Embed Size (px)

Citation preview

TOLUCA PLAZA

Offering Memorandum

10311 Riverside Drive, Toluca Lake, CA 91602

TOLUCA PLAZA

Toluca Lake, CA

ACT ID Y0120006

N O N - E N D O R S E M E N T A N D D I S C L A I M E R N O T I C E

Non-EndorsementsMarcus & Millichap is not affiliated with, sponsored by, or endorsed by any commercial tenant or lessee identified in

this marketing package. The presence of any corporation's logo or name is not intended to indicate or imply affiliation

with, or sponsorship or endorsement by, said corporation of Marcus & Millichap, its affiliates or subsidiaries, or any

agent, product, service, or commercial listing of Marcus & Millichap, and is solely included for the purpose of

providing tenant lessee information about this listing to prospective customers.

ALL PROPERTY SHOWINGS ARE BY APPOINTMENT ONLY.

PLEASE CONSULT YOUR MARCUS & MILLICHAP AGENT FOR MORE DETAILS.

DisclaimerTHIS IS A BROKER PRICE OPINION OR COMPARATIVE MARKET ANALYSIS OF VALUE AND SHOULD NOT BE

CONSIDERED AN APPRAISAL. This information has been secured from sources we believe to be reliable, but we

make no representations or warranties, express or implied, as to the accuracy of the information. References to

square footage or age are approximate. Buyer must verify the information and bears all risk for any inaccuracies.

Marcus & Millichap is a service mark of Marcus & Millichap Real Estate Investment Services, Inc. © 2016 Marcus &

Millichap. All rights reserved.

P R E S E N T E D B Y

Jeff Louks

Executive Vice President Investments

Senior Director - National Multi Housing

Group

Encino Office

Tel: (818) 212-2780

Fax: (818) 212-2710

License: CA 00908473

Brett Sanson

Vice President Investments

Director - National Multi Housing Group

Encino Office

Tel: (818) 212-2785

Fax: (818) 212-2710

License: CA 01387480

Gayle Factor

First Vice President Investments

Director - National Multi Housing Group

Encino Office

Tel: (818) 212-2756

Fax: (818) 212-2710

License: CA 01066258

TABLE OF CONTENTS

SECTION

FINANCIAL ANALYSIS 01Rent Roll Summary

Rent Roll Detail

Operating Statement

Notes

Pricing Detail

INVESTMENT OVERVIEW 02Property Overview

Regional Map

Local Map

Aerial Photo

MARKET COMPARABLES 03Comparables

Rent Comparables

MARKET OVERVIEW 04

Market Analysis

Demographic Analysis

TOLUCA PLAZA

TOLUCA PLAZA

5

FINANCIAL

ANALYSIS

FINANCIAL ANALYSIS

TOLUCA PLAZA

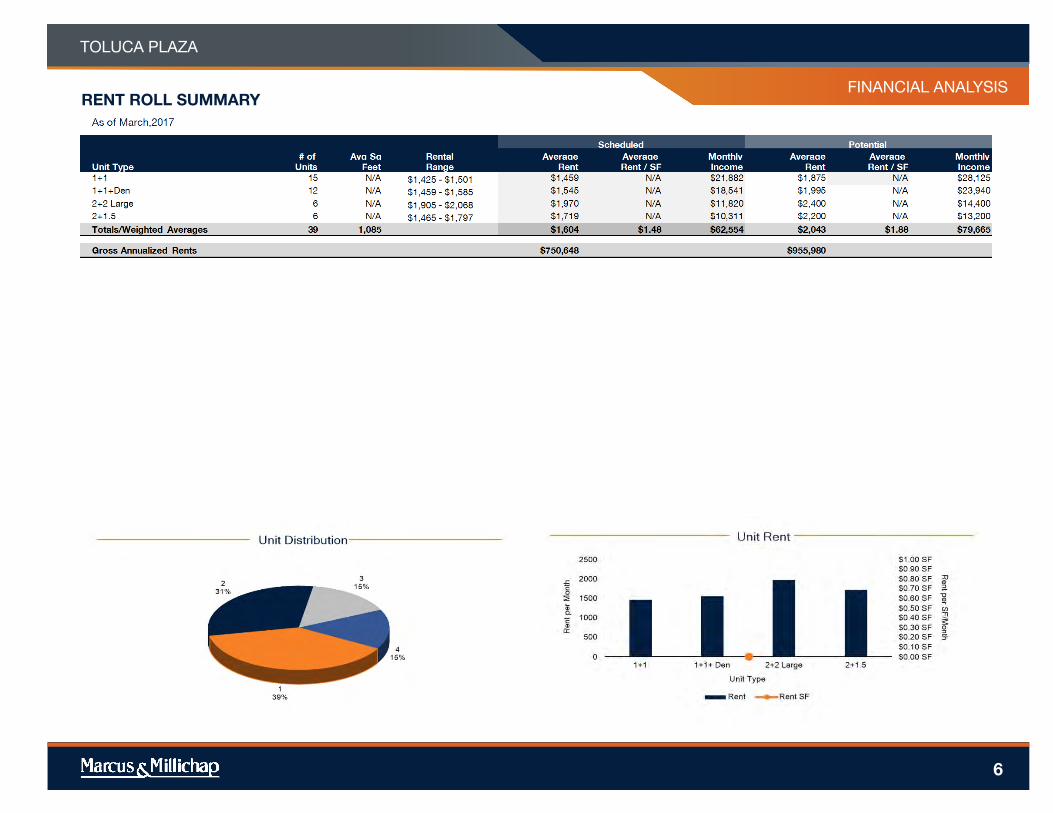

RENT ROLL SUMMARY

6

FINANCIAL ANALYSIS

TOLUCA PLAZA

7

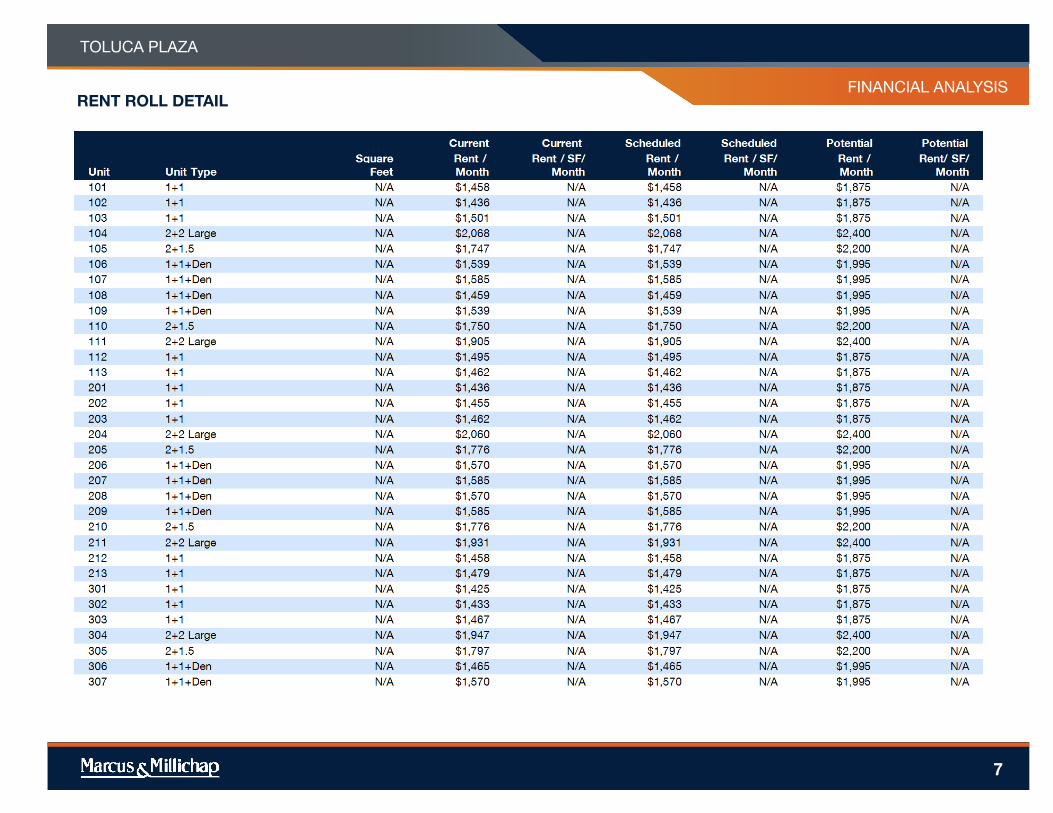

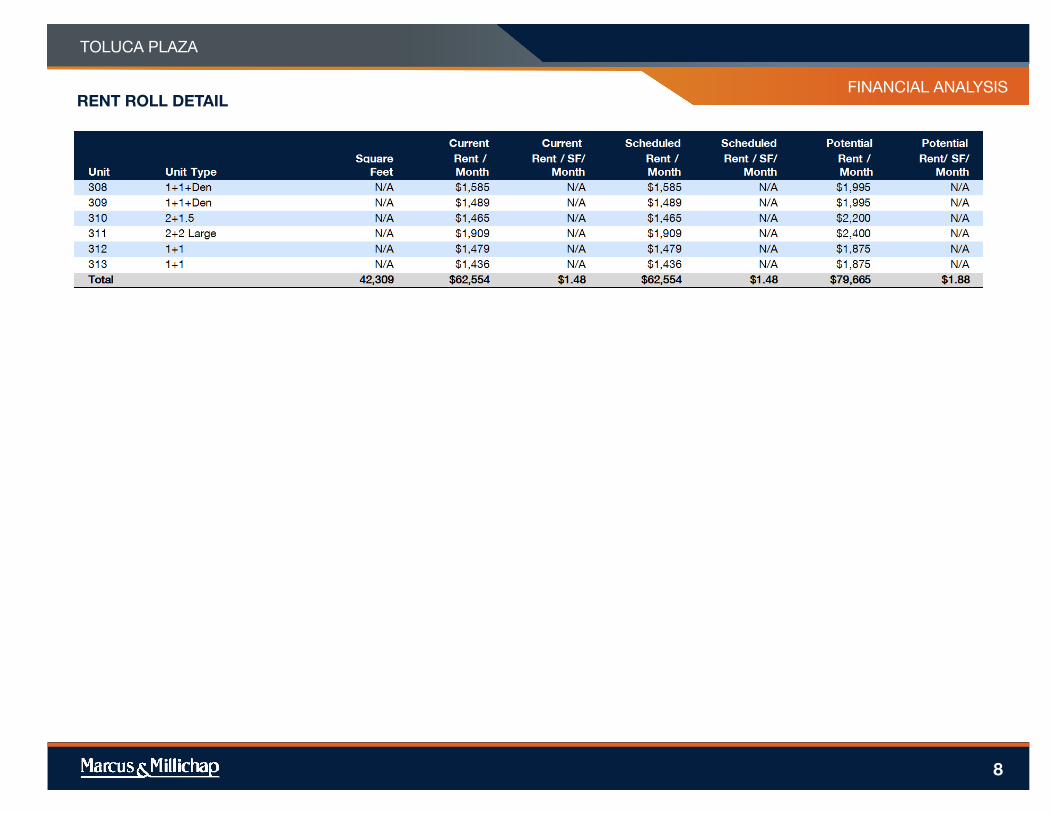

RENT ROLL DETAIL

FINANCIAL ANALYSIS

TOLUCA PLAZA

8

RENT ROLL DETAIL

FINANCIAL ANALYSIS

TOLUCA PLAZA

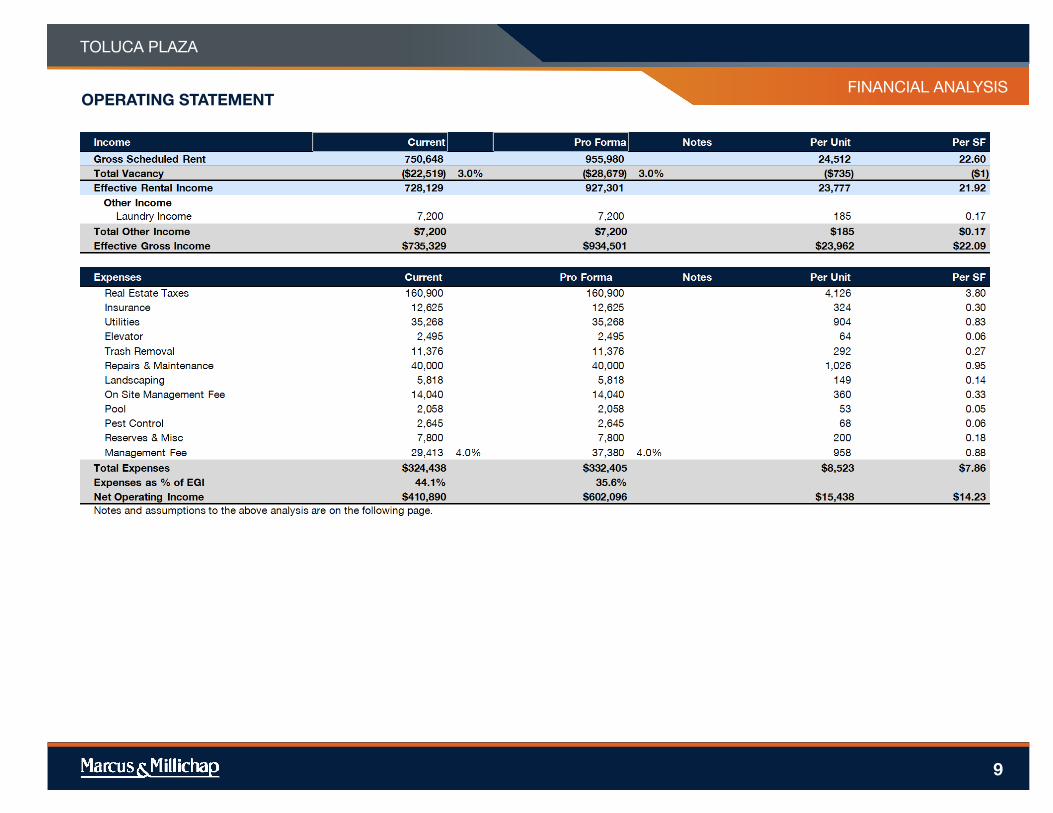

OPERATING STATEMENT

9

FINANCIAL ANALYSIS

TOLUCA PLAZA

NOTES

10

Taxes: Based off a rate of 1.191849%

Insurance: Based off 2016 P&L

Utilities: Based off 2016 P&L

Elevator: Based off 2016 P&L

Trash: Based off 2016 P&L

Landscaping: Based off 2016 P&L

On Site Mgmt: Based off industry standard estimates

Pool: Based off 2016 P&L

Pest Control: Based off 2016 P&L

Reserves & Misc.: Based off 2016 P&L

Maintenance & Repairs: Based off industry standard estimates

Management fee: Based off industry standard estimates

FINANCIAL ANALYSIS

TOLUCA PLAZA

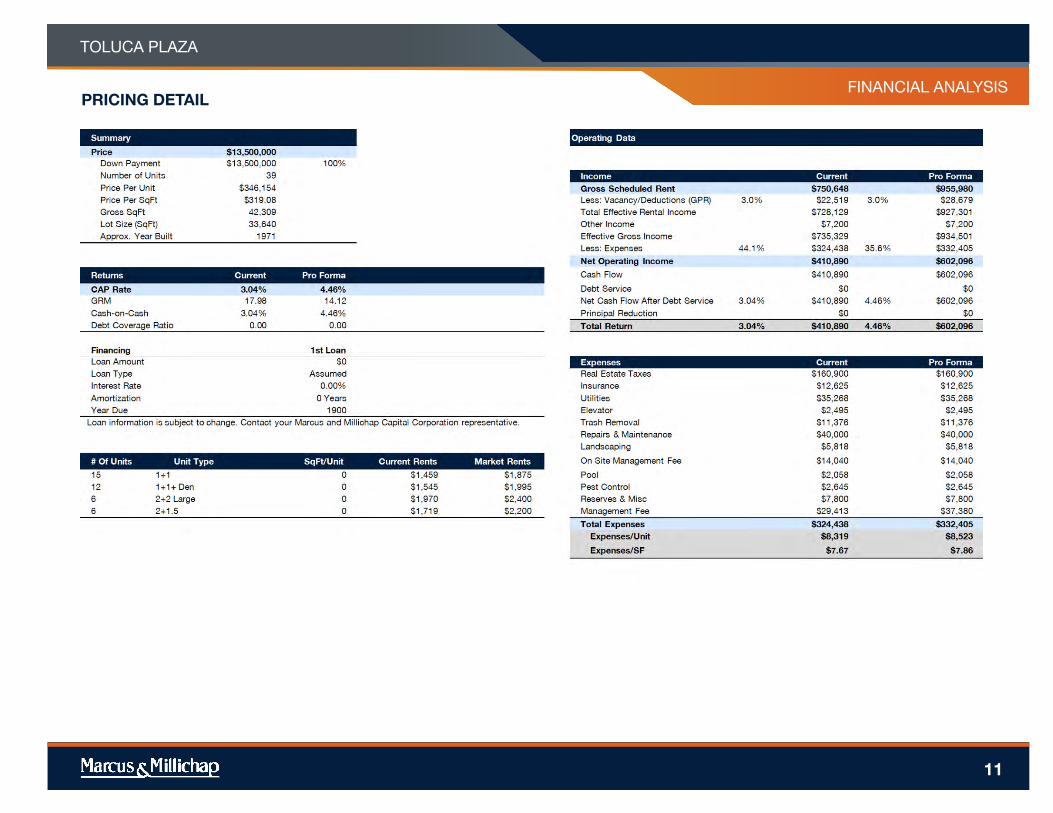

PRICING DETAIL

11

TOLUCA PLAZA

12

INVESTMENT

OVERVIEW

PROPERTY OVERVIEW

TOLUCA PLAZA

PROPERTY OVERVIEW

Toluca Plaza is a thirty nine unit apartment community in a prime Toluca Lake location. With tremendous frontage and visibility on Riverside Drive, the property is nicely

situated East of Cahuenga Boulevard and West of Clybourn Avenue and rests on two corners. Built in 1971, the property is subject to rent control. There is an attractive unit

mix of Fifteen One Bedroom/One Bath units, Twelve One Bedroom/One Bath plus Den units, Six Two Bedroom/Two Bath Units and Six Two Bedroom/One and a Half Bath

Units.

