Embed Size (px)

Citation preview

Geopolitics: the blind side

UBS research focusWealth Management Research I June 2010

Geopolitics: the blind side

Geopolitical events are hard to predict and often destabilizing

Investment decisions rarely incorporate geopolitical risks

Economic tensions raise risk of geopolitical conflict

Stress points: resources, nationalism, ideology and income gaps

Financial market impact varies widely depending on events

Preventive steps can limit losses but reactions also matter

ab

2 Geopolitics: the blind side

Contents

Editorial 3

Highlights 4

Introduction 5Why geopolitics matters

Chapter 1 10Investing under geopolitical risk

Case studies 16Geopolitical hot spots

Natural resource needs: 17• An object in motion: China’s slowdown and its implications• Energy and nationalism: Russia, its neighbors and Europe

National strategic ambitions: 20• The Middle East heats up: the gathering storm over Iran and Israel• Asia’s nuclear brinksmanship: safer or more unstable?

Non-state ideological ambitions: 23• Terrorism: the unknown unknowns

Income inequality: 24• The future of the EMU: until stress do us part• Raising barriers: the allure of trade protectionism

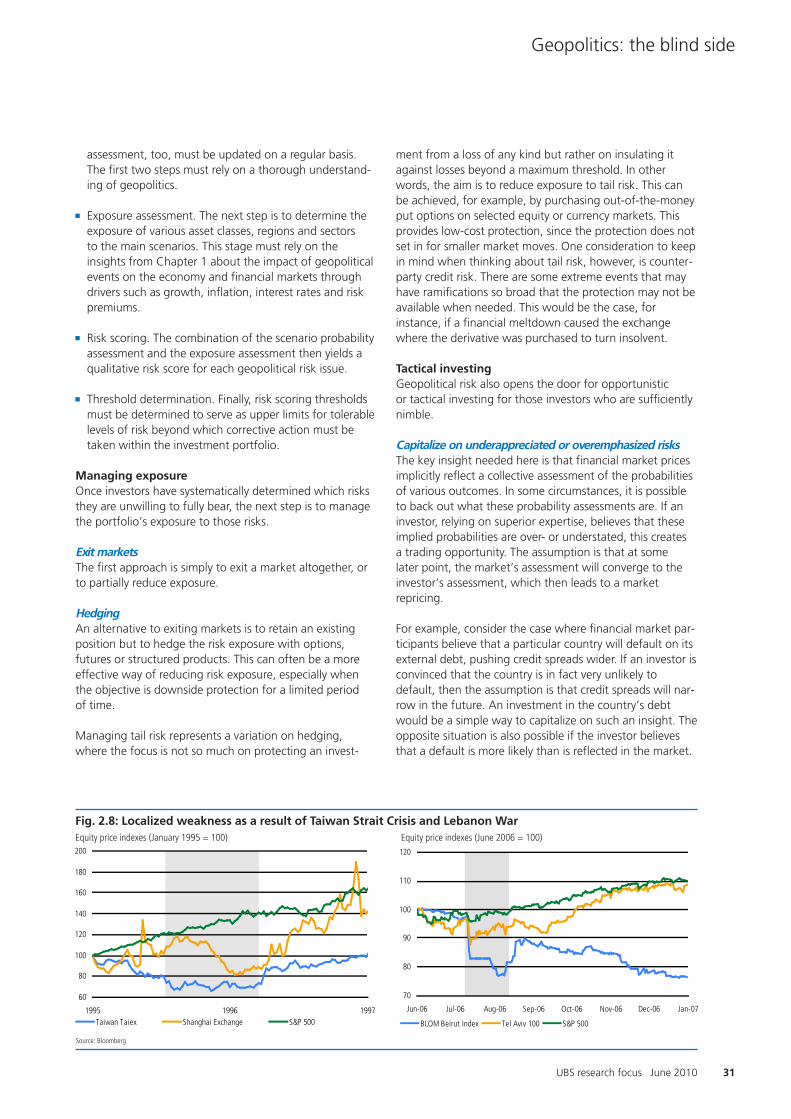

Chapter 2 28Geopolitical risk in a portfolio context

Conclusion 34The blind side

Bibliography 36

Publication details 38

This report has been prepared by UBS Financial Services Inc. (“UBS FS”) and UBS AG.Please see important disclaimer at the end of the document.Past performance is no indication of future performance. The market prices provided are closing prices on the respectiveprincipal exchange. This applies to all performance charts and tables in the publication.

3UBS research focus June 2010

Geopolitics: the blind side

Dear reader,

Geopolitical risk is in a constant state of flux, lurking in thebackground with the potential to blindside investors. Attimes, geopolitical risk is on the rise, making the world amore unstable place. Other times, the risk fades from view.

The end of the Cold War fundamentally altered the courseof history as the twentieth century drew to a close. Therelaxation of geopolitical tension in the 1990s coincidedwith the spread of globalization, quantum leaps in technol-ogy and privatization of state-owned industries, all ofwhich encouraged a further moderation of inflation andgrowing economic prosperity. In addition, the global econ-omy accrued a “peace dividend” as the threat of mutuallyassured destruction subsided and defense spending shiftedto more productive activities.

In recent years, however, economic activity and financialmarket performance have grown increasingly turbulent, inpart due to imploding asset bubbles – first technology andthen housing. But renewed geopolitical upheaval – such asthe 9/11 terrorist attacks, the proliferation of nuclearweapons capabilities in Asia and the threat of the Euro-zone’s breakup – also left their mark.

The attempted car bombing in New York’s Times Square,as well as the sinking of a South Korean warship in March,remind us how quickly events can unfold to alter thegeopolitical landscape. Moreover, the economic and politi-cal stresses that have surfaced in the aftermath of thefinancial crisis suggest that geopolitical conflict could esca-late further. Therefore, we think geopolitics will becomemuch more important in determining outcomes for theeconomy and financial markets than in the recent past.

Geopolitical events shape the economic environment andfundamental investment outlook. The type of geopoliticalevent may determine how financial markets behave andwhether the reaction is more temporary or sustained, andmore localized or global.

As economists, analysts and strategists, we calculate fore-casts using quantifiable variables that can be incorporatedinto statistical models. However, we must also consider

Kurt E. ReimanHead Thematic Research

how financial markets and the economy respond to a widespectrum of “real world” events that are not quantifiable,including the highly unpredictable realm of geopolitics. Butwhile assigning probabilities to potential geopolitical riskscenarios may be difficult, in no way should these risks bedismissed.

In our 2010 outlook, we identified the emergence ofgeopolitical threats as one of the “five things we believewill happen” this year. This statement generated numerousquestions and considerable feedback from readers whowanted a more thorough understanding of the investmentimplications.

In this UBS research focus, we seek to answer many ofthese questions, as well as: provide a useful framework forunderstanding how different geopolitical events arereflected in financial markets; survey the most potentiallyeruptive sources of conflict; illustrate how investors canpreemptively protect their portfolios from these risks; andoffer guidance on how to react to geopolitical events oncethey surface.

Mike RyanHead Wealth Management Research – Americas

4 Geopolitics: the blind side

Highlights

Economic tensions raise the risk of geopolitical conflictWe think geopolitics will become much more important indetermining economic and financial market outcomes thanin the recent past. Widespread economic dislocations, suchas higher unemployment, pervasive income inequality andmore government intervention in economic affairs, corrodepolitical stability. Tensions are already high between nationsconfronting natural resource scarcity, development of mili-tary and nuclear weapons capabilities, trade protectionismand fundamental clashes over ideology. While these trendsmay not necessarily be cause for alarm, they are certainlyworthy of greater attention. Therefore, we believe adeeper understanding of geopolitical risk and an assess-ment of the most important potential hot spots will provebeneficial to investors.

Stress points: resources, nationalism, ideology andincome gapsIn our view, geopolitical tensions fall into four broad the-matic categories: natural resource needs; national strategicambitions; non-state ideological ambitions; and incomeinequality. Each category contains different broad types ofgeopolitical threats, which themselves lead to a variety offinancial market outcomes:

Natural resource supply shocks, such as an oil embargo,would likely create stagflation, whereas a clash overaccess to resources could spark flight to safety flows.

National strategic ambitions, such as Iran’s acquisition ofa nuclear weapon or a standoff over Taiwan, would alsoincrease risk aversion. However, other strategic pursuits,like a full-scale nuclear attack or sustained armed conflictcould lead to extreme economic outcomes, such ashyperinflation or depression.

