Embed Size (px)

Citation preview

Main Office: Maharlika Hi-Way, Banga 1stPlaridel, Bulacan

Manila Office: Level 5, Tower 2, The Enterprise Center, 6766 Ayala Avenue Corner Paseo de Roxas, Makati City Telephone: (044) 670-1492 / 670-0693 / 795-0136 Fax: (044) 795-1979 Website: www.calatacorp.com

16 April 2013 MS. JANET A. ENCARNACION Head, Disclosure Department Philippine Stock Exchange, Philippine Stock Exchange Plaza Ayala Triangle, Ayala Avenue, Makati City

RE: CALATA CORPORATION 2012 ANNUAL REPORT

Dear Ms. Encarnacion, Pursuant to the Revised Disclosure Rules of the Philippine Stock Exchange (the “Exchange”), please find attached Annual Report of Calata Corporation for the year ending 31 December 2012. Very truly yours,

Atty. Jose Marie E. Fabella

Corporate Secretary / Corporate Information Officer / Compliance Officer

1

1 9 9 9 1 1 6 6 6 SEC Registration Number

C A L A T A C O R P O R A T I O N

(Company’s Full Name)

(Business Address: No. Street City/Town/Province)

Benison Paul B. De Torres 044-795-1979

(Contact Person) (Company Telephone Number)

1 2 3 1 1 7 - A Month Day (Form Type) Month Day

(Fiscal Year) (Annual Meeting)

(Secondary License Type, If Applicable)

Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings

Total No. of Stockholders Domestic Foreign

To be accomplished by SEC Personnel concerned

File Number LCU

Document ID Cashier

S T A M P S Remarks: Please use BLACK ink for scanning purposes.

M C A R T H U R H I - W A Y B A N G A 1 S T P L A R I D E L B U L A C A N

2

SECURITIES AND EXCHANGE COMMISSION

SEC FORM 17-A

ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141

OF THE CORPORATION CODE OF THE PHILIPPINES 1. For the fiscal year ended December 31, 2012

2. Commission Identification Number A19991166 3. BIR Tax Identification No. 005- 712-797-000 4. Exact name of issuer as specified in its charter Calata Corporation 5. Province, Country or other jurisdiction of incorporation or organization Philippines 6. Industry Classification Code: (SEC Use Only) .......................................................................................................................................... 7. Address of principal office Postal Code McArthur Highway, Banga 1st, Plaridel, Bulacan 3004 8. Issuer's telephone number, including area code (044) 795 - 0136 9. Former name, former address, and former fiscal year, if changed since last report. Not applicable 10. Securities registered pursuant to Sections 8 and 12 of the SRC, or Sec. 4 and 8 of

the RSA Title of Each Class Number of Shares of Common Stock

Outstanding and Amount of Debt Outstanding

Common Shares 360,112,000 shares 11. Are any or all of these securities listed on a Stock Exchange. Yes [ / ] No [ ]

3

If yes, state the name of such stock exchange and the classes of securities listed therein: Philippine Stock Exchange Common Shares 12. Check whether the issuer: (a) has filed all reports required to be filed by Section 17 of the SRC and SRC Rule

17.1 thereunder or Section 11 of the RSA and RSA Rule 11(a)-1 thereunder, and Sections 26 and 141 of The Corporation Code of the Philippines during the preceding twelve (12) months (or for such shorter period that the registrant was required to file such reports);

Yes [ / ] No [ ] (b) has been subject to such filing requirements for the past ninety (90) days. Yes [ / ] No [ ] 13. State the aggregate market value of the voting stock held by non-affiliates of the

registrant. The aggregate market value shall be computed by reference to the price at which the stock was sold, or the average bid and asked prices of such stock, as of a specified date within sixty (60) days prior to the date of filing. If a determination as to whether a particular person or entity is an affiliate cannot be made without involving unreasonable effort and expense, the aggregate market value of the common stock held by non-affiliates may be calculated on the basis of assumptions reasonable under the circumstances, provided the assumptions are set forth in this Form. (See definition of "affiliate" in “Annex B”).

DOCUMENTS INCORPORATED BY REFERENCE 15. If any of the following documents are incorporated by reference, briefly describe them and identify the part of SEC Form 17-A into which the document is incorporated: (a) Any annual report to security holders; Not Applicable (b) Any information statement filed pursuant to SRC Rule 20; Not Applicable

(c) Any prospectus filed pursuant to SRC Rule 8.1.

4

PART I - BUSINESS AND GENERAL INFORMATION Item 1. Business HISTORY Formerly known as Planters Choice Agro Products, Inc., the Company was incorporated in July 23, 1999. The Company’s initial authorized capital stock of PhP1,000,000.00 divided into 10,000 common shares with a par value of PhP100.00. Combining good business sense with hard work, quality service, and a mission to give back to the community, the store grew into one of the largest agricultural products distribution company in Bulacan. On February 22, 2010, the Company obtained approval from the SEC for the change in its corporate name to Calata Corporation. In August 17, 2011, the SEC approved the Company’s application for increase in its authorized capital stock from PhP1,000,000.00 divided into 10,000 common shares with a par value of PhP100.00 per share to PhP345,400,000.00 divided into 345,400,000 shares with a par value of PhP1.00 per share. Thereafter, in August 25, 2011, the SEC approved a further increase in the Company’s authorized capital stock to PhP845,400,000.00 divided into 845,400,000 shares with a par value of PhP1.00 per share. On February 6, 2012, the Company amended its primary purpose as a prelude to its plans to create a subsidiary to handle its retail business. On March 23, 2012, the Company made history by being the first agricultural company to conduct an initial public offering (IPO) in the Philippine Stock Exchange. Out of the said IPO, the Company was able to raise P242,412,808.76 to support the rapid growth of its current operations as well as the development of its prospective businesses. In the Philippines, the Company carries the distinction of being the leading and most complete distributor for all products available in the agricultural industry. It is the country’s largest combined distributor of agro-chemicals, feeds, fertilizers, veterinary medicines and other agricultural products coming from manufacturers or “business partners,” such as San Miguel Corporation for B-Meg Feeds and veterinary products; Syngenta, Bayer, Jardine, Dupont, Sinochem,, for agro-chemicals;; East West Seeds, Monsanto, Planters Products for agricultural seeds; and Swire, Viking for fertilizers. The Company is an emerging leader in the Philippine Agricultural Industry utilizing effective marketing strategies, strong business partnerships, as well as modern technology to accurately monitor sales and client records. The Company has increased its annual revenues from roughly PhP200 Million in 2003 to more than PhP1.8 Billion in 2010 equivalent to an 800% increase in revenues for the past 7 years of operation. In 2012, the Company recorded its highest profit in the history of its operations.

The Company has identified three (3) operating segments namely, distribution, retail and farming. CURRENT OPERATIONS Distribution: The Company currently distributes the following types of products:

5

1. Animal feeds - The Company has an exclusive distribution agreement with San Miguel Foods Inc.'s BMEG. The areas covered are the whole of Nueva Ecija, almost all of Bulacan, a third of Pampanga, and a third of Pangasinan. The feeds distribution business accounted for about 44% of the Company's total sales for 2012.

2. Fertilizers - The Company distributes almost all brands of fertilizers in the market. The two top grossing are the Swire and Viking brands. The Company distributes fertlizers in Central Luzon mainly in Bulacan, Pampanga, and Nueva Ecija. The Company closely monitors its fertilizer business because of the relatively volatile prices of fertilizers. The fertilizer distribution business accounted for about 34% of total sales in 2012.

3. Agro-chemicals - The Company distributes almost all brands of agro-chemicals in the market. The biggest contributors to the Company are the products from Syngenta Philippines with whom the Company has an exclusive distributorship agreement similar to that with BMEG. The Syngenta agreement covers the entire Central Luzon composed of the provinces of Bulacan, Pampanga, Tarlac, Nueva Ecija, Zambales, and Bataan. The Company's distribution area of Agro chemicals is the widest among all of the product lines. Sales are mainly centered on Central Luzon but also reaches Isabela, Pangasinan, Baguio and Banaue in Northern Luzon as well as Mindoro, Quezon and Bicol in Southern Luzon. The Agro-chemical distribution business accounted for about 21% of total sales in 2012.

4. Seeds, others - This segment business accounted for about 4% of total sales in 2012. Farms: The Company is currently constructing several large scale farms with an estimated total project cost of approximately P500M. The funding is sourced from internally generated funds of the Company and such other bank credit facilities. The following are the projects under construction:

1. Magnolia Broiler Breeder Farm - Total project cost is P112.98M. The project will produce eggs intended to be chicks to be grown as broilers and then sold by Magnolia to fast foods and supermarkets under the Magnolia brand name. The project will produce a total of 9.36M eggs a year.

2. Monterey Hog Breeder Farm - Total project cost is P138.47M.The project will produce piglets to be grown in hog growing farms. The project will have a total of 1,100 Sows producing the piglets. An estimated 26,460 piglets will be produced per year.

3. Magnolia Broiler Growing Farm - Total project cost is P324.86M. The project will have a capacity to grow 450,000 broiler heads at 8 growing cycles a year or a total of 3.60M broiler heads per year.

4. Monterey Hog Growing Farm - Total project cost is P56.80M. The project will have the capacity to grow 3,000 hogs at 3 cycles per year or a total of 9,000 hogs per year.

6

DEVELOPMENTAL ACTIVITIES

PROJECT NAME

LOCATION/S TOTAL PRODUCTION

TOTAL PROJECT COST

AMOUNT ALREADY SPENT

Monterey Hog Breeder

Bgy. Naganacan, Sta. Maria, Isabela

1100 Sows; 26,460 piglets

125,802,920.00

125,313,342.00

Monterey Hog Growing

Bgy. Ula, Tugbok District, Davao City

3,000 Hogs 49,879,461.00

11,522,114.00

Magnolia Broiler Breeder

Bgy. Fuyo, Ilagan, Isabela

9357660 Eggs; 48000 Breeders

55,165,738.00

55,165,738.00

Magnolia Broiler Growing

Bgy. Kinawe, Libona, Bukidnon

150,000 Birds 91,845,097.00

49,840,255.00

Bgy. Matina, Tugbok District, Davao

150,000 Birds 93,601,823.00

12,088,933.00

Bgy. Nangka, libona, Bukidnon

150,000 Birds 103,310,706.65

9,890,575.00

Retail The Company’s retail operation is carried out through Agri Phil Corporation, a wholly-owned subsidiary. Agri Phil Corporation is engaged in retail trade of feeds, agrochemicals, veterinary medicine, fertilizers and seeds. All its retail distribution products are sourced from the Company at wholesale. All sales are made within the Philippines. The retail distribution products are sold through Agri retail stores which are situated in different areas of Luzon. The products sold have been available in the market for several years. Agri Phil Corporation retail stores compete with typical poultry and agrochemical supply stores located within its distribution area.

