Embed Size (px)

Citation preview

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 1/55

PREFACE

The internship program grows the student’s potential and energetic activity to donethe work in better manner. Student can learn more through internship program to

enhance their working abilities to compete the market, to assume responsibilities,

cooperation, team work and hallmarks of modern management.

I got a chance to join the “District Accounts Office” to perform my internship. During

the internship program I learned about its functions, working and objectives and

especially dealing with subscriber which are useful tools for an organizational

structure.

However, during my internship I was to grasp the process, procedures and the basic

functions of the entire office working for the Pakistan professionals to raise the

organizational stricture.

1

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 2/55

ACKNOWLEDGEMENTSFirst of all I want to express all my humble to Allah Ta’la that these are only prayers

and heeds of my Peer Sahb that I reached to this stage and completed my internship

report.

Secondly, I am grateful to my honorable teacher Mr. Saeed Ahmed for providing me

the opportunity of doing internship in District Accounts Office, Bhakkar. I am also

thankful to all the staff of DAO Bhakkar especially both the Assistant Accounts

Officers namely Mr. Mehboob Alam and Mr. Choudhry Sagheer Ahmed for their

cooperation, valuable guidance and support throughout the internship period.

Moreover all other officers and staff members of office deserve thankfulness for their

cooperation and guidance during the course of my internship.

2

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 3/55

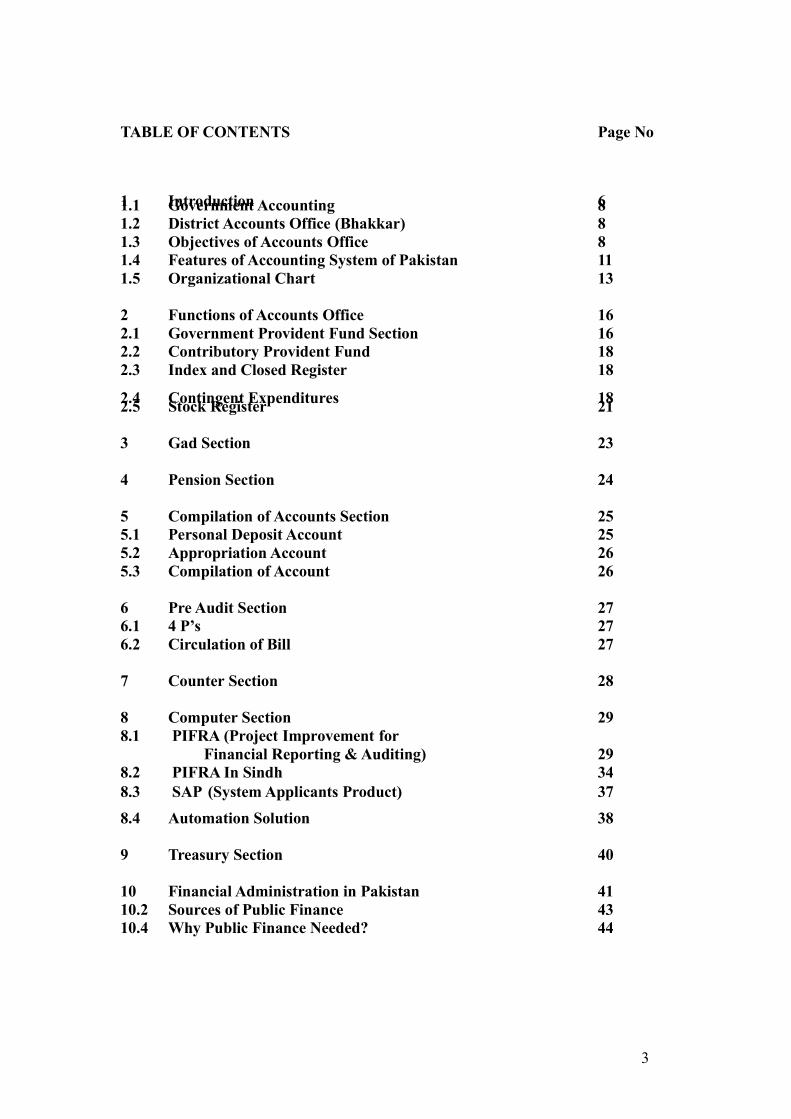

TABLE OF CONTENTS Page No

1 Introduction 61.1 Government Accounting 8

1.2 District Accounts Office (Bhakkar) 8

1.3 Objectives of Accounts Office 8

1.4 Features of Accounting System of Pakistan 11

1.5 Organizational Chart 13

2 Functions of Accounts Office 16

2.1 Government Provident Fund Section 16

2.2 Contributory Provident Fund 18

2.3 Index and Closed Register 18

2.4 Contingent Expenditures 182.5 Stock Register 21

3 Gad Section 23

4 Pension Section 24

5 Compilation of Accounts Section 25

5.1 Personal Deposit Account 25

5.2 Appropriation Account 26

5.3 Compilation of Account 26

6 Pre Audit Section 27

6.1 4 P’s 27

6.2 Circulation of Bill 27

7 Counter Section 28

8 Computer Section 29

8.1 PIFRA (Project Improvement for

Financial Reporting & Auditing) 29

8.2 PIFRA In Sindh 34

8.3 SAP (System Applicants Product) 37

8.4 Automation Solution 38

9 Treasury Section 40

10 Financial Administration in Pakistan 41

10.2 Sources of Public Finance 43

10.4 Why Public Finance Needed? 44

3

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 4/55

11 Role of Pakistan Audit & Accounts Department 47

11.1 Pakistan Audit & Accounts Department 47

11.2 Reasons for Keeping Huge Record 48

11.3 Purpose of Audit & Accounts Department 51

12 Functions & Powers of Auditor General of Pakistan 53

4

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 5/55

DEDICATION

I dedicate all my efforts to my venerable & Honorable

Sheikh E Tareqat Ustad-Ul-Hufaaz Faqeer Ahmed Yar Sarsi

Damat Brakat uhu mul Alia

5

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 6/55

Chapter 1

DISTRICT ACCOUNTS OFFICE

Introduction

Prior to 1970, only Audit and Accounts office which is called Accountant

General Office was functioning at provincial level. The claim pertaining to office,

civil employees serving in district were sent to that office which take much time in

disposal only treasury function was performed in each district. Only monthly pay of

civil employees was admitted by the treasury in a district. That pay was further post

audited in AG’s office.

Payment of Government Provident Fund final settlement, pension payment,

loan & advances and payment of Gazetted government servants were made and when

payment authorities were issued by the AG’s office and received in treasury. The civil

employees were facing hardship and they had to pay many visits in AG’s office at

provincial headquarter to get their claim stalled.

They government of Pakistan felt these hardships of the civil employees of

district as well as work load in AG’s office and accordingly the government

introduced the District Accounts Office scheme in each district in Pakistan to save the

employees from hardships in settlement of their financial problems as well as to

streamline the Accounts of Provincial government.

That was the reason; the government introduced the district accounts office

scheme under a technical term “E-Modernization and Mechanization of system of

Accounts in Pakistan.” In June, 1969 some district accounts offices were established

in Baluchistan and NWFP and thereafter on success of these offices, more accounts

offices were opened in all the provinces of Pakistan.