Ideological clashes usually surface in the form of suddenterrorist attacks, which are usually associated with flight-to-safety flows. But the outcome could be more devas-tating if the attack arrives in the form of a nuclear deviceor biological agent.

Income inequality could lead to trade wars and currencycrises, which would likely spell deflation and depression.

Geopolitical events are hard to predict and oftendestabilizingInvestors experienced two of the worst financial marketdownturns in postwar history during the past decadealone. There were some who saw problems on the hori-zon, but few predicted the two systemic shocks that fullyundermined confidence. Some viewed technology sharesas expensive before the bubble burst in 2000 and manythought the housing market was due for a correction in

2007. However, the 9/11 terrorist attacks and the glo balcredit crunch – two events that are defined by a “before”and an “after” – took nearly everyone by surprise.

Geopolitical events often appear unpredictable and uncer-tain before they take place. As a result, market participantsfrequently treat the subject as an afterthought. However,we think this is a mistake. Geopolitics can heavily influenceeconomic growth and asset returns and can blindside aninvestment portfolio.

Financial market impact varies widely depending onthe eventThe defining geopolitical events of the past century – thetwo world wars, the Cuban Missile Crisis, the OPEC oilembargo, the end of the Cold War and the 9/11 terroristattacks, to name a few – were felt in financial markets, butthe outcomes were highly varied. Some were long-lasting,some were short-lived. Certain events had a localizedimpact, while others were truly global. And some disruptedeconomic activity, while others were more benign.

Geopolitics must be understood as a type of risk that inter-acts with other sources of risk in an investment portfolio. Anegative geopolitical event will tend to increase the riskpremium and alter the direction of asset prices. However,when a geopolitical event also depresses economic growthand changes the course of inflation, then the effect onfinancial markets is likely to be more sustained. The direc-tion of the impact will depend on the asset in question,and the magnitude will depend on the severity and resolu-tion of the incident.

Preventive steps can limit losses but reactions alsomatterDiversification and ongoing risk assessment are importantprecautionary measures to limit losses, but how one reactsto the shock of a geopolitical event can be just as important,if not more so. When there is little transmission of a geopo-litical shock to the broader economy, as is often the case withsmaller-scale terrorist attacks, the effect on financial marketsmay be only temporary. As a result, the cost of hedging thesefleeting risks would likely outweigh the benefit.

One option to consider when investing during prolongedperiods of heightened geopolitical risk is to target assetsthat would be expected to perform well both in a baselinescenario and when tensions boil over. Another is to seeknatural hedges. For example, commodities would stand togain from conflict in the Middle East or a standoff overresource access between China and India. In addition, allocations to higher-quality government bonds, such as US Treasury securities, can offset declines when uncer-tainties surge.

Geopolitics: the blind side

5UBS research focus June 2010

Geopolitics: the blind side

Geopolitics reconsideredWith the world economy as globalized as it is today,regional or domestic events transmit rapidly to the interna-tional stage and can take many forms. People often thinkgeopolitics is primarily concerned with armed conflictbetween nations. While this certainly plays an importantrole, the concept is far broader:

A currency devaluation led to the 1994 Mexican pesocrisis.

The imposition of tariff barriers in the 1930s is widelyconsidered to have contributed to the severity of theGreat Depression.

The 2001 terror attacks in New York City quickly led totwo separate wars on the other side of the world, involv-ing the armed forces of multiple nations.

Each of these geopolitical events had massive financial and economic consequences. But too often, financial andeconomic decisions are made independently of politicalconsiderations. When attempting to predict future out-comes, financial analysts and economists typically lump“politics” in with other variables that are too uncertain andtherefore difficult to predict. In statistics, this is called the“error term.”

In 1943, sociologist Werner Cahnman defined geopoliticsthis way: “Historic forces operating within a geographicframework are supposed to condition political actionwhich, in turn, is to determine the course of economicdevelopment.” Notice how geopolitics is ultimately abouteconomics. In 2009, however, political scientists Ian Brem-mer and Preston Keat defined geopolitics as “the study ofhow geography, politics, strategy, and history combine togenerate the rise and fall of great powers and wars amongstates.” Although Bremmer and Keat do not specificallymention economic factors, they consider the “rise and fallof great powers” as principally an economic concept. Inother words, economics and geopolitics are inseparable.

A world at a crossroadsGeopolitical risk refers to low-probability, high-impactevents. They are the types of events that are proverbial“bolts out of the blue” or that appear unpredictable andhighly uncertain before they take place. But while geopoli-tics may be difficult to include in statistical forecastingtools, we have just demonstrated that it cannot be completely ignored either. After a decade bookended byan imploding tech bubble and the worst global recession in postwar history, investors have become acutely aware of how unanticipated events can blindside an investmentportfolio. Some saw dark clouds looming; few bracedthemselves.

Geopolitical risk on the riseIn our view, investors would be well advised to give moreattention to the effects of geopolitical risk on the economyand financial markets. Many signs point to an increasedlevel of geopolitical risk in the world today:

The fragile state of the world economy

The increased role of government in economic affairs

High unemployment rates and widespread incomeinequality

Decreased support for free trade measures and greateruse of protectionism

Growing scarcity of certain natural resources

Steadily higher military spending

Shifts in the global balance of power

Fundamental clashes over ideology

The heightened level of tension in key global hot spots

Introduction

Why geopolitics matters

6 Geopolitics: the blind side

Introduction

Fragile state of the world economyAlthough the global economy is steadily recovering fromthe recent “Great Recession,” the collateral damageremains acute and will take years, if not decades, to heal.Governments were quick to respond with fiscal stimulusand monetary policy measures. However, a sustainablegrowth path remains elusive for many developed countriesbecause of high household debt levels, depressed housingvalues and a diminished appetite for consumer credit.

Increased role of the state in economic affairsDeveloped countries face the greatest hurdles in gettingtheir economies back on a sustainable path. Unsurprisingly,they have also seen the largest increase in the role of gov-ernment in their economies (see Fig. 1). Meanwhile, moreand more disillusioned people, having concluded that“free markets” were largely responsible for creating thesystemic failures of the global financial system in the firstplace, are demanding that their governments solve theirfinancial and economic problems. In this tightly intercon-nected world, the heightened role of the state in economicaffairs suggests that geopolitics will become much moreimportant in determining outcomes for the economy andfinancial markets than in the recent past.

High unemployment rates and widespread incomeinequalityIn addition to bailing out the financial industry and provid-ing liquidity to financial markets, this new increased levelof government intervention in the economy is aimed atreducing unemployment, which has soared to the highestlevels in a generation in many countries, and at protectingthreatened key domestic industries (see Fig. 2). Youthunemployment is rampant in Europe and North America.Highly skilled workers in many industries, such as construc-tion, wholesale distribution and retail, face structuralimpediments to finding new employment as a result ofpermanent job losses. This comes at a time when rising levels of public debt are constraining governments in

their efforts to fund important social programs. And nowthat lifestyles are less often financed by credit, widespreadincome inequality is much more apparent, exposing thereality that incomes have stagnated for the past threedecades except for the highest earners (see Fig. 3).

Decreased support for free trade and greater use of protectionismSources of stress are not just confined to the weak finan-cial and employment conditions in developed countries;many of today’s problems transcend national boundaries.High unemployment has predictably stoked protectionistsentiment as politicians and special interest groups fightfor their constituencies. Moreover, increased governmentspending in the economy, a crowded regulatory reformagenda, slow progress on global trade liberalization andthe announcement of new tariff and non-tariff measuresall point to a rise in the use of protectionism. Against sucha backdrop, the long-enduring march of globalizationappears to be at a crossroads. The outcome – more conflictand heightened protectionism, on the one hand, or deeperintegration on the other – hinges more on political willthan on economic considerations.

These protectionist tendencies serve as an importantreminder that economic integration is only as strong as theinternational and national political institutions that arethere to support it. One needs to look no further than theEurozone to see how an underdeveloped political frame-work failed to prevent member states from getting into fis-cal hot water, which is heightening speculation about thefuture stability of the common currency and the potentialfor the whole experiment to unravel.