Currently, the Company, has 116 retail outlets situated in 16 provinces in the Philippines (Region I, II, III and IV-A) as follows:

Regions Provinces No. of Stores

Ilocos Region

Ilocos Norte 7

Ilocos Sur 4 La Union 6 Pangasinan 20

Cagayan Valley

Cagayan 6 Isabela 7

Nueva Vizcaya 3

Central Luzon

Bataan 4 Bulacan 10 Nueva Ecija 13

Pampanga 6

7

Tarlac 6

CALABARZON

Cavite 3 Laguna 8 Batangas 7 Quezon 6

Total Number of Stores 116

Based on its Audited Financial Statement as of December 31, 2012, the Company’s Sales according to its operating segments are as follows:

Distribution Retail Farming

2012 2012 2012

Sales P1,467,475 P738,527 P- Cost of sales (1,276,558) (671,805) - Other operating income 29,218 - - Operating expenses (20,010) (59,122) - Finance income 10,404 98 - Finance costs - - - Provision for income tax (44,858) (2,280) -

Profit (loss) for the year 165,671 5,418 - Interest - - Taxes 44,858 2,280 - Depreciation and amortization 8,901 4,675 -

EBITDA P219,,430 P12,373 P-

Distribution For its Distribution segment, the breakdown of the Company’s sales as reported in the Audited Financial Statements are as follows:

December 31, 2012 % of the total sales Feeds P957,129,439 43.39 Fertilizers 728,468,890 33.02 Chemicals 448,392,575 20.33 Seeds 72,011,003 3.26 TOTAL P2,206,001,907 100.00

DISTRIBUTION PRODUCTS OF CALATA CORPORATION AS OF 31 DECEMBER 2012

FEEDS A. HOGS

FEED TYPE

DESCRIPTION

BRAND

PIGLET BOOSTER This is a supplement or milk replacer if the milk supply of the

B-meg Premium Baby Pig Booster

8

sow is inadequate to feed the piglets, given to piglets from 5 to 20 days of age.

PRE- STARTER

This feed type is given to pigs from 21 to 50 days of age and weighing about 5 to 12 kilograms.

B-meg Premium Hog Pre-Starter Pellet

B-meg Dynamix Hog Pre-Starter Pellet

STARTER Given to pigs weighing about 12 to 25 kilograms and 51 to 80 days of age

B-meg Premium Hog Starter Pellet

B-meg Dynamix Hog Starter Pellet

B-meg Expert Hog Starter Crumble

B-meg Expert Hog Starter Mash

B-meg Jumbo Hog Starter Mash

GROWER

Next given to pigs when they are about 25 to 60 kilograms and 81 to 120 days of age

B-meg Bonanza Hog Grower Pellet

B-meg Dynamix Hog Grower Pellet1

B-meg Dynamix Hog Grower Pellet3

B-meg Expert Hog Grower Pellet / Mash

B-meg Jumbo Hog Grower Mash

B-meg Premium Hog Grower Pellet

FINISHER

Given when pigs reach 60 to 80 kilograms or about 121 to 145 days of age.

B-meg Bonanza Finisher Pellet

B-meg Expert Finisher Pellet

B-meg Premium Finisher Pellet

GESTATION/BREEDER

Feed type given to gilt/sow from 1 to 100 days of conception

B-meg Bonanza Hog Gestating Pellet

B-meg Bonanza Hog Breeder Pellet

B-meg Dynamix Hog Gestating Pellet1

B-meg Dynamix Hog Gestating Pellet2

B-meg Expert Brood Sow Pellet1

B-meg Expert Brood Sow Mash

B-meg Jumbo Hog Brood Sow Mash

9

B-meg Jumbo Hog Gestating Mash

B-meg Premium Hog Gestating Pellet

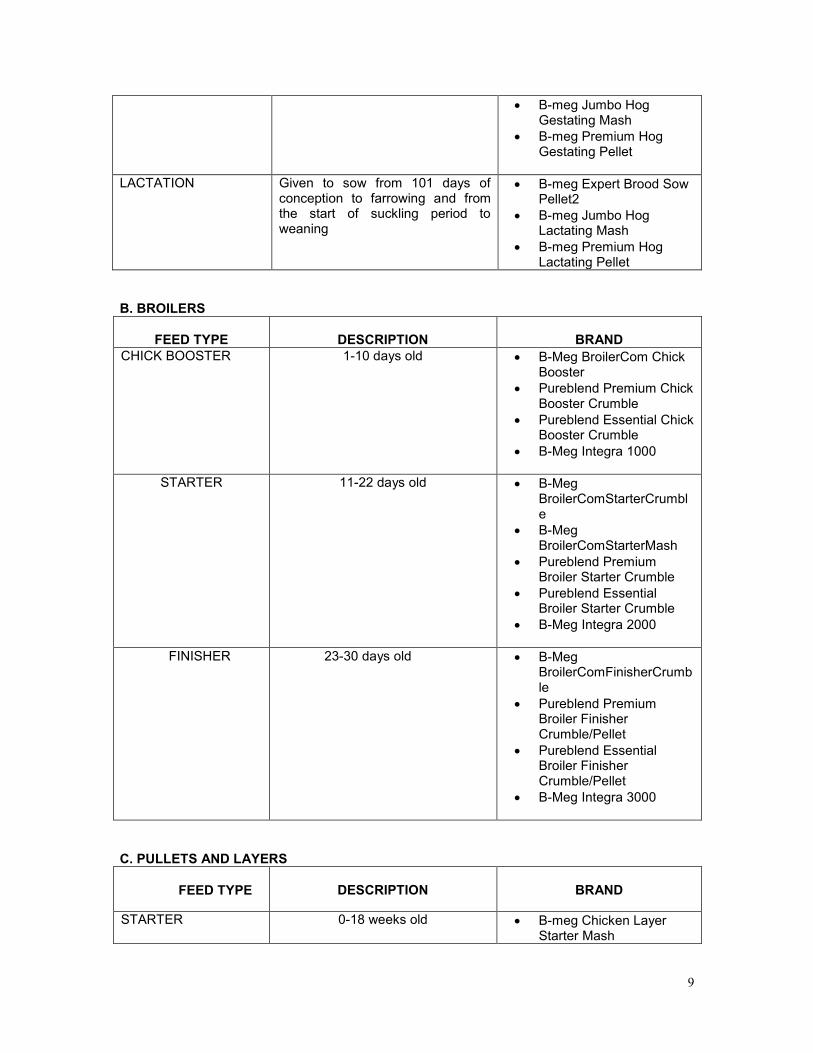

LACTATION

Given to sow from 101 days of conception to farrowing and from the start of suckling period to weaning