In 1970, the scheme was established fully at all district levels. Since these

offices were meant for the early solution of financial problem of the civil servant of

provincial governments therefore the expenditure on this scheme is being borne by the

6

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 7/55

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 8/55

Government Accounting:

Government of every country has to perform variety of functions. It

has to defend the country from foreign aggression, maintain Law and Order in thecountry provide educational and health facilities to the people and also to finance

several development projects. All these objectives require heavy expenditure. Those

are met by imposing taxes on the people of country. It is the duty of executive

government to maintain a record of all its income and expenditure. This recording of

government receipts and expenditures is called government accounting. These are

done by Accounts Offices which are located at all the four provinces of Pakistan

called District Accounts Offices.

District Accounts Office (Bhakkar)

It is situated near district courts Bhakkar city. Where did my

Internship. It is the place where accounts of government employees, government

receipts and payments or expenditures are maintained. District Accounts offices from

all over the country collect and compile the data about government employees,

government receipts and payments. These offices are controlled by the District

Accounts Officer which is the head of these offices. Assistant Accounts officer (AAO)

assists him. Assistant Accounts Officer is assisted by the Senior Auditors and Junior

Auditors.

District accounts offices makes closings of accounts on yearly, half yearly and

on monthly basis. Financial year starts from 30 June and ends on 1 July. I saw the

yearly closings during my Internship. This was very busy period for both accounts

office staff and the other government employees of various government departmentswho are concerned with it.

OBJECTIVES OF ACCOUNTS OFFICE

Following are the main objectives of district accounts offices. Those are

discussed below.

(I) Provide Basic Data for Budgeting

A budget is a proposed work programmed, with estimates of the funds

8

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 9/55

necessary to execute it. A work programmed is a plan. The process of preparing

estimates and organizing them into a coherent agency budget necessarily involves

planning. The budget may, therefore, be said to represent a plan or a considerablenumber of plans in different areas of public functions.

The treasury officers/district accounts officers and departmental officers

render accounts of their transactions monthly to their respective accounts offices. The

accounts relating to Defense, Railways and other departmentalized accounts are

compiled by the departments themselves and submitted monthly to the Accountant-

General Pakistan Revenues for amalgamation in the monthly Civil Account of the

Federal Government. From these monthly accounts the annual accounts, i.e. the

Finance and Appropriation Accounts of the Federal and Provincial Governments are

prepared.

The Appropriation Account of Defense, Railways & other departmentalized

accounts are prepared by the concerned departments/ministries and submitted to the

Auditor-General for certification and onward submission to the Government. The

annual accounts of the Federal and Provincial Governments are consolidated in the

Combined Finance & Revenue Accounts (i.e., General Financial Statement). This is

prepared from the audited Finance Accounts of the Federal and Provincial

Governments.

(ii) Provide Basic Data for Policy Making

As DAO’s helps in preparing budget for financial year they also provide

help in policy making of the executive government. On basis of provided facts and

figures the government decides what is needed to government organizations or

departments and what areas are left for preference and what steps should be taken to

improve those areas in the next budget. Due to the budget is a plan itself. Although

plan is another operation but budget gives base to plan. For example, if a government

gives 9 Billion to education sector or department and the next year the facts and

figures provided, states that some areas of technical education was remained

undeveloped therefore more financial support would be required to fulfill such

9

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 10/55

requirement then it would be consulted and government would decide to remove such

deficiency in the fore coming budget.

(iii) Establishment of Government Financial Propriety

Government wants that DAO’s should use government property i.e.

pubic finance as they are the owner of it. This means as they try to use their

money with protection and proper management and not to misuse of their money.

Moreover they want to invest their money in those areas where from they can get

more benefits rather investing in wrong areas. Such qualities government expects

from DAO’s. Public finance is that which is given to DAO's in order to fulfill the

individual requirement other than eating, drinking and clothing, etc. Such as

protection of life, construction of roads, railways, bridges and irrigation canals

and establishment of hospitals, universities and ordinance factories, etc. These are

those requirements of individuals which cannot be bear by the individuals

themselves, therefore the state done it by providing Public Finance by means of

raising revenues and then incurring expenditure to district Accounts

offices.

(iv) Treasury functions

Governments need to ensure both efficient implementation of their

budgets and good management of their financial resources. Spending agencies

must be provided with the funds needed to implement the budget in a timely

manner, and the cost of government borrowing must be minimized. Sound

management of financial Assets and Liabilities are also required. Financial

management within the government includes various activities: formulation of

fiscal policy; budget preparation; budget execution; management of financial

operations; accounting; and auditing and evaluation. Within this broad financial

management function, the Treasury function is to achieve the set of specific

objectives mentioned above. It covers the following activities:

1. Cash management;

2. Management of government bank accounts;

3. Financial planning and forecasting of cash flows;

10

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 11/55

4. Public debt management;

5. Administration of foreign grants and counterpart funds frominternational aid;

6. Financial assets management

Accountant General is the head of a District Accounts Office, who keep the accounts

of the Federal Government and when used in relation to treasury, the head of DAO to

whom the accounts of treasury are rendered.

FEATURES OF ACCOUNTING SYSTEM OF PAKISTAN:Accounting system of Pakistan has several features discussed as under.

(I) Cash Book:

Accounting system of Pakistan is based on actual receipts and

payments of cash and not on the basis of accruals of right and obligations. This

book is maintained at District Accounts Office.

(II) Single Entry System:

Accounting transactions are recorded on single entry system. Now

Government developing its system to New Accounting Model and doing

double entry system with help of computer software SAP. Now accounting

transactions are recording on double entry system.

(III) Basic Accounting Unit:

DAO’s of civil Government are the basic accounting units in Pakistan.

These offices perform the dual function of maintaining the accounts and

auditing. Therefore DAO’s are consisting of Audit staff under the AGP

(Auditor General of Pakistan) and Account staff under the Control of Finance

Department of provincial Government.

(IV) Closing the Accounts:

Formally accounts of the Government of Pakistan are closed annually

or at the end of each financial year. But DAO’s closed its accounts on half

yearly and monthly basis which helps the DAO’s to constitute annually

closing. Government financial year starts from 1st July and ends on 30th June

11

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 12/55

every year.

(V) Compilation and Consolidation of Accounts:

After the basic accounting units have put together the figures of

Expenditures and receipts etc. In different heads of accounts these are sent to

the accounts and audit department for compilation. After compilation of

accounts these are sent to executive government.

(VI) Centralization of Accounts:

The government accounts of Pakistan are centralized in the sense that

while the receipts are made by the administrative departments. The need to

remove this anomaly has been felt and duty of maintaining the initial and

intermediate accounts is being entrusted to the department concerned. So far

this process has been completed in respect of Defense, Pwd, Foreign affairs,

Railways, Forest, National savings, Post office, Telephones and Telegraphs

etc. Same process prevails in other departments and is under review and study.

(VII) New Accounting Model

NAM has been adopted as the accounting model for Pakistan.

Recording of commitments, fixed assets and certain Assets and Liabilities are

the aspects and features of NAM.

(I) Commitments

Recording of commitments did not have an immediate impact on the

cash position but do have effect on the budget availability.

(ii) Fixed Assets

NAM introduces recording of Fixed Assets which would help ineffective maintenance and monitoring. The availability of a list of Fixed Assets

and their value would greatly help in assigning responsibility for the care and

maintenance of accounts.

