Embed Size (px)

Citation preview

1/47

An E3 Econometric Analysis of CDM and Technology Transfer between Japan

and China

Mitsuo YAMADA

ECS/IIASA, Schlossplatz 1, A-2361 Laxenburg, Austria(Chukyo Univ., Nagoya, Japan)

[email protected]@mecl.chukyo-u.ac.jp

International Energy Workshop 2005, Kyoto, Japan, July 5 2005

2/47

Contents

1 Introduction

2 Methodology

3 Features of the model

4 Some simulation results

5 Concluding remarks

4/47

1.2China

0

200

400

600

800

1000

1200

1400

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

Bil. U

S$

in 2

000

mar

ket

pric

es

- 2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

%

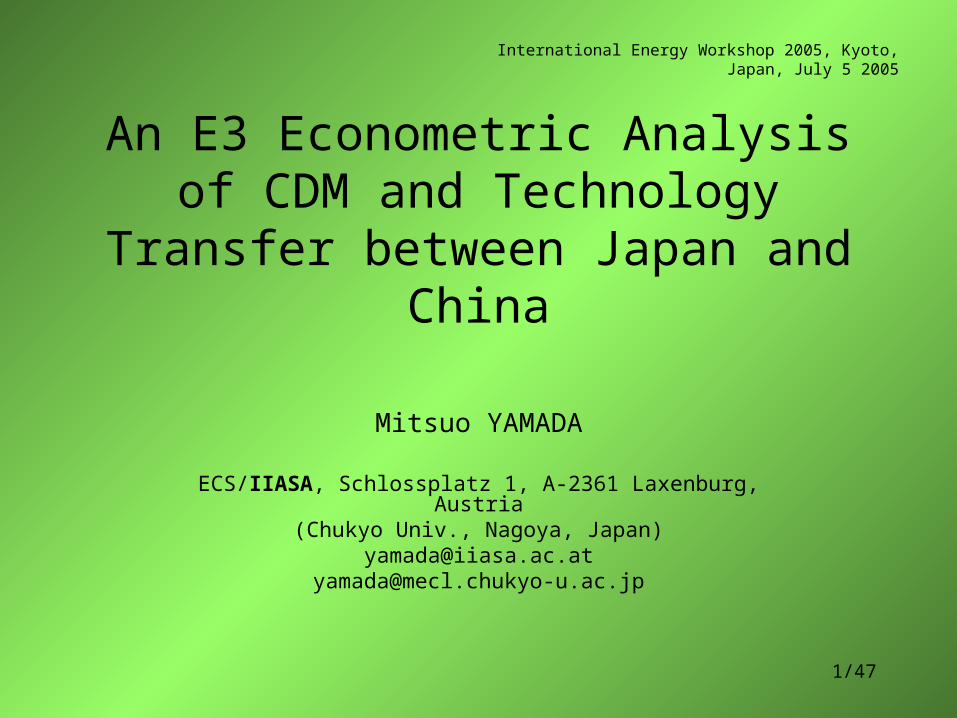

GDP Grwoth Rate av=9.3 av=9.4

J apan

0

1000

2000

3000

4000

5000

6000

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

Bil. U

S$

in 2

000

mar

ket

pric

es

- 2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

%

GDP Grwoth Rate av=4.0 av=1.2

Figure 1: GDP and its Growth in China and Japan

5/47

China

0

200000

400000

600000

800000

1000000

1200000

1400000

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

ktoe

0

500

1000

1500

2000

2500

3000

3500

4000

ktoe

/Bil.$

in 2

000

mar

ket

pric

es

Primary Energy Supply Energy Intensity to GDP

J apan

0

200000

400000

600000

800000

1000000

1200000

1400000

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

ktoe

0

500

1000

1500

2000

2500

3000

3500

4000

ktoe

/Bil.$

in 2

000

mar

ket

pric

es

Primary Energy Supply Energy Intensity to GDP

Figure 2: Primary Energy Supply and Energy Intensity of GDP in China and Japan

6/47

Figure 3: Total CO2 Emissions and Carbon Intensity of PES in China and Japan

0.8-0.5

2.90.1

China

0

500

1000

1500

2000

2500

3000

3500

4000

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

Mt-

CO

2

2.0

2.1

2.2

2.3

2.4

2.5

2.6

2.7

2.8

2.9

3.0

Mt-

CO

2/M

toe

CO2 CO2 PES ratio

J apan

0

500

1000

1500

2000

2500

3000

3500

4000

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

Mt-

CO

2

2.0

2.1

2.2

2.3

2.4

2.5

2.6

2.7

2.8

2.9

3.0

Mt-

CO

2/M

toe

CO2 CO2 PES ratio

7/47

GDPGDP

energy

energy

COCO

2

2Kaya Identity:

• High growth requires faster improvement in energy efficiency.

