Embed Size (px)

Citation preview

Checkpoint Contents

Accounting, Audit & Corporate Finance Library

Editorial Materials

Accounting and Financial Statements (US GAAP)

Cash, Tax, and Other Bases of Accounting

Chapter 1 An Introduction to OCBOA Financial Statements

100 Background Information

100 Background Information

100.1 Bases of accounting other than GAAP [referred to in the authoritative literature as “special purpose frameworks”

or “other comprehensive bases of accounting” or (OCBOAs)] are a widely used alternative to the numerous and

sometimes complex accounting requirements prescribed by generally accepted accounting principles (GAAP). Also

contributing to the use of OCBOAs is the availability of inexpensive accounting software, which allows individuals more

familiar with tax laws than GAAP to maintain records and prepare financial statements with relative ease. 1

Unfortunately, limited authoritative guidance on applying other comprehensive bases of accounting exists.

100.2 References to OCBOAs appear in Statements on Auditing Standards (SASs) and Statements on Standards for

Accounting and Review Services (SSARS). AU-C 210, Terms of Engagement [formerly SAS No. 84 (AU 315) and SAS

No. 108 (AU 311)], requires the auditor to determine the acceptability of the financial reporting framework applied in

the preparation of the financial statements. Ordinarily, that framework is provided by GAAP; but AU-C 800, Special

Considerations—Audits of Financial Statements Prepared in Accordance With Special Purpose Frameworks [formerly

SAS No. 62 (AU 623)], and SSARS No. 19 (AR 60.04) allow special purpose frameworks to be used. AU-C 800

describes the following special purpose frameworks:

• Cash Basis. A basis of accounting used by the reporting entity to record cash receipts and disbursements. It

includes modifications of the cash basis having substantial support (for example, recording depreciation on fixed

assets), commonly known as the modified cash basis.

• Regulatory Basis. A basis of accounting used by the reporting entity to comply with the requirements or financial

reporting provisions of a regulatory agency to whose jurisdiction the entity is subject (for example, a basis of

accounting that insurance companies use pursuant to the accounting practices prescribed or permitted by a state

insurance commission).

• Tax Basis. A basis of accounting the reporting entity uses to file its tax return for the period covered by the

financial statements.

• Contractual Basis. A basis of accounting used by the entity to comply with an agreement between the entity and

one or more third parties other than the auditor.

Page 1 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

• Other Basis. A basis of accounting utilizing a definite set of logical and reasonable criteria that is applied to all

material items within the financial statements. 2

According to AU-C 800.07, the cash, tax, regulatory, and other bases of accounting are commonly referred to as other

comprehensive bases of accounting. While AU-C 800 predominantly uses the term special purpose framework, this

Guide continues to predominantly use the term other comprehensive basis of accounting or OCBOA.

100.3 SSARS No. 19 (AR 60.04) revised the definition of OCBOA as it relates to compilation and review

engagements, indicating that an OCBOA is a definite set of criteria, other than U.S. GAAP or International Financial

Reporting Standards (IFRS), having substantial support underlying the preparation of financial statements prepared

according to such basis. While that definition added a reference to IFRS, as discussed in paragraph 100.42, this Guide

does not address IFRS. Additionally, SSARS No. 19 indicates that ordinarily a modification would have substantial

support if the method is equivalent to the accrual basis of accounting for that item and if the method is not illogical.

100.4 AU-C 800 provides the primary guidance for disclosures in OCBOA financial statements. When special purpose

financial statements contain items that are the same as, or similar to, those in financial statements prepared in

accordance with GAAP, AU-C 800.17 states that the financial statements should include informative disclosures

similar to those required by GAAP. In addition, it states that additional disclosures, beyond those specifically required

by the framework, related to matters that are not specifically identified on the face of the financial statements, or other

disclosures, might be necessary for the financial statements to achieve fair presentation. The discussion beginning at

paragraph 300.6 addresses the applicability of this guidance to compiled or reviewed financial statements.

FASB Codification

100.5 GAAP measurement and disclosure requirements can be found in the FASB Accounting Standards Codification.

The FASB Accounting Standards Codification (FASB ASC or the Codification) is the single source of authoritative

nongovernmental U.S. generally accepted accounting principles (GAAP). Other accounting literature not included in

the Codification is nonauthoritative.

Clarity Project of the Auditing Standards Board

100.6 In response to growing concerns about the complexity of auditing standards and to converge U.S. GAAS with

International Standards on Auditing, the Auditing Standards Board has been working on the Clarity Project to revise all

existing standards and to design a format under which all new standards will be issued. In October 2011, the AICPA

issued:

• SAS No.122, Statements on Auditing Standards: Clarification and Recodification. This represents a completely

new set of auditing standards revised in format, structure, style, and content from the existing standards. It

supersedes all existing SASs through SAS No. 121, except:

•• SAS No. 51, Reporting on Financial Statements Prepared for Use in Other Countries. (Subsequently

superseded by SAS No. 124.)

Page 2 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

•• SAS No. 59, The Auditor's Consideration of an Entity's Ability to Continue as a Going Concern.

(Subsequently superseded by SAS No. 126.)

•• SAS No. 65, The Auditor's Consideration of the Internal Audit Function in an Audit of Financial

Statements. (Currently being redrafted and will be superseded when the clarified version is issued.)

•• SAS No. 87, Restricting the Use of an Auditor's Report. (Subsequently superseded by SAS No. 125.)

•• SAS No. 117 on compliance audits and SAS Nos. 118-120 on supplementary information. These

standards were previously issued in clarified format and are already effective.

• SAS No. 123, Omnibus Statement on Auditing Standards—2011. Amends SAS Nos. 117, 118, and 122 to

address matters that arose after the clarified standards were finalized.

• SAS No. 124, Financial Statements Prepared in Accordance with a Financial Reporting Framework Generally

Accepted in Another Country. This is the clarified and recodified version of SAS No. 51, Reporting on Financial

Statements Prepared for Use in Other Countries.

All auditing interpretations corresponding to a SAS were considered in the development of the clarified standards and

incorporated as necessary. Generally, the interpretations have been withdrawn, except for certain interpretations that

were retained and revised to reflect the issuance of SAS No. 122. Going forward, the ASB will continue to issue SASs

to create, amend, or supersede the auditing standards as necessary.

100.7 Effective Date

With a few exceptions, all of the clarified standards are effective for audits of financial statements for periods ending on

or after December 15, 2012. Generally early adoption of SAS Nos. 122-126 is not permitted. However, an auditor may

implement aspects of SAS Nos. 122-126 early as long as he or she continues to comply with existing standards. See

the discussion of the implementation approach in this Guide beginning at paragraph 100.16.

100.8 SAS No. 125

In December 2011, the ASB issued SAS No. 125, Alert That Restricts the Use of the Auditor's Written Communication.

SAS No. 125 supersedes SAS No. 87 (AU 532), Restricting the Use of an Auditor's Report, and amends, among other

standards, AU-C 260, The Auditor's Communication With Those Charged With Governance, and AU-C 265,

Communicating Internal Control Related Matters Identified in an Audit. SAS No. 125 is effective for the auditor's written

communications related to audits of financial statements for periods ending on or after December 15, 2012.

Page 3 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

100.9 SAS No. 126

In July 2012, the ASB issued SAS No. 126, The Auditor's Consideration of an Entity's Ability to Continue as a Going

Concern (Redrafted), which supersedes SAS No. 59 of the same name. In issuing SAS No. 126, the ASB followed the

format of the other clarified SASs, but did not converge with the ISAs, pending the FASB's anticipated development of

accounting guidance addressing going concern. (At the time this Guide was completed, the FASB had indicated on its

Projects webpage that an exposure draft would be issued in the fourth quarter of 2012.) Accordingly, SAS No. 126

does not change or expand SAS No. 59 in any significant respect. SAS No. 126 has the same effective date as the

other clarified auditing standards.

100.10 Form and Structure of the Standards

The clarified standards were developed using formatting techniques, such as bulleted lists, that make them easier to

read and understand. In addition, each clarified standard is divided into the following topics:

• Introduction. Includes matters such as the purpose and scope of the guidance, subject matter, effective date,

and other introductory material.

• Objectives. Establishes objectives that allow the auditor to understand what he or she should achieve under the

standards. The auditor uses the objectives to determine whether additional procedures are necessary for their

achievement and to evaluate whether sufficient appropriate audit evidence has been obtained.

• Definitions. Provides key definitions that are relevant to the standard.

• Requirements. States the requirements that the auditor is to follow to achieve the objectives unless the

standard is not relevant or the requirement is conditional and the condition does not exist.

