Embed Size (px)

Citation preview

11 October, 2016, Petten

#REmap

◉ IRENA’s REmap programme explores potential, cost and benefits

of doubling the share of renewables in global energy mix (SE4ALL

objective), key to realize SDG 7: Affordable and clean energy

◉ Technology Options:

◎ This is no a target setting exercise

◎ Each technology option is characterized by its cost and potentials

◎ Technology options can be combined into roadmaps or plans and translated into

policy action

◉ Includes power, district heat, end-uses (industry, transport, buildings)

◎ Including sector coupling and power systems aspects

◉ Developed together with and validated by country experts

The REmap approach

2

#REmap

◉ REmap global analysis issued March 2016

◉ Today 50 country roadmaps covering 85% of global energy use ◉ 10 country reports, 4 regional reports

◉ Bottom-up analysis of technology options to accelerate RE use ◉ Developed in close cooperation with country experts

◉ Leading institutes CNREC, NREL, UCC etc.

◉ All data, assumptions and detailed results are available online: ◉ www.irena.org/remap - new REmap on REsource Dashboard

◉ Analysis can inform areas for cooperation and joint action, including

investment, cost, benefits (climate, environment, security, macro-

economics) of possible new RE objectives

Country potentials and technology roadmaps

3

#REmap

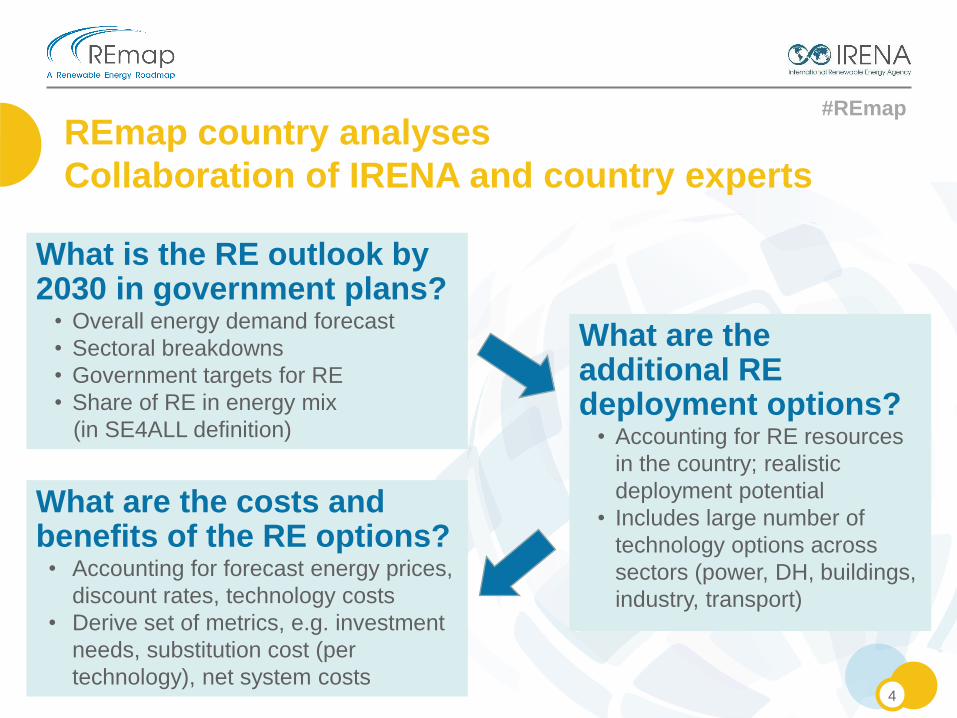

REmap country analyses

Collaboration of IRENA and country experts

4

What is the RE outlook by 2030 in government plans?

• Overall energy demand forecast

• Sectoral breakdowns

• Government targets for RE

• Share of RE in energy mix

(in SE4ALL definition)

What are the costs and benefits of the RE options? • Accounting for forecast energy prices,

discount rates, technology costs

• Derive set of metrics, e.g. investment

needs, substitution cost (per

technology), net system costs

What are the additional RE deployment options?

• Accounting for RE resources

in the country; realistic

deployment potential

• Includes large number of

technology options across

sectors (power, DH, buildings,

industry, transport)

#REmap

◉ Sustainable energy and climate change objectives can be reached

by doubling the share of renewable energy by 2030

◉ Doubling renewables in the world’s energy mix by 2030 will lead to

savings exceeding costs up to 15 times

◉ Savings related to air pollution alone are up to 10 times more

than costs

◉ The transition to renewables, with greater energy efficiency, can

limit the global temperature increase to below 2 degrees

◉ Doubling the share of renewable energy by 2030 is feasible, but

only with immediate, concerted action in transport, buildings

and industry

REmap 2030 highlights

5

#REmap

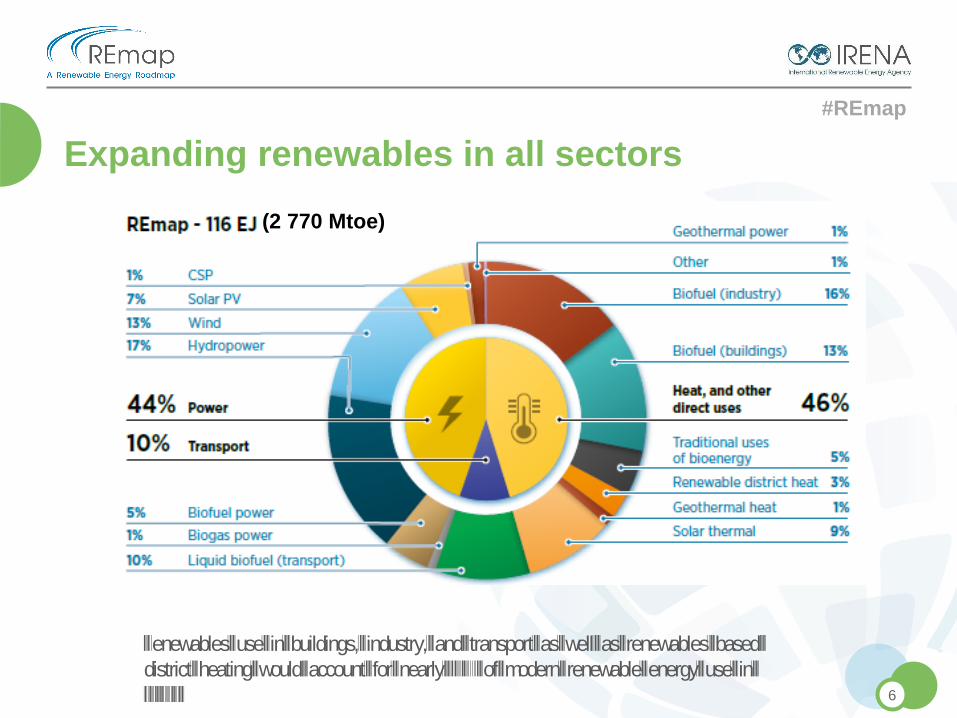

Renewables use in buildings, industry, and transport as well as renewables-based

district heating would account for nearly 60% of modern renewable energy use in

2030

Expanding renewables in all sectors

6

(2 770 Mtoe)

