Embed Size (px)

Citation preview

INVESTMENT MANAGEMENT

Investment management is the professional management of various securities (shares, bonds etc) and other assets (e.g. real estate), to meet specified investment goals for the benefit of the investors. Investors may be institutions (insurance companies, pension funds, corporations etc.) or private investors (both directly via investment contracts and more commonly via collective investment schemes e.g. mutual funds) .

The term asset management is often used to refer to the investment management of collective investments, whilst the more generic fund management may refer to all forms of institutional investment as well as investment management for private investors. Investment managers who specialize in advisory or discretionary management on behalf of (normally wealthy) private investors may often refer to their services as wealth management or portfolio management often within the context of so-called "private banking".

The provision of 'investment management services' includes elements of financial analysis, asset selection, stock selection, plan implementation and ongoing monitoring of investments.

Outside of the financial industry, the term "investment management" is often applied to investments other than financial instruments. Investments are often meant to include projects, brands, patents and many things other than stocks and bonds. Even in this case, the term implies that rigorous financial and economic analysis methods are used. Applied Information Economics is one approach developed to apply statistically and economically sound optimization methods to portfolios of other types of investments.

Investment management is a large and important global industry in its own right responsible for caretaking of trillions of dollars, euro, pounds and yen. Coming under the remit of financial services many of the world's largest companies are at least in part investment managers and employ millions of staff and create billions in revenue.

Fund manager (or investment advisor in the U.S.) refers to both a firm that provides investment management services and an individual(s) who directs 'fund management' decisions.

Industry scope

The business of investment management has several facets, including the employment of professional fund managers, research (of individual assets and asset classes), dealing, settlement, marketing, internal auditing, and the preparation of reports for clients. The largest financial fund managers are firms that exhibit all the complexity their size demands. Apart from the people who bring in the money (marketers) and the people who direct investment (the fund managers), there are compliance staff (to ensure accord with legislative and regulatory constraints), internal auditors of various kinds (to examine internal systems and controls), financial controllers (to account for the institutions' own

money and costs), computer experts, and "back office" employees (to track and record transactions and fund valuations for up to thousands of clients per institution).

Key problems of running such businesses

• Revenue is directly linked to market valuations, so a major fall in asset prices causes a precipitous decline in revenues relative to costs;

• Above-average fund performance is difficult to sustain, and clients may not be patient during times of poor performance;

• Successful fund managers are expensive and may be headhunted by competitors; • Above-average fund performance appears to be dependent on the unique skills of

the fund manager; however, clients are loath to stake their investments on the ability of a few individuals- they would rather see firm-wide success, attributable to a single philosophy and internal discipline;

• Evidence suggests that size of an investment firm correlates inversely with fund performance, i.e., the smaller the firm the better the chance of good performance.

• Analysts who generate above-average returns often become sufficiently wealthy that they eschew corporate employment in favor of managing their personal portfolios.

The most successful investment firms in the world have probably been those that have been separated physically and psychologically from banks and insurance companies. That is, the best performance and also the most dynamic business strategies (in this field) have generally come from independent investment management firms.

Investment managers and portfolio structures

At the heart of the investment management industry are the managers who invest and divest client investments.

A certified company investment advisor should conduct an assessment of each client's individual needs and risk profile. The advisor then recommends appropriate investments.

Asset allocation

The different asset classes are stocks, bonds, real-estate, derivatives, and commodities. The exercise of allocating funds among these assets (and among individual securities within each asset class) is what investment management firms are paid for. Asset classes exhibit different market dynamics, and different interaction effects; thus, the allocation of monies among asset classes will have a significant effect on the performance of the fund. Some research suggests that allocation among asset classes has more predictive power than the choice of individual holdings in determining portfolio return. Arguably, the skill of a successful investment manager resides in constructing the asset allocation, and separately the individual holdings, so as to outperform certain benchmarks (e.g., the peer group of competing funds, bond and stock indices).

Long-term returns

It is important to look at the evidence on the long-term returns to different assets, and to holding period returns (the returns that accrue on average over different lengths of investment).

Diversification

Against the background of the asset allocation, fund managers consider the degree of diversification that makes sense for a given client (given its risk preferences) and construct a list of planned holdings accordingly. The list will indicate what percentage of the fund should be invested in each particular stock or bond. The theory of portfolio diversification was originated by Markowitz and effective diversification requires management of the correlation between the asset returns and the liability returns, issues internal to the portfolio (individual holdings volatility), and cross-correlations between the returns.

Investment styles

There are a range of different styles of fund management that the institution can implement. For example, growth, value, market neutral, small capitalization, indexed, etc. Each of these approaches has its distinctive features, adherents and, in any particular financial environment, distinctive risk characteristics.