(iii) Certain Assets & Liabilities

The recording of certain Assets and Liabilities as part of modified cash

basis of accounting will help in providing useful information for decision

making and for disclosure in the financial statements. The difference

12

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 13/55

should be noted that using the cash basis of accounting or previous system

of accounting helps in controlling the cash against budget amounts and

allows only the statement of receipts & payments to be generated. TheModified Cash Basis of accounting or NAM on the other hand helps in

controlling not only cash but also commitments against budget allowing

the production of statement of Assets and Liabilities and a cash flow

statement.

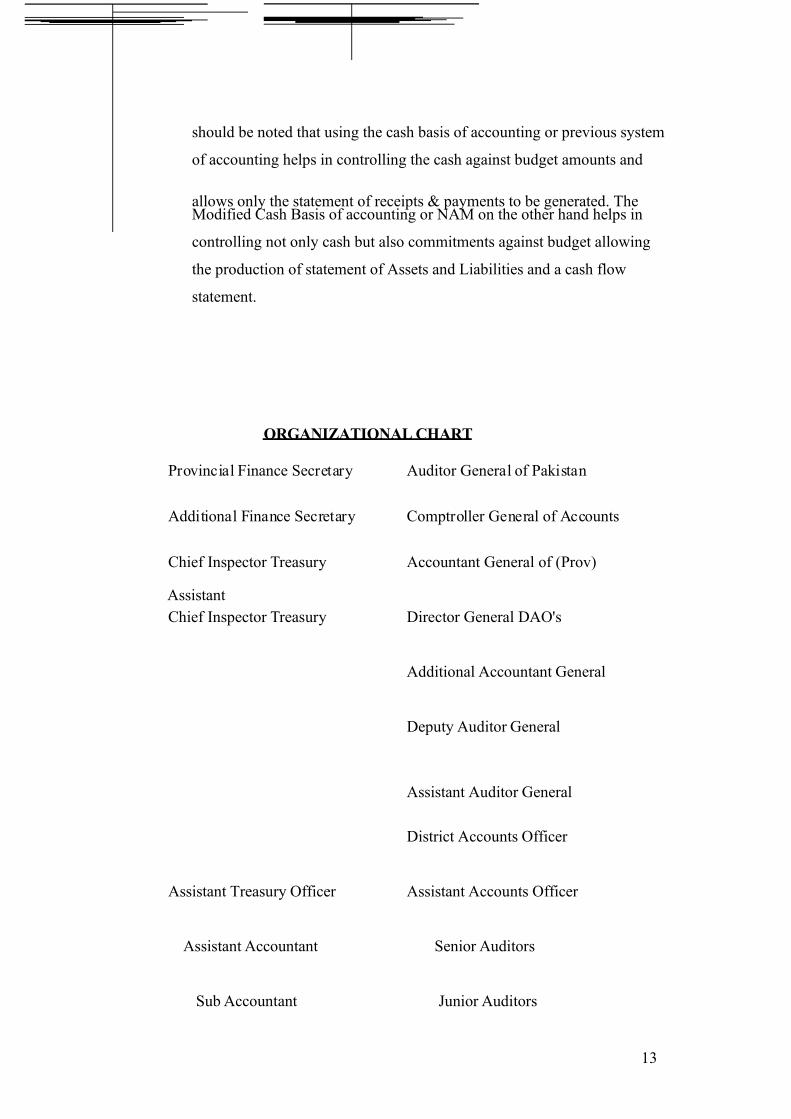

ORGANIZATIONAL CHART

Provincial Finance Secretary Auditor General of Pakistan

Additional Finance Secretary Comptroller General of Accounts

Chief Inspector Treasury Accountant General of (Prov)

Assistant

Chief Inspector Treasury Director General DAO's

Additional Accountant General

Deputy Auditor General

Assistant Auditor General

District Accounts Officer

Assistant Treasury Officer Assistant Accounts Officer

Assistant Accountant Senior Auditors

Sub Accountant Junior Auditors

13

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 14/55

Overview of Administrative Arrangements:

This section provides an overview of how the Government of Pakistan isorganized administratively to record, compile and reporting financial information.

1. Auditor General:

The Auditor General’s role and powers are established in the constitution of

Pakistan 1973 (Articles 168 to 171) and defined further in Pakistan (Audit and

Accounts) Order 1973. While retaining overall responsibility for the accounts of the

Federation and Provinces, this responsibility is delegated to the Comptroller or

controller-General, in order to maintain independence between the audit function and

the accounting function.

2. Controller-General or Comptroller-General:

The Controller-General is responsible for matters of accounting policy and

procedure in relation to the accounts of the Federation and Provinces, as delegated by

the Auditor-General. The Controller-General is responsible for the overall operations

of the accounting offices within Pakistan Audit department and for the production of

timely financial reports of the Government and its accounting entities. Controller-

General is now called Comptroller-General due to the computerized accounting

system.

3. Accountant Generals:

The Accountant Generals are established in each Province and the Federal

government, and each report to the Controller-General. These officers are responsible

for the overall operations of accounting offices within their jurisdiction (e.g. a

Province), and deal with matters of accounting policy and procedure in those areas. In

case of Federal Government the AGPR (Accountant General Pakistan

Revenues) is located in Islamabad with Sub-Office in each of the Provincial capitals

and other designated areas. All AGPR Sub-Offices (Now referred to as Deputy

General Pakistan Revenues), report monthly accounting information, in respect of

Federal transactions to AGPR Islamabad. As well as performing a consolidation

14

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 15/55

function, each AG Office and the AGPR have their own accounting offices for

processing accounting transactions arising within the locality of their office.

4. District Accounts Officer:

Each Province is further divided into districts. Each district contains its own

District Accounts Office. The DAO’s are responsible for processing all accounting

transactions from the various departments in that district. The DAO’s maintains

records of payment and receipts for Federal and Provincial transactions (In separate

ledgers) and submit consolidated monthly accounts to the respective AGPR sub-office

or AG office. In Bhakkar DAO’s branch Mr. Tasawur Ali is District Accounts Officer.

5. Assistant Accounts Officer:

Accounts officer works under the District Accounts Officer. In Bhakkar DAO

branch Mr. Choudhry Sagheer Ahmed is Assistant Accounts Officer. Senior and Junior

auditors work under his command. Or he deals with them. Assistant Accounts Officer

and Assistant Treasury Officer both are the subordinates of District Accounts Officer.

AAO is the federal employer and his head is the Auditor General. Where as Assistant

Treasury Officer is the Provincial Government employer. His head is Accountant

General of Province. There are five Accountant Generals in Pakistan. These all are

responsible to transfer complete reports to Auditor General of Pakistan. And Auditor

General is answerable and responsible to President of Pakistan. He also deals with

trainees. For instance, NIP trainees and as I went there for my 6 to 8 weeks MBA

internship program.

15

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 16/55

Chapter 2

FUNCTIONS OF ACCOUNTS OFFICE

The district accounts offices in Pakistan are mini Accountant General’s Offices

in each district. These offices perform same function at district level as performs by

the Accountant General’s Office at provincial headquarter. The claims of G.P funds,

pay and allowances, loans, advances, pension and refund of revenue are pre-audited

for payment to civil employees posted at district.

