Embed Size (px)

Citation preview

Emerging Financial Markets11. Raw Materials & Natural Resources

Prof. J.P. Mei

Note: Most materials used here are adopted from a research from Naissance. It is to be used for classroom discussion only.

Raw materials - Superior risk vsreturn tradeoff

Raw

Mat

eria

lsRa

w M

ater

ials

•• Unprecedented consumption (China, Unprecedented consumption (China, India) constrained supplyIndia) constrained supply

•• Possible upPossible up--tick in Economy will lift pricestick in Economy will lift prices

•• Pressure on US$ = migration to hard Pressure on US$ = migration to hard assetsassets

•• Low Correlation to stocks, bonds, Low Correlation to stocks, bonds, propertyproperty

•• Pension Funds ‘waking up’Pension Funds ‘waking up’

Superior Risk / Return TradeoffRa

w M

ater

ials

Raw

Mat

eria

ls

Equities (last 5 years)

Equities (Historical)

Naissance Raw Materials

Real Estate

Corporate Bonds

US Treasury Bill

-4

0

4

8

12

16

0 5 10 15 20 25

Risk - Annualized Std. Deviation %

Annu

aliz

ed R

etur

n %

better value

worse value

Rising Population = Rising demand

Raw

Mat

eria

lsRa

w M

ater

ials

Growth Means ConsumptionRa

w M

ater

ials

Raw

Mat

eria

ls

Source: World Bank

0 10 20 30 40 50 60

Years

China 1977 - 1987

Republic of Korea 1966 - 1977

India 1980 - 1998

Brazil 1961 - 1979

Turkey 1857 - 1877

Japan 1885 - 1919

Unites States 1839 - 1886

United Kingdom 1780 - 1888

Doubling of GDP per person

Unprecedented ConsumptionRa

w M

ater

ials

Raw

Mat

eria

ls

Source:Goldman Sachs

Estimated Year China, India and Russia GDP surpass developed economies

2000 2010 2020 2030 2040 2050

China

India

Russia

UK Germany Japan USA

Italy France Germany Japan

Italy France Germany

China: Give vs TakeRa

w M

ater

ials

Raw

Mat

eria

ls

Source: Rio Tinto

Alumina Lead Molybdenum TinBorates Salt Talc Thermal CoalCopper TiO2 feedstockIron Ore Zinc

Copper Steel Aluminum MagnesiumNickel Titanium Pigments Lead ZincPlatinum

Raw Materials

Processsed Materials

ExporterImporter

ExporterImporter

Example: Iron oreRa

w M

ater

ials

Raw

Mat

eria

ls

China - iron ore imports

0

50

100

150

200

250

300

350

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

Mill

ion

tonn

es

Source: Financial Times

(in orange: forecasts)

