Embed Size (px)

Citation preview

ADB SME DEVELOPMENT TA

BACKGROUND REPORT

THE CREDIT INFORMATION ENVIRONMENT IN INDONESIA: OPPORTUNITIES FOR CREDIT

PROVIDERS AND INDONESIAN BUSINESSES

BRUCE BARGON

JULY 2001

Published by: ADB Technical Assistance

SME Development State Ministry for Cooperatives & SME

Jalan Rasuna Said Kav.3 Jakarta 12940

Tel: ++62 21 520 15 40 Fax: ++62 21 527 94 82

e-mail: [email protected]

ADB SME DEVELOPMENTTA

I

I. TABLE OF CONTENTS

I. TABLE OF CONTENTS ...........................................................................................I

II. LIST OF ABBREVIATIONS ...................................................................................III

III. LIST OF FIGURES ................................................................................................ IV

IV. EXECUTIVE SUMMARY ........................................................................................ V

V. RINGKASAN EKSEKUTIF.................................................................................... IX

1 INTRODUCTION .....................................................................................................1 1.1 Background..............................................................................................................1 1.2 Scope of the study ...................................................................................................1

2 EXPECTED CREDIT REPORTING OUTCOMES ...................................................2

3 BANK INDONESIA’S DEBTOR INFORMATION SYSTEM EVALUATION OF OPERATIONAL EFFECTIVENESS ........................................................................4

3.1 Summary..................................................................................................................4 3.2 Benchmarking the debtor information system against international practice...........4 3.3 Benchmarking results summary...............................................................................5

4 FACTORS POTENTIALLY IMPEDING DEVELOPMENT OF A CREDIT INFORMATION SYSTEM........................................................................................6

4.1 Problems in confirming customer identity ................................................................6 4.2 Difficulties in confirming business ownership and legal status ................................7 4.3 Willingness of banks and other lenders to share customer data .............................8 4.4 Credit Bureau Ownership and Control .....................................................................8 4.5 Data Quality Standards............................................................................................8 4.6 Communications Technology...................................................................................8 4.7 Legislation................................................................................................................8

5 MODELS WHICH COULD BE USED TO ESTABLISH A CREDIT REPORTING SERVICE IN INDONESIA......................................................................................10

5.1 Ownership..............................................................................................................10 5.1.1 Ownership of the credit bureau remains with Bank Indonesia 10 5.1.2 Formation of a new industry controlled company to assume credit bureau

operations 11 5.2 Operational issues .................................................................................................11 5.2.1 Assumed Bank Indonesia control of the credit bureau 11 5.2.2 Assumed Industry control of the credit bureau. 12 5.3 Set-up costs ...........................................................................................................12 5.3.1 Building a credit reporting system independent of the major international vendors

12

ADB SME DEVELOPMENTTA

II

5.3.2 Building a system in partnership with a major international vendor: 13 5.4 Background To Other Regional Credit Reporting Services ...................................13 5.4.1 Established Credit Bureaus 14 5.4.2 Developing Credit Bureaus 14 5.4.3 Summary Of Regional Bureaus 15 5.4.4 Three Regional Credit Bureaus - ownership and operational issues 16

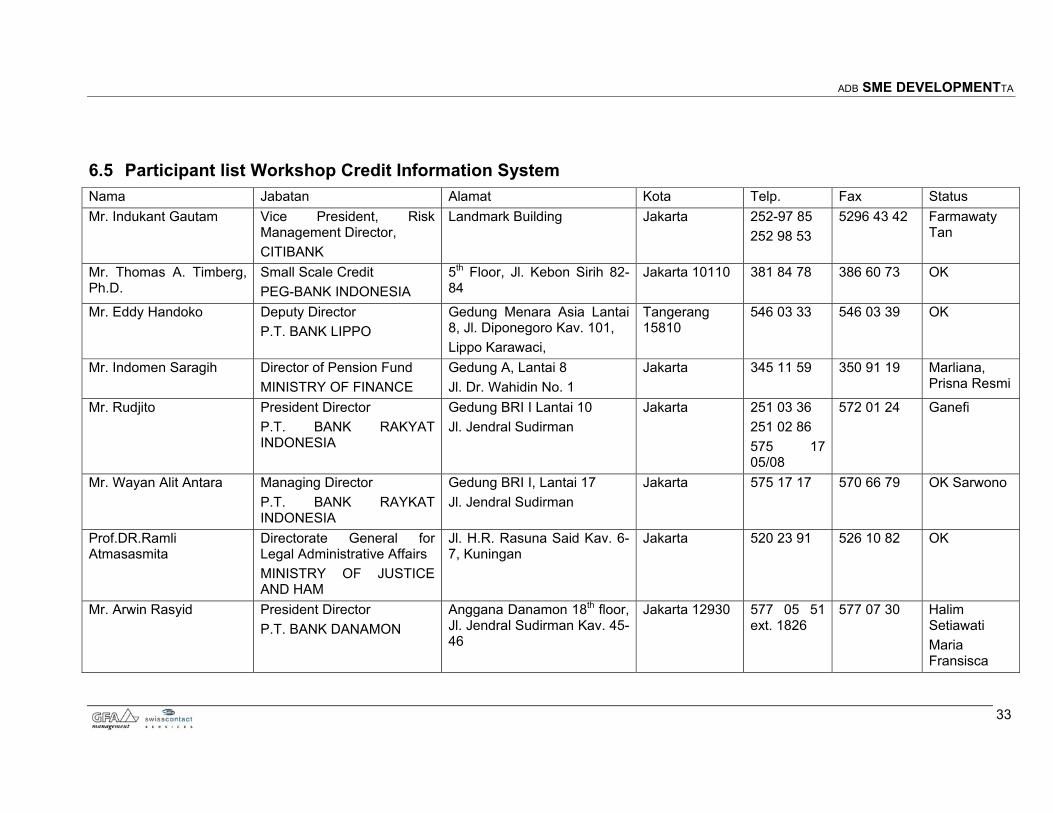

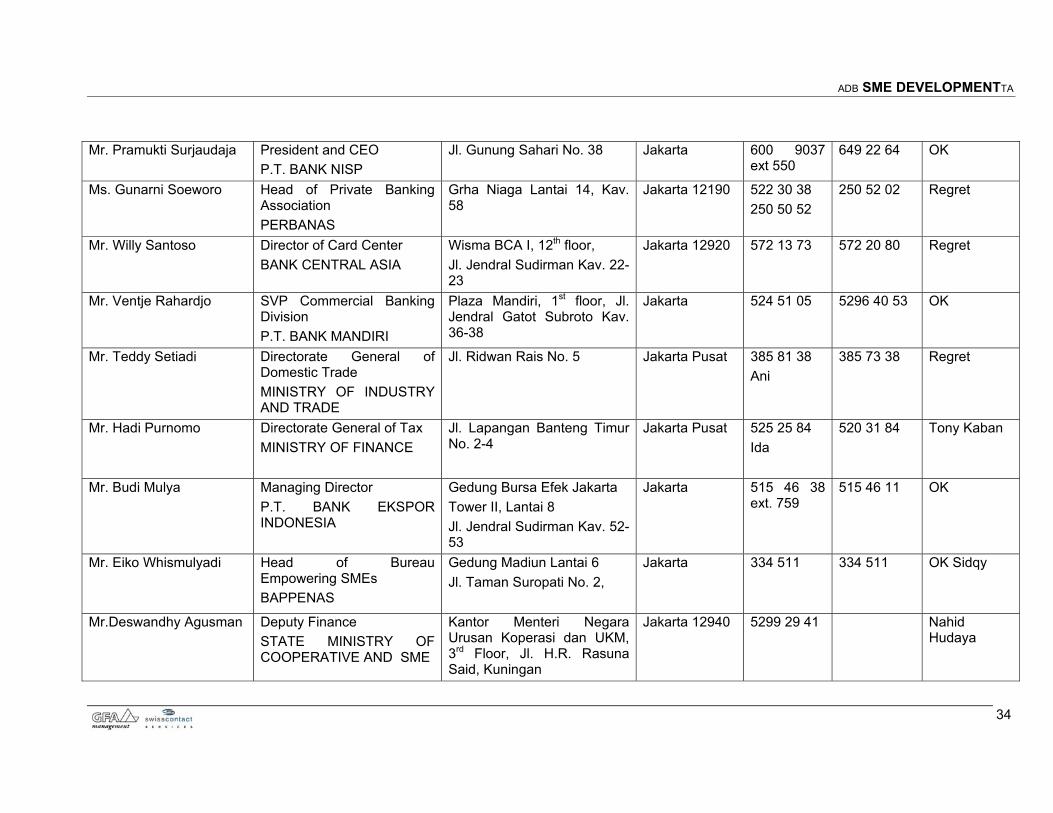

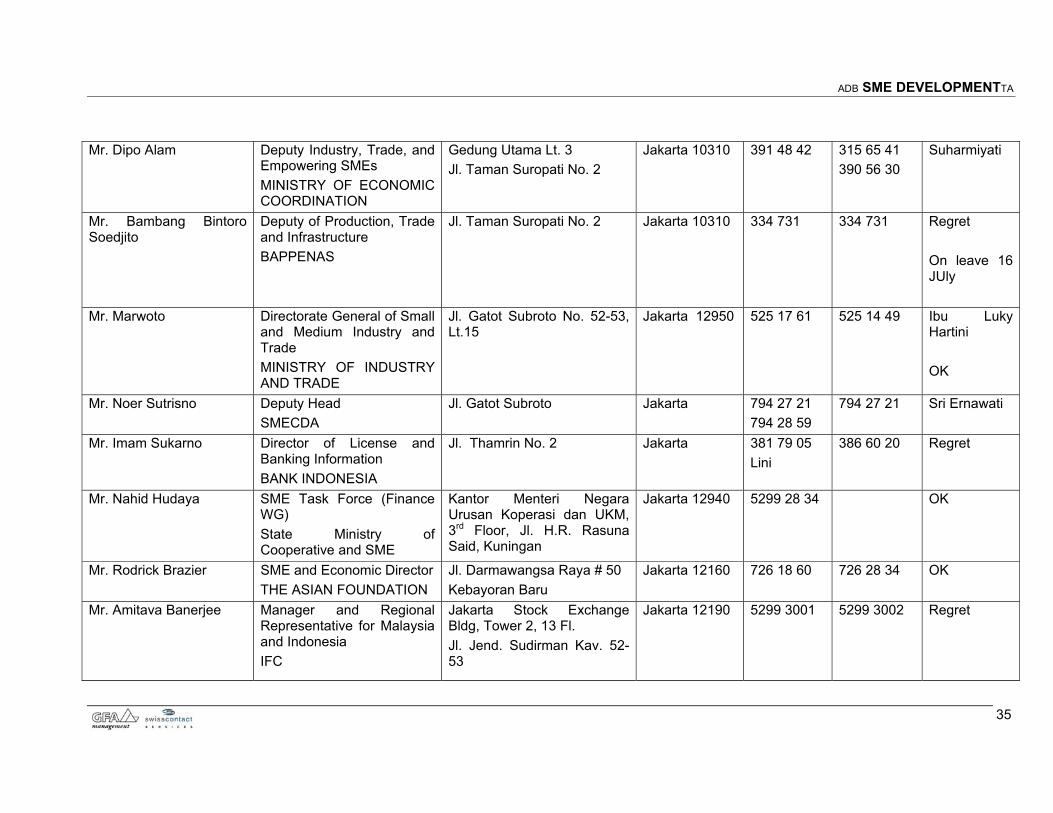

6 APPENDICIES.......................................................................................................17 6.1 Evaluation of Bank Indonesia’s – Debtor Information System ...............................17 6.2 Benchmarking Bank Indonesia’s debtor information system .................................21 6.2.1 Benchmarking Against Public Credit Registries 21 6.2.2 Benchmarking Against Private Sector Credit Bureaus 24 6.3 Customer identification ..........................................................................................26 6.3.1 National Identity Card (Kartu Tanda Penduduk, KTP) 26 6.3.2 Tax Object Master Number (NPWP) 28 6.4 Company / Business Structures and Company Registers .....................................29 6.4.1 Business Structures 29 6.4.2 Regulatory / Registration Authorities 30 6.5 Participant list Workshop Credit Information System.............................................33 6.6 Summary Question and Answers Workshop on Credit Information System..........37 6.7 Presentation Workshop..........................................................................................39

