Embed Size (px)

Citation preview

US - Swiss Double Taxation Treaty

17 November 2010

Confidential

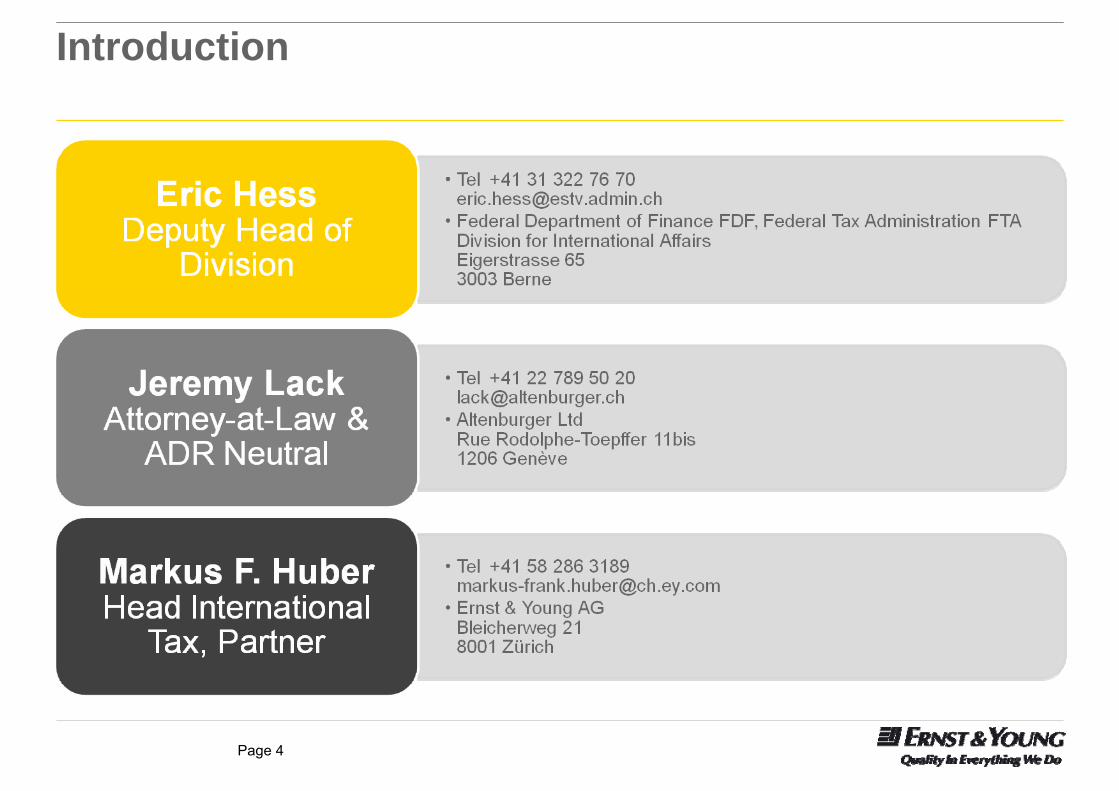

Eric Hess, Federal Tax Administration FTA

Jeremy Lack, Altenburger Ltd legal + tax

Markus F. Huber, Ernst & Young AG

Page 2

Agenda

► Introduction► Development of treaty policy► Looking back► Protocol 2009► Outlook► Closing remarks

Introduction

Page 4

Introduction

Development of Treaty Policy

Page 6

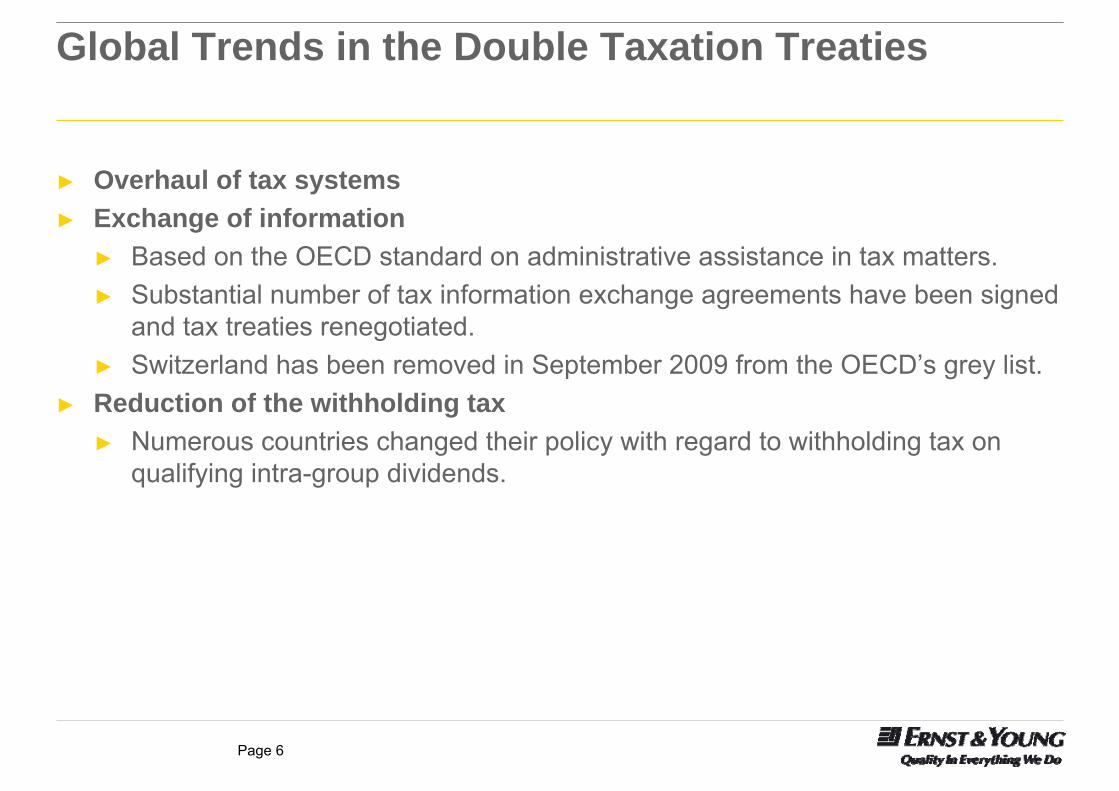

Global Trends in the Double Taxation Treaties

► Overhaul of tax systems► Exchange of information

► Based on the OECD standard on administrative assistance in tax matters.► Substantial number of tax information exchange agreements have been signed

and tax treaties renegotiated. ► Switzerland has been removed in September 2009 from the OECD’s grey list.

► Reduction of the withholding tax► Numerous countries changed their policy with regard to withholding tax on

qualifying intra-group dividends.

Page 7

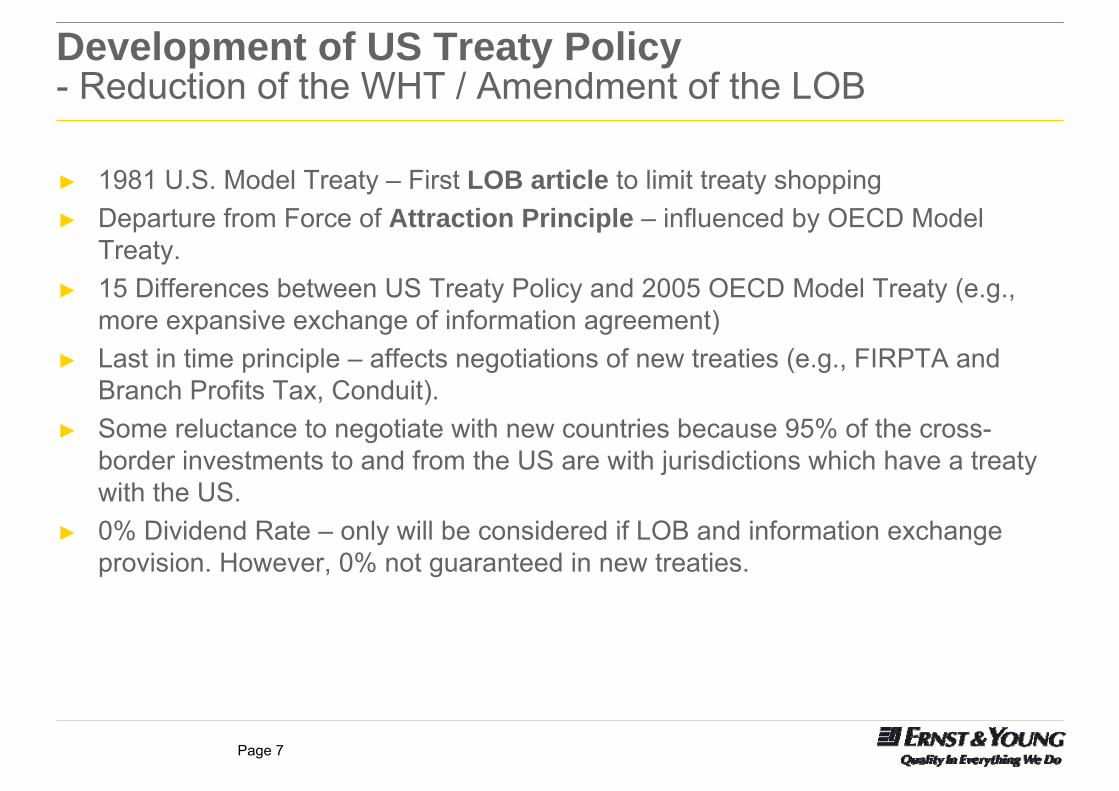

Development of US Treaty Policy- Reduction of the WHT / Amendment of the LOB

► 1981 U.S. Model Treaty – First LOB article to limit treaty shopping► Departure from Force of Attraction Principle – influenced by OECD Model

Treaty. ► 15 Differences between US Treaty Policy and 2005 OECD Model Treaty (e.g.,

more expansive exchange of information agreement)► Last in time principle – affects negotiations of new treaties (e.g., FIRPTA and

Branch Profits Tax, Conduit). ► Some reluctance to negotiate with new countries because 95% of the cross-

border investments to and from the US are with jurisdictions which have a treaty with the US.

► 0% Dividend Rate – only will be considered if LOB and information exchange provision. However, 0% not guaranteed in new treaties.