The account of federal/provincial government are compiled at district level

and monthly account after consolidation is submitted to the accountant general’s

office at provincial headquarter for merge in provincial account. Various functions of

accounts office are categorized and divided or converted into different sections due to

huge amount of work. These sections are discussed chapter wise one by one below.

Government Provident Fund Section

The district accounts officer is responsible to maintain Government Provident

Fund accounts of civil employees of his district like a banker. G.P Fund is a

compulsory saving scheme for the benefit of civil employees. A monthly deduction at

fixed rate, pay scale wise is made on this account form on the basis of salaries of

employees. These monthly deductions are maintained in the individual ledger account

in district account office. The total accumulation along with interest accrued thereon

is paid to employee on his retirement from service.

G.P Fund Advance

During the service an employee ca take advance from his G.P Fund account

for some immediate reason i.e. on prolonged illnesses; repair of house and for

other obligatory expenses. These advances are refundable by the civil

employee and accounted for in his ledger account. A civil employee can take

three times 80% non refundable advances during

16

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 17/55

his entire service on reaching the age of 45years, 50 years and 55 years.

These advances are treated part of final payment of his G.P Fund account. The

district accounts officer is responsible to maintain accurate accounts in ledger account

of subscriber. Deductions made from pay bills are regularly posted in ledger account

by the concerned auditor posted in G.P Fund section under the supervision of assistant

account officer. A Subscriber is a person who desires an advance out of his G.P Fund.

Accounts officer, the head of accounts office is a person who sanctions such

advancer in his favor if admissible to him. A bill on proper form is prepared by the

department. The bill along with sanction letter is deposed at pre audit counter of

district accounts office. The counter section issues a token to the department in like of

claim. And sends claim in G.P Fund section. This sanction passes bill in ledger

account of the subscriber and record a payment order on it. The D.A.O signs this

payment order. D.A.O and special seal is embossed know.

This passed bill is sent to the counter section and hater record payment order

No on it as well as in advice sheet. It is then delivered to department and token is

received back.

G.P Fund Balance Sheet

The district accounts officer is required to issue a G.P Fund balance sheet

in each year after closing of yearly account showing G.P Fund balance up to 30th June

each year and interest earned by the subscriber. This balance sheet is for the

satisfaction of a subscriber.

G.P Fund Final payment

On retirement of a subscriber his G.P Fund final payment case is prepared by

the department and sent to the district accounts office for final settlement of his

account. The district accounts officer after the rough verification of his account issues

a G.P Fund final payment authority in his favor. On the basis of that authority the

17

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 18/55

department sends claim and it is passed by the recording pay order as per procedure

mentioned above.

C.P (Contributory Provident) Fund

Now a day’s contract employment system is applied in Pakistan. So

Contributory Provident (C.P) Fund is deducted from the pays of employees. There is

no pension for the contract employees. In budget announcement 2008-09 the

government did permanent all the contract employees but there is no a correct

decision about their CPF/GPF deduction because GPF deduction is compulsory on

permanent employees. CPF is started in 1935 in NWFP in 1970.

Index and closed Register

Every employ have its own GP Fund number. GP Fund start from Index

register in which the name of employee, father name, CNIC No. Job code and

department is mentioned. In GP Fund nomination is necessary in case of death of

employee. The nominator can draw the GP Fund after the death of employee. When

employee goes on retirement his account is closed in closed register.

CONTINGENT EXPENDITURES

The term contingent expenditure or contingent charges mean the amount spent

for management of an office or an accounts office. E.g. the payments of office rent,

purchase of consumable and permanent stores, payment of expenses for heating,

lighting, water, repair etc.

The contingent charges may be divided into following kinds.

i) Contract Contingent Charges

These are the expenditures for which a lump sum amount is placed

annually at the disposal of the drawing officer. The drawing officer can

utilize this amount for the special purpose without any prior approval

of the higher authorities.

ii) Self Regulated Contingencies

These include the contingent charges as may be regulated by scale

18

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 19/55

limits and drawn by the competent authority.

iii) Special ContingenciesThese include such contingent charges (recurring or non-recurring)

which can not be incurred without the prior approval of the competent authority.

iv) Fully Vouched Contingencies

It comprises of the contingencies requires no special sanction or

countersignature of the higher authorities but may be incurred by the

head of office.

RULES REGARDING THE INCURRING THE CONTINGENT EXPENSES

The drawing and distribution officer should follow the following rules

while incurring the contingent expenditures.

1. He should exercise such vigilance in respect of contingent charges as a

man of ordinary prudence would do in his own case, while spending

money.

2. The drawing Officer must see that the rules governing to a particular type

of contingent expenditure are fulfilled.

3. He should draw amounts from the treasury, which is required for

immediate disbursements or has already been paid from the permanent

advance.

4. The drawing officer must see that the expenditures are necessary for

efficient running of the office.

5. The calculation of the vouchers and bill should be checked carefully.

PROCEDURE TO INCUR THE CONTINGENT EXPENDITURES

Following procedure is adopted for incurring the contingent

expenditures.

1. The request for purchase of any article of expenditure is initiated by the

store In charge.

2. ON receipt of the request the drawing officer/head of office examine the

budget allocation. If the funds are available to meet the expenditures

19

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 20/55

allows incurring such expenditures. Sometimes, the sanction of higher

competent authority is obtained. This is done when the expenditures to be

incurred are of the heavy amounts.3. A committee comprising of senior officials of the office is constituted to

look after the procedure of incurring the contingent expenditures and assist

the head of office for these purposes.

4. Quotations and tenders are invited where necessary. Quotations are invited

if the amount is more than Rs.10, 000. Tender in the press are invited for

Rs. 100,000 and above.

5. On the receipts of tenders/quotations, these are opened by the head of

office, in the presence of purchasing committee. All the members of the

committee are to analyses the different offers. The lowest offer is to be

accepted. However, if the head of office think it justified, he can reject all

the offers and call fresh tenders/quotations.

6. A comparative statement is prepared and signed by all the members of

committee. Then the orders for supply of articles are placed to the supplier

so selected.

7. The supplier issues, bill or invoice to the office. This bill is entered and a

contingent bill is prepared in the prescribed form for withdrawal of amount

from the treasury. Sometimes the amount (if available) is paid out of

permanent advance, and article is acquired.

8. When bill is passed by the DAO, the amount is drawn from the bank and

payment is made to supplier. The article so acquired is entered into the

stock register (if applicable), if the amount had been paid out of permanent

advance, it is adjusted in the Contingent Charges Register and cash book.

9. The amount is entered in the cash book, when the amount is drawn and

payment is made.

STOCK REGISTER

The articles purchased for the purpose of use in government accounts offices

20

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 21/55

are called as Stocks. Proper record of such stocks purchased and disposed is essential

for effective control of such articles. For this purpose stock registers are maintained in

which all the purchases and disposal of articles are entered. The stocks purchased may be of the following two types.

i) Permanent Articles

ii) Consumable Articles

i) Permanent Articles

It means the articles whose life is long enough to be used for number

of years. These articles can be shown as used or consumed. But when

they become unserviceable they are written off or disposed off. For this purpose a report is prepared and sent to the controlling officer. The

controlling officer after inspection can order for writing off these

articles. Sometimes these articles are sold off at the auction. It is called

disposal of these articles. All type of machinery and plant, equipments,

furniture & fixes, electric appliances etc.

REGISTER FOR PERMANENT ARTICLES

A separate register is maintained by each department for the record of

permanent articles. This register is called as Stock Register for permanent articles.

