Embed Size (px)

Citation preview

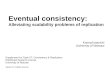

12-1

Unique Characteristics of Life Insurance

1. The event insured is an eventual certainty and the probability of loss increases from year to year.

2. Life insurance does not violate requisites of an insurable risk; it is not the possibility of death that is insured, but of untimely death.

3. There is no possibility of partial loss. Therefore all policies are cash payment policies.

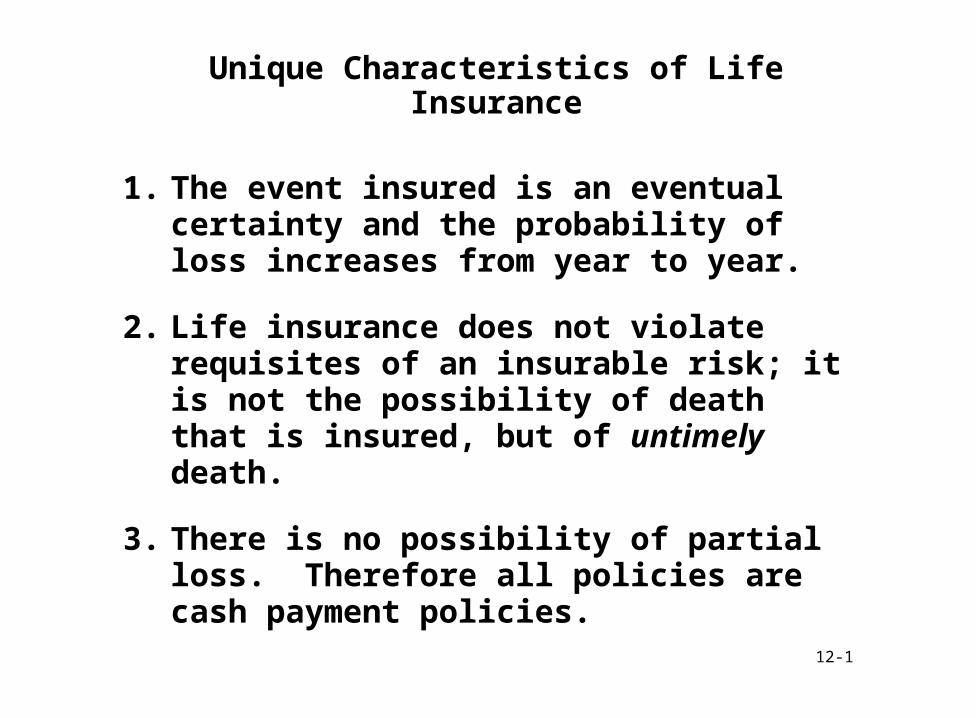

12-2

Life Insurance - Not a Contract of Indemnity

1. Principle of indemnity applies on a modified basis in the case of life insurance.

2. When person taking out the policy is the insured, insurable interest is not an issue.

• every individual has an unlimited insurable interest in his or her own life

• that insurable interest may be freely assigned

