Embed Size (px)

Citation preview

Te

Aa

b

a

KMPfDm

1

m(b2om(

(

1d

Management Accounting Research 20 (2009) 263–282

Contents lists available at ScienceDirect

Management Accounting Research

journa l homepage: www.e lsev ier .com/ locate /mar

he design and use of performance management systems: Anxtended framework for analysis

ldónio Ferreiraa,1, David Otleyb,∗

Department of Accounting and Finance, Monash University, Building 11E, VIC 3800, AustraliaLancaster University Management School, Lancaster LA1 4YX, UK

r t i c l e i n f o

eywords:anagement control systems

erformance management systemsrameworkesign and use of performanceanagement systems

a b s t r a c t

Issues in the area of performance management and management control systems are typ-ically complex and intertwined, but research tends to be based on simplified and partialsettings. Simplification has made the work easier to carry out, but it has come at the priceof increased ambiguity and conflicting findings from different studies. To help mitigatethese issues, this paper puts forward the performance management systems frameworkas a research tool for describing the structure and operation of performance managementsystems (PMSs) in a more holistic manner. The framework was developed from the relevantliterature and from our observations and experience. In particular, it elaborates the 5 ques-tions of Otley’s [Otley, D., 1999. Performance management: a framework for managementcontrol systems research. Management Accounting Research 10, 363–382] performancemanagement framework into 12 questions and integrates aspects of Simons’ levers ofcontrol framework.

Anecdotal evidence suggests that the extended framework provides a useful research toolfor those wishing to study the design and operation of performance management systemsby providing a template to help describe the key aspects of such systems. It allows an holisticoverview to be taken while making this a feasible task. The paper uses material from twofield studies to illustrate how the framework can be used to provide an overview of the

mana

major performance. Introduction

The literature in the area of performance manage-ent systems (PMSs) and management control systems

MCSs) increasingly recognises the need for research to beased on more coherent theoretical foundations (Chenhall,

003; Covaleski et al., 2003). Researchers suggest that the-ry be used to contextualise findings and to provide aore systematic development of knowledge in the fieldChapman, 1997). Others note that the difficulty in making

∗ Corresponding author. Tel.: +44 1524 593636; fax: +44 1524 847321.E-mail addresses: [email protected]

A. Ferreira), [email protected] (D. Otley).1 Tel.: +61 3 9905 2467; fax: +61 3 9905 5475.

044-5005/$ – see front matter © 2009 Published by Elsevier Ltd.oi:10.1016/j.mar.2009.07.003

gement issues within an organization.© 2009 Published by Elsevier Ltd.

significant progress in the field partially derives from thecompartmentalised approach typically followed by empir-ical research (Chenhall, 2003; Covaleski et al., 2003). Therehas been a tendency to focus only on specific aspects ofcontrol systems, as opposed to adopting a more compre-hensive and integrated approach (Chenhall, 2003; Dent,1990; Malmi and Brown, 2008). Although this may be dueto access or time limitations, or to the difficulty of gen-erating and managing such complex datasets, the lack ofa more complete description of the totality of a controlsystem contributes to spurious findings, ambiguity, and

potentially to conflicting results (Chenhall, 2003). Oth-ers have maintained that our understanding of MCSs willremain ‘piecemeal’ for as long empirical research continuesto ignore the interdependency between different controlmechanisms operating at the same time in the same orga-

t Accoun

264 A. Ferreira, D. Otley / Managemennization (Abernethy and Brownell, 1997). Therefore, weargue that research would benefit from a framework thatprovides a broad view of the key aspects of a MCS andthat allows researchers to obtain an holistic overview inas efficient way as possible. This paper proposes such aframework.

It is organized as follows. The following section outlinessome of the frameworks found in the literature, plac-ing particular emphasis on the two that our study buildsupon. Section 3 puts forward the performance manage-ment systems (PMSs) framework itself, with its theoreticaldevelopment being elaborated in Section 4. This is fol-lowed by a discussion on the use of the framework and aconclusion. Two applications of the framework to specificorganizations are briefly presented in Appendix A.

2. Management control systems

Much of the early literature on this topic has been cate-gorized under the heading of management control systems,following the seminal work of Robert Anthony (1965).However, in our view, this has become a more restric-tive term than was the original intention and we prefer touse the more general descriptor of performance manage-ment systems (PMSs) to capture an holistic approach to themanagement and control of organizational performance.We see this term as including all aspects of organizationalcontrol, including those included under the heading ofmanagement control systems.

MCSs have been conceptualised in various ways. Theclassic view, outlined in Anthony’s (1965) work, divided therealm of control between strategic planning, managementcontrol, and operational control. He defined managementcontrol as “the process by which managers assure thatresources are obtained and used effectively and efficientlyin the accomplishment of the organization’s objectives”(p. 17). However, this approach resulted in a disconnectbetween MCS and strategic planning and between MCS andoperational control (Langfield-Smith, 2007; Otley, 1999).Further, it encouraged a narrow view of MCSs that fallsshort of capturing the richness of issues and relationshipsimplicated in MCS design and use. In particular, it concen-trated on formal (and usually accounting) controls withoutsetting them in their wider context.

A number of MCS definitions have been proposed inmore recent years (for a review and discussion see Malmiand Brown (2008)). While Simons (1995) views MCSs asthe means used by senior managers to successfully imple-ment their intended strategies, others have defined MCS asthe systematic use of management accounting in conjunc-tion with other forms of control such as personal or culturalcontrols to achieve some goal (Chenhall, 2003). A broadernotion of MCSs encompasses the entire strategic process,that is, it includes both strategic formulation (Mintzberg,1978) and strategic implementation (Merchant and Otley,2007).

We acknowledge that the concept of PMSs is a difficultone to establish. However, we view PMSs as the evolv-ing formal and informal mechanisms, processes, systems,and networks used by organizations for conveying the keyobjectives and goals elicited by management, for assisting

ting Research 20 (2009) 263–282

the strategic process and ongoing management throughanalysis, planning, measurement, control, rewarding, andbroadly managing performance, and for supporting andfacilitating organizational learning and change. Hence weuse the term performance management system to encap-sulate these more general processes, and our workingdefinition of a PMS includes both the formal mechanisms,processes, systems, and networks used by organizations,and also the more subtle, yet important, informal controlsthat are used (Chenhall, 2003; Malmi and Brown, 2008).It is also based on the premise that key objectives andgoals are set by managers at every level, but it does notassume that these objectives and goals are necessarily theones that best serve the organization as a whole. This isconsistent with Abernethy and Chua (1996), who followthe view that objectives are set by the “dominant orga-nizational coalition” (p. 573) in that it is managers whoare entrusted the responsibility of setting organizationalobjectives, taking into consideration the expectations ofthe relevant stakeholders. The definition views the PMSsas performing a supporting role for a broad range of man-agerial activities, including strategic processes — whichinvolve strategic formulation and strategic implementa-tion (Mintzberg et al., 2003; Pearce and Robinson, 2007) —and ongoing management. Also, through its learning andchange facilitation role, a PMS can support or foster emer-gent strategies (Mintzberg, 1978).

We next discuss Otley’s (1999) performance manage-ment framework and Simons’ (1995) levers of controlframework. These frameworks are examined more closelybecause both played a major role in the development of theextended framework.

2.1. Otley’s (1999) performance management framework

Otley (1999) proposed an inductively generated frame-work for studying the operation of MCSs, drawing upon theextant body of knowledge in the field and on his researchexperience. In essence, the framework highlights five cen-tral issues which he argues need to be considered as part ofthe process of developing a coherent structure for perfor-mance management systems. The framework was intendedto aid the description of MCSs and to be a first step towardsdeveloping a more comprehensive framework.

