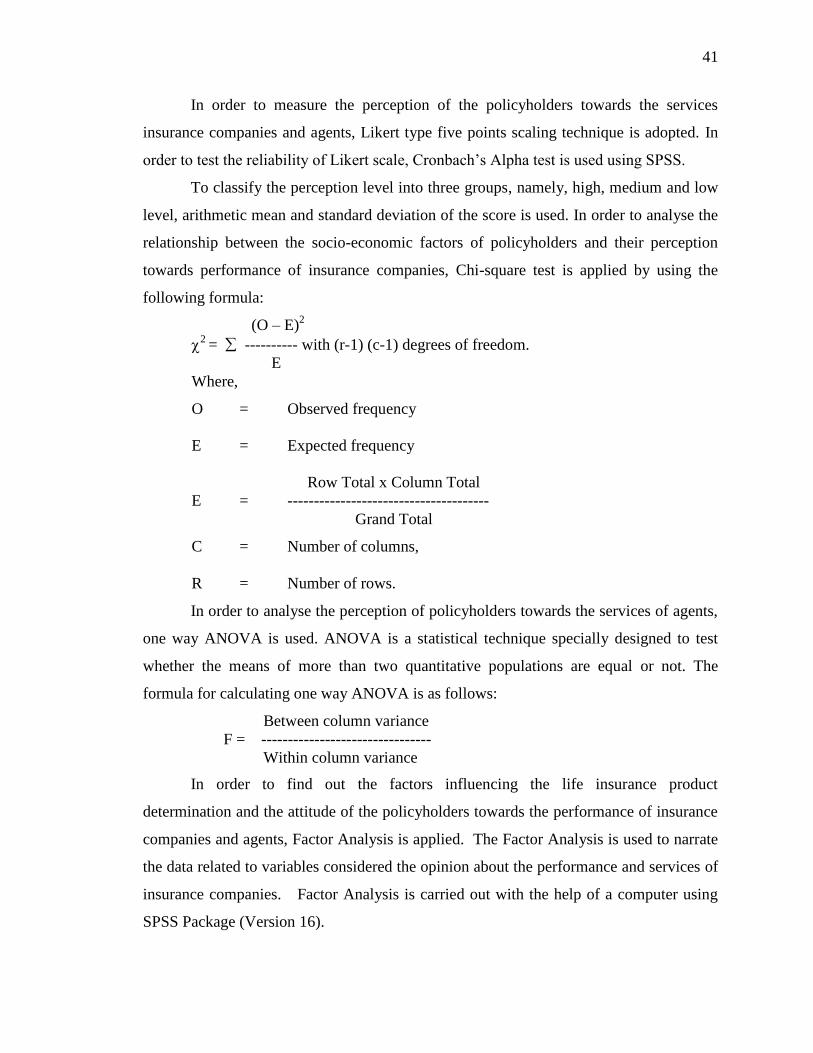

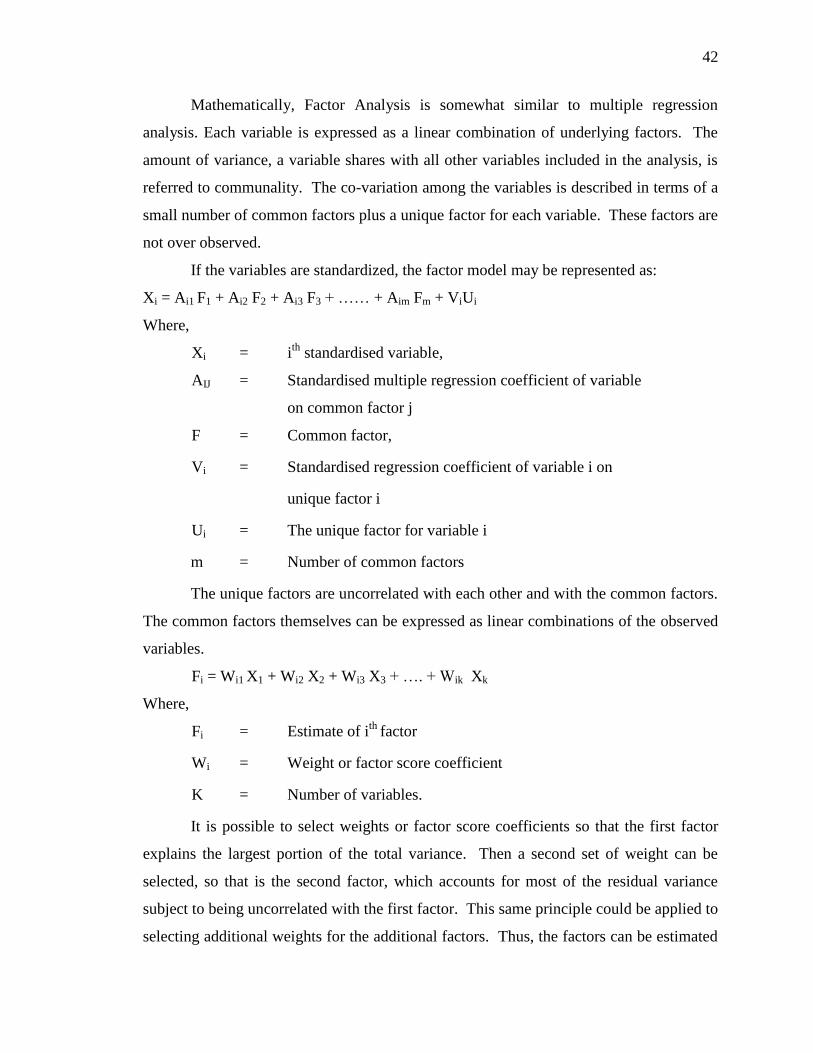

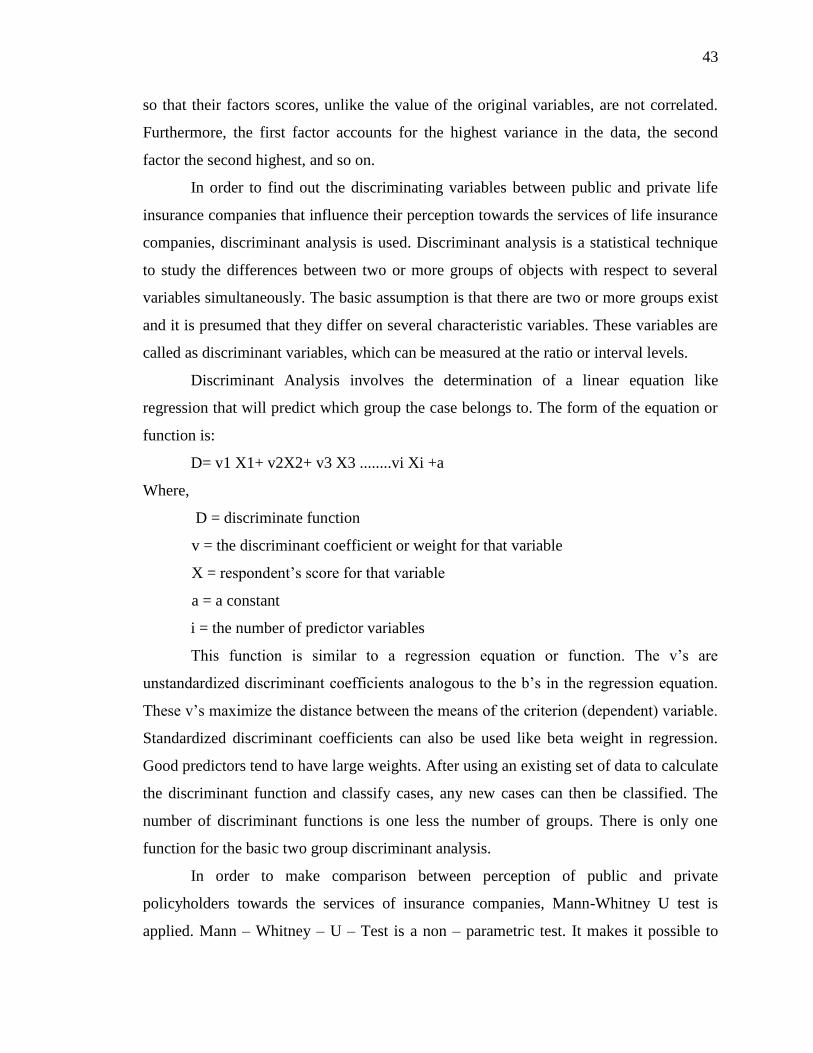

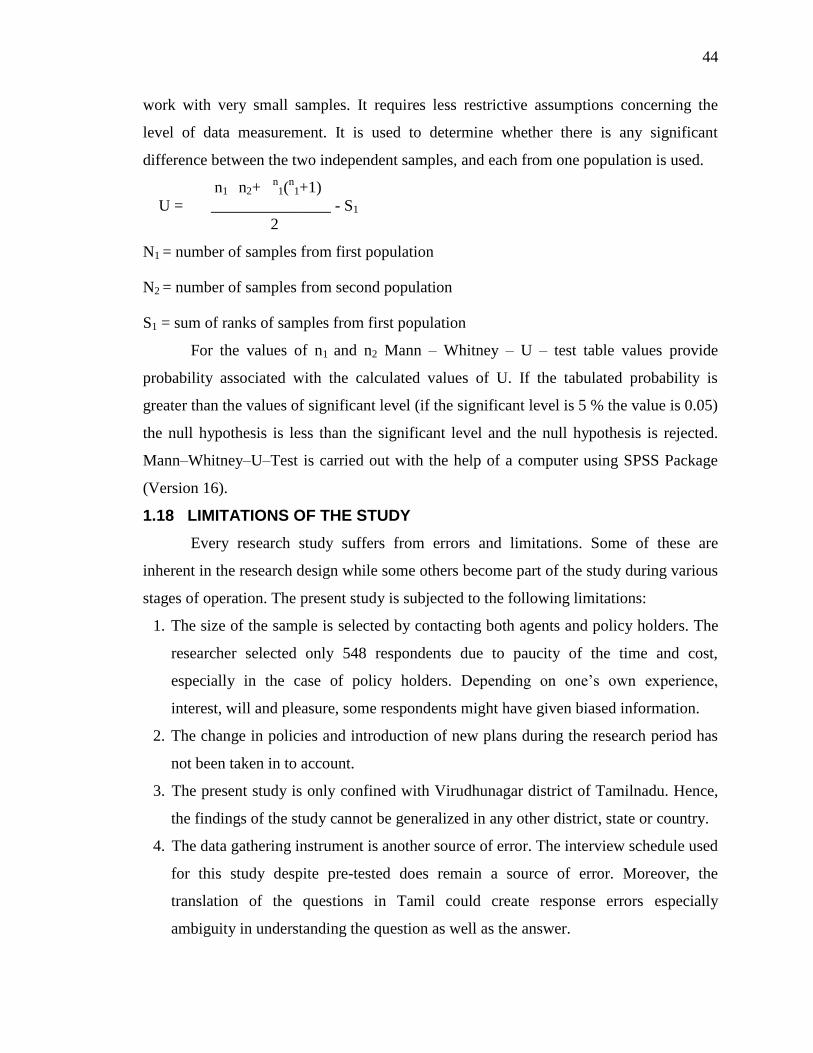

Embed Size (px)

Citation preview

1.1 INTRODUCTION

Risks are inherent in all forms of economic, political, social, environmental and

business activities. Planning alone cannot solve or protect one against uncertainties.

Insurance is a device by which the loss likely to be caused by an uncertain event and

spread over a number of persons who are exposed to it is compensated to those who

propose to insure themselves against such an event. The essence of insurance is the

elimination of risk and substitution of certainty for uncertainty. Insurance is thus a co-

operative way of spreading risk. A contract of insurance is a contingent agreement. A

contract of insurance other than life insurance is a contract of indemnity.1

Insurance is the subject matter of solicitation. This is the essence of the concept of

insurance. Insurance has emerged and developed as a self-felt need among the people.2

Insurance is a contract, which provides financial risk coverage to the insured against any

adverse event.3 The insurance services can be described as a product in the form of a

written legal contract (insurance document) plus a bundle of services associated with it.

Services are activities and/or benefits that one party offers to the other and that services

are necessarily intangible and do not result in the ownership of anything.4

Life insurance, like the joint family system in India offers security to the family in

the midst of uncertainty about the span of life of the earning member. In life insurance,

the uncertain element is the time when death of the insured will occur. Life insurance is a

contract whereby, the insurer, in consideration of a premium paid either in a lump sum or

in periodical installments, undertakes to pay an annuity or a certain sum of money, either

on the death of the insured or on the expiry of a certain number of years, whichever is

earlier. Life insurance is made available to the public through the medium of contract that

detail the agreement.5

1B. S. Bodla, M. C. Garg, and K. P. Singh, Insurance, Deep and Deep Publications

Private Limited, New Delhi, 2004, p.4. 2S. Banumathy, and G. Karunanithi, “Pension Plan Scheme of LIC of India and other

Insurance Companies – A comparative study”, Life Insurance To-day, Kolkatta,

September 2005, pp.10-13. 3 S. Shajahan, Services Marketing, Himalaya Publishing House, New Delhi, 2005, p.203. 4P. Periasamy, Principles and Practice of Insurance, Himalaya Publishing House, New

Delhi, 2001, p.3. 5 Ibid., p. 27.

2

Life Insurance is unique in one aspect. As an instrument of economic security, it

is incomparable. No other mode of savings can provide, what is provided by life

insurance product. It also takes care of tomorrow‟s bread, clothing and shelter. Death is

certain, but it is the time of death, that is most uncertain. Life Insurance Policies seek to

offer certainty of that uncertainty. 6

Risk cover is the primary benefit offered by the

insurance contract besides providing supplementary benefits, like, bonus, income tax

rebates, housing loan facility and so on.

Life Insurance is the only method to be used as a hedge against possibilities of the

savings period being cut-short. A policy of insurance from its beginning guarantees the

full value as against other forms of savings. While comparing the returns from insurance

cover with other forms of savings, one should take into account the cost of providing

insurance cover as well.

The Indian life insurance industry is one of the oldest in the world and has

witnessed dramatic changes in the last two decades. In 1818, a formal insurance company

was formed in Kolkata. Insurance business was subjected to Indian Companies Act 1866,

without any specific regulations. The practices adopted by the insurance players were

becoming detrimental to public interest and the government decided to regulate by the

promulgation of Indian Life Assurance Act, 1912. The Insurance Act of 1938 was passed

to ensure comprehensive supervision of insurance company related matters and direct

control of the government over the insurers. In the year 1956, the government of India

nationalized the insurance sector. Life Insurance Corporation of India was formed by an

Act of Parliament, viz., LIC Act, 1956.7