3. Persons other than insured must have an insurable interest only at inception of policy.

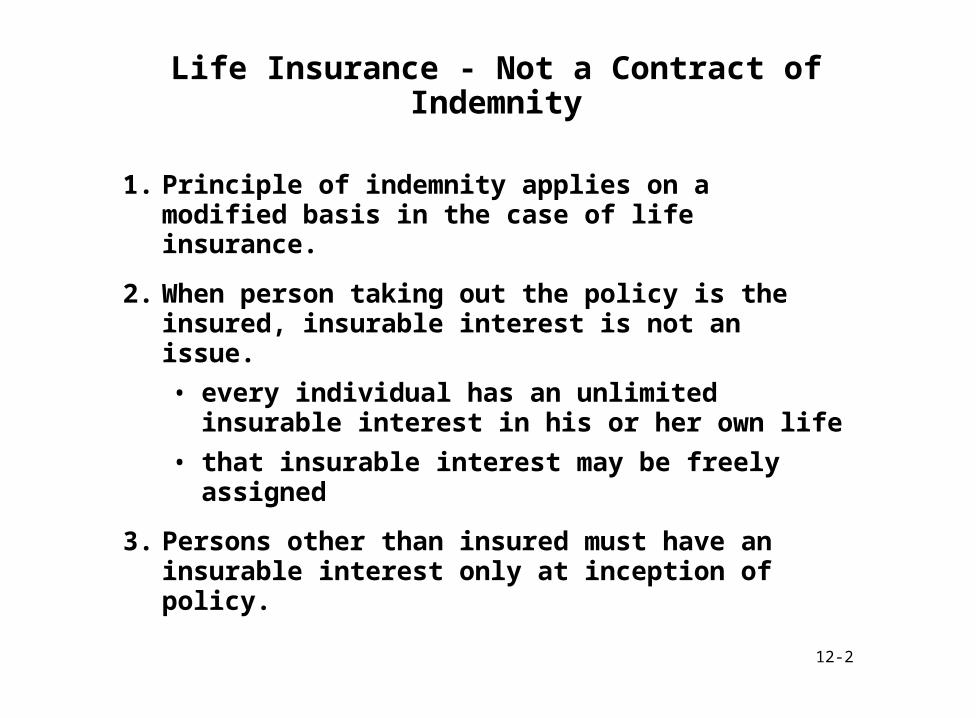

12-3

Types of Life Insurance

Term Insurance Cash Value InsurancePure Protection Insurance and Savings

Term Insurance Whole Life Insurance

Endowment Insurance

Universal Life Insurance

Adjustable Life Insurance

Variable Life Insurance

12-4

Rationale for Different Forms

1. Simplest form of life insurance is yearly renewable term.

• Provides coverage for one year only

• Permits insured to renew for successive years at higher premium

• Increasing mortality produces increasing rates as the insured grows older

12-5

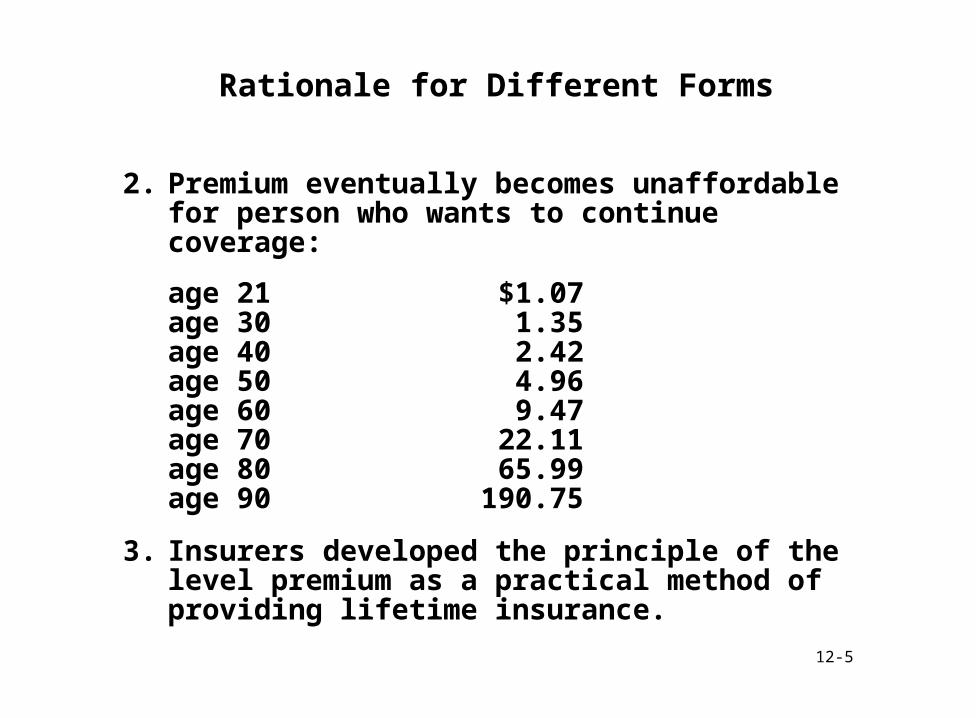

Rationale for Different Forms

2. Premium eventually becomes unaffordable for person who wants to continue coverage:

age 21 $1.07age 30 1.35age 40 2.42age 50 4.96age 60 9.47age 70 22.11age 80 65.99age 90 190.75

