Embed Size (px)

Citation preview

CHAPTER 1

PREAMBLE

1.1 History of Indian Pharma Industry

Indian Pharmaceutical Industry has 125-years old history, a humble beginning with Bengal

Chemical & Pharmaceutical Ltd. This was an example of a doctor and chemist joining hands to

lay the foundation of the chemical and pharmaceutical industries in India. Dr. Prafulla Chandra

Ray conceived an idea of starting chemical and pharmaceutical manufacture in the country with

twofold object of making India self-sufficient in drugs and chemicals and opening an

employment to the Pharma/Science graduates, an educated middle class. Very soon

Dr.Amulyacharan, a fellow student and a successful medical practitioner, joined Dr. Prafulla

Ray. Joining of Dr. Amulyacharan, proved to be invaluable. Both started with a meager capital

of Rs. 700, which increased to modest Rs. 23,500 in the first year.

The first factory was established in the suburb of Calcutta-at Maniktala. This factory started

manufacturing Sulphuric acid and pharmaceuticals in large scale. Another factory was

established in 1921, at Panihati, for producing Alums. In next 25 years, injectable drugs,

vaccines, gland products, vitamin preparations’ manufacturing was started. Bengal Chemical

established another factory in Mumbai in 1938 due to transport issues and to overcome excise

barriers. On June 16, 1944, the great patriot, a visionary scientist and very great educationist, Dr.

Prafulla Chandra Ray breathed his last in Mumbai.

In 1951-52, for the first time in the history of Drug Control Organization in the country, a full

time Drug Controller with Pharmacy Qualification was appointed by Bombay Government and

he was none other than late Mr. B V Patel. He is recognized even today as father of Drugs

Control movement in India.

In 1959, Bombay Government took another landmark decision and created a position of

Directorate of Drugs Control, under whom either Directorate of Health Services or Drugs

Controllers of other states would report. In 1969, the first separate faculty of Pharmacy was

instituted in Gujarat University.

The other meritorious name in Pharma Industry could be that of Dr. R S Vedaraman, the

Controller General of Patents, Trademarks & Designs, appointed by the Government Of India.

He did wonderful job from 1968 to 1982. He easily qualifies as a single most person, who

changed the destiny of the Indian Pharmaceutical Industry by crafting the INDIAN PATENT

ACT 1970. This is the time; all multinational corporations operating in India had sleepless night.

All possible tricks, allurements and shenanigans were employed to torpedoe the bill. It was very

difficult to crack the hard nut like Dr. Vedaraman. He not only protected and preserved the 1970

Patent Act, but ensured that India joins the Paris convention. He had led Indian delegations to

various International Conferences on IPR. He was also instrumental in getting sanctions from

Finance Ministry, Govt. of India, for setting up patent offices in Mumbai, Chennai and Delhi.

Mr. V C Sane was the first Drugs Inspector in the country, and was appointed on 1st November,

1942. Later on he became FDA – Commissioner of Maharashtra. He developed programs for

Consumer awakening and also training programs for Inspectors.

Prof. M L Schroff had a vision to give practical shape and direction to pharmaceutical education

and also to the organization of pharmacy profession. He worked against many odds. A regular B

Pharm course of three years duration was introduced in July, 1937. Professor Schroff started the

United Provinces Pharmaceutical Association, in December 1935. This was re-christened as the

Indian Pharmaceutical Association in December 1939.

Prof. Madan Lal Khorana has a long and distinguished career as a teacher and Research Guide,

having taught more than 300 students, trained over of M. Sc., M. Sc., (tech), PhD (tech). During

his tenure as chairperson of Education committee of the Indian Pharmaceutical Association,

BOMBAY COLLEGE OF PHARMACY at Kalina was established.

There are many eminent personalities, who contributed in their own way for development of

Pharmaceutical Industry in India.