Heightened level of tension in key global hot spotsStrong political institutions are also necessary to advancecommon international security goals, such as confrontingterrorist threats and controlling the proliferation of nuclearweapons capabilities (not to mention ensuring they are

0

5

10

15

20

25

1990 1994 1998 2002 2006 2010

France Greece Germany Japan

Spain Switzerland UK US

Fig. 2: A sharp upturn in unemploymentUnemployment rate for selected countries, in %

Source: Bloomberg

0

25

50

75

100

125

1950 1960 1970 1980 1990 2000 2010

G7 Advanced economies

Fig. 1: Increased government role in the economyPublic debt as a share of GDP, in %

Source: International Monetary Fund

7UBS research focus June 2010

Geopolitics: the blind side

never used). But just as commitments are being made tofurther reduce stockpiles of nuclear weapons and to pre-vent disused nuclear materials from ending up in the handsof terrorists, security experts believe that many countries,including Iran, are steadily advancing – and may even beaccelerating – their acquisition of nuclear weapons capabil-ities (see Fig. 4 and Fig. 5). Nuclear proliferation stands todisrupt the regional balance of power in areas wherenuclear capabilities have developed and also raises uncer-tainty about the global balance of power. With nuclearproliferation increasingly likely in the years ahead, theimplications for international security are more uncertainthan ever.

Steadily higher military spendingAfter declining for many years, military expenditures haverisen steadily since the turn of the century and now exceedthe level that prevailed at the end of the Cold War (see Fig.6). The bulk of the increase in defense spending has takenplace in North America and Asia. Financing for the War on

Terror in Iraq and Afghanistan explains much of the spend-ing surge in North America, whereas the growth in defensespending in Asia is primarily the result of China’s aim toexpand its naval power beyond its own coastline. Whilethe overall trend in military expenditures does not ensurearmed conflict down the road, it does raise the stakes.

Growing scarcity of certain natural resourcesEfforts to control greenhouse gas emissions and improvethe efficiency of natural resource use have also been metwith frustration as political leaders fail to agree on a set of binding environmental principles. Natural resources areagain in great demand and increasingly scarce, leading tohigher input prices, a shift in alliances for industrial andenergy commodities and strategic stockpiling of invento-ries. A marked increase in commodities prices would likelybecome an additional source of instability much like the situation that occurred in 2007 and 2008, when agricul-ture and energy prices led to massive protests (see Fig. 7).Moreover, the simple fact that a country is an exporter

Fig. 5: Nuclear weapons states and programs

Source: Carnegie Endowment for Internationa Peace, Comprehensive Test Ban Treaty Organization Preparatory Commission

0

15

30

45

60

75

1945 1955 1965 1975 1985 1995 2005

US Former Soviet Union/Russia UK, France & China Total

Fig. 4: A steady destocking of nuclear weaponsGlobal nuclear weapons stockpiles, in thousands of warheads

Source: Norris and Kristensen (2009)

Country Date of first test Code name Comprehensive Test

Ban Treaty Status

Declared nuclear weapons states

US July 16, 1945 Trinity Signatory

Russia (former Soviet Union) August 29, 1945 First Lightning Ratifier

UK October 3, 1952 Hurricane Ratifier

France February 13, 1960 Gerboise Bleue Ratifier

China October 16, 1964 Lop Nor Signatory

India May 18, 1974 Smiling Buddha Non-signatory

Pakistan May 28, 1998 Chagai Hill Non-signatory

North Korea October 9, 2006 -- Non-signatory

Undeclared nuclear weapons states

Israel -- -- Signatory

States with suspected clandestine programs

Iran -- -- Signatory

30

35

40

45

50

55

1920 1935 1950 1965 1980 1995 2010

Excluding capital gains Including capital gains

Fig. 3: Highest earners take a larger share of the pieIncome share for the top 10% of earners in the US, in %

Note: Income is defined as market income and excludes government transfers.Source: Saez and Piketty (2009)

8 Geopolitics: the blind side

Introduction

of an economically important commodity significantlyinfluences relations among states and complicates important international security objectives, such as the difficulty in applying trade sanctions against Iran for its fail-ure to comply with international regulations regarding itsnuclear program.

Shifts in the global balance of powerRapid rates of economic growth in emerging market coun-tries is often considered in purely economic terms, butthere is also currently a very important geopolitical dynamictaking shape. Notice how in the aftermath of the financialcrisis, the G7 (an association of mostly developed nations)has been almost completely supplanted by the G20 (anassociation of emerging market and developed countries).This is hardly surprising. The financial crisis erupted indeveloped countries where it left many structural problemsin its wake, whereas emerging market countries cameaway relatively unscathed.

China is now the third largest economy in the world (calcu-lated using market exchange rates) and will soon eclipseJapan for the number two spot. This means that the great-est imbalances in international trade and finance – China’sstockpiling of US dollar-denominated foreign exchangereserves and the persistently large US current accountdeficit – exist between the world’s largest and soon-to-besecond-largest economies (see Fig. 8). It is for this reasonthat Larry Summers, former US Treasury Secretary, spoke ingeopolitical terms when he dubbed this relationship the“balance of financial terror.” It explains why the US is cau-tious about branding China a “currency manipulator” andwhy China is careful about how it phrases its views on theUS trade deficit and debt buildup. For either side to be cav-alier with this much at stake would be foolish.

This relative shift of economic power underscores an evolu-tion in the global geopolitical landscape from a worldlargely dominated by the US to a multi-polar world wherethe US is still the greatest power – but the gap betweenthe US and the rest is narrowing. As the relative balance ofpower shifts between and among nations, geopoliticalactivity will likely increase, with nations still adjusting tothe new strategic equilibrium. There may come a pointwhen nations “test” each other, trying to determine thelimits of power. Arguably, this is what Russia is doing nowin some former Soviet republics, such as Georgia andUkraine, and what Iran is doing as it continues to developa nuclear program. We could also look at China’s currencypolicy in this light. With the strategic boundaries betweensome great powers less defined than they once were,greater friction could emerge between current and emerg-ing great powers.

Pointing fingersThe world economy is far more interconnected than everbefore, which, in “normal” times, would be a sign ofgreater cohesion among countries and would tend toreduce the threat of geopolitical events. Unfortunately,these are not normal times. Policymakers will need to focuson pain management and important domestic problems.They will need to grapple with tough decisions about howto reduce unemployment, control public debt growth, raisedomestic exporters’ international competitiveness, regulatethe financial sector and retain access to scarce naturalresources. But after increasing the public sector debt loadand running an exceptionally loose monetary policy, policy-makers are facing these challenges with ever feweroptions. An increase in voter dissatisfaction could triggerincreased popular support for protectionist measures tosolve domestic economic concerns.

0

100

200

300

400

500

600

2000 2002 2004 2006 2008 2010

Energy Metals Food

Fig. 7: Energy and metals prices have reboundedCommodity price indices (January 2000 = 100)

Source: International Monetary Fund

0.8

0.9

1.0

1.1

1.2

1.3

1988 1992 1996 2000 2004 2008

Fig. 6: Sharp rise in post-Cold War military spendingWorld military expenditures, in trillions of USD

Note: Data for 1991 are unavailable.Source: Stockholm International Peace Research Institute Yearbook 2009, SIPRI Military Expenditure Database

9UBS research focus June 2010

Geopolitics: the blind side

A risk too important to be ignoredBecause geopolitics is unpredictable and cannot be timed,it is often treated as an afterthought when making invest-ment decisions, but it should not be ignored. According toBremmer and Keat, “A growing number of investors andpolicymakers understand the importance of political risk.Yet, they also know that they lack a comprehensive andsystemic set of tools for evaluating these risks.” While wedo not attempt to assign probabilities and timing to themajor hot spots throughout the world, we think theseevents can be better understood and evaluated in order toreduce the overall level of risk within an investment portfo-lio. In Chapter 1, we review the geopolitical hot spots thatwe think are the most potentially destabilizing to financialmarkets.

We have developed a framework for incorporating geopo-litical risk into the investment decision-making process. Wewill take these matters up in Chapters 1 and 2. Chapter 1explains how geopolitical risks can affect key economicvariables and asset classes, while Chapter 2 evaluates theserisks in a portfolio context. While this type of analysis doesnot lend itself to specific investment recommendations,there are numerous benefits, such as having a betterunderstanding of how geopolitics affects your investments,and knowing how to react to various geopolitical events,as well as how to better protect against them.

-3

-2

-1

0

1

2

3

1996 1998 2000 2002 2004 2006 2008 2010

US Oil exporters Germany and Japan

Other CA deficit countries China and emerging Asia Rest of the world

Fig. 8: Global imbalances continueCurrent account balance for selected countries and regions, in % of world GDP

Source: International Monetary Fund

10 Geopolitics: the blind side

Geopolitics matters to financial marketsThe idea that geopolitics influences financial market per-formance may seem intuitive to most investors. However, ifthe idea is so obvious, then why is the topic given such lit-tle time and attention in financial circles? Moreover, whengeopolitical events are finally discussed in a financial mar-ket context, why are they almost always mentioned inpassing as a blanket risk to equity market performance,without much reflection on some of the potential futurescenarios and implications for other asset classes?