Performance measurement

Fund performance is the acid test of fund management, and in the institutional context accurate measurement is a necessity. For that purpose, institutions measure the performance of each fund (and usually for internal purposes components of each fund) under their management, and performance is also measured by external firms that specialize in performance measurement.

Absolute versus relative performance

In the USA and the UK, two of the world's most sophisticated fund management markets, the tradition is for institutions to manage client money relative to benchmarks. For example, an institution believes it has done well if it has generated a return of 5% when the average manager generates a 4% return.

Risk-adjusted performance measurement

Performance measurement should not be reduced to the evaluation of fund returns alone, but must also integrate other fund elements that would be of interest to investors, such as the measure of risk taken. Several other aspects are also part of performance measurement: evaluating if managers have succeeded in reaching their objective, i.e. if

their return was sufficiently high to reward the risks taken; how they compare to their peers; and finally whether the portfolio management results were due to luck or the manager’s skill. The need to answer all these questions has led to the development of more sophisticated performance measures, many of which originate in modern portfolio theory.

What Is Investment• Many interpretations• Lending money to another for a return• Purchase of shares, real estate, Gold for capital appreciation • An insurance plan or Pension plan• Investment is a commitment of funds for earning additional income• Investment is considered as the sacrifice of certain present value of money in

anticipation of a reward

Definition of Investment• Fisher & Jordan – An investment is a commitment of funds made in the

expectation of some positive rate of returns• F. Amling – The purchase by an individual or Institutional investor of a financial

or real asset that produces a return in proportion to the risk the Investor assumed over some future investment period

Investment Scenario• Today, managing investment has become much more challenging and complex

than ever• Unprecedented volatility of stock market• Mutual funds• Derivatives• Debt market• Bank/ Company deposits• Gold• Real estate• Plethora of investment instruments to choose from

Classification of investment• Financial investment • Economic investment

Financial investment• It means employment of funds in the form of assets with the objective of earning

additional income or appreciation in the value of investment in future• Assets for investment vary with respect to risk, Safety and return• Bank deposits, Bonds, Shares, Mutual funds

Economic investment• It is net addition to the capital stock of the society • Investment in those goods and services which are used for the production of other

goods and services• Building, Machineries, Inventories

Investment Involves 1. Real assets • Real assets are tangible assets like land, buildings, bullions

2. Financial assets• Financial assets are instruments having an indirect claim to real assets held by

some others

Investment Objectives Maximization of the economic welfare of the investor in the long run. Maximization of wealth and the liquidity offered by the wealth.

Objectives Involves• Return• Capital appreciation• Safety• Liquidity• Hedge against inflation• Tax planning

Return• Investment is a commitment of funds made in the expectation of some positive

return.• Investor while making investments consider many aspects related to return such

as the timing, frequency and quantum of return

Capital Appreciation• It is an important objective of investment • Before investment investors should identity the assets which appreciate in value• Real asset or financial asset