ADB SME DEVELOPMENTTA

III

II. LIST OF ABBREVIATIONS

ADB Asian Development Bank

BPR Bank Perkreditan Rakyat; Rural banks,

BUUD Badan Usaha Unit Desa; Village Business Unit

C.V. Comanditer Venootschap

DIS Debtor Information System

GABKOP Gabungan Koperasi; Association of Cooperatives

IFSI Integrated Financial Supervisory Institution

KTP Kartu Tanda Penduduk; Identity Card

KUD Koperasi Unit Desa; Village Unit Cooperative

KUK Kredit Usaha Kecil; Small Business Credit

NPWP Nomor Pokok Wajib Pajak; Tax Object Master Number

P. T. Perseroan Terbatas; Limited Liability Company

PCR Public Credit Registry

PERUM Perusahaan Umum; Public Enterprise

RT Rukun Tetangga; Neighbourhood ward

RW Rukun Warga, neighborhood association

TA Technical Assistance

UD Usaha Dagang; Trading Company

UDKP Unit Dagang dan Kredit Pedesaan; Village Trading and Credit Unit

ADB SME DEVELOPMENTTA

IV

III. LIST OF FIGURES

Figure 1: Price estimation independent system..............................................................13 Figure 2: Price estimation partnership system................................................................13 Figure 3: Summary of regional bureaus..........................................................................15 Figure 4: Credit Providers excluded from DIS ................................................................17 Figure 5: Credit KUK statistic June 2000........................................................................18 Figure 6: Comparison DIS with 23 public credit registries ..............................................22 Figure 7: Comparison of operational characteristics PCR and DIS ................................26

ADB SME DEVELOPMENTTA

V

IV. EXECUTIVE SUMMARY

Scope of the study Expected outcomes from the operation of a fully functional credit reporting service

in Indonesia. Evaluation of Bank Indonesia’s Debtor Information System, benchmarking the

system against international credit reporting practice. Determination of the ability of DIS to meet users needs and the Government’s SME objectives.

Factors, which may impede the development of an effective credit information system in Indonesia.

Models, which could be used to establish a private and/or public credit reporting, service in Indonesia.

Background to other credit reporting services in the Asia Pacific Region. Recommended Future Action.

Conclusions arising from the study A world-class credit reporting service can be developed for Indonesia. The service should not be restricted to the banking sector or limited to SME credit

activity. It should include all classes of credit and be capable, over time, of including credit providers outside the financial services sector.

There are no apparent legal impediments to its establishment. Such a service does not currently exist. The only source of (shared) credit

information is Bank Indonesia. The debtor information system, operated by Bank Indonesia was not designed to

be a fully functional credit bureau. It falls short of best international practice and does not deliver the service standards that are required. It has some valuable features that should be preserved for the future.

There are various models that could be used to establish a credit reporting service in Indonesia and these are briefly outlined in this summary. They are covered in more detail in Section 4 of the main report.

Recommendations The Inter-ministerial Task Force to meet as soon as practicable to determine

whether the credit bureau initiative is to proceed. Stakeholders to meet to determine ownership and other corporate governance

issues covering the proposed credit bureau’s operations. A Steering Committee to be formed to manage the project. Steering Committee to commission a feasibility/scoping study to conduct a detailed

assessment of the proposed credit bureau operation including the possible redeployment of the Debtor Information System.

Probable elapsed time for the study is two months at an estimated cost of $US 100,000 to $US 120,000.

This study would prepare system specifications covering the functionality of the proposed credit reporting system,(possibly including a redesign of the DIS system). Based on this a Request For Information, (RFI) would be prepared for distribution to potential credit reporting system suppliers.

Steering Committee to prepare and distribute RFI.

ADB SME DEVELOPMENTTA

VI

Receive RFI responses and determine which most closely match the system requirements. Prepare a Request For Proposal (RFP) and distribute to selected suppliers.

Open negotiations with selected suppliers.

Expected outcomes An international standard credit reporting system will benefit credit providers by:

Reducing the incidence of non-performing loans through instant access to better, more comprehensive credit risk information.

Improving productivity in loan assessment processes by the introduction of bureau based credit risk scoring and automated systems.

Lowering processing and bad debts costs to improve the profitability of SME lending and encourage market sector growth.

Opening up opportunities for a significant expansion of the consumer credit market.

Over time, through the improvement in credit information, will reduce reliance by lenders on collateral to secure small business lending.

SMEs and individual borrowers will also benefit by: Substantial reductions in the time required to receive credit approval. As banks are more able to confirm owners’ prior credit histories, newly established

SMEs will have easier access to financial services. Interest charges for small business loans should reduce as the credit risk

environment improves. The build up of credit history information will mean Micro enterprises will have a

better opportunity to grow to SMEs as their access to financial services improves. All borrowers will experience greater flexibility in their relationships with lenders. SMEs will experience a freeing up of working capital as ‘credit reputation collateral’

allows banks to reduce their reliance on traditional collateral. (see main report for a more complete explanation of the above points)

Bank Indonesia’s Debtor Information System (DIS) evaluation of operational effectiveness - Summary

DIS provides a basic service, but the system’s effectiveness is limited. Because DIS forms part of Bank Indonesia’s banking supervision function,

reporting requirements exceed what is normally required for credit reporting and impose unnecessary costs on DIS users.

Database technology is adequate for current restricted operations, but the range of products and service delivery is inadequate and does not meet international standards.

The Debtor Information System contains valuable information, which could be modified to form the basis of an expanded credit reporting operation.

Benchmarking DIS against international best practice The Debtor Information System compared favourably against twenty-three public

credit registries. It was within the mainstream of the benchmark group. The depth of information held by DIS on commercial credit (business) loans was superior to that recorded by most other organisations in the sample group.

The Debtor Information System failed to meet international private sector credit reporting standards. System functionality was limited and the range of products

ADB SME DEVELOPMENTTA

VII

and quality of service delivery fell well short of those provided by the leading private sector bureaus.

Alternative models for establishing a credit reporting service in Indonesia Alternative 1: Ownership of the credit bureau remains with Bank Indonesia.

The options for this alternative are o to extend the functionality of DIS: Extend the functionality of the Debtor

Information System by contracting with a third party (possibly the original designer of the DIS software) to investigate, design and build a credit reporting system modelled on international best practice and modified for Indonesian conditions.

o to enter into a credit bureau software licence agreement Enter into an agreement with one of the specialised international credit reporting system suppliers (all of whom have extensive operating experience) for the installation of a basic operational credit-reporting platform, customised to Indonesian conditions

Alternative 2: Formation of an industry controlled company to assume credit bureau operations. Shareholding in the credit bureau company is shared equally by the initial stakeholders/customers (the commercial banks), with provision for new stakeholders to be invited to participate at a later date. There is a possible coordinating role here for the Bank Associations.

Experience elsewhere has shown that the active participation of an international credit-reporting group at a Board and operational level will make a valuable contribution to the growth and eventual success of the bureau.

SET-UP COSTS (indicative) A: Building a credit reporting system independent of the major international

vendors o Total project costs $ 3,580,000 to $ 4,275,000 o Total elapsed time 2 to 3 years

B: Building a system in partnership with a major international vendor o Total project costs $ 3,055,000 o Total elapsed time 1 year to 18 months

The costs for both scenarios exclude: Physical set up of the data centre; Communication interfaces and software; Salary costs for bureau staff, system operators, programmers, administration Customer support costs (ongoing eduction and training); Communication costs, etc.

BACKGROUND TO OTHER REGIONAL CREDIT REPORTING SERVICES Several countries in the region currently have established or are developing credit-

reporting operations. These are: Australia; China (Hong Kong); India; Japan; Malaysia; New Zealand; Philippines; South Korea; Taiwan; Thailand

Established Credit Bureaus operate in Australia, Hong Kong, Japan (3 bureaus), Malaysia (private bureau), New Zealand, Philippines, South Korea and Taiwan.

Developing Credit Bureaus: o The credit bureau in Malaysia owned by Bank Negara has outsourced its

bureau system development to a private partnership, consisting of a New Zealand and a Malaysian owned company. The bureau is not yet operational.

ADB SME DEVELOPMENTTA

VIII

o A Shanghai privately owned bureau, supported by The Peoples Bank of China is building its own credit reporting system. The bureau is not yet fully operational and it is understood the Bank of China may have to introduce legislation to give the bureau full authority to operate.

o A privately owned credit bureau in Thailand is majority owned by the Thai Bankers Association with minority shareholdings held by Trans Union Corp (a major international vendor) and a Thai affiliate of Dun and Bradstreet. The bureau has outsourced its operations to the Dun & Bradstreet affiliate, which has licensed the credit bureau software from Trans Union Corporation. The bureau is partly operational.

o A privately owned credit bureau in India is majority owned by the State Bank of India and the Housing Development Corporation, with minority shareholders, Trans Union Corp and Dun & Bradstreet (USA). The project has the active support of the Reserve Bank of India. The company is licensing credit bureau software from Trans Union Corp. It is not yet operational.

ADB SME DEVELOPMENTTA

IX

V. RINGKASAN EKSEKUTIF

Ruang Lingkup Studi Outcomes diharapkan berupa beroperasinya jasa informasi kredit secara penuh di

Indonesia. Evaluasi dari Sistem Informasi Debitur (SID) di Bank Indonesia,

membandingkannya dengan praktek internasional dalam jasa informasi kredit. Menentukan kemampuan SID dengan kebutuhan pengguna dan tujuan pemerintah.

Beberapa faktor mungkin dapat menghalangi pembangunan sebuah sistem informasi kredit di Indonesia.

Beberapa model dapat digunakan dalam membangun sebuah jasa informasi kredit swasta dan atau pemerintah di Indonesia.