LIC of India, the capital intensive business, provides the most important financial

instrument to customers aimed at protection as well as long term savings. For 43 years,

Life Insurance Corporation of India enjoyed monopolistic status. The Government of

6 “Think of Tomorrow, Insurance Today”, Editorial, Yogakshema, LIC, Mumbai, Vol.36,

No.6, June 1993, p.3.

7Thirumaran and K. Jaiganesh, “Satisfaction of Policyholders Services Provided by LIC

of India at Thanjavur Division”, IJEMS, New Delhi, Vol. 2, Issue. 9, September 2012,

p.1.

3

India decided to open up the markets for private and foreign entrepreneurs. In 1999, the

Insurance Regulatory and Development Authority (IRDA) Act was passed in the

parliament and the IRDA was set-up to monitor, regulate and control the affairs of the

various life and general insurance companies in India.

Private insurance companies are competing with the Life Insurance Corporation

of India to tap the immense insurance market potential of India. Any new player entering

the insurance business would try to differentiate its product offering, but it is the service

delivery system which would become the key differentiator.

One of the most curious aspects of insurance services is that customers expect

quality and customization simultaneously. These two aspects must be tailor made to

retain the customers in the long run.

Insurance Companies are focusing on customer satisfaction through increased

customer choice and lower premiums, while ensuring the financial security of the

insurance market. Insurance companies are targeting upon the customers by giving them

a basket of returns with a mission to make them delight and satisfied. The Insurance

sector has obviously started growing at a rapid rate after the sector was opened up. The

credit for enlarging the market should however, goes to the private sector as they came up

with an aggressive market strategy to establish their presence. The public sector has in its

turn, redrawn its priorities, revamped their marketing strategy, and together the public

and private sectors have enlarged the market. India, with its huge middle class

households, has exhibited potential for the insurance industry. This has made

international players to look at the Indian market. Moreover, saturation of markets in

many developed economies has made the Indian market all the more attractive for global

insurance majors.

The liberalization of insurance industry has been spurred by product innovation,

vibrant distribution channels coupled with targeted publicity and promotional campaign

by the insurers. Innovations have come not only in the form of benefits attached to the

products, but also in the delivery mechanism through various marketing tie-ups both

within the realm of financial services and outside.

In the beginning, insurance was looked at as a 'tax-benefit' investment. Slowly,

however the mindset of the common man is changing. Life Insurance is now looked as an

4

investment vehicle. With the introduction of private players in the sector, there has been

more transparency and flexibility in the sector.

Even though, life insurance companies offer risk cover along with saving element,

and liquidity facility, people do not come forward to invest in it. The insurance industry

is therefore, forced to do a rethink on the customer, his needs, his preferences and the

solutions necessary to serve and satisfy him. Unless the customer becomes the focus of

the business, value – addition to services will not be a priority. The insurance companies

have to find ways to make their services more tangible. In order to increase the

productivity of providers who are inseparable from their products, to standardize the

quality and to improve the demand situations and supply capacities in the face of service

perishability. Informing, educating, motivating, persuading, advising and other services

prior to, at the time of and after the issuance of the insurance document make the

purchase of insurance dissimilar from purchasing other products and from even other

services.

Better services, individual attention and pure transparency have given the private

sector an upper hand. But with a huge unorganized market in India yet to tap the

insurance companies in India have a voluminous market to explore. Hence, it is necessary

to understand the perception of the policyholders towards the services of insurance

companies in order to improve their services and to explore their market.

