Embed Size (px)

Citation preview

18 - 1©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Chapter 18

More on Understanding

Corporate Annual Reports

18 - 2

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Learning Objective 1

Contrast accounting for

investments using the equity

method and the market method.

18 - 3

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Intercorporate Investments

How do we account for intercorporate investments?

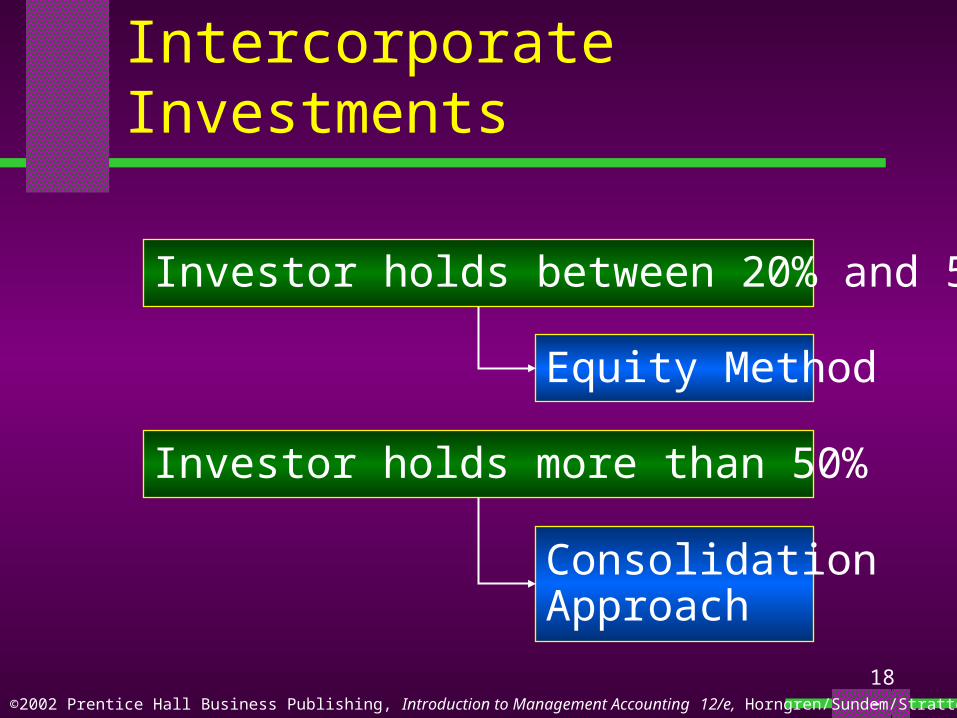

Investor holds less than 20%

Market Method

18 - 4

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Intercorporate Investments

Investor holds between 20% and 50%

Equity Method

Investor holds more than 50%

ConsolidationApproach

18 - 5

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

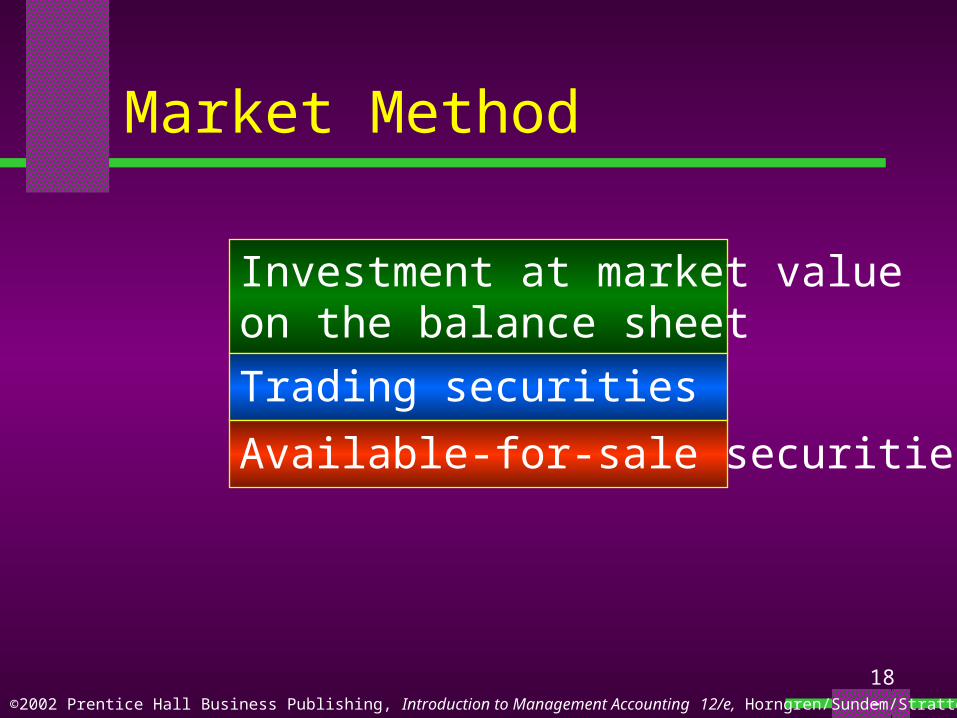

Market Method