The past century produced its share of monumental geopo-litical events (see Fig. 1.1). Given the magnitude, the biggersurprise would have been if these events had had no impacton financial markets at all. Indeed, these events did pullworld equity market indexes sharply lower (see Fig. 1.2).But each event has to be understood in its own context.

Bucking the broader global trend, US and UK equities gen-erated modest but positive real (inflation-adjusted) returnsduring World War II (WWII), which may have conditionedmany Anglo-Saxon investors to conclude that this periodwas just an extension of the economic recovery that fol-

lowed the Great Depression. But this would be a mistake,since it was the large mobilization of labor and resourcestoward supplying the war effort that benefited equities,despite the high rates of inflation that emerged.

On the other hand, German, Japanese and, to a lesserextent, French equity markets were dealt a serious blowduring WWII given hyperinflation and destruction to thecountries’ infrastructure and productive capacity. The 1973Organization of the Petroleum Exporting Countries (OPEC)oil embargo and accompanying stagflation also reducedreal equity returns to the same extent as during the twoworld wars, and the impact was felt pretty evenly through-out the world. And although the 9/11 terrorist attackswere a localized event, they had a sustained global impacton equity markets (see Fig. 1.3). This is quite possiblyrelated to the fact that the global economy was already inthe midst of a slowdown in response to the bursting of thetech bubble when the attacks took place.

Meanwhile, the Cuban Missile Crisis had a temporaryimpact on financial markets. Although the crisis broughtthe world to the brink of what could have been nuclear

Chapter 1

Investing under geopolitical risk

Geopolitics drives economic growth and asset returns. But since probability, causality,timing, magnitude and impact are difficult to assess, market participants rarely givegeopolitics the full attention it deserves. We think a deeper understanding will yieldbenefits to investors.

Fig. 1.1: Major geopolitical events of the past century

Source: UBS WMR

Date Event

28 Jul 1914 to 11 Nov 1918 World War I

1 Sep 1939 to 2 Sep 1945 World War II

25 Jun 1950 to present Korean War (ceasefire signed 27 July 1953)

1959 to 30 Apr 1975 Vietnam War

29 Oct 1956 to 6 Nov 1956 Suez Crisis

14 Oct 1962 to 28 Oct 1962 Cuban Missile Crisis

19 Oct 1973 to 18 Mar 1974 OPEC oil embargo

9 Nov 1989 Fall of the Berlin Wall

11 Sep 2001 to present 9/11 terrorist attacks and War on Terrorism

-100

-75

-50

-25

0

25

50

75

France Germany Japan UK US World World ex-US

World War I (1914-18) World War II (1939-48) Oil shock (1973-74)

Fig. 1.2: Different events, countries and outcomesReal equity return over selected periods, in %, calendar year returns

Source: Dimson, Marsh and Staunton (2008)

11UBS research focus June 2010

Geopolitics: the blind side

annihilation, the economy was never affected and politicalleaders found a peaceful solution. The crisis was reflectedin equity markets predominantly through heightened riskaversion and subsequent normalization when tensionseased (see Fig. 1.4).

The nexus of geopolitics and financeThe key to assessing the investment implications of geopol-itics lies in understanding how it affects the main drivers of investment returns. Fortunately, the same variables thatare relevant in any generic investment context are also relevant for assessing the impact of geopolitical events (see Fig. 1.5).

Imagine an idealized situation when financial markets capture all available information. In other words, stock and bond prices reflect the expected real interest rate andinflation rate, a risk premium to compensate for the uncertainty associated with risky investments and a liquid-ity premium to compensate for the risk of being unable torapidly convert an investment into cash. In addition, stockprices reflect earnings growth prospects, while corporatebond prices anticipate future credit trends and defaultrisks. Any short-term market price fluctuations from thisidealized starting point would result from changes to anyof these variables.

To the extent that political and geopolitical events affectthese factors, they have the potential to exert an influenceon financial market performance. The difficulty stems fromthe fact that geopolitical events often affect several vari-ables at the same time, thereby making attribution and anoverall assessment less straightforward than meets the eye.

To illustrate, assume for a moment that a conflict eruptsbetween two neighboring states, diplomatic solutions areexhausted and military action looms. Such news, if unex-pected, is likely to affect the following market drivers:

60

70

80

90

100

110

Jan-62 Apr-62 Jul-62 Oct-62 Jan-63 Apr-63 Jul-63 Oct-63 Jan-64

S&P 500 DAX

Fig. 1.4: Cuban Missile Crisis pulls equities lowerEquity price indexes (January 1962 = 100)

Source: Bloomberg

Fig. 1.3: 9/11 has sustained impact on global equitiesEquity price indexes (January 2000 = 100)

Source: Bloomberg

Flight to quality flows, as well as heightened liquiditypreferences and risk aversion, would tend to depress realinterest rates

Prospects for increased defense spending would likelypush inflation expectations higher

Increased uncertainty would be expected to increase therisk premium, at least among the affected countries

Meanwhile, a sustained military offensive could lead to:

A decline in trade, labor and investment flows, whichwould reduce economic growth prospects in more thanjust the affected countries

Higher commodity prices (for example, energy), whichwould weigh on economic growth and increase inflationexpectations, potentially across the global economy

A diversion of resources (including labor) to military usewould also likely drive up the cost of goods and wages

A negative geopolitical event that increases the risk pre-mium will typically alter the direction of asset prices. If theevent also depresses economic growth and boosts infla-tion, such as with a sustained military offensive, then theeffect on financial markets may be more long lasting (see

20

40

60

80

100

120

2000 2001 2002 2003 2004

S&P 500 FTSE DAX Nikkei 225

Fig. 1.5: The main drivers of investment returnsImpact on financial markets assuming an increase in each variable

Source: UBS WMR

Variable Stocks Bonds

Real interest rates – –

Inflation expectations – –

Risk premium – –

Growth expectations (economic, earnings) + neutral

Credit trends ? + (corporate bonds)

Liquidity premium – –

Negative inflation High inflationLow inflation

Deflation Stagflation

Goldilocks

High

gro

wth

Low

gro

wth

Neg

ativ

e gr

owth

Supercycle

12 Geopolitics: the blind side

Chapter 1

the box on page 15 for a more detailed discussion). Thedirection of the impact will depend on the asset in ques-tion, and the degree of the impact will depend on theseverity and the resolution of the incident.

The economic consequences of geopoliticsSince geopolitical events typically involve an abrupt changein behavior among conflicting parties, the impact on eco-nomic activity will almost always be disruptive and rarelygradual. The disruption can be small or large, and it canaffect political, business and personal ties to differentdegrees, depending on the severity and type of event (seeFig. 1.6). The shock generates a high degree of uncertainty,which is then reflected in a loss of business and consumerconfidence. These declines are typically large and signifi-cant relative to the trends in place before the shock.

The ensuing further erosion or recovery of confidencedepends on the nature of the geopolitical event and itsultimate resolution. If the shock is more temporary, such asa localized terrorist attack or a border conflict, then theeconomic consequences will likely be minimal and thefinancial market outcome will amount to flight to safetyflows. If allowed to persist, the large negative blow to con-fidence can linger as sentiment feeds on itself. Sustainednegative geopolitical events – such as global wars, resourcesupply shocks and trade protectionism – often produceshifts, or breaks, in existing trends and behavior, which canthen lead to a slowing of economic activity and changes inthe inflation outlook.

Fig. 1.6: Transmission of geopolitical shocks to economics

Since a sustained geopolitical event often affects the rela-tionship between two or more sovereign nations, itsimpact on economic activity will be visible in trade, capital(portfolio and foreign direct investments) and labor flows.This is the case even when the geopolitical event is con-fined to a conflict within a nation, such as a civil war orwhen a terrorist group attacks a sovereign state. In the for-mer, economic relationships with other nations would bealtered since capital and labor would be used to fight awar instead of to produce goods and services. In the latter,the attacked nation might change its trade policy withnations it considers “friendly” to the terrorist group thatcarried out the attack.

Sustained geopolitical events will also have a visible effecton the fiscal balance of the affected countries. Dependingon the severity of the event, fiscal consequences includeincreased government spending for counterterrorism sur-veillance and protection, as well as defense spending andinfrastructure reconstruction. The implication is that fiscaldeficits and debt-to-GDP ratios tend to rise in countriesaffected by geopolitical conflicts. With most countriesalready experiencing a sharp deterioration in these metricsin the aftermath of the financial crisis, a severe geopoliticalconflict would impair global fiscal balances even further(please see the April 2010 edition of the UBS researchfocus for more information on public debt).