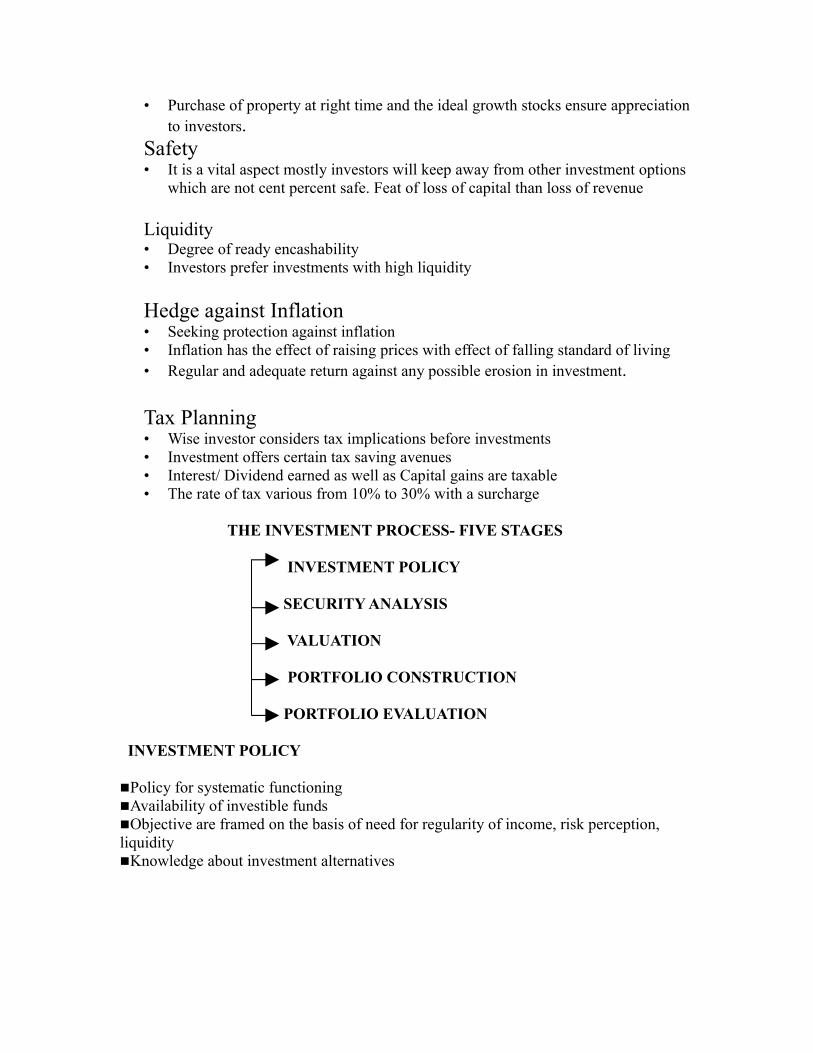

• Purchase of property at right time and the ideal growth stocks ensure appreciation to investors.

Safety• It is a vital aspect mostly investors will keep away from other investment options

which are not cent percent safe. Feat of loss of capital than loss of revenue Liquidity• Degree of ready encashability• Investors prefer investments with high liquidity

Hedge against Inflation• Seeking protection against inflation• Inflation has the effect of raising prices with effect of falling standard of living• Regular and adequate return against any possible erosion in investment.

Tax Planning• Wise investor considers tax implications before investments• Investment offers certain tax saving avenues• Interest/ Dividend earned as well as Capital gains are taxable• The rate of tax various from 10% to 30% with a surcharge

THE INVESTMENT PROCESS- FIVE STAGES

INVESTMENT POLICY SECURITY ANALYSIS

VALUATION

PORTFOLIO CONSTRUCTION

PORTFOLIO EVALUATION INVESTMENT POLICY

Policy for systematic functioningAvailability of investible fundsObjective are framed on the basis of need for regularity of income, risk perception, liquidityKnowledge about investment alternatives

SECURITY ANALYSIS

The securities to be bought have to be scrutinized through the market, industry and company analysis

VALUATIONHelps investor to determine the return and risk expected from an investment in the common stockIntrinsic value of the share is measured through the book value of the share and the price earning ratio.

PORTFOLIO CONSTRUCTIONPortfolio is a combination of securitiesPortfolio is constructed in a manner to meet the investors goalsMaximum return with minimum riskDiversifies portfolio and allocation of funds among the selected securities

PORTFOLIO EVALUATIONThe portfolio has to be managed efficientlyThe efficient management requires evaluation This process consist of portfolio appraisal and revision

PORTFOLIO APPRAISALThe return and risk performance of the security vary from time to time The variability of the returns of the securities is measured and comparedThe appraisal warns the loss and steps can be taken to avoid such losses

PORTFOLIO REVISIONRevision depends on the results of the appraisalTo keep the return at a particular level necessitates the investor to revise the components of the portfolio periodically

FUNDAMENTAL ANALYSIS:

Introduction

Fundamental analysis is the cornerstone of investing. In fact, some would say that you aren't really investing if you aren't performing fundamental analysis. Because the subject is so broad, however, it's tough to know where to start. There are an endless number of investment strategies that are very different from each other, yet almost all use the fundamentals.

The goal of this tutorial is to provide a foundation for understanding fundamental analysis. It's geared primarily at new investors who don't know a balance sheet from an income statement. While you may not be a "stock-picker extraordinaire" by the end of this tutorial, you will have a much more solid grasp of the language and concepts behind security analysis and be able to use this to further your knowledge in other areas without feeling totally lost.

The biggest part of fundamental analysis involves delving into the financial statements. Also known as quantitative analysis, this involves looking at revenue, expenses, assets, liabilities and all the other financial aspects of a company. Fundamental analysts look at this information to gain insight on a company's future performance. A good part of this tutorial will be spent learning about the balance sheet, income statement, cash flow statement and how they all fit together

What is Fundamental Analysis?

A method of evaluating a security by attempting to measure its intrinsic value by examining related economic, financial and other qualitative and quantitative factors. Fundamental analysts attempt to study everything that can affect the security's value, including macroeconomic factors (like the overall economy and industry conditions) and individually specific factors (like the financial condition and management ofcompanies).

The end goal of performing fundamental analysis is to produce a value that an investor can compare with the security's current price in hopes of figuring out what sort of position to take with that security (under priced = buy, overpriced = sell or short).

Securities market lineThe securities market line (SML) graphs the relationship between risk and return. The securities market line is a straight line. It touches the efficient frontier and passes though the risk free rate of return.

The SML lies above the efficient frontier, except at the one point where it touches. This shows that the availability of a risk free asset improves the returns available for a any given level of risk and vice-versa. The line that graphs the systematic, or market, risk versus return of the whole market at a certain time and shows all risky marketable securities.