Investment at market valueon the balance sheet

Trading securities

Available-for-sale securities

18 - 6

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

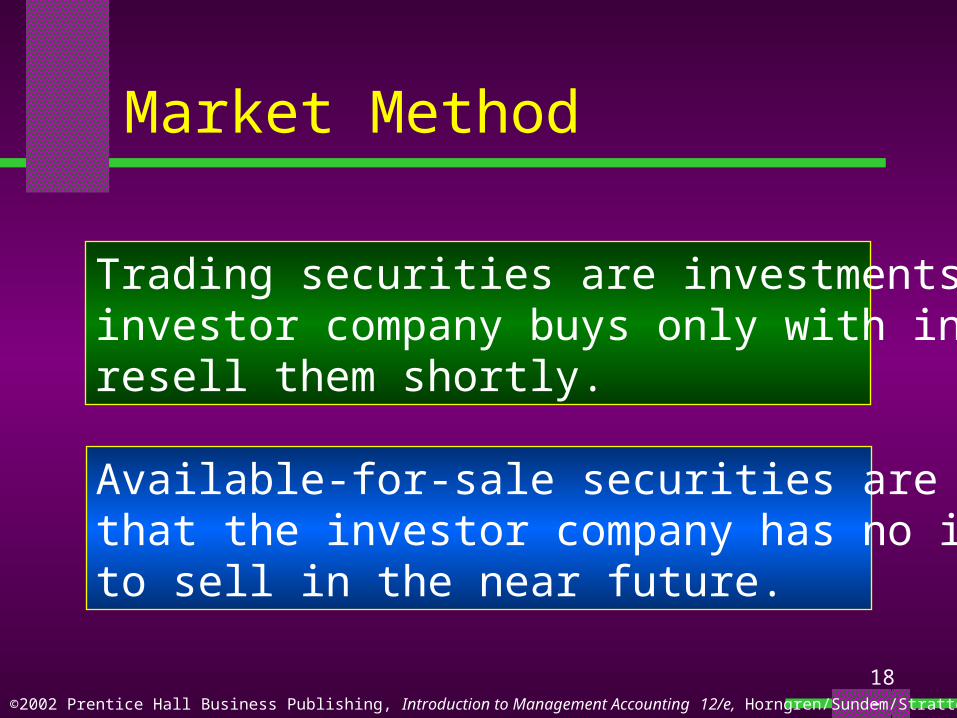

Market Method

Trading securities are investments that theinvestor company buys only with intent toresell them shortly.

Available-for-sale securities are investmentsthat the investor company has no intentionto sell in the near future.

18 - 7

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

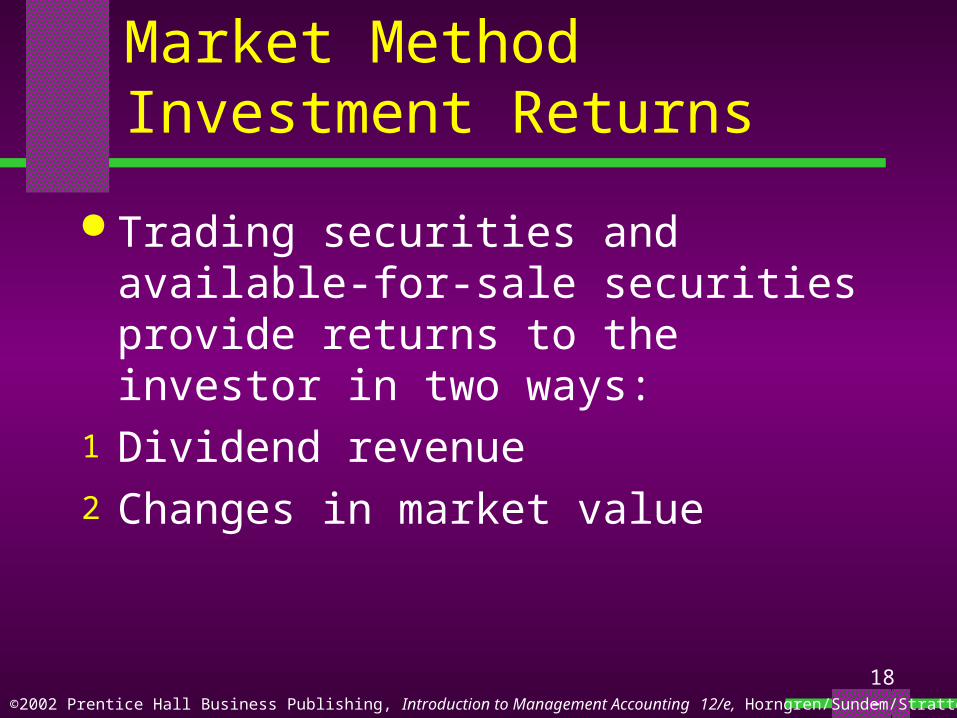

Market Method Investment Returns

Trading securities and available-for-sale securities provide returns to the investor in two ways:

1 Dividend revenue2 Changes in market value

18 - 8

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Market MethodInvestment Returns

Dividends are recorded on the incomestatement when earned for both typesof investments.

