Embed Size (px)

Citation preview

Chapter 9Property and transaction taxation

Contents

Summary 277

9.1 Introduction 277

9.2 Broad international comparisons 278

9.3 Recurrent taxes on immovable property 279

9.4 Recurrent taxes on net wealth 281

9.5 Estate, inheritance and gift taxes 282

9.6 Taxes on fi nancial and capital transactions 284

AppendicesAppendix 9.1: Taxes on immovable property 290Appendix 9.2: Estate, inheritance and gift taxes 293Appendix 9.3: Taxes on the transfer of real estate 296Appendix 9.4: Examples of other fi nancial and capital transaction taxes 297

Page 277

9. PROPERTY AND TRANSACTION TAXATION

SUMMARY

Although Australia has a comparatively high reliance on property and transaction taxes (3.0 per cent of GDP) and is seventh highest of the OECD-30, in terms of the OECD-10, Australia’s overall tax burden is much closer to the unweighted average (2.7 per cent).

Most property and transaction taxes in Australia are levied by sub-national governments — the State, Territory and local governments.

Australia’s tax burden from taxes on immovable property is below the unweighted average of the OECD-10.

Of the OECD-10, Australia has the highest financial and capital transaction tax burden (includes taxes such as stamp duties on conveyances).

Australia’s top rate for stamp duty on conveyances (7 per cent) is the equal second highest of the OECD-10.

Australia is the only OECD-10 country which does not levy either a recurrent wealth tax, or any estate, inheritance or gift taxes.

9.1 INTRODUCTION

Property and transaction taxes cover taxes levied on the use, ownership or transfer of property, including:

• taxes on immovable property, for example, land tax and municipal rates;

• taxes on net wealth;

• taxes on the change of ownership of property through inheritance or gift; and

• taxes on financial and capital transactions, for example, stamp duties on conveyances and cheques.

This chapter compares Australia’s property and transaction tax burden with the other OECD-10 countries over these four sub-categories. Information on the comparison across the OECD-30 is included in Chapter 3.

As for other areas where the OECD data are disaggregated finely, there are classification issues which mean that particular care needs to be taken in making comparisons across countries (and through time).

International comparison of Australia’s taxes

Page 278

A wide variety of taxes fall into the property and transaction taxes category and there is considerable diversity between countries in the implementation and design of these taxes.

In Australia, virtually all taxes covered by this category are levied by the sub-national governments. In the other OECD-10 countries, the levels of government imposing these taxes differ. For the majority, sub-national governments are more reliant on these taxes than national governments as a source of revenue.

9.2 BROAD INTERNATIONAL COMPARISONS

As discussed in Chapter 3, Australia has a comparatively high reliance on property and transaction taxes (3.0 per cent of GDP) and is eighth highest of the OECD-30. In terms of the OECD-10, Australia’s overall tax burden in this category is much closer to the unweighted average. Australia is fourth highest in terms of tax burden of the OECD-10 (see Chart 9.1).

Chart 9.1: Property and transaction tax burden OECD-10, taxation revenue as a proportion of GDP, ordered by tax burden, 2003

0

1

2

3

4

5

NZ

Irela

nd

Net

herla

nds

Sw

itzer

land

Japa

n

Spa

in US

Can

ada

UK

0

1

2

3

4

5

Immovable property Recurrent taxes on net wealth Estate, gift and inheritanceTransactions Other property

Aus

tral

ia

Unweighted average

Per cent of GDP Per cent of GDP

Source: OECD Revenue Statistics, 2005. As is the case for all OECD countries, there is considerable diversity across the OECD-10 in the mix of property and transaction taxes.

As shown in Chart 9.2, the Australian mix is quite different from the average OECD-10 mix. Australia’s proportion of the tax mix from immovable property taxes is below the average, whereas Australia’s transaction tax burden is significantly above the average.

Australia does not have wealth taxes or estate, inheritance and gift taxes. The other OECD-10 countries all levy at least one of these types of taxes. (New Zealand imposes a gift tax, but the revenue collected from this tax is less than 0.01 per cent of GDP.)

Chapter 9: Property and transaction taxation

Page 279

Chart 9.2: Australia’s property and transaction tax mix OECD-10, 2003

Australia OECD-10 average

Property taxes

Transaction taxes

Property taxes

Transaction taxes

Other

Wealth taxes Estate & gift

Source: OECD Revenue Statistics, 2005.

9.3 RECURRENT TAXES ON IMMOVABLE PROPERTY

Recurrent taxes on immovable property are defined by the OECD as taxes levied regularly in respect of the use or ownership of immovable property. Usually, these taxes are levied on land and/or buildings.

In Australia’s case, the majority of revenue under this category is from local government rates. Land taxes levied by State and Territory governments are also a significant component.

Taxes on immovable property do not include taxes on incomes flowing from property ownership (for example, rental income) or taxes on incomes flowing from the sale of property (for example, capital gains). These types of taxes are included in the relevant categories of income taxation revenue.

While Australia has the seventh highest immovable property tax burden (1.4 per cent of GDP) of the OECD-30, it is below the average of the OECD-10 (1.6 per cent).

Of the OECD-10, the United Kingdom has the highest reliance on immovable property taxes, and the United States, Canada, Japan and New Zealand are also relatively heavily reliant.

International comparison of Australia’s taxes

Page 280

Chart 9.3: Taxes on immovable property OECD-10, taxation revenue as a proportion of GDP, ordered by tax burden, 2003

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5S

witz

erla

nd

Irela

nd

Spa

in

Net

herla

nds

NZ

Japa

n

Can

ada

US

UK

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

A

Unweighted average

Aus

tral

ia

Per cent of GDP Per cent of GDP

Source: OECD Revenue Statistics, 2005. Among the OECD-10, these types of taxes are generally levied by sub-national governments. As such, analysis of their characteristics is more difficult, because information on rates and bases is not as readily available and can vary widely within countries.

Table 9.1 summarises the number of these types of taxes levied in the OECD-10 and the different levels of government levying them. Table 9.2 summarises the tax bases used in the OECD-10. Comparable information on rates and bases is not readily available and the information in the following tables must be treated with caution as the detailed information has not been verified with the individual countries.

Table 9.1: Number of recurrent taxes on immovable property in the OECD-10 countries National government State government Local government Australia - 1 1

Canada - - 1

Ireland - - 1

Japan - - 3

Netherlands - - 1

New Zealand - - 1

Spain - - 1

Switzerland - 1 -

United Kingdom 1 - 1

United States - 1 1 Source: Various, see Chapter 1 (1.4.1).