The pages for this register are consecutively numbered and each page is used for

writing one article. A certificate to the total pages of the register is given at the

beginning. An index is also given in this register at the beginning to make the tracing

of particular page easy.

Method of Filling Stock Register

1. Year of Account

The calendar year in which the transaction for the purchase or sale of article

takes place is recorded under this column.

2. Balance Brought Forward

The number of articles available before the transaction takes place is recorded

under this column.

3. Date of Purchase

This means the date on which the article is purchased from the suppliers and

received in the office.

21

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 22/55

4. Bill in Which Charges

It refers to the No. and date of the contingent bill in which the cost of article

was drawn from the treasury.

5. Nos. of Articles

Total numbers of articles purchased is written under column 5.

6. Price

This means the total amount of articles purchased.

7. for Which Use

Under this column, the purpose for which the article is to be used or being

used is written.

8. Total

The total numbers of articles are recorded in this column. The total is obtained by adding the balance and purchased.

9. No. of Articles Disposed

This means how many articles in number disposed i.e. 1, 2 or 3 etc

10. Why & How Disposed?

This means the reason for disposal of articles along with the means of

disposal.

11. Sale Price

The amount realized by the sale of articles (if any) is written in this column.

12. When Credited to GovernmentIn this column, the date on which the amount realized is deposited in

treasury/bank is written.

13. Original Price

This means the price which was paid when the asset was acquired.

14. Balance Carried Over

The numbers of articles in this accounts office after the transaction is written

in this column. It is equal to total articles minus articles disposed.

15. Initial of Govt ServantIn this column the controlling officer initials when he verifies the entries.

16. Remarks

An explanatory note is recorded in this column.

22

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 23/55

Chapter 3

GAD SECTION

Payment of salaries, TA (traveling Allowance), Medical charges etc pertaining

to the gazette officer posted in district are pre-audited in this section. The claims of

gazette officers are presented at pre audited by the concerned auditors and after recording payment orders thereon these bills are sent to the district accounts officer

for signing of pay order and after embossing special seal thereon these are sent back

to the counter section for delivery to the claimants. All personal record relating to a

gazette officer is available and maintained in this section.

Chapter 4

23

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 24/55

PENSION SECTION

Pension claim of a retired official is prepared by his department on prescribed

forms and duty sanction is forwarded to pension section of district accounts officer.The auditor in this section the auditor on receipt of pension papers applies checks,

length of services, no demand certificates, of pay correctness drawn by him from time

to time and entitlement of pension are verified minutely.

After due check, pension payment order is prepared and put up to the district

accounts officer for final signature. Pension payment order in favor of pensioner is

finally issued to the bank for payment. First payment to the pensioner is always made

on due verification and identifications by the district accounts officer. In order to

facilitate pensioners, they are authorized to draw pension from any bank of their

choice.

Chapter 5

24

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 25/55

COMPILATION OF ACCOUNTS SECTION

All vouchers on which payment is make to government department both

federal and provincial and all challan on which money is received on behalf of thegovernment by the bank are forwarded by the banks to the district accounts office

daily. Daily scrolls (debit & Credit) of the state bank are compiled in this section in

the proper accounts.

Receipts and Payments

On receipt of these payments and receipts vouchers, the compilation section

of accounts office posts them in Daily Cash Book and at close of the month

consolidate

all the payment and receipt department wise. Thereafter a monthly consolidated

account

is prepared and sent to the accountant general office of province for further

consolidation

of accounts at provincial level. The figures of monthly account both for Receipts and

Payments are intimated to finance department/auditor general of Pakistan.

Closing of the Year

At the close of each financial year, the yearly account is prepared by the

accountant general reflecting the figures of receipts and payments of the whole

province.

Personal Deposit Account

Besides, the preparation of monthly account, the compilation section of DAO

also performs the duties of maintenance of personal deposit, accounts of courts and

payment against those personal accounts. Personal ledger accounts of some

departments are also kept in compilation section. The payment against these personal

ledger accounts are made on tendering cheques by the departments.

Record of Advances

Advances of house building, Motor car, Motorcycle and cycle made to

25

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 26/55

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 27/55

Chapter 6

PRE AUDIT SECTIONThis section deals with the audit of personal claims of non gazette civil

servants and claims of contingencies of departments. The claim of an office regarding

purchases of officer equipment, utilities and commodities are pre audited in this

section. All claims after mentioning their nature are submitted to this section by the

departments through pre audit counter.

4 P’s

The auditor conducts the audit of the bills on four P’s bases.

1. Provision:

The auditor checks that there is any budget for the department or not then send

a bill.

2. Procedure:

The department has adopted a specific procedure or not.

3. Power

The auditor checks that the DDO (District Disbursing Officer), that prepared

the bill have the authority for certain expenditure or not.

4. Purpose:

He checks the purpose of expenditure that for which purpose the fund is

utilized. Claims are checked by the auditors posted in this section with reference to

the availability of budget, conformity to the rules and sanction accorded by the

competent authorities and supporting vouchers. Similarly, claims of non-gazette civil

servants on account of pay, T.A, Medical etc. also scrutinized with reference to

entitlement of pay scale prescribed for them

Circulation of Bill

After the claims are admitted, necessary pay orders are recorded thereon and

submitted to the district accounts officer for signings the pay orders and embossing

special seal. These passed claims are returned to the department through pre audit

counter. If the auditor is not satisfied about the information are given in the bill then

he did not pass the bill and returns that bill to the concerned department.

27

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 28/55

Chapter 7

COUNTER SECTION

1. Receipt of Claims

All kinds of claims in this section on receipt of a claim that the auditor

posted in this section issues a brass token in line of claim. All the receipts of bills

in a day is distributed amount relevant sections for pre audit and recording pay

orders these bills are received back in counter section. These passed/uncased bills

are delivered to persons on return of token issued to them.

2. Daily Sheet

A daily advice sheet of payment orders is prepared in this section and sent

to bank in support of pay orders recorded on bill.

3. Token Census

On the end of every month a Token Census Report is prepared in

which issued token and in hand tokens are mentioned. If the tokens are lost

then the token issuer is responsible for it.

28

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 29/55

Chapter 8

COMPUTER SECTION

The present age is of scientific age and every being is done through electronic

media. The federal & provincial government desire facts and figures immediately.

Moreover, the volume of work is greater as compared to the past. It is very difficult to

do jobs manually. Therefore to meet the day to day requirements the government has

installed Computers in each accounts office to avoid manual labor as well as to have

immediate information.

In district accounts office all the primary accounts have been feed in computer

and benefit is being taken gradually with the operation of these machines and with the

passage of time manual work will be totally stopped and every account maintained by

the computer.

PIFRA (Project Improvement for Financial Reporting & Auditing)

The World Bank and developed countries provides financial aid to developing

countries. But they were not ready to provide more aid. They said that the system of

preparation of accounts and audit is not proper in Pakistan. They said that there is

misuse of financial aids and chances of manipulation are high.

Now World Bank gave a project named as PIFRA which stands for Project

Improvement for Financial Reporting and Auditing. So they prepare software for this

purpose. The Govt. of Pakistan took an initiative to address the shortcomings of the

financial reporting system and to ensure good governance. The IMF carried out a

survey in Government Accounting in early 1990s, followed by a diagnostic study

sponsored by the World Bank. As a result, the Project to Improve Financial Reporting

and Auditing (PIFRA) was introduced by the Auditor General of Pakistan in 1994.

