Embed Size (px)

Citation preview

w w w . i m d . c h N o . 1 7 8 O c t o b e r 2 0 0 9

SUPPLY CHAIN FINANCE – WHAT’S IT WORTH?

Supply Chain Finance (SCF) represents

an innovative opportunity to reduce

working capital. Its underlying

mechanism is reverse factoring making

the technique buyer- rather than

supplier-centric. Implementing SCF is a

difficult and time-consuming task that

requires top management attention.

Yet, it promises significant savings. Our

survey results show that, on average,

companies reduce working capital by

13% and suppliers reduce working

capital by 14%. Three factors differentiate

successful implementations of SCF

from less successful ones: Choosing

the right banking partner, ensuring CEO

sponsorship, and involving at least

60% of the supply-base.

Working capital reduction is not

exactly the new kid on the block:

Business press articles have

heralded its benefits for nearly two

decades; it has been explored in

detail in scientific journals for about a

centur y; and numerous conferences

unite practitioners to discuss best

practices ever y year. But, for some

companies, the topic has recently

moved to the top of the agenda. With

banks less willing to hand out loans,

companies are finding it difficult to

maneuver.

Despite the longstanding attention

to reducing working capital, the only

component that has dropped over

the years is inventor y – representing

a mere 30% of total working capital.

Collection and payment delays have

remained largely flat with most

companies sticking to industr

y standards and collecting and

paying invoices after 30 or 45 days.

Also, most continue to keep

suppliers at arm’s length. One

executive we recently inter viewed

described his company’s approach

to negotiating payment terms as a

“no tolerance” strategy.

In the past, suppliers often reacted

to these long payment delays by

factoring their receivables

when they needed cash.1

Factoring is

a transaction in which suppliers sell

receivables to factors for immediate

cash. Because the receivables are

sold rather than pledged, factoring

is different from borrowing – there

are no liabilities on the suppliers’

balance sheet.2

Typically, suppliers

sell receivables from more than one

buyer. Thus, factors have to evaluate

buyer portfolios before entering an

agreement. This has made factoring

an expensive source of finance in

emerging markets. A lack of historic

credit information or credit bureaus,

fraud, and weak legal environments

have meant high operating costs.

Today some buyers are recognizing

their suppliers’ difficulties in

accessing finance. And instead of

taking a “no tolerance” approach,

they have started to implement

a collaborative approach termed

Reverse Factoring or Supply Chain

Finance. This technique’s underlying

mechanism is factoring. There are,

however, three important differences.

Ralf W. Seifert IMD Professor of Operations Management

Daniel Seifert Research Assistant, Ecole Polytechnique Fédérale de Lausanne

First, since the technique is buyer-centric,

factors do not have to evaluate heterogeneous

buyer portfolios and can charge lower fees.

Second, since these buyers are usually

investment grade companies, factors carr

y less risk and can charge lower interest

rates. Third, as the buyers participate actively,

factors obtain better information and can

release funds earlier.