• Application and Other Explanatory Material. Provides further guidance to the auditor in applying or

understanding the requirements. While this material does not in itself impose a requirement, auditors should

understand this guidance. How it is applied will depend on professional judgment in the circumstances

considering the objectives of the standard. The requirements section references the applicable application and

explanatory material. Also, when appropriate, considerations relating to smaller and less complex entities are

included in this section.

100.11 A standard may also contain exhibits or appendices. Appendices to a standard are part of the application and

other explanatory material. The purpose and intended use of an appendix is explained in the standard or in the title

and introduction of the appendix. Exhibits to standards are interpretive publications. Interpretive publications are not

auditing standards and do not contain requirements. Rather, they are recommendations on applying the standards in

particular circumstances that are issued under the authority of the Auditing Standards Board. Auditors are required to

consider applicable interpretive publications when planning and performing the audit.

Page 4 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

100.12 New AU Section Organization

Within the AICPA Professional Standards, the clarified standards (SAS Nos. 122-126) use “AU-C” section numbers

instead of “AU” section numbers. “AU-C” is being used temporarily to avoid confusion with references to existing “AU”

sections, which remain effective through 2013. The “AU-C” identifier will revert to “AU” in 2014, when the clarified

standards are fully effective for all engagements. The organization of the new AU-C sections is as follows:

• Preface.

• Glossary.

• AU-C Section 200-299: General Principles and Responsibilities.

• AU-C Section 300-499: Risk Assessment and Response to Assessed Risks.

• AU-C Section 500-599: Audit Evidence.

• AU-C Section 600-699: Using the Work of Others.

• AU-C Section 700-799: Audit Conclusions and Reporting.

• AU-C Section 800-899: Special Considerations.

• AU-C Section 900-999: Special Considerations in the United States

• Exhibits and Appendixes.

100.13 An exhibit to SAS No. 122 contains a two-part cross-reference of AU-C and AU section numbers. One part of

the cross-reference shows which existing AU sections are encompassed by each new AU-C section. The other part of

the cross-reference shows, for each existing AU section, where the corresponding guidance can be found in the new

AU-C sections.

Page 5 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

100.14 Preface

AU-C Preface, Principles Underlying an Audit Conducted in Accordance With Generally Accepted Auditing Standards,

contains the principles underlying an audit conducted in accordance with generally accepted auditing standards (the

principles). These principles are not requirements and are not authoritative. They provide a framework that is helpful in

understanding and explaining an audit and are organized to provide a structure for the codification of SASs. The

structure addresses the purpose of an audit, responsibilities of the auditor, performance of the audit, and reporting.

100.15 Implementation of the Clarified Auditing Standards

With a few exceptions, all of the clarified auditing standards are effective for audits of financial statements for periods

ending on or after December 15, 2012. Generally early adoption of SAS Nos. 122-126 (the clarified standards) is not

permitted. However, an auditor may implement aspects of the clarified standards early as long as he or she continues

to comply with existing standards.

100.16 Implementation in this Guide

The majority of the requirements in the clarified standards are consistent with the requirements in the pre-clarified

standards. Thus, the changes to the standards, although extensive, do not create many substantive changes in

practice. Therefore, the discussions throughout this Guide and references to authoritative auditing literature have been

updated for the clarified standards.

100.17 If there has been a change in the standards that will cause a change in practice, the authors have provided a

discussion of both the pre-clarified and clarified auditing standards, including appropriate references to the pre-clarified

authoritative literature. Therefore, unless a difference is specifically highlighted, the auditor using the updated

guidance in this Guide is also continuing to comply with existing standards. As a result, auditors may use this edition of

the Guide both before and after the effective date of the clarified standards.

100.18 Significant Changes to OCBOA Engagements

AU-C 800 supersedes the portion of SAS No. 62 that provides the current guidance for auditing OCBOA financial

statements. Some of the changes under the new standard that impact OCBOA audit engagements include:

• Changed definition of an OCBOA. AU-C 800 as initially issued eliminated the use of a “definite set of criteria

having substantial support that is applied to all material items appearing in financial statements, such as the price-

level basis of accounting.” However, as discussed in paragraph 100.2, that definition was added back (excluding

the mention of the price-level basis of accounting, which has been eliminated in the clarified auditing standard).

The contractual basis is added as one type of OCBOA that is not separately defined in SAS No. 62.

• New terminology. Throughout the new standard, the use of the term other comprehensive basis of accounting

has generally been replaced by the term special purpose framework, although use of the existing term is still

appropriate for the cash, tax, regulatory, and other bases of accounting.

• Acceptability of the Reporting Framework. AU-C 800.10 requires the auditor to determine whether the special

purpose framework used to prepare the entity's financial statements is acceptable by obtaining an understanding

Page 6 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

of (a) the purpose for which the financial statements are prepared, (b) the intended users, and (c) the steps taken

by management to determine that the framework is acceptable in the circumstances.

• Preconditions for the Audit. AU-C 800.11 requires the auditor to obtain management's agreement that it

acknowledges and understands its responsibility to include all informative disclosures that are appropriate for the

special purpose framework used to prepare the financial statements. Management's acknowledgment and

understanding should also cover any additional disclosures necessary to achieve fair presentation in the financial

statements. The auditor should evaluate whether such disclosures are necessary.

• Regulatory and Contractual Bases. When the special purpose framework is the regulatory or contractual basis,

certain performance, reporting, and/or presentation requirements exist under AU-C 800. Those requirements are

discussed in Chapters 6, 7, and 9.

• Reporting. Several new requirements exist in the area of reporting that impact all types of special purpose

frameworks pursuant to AU-C 800. Those requirements are discussed in Chapter 7.

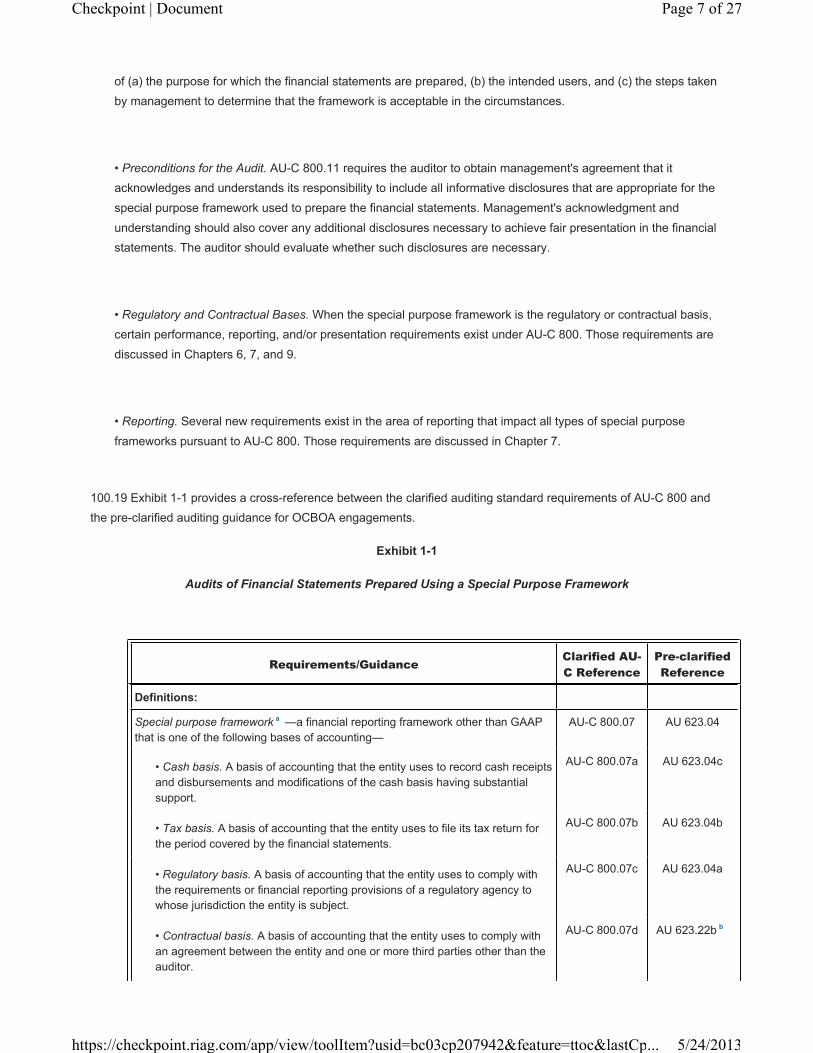

100.19 Exhibit 1-1 provides a cross-reference between the clarified auditing standard requirements of AU-C 800 and

the pre-clarified auditing guidance for OCBOA engagements.

