Embed Size (px)

Citation preview

17th September 2015Craig Henry

CRACKING THE CONNECTEDDIGITAL CONSUMER ENGAGEMENT

Copy

right

©20

13 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

2

Copy

right

©20

13 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

3

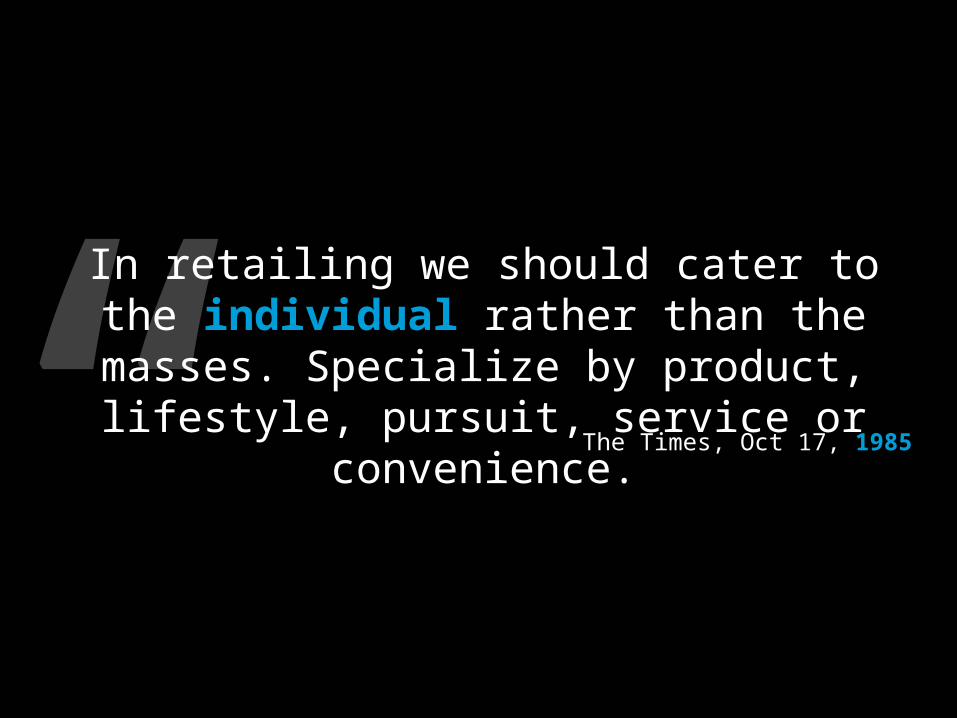

“ ”In retailing we should cater to the individual

rather than the masses. Specialize by product, lifestyle, pursuit, service or convenience.