Located in one of the most desirable pockets in the San Fernando Valley, Toluca Plaza easily attracts residents with its convenient and central location. It’s walking distance

to plenty of shopping, dining and entertainment on Riverside Drive. Some notable Los Angeles destinations are close by such as Universal Studios, Warner Brothers Studios,

Universal City Walk, Hollywood Bowl, Griffith Park and the Los Angeles Zoo. In addition, easy freeway access allows res idents to get to Hollywood, Burbank and other major

employment centers quickly.

Along with the highly desirable location, Toluca Plaza offers residents an array of amenities such as very spacious units, central air conditioning and heat, balconies, pool,

fitness center, leasing office, controlled access, gated tuck under and carport parking and an onsite laundry facility.

Toluca Plaza is an extremely rare, value add opportunity to own a thirty nine unit building in a highly desirable location that has huge upside in rents as units turn. Properties

of this quality and location rarely become available. This property has been with this current family for approximately 40 years.

PROPERTY OVERVIEW

Spacious Floorplans, with Excellent Unit Mix, and each Unit has at least One Balcony

Fitness Center and Leasing Office

Elevator and Pool

Central Air and Heat

Gated Tuckunder and Carport Parking (41 Tuckunder/ 24 Covered/ 1 vendor Slot-66

total)

Controlled Access

Each Unit has One Balcony while the Corner Units have Two

13

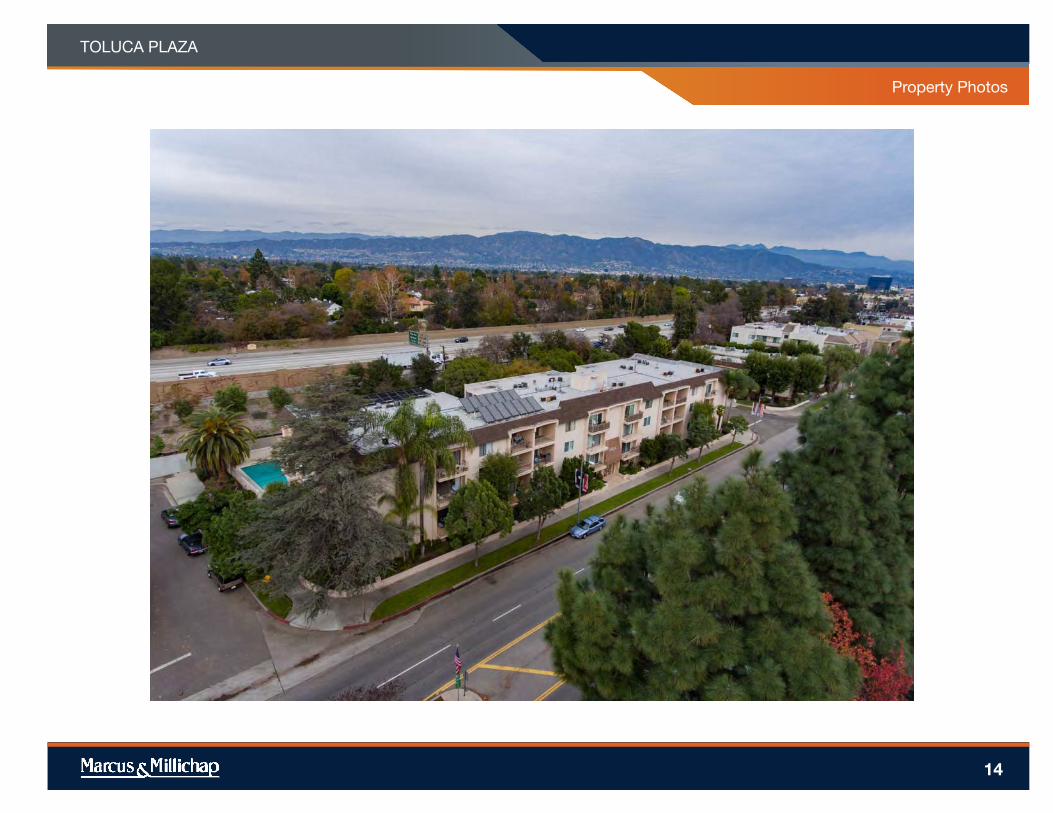

Property Photos

TOLUCA PLAZA

14

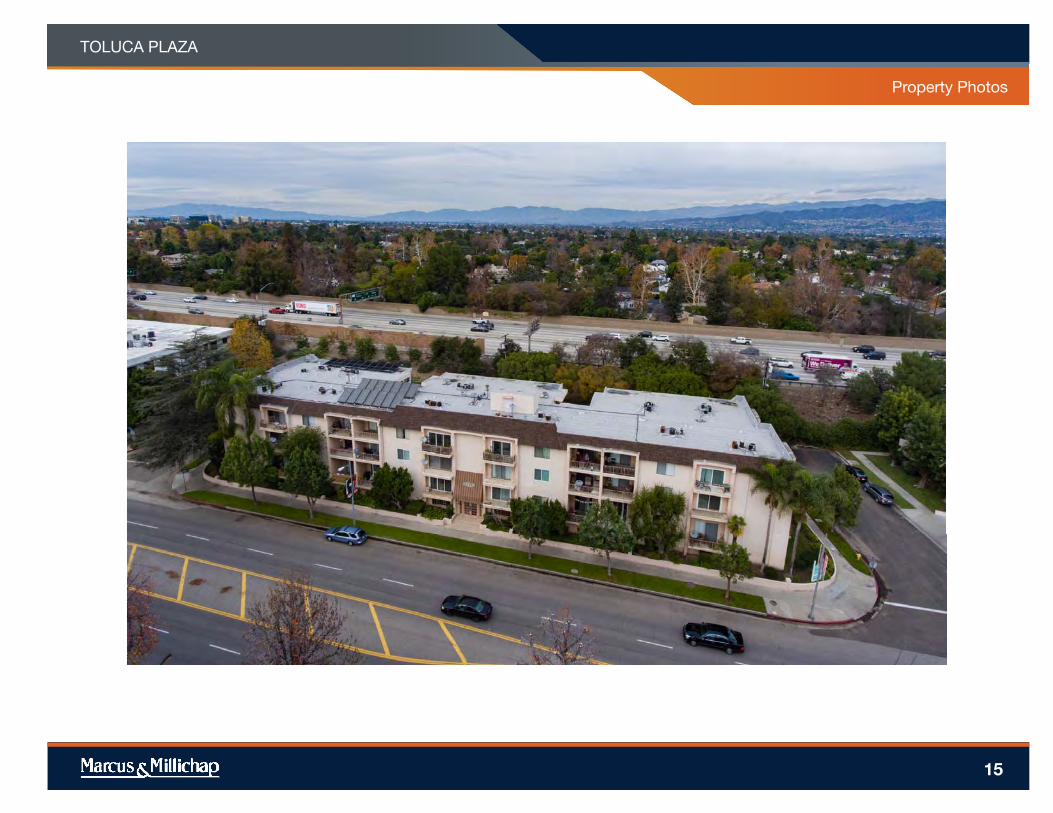

Property Photos

TOLUCA PLAZA

15

Property Photos

TOLUCA PLAZA

16

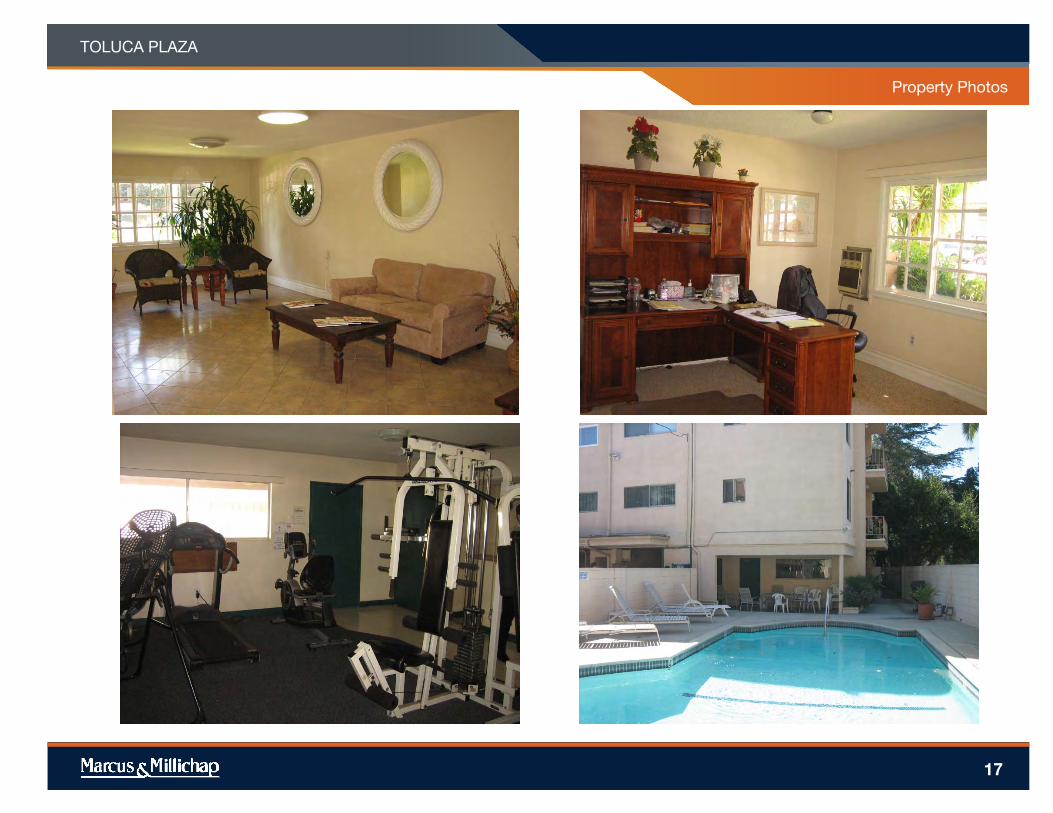

Property Photos

TOLUCA PLAZA

17

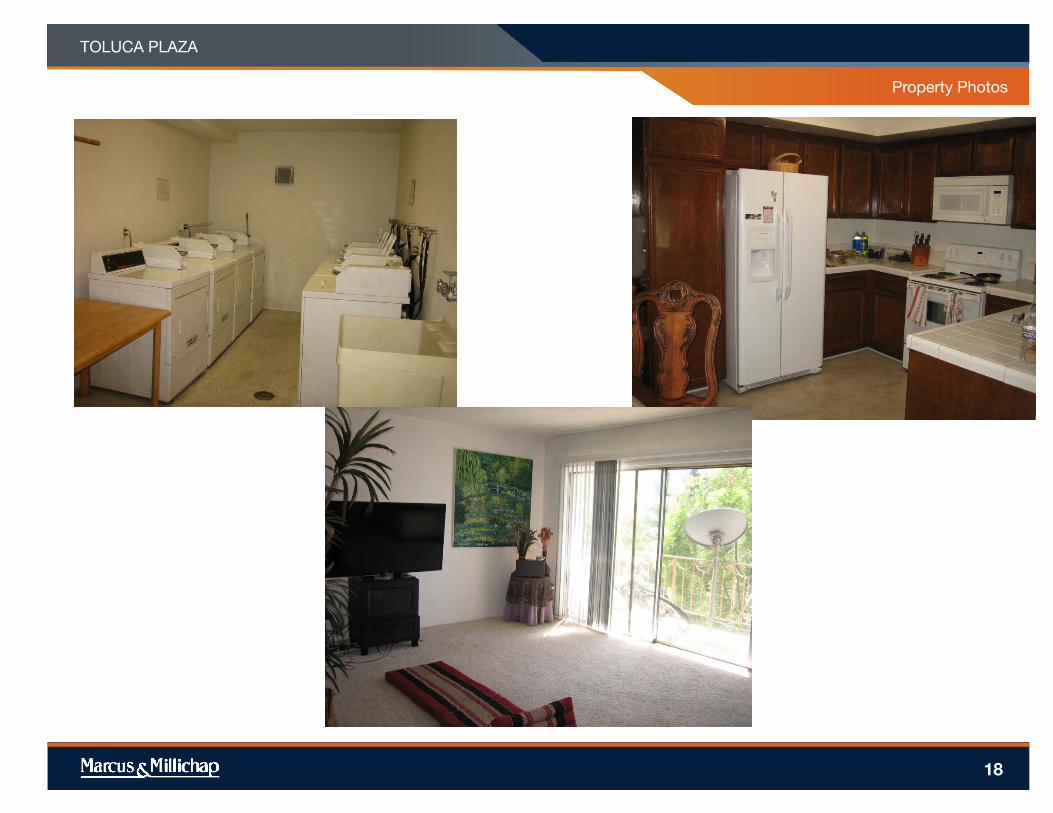

Property Photos

TOLUCA PLAZA

18

REGIONAL MAP

TOLUCA PLAZA

19

LOCAL MAP

TOLUCA PLAZA

20

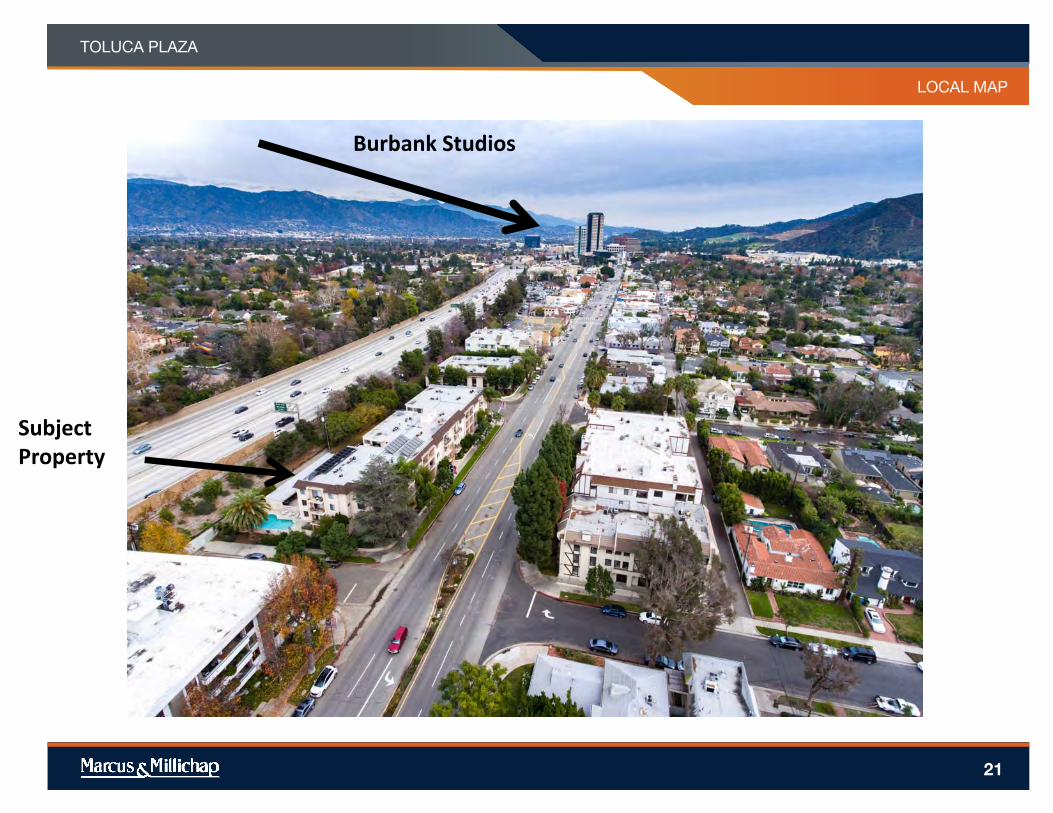

LOCAL MAP

TOLUCA PLAZA

21

Burbank Studios

Subject Property

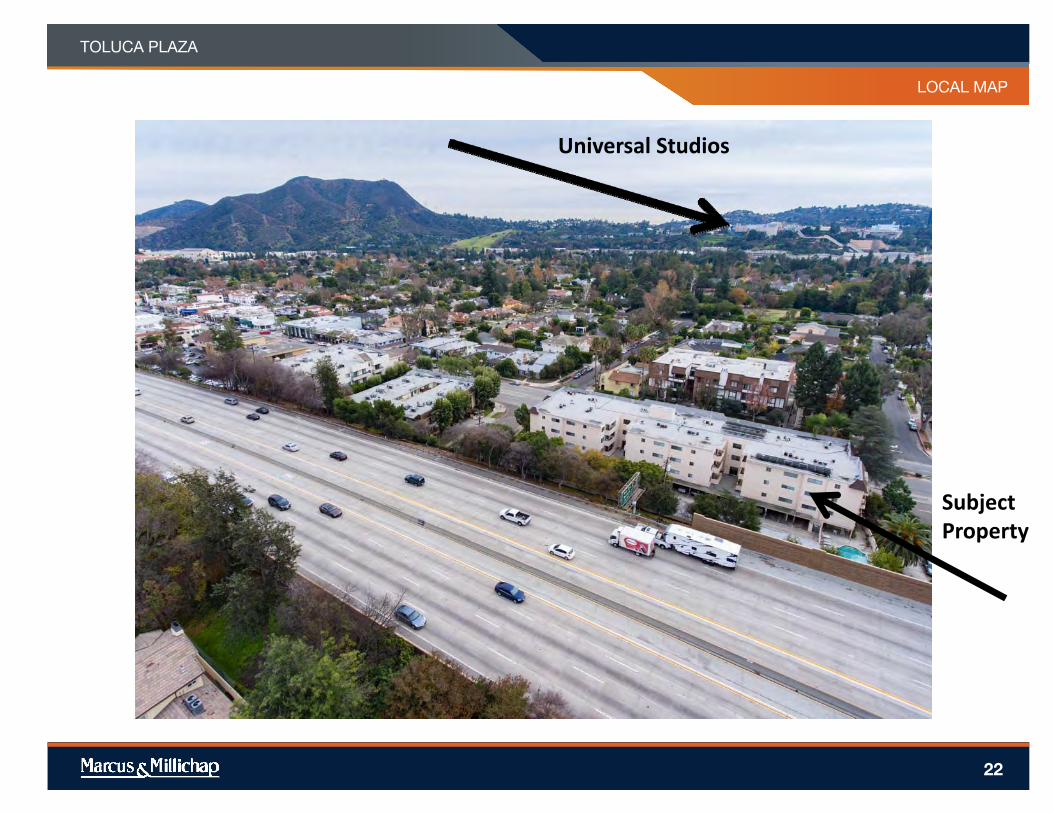

LOCAL MAP

TOLUCA PLAZA

22

Universal Studios

Subject Property

LOCAL MAP

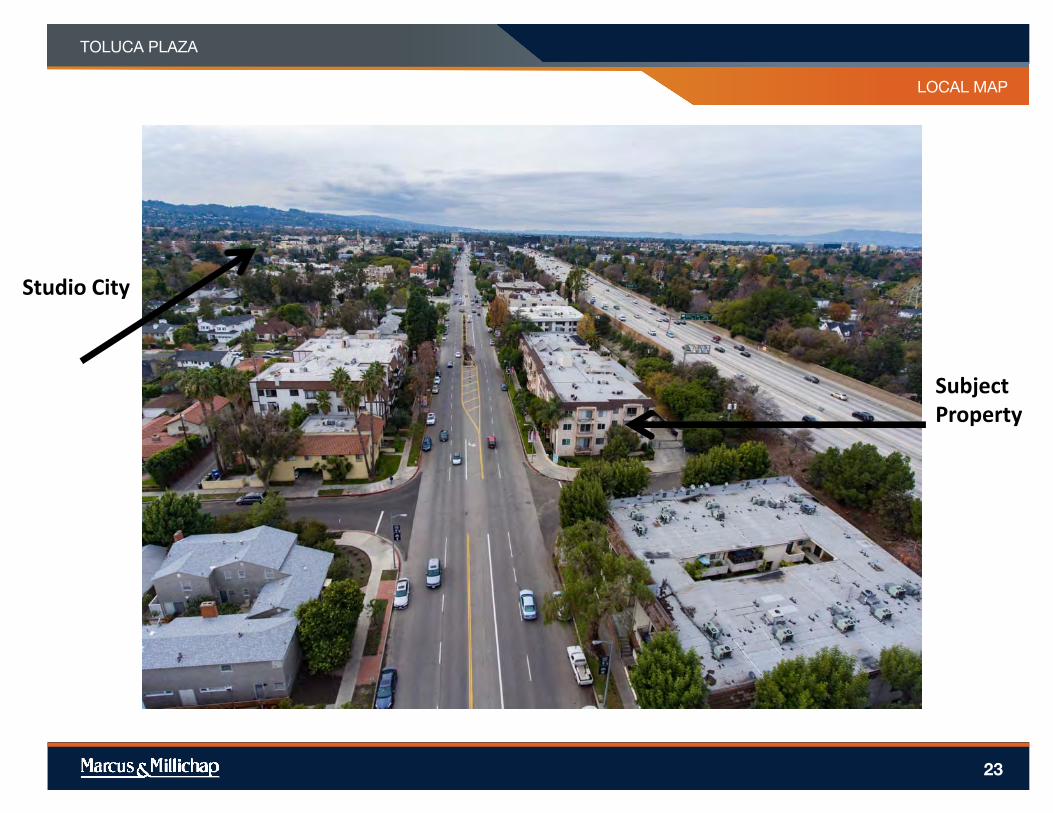

TOLUCA PLAZA

23

Studio City

SubjectProperty

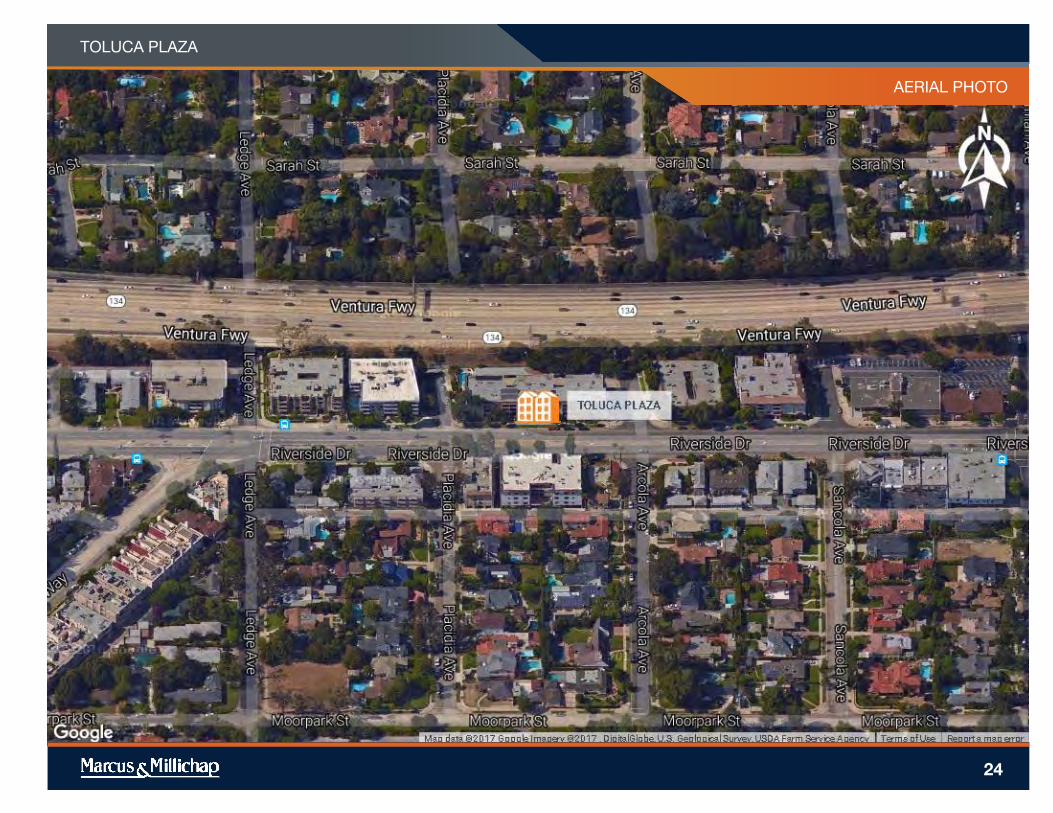

AERIAL PHOTO

TOLUCA PLAZA

24

TOLUCA PLAZA

25

MARKET

COMPARABLES

8

TOLUCA PLAZA

SALES COMPARABLES MAP

26

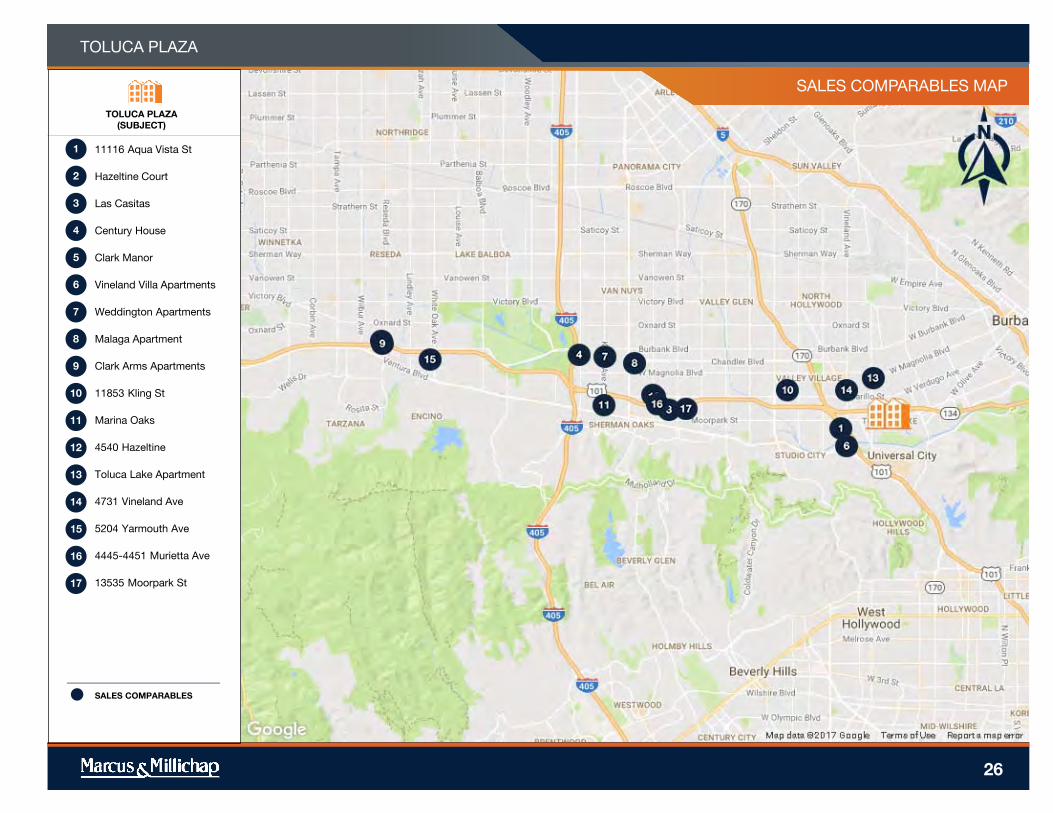

TOLUCA PLAZA

(SUBJECT)