Changes in market value are accountedfor differently for trading securities thanfor available-for-sale securities.

18 - 9

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Changes in Market ValueTrading Securities

As the market value of trading securitieschanges, companies report the gains fromincreases in price and losses from decreasesin price in the income statement.

18 - 10

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Changes in Market ValueTrading Securities

Gains and losses that arise as market values ofavailable-for-sale securities rise and fall are notshown on the income statement.

Unrealized gains and losses are added to aseparate valuation allowance account in thestockholders’ equity section of the balance sheet.

18 - 11

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

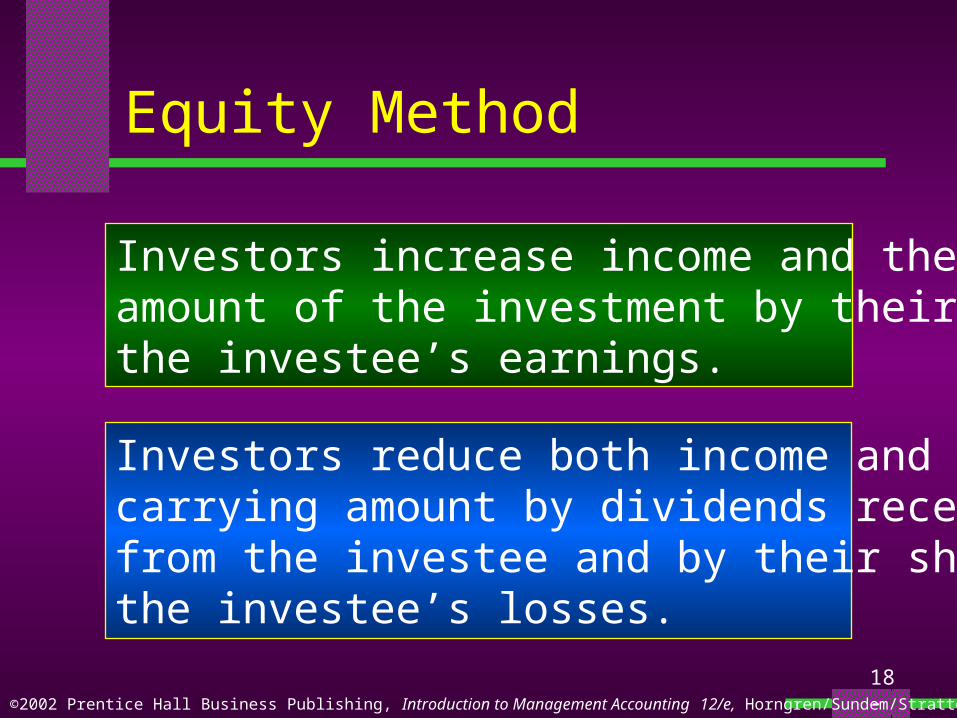

Equity Method

Investment at the acquisition cost adjustedfor dividends received and the investor’sshare of earnings or losses of the investeeafter the date of investment.

18 - 12

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Equity Method

Investors increase income and the carryingamount of the investment by their share ofthe investee’s earnings.

Investors reduce both income and thecarrying amount by dividends receivedfrom the investee and by their share inthe investee’s losses.

18 - 13

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Learning Objective 2

Explain the basic ideas and

methods used to prepare

consolidated financial

statements.

18 - 14

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Consolidated Financial Statements