Technical Analysis

A method of evaluating securities by analyzing statistics generated by market activity, such as past prices and volume. Technical analysts do not attempt to measure a security's intrinsic value, but instead use charts and other tools to identify patterns that can suggest future activity

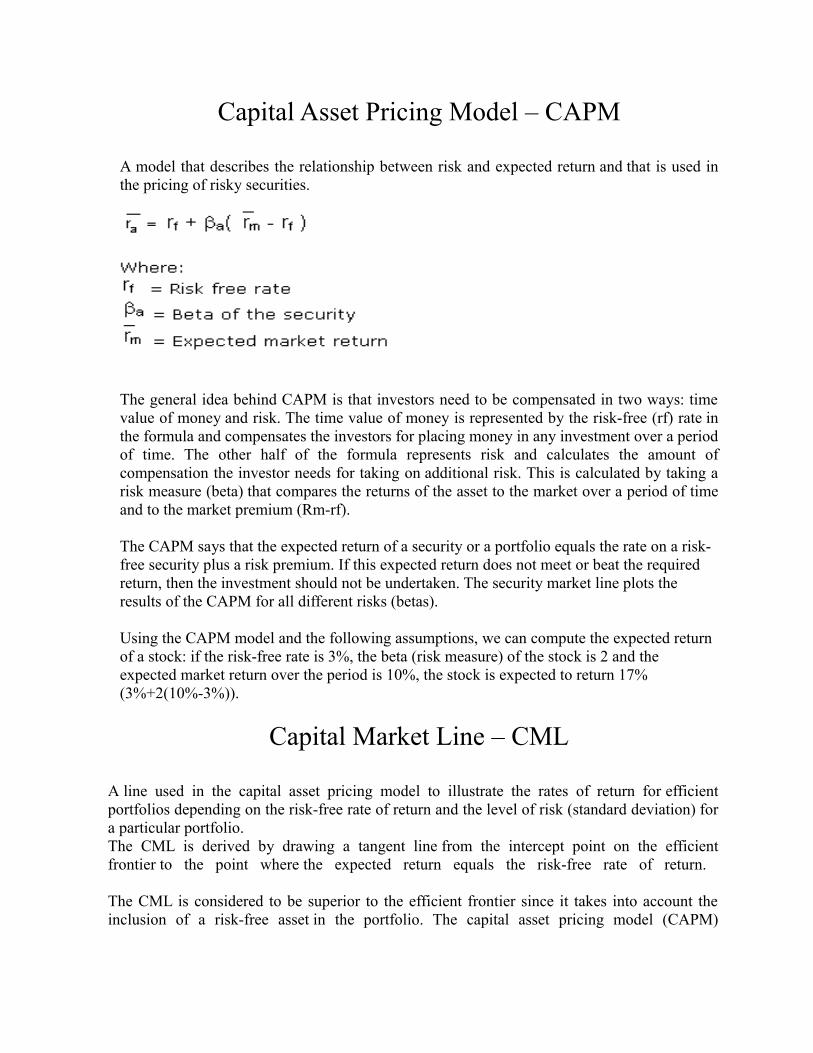

Capital Asset Pricing Model – CAPM

A model that describes the relationship between risk and expected return and that is used in the pricing of risky securities.

The general idea behind CAPM is that investors need to be compensated in two ways: time value of money and risk. The time value of money is represented by the risk-free (rf) rate in the formula and compensates the investors for placing money in any investment over a period of time. The other half of the formula represents risk and calculates the amount of compensation the investor needs for taking on additional risk. This is calculated by taking a risk measure (beta) that compares the returns of the asset to the market over a period of time and to the market premium (Rm-rf).

The CAPM says that the expected return of a security or a portfolio equals the rate on a risk-free security plus a risk premium. If this expected return does not meet or beat the required return, then the investment should not be undertaken. The security market line plots the results of the CAPM for all different risks (betas).

Using the CAPM model and the following assumptions, we can compute the expected return of a stock: if the risk-free rate is 3%, the beta (risk measure) of the stock is 2 and the expected market return over the period is 10%, the stock is expected to return 17% (3%+2(10%-3%)).

Capital Market Line – CML

A line used in the capital asset pricing model to illustrate the rates of return for efficient portfolios depending on the risk-free rate of return and the level of risk (standard deviation) for a particular portfolio.The CML is derived by drawing a tangent line from the intercept point on the efficient frontier to the point where the expected return equals the risk-free rate of return.

The CML is considered to be superior to the efficient frontier since it takes into account the inclusion of a risk-free asset in the portfolio. The capital asset pricing model (CAPM)

demonstrates that the market portfolio is essentially the efficient frontier. This is achieved visually through the security market line (SML).