Page 8

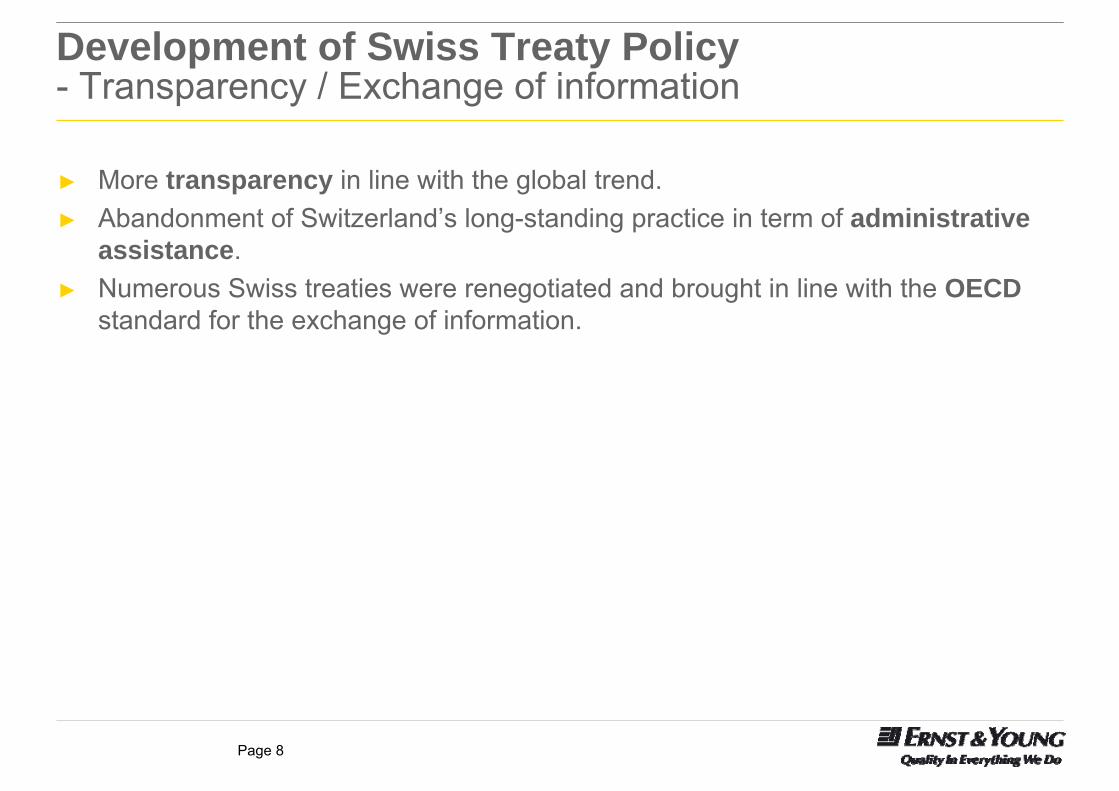

Development of Swiss Treaty Policy- Transparency / Exchange of information

► More transparency in line with the global trend.► Abandonment of Switzerland’s long-standing practice in term of administrative

assistance.► Numerous Swiss treaties were renegotiated and brought in line with the OECD

standard for the exchange of information.

Looking back

Page 10Eric Hess / Deputy Head of the International Division /

Federal Tax Administration / Berne

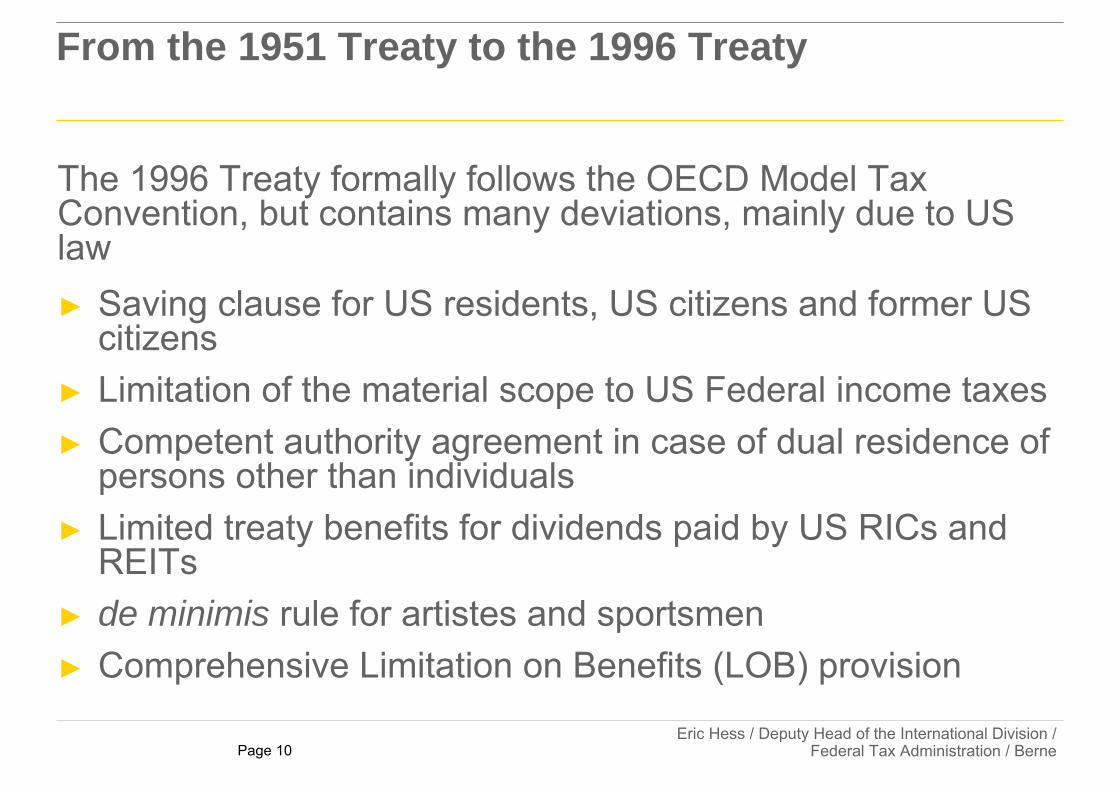

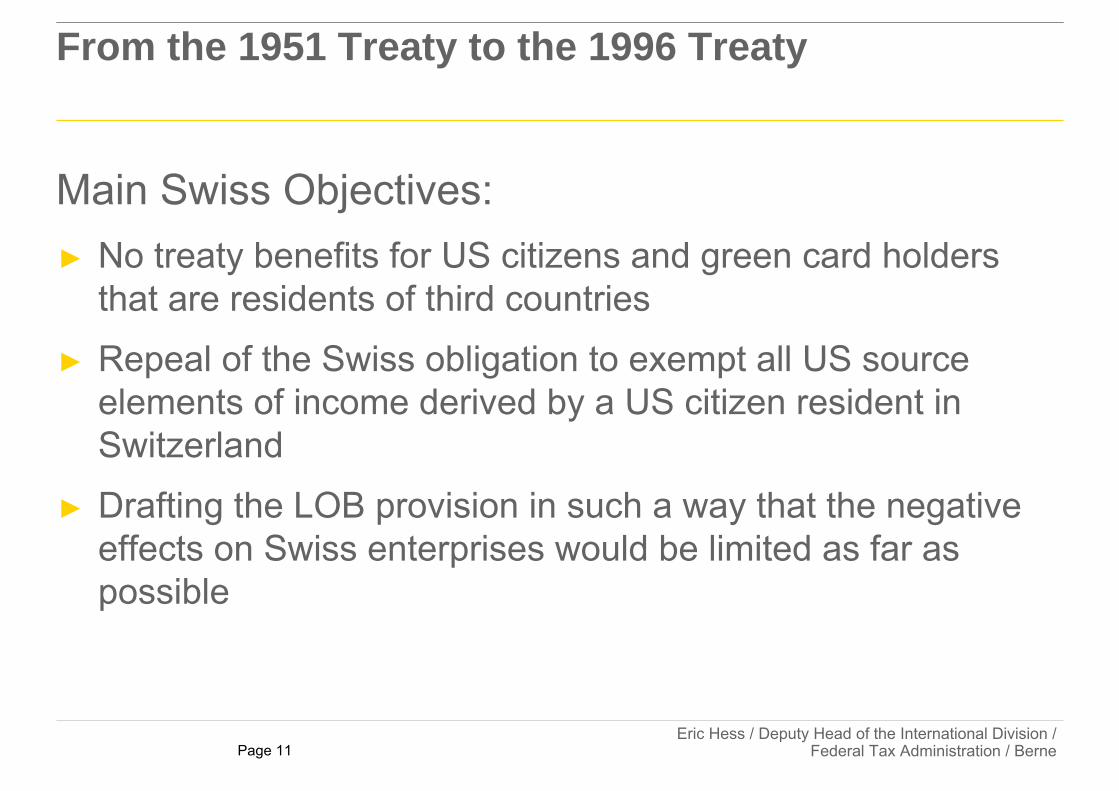

From the 1951 Treaty to the 1996 Treaty

The 1996 Treaty formally follows the OECD Model Tax Convention, but contains many deviations, mainly due to US law► Saving clause for US residents, US citizens and former US

citizens► Limitation of the material scope to US Federal income taxes► Competent authority agreement in case of dual residence of

persons other than individuals► Limited treaty benefits for dividends paid by US RICs and

REITs► de minimis rule for artistes and sportsmen► Comprehensive Limitation on Benefits (LOB) provision

Page 11Eric Hess / Deputy Head of the International Division /

Federal Tax Administration / Berne

From the 1951 Treaty to the 1996 Treaty

Main Swiss Objectives:► No treaty benefits for US citizens and green card holders

that are residents of third countries

► Repeal of the Swiss obligation to exempt all US source elements of income derived by a US citizen resident in Switzerland

► Drafting the LOB provision in such a way that the negative effects on Swiss enterprises would be limited as far as possible