Latar belakang dari beberapa jasa informasi kredit di wilayah Asia Pasifik. Rekomendasi kegiatan masa yang akan datang.

Kesimpulan yang muncul dari studi Sebuah jasa informasi kredit kelas dunia dapat dikembangkan untuk Indonesia. Jasa tersebut tidak hanya dibatasi untuk sektor perbankan atau terbatas untuk

penyaluran kredit kepada UKM. Tetapi juga termasuk untuk seluruh tingkatan kredit dan dapat dipergunakan sepanjang waktu termasuk oleh penyedia kredit selain sektor jasa keuangan.

Tidak ada halangan legal yang nyata untuk mendirikannya. Jasa seperti ini belum ada. Satu-satunya sumber informasi kredit yang digunakan

bersama adalah Bank Indonesia. Sistem Informasi Debitur yang dilaksanakan oleh Bank Indonesia tidak dirancang

untuk berfungsi seperti layaknya biro kredit. Kondisinya sangat jauh dari praktek terbaik internasional dan tidak dapat menyediakan layanan yang sesuai standar. Terdapat beberapa aspek yang bernilai dan dapat dipertahankan untuk masa yang akan datang.

Terdapat beberapa model yang dapat digunakan untuk membangun sebuah jasa informasi kredit di Indonesia dan akan dijelaskan dalam ringkasan ini. Uraian detail tentang hal ini terdapat dalam Bagian 4 di laporan utama.

Rekomendasi Kelompok kerja antar Departemen secepatnya bertemu untuk menentukan apakah

gagasan pembentukan biro kredit dapat diproses lebih lanjut. Stakeholders melakukan pertemuan untuk menentukan kepemilikan dan ruang

lingkup issu corporate governance yang dapat diusulkan termasuk dalam operasi biro kredit.

Sebuah Steering Committee dibentuk untuk mengelola proyek ini. Steering Committee mempersiapkan studi kelayakan dalam rangka melaksanakan

penilaian detail dari beroperasinya sebuah biro kredit termasuk didalamnya kemungkinan menata kembali Sistem Informasi Debitur.

Kemungkinan waktu yang dibutuhkan untuk studi sekitar 2 bulan dan diperkirakan memerlukan biaya senilai $US 100,000 hingga $US 120,000.

ADB SME DEVELOPMENTTA

X

Studi ini akan mempersiapkan spesifikasi sistem yang akan dipergunakan oleh sistem informasi kredit yang diusulkan (kemungkinan termasuk merancang kembali dari Sistem Informasi Kredit. Berdasarkan permintaan terhadap informasi, maka permintaan informasi tersebut akan didistribusikan kepada pemasok potensial sistem infiomasi kredit.

Steering Committee perlu dipersiapkan dan mendistribusikan RFI. Tanggapan terhadap RFI diterima dan tentukan sistem yang sesuai kebutuhan.

Persiapkan permintan pengajuan proposal (RFP) dan dibagikan kepada pemasok terbatas.

Buka negosiasi dengan supplier terpilih.

Outcomes yang diharapkan Sebuah sistem informasi kredit berstandar internasional akan memberikan manfaat kepada lembaga penyedia kredit:

Mengurangi terjadinya kredit macet melalui akses yang cepat dan baik serta komprehensif terhadap informasi resiko kredit.

Memperbaiki produktivitas proses penilaian kredit dengan memperkenalkan sebuah biro yang didasarkan kepada skor resiko kredit dan otomatisasi sistem.

Proses yang lebih sederhana dan rendahnya biaya kredit macet akan meningkatkan keuntungan dari penyaluran kredit kepada UKM dan mendorong pertumbuhan pasar kredit UKM.

Membuka kesempatan untuk pengembangan yang signifikan dari pasar kredit individu

Perbaikan informasi kredit dari waktu ke waktu akan mengurangi ketergantungan pemberi kredit kepada agunan sebagai persyaratan penyaluran kredit kepada UKM yang aman.

UKM dan peminjam individu juga akan memperoleh manfaat: Pengurangan waktu yang dibutuhkan untuk menerima persetujuan kredit. Karena bank dapat melakukan konfirmasi mengenai sejarah kredit sebelumnya

dari pemilik; maka perusahaan UKM yang baru dapat lebih mudah akses ke jasa keuangan

Tingkat bunga yang akan dibebankan kepada pinjaman UKM akan lebih rendah karena adanya perbaikan terhadap kondisi resiko kredit.

Tersedianya sejarah informasi kredit akan memberikan kesempatan kepada perusahaan mikro berkembang menjadi UKM dan pada gilirannya akan memperbaiki akses kepada jasa keuangan.

Semua peminjam akan mempunyai fleksibilitas yang lebih besar dalam berhubungan dengan pemberi pinjaman.

Pengalaman UKM dalam memperoleh modal kerja sebagai “reputasi kredit sebagai agunan” dan akan mengurangi persyaratan bank terhadap agunan tradisionil.

(lihat laporan utama untuk memperoleh penjelasan yang lebih lengkap mengenai point diatas )

Sistem Informasi Debitur (SID) Bank Indonesia evaluasi dari efektiivtas operasional Ringkasan

SID menyediakan jasa dasar, tetapi efektivitas sistem ini terbatas. Karena SID di Bank Indonesia sebagai bagian dari fungsi pengawasan bank,

maka laporan yang diperlukan lebih besar dari yang biasanya secara normal

ADB SME DEVELOPMENTTA

XI

diperlukan untuk informasi kredit dan menimbulkan biaya yang tidak perlu bagi pengguna SID .

Tekonologi database cukup memadai untuk penggunaan saat ini yang terbatas, tetapi rentang dari produk dan layanan yang diberikan kurang memadai, dan tidak sesuai dengan standar internasional.

Sistem Informasi Debitur mengandung informasi yang berharga, yang dapat dimodifikasi sebagai dasar dari beroperasinya sistem informasi kredit.

Mensejajarkan SID terhadap praktek terbaik internasional Sistem Informasi Debitur cukup baik dibandingkan dengan 23 lembaga umum

yang mencatat kredit. Posisinya adalah ditengah dari kelompok yang dijadikan acuan. Informasi detail yang dimiliki SID tentang kredit bank umum sangat banyak dicatat dibandingkan dengan yang dimiliki lembaga lain dalam kelompok contoh.

Sistem Informasi Debitur tidak sesuai dengan standar internasional tentang informasi kredit swasta. Fungsi SID terbatas dan rentang produk serta kualitas layanan yang diberikan juga kecil dibandingkan dengan yang diberikan biro kredit swasta ternama.

Model alternatif untuk membangun sebuah jasa informasi kredit di Indonesia Alternatif 1: Kepemilikan biro kredit tetap oleh Bank Indonesia. Pilihan untuk

alternatif ini adalah o memperluas fungsi dari SID: Memperluas fungsi dari Sistem Informasi

Debitur melalui perjanjian dengan pihak ketiga (mungkin dengan disainer dari perangkat lunak SID) untuk menyelidiki, mendisain dan membangun model sistem informasi kredit berdasarkan praktek terbaik internasional dan disesuaikan dengan kondisi Indonesia.

o melakukan kerjasama dengan pemegang lisensi perangkat lunak biro kredit. Kerjasama dengan sebuah supplier sistem informasi kredit internasional (hampir semuanya telah berpengalaman) untuk melakukan pemasangan dasar dari operasional kredit informasi yang sesuai dengan kondisi Indonesia.

Alternatif 2: Pembentukan sebuah industri yang melakukan kontrol terhadap perusahaan yang mengoperasikan biro kredit. Kepemilikan dalam perusahaan biro kredit adalah sama untuk setiap stakeholder/pelanggan (bank umum) dengan memberikan peluang kepada stakeholder baru untuk ikut serta. Disini ada kemungkinan untuk melakukan koordinasi dengan Asosiasi Bank.

Pengalaman ditempat lain menunjukkan bahwa partisipasi aktif dari sebuah kelompok informasi kredit internasional baik pada tingkat pengurus maupun operasional akan memberikan kontribusi yang berharga untuk perkembangan dan sukses dari biro.

Biaya Pendirian (indikasi) A: Membangun sistem informasi kredit yang tidak tergantung kepada vendor

internasional o Biaya total proyek $ 3,580,000 to $ 4,275,000 o Waktu total yang diperlukan 2 hingga 3 tahun

B: Membangun sistem informasi melalui kerjasama dengan vendor internasional o Biaya proyek total $ 3,055,000 o Waktu total yang diperlukan 1 tahun hingga 18 bulan

ADB SME DEVELOPMENTTA

XII

Biaya untuk kedua skenario tidak termasuk: pembangunan pusat data, jaringan dan perangkat lunak komunikasi, gaji untuk staf biro, operator sistem, programmer, administrasi pendukung pelanggan (pendidikan dan pelatihan yang terus menerus), biaya komunikasi, dll.

Latar belakang terhadap Jasa Informasi Kredit di Wilayah Lain Beberapa negara di kawasan ini telah mendirikan atau mengembangkan operasi

biro informasi kredit. Diantaranya: Australia; China (Hong Kong); India; Jepang; Malaysia; New Zealand; Philipina; Korea Selatan; Taiwan; Thailand

Biro kredit telah didirikan dan beroperasi di Australia, Hong Kong, Japan (3 biro), Malaysia (biro swasta), New Zealand, Philipina, Korea Selatan, dan Taiwan.

Mengembangkan Biro Kredit: o Biro kredit di Malaysia dimiliki oleh Bank Negara dan mengsubkontrakkan

sistemnya kepada perusahaan swasta yang dikembangkan bersama oleh perusahaan Malaysia dan New Zealand. Biro ini belum beroperasi.

o Sebuah biro swasta di Shanghai didukung oleh The Peoples Bank of China dalam pendirian sistem informasi kredit. Saat ini belum sepenuhnya beroperasi dan Bank of China sedang mempersiapkan landasan hokum untuk beroperasinya biro ini secara penuh.

o Sebuah biro kredit swasta di Thailand mayoritas dimiliki oleh Asoasiasi Perbankan Thailnad dengan kepemilikan yang terbatas dari Trans Union Corp (sebuah vendor utama internasional) dan afiliasi Dun and Bradstreet. Biro ini juga mengsubkontrakkan operasinya kepada afiliasi Dun & Bradstreet , yang memiliki lisensi perangkat lunak biro kredit dari Trans Union Corporation. Biro ini sebagian telah beroperasi.

o Biro kredit swasta di India mayoritas dimiliki oleh State Bank of India dan the Housing Development Corporation, dengan kepemilikan terbatas, Trans Union Corp and Dun & Bradstreet (USA). Proyek ini memperoleh dukungan penuh dari the Reserve Bank of India. Perusahaan ini memperoleh lisensi perangkat lunak biro kredit dari Trans Union Corp. Saat ini belum beroperasi.

