Embed Size (px)

Citation preview

12. FINLAND: ECONOMIC DOCTRINES 1945 - 1990

1. Preliminary considerations

2. The accumulation doctrine

3. The exchange rate as anchor of policy

1. Finland in 1945 – 1990: Preliminary considerations

the decades after WWII were the high period of keynesianism globally, not so in Finland (illustrating a certain Finnish ’exceptionalism’)

Finland after WWII was not a mature capitalis economy but an economy lagging behind and hoping to catch up relative to Sweden and others

The economic structure was charaterized by the large share of population in agruculture

There was shortage of capital to build up industry, needed to finance imports and to pay war reparations to the Sovjet Union, to create infrastructure and to exploit the natural resources in Northern Finland

There was excess supply of labor due to high fertility and declining share of population in agriculture, large-scale emigration

The trade balance (blue), the war reparations (green) and the current account (the line), all in relation to GDP

Cont. Trade was gradually liberalized and the Finnih markka made convertible (in the late 1950s)

but capital imports remained tightly regulated

Finland was and is a small open economy (competitiveness important)

The external constraint (shortage of foreign exchange) was often binding, a source of problem for macroeconomic developments and policies

Regulation was widespread after the war, notably regulation of the financial system. More generally, the state was a powerful actor which intervened extensively by regulation to affect investment, saving, price developments …

Corporatism was of great importance for policies

Politics was characterized by splits within the labor movement; government coalitons were often short-lived

Overall economic developments were characterized by volatility or instability

2. The accumulation doctrine

Finland pursued supply side policies with emphasis on the accumulation of capital (cf. Marx: ”Accumulate, accumulatte! That is Moses and the Prophets.”)

The rationale was spelled out in 1952 by Urho Kekkonen in a small book ”Onko maallamme malttia vaurastua?” (Does our country have the patience to become wealthy?): he argued for forced saving in the form of government budget surpluses to finance heavy investment, particularly in the North

FISCAL POLICY. The government had no ambitions to stabilize the economy by fiscal policy but emphasized budget balance (as did civil servants)

The balanced budget doctrine was associated with procyclical policies that were destabilizing for the economy

This policy kept government debt at a low level (roughly 10 per cent of GDP)

Cont.

The government aimed at budget balance in cash terms, using tax financing not only for government consumption and transfers but also for investment and for lending to the private sector (to finance investment)

The external constraint contributed to destabilizing policies: an increase in exports improving the trade balance allowed lax policies while a fall in exports, by weakeneing the trade and current accounts, called for tighter fiscal and monetary policies

Financial constraints were key determinants of economic policy. The government was mostly not allowed to borrow from the central bank (which was independent), foreign capital was regulated or not available, there was no domestic bond market of any significance and banks were unwilling to lend to the government!

Mauno Koivisto, as prime minister, had more or less to beg the commercial banks to lend money to the government in certain situations of cash shortage. Somewhat remarkable that a financially solid government was squeezed in this way

Cont.

• TAX POLICY was structured so as to given business strong incentives to invest: high statutory tax rate (even 40 per cent), ample opportunities to reduce or avoid taxes by investment and generous depreciation allowances

• Dividends were taxable with the normal income tax rate but long-term capital gains (more than 10 years) were not taxed at all

• In practice the tax rate on capital income was very low – provided that the company invested heavily and the owner took out the profit in the form of long-term capital gains

• This policy gave strong incetives to invest but had also strong ’lock-in’ effects, such that resources could not easily be reallocated and were often inefficiently allocated

• Also, tax deductibility of interest expenses favoured debt financing, with the implication that the financial structure of firms was weak (high debt/equity ratio)

186018711882189319041915192619371948195919701981199220030

10

20

30

40

50

60

70

80

Valtion bruttovelka/BKT.

Lähde: Valtiokonttori/Mika Arola.

Central government debt in Finland, 1860-2011, % of GDP

Central government debt, per cent of GDP

General government saving and investment, % of GDP

General government financial saving (pillars) and central government financial saving (light blue line), scale to left

Cont.