Exhibit 1-1

Audits of Financial Statements Prepared Using a Special Purpose Framework

Requirements/Guidance Clarified AU-

C Reference

Pre-clarified

Reference

Definitions:

Special purpose framework a —a financial reporting framework other than GAAP

that is one of the following bases of accounting—

AU-C 800.07 AU 623.04

• Cash basis. A basis of accounting that the entity uses to record cash receipts

and disbursements and modifications of the cash basis having substantial

support.

AU-C 800.07a AU 623.04c

• Tax basis. A basis of accounting that the entity uses to file its tax return for

the period covered by the financial statements.

AU-C 800.07b AU 623.04b

• Regulatory basis. A basis of accounting that the entity uses to comply with

the requirements or financial reporting provisions of a regulatory agency to

whose jurisdiction the entity is subject.

AU-C 800.07c AU 623.04a

• Contractual basis. A basis of accounting that the entity uses to comply with

an agreement between the entity and one or more third parties other than the

auditor.

AU-C 800.07d AU 623.22b b

Page 7 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

Requirements/Guidance Clarified AU-

C Reference

Pre-clarified

Reference

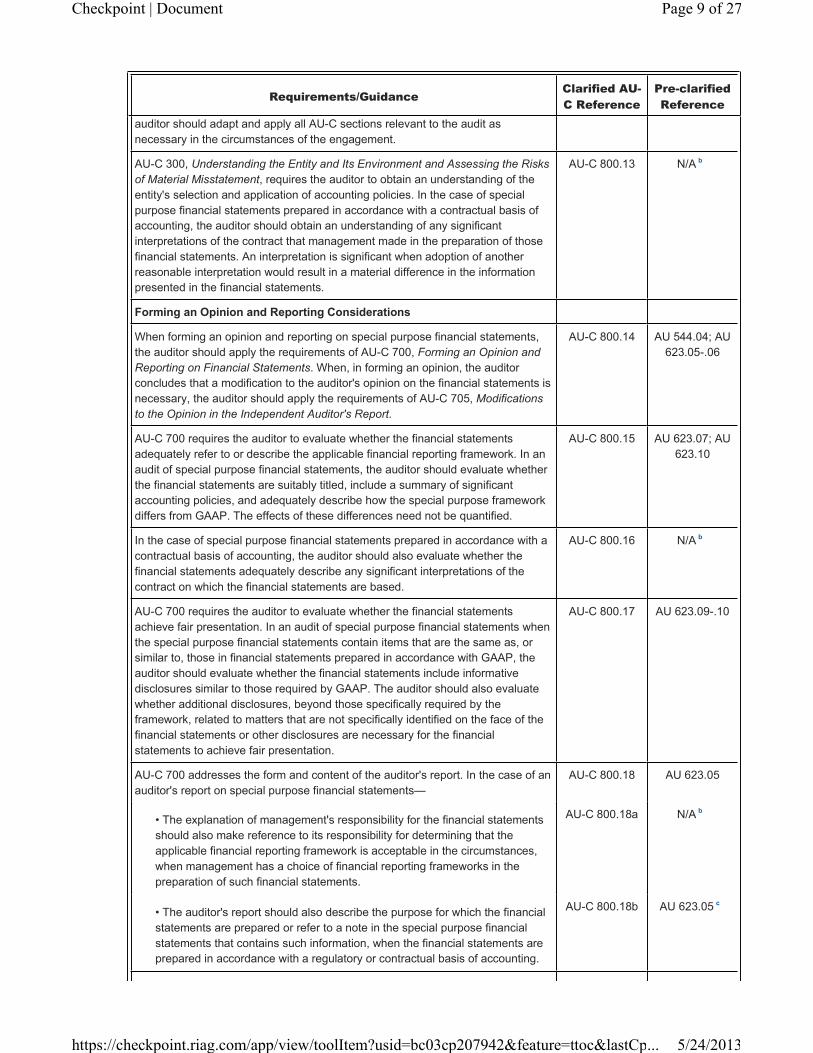

• Other basis. A basis of accounting that utilizes a definite set of logical and

reasonable criteria that is applied to all material items appearing in financial

statements.

AU-C 800.07e AU 623.04d

Reference to financial statements in AU-C 800 means a complete set of special

purpose financial statements, including the related notes. The related notes

ordinarily comprise a summary of significant accounting policies and other

explanatory information. The requirements of the applicable financial reporting

framework determine the form and content of the financial statements and what

constitutes a complete set of financial statements.

AU-C 800.08 AU 623.02

Requirements:

Considerations When Accepting the Engagement

AU-C 210, Terms of Engagement, requires the auditor to determine whether the

financial reporting framework used in the preparation of the financial statements is

acceptable. For an audit of special purpose financial statements, the auditor

should obtain an understanding of—

AU-C 800.10 N/A b

• the purpose for which the financial statements are prepared,

• the intended users, and

• the steps taken by management to determine that the applicable financial

reporting framework is acceptable in the circumstances.

AU-C 210 requires the auditor to establish whether the preconditions for an audit

are present, including whether the financial reporting framework to be applied in

the preparation of the financial statements is acceptable. When auditing special

purpose financial statements, the auditor should obtain management's agreement

that it acknowledges and understands its responsibility to include all informative

disclosures that are appropriate for the special purpose framework used to

prepare the entity's financial statements, including—

AU-C 800.11 N/A b

• A description of the special purpose framework, including a summary of

significant accounting policies, and how the framework differs from GAAP, the

effects of which need not be quantified.

AU-C 800.11a N/A b

• Informative disclosures similar to those required by GAAP, in the case of

special purpose financial statements that contain items that are the same as,

or similar to, those in financial statements prepared in accordance with GAAP.

AU-C 800.11b N/A b

• A description of any significant interpretations of the contract on which the

special purpose financial statements are based, in the case of special purpose

financial statements prepared in accordance with a contractual basis of

accounting.

AU-C 800.11c N/A b

• Additional disclosures beyond those specifically required by the framework

that may be necessary for the special purpose financial statements to achieve

fair presentation.

AU-C 800.11d N/A b

Considerations When Planning and Performing the Audit

AU-C 200, Overall Objective of the Independent Auditor and the Conduct of an

Audit in Accordance With Generally Accepted Auditing Standards, requires the

auditor to comply with all AU-C sections pertinent to the audit. Accordingly, in

planning and performing an audit of special purpose financial statements, the

AU-C 800.12 AU 623.02

Page 8 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

Requirements/Guidance Clarified AU-

C Reference

Pre-clarified

Reference

auditor should adapt and apply all AU-C sections relevant to the audit as

necessary in the circumstances of the engagement.

AU-C 300, Understanding the Entity and Its Environment and Assessing the Risks

of Material Misstatement, requires the auditor to obtain an understanding of the

entity's selection and application of accounting policies. In the case of special

purpose financial statements prepared in accordance with a contractual basis of

accounting, the auditor should obtain an understanding of any significant

interpretations of the contract that management made in the preparation of those

financial statements. An interpretation is significant when adoption of another

reasonable interpretation would result in a material difference in the information

presented in the financial statements.

AU-C 800.13 N/A b

Forming an Opinion and Reporting Considerations

When forming an opinion and reporting on special purpose financial statements,

the auditor should apply the requirements of AU-C 700, Forming an Opinion and

Reporting on Financial Statements. When, in forming an opinion, the auditor

concludes that a modification to the auditor's opinion on the financial statements is

necessary, the auditor should apply the requirements of AU-C 705, Modifications

to the Opinion in the Independent Auditor's Report.

AU-C 800.14 AU 544.04; AU

623.05-.06

AU-C 700 requires the auditor to evaluate whether the financial statements

adequately refer to or describe the applicable financial reporting framework. In an

audit of special purpose financial statements, the auditor should evaluate whether

the financial statements are suitably titled, include a summary of significant

accounting policies, and adequately describe how the special purpose framework

differs from GAAP. The effects of these differences need not be quantified.

AU-C 800.15 AU 623.07; AU

623.10

In the case of special purpose financial statements prepared in accordance with a

contractual basis of accounting, the auditor should also evaluate whether the

financial statements adequately describe any significant interpretations of the

contract on which the financial statements are based.

AU-C 800.16 N/A b

AU-C 700 requires the auditor to evaluate whether the financial statements

achieve fair presentation. In an audit of special purpose financial statements when

the special purpose financial statements contain items that are the same as, or

similar to, those in financial statements prepared in accordance with GAAP, the

auditor should evaluate whether the financial statements include informative

disclosures similar to those required by GAAP. The auditor should also evaluate

whether additional disclosures, beyond those specifically required by the

framework, related to matters that are not specifically identified on the face of the

financial statements or other disclosures are necessary for the financial

statements to achieve fair presentation.