3. Insurers developed the principle of the level premium as a practical method of providing lifetime insurance.

12-6

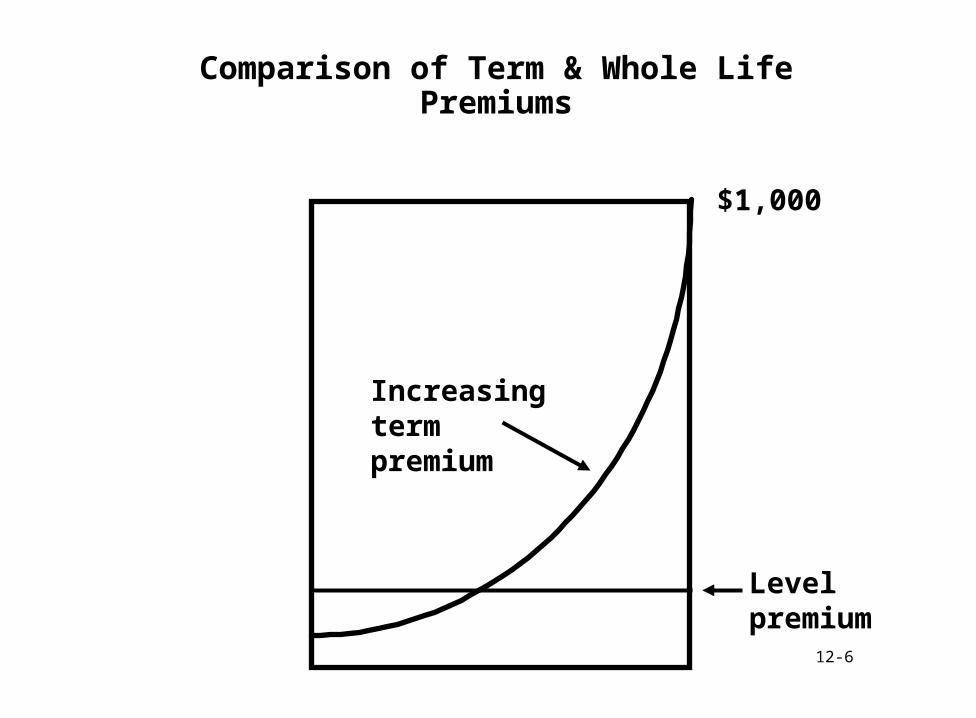

Comparison of Term & Whole Life Premiums

Level premium

Increasing termpremium

$1,000

12-7

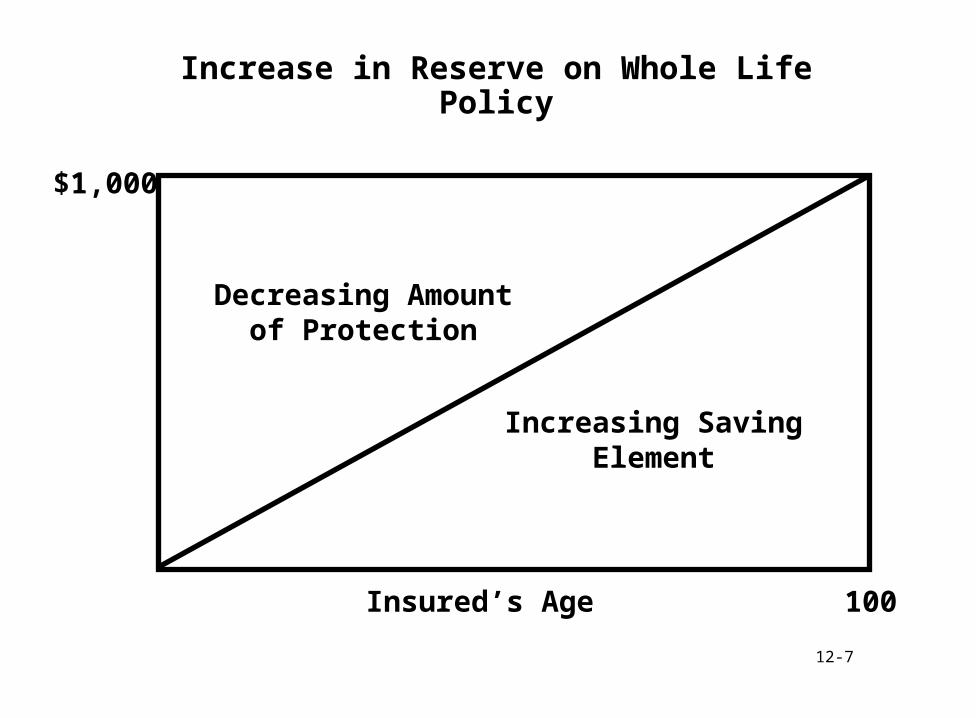

Increase in Reserve on Whole Life Policy

$1,000

Insured’s Age 100

Increasing SavingElement

Decreasing Amountof Protection

12-8

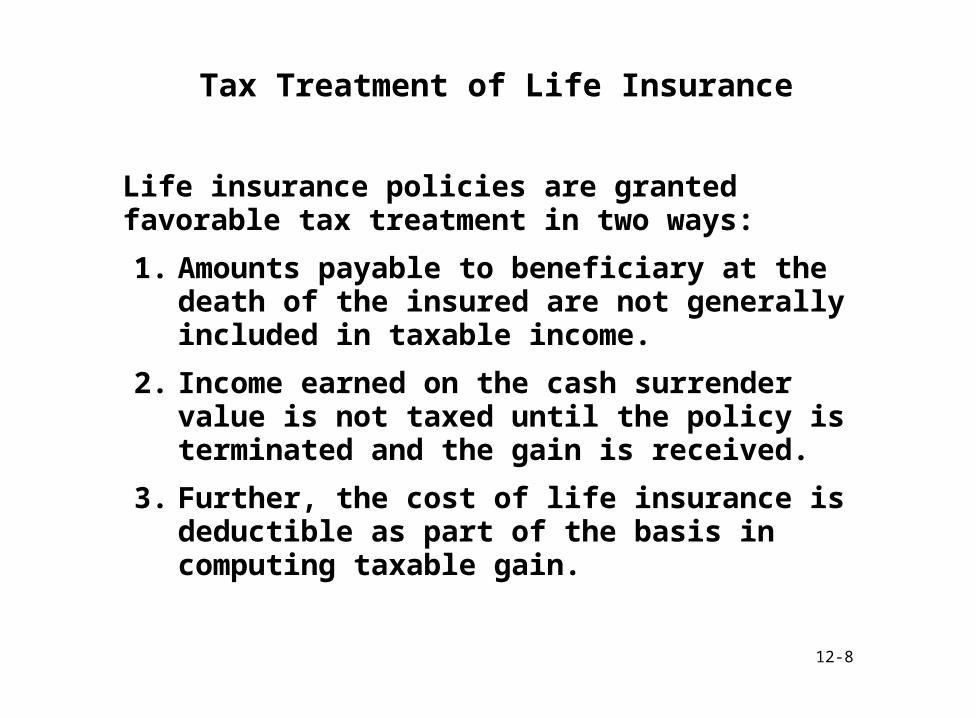

Tax Treatment of Life Insurance

Life insurance policies are granted favorable tax treatment in two ways:

1. Amounts payable to beneficiary at the death of the insured are not generally included in taxable income.

2. Income earned on the cash surrender value is not taxed until the policy is terminated and the gain is received.

3. Further, the cost of life insurance is deductible as part of the basis in computing taxable gain.

12-9

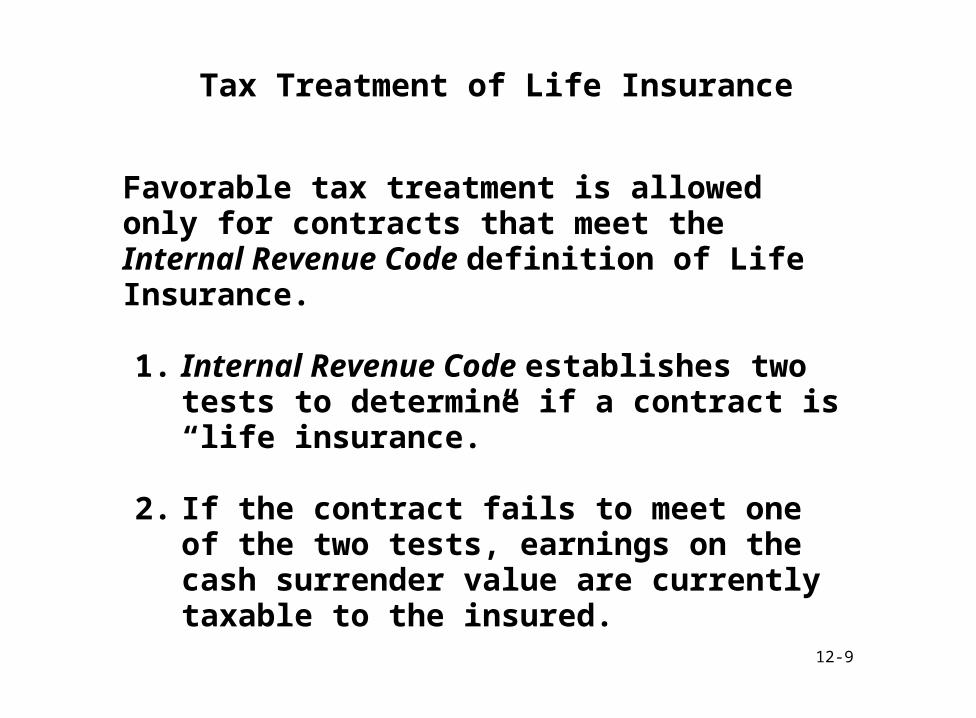

Tax Treatment of Life Insurance

Favorable tax treatment is allowed only for contracts that meet the Internal Revenue Code definition of Life Insurance.