Portfolio Management

The art and science of making decisions about investment mix and policy, matching investments to objectives, asset allocation for individuals and institutions, and balancing risk vs. performance

SECURITY ANALYSIS

Security Analysis, authored by professors Benjamin Graham and David Dodd of Columbia University, laid the intellectual foundation for what would later be called "value investing". The work was first published in 1934, following unprecedented losses on Wall Street. In summing up lessons learned, Graham and Dodd chided Wall Street for its myopic focus on a company's reported earnings per share, and were particularly harsh on the favored "earnings trends." They encouraged investors to take an entirely different approach by gauging the rough value of the operating business that lay behind the security. Graham and Dodd enumerated multiple actual examples of the market's tendency to irrationally under-value certain out-of-favor securities. They saw this tendency as an opportunity for the savvy.

At bottom, Security Analysis stands for the proposition that a well-disciplined investor can determine a rough value for a company from all of its financial statements, make purchases when the market inevitably under-prices some of them, earn a satisfactory return, and never be in real danger of permanent loss. Warren Buffett, the only student in Graham's investment seminar to earn an A+, made billions of dollars by methodically and rationally implementing the tenets of Graham and Dodd's book.

Security Analysis is still used as a textbook at Columbia University. Security Analysis also represents the genesis of financial analysis and fundamental analysis. However, in the 1970s Graham stopped advocating a careful use of the techniques described in his text in selecting individidual stocks, citing the extensive efforts and costs required to generate superior returns in a modern efficient market. Instead, Graham later suggested the use of one or two simple criteria to the investor's entire portfolio, focusing on results of the group rather than on individual securities.[1]

Systematic Risk

Risk which is common to an entire class of assets or liabilities. The value of investments may decline over a given time period simply because of economic changes or other events that impact large portions of the market. Asset allocation and diversification can protect against systematic risk because different portions of the market tend to underperforms at different times. also called market risk.

The risk inherent to the entire market or entire market segment. Also known as "un-diversifiable risk" or "market risk."

Market risk

Market risk is the risk that the value of an investment will decrease due to moves in market factors. The four standard market risk factors are:

• Equity risk , or the risk that stock prices will change. • Interest rate risk , or the risk that interest rates will change. • Currency risk , or the risk that foreign exchange rates will change. • Commodity risk , or the risk that commodity prices (i.e. grains, metals, etc.) will

change.

Measuring

Market risk is typically measured using a Value at Risk methodology. Value at risk is well established as a risk management technique, but it contains a number of limiting assumptions that constrain its accuracy. The first assumption is that the composition of the portfolio measured remains unchanged over the single period of the model. For short time horizons, this limiting assumption is often regarded as acceptable. For longer time horizons, many of the transactions in the portfolio may mature during the modeling period. Intervening cash flow, embedded options, changes in floating rate interest rates, and so on are ignored in this single period modeling technique.

Market risk can also be contrasted with Specific risk, which measures the risk of a decrease in ones investment due to a change in a specific industry or sector, as opposed to a market-wide move.

Unsystematic Risk

Risk that affects a very small number of assets. Sometimes referred to as specific risk. The risk of price change due to the unique circumstances of a specific security, as opposed to the overall market. This risk can be virtually eliminated from a portfolio through diversification.

Technical analysts A method of evaluating securities by analyzing statistics generated by market activity, such as past prices and volume. Technical analysts do not attempt to measure a security's intrinsic value, but instead use charts and other tools to identify patterns that can suggest future activity.

Technical analysis is the study of past financial market data, primarily through the use of charts, to forecast price trends and make investment decisions. In its purest form, technical analysis considers only the actual price behavior of the market or instrument, based on the premise that price reflects all relevant factors before an investor becomes aware of them through other channels.

Technical analysts (or technicians) identify non-random price patterns and trends in financial markets and attempt to exploit those patterns.[1] While technicians use various methods and tools, the study of price charts is primary. Technicians especially search for archetypal patterns, such as the well-known head and shoulders reversal pattern, and also study such indicators as price, volume, and moving averages of the price. Many technical analysts also follow indicators of investor psychology (market sentiment).

Technicians seek to forecast price movements such that large gains from successful trades exceed more numerous but smaller losing trades, producing positive returns in the long run through proper risk control and money management.

There are several schools of technical analysis. Adherents of different schools (for example, candlestick charting, Dow Theory, and Elliott wave theory) may ignore the other approaches, yet many traders combine elements from more than one school. Technical analysts use judgment gained from experience to decide which pattern a particular instrument reflects at a given time, and what the interpretation of that pattern should be. Technical analysts may disagree among themselves over the interpretation of a given chart.