Page 12 © B. Sambeth Glasner & J. Lack 2008-10. All rights reserved

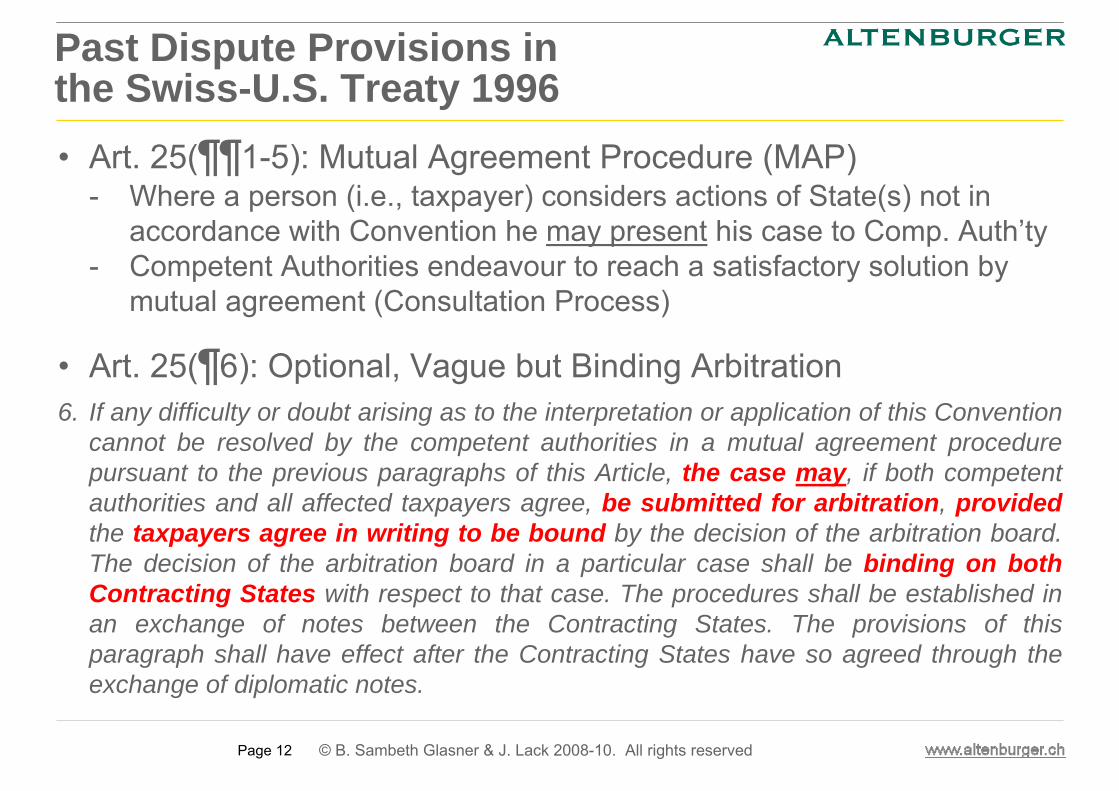

Past Dispute Provisions in the Swiss-U.S. Treaty 1996 • Art. 25(¶¶1-5): Mutual Agreement Procedure (MAP)

- Where a person (i.e., taxpayer) considers actions of State(s) not in accordance with Convention he may present his case to Comp. Auth’ty

- Competent Authorities endeavour to reach a satisfactory solution by mutual agreement (Consultation Process)

• Art. 25(¶6): Optional, Vague but Binding Arbitration6. If any difficulty or doubt arising as to the interpretation or application of this Convention

cannot be resolved by the competent authorities in a mutual agreement procedure pursuant to the previous paragraphs of this Article, the case may, if both competent authorities and all affected taxpayers agree, be submitted for arbitration, providedthe taxpayers agree in writing to be bound by the decision of the arbitration board. The decision of the arbitration board in a particular case shall be binding on both Contracting States with respect to that case. The procedures shall be established in an exchange of notes between the Contracting States. The provisions of this paragraph shall have effect after the Contracting States have so agreed through the exchange of diplomatic notes.

Protocol 2009

Page 14

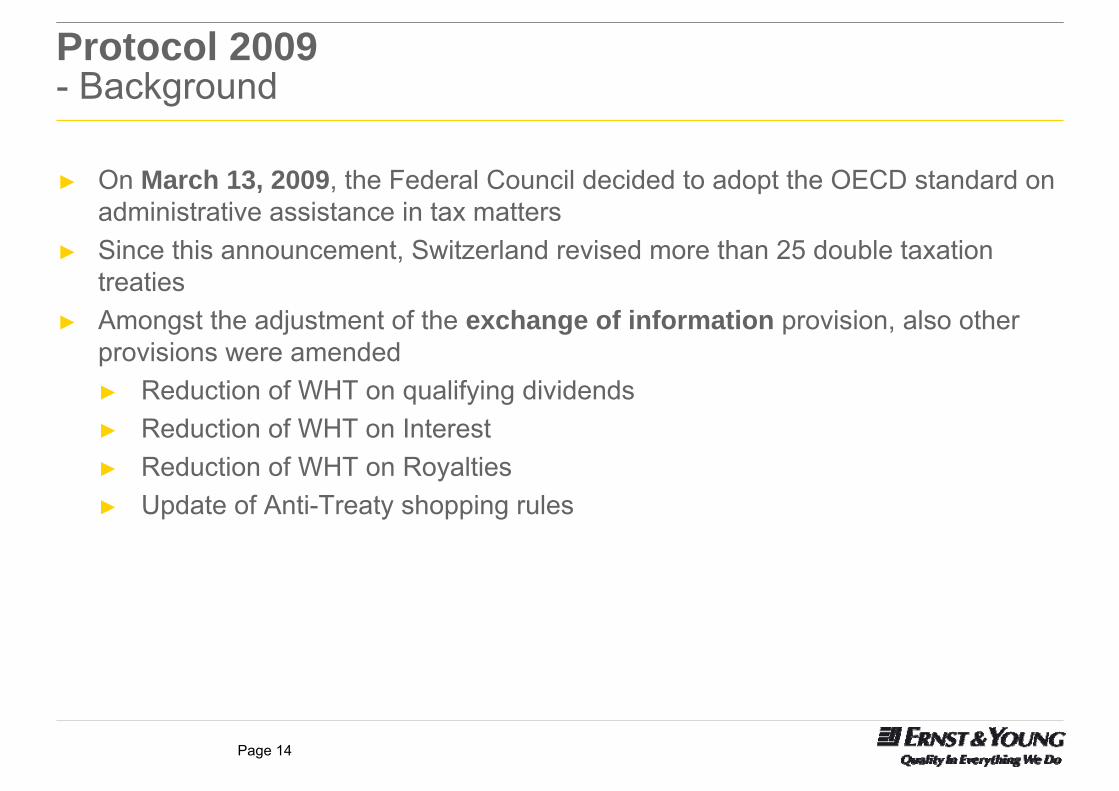

Protocol 2009- Background

► On March 13, 2009, the Federal Council decided to adopt the OECD standard on administrative assistance in tax matters

► Since this announcement, Switzerland revised more than 25 double taxation treaties

► Amongst the adjustment of the exchange of information provision, also other provisions were amended ► Reduction of WHT on qualifying dividends► Reduction of WHT on Interest ► Reduction of WHT on Royalties ► Update of Anti-Treaty shopping rules

Page 15Eric Hess / Deputy Head of the International Division /

Federal Tax Administration / Berne

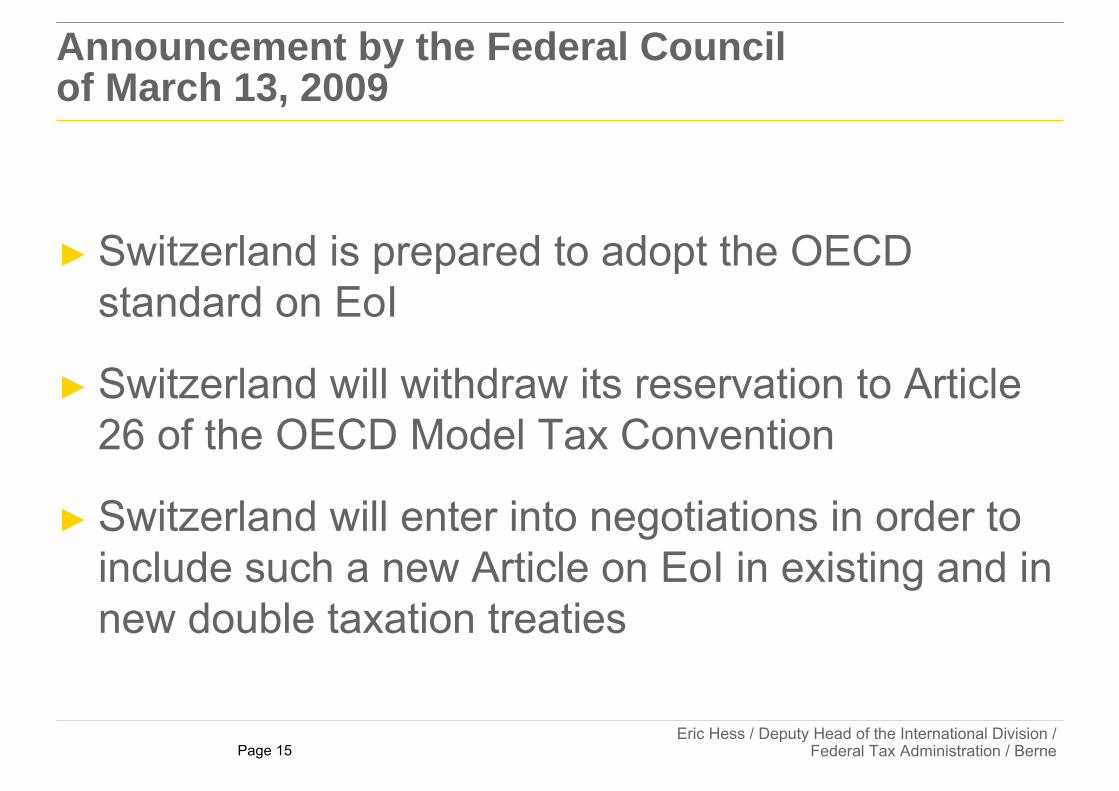

Announcement by the Federal Council of March 13, 2009

► Switzerland is prepared to adopt the OECD standard on EoI

► Switzerland will withdraw its reservation to Article 26 of the OECD Model Tax Convention

► Switzerland will enter into negotiations in order to include such a new Article on EoI in existing and in new double taxation treaties