AU-C 800.17 AU 623.09-.10

AU-C 700 addresses the form and content of the auditor's report. In the case of an

auditor's report on special purpose financial statements—

AU-C 800.18 AU 623.05

• The explanation of management's responsibility for the financial statements

should also make reference to its responsibility for determining that the

applicable financial reporting framework is acceptable in the circumstances,

when management has a choice of financial reporting frameworks in the

preparation of such financial statements.

AU-C 800.18a N/A b

• The auditor's report should also describe the purpose for which the financial

statements are prepared or refer to a note in the special purpose financial

statements that contains such information, when the financial statements are

prepared in accordance with a regulatory or contractual basis of accounting.

AU-C 800.18b AU 623.05 c

Page 9 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

Requirements/Guidance Clarified AU-

C Reference

Pre-clarified

Reference

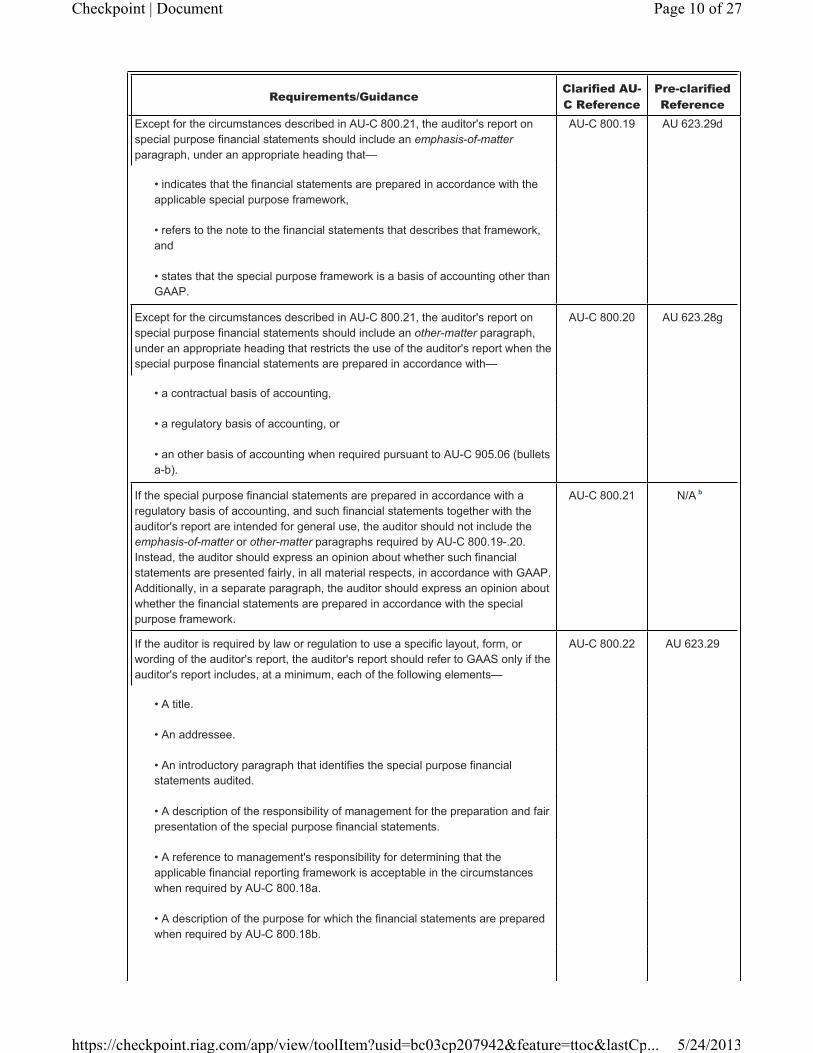

Except for the circumstances described in AU-C 800.21, the auditor's report on

special purpose financial statements should include an emphasis-of-matter

paragraph, under an appropriate heading that—

AU-C 800.19 AU 623.29d

• indicates that the financial statements are prepared in accordance with the

applicable special purpose framework,

• refers to the note to the financial statements that describes that framework,

and

• states that the special purpose framework is a basis of accounting other than

GAAP.

Except for the circumstances described in AU-C 800.21, the auditor's report on

special purpose financial statements should include an other-matter paragraph,

under an appropriate heading that restricts the use of the auditor's report when the

special purpose financial statements are prepared in accordance with—

AU-C 800.20 AU 623.28g

• a contractual basis of accounting,

• a regulatory basis of accounting, or

• an other basis of accounting when required pursuant to AU-C 905.06 (bullets

a-b).

If the special purpose financial statements are prepared in accordance with a

regulatory basis of accounting, and such financial statements together with the

auditor's report are intended for general use, the auditor should not include the

emphasis-of-matter or other-matter paragraphs required by AU-C 800.19-.20.

Instead, the auditor should express an opinion about whether such financial

statements are presented fairly, in all material respects, in accordance with GAAP.

Additionally, in a separate paragraph, the auditor should express an opinion about

whether the financial statements are prepared in accordance with the special

purpose framework.

AU-C 800.21 N/A b

If the auditor is required by law or regulation to use a specific layout, form, or

wording of the auditor's report, the auditor's report should refer to GAAS only if the

auditor's report includes, at a minimum, each of the following elements—

AU-C 800.22 AU 623.29

• A title.

• An addressee.

• An introductory paragraph that identifies the special purpose financial

statements audited.

• A description of the responsibility of management for the preparation and fair

presentation of the special purpose financial statements.

• A reference to management's responsibility for determining that the

applicable financial reporting framework is acceptable in the circumstances

when required by AU-C 800.18a.

• A description of the purpose for which the financial statements are prepared

when required by AU-C 800.18b.

Page 10 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

Requirements/Guidance Clarified AU-

C Reference

Pre-clarified

Reference

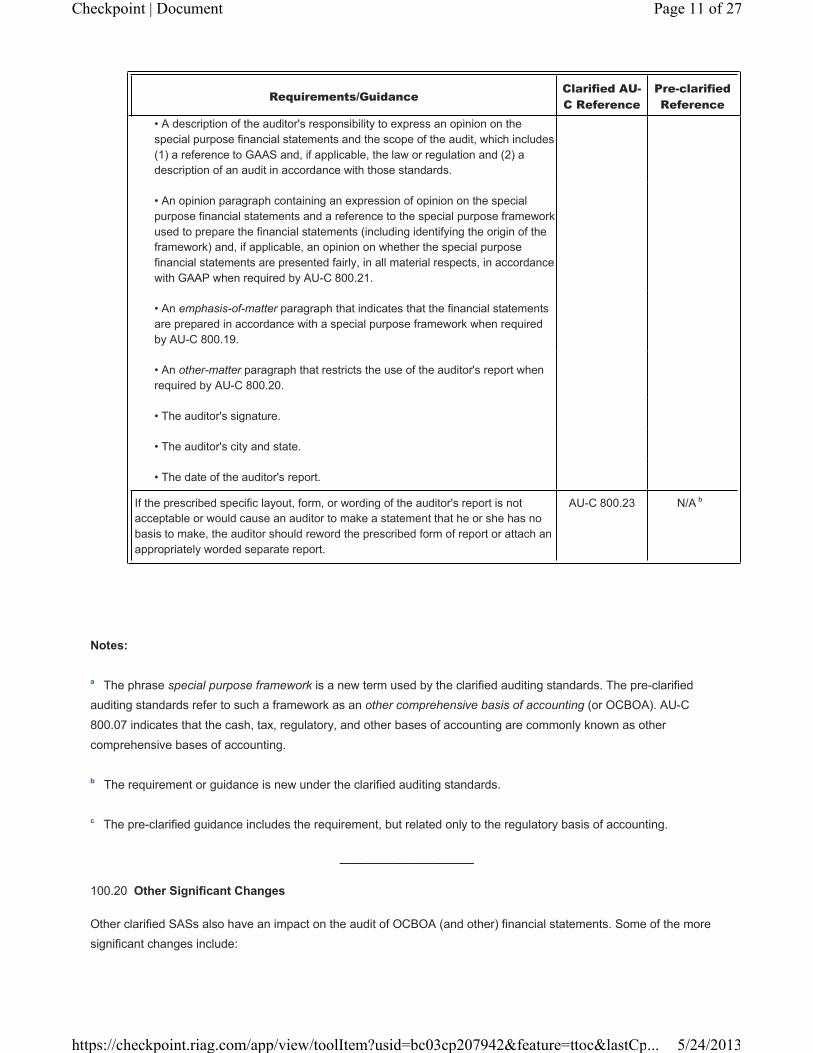

• A description of the auditor's responsibility to express an opinion on the

special purpose financial statements and the scope of the audit, which includes

(1) a reference to GAAS and, if applicable, the law or regulation and (2) a

description of an audit in accordance with those standards.