1. Internal Revenue Code establishes two tests to determine if a contract is “life insurance.”

2. If the contract fails to meet one of the two tests, earnings on the cash surrender value are currently taxable to the insured.

12-10

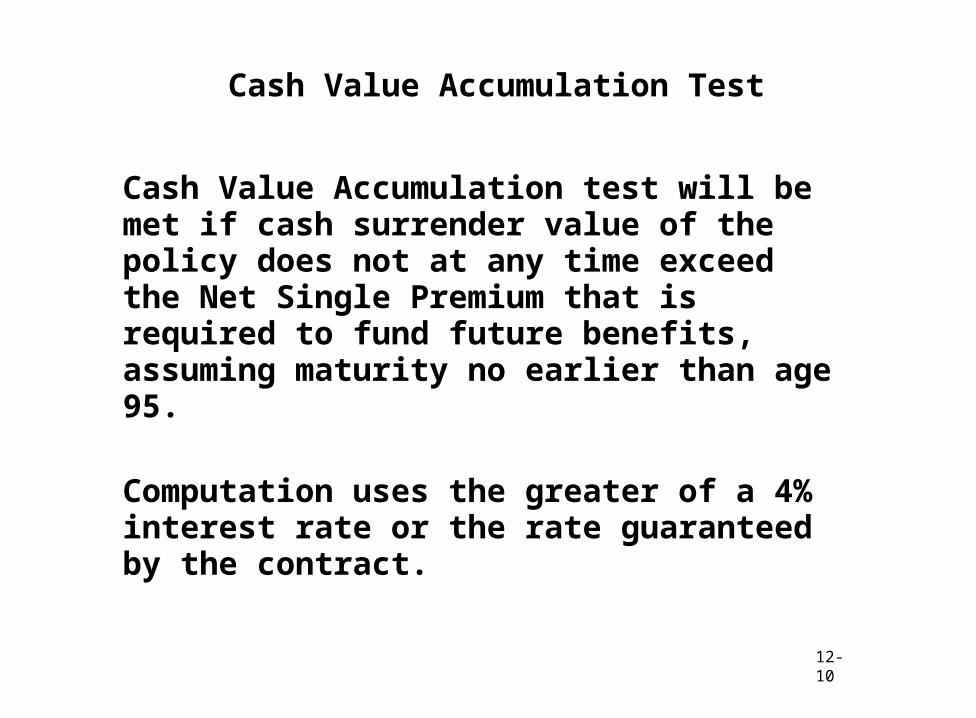

Cash Value Accumulation Test

Cash Value Accumulation test will be met if cash surrender value of the policy does not at any time exceed the Net Single Premium that is required to fund future benefits, assuming maturity no earlier than age 95.

Computation uses the greater of a 4% interest rate or the rate guaranteed by the contract.