11116 Aqua Vista St

Hazeltine Court

Las Casitas

Century House

Clark Manor

Vineland Villa Apartments

Weddington Apartments

Malaga Apartment

Clark Arms Apartments

11853 Kling St

Marina Oaks

4540 Hazeltine

Toluca Lake Apartment

4731 Vineland Ave

5204 Yarmouth Ave

4445-4451 Murietta Ave

13535 Moorpark St

SALES COMPARABLES

1

2

3

4

5

7

8

13

14

15

16

17

6

9

10

11

12

27

Avg. 3.67%

0

1

1

2

2

3

3

4

4

5

5

Toluca

Plaza

11116 Aqua

Vista St

Hazeltine

Court

Las Casitas Century

House

Clark Manor Vineland

Villa

Apartments

Weddington

Apartments

Malaga

Apartment

Clark Arms

Apartments

11853

Kling St

Marina Oaks 4540

Hazeltine

Toluca Lake

Apartment

4731

Vineland

Ave

5204

Yarmouth

Ave

4445-4451

Murietta

Ave

13535

Moorpark St

PROPERTY NAMETOLUCA PLAZA

COMPARABLES

Average Cap Rate

SALES COMPARABLES SALES COMPS AVG

28

Avg. 15.89

0

2

4

6

8

10

11

13

15

17

19

Toluca

Plaza

11116 Aqua

Vista St

Hazeltine

Court

Las Casitas Century

House

Clark Manor Vineland

Villa

Apartments

Weddington

Apartments

Malaga

Apartment

Clark Arms

Apartments

11853

Kling St

Marina Oaks 4540

Hazeltine

Toluca Lake

Apartment

4731

Vineland

Ave

5204

Yarmouth

Ave

4445-4451

Murietta

Ave

13535

Moorpark St

PROPERTY NAMETOLUCA PLAZA

COMPARABLES

Average GRM

SALES COMPARABLES SALES COMPS AVG

29

Avg. $304.80

$0.00

$40.00

$80.00

$120.00

$160.00

$200.00

$240.00

$280.00

$320.00

$360.00

$400.00

Toluca

Plaza

11116 Aqua

Vista St

Hazeltine

Court

Las Casitas Century

House

Clark Manor Vineland

Villa

Apartments

Weddington

Apartments

Malaga

Apartment

Clark Arms

Apartments

11853

Kling St

Marina Oaks 4540

Hazeltine

Toluca Lake

Apartment

4731

Vineland

Ave

5204

Yarmouth

Ave

4445-4451

Murietta

Ave

13535

Moorpark St

PROPERTY NAMETOLUCA PLAZA

COMPARABLES

Average Price Per Square Foot

SALES COMPARABLES SALES COMPS AVG

30

Avg. $252,840

$0

$40,000

$80,000

$120,000

$160,000

$200,000

$240,000

$280,000

$320,000

$360,000

$400,000

Toluca

Plaza

11116 Aqua

Vista St

Hazeltine

Court

Las Casitas Century

House

Clark Manor Vineland

Villa

Apartments

Weddington

Apartments

Malaga

Apartment

Clark Arms

Apartments

11853

Kling St

Marina Oaks 4540

Hazeltine

Toluca Lake

Apartment

4731

Vineland

Ave

5204

Yarmouth

Ave

4445-4451

Murietta

Ave

13535

Moorpark St

PROPERTY NAMETOLUCA PLAZA

COMPARABLES

Average Price Per Unit

SALES COMPARABLES SALES COMPS AVG

PROPERTY NAME

MARKETING TEAM

TOLUCA PLAZA

COMPARABLES

rentpropertyname1

rentpropertyaddress1

rentpropertyname1

rentpropertyaddress1

rentpropertyname1

rentpropertyaddress1

31

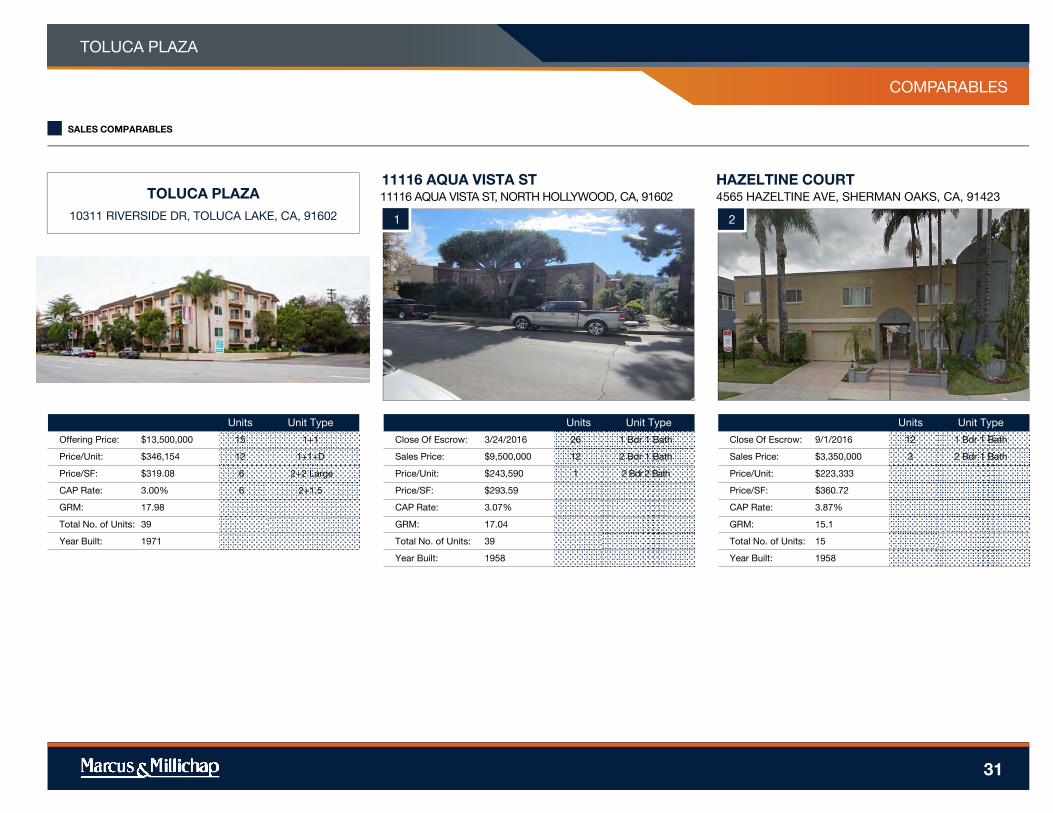

SALES COMPARABLES

rentpropertyaddress1

673 VISTA ISLE DRIVE

673 VISTA ISLE DRIVE, SUNRISE, FL, 33325

TOLUCA PLAZA

10311 RIVERSIDE DR, TOLUCA LAKE, CA, 91602

Units Unit Type

Offering Price: $13,500,000 15 1+1

Price/Unit: $346,154 12 1+1+D

Price/SF: $319.08 6 2+2 Large

CAP Rate: 3.00% 6 2+1.5

GRM: 17.98

Total No. of Units: 39

Year Built: 1971

11116 AQUA VISTA ST, NORTH HOLLYWOOD, CA, 91602

11116 AQUA VISTA ST

1

Units Unit Type

Close Of Escrow: 3/24/2016 26 1 Bdr 1 Bath

Sales Price: $9,500,000 12 2 Bdr 1 Bath

Price/Unit: $243,590 1 2 Bdr 2 Bath

Price/SF: $293.59

CAP Rate: 3.07%

GRM: 17.04

Total No. of Units: 39

Year Built: 1958

4565 HAZELTINE AVE, SHERMAN OAKS, CA, 91423

HAZELTINE COURT

Units Unit Type

Close Of Escrow: 9/1/2016 12 1 Bdr 1 Bath

Sales Price: $3,350,000 3 2 Bdr 1 Bath

Price/Unit: $223,333

Price/SF: $360.72

CAP Rate: 3.87%

GRM: 15.1

Total No. of Units: 15

Year Built: 1958

2

PROPERTY NAME

MARKETING TEAM

TOLUCA PLAZA

COMPARABLES

rentpropertyname1

rentpropertyaddress1

rentpropertyname1

rentpropertyaddress1

rentpropertyname1

rentpropertyaddress1

32

SALES COMPARABLES

Units Unit Type

Close Of Escrow: 11/29/2016 13 1 Bdr 1 Bath

Sales Price: $6,300,000 7 2 Bdr 2 Bath

Price/Unit: $315,000

Price/SF: $354.01

CAP Rate: 3.45%

GRM: 16.5

Total No. of Units: 20

Year Built: 1978

LAS CASITAS

3

13830 MOORPARK ST, VAN NUYS, CA, 91423 5307 SEPULVEDA BLVD, SHERMAN OAKS, CA, 91411

CENTURY HOUSE

4

Units Unit Type

Close Of Escrow: 12/16/2015 65 1 Bdr 1 Bath

Sales Price: $15,625,000 7 2 Bdr 2 Bath

Price/Unit: $217,014

Price/SF: $282.95

CAP Rate: 3.67%

Total No. of Units: 72

Year Built: 1969

18553 CLARK ST, TARZANA, CA, 91356

CLARK MANOR

5

Units Unit Type

Close Of Escrow: 11/8/2016 13 3 Bdr 2 Bath

Sales Price: $12,075,000 9 2 Bdr 2 Bath

Price/Unit: $251,562 11 2 Bdr 1 Bath