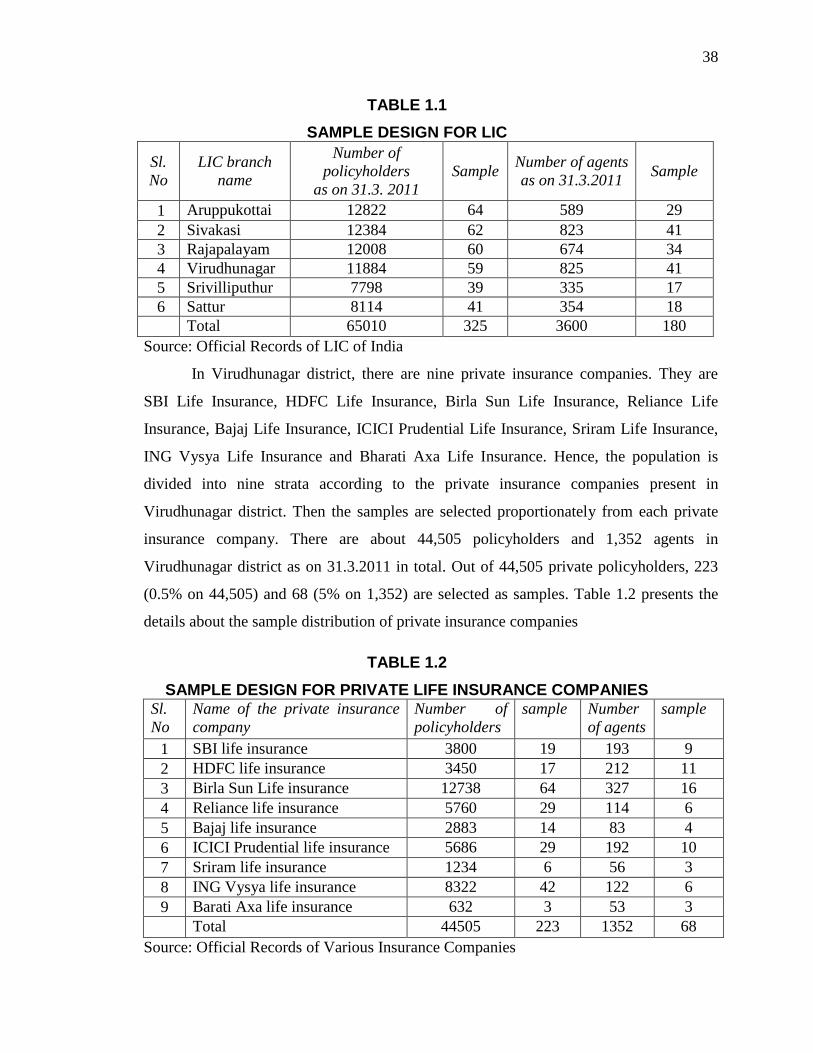

1.2 STATEMENT OF THE PROBLEM

Many policyholders take up life insurance policies for the purpose of giving

economic protection to their children when they attain majority. The lump sum available

on maturity of the policy may be utilized for education, marriage, self-employment and

other useful purposes. Even though policyholders take up life insurance for the purpose

of covering the risk, many policyholders have a strong feeling that life policies act as

long-term investments. Life Insurance facilitates long-term savings through easy

installments, new housing loans and ordinary loans for meeting urgent financial

commitments. Policyholders are also desirous of keeping their savings to meet the current

needs and to provide for their old age requirements. The life insurance companies also

offer pension-linked life insurance policies to persons nearing retirement from

employment. In a large number of cases, the policyholders take life insurance policies for

5

the benefit of the dependents and some people adopt life insurance for the purpose of tax

planning. Every person takes up life insurance policies providing adequate insurance

cover for dependents.

Customer service is the ability of an organisation to constantly and consistently

give the customer what they want, need and expect. Quality in customer service is critical

to success in any liberalized environment. The primary focus of the insurance companies

in the liberalized era is delivering quality service. It is highly essential to bring about

quality improvement in the service of the life insurance companies, as the customers‟

tastes, preferences and requirements are ever changing. Quantifying service quality

measurements will help the companies to direct their efforts towards service

improvement. This involves an understanding of the customer expectations and

perceptions of the services.

Liberalization and Globalization made insurance industry a competitive one from

near monopoly position. Now-a-days, qualities of policyholders‟ level of service are

playing an important role not only for retaining policyholders but also for expanding.

Therefore, it is essential that the insurance industries need to assess their policyholders‟

perception towards service being offered by them.

Insurance products are basically risk protection products. But in India, it is the

most mis-sold product and it is sold as an investment product rather than a risk protection

product. Therefore, the policyholders‟ intent for buying an insurance policy itself is a

research question. So, finding out the reasons and factors influencing the selection of life

insurance product is necessary for better service.

The retention of policyholders largely revolves around the identification and

satisfaction of policyholders‟ needs and requirements. Policyholders‟ satisfaction or

dissatisfaction gives an opportunity for improving the quality of service in order to

remain commercially competitive and to develop market base.

A sincere attempt has been made by the researcher to analyse the perception of

policyholders towards the services of insurance companies and agents. Hence, the present

study analyses the perception of policyholders towards the services rendered by the

public and private insurance companies and agents in Virudhunagar district to offer

valuable suggestions to improve their service quality.

6

1.3 REVIEW OF LITERATURE

Knowledge of various studies made already is essential for better understanding

of the research problem. It enables easy identification of various dimensions and issues

relating to the study. This chapter presents a brief chronological account on the various

studies already done by various researchers related to the subject under study.

E. Scott Maynes and Loren V. Geistfeld (1974) in their research paper titled, “The

Life Insurance Deficit of American Families: A Pilot Study” indicated that perhaps 50

per cent of families may suffer a serious life insurance deficit. Other families had life

insurance surpluses. The deficit was affected by family net worth, educational objectives,

age and number of children, age of household head and family income goals.8

S. Srinivasamoorthy (1982) in his research report titled, “Improvement in

Productivity of Administrative Personnel in the Field of Insurance” highlighted the major

issues related to the productivity of administrative personnel in LIC of India. The impact

of major issues on productivity had been analysed in that paper.9

R. Meena (1986) in her thesis titled, “Utilisation of Life Insurance Corporation by

Policyholders of Madurai City: An Empirical Study” had studied the utilisation of the

LIC by policyholders and analysed the various factors which influenced the level of

utilisation. She concluded that unless the corporation made its schemes attractive and

effective, with good returning capacity and high bonus to the policyholders, it was bound

to fail in its operations. She had also suggested that expenditure be curtailed so that the

corporation can pay better returns.10

8 E. Scott Maynes and Loren V. Geistfeld, “The Life Insurance Deficit of American

Families: A Pilot Study”, Journal of Consumer Affairs, Malden, USA, June 1974, Vol. 8,

Issue 1, pp. 37 – 60.

9S. Srinivasamoorthy, “Improvement in Productivity of Administrative Personnel in the

Field of Insurance” Federation of Insurance Institute, Hyderabad, 1982.

10R. Meena, “Utilisation of Life Insurance Corporation by Policyholders of Madurai City:

An Empirical Study” Ph.D thesis, Madurai Kamaraj University, Madurai, 1986.

7

S. Mohammad Talha (1991) in his study titled, “An Appraisal of Investment

Policies of LIC” had mentioned various investment policies followed by LIC, growth of

life insurance business in India and suggestions for increasing it.11

M. Muthupandi (1995) in his thesis titled, “A Study of Utilisation of Life

Insurance Corporation of India by Policyholders in Madurai Division” studied the socio-

economic factors which influenced the level of utilisation of the services of the LIC of

India by policyholders. He found out that there were many policyholders who had taken

only one life insurance policy. He suggested that employees of various undertakings such

as government department, transport undertakings, schools, colleges, universities, textile

mills, and factories must be persuaded to take up policies. He also suggested that policy

loan was granted only on policies which had crossed atleast three years without any

lapse.12

Rudra Saibaba, Prakash, and Kalyani (2002) in their research paper titled,

“Perception and Attitude of Women towards Life Insurance Policies” found that many of

the respondents opined that agents were not concentrating on the customers services. As a

result they were facing some inconvenience regarding the payment of premiums on the

due date and could not avail other benefits from LIC such as policy loan, housing loan,

and the like. The study suggested that there is a need to improve customers‟ relations

maintenance by LIC for the increased satisfaction of the customers.13

P. Anbuoli (2003) in his doctoral thesis titled, “Role of Employees Unions in Life

Insurance Corporation of India” studied the role of unions in the era of globalisation in

public sector undertakings and various industries. He also studied the various life

insurance needs of the community that would arise in the changing social and economic

11S. Mohammad Talha, “An Appraisal of Investment Policies of LIC”, Unpublished

Thesis, June 1991.

12 M. Muthupandi, “A Study of Utilisation of Life Insurance Corporation of India by

Policyholders in Madurai Division” Ph.D thesis, Madurai Kamaraj University, Madurai,

August 1995.

13Rudra Saibaba, Prakash, and Kalyani, “Perception and Attitude of Women Towards

Life Insurance Policies”, Indian Journal of Marketing, New Delhi, Vol. XXXII, No. 12,

December 2002, pp. 10-12.

8

environment. He suggested the way for maximizing the mobilization of people‟s savings

by making insurance linked savings adequately attractive.14

Pin Luarn, Tom M. Y. Lin and Peter K. Y. Lo (2003) in their research paper

titled, “An exploratory study of advancing mobilization in the life insurance industry: the

case of Taiwan‟s Nan Shan Life Insurance Corporation” suggested a conceptual

framework for mobilization in the life insurance industry, and formulated possible

research propositions incorporating a number of variables. The study also suggested a

total of ten key success factors for the implementation of mobilization in the life

insurance industry.15

Prakashvel, Ravi Chandran and Chan Kok Eng (2005) in their research work

titled, “An Exploratory Study on the Role Played by Product, Service and Behavioural

Factors in the Purchase of Life Insurance Policies in the Klang Valley, Malaysia” stated

that the companies selling life insurance policies should aim at continuous research to

understand the customers‟ decision making and came out with suitable strategies to offer

them the right product. They found that majority of the respondents were found to opine

that the purchase of life insurance policies were very beneficial as it ensured continual

stream of income to family in the event of adversity strikes. They also found that when a

buyer was motivated to purchase a life insurance, the buyer would first be influenced by

the perception towards the benefit of owning it.16

Sudarshena Reddy (2005) in his research paper titled, “Customer Perception

towards Private Life Insurance Companies Policies with Reference to Bangalore City”

had explained the psychological factors such as motivation, personality, perception,

learning, values, belief, attitude and life cycle which influenced the customer behaviour.

14P. Anbuoli, “Role of Employees Unions in Life Insurance Corporation of India” Ph.D

thesis, Madurai Kamaraj University, Madurai, November 2003.