#REmap

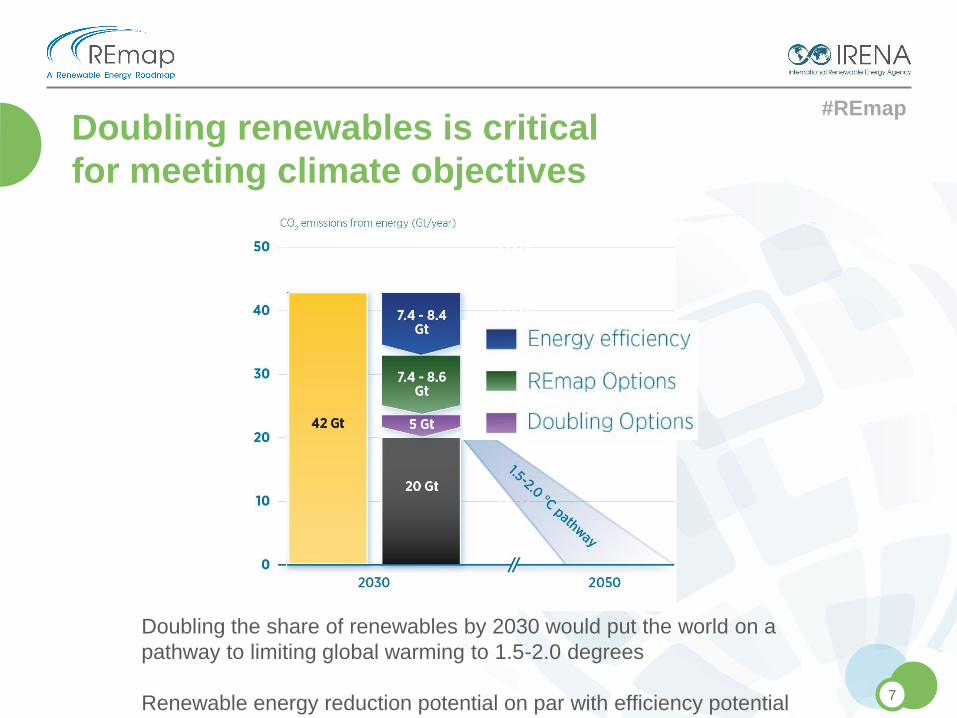

Doubling the share of renewables by 2030 would put the world on a

pathway to limiting global warming to 1.5-2.0 degrees

Renewable energy reduction potential on par with efficiency potential

Doubling renewables is critical

for meeting climate objectives

7

#REmap

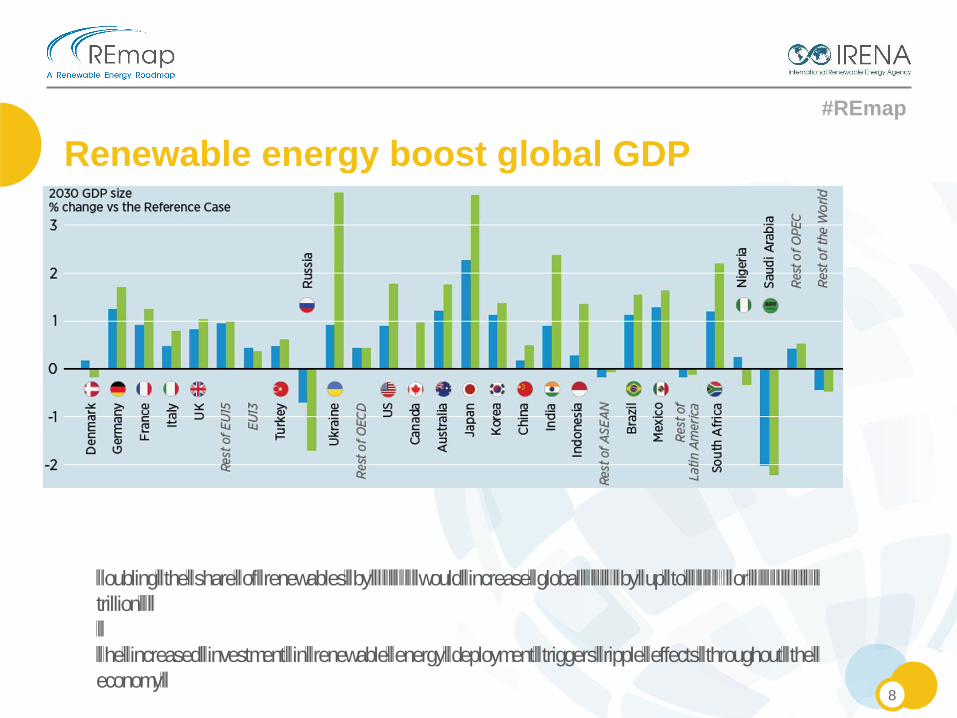

Doubling the share of renewables by 2030 would increase global GDP by up to 1.1% or USD 1.3

trillion

The increased investment in renewable energy deployment triggers ripple effects throughout the