The main objective of this project is to computerize the whole accounting andauditing system of the country. The idea behind computerizing the whole system is to

29

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 30/55

generate timely, accurate and reliable financial statements; to monitor fiscal deficit; to

forecast flow of cash; to manage public debt and to achieve effective financial

controls.

The accounting system of Pakistan was inherited from the century old

accounting system of the Indian govt. The old accounting system lacks timeliness,

accuracy and most importantly transparency. Accounts of any organization, large or

small, are the most important tool for curbing the corruption by keeping an eye on ins

and outs of the money and more importantly they give the overall inner picture of the

organization to the stakeholders which helps them take better financial decisions.

While talking about the country as an organization the importance of the

accounts becomes much more vital. The stakeholders are everyone, be that any

foreign aid entity, any govt. department, govt. employees, provincial or district govt.,

any bank, any foreign govt. etc. You name it and they are there. So the importance of

these accounts increases manifolds.

Furthermore, the old manual system was like a haunting monster also for a

common government employee. There are three main things which a common govt.employee comes to an accounts office for, viz. salary, general provident fund and

pension. Our experience shows that in the old system a common man had a series of

unlimited problems and hurdles to face in order to get his financial claims. His fever

started a week before he had to visit the accounts office for any of the financial

claims.

But, unfortunately, till the recent past our governments did not pay proper

attention to overcome these problems. Due to which the exact and clear picture of the

economy of the country is still not visible to virtually anybody and on the other hand

common man face enormous difficulties in receiving his financial claims.

After the introduction of PIFRA this ultimate goal would be achieved soon.

That is why this project was introduced. The main objectives are to achieve timely,

accurate and complete accounts with transparency and most importantly to facilitate

the common govt. employee regarding their financial claims. But, there is a lot more

to be done to achieve this goal.

30

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 31/55

NEED OF PIFRA

1. The assessment of public sector accounting and auditing is generally meant to help

implement a more effective public financial management (PFM) through better

quality accounting and public audit Processes in Pakistan and to provide greater

stimulus for more cost effective outcomes of government spending. More specific

objectives are: (a) to provide the country's accounting and audit authorities and other

interested stakeholders with a common, sound knowledge as to where local practices

stand in accordance with international standards of financial reporting and auditing;

(b) to assess the prevailing variances; (c) to chart paths for improving the accordance

with international standards; and (d) to provide a continuing basis for measuring

improvements.

2. As part of the general support program in South Asia for assessment and

improvement of public sector accounting and auditing, the World Bank, with the

cooperation of member governments, is conducting a Review of Public Sector

Accounting and Auditing Practices in member countries. In conducting thisassessment, a set of diagnostic questionnaires [developed to be consistent with the

context of the PFM Performance Measurement Framework used by the Public

Expenditure and Financial Accountability (PEFA) Program ], was used to gather

substantial insight into country performance with regard to the external auditing and

financial statement reporting PFM indicators. Annex A discusses the methodology

used for conducting the assessment in this report.

3. The diagnostic questionnaire was used to gather information on national standards

and practices for accounting, financial reporting, and auditing in the government

budget sector and in the state-owned enterprise (SOE) sector. Conducted in

cooperation with country authorities, the diagnostic questionnaires incorporate the

principles contained in the public sector accounting and auditing standards

promulgated by the International Federation of Accountants (IFAC) and the

International Organization of Supreme Audit Institutions (INTOSAI). Annex B

summarizes the international accounting and auditing frameworks that were used in

31

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 32/55

this assessment. The responses to these questionnaires stimulated further discussions

among the World Bank team and senior staff in the offices of the Auditor General of

Pakistan (AGP) and Controller General of Accounts (CGA). These discussionsexamined accounts and audit reports and working papers as a means to jointly explore

the quality of processes and products.

4. The maintenance system for public accounts in Pakistan is long standing. Since

1997, the World Bank Project for Improvement of Financial Reporting and Auditing

(PIFRA) has supported the comprehensive reform efforts by the Government of

Pakistan to streamline its accounting and auditing systems and procedures, while

developing the institutional and individual capacities for better public financial

management. The initial reforms included some separation of audit and accounts

activities through promulgation of legislation relating to separate roles for the Auditor

General and the Controller General of Accounts. They also included designing

modern accounting and auditing processes and devising a comprehensive human

resource management plan. The replacement of inefficient manual and outdated

accounting processes in the general government sector by faster and updated

computerized programs (using the accounting software package SAP R/3) is

underway with a program to computerize all district accounting offices by the end of

2007. Annex C includes excerpts from Pakistan auditing and accounting legislation.

5. The second phase of the PIFRA project, PIFRA II, will help the government to

build capacity to improve the accuracy, comprehensiveness, reliability, and timeliness

of intra-year and year-end government financial reports at federal and provincial

levels. The PIFRA II will also initiate the process at district and sub district levels

thereby strengthening the financial accountability cycle. The project would therefore

directly support the commitment of the Government of Pakistan in improving public

financial management, accountability, and transparency, and enhance the capacity of

public sector managers to meaningfully use credible financial information for better

and informed decision-making. It will facilitate public oversight of the use of public

monies, and increase the national and international credibility of the national and

provincial governments' financial statements and assurance processes.

32

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 33/55

6. The reform efforts need to include identification of the relevant international

standards of accounting and auditing applicable to the public sector and help achievecompliance with those standards. Adoption of International Public Sector Accounting

Standards (IPSAS) for accounting and financial reporting and the IFAC-issued

International Standards on Auditing (ISA) in addition to the INTOSAI Auditing

Standards are important steps in improving the basis for adequate public financial

management.

PIFRA Components

FABS (Financial Accounting & Budgeting System

Government Auditing

Training

Change Management (HRM)

In order to achieve the targets of PIFRA, New Accounting Model (NAM) was

introduced to replace the old accounting practices. This system is mainly bases on the

modified cash basis accounting. The bases of the Modified Cash basis accounting are:

Double Entry Bookkeeping system

Recording of Commitments

Fixed Assets Recording

The Salient features of NAM are:

Integration of Budget & Expenditure Flow

Accurate and ν Timely Reporting

Cash Forecasting

International Credibility

Assets will be recorded

Commitments will be Recorded

What PIFRA means to us?

National Level

Integration of Budget & Expenditure information flow

33

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 34/55

Accuracy and timeliness in Reporting

Cash Forecasting

International credibilityTransparency in accounting system

Good governance

Elimination of fraudulent activities

Individual Level

Integration of Salary Network

Pension / Commutation Calculation through system

Consolidated Personal Information

Updated GP Fund Accounts

GP Fund calculation through the system

PIFRA in Sindh

This project is being carried out in phases throughout the country. There are

number of steps in which the project is implemented in the provinces. The first and

most important phase is to computerize the accounting offices and then implement

various prescribed modules.

There are 23 District in Sindh province. PIFRA is being implemented District

wise. The implementation was divided in phases. Initially, Two Districts were selected

as Pilot Sites viz. Karachi and Hyderabad. After the successful start of the PIFRA on

these sites, three more sites were selected as Rollout Sites, namely, Sukkur,

Nawabshah & Larkana. The system here was also started with success.