15Pin Luarn, Tom M. Y. Lin and Peter K. Y. Lo, “An exploratory study of advancing

mobilization in the life insurance industry: the case of Taiwan‟s Nan Shan Life Insurance

Corporation” Internet Research, Canada, Vol. 13, Issue 4, 2003, pp.297 – 310.

16Prakashvel, Ravichandran, and Chan Kok Eng, “An Exploratory Study on the Role

Played by Product, Service and Behavioural Factors in the Purchase of Life Insurance

Policies in the Klang Valley, Malaysia”, The Journal of Insurance Institute of India,

Mumbai, Vol. XXXI, No. 1, January – June 2005, pp. 7 -23.

9

He studied the customers‟ opinion on whether private insurance policies were better

alternatives of public insurance companies‟ policies or not. He analysed the customer

perception about hidden cost of private insurance policies. He suggested that private

companies might make extra effort for the convenience of the potential customers.17

Ravi Kumar Sharma (2005) in his research paper titled, “Insurance perspectives in

Eastern UP – An Empirical Study” observed that LIC of India had higher brand

awareness in rural sector and thus had a higher brand image. LIC agents were more active

than other private insurance agents. He also observed that the rural people had less faith

on private players. So, it was a must to educate the rural population about the rigidity and

longevity of the insurance companies and how IRDA safeguarded their interests.18

Gautam Bansal and Pawan Tanerja (2005) in their research work titled, “Life

Insurance Advertisements on Television: A study on quality of Illustrations” observed

that life insurance advertisements on TVs would be more effective and had better

influence if they had emotional appeals. Materialism should not be stressed, as subject

matter was more socially oriented.19

K. Prakashvel (2005) in his thesis titled, “Marketing of Life Insurance in

Malaysia” studied the benefits expected by the insured from life insurance policies and

also studied the sources of influence in the need recognition phase by the insured. He

found out that the specific needs influencing the insured population to go for the purchase

of life insurance policies. He also found out that hard selling practices were followed in

the promotion of life insurance policies by the sales agents.20

17Sudarshena Reddy, “Customer Perception towards Private Life Insurance Companies

Policies with Reference to Bangalore City”, Indian Journal of Marketing, New Delhi,

Vol. XXXV, No. 8, April 2005, pp. 9 -14.

18Ravi Kumar sharma, “Insurance perspectives in Eastern Up – An empirical study”,

Indian Journal of Marketing, New Delhi, Vol. XXXV, No. 8, August 2005, pp. 14-20.

19Gautam Bansal and Pawan Tanerja, “Life Insurance Advertisements on Television: A

study o n quality of Illustrations”, Indian Journal of Marketing, New Delhi, Vol. XXXV,

No. 8, August 2005, pp. 34-38.

20K. Prakashvel, “Marketing of Life Insurance in Malaysia” Ph.D thesis, Madurai

Kamaraj University, Madurai, September 2005.

10

Tienyu Hwang and Simon S. Gao (2005) in their research paper titled, “An

Empirical Study of Cost Efficiency in the Irish Life Insurance Industry” investigated

scale economies and cost efficiency in the Irish life insurance industry by using the

translog cost function and distribution-free method. Increasing returns to scale were

found in the industry but the magnitude of cost economies varied with firm size. This

study indicated that firms with larger market shares were more likely to exhibit cost

efficiency. Furthermore, this study showed that bancassurance firms were more cost

efficient than other types of insurers in the Irish life insurance industry, which provided

new insights into the cost efficiency of bancassurance.21

Meador, Joseph W, Chugh and Lal C (2006) in their research paper titled,

“Demutualization in the Life Insurance Industry: A Study of Effectiveness” investigated

the effectiveness of demutualization as a strategic response to the challenges posed by

these sweeping changes. The study found that the demutualized firms generally had

implemented a successful strategy based on higher growth, greater profitability, cost

effectiveness and shifts in product mix. Also, they found that management took greater

risk in the investment portfolio. In addition, demutualization unlocks value lying dormant

in the mutuals' surplus. They concluded that the demutualized firms had generated

substantial excess returns over several stock market indexes, creating significant

economic value.22

Nalini Prava and Tripathy (2006) in their research paper titled, “An Application

of Factor Analysis Approach towards Designing Insurance Products in India” said that it

had been half a decade since the insurance market was privatized and today there were

many innovative customized products available. The Indian insurable industry was

witnessing a plethora of changes as consumers were given more options to choose from

custom made products, better transparency, improved technologies and processes and

21Tienyu Hwang and Simon S. Gao, “An Empirical Study of Cost Efficiency in the Irish

Life Insurance Industry”, International Journal of Accounting, Auditing and Performance

Evaluation, Philadelphia, USA, Vol. 2, No.3, 2005, pp. 264 – 280.

22Meador, Joseph W, Chugh and Lal C in their research paper titled, “Demutualization in

the Life Insurance Industry: A Study of Effectiveness”, Review of Business, Boston,

USA, January 1, 2006, p. 9.

11

better service standards. The three pieces like people, procedure and process should be

carefully evaluated to sell a product among the targeted customers.23

Madhukar Palli (2006) in her research paper titled, “A Study on Assessing Life

Insurance Potential in India” focused on risk security, the core product of life insurance.

It provided estimates of the Life Insurance gap to maintain dependents living standards

after the death of the primary wage earner. Because inadequately protected families often

put burden on public resources for their welfare. The primary drivers of demand for risk

security were 'Age', 'Income', 'Affordability', 'Wealth' and finally, 'the desire to protect

income from Inflation'. Though aggregate demand was driven by these factors, various

researches had shown that there was little correlation between a specific family's need for

security and its actual purchase of insurance. Many families, especially young ones, had

either no risk security or inadequate security. This report examined the extent to which

people were underinsured by measuring a 'life assurance security gap'. This gap was

computed as the mean ratio of recommended insurance to household earnings and the

mean ratio of actual insurance to household earnings.24

A. G. V. Narayanan (2006) in his doctoral thesis, “Rural Marketing Strategies for

Life Insurance Products in Coimbatore District” studied the rural customers‟ attitude

towards insurance and insurance products. He suggested that the non-policyholders also

looked as rational as they don‟t go by the mass appeal of the celebrities. The insurers,

instead of spending a huge sum on mass media, could turn to judicious mix of

conventional and non-conventional medias. In other aspects like social responsiveness,

attitude towards insurance as a promotional offer and brand switch, the non-policyholders

did not differ much from the policyholders.25

23Nalini Prava and Tripathy, “An Application of Factor Analysis Approach towards

Designing Insurance Products in India” Insurance Chronicle, Chennai, The ICFAI

University Press, Hyderabad, February 2006, pp. 84 – 90.

24Madhukar Palli, “A Study on Assessing Life Insurance Potential in India”, Bimaquest,

Pune, Vol. 6, Issue 2, July 2006, pp. 22-38.

25A.G.V. Naryyanan, “Rural Marketing Strategies for Life Insurance Products in

Coimbatore District”, Ph.D thesis, Alagappa University, Karaikudi, September 2006.

12

Venkata Ramana (2006) in his research paper titled, “Protection of Policyholders‟

Interest: Origin and Development of Statutory Safeguards in Consumer Insurance

Contracts” said that the process of statutory reforms and revisions from time to time, had

made the consumer insurance contracts more and more comprehensive and consumer

friendly.26

Chiang Ku Fan and Chen – Liang Cheng (2006) in their research paper titled, “A

Study to Identify the Training Needs of Life Insurance Sales Representatives in Taiwan

Using the Delphi Approach” identified the needs for continuing professional

development for life insurance sales representatives and examined the competencies

needed by those sales representatives. A modified Delphi technique was used. Most life

insurance companies in the USA implemented an education and training plan advocated

by the Life Office Management Association. Insurance companies in Taiwan implement

similar education and training plans, but they did not seem to result in the successful

performance of their sales representatives. Besides augmenting knowledge of various

financial products and marketing approaches, this study also suggested that life insurance

companies needed to train their sales representatives to an adequate standard in

competencies of problem solving, communication, information technology utilization,

culture compatibility, emotional intelligence, collective competence and ethics.27

Vinayagamoorthy (2006) in his research paper titled, “Indian Insurance: Modern

Marketing Approach” highlighted the competition, information, technology, product

innovations, distribution network, customer education, services and modern marketing

approach. He also found the marketing strategy for insurance in the emerging scenario.

R-> STP -> MM -> I -> C

Where, R -> Market Research, STP -> Segmentation, Targeting, Positioning,

I -> Implementation, C -> Control

26Venkata Ramana, “Protection of Policyholder‟s Interest: Origin and Development of

Statutory Safeguards in Consumer Insurance Contracts”, The Insurance Chronicle, The

University Press, Chennai, Vol. VI, No. 9, September 2006, PP. 60-64.

27Chiang Ku Fan and Chen – Liang Cheng, “A Study to Identify the Training Needs of

Life Insurance Sales Representatives in Taiwan Using the Delphi Approach”,

International Journal of Training and Development, Malden, USA, Vol. 10, No. 3.

September 2006, pp. 212-226.