ADB SME DEVELOPMENTTA

1

1 INTRODUCTION

1.1 Background The Government of Indonesia is concerned with the inadequate level of financial services available to small and medium enterprises (SMEs) and the barrier this places in the way of their future growth. The Government believes that SME access to financial services and credit would improve, if a reliable credit information system were developed. On behalf of the Government an inter-ministerial task force commissioned a study to evaluate existing credit information sources in Indonesia, including the Debtor Information System operated by Bank Indonesia. The objective of this study is to determine what action would be required to establish an effective credit reporting system, capable of meeting the information needs of the banks and other financial institutions and as a consequence, freeing up access to improved credit facilities for SMEs.

1.2 Scope of the study Expected outcomes from the operation of a fully functional credit reporting service in

Indonesia. Evaluation of Bank Indonesia’s Debtor Information System, benchmarking the system

against international credit reporting practice. Determination of the ability of DIS to meet users needs and the Government’s SME objectives.

Factors which may impede the development of an effective credit information system in Indonesia.

Models which could be used to establish a private and/or public credit reporting service in Indonesia.

Background to other credit reporting services in the Asia Pacific Region. Recommended Future Action.

ADB SME DEVELOPMENTTA

2

2 EXPECTED CREDIT REPORTING OUTCOMES An international standard credit reporting system will benefit credit providers by:

Reducing the incidence of non-performing loans Using a credit reporting service to assess all loan applications will reduce non-performing loans and bad debt write offs by at least 25%. By pooling credit history information from a wide group of lenders, a credit reporting service can make a borrower’s complete credit history available to potential lenders. Informed lenders can then avoid extending loans to high-risk borrowers who have poor repayment histories. Borrowers will be aware that their performance is known to the credit reporting service. The information recorded will become part of the borrower’s lending profile or ‘reputation collateral’. Any late payments or default will reduce the value of this collateral and as a result, adversely impact the borrower’s ability to borrow further in the future. ‘Reputation collateral’ can be particularly significant for an SME’s ability to obtain working capital for future expansion.

Improving productivity in the loan assessment process The use by a lender of credit bureau data and automated credit risk scoring techniques can reduce the time needed to process and approve or decline a credit request for a small business down to 15 minutes.1 This compares with present credit approval times ranging from three to five days for personal credit and three to four weeks for a small business loan.

Lower processing and bad debts costs will enable banks to expand their lending to SMEs As the cost of processing loan applications is reduced and the incidence of non-performing loans and bad debts also declines, banks and other lenders will find it more profitable to lend to small businesses. For example, with the introduction of SME credit risk scores in the United States between 1994 and 1998, loans to small businesses grew by 78.5%. Similar increases in SME lending have been noted in Australia by the local credit bureau.

Over time credit bureau information will reduce reliance by lenders on collateral to secure small business lending Over a period July 1999 to May 2000 the World Bank conducted surveys of credit information registry usage by banks in Latin America. The survey covered most nations in the region. If it can be assumed that the credit risk environment of at least some Latin American countries is similar to Indonesian conditions, then one finding of the surveys may be particularly relevant. Banks were asked to rank the importance of credit registry information relative to other measures of credit worthiness. Of the various categories measured, twice as many banks ranked a company’s credit payment history as being more important to their credit review process than the value of collateral.2

1 World Bank SME Issues Vol 1, Number 2, November 2000, ‘Credit Scoring A Tool for More Efficient SME Lending’. 2 Credit Reporting Systems Around The Globe: The State of the Art in Public and Private Credit Registries, June 2000, page 24.

ADB SME DEVELOPMENTTA

3

SMEs and individuals will also benefit from the operations of a credit bureau:

Substantial reductions in the time required for credit approval As the efficiency of lenders’ credit assessment processes improves, borrowers will receive faster responses to their applications for credit and credit application procedures will become simpler and less time consuming.

Recently established small businesses will have easier access to credit The availability of credit history information on businesses and their owners will make it easier for lenders to confirm the personal credit histories (reputation collateral) of the owners of a newly established business. To quote The Senior Vice President, Fair Isaac & Co., a company which pioneered the development of SME credit risk scoring models, ‘Fair Isaac has found a surprising amount of statistical correlation between SME credit payment behaviour and the personal credit and financial status of the principals’. This is also the experience of Decision Advantage Pty Ltd., a leading supplier of credit risk scoring systems in the Asia Pacific region.

Interest charges for small business loans should decline as risk of lending improves Interest charges are influenced by many factors and the cost of bad debts and non-performing loans has an important influence on rates charged. As costs and credit risk decrease, lenders will have improved interest rate flexibility

Micro enterprises will have a better opportunity to grow to SMEs Should a decision be made to record smaller loans of less than Rp 50 million, then the lending patterns of many more individuals and micro businesses will be recorded by the credit bureau. This will give them the opportunity to build a good credit reputation. That credit reputation can in turn improve their access to better financial services. Experience with micro financing strongly suggests that micro enterprises have the potential to grow, provided they are able to gain access to working capital. As they gain access to financial services, they are able to grow out of the micro stage and graduate to the SME category.3

All borrowers will experience greater flexibility in their relationships with lenders As individuals and SMEs establish their credit reputations via the credit registry, their ability to ‘shop’ for credit facilities will improve. Whilst some lenders could see this as threatening, experience elsewhere shows that this trend is associated with an increase in total market size and increased credit demand.

SMEs will experience a freeing up of working capital As lenders move away from the present focus on obtaining collateral, the capital which SMEs now have tied up in secured collateral will become available for use as working capital to grow the business.

3 ‘SME Financing Lessons for Micro Finance’ SME Issues Vol 1, No 1, November 2000

ADB SME DEVELOPMENTTA

4

3 BANK INDONESIA’S DEBTOR INFORMATION SYSTEM EVALUATION OF OPERATIONAL EFFECTIVENESS

3.1 Summary

A basic service The Debtor Information System (DIS) provides a basic credit risk information service to the commercial banks. The DIS database of business and consumer credit transactions holds comprehensive information on each loan. Disciplined reporting standards have also contributed value by ensuring the integrity and accuracy of information in the database.

The system’s effectiveness is limited Participation is restricted to the commercial banks. The reporting of loan details is limited to amounts of Rp 50 million and above. Possibly no more than ten percent of commercial bank loans are recorded. Many credit providers, including venture capital banks, rural banks and cooperatives are not permitted to participate in the service. As a consequence it appears likely that the majority of smaller business loans and almost all consumer credit loans are not recorded by DIS.

Bank Indonesia’s reporting requirements are excessive for normal credit reporting The detailed and extensive information required of the commercial banks by Bank Indonesia is primarily used for bank supervision, i.e. monitoring the industry’s credit risk exposure. The information gathered is in excess of what is required by a credit reporting operation. The costs associated with the collection of data are a barrier to any broadening of the DIS service. It could be expected that the commercial banks would resist reporting a greater range of loans to DIS under current information requirements. Non-bank credit providers would be faced with substantial additional operating costs. Database technology is adequate for current operations, but service delivery and enquiry system are inadequate and do not meet international standards (see Benchmarking Appendix 2). It is questionable whether the present hardware/software combination is compatible with the requirements of an international standard credit reporting system. The Debtor Information System contains valuable information, which could be modified to form the basis of an expanded credit reporting operation (see Appendix 1 for a more detailed assessment).

3.2 Benchmarking the debtor information system against international practice

The Debtor Information System was benchmarked against two distinctly different credit-reporting systems.

Public Credit Registries

ADB SME DEVELOPMENTTA

5

A selected sample of twenty- three public credit registries, all of which are operated and funded by central banks. Participation in public credit registries is almost always restricted to those banks supervised by the central bank. Participation and the reporting of customer account data are compulsory. The primary purpose of data collection is bank supervision.

Private Sector Credit Bureaus A comparison drawn from nine private sector credit reporting systems. Private sector bureaus may be owned by a consortium of credit bureau users (banks, finance companies etc.) or may be private or public listed companies. Participation is voluntary and usually includes a wide range of credit providers (some Asia Pacific private sector bureaus are limited to financial institutions). The reporting of credit data to the bureau is governed by a written agreement. The primary purpose of data collection is to improve credit risk assessment.

3.3 Benchmarking results summary

Public credit registries The Debtor Information System compared favourably with the other twenty-three public credit registries. It was within the mainstream of the benchmark group. The depth of information held by DIS on commercial credit (business) loans was superior to that recorded by most other organisations in the sample group.

Private sector credit bureaus The Debtor Information System falls short of international private sector credit reporting standards. The DIS information is limited to a very small percentage of credit transactions, compared to private bureau operations. The service provided does not meet the operational characteristics of the leading private sector bureaus. (Refer to Appendix 2 for more detailed results)

ADB SME DEVELOPMENTTA

6

4 FACTORS POTENTIALLY IMPEDING DEVELOPMENT OF A CREDIT INFORMATION SYSTEM

There are seven areas of potential difficulty, which could impede the development of an effective credit reporting system.

Problems in confirming customer identity. Difficulty in confirming business ownership and legal status. Willingness of banks and other credit providers to share customer data. Credit bureau ownership and control issues. Data quality – accuracy of data reported. Communications technology – mainly affecting major banks. Legislation

formal recognition/authorisation limited protection against defamation data use/privacy legislation.

4.1 Problems in confirming customer identity

Name and Address This is a problem shared with other countries in the region where name and address information does not fit within an easily recognisable format, suitable for automated data matching systems. Similar difficulties are encountered in Thailand, Malaysia, India, Pakistan and the Philippines. In Indonesia naming conventions permit a considerable variety and combination of given and family names. The use of single letter names is common. Similarly address information does not appear to conform to clearly laid down standards. It is understood the postal authorities provide guidelines for address layout, but that these guidelines are often ignored. The combination of non-conformist name and address data adds considerable complexity to any system, which is attempting to match incoming online enquiry data to stored records. Fortunately in Indonesia all citizens are issued with a national identity card (Kartu Tanda Penduduk) KTP at age 18. The KTP contains extensive information, which can be used to verify a potential credit customer’s identity, including an identity number. It is recognised that the integrity of KTP is flawed, due to the ability of individuals to obtain more than one card. However the KTP is a valuable additional means of identity verification which, if added to customer name and address and employment information obtained by banks, can be effectively used by an automated data matching system. An independent expert, experienced in credit bureau data matching techniques, has assessed examples of Indonesian name and address usage and the data held on the KTP. He is of the opinion that an effective data matching system-covering individuals can be built in Indonesia (see Appendix 3 KTP).

ADB SME DEVELOPMENTTA

7

NPWP (Tax Object Master Number) Bank Indonesia requires commercial banks to obtain the NPWP of all individuals and businesses applying for a loan of Rp 50 million and over. The NPWP has high integrity and is an ideal identifier for data matching purposes. Until recently it was only issued to businesses and individuals who earn taxable income from more than one source (eg., not people employed by businesses or government). As a result it is estimated that less than five percent of taxpayers are currently issued with a NPWP. The Government has a program to increase NPWP penetration to five million by the end of 2002. If the use of NPWP were to become widespread it would be an invaluable identifier for use in credit risk assessment (see Appendix 4 NPWP).

4.2 Difficulties in confirming business ownership and legal status At present information concerning the legal status of a registered business (C.V., P.T., Koperasi) appears to be split across three government bodies:

Ministry of Industry and Trade, Directorate of Business Development and Company Registration

Ministry of Justice and Human Rights State Ministry for Cooperatives and Small & Medium Business.