Figure 4: Simple Prediction

CO2Emission

CarbonIntensityof PES

EnergyIntensityof GDP

GDPgrowth Others

J apan 1990-2002 0.76 -0.47 0.08 1.16 -0.012002- 1.50 -0.50 0.00 2.00

China 1990-2002 2.91 0.09 -6.02 9.41 -0.57(1)2002- 4.50 -0.50 -4.00 9.00(2)2002- 2.50 -0.50 -6.00 9.00

0

2000

4000

6000

8000

10000

12000

14000

2000

2003

2006

2009

2012

2015

2018

2021

2024

2027

2030

Mt-

CO

2 J apanChina(1)China(2)

8/47

Issues for China

• What sector improved in energy efficiency?– Final consumption of energy for Industry, Transport, and

Residential/Commercial• Change in the industrial structure• Diffusion of energy-efficient commodities

– Electricity Generation Sector• Fuel shift from coal to natural gas• Fuel efficiency improvement

• How attained?– Clean Development Mechanism (CDM)– Government-based cooperative activities– Technology transfer through Foreign Direct Investment (FDI)

9/47

Figure 5: Emissions of Greenhouse Gases in Japan

1000.0

1050.0

1100.0

1150.0

1200.0

1250.0

1300.0

1350.0

1400.0Kyo

to P

roto

col

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2010

Tar

get

2010

Tar

get

Mil.Ton

CO

2

SF6PFCsHFCsN2OCH4CO2

Economic Growth& CurrentMeasures

New MeasuresRequired

KyotoMechanism& Sink

11/47

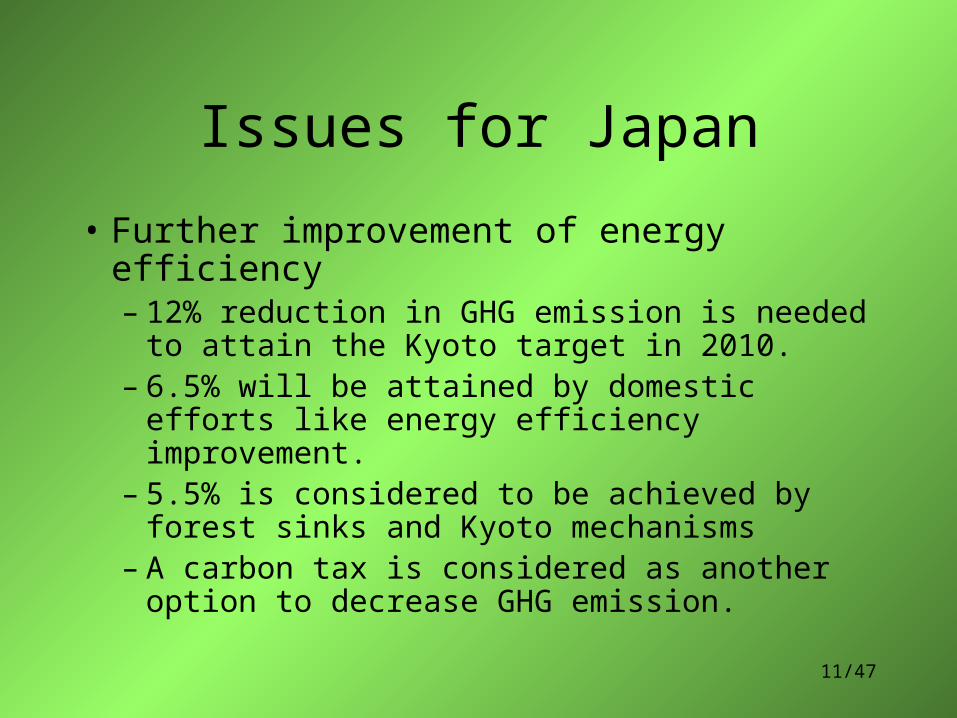

Issues for Japan

• Further improvement of energy efficiency– 12% reduction in GHG emission is needed to

attain the Kyoto target in 2010.– 6.5% will be attained by domestic efforts like

energy efficiency improvement.– 5.5% is considered to be achieved by forest

sinks and Kyoto mechanisms– A carbon tax is considered as another option to

decrease GHG emission.

14/47

• ZhongXiang Zhang (2004) investigates the role of China under the Kyoto Protocol, using marginal abatement cost functions. – Broadening the scope of the market of tradable permits from no emissions

trading to full global trading, it is found that the gain of the OECD as a whole increases as the market expands.

– The developing countries also benefit from such an expansion (through financing and emission reduction).