12-11

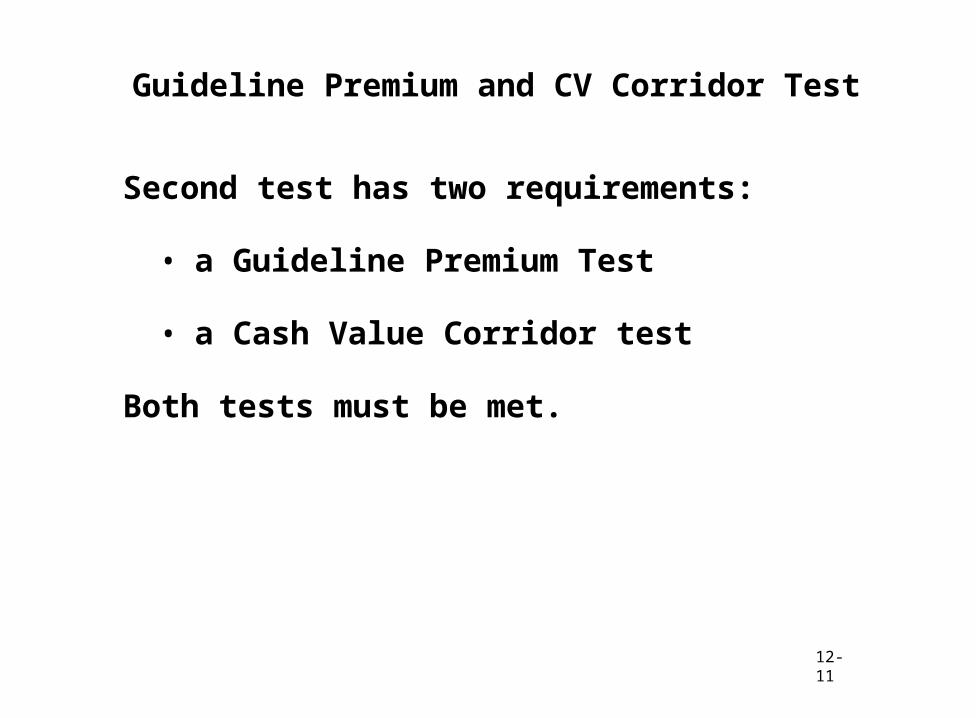

Guideline Premium and CV Corridor Test

Second test has two requirements:

• a Guideline Premium Test

• a Cash Value Corridor test

Both tests must be met.

12-12

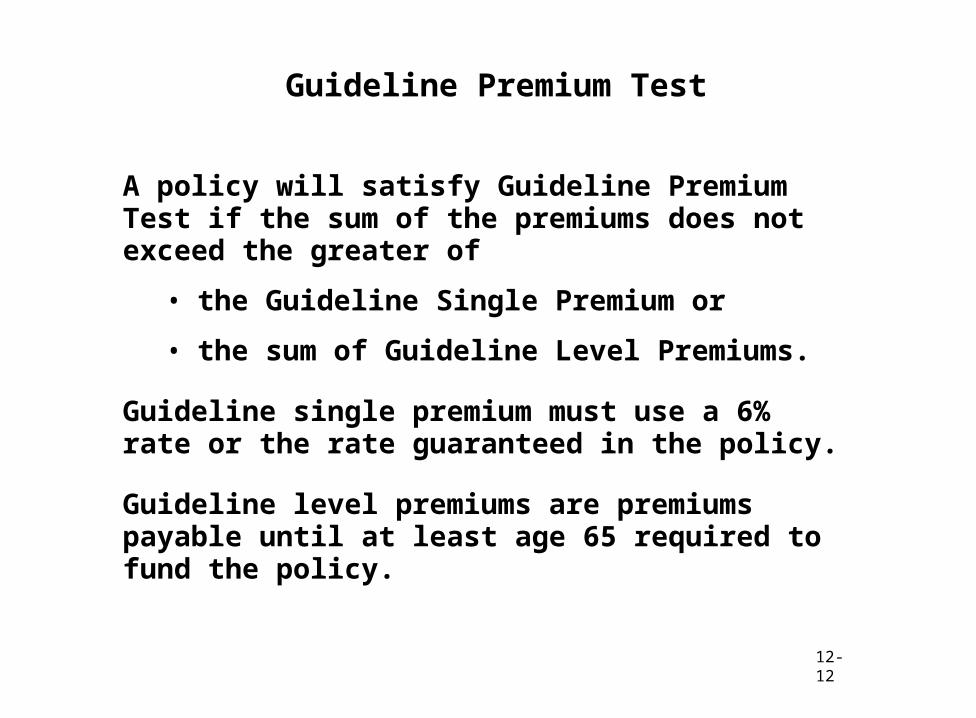

Guideline Premium Test

A policy will satisfy Guideline Premium Test if the sum of the premiums does not exceed the greater of

• the Guideline Single Premium or

• the sum of Guideline Level Premiums.

Guideline single premium must use a 6% rate or the rate guaranteed in the policy.

Guideline level premiums are premiums payable until at least age 65 required to fund the policy.