The Times, Oct 17, 1985

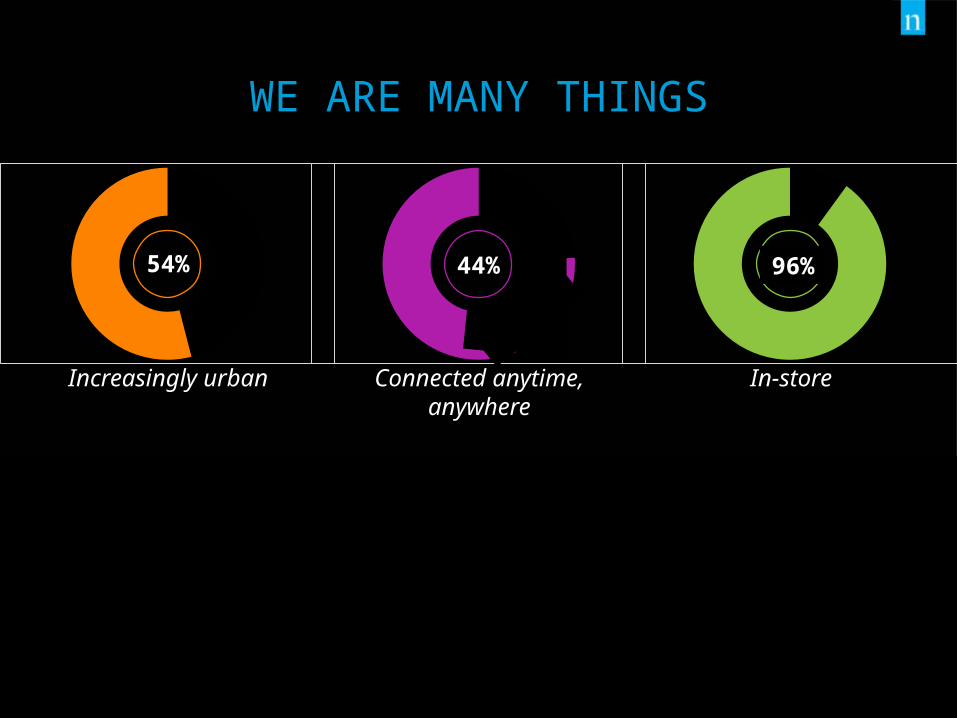

WE ARE MANY THINGS

54% 44% 90%

Increasingly urban Connected anytime,anywhere

In-store

194,000Households access Branded CPG Retail

96%

Copy

right

©20

12 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

6

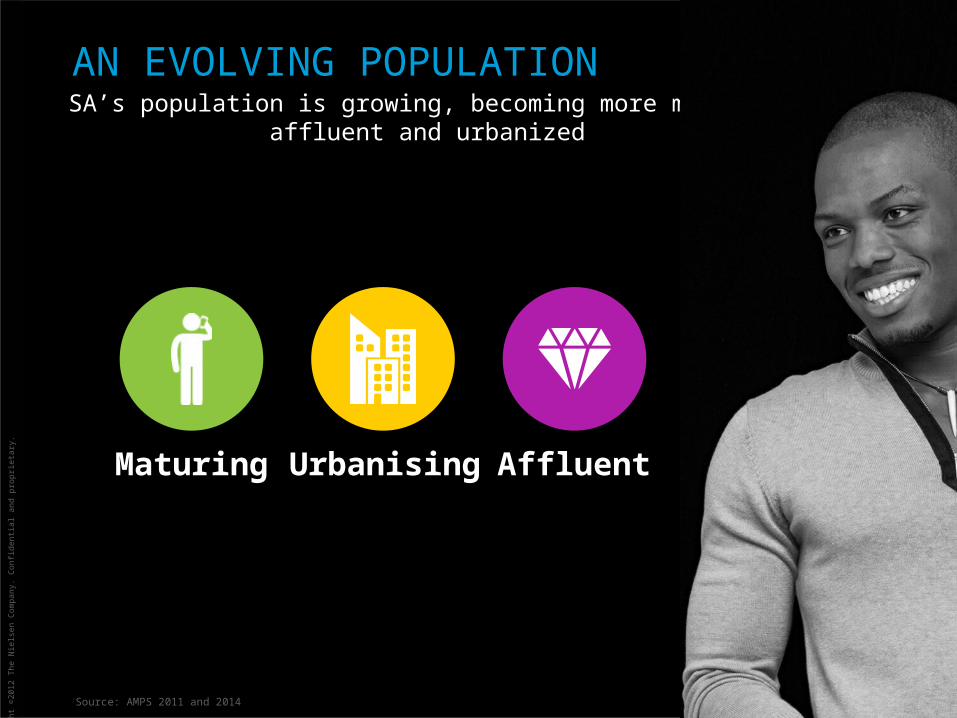

AN EVOLVING POPULATIONSA’s population is growing, becoming more mature,

affluent and urbanized

:Source: AMPS 2011 and 2014

Maturing Urbanising Affluent

CONNECTIVITY IS OUR UNIVERSAL DNA

Online

42%World

Access

2 Billion2015

Influence

73%Global Consumers Trust

Online Comments

Source: internetworldstats.com and Nielsen online Dec 2013

33% Use mobile to shop

CONNECTIVITY DRIVING THE GROWTHIN DIGITAL RETAILING

Over 1,000,000,000global consumers willing to grocery shop online

25% already grocery shopping online

THE DISCERNING SHOPPER

Loyalty

Price sensitive

Promo sensitive

Private Labels

GLOBAL CONSUMER CONFIDENCE REMAINS STABLE

45 78 87 99 101 107 108 120 122 131

IndiaIndonesia

PhilippinesUAE

China

USA

UK

SA

Denmark

South Korea

Global consumer confidence remains very stable, led by APac

LATAM declined 3 points driven by Chile and Brazil

Tier II DevelopingTier I Developing Developed

Copy

right

©20

12 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

11

CLAIMED IMPACT ON PURCHASE BEHAVIORPrice remains the priority

34% (Increased from 25%)

buy in BULK to get lower prices

85% actively look to buy

groceries at the lowest prices

1 in 4 downgrades to

CHEAPER BRANDS

54% cut down on LUXURY

categories

Nielsen Retail Measurement Data; Value in USD Adjusted for Inflation – Latest 12 Month