Source: UBS WMR

Present

T E M P O R A R Y

Trade protectionismCurrency crisis Resource supply shock

Conflict over resourcesP E R S I S T E N T

Flight to safetyTerrorist attackAccess to nuclear weaponsBorder / territory disputeConflict over resources

Terrorist attackNuclear attackSustained global war

13UBS research focus June 2010

Geopolitics: the blind side

*Historical experience shows that hyperinflation results after sustained global wars.Source: UBS WMR

Sources of stress Geopolitical events Specific shock or trigger Asset consequences

G E O P O L I T I C A L E V E N T S I M P A C T O N A S S E T S

Natural resource needs

National strategic ambitions

Non-state ideological ambitions

Income inequality

• Resource supply shock

• Conflict over resources

• Access to nuclear weapons• Border / territory dispute

• Terrorist attack

• Terrorist attack

• Sustained global war*• Nuclear attack

• Trade protectionism• Currency crisis

• Russian energy embargo• Oil supply disruption

• Standoff over resource access between China and India• Coup in Saudi Arabia • Disputed water access rights

• Iran / North Korea develop nuclear capabilities• Taiwan / China escalation

• Car bomb in Times Square

• Nuclear or biological attack

• Broad escalation of military conflict • Use of nuclear first-strike capabilities

• US / China trade war• Euro collapse• US dollar collapse

Stagflation• Government bond prices down • Stocks mixed• Gold up• Commodities mixed

Flight to safety• Government bond prices up• Stocks down• Gold up• Reserve currency up• Commodities mixed

Hyperinflation• Paper assets down• Hard assets up

O RDepression / deflation• Government bond prices mixed• Stocks down• Gold mixed• Commodities down

Fig. 1.7: The varied effects of geopolitical shocks on financial markets

Bridging the divideWe can now see that there are not only numerous types ofgeopolitical events, but also a wide array of potentialfinancial market outcomes. By identifying the geopoliticalevents and potential triggers, the economic and financialmarket consequences begin to take shape. Therefore, webuilt a framework in order to bridge the gap betweengeopolitical events and financial markets. We categorizedgeopolitical stresses along four thematic lines and alsoincluded examples of specific events and triggers. For eachof these events, we identify the likely consequences forfinancial markets. While the framework is only as strong asthe level of understanding and nuanced assessment ofeach separate geopolitical conflict, we think it represents amarked improvement in how to think about geopoliticalrisk in an investment context. Fig 1.7 illustrates ourapproach.

Four thematic categories of geopolitical stressIn general, we think the four main geopolitical clustersinclude: natural resource scarcity, national strategic ambi-tions, non-state ideological ambitions and income inequality.

Natural resource needs. Endowment of critical naturalresources confers a strong geopolitical advantage toexporting countries. As we explore in detail in thegeopolitical case studies, Russia might seek to leverage

its position as Europe’s natural gas supplier through anembargo. As well, Iran could disrupt oil supplies in reac-tion to economic sanctions aimed at curbing its nuclearprogram or a preventive strike by Israel. Actions thatrestrict the supply of natural resources will most likelyconstrain economic activity and raise inflation, at least inthe short term, which would be a positive scenario forcertain commodity subsectors. However, not all clashesover resources lead to stagflation. Importing countrieswill do everything in their power to secure access to natural resources. A military standoff would likely triggerheightened risk aversion and an increase in the risk premium.

National strategic ambitions. When countries buildnew strategic capabilities or attempt to exert influenceover others, such as the pursuit of nuclear weapons inAsia, the initial phase can lead to a flight to safety. Even-tually, however, these developments can lead to armedconflict (see the box on page 15 for a more detailed dis-cussion). Geopolitical events that involve strategic ambi-tions tend to be negative for growth and fairly neutralfor inflation, assuming they do not escalate into a multi-country war or nuclear attack. The typical reaction inthese more muted scenarios, especially if the potentialfallout is large but the event is short-lived, is to parkmoney in safe haven assets, which currently include US

Europe after the devastation wrought during the twenti-eth century, hence the importance attached to maintain-ing the currency union.

Taking stockThis categorization of geopolitical conflicts is meant as aframework for evaluating geopolitical risk and its implica-tions for economic activity and financial markets. Clearly,the location, duration, magnitude, impact and catalyst ofeach geopolitical event will have a material effect on howgeopolitical risk manifests itself in various asset markets,hence the reason we provide detailed case studies ofpotential geopolitical hot spots. In Chapter 2, we will illus-trate how investors can preemptively protect their portfo-lios from the negative consequences of geopolitical riskand, most important, provide advice on how to react tothese events once they surface.

14 Geopolitics: the blind side

Chapter 1

Treasuries and gold. However, other strategic pursuits,such as a full-scale nuclear attack or sustained armedconflict, could lead to extreme economic outcomes, suchas hyperinflation or deflation.

Non-state ideological ambitions. Fundamentalistviews and ideological ambitions become geopoliticalevents when they erupt in the form of terrorist attacks.According to a recent study (Carrera and Mussio), terror-ist attacks usually only have a fleeting impact on equityreturns. The authors calculated the deviation from trendof daily equity returns for six countries in order to gaugethe strength of the impact of terrorist attacks on equi-ties. They conclude that only a small share of the 1,312recorded attacks from 1 January 2001 to 31 December2006 had a statistically significant negative effect onstock prices on that day, and this usually faded soonthereafter (see Fig. 1.8). Unsurprisingly, the magnitude ofthe effect was substantial for statistically significantevents, even after 11 days (see Fig. 1.9). Of all the terror-ist incidents, the authors concluded that only the 9/11attacks had a structural impact on equity market funda-mentals. If future terrorist incidents undermine vital infra-structure, such as a nuclear or biological attack, they willlikely have a persistent and damaging effect on equities(see the box on page 33 for a more detailed discussion).

Income inequality. Protectionism is a greater risk whenlabor markets are weak, as is the case now. Trade warsand currency crises are usually the by-products of incomeinequality among countries and the consequences areusually deflationary, as reduced trade flows would likelydepress overall economic activity. They also carry thepotential for a wider escalation of conflict. At its mostbasic level, the present crisis within the EMU stems fromincome inequality and differences in competitivenessamong member states. Recall that the EMU developedas an effort to reduce the potential for war within

0

10

20

30

40

1-day 6-day 11-day

Colombia India Spain Thailand UK US

Fig. 1.8: Small share of statistically significant attacksShare of terrorist attacks with statistical significance, in %

Note: Share of terrorist attacks that led to statistically significant negative equity returns on the day of the attackand after 6 and 11 days.Source: Carrera and Mussio (2009)

1-day 6-day 11-day

Min Max Min Max Min Max

Colombia -1.0 -12.4 -3.0 -24.8 -6.0 -14.2

India -1.4 -6.0 -2.6 -5.0 -2.4 -5.8

Spain -1.5 -4.1 -6.4 -8.4 -8.3 -9.2

Thailand -1.9 -16.8 -5.2 -11.1 -3.8 -16.1

UK -1.6 -1.9 -1.7 -1.7 -3.8 -3.8

US -1.3 -3.0 -4.0 -5.1 na na

Fig. 1.9: Range of negative impact can be quite largeRange of significant negative equity returns

Note: Minimum and maximum of statistically significant negative equity returns on the day of the attack and after6 and 11 days.Source: Carrera and Mussio (2009)

15UBS research focus June 2010

Geopolitics: the blind side

Each of the geopolitical hot spots that we outline in thecase studies has the potential to result in armed confronta-tion. When thinking about negative geopolitical events,war has the most devastating economic and social impact.It thus represents a worst-case scenario for how geopoliti-cal events impact trade, capital and labor flows, as well asthe overall level of economic activity.