economy

Renewable energy boost global GDP

8

#REmap

REmap country and regional reports

9

November 2014 January 2015 November 2015 June 2014

October 2015

◉ Purpose: translate analysis into actionable options

◉ Dominican Republic, Germany, India, Indonesia,

China, Mexico, Poland, UAE, United States, Ukraine,

Africa, ASEAN and G20 analysis completed

◉ EU, Russia, South Africa and Thailand reports in

preparation

#REmap

◉ Project for the European Commission, in cooperation with MS

◉ Goal: advise regarding options in all sectors and their implications

to meet the 27% 2030 RE target and role RE can play for

decarbonisation

◉ 1st working group meeting Brussels 20 October

◉ Prepared detailed PLEXOS model to study power sector flexibility

and integration issues

◉ Detailed REmap analysis for 11 largest EU countries (70% of energy

use), streamlined quickscan analysis for the remaining 17 members

◉ Belgium, Cyprus, Denmark, France, Germany, Italy,

Netherlands, Poland, Spain, Sweden, UK

◉ Calibrated Reference Case with latest PRIMES Reference

Scenario

REmap EU – scope and timeline

10

#REmap

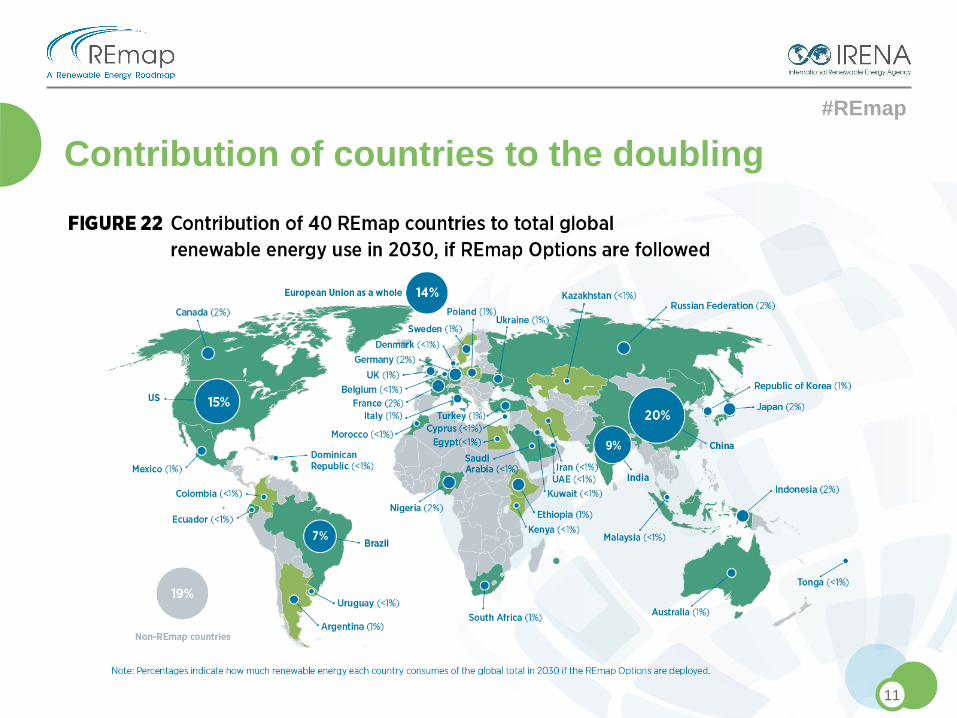

Contribution of countries to the doubling

11

#REmap

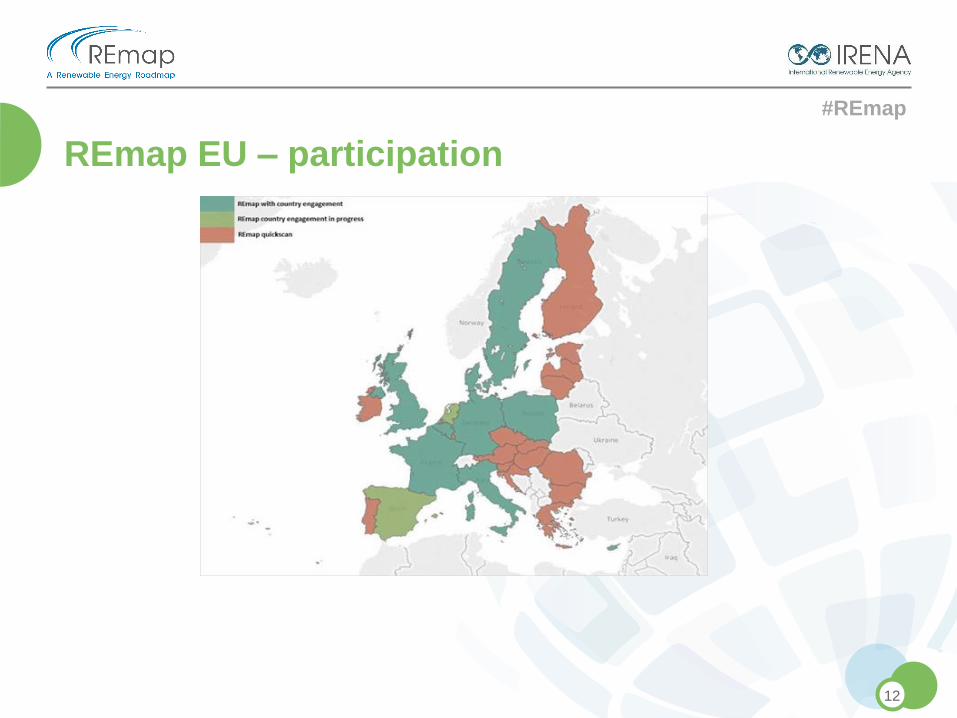

REmap EU – participation

12

#REmap

◉ Climate change is high on the agenda and EU has a central role

◉ 2017 German Presidency of the G20 focus on decarbonisation

◉ Marrakech RE day at COP22

◉ Various other climate related discussions (eg UNFCCC)

◉ Need to understand the role of RE in view of the CO2 commitments

◉ Currently EU not on a decarbonisation path to 2050

◉ Many challenges to deployment of RE and EE in end-use

sectors – potential and cost/benefits needs to be understood

better

◉ Role countries need to play toward realising the EU target unclear

◉ Need to assess cost-effectiveness of different allocation

mechanisms to reach 27% and go beyond in RE share

REmap EU – relevance to policy discussions

13

#REmap

◉ Reference Case: ◉ Most countries on path to reach 2020 targets (FR, IE, MT, LU, NL,

UK challenging)

◉ 25% RE share in GFEC by 2030, lower than the 27% target

◉ 270 Mtoe per year gross final RE consumption

◉ High RE deployment in power sector (ETS), in end-uses (non-ETS)