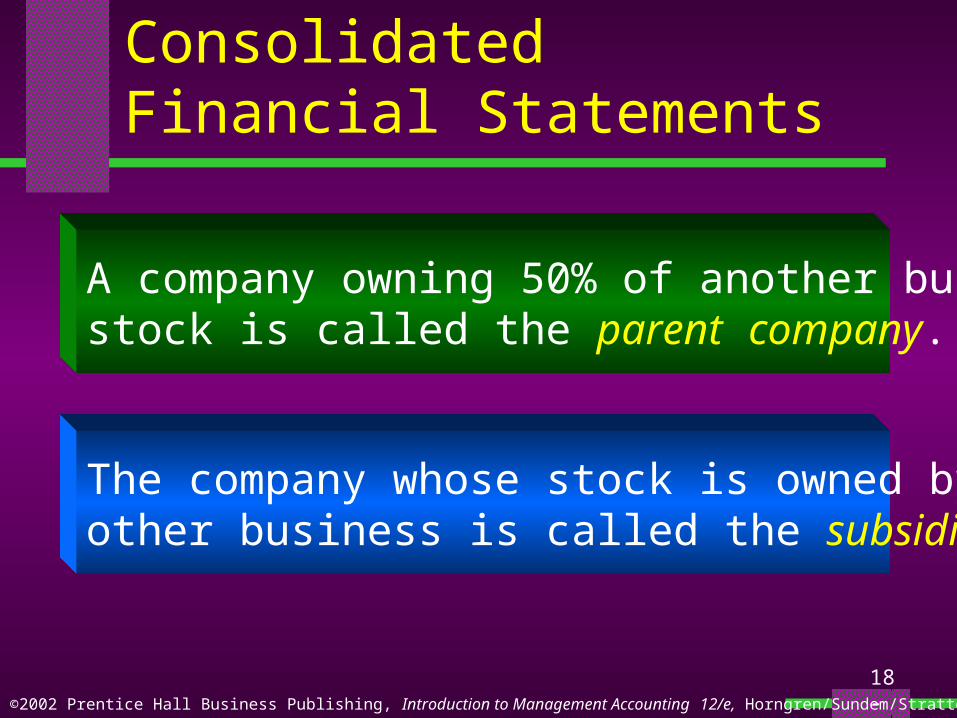

A company owning 50% of another business’sstock is called the parent company.

The company whose stock is owned by theother business is called the subsidiary.

18 - 15

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Consolidated Financial Statements

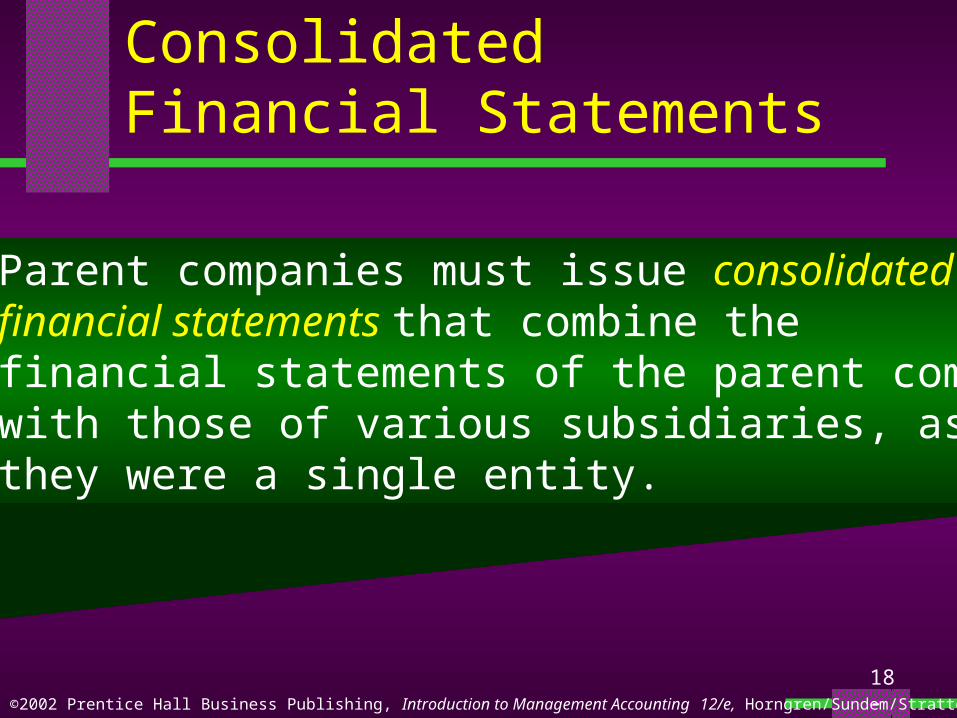

Parent companies must issue consolidatedfinancial statements that combine thefinancial statements of the parent companywith those of various subsidiaries, as ifthey were a single entity.