– Inclusion of China in the emission trading framework increases the total supply of emission permits, so decrease the price of the emission permits.

– China is expected to emerge as the dominant host country of CDM projects.

– According to his study, the US and Japan are required higher emission reductions than the EU, so the gains of the two countries depend on the expansion of the emission permits trading market.

• This study shows the importance of China in the global trading market of CO2 emission permits.

• China is expected the dominant host country of the CDM projects, and Japan is also recognized as one of the important potential investing countries for the CDM projects.

• We will focus on the international cooperation between China and Japan through the CDM projects for the challenging reduction of GHG emissions, using an E3 econometric model.

15/47

3 Features of the Model

• Our model( KeYMERIT-E3 ) consists of – two sub-models, one for Japan and China each, and a

sub-model of international trade.– Each country’s sub-model is developed as an E3 multi-

sectoral model, which integrates a macro model and an input-output model into one model, including energy and environment parts.

– There are 21 sectors in each country’s model» KeYMERIT-E3: Kinoshita-Yamada Multi-sectoral and

Multi-regional Econometric Model for the Research on Industry and Trade – E3 version

16/47

Figure 6: The structure of the Model: KeYMERIT-E3

Japan China

International Trade

The US EU15 Other DC ROW

ASEANHK & Taipei

macro

sector

energy

CO2

macro

sector

energy

CO2

Korea

25/47

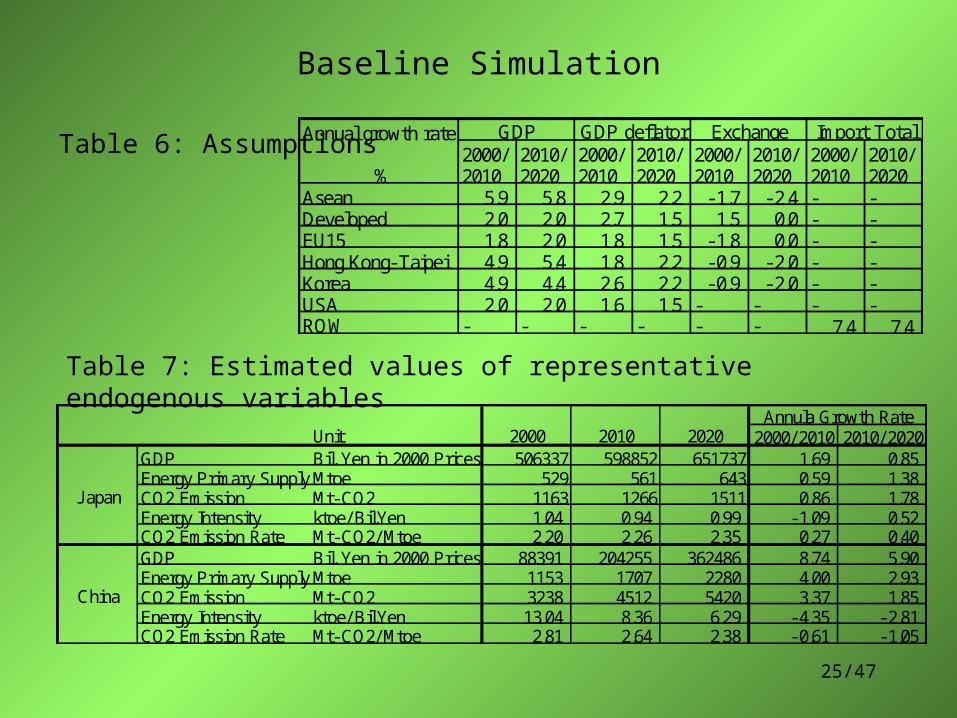

Baseline Simulation

Table 6: AssumptionsAnnual growth rate

%2000/2010

2010/2020

2000/2010

2010/2020

2000/2010

2010/2020

2000/2010

2010/2020

Asean 5.9 5.8 2.9 2.2 -1.7 -2.4 - -Developed 2.0 2.0 2.7 1.5 1.5 0.0 - -EU15 1.8 2.0 1.8 1.5 -1.8 0.0 - -Hong Kong-Taipei 4.9 5.4 1.8 2.2 -0.9 -2.0 - -Korea 4.9 4.4 2.6 2.2 -0.9 -2.0 - -USA 2.0 2.0 1.6 1.5 - - - -ROW - - - - - - 7.4 7.4