limited deployment

◉ REmap case ◉ Up to 33% RE share by 2030 possible

◉ Additional potential in wind, solar PV, biofuels for transport and

biofuels for industry

◉ Germany, France, UK and Italy half of all RE use by 2030

◉ Only with the additional wind and solar potential, gap from 25% to

27% can be closed, but unclear whether the most cost-effective path

◉ 50% of all RE use is bioenergy

◉ 51% of all RE use is RE power, 36% heating/cooling, 13% transport

REmap EU – developments in total RE use to 2030

14

#REmap

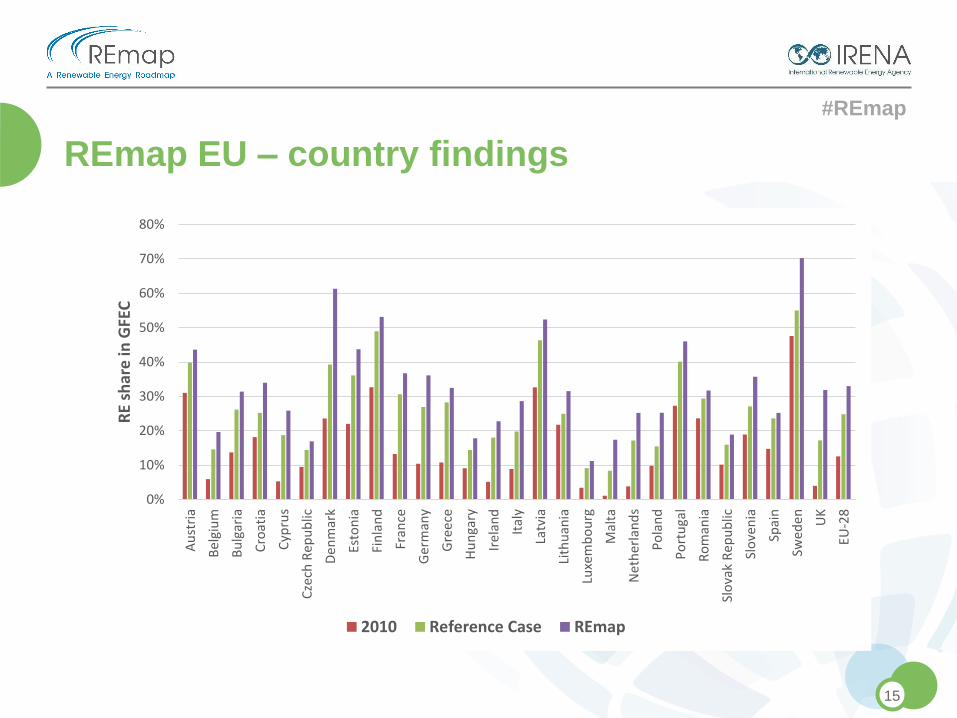

REmap EU – country findings

15

0%

10%

20%

30%

40%

50%

60%

70%

80%

Au

stri

a

Be

lgiu

m

Bu

lgar

ia

Cro

atia

Cyp

rus

Cze

ch R

epu

blic

De

nm

ark

Esto

nia

Fin

lan

d

Fran

ce

Ger

man

y

Gre

ece

Hu

nga

ry

Ire

lan

d

Ital

y

Latv

ia

Lith

uan

ia

Luxe

mb

ou

rg

Mal

ta

Net

her

lan

ds

Po

lan

d

Po

rtu

gal

Ro

man

ia

Slo

vak

Rep

ub

lic

Slo

ven

ia

Spai

n

Swed

en

UK

EU-2

8

RE

shar

e in

GFE

C

2010 Reference Case REmap

#REmap

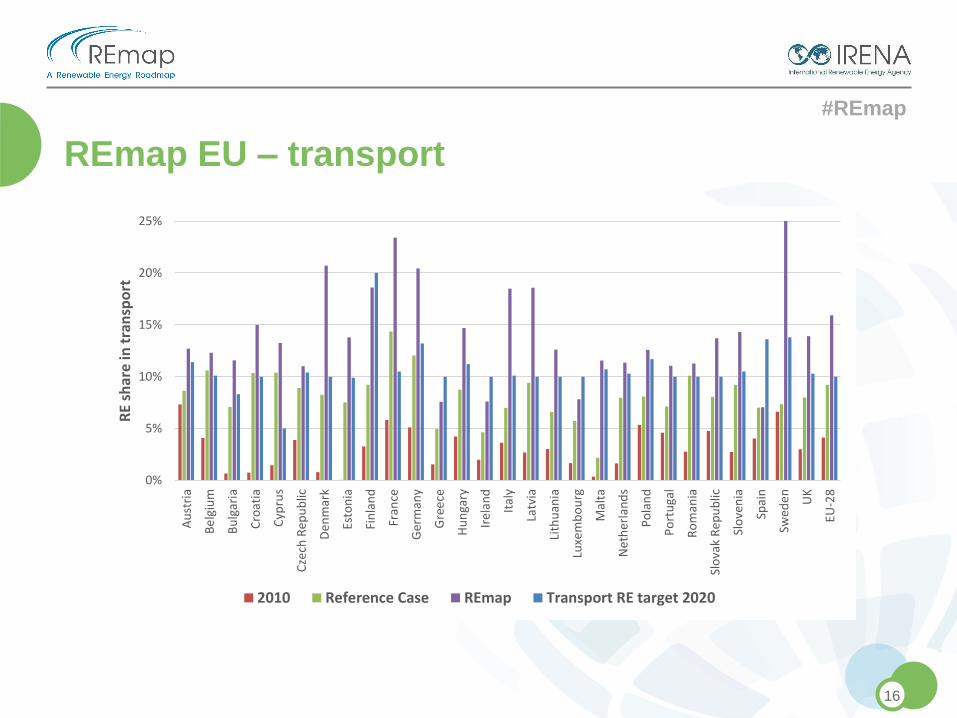

REmap EU – transport

16

0%

5%

10%

15%

20%

25%

Au

stri

a

Be

lgiu

m

Bu

lgar

ia

Cro

atia

Cyp

rus

Cze

ch R

epu

blic

De

nm

ark

Esto

nia

Fin

lan

d

Fran

ce

Ger

man

y

Gre

ece

Hu

nga

ry

Ire

lan

d

Ital

y

Latv

ia

Lith

uan

ia

Luxe

mb

ou

rg

Mal

ta

Net

her

lan

ds

Po

lan

d

Po

rtu

gal

Ro

man

ia

Slo

vak

Rep

ub

lic

Slo

ven

ia

Spai

n

Swed

en

UK

EU-2

8

RE

shar

e in

tra

nsp

ort

2010 Reference Case REmap Transport RE target 2020

#REmap

REmap EU – transport

17

◉ Just above 4% of the sector’s energy use is biofuels today

◉ Few countries have high RE shares (eg Sweden, Finland)

◉ In REmap, 16.5% RE share possible (13.5% biofuels, 3% RE power

– partly from modal shift opportunities)

◉ Biofuels demand triples to 60+ billion liter per year by 2030

◉ Challenges around realising the potential:

◉ Investments in biofuels have slowed down

◉ Lower profitability of ethanol producers in the past years

◉ Concerns on sustainability of biofuels (GHG emissions, iLUC)

◉ Advanced biofuel deployment is limited, and production costs high

◉ Limited solutions for aviation and shipping

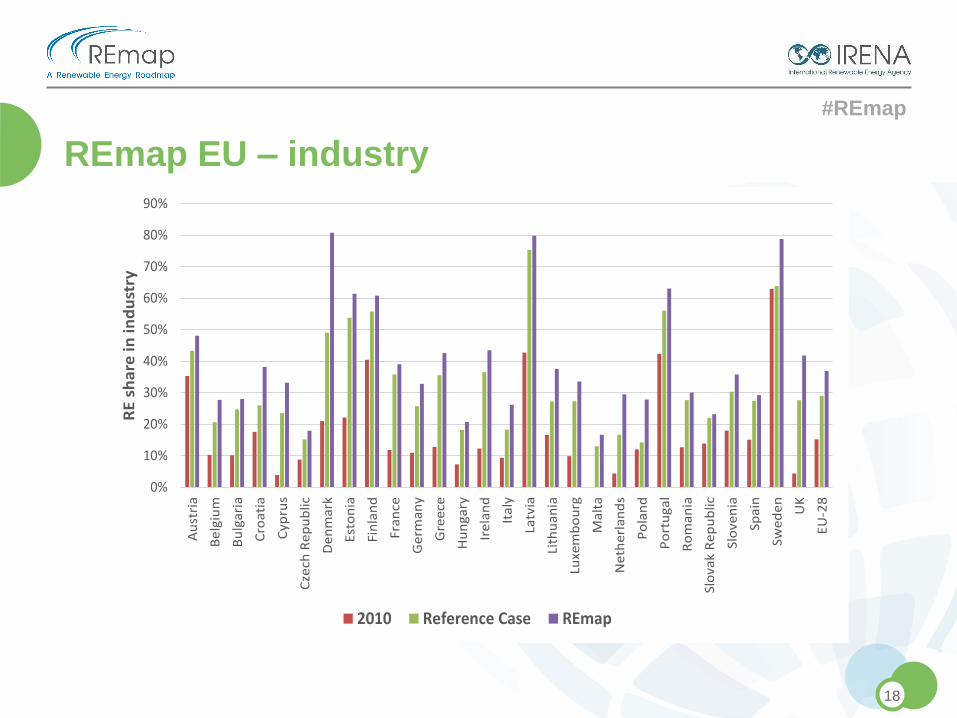

#REmap

REmap EU – industry

18

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%A

ust

ria

Be

lgiu

m

Bu

lga

ria

Cro

ati

a

Cyp

rus

Cze

ch R

ep

ub

lic

De

nm

ark

Est

on

ia

Fin

lan

d

Fra

nce

Ge

rma

ny

Gre

ece

Hu

ng

ary

Ire

lan

d

Ita

ly

Latv

ia

Lith

ua

nia

Luxe

mb

ou

rg

Ma

lta

Ne

the

rla

nd

s

Po

lan

d

Po

rtu

ga

l

Ro

ma

nia

Slo

vak

Re

pu

blic

Slo

ven

ia

Spa

in

Swe

de

n

UK

EU

-28

RE

sh

are

in

in

du

stry

2010 Reference Case REmap

#REmap

REmap EU – industry

19

◉ Represents 1/3 of EU’s total energy demand, 20% RE share in 2014

◉ Potential to reach 37% by 2030 (50% biofuels, 35% RE power, 15%

SWH, geothermal, heat-pumps, RE-based district heat)