18 - 16

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

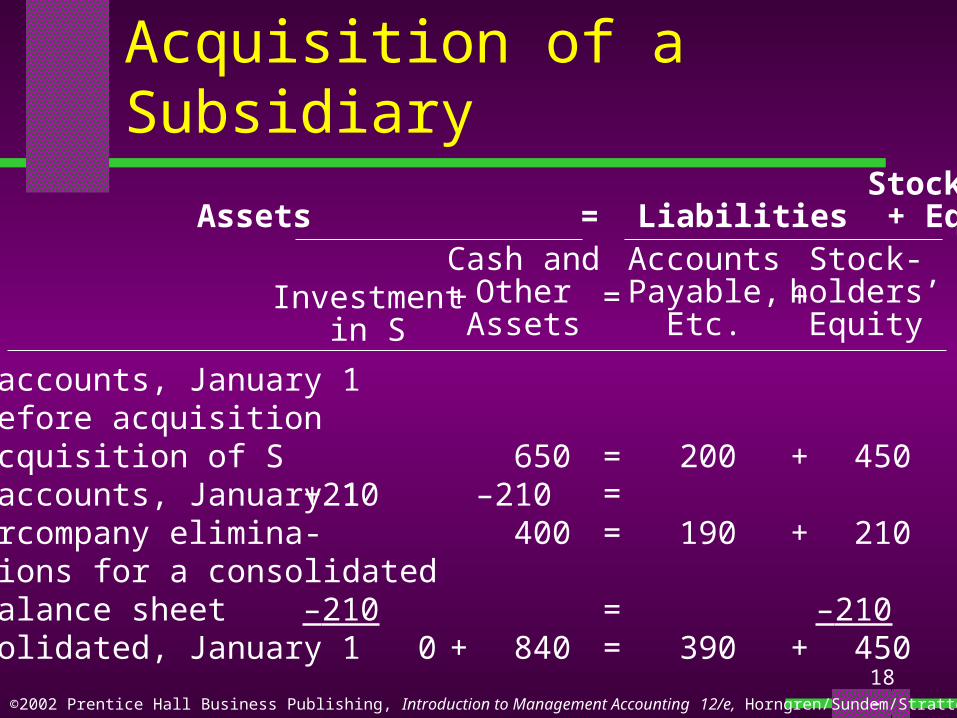

Acquisition of a Subsidiary

Suppose Company P (parent) acquired 100% of the common stock of Company S (subsidiary) for $210 million in cash at the beginning of the year.

The balance sheet accounts of both companies are analyzed in the following table (in millions of dollars):

18 - 17

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Acquisition of a Subsidiary

P’s accounts, January 1 Before acquisition Acquisition of SS’s accounts, January 1Intercompany elimina- tions for a consolidated balance sheetConsolidated, January 1

+210

–210 0

650–210 400

840

200

190

390

450

210

–210 450

Stockholders’Assets = Liabilities + Equity

Investmentin S

Cash andOtherAssets

AccountsPayable,

Etc.

Stock-holders’Equity

+ =

+

===

==

+

+

+

+

18 - 18

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Acquisition of a Subsidiary

P pays the $210 million to the formerowners of S as private investors.

The $210 million is not an addition tothe existing assets and stockholders’equity of S.

18 - 19

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Acquisition of a Subsidiary

Each legal entity has itsindividual set of books.

The consolidated entity does notkeep a separate set of books.

18 - 20

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Acquisition of a Subsidiary

To avoid double-counting, we eliminate the evidence of ownership present in two places.

1 The Investment in S on P’s books2 The Stockholders’ Equity on S’s books

18 - 21

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

After Acquisition

Investments in 50%- to 100% ownedsubsidiaries, such as the investment inS, are carried in the investor’s balancesheet by the equity method.

18 - 22

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Minority Interests

The Minority Interests account showsthe outside stockholders’ interest, asopposed to the parent’s interest, in asubsidiary corporation.

18 - 23

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Investments in Affiliates

Investments in equity securities that represent 20%to 50% ownership are frequently called investmentsin affiliates or investments in associates.

They are accounted for under the equity method.

18 - 24

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Learning Objective 3

Describe how goodwill arises

and how to account for it.

18 - 25

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Accounting for Goodwill

Suppose, using our previous example, that the price were $40 million higher, or a total of $250 million cash.

For simplicity, assume that the fair values of the individual assets of S are equal to their book values.

The balance sheets immediately after the acquisition are:

18 - 26

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Accounting for Goodwill

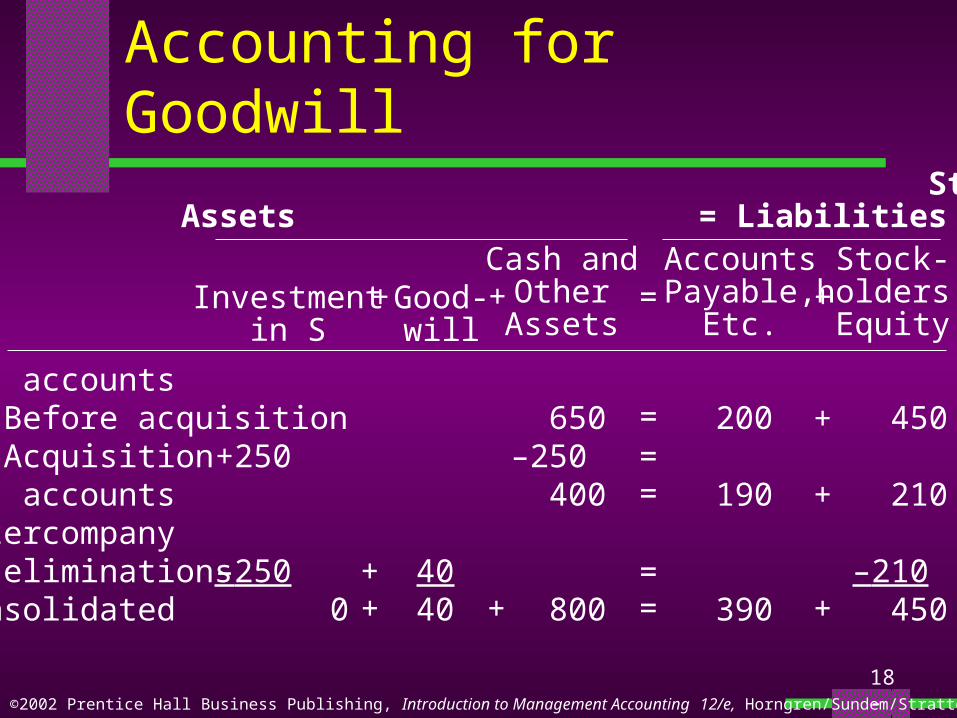

P’s accounts Before acquisition AcquisitionS’s accountsIntercompany eliminationsConsolidated

+250

–250 0

650–250 400

800

200

190

390

450

210

–210 450

Stockholder’Assets = Liabilities + Equity

Investmentin S

Cash andOtherAssets

AccountsPayable,

Etc.

Stock-holders’Equity

+

=

+

==

=

=

=

+

+

+

+

Good-will

4040 ++

+

18 - 27

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Accounting for Goodwill

What if the book valuesof the individual assetsof S are not equal totheir fair values?

18 - 28

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

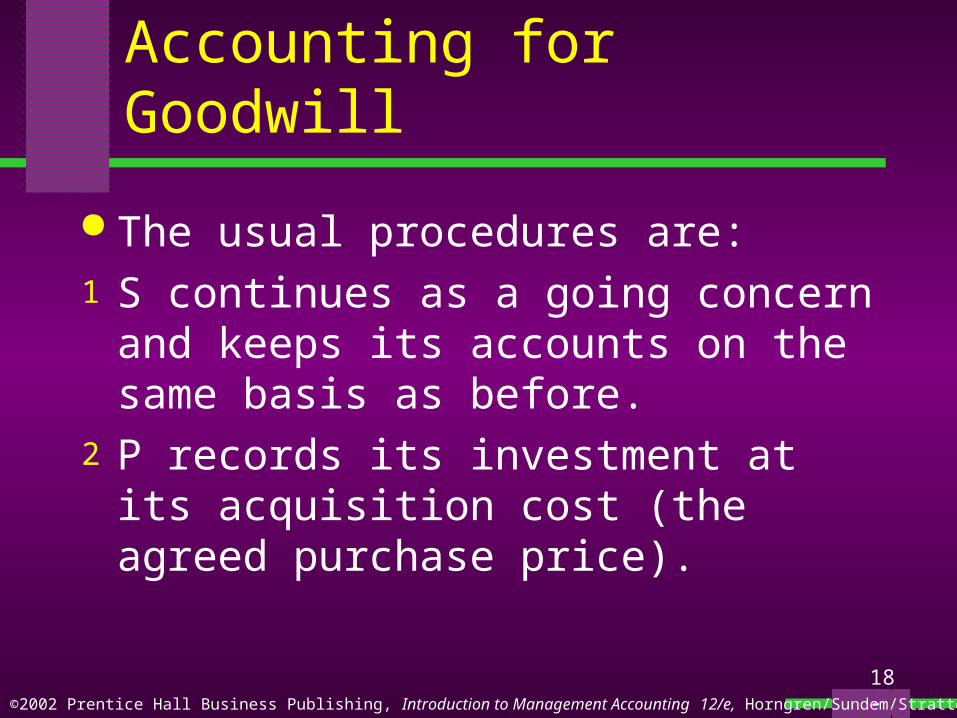

Accounting for Goodwill

The usual procedures are:1 S continues as a going concern and keeps

its accounts on the same basis as before.2 P records its investment at its acquisition

cost (the agreed purchase price).