The first area addressed by his framework relates to theidentification of the key organizational objectives and theprocesses and methods involved in assessing the level ofachievement in each of these objectives. The second arearelates to the process of formulating and implementingstrategies and plans, as well as the performance mea-surement and evaluation processes associated with theirimplementation. The third area relates the process of set-ting performance targets and the levels at which suchtargets are set. The fourth area draws attention to rewardssystems used by organizations and to the implications ofachieving or failing to achieve performance targets. The

final key area concerns the types of information flowsrequired to provide adequate monitoring of performanceand to support learning.A number of studies have drawn on Otley’s (1999)framework. Ferreira (2002) used the framework to struc-

t Accoun

tbSpiMtjepf

sMeowcaftinusTwaefia2iibit

OttitsooSoyf(fiaitaFfp

A. Ferreira, D. Otley / Managemen

ure the evidence from four case studies, as well as theasis for interpretation and identification of key issues.imilarly, Tuomela (2005) has drawn on this framework toresent the findings of his case study that investigated the

ntroduction of a new performance measurement system.ore recently, Stringer (2007) has drawn extensively on

he framework to evaluate research published in two majorournals. She found that less than one tenth of the studiesxamined displayed an integrated approach to the study oferformance management and that research is generallyragmentary.

The framework proposed by Otley has a number oftrengths. First, it provides a helpful structure for analysingCS by focusing on five key areas. The framework seems

specially useful for this purpose because it considers theperation of the MCS as a whole and because it can be usedith both for-profit and not-for-profit organizations. This

ontrasts with other frameworks, such as value based man-gement frameworks (e.g. Ittner and Larcker, 2001), whichocus only on for-profit entities. Stringer (2007) maintainshat the main strength is the breath of performance issuest includes and its integrated nature. Second, the generalature of the framework enables other frameworks to besed to complement its interpretations and insights, ashown by the Tuomela (2005) and Ferreira (2002) studies.hird, its application has been reported to be straightfor-ard, the areas to be addressed are clear and unambiguous,

nd the questions asked appear meaningful at different lev-ls of management (Ferreira, 2002). Finally, the frameworkacilitates the process of dealing with data, a particularlymportant aspect given the difficulty of dealing with largemounts of information in case-based research (Ferreira,002). Although ‘a way of seeing is a way of not see-

ng’ (Otley, 2008; Poggi, 1965), the framework provides anmmediate degree of insight without imposing any evidentarriers to observing other relevant aspects. In particular,

t encourages an overview of all control mechanisms in useo be taken.

However, there are also a number of weaknesses intley’s framework. Firstly, it does not explicitly consider

he role of vision and mission in MCSs, despite the facthat these may be key elements of the process of controln organizations (Simons, 1995). It is only via key objec-ives that the framework touches this area of the controlystem, although it does not explicitly address the issuesf what mechanisms and processes are used to bring thebjectives to the awareness of employees and managers.econd, the framework can be interpreted as being focusedn what Simons (1995) calls diagnostic control systems,et the importance of considering all four levers of controlor understanding the nature of MCSs has been establishedFerreira, 2002; Henri, 2006; Widener, 2007). Third, theramework does not stress the ways in which account-ng and control information is used by organizations, asgainst the existence of formal control mechanisms. Themportance of MCS use is now a well-established aspect of

he literature (Hopwood, 1972; Otley, 1978; Simons, 1995)nd its omission constitutes a blind spot in the framework.ourth, the framework tends to look at control systemsrom a static perspective, perhaps giving a ‘snapshot’ at aoint in time, but equally ignoring the dynamics of controlting Research 20 (2009) 263–282 265

system change and development. A more explicit consid-eration of the process of change and of its dynamics wouldclearly enrich the study of MCS. Finally, it has also beennoted that the interconnections between different partsof the performance management system are not explicitlyaddressed (Malmi and Granulund, 2005; Stringer, 2007).

2.2. Simons’ (1995) levers of control framework

Simons (1995) proposed the levers of control (LOC)framework as a tool for the implementation and controlof business strategies. According to Simons, the frame-work is an ‘action-oriented theory of control’ (pp. ix) thatresulted from over 10 years of work, including case studiesand related discussions with senior executives and man-agers. Four key concepts are attached to Simons’ LOC: corevalues, risks to be avoided, critical performance variables,and strategic uncertainties. Each of these is directly con-trolled by a particular system or, as designated by Simons,a LOC. Core values are controlled by the beliefs system,which guides the creative process of exploring new oppor-tunities and instils widely shared beliefs (Simons, 1995).Risks to be avoided are controlled by the boundary system,which plays the negative, limiting role of circumscribingthe domain where the company seeks new opportunities(Simons, 1995). Critical performance variables are con-trolled by the diagnostic control system, whose functionis to monitor, assess and reward achievement on key areasof performance (Simons, 1995). Finally, strategic uncertain-ties are controlled by the interactive control system, whoserole is to encourage organizational learning and the pro-cess of development of new ideas and strategies (Simons,1995). Simons argues that a successful implementation ofstrategy requires companies to use all the four levers in anappropriate combination.

This framework provides a usefully broad perspective,yet it is limited by the fact that the same control mech-anism may be part of more than one lever of control(Ferreira, 2002); the difference comes from the empha-sis that is given in the use of the control mechanisms. Forinstance the balanced scorecard has been found to be usedboth diagnostically and interactively (Tuomela, 2005), ashave budgets (Abernethy and Brownell, 1999). Diagnosticuse of MCS follows the mechanistic, repressive, traditionalcontrol approach, while interactive use of MCS takes anorganic, constructive, learning-oriented control approach.Bisbe and Otley (2004) examined the relationship betweeninteractive use of MCS and innovation and found that thedirection of the relationship was contingent upon the levelof innovation in the firm. For high-innovation companies,interactive use of MCS was negatively associated with inno-vation, while in low-innovation companies the analysissuggested the opposite (although not entirely conclu-sively). Henri (2006) found that diagnostic use of MCS had anegative effect on strategic capabilities (i.e. market orienta-tion, entrepreneurship, innovativeness, and organizational

learning) and that interactive use had a positive effect. Thisdistinction between diagnostic and interactive use is there-fore of particular interest in the extended framework.Research has also looked at other levers of control (e.g.Collier, 2005; Ferreira, 2002; Tuomela, 2005; Widener,

t Accoun

266 A. Ferreira, D. Otley / Managemen2007). Collier (2005) used Simons’ LOC framework to studythe interaction between belief and boundary systems andbetween diagnostic and interactive control systems in anentrepreneurial organization. Other research has drawn onthe LOC framework to structure and interpret case study’sevidence regarding MCS issues (Ferreira, 2002; Tuomela,2005). Importantly, Widener (2007) found that evidenceof interdependence and complementarity between all fourLOC and that the full benefit of performance measurementarises when they are used both diagnostically and inter-actively. Consistent with Simons’s (1995, 2000) argument,she also noted that the “result suggests that managers mustconsider all four control systems when designing their con-trol system” (p. 782) to increase its effectiveness and thustranslate it into organizational performance.

Research has identified a number of strengths andweaknesses in Simons’ LOC framework. In terms ofstrengths, it has been pointed out that the frameworkstrongly focuses on strategic issues and on its implicationsfor the control system. It also offers a broad perspectiveof the control system by looking at the range of controlsemployed and how they are used by companies (Ferreira,2002). The association of specific uses to particular controlmechanisms enables a better understanding of the designof the MCS. Importantly, the LOC framework provides atypology for alternative uses of the MCS that is widelyviewed in the literature as meaningful and helpful (e.g.Abernethy and Lillis, 2001; Bisbe et al., 2007; Bisbe andOtley, 2004; Henri, 2006; Widener, 2007). This aspect isparticularly important because the way controls are usedis key to establishing whether all four LOC are employedand to assess the balance (or otherwise) between positiveand negative controls (Ferreira, 2002; Simons, 1995).

In terms of weaknesses, Collier (2005) maintains thatthe LOC framework does not give sufficient emphasisto socio-ideological controls. This is consistent with theobservation that the framework is strongly focussed on thetop level of management and that it does not cope well withthe range of informal controls that exist in organizations,particularly in small ones (Ferreira, 2002) or on the opera-tion of controls at lower hierarchical levels. It is thereforeunlikely that Simons’ LOC framework adequately explainsthe operation of the whole control system, a problem thatbecomes more acute when informal controls are particu-larly important.2 Another weakness is that the meaningsof the concepts embedded in the LOC (e.g. core values) arediffuse, leaving plenty of scope for subjective interpreta-tion (Ferreira, 2002). There is also an important ambiguityin the definition of ‘interactive controls’ which we notelater and suggest that this concept is split into two dis-tinct components: interactive use of controls, and strategicvalidity controls. Finally, the framework is not susceptible

to universal applicability. In some organizations, such assubsidiaries, belief and boundary systems may be largelybeyond the domain of control of the subsidiary (Ferreira,2002). In such instances, only the consideration of the2 Otley’s (1999) framework also does not explicitly address the issue ofinformal controls, but its operational nature and presentation in questionform make the issue less problematic.

ting Research 20 (2009) 263–282

extended organization enables the identification of con-trol mechanisms that match all LOC and, hence, providea comprehensive perspective of the control system.