In these sites, initially, the salaries of the govt. employees were computerized through

HR Module and then other financial claims from various offices were entered into the

computerized system through FI Module. Before starting the project at rest of the

Replication sites, the system of Workflow (Electronically Generated Cheque System)

was implemented at the already productive (online) sites, at the initiative of the

Accountant General Sindh.

34

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 35/55

The target was to make all the sites productive by the end of January 2008, but

due to province wide riots after the sudden death of Ms. Benazir Bhutto, some of the

District Accounts Offices were severely damaged and the plan was revised.

The Accountant General Sindh succeeded to bring one site i.e. Ghotki, online

in December 2007 and on site i.e. Thatta in January 2008. According to the revised

plan four sites viz. Tando M. Khan, Matiari and Sanghar were made productive in the

month of February 2008. Moreover, Shikarpur, Jacobabad, Khairpur, Tando Allah Yar,

Mirpurkhas, Umarkot, Mithhi and Badin were inaugurated by the Accountant General

Sindh in March 2008. This was one of the greatest achievements of the Accountant

General Sindh and PIFRA.

Pension and GP Fund Functionalities (HR Module)

HR Module covers Salary, Pension and GP Fund Functionalities or govt.

employees. It has been mentioned above that when the site (District Accounts Office)

is made productive/online the salary of the employees of that district is paid through

the system. As for the Pension and GP Fund Modules, they are being currently in the

implementation phase. These functionalities are started after a reasonable time iselapsed after the productivity of district, so that the users become more acclimatize

with the system. The pension and GPF Functionalities have been successfully started

at AG Sindh and District Accounts Office Hyderabad, so far. Currently these

functionalities are being extended in DAOs Sukkur, Nawabshah and Larkana. As soon

as they are successfully implemented in these sites, the rest of the sites will also be

brought on the same system. In these functionalities one of the most important tasks is

to update the past information regarding their Provident Fund deduction of the

employees who are in the service well before the system was introduced. This

updating will ultimately facilitate the employee at the time of their retirement.

Budget Availability Check (FI Module)

There are numerous functionalities in FI Module. So far, several

functionalities have been implemented in AG Sindh and its DAOs, e.g. Civil

Accounts, Workflow, etc. But there are still some which are in the implementation

phase.

35

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 36/55

One of the most important functionalities is Budget Availability Check. In fact,

this functionality shows the beauty of the system. The idea is that no financial claim is

entertained through the system if the budget in the relevant head of account is notavailable. This prevents any wrong payment, intentionally or unintentionally.

Moreover, it also keeps the accounts updated and error-free. This system has been

successfully implemented in the AG Sindh office, being the pilot site. The next target

is to implement this functionality at all the productive sites.

Capacity Building

PIFRA revolutionized the accounting system by introducing the New

Accounting Model and computerized environment in the govt. accounting offices

throughout the country. The most difficult task in the implementation of the project

was to change the behavior and mindset of the working staff. The staff was highly

expert in the current accounting system and well versed with the relevant regulations.

But, most of them were not knowledgeable about the computers and its working. So,

implementing such an advanced computerized solution in these offices was a gigantic

task and a great challenge. The only way to achieve the desired goal was to impart

proper training in the existing staff.

PIFRA organized exhaustive training programs throughout the country and

trained hundreds of employees of not only the accounting offices but also the DDOs

(Drawing and Disbursing Officers) of all the departments.

In AG Sindh, initially, PIFRA trained 25 staff members, who then extended

their expertise and trained more than 500 officers/officials of the office, and the

practice is still going on. Currently, the trainings from PIFRA are also being carried

out and a number of officers/officials of various District Accounts Offices are being

trained for the successful implementation of the project.

Its important to mention that the AG Sindh, himself, took initiative to organize

various capacity building programs for not only its own officers/officials but also the

Nazims, District Coordination Officers and Executive District Officers (Finance &

Planning).

The AG office organized a series of workshop regarding District Budgeting

36

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 37/55

and Expenditure Authorization. In the first two phases the EDOs of all the Districts

were given comprehensive training regarding preparation of District Govt. Budget. As

a result all the District Governments of Sindh prepared their own budget for the firsttime in FY 2005-06. In the third and final phase a grand workshop was organized in

which the Nazims, DCOs and EDOs of all Districts were given the overview of the

District Budgeting, the Schedule of Authorized Expenditure and PIFRA.

Moreover, two very important workshops were organized by the AG Sindh for

the staff of the District Accounts Offices vis-à-vis Monthly Civil Accounts through

SAP System. The workshops were arranged at two remotest sites of Sindh i.e. Mithhi

and Ghotki. The Accountant General Sindh himself attended the meeting which

depicts the seriousness and importance of the events.

Furthermore, five District Accounts Officers Conferences have been organized

in the last four years. The purpose of these conferences is to discuss the problems and

issues regarding the implementation of the project and to find the solutions then and

there. Besides, the DAOs, themselves, are also given brief training on diverse

activities.

As a result, the PIFRA has been so far a successful project in Sindh regarding

the FABS component. The World Bank has paid number of visits to the AG Sindh and

always applauded the efforts of this office and appreciated the outcomes.

SAP (System Applicants Product)

SAP was founded in 1972 in Walldorf, Germany. It stands for Systems,

Applications and Products in Data Processing. Over the years, it has grown and

evolved to become the world premier provider of client/server business solutions for

which it is so well known today. The SAP R/3 enterprise application suite for open

client/server systems has established a new standard for providing business

information management solutions.

SAP products are considered excellent but not perfect. The main problems with

software product are that it can never be perfect. The main advantage of using SAP as

your company ERP system is that SAP have a very high level of integration among its

37

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 38/55

individual applications which guarantee consistency of data throughout the system

and the company itself.

In a standard SAP project system, it is divided into three environments, Development,

Quality Assurance and Production

The development system is where most of the implementation work takes

place. The quality assurance system is where all the final testing is conducted before

moving the transports to the production environment. The production system is where

all the daily business activities occur. It is also the client that all the end users use to

perform their daily job functions.

To all company, the production system should only contain transport that has

passed all the tests. SAP is table drive customization software. It allows businesses to

make rapid changes in their business requirements with a common set of programs.

User-exits are provided for business to add in additional source code. Tools such as

screen variants are provided to let you set fields attributes whether to hide, display

and make them mandatory fields.

SAP is using in all accounts offices of Pakistan and fulfills the needs of

compilation of accounts and audit. It is especially designed and prepared for the field

of accounting and auditing. So in this way the chances of frauds and manipulation in

accounts are low.WAPDA, PIA and some other big organizations are also using SAP.

Automation Solution (SAP)

In order to keep the uniformity a common automation solution has been

chosen for the whole country under this project. The world-renowned state-of-the-art

integrated software SAP is the Enterprise Resource Plan (ERP) which is being

implemented at all the accounting entities overall the country. There are number of

functionalities available in this ERP, which are highly flexible in nature and can be

modified according to the requirements of the particular organization. Keeping in

view the requirements at the country level, the Govt. of Pakistan has purchased three

most essential modules of SAP. They are:

Basis (System Administration) Module

38

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 39/55

This module covers the overall system administration. The user authorization,

the working of the main servers, the roles of particular users, the connectivity between

all the sites in the country and various server-related issues are covered in thismodule.