18 - 29

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

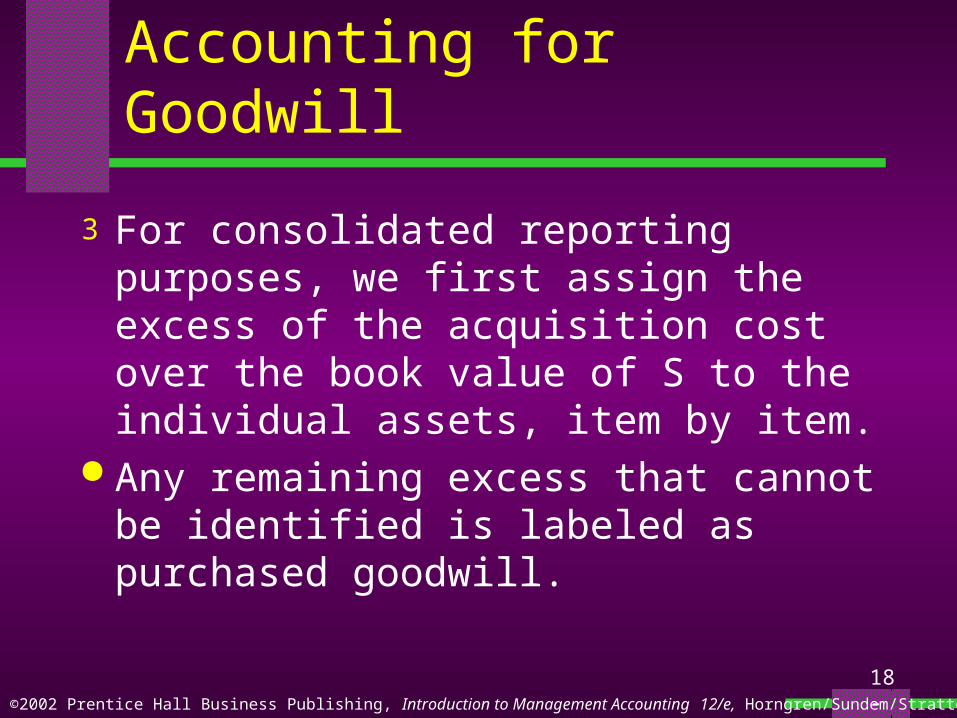

Accounting for Goodwill

3 For consolidated reporting purposes, we first assign the excess of the acquisition cost over the book value of S to the individual assets, item by item.

Any remaining excess that cannot be identified is labeled as purchased goodwill.

18 - 30

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

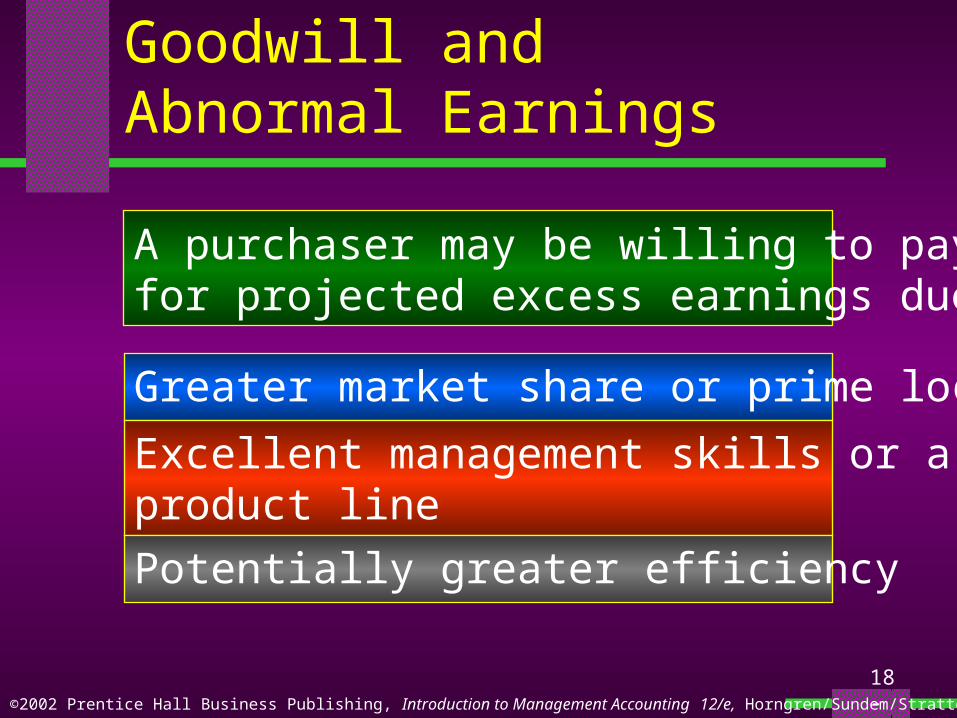

Goodwill and Abnormal Earnings

A purchaser may be willing to pay extrafor projected excess earnings due to:

Greater market share or prime location

Excellent management skills or a uniqueproduct line

Potentially greater efficiency

18 - 31

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Learning Objective 4

Explain and use a variety of

popular financial ratios.

18 - 32

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Financial Statements

Financial statements, expressed incomponent percentages, are calledcommon-size statements.