Page 16Eric Hess / Deputy Head of the International Division /

Federal Tax Administration / Berne

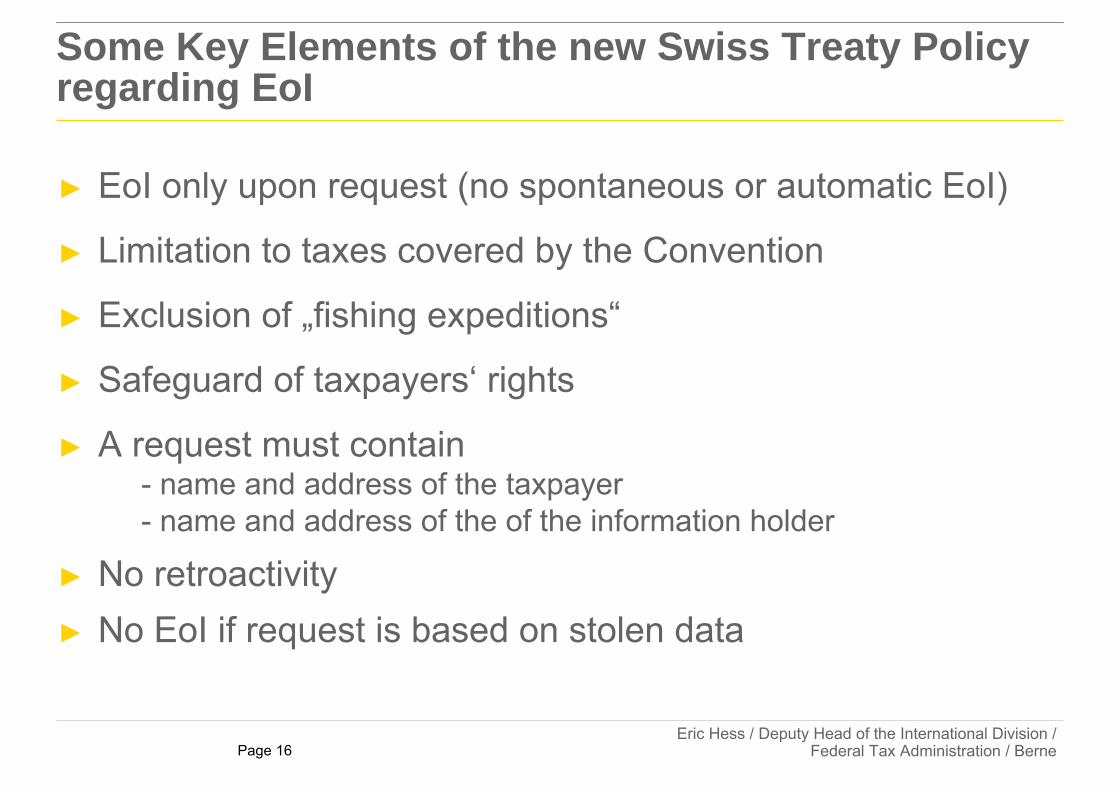

Some Key Elements of the new Swiss Treaty Policy regarding EoI

► EoI only upon request (no spontaneous or automatic EoI)

► Limitation to taxes covered by the Convention

► Exclusion of „fishing expeditions“

► Safeguard of taxpayers‘ rights

► A request must contain- name and address of the taxpayer - name and address of the of the information holder

► No retroactivity► No EoI if request is based on stolen data

Page 17Eric Hess / Deputy Head of the International Division /

Federal Tax Administration / Berne

Treaty Negotiations – How far have we come to date?

Treaties initialed 31 US: √

Treaties signed 23 US: √

Treaties approved by Swiss Parliament 10 US: √

Treaties in effect 2 France(Spain)

Page 18Eric Hess / Deputy Head of the International Division /

Federal Tax Administration / Berne

Scope of the 2009 Protocol

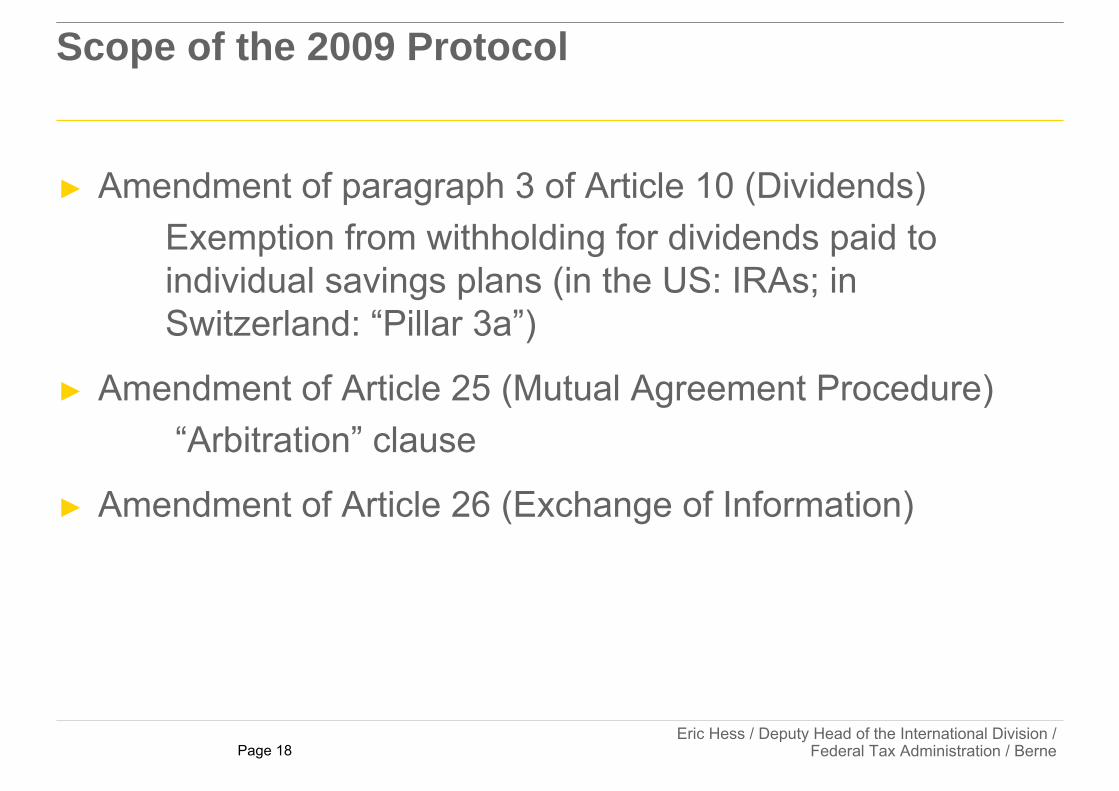

► Amendment of paragraph 3 of Article 10 (Dividends)Exemption from withholding for dividends paid to individual savings plans (in the US: IRAs; in Switzerland: “Pillar 3a”)

► Amendment of Article 25 (Mutual Agreement Procedure)“Arbitration” clause

► Amendment of Article 26 (Exchange of Information)

Page 19Eric Hess / Deputy Head of the International Division /

Federal Tax Administration / Berne

The new EoI provision with the U.S.

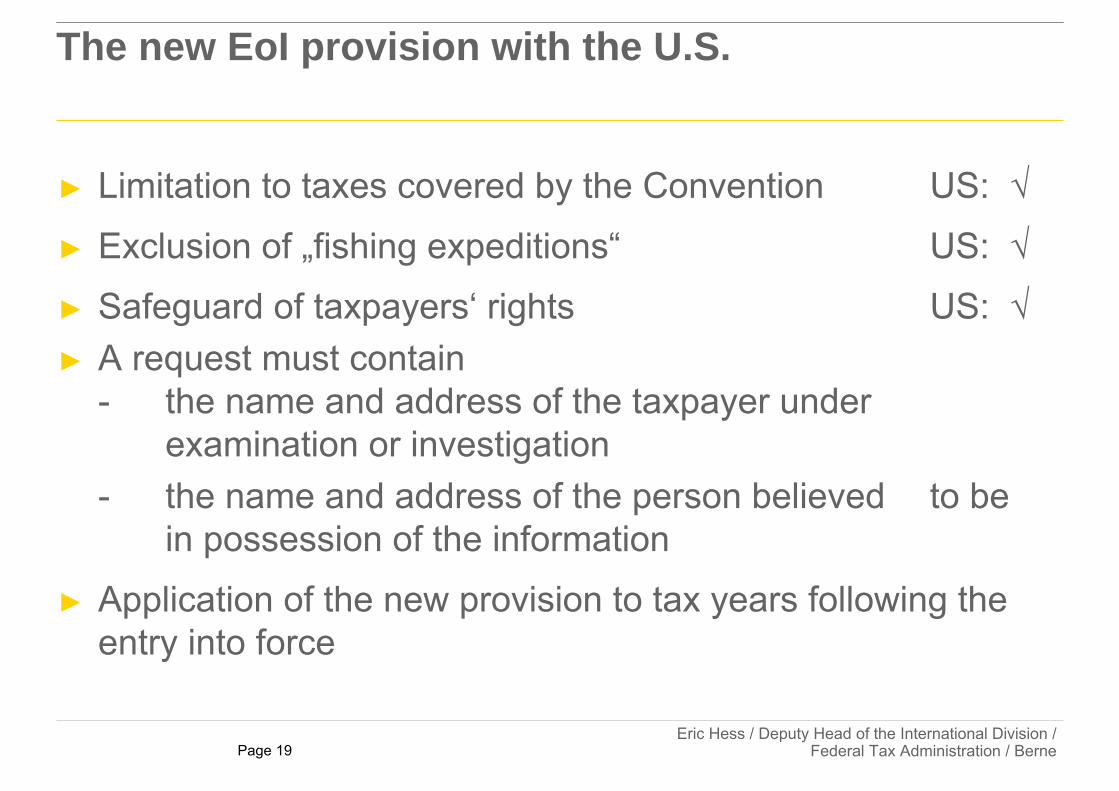

► Limitation to taxes covered by the Convention US: √

► Exclusion of „fishing expeditions“ US: √

► Safeguard of taxpayers‘ rights US: √► A request must contain

- the name and address of the taxpayer under examination or investigation

- the name and address of the person believed to be in possession of the information