There are various common features and points ofcontact between Simons’ (1995) and Otley’s (1999) frame-works. Strategy is the key feature that is explicitly commonto both frameworks. However, no doubt Otley’s objec-tives influence and are influenced by beliefs and boundarysystems. They also impact upon both diagnostic andinteractive control systems through the use of perfor-mance measures. The issues of target setting and ofrewards, addressed by Otley independently, are concen-trated essentially on Simons’ diagnostic control systems,while information flows are embedded in all LOC.

3. The performance management systemsframework

Considering the widespread acceptance of the need toadopt a more comprehensive approach to the study of MCS(Chenhall, 2003; Covaleski et al., 2003) that takes researchbeyond specific aspects of control systems (Malmi andBrown, 2008), and the limitations of existing frameworks,we put forward a proposal for an extended framework.The extended framework aims to provide a broad view ofthe key aspects of PMSs and to form the basis upon whichfurther investigations can be developed.

The approach followed has been to extend Otley’s(1999) framework to address the issues outlined above.This was thought appropriate because the framework sug-gests a number of issues to be considered in designingand operating a control system, rather than adopting aprescriptive approach based on an ‘ideal model’. If such amodel exists it is likely to be contingent upon a wide rangeof factors as discussed by contingency research (Chenhall,2003; Otley, 1980). However, no such contingency theoryis developed here; rather the focus of the framework andits extension is to provide a descriptive tool that may beused to amass evidence upon which further analysis can bebased. However, it is believed that the questions proposedprovide a powerful means of relatively quickly outliningthe main features of a PMS in a comprehensive manner, andthe ways in which it is used in the context of a specific orga-nization. The theoretical development of the framework isprovided in the next section, but it also draws upon ourunderstanding of the issues that are associated with PMSs.

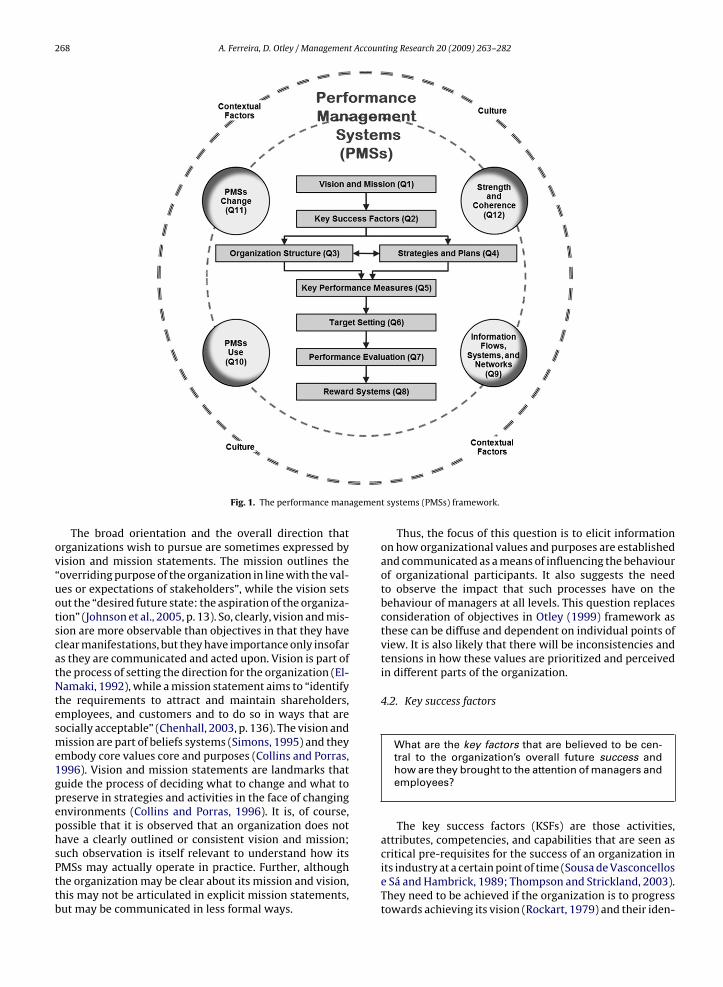

The extended framework, which we name performancemanagement systems framework, represents a progres-sion from Otley’s 5 ‘what’ questions to 10 ‘what’ and 2‘how’ questions. The naming of the framework as ‘perfor-mance management systems’ aims to reflect a shift fromthe traditional compartmentalised approaches to controlin organizations — such as Anthony’s (1965) — to a broaderperspective of the role of control in the managing orga-nizational performance. It also aims to give a managerialemphasis, by integrating various dimensions of manage-

rial activity with the control system. The 12-question PMSsframework is outlined below:1. What is the vision and mission of the organizationand how is this brought to the attention of managers

t Accoun

1

1

1

waitea

A. Ferreira, D. Otley / Managemen

and employees? What mechanisms, processes, andnetworks are used to convey the organization’s over-arching purposes and objectives to its members?

2. What are the key factors that are believed to be centralto the organization’s overall future success and how arethey brought to the attention of managers and employ-ees?

3. What is the organization structure and what impactdoes it have on the design and use of performancemanagement systems (PMSs)? How does it influenceand how is it influenced by the strategic managementprocess?

4. What strategies and plans has the organization adoptedand what are the processes and activities that it hasdecided will be required for it to ensure its success?How are strategies and plans adapted, generated andcommunicated to managers and employees?

5. What are the organization’s key performance measuresderiving from its objectives, key success factors, andstrategies and plans? How are these specified and com-municated and what role do they play in performanceevaluation? Are there significant omissions?

6. What level of performance does the organization needto achieve for each of its key performance measures(identified in the above question), how does it go aboutsetting appropriate performance targets for them, andhow challenging are those performance targets?

7. What processes, if any, does the organization followfor evaluating individual, group, and organizationalperformance? Are performance evaluations primarilyobjective, subjective or mixed and how important areformal and informal information and controls in theseprocesses?

8. What rewards — financial and/or non-financial — willmanagers and other employees gain by achievingperformance targets or other assessed aspects of per-formance (or, conversely, what penalties will theysuffer by failing to achieve them)?

9. What specific information flows — feedback and feed-forward —, systems and networks has the organizationin place to support the operation of its PMSs?

0. What type of use is made of information and of the var-ious control mechanisms in place? Can these uses becharacterised in terms of various typologies in the liter-ature? How do controls and their uses differ at differenthierarchical levels?

1. How have the PMSs altered in the light of the changedynamics of the organization and its environment?Have the changes in PMSs design or use been made in aproactive or reactive manner?

2. How strong and coherent are the links between the com-ponents of PMSs and the ways in which they are used(as denoted by the above 11 questions)?

The above 12 questions form the extended PMSs frame-ork. Although not exhaustive, all the questions listed

bove have been found by the authors to yield significantnsight into the various aspects of PMSs design and use, ando form a coherent framework that can be used to structurenquiry in this field. Although they have an underlying logicnd may therefore at first sight appear to espouse a nor-

ting Research 20 (2009) 263–282 267

mative framework, this is not the case. Rather, they can beused to facilitate the description of PMSs design and use inpractice, without any prior assumption as to whether theexistence or absence of a particular feature is a good or badthing. They are put forward as an heuristic tool to facilitatethe rapid description of significant aspects of PMSs designand operation. The 12 questions are shown schematicallyin Fig. 1.