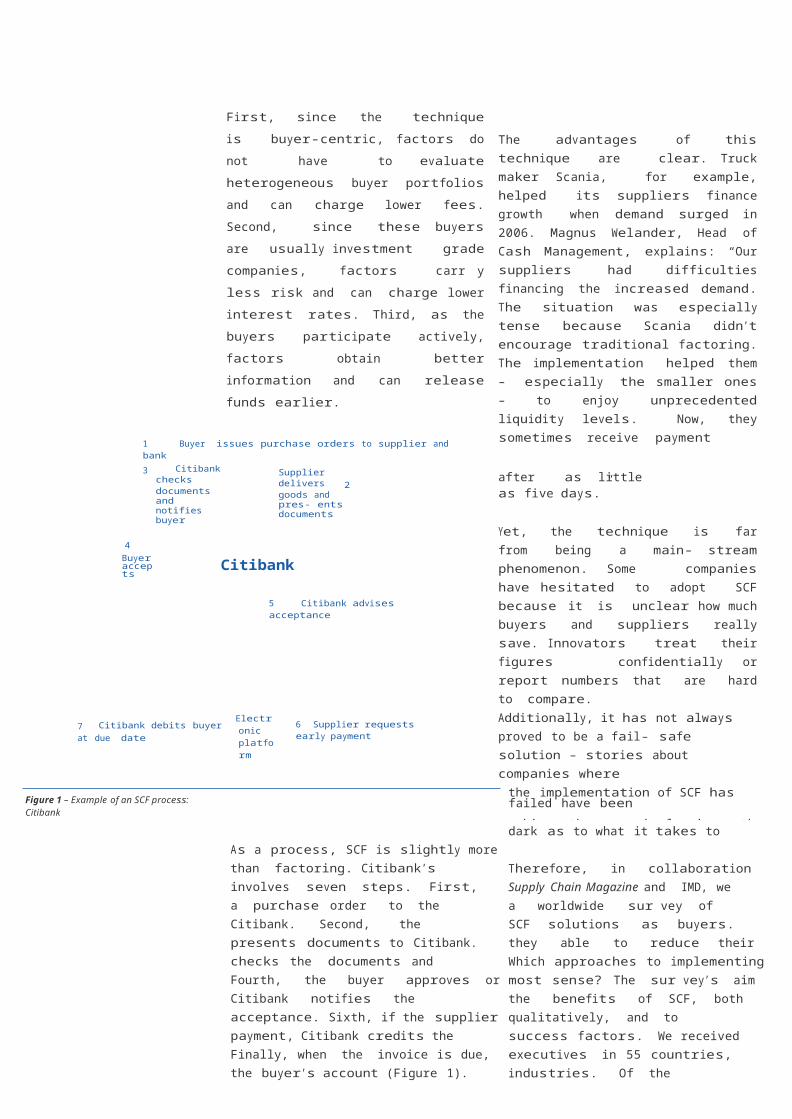

1 Buyer issues purchase orders to supplier and bank

The advantages of this technique are clear.

Truck maker Scania, for example, helped its

suppliers finance growth when demand surged

in 2006. Magnus Welander, Head of Cash

Management, explains: “Our suppliers had

difficulties financing the increased demand. The

situation was especially tense because Scania

didn’t encourage traditional factoring. The

implementation helped them – especially the

smaller ones – to enjoy unprecedented liquidity

levels. Now, they sometimes receive payment3 Citibank checks

documents and notifies buyer

4

Buyer accepts

Supplier delivers 2 goods and pres- ents documents

Citibank

5 Citibank advises acceptance

after as little as five days.”

Yet, the technique is far from being a main-

stream phenomenon. Some companies have

hesitated to adopt SCF because it is unclear

how much buyers and suppliers really save.

Innovators treat their figures confidentially

or report numbers that are hard to compare.

7 Citibank debits buyer at due dateElectronic platform 6 Supplier requests early payment Additionally, it has not always proved to be a fail-

safe solution – stories about companies where

Figure 1 – Example of an SCF process: Citibank the implementation of SCF has failed have been

making the rounds leaving other firms in the

dark as to what it takes to succeed.

As a process, SCF is slightly more complicated

than factoring. Citibank’s process, for example, Therefore, in collaboration with Springer’s

involves seven steps. First, the buyer sends Supply Chain Magazine and IMD, we conducted

a purchase order to the supplier and notifies a worldwide sur vey of executives who use

Citibank. Second, the supplier delivers and SCF solutions as buyers. How much were

presents documents to Citibank. Third, Citibank they able to reduce their working capital?

checks the documents and notifies the buyer. Which approaches to implementing SCF made

Fourth, the buyer approves or rejects. Fifth, most sense? The sur vey’s aim was to assess

Citibank notifies the supplier of the buyer’s the benefits of SCF, both quantitatively and

acceptance. Sixth, if the supplier requests early qualitatively, and to statistically derive the key

payment, Citibank credits the supplier’s account. success factors. We received 213 replies from

Finally, when the invoice is due, Citibank debits executives in 55 countries, covering all major