► Application of the new provision to tax years following the entry into force

Page 20 © B. Sambeth Glasner & J. Lack 2008-10. All rights reserved

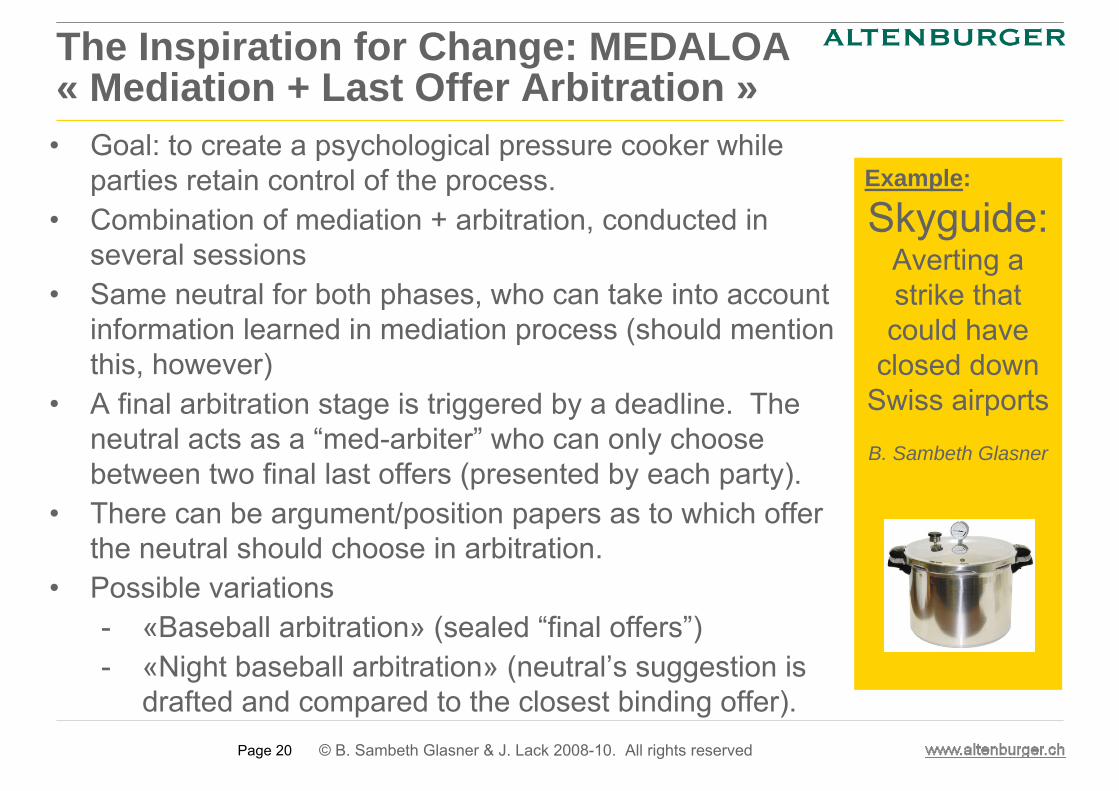

Example:

Skyguide:Averting a strike that could have

closed down Swiss airports

B. Sambeth Glasner

• Goal: to create a psychological pressure cooker while parties retain control of the process.

• Combination of mediation + arbitration, conducted in several sessions

• Same neutral for both phases, who can take into account information learned in mediation process (should mention this, however)

• A final arbitration stage is triggered by a deadline. The neutral acts as a “med-arbiter” who can only choose between two final last offers (presented by each party).

• There can be argument/position papers as to which offer the neutral should choose in arbitration.

• Possible variations- «Baseball arbitration» (sealed “final offers”)- «Night baseball arbitration» (neutral’s suggestion is

drafted and compared to the closest binding offer).

The Inspiration for Change: MEDALOA « Mediation + Last Offer Arbitration »

Page 21 © B. Sambeth Glasner & J. Lack 2008-10. All rights reserved

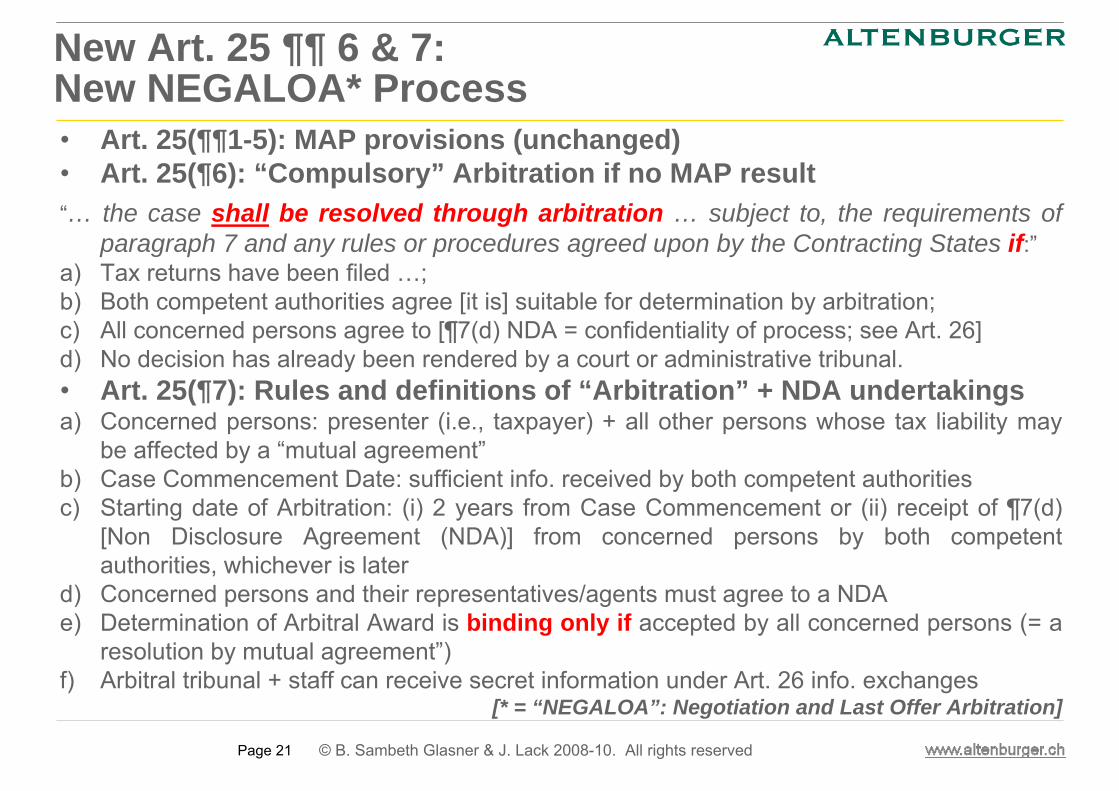

New Art. 25 ¶¶ 6 & 7: New NEGALOA* Process• Art. 25(¶¶1-5): MAP provisions (unchanged)• Art. 25(¶6): “Compulsory” Arbitration if no MAP result“… the case shall be resolved through arbitration … subject to, the requirements of

paragraph 7 and any rules or procedures agreed upon by the Contracting States if:”a) Tax returns have been filed …;b) Both competent authorities agree [it is] suitable for determination by arbitration; c) All concerned persons agree to [¶7(d) NDA = confidentiality of process; see Art. 26]d) No decision has already been rendered by a court or administrative tribunal.• Art. 25(¶7): Rules and definitions of “Arbitration” + NDA undertakingsa) Concerned persons: presenter (i.e., taxpayer) + all other persons whose tax liability may

be affected by a “mutual agreement”b) Case Commencement Date: sufficient info. received by both competent authoritiesc) Starting date of Arbitration: (i) 2 years from Case Commencement or (ii) receipt of ¶7(d)

[Non Disclosure Agreement (NDA)] from concerned persons by both competent authorities, whichever is later

d) Concerned persons and their representatives/agents must agree to a NDAe) Determination of Arbitral Award is binding only if accepted by all concerned persons (= a

resolution by mutual agreement”)f) Arbitral tribunal + staff can receive secret information under Art. 26 info. exchanges

[* = “NEGALOA”: Negotiation and Last Offer Arbitration]

Page 22 © B. Sambeth Glasner & J. Lack 2008-10. All rights reserved

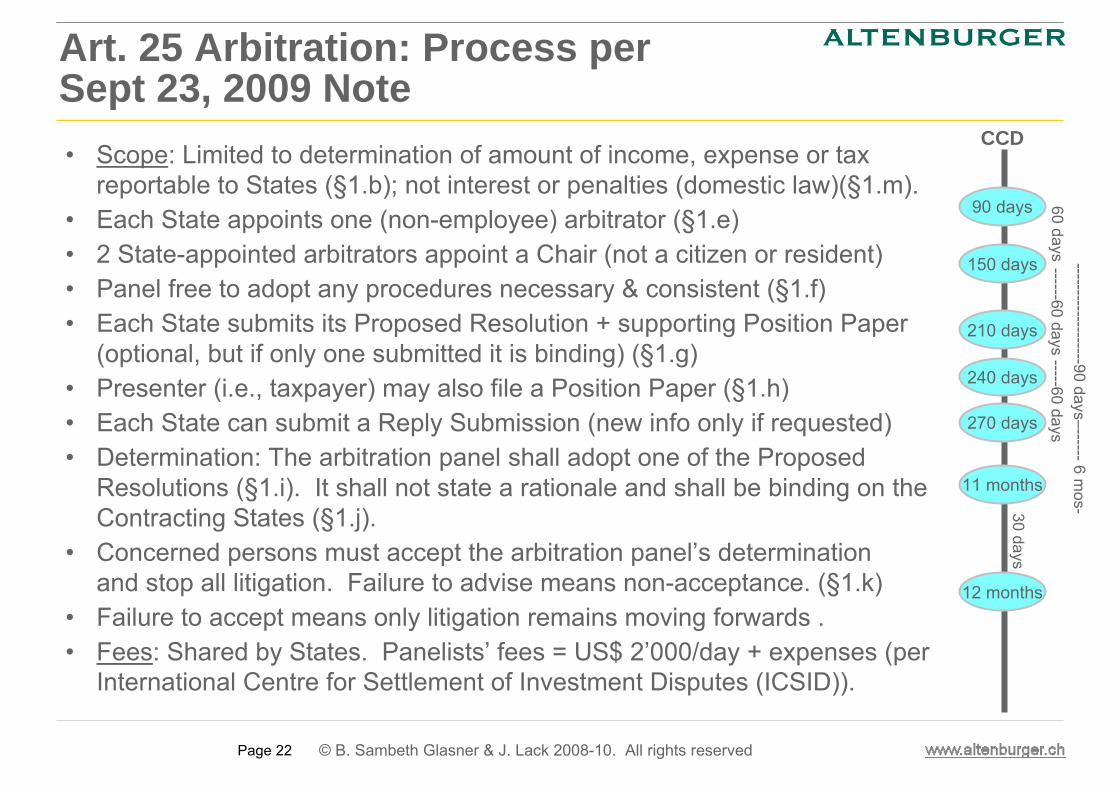

Art. 25 Arbitration: Process per Sept 23, 2009 Note• Scope: Limited to determination of amount of income, expense or tax

reportable to States (§1.b); not interest or penalties (domestic law)(§1.m).• Each State appoints one (non-employee) arbitrator (§1.e) • 2 State-appointed arbitrators appoint a Chair (not a citizen or resident)• Panel free to adopt any procedures necessary & consistent (§1.f)• Each State submits its Proposed Resolution + supporting Position Paper

(optional, but if only one submitted it is binding) (§1.g)• Presenter (i.e., taxpayer) may also file a Position Paper (§1.h)• Each State can submit a Reply Submission (new info only if requested)• Determination: The arbitration panel shall adopt one of the Proposed

Resolutions (§1.i). It shall not state a rationale and shall be binding on the Contracting States (§1.j).