◉ Challenges around realising the potential:

◉ Deployment of RE in energy-intensive sectors (iron/steel, cement,

aluminium, petrochemicals) is limited and technologies currently not fully

commercialised

◉ Integration of heating/cooling technologies may require process

modifications

◉ Maintaining cost-competitiveness is essential for the sector

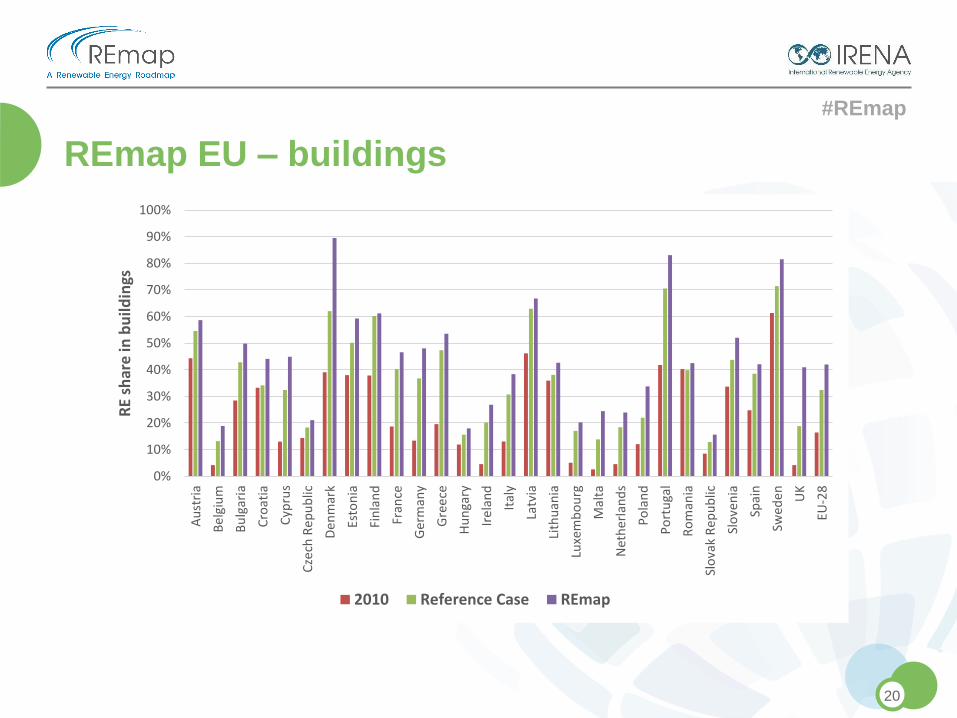

#REmap

REmap EU – buildings

20

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%A

ust

ria

Be

lgiu

m

Bu

lgar

ia

Cro

atia

Cyp

rus

Cze

ch R

epu

blic

De

nm

ark

Esto

nia

Fin

lan

d

Fran

ce

Ger

man

y

Gre

ece

Hu

nga

ry

Ire

lan

d

Ital

y

Latv

ia

Lith

uan

ia

Luxe

mb

ou

rg

Mal

ta

Net

her

lan

ds

Po

lan

d

Po

rtu

gal

Ro

man

ia

Slo

vak

Rep

ub

lic

Slo

ven

ia

Spai

n

Swed

en

UK

EU-2

8

RE

shar

e in

bu

ildin

gs

2010 Reference Case REmap

#REmap

REmap EU – buildings

21

◉ Represents 40% of EU’s total energy demand, 32% RE share in 2014

◉ Potential to reach 42% by 2030

◉ Various RE technologies have potential

◉ 1/3 biofuels, 1/3 RE power, 1/3 SWH, geothermal, heat-pumps, RE-

based district heat

◉ Challenges around realising the potential

◉ New buildings attract more investments in RE than existing stock

◉ Renovation rates are slow

◉ Integration of heating/cooling technologies may require process

modifications

◉ Cost-competitiveness is key

#REmap

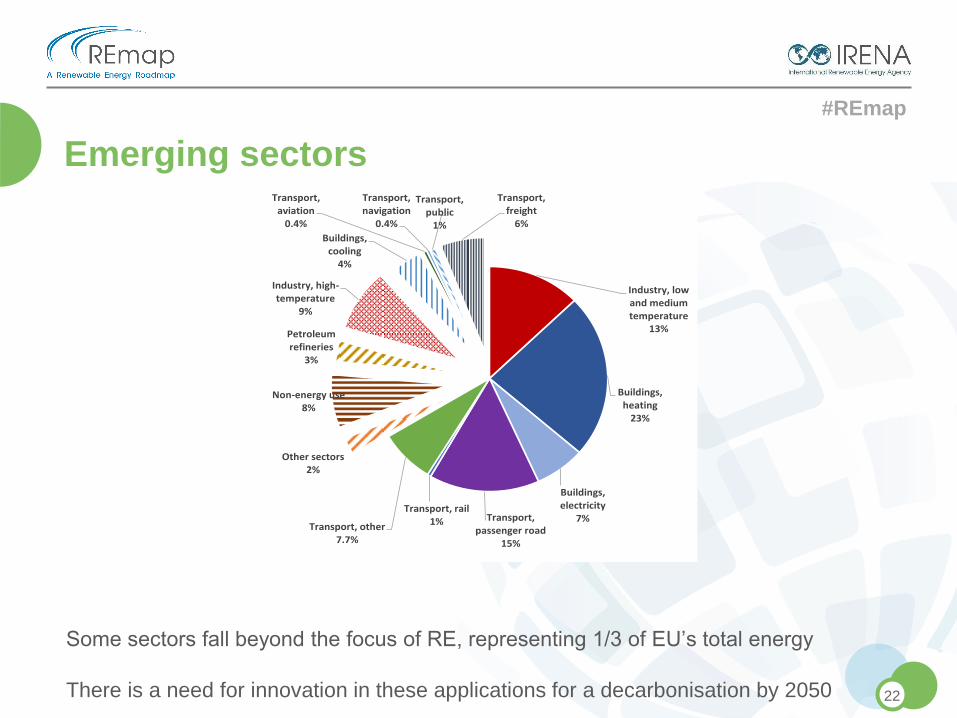

Emerging sectors

22

Industry, low and medium temperature

13%

Buildings, heating

23%

Buildings, electricity

7%Transport, passenger road

15%

Transport, rail1%Transport, other

7.7%

Other sectors2%

Non-energy use8%

Petroleum refineries

3%

Industry, high-temperature

9%

Buildings, cooling

4%

Transport, aviation

0.4%

Transport, navigation

0.4%

Transport, public

1%

Transport, freight

6%

Some sectors fall beyond the focus of RE, representing 1/3 of EU’s total energy

There is a need for innovation in these applications for a decarbonisation by 2050