The likelihood of war…According to the “liberal peace” view, trade interdepend-ence deters conflict and promotes peace by generatingeconomic benefits and raising the cost of conflict. Theopposing “realist” view states that trade may create con-flict by intensifying competition and increasing depend-ence on strategic goods. A recent paper (Glick and Taylor)provides empirical evidence for the liberal peace view. Theauthors estimate the likelihood of war between nationpairs based on:

The level of their bilateral trade

Whether they share land borders

Whether they are members of the same alliance

Whether one or more is a major power

The number of years of peace since the last conflict

The results for 9,942 country pairs from 1870 to 1997show that bilateral trade lowers the probability of war byabout 50%. This is good news since globalization has ledto a higher degree of trade interconnectedness over thepast several decades (see Fig. 1.10). Of course, factors

0

6

12

18

24

30

1970 1980 1990 2000 2010

Fig. 1.10: Steadily higher share of trade in global GDPGlobal exports as a share of GDP, in %

Source: Thomson Financial

-100

-75

-50

-25

0

25

0 1 2 3 4 5 6 7 8 9 10

Trade between belligerents Trade between belligerents and neutrals

Fig. 1.11: Impact of war on tradeContemporaneous and lagged impact of war on level of trade, in %

Note: The impact is calculated with a regression that controls for other drivers of trade. It measures the dropin the pre-war level of trade in the year of the war outbreak and subsequent years.Source: Glick and Taylor (2005)

other than trade activity influence the decision to go towar and can even outweigh the importance of tradelinks between countries.

…and its economic consequencesThese same authors developed a model to estimate theimpact of war on the level of trade among country pairs.To control for other factors that affect bilateral trade,they include variables such as a country’s share of globalGDP, per-capita GDP, shared land borders, whether thecountries share a common language, distance betweenthe capital cities and others. Their model points to astrong negative impact of war on trade (see Fig. 1.11).For 11,535 country pairs from 1870 to 1997, warreduces bilateral trade among warring states by a whop-ping 85% in the year when war breaks out. Furthermore,the impact on bilateral trade lingers even after the war isover and usually takes 10 years from the start of the warto fully recover. Five years after the cessation of war,bilateral trade is still 43% below its pre-war level.

Even the trade relationships of neutral countries areaffected. The model estimates that bilateral tradebetween a neutral country and a country that is at warfalls by 12% in the year a war begins. Only after eightyears is trade restored to pre-war levels. Thus, war has a large and persistent effect on the bilateral trade of belligerent and neutral countries. The loss in tradedirectly affects GDP growth and indirectly alters capitalflows and exchange rates. The magnitude of the esti-mated impact of wars on economic activity suggests that the consequences for asset markets and financialportfolios are great.

War: the most devastating geopolitical risk

Global tectonic shiftsAs we discussed in the Introduction, geopolitical risk maybe difficult to quantify and assess in terms of probability,but this does not mean it should be ignored altogether.Many of the steps leading to geopolitical unrest can beseen in advance; however, sometimes, geopoliticalshocks appear out of nowhere. Even if the timing andmagnitude of the fallout are uncertain, a thoughtfulconsideration of the risks can provide important informa-tion to investors. We have identified several geopoliticalhot spots that have the potential to impact financialmarkets in the intermediate to long term. In this section,we present some background information for each ofthese events and the steps that could lead to an escala-tion of conflict. In Chapter 1 and Chapter 2, we considerthese events in more general terms and show how theycould potentially impact financial markets and invest-ment portfolios.

Common geopolitical themesWe conclude that the critical geopolitical hot spotsthroughout the world can be broadly classified accordingto the four sources of stress we outlined in Chapter 1: natural resource needs (China, Russia); national strategicambitions (Iran, Asian nuclear); non-state ideological ambi-tions (terrorism) and income inequality (EMU breakup,trade protectionism). While we would agree with manyobservers who believe geopolitical stress is rooted in reli-gious, cultural and ethnic tensions, we think these areeither reinforced by or directed through each of these fouraforementioned main channels. There is definitely someoverlap among the four categories; for example, Iran’snuclear pursuits are clearly strategic but are also shaped byits role as a supplier of important energy commodities andhow it sees itself relative to richer developed countries.Having said this, the categories help to give some order towhat is otherwise a mostly chaotic subject.

16 Geopolitics: the blind side

CASE STUDIES

Geopolitical hot spots

Geopolitical hot spots can quickly deteriorate from a system of managed tension into afull-blown crisis. Although hard to quantify, an understanding of the most significantgeopolitical issues and potential future scenarios is a key input into sound financial riskmanagement.

Income inequality:• The future of the EMU: until stress do

us part• Raising barriers: the allure of trade

protectionism

Natural resource needs:• An object in motion: China’s slowdown

and its implications• Energy and nationalism: Russia, its neigh-

bors and Europe

National strategic ambitions:• The Middle East heats up: the gathering

storm over Iran and Israel• Asia’s nuclear brinksmanship: safer or more

unstable?

Non-state ideological ambitions:• Terrorism: the unknown unknowns

17UBS research focus June 2010

An object in motion: China’s slowdownand its implications

The consequences of inflexibilityOne might expect a report about geopolitical risks to fea-ture a discussion of potential friction points between Chinaas the emerging economic (and likely military) superpowerand the rest of the world. And, indeed, China’s expansiondoes create these types of risks. However, given the widelyheld view that China’s high growth rates will continueuninterrupted for years, we also believe that investorsshould not ignore risks associated with an unexpectedslowdown in this strong economic growth. We viewChina’s natural resource needs, domestic demographicprofile, national strategic interests and central economicplanning as important geopolitical and economic risks.

Resource hunger and neighborhood tensionsChina is now the world’s second-largest consumer ofcrude oil, over half of which is obtained through imports,and the leading consumer of copper, aluminum and zinc(see Fig. CS1). According to journalist Robert Kaplan in theMay/June 2010 edition of Foreign Affairs, “China’s actionsabroad are propelled by its need to secure energy, metalsand strategic minerals in order to support the rising livingstandards of its immense population, which amounts toone-fifth of the world’s total.” Throughout human history,competition for scarce natural resources has often been aflashpoint among and within societies. For any large eco-nomic and military power, the use of force becomes a morelikely option when resource prices are high.

Today, world trade routes are secured primarily by the USNavy. However, China is also developing a naval force inorder to support and protect its own growing global eco-

nomic interests, including the safe transport of naturalresources and traded goods (see Fig. CS2). The short-termrisk of China’s naval buildup is that it raises the odds of anaccidental skirmish with the US; the longer-term conse-quences relate to how it could shift the balance of militarypower in the area off China’s immediate coastline. AsChina becomes more influential in the region, the status ofTaiwan and long-running but largely dormant territorialdisputes with Japan and India become relevant sources ofpotential conflict. Given US security guarantees for bothTaiwan and Japan, an escalation of tensions in these areascould degenerate into a wider confrontation betweenChina and the US. Similarly, the stakes could be high ifChina’s territorial dispute with India over the disputed terri-tory of Arunachal Pradesh heats up.

Growing income, age and gender gapsChina faces several societal imbalances that could createinternal tensions and instability. An expanding income gapbetween China's rural and urban dwellers could be fertileground for internal discord. Also, similar to societies in theindustrialized countries, China's population is steadilyaging. In fact, it will age more quickly than that of both theUS and Europe from now through 2050, with its working-age population probably peaking in about five years (seeFig. CS3). China’s unbalanced gender structure could alsocreate internal discontent. Partly as a result of its one-childpolicy, expanding access to better prenatal diagnostics andother cultural factors, the Chinese male-to-female ratio forchildren aged 0-4 years is now at 1.23. In other words,there are 23% more young boys than girls (see Fig. CS4).

While not necessarily directly impacting geopolitical risks,these dramatic demographic shifts, in conjunction with arelatively inflexible political system, do have the potentialto create social instability, with consequences for China's

0

10

20

30

40

50

Iron

ore

Coal

Cott

on

Copp

er

Alum

inum

Soyb

eans

Corn Oil

Fig. CS1: A voracious appetite for resourcesChina's share of global commodity demand, in %

Source: Bloomberg, Thomson Financial

0

200

400

600

800

1,000

2010 2015China US

Fig. CS2: Chinese military spending growing rapidlyEstimated military spending, in billions of USD

Source: US Department of Defense, US Office of Management and Budget

CASE STUDIES Natural resource needs

economic growth and political institutions. We do notbelieve China’s restrictions on freedom of expression creategeopolitical risks per se. But free speech limitations makethe Chinese political system, in our opinion, less flexibleand therefore more vulnerable to shocks. Given China’smuch larger share of global economic output today, anincident similar to Tiananmen Square in 1989 or a politicalpower struggle would create far greater economic shock-waves.

Consequences of the state's firm grip on the economyKeep in mind that much of China’s economy is still con-trolled by the state:

The country’s managed exchange rate is the most obvi-ous source of geopolitical friction. As we note in the sec-tion on protectionism, nations that feel threatened orunfairly treated by China’s currency policy may imple-ment trade-related retaliatory measures. The currencypolicy also runs the risk of leaving China’s economyoverly dependent on exports.

Subsidized electricity prices risk sending the wrong pricesignals to consumers and producers, creating the poten-tial for enormous resource inefficiencies.