Chapter 9: Property and transaction taxation

Page 281

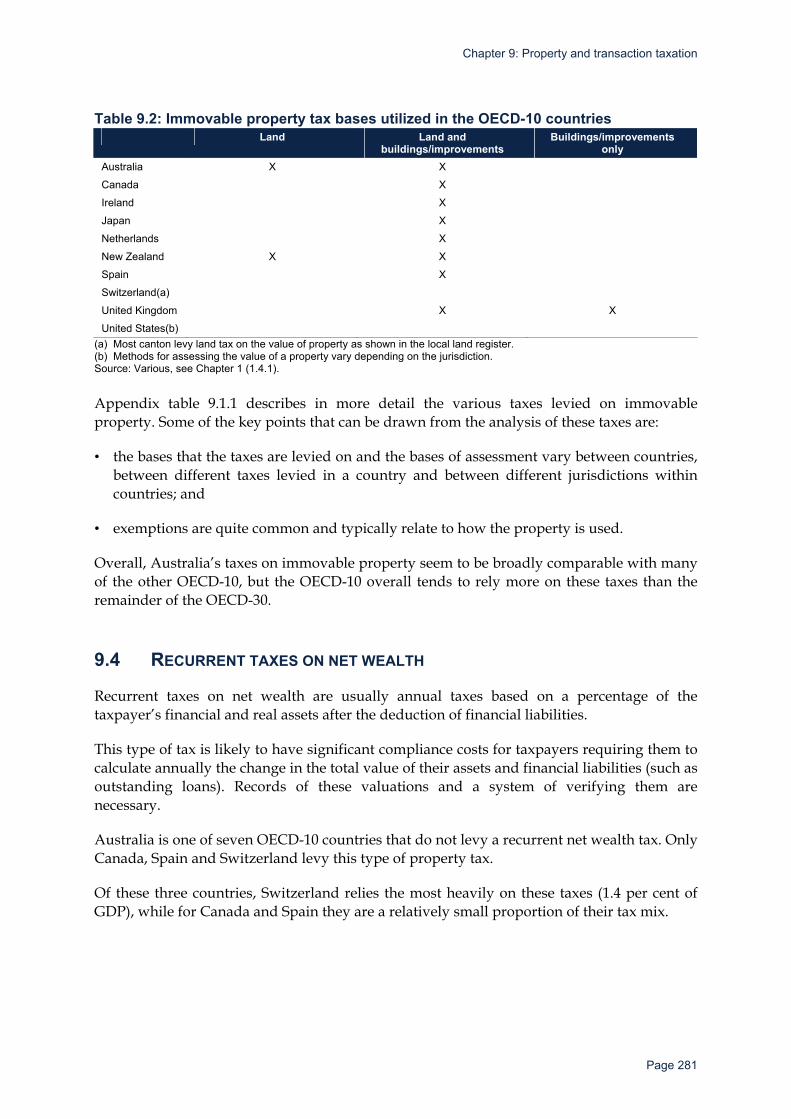

Table 9.2: Immovable property tax bases utilized in the OECD-10 countries

Land Land and buildings/improvements

Buildings/improvements only

Australia X X

Canada X

Ireland X

Japan X

Netherlands X

New Zealand X X

Spain X

Switzerland(a)

United Kingdom X X

United States(b) (a) Most canton levy land tax on the value of property as shown in the local land register. (b) Methods for assessing the value of a property vary depending on the jurisdiction. Source: Various, see Chapter 1 (1.4.1). Appendix table 9.1.1 describes in more detail the various taxes levied on immovable property. Some of the key points that can be drawn from the analysis of these taxes are:

• the bases that the taxes are levied on and the bases of assessment vary between countries, between different taxes levied in a country and between different jurisdictions within countries; and

• exemptions are quite common and typically relate to how the property is used.

Overall, Australia’s taxes on immovable property seem to be broadly comparable with many of the other OECD-10, but the OECD-10 overall tends to rely more on these taxes than the remainder of the OECD-30.

9.4 RECURRENT TAXES ON NET WEALTH

Recurrent taxes on net wealth are usually annual taxes based on a percentage of the taxpayer’s financial and real assets after the deduction of financial liabilities.

This type of tax is likely to have significant compliance costs for taxpayers requiring them to calculate annually the change in the total value of their assets and financial liabilities (such as outstanding loans). Records of these valuations and a system of verifying them are necessary.

Australia is one of seven OECD-10 countries that do not levy a recurrent net wealth tax. Only Canada, Spain and Switzerland levy this type of property tax.

Of these three countries, Switzerland relies the most heavily on these taxes (1.4 per cent of GDP), while for Canada and Spain they are a relatively small proportion of their tax mix.

International comparison of Australia’s taxes

Page 282

Chart 9.4: Recurrent wealth tax burden OECD-10, taxation revenue as a proportion of GDP, ordered by tax burden, 2003

0.0

0.5

1.0

1.5

Irela

nd

Japa

n

Net

herla

nds

NZ

UK

US

Spa

in

Can

ada

Sw

itzer

land

0.0

0.5

1.0

1.5

Unweighted average

Aus

tral

ia

Per cent of GDP Per cent of GDP

Source: OECD Revenue Statistics, 2005.

9.5 ESTATE, INHERITANCE AND GIFT TAXES

Australia is one of two OECD-10 countries that do not impose any estate, inheritance and gift taxes.

Of the OECD-10, Japan, the Netherlands and the United States rely most heavily on these taxes. Even for these countries, they are not a significant part of their tax base, accounting for around 0.3 per cent of GDP.

New Zealand collected approximately NZ$2 million from its gift tax in 2003, which is less than 0.01 per cent of its GDP.

Chapter 9: Property and transaction taxation

Page 283

Chart 9.5: Estate, gift and inheritance tax burden OECD-10, taxation revenue as a proportion of GDP, ordered by tax burden, 2003

0.0

0.2

0.4

0.6

Can

ada

NZ

Irela

nd

Spa

in

Sw

itzer

land UK

Japa

n

Net

herla

nds

US

0.0

0.2

0.4

0.6

Unweighted average

Aus

tral

ia

Per cent of GDP Per cent of GDP

Source: OECD Revenue Statistics, 2005. In Canada, these taxes are not directly levied, but they are effectively imposed through deemed disposition provisions in income tax legislation.

Table 9.3: Summary of estate, inheritance and gift taxes in the OECD-10 countries Estate/Inheritance tax Gift tax

Australia

Canada(a)

Ireland X X

Japan X X

Netherlands X X

New Zealand X

Spain X X

Switzerland X X

United Kingdom X

United States X X (a) While Canada does not levy any estate, inheritance or gift taxes, they are effectively imposed through deemed disposition

provisions in income tax legislation. Source: Various, see Chapter 1 (1.4.1).