There are two aspects that permeate the PMSs thatare not explicitly addressed by the above questions. Theseare contextual factors and organizational culture. First, theliterature has shown that variables relating to externalenvironment, strategy, culture, organizational structure,size, technology, and ownership structure have an impacton control systems design and use (e.g. Chow et al., 1999;Firth, 1996; Gordon and Narayanan, 1984; Govindarajan,1988; Khandwalla, 1972, 1974; O’Connor et al., 2004;Perrow, 1967; Simons, 1987). Consequently, the study ofthe operation of the PMSs would require their consider-ation even if only implicitly. Note, however, that strategyand organizational structure are two of these factors thatare already explicitly built into the framework becausethey are significantly influenced by the organization itself.The other factors can be seen primarily as external influ-ences. Second, organizational culture, a notable contextualvariable, pervades the entire control system influencingchoices and behaviours of individuals (Hofstede, 1984;Trompenaars and Hampden-Turner, 1997). So, as with theother external contextual factors, the study and under-standing of the operation of the control system benefitsfrom the consideration of the impact of culture. But we havenot included these factors within the framework as we viewthem more as contingent variables that might explain whycertain patterns of control are more or less effective, ratherthan characteristics of the control system that need to beincorporated into a description.

4. Theoretical development

4.1. Vision and mission

What is the vision and mission of the organizationand how is this brought to the attention of managersand employees? What mechanisms, processes, andnetworks are used to convey the organization’s over-arching purposes and objectives to its members?

Performance management begins with purposes andobjectives. It has been long established that a fundamen-tal requirement for control is the existence of objectives,which are the used to evaluate performance (Otley andBerry, 1980). Organizations have to meet multiple andsometimes competing objectives (Chenhall, 2003), and

these are typically set out by senior managers to meet keystakeholders expectations (Otley, 2008). The corollary ofhaving to satisfy multiple objectives is that performancebecomes a multi-dimensional concept for which no singleoverriding measure is adequate (Otley, 2008).

268 A. Ferreira, D. Otley / Management Accounting Research 20 (2009) 263–282

agemen

Fig. 1. The performance manThe broad orientation and the overall direction thatorganizations wish to pursue are sometimes expressed byvision and mission statements. The mission outlines the“overriding purpose of the organization in line with the val-ues or expectations of stakeholders”, while the vision setsout the “desired future state: the aspiration of the organiza-tion” (Johnson et al., 2005, p. 13). So, clearly, vision and mis-sion are more observable than objectives in that they haveclear manifestations, but they have importance only insofaras they are communicated and acted upon. Vision is part ofthe process of setting the direction for the organization (El-Namaki, 1992), while a mission statement aims to “identifythe requirements to attract and maintain shareholders,employees, and customers and to do so in ways that aresocially acceptable” (Chenhall, 2003, p. 136). The vision andmission are part of beliefs systems (Simons, 1995) and theyembody core values core and purposes (Collins and Porras,1996). Vision and mission statements are landmarks thatguide the process of deciding what to change and what topreserve in strategies and activities in the face of changingenvironments (Collins and Porras, 1996). It is, of course,possible that it is observed that an organization does nothave a clearly outlined or consistent vision and mission;

such observation is itself relevant to understand how itsPMSs may actually operate in practice. Further, althoughthe organization may be clear about its mission and vision,this may not be articulated in explicit mission statements,but may be communicated in less formal ways.t systems (PMSs) framework.

Thus, the focus of this question is to elicit informationon how organizational values and purposes are establishedand communicated as a means of influencing the behaviourof organizational participants. It also suggests the needto observe the impact that such processes have on thebehaviour of managers at all levels. This question replacesconsideration of objectives in Otley (1999) framework asthese can be diffuse and dependent on individual points ofview. It is also likely that there will be inconsistencies andtensions in how these values are prioritized and perceivedin different parts of the organization.

4.2. Key success factors

What are the key factors that are believed to be cen-tral to the organization’s overall future success andhow are they brought to the attention of managers andemployees?

The key success factors (KSFs) are those activities,attributes, competencies, and capabilities that are seen as

critical pre-requisites for the success of an organization inits industry at a certain point of time (Sousa de Vasconcellose Sá and Hambrick, 1989; Thompson and Strickland, 2003).They need to be achieved if the organization is to progresstowards achieving its vision (Rockart, 1979) and their iden-

t Accoun

ts

tshieal2strrvr(cts

4

fbtti(iTioocswptmbpsaabicscflt

comprises both strategic formulation (i.e. the product ofstrategic analysis and strategic choice) and strategic imple-mentation (Langfield-Smith, 2007; Mintzberg et al., 2003;

A. Ferreira, D. Otley / Managemen

ification and monitoring are essential for the fulfilment oftrategic goals (Rangone, 1997).

KSFs are those that are perceived to be important byhe managers concerned, rather than necessarily repre-enting any objective or external point of view. Managers,owever, have been cautioned to “resist the temptation to

nclude factors that have only minor importance” in that anxtensive list of KSFs defeats the purpose of focusing man-gement attention on the items which are “truly critical toong term competitive success” (Thompson and Strickland,003, p. 108). KSFs are a codification of the vision and mis-ion in more concrete terms and in a more compressedimeframe, recognising that control measures need to beeported on a routine basis. For instance, managers mayegard growth of revenue in foreign markets as a KSF for aision of becoming a global market leader, or the transfer-ing of production to countries with lower operating costse.g. China, India) for a vision of leading the industry in lowost. KSFs represent major factors on different timescaleshat would indicate whether the vision and mission is beinguccessfully pursued.

.3. Organization structure

What is the organization structure and what impactdoes it have on the design and use of performancemanagement systems (PMSs)? How does it influenceand how is it influenced by the strategic managementprocess?

The classic view of organizations suggests that they areormed to carry out activities that could be carried outy markets to increase efficiency through the reduction ofransaction costs (Coase, 1937). Organization structures arehen formed as means of establishing formally the spec-fication of individual roles and tasks to be carried outChenhall, 2003) and in doing so, they entrust and empowerndividuals to act within their sphere of responsibility.here are multiple forms of organization structure and theynvolve choices regarding decentralisation/centralisationf authority, differentiation/standardization, and the levelf formalisation of rules and procedures, as well asonfiguration (Johnson et al., 2005). Configuration “con-ists of the structures, processes and relationships throughhich the organization operates” (Johnson et al., 2005,. 396; emphasis added). Structures include the func-ional, the multidivisional, the holding company, the

atrix, the transnational, the team-based, and the projectased. Processes include supervision, planning, and marketrocesses, while relationships refer to internal relation-hips and external relationships — outsourcing, strategiclliances, networks, and virtual organizations (Johnson etl., 2005). Organization structure determines the responsi-ilities and accountabilities of organizational participants;

t equally defines the activities that individuals with spe-

ific roles should not pay attention to. It is then noturprising that these “arrangements influence the effi-iency of work, the motivation of individuals, informationows and control systems and can help shape the future ofhe organization” (Chenhall, 2003, p. 145).ting Research 20 (2009) 263–282 269

Hence, organizational structure is clearly a fundamen-tal control element, and one which has become subject tochange and amendment.3 It is, at a minimum, a constrainton PMSs design and use, and in the longer-term a necessaryissue that requires specific consideration as organizationsgrow and develop. Many control processes operate hori-zontally rather than vertically, although these typically usenon-financial measures. However, the extant control lit-erature seems to concentrate on vertical controls ratherthan those which follow business processes or value chains.Also, organizations are sometimes part of wider networksor alliances that impact upon their control arrangements,and these need to be considered explicitly. Finally controlsare sometimes built into the physical structure or orga-nizational architecture (e.g. production systems; kan-baninventory controls) which might get overlooked by con-ventional approaches to the study of MCSs.

Organization structure decisions are linked to KSFs aswell as to strategic decisions. The identification of KSFsrequires organizations to assess the suitability of the exist-ing structures. For instance, a KSF like “to have the abilityto respond quickly to market conditions” may requirethe organization to embrace decentralisation or to formteam-based structures (structures), to reengineer processes(processes), or to form strategic alliances (relationships), allof which are examples of configuration changes as definedpreviously (Johnson et al., 2005). There is also a relation-ship between organization structure and strategy, but thisappears to be bi-directional. Some research suggests thatstructure needs to be matched to strategy (Chandler, 1962;Chenhall, 2003; Thompson and Strickland, 2003) — e.g.diversification strategies requiring divisional structures —while other research suggests that structure precedes strat-egy to the extent that it limits the scope and the authorityof managers to develop strategies (Donaldson, 1987). Therelationship is likely to be complex, with the balance ofpower leaning towards corporate and perhaps businessstrategy in affecting organization structure, but towardsorganization structure in affecting operating strategy. It isalso likely to be associated with whether the organizationis experiencing an evolutionary or revolutionary stage ofdevelopment (Greiner, 1998), with strategy being likelyto follow structure in an evolutionary stage and structurelikely to follow strategy in a revolutionary stage. This issueis beyond the scope of this study and we maintain thatstrategy and structure are mutually interdependent in thatthey constrain and support each other. This view is con-sistent with Chenhall (2003), who argues that strategy islikely to be implicated in the relationship between MCS andstructure and recommends they be examined together.