12-13

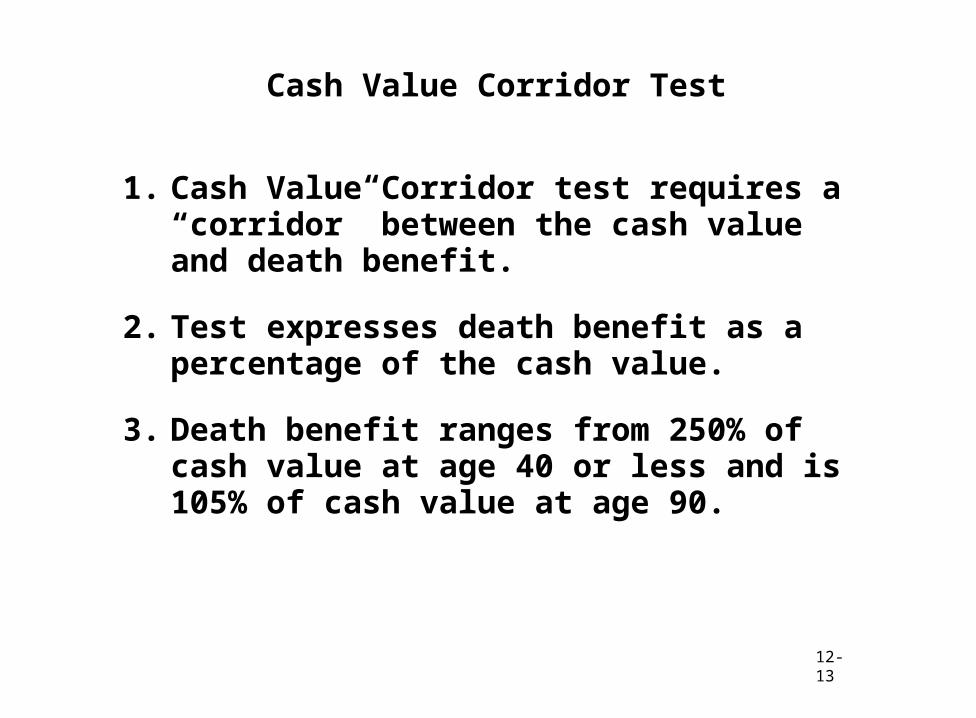

Cash Value Corridor Test

1. Cash Value Corridor test requires a “corridor” between the cash value and death benefit.

2. Test expresses death benefit as a percentage of the cash value.

3. Death benefit ranges from 250% of cash value at age 40 or less and is 105% of cash value at age 90.

12-14

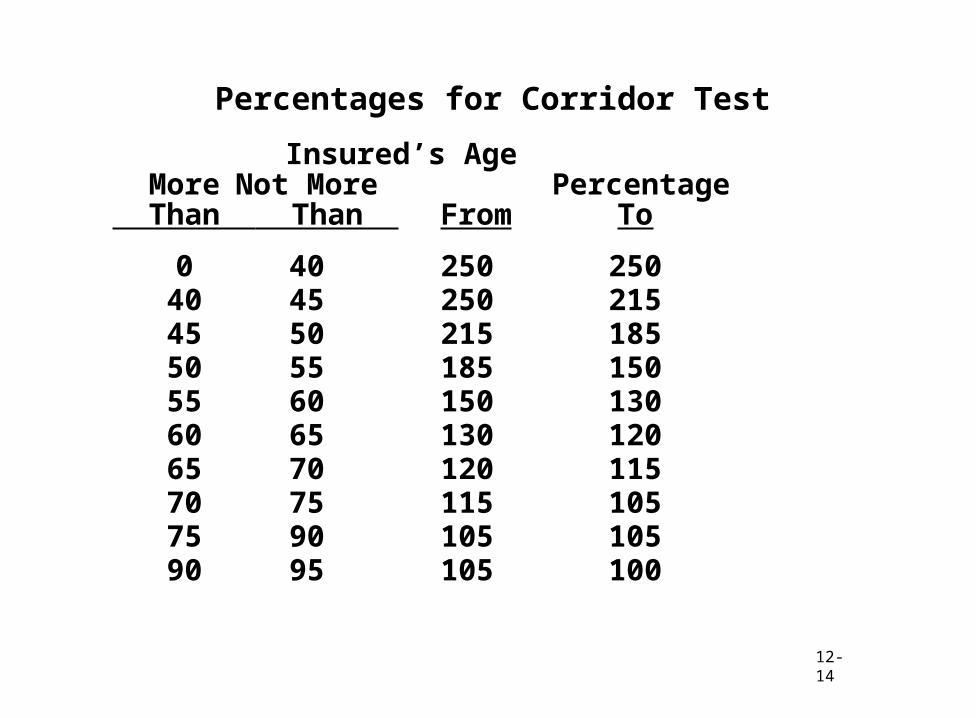

Percentages for Corridor Test

Insured’s Age More Not More Percentage

Than Than From To

0 40 250 25040 45 250 21545 50 215 18550 55 185 15055 60 150 13060 65 130 12065 70 120 11570 75 115 10575 90 105 10590 95 105 100