the buyer’s account (Figure 1). industries. Of the respondents, 23 reported

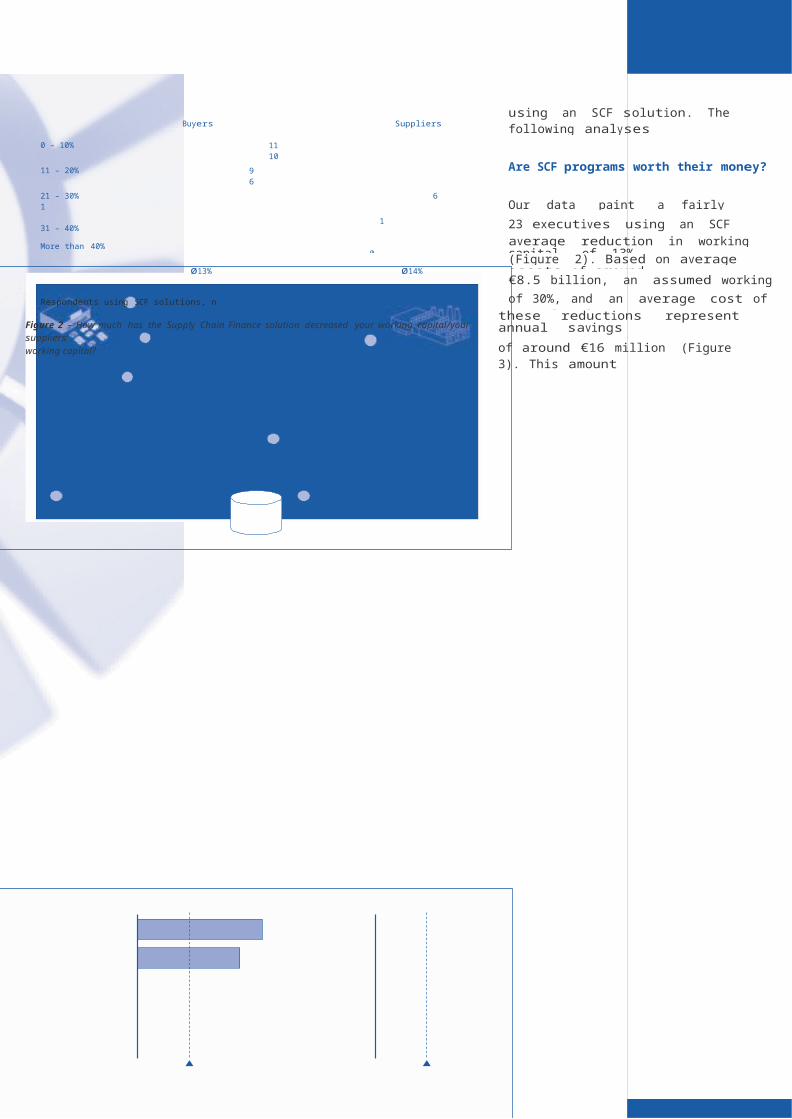

Buyers Suppliersusing an SCF solution. The following analyses

are based on their answers.0 – 10% 11 10

11 – 20% 9 6 Are SCF programs worth their money?

21 – 30% 1 6Our data paint a fairly positive picture: The

31 – 40% 01 23 executives using an SCF solution report an

More than 40% 20

average reduction in working capital of 13%

(Figure 2). Based on average assets of aroundø13% ø14%

€8.5 billion, an assumed working capital ratio

Respondents using SCF solutions, n = 23 of 30%, and an average cost of capital of 5%,

Figure 2 – How much has the Supply Chain Finance solution decreased your working capital/your suppliers’working capital?

these reductions represent annual savings

of around €16 million (Figure 3). This amount

Improvement of supplier relations 52%

Reduction of prices26%

Information gain about suppliers' finances17%

None

SUPPLY CH A IN FIN A NCE – W H AT’S IT WORTH?

compares with an investment of € 0.1-1.5

million in information technology as suggested

by the Aberdeen Group in their Technology

Platforms for Supply Chain Finance report.3

Even if the savings are lower than suggested

by the above business case, the program should

still break even in less than a year.

Similarly encouraging is the obser vation that

Assumptions

• Working capital over assets: 30%

• Working cap- ital reduction due to SCF:13%

• Risk freerate: 3%

Assets

Working capital

Working capital reduction

Annual cost savings

Smallest risk premium: 0%

8,531.0

2,559.3

332.7

10.0

Average risk premium: 2%

8,531.0

2,559.3

332.7

16.4

Largest risk premium: 9%

8,531.0

2,559.3

332.7

39.9

SCF seems to help suppliers too. The same

23 executives report that, on average, their

suppliers were able to reduce working capital

by 14% by participating in the SCF program.

Asked about intangible benefits, more than

half of the respondents – 57% – say that SCF

helps standardize payment terms and 52%

say that SCF helps improve supplier relations

(Figure 4). Asked how SCF links back to other

projects, 68% say that its implementation

improves Purchase-to-Pay processes, 14% say

that it improves Order-to-Cash processes, and

another 14% say that it improves Record-to-

Report processes. Intangible benefits attributed

to suppliers include more transparency and

fewer disputes (65% and 52% respectively of

these respondents). Finally, executives seem

to perceive the drawbacks as limited: 30%

perceive no drawbacks at all. Of the rest, 44%

report reduced credit availability, 31% report

pressure to guarantee payments, and 25%

report other drawbacks.