However, the question elicits the broader relation-ship between organization structure and the strategicmanagement process. The strategic management process

Pearce and Robinson, 2007). The formulation of strategy is

3 Organizational design initiatives can take the form of restructuring,reengineering and rethinking — Keidel (1994).

t Accoun

270 A. Ferreira, D. Otley / Managemenconcerned with deciding the path to undertake to achievethe organization’s objectives, while the implementationof strategy focuses on ensuring that the strategic choicesare carried through and monitored to ensure they deliverdesired outcomes (Mintzberg et al., 2003). Organizationstructure conditions and is conditioned by the strategicprocess, as it is by the strategy itself.

4.4. Strategies and plans

What strategies and plans has the organizationadopted and what are the processes and activities thatit has decided will be required for it to ensure its suc-cess? How are strategies and plans adapted, generatedand communicated to managers and employees?

Strategy is the direction the organization chooses topursue over the long term as the means of achieving orga-nizational objectives (Johnson et al., 2005; Thompson andStrickland, 2003). The strategy literature argues that theorganization needs to develop the strengths that match itsKSFs (e.g. Ansoff, 1965; Porter, 1980; Sousa de Vasconcellose Sá and Hambrick, 1989) to achieve the desired outcomesit sets for itself. A key element of this entails translat-ing strategic goals into operating goals to attain alignment(Chenhall, 2003; Kaplan and Norton, 1996). Research alsosuggests that a match between the environment, strategy,and internal structures (such as MCS) is associated withhigher performance (Govindarajan, 1988; Govindarajanand Gupta, 1985).

The literature focusing on the relationship betweenstrategy and MCS is now relatively abundant (for a reviewof the literature see Langfield-Smith, 1997, 2007), but itwas not until the 1980s that strategy began to be con-sidered as a contingent variable for MCS design and use(e.g. Daft and Macintosh, 1984; Govindarajan and Gupta,1985; Simons, 1987). Different strategies and plans requirechanges to control configurations (Otley, 1999) to ensurethat the effectiveness of the MCS is achieved. However ourunderstanding of the relationships between strategy andMCS remains limited (Langfield-Smith, 2007; Otley, 1999).

Various strategy typologies have been proposed overthe years. These include Miles and Snow’s (1978) defender,analyser, prospector and reactor strategies, Porter’s (1980)cost leadership and differentiation strategies, Miller andFriesen’s (1982) conservative and entrepreneurial strategy,and Govindarajan and Gupta’s (1985) build, hold, harveststrategies, which were based on the eight types — i.e.aggressive build, gradual build, selective build, aggressivemaintain, selective maintain, competitive harasser, proveviability and divest — proposed by MacMillan (1982). Allthese typologies represent a useful way of looking at aparticular organization’s strategy and a way to reflect onhow they are translated into the PMSs. The observation of

the strategic typology the organization has selected cangive insights into the way it sees itself. But the frame-work deliberately does not specify any particular strategictypology as a preferred basis for analysis, not least becausesome of these typologies are not suitable for use in not-for-ting Research 20 (2009) 263–282

profit organizations. The literature review conducted byLangfield-Smith (2007) provides a sound basis from whichto begin untangling the relationships between strategy andPMSs.

The focus of this question is on the actions that manage-ment have identified as being necessary for the successfuldevelopment of the organization. Thus, the emphasis is onthe actions that are thought likely to achieve outcomes (i.e.relationship between means and ends). It is possible thatwe could observe that an organization has clear goals andobjectives — perhaps expressed through mission and visionstatements — and has identified the appropriate KSFs, buthas not thought through what actions will be necessary toachieve such goals (i.e. a strategic planning failure). Alter-natively, it may have explicitly decided that it will notoperate through a detailed planning process, but adopt amore flexible, adaptive approach to respond to environ-mental uncertainties. That is, forecasting is believed to be sounreliable, that it is thought better not to plan, but to havethe capacity to respond quickly to events as they unfold(e.g. as in agile manufacturing). The literature on beyondbudgeting clearly makes the point that planning has lostmuch of its relevance in today’s highly competitive andchanging environments (Hope and Fraser, 2003a,; Player,2003). Finally, we have included the process of devisingand communicating strategies and plans in this area ofthe PMSs framework. This process can be as important asthe outcome of the strategic planning and thus it warrantsexplicit consideration. Lack of direction is one of the keycontrol problems observed in practice (Merchant and Vander Stede, 2007) and failure to communicate strategies andplans to organizational members may result in a lack ofunderstanding of how individual actions contribute to theoverall strategy. Thus, the stance taken is that of commu-nicating intended strategies, not of developing emergentstrategies. The issue of emergent strategies (Mintzberg,1978) will be dealt with in question ten, which focuses onhow the use of the PMSs may support strategy formation.

The question also elicits the nature of strategic man-agement process by asking how strategies and plans aregenerated and communicated to managers and employees.The process can follow the traditional top-down approach— where top managers undertake the strategic thinking,decision-making, planning, and then communicate it tothe wider organization — or it can follow a bottom-upapproach — where there is involvement of all levels ofmanagement in the strategic process. Empowerment hasbecome more important with the rise of the ‘lean’, ‘de-layered’, horizontal organizations, in place of hierarchicaland vertical organizations (Otley, 1994). Although there arestrong advocates for the top-down approach to strategicchange (Kotter, 1995), research shows that top managersfind it difficult to control how such change is understoodby middle managers and that, as a consequence, they oughtto place greater emphasis on the adaptation of emergentstrategies (Balogun and Johnson, 2004). It appears clear

that a wider involvement of lower echelons of managementin the strategic management process is likely to result ingreater understanding the strategic intent, acceptance ofthe path to be undertaken and, importantly, provide forbroader organizational alignment.

t Accoun

spwi

4

fioteiimsrtseswd

mgptaatommfsiaoswS

tam

m

S

A. Ferreira, D. Otley / Managemen

Compared to Otley’s (1999) framework, this questionhows two differences. The issue of how strategies andlans are generated and communicated has been added,hile the issue of performance measures has been explic-

tly separated and further elaborated in the next question.

.5. Key performance measures

What are the organization’s key performance mea-sures deriving from its objectives, key success factors,and strategies and plans? How are these specified andcommunicated and what role do they play in perfor-mance evaluation? Are there significant omissions?

Key performance measures are the financial or non-nancial measures (metrics) used at different levels inrganizations to evaluate success in achieving their objec-ives, KSFs, strategies and plans, and thus satisfying thexpectations of different stakeholders.4 They are explic-tly identified in the PMSs framework to reflect both themportance that is attached to performance measures in

ost contemporary organizations and the influence thatuch measures have on individual behaviour. This questionelates to Simons’ (1995) critical performance variables;hat is, those measures that are directly linked with theuccess of the organization. However, the question alsoncompasses Simons’ (1995) ‘interactive’ use of controlystems to the extent that it refers to those measures onhich senior managers focus their attention and use torive subordinate behaviour.5

The question is explicit about whether performanceeasures are derived from objectives, KSFs, and strate-

ies and plans to the extent that identification of suitableerformance measures is part of the strategic implemen-ation process (Johnson et al., 2005) and indicative of thelignment between operations and strategy. This idea oflignment is consistent with Chenhall (2005), who referso the links between operations and strategy and goals asne of the features of integrative strategic performanceeasurement systems. Furthermore, Ittner and Larckeraintain that “the choice of performance measures is a

unction of the organization’s competitive environment,trategy, and organizational design” (2001, p. 379). Theres evidence that alignment between performance measuresnd strategy affect performance; in particular, the pairingf quality-based manufacturing strategies with the exten-ive use of subjective non-financial performance measuresas found to have a positive performance effect (Van der

tede et al., 2006).Care needs to be taken both to observe the measures

hat are actually in use and also areas where measuresre absent or limited in scope. It is a truism that what iseasured tends to drive out what is not measured and so

4 Key performance measures are sometimes referred to as key perfor-ance indicators or simply KPIs.5 We will develop the idea of how performance measures are used in

ection 4.10.

ting Research 20 (2009) 263–282 271

omissions may be as influential as measures in use. Fur-ther, the number of such ‘key’ measures is also of relevance,as managers’ limited attention span means that the useof many performance measures reduces their impact. Forinstance, the proponents of the balanced scorecard addressthis issue by recommending a maximum of 25 performancemeasures in total (Kaplan and Norton, 1996). The articu-lation of measures between organizational levels is also ofinterest, especially as non-financial performance measuresmay well have to be different at different organizationallevels. Similarly, the explicit development of causal rela-tionships between measures in some form of causal model(such as ‘strategy maps’ (Kaplan and Norton, 2000, 2004))also provides evidence of how an organization views itsperformance measures.