GDP GDP deflator Exchange Import Total

2000/ 2010 2010/ 2020GDP Bil. Yen in 2000 Prices 506337 598852 651737 1.69 0.85Energy Primary SupplyMtoe 529 561 643 0.59 1.38CO2 Emission Mt-CO2 1163 1266 1511 0.86 1.78Energy Intensity ktoe/ Bil.Yen 1.04 0.94 0.99 -1.09 0.52CO2 Emission Rate Mt-CO2/ Mtoe 2.20 2.26 2.35 0.27 0.40GDP Bil. Yen in 2000 Prices 88391 204255 362486 8.74 5.90Energy Primary SupplyMtoe 1153 1707 2280 4.00 2.93CO2 Emission Mt-CO2 3238 4512 5420 3.37 1.85Energy Intensity ktoe/ Bil.Yen 13.04 8.36 6.29 -4.35 -2.81CO2 Emission Rate Mt-CO2/ Mtoe 2.81 2.64 2.38 -0.61 -1.05

J apan

China

Annula Growth Rate2000 2010 2020Unit

Table 7: Estimated values of representative endogenous variables

26/47

J apan

0

200000

400000

600000

800000

1000000

1200000

1400000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Billio

n Yen

in 2

000

Mar

ket

Pric

es

J X21 J X20 J X19 J X16 J X15 J X14 J X13 J X12 J X11 J X10 J X09 J X08 J X07 J X06 J X05 J X04 J X03 J X02 J X01

Figure 9: Industrial Structure of Japan

27/47

China

0

20000

40000

60000

80000

100000

120000

140000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Billio

n Yua

n in

200

0 M

arke

t Pric

es

CX21 CX20 CX19 CX18 CX17 CX16 CX15 CX14 CX13 CX12 CX11 CX10 CX09 CX08 CX07 CX06 CX05 CX04 CX03 CX02 CX01

Figure 10: Industrial Structure of China

28/47

4 Some Simulation Results

• The introduction of energy-efficient technology is important to attain the goals of economic development and global environment improvement for China.

• Japan has incentives to cooperate because of her own interest in the compliance of the Kyoto Protocol.

• Simulations

– Case-1: China introduces new technologies (NGCC and IGCC) in the electricity sector to improve energy efficiency.

– Case-2: A carbon tax (2400Yen/tC – approximately 5Euro/tCO2) is introduced in Japan and China.

30/47

Case-1a NGCC in China

• Efficiency improvement(2010-2020) in thermal power stations by energy shift from coal to natural gas in China– NGCC (Natural gas-fired Combined Cycle )– 600 MW x 20 units per year for 10 years– Construction Cost 500$/kW (in 2000 US dollars) – Thermal efficiency 53.6%– Operation starts five years after construction – The first construction starts in 2006– After operation, old coal thermal stations are replaced at the same

volume. – Main equipment, combustion turbine, (27.7% of total cost) is

imported from developed countries.– Import share from Japan is 20% (the US 50%, EU15 30%).

31/47

Case-1b IGCC in China

• Efficiency improvement (2010-2020) in thermal power stations by introducing new Clean Coal technology– IGCC (Integrated Coal Gasification Combined Cycle)– 600 MW x 20 units per year for 10 years– Construction Cost 1,262$/kW (in 2000 US dollars) – Thermal efficiency 43.1%– Operation starts after 5 years construction – The first construction starts in 2006– After operation, an old coal thermal station is replaced at the same

volume. – Main equipment, gasifier and combustion turbine (42.4% of total

Cost), is imported from the developed countries.– Import share from Japan is 20% (the US 50%, EU15 30%).