Europe

8%6%

17%

4%

11%4% 1%

Large SupermarketHypermarketTraditionalConvenienceSmall SupermarketDrugHard DiscounterOtherBarKioskSpecialty

25%

24%

12%

19%

35%

12%

6%

14%

China

33%

4%

LatinAmerica

Africa /Middle East

13%

11%

34%1%

18%

9%

4%

6%5%

1%

42%

4%

6%5%

4% 1%

CHANNEL PREFERENCES ARE REGIONAL

NorthAmerica

41%

32%

20%

7% 1%

North America

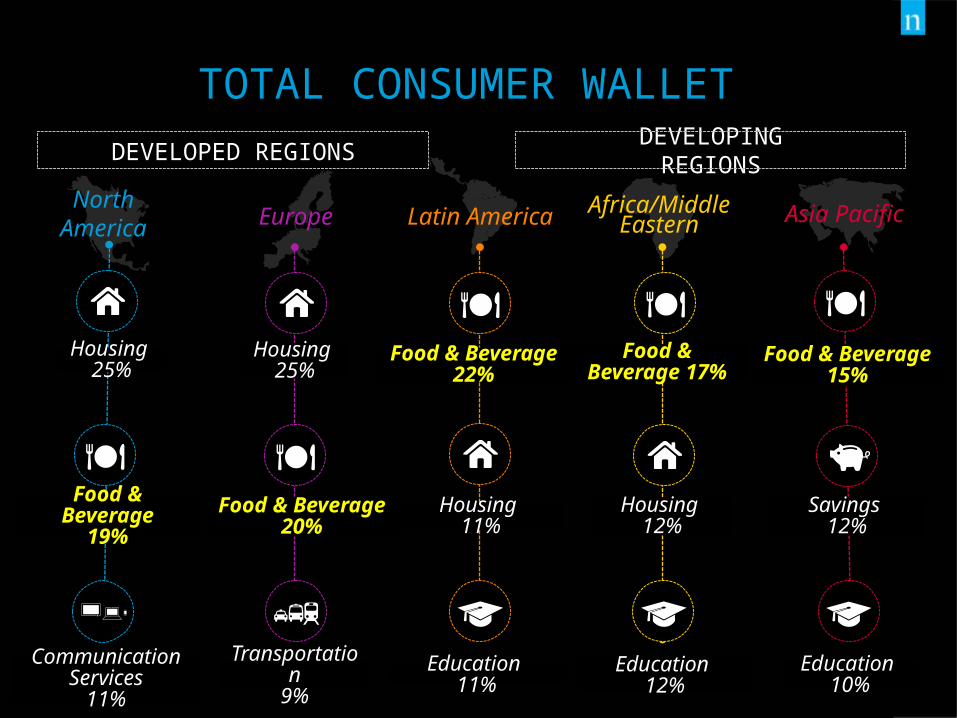

TOTAL CONSUMER WALLET DEVELOPED REGIONS

Housing 25%

Food & Beverage19%

Communication Services

11%

Europe

Housing 25%

Food & Beverage20%

Transportation9%

Latin America Africa/Middle Eastern Asia Pacific

DEVELOPING REGIONS

Housing 11%

Food & Beverage22%

Education 11%

Food & Beverage15%

Education 10%

Savings 12%

Food & Beverage 17%

Housing 12%

Education 12%

Copy

right

©20

13 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

14

Copy

right

©20

12 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

15

NEW SHOPPER AGENDA

:Source: AMPS 2011 and 2014

Different

NOW Wellness

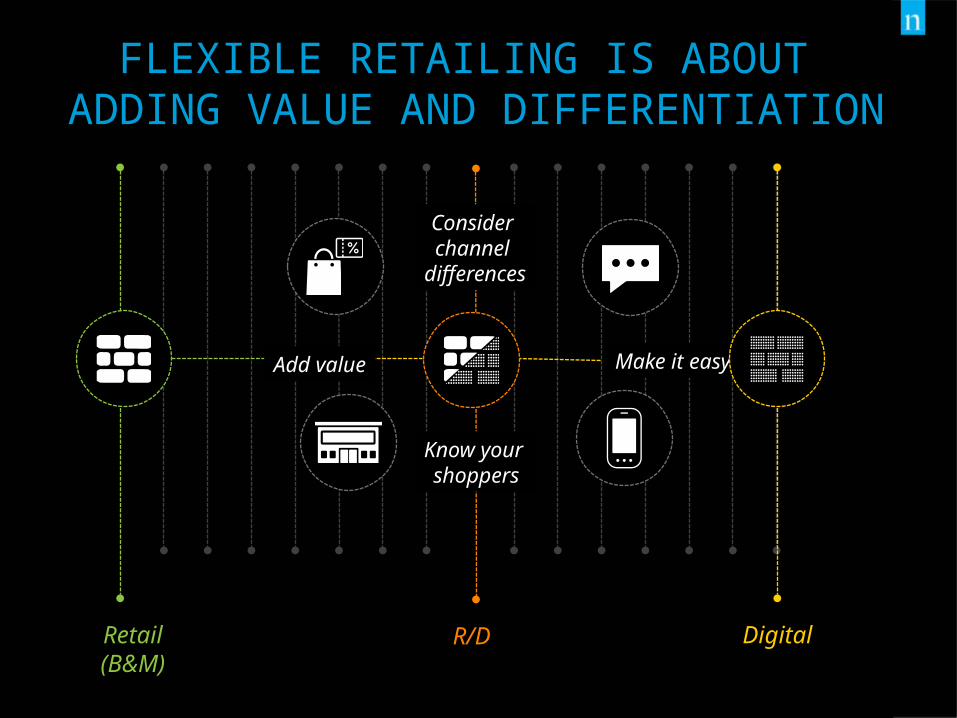

FLEXIBLE RETAILING IS ABOUT ADDING VALUE AND DIFFERENTIATION

Retail (B&M)

Add value Make it easy

Consider channel

differences

Know your shoppers

R/D Digital

THROUGH AN UNDERSTANDING OF WHAT DRIVES CONSUMERS

Retail (B&M) R/D Digital

Catalysts:• 68% Price• 61% Enjoyable• 55% Quality• 46% Convenience • 36% Selection

Catalysts:Anytime, anywhere,Digital touch points

Finding storesMaking lists