Price/SF: $271.00 11 1 Bdr 1 Bath

Cap Rate: 4.11% 4 Studio 1 Bath

GRM: 14.36

Total No. of Units: 48

Year Built: 1960

PROPERTY NAME

MARKETING TEAM

TOLUCA PLAZA

COMPARABLES

rentpropertyname1

rentpropertyaddress1

rentpropertyname1

rentpropertyaddress1

rentpropertyname1

rentpropertyaddress1

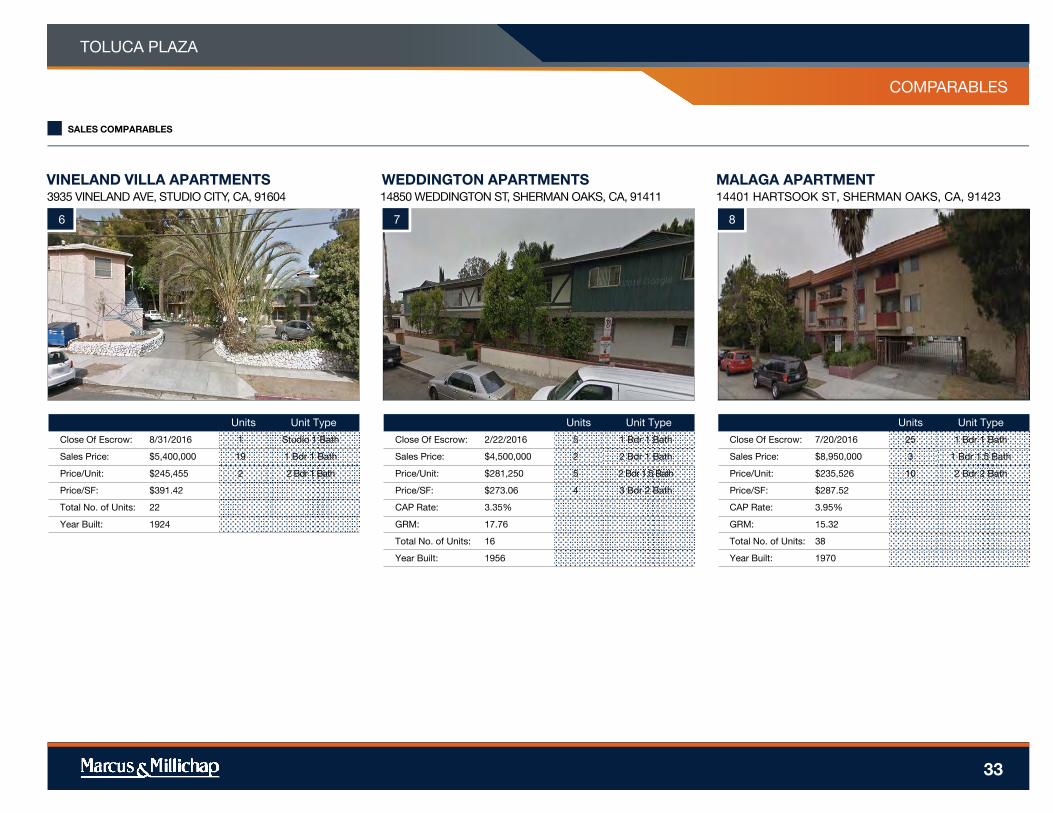

33

SALES COMPARABLES

Units Unit Type

Close Of Escrow: 8/31/2016 1 Studio 1 Bath

Sales Price: $5,400,000 19 1 Bdr 1 Bath

Price/Unit: $245,455 2 2 Bdr 1 Bath

Price/SF: $391.42

Total No. of Units: 22

Year Built: 1924

VINELAND VILLA APARTMENTS

6

3935 VINELAND AVE, STUDIO CITY, CA, 91604 14850 WEDDINGTON ST, SHERMAN OAKS, CA, 91411

WEDDINGTON APARTMENTS

7

Units Unit Type

Close Of Escrow: 2/22/2016 5 1 Bdr 1 Bath

Sales Price: $4,500,000 2 2 Bdr 1 Bath

Price/Unit: $281,250 5 2 Bdr 1.5 Bath

Price/SF: $273.06 4 3 Bdr 2 Bath

CAP Rate: 3.35%

GRM: 17.76

Total No. of Units: 16

Year Built: 1956

14401 HARTSOOK ST, SHERMAN OAKS, CA, 91423

MALAGA APARTMENT

Units Unit Type

Close Of Escrow: 7/20/2016 25 1 Bdr 1 Bath

Sales Price: $8,950,000 3 1 Bdr 1.5 Bath

Price/Unit: $235,526 10 2 Bdr 2 Bath

Price/SF: $287.52

CAP Rate: 3.95%

GRM: 15.32

Total No. of Units: 38

Year Built: 1970

8

PROPERTY NAME

MARKETING TEAM

TOLUCA PLAZA

COMPARABLES

rentpropertyname1

rentpropertyaddress1

rentpropertyname1

rentpropertyaddress1

rentpropertyname1

rentpropertyaddress1

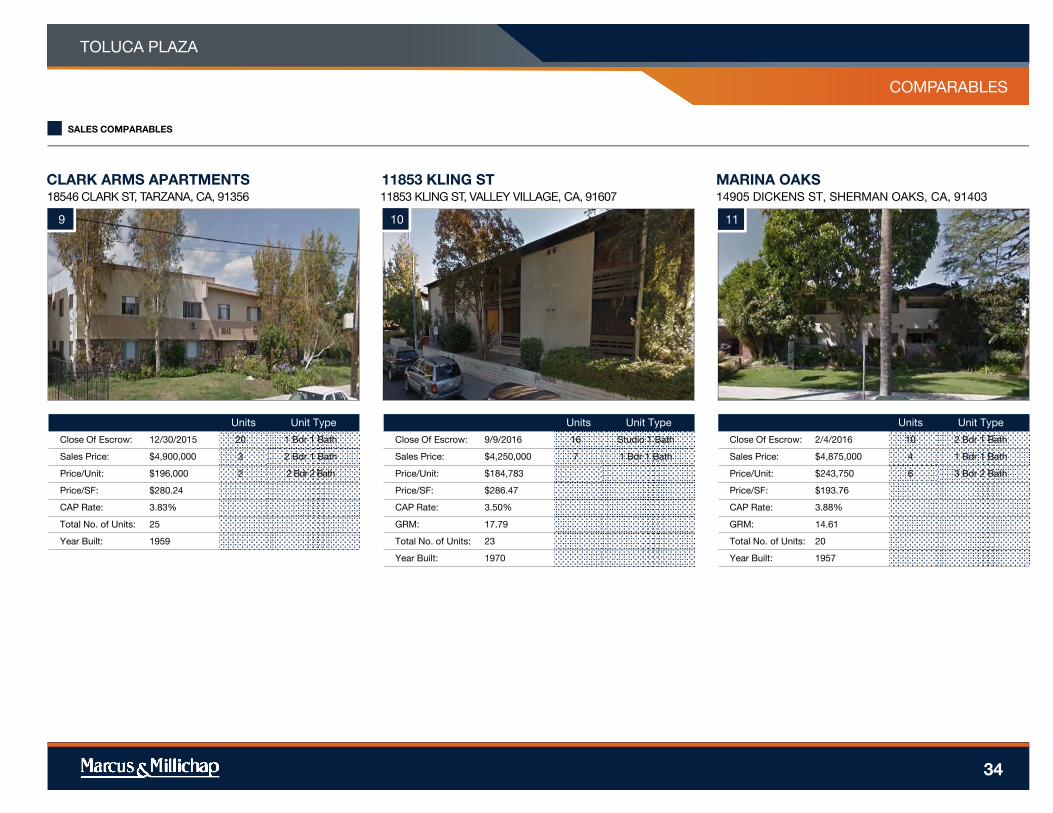

34

SALES COMPARABLES

Units Unit Type

Close Of Escrow: 12/30/2015 20 1 Bdr 1 Bath

Sales Price: $4,900,000 3 2 Bdr 1 Bath

Price/Unit: $196,000 2 2 Bdr 2 Bath

Price/SF: $280.24

CAP Rate: 3.83%

Total No. of Units: 25

Year Built: 1959

CLARK ARMS APARTMENTS

9

18546 CLARK ST, TARZANA, CA, 91356 11853 KLING ST, VALLEY VILLAGE, CA, 91607

11853 KLING ST

10

Units Unit Type

Close Of Escrow: 9/9/2016 16 Studio 1 Bath

Sales Price: $4,250,000 7 1 Bdr 1 Bath

Price/Unit: $184,783

Price/SF: $286.47

CAP Rate: 3.50%

GRM: 17.79

Total No. of Units: 23

Year Built: 1970

14905 DICKENS ST, SHERMAN OAKS, CA, 91403

MARINA OAKS

Units Unit Type

Close Of Escrow: 2/4/2016 10 2 Bdr 1 Bath

Sales Price: $4,875,000 4 1 Bdr 1 Bath

Price/Unit: $243,750 6 3 Bdr 2 Bath

Price/SF: $193.76

CAP Rate: 3.88%

GRM: 14.61

Total No. of Units: 20

Year Built: 1957

11

PROPERTY NAME

MARKETING TEAM

TOLUCA PLAZA

COMPARABLES

rentpropertyname1

rentpropertyaddress1

rentpropertyname1

rentpropertyaddress1

rentpropertyname1

rentpropertyaddress1

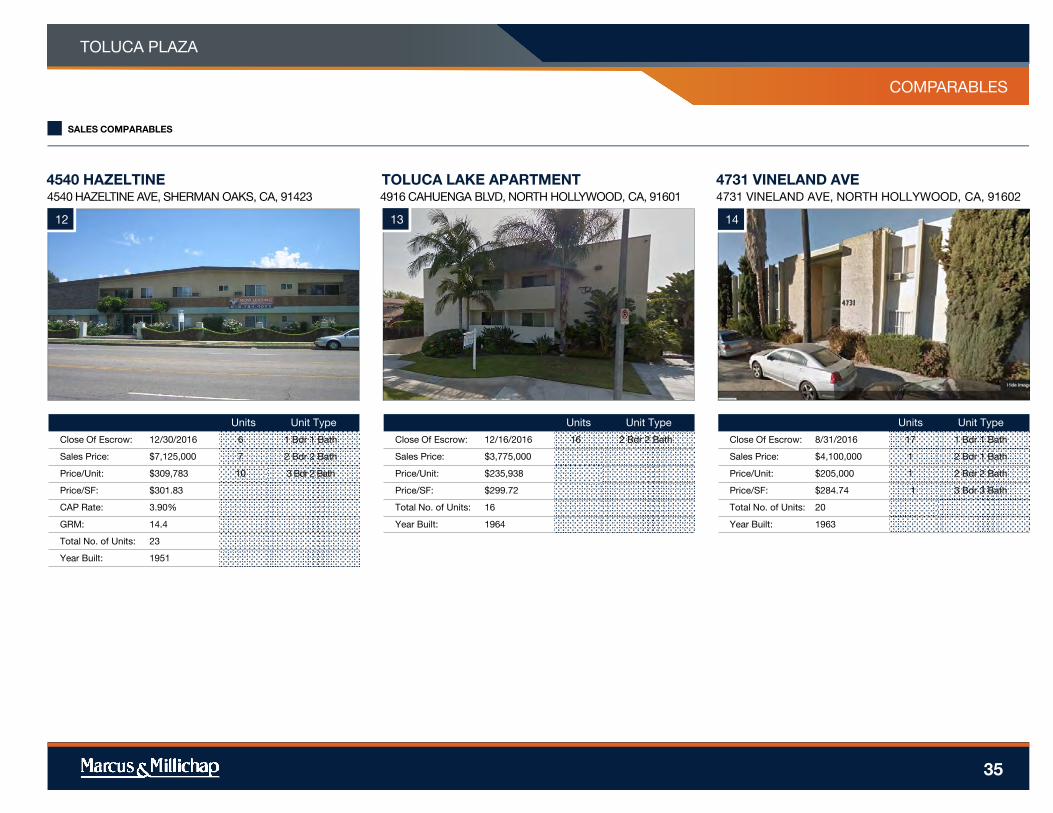

35

SALES COMPARABLES

Units Unit Type

Close Of Escrow: 12/30/2016 6 1 Bdr 1 Bath

Sales Price: $7,125,000 7 2 Bdr 2 Bath

Price/Unit: $309,783 10 3 Bdr 2 Bath

Price/SF: $301.83

CAP Rate: 3.90%

GRM: 14.4

Total No. of Units: 23

Year Built: 1951

4540 HAZELTINE

12

4540 HAZELTINE AVE, SHERMAN OAKS, CA, 91423 4916 CAHUENGA BLVD, NORTH HOLLYWOOD, CA, 91601

TOLUCA LAKE APARTMENT

13

Units Unit Type

Close Of Escrow: 12/16/2016 16 2 Bdr 2 Bath

Sales Price: $3,775,000

Price/Unit: $235,938

Price/SF: $299.72

Total No. of Units: 16

Year Built: 1964

4731 VINELAND AVE, NORTH HOLLYWOOD, CA, 91602

4731 VINELAND AVE

Units Unit Type

Close Of Escrow: 8/31/2016 17 1 Bdr 1 Bath

Sales Price: $4,100,000 1 2 Bdr 1 Bath

Price/Unit: $205,000 1 2 Bdr 2 Bath

Price/SF: $284.74 1 3 Bdr 3 Bath

Total No. of Units: 20

Year Built: 1963

14

PROPERTY NAME

MARKETING TEAM

TOLUCA PLAZA

COMPARABLES

rentpropertyname1

rentpropertyaddress1

rentpropertyname1

rentpropertyaddress1

rentpropertyname1

rentpropertyaddress1

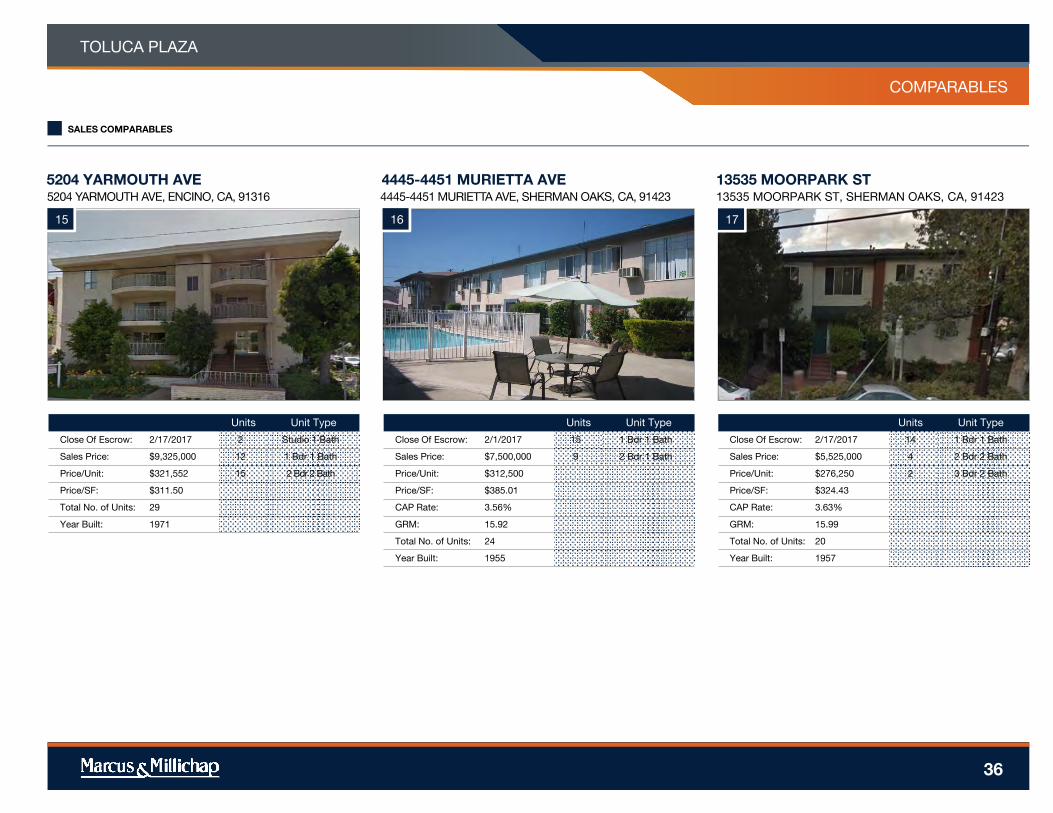

36

SALES COMPARABLES

Units Unit Type

Close Of Escrow: 2/17/2017 2 Studio 1 Bath

Sales Price: $9,325,000 12 1 Bdr 1 Bath

Price/Unit: $321,552 15 2 Bdr 2 Bath

Price/SF: $311.50

Total No. of Units: 29

Year Built: 1971

5204 YARMOUTH AVE

15

5204 YARMOUTH AVE, ENCINO, CA, 91316 4445-4451 MURIETTA AVE, SHERMAN OAKS, CA, 91423

4445-4451 MURIETTA AVE

16

Units Unit Type

Close Of Escrow: 2/1/2017 15 1 Bdr 1 Bath

Sales Price: $7,500,000 9 2 Bdr 1 Bath

Price/Unit: $312,500

Price/SF: $385.01

CAP Rate: 3.56%

GRM: 15.92

Total No. of Units: 24

Year Built: 1955

13535 MOORPARK ST, SHERMAN OAKS, CA, 91423

13535 MOORPARK ST

Units Unit Type

Close Of Escrow: 2/17/2017 14 1 Bdr 1 Bath

Sales Price: $5,525,000 4 2 Bdr 2 Bath

Price/Unit: $276,250 2 3 Bdr 2 Bath

Price/SF: $324.43

CAP Rate: 3.63%

GRM: 15.99

Total No. of Units: 20

Year Built: 1957

17

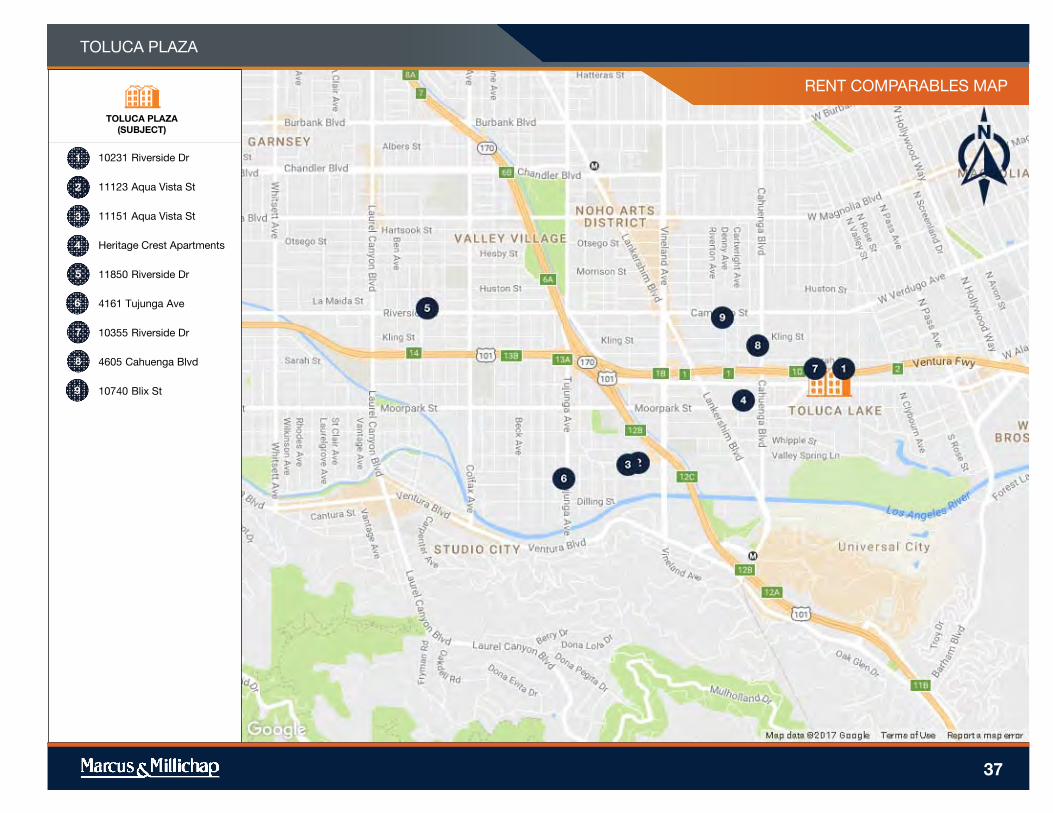

8

TOLUCA PLAZA

RENT COMPARABLES MAP

TOLUCA PLAZA

(SUBJECT)