32/47

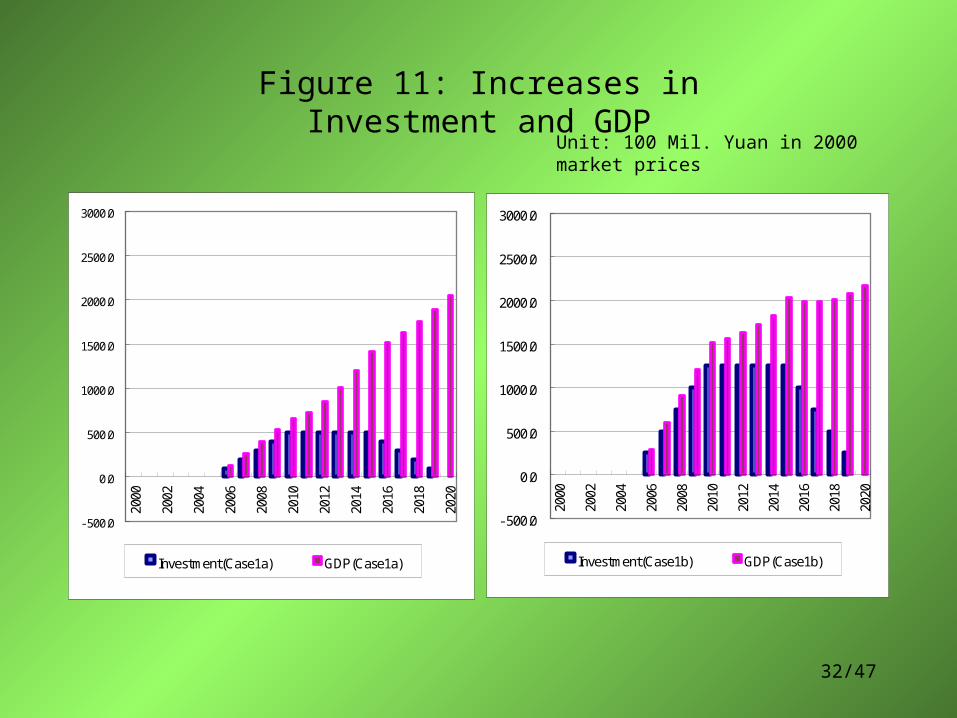

Figure 11: Increases in Investment and GDP

Unit: 100 Mil. Yuan in 2000 market prices

-500.0

0.0

500.0

1000.0

1500.0

2000.0

2500.0

3000.0

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

Investment(Case1a) GDP(Case1a)

-500.0

0.0

500.0

1000.0

1500.0

2000.0

2500.0

3000.0

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

Investment(Case1b) GDP(Case1b)