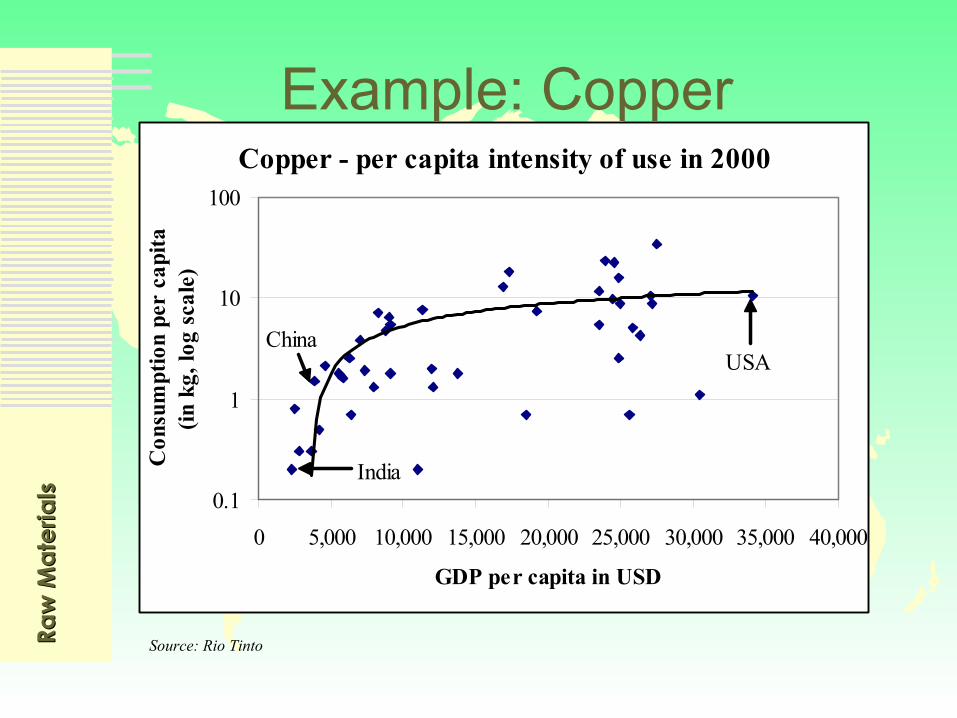

Example: CopperRa

w M

ater

ials

Raw

Mat

eria

ls

Source: Rio Tinto

Copper - per capita intensity of use in 2000

0.1

1

10

100

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000

GDP per capita in USD

Con

sum

ptio

n pe

r ca

pita

(in k

g, lo

g sc

ale)

USAChina

India

Example: Chinese Timber ImportsRa

w M

ater

ials

Raw

Mat

eria

ls

Source: FAO

2003 – 2005 estimates

Rising Chinese imports

0

10

20

30

40

50

1997 1998 1999 2000 2001 2002 2003 2004 2005

Mill

ion

Cubi

c Met

ers

Chinese Timber Consumption: Driving ForcesRa

w M

ater

ials

Raw

Mat

eria

ls

•• Privatization of statePrivatization of state--owned housingowned housing

•• 2008 Beijing Olympics: 2nd largest public 2008 Beijing Olympics: 2nd largest public work i.e. 100 work i.e. 100 –– 130 million square feet of 130 million square feet of new housing (670,000 units) new housing (670,000 units)

•• 1998 Logging Ban implemented due to 1998 Logging Ban implemented due to erosion = constraints in forest usageerosion = constraints in forest usage

•• Explosive industrial growth (Explosive industrial growth (ieie GDP +8,5%)GDP +8,5%)

Timber Investment ReturnsRa

w M

ater

ials

Raw

Mat

eria

ls

Source: Hancock Timber Resource Group

Performance of Timber Portfolios in different regions over the past 20 years

0%

5%

10%

15%

20%

10.00% 15.00% 20.00% 25.00% 30.00%

Pacific Northwest

British Columbia

New Zealand

Fewer CompetitorsRa

w M

ater

ials

Raw

Mat

eria

ls

Source: Cazenove

Proportion of production controlled by top 5 producers

0%

20%

40%

60%

80%

100%

Platin

umDiam

onds

Traded

iron o

re

Titaniu

m feed

stock

Nickel

Traded

Therm

al Coa

lAlum

inaCop

per

Alumini

umCok

ing C

oal

Gold Zinc Steel

Pension Funds ‚Waking Up‘

Raw

Mat

eria

lsRa

w M

ater

ials

•• Largest Dutch Pension Fund (ABP) Largest Dutch Pension Fund (ABP) allocating up to 5% of $160 billion allocating up to 5% of $160 billion

•• Goldman Sachs now recommends Goldman Sachs now recommends allocation of 5% to US institutionsallocation of 5% to US institutions

•• AIG established own raw materials AIG established own raw materials index, allocating 3% of own fundsindex, allocating 3% of own funds‘Sheep like behavior’ will drive raw ‘Sheep like behavior’ will drive raw material price increasesmaterial price increases

Raw

Mat

eria

lsRa

w M

ater

ials

Raw Material Index CompositionAgriculture Orange Juice 0.66% ForestryWheat 2.33% Oats 0.50% Timber 10.00%Corn 1.33% Silk 0.15% Rubber 1.00%Cotton 1.00% Flaxseed 0.15%Soybeans 1.00% Industrial MetalsLive Cattle 1.00% Precious Metals Copper 7.00%Coffee 1.00% Gold 15.00% Iron Ore 6.00%Rice 1.00% Platinum 6.00% Nickel 4.00%Palm Oil/Soybean Oil 1.00% Silver 2.00% Aluminum 1.20%Live Hogs 0.67% Palladium 1.75% Lead 0.50%Sugar 0.66% Zinc 0.40%Azuki Beans 0.66% Energy Tin 0.40%Cocoa 0.66% Crude Oil 20.00%Wool 0.66% Heating Oil/Diesel 3.00%Barley 0.66% Unleaded Gas 3.00%Canola 0.66% Natural Gas 3.00% Total 100.00%