B-meg Expert Brood Sow Pellet2

B-meg Jumbo Hog Lactating Mash

B-meg Premium Hog Lactating Pellet

B. BROILERS

FEED TYPE

DESCRIPTION

BRAND

CHICK BOOSTER 1-10 days old B-Meg BroilerCom Chick Booster

Pureblend Premium Chick Booster Crumble

Pureblend Essential Chick Booster Crumble

B-Meg Integra 1000

STARTER 11-22 days old B-Meg BroilerComStarterCrumble

B-Meg BroilerComStarterMash

Pureblend Premium Broiler Starter Crumble

Pureblend Essential Broiler Starter Crumble

B-Meg Integra 2000

FINISHER 23-30 days old B-Meg BroilerComFinisherCrumble

Pureblend Premium Broiler Finisher Crumble/Pellet

Pureblend Essential Broiler Finisher Crumble/Pellet

B-Meg Integra 3000

C. PULLETS AND LAYERS

FEED TYPE

DESCRIPTION

BRAND

STARTER 0-18 weeks old B-meg Chicken Layer Starter Mash

10

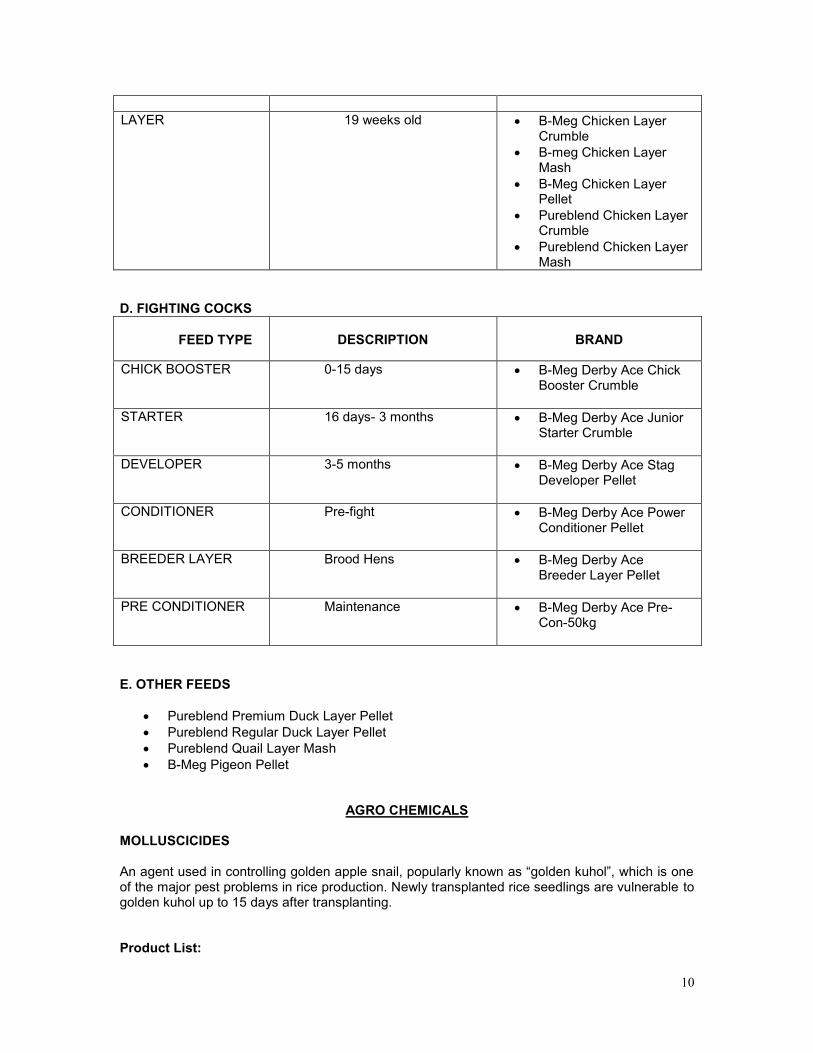

LAYER 19 weeks old B-Meg Chicken Layer

Crumble B-meg Chicken Layer

Mash B-Meg Chicken Layer

Pellet Pureblend Chicken Layer

Crumble Pureblend Chicken Layer

Mash

D. FIGHTING COCKS

FEED TYPE

DESCRIPTION

BRAND

CHICK BOOSTER 0-15 days B-Meg Derby Ace Chick Booster Crumble

STARTER 16 days- 3 months B-Meg Derby Ace Junior Starter Crumble

DEVELOPER 3-5 months B-Meg Derby Ace Stag Developer Pellet

CONDITIONER Pre-fight B-Meg Derby Ace Power Conditioner Pellet

BREEDER LAYER Brood Hens B-Meg Derby Ace Breeder Layer Pellet

PRE CONDITIONER Maintenance B-Meg Derby Ace Pre-Con-50kg

E. OTHER FEEDS

Pureblend Premium Duck Layer Pellet Pureblend Regular Duck Layer Pellet Pureblend Quail Layer Mash B-Meg Pigeon Pellet

AGRO CHEMICALS MOLLUSCICIDES An agent used in controlling golden apple snail, popularly known as “golden kuhol”, which is one of the major pest problems in rice production. Newly transplanted rice seedlings are vulnerable to golden kuhol up to 15 days after transplanting. Product List:

11

Aquadin Kuhol Kill Primalex Sure Bayluscide Maso RiceSaver 25SC Surekill Bayonet Metabait Sakuhol Trap Doblado Niclomax SnailKill Exos Niclos Stop Hit Porsnail SuperKill

HERBICIDES A chemical pesticide designed to control or destroy plants, weeds, or grasses. Herbicides tend to have wide-ranging effects on non-target species (other than those the pesticide is meant to control or kill). Product List: Advance EC Grassedge Rainbow Tornado Round-up Agroxone Grastop 70EC RiceBro Triple 2,4-D Amine Sencor Almix Red Hedonal RiceStar Xtra Vast 2,4-D Ester Sharpshooter Amine 2, 4-D Klick Rogue EC Axle SL160 Slash Advice Londax Ronstar Clear Out Stand-Out Clincher Hedonal Sofit Demolition 16SL Touchdown Devast Machete EC Sonic Gramoxone Weed Blaster (R) Direk 800 Nominee Super 2,4D Ester Lebron 160SL Weedban Ester 24-D Onecide Super Herbicide Massive Exceed Post Herb 10%SC Tiara SC50 Mower EC Gallant Pyanchor 5EC TopShot Power INSECTICIDES A chemical used specifically to kill or control the growth of insects. Farmers spray insecticides like Dichlorovas, Carbofuran, Cypermethrin, Chlorpyrifos and Lambda- Cyhalothrin to insects such as stem borers, sap feeders, defoliators and grain/root feeders. Product List: Actara Cymbush Mesurol SuperLambda 25 EC Agri-Mek 1.8EC Cypex liter + Mighty Crop Nurelle Superquick Alika Dantop Oshin 20SG Tango Applaud Decis 2.5 Padan Tamaron Arnis Dichlorvos Panlaban Top Rank 50SP Ascend Etrofolan Parapest Trebon Attack Extreme Pegasus Trigard Baythroid 050 Fenos Pennant Tsunami Bida Flash Perfecthion Vapona Bigathrin Fuerza Prevathon Vasthrin 5EC Bigboss Furadan ULTRA Pro Axis Vectron 10EW Blizzard 50SP Hercules Provado Supra Victor 20WP Boxer Hopcin Rampage Vindex Boltrin Hytox Rimon Voliam Flexi Breaker 31.5 EC Ingram 50 SP Selecron Wave 2.5EC Brodan Karate EC Sevin Wildkid

12

Bug Buster Lakas 5 EC Siga WokTap Bulldock Lannate Slam! 2.5EC Xentari Bushwack Lanus Smash Zorro Carbomax 3G Larvin Solomon Cardinal Lebaycid Starkle Cartap ES Legend Steward Chess 50- WG Lorsban Sumicidin Chix Magnum Sumithion Confidor Malathion Super Cartap Cruiser 350 FS Marshall 200SC Super Insecticide Cyclone Matador Super Seven FUNGICIDES A fungicide is a chemical pesticide compound that kills or inhibits the growth of fungi1. () In agriculture, fungicide is used to control fungi that threaten to destroy or compromise crops. Product List: Aliette Curzate Goldazim Ridomil Gold Amistar Daconil Ivazeb Score Antracol WP70 Dithane Kocide Sundazim Anvil 5 SC Folicur WP25 Manager Venom Armure Fundazol 50WP. Marthseb 80 WP Vondozeb Armor Fungitox Micron Benomyl Fungufree 80WP Previcur N Benophyl Funguran Revus 250 SC Benostar 50 WP Gardenil Rovral FOLIARS AND GROWTH STIMULANTS Products used to create a synergistic effect to dramatically speed up vegetative growth and increase root mass for a healthier plant and root system. Product List: Agrowell GNSO Hoestick Siam Bloom Anaa-1000ml Golden Mango Set Humus WSG 56.9 Siam Grower Algafer - 1000 GreenBee All Purpose Kasunod Foliar Star Foliar Orange Atonik Stimulant Grobest Maxigrain Star Foliar Yellow Bayfolan Growmax Pink Mega Booster Steady 10 WP Berelex - Tablet Growmax Orange Mega F21 Stimulate Cal-Guard r Haifa Grow MegaBoom Stoller CaB Crop Giant Orange Harvest More - 20-20-20 Nevirol Wokozim Crop Giant Yellow Harvest More 20-5-30 Orgamin Xemas Cultar Harvest More 30-10-10 Peters - 20-20-20 Yield Master 15-15-30 DeltaSpray 20-20-20 Harvest More 5-5-45 Peters - 9-45-15 Zinc Metalate Ethrel 24 X 500ml Harvest More 04-00-48 Peters 15-10-30 X-Rice (X-Factor) FG Power Foliar Harvest More 15-15-30 Peters 30-10-10 Flower Power Harvest Richer Root Feed Fruit Power Hormex Stand

1Definition taken from http://www.wisegeek.com/what-are-fungi.htm

13

RODENTICIDES These are chemical substance used to kill rats, mice, and other rodent pests. Product List: Klerat+Bitrex Racumin Ratkill Zinc Phosphide TERMITICIDE A chemical substance used as an effective form of termite control for residential, commercial, and industrial use. Product List: Biflex Hometrek Leadrex Lentrek Termex

FERTILIZERS

A fertilizer is a substance containing one or more recognized plant nutrients that is used for its plant nutrient content or that is designated for use, or claims to have value, in promoting plant growth. Fertilizers enhance the natural fertility of the soil or replace the chemical elements taken from the soil by previous crops. Recognized plant nutrients include: 1. Primary nutrients

Nitrogen Phosphorous Potassium

2. Secondary nutrients

Calcium Magnesium Sulfur

3. Micronutrients

Boron Manganese Chlorine Molybdenum Cobalt

Sodium Copper Zinc Iron

FERTILIZER GRADES

UREA (46-0-0) Markang Bulaklak 46-0-0 Swire 46-0-0 Universal Harvester 46-0-0 Viking 46-0-0 Sinochem 46-0-0

AMMONIUM SULFATE (21-0-0)

Markang Bulaklak 21-0-0 Sunrise 21-0-0 Swire 21-0-0 Universal Harvester 21-0-0

AMMONIUM PHOSPHATE (16-20-0)

Philphos 16-20-0 Swire 16-20-0 Universal Harvester 16-20-0

POTASH (0-0-60)

Atlas 0-0-60

OTHERS

Atlas 14-14-14 – Zircon Philphos 14-14-14 Swire 14-14-14 – Zircon UH 14-14-14 –Zircon Atlas 17-0-17 50 kgs. Viking 16-16-16 - Zircon Bulaklak 25-0-0

SEEDS Product List: Bitter Gourd Hot Pepper Pumpkin Sweet Pepper Cabbage Pechay Ridge Gourd Tomato Cauliflower Mustaza Patola Watermelon Radish Onion Bottle Gourd Sweet Corn Cucumber Papaya Sitao DK818RRC2/YG Eggplant Carrot Snap Beans DK9132RRC2/YG Glutinous Corn Okra Cow Pea

As of December 31, 2012, the Company does not have income derived from foreign sales nor has it developed a new product.

FEEDS DISTRIBUTION BUSINESS FLOWCHART B-MEG

AGRO CHEMICALS, FERTILIZERS, SEEDS DISTRIBUTION FLOWCHART

FEEDS SMFI, INC.

CALATA

Bulacan Pampanga Pangasinan Nueva Ecija North

Nueva Ecija South

DEALERS

Bulacan Pampanga Pangasinan

Nueva Ecija – North Nueva Ecija – South

AGRI PHIL CORP

INDUSTRY OVERVIEW

The Philippine economy is highly dependent on agriculture. Two thirds of its current population of 75.3 million and three fourths of the poor depend on agriculture for their livelihood. While only a fifth of all the goods and services the country produces and a third of its exports come from the sector, it employs about half of the total workforce. Agriculture and fisheries registered an overall growth rate of 4.01% in 2001,

CHEMICALS SYNGENTA Bayer CB Andrew Asia, Inc. Jardine Distribution, Inc. Leads Agricultural Products Corp Planters Products, Inc Sinochem Crop Protection (Phil), Inc.