13

He also suggested that in order to achieve the competitive edge over others, it is

important to standardize the process and bring out quality improvement and get feedback

from the customers regarding the quality of services rendered.28

Vytnutas Kindurys (2006) in his research paper titled, “The Experience and

Problems of Insurance Marketing Application in Lithuania” summarized insurance

marketing application experience in Lithuanian insurance companies. It analysed

necessity and possibilities of insurance services marketing application in Lithuanian

insurance companies.29

Chakrabarty (2007) in his study titled, “Efficiency of LIC: Post – liberalization

and globalization” measured the efficiency of LIC in the state of West Bengal, with the

thrust on agent‟s ability and business performance during the post liberalization and

globalization period. He revealed that in the period of liberalization and globalization in

India, LIC was very efficient in insurance market towards a) Agents‟ liability and b)

Business performance. He also proved that the efficiency of LIC of India was not shaken

even during the post liberalization and globalization period.30

M. Gurupandi (2007) in his doctoral thesis titled, “Attitude of the Policyholders

towards Life Insurance Corporation of India – A Study with Special Reference to

Ramanathapuram District” studied the utilization of Life Insurance Corporation (LIC) by

policyholders in Ramanathapuram district. He found out that majority of them had taken

LIC policies for income tax purposes. He identified the factors which the consumers took

into consideration before selecting life insurance product. The prospective customers,

who intended to buy the insurance products and avail the services for the first term, could

31

Vinayagamoorthy, “Indian Insurance: Modern Marketing Approach”, Southern

Economist, Bangalore, Vol. 45, No. 12, October 15, 2006, pp. 17-19.

29Vytnutas Kindurys, “The Experience and Problems of Insurance Marketing Application

in Lithuania”, Vadbya / Management, USA, Vol. No. 3-4, 2006, pp. 36 – 42.

30Amit Kr. Chakrabarty, “Efficiency of LIC – Post liberalization and globalization”, The

Insurance Chronicle, Chennai, Vol. 45, No. 19, January 1, 2007, pp. 23-27.

14

get benefited as they could select the best service provider that could provide all those

factors in the most comprehensive way.31

Syed Maruf Reza and Mohammed Masum Iqbal (2007) in their research paper

titled, “Life Insurance Marketing in Bangaladesh” had attempted to critically describe the

marketing of insurance in Bangladesh. The study depicted that insurance companies were

not marketing oriented and they were also void of marketing research. The study showed

the mentionable problems of insurance marketing in Bangladesh such as low per capita

income, poor knowledge of agents, illiteracy of prospects (target customers), religious

superstition, low awareness of prospects, low savings of target market, lack of continuity,

lack of reminder, negligence of policy holders, poor services to policy holders, low return

to the consumers, and lack of reliability and so on. To overcome the setback and improve

the performance of insurance marketing, some measures could be taken like, more

training to sales force, building awareness of prospects, diversified policies, more

marketing research for improved strategies, improving commitment of sales force, new

legislation, improve professional ethics, quick settlement of claims, expansion of

coverage and so on.32

D. Ramkumar (2007) in his thesis titled, “An Analysis of Relationship Marketing

in Life Insurance Companies in Madurai Division” studied the basic constructs of

Relationship Marketing Orientation (RMO) among the agents and also studied the

relationship between the profile of the agents and their relationship marketing orientation.

He found out that the determinants of RMO also required both theoretical and empirical

investigation, after all, managers need to know how they could be instrumental in shaping

the RMO of their agents.33

31M. Gurupandi, “Attitude of the Policyholders towards Life Insurance Corporation of

India – A Study with Special Reference to Ramanathapuram District”, Ph.D thesis,

Madurai Kamaraj University, Madurai, June 2007.

32Syed Maruf Reza and Mohammed Masum Iqbal, “Life Insurance Marketing in

Bangaladesh”, Daffodil International University Journal of Business and Economics,

Bangaladesh, Vol. 2, No. 2, July 2007, pp. 87 – 103.

33D.Ramkumar, “An Analysis of Relationship Marketing in Life Insurance Companies in

Madurai Division” Ph.D thesis, Madurai Kamaraj University, Madurai, September 2007.

15

Ogenyi Ejye Omar (2007) in his research paper titled, “The Retailing of Life

Insurance in Nigeria: An Assessment of Consumers‟ Attitudes” found that lack of

confidence in the insurance companies had the most negative effect on life insurance

purchase. Ignoring risks and reliance on family for help in emergencies were the other

main factors preventing purchase. He also revealed that intention was determined by

normative factors rather than the attitudinal factors. The recommendation was that

marketers should target marketing communication efforts.34

G. Karunanithi (2007) in his thesis titled, “Services Marketing of Life Insurance

Corporation of India in Madurai Division – A Study in View of Global Environment”

studied the attitude of the policyholders towards LIC of India and appraise the customers‟

services provided by LIC of India. He also studied the role of LIC agents in promoting

the life insurance marketing. He found that educational status of agents had no

relationship with level of attitude of the agents. He also found out the facts that the

factors like product attributes, customer delight, payment mode, product flexibility, risk

coverage, grace period, professional advisor and maturity period were likely to influence

the policyholders to choose the LIC product.35

T. R. N. Sivakumar (2007) in his thesis titled, “Attitude of Policyholders towards

Life Insurance Schemes of Life Insurance Corporation of India in Madurai Division”

studied the attitude of the policyholders in Madurai division and the life insurance

schemes of the Life Insurance Corporation of India. He found that the respondents

expected the LIC of India to reduce the period of surrender and to increase the surrender

value. He also found that there was significant relationship between sample respondent‟s

personal profile such as gender, age, marital status, family type, size of family, literacy

level, occupation, annual family income, residential status and their level of opinion on

the LIC of India. The study insisted that the LIC of India should provide huge funds to

34Ogenyi Ejye Omar, “The Retailing of Life Insurance in Nigeria: An Assessment of

Consumers‟ Attitudes”, Journal of Retail Marketing Management Research, Pune, Vol. 1

No.1, October 2007, pp. 41- 47.

35G. Karunanithi, “Services Marketing of Life Insurance Corporation of India in Madurai

Division – A Study in View of Global Environment”, Ph.D thesis, Madurai Kamaraj

University, Madurai, December 2007.

16

the central government and various state governments for constructing and developing

infrastructural facilities and also support to develop the national economy.36

R. Venkatesan (2007) in his thesis titled, “A Study on the Behavioral Pattern of

the LIC Policyholders with Reference to Life Insurance Schemes in the Madurai Division

of the Life Insurance Corporation of India” had studied the extent of utilisation of the

services of Life Insurance Corporation (LIC) by policyholders. He concluded that a good

insurance company was one that was financially strong, provided fair and prompt claims

settlement and provided good service before and after a loss. He had also suggested that

the return on life insurance had to be higher than that from savings media. He found that

age, sex, educational level, marital status, occupation and income influenced the level of

attitude of policyholders.37

Paromita Goswami (2007) in his research paper titled, “Customer Satisfaction

with Service Quality in the Life Insurance Industry in India” attempted to understand the

dimensions of service quality, which helped in ensuring maximum customer satisfaction,

and hence, helped life insurers to acquire a larger share of the market. It was found that

the responsiveness dimension of service quality provided maximum customer satisfaction

in the life insurance industry in India.38

V.V. Seshamohan and M.S. Narayana (2008) in their article titled, “Feedback of

Policyholders towards SBI Life Insurance” analysed the attitudes of policyholders

towards various aspects of the life insurance products of SBI life. They found that the top

four places were taken by LIC, SBILife, ICICI Prudential and Bajaj Allianz respectively.

They also pointed out that the LIC of India and many private sector companies were now

36T. R. N. Sivakumar, “Attitude of Policyholders towards Life Insurance Schemes of Life

Insurance Corporation of India in Madurai Division”, Ph.D thesis, Madurai Kamaraj

University, Madurai, December 2007.

37R. Venkatesan, “A Study on the Behavioral Pattern of the LIC Policyholders with

Reference to Life Insurance Schemes in the Madurai Division of the Life Insurance

Corporation of India”, Ph.D thesis, Madurai Kamaraj University, Madurai, December

2007.

38Paromita Goswami, “Customer Satisfaction with Service Quality in the Life Insurance

Industry in India”, The Icfai Journal of Services Marketing, Hyderabad, Vol. V, No. 1,

2007, pp. 25 – 30.

17

competing in the market. In the quest for gaining business and financial objectives, the

social objectives might be undermined. It was in this direction, that the companies in the

insurance sector had to plan and implement their strategies whether necessary or not.39

James C. Hao (2008) in his study titled, “Measuring Cost Efficiency in the

Taiwan Life Insurance Industry” examined the effects of increasing competition on the

structure of the Taiwan life insurance industry. A flexible stochastic cost frontier was

estimated for the industry using a sample of 25 firms over six years. The estimated

frontier was then used to compute measures of economic scale, and total efficiency for

different company size groups. The results showed that, on average, larger life insurance

companies were more efficient than smaller companies, but there were substantial

variations in the degree of efficiency within size groups.40

N. Panchanatham, Senthil Kumar, Jhansi, and Mani (2008) in their research paper

titled, “A Study on Policyholder‟s Expectation and Preference towards Selected Private

Life Insurance Companies in Karur District” had found that there was no significant

difference between the gender, age and media for advertising. It also found that there was

a relationship between the income and customer expectation about Life Insurance

Company.41

Jyoti Budhraja (2008) in his research paper titled, “Causes of Stress among

Insurance Employees: An Empirical Study” studied the causes of stress among insurance

employees. The paper analysed both organizational and individual factors for availing a

focused perspective on the causes of stress. It also identified that the employees mostly

39V.V. Seshamohan and M.S. Narayana “Feedback of Policyholders towards SBI Life

Insurance”, Marketing Mastermind, Hyderabad, Vol. VIII, No. 4, April 2008, pp. 43 –

45.

40James C. Hao, “Measuring Cost Efficiency in the Taiwan Life Insurance Industry”,

International Journal of Management, Canada, Vol. 25, No. 2, June 2008, pp. 279 – 285.

41N. Panchanatham, Senthil Kumar, Jhansi, and Mani “A Study on Policyholder‟s

Expectation and Preference towards Selected Private Life Insurance Companies in Karur

District”, Indian Journal of Marketing, New Delhi, Vol. , No. , August 2008, pp.