International comparison of Australia’s taxes

Page 284

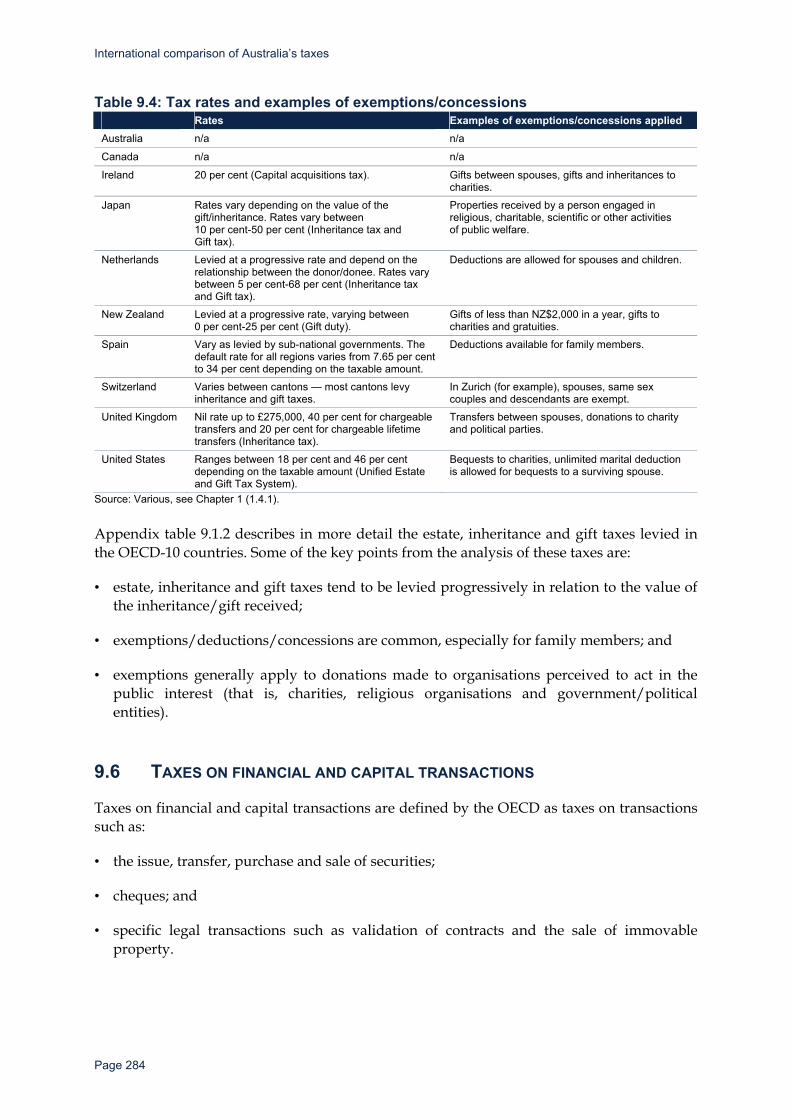

Table 9.4: Tax rates and examples of exemptions/concessions Rates Examples of exemptions/concessions applied Australia n/a n/a

Canada n/a n/a

Ireland 20 per cent (Capital acquisitions tax). Gifts between spouses, gifts and inheritances to charities.

Japan Rates vary depending on the value of the gift/inheritance. Rates vary between 10 per cent-50 per cent (Inheritance tax and Gift tax).

Properties received by a person engaged in religious, charitable, scientific or other activities of public welfare.

Netherlands Levied at a progressive rate and depend on the relationship between the donor/donee. Rates vary between 5 per cent-68 per cent (Inheritance tax and Gift tax).

Deductions are allowed for spouses and children.

New Zealand Levied at a progressive rate, varying between 0 per cent-25 per cent (Gift duty).

Gifts of less than NZ$2,000 in a year, gifts to charities and gratuities.

Spain Vary as levied by sub-national governments. The default rate for all regions varies from 7.65 per cent to 34 per cent depending on the taxable amount.

Deductions available for family members.

Switzerland Varies between cantons — most cantons levy inheritance and gift taxes.

In Zurich (for example), spouses, same sex couples and descendants are exempt.

United Kingdom Nil rate up to £275,000, 40 per cent for chargeable transfers and 20 per cent for chargeable lifetime transfers (Inheritance tax).

Transfers between spouses, donations to charity and political parties.

United States Ranges between 18 per cent and 46 per cent depending on the taxable amount (Unified Estate and Gift Tax System).

Bequests to charities, unlimited marital deduction is allowed for bequests to a surviving spouse.

Source: Various, see Chapter 1 (1.4.1). Appendix table 9.1.2 describes in more detail the estate, inheritance and gift taxes levied in the OECD-10 countries. Some of the key points from the analysis of these taxes are:

• estate, inheritance and gift taxes tend to be levied progressively in relation to the value of the inheritance/gift received;

• exemptions/deductions/concessions are common, especially for family members; and

• exemptions generally apply to donations made to organisations perceived to act in the public interest (that is, charities, religious organisations and government/political entities).

9.6 TAXES ON FINANCIAL AND CAPITAL TRANSACTIONS

Taxes on financial and capital transactions are defined by the OECD as taxes on transactions such as:

• the issue, transfer, purchase and sale of securities;

• cheques; and

• specific legal transactions such as validation of contracts and the sale of immovable property.

Chapter 9: Property and transaction taxation

Page 285

In Australia, examples of such taxes would include stamp duties on residential conveyances, non-residential conveyances, mortgages, leases, shares, rental arrangements and other products.

Australia has the highest reliance on transaction taxes such as stamp duties on conveyances (1.6 per cent of GDP) of the OECD-10 (unweighted average of 0.7 per cent).

Of the other OECD-10 countries, Spain (1.3 per cent) and Ireland (1.2 per cent) also rely relatively heavily on these taxes compared to the other OECD-10 countries.

Again, as noted earlier, there are classification issues when the OECD tax data are disaggregated.

Some sub-national governments in both Canada and the United States impose taxes on the transfer of real estate, but revenues from these taxes are not reported under this sub-category.

• For Canada, revenues from land transfer taxes are reported under the ‘other (non-recurrent) property tax’ category in the OECD’s Revenue Statistics 2005 Edition (4520). Statistics Canada has advised that land transfer taxation revenue totalled C$1.9 billion in 2004 (around 0.1 per cent of GDP).

• For the United States, revenues from real estate transfer taxes are reported under another category in the OECD’s Revenue Statistics 2005 Edition — ‘recurrent taxes on the use of goods or on the permission to perform activities’ (5213). Revenue collections from document and stock transfer taxes for state governments only were US$7.9 billion in 2004 (around 0.1 per cent of GDP).

New Zealand imposes two financial and capital transaction duties — cheque duty and an approved issuer levy (approved issuers are required to pay a levy for the right to issue securities that are subject to a zero rate of non-resident withholding tax). For 2003, New Zealand reported revenue collections of NZ$56 million (less than 0.1 per cent of GDP) under this sub-category.

International comparison of Australia’s taxes

Page 286

Chart 9.6: Transaction tax burden OECD-10, taxation revenue as a proportion of GDP, ordered by tax burden, 2003

0.0

0.6

1.2

1.8C

anad

a

NZ

US

Japa

n

Sw

itzer

land UK

Net

herla

nds

Irela

nd

Spa

in

0.0

0.6

1.2

1.8

Unweighted average

Per cent of GDP Per cent of GDP

Aus

tral

ia

Source: OECD Revenue Statistics, 2005. Note: Revenues from Bank Accounts Debits tax (BAD tax) is included in the total figure for Australia. Under the Intergovernmental Agreement on the Reform of Commonwealth-State Financial Relations, all States and Territories abolished BAD tax by 1 July 2005 (New South Wales abolished BAD tax on 1 January 2002). The most significant component of this category of taxes for Australia is the State and Territory stamp duties on conveyances (taxes on the sale of land and buildings).