• An opinion paragraph containing an expression of opinion on the special

purpose financial statements and a reference to the special purpose framework

used to prepare the financial statements (including identifying the origin of the

framework) and, if applicable, an opinion on whether the special purpose

financial statements are presented fairly, in all material respects, in accordance

with GAAP when required by AU-C 800.21.

• An emphasis-of-matter paragraph that indicates that the financial statements

are prepared in accordance with a special purpose framework when required

by AU-C 800.19.

• An other-matter paragraph that restricts the use of the auditor's report when

required by AU-C 800.20.

• The auditor's signature.

• The auditor's city and state.

• The date of the auditor's report.

If the prescribed specific layout, form, or wording of the auditor's report is not

acceptable or would cause an auditor to make a statement that he or she has no

basis to make, the auditor should reword the prescribed form of report or attach an

appropriately worded separate report.

AU-C 800.23 N/A b

Notes:

a The phrase special purpose framework is a new term used by the clarified auditing standards. The pre-clarified

auditing standards refer to such a framework as an other comprehensive basis of accounting (or OCBOA). AU-C

800.07 indicates that the cash, tax, regulatory, and other bases of accounting are commonly known as other

comprehensive bases of accounting.

b The requirement or guidance is new under the clarified auditing standards.

c The pre-clarified guidance includes the requirement, but related only to the regulatory basis of accounting.

____________________

100.20 Other Significant Changes

Other clarified SASs also have an impact on the audit of OCBOA (and other) financial statements. Some of the more

significant changes include:

Page 11 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

• New audit reports. The new authoritative guidance for reporting is covered by several clarified SASs including,

Forming an Opinion and Reporting on Financial Statements, Modifications to the Opinion in the Independent

Auditor's Report, and Emphasis-of-Matter Paragraphs and Other-Matter Paragraphs in the Independent Auditor's

Report. The audit report will look quite different once the clarified SASs are effective.

• Changes to the engagement letter. The clarified SAS, Terms of Engagement, provides certain changed

requirements for the written agreement between the auditor and company management.

• Revisions to the management representation letter. The clarified SAS, Written Representations, supersedes

SAS No. 85 and provides changes to the management representation letter.

100.21 See the discussion beginning at paragraph 100.16 for an explanation of how the clarified auditing standards

have been incorporated within the Guide. Chapter text as well as the illustrative reports, engagement letters,

management representation letters, and all other impacted forms and checklists have been revised to comply with the

clarified auditing standards.

Clarified SSARS Project

100.22 Proposed Clarified SSARS, Association With Unaudited Financial Statements

There is currently a hole in the SSARS literature, as the guidance in AR 100.03 was not carried forward by SSARS No.

19. Once the clarified auditing standards become effective for audits of periods ending on or after December 15, 2012,

there will also be a hole in the auditing literature. Since May 2010, the ARSC has been working on a standard that will

address “association.” Most recently, at the ARSC's May 2012 meeting, a proposed SSARS, Association With

Unaudited Financial Statements, was discussed. The SSARS Association ED was voted for exposure and exposed in

June 2012. Comments are requested by November 30, 2012.

100.23 The new proposed SSARS addresses the accountant's responsibility when the accountant is associated with

financial statements that have not been compiled, reviewed, or audited (i.e., unaudited financial statements). The

accountant is considered to be associated with the unaudited financial statements when:

• The accountant permits the use of the accountant's name in a report, document, or written communication

containing unaudited financial statements that have not been prepared in whole or part by the accountant, or

• The accountant prepares, in whole or in part, unaudited financial statements for the entity, even though the

accountant does not append his or her name to the unaudited financial statements.

100.24 When the accountant's name is associated with unaudited financial statements the accountant did not prepare,

the accountant should:

a. Read the unaudited financial statements.

Page 12 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

b. Consider whether the statements appear free from material inconsistencies with other knowledge or information

of which the accountant may be aware.

c. After performing a. and b., if the accountant decides to allow the use of the accountant's name, the accountant

should request that the entity clearly indicate that the financial statements were not compiled, reviewed, or

audited.

100.25 When the accountant's name is associated with unaudited financial statements the accountant prepared and

the client did not engage the accountant to perform a compilation or review, the accountant should request that the

entity clearly indicate that the financial statements were not compiled, reviewed, or audited.

100.26 This proposed SSARS is expected to be effective for unaudited financial statements with which the accountant

is associated on or after December 15, 2014. Early implementation will be required if the accountant early implements

the proposed revised Interpretation No. 101-3, “Nonattest Services.” (See the discussion of the proposed changes to

ET 101-3 in section 902.) Otherwise, early implementation would be permitted. As of the date of this Guide, ARSC

plans to vote this SSARS final in February 2013. Accountants can monitor the status of this project at www.aicpa.org.

100.27 Clarified SSARS, Compilation of Financial Statements, Exposure Draft

ARSC has exposed clarified compilation standards that, if approved, would be effective for compilations of financial

statements of periods ending on or after December 15, 2014. Early implementation is required if the accountant early

implements the proposed revised Interpretation No. 101-3, “Nonattest Services.” (See the discussion of the proposed

changes to ET 101-3 in section 902.) Otherwise, early implementation would not be permitted. The exposure draft

would supersede AR 60, AR 80, AR 110, AR 300, and AR 600.

100.28 Some of the more significant changes from current compilation standards include the following—

• Changing the Standard to be engagement driven versus submission driven. The proposed SSARS would only

require a compilation if the accountant is engaged to perform that service. This means an accountant can prepare

financial statements, submit them to his or her clients, and, if they are not engaged to compile, they do not have to

follow the compilation standard. This change is consistent with the proposed changes to ET 101-3 discussed in

section 902 that would clarify that preparing financial statements is a nonattest service.

• Separating the normal recurring compilation guidance and the more specialized compilation guidance into

separate sections. The proposed SSARS would result in AR 70, Association with Unaudited Financial Statements;

AR 80, Compilation of Financial Statements (Revised); and AR 85, Compilation of Financial Statements—Special

Considerations.

• Separating requirements from application and other explanatory material. This is consistent with the format used

for the recent clarified auditing standards.

Page 13 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

• Distinguishing between emphasis-of-matter and other-matter paragraphs and designating when these types of

paragraphs should be used.

• Requiring an emphasis-of-matter paragraph when the financial statements have been prepared in accordance

with a special purpose framework.

• Changing the term OCBOA to special purpose framework to be consistent with the auditing standards.

• Changing all reports. In addition to using sections with headings, the accountant's compilation report should

name the city and state of the issuing office.

• If the financial statements are prepared in accordance with an OCBOA (or a contractual basis of accounting) and

omit substantially all disclosures, the report must highlight in a separate paragraph that the OCBOA (or the

contractual basis of accounting) is different than GAAP. If such financial statements include disclosures, the report

should reference the note to the financial statements that describes the OCBOA (or contractual basis of

accounting). Also, there are additional reporting requirements if management of the entity has a choice of financial

reporting frameworks or when the financial statements are prepared in accordance with a regulatory or contractual

basis of accounting.

• Engagement letters must be signed by the accountant or accounting firm and management or those charged

with governance.

100.29 Future editions of this Guide will update the status of this exposure draft. Accountants may also monitor the

SSARS Clarity Project at www.aicpa.org.

100.30 Proposed Clarified SSARS, Review of Financial Statements

The ARSC is also currently working on a proposed clarified review standard. An exposure draft is expected in late

2012. The clarified review SSARS is expected to be effective for reviews of financial statements for periods ending on

or after December 15, 2014.

OCBOA and Accounting Standards Overload

100.31 On and off for decades, the AICPA has examined the issue of standards overload. A solution often mentioned

is the use of OCBOA financial statements. One of the earliest examinations was performed by the AICPA's Special

Committee on Accounting Standards Overload. In 1981, that committee was formed to consider alternative means of

Page 14 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

providing relief from accounting standards that were not cost-effective, particularly for small, closely held companies.

In its final report published in 1983, the committee concluded:

Small, nonpublic entities can gain some measure of relief from accounting standards overload by issuing

compiled, reviewed, or audited financial statements prepared on a comprehensive basis of accounting

other than GAAP in accordance with existing disclosure and measurement standards and with the

existing reporting requirements for CPAs.