• Concerned persons must accept the arbitration panel’s determination and stop all litigation. Failure to advise means non-acceptance. (§1.k)

• Failure to accept means only litigation remains moving forwards .• Fees: Shared by States. Panelists’ fees = US$ 2’000/day + expenses (per

International Centre for Settlement of Investment Disputes (ICSID)).

90 days 60 days

150 days

210 days

------60 days -----60 days

270 days

240 days

-------------------90 days–------6 mos-

11 months

30 days

12 months

CCD

Outlook

Page 24

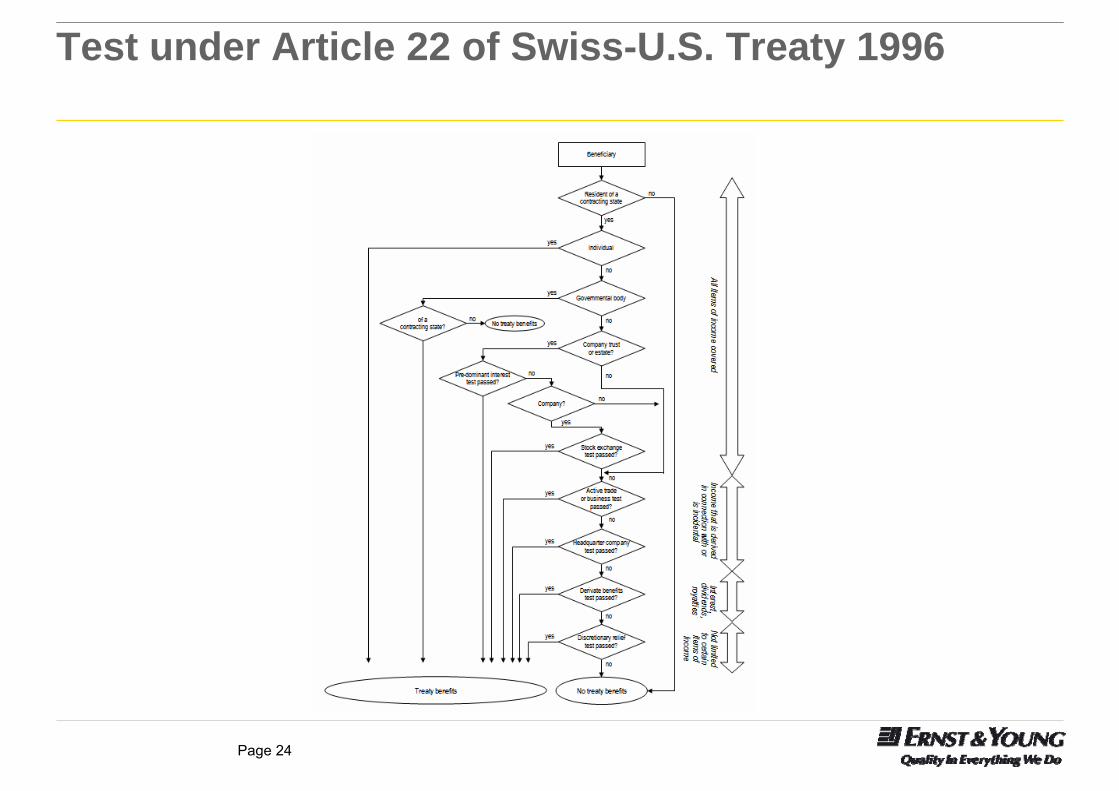

Test under Article 22 of Swiss-U.S. Treaty 1996

Page 25

Outlook (1)- Limitation on benefits

► Based on the U.S. Model Treaty 2006 (selected items) ► No Headquarters Test.► No provision Triangular Cases.► No Limited Derivative Benefits Test.► Increased requirements for the Stock Exchange Test. ► Ownership Test is a two-step test.► Active Trade or Business Test.

Page 26

Outlook (2)- Latest treaties negotiated by the US (Hungary/Chile)

► Hungary and Chile revised their income tax treaties with the U.S and include a new LOB clause.

► In contrast to the U.S. Model Treaty 2006, both LOB clause include a▬ Headquarters Test and ▬ a provision regarding the triangular cases which is very similar to the provision in the

Swiss-U.S. Treaty 1996. ► 0% WHT has not be granted.

Page 27

Outlook (3)- Latest treaties negotiated by the US (Netherlands)

► In 2004 the Netherlands and U.S. amended the treaty of 1992.► Reduction of the WHT on qualifying dividends from 5% to 0%.► Introduction of an updated LOB clause. ► For the 0% WHT, additional requirements have to be satisfied.► New term of “equivalent beneficiaries” in the Derivate Benefits Test.► New requirement of the “substantial presence” to the Stock Exchange Test.

Page 28Eric Hess / Deputy Head of the International Division /

Federal Tax Administration / Berne

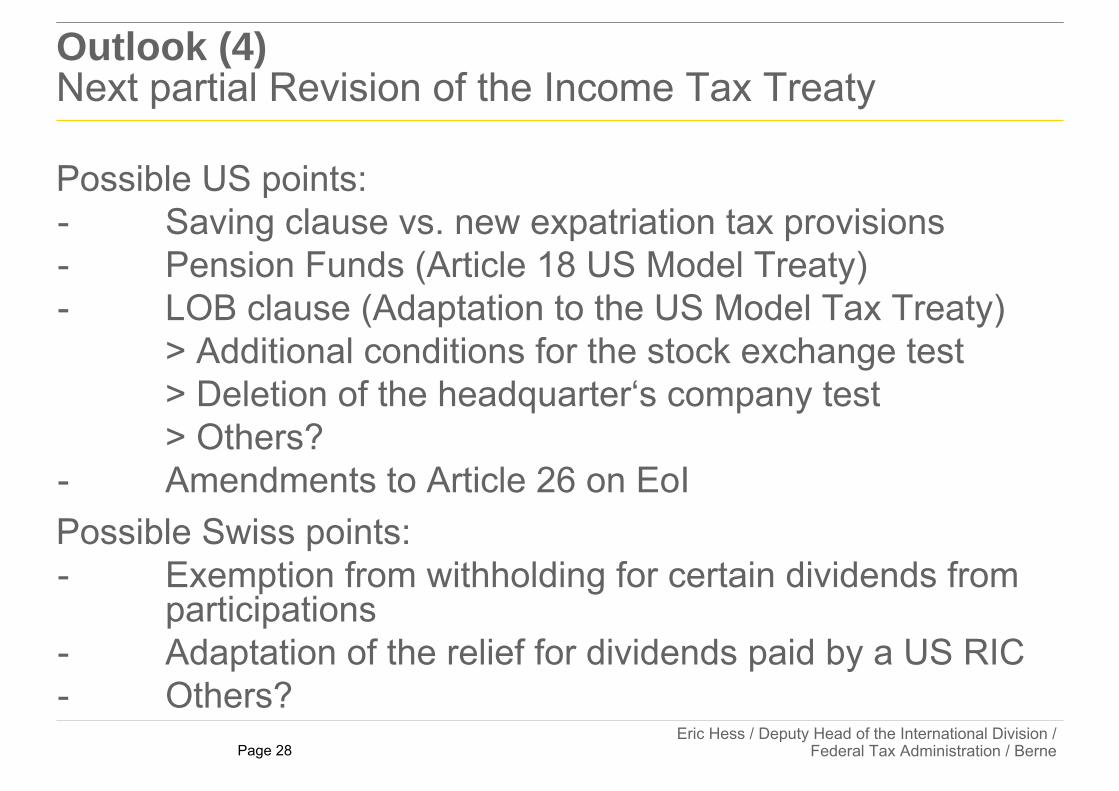

Outlook (4)Next partial Revision of the Income Tax Treaty

Possible US points:- Saving clause vs. new expatriation tax provisions- Pension Funds (Article 18 US Model Treaty)- LOB clause (Adaptation to the US Model Tax Treaty)

> Additional conditions for the stock exchange test> Deletion of the headquarter‘s company test> Others?

- Amendments to Article 26 on EoIPossible Swiss points:- Exemption from withholding for certain dividends from

participations- Adaptation of the relief for dividends paid by a US RIC- Others?

Page 29Eric Hess / Deputy Head of the International Division /

Federal Tax Administration / Berne

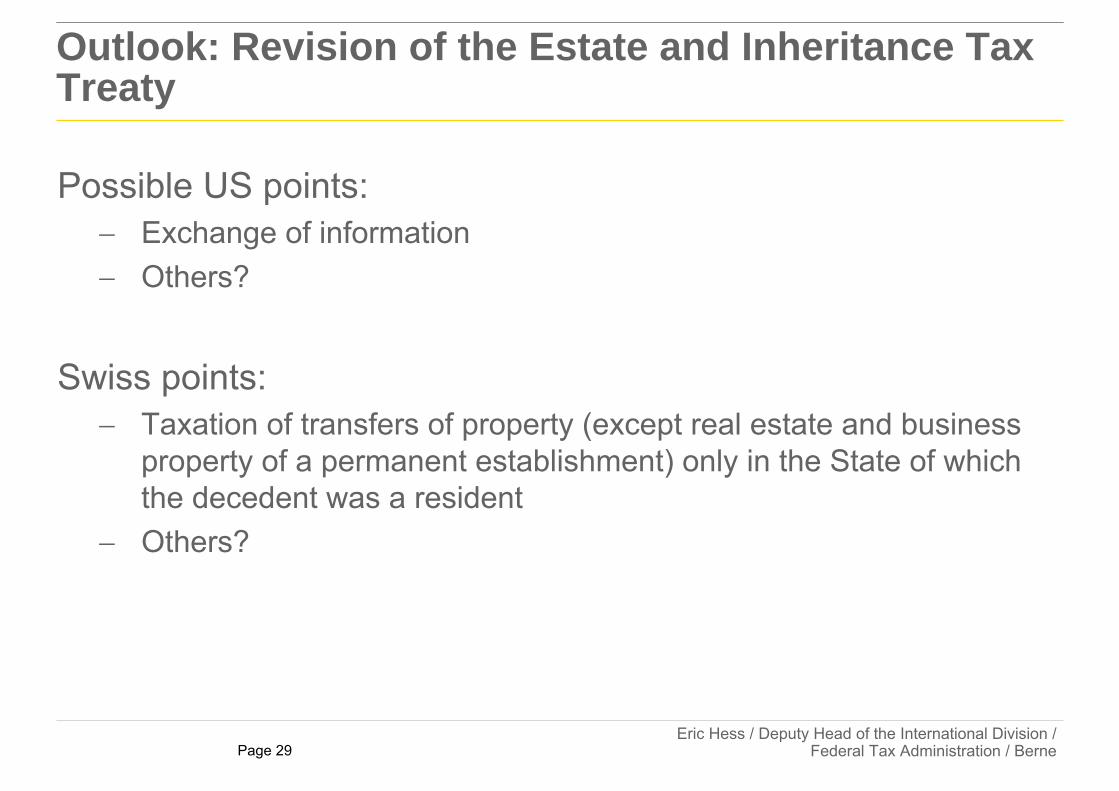

Outlook: Revision of the Estate and Inheritance Tax Treaty

Possible US points: Exchange of information Others?