• In 2003-04, around 80 per cent of the revenue from taxes on financial and capital transactions was attributable to stamp duties on conveyances for Australia. Revenue collections from stamp duties on conveyances vary with property values and with the level of market activity, so this revenue source can be subject to greater variability than other sources.

• Revenue from stamp duties on conveyances of real property makes up the majority of conveyance duty revenue collections for the Australian States and Territories.

Apart from New Zealand, all other OECD-10 countries levy taxes on the transfer of real estate.

Appendix table 9.1.3 provides some details of these taxes in the OECD-10. Again, comparable information on these types of taxes is not readily available and the information in this table must be treated with caution as it has not been verified with the individual countries.

Chapter 9: Property and transaction taxation

Page 287

Table 9.5: Level of government levying taxes on the transfer of real estate Australia State Canada Provincial and Local Ireland National Japan National and Local (prefectures) Netherlands National New Zealand n/a Spain Local (Autonomous Communities) Switzerland Canton and Local (Communes) United Kingdom National United States State and Local (County)

Source: Various, see Chapter 1 (1.4.1).

Chart 9.7: Top tax rate applied on the transfer of real estate OECD-10, 2005

0

1

2

3

4

5

6

7

8

9

10

NZ

Can

ada

US

Sw

itzer

land

Japa

n

UK

Net

herla

nds

Spai

n

Irela

nd

0

1

2

3

4

5

6

7

8

9

10Per cent Per cent

Aus

tral

ia

Source: Various, see Chapter 1 (1.4.1). Australia’s top rate for stamp duty on conveyances (7 per cent) is the equal second highest of the OECD-10.

• The top conveyance duty rate of 7 per cent is the marginal rate applying to residential conveyances over A$3 million in New South Wales.

In addition to stamp duty on conveyances, the Australian States and Territories also levy a number of other financial transaction taxes, including stamp duties on mortgages, leases, shares and rental arrangements. Nearly all other OECD-10 countries also levy taxes on one or more of these transactions (Appendix table 9.1.4).

The goods and services tax (GST) was intended to replace a majority of these financial and capital transactions taxes in Australia. In 2005, the Australian Government proposed a timetable for the elimination of the remaining State and Territory taxes listed in the Intergovernmental Agreement on the Reform of Commonwealth-State Financial Relations (the agreement which provides for all GST revenue to be paid to the States and Territories).

International comparison of Australia’s taxes

Page 288

• These taxes are stamp duties on mortgages, leases, cheques, shares, rental arrangements and business conveyances.

At the time of writing this report, complete agreement has not been reached between the Australian Government and all the States and Territories on the timetables for abolishing these taxes.

• Nonetheless, some States and Territories intend to abolish a number of these taxes over the next few years.

It is possible that in many OECD countries other general taxes, like VAT or capital gains tax, are applied to these transactions. For example, tax rates on the transfer of real estate in other countries might be quite low as other taxes that apply to the same base are relatively high, or taxes may be calculated on a VAT inclusive price. In addition, the interactions between these taxes could vary significantly from country to country and they have not been fully explored here. As a result, the total tax burden on financial and capital transactions may vary significantly from the revenue collections of financial and capital transaction taxes in OECD countries.

Chapter 9: Property and transaction taxation

Page 289

REFERENCES

Australian Bureau of Statistics, 2005, Taxation Revenue 2003-04 (Reissue), cat. no. 5506.0, ABS, Canberra.

Bird, R M and Slack, E 2004, International Handbook of Land and Property Taxation, Edward Elgar, Cheltenham, United Kingdom.

Brown, P K and Hepworth, M A 2002, A Study of European Land Tax Systems, Lincoln Institute of Land Policy, Cambridge M A, United States of America.

Franzsen, R C D and McCluskey, W J 2005, An Exploratory Overview of Property Taxation in the Commonwealth of Nations, Lincoln Institute of Land Policy, Cambridge MA, United States of America.

Greater Zurich Area, Swiss Tax System, viewed 30 March 2006, www.greaterzuricharea.ch/default_en.asp?pgn=/content/03/03_005en.asp.

International Bureau of Fiscal Documentation.

Location: Switzerland 2002, The Advantages of the Swiss Tax System 2002 Edition, Location: Switzerland, Zurich.

Lymer, A and Oats, L 2005, Taxation: Policy and Practice 12th Edition 2005-06, Fiscal Publications, Birmingham.

Ministry of Finance 2005, An Outline of Japanese Taxes 2005, The Japanese Government, Tokyo.

Ministry of Finance 2005, Taxation in the Netherlands 2005, The Hague.

Ministry of Industry, Tourism and Trade 2005, A guide to business in Spain, Madrid.

National Association of Realtors 2005, Summary of real estate transfer taxes by State, viewed 31 March 2006, www.realtor.org/SG3.nsf/files/TransferTaxRates(8-05).pdf/$FILE/TransferTaxRates(8-05).pdf.

New South Wales Treasury 2005, Interstate Comparison of Taxes 2005-2006, NSW Treasury, Sydney.

Oasis, Stamp duty in Ireland, Irish eGovernment, viewed 31 March 2006, oasis.gov.ie/housing/buying_a_house_or_flat/stamp_duty.html?CONTACTSID=46efb796817bb53985193b99a61daa69.

OECD 2005, Revenue Statistics 1965-2004, OECD, Paris.

PricewaterhouseCoopers Canada 2005, Tax Facts and Figures — for Individuals and Corporations — Canada 2005, PwC, Canada.

International comparison of Australia’s taxes

Page 290

APP

END

IX 9

.1: T

AXE

S O

N IM

MO

VAB

LE P

RO

PER

TY

Cou

ntry

Ta

x R

ate

Bas

e Ex

empt

ions

Le

vel o

f go

vern

men

t O

ther

Aus

tralia

La

nd ta

x R

ates

are

pr

ogre

ssiv

e an

d va

ry a

cros

s ju

risdi

ctio

ns.

Land

— u

nim

prov

ed v

alue

. A

prin

cipa

l pla

ce o

f res

iden

ce is

gen

eral

ly

exem

pt, a

s is

land

use

d fo

r prim

ary

prod

uctio

n.

Land

ow

ned

by re

ligio

us b

odie

s an

d sc

hool

s.

Sta

te

Gen

eral

ly, l

iabi

lity

rest

s pr

imar

ily w

ith th

e ow

ner a

t a

parti

cula

r poi

nt in

tim

e.

R

ates

V

ary

acro

ss

juris

dict

ions

. V

arie

s ac

ross

juris

dict

ions

— la

nd

or la

nd a

nd im

prov

emen

ts.

Var

y ac

ross

juris

dict

ions

— c

omm

on

exem

ptio

ns in

clud

e pu

blic

ly o

wne

d la

nd,

publ

ic h

ospi

tals

, lib

rarie

s, c

emet

erie

s,

char

ities

, chu

rch

land

s, u

nive

rsiti

es, s

choo

ls

and

fore

ign

emba

ssie

s.