4.6. Target setting

What level of performance does the organization needto achieve for each of its key performance measures(identified in the above question), how does it go aboutsetting appropriate performance targets for them, andhow challenging are those performance targets?

Target setting is a critical aspect of performance man-agement (Ittner and Larcker, 2001; Otley, 1999; Stringer,2007). It should then be no surprise that the issue of set-ting targets and using them for evaluating and rewardingperformance has been the subject of discussion in the liter-ature and is likely to continue to receive attention in yearsto come (Covaleski et al., 2003). However, Stringer (2007)notes that field research has failed to provide an in-depthanalysis of these issues, particularly in regard to the rela-tionship between target setting and other aspects of thePMS.

This question, which has been left unchanged fromthe original Otley’s (1999) framework, reflects the univer-sal tension between what is desired and what is thoughtto be feasible in determining targets for all aspects oforganizational performance. The process of target setting(e.g. imposition, consultation, participation) may be asimportant as the outcome (e.g. perceived target difficulty)(Emmanuel et al., 1990). The literature on budgetary con-trol provides a good guide to the major issues involved(e.g. Libby, 2001; Shields and Shields, 1998), and it is alsoapplicable to a wider set of non-financial targets, as evi-denced in balanced scorecard implementations. Researchhas found that target levels have effects on performance,with moderately difficult goals enhancing group perfor-mance (Fisher et al., 2003), with evidence that, in practice,targets tend to be 80 to 90 per cent achievable and thisis regarded as desirable (Merchant and Manzoni, 1989).Aggressive target setting in situations where there isneed for cooperation between units is not associated with

higher performance (Chan, 1998), as managers become lesswilling to make concessions and take longer to reach agree-ments (Smith et al., 1982). However, the embedding ofcontinuous improvement into targets appears increasinglyinescapable, as companies face competitive and globalised

t Accoun

272 A. Ferreira, D. Otley / Managemenmarkets (Chenhall, 2003). Also, the use of benchmarking(Elnathan et al., 1996; Spendolini, 1992), particularly theuse of external benchmarks, appears to provide a greaterdegree of legitimacy for targets, as shown by their use in thehealth sector (Northcott and Llewellyn, 2003), and has beenstrongly advocated by the beyond budgeting movement(Hope and Fraser, 2003b).

4.7. Performance evaluation

What processes, if any, does the organization followfor evaluating individual, group, and organizationalperformance? Are performance evaluations primarilyobjective, subjective or mixed and how important areformal and informal information and controls in theseprocesses?

The area of performance evaluation represents a criti-cal nexus in control activities. Managers tend to be mostaffected by areas that senior managers signal as important,with success in these areas potentially determining statusand progression in the organization. Thus both formal per-formance evaluation activities and informal indications ofwhat is felt to be important are both covered in this ques-tion. It is particularly important to distinguish betweenperformance evaluation routines (often orchestrated bythe human resources function) and those actually operatedby senior managers. Again, this is an area where subordi-nates’ perceptions of what is believed to be the situationare even more important than the formal situation, withresearch showing that trust between the parties plays amajor role (Gibbs et al., 2004). It is important to note thatthis question is not concerned exclusively with individ-ual performance evaluations, even though they are likelyto be the most observable. It also includes the evaluationof the performance of various groups of individuals (e.g.teams, departments, and divisions) and, more generally,the organization as a whole. Research shows that per-formance evaluations of business units that use balancedscorecards place greater emphasis on common measuresthan on unique measures (Banker et al., 2004; Lipe andSalterio, 2000) and that they are influenced by strategi-cally linked measures only to the extent that business unitstrategies are communicated in detail to evaluators (Bankeret al., 2004). Research has also found that managers who areevaluated on the basis of company profits achieve higherjoint outcomes when following a team orientation than anindividualistic orientation (Schulz and Pruitt, 1978). Thereis also research that shows that cooperation and integrativeproblem solving among executives occurs more frequentlywhen performance evaluations focus on corporate prof-its rather than on divisional profits (Ackelsberg and Yukl,1979).

Performance evaluations can be objective, subjective,

or fall in-between these two extremes. Under subjectiveperformance evaluations, the specific weightings placedon the various dimensions of performance are unknownto the evaluee and determined subjectively by the evalu-ator. However, the evaluator may make these weightingsting Research 20 (2009) 263–282

more explicit by flagging which aspects are more impor-tant. The use of subjective evaluations has the importantadvantage of enabling evaluators to correct for identifiableflaws in performance measurement (Gibbs et al., 2004), butthey also come at the cost of expensive managerial timeand perceptions of bias. The use of subjective performanceevaluations in conjunction with the balanced scorecard hasattracted criticism for permitting favouritism and for cre-ating uncertainty about evaluation criteria (Ittner et al.,2003). Other research on the use of subjective evaluationshas found them to be positively related to the level ofspending on training, the severity of the consequences ofmissing targets, the extent of interdependency betweensubunits, and increased pay satisfaction and productivity(Gibbs et al., 2004). In contrast, under objective perfor-mance evaluation there is no scope for ambiguity in theweightings; assessment is based only on the actual resultsand, typically, they do not allow for adjustments to theagreed standards of performance nor to their weightings.Therefore, objective, formulaic performance evaluationsare likely to be acceptable in situations where the input-output relationship is clear, the performance is controllableor, when it is accepted as part of institutionalised prac-tice. Further, the whole area of ‘gaming’ behaviour (Argyris,1952; Hofstede, 1968) and the degree to which it is stimu-lated by different patterns of use of performance measuresis covered by this question.

Relative performance evaluations (RPEs) are a practicethat is attracting increased attention. They reflect instanceswhere the performance of an individual or entity is mea-sured in relation to that of another (Dye, 1992) in anattempt to eliminate distortions caused by uncontrollablefactors. RPEs have also been hailed as a solution to the ‘fixedperformance contract’ problem (Hope and Fraser, 2003b).However, there is little evidence to suggest that RPEs areeffective, even though the underlying principle is appealing(see Hansen et al. (2003) for a useful review of the ‘BeyondBudgeting’ approach). Dye (1992) shows that the benefitsof RPEs are a positive function of the number of projectsthat executives have available to them, while Aggarwaland Samwick (1999) conclude that the high administra-tive costs of RPEs are likely to explain their low adoption inexecutive contracts. To the best of our knowledge there isno evidence in the literature of the use and effectiveness ofRPEs at lower levels of management, although there is evi-dence that the introduction of RPEs in the health care in theUK has been highly problematic (Northcott and Llewellyn,2003).