China’s subsidized bank lending risks redirecting finan-cial and natural resources into unproductive assets andcreating excess capacity within certain favored industrysectors that might then require their own price supportsand subsidies.

While the financial crisis seems to have shown that “freemarket capitalism” certainly has its limitations, centralplanning could result in a misallocation of resources thatmay lead to frictions with trading partners and ultimatelyhobble the Chinese economy.

Energy and nationalism: Russia, itsneighbors and Europe

Resource ownership lends powerRussia’s growing strength as an oil and natural gasexporter has reinforced its claim to power in the Eurasianregion (see Fig. CS5). Rather than integrating into the“Western” bloc as a strategic partner post the Iron Cur-tain’s fall, Russia often takes a decisively confrontationalstance. The oil price spike following the war in Georgiaand repeated disruptions of Western Europe’s gas supplyafter Russia’s disagreements with pipeline transit statesexemplify that access to scarce resources remains thegreatest leverage that Russia can exert over its neighborsand internationally.

Moscow’s firm grip on the energy sectorThe state’s grip on the Russian energy sector has beenexpanded in recent years, for instance, with the arrest ofMikhail Khodorkovsky of private oil company Yukos in2003 and the restructuring of the strategic Sakhalin proj-ect, for which Royal Dutch Shell had to give up majorityownership in 2006. The natural gas sector is dominated bymajority state-owned Gazprom, which owns the pipelineinfrastructure and so far holds a legal monopoly on naturalgas exports.

Resources + Russian nationalism = Russian resourcenationalism?Since the Soviet Union’s breakup, Russia has sought tomaintain strong links across Central Asia and EasternEurope to reestablish itself as a major power and to unifyits diverse regions as one nation. Taking a tougher stancein its energy policy against outside powers could be onefactor in this contest; fierce competition with the EU andthe US for political influence in the region could beanother. The victory of Russia-leaning Viktor Yanukovych inUkraine’s February 2010 election was widely perceived as a

18 Geopolitics: the blind side

0

6

12

18

24

30

1950 1970 1990 2010 2030 2050

China Europe US

Fig. CS3: China to age faster than the US and EuropeShare of population age 65 years and older, in %

Source: United Nations Population Division

1.00

1.05

1.10

1.15

1.20

1.25

1995-2000 2005-2010 2015-2020 2025-2030 2035-2040 2045-2050

China Europe US

Fig. CS4: China’s surplus of boysNumber of male births per female birth

Source: United Nations Population Division

19UBS research focus June 2010

Geopolitics: the blind side

success. Sizzling conflicts in the Caucasus, through which a number of important pipelines run, have caused instabil-ity, and the March 2010 bombings in Moscow might make future Russian military intervention in the regionmore likely.

Russia’s National Security Strategy of 2009 explicitly namedthe expansion of the North Atlantic Treaty Organization(NATO) in Eastern Europe a threat. For now, the accessionof Georgia and Ukraine has been put on hold. Also, USplans to station a missile defense system in Eastern Europe,which Russia had perceived as a blatant offense, have beenabandoned for the time being. The underlying conflicts ofinterest continue to be in place, however, and couldquickly resurface if the Western allies’ position changes.

Russia will also reap the benefits of higher energy prices,even though the rest of the economy is suffering from asevere recession and unemployment is rising. In this difficult economic environment, populist pressures couldbe on the rise. Furthermore, former president VladimirPutin, who promoted state dominance in the energy sec-tor, could reclaim the presidency in 2012; under his leader-ship, Russian resource nationalism would likely experiencea resurgence.

A disruption of energy suppliesRussia supplies 33% of Western Europe’s oil imports and40% of its gas imports, according to Europe’s Energy Por-tal. Such a high level of dependence makes a disruption ofsupply channels particularly harmful to European economicgrowth. Any cutoff of oil and natural gas supplies or insta-bility due to incendiary conflicts in the Caucasus regionwould cause energy prices to rise and have an adverseeffect on global economic growth (see Fig. CS6). Accord-ing to the International Energy Agency, a sustained USD 10per barrel increase in the price of oil could lower globalGDP growth by 0.5 percentage points in the subsequentyear. Reduced private sector influence in Russia’s energymarket could also reduce investment in further explorationand returns on investments, which would trigger evenmore supply pressures and higher energy prices.

0

50

100

150

200

250

300

Saud

i Ara

bia

Cana

da Iran

Iraq

Kuw

ait

Vene

zuel

a

UAE

Russ

ia

Liby

a

Nig

eria

Kaza

khst

an US

Chin

a

Qat

ar

Braz

il

0

300

600

900

1,200

1,500

1,800

Proven crude oil reserves (billion barrels, lhs)Proven natural gas reserves (trillion cubic feet, rhs)

Fig. CS5: Proven energy reservesCrude oil, in billion barrels Natural gas, in trillion cubic feet

Source: Energy Information Administration

0

40

80

120

160

2000 2002 2004 2006 2008 2010 2012

0

4

8

12

16

Crude oil (lhs) Natural gas (rhs)

Fig. CS6: A barometer of resource nationalism?Crude oil prices, in USD per barrel Natural gas prices, in USD per million BTUs

Source: Bloomberg

The Middle East heats up: thegathering storm over Iran and Israel

Heightened level of concernThe US desire to curb Iran’s nuclear ambitions is nothingnew, and during his first few months in office, PresidentObama pursued diplomacy over economic sanctions andmilitary force. Despite US outreach, Iran seems more closedto nuclear negotiations since the widely debated June2009 presidential election of Mahmoud Ahmadinejad. Theviolent crackdown on the protests that erupted after theelection have the US concerned with the regime’s humanrights violations, support for terrorism and threats tonational and global security, not to mention their nuclearaspirations. Iran denies it is developing nuclear weapons;however, its rejection of the UN Security Council’s offer toenrich uranium abroad – as well as the latest InternationalAtomic Energy Agency report of violations surroundinguranium enrichment, nuclear payloads and new enrich-ment plants – has left the international community increas-ingly concerned about Iran’s intentions.

Living with a nuclear IranSuzanne Maloney of the Brookings Institute believes thepolitical crisis in Iran is weakening the probability of suc-cessful engagement with the West: “the reality is that theviolence and continuing turmoil has made it almost impos-sible to envision a successful negotiation with Tehran inanywhere near the timeframe necessary to avert Iran’snuclear ambitions.” As the international community con-tinuously debates the best course of action, Iran may cur-rently, and certainly in the next five years, have nuclearweapons capabilities. The US would have to respond to anuclear Iran with clear guidelines surrounding unaccept-able behavior and be prepared to use military force ifTehran does not abide. James Lindsay and Ray Takeyh ofthe Council on Foreign Relations have laid out conditionsTehran must adhere to for successful containment to bepossible: “no initiation of conventional warfare againstother countries; no use or transfer of nuclear weapons,materials, or technologies; and no stepped-up support forterrorist or subversive activities.” Compliance with the list’srequirements is certainly achievable, but the questionremains whether Iran would take the US threat seriouslyafter once insisting it would never allow a nuclear Iran andthen being forced to accept it.

While containment of a nuclear Iran may be possible, it isfar more likely that its acquisition of nuclear capabilities willcreate further instability in the Middle East. The compli-cated and often conflicting outcomes of diplomacy, multi-lateral sanctions and military action are unknown. But it isquite likely that a nuclear Iran could emerge as a dominantpower in the Middle East, raising fears of nuclear strikes

and global war, driving a nuclear arms race among theGulf States and undermining the Nuclear NonproliferationTreaty (NPT). This is a situation the US and its allies wouldlike to prevent with sanctions – though military optionshave not been taken off the table.

Complications around successful sanctionsDuring trips to the Middle East, US Defense SecretaryRobert Gates noted that sanctions have only worked,“because there was very broad international support andthere were very few cheaters.” Success of sanctions onrefined petroleum would depend on Russia, which sellsmilitary goods to Iran, as well as China, which imports11% of its oil from Iran. Even with international support,sanctions could backfire and increase support for theregime if the negative effects felt by the Iranian populationare used to promote anti-American sentiment. This leavesthe US in the unenviable position of supporting the opposi-tion while aiming sanctions at the Revolutionary Guardsand the Ahmadinejad regime, despite sending signals toIran that it is no longer interested in diplomacy. US failureto diffuse the situation, either through diplomacy or sanc-tions, could prompt Israel to launch a preventive strikeagainst Iran in an effort to protect what it considers an“existential” threat to its existence.