Loca

l

Can

ada

Pro

perty

tax

Rat

es v

ary

by c

lass

of

pro

perty

and

fro

m m

unic

ipal

ity

to m

unic

ipal

ity.

Land

and

impr

ovem

ents

. E

xem

ptio

ns in

clud

e ch

urch

es, c

emet

erie

s,

Indi

an la

nds,

pub

lic h

ospi

tals

, cha

ritab

le

inst

itutio

ns a

nd e

duca

tiona

l ins

titut

ions

.

Loca

l

Irela

nd

Rat

es

Fixe

d ev

ery

year

by

loca

l aut

horit

ies

as a

mul

tiple

of t

he

rate

able

val

ue o

f th

e pr

oper

ty.

Land

and

impr

ovem

ents

— ta

xabl

e va

lue

is b

ased

on

annu

al re

ntal

va

lue

of th

e ra

teab

le p

rope

rty.

Dom

estic

and

agr

icul

tura

l pro

perty

is

outs

ide

the

scop

e of

the

tax.

C

omm

on e

xem

ptio

ns in

clud

e pr

oper

ty u

sed

excl

usiv

ely

for t

he p

urpo

se o

f pub

lic re

ligio

us

wor

ship

, art

galle

ries,

mus

eum

s, a

nd

libra

ries,

pro

perty

use

d fo

r edu

catio

nal

purp

oses

, bur

ial g

roun

ds o

r cre

mat

oriu

ms.

Loca

l A

loca

l tax

on

the

occu

patio

n of

imm

ovab

le

prop

erty

for n

on-r

esid

entia

l is

pay

able

by

the

occu

pier

.

Japa

n P

rope

rty ta

x Th

e st

anda

rd ra

te

is 1

.4 p

er c

ent,

max

imum

rate

is

2.1

per

cen

t.

Land

, bui

ldin

gs a

nd d

epre

ciab

le

busi

ness

ass

ets.

Th

e ta

x ba

se fo

r lan

d an

d bu

ildin

gs

is th

eir v

alue

ass

esse

d by

m

unic

ipal

ities

, bas

ed o

n m

arke

t pr

ices

.

Sta

ndar

d ex

empt

ions

are

ava

ilabl

e fo

r lan

d (o

f val

ue u

p to

¥30

0,00

0) a

nd h

ousi

ng

(val

ue u

p to

¥20

0,00

0).

Pro

perty

use

d as

pub

lic ro

ads

or c

emet

erie

s,

or fo

r edu

catio

nal,

relig

ious

, or s

ocia

l wel

fare

is

exe

mpt

.

Loca

l

C

ity p

lann

ing

tax

Max

imum

of

0.3

per c

ent.

Impo

sed

on th

e ow

ners

of l

and

and

build

ings

loca

ted

with

in a

n ur

ban

prom

otio

n ar

ea. A

ppra

ised

val

ue

for p

rope

rty ta

xes

is u

sed.

Lo

cal

May

be

impo

sed

by c

ities

, to

wns

and

vill

ages

un

derta

king

pro

ject

s un

der

the

City

Pla

nnin

g La

w.

La

nd d

evel

opm

ent

tax

At t

he d

iscr

etio

n of

lo

cal a

utho

ritie

s.

Impo

sed

on d

evel

oper

s of

land

and

is

bas

ed o

n th

e de

velo

ped

area

.

Loca

l

Chapter 9: Property and transaction taxation

Page 291

App

endi

x 9.

1: T

axes

on

imm

ovab

le p

rope

rty

(con

tinue

d)

Cou

ntry

Ta

x R

ate

Bas

e Ex

empt

ions

Le

vel o

f go

vern

men

t O

ther

Net

herla

nds

Imm

ovab

le

prop

erty

taxe

s R

ate

diffe

rs fo

r ea

ch m

unic

ipal

ity.

Diff

eren

t rat

es m

ay

appl

y fo

r co

mm

erci

al p

rope

rty

and

priv

ate

prop

erty

.

Land

and

impr

ovem

ents

. E

xem

ptio

ns in

clud

e na

tura

l site

s, p

ublic

ro

ads,

pub

lic w

ater

way

s, p

rope

rty m

ainl

y us

ed fo

r pub

lic w

orsh

ip, f

orei

gn e

mba

ssie

s an

d co

nsul

ates

, pub

lic g

arde

ns, p

ublic

pa

rks,

cem

eter

ies,

and

cre

mat

oriu

ms.

Loca

l Th

e ta

x co

nsis

ts o

f:

(1)

a pa

rt le

vied

on

owne

rs

of im

mov

able

pro

perty

; an

d (2

) a

part

levi

ed o

n th

e us

ers

of im

mov

able

pr

oper

ty.

New

Zea

land

R

ates

V

arie

s de

pend

ing

on th

e ty

pe o

f rat

e im

pose

d.

Var

ies

— th

ere

are

four

sys

tem

s of

gen

eral

ratin

g. T

hey

incl

ude

by

capi

tal (

land

and

impr

ovem

ents

) va

lue,

by

unim

prov

ed la

nd v

alue

, by

the

annu

al re

ntal

val

ue o

f the

pr

oper

ty a

nd b

y th

e ar

ea s

yste

m.

Exe

mpt

ions

incl

ude

prop

erty

use

d fo

r re

ligio

us, c

harit

able

and

edu

catio

nal

purp

oses

; her

itage

pro

perty

; com

mun

ity

land

; and

Mao

ri an

d bu

rial g

roun

ds.

Loca

l

Spa

in

Taxe

s on

real

es

tate

G

ener

al ta

x ra

tes

are

0.4

per c

ent f

or

urba

n pr

oper

ty a

nd

0.3

per c

ent f

or ru

ral

prop

erty

, but

hig

her

rate

s m

ay a

pply

.

Land

and

bui

ldin

gs.

Exe

mpt

ions

incl

ude

prop

erty

ow

ned

by th

e ch

urch

and

Red

Cro

ss; d

iplo

mat

ic p

rem

ises

; sc

hool

s.

Loca

l Th

e ta

xabl

e ba

se is

the

cada

stra

l val

ue. T

he

cada

stra

l val

ue is

upd

ated

ev

ery

eigh

t yea

rs w

ith

refe

renc

e to

the

mar

ket

valu

e of

the

prop

erty

, in

clud

ing

the

valu

e of

land

an

d bu

ildin

gs.

Sw

itzer

land

La

nd ta

x R

ates

var

y be

twee

n 0.

3 pe

r cen

t and

4

per c

ent.

The

appl

icat

ion

of th

e ta

x ca

n va

ry

acro

ss ju

risdi

ctio

ns. N

on-fa

rm

prop

ertie

s ar

e us

ually

ass

esse

d w

ith

resp

ect t

o th

eir m

arke

t val

ue,

whe

reas

farm

and

fore

stry

pro

perti

es

mea

sure

thei

r ear

ning

pow

er.