Checking pricesResearching

SharingPurchasing

DIFFERENTATION OFTEN PROVIDED BY DIGITAL TOOLS

Hand held barcode scanner

Login to WIFI while in-store to get more

offers

RETAIL + DIGITAL

Use in-store computers to

view extended retailer

ranges online

Scan QR code with mobile

while in-store

Download retailer

app/loyalty program to

phone to receive offers while in-store

Order online and use

drive thru pick-up

Virtual Supermarket

DIGITAL

Order online for delivery

to home

Order online pick-up curb

side

Online automatic

subscription

Order online pick-up in-store

Self check-out

RETAIL

Online ormobile shopping

lists

Online or mobile coupons

Copy

right

©20

12 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

19

90% BELIEVE GOING TO THE GROCERY

STORE IS AN

ENJOYABLE AND ENGAGING

EXPERIENCE

Copy

right

©20

12 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

20

ONLINE OR MOBILE COUPONS (18%) AND MOBILE SHOPPING

LISTS (15%) ARE THE MOST CITED FORMS OF IN-

STORE DIGITAL ENGAGEMENT AMONG GLOBAL RESPONDENTS

Copy

right

©20

12 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

21

&

Copy

right

©20

12 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

22

Winners will find the harmony between R & D

Solutions vs product will create distinction

Format relevance will have to rethink itself

‘Connected’ Shoppers will be the reason you succeed

lines between B&M and Digital will continue to blur

THE RETAIL ROAD AHEAD