12-15

Current Life Insurance Products

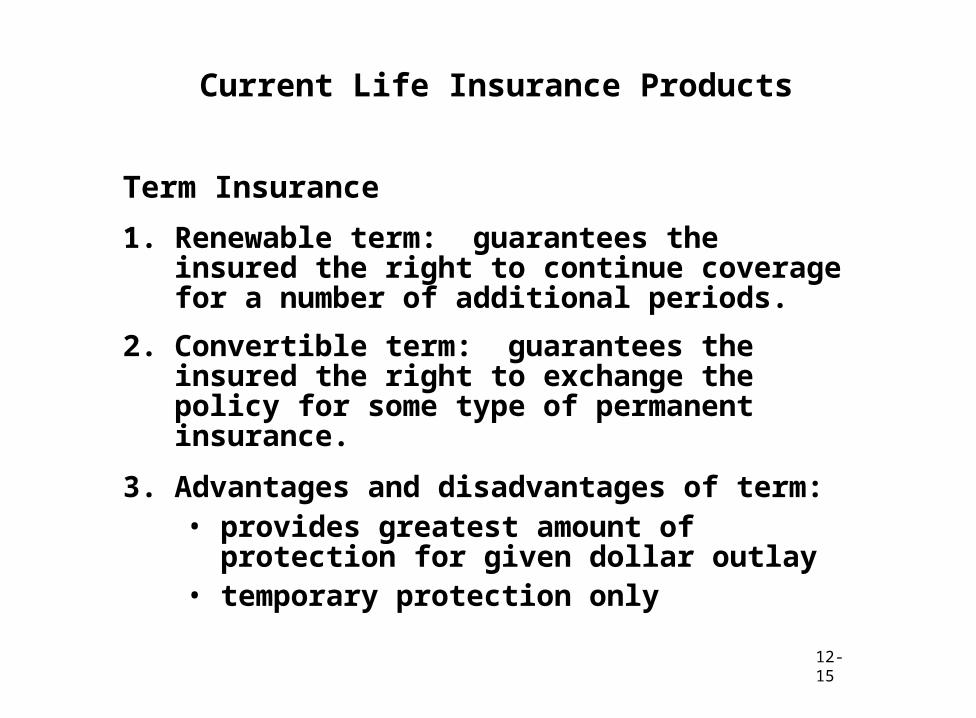

Term Insurance

1. Renewable term: guarantees the insured the right to continue coverage for a number of additional periods.

2. Convertible term: guarantees the insured the right to exchange the policy for some type of permanent insurance.

3. Advantages and disadvantages of term:• provides greatest amount of protection for

given dollar outlay• temporary protection only

12-16

Current Life Insurance Products

Whole Life

1. Straight whole life provides protection for insured’s entire lifetime (until age 100) with premiums payable for lifetime.

2. Limited-pay whole life provides protection for entire lifetime (until age 100) with (higher) premiums payable for a shorter time.

12-17

Current Life Insurance Products

Universal Life

1. Introduced in 1979 by subsidiary of stock brokerage firm, E.F. Hutton.

2. Subject to specified limitations, premium, cash value, and level of protection can be adjusted up or down to meet insured’s needs.

3. Premiums are credited to a fund, which is credited with policy’s share of investment earnings.

4. Fund provides source of funds to pay cost of pure protection (term) under the policy.

12-18

Current Life Insurance Products

Variable Life Insurance

1. A whole life contract in which insured has the right to direct how cash value will be invested.

2. Insured bears the investment risk in the form of fluctuations in cash value and amount of protection.

3. Amount of premium is fixed, but cash value and face amount vary, subject to a minimum.

12-19

Current Life Insurance Products

Adjustable Life Insurance

1. Allows the buyer to adjust face amount of the policy and premium over time.

2. Relationship between premium and amount of protection determine the cash value.

3. Based on this relationship, an adjustable life policy may be term or whole life.

4. When premiums paid exceed the cost of protection, the cash value increases.

5. When cost of protection exceeds premium, cash value or face amount decreases.

12-20

Current Life Insurance Products

Endowment Life Insurance

1. Endowment contracts no longer meet the Internal Revenue Code definition of life insurance.

2. Endowment policies are issued for a term period such as 10 or 20 years.

3. Endowment policies promise to pay face amount if the insured dies during the policy period and also to pay the face amount if the insured survives the policy period.

12-21

Participating & Non-Participating Life Insurance

1. Participating policies pay dividends

2. Originally issued only by mutual insurers

3. Dividend varies from margin built into premium

12-22

General Classifications of Life Insurance

1. Ordinary life - 60.6% of insurance in force

2. Industrial - less than 1% (0.2%) today, compared with 10% at one time

3. Group life - 37.5% of life insurance in force.

4. Credit life insurance - about 1.8%

Total life insurance in force exceeds $13 trillion

12-23

Other Types of Life Insurance

Besides life insurance issued by legal reserve insurers, a small amount (about 2.5%) of life insurance is written by other types of insurers.

1. Savings bank life insurance (NY, Mass, Conn)

2. Fraternal life insurance

3. Veterans life insurance

4. Wisconsin state life insurance fund