Swiss points: Taxation of transfers of property (except real estate and business

property of a permanent establishment) only in the State of which the decedent was a resident

Others?

Page 30 © B. Sambeth Glasner & J. Lack 2008-10. All rights reserved

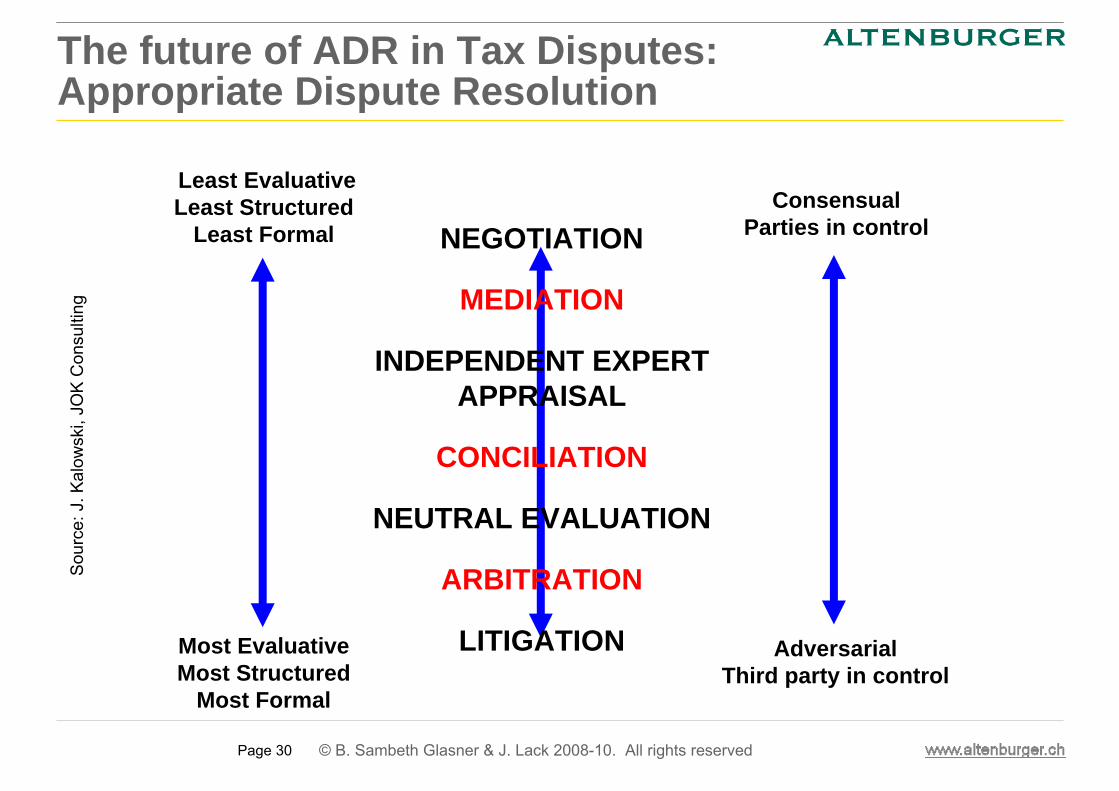

The future of ADR in Tax Disputes: Appropriate Dispute Resolution

Least EvaluativeLeast Structured

Least Formal

Most EvaluativeMost Structured

Most Formal

Consensual Parties in control

Adversarial Third party in control

NEGOTIATION

MEDIATION

INDEPENDENT EXPERT APPRAISAL

CONCILIATION

NEUTRAL EVALUATION

ARBITRATION

LITIGATION

Sou

rce:

J. K

alow

ski,

JOK

Con

sulti

ng

Page 31 © B. Sambeth Glasner & J. Lack 2008-10. All rights reserved

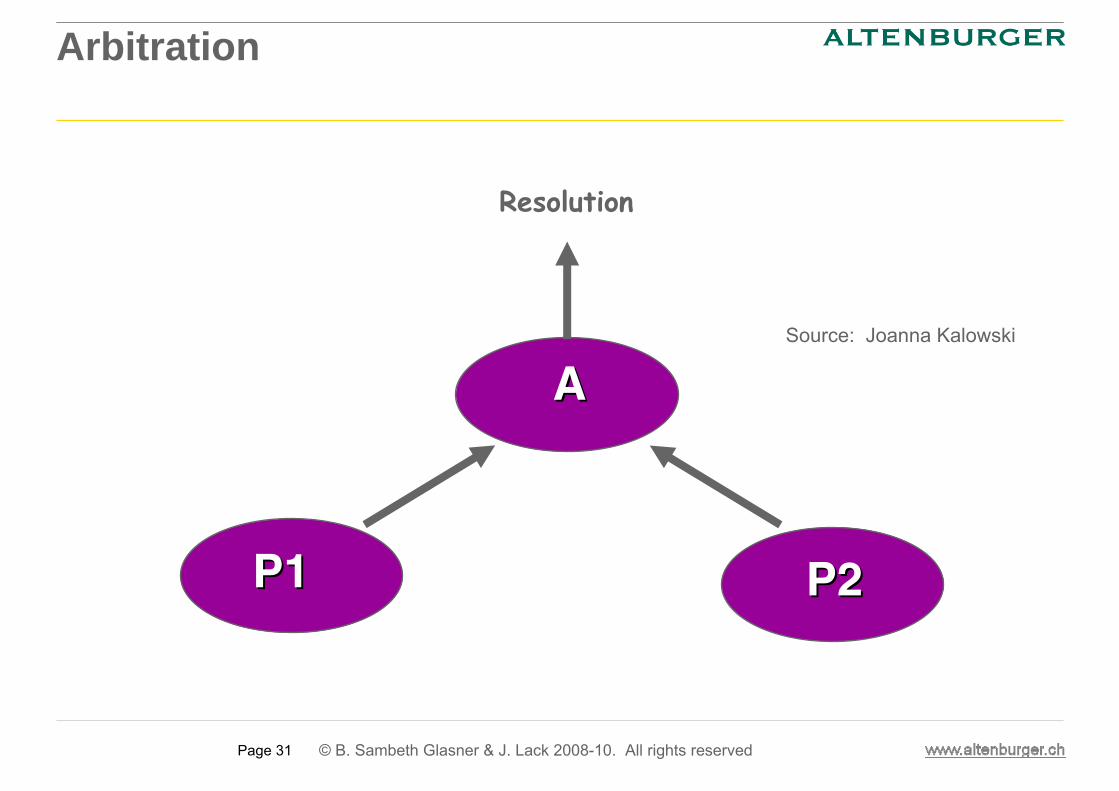

AA

P1P1 P2P2

Resolution

Source: Joanna Kalowski

Arbitration

Page 32 © B. Sambeth Glasner & J. Lack 2008-10. All rights reserved

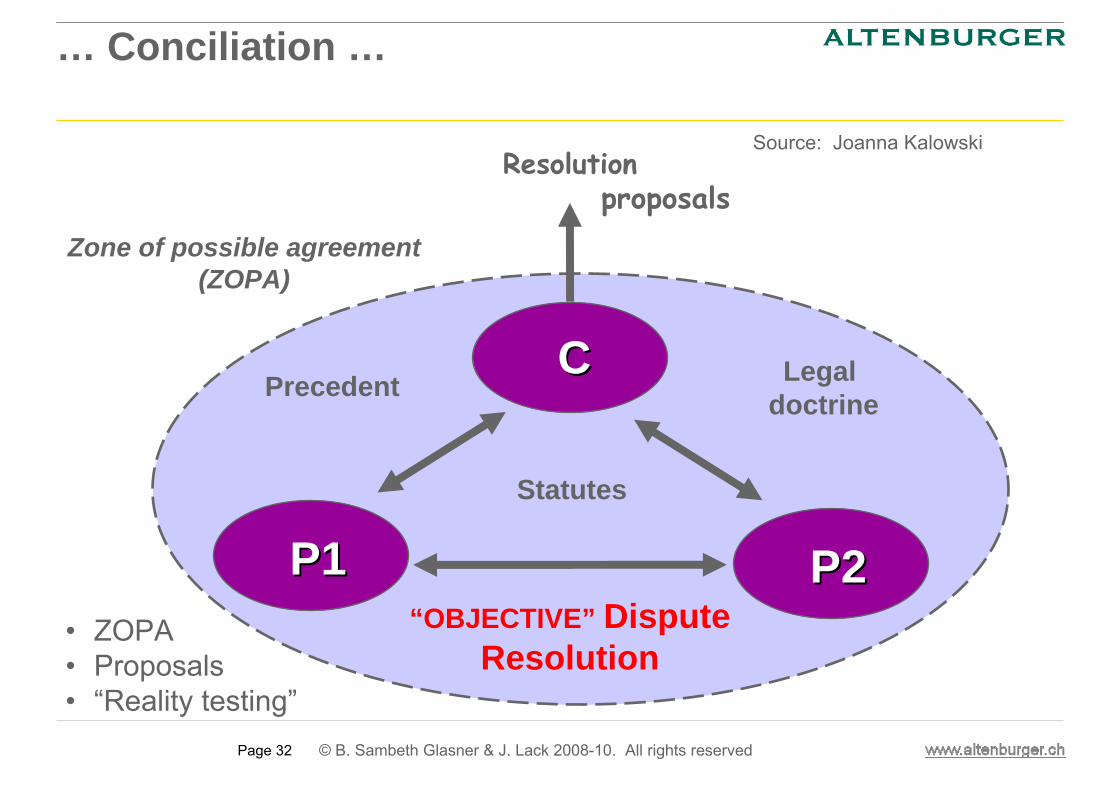

P1P1 P2P2

CCPrecedent Legal

doctrine

“OBJECTIVE” Dispute Resolution

Statutes

Resolutionproposals

Source: Joanna Kalowski

Zone of possible agreement(ZOPA)

• ZOPA• Proposals• “Reality testing”