C

anto

n/Lo

cal

Prim

arily

a c

omm

unal

(lo

cal)

tax.

Uni

ted

Kin

gdom

B

usin

ess

rate

s Fo

r the

yea

r end

ing

31 M

arch

200

6,

the

rate

is

42.2

per

cen

t in

Eng

land

(sim

ilar

rate

s ap

ply

in

Sco

tland

and

W

ales

).

Land

and

impr

ovem

ents

(c

omm

erci

al o

nly)

. E

xem

ptio

ns in

clud

e ag

ricul

tura

l lan

d an

d bu

ildin

gs; p

lace

s of

pub

lic w

orsh

ip;

prop

ertie

s oc

cupi

ed b

y ch

arita

ble

and

spor

ting

orga

nisa

tions

; and

dip

lom

atic

pr

emis

es.

Nat

iona

l Th

e ta

x is

pay

able

by

the

occu

pier

. R

atea

ble

valu

es, w

hich

are

as

sess

ed e

very

five

yea

rs,

are

curr

ently

bas

ed o

n m

arke

t ren

ts o

n 1

Apr

il 20

03.

International comparison of Australia’s taxes

Page 292

App

endi

x 9.

1: T

axes

on

imm

ovab

le p

rope

rty

(con

tinue

d)

Cou

ntry

Ta

x R

ate

Bas

e Ex

empt

ions

Le

vel o

f go

vern

men

t O

ther

Uni

ted

Kin

gdom

(c

ontin

ued)

C

ounc

il ta

x R

ates

are

set

by

each

loca

l go

vern

men

t.

Bui

ldin

gs (r

esid

entia

l onl

y).

Exe

mpt

ions

incl

ude

prop

ertie

s th

at a

re

owne

d by

cha

rity,

kep

t for

occ

upat

ion

by

min

iste

rs o

f rel

igio

n, o

ccup

ied

by s

tude

nts;

an

d oc

cupi

ed o

r man

aged

by

an e

duca

tiona

l es

tabl

ishm

ent o

r cha

ritab

le b

ody.

Loca

l Th

e ta

x is

pay

able

by

the

occu

pier

.

Uni

ted

Sta

tes

Rea

l est

ate

ta

xes

Var

ies

acro

ss

juris

dict

ions

. M

etho

ds fo

r ass

essi

ng th

e va

lue

of a

pro

perty

var

y de

pend

ing

on

the

juris

dict

ion.

Lo

cal

Sou

rce:

Var

ious

, see

Cha

pter

1 (1

.4.1

).

Chapter 9: Property and transaction taxation

Page 293

APP

END

IX 9

.2: E

STA

TE, I

NH

ERIT

AN

CE

AN

D G

IFT

TAXE

S

Cou

ntry

Ta

x R

ate

Bas

e Ex

empt

ion

Leve

l of

gove

rnm

ent

Add

ition

al in

form

atio

n

Aus

tralia

A

ustra

lia d

oes

not i

mpo

se e

stat

e, in

herit

ance

or g

ift ta

xes.

Can

ada

No

Can

adia

n ju

risdi

ctio

n im

pose

s a

gift

or in

herit

ance

tax

per s

e. T

hey

are

effe

ctiv

ely

impo

sed

thro

ugh

deem

ed d

ispo

sitio

n pr

ovis

ions

in

inco

me

tax

legi

slat

ion.

D

eem

ed

disp

ositi

on

thro

ugh

a gi

ft

As

per i

ncom

e ta

x ra

te.

A p

erso

n w

ho g

ifts

prop

erty

to

anot

her i

s de

emed

to h

ave

rece

ived

pr

ocee

ds e

qual

to it

s fa

ir m

arke

t va

lue.

The

dee

med

pro

ceed

s m

ay

caus

e th

e do

nor t

o re

cogn

ise

inco

me,

re

capt

ured

dep

reci

atio

n or

cap

ital

gain

s.

Dep

ends

on

the

prop

erty

invo

lved

. Als

o, a

sp

ouse

may

tran

sfer

pro

perty

to th

e ot

her

spou

se w

ithou

t attr

actin

g lia

bilit

y.

D

eem

ed

disp

ositi

on

thro

ugh

deat

h

As

per i

ncom

e ta

x ra

te.

Sim

ilar t

o ab

ove.

The

dec

ease

d is

de

emed

to h

ave

disp

osed

of a

ll pr

oper

ty o

wne

d im

med

iate

ly b

efor

e th

e tim

e of

dea

th. N

ote

that

dee

med

ca

pita

l gai

n is

onl

y th

e in

crea

se in

va

lue

of a

sset

s, n

ot th

e to

tal v

alue

.

A s

pous

e m

ay tr

ansf

er p

rope

rty to

the

othe

r sp

ouse

with

out a

ttrac

ting

liabi

lity.

Irela

nd

Cap

ital

acqu

isiti

ons

tax

A s

ingl

e ra

te o

f 20

per

cen

t, w

hich

ap

plie

s to

any

ac

cum

ulat

ed g

ifts

and

inhe

ritan

ces

over

the

rele

vant

cl

ass

thre

shol

d.

Levi

ed o

n th

e re

ceip

t of g

ifts,

or o

n th

e su

cces

sor o

f pro

perty

pas

sing

on

dea

th. T

he ta

xabl

e va

lue

is th

e m

arke

t val

ue o

n th

e da

te o

f the

gift

or

suc

cess

ion.

A n

umbe

r of e

xem

ptio

ns in

clud

ing,

but

not

lim

ited

to, g

ifts

pass

ing

betw

een

spou

ses,

gi

fts a

nd in

herit

ance

s to

cha

rity;

sm

all g

ifts

up to

€1,

270

per y

ear,

gifts

and

inhe

ritan

ces

of li

fe in

sura

nce

polic

ies.

Nat

iona

l

International comparison of Australia’s taxes

Page 294

App

endi

x 9.

2: E

stat

e, in

herit

ance

and

gift

taxe

s (c

ontin

ued)

C

ount

ry

Tax

Rat

e B

ase

Exem

ptio

n Le

vel o

f go

vern

men

t A

dditi

onal

info

rmat

ion

Japa

n In

herit

ance

tax

Bet

wee

n 10

per

cen

t an

d 50

per

cen

t de

pend

ing

on th

e si

ze o

f the

in

herit

ance

.

Impo

sed

on th

e to

tal v

alue

of a

ll pr

oper

ties

acqu

ired

thro

ugh

an

inhe

ritan

ce o

r a b

eque

st (l

ess

liabi

litie

s an

d fu

nera

l exp

ense

s).

Val

uatio

n of

pro

perti

es is

bas

ed o

n m

arke

t pric

e.

Exe

mpt

ions

incl

ude,

but

are

not

lim

ited

to,

life

and

pers

onal

acc

iden

t ins

uran

ce

proc

eeds

; ret

irem

ent a

nd s

imila

r ben

efits

; an

d pr

oper

ties

rece

ived

by

a pe

rson

en

gage

d in

relig

ious

, cha

ritab

le, s

cien

tific

or

othe

r act

iviti

es fo

r pub

lic w

elfa

re.