The Directorate of Business Development and Company Registration has a partly automated database covering registration and ownership of P.T. Limited. C.V.s and Cooperatives. It is the largest of the three databases, but is stated to have records on no more than fifty percent of trading companies. The Directorate’s automation program is only partly complete and appears to be stalled. The Ministry of Justice has a partly automated database of P.T. Limited company certification details. The automation project is recent and progressing. It is understood that the Ministry for Cooperatives has an automated database of cooperatives but details of its operation are not known. This division of business certification and registration can lead to duplication and additional costs for credit providers. Consideration should be given to the establishment of one single business registration authority. The adverse impact of three separate sources of business registration information on the credit assessment process for business loans is noticeable. During this study, two commercial banks demonstrated the labour intensive data gathering process involved in confirming the legal status and ownership of business enterprises applying for loans. It appears that very few, if any credit providers contact the three business registries to confirm business certification or ownership details for the purpose of loan assessment. A centralised, automated, ‘one stop’ business registration authority would benefit both lenders and small medium enterprises. Access to such a registry by a centralised credit reporting service would significantly improve that service’s ability to cross-reference the credit histories of individual business people with credit files of the businesses which they control (see Appendix 5 – Company Registries).

ADB SME DEVELOPMENTTA

8

4.3 Willingness of banks and other lenders to share customer data Prior to the recent economic difficulties experienced by a number of countries in the Asia Pacific Region, many credit providers were reluctant to share customer credit information. That situation is now changing and credit reporting systems are being established/expanded in a number of countries in the region (addressed in Section 5 of this report). At issue is the concern of lenders that in sharing their customer information through a credit bureau, that information may be misused by a competitor. This concern does not apply to the Debtor Information System, due to the strict controls and penalties for misuse, imposed by Bank Indonesia. If a prospective credit reporting system is to be expanded beyond the commercial banks to include other credit providers, a similar control mechanism will need to be put in place. There are several ways in which this can be achieved and these are addressed in Section 4.

4.4 Credit Bureau Ownership and Control A strength of the current DIS service is that the commercial banks have confidence that Bank Indonesia is not biased in favour of a particular bank or banks and is not subject to any undue influence which might result in a bank being disadvantaged. This will be a crucial issue for any new credit reporting service. It must be able to demonstrate an ownership structure, which is resistant to any attempt by an stakeholder to divert the bureau’s business direction or overall policies. The operational management of the bureau must also be seen to be unbiased and independent of outside influence. There are means to achieve this, including separating ownership from the day-to-day operations of the credit bureau. These are addressed in Section 4.

4.5 Data Quality Standards The maintenance of accuracy in reporting data to the bureau is a constant issue for credit bureaus worldwide. In the case of DIS this is assured by the power of Bank Indonesia to impose fines for non-compliance. If there were some means by which this level of regulated data quality standard could be maintained in an expanded credit reporting operation, this should be given close attention. Possibly the soon to be established Integrated Financial Supervisory Institution, IFSI, would be an appropriate body. Alternatively a good spread of credit bureau ownership, supportive of a Board of Directors willing to impose strong sanctions for non- compliance, would achieve a similar result.

4.6 Communications Technology This is probably not a problem for smaller credit bureau users, who would have enquiry access via an Internet service provider. There may be some initial problems for larger banks that are likely to wish to use high volume CPU-to-CPU links. This is an area to be explored with Indonesian telecom service suppliers.

4.7 Legislation There appear to be no legislative or regulatory barriers to the establishment of a comprehensive credit reporting system.

ADB SME DEVELOPMENTTA

9

The Banking Act 1998 permits banks to exchange credit information about their customers. It is understood that a new Draft Credit Law being considered by Parliament encourages the sharing of credit information to establish a debtor’s ability to service a proposed loan. There may be problems with defamation action, where a credit bureau report is claimed to have damaged an individual or business. Consideration should be given to permitting a ‘qualified’ defence to defamation where the published information is shown to be true or in the public interest. This is an issue requiring expert advice, but it is not perceived to be serious enough to prevent establishment of a credit bureau. Data privacy legislation covering the collection and use of credit bureau information and giving data subjects a right of access and correct is recommended. As the operations of the credit reporting system expand and become universal, there will be an increased risk of unauthorised use of credit data that could lead to growing public concern about the existence of a ‘secretive’ centralised database of sensitive personal data.

ADB SME DEVELOPMENTTA

10

5 MODELS WHICH COULD BE USED TO ESTABLISH A CREDIT REPORTING SERVICE IN INDONESIA

5.1 Ownership

5.1.1 Ownership of the credit bureau remains with Bank Indonesia Bank Indonesia would have two options to develop a fully functional bureau.

Extend the functionality of DIS Extend the functionality of the Debtor Information System by contracting with a third party (possibly the original designer of the DIS software) to investigate, design and build a credit reporting system modelled on international best practice and modified for Indonesian conditions. There are a number of experienced data base software design companies with the potential capacity to build a credit reporting system. An issue for Bank Indonesia would be that it is unlikely that any of them would have prior experience in the specialised requirements of an operating credit reporting system. In effect Bank Indonesia would be paying a ‘learning’ premium with no guarantee as to completion time, eventual cost, operational efficiencies, or compatibility with other credit reporting systems. It is unlikely that any of the specialised international suppliers of credit reporting system would be prepared to take up a credit reporting system design contract which involved transferring ownership rights to Bank Indonesia for key source or object code.

Enter into a credit bureau software licence agreement Enter into an agreement with one of the specialised international credit reporting system suppliers (all of whom have extensive operating experience) for the installation of a basic operational credit-reporting platform, customised to Indonesian conditions. This option provides two further implementation models.

Invite tenders for the design and installation of a fully functional credit reporting software system, customised to Indonesian conditions. Operational responsibility to be assumed by Bank Indonesia upon acceptance of the system. Computer hardware, operating systems and any third party software to be the responsibility of Bank Indonesia. The credit bureau system supplier would provide training to Bank Indonesia staff. Software maintenance, system upgrades and new product release would be negotiated. An up front fee would be payable, plus an annual licence fee, probably linked to credit bureau enquiry volumes.

All of the above as part of a partnership agreement involving the formation of a joint venture company to take responsibility for design and installation of the new system and operational management of the bureau, following acceptance of the system. In this model the software system supplier would take equity share and have an ongoing role in the management of the bureau. The model also presents opportunities to negotiate credit bureau system set up costs and negotiate ongoing access to new product releases.

ADB SME DEVELOPMENTTA

11

5.1.2 Formation of a new industry controlled company to assume credit bureau operations

An issue arising from this option is what ownership structure is likely to be acceptable to current and future users of the existing DIS service. The commercial banks have expressed a concern that private sector ownership of the credit bureau must continue to ensure that no bank is disadvantaged through misuse of its customer account data reported to the bureau, nor as a result of policy decisions, which may advantage a competitor. This issue can be addressed in three ways:

Shareholding in the credit bureau company is shared equally by the initial stakeholders/customers (the commercial banks), with some provision for new stakeholders to be invited to participate at a later date. Board participation should reflect the shareholding structure, although not all shareholders would necessarily serve on the Board (too large a Board could cause problems). There could be a role here for the Bank Associations.

As for above, plus Bank Indonesia (and/or its regulatory successor) be invited to assume an equity position, possibly via a subsidiary of Bank Indonesia, given the equity ownership limitations imposed on the Bank. The participation of Bank Indonesia would add to the credibility and stability of the new operation.

Either of the above options plus inviting a successful credit bureau system supplier to participate as a shareholder. Experience elsewhere has shown that the active ongoing participation of one of the major international credit reporting groups at a Board and operational level can be of benefit by bringing a broad level of practical experience to bear on any issues that may arise. The possibility of equity participation for a system supplier may provide additional flexibility in negotiating software licence fees, set up costs and access to new products.

5.2 Operational issues

5.2.1 Assumed Bank Indonesia control of the credit bureau Issues which need to be addressed:

Management and entrepreneurial skills Does Bank Indonesia have people with the management, technical and entrepreneurial skills and attitudes necessary to operate a world-class credit bureau service? Generally speaking government agencies are not best suited to act as service providers. Government structure, culture and capacity to respond to change are not the best models for operating in customer-oriented environments. Government agencies are not always flexible or innovative, nor do they respond well to the pressure of market forces. To an extent this is demonstrated in the operations of public credit reporting registers operated by central banks in other countries. They tend to be under utilised by credit providers, with a limited number of information providers and a limited product range. Most do not provide data subjects with a right of access to their files.

Regulation of data Whilst Bank Indonesia retains regulatory control of the commercial banks, there is an important role for it in using its authority to control the supply and use of credit bureau information and in maintaining data quality standards.

ADB SME DEVELOPMENTTA

12

Future of Bank Indonesia? The future role of Bank Indonesia as a bank regulator is yet to be resolved. Should the bank no longer have this function, its role in continuing to control credit bureau operations is open to question.

5.2.2 Assumed Industry control of the credit bureau. Issues which need to be addressed:

Maintaining data quality What measures can be put in place to ensure the quality and timeliness of data reported to the credit bureau? Consideration should be given during the first two years of the bureau’s operations to maintaining legislation mandating the reporting of credit data to the bureau. This may mean initially restricting participation in the bureau to commercial banks (under the regulation of Bank Indonesia), plus certain other key credit providers who are prepared to give written guarantees of their compliance with the data reporting standards adopted by the commercial banks. Moving beyond the first two years, it could be expected that the growing value of bureau membership will enable the bureau to require contractual guarantees of data, backed by the threat of expulsion from the bureau for non compliance. It is at this point that credit bureau membership would be expanded to include most non-bank credit providers.

Management independence Operational independence and data security are important issues for the commercial banks. It is essential that credit bureau management is seen to be independent of any single or group of stakeholders. There also needs to be in place legislation or regulations to deter misuse of credit bureau data. Failing that, the Board and membership of the bureau must agree to a strictly enforced set of standards (code of conduct) which bureau management is fully empowered to enforce.

Role of international partner Operational independence is likely to be more readily achieved where credit bureau operations have been outsourced to a third party, either a international credit bureau operator, or a joint venture company, in which the international operator has a shareholding.

5.3 Set-up costs The following very preliminary estimates are intended to give an indication only and are examples of the ranges that could exist. Considerable further analysis would be required before a Request For Tender could be prepared. Set up costs could also vary depending on which development options were chosen. Costs are shown in $US based on comparable costings from Australia.

5.3.1 Building a credit reporting system independent of the major international vendors

The costs for both scenarios shown on the previous page exclude: Physical set up of the data centre; Communication interfaces and software;

ADB SME DEVELOPMENTTA

13

Salary costs for bureau staff, system operators, programmers, administration etc.; Customer support costs (ongoing education and training); Communication costs; Computer terminal equipment; Office fit out.