Technical analysis is frequently contrasted with fundamental analysis, the study of economic factors that some analysts say can influence prices in financial markets. Pure technical analysis holds that prices already reflect all such influences before investors are aware of them, hence the study of price action alone. Some traders use technical or fundamental analysis exclusively, while others use both types to make trading decisions.

RETURN

Return is the primary motivating force that drives investment. It is representing the reward for undertaking investment. Components of return are:

Current return- it measured as the periodic income in relation to the beginning price of the investment.

Capital return- the price appreciation or depreciation divided by the beginning price of the asset. Assets like equity stock

Total return for any security is defined as: Total return = current return + capital return

NOMINAL RETURN CAPITAL APPRECIATION DIVIDENDS COMPOUND RATE OF RETURN HOLDING PERIOD RETURN

CAPITAL APPRECIATION

Investment in assets whose face value increases with passage of timeCapital appreciation of investments ensures that the purchasing power of investment keep pace with inflation (prevents eroding value)

DIVIDENDS

When you invest in company shares your annual returns come form dividends

COMPOUND RATE OF RETURN

When the interest earns interest the security is said to be paying a compound interestThe interest earned amount is automatically reinvested as the same rate as applicable to the original investment.

HOLDING PERIOD RETURN

Investments are made for a certain period. The HPR takes into account the total returns to an investor in that period, including both interest or dividend, and capital gains, if any.

HPR = Total income during holding period (Dividend/ Interest + Capital Gain) ÷ Purchase price X 100

FACTORS DETERMINING RETURN ON INVESTMENT

Price of the stockType of the stockIssue price of the stockReserve for dividendFuture projects of the companyGoodwill of the companyGovt. rules and polices.

RISK

Risk is defined as possibility of meeting danger or of suffering from harm or loss.In financial terms, it implies possibility of receiving less return than expected orNot receiving any return at all orEven not getting your principal amount backThe probability of actual return being less than the expected return or the probability of adverse return“Worry is not a sickness but a sign of health if you are not worried you are not risking enough”You cannot be rich without taking risksRisks and rewards go hand in handHigher the risks, higher the returns the investment is expected to generate.You should take calculated, not reckless risks Every investment opportunity is exposed to some risk or the otherA full understanding of the various important risks is essential for taking calculated risks and making sensible investment decisions. RISKS CLASSIFICATIONS 1. Systematic Risks

Market risk Interest rate risk Purchasing power risk

2. Unsystematic risks

Business Risk Financial Risk Insolvency or Default Risk

3. Other risks

Political risk Management risk Marketability Risk

Total Risk = Systematic Risk + Unsystematic Risk

SYSTEMATIC RISK It emanates from three sources:Market risk

Interest rate riskInflation risk

SYSTEMATIC RISKExternal factors that cannot be controlled cause risks which are known as systematic risksSystematic risk are non diversifiableArise out of factors such as market, nature of industry, state of economy etc.

MARKET RISKMarket risk is the risk of movement in security prices due to factors that affect the market as a whole, rather than particular companies or industries.Investors reaction towards various events is the main factor affecting the market risk. Business recession, depression, long term changes in consumption pattern.Unexpected war, election, instability of Govt., demise of head of state, speculative activity in the market.The fall or rise in the prices of security causes a fear of loss or utmost confidence in the minds of investors.When investors sharply react to a loss, it will result in excessive selling, pushing prices downInvestors reaction to gain will result in more buying, pushing prices upGood economic forecasting is the key to anticipating changes in the stock and bond markets.

INTEREST RATE RISKA change in interest rate is a major source of risk to the holders of bonds & debentures.An increase in interest rate will result in decrease in demand for securities.Increase in interest rate will result in increased earnings to lending institutionsCompanies using borrowed funds, will result in lower earnings, lower dividends, and consequent lower share prices. Securities produce cash income streams over future time periods. They are discounted by the market to yields present values which influence prices of these securities. When ever the discount factor changes or cash stream changes, prices also change.Rise in market interest rate causes a decline in market prices of securities and vice versa.

PURCHASING POWER RISK/ INFLATION RISKPurchasing power risk is the probable loss in purchasing power of returns to be received.If inflation occurs during future period the buying power of cash interest/dividend income is likely to be received would decline. If rate of inflation is equal to the money rate of return, the investor does not add anything to his existing wealth since he obtains zero rate of return.Investment is considered as postponement of consumption

UNSYSTEMATIC RISKRisk due to uncertainty surrounding a particular firm or industry.It is unique & peculiar to a firm or industryDue to factors like managerial inefficiency, technological change, availability if raw material, changes in consumer preference, labor problems Unsystematic risk emanates from three sourcesBusiness riskFinancial riskDefault or insolvency risk

BUSINESS RISKBusiness risk is that portion of risk caused by prevailing environment of businessVariation that causes in operating environmentBusiness risk can be of two broad categories 1. Internal business risk 2. External business risk