FERTILIZERS

Yara International ASA, et al.

OTHERS

MONSANTO PHILIPPINES, INC.

East West Seeds, et al.

CALATA CORPORATION

BULACAN

DEALERS

AGRI PHIL CORPORATION

which was mainly contributed by: crops (2.58%), livestock (2.87%), poultry (7.80%), and fisheries (6.05%). Of the crops, the major contributors were rice (4.56%), coconut (1.69%), and banana (2.66%). In terms of area, about a third of the country's 30 million hectares is agricultural. Traditional and current uses of the agricultural land consist of:

Food crops - 52% (coconut, sugar cane, industrial crops, fruits,

vegetables, root crops) Food grains - 31% (rice and other grain crops) Non-food - 17 per cent (pasture and cut flowers)

Low productivity and low incomes from agriculture and fisheries are consistent with the prevalence of rural poverty. The situation is further aggravated by low farm gate prices of produce and high retail prices of food, which are among the highest in the region.

Location: Southeastern Asia, archipelago between the Philippine Sea and the South China Sea, east of Vietnam

Area: total: 300,000 square kilometers

land: 298,170 square kilometers

water: 1,830 square kilometers

Agricultural land area: 9.560 million hectares (2002 CAF)

arable land: 4.858 million hectares

permanent cropland: 4.193 million hectares

permanent meadows/pastures: 0.129 million hectares

forest land: 0.074 million hectares

other lands: 0.307 million hectares

About 32% of the country's total land area constitutes the agricultural land. Of this, 51% and 44% were arable and permanent croplands, respectively. (Bureau of Agricultural Statistics, 2010)

Agriculture grew by 2.92 percent in 2012. Production in the crops, livestock and poultry subsectors put up a combined growth rate of 3.60 percent. This was pulled down by the fisheries subsector which output dropped by 0.04 percent. Overall, agriculture output grew by 2.92 percent. At current prices, value of agricultural production amounted to P1.4 trillion, higher by 1.17 percent from the 2011 level.

Crop production which accounted for 51.46 percent of total agricultural output increased

by 4.14 percent during the year. The main sources of growth were palay and corn where outputs went up by 8.08 percent and 6.25 percent, respectively. At current prices, the subsector grossed P797.7 billion or 0.80 percent lower from the 2011 earnings.

Livestock production inched up by 1.10 percent. The subsector shared 16.07 percent in

the total agricultural production. Hog production grew by 1.71 percent. Carabao, cattle and goat

recorded lower production during the year. The subsector grossed P214.3 billion at current prices, up by 0.94 percent from last year’s level.

The poultry subsector posted a 4.53 percent increase in output. It accounted for 14.27 percent of the total agricultural production in 2012. Chicken was the main source of growth with its 4.61 percent output increment. Gross value of poultry production amounted to P167.1 billion at current prices. This was higher by 5.24 percent from last year’s record.

On the average, farmgate prices declined by 1.70 percent this year. The crops subsector had an average price reduction of 4.74 percent. Prices in the livestock subsector were down by an average of 0.16 percent. An average price increase of 0.68 percent in the poultry subsector was noted during the year. The fisheries subsector recorded an average price increment of 5.59 percent.

The Company’s Distribution covers Regions I, II, III and IV-A of the Philippines depending on the types of products:

1. Animal feeds - The areas covered are the whole of Nueva Ecija, almost all of Bulacan, a third of Pampanga, and a third of Pangasinan.

2. Fertilizers - The Company distributes fertlizers in Central Luzon mainly in Bulacan, Pampanga, and Nueva Ecija.

3. Agro-chemicals - The Company distributes almost all brands of agro-chemicals in the market. It covers the entire Central Luzon composed of the provinces of Bulacan, Pampanga, Tarlac, Nueva Ecija, Zambales, and Bataan. The Company's distribution area of Agro chemicals is the widest among all of the product lines. Sales are mainly centered on Central Luzon but also reaches Isabela, Pangasinan, Baguio and Banaue in Northern Luzon as well as Mindoro, Quezon and Bicol in Southern Luzon.

4. Seeds, others - Regions I, II, III and IV-A of the Philippines.

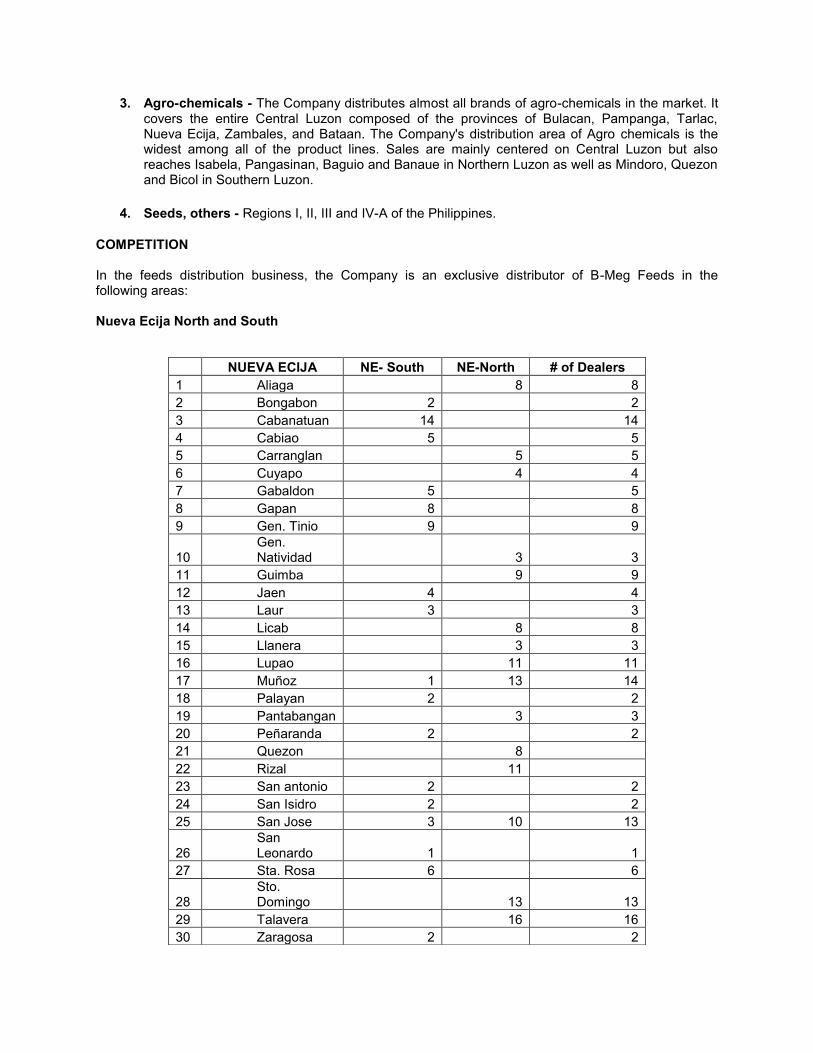

COMPETITION In the feeds distribution business, the Company is an exclusive distributor of B-Meg Feeds in the following areas: Nueva Ecija North and South

NUEVA ECIJA NE- South NE-North # of Dealers 1 Aliaga 8 8 2 Bongabon 2 2 3 Cabanatuan 14 14 4 Cabiao 5 5 5 Carranglan 5 5 6 Cuyapo 4 4 7 Gabaldon 5 5 8 Gapan 8 8 9 Gen. Tinio 9 9

10 Gen. Natividad 3 3

11 Guimba 9 9 12 Jaen 4 4 13 Laur 3 3 14 Licab 8 8 15 Llanera 3 3 16 Lupao 11 11 17 Muñoz 1 13 14 18 Palayan 2 2 19 Pantabangan 3 3 20 Peñaranda 2 2 21 Quezon 8 22 Rizal 11 23 San antonio 2 2 24 San Isidro 2 2 25 San Jose 3 10 13

26 San Leonardo 1 1

27 Sta. Rosa 6 6

28 Sto. Domingo 13 13

29 Talavera 16 16 30 Zaragosa 2 2

Bulacan

BULACAN # of Dealers 1 Angat 16 2 Balagtas 4 3 Bustos 10 4 Bulacan 7 5 Baliuag 36 6 Bocaue 3 7 Calumpit 13 8 Guiguinto 8 9 Hagonoy 10 10 Malolos 10 11 Marilao 4 12 Norzagaray 8 13 Pandi 10 14 Paombong 3 15 Plaridel 19 16 Pulilan 31

17 San Rafael 18

18 Sta. Maria 38

TOTAL 248

TOTAL 71 125 177

East Pangasinan

EAST PANG # of Dealers 1 Asingan 9 2 Alcala 5 3 Balungao 3 4 Bautista 1 5 Bayambang 6 6 Natividan 5 7 Rosales 2 8 San Nicolas 3 9 San Quintin 1

10 Santa Maria 6

11 Santo Tomas 1

12 Tayug 10 13 Umingan 9 14 Villasis 4 TOTAL 65

Pampanga

PAMPANGA # of Dealers

1 Angeles

6 2 Arayat 8 3 Candaba 4 Mabalacat 5 5 Macabebe 6 Magalang 17 7 Masantol 1 8 Mexico 16 9 Minalin 3

10

San Fernando City 7

11 Santa Ana 3

12 Santo Tomas

TOTAL 66 There are at least twenty seven (27) major feed brands competing with B-Meg in the aforementioned areas, namely: Goldmix, Highgrade, Pigrolac, Phimico, Altlas, Robina, Feed Pro, GMP, CJ, I Feeds, Denka, Premijum Valiant, Sunjin, Hover, Purina, Danway, New Hope, Excel, Ace, Global, Vitarich, Amigo, Mulitive, Viking, Monarch, Master Gain and Legend. Based on survey from gathered field data on the sale of feeds, the Company, through the sale of its B-meg Feeds, leads other brands being sold in its respective areas of operations.