18

suffered from stress due to heavy work load and unattainable targets, thereby generating

work life imbalance and anxieties.42

Xiang, Jiang Ni, and Weiqi Wu (2008) in their research paper titled, “Statistical

Analysis and Empirical Study for Life Insruance” analysed the importance of insurance

and the application of probability statistics in the insurance, briefly described several

parameter models about life distribution. The paper discussed the establishment and use

of the life table, and statistically analysed the profit and loss and insured amount in life

insurance.43

Andy C W Chui and Chuck C Y Kwok (2008) in their research paper titled,

“National Culture and Life Insurance Consumption” examined the way national culture

affects consumption patterns of life insurance across countries. The findings showed that

individualism indeed had a significant, positive effect on life insurance consumption,

whereas, power distance and masculinity/femininity had significant, negative effects.44

Marijana Ćurak and Sandra Lončar (2008) in their research paper titled,

“Insurance Development and Economic Growth NEXUS” examined empirically, whether

the insurance sector played a growth-supporting role while controlling for other

influences on economic growth. Life insurance development was significantly and

positively related to economic growth.45

Lavanya Vedagiri Rao (2008) in her research paper titled, “Innovation and New

Service Development in Select Private Life Insurance Companies in India” found that all

42Jyoti Budhraja “Causes of Stress among Insurance Employees: An Empirical Study”,

Icfai Journal of Management Research, Hyderabad, Vol. VII, No. 10, October 2008, pp.

1 – 17.

43Xiang, Jiang Ni, and Weiqi Wu, “Statistical Analysis and Empirical Study for Life

Insurance”, International Journal of Business and Management, Canada, Vol. 3, No. 10,

2008, pp. 23 – 29.

44Andy C W Chui and Chuck C Y Kwok, “National Culture and Life Insurance

Consumption”, Journal of International Business Studies, East Lansing, USA, 2008, pp.

88–101.

45Marijana Ćurak and Sandra Lončar in their research paper titled, “Insurance

Development and Economic Growth NEXUS”, Journal of International Research

Publications: Economy and Business, Bulgaris, Volume 3, 2008, pp. 35 – 42.

19

the ten private life insurance companies had a formal NSD (New Service Development)

unit and the top executives and research and development department participated in the

creation of new services. The role of customers was also considered important. The

results showed that there was potential for increasing customer involvement in the NSD

process. Another observation from the study was that the top executives of all the ten

companies participated in the idea generation stage.46

Jayanthi Ranjan and Saani Khalil (2008) in their research paper titled, “Building

Data Warehouse at Life Insurance Corporation of India: a case study” presented a case

description into the new IT strategies in general and Data Warehouse in particular

adopted by Indian insurance giant, Life Insurance Corporation (LIC). LIC, a public sector

enterprise, was the largest insurance company in India, selling insurance products and

related services. The case examined the need to build IT–data centre at LIC. The case

examined how LIC gear up to sustain the leadership status in Indian life insurance

industry by revisiting its IT resources.47

N. Kathirvel (2009) in his research paper titled, “Impact of Media Advertisement

on Life Insurance with Reference to Coimbatore City” studied the awareness of life

insurance advertisements in media, and analysed the extent of penetration of life

insurance. He found that the respondents of Coimbatore city preferred life insurance

policy the most. They wanted the life insurance policies to specially benefit the

agriculturist, so as to improve their cost of living and standard. They felt that the

government should take necessary steps to make life insurance policy compulsory for

every individual. Moreover, commercial channels were the best sources for telecasting

the life insurance advertisements.48

46Lavanya Vedagiri Rao, “Innovation and New Service Development in Select Private

Life Insurance Companies in India”, Communications of the IBIMA, Norristown, USA,

Volume 1, 2008, pp. 128 – 136.

47Jayanthi Ranjan and Saani Khalil, “Building Data Warehouse at Life Insurance

Corporation of India: a case study”, International Journal of Business Innovation and

Research, Dartmouth, USA, Vol. 2, No.3, 2008, pp. 241 - 261.

48N. Kathirvel, “Impact of Media Advertisement on Life Insurance with Reference to

Coimbatore City”, The Icfai University Journal of Risk and Insurance, Hyderabad, Vol.

VI, No. 2, April 2009, pp. 44-52.

20

C. Vijayakumar and P. Umamaheswari (2009) in their research paper titled, “A

study on 360 degree performance appraisal systems in Reliance Life Insurance,

Udumalpet” analysed the capabilities and execution with regard to business acumen,

customer focus, values and ethics, vision and purpose, bias for action, commitment,

teamwork, innovation, developing people performance and decision making. The study

found that there was no significant difference between the opinion of customers and

managers towards the satisfaction level of employees regarding job knowledge / skill.49

Pa. Keerthi and R. Vijayalakshmi (2009) in their study titled, “A Comparative

Study on the Perception Level of Services Offered by LIC and ICICI Prudential”

analyzed the level of satisfaction and satisfaction level of the policyholders from the

services offered by LIC and ICICI Prudential. They concluded that all the policyholders

of both LIC and ICICI Prudential had shown their satisfaction towards the services of

both insurance companies. Both LIC and ICICI Prudential did not show any difference in

delivery of services in case of two factors namely, gender and income of policyholders.

But in case of other demographic factors such as age, marital status, number of family

members in the family, education and occupation of respondents both the insurance

company had shown their variation in delivering the service.50

Ashok Khurana in his research paper titled, “An Empirical Study on Performance

of Unit Linked Pension Plans of Selected Private Sector Life Insurance Companies”

compared the performance of pension funds and found out the best performing pension

fund amongst the selected insurance players. He found that the pension plan of ICICI

Prudential was the most reasonable as far as diverse charges in the selected unit linked

49C. Vijayakumar and P. Umamaheswari “A study on 360 degree performance appraisal

systems in Reliance Life Insurance, Udumalpet”, Icfai Journal of Management Research,

Hyderabad, Vol. VIII, No. 7, July 2009, pp. 65 – 78.

50Pa. Keerthi and R. Vijayalakshmi, “A Comparative Study on the Perception Level of

Services Offered by LIC and ICICI Prudential”, Indian Journal of Marketing, New Delhi,

Vol. XXXIX, No. 8, August 2009, pp. 41 - 54.

21

pension plans were concerned. He also found that the performance of the selected

pension funds did not differ significantly in comparison to its benchmark index.51

J. Chandra Prasad, S. Hari Babu, K. Chiranjeevi and K.V.V.S Visweswara Rao in

their research paper titled, “Unit Linked Insurance Plans – The Tasters‟ Perceptions on

the Mixed Bag of Fruits” brought out the perceptions of investors on ULIPs with respect

to other investment instruments. They found that demographic characteristics had a

significant impact over the level of investment in ULIPs. They also found that agents

were the most preferred channels of distribution of insurance policy.52

P. K. Gupta (2009) in his research paper titled, “Exploring Rural Markets for

Private Life Insurance Players in India” examined the current status of rural insurance

penetration and explored the reasons for poor performance of the private players in this

segment. The paper critically examined the marketing strategies of private life insurance

players in the rural segment and offered suggestions for enhancing penetration and brand

image. He found that the fear of life had not been commercially communicated to the

rural masses since long. The income levels and lack of awareness were the important

reasons for rural population not being insured. This was an important implication for

private players.53

Rajesh C. Jampala and B. Venkateswara Rao in their research paper titled, “Sales

Promotion in the Insurance Sector: A Study of LIC” unveiled the increasing significance

of sales promotion strategies which, in turn, influenced the behaviour of consumers in a

desired way. The paper attributed the reasons for the phenomenal usage of sales

promotional measures to the increasing competition, declining brand loyalty and

consumer sensitivity. He discussed about various strategies adopted by LIC of India,

51Ashok Khurana, “An Empirical Study on Performance of Unit Linked Pension Plans of

Selected Private Sector Life Insurance Companies”, Indian Journal of Finance, New

Delhi, Vol. III, No. 11, November 2009, p. 17 – 23.

52J. Chandra Prasad, S. Hari Babu, K. Chiranjeevi and K.V.V.S. Visweswara Rao, “Unit

Linked Insurance Plans – The Tasters‟ Perception on the Mixed Bag of Fruits”, Indian

Journal of Finance, New Delhi, Vol. III, No. 11, November 2009, p. 42 – 52.

53P. K. Gupta, “Exploring Rural Markets for Private Life Insurance Players in India”, The

Icfai University Journal of Risk and Insurance, Hyderabad, Vol. VI, No. 3 &4, 2009, pp.

7-21.

22

which include consumer promotion strategy, trade promotion strategy, and sales force

promotion strategy.54

Mekala Mary Selwyn in her paper titled, “An Evaluation of Distribution Channels

in Life Insurance: Agents vs Bancassurance” outlined the insurance industry in India

which was witnessing a rapid growth. She focused on the evolution of different

distribution channels in the insurance industry. She found that insurance players were

adopting different strategies for the changing environment and the growing

competition.55

Sanchit Maini and Sumit Narayanan in their paper discussed about policyholders‟

reasonable expectation by the actuarial professors, the regulations and the courts. The

equitable life judgement was the first extensive legal test of policyholders‟ reasonable

expectations and had significant impact on the life insurance industry. It was an

opportune time for the actuarial professors and insurance industry in India to address

various facts of measuring, managing and monitoring policyholders‟ reasonable

expectations.56

E. R. Mohankumar in his study titled, “Customer Perception and Attitude towards

the Products of Birla Sun life Insurance” aimed at knowing the customer perception and

attitude towards the products of Birla Sun Life Insurance. He found that the respondents

had invested more in life insurance schemes, which was a positive stroke to the insurers.