#REmap

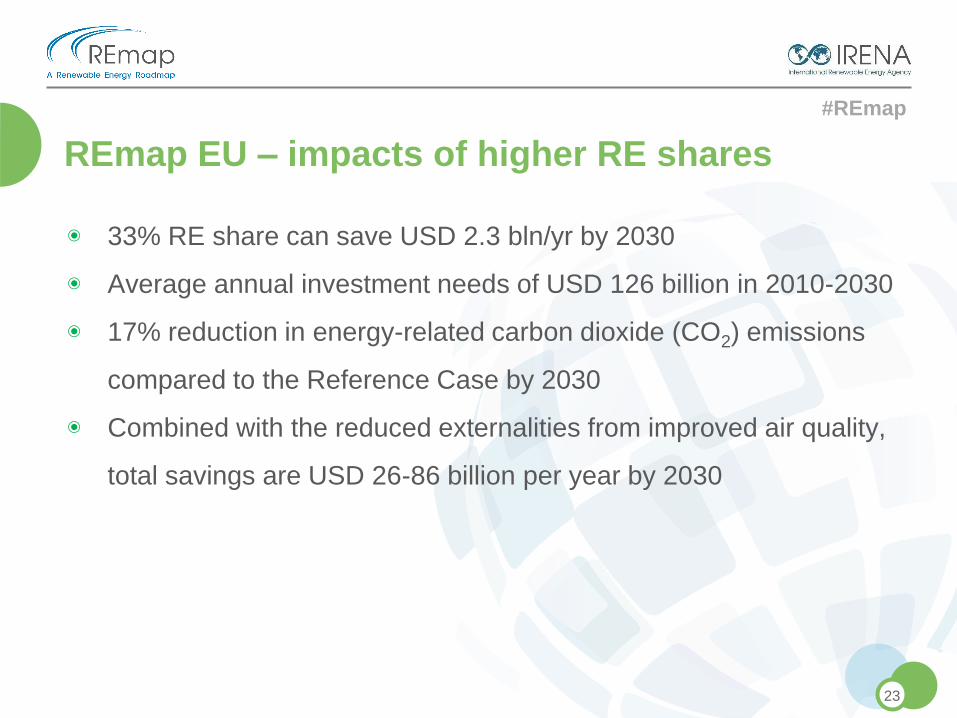

REmap EU – impacts of higher RE shares

23

◉ 33% RE share can save USD 2.3 bln/yr by 2030

◉ Average annual investment needs of USD 126 billion in 2010-2030

◉ 17% reduction in energy-related carbon dioxide (CO2) emissions

compared to the Reference Case by 2030

◉ Combined with the reduced externalities from improved air quality,

total savings are USD 26-86 billion per year by 2030

#REmap

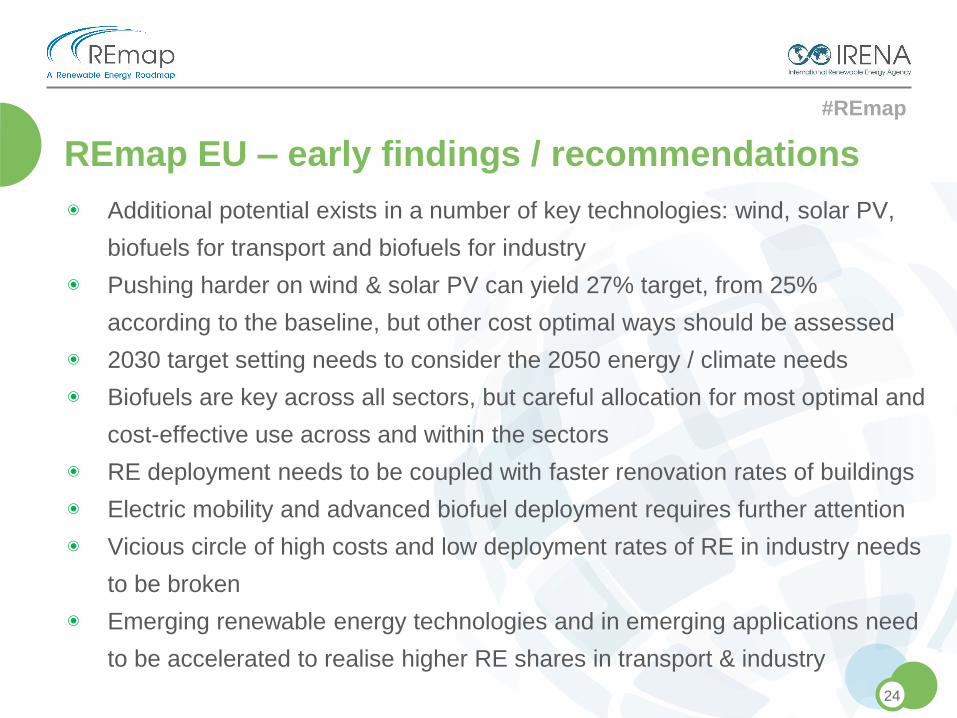

REmap EU – early findings / recommendations

24

◉ Additional potential exists in a number of key technologies: wind, solar PV,

biofuels for transport and biofuels for industry

◉ Pushing harder on wind & solar PV can yield 27% target, from 25%

according to the baseline, but other cost optimal ways should be assessed

◉ 2030 target setting needs to consider the 2050 energy / climate needs

◉ Biofuels are key across all sectors, but careful allocation for most optimal and

cost-effective use across and within the sectors

◉ RE deployment needs to be coupled with faster renovation rates of buildings

◉ Electric mobility and advanced biofuel deployment requires further attention

◉ Vicious circle of high costs and low deployment rates of RE in industry needs

to be broken

◉ Emerging renewable energy technologies and in emerging applications need

to be accelerated to realise higher RE shares in transport & industry

#REmap

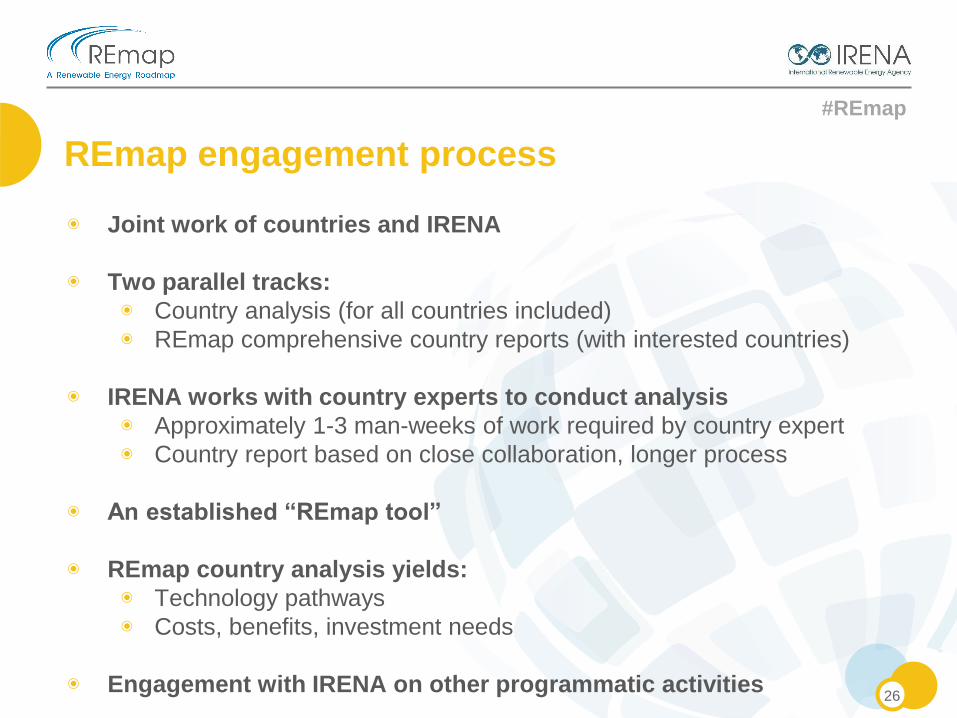

◉ Joint work of countries and IRENA

◉ Two parallel tracks:

◉ Country analysis (for all countries included)

◉ REmap comprehensive country reports (with interested countries)

◉ IRENA works with country experts to conduct analysis

◉ Approximately 1-3 man-weeks of work required by country expert

◉ Country report based on close collaboration, longer process

◉ An established “REmap tool”

◉ REmap country analysis yields:

◉ Technology pathways

◉ Costs, benefits, investment needs

◉ Engagement with IRENA on other programmatic activities

REmap engagement process

26

#REmap

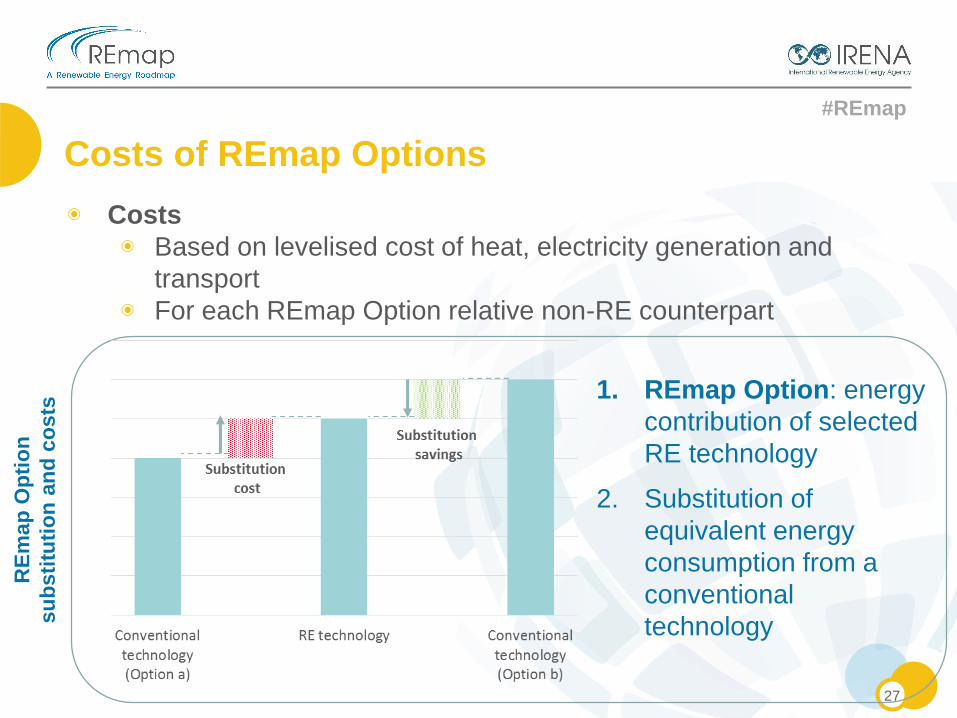

◉ Costs

◉ Based on levelised cost of heat, electricity generation and

transport

◉ For each REmap Option relative non-RE counterpart

Costs of REmap Options

27

1. REmap Option: energy

contribution of selected

RE technology

2. Substitution of

equivalent energy

consumption from a

conventional

technology

RE

map

Op

tio

n

su

bsti

tuti

on

an

d c

osts

#REmap

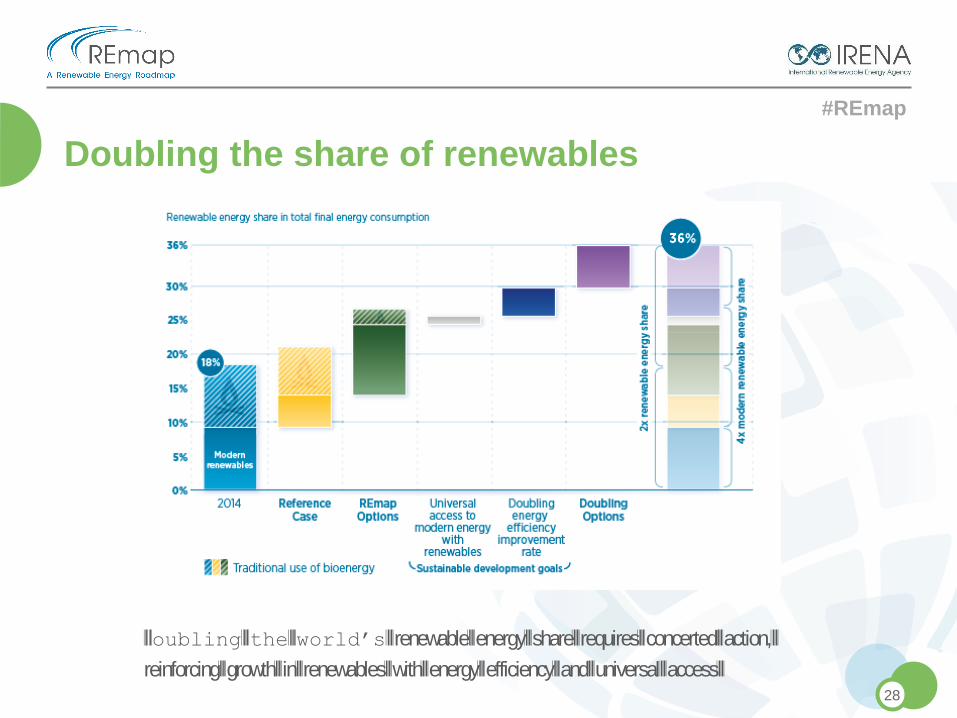

Doubling the world’s renewable energy share requires concerted action,

reinforcing growth in renewables with energy efficiency and universal access

Doubling the share of renewables

28

#REmap

29

Correct

for market

distortions to

create a level

playing field

Introduce

greater flexibility

into energy

systems and

accommodate

the variability of

key renewable

energy sources

Develop and

deploy

renewable

heating and

cooling solutions

