an alternative platform to AWS to avoid furthering Amazon’s advantage

Source: Amazon Annual Reports, Lit. Search

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 10

Key messages

Bricks & Mortar retail growth is

dead

Amazon and Alibaba are the

undisputed leaders in e-commerce

E-commerce will

fundamentally change the nature of packaging

Clear, bold strategies are needed in this era of potential

disruptions

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 11

Last-mile

E-commerce value chain requires more secondary packaging, driving significant packaging volume growth: Amazon example

Fulfilment center (FC)

Delivery station

Sortation center (SC)

USPS Drop Off Point

Final destination (consumer residence

or locker/pickup point)Prime Now Hub(In/near urban

areas)

Product Manufacturer / retailer warehouse

Marketplace sellers & seller-fulfilled prime

FBA &

Am

azon

priva

te la

bel

Source: Expert interviews; Jefferies

US MODEL - ILLUSTRATIVE

“We believe European packaging leaders are well placed to benefit from European e-commerce growth. Jefferies estimates e-commerce represents 5%-10% of group sales and typically one-third of incremental 2017-18 volume growth.

Jefferies, Jan 2018

Increased need for secondary packaging vs. Bricks & Mortar

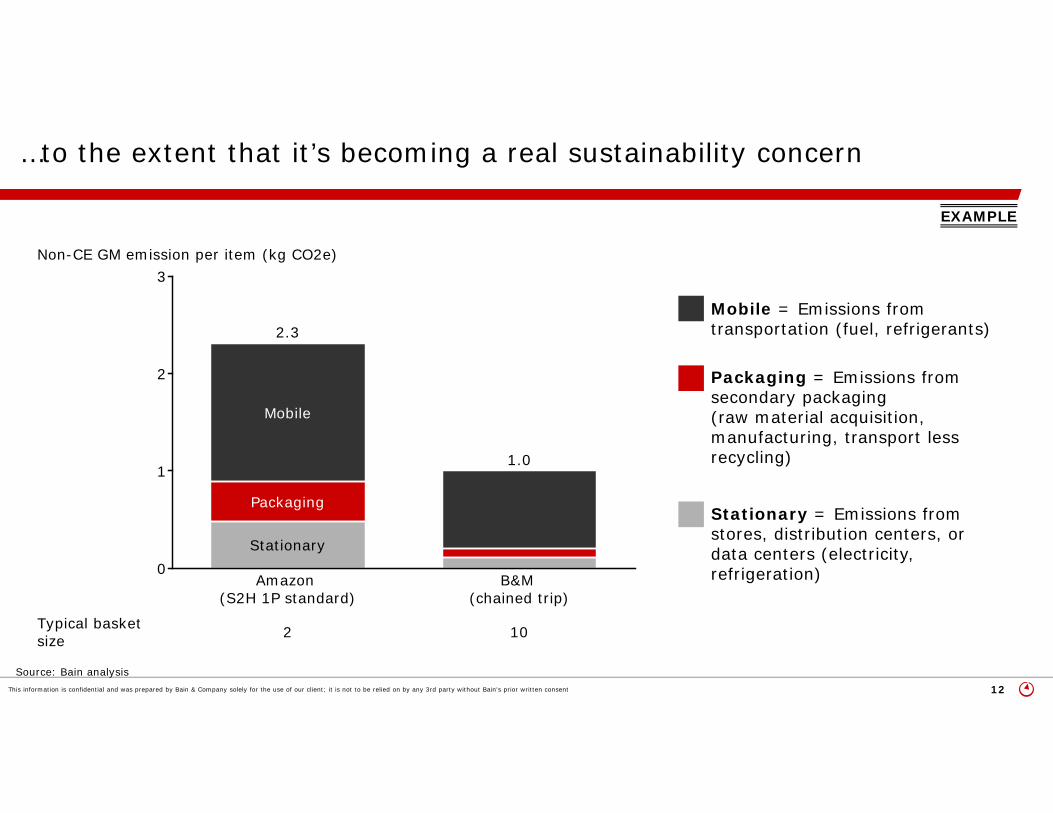

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 12

0

1

2

3Non-CE GM emission per item (kg CO2e)

Amazon(S2H 1P standard)

Stationary

Packaging

Mobile

2.3

B&M(chained trip)

1.0

2 10Typical basketsize

EXAMPLE

…to the extent that it’s becoming a real sustainability concern

Source: Bain analysis

• Mobile = Emissions from transportation (fuel, refrigerants)

• Packaging = Emissions from secondary packaging (raw material acquisition, manufacturing, transport less recycling)

• Stationary = Emissions from stores, distribution centers, or data centers (electricity, refrigeration)

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 13

The role and importance of primary packaging is also shifting

Source: LEGO website

FROM SHOWING THE PACKAGE… …TO SHOWING THE PRODUCT

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 14

White label is changing the competitive landscape in some categories

Source: Amazon website

FROM BRANDED PRODUCTS… …TO WHITE LABEL PACKAGING

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 15

Requirements for packaging are changing: example pleasure and pain points along the online packaging customer journey

Source: Stora Enso

0 10 20 30 40%

% of responses

A personal touch

Eco-friendly material

Packed tight, little filling

Give-aways inside

Nicely wrapped inside

Smart opening features

Attractive design

POSITIVE EXPERIENCES PAIN POINTS

0 10 20 30 40%

% of responses

Difficult to carry

Difficult to reseal

Boring brown box

Unprotected items

Not eco-friendly

Too bulky / lots of filling

Weak, damaged

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 16

Key messages

Bricks & Mortar retail growth is

dead

Amazon and Alibaba are the

undisputed leaders in e-commerce

E-commerce will fundamentally

change the nature of packaging

Clear, bold strategies are needed in this

era of potential

disruptions

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 17

So far so good: lots of positives for packaging companies…

•Corrugated boxes

•Containerboard

•Innovative packaging design

•Intelligent packaging solutions

•Tailored packaging

MORE DEMAND FOR…

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 18

…but also many uncertainties and potential disruptions

•How will last mile deliveries evolve, in format and cost?

•What are the next categories where Amazon/Alibaba will wipe out competition?

• Is this going to be a cost or design/innovation game? How will technology change the packaging demand and solutions?

•Where to place new capacity, to capture the new demand?

•How will the sustainability issue be tackled – by consumers and governments, and how will it impact the choice of materials, plastics vs. fiber-based?

This information is confidential and was prepared by Bain & Company solely for the use of our client; it is not to be relied on by any 3rd party without Bain's prior written consent 19

In conclusion: doing your strategy homework properly is a safe bet in this era of potential disruptions in packaging

StrategicFoundation Priorities

Transformation journey

Ambition

Howto Win

Whereto Play

CHOICES

• How are the packaging ‘rules of the game’ changing with e-commerce?

• What are the biggest uncertainties and potential outcomes?

• Where should we invest?- Geographies- Product categories- Customers/segments

• How are we differentiated?

• What are our selected few priority initiatives?

• Do we have the right people to lead the change?

• How will we track success and course-correct if needed?