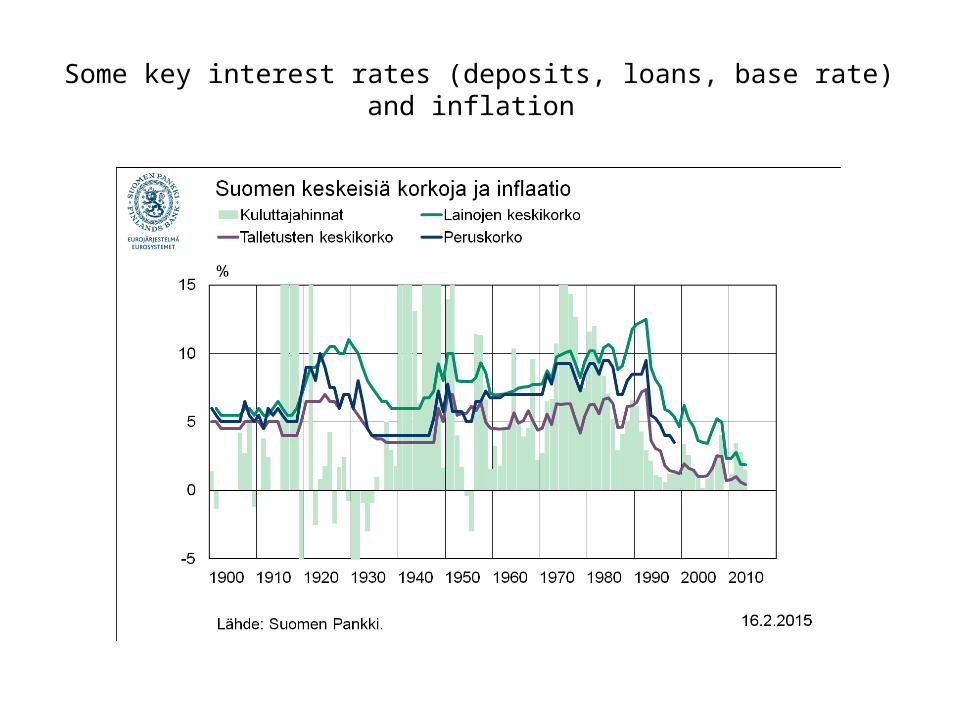

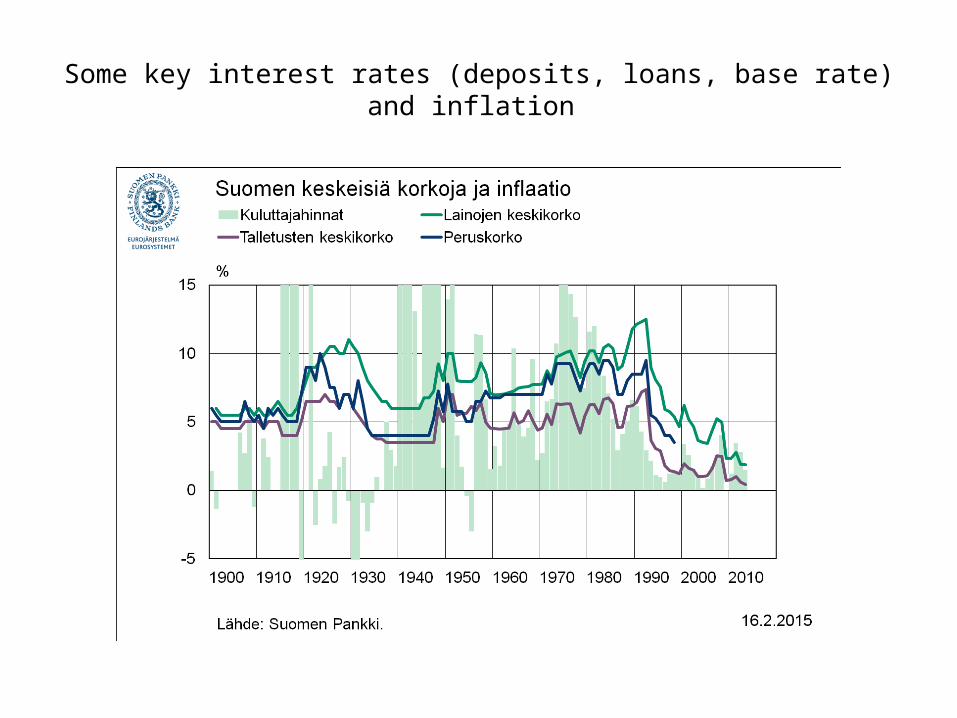

• MONETARY AND CREDIT POLICY. The discount rate, the interest rate paid by banks when borrowing from the central bank, was for political reasons kept low and stable (a ’Keynesian’ element of policy?)

• There was noramlly excess demand for credit and therefore credit rationing, the allocation of the (scarce) credits then depending on considerations by the banks and (to some extent) recommendations of the Bank of Finland (which gave priority to industrial investment while discouraging consumption loans )

• Banks were normally indebted to the central bank (instead of having positive reserves in the central bank). Each bank had a quota for CB-boroowing. Additional borrowing (above the quota) raised the marginal cost of borrowing, and this marginal cost was the main instrument of monetary policy

• Interest rates on bank loans and deposits were often negative in real terms, meaning that almost any investment would be profitable – if you could borrow

The base rate or discount rate of the Bank of Finland

Various marginal rates of interest for central bank financing of banks (changing a lot and mostly being much higher than the discount rate)

The rate of consumer price inflation

Some key interest rates (deposits, loans, base rate) and inflation

Some key interest rates (deposits, loans, base rate) and inflation

Cont.

• EXCHANGE RATE POLICY was in these times considered an instrument of policy separate from interest rate policy (given foreign exchange regulation and the pegged exchange rate)

• Finland undertook rather large devaluations with roughly 10 year intervals (the ’devalution cycle’)

• The devaluation cycle was not only a passive reaction to preceding inflation but was rather an element of the accumulation policy by raising profits and by assuring the export sector that profitability of investment would be ensured if need be by a devaluation (thereby reducing the risks of investment)

• INCOMES POLICY, occasionally in the form of lagre packages with heavy government involvment, were often used with a view to wage moderation and the preservation of competitiveness and profitability of business

The markka was devalued again and again

The accumulation policy: results, consequences

1. The doctrine achieved what it set out to achieve: a very high rate of investment (the highest among 22 countries, cf. Matti Pohjolas ”Tehoton pääoma”)

2. Macroeconomic developments were unstable partly because of the structure of the economy (narrow export base) but also because of the focus of policy on growth and neglect of stabilization

3. Economic growth was rapid but not impressivly so in light of the extremely high share of investment and low consumption

4. There was increasing evidence of distorted investment decisions (too low required return on capital) and misallocation of resources in favor of excessive capital intensity, which reduced efficiency and stability (encouraging tax-induced investments in boom times etc.)

5. The distortions were accentuated ncreased by high and increasing inflation, nottably in the aftermath of the first oil crisis.

In all, in the first decades after WW2 Finland was a highly regulated (and therefore financially stable) country with all policies geared towards achieving and maintaining a high rate of capital accumulation without regard to microeconomic efficiency