Nat

iona

l G

ifts

with

in th

ree

year

s be

fore

dea

th a

re in

clud

ed in

th

e ta

xabl

e ba

se, b

ut a

ny

gift

tax

paya

ble

is c

redi

ted

agai

nst t

he in

herit

ance

tax.

G

ift ta

x B

etw

een

10 p

er c

ent

and

50 p

er c

ent

depe

ndin

g on

the

size

of t

he g

ift.

Impo

sed

on p

rope

rty g

iven

as

a gi

ft.

Exe

mpt

ions

incl

ude,

but

are

not

lim

ited

to,

gifts

from

a c

orpo

ratio

n; s

ums

rece

ived

by

depe

ndan

ts fo

r liv

ing

and

educ

atio

nal

expe

nses

; pro

perti

es re

ceiv

ed b

y a

pers

on

enga

ged

in re

ligio

us, c

harit

able

, sci

entif

ic o

r ot

her a

ctiv

ities

for p

ublic

wel

fare

; and

po

litic

al c

ontri

butio

ns.

Nat

iona

l

Net

herla

nds

Suc

cess

ion

duty

Le

vied

at a

pr

ogre

ssiv

e ra

te

(bet

wee

n 5

per c

ent

and

68 p

er c

ent)

depe

ndin

g on

the

prox

imity

of t

he

rela

tions

hip

betw

een

the

dece

ased

/don

or

and

the

valu

e of

the

inhe

ritan

ce.

Impo

sed

if pr

oper

ty is

acq

uire

d by

in

herit

ance

or b

y gi

ft an

d th

e de

ceas

ed/d

onor

was

/is a

resi

dent

of

the

Net

herla

nds.

Ded

uctio

ns a

re a

llow

ed fo

r spo

uses

and

ch

ildre

n. G

ifts

to c

erta

in m

useu

ms.

N

atio

nal

Levi

ed o

n th

e be

nefic

iary

/don

ee.

New

Zea

land

G

ift d

uty

Mar

gina

l rat

es ra

nge

from

0 p

er c

ent t

o 25

per

cen

t de

pend

ing

on th

e va

lue

of th

e gi

ft.

Pay

able

on

gifts

of a

ll pr

oper

ty in

N

ew Z

eala

nd a

nd g

ifts

of p

rope

rty

situ

ated

out

side

New

Zea

land

if th

e do

nor i

s do

mic

iled

in N

ew Z

eala

nd.

Exe

mpt

ions

incl

ude,

but

are

not

lim

ited

to

gifts

of l

ess

than

NZ$

2,00

0 in

agg

rega

te fo

r on

e ca

lend

ar y

ear;

gifts

to m

aint

ain

educ

atio

n of

rela

tives

; gift

s to

cha

ritie

s an

d gr

atui

ties.

Nat

iona

l

Spa

in

Inhe

ritan

ce a

nd

gift

tax

Var

ies

depe

ndin

g on

re

gion

. The

def

ault

rate

for a

ll re

gion

s va

ries

from

7.

65 p

er c

ent t

o 34

per

cen

t de

pend

ing

on th

e ta

xabl

e am

ount

.

Tran

sfer

red

asse

ts a

re v

alue

d at

th

eir f

air m

arke

t val

ue.

Ded

uctio

ns a

vaila

ble

for f

amily

mem

bers

. A

uton

omou

s co

mm

uniti

es

A re

cipi

ent w

ho is

a

resi

dent

of S

pain

is li

able

to

this

tax

with

rega

rd to

pr

oper

ty in

Spa

in o

r abr

oad,

ac

quire

d th

roug

h a

grat

uito

us tr

ansf

er.

Non

-res

iden

ts a

re s

ubje

ct

to th

is ta

x w

ith re

gard

to

any

asse

ts lo

cate

d in

S

pain

.

Chapter 9: Property and transaction taxation

Page 295

App

endi

x 9.

2: E

stat

e, in

herit

ance

and

gift

taxe

s (c

ontin

ued)

C

ount

ry

Tax

Rat

e B

ase

Exem

ptio

n Le

vel o

f go

vern

men

t A

dditi

onal

info

rmat

ion

Sw

itzer

land

In

herit

ance

and

gi

ft ta

xes

The

effe

ctiv

e ta

x bu

rden

var

ies

betw

een

cant

ons,

bu

t usu

ally

is b

ased

on

the

degr

ee o

f re

latio

nshi

p an

d/or

th

e re

ceiv

ed

amou

nt. R

ates

ra

nge

from

10

per

cen

t to

50 p

er c

ent.

For t

ax p

urpo

ses,

ther

e is

gen

eral

ly

no d

istin

ctio

n be

twee

n in

herit

ance

s an

d gi

fts. T

he ri

ght t

o le

vy in

herit

ance

an

d gi

ft ta

xes

on m

ovab

le p

rope

rty is

le

ft to

the

cant

on in

whi

ch th

e de

scen

dant

had

thei

r las

t res

iden

ce,

and

to th

e ca

nton

in w

hich

the

dono

r ha

s th

eir r

esid

ence

, res

pect

ivel

y.

For e

xam

ple,

in th

e ca

nton

of Z

uric

h,

spou

ses,

sam

e-se

x co

uple

s an

d de

scen

dant

s ar

e ex

empt

.

Can

tons

M

ost c

anto

ns le

vy

inhe

ritan

ce a

nd g

ift ta

xes.

Uni

ted

Kin

gdom

In

herit

ance

tax

A n

il ra

te a

pplie

s up

to

£27

5,00

0. A

bove

th

is a

mou

nt, t

he ra

te

is 4

0 pe

r cen

t for

ch

arge

able

tran

sfer

s an

d 20

per

cen

t for

ch

arge

able

life

time

trans

fers

.

Levi

ed o

n th

e tra

nsfe

r of a

ll pr

oper

ty

pass

ing

on d

eath

(cha

rgea

ble

trans

fers

).

Exe

mpt

ions

incl

ude,

but

are

not

lim

ited

to,

trans

fers

bet

wee

n sp

ouse

s, re

gula

r gift

s,

gifts

up

to £

3,00

0 in

a ta

x ye

ar, a

nd

dona

tions

to c

harit

y an

d po

litic

al p

artie

s.

Nat

iona

l It

is a

lso

levi

ed o

n ce

rtain

gi

fts m

ade

with

in th

e se

ven

year

s be

fore

the

deat

h of

a p

erso

n. It

is

levi

ed o

n w

orld

wid

e pr

oper

ty o

f dom

icile

d in

divi

dual

s an

d tru

sts.

N

on-d

omic

iled

indi

vidu

als

are

liabl

e to

tax

only

on

asse

ts s

ituat

ed in

the

Uni

ted

Kin

gdom

.

Uni

ted

Sta

tes

Uni

fied

Est

ate

and

Gift

Tax

S

yste

m

Ran

ges

betw

een

18 p

er c

ent a

nd

46 p

er c

ent

depe

ndin

g on

the

taxa

ble

amou

nt.