for urban

development

projects and

industry

Promote

transport based on

renewable power

and biofuels

Ensure

the sustainable,

affordable and

reliable supply of

bioenergy

feedstocks

Key Action Areas

#REmap

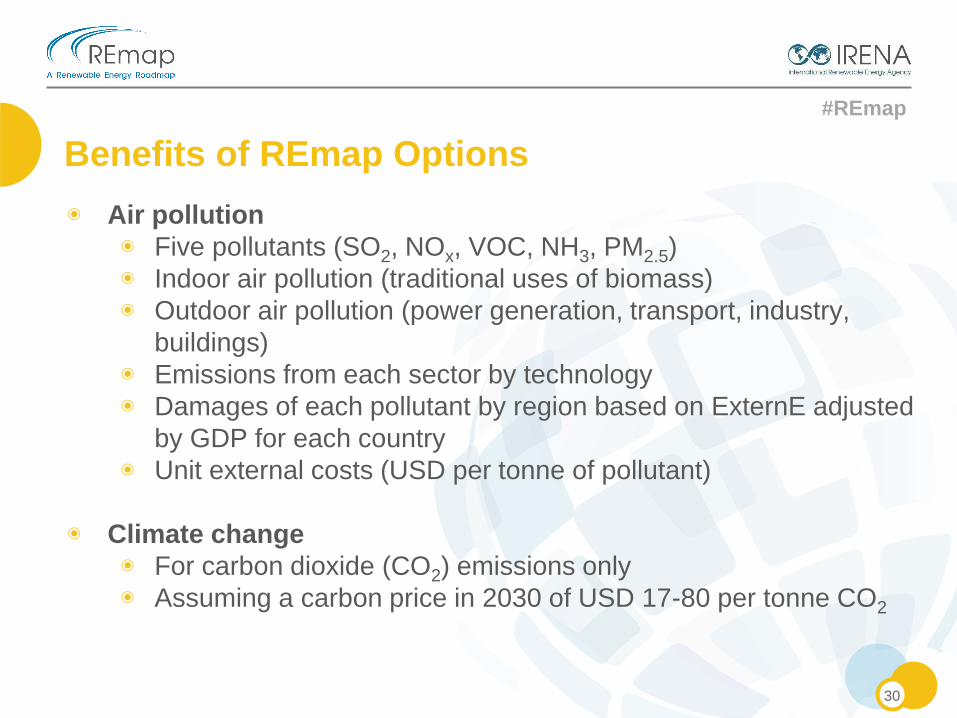

◉ Air pollution

◉ Five pollutants (SO2, NOx, VOC, NH3, PM2.5)

◉ Indoor air pollution (traditional uses of biomass)

◉ Outdoor air pollution (power generation, transport, industry,

buildings)

◉ Emissions from each sector by technology

◉ Damages of each pollutant by region based on ExternE adjusted

by GDP for each country

◉ Unit external costs (USD per tonne of pollutant)

◉ Climate change

◉ For carbon dioxide (CO2) emissions only

◉ Assuming a carbon price in 2030 of USD 17-80 per tonne CO2

Benefits of REmap Options

30

#REmap

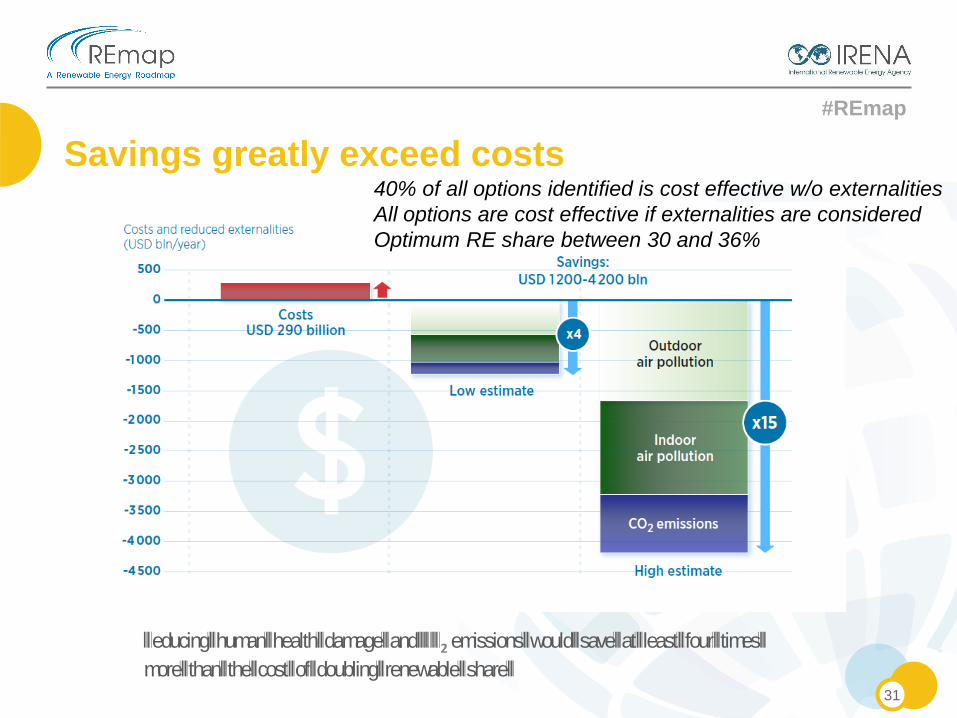

Reducing human health damage and CO2 emissions would save at least four times

more than the cost of doubling renewable share

Savings greatly exceed costs

31

40% of all options identified is cost effective w/o externalities

All options are cost effective if externalities are considered

Optimum RE share between 30 and 36%

#REmap

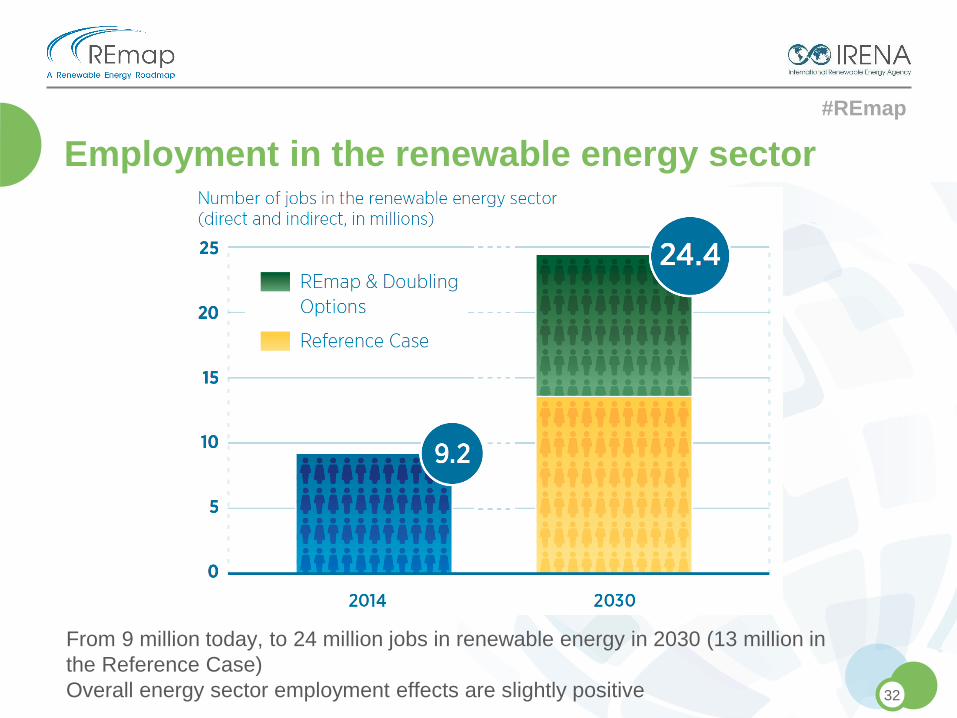

Employment in the renewable energy sector

32

From 9 million today, to 24 million jobs in renewable energy in 2030 (13 million in

the Reference Case)

Overall energy sector employment effects are slightly positive