Financial Module

This module covers the financial side of the system. The generation of various

financial reports, like monthly, quarterly and annual accounts, etc.; the budget

preparation and maintenance and expenditure booking into the system, project &

commitment accounting are some of the tasks which are performed using this module.

Human Resource (HR) Module

In HR module, the update record of the employee, the updated GP Fund

account, its calculation and payment; the pension/commutation calculation and

payment; and salaries of the govt. employees are operated through the system.

Chapter 9

39

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 40/55

TREASURY SECTION

The treasury of district is conducted under the supervision of district accounts

officer. A contract staff has been employed in treasury who deals with the public onaccount of sale of different kinds of stamps and stamp papers. The controller of

stamps Karachi supplies stamps papers and other stamps to district accounts officer

and then later after sale deposits & sale proceeds with the government account. All

kind of valuables which are detected by the police department are also kept in treasury

for safe custody in double locks and returned as when demanded.

The Treasury function covers the following activities.

1. Cash management;

2. Management of government bank accounts;

3. Financial planning and forecasting of cash flows;

4. Public debt management;

5. Administration of foreign grants and counterpart funds from international

aid;

6. Financial assets management

Chapter 10

40

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 41/55

FINANCIAL ADMINISTRATION

The Financial administration means the operations designed to make funds

available to the officials and to ensure their lawful and efficient use.The principle parties involved are:

1. The executive which needs funds.

2. The legislative bodies which grant funds.

3. The executive officials which controls the expenditure of funds and,

4. The audit and accounts offices which determine the legality and propriety of

the use of the funds.

In a small organization, the financial management is simple but in big

organizations like federal government, provincial governments and

autonomous bodies the setup, procedures and problems are complex. The

financial management deals with all the money aspects. The earnings, savings,

borrowings, spending and investing of monetary funds are parts of this

financial management. It also consists of providing and utilizing the money,

capital rights, credits and funds of any period which are required in the

operation of an organization.

Executive

The executive is responsible for the formulation of the financial policy

of the government; questions of policy may arise at any time in the day to day

administration but the questions specifically arise when budget is under

preparation. After the budget estimates for a year have been consolidated by

the finance division/department. They are placed before the cabinet which has

to decide as to what new schemes, proposed by the operating agencies should

be admitted, how funds are to be obtained to meet the expenditure, which

taxation policy is to be followed and so on.

Parliament

According to the democratic principle, no tax can be levied or

41

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 42/55

collected and no expenditure can be incurred by the government unless it is

first consented by the parliament.

Therefore, before the government can work on the budget plan, it has to get it passed by the parliament. This is known as enactment of the budget.

ADMINISTRATIVE CONTROL

The administrative control is exercised by the executive through

ministry of finance/finance department. The budget is prepared by various

administrative units; it is finally consolidated by ministry of finance/finance

department and then presented to parliament. After the budget is passed, the

execution thereof is the responsibility of ministry of finance/finance

department. It is concerned not only with the supervision of all aspects of the

nation’s finances but also with the economic planning. The control of the

ministry of finance/finance department is all pervasive characteristics of the

public administration.

Public Expenditure

The public expenditure may be categorized as under.

1 Maintenance and equipment of Armed Forces including police in peace

and war.

2 Administration of justice.

3 Maintenance of the ceremonial head of state and diplomatic representative

abroad.

4 Maintenance of machinery of civil government including ministries,

legislative and civil servants.

5 Public debt charges including payment of principle and interest.

6 Expenditure directly devoted in formation of industry and commerce.

7 Social welfare, health, education, old age pension etc.

Sources of Public Finance

42

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 43/55

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 44/55

collective noun and means collections of people and as an adjective it implies

belonging to people. The word Finance means money. It also signifies “Money

Matters” and their “Management” by taking together these terms means “MoneyMatters pertains to a State”. Public finance is one of those subject which lie in

between economic and politics and it signifies the income and expenditure of

public authorities and adjustment with one another. The term “Public Authorities”

broadly speaking includes federal government, provincial government, autonomous

organizations and local bodies.

Why Public Finance Needed?

One can ask why a state wants the finance. The answer is not very far to seek.

As human beings have certain wants for their satisfactions such as eating, drinking

and clothing etc. but there are certain wants such as protection of life and property,

construction of railways, roads, bridges and irrigation canals, hospitals, universities

and ordinance factories etc. which one can’t do in his individual capacity and has to

look to the state for doing the needful. So in order to perform this task, the state does

require finance and that is done by collecting revenues and then incurring

expenditure. The best system of public finance is one that secures the maximum social

advantages-greatest good of greatest number from the operation which it conducts.

The proper role of government provides a starting point for the analysis of public

finance. In theory, private markets will allocate goods and services among individuals

efficiently (in the sense that no waste occurs and that individual tastes are matching

with the economy's productive abilities). If private markets were able to provide

efficient outcomes and if the distribution of income were socially acceptable, then

there would be little or no scope for government. In many cases, however, conditions

for private market efficiency are violated. For example, if many people can enjoy the

same good at the same time (non-rival, non-excludable consumption), then private

markets may supply too little of that good. National defense is one example of non-

rival consumption, or of a public good.

"Market failure" occurs when private markets do not allocate goods or services

efficiently. The existence of market failure provides an efficiency-based rationale for collective or governmental provision of goods and services. Externalities, public

44

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 45/55

goods, informational advantages, strong economies of scale, and network effects can

cause market failures. Public provision via a government or a voluntary association,

however, is subject to other inefficiencies, termed "government failure."

Under broad assumptions, government decisions about the efficient scope and

level of activities can be efficiently separated from decisions about the design of

taxation systems (Diamond-Mir lees separation). In this view, public sector programs

should be designed to maximize social benefits minus costs (cost-benefit analysis),

and then revenues needed to pay for those expenditures should be raised through a

taxation system that creates the fewest efficiency losses caused by distortion of

economic activity as possible. In practice, government budgeting is substantially more

complicated and often results in inefficient practices.

Government can pay for spending by borrowing ( borrowing), although

borrowing is a method of distributing tax burdens through time rather than a

replacement for taxes. A deficit is the difference between government spending and

revenues. The accumulation of deficits over time is the total public debt. Deficit

finance allows governments to smooth tax burdens over time, and gives governments

an important fiscal policy tool. Deficits can also narrow the options of successor

governments.

Public finance is closely connected to issues of income distribution and social

equity. Governments can reallocate income through transfer payments or by designing

tax systems that treat high-income and low-income households differently.

The "Public Choice" approach to public finance seeks to explain how self-

interested voters, politicians, and bureaucrats actually operate, rather than how they

should operate.

Government expenditures

Economists classify government expenditures into three main types. Government

purchases of goods and services for current use are classed as government

consumption. Government purchases of goods and services intended to create future

benefits--- such as infrastructure investment or research spending--- are classed as

45

7/31/2019 15910004 Account Office Internship Report 03336845811

http://slidepdf.com/reader/full/15910004-account-office-internship-report-03336845811 46/55

government investment. Government expenditures that are not purchases of goods

and services, and instead just represent transfers of money--- such as social security

payments--- are called transfer payments.

Government operations

Government operations are those activities involved in the running of a state or a

functional equivalent of a state (for example, tribes, secessionist movements or

revolutionary movements) for the purpose of producing value for the citizens.

Government operations have the power to make, and the authority to enforce rules