Given the wide range of outcomes, it is

legitimate to ask if there are differences in

the way businesses implement SCF. What

distinguishes a successful from a less

successful implementation? Our data reveal

three key success factors.

Averages of 23 companies using SCF solution, € million

Figure 3 – Supply Chain Finance – Business Case

Second, roughly half of these respondents –

52% – say that internal sponsorship plays an

important role. Consistently, our regressions

found implementations to be more than twice

as successful when the CEO rather than the

CFO leads them. The message is clear –

although it might be tempting to delegate, CEOs

should personally lead the effort. Individual

departments do not seem to have the required

leverage to keep the stakeholders – especially

suppliers – at the table.

Standardization of payment terms

Other 4%

Percent of respondents using SCF solutions, n = 23

Figure 4 – What other benefits has your company experienced?

57%

First, the majority of executives – 65% – say

that the banking partner is a key success

factor (Figure 5). We tested this assertion

by regressing working capital reduction on

banking relationship strength and found this

factor to be positively related at a statistically

highly significant level. Thus, executives should

invest sufficient time into selecting a banking

partner. Important criteria that we determined

during in-depth follow-up inter views included

the bank’s geographic reach, its legal expertise

Banking partner

Internal sponsorship

Other (mostly supplier involvement)

IT implementing partner

Technology platform

Percent of respondents using SCF solutions, n = 23

17%

13%

0%

52%

65%

and its financial muscle. Figure 5 – What were key success factors in implementing the Supply Chain Finance solution?

IMD

is c

omm

itte

d to

en

viro

nm

enta

l sust

ainab

ility

and

ful

ly o

ffse

ts it

s C

O2

foot

prin

t w

ith

Finally, some executives – 17% – stress the

need for supplier involvement. Our in-depth

inter views suggest that companies face

difficulties in convincing suppliers to participate

in SCF programs. One executive reported that

suppliers would rather accept late payment

than be involved in a seemingly complicated

program that they did not understand.

Executives should, therefore, critically assess

which suppliers to include in the first wave

and which ones to include in the final rollout.

Our tests suggest that implementations are

most successful when they include at least 60%

of the supply-base in the first wave.

This finding is consistent across different life

cycle stages, i.e., implementation and operation.

Given the attractive benefits and the clear key

success factors, we recommend executives

take a closer look at SCF. It will not solve the

liquidity issues that some companies will face

over the next months. But it seems a sustainable

approach to reducing working capital in the long

run. As our analysis suggests, there are three

key success factors that companies should

focus on: Choosing the right banking partner,

ensuring CEO sponsorship, and involving at

least 60% of the supply-base.

Contrary to our expectations, cross-functional

teams do not appear to play a role. At least

statistically, it does not matter which or how

many departments a company involves. The

most successful implementations involve five

departments (Finance, Purchasing, Supply Chain

Management, IT, Legal), but implementations

that involve only two departments (Finance,

Purchasing) closely track their performance.

Admittedly, getting these three factors right

is a difficult and time-consuming task and is

one of the reasons that companies have been

slow to adopt the technique. But persevere

and the payoffs, in terms of working capital

reduction, will be worth working for. So while

it may no longer be the new kid on the block,

it seems working capital reduction will

continue to create a buzz for some time to

come.

We recommend

executives take a closer

look at SCF.

1. Some suppliers employ early payment discounts instead of factoring. Early payment discounts, however, are a far more expensive source of finance. The most common discount scheme (2/10 net 30) implies an annual interest rate of over 43% whereas factoring commonly entails an annual interest rate of 6%.

2. There are, however, variants. Recourse factoring, for example, creates a liability that is contingent upon the

buyer’s payment. For further information see

Klapper, L. (2005). The Role of “Reverse Factoring”

in Supplier Financing of Small and Medium Sized

Enterprises. Working Paper, The World Bank, 2005.

3. Aberdeen Group (2007). Technology Platforms for Supply

Chain Finance. Aberdeen Group, Inc., Boston, MA, March

2007.

Chemin de Bellerive 23

P.O. Box 915, CH-1001 Lausanne

Switzerland

IMD is ranked first in executive education outside the US and second worldwide (Financial

Times, 2009). IMD’s MBA is ranked number one worldwide (The Economist, 2008).

No part of this publication may be reproduced without written authorization © IMD, October 2009

central tel: +41 21 618 01 11

central fax: +41 21 618 07

www.imd.ch