Levi

ed o

n th

e ac

cum

ulat

ive

tota

l va

lue

of a

ll tra

nsfe

rs m

ade

by a

n in

divi

dual

dur

ing

life

and

at th

e tim

e of

dea

th. A

pplie

s to

all

Uni

ted

Sta

tes

citiz

ens

and

fore

ign

natio

nals

who

are

U

nite

d S

tate

s re

side

nts

at th

e tim

e of

de

ath.

App

lies

also

to n

on-r

esid

ents

on

pro

perty

that

is d

eem

ed to

hav

e a

Uni

ted

Sta

ted

loca

tion.

Pro

perty

is

valu

ed a

t the

fair

mar

ket v

alue

at

time

of d

eath

.

The

valu

e of

the

gros

s es

tate

is re

duce

d by

: (1

) ex

pens

es a

nd lo

sses

; (2

) m

ortg

ages

and

inde

bted

ness

; (3

) ce

rtain

taxe

s im

pose

d by

Uni

ted

Sta

tes

stat

es o

r for

eign

cou

ntrie

s on

tran

sfer

s m

ade

for p

ublic

, cha

ritab

le o

r rel

igio

us

purp

oses

; and

(4

) be

ques

ts to

cha

ritie

s. A

lso,

an

unlim

ited

mar

ital d

educ

tion

is a

llow

ed fo

r be

ques

ts to

a s

urvi

ving

spo

use.

An

excl

usio

n ap

plie

s to

gift

s up

to th

e va

lue

of U

S$1

2,00

0 pe

r don

ee in

one

yea

r.

A

lso

impo

ses

a ge

nera

tion

skip

ping

tran

sfer

tax

(GS

TT) o

n tra

nsfe

rs m

ade

to b

enef

icia

ries

who

are

m

ore

than

one

gen

erat

ion

youn

ger t

han

the

dono

r. N

ote:

the

esta

te ta

x an

d G

STT

are

sch

edul

ed to

be

com

plet

ely

phas

ed o

ut

by 2

010.

Sou

rce:

Var

ious

, see

Cha

pter

1 (1

.4.1

).

International comparison of Australia’s taxes

Page 296

APP

END

IX 9

.3: T

AXE

S O

N T

HE

TRA

NSF

ER O

F R

EAL

ESTA

TE

Cou

ntry

To

p ra

te(a

) Pr

ogre

ssiv

e ra

te s

truc

ture

Ex

ampl

es o

f exe

mpt

ions

(b)

Leve

l of

gove

rnm

ent

Add

ition

al in

form

atio

n

Aus

tralia

7

per c

ent

Yes

Firs

t hom

e ow

ners

can

rece

ive

disc

ount

s/ex

empt

ions

for l

ower

val

ued

prop

ertie

s.

Sta

te

Rat

es v

ary

acro

ss S

tate

s an

d Te

rrito

ries,

m

axim

um ra

tes

vary

from

3.7

5 pe

r cen

t to

7 pe

r cen

t. Th

e m

axim

um ra

te o

f 7 p

er c

ent i

s fo

r tra

nsfe

rs o

ver A

$3 m

illio

n in

N

ew S

outh

Wal

es.

Can

ada

2 pe

r cen

t Ye

s (g

ener

ally

) In

Ont

ario

, for

exa

mpl

e, a

refu

nd is

ava

ilabl

e fo

r firs

t tim

e pu

rcha

sers

of a

new

ly c

onst

ruct

ed

hom

e.

Pro

vinc

ial/L

ocal

R

ates

var

y ac

ross

pro

vinc

es (s

ix p

rovi

nces

im

pose

land

tran

sfer

taxe

s). A

few

pro

vinc

es

levy

regi

stra

tion

fees

rath

er th

an tr

ansf

er

taxe

s.

Irela

nd

9 pe

r cen

t Ye

s Fi

rst h

ome

owne

rs a

re e

xem

pt fo

r low

to

mid

-cos

t hou

ses.

N

atio

nal

Rat

es v

ary

for d

iffer

ent d

efin

ition

s of

pu

rcha

sers

. Th

e m

axim

um ra

te o

f 9 p

er c

ent i

s fo

r tra

nsfe

rs o

ver €

635,

000

for a

ll pu

rcha

sers

.

Japa

n 4

per c

ent

Nat

iona

l: va

rious

flat

am

ount

s de

pend

ing

on v

alue

. P

refe

ctur

e: fl

at 4

per

cen

t.

Exe

mpt

ions

bel

ow th

resh

old

leve

ls.

Nat

iona

l/Pre

fect

ure

Net

herla

nds

6 pe

r cen

t N

o E

xem

ptio

ns fo

r acq

uisi

tions

by

child

ren,

ac

quis

ition

s by

pub

lic o

rgan

isat

ions

, agr

icul

tura

l la

nd a

nd b

uild

ings

.

Nat

iona

l

New

Zea

land

-

- -

- -

Spa

in

7 pe

r cen

t N

o Fi

rst s

ale

of p

rope

rty (V

AT

is a

pplie

d in

stea

d).

Aut

onom

ous

com

mun

ities

Sw

itzer

land

3.

3 pe

r cen

t

C

anto

n/Lo

cal

A fe

w c

anto

ns le

vy tr

ansf

er fe

es ra

ther

than

tra

nsfe

r tax

es.

Uni

ted

Kin

gdom

4

per c

ent

Yes

Exe

mpt

ion

for n

on-r

esid

entia

l lan

d in

di

sadv

anta

ged

area

s.

Nat

iona

l H

ighe

r tax

free

thre

shol

ds fo

r res

iden

tial

prop

erty

in d

isad

vant

aged

are

as.

Uni

ted

Sta

tes

2 pe

r cen

t M

ixtu

re o

f pro

gres

sive

and

flat

st

ruct

ure.

Sta

te/L

ocal

(C

ount

y)

(a)

Top

rate

acr

oss

all j

uris

dict

ions

levy

ing

such

a ta

x.

(b)

Doe

s no

t cov

er a

ll ex

empt

ions

/con

cess

ions

. S

ourc

e: V

ario

us, s

ee C

hapt

er 1

(1.4

.1).

Chapter 9: Property and transaction taxation

Page 297

APPENDIX 9.4: EXAMPLES OF OTHER FINANCIAL AND CAPITAL TRANSACTION TAXES

Country Other types of transactions taxed Australia Mortgages, leases, share transfers, rental arrangements

Canada No examples could be found

Ireland Mortgages, leases, share transfers

Japan Transfer of mining rights, intangible property rights, leases, shares, debentures, promissory notes

Netherlands Share transfers

New Zealand Cheques

Spain Deeds, leases, moveable assets

Switzerland Shares and other financial instruments

United Kingdom Other main stamp duties beside stamp duty on property transfer, are on leases and share transactions

United States Some States levy taxes on mortgages, car hire Source: Various, see Chapter 1 (1.4.1).