33/47

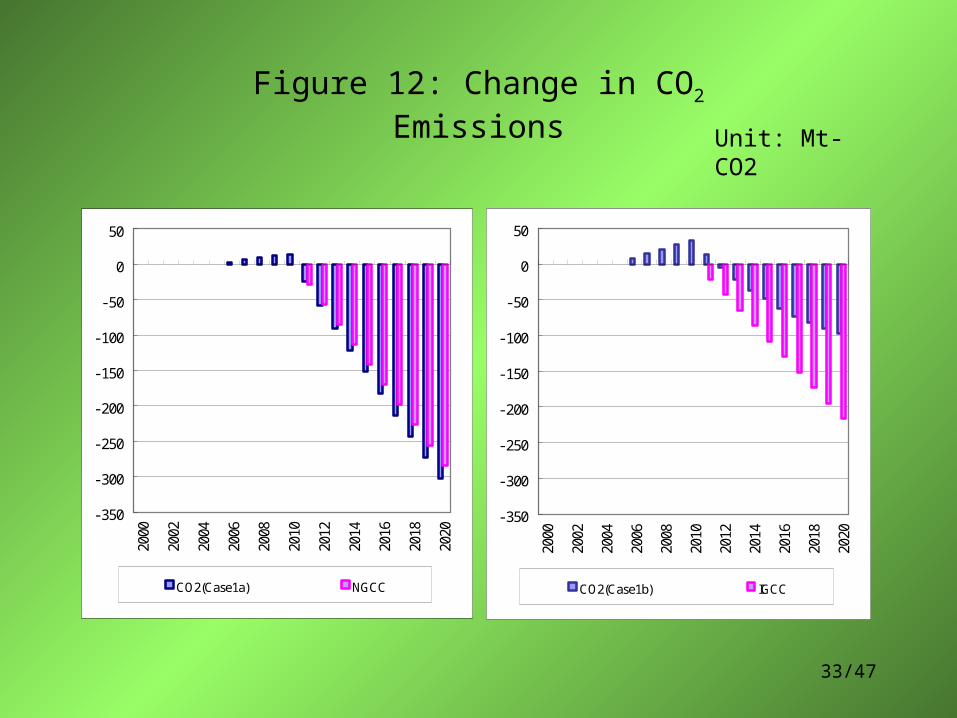

Figure 12: Change in CO2 Emissions

Unit: Mt-CO2

-350

-300

-250

-200

-150

-100

-50

0

50

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

CO2(Case1a) NGCC

-350

-300

-250

-200

-150

-100

-50

0

50

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

CO2(Case1b) IGCC

34/47

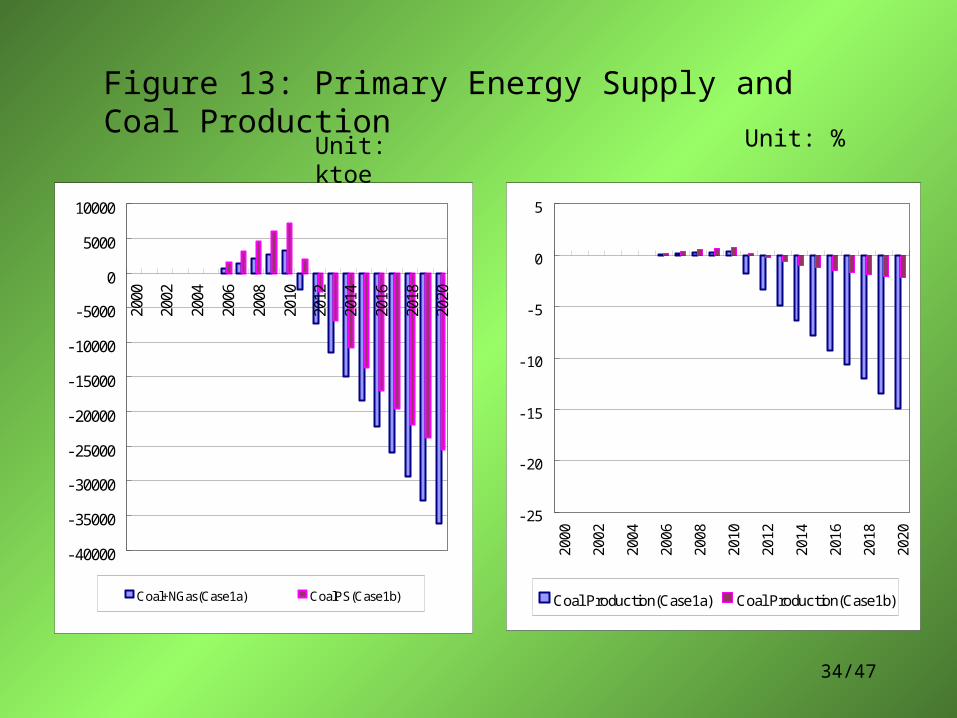

Figure 13: Primary Energy Supply and Coal Production

Unit: %

-40000

-35000

-30000

-25000

-20000

-15000

-10000

-5000

0

5000

10000

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

Coal+NGas(Case1a) CoalPS(Case1b)

Unit: ktoe

- 25

- 20

- 15

- 10

- 5

0

5

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

Coal Production(Case1a) Coal Production(Case1b)

35/47

Unit NGCC IGCC Ratio

100 Mil. Yuan 4967.0 12536.8 0.40

Direct Mt-CO2 1560.6 1190.5 1.31

Total Mt-CO2 1619.2 402.2 4.03

Direct Yuan/ t-CO2 318.3 1053.1 0.30

Total Yuan/ t-CO2 306.8 3117.4 0.10

Direct Yen/ t-CO2 4143 13709 0.30

Total Yen/ t-CO2 3993 40584 0.10

Direct US$/ t-CO2 38.4 127.2 0.30

Total US$/ t-CO2 37.1 376.6 0.10

CO2Reductio

nCO2

Reduction CostCO2

Reduction CostCO2

Reduction Cost

Investment Cost

Table 8: GHG Reduction Cost of NGCC and IGCC for 10 Years

36/47

• NGCC directly reduces CO2 emission by 30% more than IGCC; 1560 Mt-CO2 and 1190 Mt-CO2 for ten years respectively.

• Investment cost of NGCC is 40% of that of IGCC.• GHG reduction cost of NGCC investment is 30% cost of

IGCC, though we ignore the operational cost.• If we consider social effect, the cost difference exaggerates

up to 10%

• Investment increases GDP in both case. Investment brings CO2 increase, which offsets partly the CO2 reduction brought by introduction new technology.

• Coal production reduces in both cases, but high reduction appears in the NGCC case because of its energy shift to natural gas. Restructuring in the coal industry will be required especially in NGCC case.

37/47

Figure 14: Effects on Machinery Products and GDP in Japan

Unit: %

-0.1

-0.05

0

0.05

0.1

0.15

0.2

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

X12(Case1a) GDP(Case1a)

-0.1

-0.05

0

0.05

0.1

0.15

0.2

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

X12(Case1b) GDP(Case1b)

38/47

• The impact on Japan is higher for IGCC, because its higher investment induces larger volume of machinery trade directly.

• Effect on Japan is mainly positive on GDP and machinery production.

• The induced CO2 increase in Japan is 0.4 Mt-CO2 and 3.1 Mt-CO2 for ten years respectively, which is almost negligible compared to the value in China.