INTERNAL BUSINESS RISK

Fluctuation in sales : loss of sales means loss of profitR&D : R&D is required for constant innovation & for operational efficiencyHRM : operational efficiency depends on management of personnelFixed cost : cost should be justifiable & not to affect profitabilityProduction of single product

EXTERNAL BUSINESS RISK

Business cycle : fluctuation in business cycle leads to fluctuation in earningsDemographic factor: distribution of population by age group, health, education and lack of skill of employees, attitude to work.Government polices: Risk due to Govt. polices, FDI, Disinvestment, nationalization etcSocial & Regulatory factors : General operating environment of business, environmental protection act, price control, fixation of quotas, import- export control FINANCIAL RISKSThe way the company handles its financial activitiesIt can be ascertained by the analysis of capital structure of the firmHigh employment of debt in business

DEFAULT RISK

This risk due to inability of firm to satisfy the needs of investors like interest, dividend, repayment of capital etc The default risk arises due to deterioration of financial strength of the companyAdverse movements in liquidity, solvency, operating expenses

> OTHER RISKSPolitical riskManagement riskMarketability risk

POLITICAL RISKMainly for investment in foreign securitiesChange in foreign Govt.Nationalization of business in foreign country.Inability of Govt. to handle indebtedness

MANAGEMENT RISKTotal variability of return caused by management decisionHowever qualified & capable management team there are chances of judgmental errors and wrong decisions

MARKETABILITY RISKLoss of liquidity and monitory loss in conversion from one asset to another.

STOCK EXCHANGE

A stock exchange, share market or bourse is a corporation or mutual organization which provides facilities for stock brokers and traders, to trade company stocks and other securities. Stock exchanges also provide facilities for the issue and redemption of securities, as well as, other financial instruments and capital events including the payment of income and dividends. The securities traded on a stock exchange include: shares issued by companies, unit trusts and other pooled investment products and bonds. To be able to trade a security on a certain stock exchange, it has to be listed there. Usually there is a central location at least for recordkeeping, but trade is less and less linked to such a physical place, as modern markets are electronic networks, which gives them advantages of speed and cost of transactions. Trade on an exchange is by members only. The initial offering of stocks and bonds to investors is by definition done in the primary market and subsequent trading is done in the secondary market. A stock exchange is often the most important component of a stock market. Supply and demand in stock markets is driven by various factors which, as in all free markets, affect the price of stocks (see stock valuation).

There is usually no compulsion to issue stock via the stock exchange itself, nor must stock be subsequently traded on the exchange. Such trading is said to be off exchange or over-the-counter. This is the usual way that bonds are traded. Increasingly, stock exchanges are part of a global market for securities.

The role of stock exchanges

Raising capital for businesses Mobilizing savings for investment Facilitating company growth Redistribution of wealth Corporate governance Creating investment opportunities for small investors Government capital-raising for development projects Barometer of the economy

ONLINE SECURITIES TRADING

Shares and other financial products or securities (e.g. bonds, foreign exchange and managed investment funds) (Securities) may be exchanged or traded online using the internet (Exchanges). The Internet helps drive down transaction costs, facilitate cross-border transactions and avoid the need to conduct trades using intermediaries.

As the trend of doing thing through Internet is growing very rapidly and everyone in today’s life want to do every with the mouse clicks while sitting around his desk. Thus if you are an investor and want to do online trading, it is necessary for you to know well about online trading before actually staring trading online. These are various trading academies giving training on online trading. These institutions are also providing online training.

Objectives of online securities trading

Increase transparence in the markets. Enhance market quality through improved liquidity, by increasing quote continuity

and market depth. Reduce settlement risks due to open trade, by elimination of mismatches. Provide management information system. Introduce flexibility in system, to handling growing volumes easily and to support

nationwide expansion of market activity.

Through online trading three fundamental objectives of securities regulation can be easily achieved these are :

1. Investor’s protection. 2. Creation of a fair and efficient market. 3. Reduction of the systematic risks.

SECURITIES AND EXCHANGE BOARD OF INDIA (SEBI)

The Securities and Exchange Board of India came into being in April 1988 to promote orderly and healthy development of the securities markets and to provide adequate investor protection. It was a long –felt need to establish a competent authority in order to liberate the growing security market from the existing trading malpractices and inadequacies prevailing in the market. Headquarters in Bombay, SEBI’s function is to ensure a conductive environment for growth in the capital market. The environment includes the rules and regulations, the institutions and these interrelationships, instruments, practices, infrastructure and policy framework. A legal body, SEBI caters to the need of the issue of securities, the investor and the market intermediaries. SEBI has also been releasing a number of guidelines for playing the market. The new framework aims at better investor protection through improved disclosure requirements, accounting standards, compensation and arbitration, small investor’s protection fund, steps against insider trading and other malpractices.