This proved the point that there was a strong presence of insurance in Mysore City. He

also found that majority of the respondents were insurance policy holders, the insurance

business dominated by LIC, still there were larger market opportunities for other private

players. Awareness of Birla Sun Life Insurance in Mysore City was high and this was

54Rajesh C. Jampala and B. Venkateswara Rao, “Sales Promotion in the Insurance Sector:

A Study of LIC”, www. Icfaiuniversitypress.org/books/iuponinsurance-ovw.asp, 2010.

55Mekala Mary Selwyn, “An Evaluation of Distribution Channels in Life Insurance:

Agents vs Bancassurance”, www.Icfaiuniversitypress.org/books/iuponinsurance-ovw.asp,

2010.

56Sanchit Maini and Sumit Narayanan, “On Policyholders Reasonable Expectation”,

www.actuariesindia.org, 2010.

23

created by Birla Sun Life Insurance Advisors. According to the survey most of the

respondents liked Birla Sun Life Insurance because of its Brand name and for its services

provided to the Clients. The main purpose of life insured was for risk coverage and

savings. As the products of Birla Sun Life Insurance were good and it has also found out

that there was a wide market in Mysore for Birla Sun Life Insurance.57

John Sullivan in his research titled, “African Americans Value Life Insurance

Protection More than General Population” compared the financial goals of African

Americans to the general population and found that the top three goals–having enough

money for a comfortable retirement; having adequate health insurance; and paying off

debts such as student loans, credit card debt and mortgage–were the same. However,

African Americans placed more importance on having life insurance and having a plan to

replace income if unable to work than the general population. He found that the financial

goals vary depending on age. He also found that a third of African Americans indicated

that their risk tolerance levels had decreased over the past years. This implied that

African Americans now might be more conservative with their investments. As a result,

their savings might not grow fast enough for them to achieve their various financial

goals. African Americans were more receptive to buy life insurance today than in the

past and that they had a more positive attitude towards life insurance companies.58

Donghui Li, Fariborz Moshirian, Pascal Nguyen, Timothy Wee in their research

paper titled, “The Demand for Life Insurance in OECD Countries” examined the

determinants of life insurance consumption in OECD countries. They found that there

was a significant positive income elasticity of life insurance demand. Demand also

increased with the number of dependents and level of education, and decreased with life

expectancy and social security expenditure. The country's level of financial development

and its insurance market's degree of competition appeared to stimulate life insurance

57E. R. Mohankumar, “Customer Perception and Attitude towards the Products of Birla

Sun life Insurance”, www.indiastudychannel.com/.../4945-Customer-perception-attitude-towards-products -Birla- Sun-Life-Insurance.aspx, 2010.

58John Sullivan, “African Americans Value Life Insurance Protection More than General

Population”,www.investmentadvisor.com/.../LIMRA-African-Americans-Value-Life-Insurance-Protection-More-Than-General-Population.aspx, 2010.

24

sales, whereas, high inflation and real interest rates tend to decrease consumption.

Overall, life insurance demand was better explained when the product market and socio-

economic factors were jointly considered.59

B. Douglas Bernheim, Solange Berstein, Jagadeesh Gokhale and Laurence J.

Kotlikoff in their research paper titled, “Saving and Life Insurance Holdings at Boston

University – a Unique Case Study” examined the saving and insurance behaviour of 386

Boston University (BU) employees who volunteered to receive financial planning based

on ES Planner (Economic Security Planner)–a detailed life-cycle financial planning

model developed by Economic Security Planning, Inc. Because the employees received

their own financial plan, they had a strong incentive to provide full and accurate financial

information. They found that the correlation between ES Planner's saving and insurance

prescriptions and the actual decisions being made by BU employees was very weak in the

case of saving and essentially zero in the case of life insurance. Many employees were

spending far more and saving far less than they should, while others were under-spending

and over saving. The same hold for life insurance. The degree of under-insurance seemed

particularly acute. They also found that planning shortcomings were common among

high-income professors with significant financial knowledge as they were among low-

income staff with limited financial knowledge.60

Pin Luarn, Tom M. Y. Lin, and Peter K. Y. Lo in their research paper titled, “An

Exploratory Study of Advancing Mobilisation in the Life Insurance Industry: The Case of

Taiwan‟s Nan Shan Life Insurance Corporation” employed a case study method, using

in-depth interviews of 29 corporate managers and experts to understand the current state

of mobilization in the life insurance industry. The study suggested a conceptual

framework for mobilization in the life insurance industry, and formulated possible

research propositions incorporating a number of variables. The study also suggested a

59Donghui Li, Fariborz Moshirian, Pascal Nguyen, Timothy Wee, “The Demand for Life

Insurance in OECD Countries”,http://findarticles.com /p/articles/mi_hb6645 /is_3_74/

ai_n29373223/pg_13/?tag=content;col1, 2010.

60B. Douglas Bernheim, Solange Berstein, Jagadeesh Gokhale and Laurence J. Kotlikoff,

“Saving and Life Insurance Holdings at Boston University – a Unique Case Study”, http://

ner.sagepub.com/content/ 198/1 /75.abstract, 2010.

25

total of ten key success factors for the implementation of mobilization in the life

insurance industry.61

Chiang Ku Fan and Shu Wen Cheng in their research paper titled, “An Efficiency

Comparison of Direct and Indirect Channels in Taiwan Insurance Marketing” compared

the efficiency of bancassurance, and an indirect marketing channel formed through the

creation of subsidiaries, with an insurer's own team, a direct marketing channel, in the

Taiwan insurance sector. They found that the efficiency score of a direct marketing

channel was significantly higher than that of a comparable indirect marketing channel.

The efficiency relationship between the indirect marketing channel and the direct

marketing channel were independent. A marketing efficiency evaluation, when divided

into different marketing channels for evaluation, provided meaningful results for

marketing decision-makers.62

Tajudeen Olaleken Yusuf, Ayantunji Gbadamosi and Dallah Hamadu (2009) in

their research paper titled, “Attitude of Nigerians‟ towards Insurance Services: An

Empirical Study” described Nigerians attitudes towards the insurance institution. The

attitudes, most often negative, were mirrored through low patronage of insurance

services. It discussed the social cultural factors that account for these attitudes and what

role the marketing strategies could play to change such negative tide. The findings

presented different demographical factors and their attitudes towards insurance

companies and their services.63

S. Raju and M. Gurupandi in their research paper titled, “Analysis of the Socio –

Economic Background and Attitude of the Policyholders towards Life Insurance

61Pin Luarn, Tom M. Y. Lin, and Peter K. Y. Lo in their research paper titled, “An

Exploratory Study of Advancing Mobilisation in the Life Insurance Industry: The Case of

Taiwan‟s Nan Shan Life Insurance Corporation”,http://www.emeraldinsight.com

/journals.htm? articleid = 863785&show = html. 2010.

62Chiang Ku Fan and Shu Wen Cheng, “An Efficiency Comparison of Direct and Indirect

Channels in Taiwan Insurance Marketing”, http:// www.emeraldinsight.com /journals.htm

?issn=17505933&volume=3&issue=4&articleid=1817108&show=html&PHPSESSID=62

jnivlbrks7s65icb20s3ptu2, 2010. 63Tajudeen Olaleken Yusuf, Ayantunji Gbadamosi and Dallah Hamadu, “Attitude of

Nigerians towards Insurance Services: An Empirical Study”, African Journal of

Accounting, Economics, Finance and Banking Research, Africa, Vol. 4, No. 4, 2010, pp.

121 – 129.

26

Corporation of India” attempted to study the socio-economic background and attitude of

the policyholders towards LIC in Ramanathapuram District. The factors like sex of the

policyholders, occupation and patronage mentality of the policyholders did not influence

the level of attitude.64

K. P. Rajalakshmi and K. Javahar Rani (2010) in their research paper titled, “A

Study on the Perception of Insurance Policyholders regarding Met Life Insurance”

highlighted the latest development in optimizing and financial resources ensuring

maximum customer satisfaction and to gain larger share in the market. They found that

there was no difference between the satisfaction level of the respondents among various

age groups, gender and income level of respondents. They also found that customers

were very much interested to invest, if the premium rates were reduced and the company

offers flexible plans for the policyholders.65

S. Ayem Perumal (2010) in his research paper titled, “Impact of Economic

Globalisation and Consumer Expectation in Life Insurance” identified the attributes

relating to customer expectation and their influence on the purchase of Life insurance

products from LIC and Private Life Insurance Companies (PLIC). He found that the

expectations of the customers of LIC and PLIC were very high and had not been met by

the insurance companies. Transperancy and extra coverage expectations were high in the

case of LIC and PLIC customers. The customers of LIC had a higher level of corporate

image expectations. He suggested that both LIC and the private insurance companies

should device their schemes with due considerations to meet the challenges in the global

era.66

64S. Raju and M. Gurupandi, “Analysis of the Socio – Economic Background and Attitude

of the Policyholders towards Life Insurance Corporation of India”,www

.smartjournalalbms. org, 2010.

65K. P. Rajalakshmi and K. Javahar rani, “A Study on the Perception of Insurance

Policyholders regarding Met Life Insurance”, International Journal of Enterprise and

Innovation Management Studies, Singapore, Vol. 1, No. 2, Jan – June 2010, pp. 97 – 104.

66S. Ayem Perumal, “Impact of Economic Globalisation and Consumer Expectation in

Life Insurance”, Southern Economist, Bangalore, Vol. 48, No. 21, March 1, 2010, pp. 8 -

10.

27

Ashok Shanubhogue and Mayank V. Bhatt (2010) in their research paper titled,

“Business Opportunities for Insurance Sector: An Empirical Study among Teachers of S.