39/47

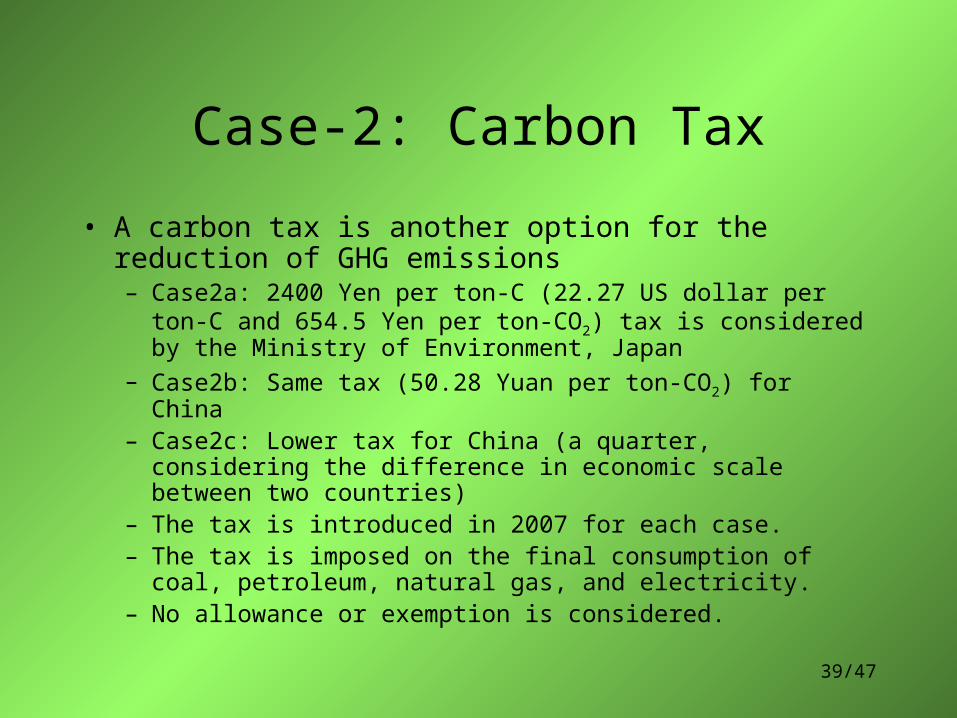

Case-2: Carbon Tax

• A carbon tax is another option for the reduction of GHG emissions– Case2a: 2400 Yen per ton-C (22.27 US dollar per ton-C and 654.5

Yen per ton-CO2) tax is considered by the Ministry of Environment, Japan

– Case2b: Same tax (50.28 Yuan per ton-CO2) for China– Case2c: Lower tax for China (a quarter, considering the difference

in economic scale between two countries)– The tax is introduced in 2007 for each case.– The tax is imposed on the final consumption of coal, petroleum,

natural gas, and electricity.– No allowance or exemption is considered.

40/47

Figure 15: Impacts in Japan

• Price increases in energy sectors are 3 or 5 % points.

• GDP deflator increases up to 3 %.

• GDP deceases by 0.14% or 0.43% .

• The difference in primary-energy supply and CO2 reduction will be 1% or less. - 2

- 1

0

1

2

3

4

5

GDP

GDP D

eflat

or

Pet

ro.P

rice

Coa

l Price

Elec

. and

NG

asPrice

Prim

.En.

Sup

ply

CO

2

% 20102020

41/47

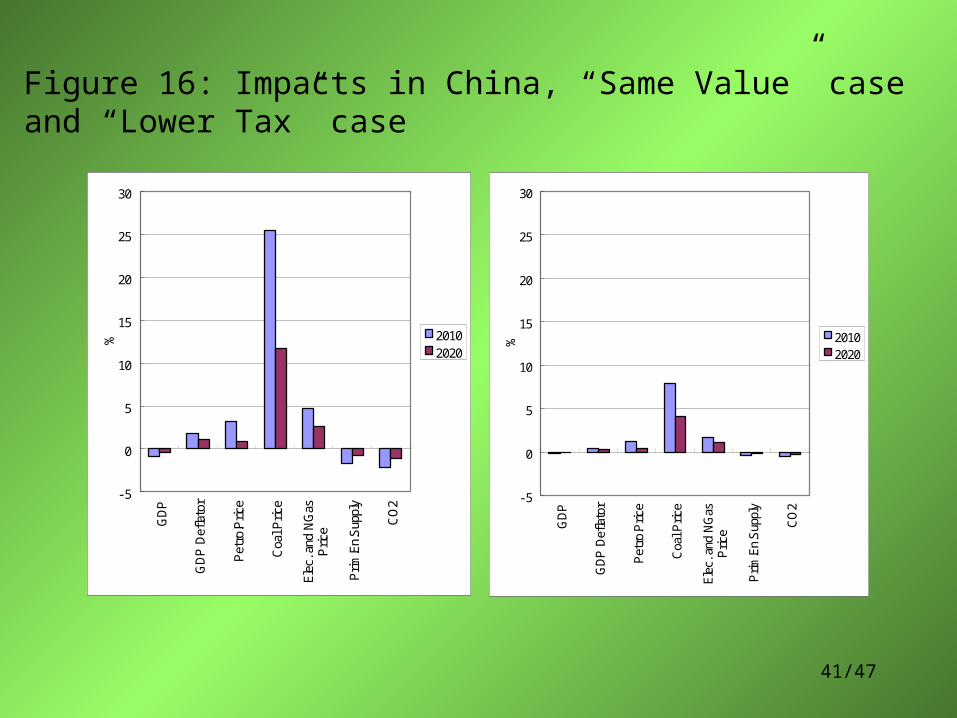

Figure 16: Impacts in China, “Same Value” case and “Lower Tax” case

-5

0

5

10

15

20

25

30

GD

P

GD

P D

eflat

or

Pet

ro.P

rice

Coa

l Pric

e

Elec

. and

NG

asPric

e

Prim

.En.