100.32 In 1995, the Private Companies Practice Section of the AICPA appointed the Special Task Force on Standards

Overload. Recognizing the increasing use of OCBOA and the confusion surrounding required disclosures (especially

in light of “disclosure only” accounting standards), the committee's August 1996 report included a recommendation that

standard setters provide more specific guidance on disclosures in OCBOA financial statements. In response to that

request, the Audit Issues Task Force of the Auditing Standards Board issued Interpretation 14 of AU 623.

100.33 Private Company Financial Reporting Task Force Report

In 2004, the AICPA appointed a Private Company Financial Reporting Task Force to gather information regarding the

needs of users of financial statements of larger or public entities versus the needs of users of financial statements of

smaller, nonpublic entities. The Task Force conducted a survey which found that certain types of financial statement

users were more likely to accept OCBOA financial statements for privately-held, for-profit companies. Specifically, 93%

of creditor/lenders, 72% of surety/bonding firms, and 58% of investor/venture capital firms have accepted OCBOA

financial statements. The survey also indicated that the size of the company is a factor in the decision to accept

OCBOA financial statements for the majority of the financial statement users that do accept them.

100.34 The Task Force concluded that GAAP should specifically address the needs of private company financial

statement users. That conclusion was based on findings that indicated many GAAP requirements are not relevant for

nonpublic companies and, in some cases, it would be more useful to require different accounting for nonpublic entity

transactions. As a result of those findings, the AICPA and FASB began working together to explore the development of

accounting standards for privately held companies. In 2006, the two organizations issued a joint proposal intended to

improve the financial reporting process for private companies. Subsequently, a joint committee was formed (the

Private Company Financial Reporting Committee) to serve as a resource to the FASB to ensure that the views of

private company constituents were considered during the standard-setting process. The Private Company Financial

Reporting Committee (PCFRC) began making recommendations regarding accounting standards proposals to the

FASB in 2007.

100.35 Blue Ribbon Panel

In December 2009, the AICPA and the Financial Accounting Foundation (FAF) announced the formation of the Blue

Ribbon Panel to address how U.S. accounting standards can best meet the needs of users of private company

financial statements. The purpose of the panel was to provide recommendations on the future of standard setting for

private companies, including whether separate, standalone accounting standards for private companies are needed.

After a series of meetings were held in 2010, the Blue Ribbon Panel delivered its report to the FAF early in 2011. The

report called for fundamental changes to the system of standard setting, including creating a new board to be

overseen by the FAF that would focus on making exceptions and modifications to U.S. GAAP for private companies

that better respond to the needs of the private company sector. The report also recommended the creation of a

differential framework (that is, a set of decision criteria) to facilitate a standard setter's ability to make appropriate,

justifiable exceptions and modifications. The FAF then embarked on an outreach program and released its proposal in

Page 15 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

the fall of that year. Roundtable meetings were held during the first quarter of 2012 for additional input and, in May

2012, the FAF announced its decision to establish the Private Company Council.

100.36 Private Company Council

At the time this Guide was completed, the Private Company Council (PCC) was still in the process of being formed. In

June 2012, the FAF issued a request for nominations for candidates to serve on the PCC and over 100 nominations

were received. At the present time, the FAF Board of Trustees continues to review the candidates nominated.

100.37 The PCC membership will ultimately comprise individuals with backgrounds and experience in using,

preparing, and auditing private company financial statements, including—

• users of private company financial statements, including bank lenders, equity investors, and/or sureties,

• preparers of private company financial statements from a variety of industries and companies of various sizes,

and

• CPA practitioners from national, regional, and local firms.

100.38 The responsibilities of the PCC will be two-fold:

a. To determine whether modifications or exceptions to existing nongovernmental U.S. GAAP are required to

address the needs of users of private company financial statements based on criteria mutually agreed to by the

PCC and the FASB.

b. To serve as the primary advisory body to the FASB on the appropriate treatment for private companies for

items under active consideration on the FASB's technical agenda.

100.39 FASB Private Company Decision-making Framework

In response to the Blue Ribbon Panel's recommendation, the FAF instructed the FASB to undertake a differential

framework project (see the discussion in paragraph 100.35), which the FASB is now calling its private company

decision-making framework project. The objective of the project is to develop a framework (set of decision criteria) for

making decisions about whether and when to adjust the requirements for recognition, measurement, presentation,

disclosure, effective dates, and transition methods for financial accounting standards that apply to private companies.

The creation of the PCC is an integral part of this FASB project. At the end of July 2012, the FASB released its initial

staff recommendations on whether and when it will be appropriate to adjust financial reporting requirements for private

companies. The recommendations are contained in a paper entitled, Private Company Decision-Making Framework: A

Framework for Evaluating Financial Accounting and Reporting Guidance for Private Companies, and the FASB has

issued an invitation to comment on the recommendations. The comment period will be open through October 31,

2012.

Page 16 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

100.40 The FASB and the PCC must first agree on the proposed decision-making framework before it will be

implemented. The framework will guide the PCC as it determines whether any modifications or exceptions to existing

GAAP are needed for private companies. Further information about this project and a link to the initial staff's

recommendations can be accessed from the FASB's Project page at www.fasb.org.

100.41 AICPA Financial Reporting Framework for Small- and Medium-sized Entities

In May 2012, the AICPA announced its plans to develop an other comprehensive basis of accounting financial

reporting framework (FRF) to meet the needs of certain privately held small- and medium-sized entities (SMEs), as

well as the users of those entities' financial statements. The AICPA envisions that this SME framework will provide a

less complicated and less costly system of accounting for SMEs that do not need GAAP financial statements. Since

the AICPA announced its development of the FRF for SMEs, it has published a short question-and-answer document

about the framework, which is available on the Private Company Financial Reporting page of the AICPA website at

www.aicpa.org. At the time this Guide was completed, the AICPA had indicated that a draft version of the framework

is scheduled for release in the fourth quarter of 2012, with the finalized framework expected in the first half of 2013. It

is anticipated that the FRF for SMEs will meet the criteria for the other basis type of OCBOA mentioned in paragraph

100.2 and discussed further beginning at paragraph 602.8.

International Financial Reporting Standards

100.42 In 2008, the Council of the AICPA designated the International Accounting Standards Board as the body to

establish international financial reporting standards for both private and public entities pursuant to Rule 202,

Compliance With Standards, and Rule 203, Accounting Principles, of the AICPA Code of Professional Conduct. This

gives AICPA members the option of using International Financial Reporting Standards as an alternative to U.S.

generally accepted accounting principles. This Guide is not designed to address issues related to financial statements

prepared in accordance with International Financial Reporting Standards.

1 There is an ongoing debate within the profession about whether accountants need to be thoroughly versed in GAAP

before they can prepare OCBOA financial statements. Because presentations and disclosures similar to GAAP may be

required or, at the very least, be necessary to make OCBOA presentations useful to readers, the authors believe

accountants should not accept an engagement to prepare OCBOA financial statements unless they have a good

foundation in generally accepted accounting principles.

2 Other basis was not included in AU-C 800 when it was originally issued. It will be added as part of a proposed SAS,

Omnibus Statement on Auditing Standards—2012, exposed at the end of August 2012 and expected to be effective at

the same time as the original AU-C 800 (that is, for audits of financial statements for periods ending on or after

December 15, 2012). Throughout this Guide, the authors have assumed that the use of the other basis will be allowed

as proposed. Practitioners can monitor the status of this exposure draft on the AICPA's website at www.aicpa.org.

© 2012 Thomson Reuters/PPC. All rights reserved.

END OF DOCUMENT -

© 2013 Thomson Reuters/RIA. All rights reserved.

Page 17 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

Checkpoint Contents

Accounting, Audit & Corporate Finance Library

Editorial Materials

Accounting and Financial Statements (US GAAP)

Cash, Tax, and Other Bases of Accounting

Chapter 1 An Introduction to OCBOA Financial Statements

101 Deciding When to Use a Special Purpose Framework

101 Deciding When to Use a Special Purpose Framework

101.1 Special purpose framework, or OCBOA, financial statements are beneficial to clients for many reasons.

Because accountants do not need to consider the measurement requirements of GAAP, OCBOA financial statements

often can be prepared on a more timely basis and at less cost to the client. For example, if depreciation is the only

difference between GAAP and the client's tax basis, using the income tax basis can eliminate the need to prepare two

sets of depreciation schedules. OCBOA financial statements also may provide information in a format familiar to the

client. For example, cash basis financial statements can answer the basic question “Where did the money go?”