P. University” found out the trend of investment in LIC and private insurance

organizations. They revealed that LIC covered the entire market of insurance. They also

revealed that irrespective of category, almost all teachers preferred LIC as opposed to

private insurances. They also found that advisors, friends and tax benefits were the most

influencing factors in purchasing the insurance.67

M. Gurupandi (2010) in his research paper titled, “Factors Influencing the

Purchase of Life Insurance Policy by Policyholders – An Analytical Study” determined

the factors which should be taken into consideration before purchasing the life insurance

policy by the policyholders. He found that product attributes, customer delight, payment

mode, product flexibility, risk coverage, grace period, professional advisor and maturity

period were the identified dimensions which influence the purchase of life insurance

products.68

R. Rajendran and B. Natarajan in their research paper titled, “The Impact of

Liberalisation, Globalisation and Privatisation (LPG) on Life Insurance Corporation of

India” compared the overall performance of LIC of India in the pre and post liberalization

era. It was found that the business in India and the business outside India as well as the

total businesses of LIC of India were always in an increasing trend. It was also found that

the LPG was incorporating a positive influence on LIC of India and its performance.69

K. Nagaraja Rao (2010) in his research paper titled, “Changing Rural Customer

Profile: A Case with Life Insurance” found that the preferences of customers were

changing towards investment policies in India. He also found that customers also

67Ashok Shanubhogue and Mayank V. Bhatt, “Business Opportunities for Insurance

Sector: An Empirical Study among Teachers of S. P. University”, Indian Journal of

Marketing, New Delhi, Vol. 40, No. 5, May 2010, pp. 52 - 56.

68M. Gurupandi, “Factors Influencing the Purchase of Life Insurance Policy by

Policyholders – An Analytical Study”, Business Plus, Sivakasi Vol. 1, No. 2, July 2010,

pp. 1-6.

69R. Rajendran and B. Natarajan, “Impact of Liberalisaiton, Privatisation and Globalisation

on Life Insurance Corporation of India”, African Journal of Business Management,

Africa, Vol. 4(8), July 18, 2010, pp. 1457-1463.

28

preferred annuities and family policies if the benefits were properly explained to them.

He concluded that bancassurance and alternate channels were on the ascendancy and had

great growth potential.70

Andre P. Liebenberg, James M. Carson and Robert E. Hoyt (2010) in their

research paper titled, “The Demand for Life Insurance Policy Loans” had examined the

demand for life insurance policy loans. They also examined the four hypotheses

traditionally associated with policy loan demand. They found that the more detailed

emergency fund proxies used here revealed a significantly positive relation between loan

demand and recent expense or income shocks.71

Manish Srivastava and Megha Rastogi (2010) in their research paper titled, “Life

Insurance and Working Women: A Critical Study of Factors Affecting the Purchase

Decision” had identified the factors perceived by working women for selecting the life

insurance products. They found that there was no difference in expectation and

satisfaction level of working women regarding life insurance. They also found that risk

coverage, company‟s brand name and father / husband‟s advice were the most influential

attributes for the purchase of insurance policy by working women. The main objective of

purchasing policies for working women was to save income tax. Majority of them had

invested their money on government approved LIC because they were risk aversive.72

Bauer, Daniel, Bergmann, Daniela, KieseL and Rüdiger (2010) in their research

paper titled, “On the Risk-Neutral Valuation of Life Insurance Contracts with Numerical

Methods in View” presented a generic model for the valuation of life insurance contracts

and embedded options. Furthermore, the study described various numerical valuation

approaches within our generic setup. The study particularly focused on contracts

containing early exercise features since these presented (numerically) challenging

70K. Nagaraja Rao, “Changing Rural Customer Profile: A Case with Life Insurance”,

Southern Economist, Bangalore, Vol. 49, No. 7, August 1, 2010, pp. 41-43.

71Andre P. Liebenberg, James M. Carson and Robert E. Hoyt, “The Demand for Life

Insurance Policy Loans”, Journal of Risk and Insurance, Hyderabad, Vol. 77, Issue 3,

September 2010, pp. 651 – 666.

72Manish Srivastava and Megha Rastogi, “Life Insurance and Working Women: A Critical

Study of Factors Affecting the Purchase Decision”, Indian Journal of Marketing, New

Delhi, Vol. 40, No. 11, November 2010, pp. 53 – 61.

29

valuation problems. Based on an example of participating life insurance contracts, it

illustrated the different approaches and compared their efficiency in a simple and a

generalized Black-Scholes setup, respectively. Moreover, they studied the impact of the

considered early exercise feature on our example contract and analyze the influence of

model risk by additionally introducing an exponential Lévy model.73

Deepika Upadhyaya and Manish Badlani (2011) in their research paper titled,

“Service Quality Perception and Customer Satisfaction in Life Insurance Companies in

India” intended to promote a better theoretical understanding and recognition of the

complexities to service quality and its measurement with respect to life insurance. This

study emphasized the role of technology to improve quality and hence customer

satisfaction.74

Syamala Rao (2012) in her research paper titled, “Policyholder‟s Perceptions on

LIC Policies and Services with Reference to Srikakulam District in Andhra Pradesh”

found that technology will play a crucial role in delivery of the service of the highest

standard to both the end customers as well as the intermediary. It helped to reduce the

cost significantly and hence, got reflected in the price of the products.75

Srinivas D. L and Anand M. B (2012) in their research paper titled, “Investors‟

Perceptions on Public and Private Life Insurance Companies in India – with Special

Reference to Life Insurance Investors in Karnataka” focused on the perception of

individual investors of life insurance. The study concentrated on the behavioral aspects of

73Bauer, Daniel, Bergmann, Daniela, KieseL and Rüdiger, “On the Risk-Neutral Valuation

of Life Insurance Contracts with Numerical Methods in View”, ASTIN Bulletin, Canada,

Vol. 40, Issue: 1, 2010, pp. 65 – 95.

74 Deepika Upadhyaya and Manish Badlani, “Service Quality Perception and Customer

Satisfaction in Life Insurance Companies in India”, International Conference on

Technology and Business Management, March 2011, pp. 1011-1024.

75 Syamala Rao, “Policyholder‟s Perceptions on LIC Policies and Services with Reference

to Srikakulam District in Andhra Pradesh”, International Journal of Management and

Social Science Research, New Delhi, Volume 1, No. 1, October 2012, pp.25-28.

30

individual investors, their policy selection behavior, factors influencing the behavior and

also the conceptual awareness level among individual investors.76

Preeti Upathyay (2013) in her research paper titled, “Satisfaction of the Policy

Holders Protection in Insurance Sector: A Case Study” analysed the public awareness

about the entry of private sector and their products. She compared various insurance

policies/schemes/products offered by the public and private insurance companies.77

It is understood from the reviews collected that there is a research gap in the area

of comparative analysis between public and private life insurance companies. In order to

fill such gap, the present study is undertaken with the following objectives.

1.4 OBJECTIVES OF THE STUDY

The following objectives are set for the present study.

1. To study the growth and development of life insurance business in India.

2. To determine the factors influencing the selection of Life insurance products in

Virudhunagar District.

3. To analyse the perception of policyholders towards the services of Life Insurance

Companies and life insurance agents in Virudhunagar District.

4. To compare the perception of policyholders towards the services of Public and

Private Life Insurance Companies in Virudhunagar District.

5. To evaluate the opinion of agents about the perception of policyholders of life

insurance companies in Virudhunagar District.

6. To offer suitable suggestions on the basis of the findings of the study.

76 Srinivas D. L and Anand M. B, “Investors‟ Perceptions on Public and Private Life

Insurance Companies in India – with Special Reference to Life Insurance Investors in

Karnataka”, International Journal of Research in Commerce and Management, Haryana,

Volume no. 1, Issue no. 12, December 2012, pp. 38-46. 77 Preeti Upathyay, “Satisfaction of the Policy Holders Protection in Insurance Sector: A

Case Study”, International Journal of Advanced Research in Computer Science and

Software Engineering, Australia, Volume 3, Issue 2, February 2013, pp. 32 – 40.

31

1.5 HYPOTHESES OF THE STUDY

On the basis of the foregoing research objectives, the following null hypotheses have

been formulated for the purpose of the present study.

1 There is no significant difference between the growth rate of public and private life

insurance companies.

2 There is no significant relationship between the level of perception of policyholders

of public and private Life Insurance companies towards the services of life insurance

companies.

3 There is no significant relationship between the level of perception of policyholders

of public and private Life Insurance companies towards the services of life insurance

agents.

4 There is no significant relationship between the socio-economic conditions of

policyholders and their level of perception towards the services of insurance

companies.

5 There is no significant relationship between the socio-economic conditions of

policyholders and their level of perception towards the services of agents.

1.6 SCOPE OF THE STUDY

The study is mainly planned to analyse the perception of the policyholders in

Virudhunagar district towards the services of life insurance companies and agents. The

study attempts to determine the factors influencing the selection of life insurance

products. The study also analyses the opinion of the agents about the perception of the

policyholders. Further, the study compares the perception of policy holders of private and

public life insurances in Virudhunagar District.

1.7 SIGNIFICANCE OF THE STUDY

A major portion of domestic savings originates in the household sector where the

preference for direct savings in the form of tangible assets still dominated over savings in

financial forms over the years. However, the share of the financial savings has gone up.

This trend has benefited several financial institutions including life insurance companies.

Any further growth in life insurance can arise from an increased volume of

savings in the household sector and transfer of savings to insurance from other competing

32

claimants. To assess the potential of life insurance companies, one should know atleast

the extent of savings in the household sector and its destination. Besides, the decision

making process has also to be understood so as to be able to devise suitable policies.

Several factors like income, its growth and distribution, social customs and traditions,

parental aspirations, and regional affinities and sectoral bonds influence the decision

making process.

Among those who prefer financial assets over physical assets, a range of