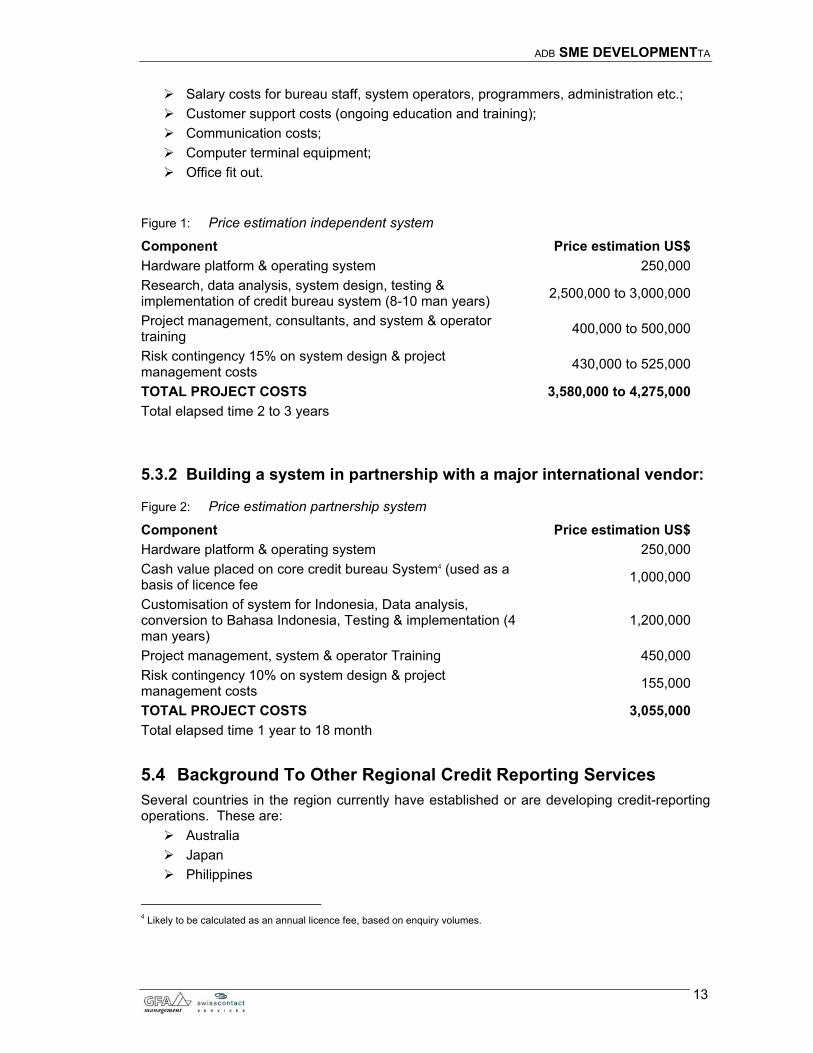

Figure 1: Price estimation independent system

Component Price estimation US$Hardware platform & operating system 250,000Research, data analysis, system design, testing & implementation of credit bureau system (8-10 man years) 2,500,000 to 3,000,000

Project management, consultants, and system & operator training 400,000 to 500,000

Risk contingency 15% on system design & project management costs 430,000 to 525,000

TOTAL PROJECT COSTS 3,580,000 to 4,275,000Total elapsed time 2 to 3 years

5.3.2 Building a system in partnership with a major international vendor:

Figure 2: Price estimation partnership system

Component Price estimation US$Hardware platform & operating system 250,000Cash value placed on core credit bureau System4 (used as a basis of licence fee 1,000,000

Customisation of system for Indonesia, Data analysis, conversion to Bahasa Indonesia, Testing & implementation (4 man years)

1,200,000

Project management, system & operator Training 450,000Risk contingency 10% on system design & project management costs 155,000

TOTAL PROJECT COSTS 3,055,000Total elapsed time 1 year to 18 month

5.4 Background To Other Regional Credit Reporting Services Several countries in the region currently have established or are developing credit-reporting operations. These are:

Australia Japan Philippines

4 Likely to be calculated as an annual licence fee, based on enquiry volumes.

ADB SME DEVELOPMENTTA

14

Thailand China (Hong Kong) Malaysia South Korea India New Zealand Taiwan

5.4.1 Established Credit Bureaus Established credit bureaus operate in Australia, Hong Kong, Japan (3 bureaus), Malaysia (private bureau), New Zealand, Philippines, South Korea and Taiwan.

5.4.2 Developing Credit Bureaus The credit bureau in Malaysia owned by Bank Negara has outsourced its bureau system development to a private consortium. It is not yet operational. The Peoples Bank of China supports the privately owned credit bureau in Shanghai. It is building its own credit bureau system and is not yet fully operational. The privately owned credit bureau in Thailand is majority owned by the Thai Bankers Association with minority shareholdings held by Trans Union Corp and a local Dun & Bradstreet affiliate. The company has outsourced its bureau operations to the Dun & Bradstreet affiliate, which has licensed credit bureau software from Trans Union Corporation. The bureau is partly operational. The privately owned credit bureau in India is majority owned by the State Bank of India and the Housing Development Corporation, with minority shareholders Trans Union Corp and Dun & Bradstreet (USA). The project has the active support of the Reserve Bank of India. The company is licensing credit bureau software from Trans Union Corp. It is not yet operational.

ADB SME DEVELOPMENTTA

15

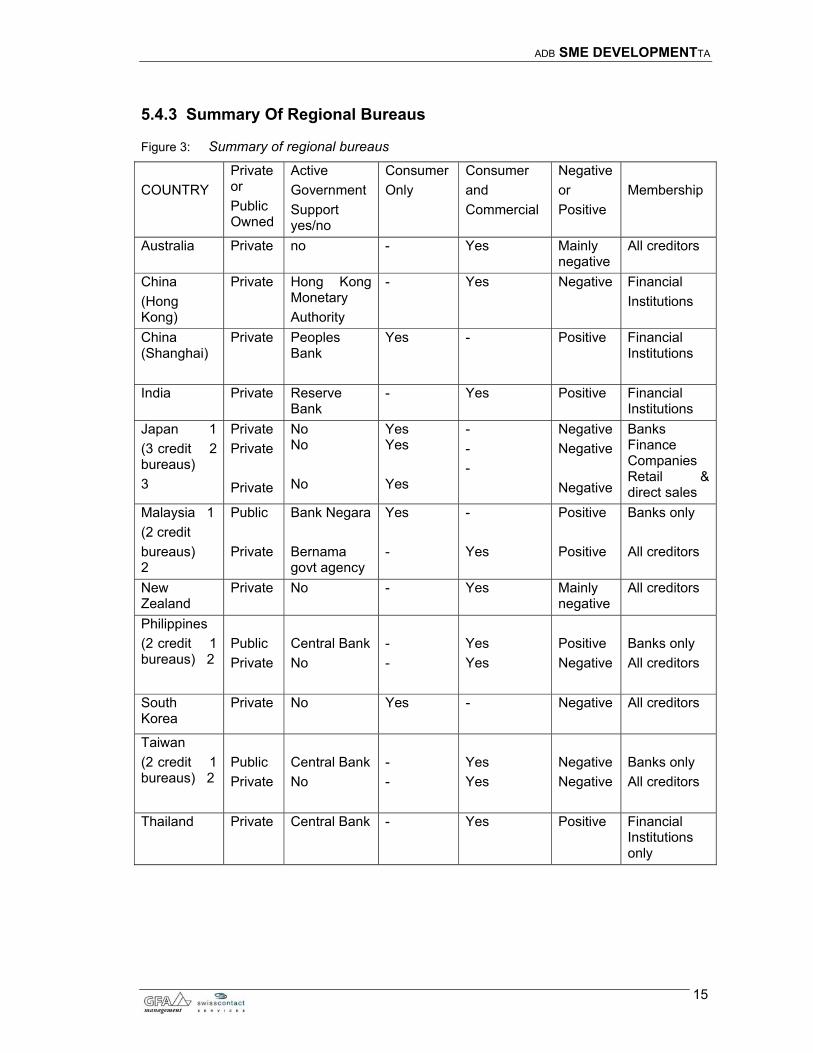

5.4.3 Summary Of Regional Bureaus

Figure 3: Summary of regional bureaus

COUNTRY

Private or Public Owned

Active Government Support yes/no

Consumer Only

Consumer and Commercial

Negative or Positive

Membership

Australia Private no - Yes Mainly negative

All creditors

China (Hong Kong)

Private Hong Kong Monetary Authority

- Yes Negative Financial Institutions

China (Shanghai)

Private Peoples Bank

Yes - Positive Financial Institutions

India Private Reserve Bank

- Yes Positive Financial Institutions

Japan 1 (3 credit 2 bureaus) 3

Private Private Private

No No No

Yes Yes Yes

- - -

Negative Negative Negative

Banks Finance Companies Retail & direct sales

Malaysia 1 (2 credit bureaus) 2

Public Private

Bank Negara Bernama govt agency

Yes -

- Yes

Positive Positive

Banks only All creditors

New Zealand

Private No - Yes Mainly negative

All creditors

Philippines (2 credit 1 bureaus) 2

Public Private

Central Bank No

- -

Yes Yes

Positive Negative

Banks only All creditors

South Korea

Private No Yes - Negative All creditors

Taiwan (2 credit 1 bureaus) 2

Public Private

Central Bank No

- -

Yes Yes

Negative Negative

Banks only All creditors

Thailand Private Central Bank - Yes Positive Financial Institutions only

ADB SME DEVELOPMENTTA

16

5.4.4 Three Regional Credit Bureaus - ownership and operational issues As part of this study, contact was made with the Managing Directors of three regional credit bureaus, Hong Kong, Thailand and India. The following questions were put to them:

What is your ownership structure? Hong Kong - 5 local banks and AMEX 37.5% Trans Union Corp 56.25% Dun & Bradstreet 6.25% Thailand - 13 Thai banks 50.0% Trans Union Corp 25.0% Business On Line (Thai) 25.0% India - State Bank of India 40.0% Housing Development Corp 40.0% Trans Union Corp 10.0% Dun & Bradstreet 10.0%

How do you ensure independent operations? Hong Kong - strong local (bank) Board representation Thailand - strong local (bank) Board representation India Reserve Bank of India – regulation guarantees the independence of

the bureau, plus the reputation of our two main shareholders. In the case of Hong Kong and Thailand it was commented that having a strong international partner who could bring its operational experience to Board meetings was useful in resolving issues which might arise from time to time.

Do you have data matching problems to overcome? Hong Kong - no, citizen identity number is secure Thailand Yes we are still working on the problem. We have a national citizen

I.D., but people can have more than one card. We are asking our members to clean up their customer information.

India Yes, a big problem. We do not have any unique identity number system and name and address information is unreliable. We will solve it, but it is taking a lot of work

Did you need special legislation to operate? Hong Kong Yes, we operate under a ‘Code of Practice for Consumer Credit Data’,

which is part of our Privacy Act legislation. Thailand No, but a draft Credit Bureau Act to spell out our function is being

debated in Parliament. India Yes, we are establishing the credit bureau on the understanding that

legislation will be in place to permit banks to exchange credit information among themselves and with none- bank finance companies. We believe we will be able to include other credit providers over time.