Brand Bulacan Nueva Ecija

North Nueva Ecija

South Pampanga Pangasinan

B-MEG 37% 24%-25% 18%-20% 10%-15% 30%-35% Pigrolac 17% 24%-25% 18%-20% 10%-15% 30%-35% Philmico

46%

50%-51% 12% 10%-15%

30%-40% Others (in the aggregate)

50%-52% 55%-70%

TOTAL 100% 100% 100% 100% 100% The Company has aggressive distribution strategies that outstands the other distributors. Calata’s computerized system contains an extensive customer database that is used to identify the buying patterns and needs of each of its customers and to guarantee the implementation of “Next Day Delivery Policy” of the Company. The Company is also engaged in distributing other agricultural products which it has no exclusivity arrangements. In ensuring Calata’s visibility in the market, the Company posts ads in public utility vehicles and public places. The Company also sponsors local government festivities such as fiesta events and improvement of its existing dealers’ stores. The Company has taken initial steps to fortify its market share in the business of feeds, agrochemical, fertilizer and seed distribution through its acquisition of Agri Phil Corporation which currently has 116 retail stores. PLANS FOR 2013 TO 2014 Distribution

1. Animal feeds - The Company will prioritize the strengthening of its existing areas of distribution. For areas outside its distribution the Company will focus on the strategy of penetration by establishing a new chain of Calata Corporation Retail Stores.

2. Fertilizers - The Company plans to be aggressive in the fertilizer business. The Company will closely monitor the price movement of fertilizers in the market and if we deem that the conditions are favorable, we will invest heavily in the business.

3. Agro-chemicals - The Company plans to be more aggressive in the agro-chemical industry compared to last year. Last year the El Nino phenomenon affected the sales of the Company in this segment. The Company plans to take advantage of more supplier deals to take advantage of incentives and lower prices.

4. Seeds, others - The Company plans to increase this business thru increased sales and profit under its retail subsidiary, Agri Phil Corporation.

CALATA CORPORATION SUPPLIERS WITH EXISTING SUPPLY CONTRACTS

SUPPLY CONTRACTS TERM / LENGTH OF

CONTRACT

FEEDS

San Miguel Foods, Inc. (B-Meg Feeds) Annual Renewal

CHEMICALS Annual Renewal

Syngenta

Bayer CropScience

Sinochem Crop Protection (Phil) Inc.

Jardine Distribution, Inc. (Chemical)

Asia Gold Trading

Leads Agricultural Product Corporation

CropChem Corporation(Biostadt Philippines Inc.)

Cropking chemical Inc.

Bongabon Farmers Trading (Sole Proprietor)

Aldiz, Inc.

Planters Products, Incorporated

United Linkage Marketing (Sole Proprietor)

Leads Environmental Health

International Veterinary & Agrochemical Inc.

Vast Agro Solutions, Inc.

JAT Agrifarm Enterprises, Inc.

Integrated Crop Trading Corporation

Pest Master (St. Anne Agro Trading)

C.B. Andrew Asia, Inc. (Pro-Chem Agritech, Inc.)

Samson Agricultural Supply (Sole Proprietor)

Global

Stoller Philippines, Inc

Igpami Mktg., Corp.

Tillermate Enterprises

SRB Commercial (Sole Proprietor)

PHILOR

Marthdave Co., Ltd.

Zagro Corporation

FERTILIZERS

Yara International ASA Annual Renewal

Aurey Wy (Sole Proprietor)

AgroTech Agricultural Products

C & T Poultry and Agricultural Supply (Sole Proprietor)

MVT Fertilizer Traders Company, Inc.

VETERINARIES

San Miguel Foods, Inc. Annual Renewal

Adrem Distribution Specialist, Inc.

JFL Agri-Ventures (Sole Proprietor)

Meditech Veterinaries

SEEDS

Monsanto Philippines, Inc.

East West Seed Company, Inc. Annual Renewal

Jenny Perez (Sole Proprietorship)

Jardine Distribution, Inc. (Seeds)

Pioneer Hi Bred Philippines Incorporated

OTHERS

Progressive Poultry Supply Corp

Tambo (Cracked Corn & Corn Grits) Annual Renewal Randy Rosario (Sprayer & Sprayer Parts)(Sole Proprietor)

SUPPLY AND DISTRIBUTION AGREEMENTS In general, all supply and distribution agreements are renewed on a yearly basis. Renewal may be express when parties opt to execute a written agreement or implied when parties continue to do business dealings with each other such as taking of orders of supplies. Except for its exclusive distribution agreement with San Miguel Foods, Inc. (Feeds), Syngenta Philippines, Inc. (Agro Chemicals) and Monsanto Philippines, Inc. (Seeds), the Company does not usually have duly executed distribution agreements with the rest of its suppliers of agro chemicals, fertilizers and seeds. Furthermore, based on industry practice, actual exclusive distribution agreements are not issued on a yearly basis. In the case of non-exclusive distribution agreements no formal agreement is executed except for some. Instead, certifications are issued to attest that the Company is a distributor of the pertinent supplier products indicating therein exclusivity or non-exclusivity. However, for other non-exclusive suppliers, certifications are not even given since supply of the products continues for so long as the Company places an order. Nevertheless, to substitute the absence of supply and distribution agreements, the Company strictly enforces proper documentation of transactions with suppliers. The Company religiously fills up Purchase Orders which upon acknowledgment by the supplier, a Sales Invoice is issued. Hence, the Purchase Order and the Sales Invoice signifies the contract / agreement between the Company and the supplier.

DEPENDENCE UPON A SINGLE CUSTOMER The Company is not dependent upon a single or a few customers, the loss of any or more of which would have a material adverse effect on the Company. There is no customer that accounts for five percent (5%) or more or the registrant’s sales. As a distributor for a considerable number of towns in several provinces, the sales of the Company are widely distributed per dealer/customer in its area of operation. While it is true that the Company has a retail subsidiary, the Company takes steps to ensure that existing dealer-customers’ sales would not be affected by carefully locating its retail stores to an area which is beyond the reach of its existing dealer-customers. If despite the fact that the location of the Company’s retail store does not encroach upon the area of its existing dealer-customers, the Company feels that said dealer-customer concerned will, in one way or the other be affected, the Company shall provide said dealer-customer additional incentive schemes, rebates and other forms of assistance to ensure that its profit will not be affected.

INTELLECTUAL PROPERTIES

Application for Registration of Trade Mark On, December 29, 2011, the Company was issued a Certificate of Registration for the trade mark “Calata Corporation and Logo” by the Intellectual Property Office of the Philippines with a term of 10 years or until December 29, 2021 subject to renewal. The description of the mark is as follows: “The mark consists of two wave-like lines of different length. The upper wave-like line is the longest of the two lines and is colored blue, while the lower wave-like line is colored red. Below the said waved-like lines is the word “CALATA”, which are all capitalized. Underneath the aforesaid word is the word “CORPORATION”, which are all capitalized but of smaller font size.” The mark shall extend to the following: chemicals used in agriculture (pesticides, fertilizer), agricultural implements, machineries and equipment, agricultural grains, seeds, foodstuffs for animals and accessories, and for business management. GOVERNMENT APPROVALS AND PERMITS The table below lists the Company’s regulatory permits:

GOVERNMENT AGENCY DESCRIPTION EXPIRY DATE

Fertilizer and Pesticide Authority License No. 02-0511-014 to operate as Area Distributor of Agricultural Pesticides

May 16, 2013

Fertilizer and Pesticide Authority License No. 013 to operate as Area Distributor of Fertilizer

May 16, 2013

Bureau of Animal Industry Registration No. D-10-443-Feed Establishment Registration Certificate

July 26, 2013

Fertilizer and Pesticide Authority Warehouse of Fertilizer and agricultural pesticides

May 16, 2013

In addition to the above-mentioned permits, the Company has secured all statutory permits material to its operations. These permits include the Mayor’s Permit, Certificate of Registration with the Bureau of Internal Revenue, Registration with the Social Security System, Philippine Health Insurance Corporation and the Home Mutual Development Fund.

Effect on existing or probable governmental regulations on the business Existing or prospective legislation on government regulation to business enterprises benefit both the business and its customers. Certificates issued by the appropriate government agencies (Bureau of Animal Industry, Fertilizer and Pesticide Authority) signify an imprimatur from government that the business in whose favor the certificates were issued has complied with all necessary requirements to safeguard the buying public without compromising the interest of the business. Likewise, this

certification, among others, becomes a source of credibility to customers, hence, can be used as a yardstick for an acceptable prospect for business transactions. While the Company has exclusive distributorship agreement with its major suppliers, it remains confident that in the highly unlikely event that it is unable to retain its exclusive distribution agreements, its proven credibility and success in the distribution business will be able to create for it alternative business opportunities. RESEARCH AND DEVELOPMENT The Company is engaged in the business of distribution of agro-chemicals, feeds, fertilizers, veterinary medicines and other agricultural products. Product research and development is conducted primarily by its key suppliers and business partners. ENVIRONMENTAL COMPLIANCE CERTIFICATES

PROJECT NAME LOCATION STATUS DATE OF ISSUANCE Monterey Hog Growing Farm

Bgy. Ula, Tugbok District, Davao City

Approved November 8, 2011

Magnolia Broiler Growing Farm

Bgy. Kinawe, Libona, Isabela

Approved December 16, 2011

Bgy. Matina, Tugbok District, Davao

Approved November 8, 2011

Bgy. Nangka, Libona, Bukidnon

Approved November 28, 2011

Monterey Hog Breeder Farm

Bgy. Naganacan, Sta. Maria, Isabela

Approved October 13, 2011

Magnolia Broiler Breeder Farm

Bgy. Fuyo, Ilagan, Isabela

Approved August 3, 2011

Cost and effects of compliance with environmental laws There is no material cost incurred in securing the Environmental Compliance Certificate (ECC) from the Department of Natural Resources (DENR). Compliance with the requirements of the DENR enables the Company to proceed with its projects subject to certain conditions and restrictions provided in said ECC.