4.8. Reward systems

What rewards — financial and/or non-financial — willmanagers and other employees gain by achievingperformance targets or other assessed aspects of per-formance (or, conversely, what penalties will they

suffer by failing to achieve them)?Rewards are typically the outcome of performance eval-uations and as such reward systems are the next logical

t Accoun

acolsTwio(ibtaftopeo(ltoro

ffitgtbgipiarqpebopasotdh

cpm(msrfe

A. Ferreira, D. Otley / Managemen

spect to consider in the analysis of PMSs. Rewards areonsidered broadly here and may range from expressionsf approval and recognition by senior management (orack of criticism), through financial rewards (bonuses andalary increases) to long-term progression and promotion.his question is carried over from Otley’s (1999) frame-ork, but now making explicit the fact that rewards can

nclude both financial and non-financial elements. It alsopens up the issue of the distinction between positivei.e. rewarded) and negative (i.e. penalised) control activ-ties, which were hinted at in Simons’ (1995) distinctionetween beliefs and boundary systems (i.e. those thingshat should be done versus those things which should bevoided). The area of non-financial rewards is worthy ofurther elaboration as it may often include quite subtle atti-udes and behaviours of superiors. Thus informal praiser criticism and general attitudes about a subordinate’srogress within the organization can significantly influ-nce the subordinates’ behaviour and thus the workingsf the PMSs. Issues of equity, fairness and inclusivenessHope and Fraser, 2003b) between different managers alsooom large in many organizations. The issues covered byhis question relate strongly to the processes and structuresf accountability (Merchant and Otley, 2007) and corpo-ate governance more generally, that are now the subjectf widespread interest in the literature.

The relationship between rewards, motivation and per-ormance is complex, perhaps more so than it appears atrst sight. It has been long recognised that reward sys-ems are used to motivate individuals to align their ownoals with those of the organization (Hopwood, 1972) andhat desired behaviours that are not rewarded tend toe neglected (Kerr, 1975). Some research, however, sug-ests that extrinsic motivation (i.e. rewards) underminesntrinsic motivation (Deci et al., 1999), but this has been dis-uted by other studies (e.g. Jenkins et al., 1998). Financial

ncentives do not necessarily translate into performances shown by Jenkins et al. (1998), who suggests a positiveelationship between financial incentives and performanceuantity (e.g. number of tasks completed), but not witherformance quality (e.g. supervisor ratings). Additionalvidence in support of a positive relationship was providedy Bonner et al. (2000), but this was only observed in halff the studies they reviewed. They also found that thisositive effect decreased as tasks became more complexnd that the relationship differed across types of incentivechemes. The effect of monetary incentives on performanceccurs when individuals possess the necessary skills, buthe increased effort generated by the monetary incentivesoes not flow through to performance when they do notave such skills (Bonner and Sprinkle, 2002).

Bonner and Sprinkle (2002) provide a theoreti-al framework to examine the relationship betweenerformance-contingent incentives, effort and perfor-ance. In particular, they examined how person variables

e.g. skills), task variables (e.g. task complexity), environ-

ental variables (e.g. assigned goals), and the incentivecheme (e.g. the rewarded dimension) intervened in theelationship between monetary incentives, effort and per-ormance. Bonner and Sprinkle found that the combinedffect of target setting and monetary incentives on per-

ting Research 20 (2009) 263–282 273

formance exceeded that of monetary incentives alone.However, they concluded that there are many unansweredimportant questions and that strong recommendationswere unwarranted.

Group reward practices have attracted increased atten-tion from both academia and practice in recent years. Suchrewards are based on collective achievement and comeunder many guises, including profit-sharing schemes,team-based incentive schemes, and gain-sharing plans.The use of group rewards faces a number of challenges,including the potential for free riders, for individuals tosee themselves as detached from the group and for a lackof equity. Furthermore, there is the difficulty of relatingindividual performance and group performance. Notwith-standing these challenges, group rewards can create anownership culture and research suggests that they areoften effective (Merchant and Van der Stede, 2007; Rosenet al., 2005). In fact, group rewards have been stronglyendorsed by some researchers due to the difficulty of iden-tifying the marginal contribution of individuals to overallperformance, and when organizations are viewed as “acomplex network of interdependent relationships” (Hopeand Fraser, 2003b, p. 107).

4.9. Information flows, systems and networks

What specific information flows — feedback and feed-forward —, systems and networks has the organizationin place to support the operation of its PMSs?

Information flows, systems and networks are essentialenabling mechanisms to any performance managementsystem (Otley, 1999); they are the binding agent that keepsthe whole system together. They act like the nervous sys-tem in the human body, transmitting information fromthe extremities to the centre and from the centre to theextremities. The question notes the difference betweenfeedback information — that is, information used to enablethe undertaking of corrective and/or adaptive courses ofaction — and feed-forward information — that is, infor-mation used to enable the organization to learn from itsexperience, to generate new ideas and to recreate strategiesand plans. In other words, it distinguishes between infor-mation flows aimed at the correction of past shortcomingsfrom those which attempt to anticipate future events andrespond in advance of their occurrence. This question rep-resents an extended version of the final question in Otley’s(1999) framework.

Feedback and feed-forward information flows areomnipresent in contemporary organizations (Otley, 1999)and they are directly related to the notions of singleloop and double loop learning (Argyris and Schön, 1974,1978). Single loop learning entails a response to a signal

of deviance from a pre-defined course of action that doesnot question the initial objectives or strategies; it sees thedeviance as the product of a deficient operationalisation(Argyris and Schön, 1978). Hence, its association with theubiquitous feedback information flows. In contrast, double

t Accoun

274 A. Ferreira, D. Otley / Managemenloop learning “involves questioning the role of the fram-ing and learning systems which underlie actual goals andstrategies” (Usher and Bryant, 1989, p. 87) and hence theirassociation with feed-forward information flows.

Systems are used to organize accounting and other con-trol information. They are part of the information system(IS) and information technology (IT) infrastructure thatpervade contemporary organizations. Enterprise ResourcePlanning (ERP) systems, for example, are not accountingsystems in the strict sense of the word, but they are inter-dependent with accounting and other control processes(Chapman, 2005). They provide a platform for account-ing and control information to flow, but they may alsocreate impediments to the design and implementation ofcontrol systems (Granlund and Mouritsen, 2003). It alsoneeds to be recognised that the well-developed and reli-able systems that are generally in place to provide financialinformation do not necessarily exist in such robust form fornon-financial information. The quality of the non-financialinformation needs to be assessed, particularly in regardto its vulnerability to manipulation and misreporting. Therelationship between accounting and IT is one of interde-pendence and mutuality, with accounting needing IT forboth reporting and performance management purposes,and IT needing accounting to justify its existence (Dechowet al., 2007).

How performance and control information is structuredis another key issue to be considered. In many organiza-tions, performance management processes revolve aroundbudgeting systems, however, increasingly organizationsare moving towards broader PMSs, such as balanced score-cards. Other operating systems, such as production, qualitycontrol, logistics systems, and customer-relationship sys-tems may be part of the overall package of systems inuse. There are also a number of additional issues to beconsidered that are related to the characteristics of theinformation flows in the PMSs. These includes issues suchas information scope (i.e. narrow scope or broad scope),timeliness (i.e. frequency and speed of reporting), aggrega-tion (i.e. by period and by functional areas), and integration(i.e. inter-relationships and interactions between subunits)(Chenhall and Morris, 1986). They also include issues suchas the level of detail, relevance, selectivity, and orientation(Amigoni, 1978).

Networks represent another layer in the IT/IS infras-tructure. Many organizations have organized their systemsin networks that are made available to various partieswithin the organization. However, information networksgo beyond formal mechanisms. Informal networks of indi-viduals can also play a key role in the dissemination of

information within the organization. This is something thatwill be shaped by and shape the prevailing organizationalculture.66 Organizational culture is not explicitly discussed in this paper,although it may be seen as implicit in the prior discussion of mission andvision. It is seen more as a contingent variable that may influence PMSdesign rather than an organizational characteristic that can be manip-ulated. However, it is recognized that culture can have both of theseattributes, and it may be a highly influential feature of PMSs use as dis-cussed in the next section.

ting Research 20 (2009) 263–282

4.10. PMSs use

What type of use is made of information and of the var-ious control mechanisms in place? Can these uses becharacterised in terms of various typologies in the liter-ature? How do controls and their uses differ at differenthierarchical levels?