China Net Imports

Σ 's 79.33%

PerformanceRa

w M

ater

ials

Raw

Mat

eria

ls

Name YTDCompounded

Annual ReturnAnnualized

STD1 S. Korean KOSPI Index 13.7% 15.8% 38.1%2 Naissance Raw Materials 14.0% 14.7% 18.1%

3Lehman Brothers Treasury Bond Index -3.1% 6.9% 9.3%

4 Barclays CTA Index 3.2% 6.5% 8.7%

5JP Morgan World Government Bond Index 4.2% 6.1% 7.3%

6Dow Jones AIG Commodity Index 5.6% 5.2% 15.3%

7 S&P Commodity Index 5.7% 4.3% 17.2%8 Treasury Bills US 0.6% 3.6% 0.5%9 S&P 500 13.7% -1.1% 18.8%

10NASDAQ Composite Index 29.9% -1.5% 37.5%

* August 1, 1998 till July 31, 2003

Low Correlation to Stocks/ BondsRa

w M

ater

ials

Raw

Mat

eria

ls

NRM EAFE S&P 500 JPMGNaissance Raw Material (NRM) 1.00

MSCI EAFE* (EAFE) 0.18 1.00

S&P 500 0.13 0.84 1.00JP Morgan Gov't Bond Index (JPMG) 0.19 0.04 -0.11 1.00

*MSCI World excluding North America

Source: MSCI, Bloomberg

Greenback vs GreenspanRa

w M

ater

ials

Raw

Mat

eria

ls

US Living beyond its means:US Living beyond its means:

US Consumer; Corp. debt at all time highsUS Consumer; Corp. debt at all time highs

Budget Deficit (financing of Iraq)Budget Deficit (financing of Iraq)

Unprecedented Trade Deficit and GrowingUnprecedented Trade Deficit and Growing

FED has ‘little rope left’ FED has ‘little rope left’

US borrowing other peoples’ savings (China, US borrowing other peoples’ savings (China, Japan) to make ends meetJapan) to make ends meet

US$ weakness shifts investor attention to hard assets

Leveraged US ConsumerRa

w M

ater

ials

Raw

Mat

eria

ls

Rising Household Debt

0

2,000

4,000

6,000

8,000

10,000

1974 1981 1988 1995 2002

in b

illio

n 19

96 U

SD

40%

50%

60%

70%

80%

90%

Household Debt Household debt as % of GDP

Uncle Sam Borrows too Much !Ra

w M

ater

ials

Raw

Mat

eria

ls

Rising Public Debt

01,0002,0003,0004,0005,0006,0007,000

1974 1981 1988 1995 2002

in b

illio

ns 1

996

US

D

30%

40%

50%

60%

70%

Public debt Public debt as % of GDP

Weaker $ needed to Reverse Trade DeficitRa

w M

ater

ials

Raw

Mat

eria

ls

Rising Current Acount Deficit

-500-400-300-200-100

0100

1974 1981 1988 1995 2002in b

illio

ns 1

996

USD

-6.0%

-4.0%

-2.0%

0.0%

2.0%

Current Account deficitCurrent account deficit as % of GDP

Investment Strategy:Ra

w M

ater

ials

Raw

Mat

eria

ls

• Highly diversified

• Index Approach

• Emphasise Commodities China / India need in greatest quantities

• Prefer Capital intensive commodities, with long lead time to adjust supply (ie 7 yrs to start new Copper mines)

• Precious Metals raised to about 25% due to US$ malaise

• 18-36 mos view – modest annual adjustments

AIG Guarantee: An Interesting Product Feature

Raw

Mat

eria

lsRa

w M

ater

ials

•• Optional Optional –– for risk averse investorsfor risk averse investors

•• AAAAAA

•• 100% capital guarantee100% capital guarantee

•• 8 years8 years•• 100% participation in capital 100% participation in capital

appreciationappreciation•• Monthly liquidityMonthly liquidity

Terms & ConditionsRa

w M

ater

ials

Raw

Mat

eria

ls

Flat Fee- with guarantee 2.00%- without guarantee 1.25%

Performance Fee 20.00%High Water Mark YesPlace of domicile Cayman IslandsMinimum Investment USD 100,000Currency of denomination EUR / USDHedging Policy Currency hedgedRedemption policy Monthly Reporting of NAV Monthly (more frequently

on request)Custodian UBSAuditors PricewaterhouseCoopersLawyers Maples & CalderPortfolio Administration Citco