Investors and creditors often useratios computed from publishedfinancial statements to analyzecompanies.

18 - 33

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Some Typical Financial Ratios

– Current ratio– Average collection period in days– Current debt to equity– Total debt to equity– Gross profit rate or percentage

18 - 34

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Some Typical Financial Ratios

– Return on sales– Return on stockholders’ equity– Earnings per share– Price earnings– Dividend yield– Dividend payout

18 - 35

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Comparisons

Evaluation of a financial ratio requires a comparison.

There are three main types of comparisons:1 With a company’s own historical ratios

(called time-series comparisons)

18 - 36

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Comparisons

2 With general rules of thumb or benchmarks3 With ratios of other companies or with

industry averages for the same period (called cross-sectional comparisons)

18 - 37

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Operating Performance Ratios

The rate of return on invested capital is an important measure of overall accomplishment:

ROI = Income ÷ Invested capital

18 - 38

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

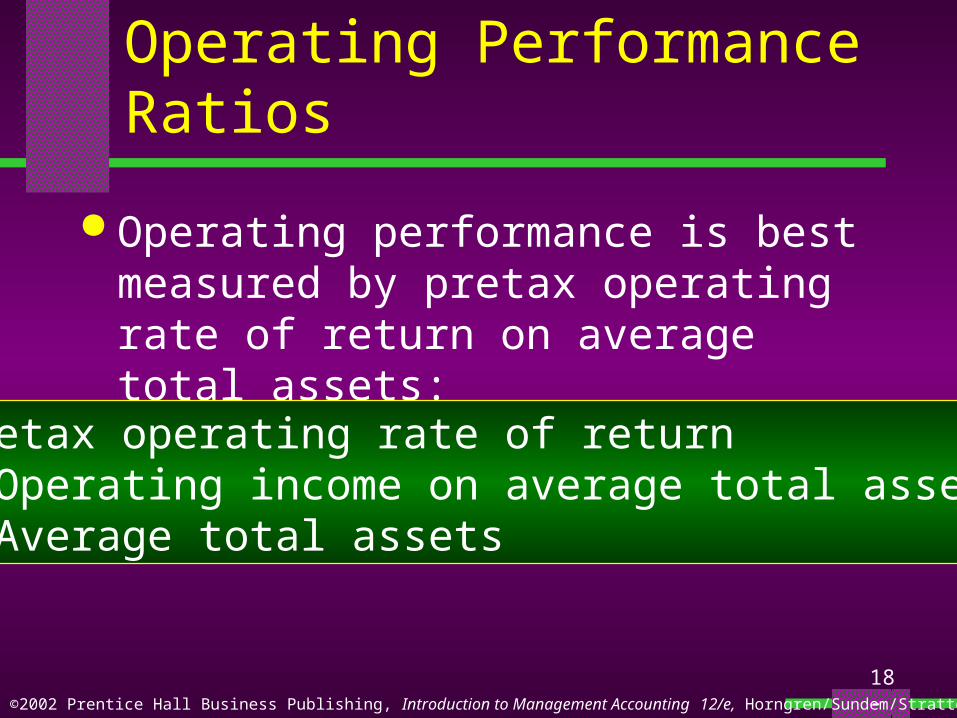

Operating Performance Ratios

Operating performance is best measured by pretax operating rate of return on average total assets:

Pretax operating rate of return= Operating income on average total assets÷ Average total assets

18 - 39

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Learning Objective 5

Identify the major implications

that efficient stock markets

have for accounting.

18 - 40

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Efficient Capital Market

An efficient capital market is one in which market prices “fully reflect” all information available to the public.

18 - 41

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Implications for Accounting in Efficient Stock Markets

Financial ratios and other data such asreported earnings help predict sucheconomic phenomena as financialfailure or earnings growth.

Accounting reports are only onesource of information.

18 - 42

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Implications for Accounting in Efficient Stock Markets

The market as a whole generally sees throughany attempts by companies to gain favorthrough the choice of accounting policiesthat tend to boost immediate income.

In the aggregate, the market is not fooled bycompanies that choose the least-conservativeaccounting policies.

18 - 43

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Implications for Accounting in Efficient Stock Markets

Thus there is evidence that the stock marketsmay indeed be “efficient,” at least in theirreflection of most accounting data.

18 - 44

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Learning Objective 6

Understand how financial

analysts use ratios and other

analysis techniques to interpret

the consolidated financial

statements of a company.

18 - 45

©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

Interpret Financial Statements

Financial analysts and other investmentadvisors use financial statements toanalyze the prospects for companiesthat they consider for investment.

They use financial ratios and othertechniques together with other informationto make investment decisions.

18 - 46©2002 Prentice Hall Business Publishing, Introduction to Management Accounting 12/e, Horngren/Sundem/Stratton

End of Chapter 18