ADB SME DEVELOPMENTTA

17

6 APPENDICIES

6.1 Evaluation of Bank Indonesia’s – Debtor Information System

Debtor Information System - part of central bank supervision The Debtor Information System (DIS) forms part of a comprehensive data-gathering and bank supervision program conducted by Bank Indonesia. DIS operates under Bank Indonesia Regulation Number 1/7/PBI/1999. The Regulation has the force of law for commercial and foreign banks subject to Bank Indonesia authority. The data-gathering program of which DIS is part has been operating in one form or another since 1973. The information collected is used primarily by Bank Indonesia to fulfil its responsibilities of bank supervision and regulation. The information reported to Bank Indonesia by the commercial banks exceeds what would normally be required for a credit-reporting service. This is because approximately seventy percent (70%) of the information appears to be used by Bank Indonesia for prudential supervision, statistical analysis and monitoring of individual bank’s exposure to bad debts and dubious lending practices. DIS supplies a basic credit risk information service to the commercial banks. DIS information is extremely comprehensive and the disciplined reporting standards imposed on the commercial banks have ensured the integrity and accuracy of information in the database. However the system’s effectiveness is limited.

Participation is restricted The reporting of information to DIS is restricted to the ‘Commercial Banks’ and branch offices of foreign banks. Whilst the commercial banks and foreign banks include all the larger Indonesian banks, a large number of credit providers are excluded. These include:

Figure 4: Credit Providers excluded from DIS

Approx. number Venture capital banks 10 Rural banks (BPR) 2,000 Credit Cooperatives 80,000 Utilities (eg Telecoms) 20 Trade (commercial) creditors 20,000+ Finance and leasing companies Not known

Majority of Loan Agreements Are Not Recorded Bank Indonesia Regulation Number 1/7/PBI/1999, Article 5 specifies that only credit facilities (loans) of Rp 50 million ($US4,330 / $A8,300) or more are to be reported to DIS by the commercial banks. The effect of this regulation is that most loans/credit facilities are not reported to DIS. For example, no credit card information is reported. There are an estimated 1.1 million active credit card accounts. A Bank Indonesia report, Statistic Kredit Koperasi Dan Kredit Usaha Kecil ( KUK – Small Business Credit), dated June 2000, includes an analysis of small business credit facilities provided by the commercial banks for the month of June 2000.

ADB SME DEVELOPMENTTA

18

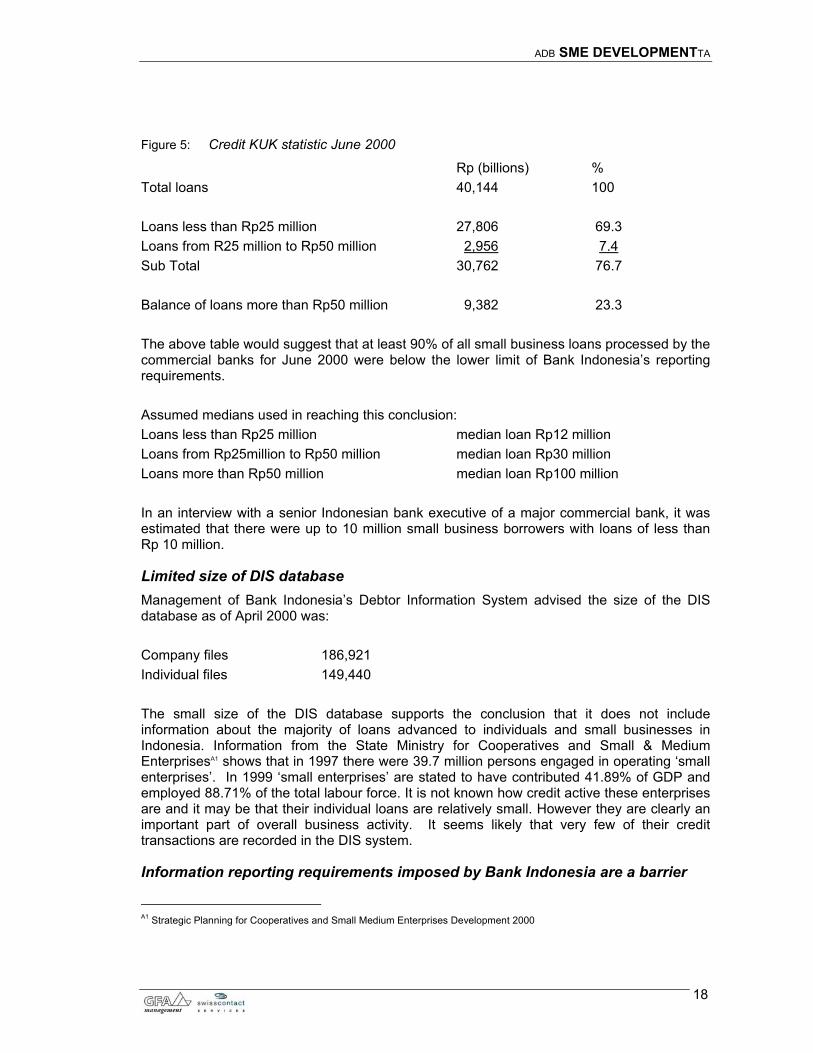

Figure 5: Credit KUK statistic June 2000

Rp (billions) % Total loans 40,144 100 Loans less than Rp25 million 27,806 69.3 Loans from R25 million to Rp50 million 2,956 7.4 Sub Total 30,762 76.7 Balance of loans more than Rp50 million 9,382 23.3 The above table would suggest that at least 90% of all small business loans processed by the commercial banks for June 2000 were below the lower limit of Bank Indonesia’s reporting requirements. Assumed medians used in reaching this conclusion: Loans less than Rp25 million median loan Rp12 million Loans from Rp25million to Rp50 million median loan Rp30 million Loans more than Rp50 million median loan Rp100 million In an interview with a senior Indonesian bank executive of a major commercial bank, it was estimated that there were up to 10 million small business borrowers with loans of less than Rp 10 million.

Limited size of DIS database Management of Bank Indonesia’s Debtor Information System advised the size of the DIS database as of April 2000 was: Company files 186,921 Individual files 149,440 The small size of the DIS database supports the conclusion that it does not include information about the majority of loans advanced to individuals and small businesses in Indonesia. Information from the State Ministry for Cooperatives and Small & Medium EnterprisesA1 shows that in 1997 there were 39.7 million persons engaged in operating ‘small enterprises’. In 1999 ‘small enterprises’ are stated to have contributed 41.89% of GDP and employed 88.71% of the total labour force. It is not known how credit active these enterprises are and it may be that their individual loans are relatively small. However they are clearly an important part of overall business activity. It seems likely that very few of their credit transactions are recorded in the DIS system.

Information reporting requirements imposed by Bank Indonesia are a barrier

A1 Strategic Planning for Cooperatives and Small Medium Enterprises Development 2000

ADB SME DEVELOPMENTTA

19

Possibly because of Bank Indonesia’s regulatory and supervisory role it requires the commercial banks to report to it, every month, very comprehensive information about their current loan activities. This information, which is recorded in the DIS database, is well in excess of what is normally required for credit reporting purposes. Any proposed expansion of DIS reporting activity (for example, removing the current Rp 50 million lower limit on the reporting of loan agreements) would possibly meet with resistance from the commercial banks, who could be concerned about the significant additional costs resulting from an increase in reporting volumes of around 900%. It could be expected that other non-bank lenders and credit providers who would otherwise wish to participate in an expanded credit reporting service, would also be concerned about the prospect of a substantial additional overhead cost.

DIS technology is adequate for existing use but may have limited growth potential. The enquiry system and communications technology is inadequate. Limited information is available about the information employed in the DIS system. The system is reported to be operating on a Compaq Alpha 1200 platform, using Oracle database management software and supporting Delphi as the primary programming language. Bank Indonesia computer division staff provide internal technical support. An Indonesian telecommunications company, PT Aplikanusa Lintasarta manages the dial up network. It is understood that Lintasarta also designed and wrote the applications software utilised by DIS. System hardware appears to be a lower end, mid-range processor when compared to high end Unix processors, however the Alpha 1200 platform is understood to have upgrade capacity. The Oracle database management software has an excellent reputation. As a programming language Borland’s Delphi software is widely regarded as second to Microsoft’s Visual Basic. However the latest version of Delphi provides a rapid development environment for Windows, capable of supporting new emerging web services. Credit enquiries are processed by means of dial up access to a DIS mailbox, using the communications network owned by Lintasarta. Enquiries are logged into the mailbox and are subsequently retrieved for processing by data entry operators. The DIS operators then re-key the enquiry information for an internal search of the DIS database. The results of the file search are transmitted to the enquiring bank’s mailbox and processed by a duly authorised bank officer. Responses from DIS take from one to three days. Possibly as a consequence of the limited scope of DIS and the delayed response times, usage of DIS is less than could be expected. DIS receives up to 500 enquiries a day from banks in the Jakarta region, plus a further 500 daily from the rest of Indonesia. Annual enquiries are stated to be approximately 160/170,000. This is low for an economy of the size of Indonesia. An initial evaluation of the DIS service suggests the current technology platform is well able to support the service’s current business volumes. It is however questionable whether the present hardware/software combination would be compatible with the requirements of an international standard credit reporting system, particularly if transaction volumes were substantially increased and users were given real-time online access to the database system. The current off-line access and enquiry processing procedures are inadequate and below comparable international practice. Very significant development work would be required to enable DIS to provide acceptable high capacity, online enquiry access and data retrieval.

Current management may not have the skills or experience to effect change Current management and technical staff may not have the experience or the skills required to bring about the major changes that would be required to develop and operate a fully

ADB SME DEVELOPMENTTA

20

functional credit reporting service. This should not be read as a criticism of current management’s effectiveness or ability to manage the present service. It is simply recognition that managing a modern credit reporting service requires an experienced team of professional credit bureau personnel.