Sup

ply

CO

2

% 20102020

-5

0

5

10

15

20

25

30

GD

P

GD

P D

eflat

or

Pet

ro.P

rice

Coa

l Pric

e

Elec

. and

NG

asPric

e

Prim

.En.

Sup

ply

CO

2

% 20102020

42/47

Figure 17: CO2 Reduction in Each Case

- 120

- 100

- 80

- 60

- 40

- 20

0C

O2(

Japa

n)

CO

2(C

hina

1)

CO

2(C

hina

2)

Mt-

CO

2

20102020

• For Japan, the proposed carbon tax reduces 11 and 16 Mt-CO2 in 2010 and 2020 respectively.

• This value is higher than that of government’s estimate, using the AIM model; 6 Mt-CO2 in 2010.

• For China, the same rate tax brings larger reduction in CO2, 95 Mt-CO2 and 58 Mt-CO2, than Japan.

• Lower (one quarter) tax rate in China of reduces China’s emissions by 24 and 14 Mt-CO2.

43/47

5 Concluding Remarks• Developing an E3 econometric model, we evaluate the impacts of

technological transfer from Japan to China, which might be possible future CDM projects.

• The basic idea of usual CDM is how much GHG will be reduced if the project is installed, comparing with the GHG emission level of typical alternative, called a baseline, if the project is not installed.

• Our evaluation is economy-wide, not just CDM project evaluation.

• Our study addresses the social evaluation in the sense that GHG emission from the initial investment activity is included and that the change in GHG emission stemmed from the other sectors’ production and household consumption is also considered.

44/47

• Two technology transfer, NGCC and IGCC, are compared.

– NGCC reduces CO2 emission more effectively than IGCC.

– However, NGCC requires primary-energy demand shift from coal to natural gas.

– Coal production reduces in both cases, but high reduction appears in the NGCC case.

– Restructuring in the coal industry will be required strongly especially in NGCC case.

45/47

– Japan receives stronger impact from IGCC, because its higher investment induces larger volume of machinery trade directly.

– The effect on Japan is positive mainly on GDP and machinery production.

– The induced CO2 increase in Japan is 0.4 Mt-CO2 and 3.1 Mt-CO2 for ten years respectively, which is almost negligible compared with the reduction in China. But they might be not negligible in the Japan’s economy.

– Japan considers to reduce 20Mt-CO2 by Kyoto Mechanisms. Compared with this value, our scenario gives 31.2 Mt-CO2 reduction per year for NGCC and 23.8 Mt-CO2 per year for IGCC, assuming that Japan’s contribution is 20 % in each project.

– For this project Japan needs 129.3 and 326.4 billion yen per year respectively, which might be financed by carbon tax revenue.

46/47

• Carbon tax effects– For Japan, the proposed carbon tax reduces 11 and 16 Mt-CO2 in

2010 and 2020 respectively.– This is higher than the estimate of the Government, 6 Mt-CO2,

using the AIM model.– The difference is explained by our ignoring some tax exemptions.

Actually our estimate of the tax revenue is 742 billion Yen, which is 1.5 times larger then the government estimate, 490 billion Yen.

– The tax reduces GDP by 0.14% and 0.43% in 2010 and 2020 respectively. This would be reduced by using the tax revenue effectively.

– For China, the same rate tax brings larger reduction in CO2, 96 Mt-CO2 and 58 Mt-CO2, than Japan.

– One quarter rate Tax of Japan reduces 24 and 14 Mt-CO2 in China.– A given carbon tax in China saves GHG gas emission more

effectively than the same tax in Japan.

47/47

• Remaining issues– Our simulation ends at 2020, this is a somewhat short

to evaluate the issues after Kyoto. We would like to extend the simulation period up to 2030.

– The RAS structure is one of the main features in our model. This is constrained as constant in our simulation, which has to be released.

– Adding the country and region sub-models, which are set as exogenous in the current model, for Korea, ASEAN, Hong Kong and Taipei, the US, EC15, other developed countries, and the rest of the world.

– IIASA has a lot of knowledge and experience in the field of energy and environment researches, so we are going to extend our research cooperatively.