EMPLOYEES As of December 31, 2012, the Company has one hundred six (134) employees broken down as follows: President and CEO (1), Chief Financial Officer and Chief Operations Officer (1), 31 managerial and 101 rank and file employees. Provided hereunder is a breakdown of the managerial and rank and file employees: General Manager (1), Treasury Head (1), Collection Head (1), Accounting Head (1), Human Resources Head (1), Purchasing Head (1), Inventory Control Head (1), Warehouse Head (1), Sales Manager – Feeds (1), Sales Manager – Chemicals (1), Logistics Head (1), Special Project Manager (4), MIS Head (1), Sales Coordinator (1), Operations Manager (2), Sales Supervisor (4), Executive Assistant – Makati (1), Executive Assistant – Bulacan (1), Legal (2), CPA (2), Internal Audit Head (1), Project Manager (1), Administrative Staff (3), Accounting Staff (7), Cashier (1), Checker (8), Collection Staff (4), Collector (6), Distributor’s Sales Representative - Bulacan (16), Distributor’s Sales Personnel – Farm Aide Technician (5), Document Controller (1), Driver (21), HR Staff (2), Inventory Audit (7), Inventory Clerk (2),

Maintenance and Mechanic (4), , Messenger – Bulacan (2), Messenger – Makati (2), MIS Assistant (2), Sales and Marketing (6), Security (1), Warehouse Assistant (1). Collective Bargaining Agreements The Company has no collective bargaining agreements with its employees and there are no organized labor organizations in the Company. The Company complies with the minimum compensation and benefits standards pursuant to Philippine law. The Company has not experienced any disruptive labor disputes, strikes or threats of strikes and the Company believes that its relationship with its employees in general is satisfactory.

RISKS RELATING TO THE COMPANY AND ITS BUSINESS The Company’s business may be affected by any program developed or supported by the Department of Agriculture of the Philippines. The Company’s revenue comes primarily from the sale of agricultural products. Any agricultural program that the Department of Agriculture develops for the farmers of the country may affect the Company’s. In the event that the government is unable to effectively implement its programs, this might result in a slowdown of the Company’s business as farmers might not have the required resources to purchase the Company’s products. There is no guarantee that the Philippine government will not change or prioritize programs for agriculture in the coming years. To mitigate this risk, the Company updates itself regularly with the Department of Agriculture’s policies or programs developed for the agricultural product industry. This allows the Company to react quickly to government programs relating to agricultural products. It also enables the Company to plan ahead to meet the Department of Agriculture’s ongoing or future policies or programs. The Company also conducts its own marketing activities to promote the use or consumption of its product. The Company intends to strengthen its marketing efforts nationwide. The Company’s business and operations may be affected by any changes in the preferences or purchasing power of consumers. The Company’s ability to increase or maintain sales is dependent on the public’s continued acceptance of its products. Changes in demographic, social or health proclivity may alter the demand for the Company’s products. Any adverse downturn in the economy of the Philippines may cause consumers to opt for cheaper or more affordable products. Cheaper alternatives are supplied by the government and the private sector, both of which are readily available in the market. To mitigate this risk, the Company, through its comprehensive line of products, provides options and alternatives to its customers, which may attract a loyal following from certain niche markets. Furthermore, the Company participates in the subsidies provided by the national government and passes the savings on to its customers and consumers. The Company may not efficiently execute its strategy to increase sales volume due to the traditional mindset of the Filipino farmer. The Company intends to grow its sales through expansion of related business activities, additional tie-ups, and aggressive marketing strategies. The success of these strategies cannot be guaranteed because farmers in the Philippines are used to traditional methods of agriculture. Thus they may not be susceptible to the innovations the Company’s products may bring. Failure to change the mindset of its target market may hinder the Company’s growth.

To mitigate this risk, the Company employs innovative marketing and sales activities in order to encourage the use and loyalty of customers. The Company provides information campaigns in the form of trainings and seminars. In addition, the Company provides initiatives such as promos, sampling, and boothing. To ensure its continuous growth and strength in sales, the Company intends to hire additional manpower for its sales and marketing team. Details on the Company’s marketing, sales, and distribution may be found in the “Information with Respect to the Company” beginning page Error! Bookmark not defined.. In terms of exclusivity of supplier contracts and their duration, the Company does not have exclusive distribution agreements with most of its suppliers. The distribution agreements are automatically renewed yearly upon the option of both parties and under terms and conditions agreed upon. Except for its exclusive distribution agreement with San Miguel Foods, Inc. (Feeds), Syngenta Philippines, Inc. (Agro Chemicals) and Monsanto Philippines, Inc. (Seeds), the Company does not have exclusive distribution agreements with the rest of its suppliers of agro chemicals, fertilizers and seeds. This means that other suppliers of the company may, without any legal impediment, enter into distribution agreements with other distributors, hence, decrease in one way or the other, supply of distribution products to the Company and consequently decrease in the sales derived from their products. In general, all supply and distribution agreements are renewed on a yearly basis. Renewal may be express when parties opt to execute a written agreement or implied when parties continue to do business dealings with each other such as taking of orders of supplies. The Company does not usually have duly executed distribution agreements with the rest of its suppliers of agro chemicals, fertilizers and seeds. Furthermore, based on industry practice, actual exclusive distribution agreements are not issued on a yearly basis. In the case of non-exclusive distribution agreements, no formal agreement is executed except for some. Instead, certifications are issued to attest that the Company is a distributor of the pertinent supplier products indicating therein exclusivity or non-exclusivity. However, for other non-exclusive suppliers, certifications are not even given since supply of the products continues for so long as the Company places an order. Nevertheless, to substitute the absence of supply and distribution agreements, the Company strictly enforces proper documentation of transactions with suppliers. The Company religiously fills up Purchase Orders which, upon acknowledgment by the supplier, a Sales Invoice is issued. Hence, the Purchase Order and the Sales Invoice signify the contract / agreement between the Company and the supplier. Considering this, the Company strictly complies with its obligation to these suppliers by implementing a strategic marketing strategy and exerting all efforts necessary in meeting targets and delivering mutually agreed upon results from sales to ensure continuity of exclusivity in the distribution of their products. This approach is likewise being implemented for suppliers with whom the Company does not have exclusive distribution agreements with. Compliance with all of the Company’s obligations with suppliers whether grantors of exclusive or non-exclusive distribution agreements shall greatly contribute in ensuring the annual renewal of the agreements with its suppliers. Apart from being a distributor of feeds, agrochemicals, fertilizers and seeds, with the Company venturing into retailing of its distribution products, competition will be expected from existing retailers. However, in order to likewise be competitive, the Company intends to take advantage of the quality of its products, especially those with which it has exclusive distribution agreements as well as its competitive pricing system. The Company likewise plans to provide rebates and incentive schemes for loyal customers of its planned retail stores and establish an effective after sales service system. Regulatory Risk

The Company’s business is subject to regulatory approvals, such as the issuance of permits for distribution and importation licenses. The products sold by the Company, such as, veterinary medicines, agrochemicals, fertilizer, pesticide and feeds must be registered with the proper government agency prior to sale or distribution. The cancellation of their registrations will adversely affect the Company’s business. The Company ensures that it secures all necessary regulatory approvals. Risk of Natural Calamities and Effects of Pestilence The Company’s revenues are highly dependent on the weather conditions in the Philippines. Severe drought or flooding in a certain agricultural region will significantly affect the productivity of the farmer. This will highly affect the demand for fertilizers, pesticides and other agricultural chemicals. Furthermore, the effects of pestilence on agricultural crops can have a significant effect on the demand for the distribution products used in growing them. Crop farmers may be unable to engage in their farming and growing activities since the agricultural land may not be fit for planting. To mitigate this risk related to natural calamities, the Company, in partnership with its key suppliers, would distribute new products manufactured through the use of modern technology to withstand if not totally resist the devastating effects forces of nature bring. The Company likewise distributes other agricultural products which are unaffected by natural calamities such as animal feeds for poultry, hogs and ducks. Lastly, to mitigate the effects of pestilence, apart from the distribution of superior quality agricultural products which can help in strengthening the immunity of plants to any damage caused, the Company designates its farm aid technicians to provide an information campaign to educate farmers on how to combat pestilence through proper farming practices as well as the introduction and proper utilization of modern farming technology. Risk of Outbreak of Animal Diseases The Company’s revenues may be affected by the outbreak of swine and poultry diseases because the demand for animal feeds will decrease. To mitigate this risk the Company in partnership with its key suppliers currently deploys farm assistant technicians in the field to prevent and/or treat the disease. In addition, the Company distributes veterinary medicines that help prevent or treat the disease. Exposure to Liquidity Risk This represents the risk or difficulty in raising funds to meet the Company’s commitment associated with financial obligation and daily cash flow requirement. The Company is exposed to the possibility that adverse exchanges in the business environment and/or its operations would result to substantially higher working capital requirements and the subsequent difficulty in financing additional working capital. The Company addresses liquidity concerns primarily through cash flows from operations and short-term borrowings, if necessary. The Company likewise regularly evaluates other financing instruments to broaden the Company’s range of financing sources. Credit Risk It is the risk that one party to a financial instrument will fail to discharge an obligation and cause the other party to incur a financial loss. In order to minimize exposure to this risk, the receivable balances are monitored on an ongoing basis with the result that the Company’s exposure to impairment is not significant. The Company deals only with creditworthy counterparty duly approved by the Board of Directors.