10231 Riverside Dr

11123 Aqua Vista St

11151 Aqua Vista St

Heritage Crest Apartments

11850 Riverside Dr

4161 Tujunga Ave

10355 Riverside Dr

4605 Cahuenga Blvd

10740 Blix St

4

7

8

9

11

20

12

14

15

16

17

13

18

10

4

7

8

9

1

2

3

5

6

37

PROPERTY NAMETOLUCA PLAZA

COMPARABLES

38

AVERAGE RENT - MULTIFAMILY

Avg. $1,890

$0

$300

$600

$900

$1,200

$1,500

$1,800

$2,100

$2,400

$2,700

$3,000

Toluca

Plaza

10231

Riverside

Dr

11123

Aqua

Vista St

11151

Aqua

Vista St

Heritage

Crest

Apartments

11850

Riverside

Dr

4161

Tujunga

Ave

10355

Riverside

Dr

4605

Cahuenga

Blvd

10740

Blix St

1 Bedroom

Avg. $2,397

$0

$300

$600

$900

$1,200

$1,500

$1,800

$2,100

$2,400

$2,700

$3,000

Toluca

Plaza

10231

Riverside

Dr

11123

Aqua

Vista St

11151

Aqua

Vista St

Heritage

Crest

Apartments

11850

Riverside

Dr

4161

Tujunga

Ave

10355

Riverside

Dr

4605

Cahuenga

Blvd

10740

Blix St

2 Bedroom

PROPERTY NAME

MARKETING TEAM

TOLUCA PLAZA

RENT COMPARABLES

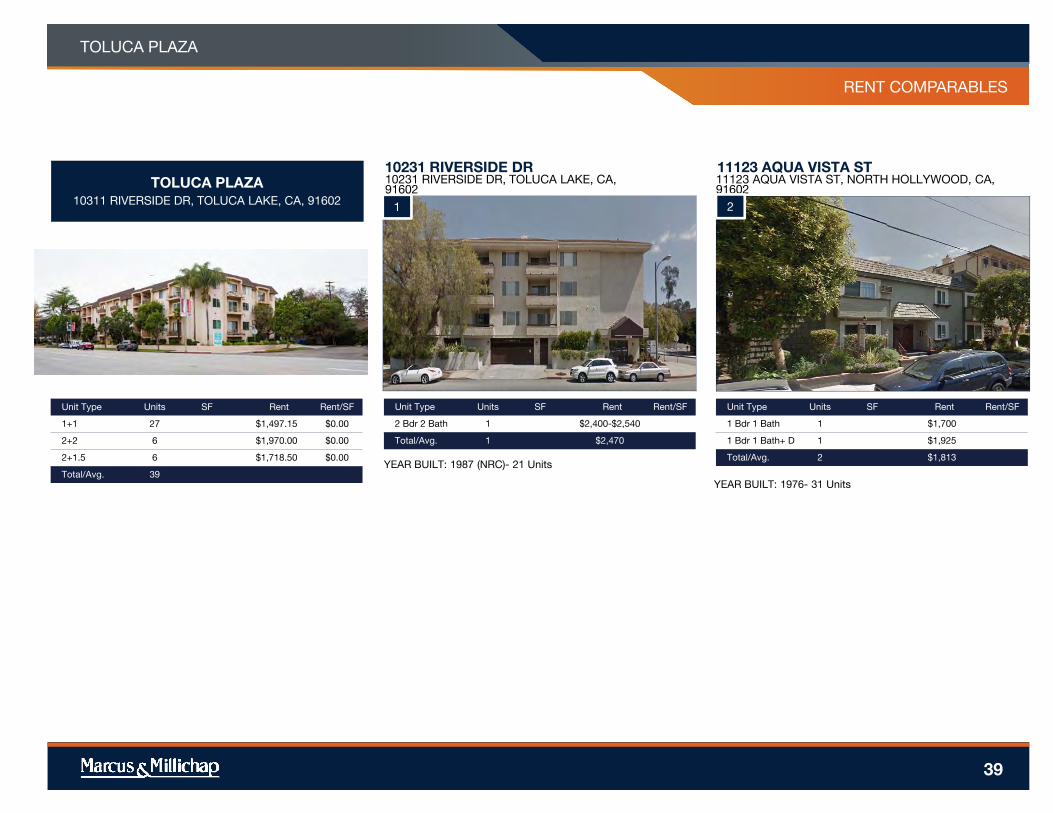

TOLUCA PLAZA

10311 RIVERSIDE DR, TOLUCA LAKE, CA, 91602

TOLUCA PLAZA

10311 RIVERSIDE DR, TOLUCA LAKE, CA, 91602

TOLUCA PLAZA

10311 RIVERSIDE DR, TOLUCA LAKE, CA, 91602

39

TOLUCA PLAZA

10311 RIVERSIDE DR, TOLUCA LAKE, CA, 91602

Unit Type Units SF Rent Rent/SF

1+1 27 $1,497.15 $0.00

2+2 6 $1,970.00 $0.00

2+1.5 6 $1,718.50 $0.00

Total/Avg. 39

10231 RIVERSIDE DR10231 RIVERSIDE DR, TOLUCA LAKE, CA, 91602

1

Unit Type Units SF Rent Rent/SF

2 Bdr 2 Bath 1 $2,400-$2,540

Total/Avg. 1 $2,470

11123 AQUA VISTA ST11123 AQUA VISTA ST, NORTH HOLLYWOOD, CA, 91602

2

Unit Type Units SF Rent Rent/SF

1 Bdr 1 Bath 1 $1,700

1 Bdr 1 Bath+ D 1 $1,925

Total/Avg. 2 $1,813YEAR BUILT: 1987 (NRC)- 21 Units

YEAR BUILT: 1976- 31 Units

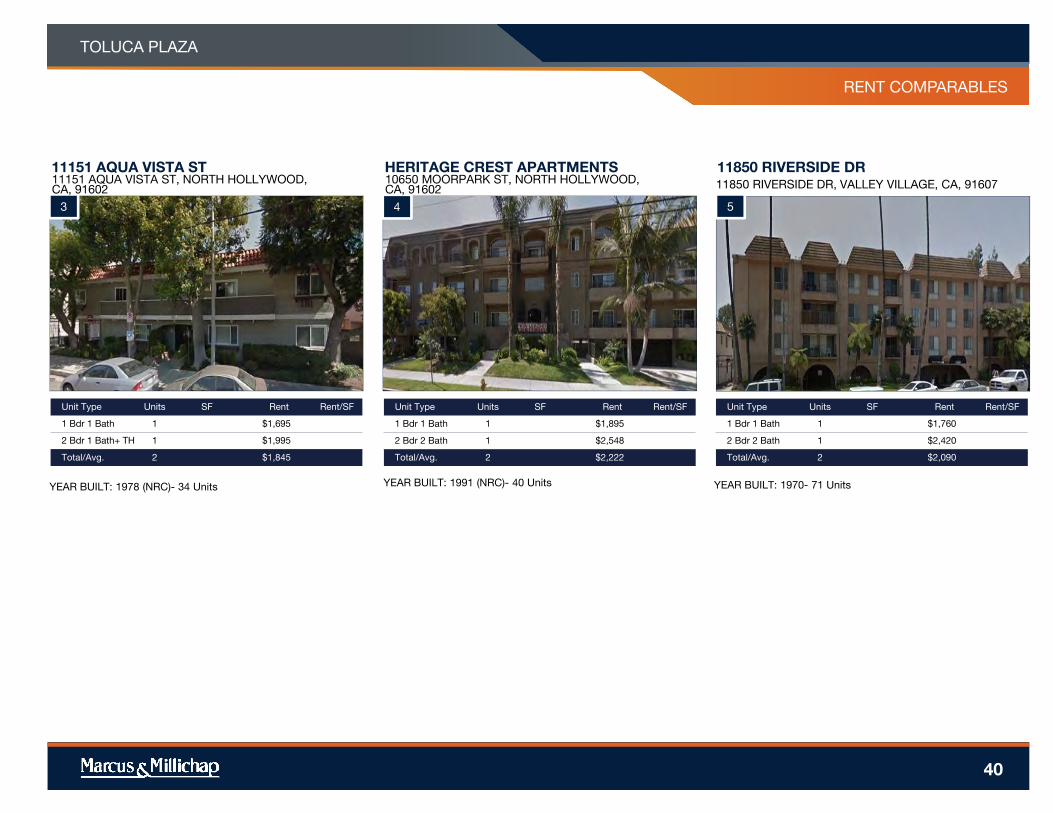

PROPERTY NAME

MARKETING TEAM

TOLUCA PLAZA

RENT COMPARABLES

11151 AQUA VISTA ST

11151 AQUA VISTA ST, NORTH HOLLYWOOD, CA, 91602

11151 AQUA VISTA ST

11151 AQUA VISTA ST, NORTH HOLLYWOOD, CA, 91602

11151 AQUA VISTA ST

11151 AQUA VISTA ST, NORTH HOLLYWOOD, CA, 91602

40

11151 AQUA VISTA ST11151 AQUA VISTA ST, NORTH HOLLYWOOD, CA, 91602

3

Unit Type Units SF Rent Rent/SF

1 Bdr 1 Bath 1 $1,695

2 Bdr 1 Bath+ TH 1 $1,995

Total/Avg. 2 $1,845

HERITAGE CREST APARTMENTS10650 MOORPARK ST, NORTH HOLLYWOOD, CA, 91602

4

Unit Type Units SF Rent Rent/SF

1 Bdr 1 Bath 1 $1,895

2 Bdr 2 Bath 1 $2,548

Total/Avg. 2 $2,222

11850 RIVERSIDE DR11850 RIVERSIDE DR, VALLEY VILLAGE, CA, 91607

5

Unit Type Units SF Rent Rent/SF

1 Bdr 1 Bath 1 $1,760

2 Bdr 2 Bath 1 $2,420

Total/Avg. 2 $2,090

YEAR BUILT: 1978 (NRC)- 34 Units YEAR BUILT: 1991 (NRC)- 40 Units YEAR BUILT: 1970- 71 Units