… Conciliation …

Page 33 © B. Sambeth Glasner & J. Lack 2008-10. All rights reserved

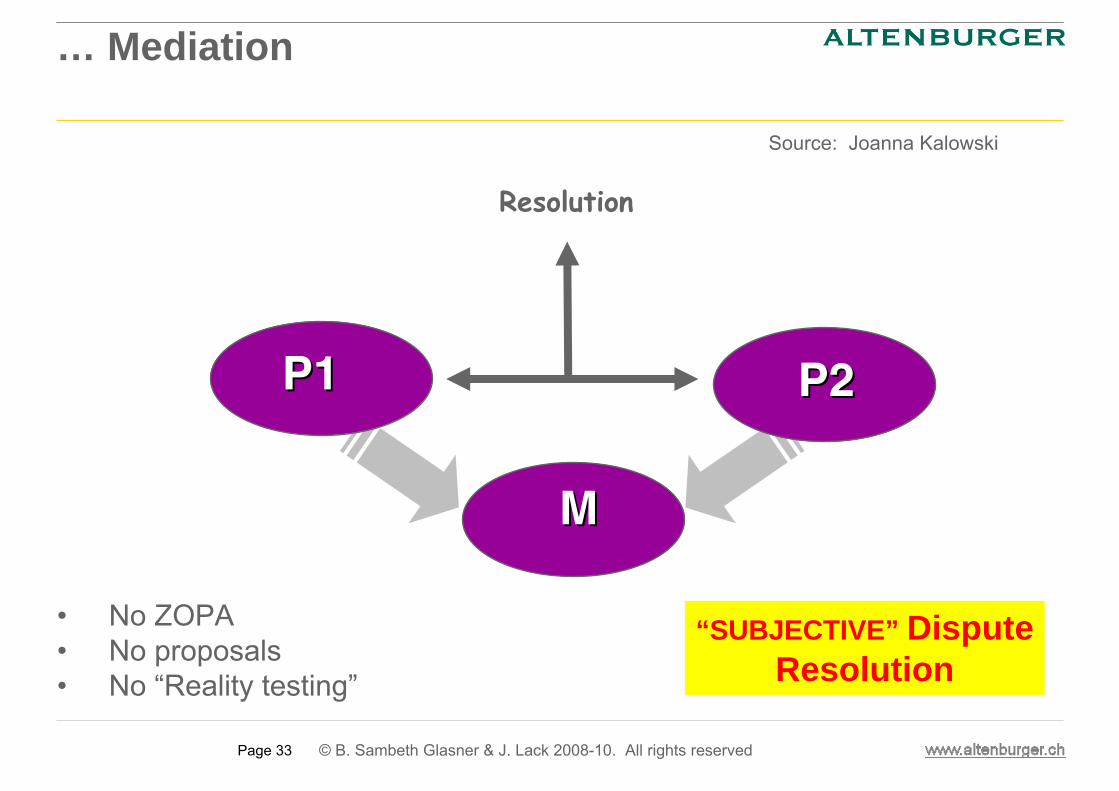

MM

P1P1 P2P2

Resolution

“SUBJECTIVE” Dispute Resolution

Source: Joanna Kalowski

• No ZOPA• No proposals• No “Reality testing”

… Mediation

Page 34 © B. Sambeth Glasner & J. Lack 2008-10. All rights reserved

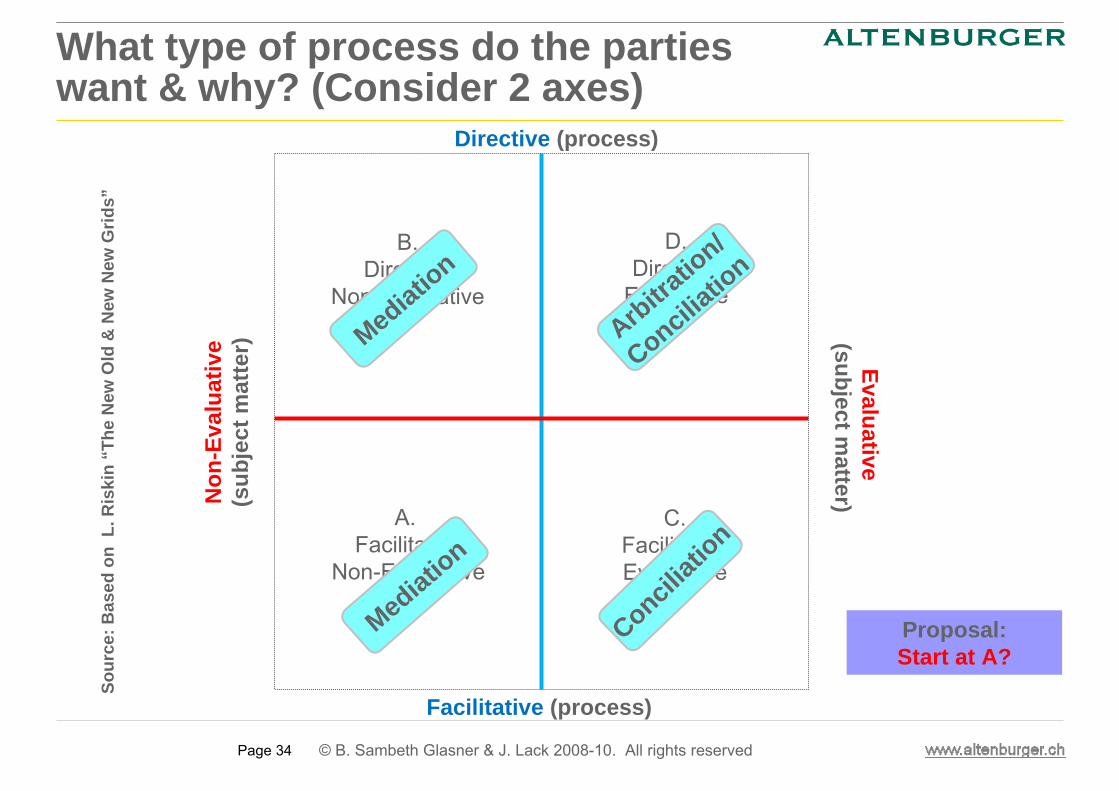

What type of process do the parties want & why? (Consider 2 axes)

Facilitative (process)

Directive (process)So

urce

: Bas

ed o

n L

. Ris

kin

“The

New

Old

& N

ew N

ewG

rids”

Non

-Eva

luat

ive

(sub

ject

mat

ter) Evaluative

(subject matter)

B.Directive

Non-Evaluative

D.Directive

Evaluative

A. Facilitative

Non-Evaluative

C.FacilitativeEvaluative

Arbitratio

n/

Conciliatio

n

Conciliat

ion

Mediation

Mediation

Proposal: Start at A?

Page 35 © B. Sambeth Glasner & J. Lack 2008-10. All rights reserved

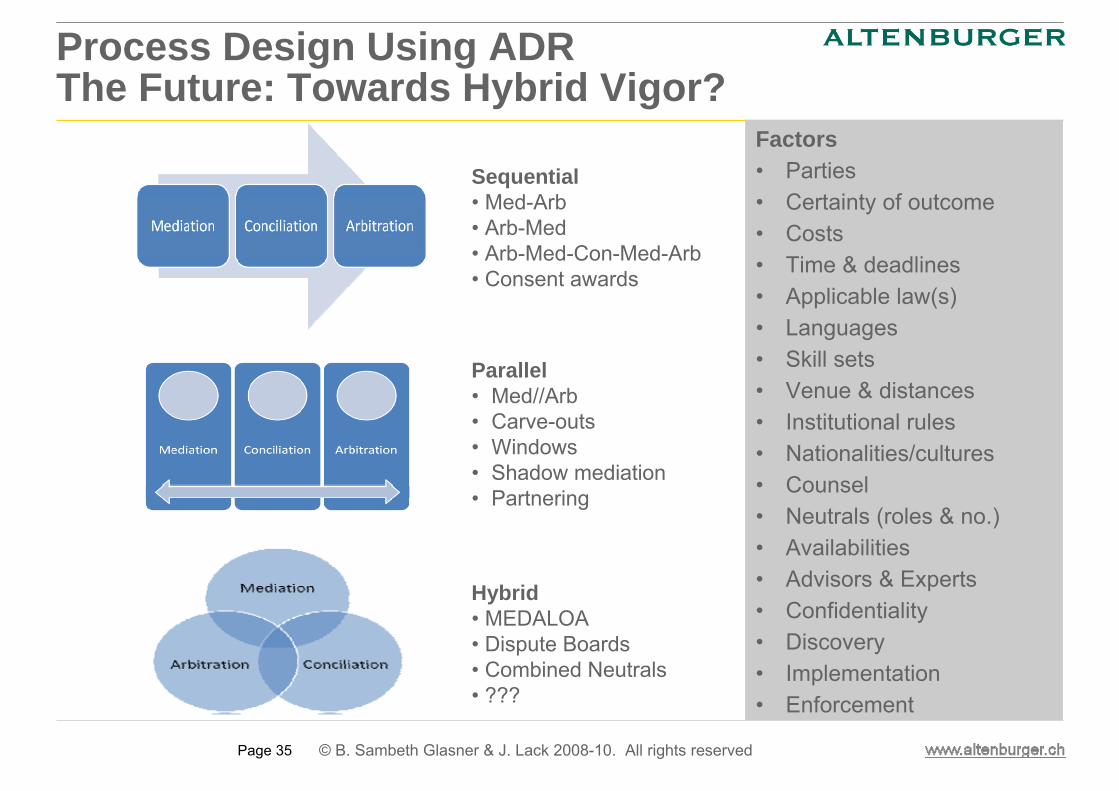

Factors• Parties• Certainty of outcome• Costs• Time & deadlines• Applicable law(s)• Languages• Skill sets• Venue & distances• Institutional rules• Nationalities/cultures• Counsel• Neutrals (roles & no.)• Availabilities• Advisors & Experts• Confidentiality• Discovery• Implementation• Enforcement

Sequential• Med-Arb• Arb-Med• Arb-Med-Con-Med-Arb• Consent awards

Parallel• Med//Arb• Carve-outs• Windows• Shadow mediation• Partnering

Hybrid• MEDALOA• Dispute Boards• Combined Neutrals• ???

Process Design Using ADR The Future: Towards Hybrid Vigor?

Closing remarks

Page 37

Closing remarks

► The new LOB clause of the recently concluded treaties with the U.S. generally comprise more restrictive requirements.

► Higher thresholds may need to be fulfilled for some of the Tests.► However, even a new LOB clause does not guarantee a WHT to 0%

on qualifying dividends.