101.2 The AICPA's Compilation and Review Alert—1996/1997 provided the following guidance on characteristics of

entities that generally are good candidates for cash or tax basis financial statements:

a. There are no third-party users of the financial statements (for example, the entity is a small closely held

business with no third-party debt).

b. The entity's debt is secured rather than unsecured.

c. The entity's creditors do not require GAAP financial statements.

d. The cost of complying with GAAP would exceed the benefits (for example, a small construction contractor who

would be required to account for long-term contracts using the percentage of completion method and would be

required to compute deferred taxes).

e. The owners and managers are closely involved in the day-to-day operations of the business and have a fairly

accurate picture of the entity's financial position.

Page 18 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

f. The business's owners are primarily interested in cash flows (for example, a professional corporation of

physicians that distributes its cash basis earnings through salaries, bonuses, and retirement plan contributions).

g. The owners are primarily interested in the tax implications of transactions (for example, partners in a

partnership who are concerned about the effects of transactions on their personal tax returns).

h. Capital expenditures and long-term financing are not significant.

i. Internal Revenue Code rules do not require the entity to prepare its tax return on the accrual basis of accounting

(for example, an entity that does not have material inventories or does not have average gross receipts that

exceed $10 million for the prior three years). 3

101.3 There are instances in which OCBOA financial statements are not appropriate, however. The entity may have

substantial unfunded obligations or commitments not recorded on the income tax basis (because they are not

deductible until paid) or the cash basis (because they have not been paid). For example, under the accrual income tax

basis (a) pension liabilities are recorded at the amount determined to be deductible, (b) leases are recorded under IRC

rules, (c) deferred compensation is recognized when paid, (d) potential environmental liabilities are recorded only

when they meet the economic performance and all events tests of the Internal Revenue Code, and (e) interest due to

a related party cannot be accrued and deducted. When such conditions exist, accountants should consider whether

the financial statements prepared using an OCBOA could be misleading—especially if the financial statements omit

substantially all disclosures.

101.4 In advising a client about the use of OCBOA financial statements, accountants must have a clear idea about the

user's needs. Perhaps a banker can use a cash basis financial statement generated by the client's computer system if

the entity accompanies it with an aged accounts receivable listing. On the other hand, an absentee owner may be able

to use compiled cash basis financial statements that omit substantially all disclosures on an interim basis but needs full

disclosure GAAP statements at year end. Companies reporting financial results to third parties ordinarily use GAAP for

financial statements. The use of GAAP promotes comparability among financial statements, and users become

familiar with GAAP through experience with it. Additionally, loan covenants may require GAAP financial statements

and failure to provide such statements may result in a loan default.

Considerations When Accepting an Audit Engagement

101.5 Is the Financial Reporting Framework Acceptable?

Under the clarified auditing standards (AU-C 210, Terms of Engagement), the auditor is required to determine whether

the financial reporting framework used in the preparation of the entity's financial statements is acceptable. AU-C

800.10 refers to that requirement and further indicates that when performing an audit of special purpose financial

statements, the auditor should obtain an understanding of—

a. The purpose for which the financial statements are prepared.

Page 19 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

b. The intended users of the financial statements.

c. The steps management has taken to determine that the applicable financial reporting framework is acceptable

in the circumstances.

101.6 In contrasting the above requirement in AU-C 800.10 to the guidance in SAS No. 62, no such requirement exists

in the pre-clarified auditing standards for the auditor to consider whether the OCBOA is an acceptable framework for

presenting and reporting on the financial statements. Accordingly, prior to the effective date of the clarified auditing

standards (that is, for audits of financial statements for periods ending on or after December 15, 2012), the new

requirements of AU-C 800.10 do not have to be followed. However, the new requirement in AU-C 800.10 is effective

for 2012 calendar year-end audit engagements.

101.7 AU-C 800.A6-.A9 provides further information about AU-C 800.10 indicating that the following factors could be

used by the auditor when he or she considers whether the specific type of special purpose framework applied in the

preparation of the financial statements is acceptable—

• The financial information needs of the intended users.

• Whether the special purpose framework applied to the financial statements encompasses financial reporting

standards that have been established by an authorized standard-setting organization that follows an established

and transparent process, for example, the AICPA or the FASB. When such is the case, the financial reporting

standards that support the special purpose framework applied will be presumed acceptable.

• When the financial reporting framework applied is required by law or regulation to be used in the preparation of

the entity's special purpose financial statements, such a financial reporting framework is presumed acceptable

(unless indications to the contrary exist). For example, this type of situation often occurs when a regulator

establishes financial reporting provisions that must be met by those entities that it regulates.

• Whether the financial reporting framework applied exhibits attributes normally exhibited by acceptable financial

reporting frameworks. However, for special purpose frameworks, the relative importance to a particular

engagement of each of the attributes normally exhibited by acceptable financial reporting frameworks is a matter

of professional judgment.

• For financial statements prepared in accordance with a contractual basis of accounting, the parties to the

contract might agree on significant interpretations of the contract, if any, that are the basis of the special purpose

Page 20 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

framework. If the parties cannot reach agreement, the auditor may determine that the framework is not

acceptable.

101.8 Preconditions for an Audit Engagement

Under the clarified auditing standards (AU-C 210), the auditor is required to establish whether certain preconditions for

an audit are present, including whether the financial reporting framework to be used in the preparation of the financial

statement is acceptable. 4 In performing an audit of special purpose financial statements, AU-C 800.11 refers to the

requirement in AU-C 210 and further requires the auditor to obtain managements' agreement that it acknowledges and

understands its responsibility to include all information disclosures that are appropriate for the special purpose

framework used to prepare the entity's financial statements. These precondition requirements are further discussed in

section 904.

When Is Each Basis Appropriate?

101.9 Absent specific guidance from financial statement users, accountants need to consider issues such as the

following before advising a client about which presentation to use.

• Does the Entity Have Inventory? If so, the pure cash basis may not be helpful.

• What Basis of Accounting Does the Entity Use in Preparing Its Income Tax Returns? If the accrual basis is used,

preparing financial statements on the same basis makes sense.

• Is the Entity Highly Leveraged? Lenders may require GAAP financial statements.

• Are There Outside Investors? GAAP financial statements may provide information needed by such users.

• Does the Entity's Cash Flow Parallel Its Income and Expenses? The pure cash basis may be appropriate.

• Does the Entity Anticipate Going Public? If so, the entity will need a history of GAAP financial statements.

• Was the Entity Formed for Tax Purposes? If the answer is yes, the owners probably are interested in the tax

effects of transactions, and the income tax basis would be appropriate.

• Is the Entity Subject to Bonding Requirements? Many bonding companies will only accept GAAP financial

statements.

Page 21 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

101.10 Cash and Modified Cash Bases

In practice, use of the pure cash basis is rare. Generally, it is limited to nonbusiness entities with very simple

operations. Entities that might use the pure cash basis of accounting include school activity funds, fairs and other civic

ventures, trusts and estates, political action committees, and political campaigns.

101.11 Use of the modified cash basis is more common. To help provide some consistency in its use, however, the

authors recommend limiting it to entities whose operations are:

a. oriented toward cash receipts and disbursements,

b. not significantly influenced by financing of sales or purchases, and

c. relatively simple and without complexities (such as manufacturing, development, or other conversion activities

or acquisitions of property and equipment) that require significant modifications.

Chapter 4 discusses both the cash basis and the modified cash basis in further detail.

101.12 Tax Basis

Typically, entities that use the tax basis of accounting are either profit-oriented enterprises (such as small closely held

companies for which conversion to GAAP would be costly), partnerships whose partnership agreements require the

use of the tax basis of accounting, or nonprofit organizations seeking relief from the requirements of GAAP.

101.13 Regulatory and Contractual Basis

Regulatory basis financial statements are prepared by many types of entities, including insurance companies, credit

unions, construction contractors, certain state and local governmental entities, and some nonprofit organizations.

Contractual basis financial statements are prepared when an entity follows the provisions of a contract or agreement,

which often requires at least some unique financial reporting calculations. Due to the unique provisions in the contract

or agreement, it is common that interpretation is necessary with regard to measurement principles for the contractual

basis.

101.14 Other Basis

As explained at paragraph 100.18, AU-C 800 defines the other basis slightly different than SAS No. 62 does. The

phrase “having substantial support,” and the price-level basis of accounting example provided in SAS No. 62, no

longer exists under AU-C 800. As the price-level basis of accounting is not included in AU-C 800 and the authors

believe the price-level basis has not been used in practice for some time, this Guide no longer discusses the price-

level basis.