PROPERTY NAME

MARKETING TEAM

TOLUCA PLAZA

RENT COMPARABLES

4161 TUJUNGA AVE

4161 TUJUNGA AVE, STUDIO CITY, CA, 91604

4161 TUJUNGA AVE

4161 TUJUNGA AVE, STUDIO CITY, CA, 91604

4161 TUJUNGA AVE

4161 TUJUNGA AVE, STUDIO CITY, CA, 91604

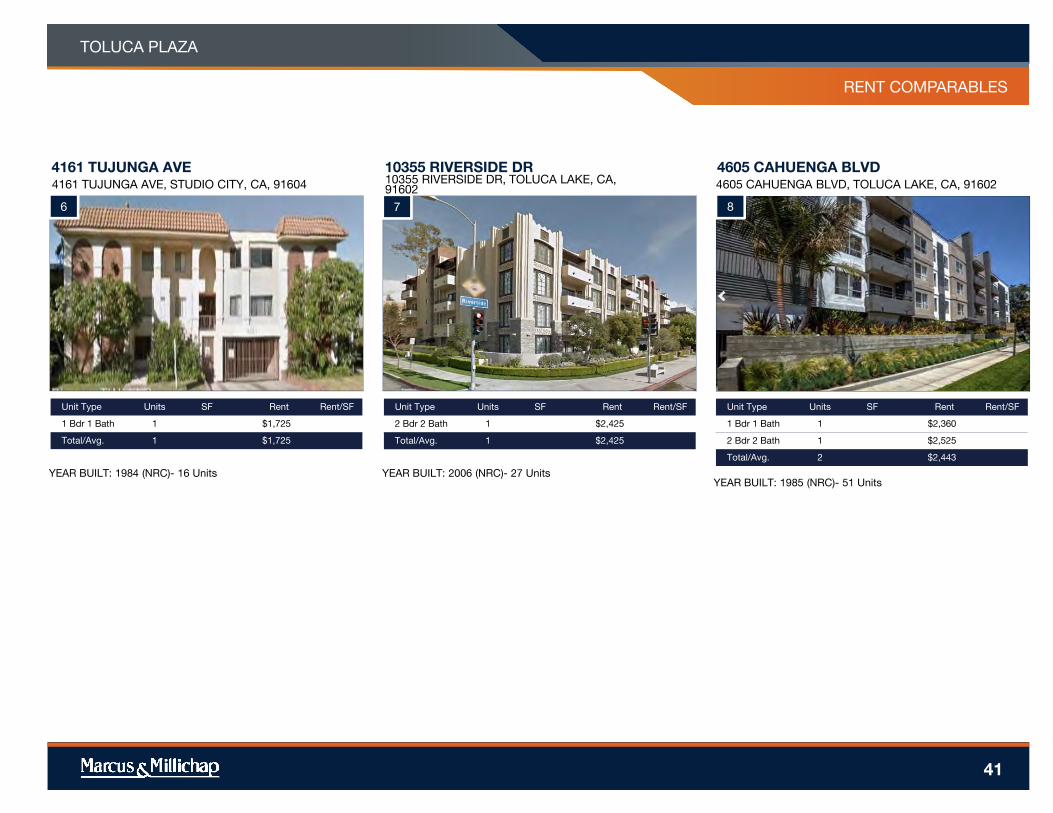

41

4161 TUJUNGA AVE4161 TUJUNGA AVE, STUDIO CITY, CA, 91604

6

Unit Type Units SF Rent Rent/SF

1 Bdr 1 Bath 1 $1,725

Total/Avg. 1 $1,725

10355 RIVERSIDE DR10355 RIVERSIDE DR, TOLUCA LAKE, CA, 91602

7

Unit Type Units SF Rent Rent/SF

2 Bdr 2 Bath 1 $2,425

Total/Avg. 1 $2,425

4605 CAHUENGA BLVD4605 CAHUENGA BLVD, TOLUCA LAKE, CA, 91602

8

Unit Type Units SF Rent Rent/SF

1 Bdr 1 Bath 1 $2,360

2 Bdr 2 Bath 1 $2,525

Total/Avg. 2 $2,443

YEAR BUILT: 1984 (NRC)- 16 UnitsYEAR BUILT: 1985 (NRC)- 51 Units

YEAR BUILT: 2006 (NRC)- 27 Units

PROPERTY NAME

MARKETING TEAM

TOLUCA PLAZA

RENT COMPARABLES

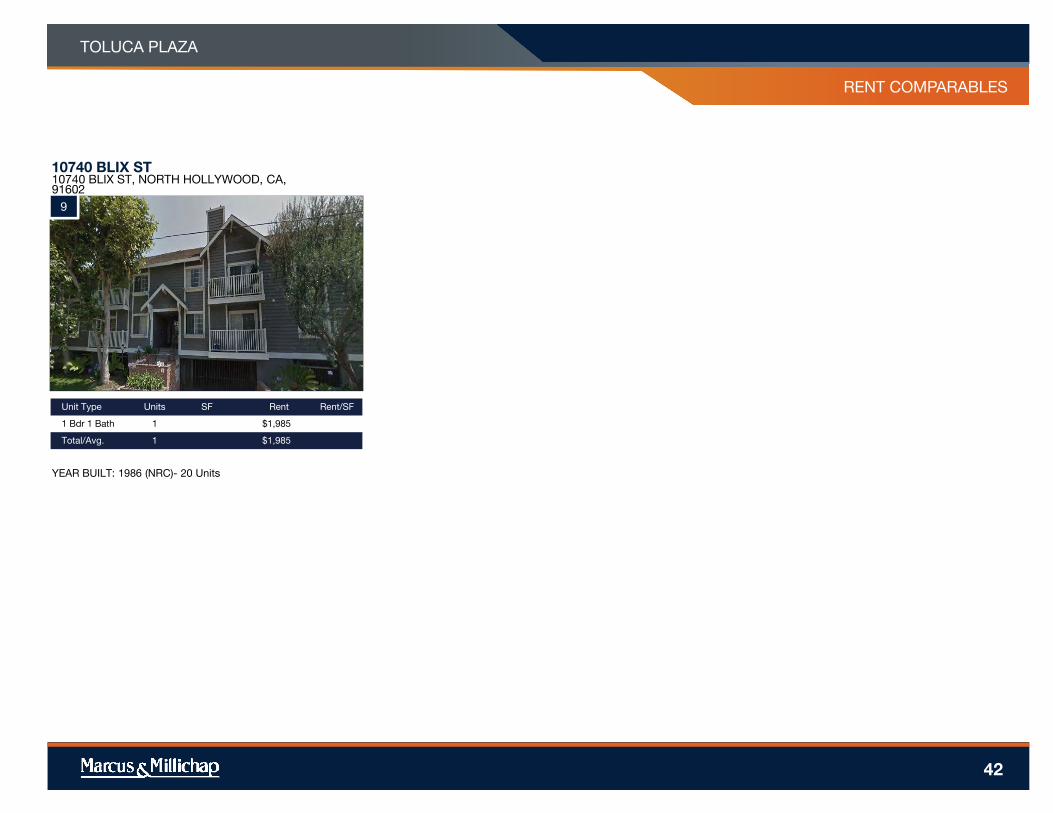

10740 BLIX ST

10740 BLIX ST, NORTH HOLLYWOOD, CA, 91602

10740 BLIX ST

10740 BLIX ST, NORTH HOLLYWOOD, CA, 91602

10740 BLIX ST

10740 BLIX ST, NORTH HOLLYWOOD, CA, 91602

42

10740 BLIX ST10740 BLIX ST, NORTH HOLLYWOOD, CA, 91602

9

Unit Type Units SF Rent Rent/SF

1 Bdr 1 Bath 1 $1,985

Total/Avg. 1 $1,985

YEAR BUILT: 1986 (NRC)- 20 Units

TOLUCA PLAZA

43

MARKET

OVERVIEW

MARKET OVERVIEW

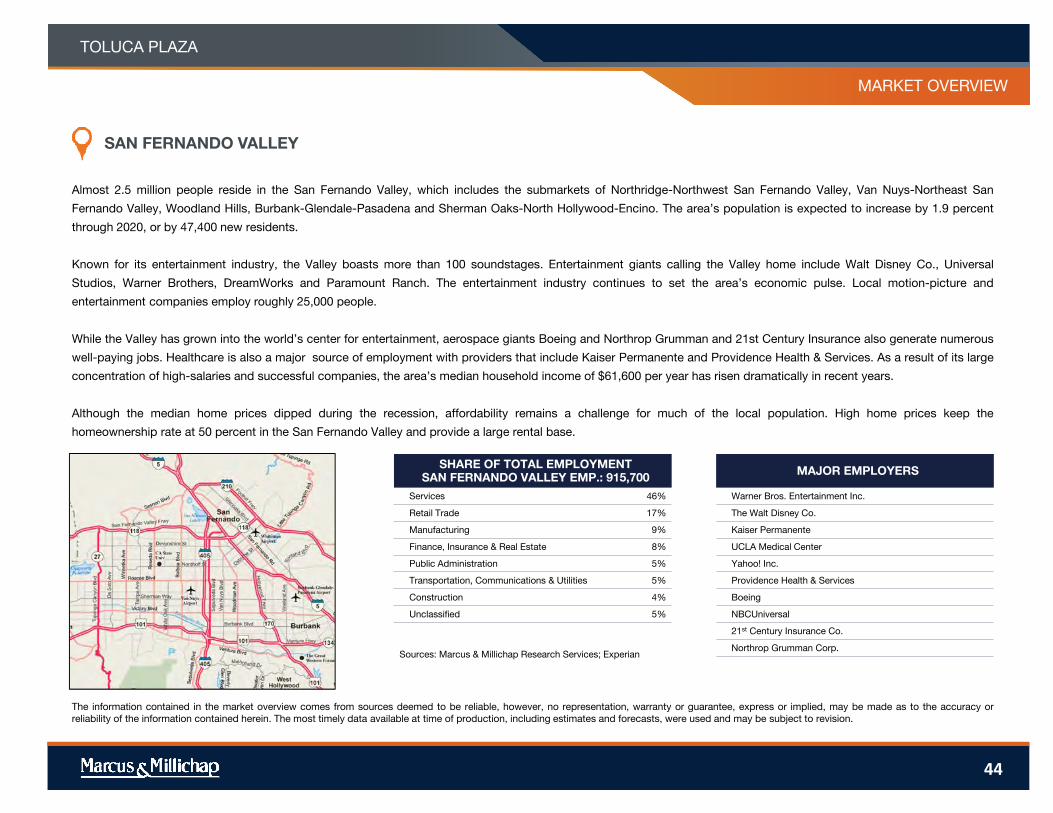

Almost 2.5 million people reside in the San Fernando Valley, which includes the submarkets of Northridge-Northwest San Fernando Valley, Van Nuys-Northeast San

Fernando Valley, Woodland Hills, Burbank-Glendale-Pasadena and Sherman Oaks-North Hollywood-Encino. The area’s population is expected to increase by 1.9 percent

through 2020, or by 47,400 new residents.

Known for its entertainment industry, the Valley boasts more than 100 soundstages. Entertainment giants calling the Valley home include Walt Disney Co., Universal

Studios, Warner Brothers, DreamWorks and Paramount Ranch. The entertainment industry continues to set the area’s economic pulse. Local motion-picture and

entertainment companies employ roughly 25,000 people.

While the Valley has grown into the world’s center for entertainment, aerospace giants Boeing and Northrop Grumman and 21st Century Insurance also generate numerous

well-paying jobs. Healthcare is also a major source of employment with providers that include Kaiser Permanente and Providence Health & Services. As a result of its large

concentration of high-salaries and successful companies, the area’s median household income of $61,600 per year has risen dramatically in recent years.

Although the median home prices dipped during the recession, affordability remains a challenge for much of the local population. High home prices keep the

homeownership rate at 50 percent in the San Fernando Valley and provide a large rental base.

MAJOR EMPLOYERS

Warner Bros. Entertainment Inc.

The Walt Disney Co.

Kaiser Permanente

UCLA Medical Center

Yahoo! Inc.

Providence Health & Services

Boeing

NBCUniversal

21st Century Insurance Co.

Northrop Grumman Corp.Sources: Marcus & Millichap Research Services; Experian

SAN FERNANDO VALLEY

TOLUCA PLAZA

SHARE OF TOTAL EMPLOYMENTSAN FERNANDO VALLEY EMP.: 915,700

Services 46%

Retail Trade 17%

Manufacturing 9%

Finance, Insurance & Real Estate 8%

Public Administration 5%

Transportation, Communications & Utilities 5%

Construction 4%

Unclassified 5%

The information contained in the market overview comes from sources deemed to be reliable, however, no representation, warranty or guarantee, express or implied, may be made as to the accuracy or

reliability of the information contained herein. The most timely data available at time of production, including estimates and forecasts, were used and may be subject to revision.

44

MARKET OVERVIEW

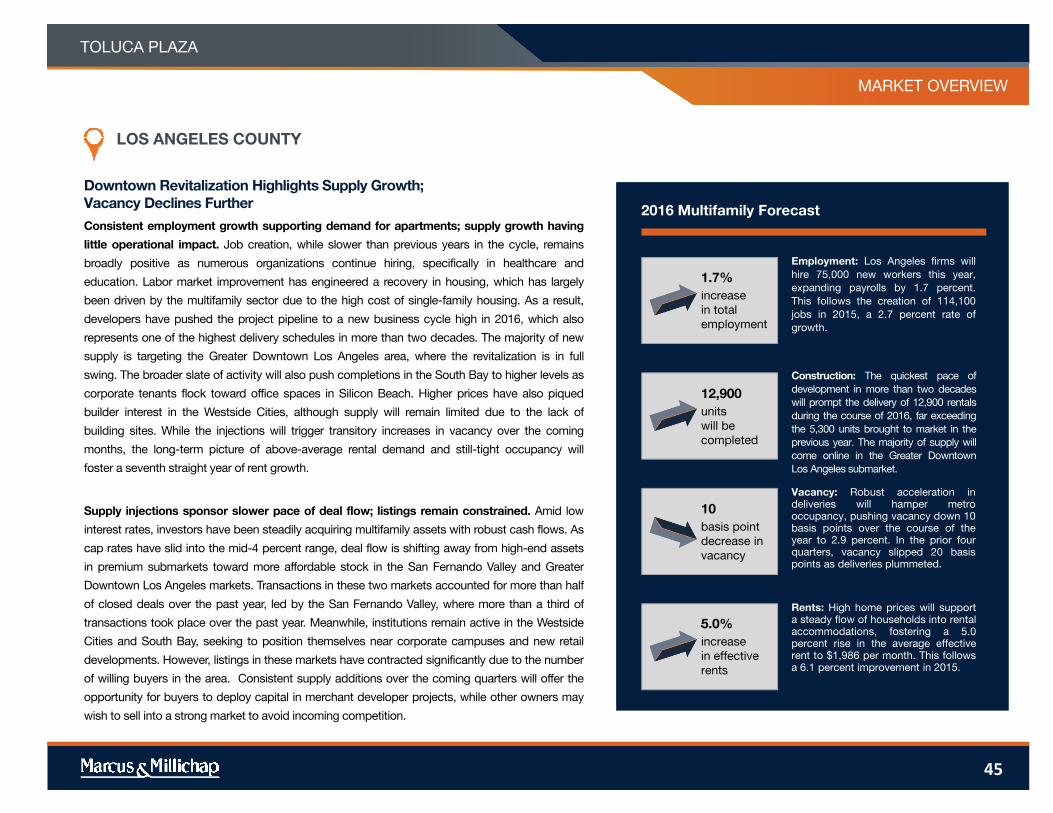

2016 Multifamily Forecast

Construction: The quickest pace of

development in more than two decades

will prompt the delivery of 12,900 rentals

during the course of 2016, far exceeding

the 5,300 units brought to market in the

previous year. The majority of supply will

come online in the Greater Downtown

Los Angeles submarket.

Vacancy: Robust acceleration indeliveries will hamper metrooccupancy, pushing vacancy down 10basis points over the course of theyear to 2.9 percent. In the prior fourquarters, vacancy slipped 20 basispoints as deliveries plummeted.

Rents: High home prices will supporta steady flow of households into rentalaccommodations, fostering a 5.0percent rise in the average effectiverent to $1,986 per month. This followsa 6.1 percent improvement in 2015.

Employment: Los Angeles firms will

hire 75,000 new workers this year,

expanding payrolls by 1.7 percent.

This follows the creation of 114,100

jobs in 2015, a 2.7 percent rate of

growth.

TOLUCA PLAZA

45

Downtown Revitalization Highlights Supply Growth;

Vacancy Declines Further

Consistent employment growth supporting demand for apartments; supply growth having

little operational impact. Job creation, while slower than previous years in the cycle, remains

broadly positive as numerous organizations continue hiring, specifically in healthcare and

education. Labor market improvement has engineered a recovery in housing, which has largely

been driven by the multifamily sector due to the high cost of single-family housing. As a result,

developers have pushed the project pipeline to a new business cycle high in 2016, which also

represents one of the highest delivery schedules in more than two decades. The majority of new

supply is targeting the Greater Downtown Los Angeles area, where the revitalization is in full

swing. The broader slate of activity will also push completions in the South Bay to higher levels as

corporate tenants flock toward office spaces in Silicon Beach. Higher prices have also piqued

builder interest in the Westside Cities, although supply will remain limited due to the lack of

building sites. While the injections will trigger transitory increases in vacancy over the coming

months, the long-term picture of above-average rental demand and still-tight occupancy will

foster a seventh straight year of rent growth.

Supply injections sponsor slower pace of deal flow; listings remain constrained. Amid low

interest rates, investors have been steadily acquiring multifamily assets with robust cash flows. As

cap rates have slid into the mid-4 percent range, deal flow is shifting away from high-end assets

in premium submarkets toward more affordable stock in the San Fernando Valley and Greater

Downtown Los Angeles markets. Transactions in these two markets accounted for more than half

of closed deals over the past year, led by the San Fernando Valley, where more than a third of

transactions took place over the past year. Meanwhile, institutions remain active in the Westside

Cities and South Bay, seeking to position themselves near corporate campuses and new retail

developments. However, listings in these markets have contracted significantly due to the number

of willing buyers in the area. Consistent supply additions over the coming quarters will offer the

opportunity for buyers to deploy capital in merchant developer projects, while other owners may

wish to sell into a strong market to avoid incoming competition.

1.7%

increase

in total

employment

12,900

units

will be

completed

10

basis point

decrease in

vacancy

increase

in effective

rents

5.0%

LOS ANGELES COUNTY

MARKET OVERVIEW

Economy

Housing and Demographics

** Trailing 12 months through 3Q

Sources: Marcus & Millichap Research Services; Economy.com; NAR

* Forecast

Sources: Marcus & Millichap Research Services; Bureau of Labor

Statistics; Economy.com

LOS ANGELES COUNTY

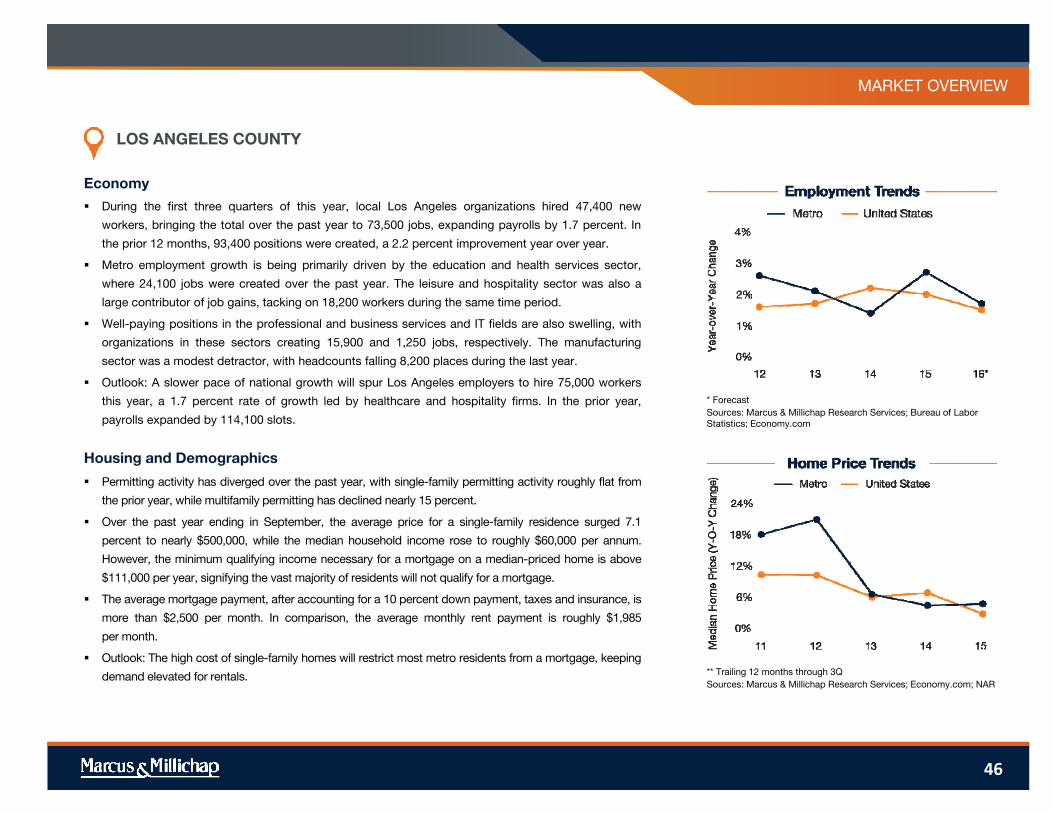

Permitting activity has diverged over the past year, with single-family permitting activity roughly flat from

the prior year, while multifamily permitting has declined nearly 15 percent.

Over the past year ending in September, the average price for a single-family residence surged 7.1

percent to nearly $500,000, while the median household income rose to roughly $60,000 per annum.

However, the minimum qualifying income necessary for a mortgage on a median-priced home is above

$111,000 per year, signifying the vast majority of residents will not qualify for a mortgage.

The average mortgage payment, after accounting for a 10 percent down payment, taxes and insurance, is

more than $2,500 per month. In comparison, the average monthly rent payment is roughly $1,985

per month.

Outlook: The high cost of single-family homes will restrict most metro residents from a mortgage, keeping

demand elevated for rentals.

During the first three quarters of this year, local Los Angeles organizations hired 47,400 new

workers, bringing the total over the past year to 73,500 jobs, expanding payrolls by 1.7 percent. In

the prior 12 months, 93,400 positions were created, a 2.2 percent improvement year over year.

Metro employment growth is being primarily driven by the education and health services sector,

where 24,100 jobs were created over the past year. The leisure and hospitality sector was also a

large contributor of job gains, tacking on 18,200 workers during the same time period.

Well-paying positions in the professional and business services and IT fields are also swelling, with

organizations in these sectors creating 15,900 and 1,250 jobs, respectively. The manufacturing

sector was a modest detractor, with headcounts falling 8,200 places during the last year.

Outlook: A slower pace of national growth will spur Los Angeles employers to hire 75,000 workers

this year, a 1.7 percent rate of growth led by healthcare and hospitality firms. In the prior year,

payrolls expanded by 114,100 slots.

46

MARKET OVERVIEW

Construction

Vacancy

* Forecast

Sources: Marcus & Millichap Research Services; MPF Research

* Forecast

Sources: Marcus & Millichap Research Services; MPF Research

LOS ANGELES COUNTY

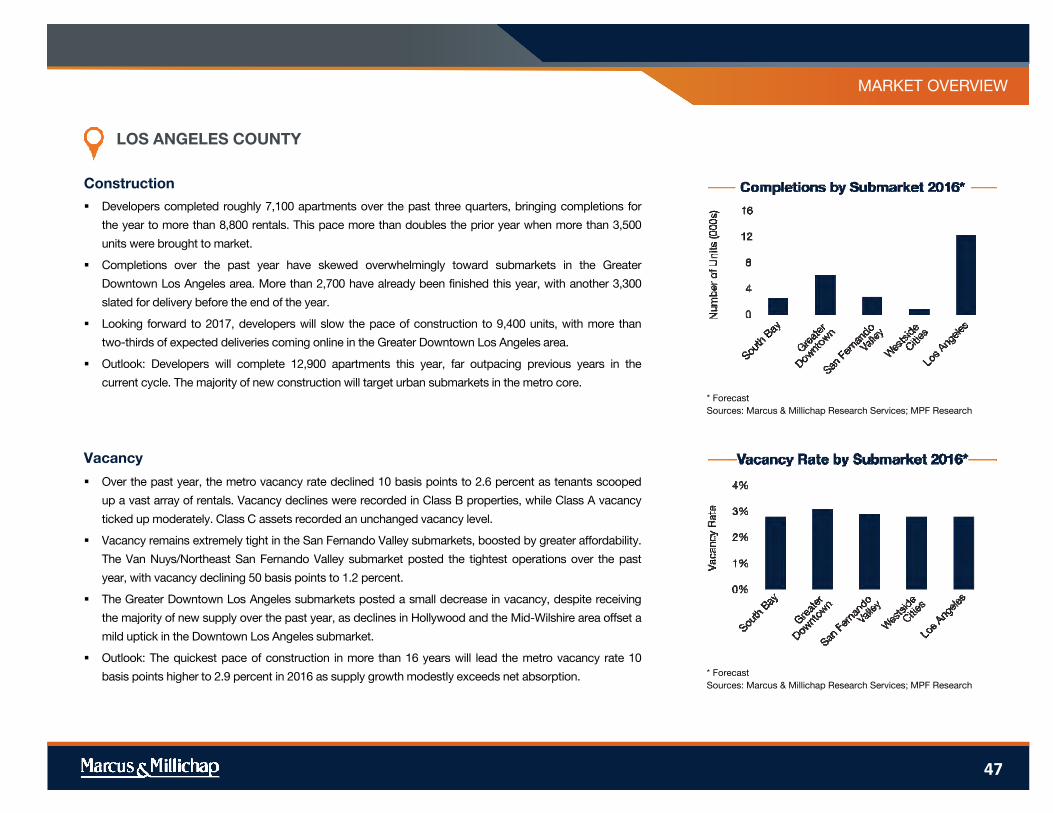

Over the past year, the metro vacancy rate declined 10 basis points to 2.6 percent as tenants scooped

up a vast array of rentals. Vacancy declines were recorded in Class B properties, while Class A vacancy

ticked up moderately. Class C assets recorded an unchanged vacancy level.