Objectives of SEBI

As per SEBI act 1992 it has mainly three objectives:

Protection of investor’s interests and thus ensuring steady flow of saving from the savers to the capital market.

Promotion of growth and development of securities market.

Regulation of securities market in order to ensue efficient services by merchant bankers, brokers, mutual funds and other intermediaries.

The role of SEBI

It is an independently constituted board with regulatory power over stock

exchanges, mutual funds and capital issues. However, there is government control in the sense of having nominees from the Ministry on its Board. The regulatory powers

given to SEBI are also subject to government directives and overrules. The power to prosecute and find defaulters is also denied. SEBI is trying to establish itself with its two- fold role of trying to implement existing legislations and of introducing new guidelines and regulations.

DEMATERIALIZATION

Demat account

Demat account, short term for dematerialized account is a type of banking account which dematerialize the paper-based physical shares. The idea of dematerialized account is to avoid the need to hold physical shares--the shares are virtually being bought and sold through the banking account. This account is popular in India and also the SEBI mandates Demat account for share trading above 500 shares.

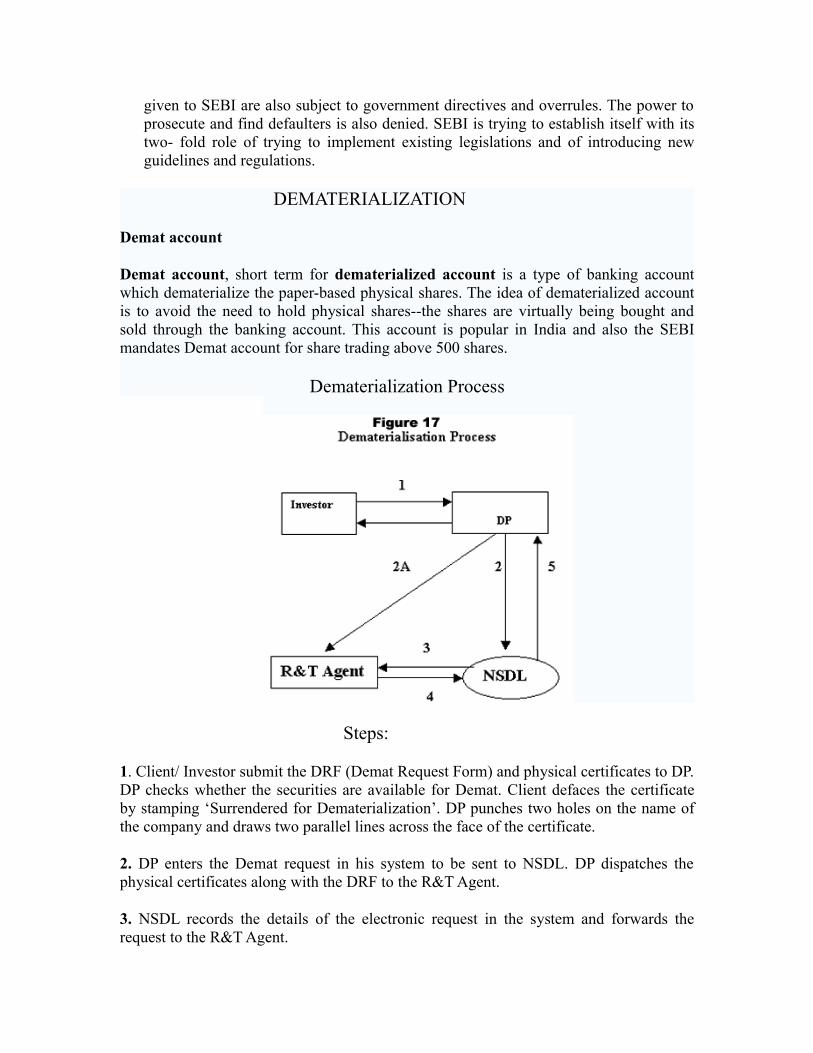

Dematerialization Process

Steps:

1. Client/ Investor submit the DRF (Demat Request Form) and physical certificates to DP. DP checks whether the securities are available for Demat. Client defaces the certificate by stamping ‘Surrendered for Dematerialization’. DP punches two holes on the name of the company and draws two parallel lines across the face of the certificate.

2. DP enters the Demat request in his system to be sent to NSDL. DP dispatches the physical certificates along with the DRF to the R&T Agent.

3. NSDL records the details of the electronic request in the system and forwards the request to the R&T Agent.

4. R&T Agent, on receiving the physical documents and the electronic request, verifies and checks them. Once the R&T Agent is satisfied, dematerialization of the concerned securities is electronically confirmed to NSDL.

5. NSDL credits the dematerialized securities to the beneficiary account of the investor and intimates the DP electronically. The DP issues a statement of transaction to the client.