101.15 Additionally, as explained in the footnote to paragraph 100.2, the acceptability of an other basis was not

provided by AU-C 800 when it was originally issued. However, it has been added as part of a proposed SAS, Omnibus

Page 22 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

Statement on Auditing Standards—2012, exposed at the end of August 2012 and expected to be effective at the same

time as the original AU-C 800 (that is, for audits of financial statements for periods ending on or after December 15,

2012). The authors assume that the use of the other basis will be allowed as proposed. It is anticipated that the FRF

for SMEs discussed at paragraph 100.41 will meet the criteria for the other basis type of special purpose framework.

Cost-effective Alternatives for Clients

101.16 As discussed in paragraph 101.1, OCBOA financial statements are one option for providing more timely

information at less cost to some clients. The following paragraphs discuss some additional options to consider when

recommending a level of service to a client. For certain clients, these options may offer cost-effective means of

meeting a client's needs.

101.17 Using OCBOAs for Interim Financial Statements and GAAP for Annual Financial Statements

One option that accountants may want to consider for some clients is using OCBOAs for preparing interim financial

statements and GAAP for preparing annual statements. Some accountants find that this is both efficient and cost

effective. Considerations when preparing and reporting on interim OCBOA financial statements are discussed in

Chapter 10.

101.18 Issuing Management-use-only Financial Statements

If financial statements are intended for management's use only, 5 accountants may be able to compile the statements

and issue an engagement letter in lieu of a compilation report. Although the engagement letter should preferably be

signed by management and include various required elements, it is not required to detail departures from GAAP or

OCBOA. Many accountants view the requirement to do so in a compilation report one of the most time-consuming

procedures of a compilation engagement. Therefore, issuing management-use-only financial statements without a

report can be easier and less costly than compiling financial statements and issuing a SSARS No. 19 compilation

report. See the discussion of management-use-only financial statements beginning at paragraph 903.18. (Engagement

letters for management-use-only financial statements are discussed beginning at paragraph 904.6.)

101.19 Compiling Financial Statements That Omit Substantially All Disclosures

If a client does not feel that full disclosure statements are cost-effective, then the accountant may compile financial

statements that omit substantially all of the disclosures required by an OCBOA as long as the accountant's report

discloses the omission, and the omission is not, to his or her knowledge, undertaken to mislead those who might

reasonably be expected to use the financial statements. If the financial statements are intended for third-party use, the

accountant should modify the report to alert users to the lack of disclosures. 6 If the financial statements are intended

for management's-use-only, the required engagement letter should include a statement that substantially all

disclosures have been omitted and a statement that material departures from GAAP or OCBOA may exist and the

effects of those departures, if any, on the financial statements may not be disclosed. See the discussion on reporting

on financial statements that omit substantially all disclosures beginning at paragraph 701.12.

101.20 Combining Alternatives to Create the Best Level of Service for the Client

The accountant may wish to consider whether some combination of these alternatives provides the best level of

service for a client. One popular option was discussed in the AICPA's Compilation and Review Alert—1999/2000. That

alert stated that to reduce the costs of preparing the financial statements and the compilation report, many CPAs:

a. Use the cash or modified cash basis of accounting for monthly financial statements.

Page 23 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

b. Omit all disclosures on those monthly financial statements.

c. Generate annual GAAP financial statements with disclosures.

Considerations when preparing and reporting on interim OCBOA financial statements are discussed in Chapter 10 of

this Guide.

Planning Form for Engagements Involving OCBOA Financial Statements

101.21 Appendix 1A provides a planning questionnaire that may be used to determine whether an OCBOA is

appropriate.

3 The IRC allows qualifying small business taxpayers to change to the cash method if they have average annual

gross receipts of $10,000,000 or less. See discussion at paragraph 500.12 for more information.

4 The phrase in this sentence beginning with the word including was added to AU-C 800 as part of a proposed SAS,

Omnibus Statement on Auditing Standards—2012, exposed at the end of August 2012 and expected to be effective at

the same time as the original AU-C 800 (that is, for audits of financial statements for periods ending on or after

December 15, 2012). Throughout this Guide, the authors have assumed that changes made to AU-C 800 by the

proposed SAS will be finalized as proposed. Practitioners can monitor the status of this exposure draft on the AICPA's

website at www.aicpa.org.

5 SSARS No. 19 (AR 60.04) defines management as “the person(s) with executive responsibility for the conduct of

the entity's operations. For some entities, management includes some or all of those charged with governance (for

example, executive members of a governance board or an owner-manager).” Management-use-only financial

statements are only appropriate for use by individuals meeting this definition of management. Considering the

intended use of the financial statement(s) is discussed further beginning at paragraph 903.18. See the discussion of

the clarified SSARS project that would impact compilations of management-use-only financial statements beginning at

paragraph 100.22.

6 This discussion regarding compilation reports of compiled financial statements with substantially all disclosures

omitted would change pursuant to the clarified compilation standards recently exposed by the ARSC. See the

discussion of the clarified SSARS project beginning at paragraph 100.22.

© 2012 Thomson Reuters/PPC. All rights reserved.

END OF DOCUMENT -

© 2013 Thomson Reuters/RIA. All rights reserved.

Page 24 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

Checkpoint Contents

Accounting, Audit & Corporate Finance Library

Editorial Materials

Accounting and Financial Statements (US GAAP)

Cash, Tax, and Other Bases of Accounting

Chapter 1 An Introduction to OCBOA Financial Statements

102 Primary Issues in Preparing OCBOA Financial Statements

102 Primary Issues in Preparing OCBOA Financial Statements

Recognition and Measurement

102.1 Transactions are recognized and measured in financial statements based on the basis of accounting used.

Thus, cash basis financial statements do not recognize or measure transactions until cash is received or paid.

Modified cash basis financial statements reflect transactions similarly except for certain transactions the entity elects to

recognize and measure otherwise (for example, capitalizing property and equipment and charging their costs to

expense over the periods benefited rather than expensing them in the period purchased). Income tax basis financial

statements recognize transactions when they would be recognized in the entity's tax return, and then measure them

based on amounts that would be reported in the return. GAAP recognition and measurement principles, such as the

requirement of FASB ASC 715-30-25-1 to recognize an asset or a liability for the funded status of a defined benefit

pension plan, are not considered in OCBOA presentations (except to the extent the cash basis has been modified to

adopt GAAP principles).

102.2 Recognizing and measuring transactions under the cash or modified cash basis is discussed in Chapter 4 of this

Guide. Chapter 5 discusses measurement and recognition principles that apply to tax basis financial statements, and

Chapter 6 discusses considerations for financial statements prepared on other bases of accounting.

Presentation

102.3 While transactions are recognized and measured following the OCBOA, they generally should be presented in

financial statements following GAAP presentation guidelines. That is, assets and liabilities should be presented in the

statement of financial position and revenues and expenses (measured in accordance with the OCBOA) should be

presented in the statement of operations. Furthermore, changes in retained earnings and other components of

stockholders' equity generally should be presented following GAAP requirements. 7 As discussed further in Chapter 3,

however, OCBOA disclosures should be similar, but not necessarily identical to, those required by GAAP. Thus, items

required to be presented on the face of GAAP financial statements sometimes may be disclosed in the notes to

OCBOA financial statements so long as the substance of the GAAP information is communicated.

102.4 Since cash basis and tax basis financial statements do not purport to present financial position and results of

operations in accordance with GAAP, they should not be captioned or otherwise referred to as “Balance Sheet,”

“Income Statement,” etc. without appropriate modification. Such titles as “Statement of Assets, Liabilities, and Equity—

Cash Basis (or Income Tax Basis),” “Statement of Assets and Liabilities Arising From Cash Transactions,” “Balance

Page 25 of 27Checkpoint | Document

5/24/2013https://checkpoint.riag.com/app/view/toolItem?usid=bc03cp207942&feature=ttoc&lastCp...

Sheet—Modified Cash Basis,” “Statement of Revenues and Expenses—Cash Basis (or Income Tax Basis),”

“Statement of Revenues Collected and Expenses Paid,” or other appropriate wording should be used.

102.5 Financial statement form and style considerations are discussed further in Chapter 2, and general presentation

issues applicable to the cash, modified cash, and income tax basis are discussed in Chapter 3. Specific presentation

issues unique to each OCBOA are addressed in the respective chapter covering that basis of accounting.

Disclosures

102.6 Financial statements prepared on an OCBOA require notes and other disclosures. (If the statements are

compiled, management may elect to omit substantially all disclosures. However, that option is not available if the

statements are reviewed or audited.) The disclosure requirements for OCBOAs are not defined in accounting literature

as they are for GAAP, however. Guidance is found in AU-C 800 and states that the basis of accounting and how it

differs from GAAP should be disclosed. It also points out that when financial statements contain items that are the