Vacancy remains extremely tight in the San Fernando Valley submarkets, boosted by greater affordability.

The Van Nuys/Northeast San Fernando Valley submarket posted the tightest operations over the past

year, with vacancy declining 50 basis points to 1.2 percent.

The Greater Downtown Los Angeles submarkets posted a small decrease in vacancy, despite receiving

the majority of new supply over the past year, as declines in Hollywood and the Mid-Wilshire area offset a

mild uptick in the Downtown Los Angeles submarket.

Outlook: The quickest pace of construction in more than 16 years will lead the metro vacancy rate 10

basis points higher to 2.9 percent in 2016 as supply growth modestly exceeds net absorption.

Developers completed roughly 7,100 apartments over the past three quarters, bringing completions for

the year to more than 8,800 rentals. This pace more than doubles the prior year when more than 3,500

units were brought to market.

Completions over the past year have skewed overwhelmingly toward submarkets in the Greater

Downtown Los Angeles area. More than 2,700 have already been finished this year, with another 3,300

slated for delivery before the end of the year.

Looking forward to 2017, developers will slow the pace of construction to 9,400 units, with more than

two-thirds of expected deliveries coming online in the Greater Downtown Los Angeles area.

Outlook: Developers will complete 12,900 apartments this year, far outpacing previous years in the

current cycle. The majority of new construction will target urban submarkets in the metro core.

47

MARKET OVERVIEW

Rents

Sales Trends

** Trailing 12 months through 3Q

Sources: Marcus & Millichap Research Services; CoStar Group, Inc.;

Real Capital Analytics

* Forecast

Sources: Marcus & Millichap Research Services; MPF Research

LOS ANGELES COUNTY

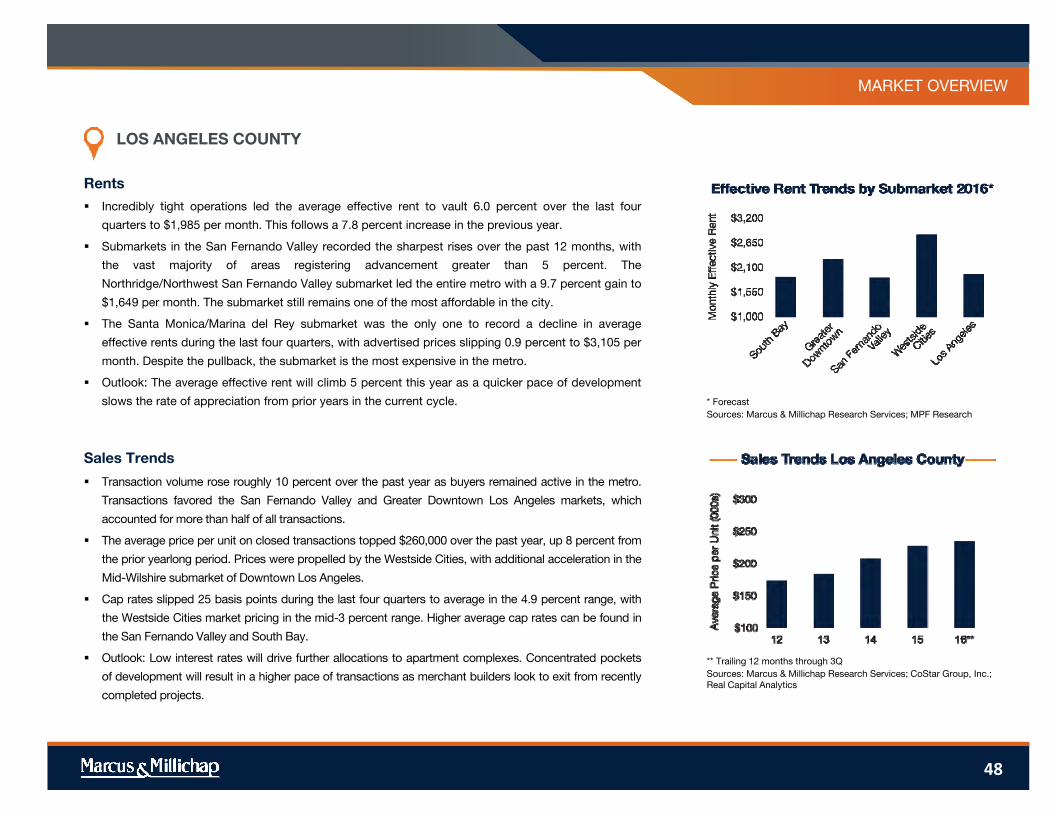

Transaction volume rose roughly 10 percent over the past year as buyers remained active in the metro.

Transactions favored the San Fernando Valley and Greater Downtown Los Angeles markets, which

accounted for more than half of all transactions.

The average price per unit on closed transactions topped $260,000 over the past year, up 8 percent from

the prior yearlong period. Prices were propelled by the Westside Cities, with additional acceleration in the

Mid-Wilshire submarket of Downtown Los Angeles.

Cap rates slipped 25 basis points during the last four quarters to average in the 4.9 percent range, with

the Westside Cities market pricing in the mid-3 percent range. Higher average cap rates can be found in

the San Fernando Valley and South Bay.

Outlook: Low interest rates will drive further allocations to apartment complexes. Concentrated pockets

of development will result in a higher pace of transactions as merchant builders look to exit from recently

completed projects.

Incredibly tight operations led the average effective rent to vault 6.0 percent over the last four

quarters to $1,985 per month. This follows a 7.8 percent increase in the previous year.

Submarkets in the San Fernando Valley recorded the sharpest rises over the past 12 months, with

the vast majority of areas registering advancement greater than 5 percent. The

Northridge/Northwest San Fernando Valley submarket led the entire metro with a 9.7 percent gain to

$1,649 per month. The submarket still remains one of the most affordable in the city.

The Santa Monica/Marina del Rey submarket was the only one to record a decline in average

effective rents during the last four quarters, with advertised prices slipping 0.9 percent to $3,105 per

month. Despite the pullback, the submarket is the most expensive in the metro.

Outlook: The average effective rent will climb 5 percent this year as a quicker pace of development

slows the rate of appreciation from prior years in the current cycle.

48

MARKET OVERVIEW

Construction and Vacancy

Rents

* Forecast

Sources: Marcus & Millichap Research Services; MPF Research

* Forecast

Sources: Marcus & Millichap Research Services; MPF Research

GREATER DOWNTOWN LOS ANGELES MARKET

LOS ANGELES COUNTY

Over the past year, greater competition for available units pushed up rental rates more than 5.0 percent to

$2,281 per month. In the previous yearlong period, average effective rent climbed 6.5 percent.

Rent gains were led by the Mid-Wilshire submarket, which recorded growth of 7.1 percent to $2,295 per

month on average. The Downtown Los Angeles submarket also performed well, tacking on 4.3 percent to

$2,251 per month. The Hollywood submarket lagged the average, swelling 3.1 percent to $2,277

per month.

Growth in average effective rents was primarily driven by Class A properties, while modest downturns

were recorded in Class B and C buildings. Class A appreciation was primarily driven by assets in

Downtown Los Angeles and Hollywood, registering growth of 11.1 percent to $2,650 per month and 8.9

percent to $2,511 per month, respectively.

Outlook: Rent growth will moderate over the coming year as supply increases are worked through,

prompting a mid-single-digit rise in average effective rent.

During the first three quarters of 2016, developers completed more than 2,770 rentals, bringing

construction to more than 3,000 units. The majority of the new units targeted sites inside the Downtown

Los Angeles submarket.

Developers will complete another 3,300 rentals in the Greater Downtown Los Angeles market before

year-end. The largest project underway, G12, located at 1200 Grand Ave., will contain 347 apartments in

a seven-story building.

The market vacancy rate ticked marginally tighter over the past year as a slight uptick in vacancy in

Downtown Los Angeles was offset by declines in the Mid-Wilshire and Hollywood neighborhoods. While

vacancy in the Mid-Wilshire and Hollywood submarkets is 2.0 percent, Downtown Los Angeles is

currently registering 3.9 percent.

Outlook: Developers will complete roughly 6,100 units this year, far exceeding the previous year’s pace of

more than 1,900 rentals. Vacancy will tick up slightly through year-end as construction accelerates.

49

MARKET OVERVIEW

Sales Trends

** Trailing 12 months through 3Q

Sources: Marcus & Millichap Research Services; MPF Research

GREATER DOWNTOWN LOS ANGELES MARKET

LOS ANGELES COUNTY

Sales volume surged more than 30 percent over the past year as investors allocated assets ahead of

several major mixed-use projects that will bring thousands of new residents into the market.

Along with greater investor interest, the average price per unit on closed deals exceeded $240,000, down

roughly $10,000 per door from the prior year. Higher-than-average prices were paid in the Mid-Wilshire

and West Hollywood areas.

Significant buyer activity pushed the average cap rate into the 4.2 percent range, down roughly 25 basis

points from the previous year as investor interest was unfazed by greater anticipated deliveries.

Outlook: Complexes near major shopping or event centers will garner significant interest from investors.

Mixed-use offerings with ground-floor retail will also see bidders as operators seek to diversify cash flows.

50

MARKET OVERVIEW

Construction and Vacancy

Rents

* Forecast

Sources: Marcus & Millichap Research Services; MPF Research

* Forecast

Sources: Marcus & Millichap Research Services; MPF Research

WESTSIDE CITIES MARKET

LOS ANGELES COUNTY

The Westside Cities market’s pricing power is rising as tenants seek out luxury apartments in coveted

neighborhoods. During the last year, the average effective rent rose 3.2 percent to $2,900 per month.

The Santa Monica/Marina del Rey submarket slipped 0.9 percent to $3,105 per month.

Rent performance was overwhelmingly driven by the Palms/Mar Vista and Brentwood/Westwood/Beverly

Hills submarkets, which recorded average effective rent growth of 6.5 percent to $2,428 per month and

5.0 percent to $3,036 per month, respectively.

While Class A properties registered tremendous rent increases, Class B assets struggled. Class A

product in Brentwood/Westwood/Beverly Hills tacked on 6.1 percent to $3,152 per month, while Class B

rental rates declined 17.9 percent to $1,925 per month.

Outlook: Average effective rents will expand 4 percent to $2,890 per month by year-end as tenants

migrate toward new apartments being constructed in the area.

Over the past four quarters, developers placed 722 rentals into service in the Westside Cities market,

slowing the pace of completions significantly from the previous year when 460 units were delivered.

Builders focused primarily on the Brentwood/Westwood/Beverly Hills and Palms/Mar Vista submarkets,

with all year-to-date completions coming to market in these two places. The Santa Monica/Marina del

Rey submarket will receive just 76 units this year.

Vacancy rose broadly across the market over the past year as higher prices prompted marginal tenant

outflows. The Palms/Mar Vista submarket was most affected, with vacancy increasing 50 basis points to

2.4 percent, while Brentwood/Westwood/Beverly Hills and Santa Monica/Marina del Rey were

unchanged and up 20 basis points, respectively.

Outlook: Developers will complete nearly 870 rentals this year as construction rebounds throughout the

county. As a result, the Westside Cities market vacancy rate will rise 30 basis points to 3.6 percent

by year-end.

51

MARKET OVERVIEW

Sales Trends

** Trailing 12 months through 3Q

Sources: Marcus & Millichap Research Services; MPF Research

WESTSIDE CITIES MARKET

LOS ANGELES COUNTY

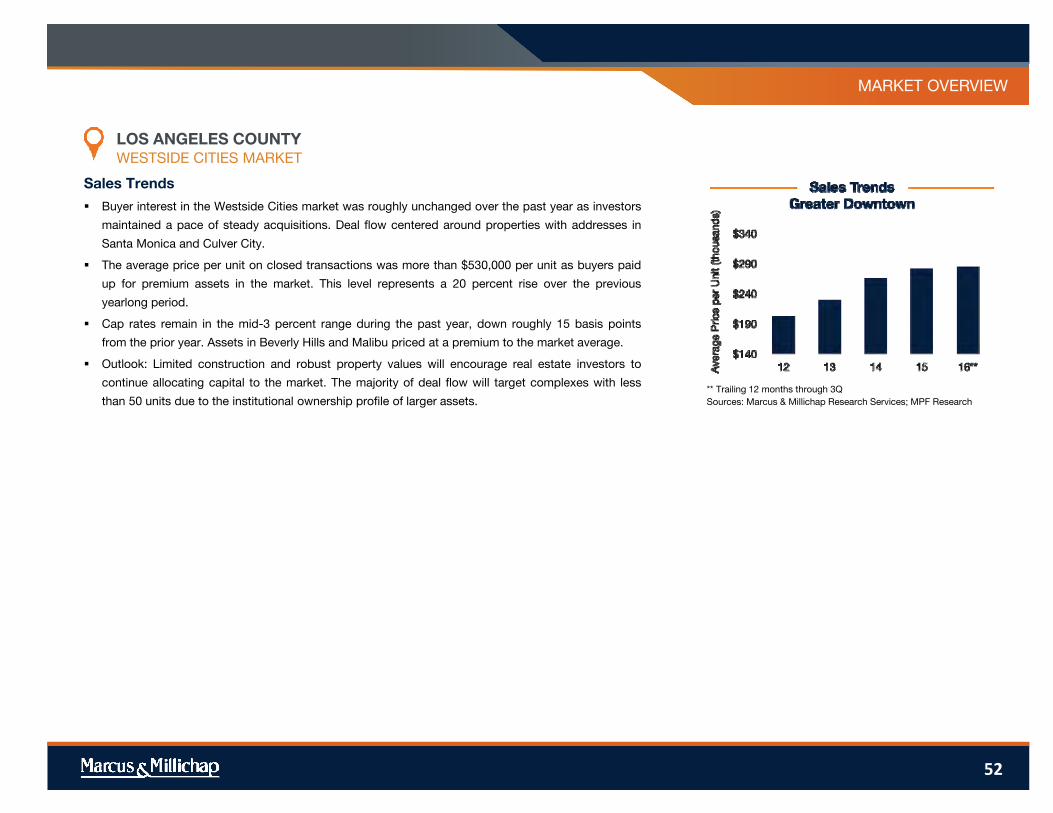

Buyer interest in the Westside Cities market was roughly unchanged over the past year as investors

maintained a pace of steady acquisitions. Deal flow centered around properties with addresses in

Santa Monica and Culver City.

The average price per unit on closed transactions was more than $530,000 per unit as buyers paid

up for premium assets in the market. This level represents a 20 percent rise over the previous

yearlong period.

Cap rates remain in the mid-3 percent range during the past year, down roughly 15 basis points

from the prior year. Assets in Beverly Hills and Malibu priced at a premium to the market average.

Outlook: Limited construction and robust property values will encourage real estate investors to

continue allocating capital to the market. The majority of deal flow will target complexes with less

than 50 units due to the institutional ownership profile of larger assets.

52

MARKET OVERVIEW

Construction and Vacancy

Rents

* Forecast

Sources: Marcus & Millichap Research Services; MPF Research

* Forecast

Sources: Marcus & Millichap Research Services; MPF Research

SAN FERNANDO VALLEY/TRI-CITIES MARKET

LOS ANGELES COUNTY

The average effective rent soared 6.9 percent over the past year to $1,865 per month as tenant demand

was roughly in line with deliveries. The Northridge/Northwest San Fernando Valley submarket recorded

the largest increase, up 9.7 percent to $1,649 per month.

All submarkets in the San Fernando Valley posted rent increases above 4.0 percent. While the

Northridge/Northwest San Fernando Valley submarket posted the biggest gain, the Van Nuys/Northeast

San Fernando Valley submarket rose 8.6 percent to $1,562 per month, contributing to strong

market performance.

The Van Nuys/Northeast San Fernando Valley submarket remains the most affordable in the San

Fernando Valley, contributing to strong rent performance even as supply growth accelerated.

Outlook: One of the most affordable markets in Los Angeles County will continue to draw renters to the

market, fostering a high-single-digit average effective rent growth over the coming year. Increased supply

will do little to halt this trend, prompting tighter vacancy in the months ahead.

Over the past four quarters, builders completed 1,500 units in the market, with the majority of

construction in the Van Nuys/Northeast San Fernando Valley submarket, where more than 790

rentals were brought to market.

Construction will remain elevated through year-end, with more than 1,600 apartments slated for

delivery. Developers will shift their emphasis to Burbank/Glendale/Pasadena submarket, where

1,480 units are underway. Altana I in Glendale is the largest project with 507 rentals.

Operational performance in the market was bifurcated, with vacancy contracting based on strong

performance in the Woodland Hills and Van Nuys/NE San Fernando Valley submarkets. The

submarkets posted vacancy declines of 30 basis points to 2.8 percent and 50 basis points to

1.2 percent.

Outlook: Completions will exceed 2,700 rentals this year as development ramps up in the market. As

a result, vacancy will be unchanged at 3.3 percent.