The use made of information and controls is a corner-stone of the PMSs. Case study evidence suggests that theuse of control information can be more significant than theformal design of the control system (Ferreira, 2002). It israther surprising that this was omitted from Otley’s (1999)framework, given the work he conducted on the effects ofdifferent uses of control information and also by other stud-ies in the area (Govidarajan, 1984; Hopwood, 1972; Otley,1978). Nevertheless, the concept of ‘use’ has not been well-developed in the literature. Apart from Hopwood’s (1972)categories — now often discussed in terms of ‘rigid’ and‘flexible’ use — perhaps the only substantial contribution isthat made by Simons (1995) in terms of his four LOC, and hisconcept of interactive use. Even this has been inadequatelymeasured in subsequent studies for, as Bisbe et al. (2007)argue, interactive control as defined by Simons can be seenas a composite of five different sub-areas — intensive useby senior managers, intensive use by operating managers,pervasiveness of face-to-face challenge and debate, focuson strategic uncertainties and a non-invasive, facilitatingand supportive involvement — each of which need to existfor control to be described as interactive (in their view). Weargue that Simons conflates the intensive use of informa-tion by managers with the identification of an inadequatestrategy. Both of these are key issues, but it seems confusingto link them together in the overall concept of ‘interactiveuse’. There is considerable scope for the development andoperationalisation of the concept of use, and for researchto ascertain the effects of different types of use of controlsystems.

Simons’ (1995) concepts of diagnostic and interactiveuse have substantial commonalities with other conceptsfound in the literature. For instance, the feedback informa-tion flows are fundamental to diagnostic use as they enablesingle loop learning, while feed-forward information, withits double loop function (Argyris and Schön, 1978), can pro-vide a check for strategic validity. The alignment betweenstrategic intent and strategic action is unlikely to persist indynamic environments and strategic dissonance will thenresult (Burgelman and Grove, 1996). Dissonance becomesstrategic at key moments typified by “the giving way of onetype of industry dynamics to another; the change of onewinning strategy into another; the replacement of an exist-ing technological regime by a new one” (Burgelman andGrove, 1996, p. 10). The role of strategic validity controlsis to signal the need to review strategies, and such revi-

sions can be facilitated by frank, open discussions betweendifferent managers and other employees (Burgelman andGrove, 1996). The use of strategic validity controls shouldnot be confused with the interactive use of other con-trols. Both diagnostic and interactive use of control systems

t Accoun

aHmo(

ipthpseatvttidcmBPctmFLttwoaw

4

ecttunt(ait

oA

A. Ferreira, D. Otley / Managemen

re key components of organizational learning processes.owever, it is the use of strategic validity controls that pri-arily serves the important role of identifying the failure

f intended strategies and the rise of emergent strategiesMintzberg, 1978).

Broadbent and Laughlin (2007)7 have built upon thedea of ‘transactional’ and ‘relational’ uses of PMSs, and thisrovides an additional dimension of ‘use’ at an organiza-ional level of analysis. Transactional use of a PMS “has aigh level of specification of ends to achieve (e.g. througherformance measures, targets etc.) as well often a clearpecification of the means needed to achieve these definednds”, whereas relational use of a PMS “can be less specificbout the ends to achieve and the means to achieve them ifhis is the view of the stakeholders designers but could beery precise if they so chose” (2007, pp. 25–26). Transac-ional and relational uses are the extremes of a continuumhat represent ideal constructions which do not necessar-ly translate neatly into practice, but they are analyticallyistinct to the extent that they represent the domains ofultural elements of instrumental rationality and of com-unicative rationality (Broadbent and Laughlin, 2007).

roadbent and Laughlin maintain that “context affects theMS functional questions and the financial transfers, yetulture expressed through communicative and instrumen-al rationalities, has an even more direct and ultimately

ore significant effect on the PMS design” (2007, p. 25).rom the perspective of our framework, Broadbent andaughlin’s work is valuable as it emphasizes an organiza-ional level of analysis of the concept of ‘use’ to complementhe typically individual level of analysis found in earlierork. That is, relational and transactional usage typifies the

verall ‘use’ made of a range of control mechanisms acrosswhole organization, or by one organization in its dealingsith others.

.11. PMSs change

How have the PMSs altered in the light of the changedynamics of the organization and its environment?Have the changes in PMSs design or use been madein a proactive or reactive manner?

Change and its dynamics have been included into thextended framework. Environments change, organizationshange, and so PMSs also need to change in order to sus-ain their relevance and usefulness. The idea of change inhe PMSs applies to both the design infrastructure thatnderpins the PMSs (e.g. the management control tech-iques and the key performance measures used) and alsoo the way performance management information is used

e.g. the aspects which are emphasized and those whichre not). However, the issue is not the process of changetself, but rather the extent and type of change that hasaken place in the PMSs design and use as a response to7 Note that this reference is to a working paper which has been devel-ped into the article that also appears in this issue of Managementccounting Research; see Broadbent and Laughlin (2009).

ting Research 20 (2009) 263–282 275

or in anticipation of changes in the organization and itsenvironment. In other words, the question draws the atten-tion to the antecedents (i.e. the causes) and consequences(i.e. the outcomes) of change in the PMSs, leaving issuesof process aside. For instance, the observer may ask whyperformance measures were introduced or removed fromthe PMSs and examine the economic and/or behaviouralimplications of those decisions, rather than dwelling onthe detail of change processes. There is also the commonsituation where organizations are working towards theimplementation of a change to rectify a known problem,but the timescale of change is often extended due to the(computer and other) systems changes which are required.

This is an area of major importance as the rate of changeincreases. The incorporation of change dynamics into theanalysis of PMSs design adds to our understanding of howdifferent PMSs components interrelate with each other. Inparticular, it draws attention to the issue of lags in PMSsdesign which can result in an extant system appearing inco-herent. These PMSs change issues clearly link to the widerarea of management accounting change more generally(e.g. Baines and Langfield-Smith, 2003; Burns and Scapens,2000; Burns and Vaivio, 2001; Busco et al., 2007; Dambrinet al., 2007; Lukka, 2007; Scapens and Jazayeri, 2003).

It is also important to consider the scope of strategicchange in the increasingly competitive environment facedby contemporary organizations. Strategies are a core com-ponent of a PMS and a strategic change can be expectedto send ripples across the entire PMSs. Thus, the extentto which strategies have changed is an issue of interestfor understanding the functioning of the PMSs. Chenhall(2003) recognises this when he states that our understand-ing of how MCSs are involved in strategic change is limitedand later provided, in his work with Euske, a range ofrelated theoretical perspectives to assist the developmentof knowledge in this area (Chenhall and Euske, 2007).

4.12. Strength and coherence

How strong and coherent are the links between thecomponents of PMSs and the ways in which they areused (as denoted by the above 11 questions)?

The strength and coherence of the links within a PMSis crucial to understanding its operation and therefore anarea that needs to be considered in the extended frame-work. Like any other system, a PMS is greater than thesum of its parts and there is a need for alignment andcoordination between the different components for thewhole to deliver efficient and effective outcomes. Althoughthe individual components of the PMSs may be appar-ently well-designed, evidence suggests that when theydo not fit well together (either in design or use) controlfailures can occur (Ferreira, 2002). The theoretical devel-

opment provided in the eleven preceding questions of thePMSs framework makes clear the key links between itscomponents and, thus provides a good starting point forquestioning, critical analysis and assessment of the bal-ance, harmony, consistency and coherence of the links in

t Accoun

276 A. Ferreira, D. Otley / Managementhe whole PMSs package. However, it is important to stressthat there are no deterministic rules here; the componentsof PMSs combine with each other and their interactionshave effects on organizational outcomes (Abernethy andBrownell, 1997).

Chenhall (2003) provides hints as to what to look forwhen examining the strength and coherence of the PMSs.He suggests that judgements should be made about theextent to which the control system “consider(s) multi-ple stakeholders; measure(s) efficiency, effectiveness andequity; capture(s) financial and non-financial outcomes;provide(s) vertical links between strategy and operationsand horizontal links across the value chain; provide(s)information on how the organization relates to its exter-nal environment and its ability to adapt” (p. 136). A keyissue to be considered here is the extent to which key per-formance measures link back to strategies (Van der Stede etal., 2006), and how strategies link back to key success fac-tors and to the over-arching objectives of the organization.In studying PMSs’ operation at different hierarchical levelsthere is also the potential to observe mismatches, perhapscaused by changes being made at one level that have yet tobe carried through to other levels.