The Company depends on its competent sales team, the loss of which could adversely affect its business and growth. The Company’s future growth is largely anchored on the continuous expansion of its product distribution. For this, its sales team plays a vital role in the attainment of the Company’s objectives. The Company currently has provided an attractive compensation and incentive scheme to prevent senior members of the sales team from joining competitor firms in the future. The Company’s reputation, business, and financial condition will be affected if the products do not meet customer’s requirements pursuant to the Company’s contracts / business arrangement with customers. The business of the Company is reliant on the quality of the products of its suppliers. Product defects will not only cause product returns but also affect the Company’s reputation as a distributor of quality products. Business dealings with customers of the Company are not accompanied by individualized and comprehensive contracts. The Company’s business practice involves issuances of invoices for orders of customers. Initially, it will appear that the absence of such individual contracts may cause problems with the Company as customers’ complaints will have no parameters and hence without limit. However, because of the confidence and commitment of the Company to satisfy customers, it has shown its willingness to address customers’ concerns. Specifically, in order to mitigate this risk, the Company carefully selects business partners who are established institutions in their field both locally and internationally. In addition, the issued invoices set out specific guidelines of reimbursement and/or product replacement whereby the Company fully reimburses the customer by replacing the defective products. Risk of loss due to returns are not borne by the Company as the costs of replacing these products are borne by the Company’s suppliers. Work Stoppage The Company is in the distribution business and the partial or total stoppage of work will significantly affect its operations. Coordination among employees is vital as each personnel in charge of a respective aspect of the distribution business is given the responsibility to ensure that the function required to be performed is in sync with the overall flow of business operations of the Company. Employee morale is likewise a key to having a dynamic and dependable workforce. The Company recognizes the importance of the workforce and ensures that all their entitlements under the law are given. In addition to that, the Company regularly holds team building activities to re-establish harmonious relationship between management and employees. Furthermore, in order not to hamper operations in the event that an employee is unable to report for work, the Company has adequately trained its employees to temporarily replace vacated responsibilities. Risk of not effectively implementing the business/expansion plan The establishment of at least one hundred (100) retail outlets under a created subsidiary is not a simple undertaking. Careful selection of strategic locations and negotiation of lease terms are important consideration, among others. Selection of trust worthy and efficient employees to operate the retail stores is also an important factor. Should the company fail in these aspects, the expansion plan may prove to be futile as the retail outlets would not be profitable. To mitigate this risk, the Company has appointed highly trained and competent personnel within its workforce to spearhead the establishment of the retail outlets. Furthermore, as supplier to the retail outlets, the Company shall provide any necessary assistance to ensure profitability such as but not

limited to lower mark ups, assistance in training of outlet personnel and assistance in the marketing of the outlet as well as its products. RISKS RELATING TO THE COMPANY’S COMMON SHARES There may be no liquidity in the market for the Offer Shares and the price of the Offer Shares may fall. The Shares listed on the PSE where trading volumes have historically been significantly smaller than on major securities markets in more developed countries and have also been highly volatile. There can be no assurance that an active market for the Offer Shares will develop following the Offer or, if developed, that such market will be sustained. The Offer Price will be determined after taking into consideration a number of factors including, but not limited to, the Company’s prospects, the market prices for shares of comparable companies and prevailing market conditions. The price at which the Shares will trade on the PSE at any point in time after the Offer may vary significantly from the Offer Price. GENERAL RISKS A slowdown in the Philippine economy could adversely affect the Company. Results of operations of the Company have generally been influenced, and will continue to be influenced by the performance of the Philippine economy. Consequently, the Company’s income and results of operations depend, to a significant extent, on the performance of the Philippine economy. The Philippine economy was adversely affected by the 1997 Asian financial crisis which caused a significant depreciation of the Philippine peso, rise in interest rates and downgrading of the Philippine local currency rating and the ratings outlook for the Philippine banking sector. While the Philippine economy has recovered from this crisis and has registered respectable positive economic growth starting 1999, it continues to be at risk from its significant budget deficit, volatile peso exchange rate and relatively weak banking sector. Any deterioration in economic conditions in the Philippines as a result of these or other risk factors, may materially adversely affect the Company’s financial condition and results of operations. There can also be no assurance that the current or future Governments will adopt economic policies conducive to sustaining economic growth. This risk is beyond the control of the Company. Political or social instability could adversely affect the financial results of the Company. The Philippines has from time to time experienced political, social and military instability and no assurance can be given that the future political environment in the Philippines will be stable. Political instability in the Philippines occurred in the late 1980’s when Presidents Ferdinand Marcos and Corazon Aquino held office. In 2000, former President Joseph Estrada resigned from office after allegations of corruption led to impeachment proceedings, mass public protests and withdrawal of support of the military. In February 2006, President Gloria Arroyo issued Proclamation 1017 which declared a state of national emergency in response to reports of an alleged attempted coup d’etat. The state of national emergency was lifted in March 2006. The country has also been subject to sporadic terrorist attacks in the past several years. The Philippine army has been in conflict with the Abu Sayyaf organization, a group alleged to have ties with the Al-Qaeda terrorist network, and identified as being responsible for kidnapping and terrorist activities.

On June 30, 2010, Benigno Aquino III was sworn in as the 15th and current president of the Republic of the Philippines. There is no assurance that the policies under the new administration will either improve or worsen the political and economic situation. Political instability in the Philippines could negatively affect the general economic conditions and operating environment in the Philippines, which could have a material impact on the Company’s business, financial condition and results of operation. This risk is beyond the control of the Company. Item 2. Properties REAL PROPERTIES The Company is currently leasing the following real properties as storage warehouses for its distribution products:

Details of the Lease Agreements Except for the Main Office which is used for administrative purposes, the Lease Agreements principally provide for the use of the specified premises as storage of the Company’s distribution products. Unless, otherwise agreed upon by the parties, all lease agreements are renewed annually upon the mutual consent of both parties and upon similar terms and conditions except for minimal increases in the lease payments on leased premises located in N.E. North Warehouse, Pampanga Warehouse and Pangasinan. The Company is leasing the Main Office, Bulacan Warehouse and N.E. South Warehouse free of rent. The Main Office and Bulacan Warehouse is owned by Avestha Holding Corporation, an affiliate, the stockholders of which are also stockholders in the Company while the N.E. South warehouse is owned by a businesswoman who has very close ties with the Calata family. Meanwhile, operating leases were entered into by the Company with the warehouse owners of N.E. North Warehouse, Pampanga Warehouse and Pangasinan Warehouse whereby the Company is paying an agreed monthly rental for the use of said warehouses.

On August 1, 2012, the Group entered into a lease agreement with KSA Realty Corporation for the lease of its office premises in Makati. The terms of the lease is for three (3) years and is subject to annual escalation rate of ten (10) percent. The lease agreement has a renewal potion. The details of the security deposit and advanced rental on this lease agreement are as follows:

Terms and conditions 2012 2011

Refundable security

deposit

Equivalent to three (3) months’ lease payment and refundable at P1,652,566 P-

DESCRIPTION ADDRESS AREA

Main Office Banga 1st, Plaridel, Bulacan 924 sqm

Warehouse (Bulacan) Banga 1st, Plaridel, Bulacan 5471 sqm

N.E. South Warehouse San Antonio, San Leonardo, Nueva Ecija

500 sqm.

N.E. North Warehouse Sto. Domingo, Nueva Ecija 300 sqm.

Pangasinan Warehouse Carriedo, Tayug, Pangasinan 1,300 sqm.

Pampanga Warehouse Lagundi, Mexico,Pampanga 406 sqm.

the end of the lease term

Advanced rental Equivalent to three (3) months’ lease payment and to be applied on the last three months of the lease term 1,652,566 -

P3,305,132 P-

The refundable security deposit and the advanced rental are recognized in the consolidated statements of financial position under other non-current assets. There were no restrictions imposed by these lease arrangements such as those concerning dividends, additional debt and further leasing. The rent expense charged to operations for the years ended December 31, 2012 and 2011 amounted to P9,888,600 and P1,206,440, respectively. Future minimum annual rentals are as follows:

2012 2011

Not later than one year P11,241,198

P1,206,440 More than one year but not later than five years 16,531,239 - P27,772,437 P1,206,440

The rent expense charged to operations for the years ended December 31, 2012, 2011 and 2010 amounted to P9,888,600, P1,206,440 and P1,229,050 respectively. The Company has likewise acquired real properties free from liens and other encumbrance, for its hog and broiler growing and breeding projects as follows:

PROJECT NAME LOCATION AREA (sq m)

TCT NO.

Monterey Hog Growing Farm

Bgy. Ula, Tugbok District, Davao City

30,114 TCT No. 146-2011014078

Magnolia Broiler Growing Farm

Bgy. Kinawe, Libona, Bukidnon

18,780 TCT No. 81936 6,281 TCT No. 81789

Bgy. Matina, Tugbok District, Davao

25,000 T-146-2011013915 20,000 T-146-2011013914 5,000 T-146-2011014631

Bgy. Nangka, Libona, Bukidnon

30,977 T-81699

Monterey Hog Breeder Farm

Bgy. Naganacan, Sta. Maria, Isabela

67,989 TCT No. 382740

Magnolia Broiler Breeder Farm

Bgy. Fuyo, Ilagan, Isabela

28,865 TCT No. 383241 28,345 TCT No. 383243

TRANSPORTATION EQUIPMENT

As reported in its Audited Financial Statements as of 31 December 2012, the Company owns transportation equipment worth Thirty Eight Million Four Hundred Sixty Eight Two Hundred Eighty Nine Pesos (Php 38,468,289). This is composed of cars, motorcycles and delivery trucks. These transportation vehicles are used by the Company for the official use of its farm aid technicians, sales personnel, delivery personnel and other employees for the purpose of carrying out the business of the Company. Item 3. Legal Proceedings As of the date of this Prospectus, to the best of the Company’s knowledge, there is no material pending legal proceedings to which the Company, its directors, shareholders, related parties or any of its affiliates is a party or of which any of their property is subject. Item 4. Submission of Matters to a Vote of Security Holders There were no matters during the fourth quarter of the fiscal year covered by this report that were submitted to a vote of security holders.

PART II - OPERATIONAL AND FINANCIAL INFORMATION Item 5. Market for Issuer's Common Equity and Related Stockholder Matters Market Information The Company’s common equity is traded on the Philippine Stock Exchange. The following is the summary of the trading prices at the PSE for each of the quarterly period beginning May 2012, which is the listing date of the Company in said exchange.