53

MARKET OVERVIEW

Sales Trends

** Trailing 12 months through 3Q

Sources: Marcus & Millichap Research Services; MPF Research

SAN FERNANDO VALLEY/TRI-CITIES MARKET

LOS ANGELES COUNTY

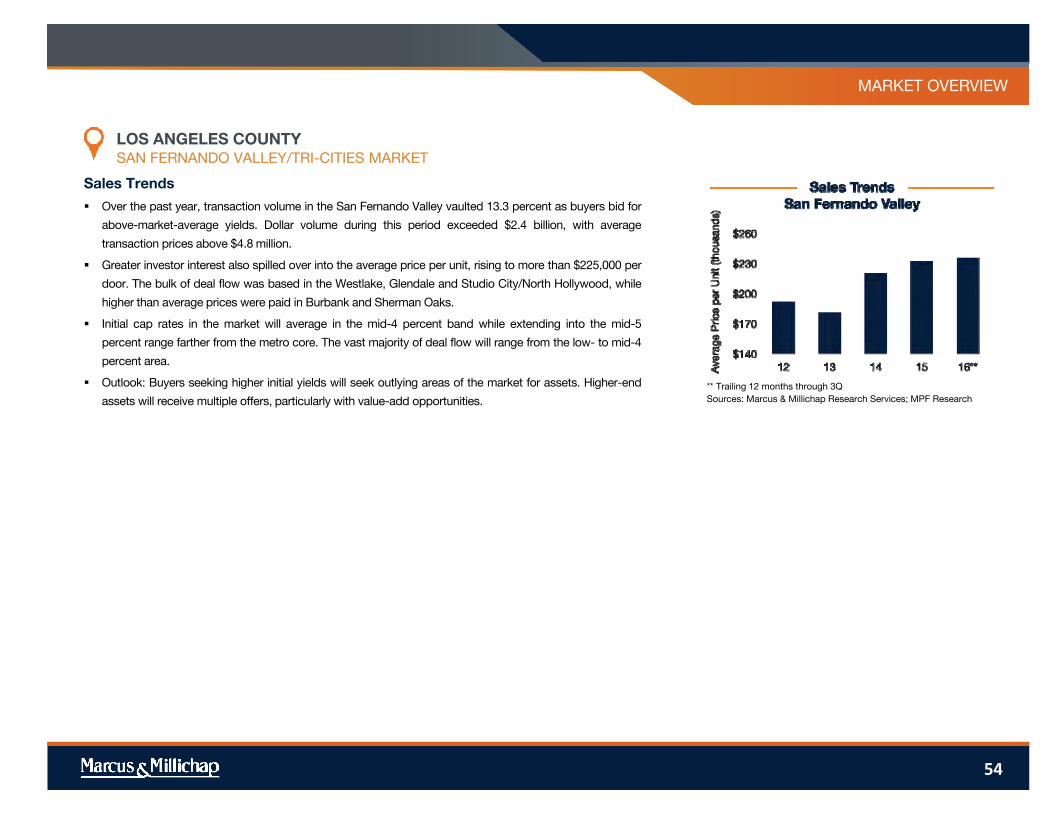

Over the past year, transaction volume in the San Fernando Valley vaulted 13.3 percent as buyers bid for

above-market-average yields. Dollar volume during this period exceeded $2.4 billion, with average

transaction prices above $4.8 million.

Greater investor interest also spilled over into the average price per unit, rising to more than $225,000 per

door. The bulk of deal flow was based in the Westlake, Glendale and Studio City/North Hollywood, while

higher than average prices were paid in Burbank and Sherman Oaks.

Initial cap rates in the market will average in the mid-4 percent band while extending into the mid-5

percent range farther from the metro core. The vast majority of deal flow will range from the low- to mid-4

percent area.

Outlook: Buyers seeking higher initial yields will seek outlying areas of the market for assets. Higher-end

assets will receive multiple offers, particularly with value-add opportunities.

54

MARKET OVERVIEW

Construction and Vacancy

Rents

* Forecast

Sources: Marcus & Millichap Research Services; MPF Research

* Forecast

Sources: Marcus & Millichap Research Services; MPF Research

SOUTH BAY/LONG BEACH MARKET

LOS ANGELES COUNTY

Surging supply growth limited the growth in average effective rents this year, rising 3.6 percent to more

than $1,900 per month. Both submarkets performed nearly identically, driven by Class A and B product.

The Long Beach submarket, benefiting from a slower pace of development, posted considerable growth

in Class A buildings, where average effective rents soared 7.7 percent to $2,308 per month. Class B

assets also benefited, swelling 8.4 percent to $1,692 per month.

South Bay assets performed incredibly well, even as construction reached the highest pace in over a

decade. Class A buildings, weighed down by pressure from new offerings, tacked on 3.4 percent to

$2,624 per month. Class B buildings bucked this trend, vaulting 8 percent to $1,992 per month.

Outlook: The influx of multiple large corporations such as Google and Snapchat to Silicon Beach will

trigger greater demand for apartments, leading the average effective rent to advance in the mid-single-

digit range.

During the last 12 months, developers completed 2,750 apartments, with the majority of the new supply

coming online in the South Bay. Less than 500 of these rentals were delivered in Long Beach.

The biggest complexes brought to market over the past year are highlighted by the two stages of the

Villas at Playa Vista and Altitude. The projects contain nearly 1,200 and 545 rentals, respectively.

Despite considerable development over the last four quarters, vacancy has moderately tightened during

this period. A minor increase in vacancy in the South Bay was offset by a sharp drop in Long Beach,

which was primarily driven by robust supply growth rather than a slowdown in demand.

Outlook: Rising construction will be offset by elevated net absorption, leading vacancy to slip marginally

through 2016. A slower pace of development next year will also boost local operations.

55

MARKET OVERVIEW

Sales Trends

** Trailing 12 months through 3Q

Sources: Marcus & Millichap Research Services; MPF Research

SOUTH BAY/LONG BEACH MARKET

LOS ANGELES COUNTY

Investor appetite is soaring in the market, with closed transactions up more than 30 percent over the past

year. Deal flow is widespread, with concentrations in Hawthorne and Long Beach. More than half of all

transactions were in these two cities.

The average price of properties that exchanged ownership over the last year rose 3.7 percent to more

than $190,000 per door. Several complexes in El Segundo and Redondo Beach traded well above the

average, while below-average prices were paid in Manhattan Beach and Hermosa Beach.

Greater investor interest in the market fostered a shrinkage in first-year yields, which were roughly

unchanged in the high-4 percent band. Cap rates can range from the mid-3 percent band to the mid-5

percent range, depending on asset quality and location.

Outlook: A rising corporate presence, coupled with robust market operations, will encourage investors to

deploy more capital. Assets near shopping destinations and major freeways will be in high demand.

56

MARKET OVERVIEW

Capital Markets

LOS ANGELES COUNTY

57

Submarket Vacancy Ranking

Rank SubmarketVacancy

Rate

Y-O-Y bps

Change

Effective Rents

Y-O-Y % Change

1 East Los Angeles 0.7% 180 $1,346 10.1%

2Van Nuys/NE San Fernando

Valley1.2% 50 $1,562 8.6%

3 South San Gabriel Valley 1.5% 250 $1,567 7.8%

4 Southeast Los Angeles 1.8% 50 $1,548 7.9%

5 Mid-Wilshire 2.0% 20 $2,295 7.1%

6 Hollywood 2.0% 60 $2,277 3.1%

7 Long Beach 2.1% 50 $1,673 3.3%

8Brentwood/Westwood/Bever

ly Hills2.3% 0 $3,036 5.0%

9Northridge/NW San

Fernando Valley2.3% -30 $1,649 9.7%

10 Palms/Mar Vista 2.4% -50 $2,428 6.5%

11 South Los Angeles 2.5% -110 $1,453 2.4%

12 South Bay 2.7% -10 $2,172 3.5%

13 Woodland Hills 2.8% 30 $2,116 6.8%

14 Santa Clarita Valley 2.9% 50 $1,895 8.1%

15Sherman Oaks/N

Hollywood/Encino3.0% -120 $2,098 4.6%

16Santa Monica/Marina del

Rey3.1% -20 $3,105 -0.9%

17 North San Gabriel Valley 3.2% 30 $1,478 6.5%

18 Antelope Valley 3.5% -20 $1,063 11.5%

19 Burbank/Glendale/Pasadena 3.6% -150 $2,144 6.3%

20 Downtown Los Angeles 3.9% -20 $2,251 4.3%

The initial reading of third quarter GDP of 2.9 percent and consistent growth

in employment are fanning expectations that the Federal Reserve will raise

its benchmark short-term lending rate at its December meeting. Other

economic data showing steady improvement in the housing market and the

stabilization of oil prices around $50 per barrel offer signals that the U.S.

economy is growing at a sustainable pace.

Increasing rental housing demand underpinned a decline in the U.S.

apartment vacancy rate of 60 basis points to 3.5 percent year to date

through the third quarter, the lowest level this cycle. Apartment builders

have responded to growing demand and favorable demographic trends by

ramping up construction. Completions will rise to 320,000 units this year and

peak in 2017.

Capital markets remain highly competitive, offering an assortment of fixed-

rate products available through commercial banks, life-insurance

companies, CMBS and agency lenders. Fannie Mae and Freddie Mac are

underwriting loans of 10 years at maximum leverage of 80 percent. Rates

will typically reside in the high-3 to low-4 percent range, depending on

underwriting criteria. Portfolio lenders will also price in this vicinity but will

typically require loan-to-value ratios in the 65 to 75 percent band. Floating-

rate bridge loans and financing for asset repositioning are typically

underwritten with LTVs 70 to 75 percent of stabilized value (80 to 85

percent of cost) and price 300 basis points above Libor for recourse deals

and extending to 450 basis points above Libor for

non-recourse transactions.

PROPERTY NAME

MARKETING TEAM

TOLUCA PLAZA

DEMOGRAPHICS

Source: © 2016 Experian

Created on January 2017

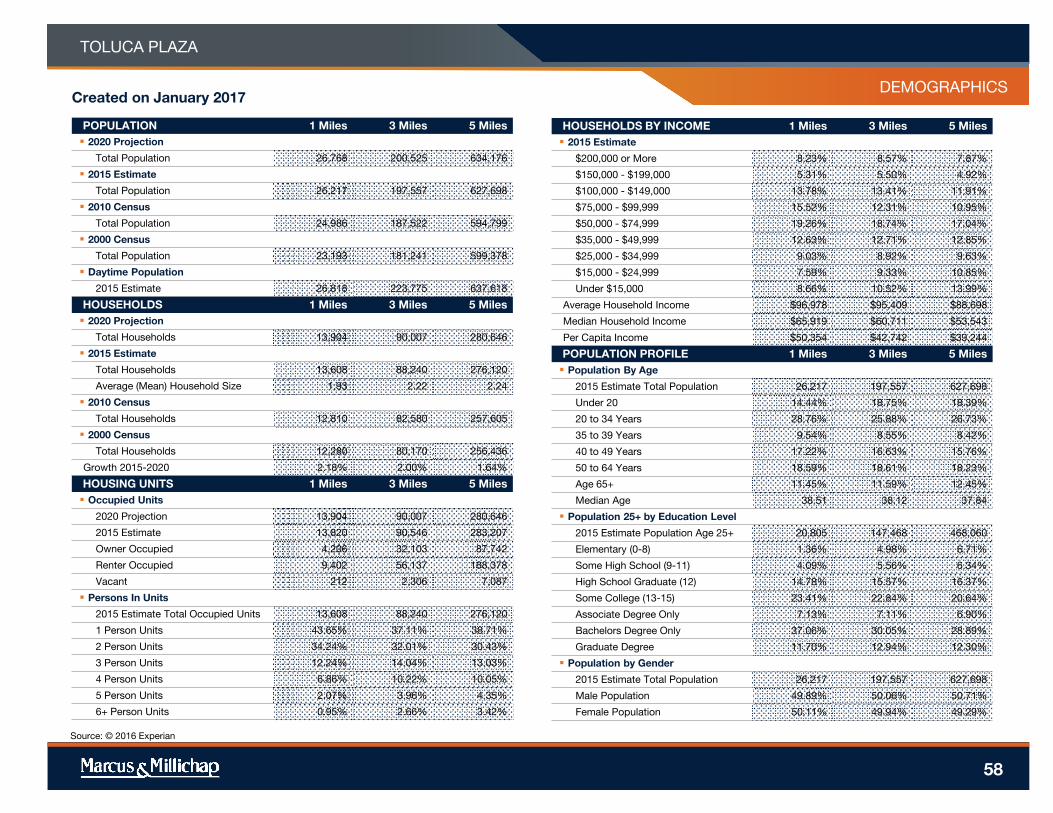

POPULATION 1 Miles 3 Miles 5 Miles

2020 Projection

Total Population 26,768 200,525 634,176

2015 Estimate

Total Population 26,217 197,557 627,698

2010 Census

Total Population 24,986 187,522 594,799

2000 Census

Total Population 23,193 181,241 599,378

Daytime Population

2015 Estimate 26,818 223,775 637,618

HOUSEHOLDS 1 Miles 3 Miles 5 Miles

2020 Projection

Total Households 13,904 90,007 280,646

2015 Estimate

Total Households 13,608 88,240 276,120

Average (Mean) Household Size 1.93 2.22 2.24

2010 Census

Total Households 12,810 82,580 257,605

2000 Census

Total Households 12,280 80,170 256,436

Growth 2015-2020 2.18% 2.00% 1.64%

HOUSING UNITS 1 Miles 3 Miles 5 Miles

Occupied Units

2020 Projection 13,904 90,007 280,646

2015 Estimate 13,820 90,546 283,207

Owner Occupied 4,206 32,103 87,742

Renter Occupied 9,402 56,137 188,378

Vacant 212 2,306 7,087

Persons In Units

2015 Estimate Total Occupied Units 13,608 88,240 276,120

1 Person Units 43.65% 37.11% 38.71%

2 Person Units 34.24% 32.01% 30.43%

3 Person Units 12.24% 14.04% 13.03%

4 Person Units 6.86% 10.22% 10.05%

5 Person Units 2.07% 3.96% 4.35%

6+ Person Units 0.95% 2.66% 3.42%

HOUSEHOLDS BY INCOME 1 Miles 3 Miles 5 Miles

2015 Estimate

$200,000 or More 8.23% 8.57% 7.87%

$150,000 - $199,000 5.31% 5.50% 4.92%

$100,000 - $149,000 13.78% 13.41% 11.91%

$75,000 - $99,999 15.52% 12.31% 10.95%

$50,000 - $74,999 19.26% 18.74% 17.04%

$35,000 - $49,999 12.63% 12.71% 12.85%

$25,000 - $34,999 9.03% 8.92% 9.63%

$15,000 - $24,999 7.59% 9.33% 10.85%

Under $15,000 8.66% 10.52% 13.99%

Average Household Income $96,978 $95,409 $88,698

Median Household Income $65,919 $60,711 $53,543

Per Capita Income $50,354 $42,742 $39,244

POPULATION PROFILE 1 Miles 3 Miles 5 Miles

Population By Age

2015 Estimate Total Population 26,217 197,557 627,698

Under 20 14.44% 18.75% 18.39%

20 to 34 Years 28.76% 25.88% 26.73%

35 to 39 Years 9.54% 8.55% 8.42%

40 to 49 Years 17.22% 16.63% 15.76%

50 to 64 Years 18.59% 18.61% 18.23%

Age 65+ 11.45% 11.59% 12.45%

Median Age 38.51 38.12 37.84

Population 25+ by Education Level

2015 Estimate Population Age 25+ 20,805 147,468 468,060

Elementary (0-8) 1.36% 4.98% 6.71%

Some High School (9-11) 4.09% 5.56% 6.34%

High School Graduate (12) 14.78% 15.57% 16.37%

Some College (13-15) 23.41% 22.84% 20.64%

Associate Degree Only 7.13% 7.11% 6.90%

Bachelors Degree Only 37.06% 30.05% 28.89%

Graduate Degree 11.70% 12.94% 12.30%

Population by Gender

2015 Estimate Total Population 26,217 197,557 627,698

Male Population 49.89% 50.06% 50.71%

Female Population 50.11% 49.94% 49.29%

58

Income

In 2016, the median household income for your selected geography is

$65,919, compare this to the US average which is currently . The

median household income for your area has changed by 33.01%

since 2000. It is estimated that the median household income in your

area will be $77,585 five years from now, which represents a change

of 17.70% from the current year.

The current year per capita income in your area is $50,354, compare

this to the US average, which is . The current year average

household income in your area is $96,978, compare this to the US

average which is .

Population

In 2016, the population in your selected geography is 26,217. The

population has changed by 13.04% since 2000. It is estimated that

the population in your area will be 26,768.00 five years from now,

which represents a change of 2.10% from the current year. The

current population is 49.89% male and 50.11% female. The median

age of the population in your area is 38.51, compare this to the US

average which is . The population density in your area is 8,343.73

people per square mile.

Households

There are currently 13,608 households in your selected geography.

The number of households has changed by 10.81% since 2000. It is

estimated that the number of households in your area will be 13,904

five years from now, which represents a change of 2.18% from the

current year. The average household size in your area is 1.93 persons.

Employment

In 2016, there are 20,366 employees in your selected area, this is also

known as the daytime population. The 2000 Census revealed that

80.74% of employees are employed in white-collar occupations in

this geography, and 19.26% are employed in blue-collar occupations.

In 2016, unemployment in this area is 8.95%. In 2000, the average

time traveled to work was 29.00 minutes.

Race and Ethnicity

The current year racial makeup of your selected area is as follows:

73.78% White, 5.59% Black, 0.07% Native American and 9.13%

Asian/Pacific Islander. Compare these to US averages which are:

White, Black, Native American and Asian/Pacific Islander. People

of Hispanic origin are counted independently of race.

People of Hispanic origin make up 18.48% of the current year

population in your selected area. Compare this to the US average of .

PROPERTY NAME

MARKETING TEAM

TOLUCA PLAZA

Housing

The median housing value in your area was $607,210 in 2016,

compare this to the US average of . In 2000, there were 4,030 owner

occupied housing units in your area and there were 8,250 renter

occupied housing units in your area. The median rent at the time was

$768.

Source: © 2016 Experian

DEMOGRAPHICS

59

www.MarcusMillichap.com

Jeff Louks

Executive Vice President Investments

Senior Director - National Multi Housing Group

Encino Office

Tel: (818) 212-2780

Fax: (818) 212-2710

License: CA 00908473

Brett Sanson

Senior Associate

Director - National Multi Housing Group

Encino Office

Tel: (818) 212-2785

Fax: (818) 212-2710

License: CA 01387480

Gayle Factor

Vice President Investments

Director - National Multi Housing Group

Encino Office

Tel: (818) 212-2756

Fax: (818) 212-2710

License: CA 01066258

P R E S E N T E D B Y

![RESEARCHARTICLE MicroRNAshsa-miR-99b,hsa-miR · PDF fileATG2A,PMEPA1, DKK3,PDCD4). ... endometriosis, cellfate decisions andangiogenesis[62–70].Hsa-miR-99b hasbeendemonstratedtotargetcomponentsofNF](https://img.pdfslide.us/doc/110x75/5a985eb07f8b9a30358d63f2/researcharticle-micrornashsa-mir-99bhsa-mir-pmepa1-dkk3pdcd4-endometriosis.jpg)