Preventive strike: buying time worth the costs? The Israeli government has signaled a willingness and anability to launch aerial, non-nuclear operations against Iranif necessary. There is precedent for such action. Israelmounted successful preventive strikes against Syria in the1980s and Iraq in the 1990s amid fears that each was onthe brink of acquiring nuclear weapons capabilities. Suc-cessful preemptive action would once again depend onintelligence of nuclear facilities, successful air attacks andfollow-up raids to destroy remaining facilities. But thiscould prove more challenging this time around given thedecentralized, hardened and dispersed facilities in Iran. Anattack would likely slow, but not end, Iran’s nuclear pro-gram and retaliation would be inevitable. Israel could facemissile counterattacks and terrorism from surrogate groupsincluding Hezbollah and Hamas, which are supplied withrockets by Iran. Other states within the region might jumpinto the conflict as a way of showing solidarity with theirArab cousins against the Israelis. The US may also bedrawn into the conflict as American interests in Iraq andAfghanistan could be compromised. Iran might target Araboil facilities in the Persian Gulf or disrupt oil shipmentsthrough the Strait of Hormuz, which ships 20% of theworld’s daily oil consumption. With Iran as the fourth-largest oil exporter in the world and second within theOrganization of the Petroleum Exporting Countries (OPEC),such a disruption in oil supplies could push prices to never-before-seen highs (see Fig. CS7 and Fig. CS8).

20 Geopolitics: the blind side

Case studies

CASE STUDIES National strategic ambitions

21UBS research focus June 2010

Geopolitics: the blind side

Asia’s nuclear brinksmanship: safer ormore unstable?

Reaching all corners of AsiaSince their invention and use to end WWII, the threat ofnuclear weapons to humanity has been persistent, even ifthe threat level has fluctuated (see Fig. CS9). Since the collapse of the Soviet Union, the most likely nations to beengulfed in nuclear war have shifted to Asia (see Fig.CS10). South Asia and the subcontinent is a region marredby a history of violence and conflict since WWII, and thetwo nations with the greatest history of conflict, India andPakistan, both have a nuclear arsenal. The instability withinAfghanistan has spread to Pakistan, where remnants of theTaliban, the radical Islamic group, and other militant insur-gents are mounting fresh attacks. However, the bigger riskof nuclear war may lie to the north. Since 2006, Commu-nist-led North Korea has claimed it possesses nuclearweapons, although other nations suspect it is in the finalstages of development. Either scenario is disconcerting for the region, given North Korea’s history of unpredictablebehavior.

On the subcontinentSince the bloody partitioning of British India in 1947, ten-sions between India and Pakistan have persisted, includingthree wars and numerous armed skirmishes. While thegenesis for the regional tension remains complex, the pri-mary source – and also the likely trigger for another war –rests with the continuing territorial dispute over Kashmir. The region’s stability was again in doubt in 1998 whenPakistan officially joined India in the possession of nuclearweapons. Pakistan has a history of supporting the extrem-ist and separatist movements in Kashmir, which acceler-ated in the years following Pakistan’s acquisition of nuclearweapons. For example, the Kargil War of 1999 was precipi-tated by Pakistani forces crossing India’s border in Kashmir.The rationale behind supporting extremist groups for Pak-

istan and its willingness to escalate conflict with India is toforce international pressure on India to come to the bar-gaining table and resolve the dispute over Kashmir.

If another deadly terrorist attack were to occur withinIndia, this could be the tipping point for a nuclear conflicton the subcontinent. Indian officials believe that some ofthe most severe terrorist attacks that have occurred withinits borders were planned in accordance with Pakistan’sInter-Services Intelligence Directorate (ISI) – including theMumbai attacks in 2008 that took 170 lives. If a nuclearwar were to break out, the loss of life – both initially withthe explosion and later on from radiation – would be cata-strophic, given the region’s high population density. India ison the record saying that it would only resort to using“nukes” if Pakistan did first. However, previous Pakistaniregimes have said they would use nukes first if necessary.

While Indian and Pakistani relations have remained tense,the spreading of the Taliban insurgency into Pakistan isworrisome given Pakistan’s possession of nuclear weapons.The Taliban came to control Afghanistan in 1996 with thehelp of the ISI. The Taliban was soundly defeated in 2001during the US-led Operation Enduring Freedom. Remnantsof the Taliban pushed across the border and reconstitutedthemselves within the Federally Administered Tribal Areasin western Pakistan. Pakistan is now waging an internalwar against the Pakistani Taliban. The outright theft ofnuclear weapons does not seem likely. Pakistan’s nuclearparaphernalia is spread out among various Pakistani mili-tary bases, and the complexity of constructing a nuclearweapon reduces the risk that insurgents could successfullylaunch and detonate a nuclear device. However, if the Tal-iban gains ground and even potentially overthrows thegovernment, this would destabilize global security giventhe potential for nuclear weapons to be sold to terroristorganizations.

0

2

4

6

8

10

Saud

i Ara

bia

Russ

ia

UAE

Iran

Kuw

ait

Nor

way

Ango

la

Vene

zuel

a

Alge

ria

Nig

eria

Iraq

Liby

a

Kaza

khst

an

Cana

da

Qat

ar

Fig. CS7: Iran is the fourth-largest oil exporterLeading oil net exporters, in millions of barrels per day, 2008

Source: Energy Information Administration

0

12

24

36

48

60

1988 1989 1990 1991 1992 1993

Fig. CS8: Oil price doubled during Kuwait invasionReal imported crude oil prices, in USD per barrel

Source: Energy Information Administration

North by northeastWhile the situation in South Asia remains delicate, someexperts would argue the larger problem within Asia lies inNorth Korea. The sinking of a South Korean naval vessel inMarch serves as a sobering reminder of the potential fortensions to spark without notice. North Korea has a historyof provocation against the US, South Korea and Japan.Some of the provocations included: attempted assassina-tion of South Korean presidents; attacks on South Koreanwarships; and terrorism and kidnapping.

While reports vary, it is believed that North Korea is at leastclose to the final stages of developing nuclear weapons, ifnot already in possession of them. It is unclear whetherNorth Korea seeks to secure nuclear capabilities in order toobtain economic and strategic advantages if it disarms, orwhether talks are just a distraction from North Korea’s aimof becoming a nuclear power. North Korea’s recent historyof erratic behavior under Kim Jong-il is worrisome andmakes determining a trigger for nuclear war all the moreproblematic. Given Kim Jong-il’s poor health, successiontalks are important to understand in which direction NorthKorean foreign policy will embark. It is likely one of KimJong-il’s sons would take over and speculation is he wouldmaintain the same belligerent foreign policy.

22 Geopolitics: the blind side

Case studies

0

4

8

12

16

20

1947 1960 1973 1986 1999 2012

Fig. CS9: The "Doomsday Clock"Minutes to "midnight"

Note: The Doomsday Clock conveys how close humanity is to catastrophic destruction – the figurative midnight –and monitors the means humankind could use to obliterate itself. First and foremost, these include nuclearweapons, but they also encompass climate-changing technologies and new developments in the life sciences thatcould inflict irrevocable harm.Source: Bulletin of the Atomic Sciences

0

60

120

180

240

300

China Pakistan India North Korea

Fig. CS10: Nuclear weapons inventory in AsiaRange of estimated nuclear warheads, April 2010

Note: Despite two well-publicized nuclear tests in 2006 and 2009, there is no publicly available evidence thatNorth Korea has nuclear warheads in operation.Source: Federation of American Scientists

23UBS research focus June 2010

Geopolitics: the blind side

Terrorism: the unknown unknowns

The real blind sideIn 2002, former US Defense Secretary Donald Rumsfelddescribed instability in the war in Afghanistan as such:“There are known knowns. These are things we know thatwe know. There are known unknowns. That is to say, thereare things that we now know we don’t know. But thereare also unknown unknowns. These are things we do notknow we don’t know.” Despite the ridicule he endured atthe time, his categorization of the different combat risksgave a great deal of insight into the complexities of strate-gic decisions at a time of war.

Terrorism falls somewhere in between the knownunknowns and the unknown unknowns. For people inmany countries, such as Israel and Northern Ireland, terror-ism has regrettably become a reality of daily existence – aknown unknown. Prior to the 2001 terrorist attacks, flyingairplanes as missiles into buildings was unthinkable to mostpeople – an unknown unknown – even for those in theintelligence community. The 9/11 attacks also representeda structural break for financial markets, as we showed inChapter 1, and they ushered in a new era of governmentspending to finance counterterrorism efforts. As a result,the threat of a terrorist attack on vital infrastructure is nowa known unknown for experts.