2012 Q2 Q3 Q4 High 24.00 10.50 7.78 Low 6.66 5.20 3.65

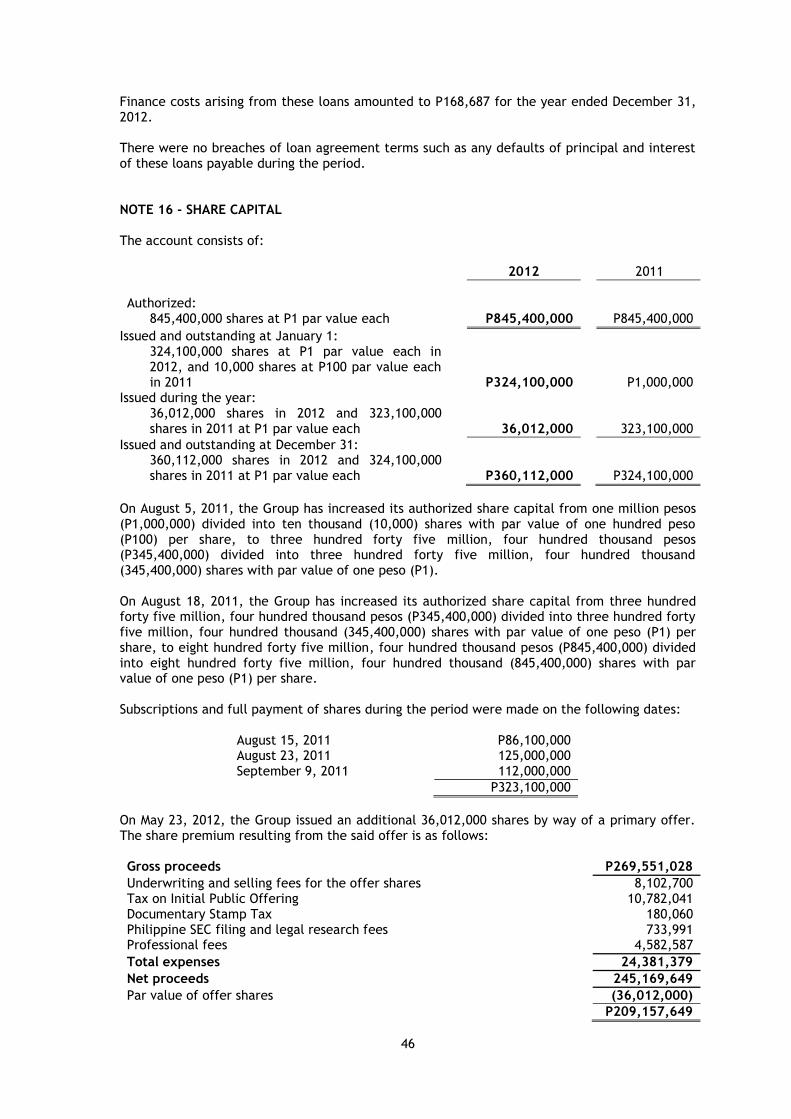

Holders As of December 31, 2012, the Company had five (5) stockholders as per its stock and transfer agent, BDO-UNIBANK, INC. – Transfer Agent. This is because all the shares have been electronically lodged with the PDTC, none of which have been uplifted. The list of shareholders reported by the Stock and Transfer Agent were as follows:

Shareholder No. of Shares Percentage 1 PCD Nominee Corp. (Filipino) 37,080,800 99.158 2 PCD Nominee Corp. (Foreign) 3,030,000 0.841 3 Cesar E. Cruz 1,000 0.000 4 Guillermo F. Gili, Jr. 100 0.000 5 Jose J. Leonardo &/or Teresita A.

Leonardo 100 0.000

360,112,000 100.00 Background of Major Shareholders (1) PHILIPPINE CENTRAL DEPOSITORY, INC. (PCD). Regulated by the Securities and Exchange

Commission (SEC), PCD is owned by major capital market players in the Philippines, namely: Philippine Stock Exchange (31.75%), Bankers Association of the Philippines (31.75%), Financial Executives Institute of the Philippines (10%), Development Bank of the Philippines (10%), Investment House Association of the Philippines (6.5%), Social Security System (5%) and Citibank N.A. (5%).

The PCD Nominee Corporation is a wholly-owned subsidiary of the Philippine Depository and Trust Corporation, Inc. (PDTC) and is the registered owner of the shares in the books of the Registrant’s stock transfer agent. The beneficial owner of such shares entitled to vote the same are PDTC’s participants, who hold the shares either in their own behalf or on behalf of their clients. The following PDTC participants hold more than 5% of the Registrant’s voting securities: a) PCIB Securities, Inc. – 60.50%; b) JAKA Securities Corp. – 11.17% and c) COL Financial Group, Inc. – 8.06%

All PSE- member brokers are Participants of PCD. Other Participants include custodian banks, institutional investors and other corporations or institutions that are active players in the Philippine equities market.

Dividends In a meeting held on November 18, 2011, the BOD unanimously approved the declaration of cash dividends in the amount of Twenty Five Million Pesos (P 25,00,000) to stockholders of record as of November 8, 2011, subject to the condition on the availability of unrestricted retained earnings to cover said dividend declaration. These dividends were paid in 2012 through offsetting of its advances to its shareholders. The dividend per share is Php 0.07. Furthermore, in a meeting held on April 16, 2012 the BOD unanimously approved the declaration of cash dividends equivalent to 25% of the issued and outstanding shares of record as of May 17, 2012, subject to the condition on the availability of unrestricted retained earnings to cover said dividend declaration. Recent Sales of Unregistered or Exempt Securities, Including Recent Issuance of Securities Constituting an Exempt Transaction No recent sales of unregistered or exempt securities, including recent issuance of securities constituting an exempt transaction Stock Option During the Annual Stockholder’s Meeting held on August 31, 2012, the issuance of a Stock Option Plan covering Fifty Million (50,000,000) Common Shares was approved, under such terms and conditions as may be subsequently determined by the Board of Directors. As of the date of this report, said terms and conditions are still being finalized. Securities Subject to Redemption or Call No securities subject to redemption or call exist or are planned.

Warrants No warrant exist are outstanding. Market Information for Securities Other Than Common Equity None Item 6. Management's Discussion and Analysis.

MANAGEMENT’S DISCUSSION & ANALYSIS OF FINANCIAL CONDITION The following management's discussion and analysis of the Company's financial condition and results of operations should be read in conjunction with the Company's audited and unaudited financial statements, including the related notes, contained in this Prospectus. This Prospectus contains forward-looking statements that involve risks and uncertainties. The Company cautions investors that its business and financial performance is subject to substantive risks and uncertainties. The Company's actual results may differ materially from those discussed in the forward-looking statements as a result of various factors, including, without limitation, those set out in "Risk Factors." In evaluating the Company's business, investors should carefully consider all of the information contained in "Risk Factors." Overview The Company saw record-breaking revenues and net income in the year 2012. Both revenues and net income in 2012 were the highest in the Company’s history. Revenues in 2012 amounted to P2.20 Billion compared to P2.00 Billion in 2011. This is an increase of P204.00 Million or 10%. The Company has been recording significant revenue growths and has not been negatively affected by the economic crisis that hit the global economy hard in 2008. In fact the Company recorded the biggest jump in its revenues in 2008 when the global economic crisis was at its strongest. The Company recorded PhP1.61 Billion in revenues in 2008 against PhP1.08 Billion in 2007 or an increase of PhP530 Million or an increase of 33%. RESULTS OF OPERATIONS Audited results for the fiscal year ended December 31, 2012 compared to Audited results for the fiscal year ended December 31, 2012 Sales for the year ended December 2012 amounted to P2.20 Billion which is the highest that the Company has achieved in its history. This represents an increase of P204.00 Million or 10% compared to the 2011 sales. The increase in sales is mainly brought about by the sales contribution of the Company’s wholly owned chain of stores under Agri Phil Corporation. The retail store chain allowed the Company to sell its products on a significantly larger area than it has previously access to. Gross Profit increased by increased by P42.38 Million or 20% compared to 2011. Besides the increase in sales, the gross profit increased because of the increase in margins enjoyed by the Company in its sales direct to end users thru its retail stores. Operating expenses increased significantly. The increase amounted to P48.03 Million or 82%. The increase is mainly due to increased expenses incurred from retail operations, which began its first full year of operations in 2012. The Company aggressively competed for market share for its retail shares thru extensive marketing activities in its area of operations. The operations of the retail stores incurred

large amounts of expenditures most notably salaries due to the large number of the Company’s stores that require a large number of people needed to operate. Other operating income increased by P19.59 Million or 203%. This is mainly due to the P8.21 Million recorded as gain from the purchase of Agri Phil Corporation. The Company also recorded a gain from a liability that was forgiven by an affiliate which amounted to P5.28 Million. Finance income increased by P6.67 Million or 174%. This is mainly due to the P7.97 Million interest from loans receivables recorded in 2011. Finance costs increased by P5.96 Million or 22%. This is mainly due to the increase in loans payable balances mainly to fund the increased operations as well as for the construction of the Company’s farms which resulted in a big increase in the Company’s property and equipment. Audited results for the fiscal year ended December 31, 2011 compared to Audited results for the fiscal year ended December 31, 2010 The year 2011 saw the highest recorded revenues and net income in the Company’s history. The Revenues amounted to P2.00 Billion in 2011 from P1.80 Billion in 2010 or an increase of P203.65 Million or 11%. The net income amounted to P100.17 Million in 2011 from P33.84 Million in 2010 or an increase of P66.34 Million or 196%. The increase in sales is mainly attributed to increased market penetration primarily through the affiliate “AGRI” retail store chain which allowed to Company to sell in markets not previously accessible. The fertilizer business also had a bigger contribution this year compared to the previous years as the Company saw favorable price movements in fertilizer products. The increase in net income is aside from the increased revenues, mainly due to the increase in the Company’s margins. The Company’s gross profit amounted to P227.31 Million and P142.65 Million in 2011 and 2010 respectively, or an increase of P84.66 Million or 59%. The Company’s operating expenses decreased, for 2011 it amounted to P63.30 Million from P67.33 Million in 2010. The decrease amounted to P4.53 Million or 7%. The decrease is mainly due to the Company’s austerity measures which has resulted in decreasing expenses for the past several years. The Company recorded finance income amounting to P3.83 Million in 2011. This is the interest from the loans receivable of the Company. The Company’s finance cost had no significant movement. FINANCIAL POSITION Audited financial position as of December 31, 2012 compared to December 31, 2011 including discussion on Material Changes to the Company’s Audited Balance Sheet as of Fiscal year ended December 31, 2012 compared to Audited Balance Sheet as of Fiscal year ended December 31, 2011 (increase/decrease of 5% or more) Total assets increased by P443.72 Million or 42%. This is mainly due to the increase of P272.68 Million in the Property and equipment of the Company which increased bue to the Construction of the Company’s farming projects. The cash balance also increased by P190.71 Million mainly due to the Company’s Initial Public Offering last year.