The future of DIS is in doubt As part of the Government’s reform of the financial sector, new legislation creating a national supervisory/regulatory body for all Indonesia financial institutions, is currently before the Parliament. The legislation, due to be approved by the end of 2001 will deliver the ‘Integrated Financial Supervisory Institution’ (IFSI). IFSI will assume the bank regulation and supervisory role currently exercised by Bank Indonesia. It is expected that IFSI will be operational by end 2002. The establishment of this new regulatory body raises a number of questions about the future of Bank Indonesia and in particular DIS. DIS is not a central, or significant part of Bank Indonesia. It operates as a small section within Bank Indonesia’s Banking Data Division, which in turn forms part of the Banking Licensing and Information Directorate. During meetings with the management of DIS, and other senior executives within Bank Indonesia, concern was expressed about the future of Bank Indonesia and its various services and functions. In particular there was doubt about the future of DIS. It was suggested the service could be overlooked in the transfer of Bank Indonesia functions to IFSI, with a resulting loss of resources. It was questioned whether IFSI would wish to assume responsibility for DIS. Should it not do so, then DIS would lose its power to require the commercial banks to report data and would lose credibility. Contrary to this view, if IFSI were to assume responsibility for DIS, this could result in a potential expansion of the service to cover all those financial institutions under the authority of IFSI. There is substantial inherent value in both the DIS database and the reporting disciplines required of the commercial banks. The reporting disciplines imposed on the commercial banks by Bank Indonesia have resulted in an accumulation of valuable, well-organised credit information in the DIS database. The basic integrity of DIS data and the depth of information held in the system is a direct result of the strong supervisory position of Bank Indonesia. DIS data would form a valuable basis for any expansion into a comprehensive credit reporting system. Regardless of any changes which might be contemplated for the future of credit reporting in Indonesia every effort should be made to preserve and utilise the existing DIS database and the reporting disciplines which regulate the supply of debtor information to DIS. (See Appendix 6 “Guide Book For Preparation of Report On Provision of Fund and Debtor Information” (hard copy only available)

ADB SME DEVELOPMENTTA

21

6.2 Benchmarking Bank Indonesia’s debtor information system Credit information systems worldwide fall into two distinct categories. These are defined as follows: Public credit registries, (PCRs) generally operated by a central bank, where participation is limited to those banks or financial institutions supervised by the central bank and participation, including the reporting of data to the PCR is compulsory. The primary purpose of data collection for most PCRs is to assist in bank supervision. The benchmarking of the DIS service with other PCRs draws on information contained in a report published by the World Bank in June 20005. Private sector credit bureaus may be private or public listed companies or owned by a consortium of credit bureau users (banks, finance companies etc.). Membership of private sector bureaus is voluntary and normally includes a wide range of credit providers from banks to small retail outlets. The reporting of data to the bureau is usually governed by a written agreement. The primary purpose of data collection for private credit bureaus is to assist credit providers to make better-informed credit risk assessment decisions The benchmarking of DIS against private sector credit bureau practice is based on this author’s personal knowledge of international private sector operations.

6.2.1 Benchmarking Against Public Credit Registries

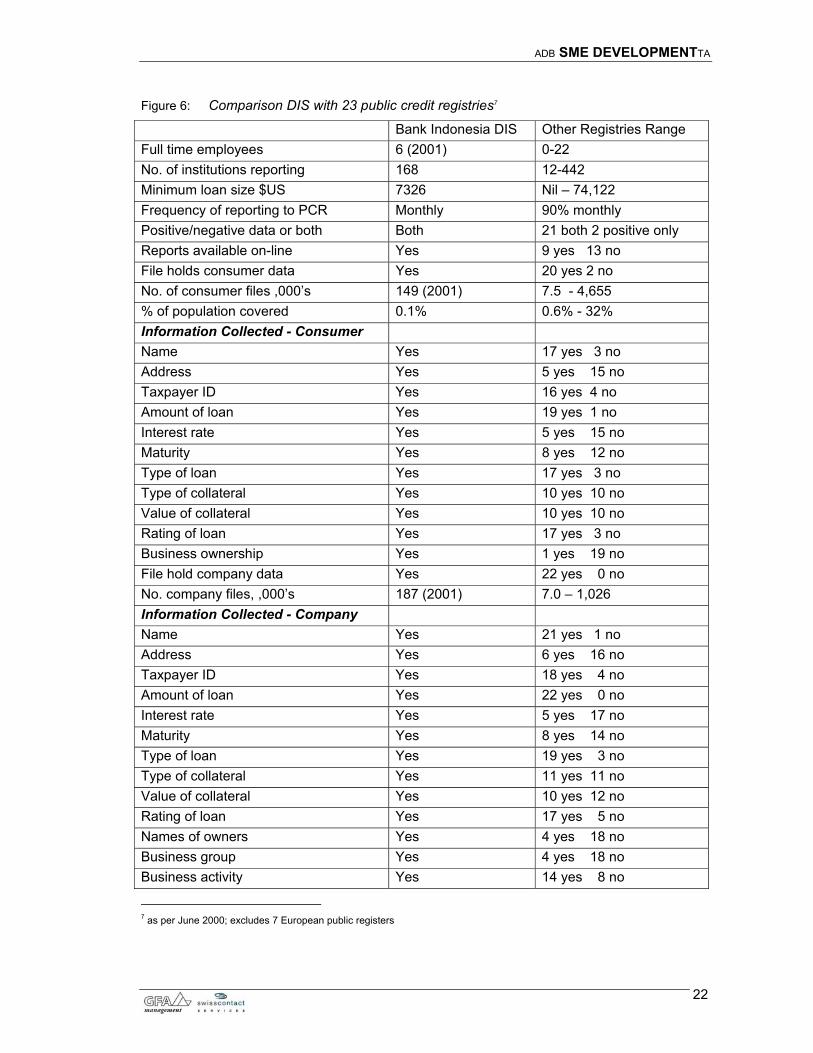

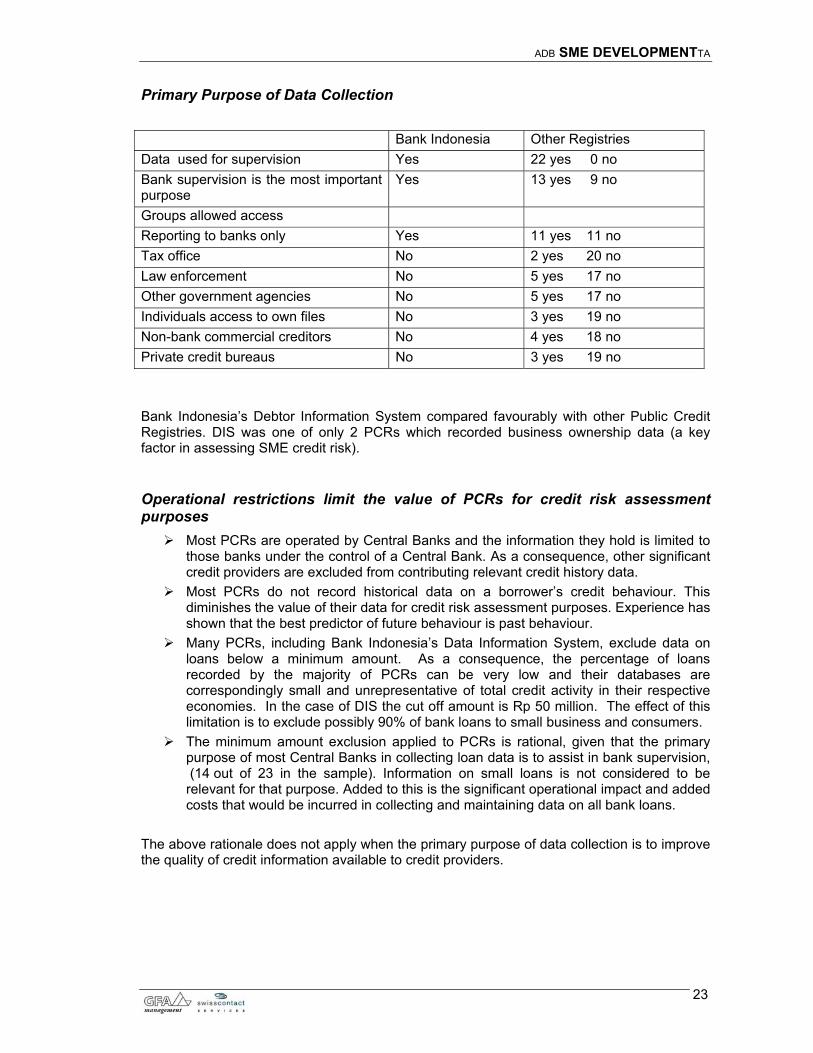

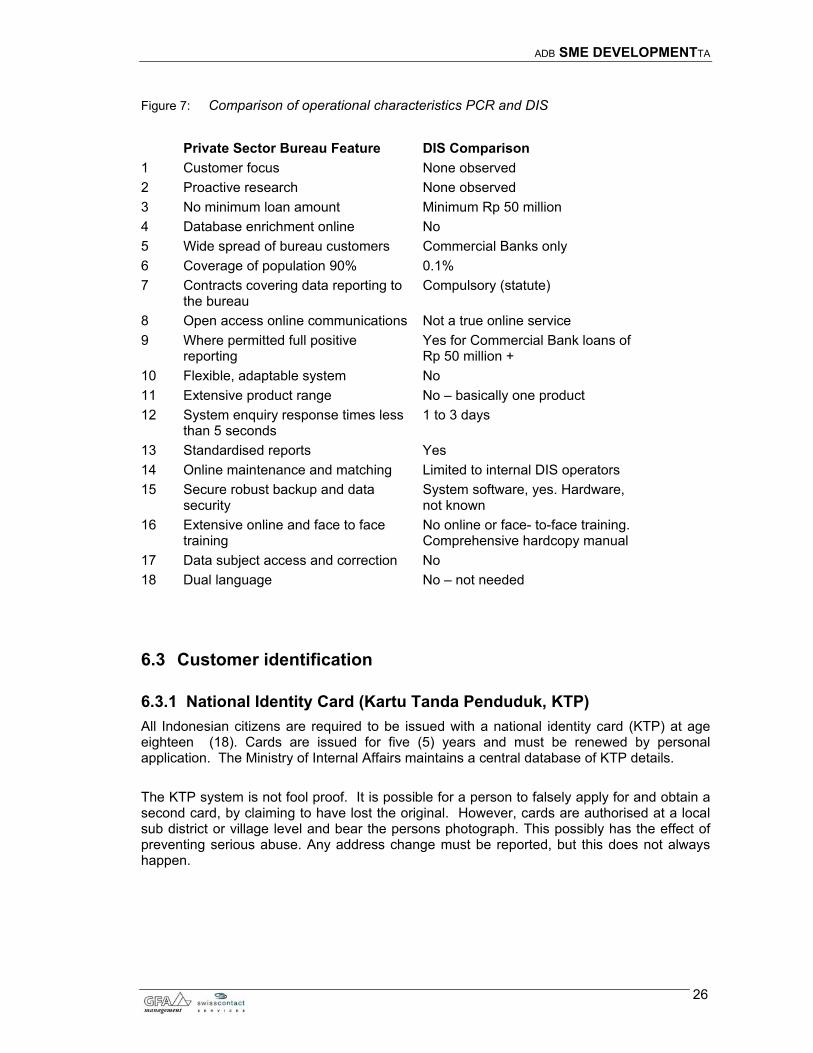

Sample of 23 selected Public Credit Registries (PCRs) including DIS6 -overall findings

The Debtor Information System operated by Bank Indonesia compares favourably with other public credit registries. It is within the mainstream of the benchmark group.

The information DIS holds on commercial credit loans is more comprehensive than

that held by most other PCRs. However, the DIS database of consumer credit loans had the lowest market penetration of PCRs in the sample.

5 Credit Reporting Systems Around the Globe – The State of the Art in Public and Private Credit Registries, Author Margaret Miller, Economist World Bank, June 2000. 6 Credit Reporting Systems Around the Globe – World Bank, June 2000

ADB SME DEVELOPMENTTA

22

Figure 6: Comparison DIS with 23 public credit registries7