In 1935, Dr.Khwaja Abdul Hameid set up a CIPLA (Chemical Industrial & Pharmaceutical

Laboratories Ltd.) Dr. Hameid’s obsession that India could manufacture sophisticated allopathic

products bore fruits at later stage. Dr. Y K Hameid , a second child of Dr. K A Hameid got

headlong into R &D at CIPLA in 1960. He took tremendous interest in manufacturing FINE

CHEMICALS, STEROIDS, ALKALOIDS, & NATURAL PRODUCTS he went on to

consolidate CIPLA to number ONE POSITION in today’s Indian Pharma Market. DR. Y K

Hameid played a vital role in Indian Patent act 1970.

Another development was in Gujarat region. Dr. Indravadan Mody & Late Mr. Ramanbhai

Patel, the two college mates came together to start CADILA in 1951.After 45 years association ,

CADILA LABORATORIES was re-engineered by the founder directors in June,1995 and the

two new companies were formed - CADILA HEALTHCARE( owned by Patel group) and

CADILA PHARMACEUTICALS (owned by Modi group).

In North India, under the leadership of Late Dr. Parvinder Singh, RANBAXY

LABORATORIES was taking shape. Dr.Singh realized that to meet domestic and International

challenges, management needs to change attitudes and systems. He brought changes in the

organization by decentralizing, open communications, accurate information, flexible planning,

rapid response, and by motivating the team.

In south India, Late Dr. Anji Reddy played role in the growth of Bulk Drugs sector, who started

Dr. Reddy’s Laboratories Ltd, in 1984. Later on he set up Dr. Reddy’s Research Foundation a

research arm of Dr. Reddy’s Group. This is the first institute in India, to take ‘Basic Research’.

They have 55 patents with United States. Today Dr. Reddy’s annual turnover has passed

Rs.12000 crores.

1975-1990 period, with no exaggeration, can be underlined a period of boom to Indian Pharma

Industry. Lots of Indian Pharma Companies got registered e.g. LUPIN, SUN Pharma,

MANKIND, ALKEM, EMCURE, GLENMARK, MACLEODS, TORRENT etc.

However, until then, MNCs were doing R&D and getting Patents, whereas, most of the Indian

companies were producing finished products whose patent was expired.

1.2 Prior to Indian Patent Act 1970.

Prior to 1970, Indian Pharma Industry was dominated by Multinational companies (MNCs) with

68% market share. The then patent act, prevented Indian companies to produce new drugs. The

MNCs were keener to process imported bulk drugs than develop the industry from basic stages.

Thus, prices of drugs were very high. India was more dependent on imports. Imports constricted

consumption in a country.

1.3 Period between 1970 &1980

The change in Patent act, motivated industry and large scale production of bulk drugs started in

India. The development of Bulk Drugs sector is actually the most important achievement of the

Pharmaceutical industry in India. This led to the transformation of the Industry. The imports got

reduced and were replaced by indigenous materials. This further led to an increase in

consumption and unprecedented growth in formulations activities. This growth was spearheaded

by the Indian companies. Slowly but surely, MNCs started losing their domination and a market

share.

The environment was much favorable to Indian industries, which benefited many Indian

entrepreneurs. Many new companies were registered, which have become now giants not only in

Domestic market but have marked their space in the Global market too! To name few- Ranbaxy,

Sun Pharma, Lupin laboratories, Glenmark, Cadilla, Ipca, Dr. Reddys, CIPLA, Aurobindo, etc.

1.4 Indian Pharma industries after 1990.

India today produces almost 400 bulk drugs ranging from pain killers to antibiotics, cardiac,

anti-diabetic products. Processes like synthesis, fermentation, extraction etc. are well developed

indigenously.

Indian companies developed their own processes which are far better than Innovators. They are

superior and more cost-effective. India has become largest exporter of Active Pharmaceutical

Ingredients (API). Many of our APIs are exported to regulatory markets such as USA, UK,

Australia, Japan, Latin America and other countries.

The Indian Patent Act of 1970 and aggressive entrepreneurship helped Indian Pharma Industry

to put an industry on Global map. Prior to TRIPS, there were 47 other countries that did not

provide product patent despite that, Pharmaceutical Industry remained underdeveloped in those

countries. Many of these countries like Ghana, Iran, Iraq, Malawi, Pakistan, Vietnam, and

Uruguay lacked talents, entrepreneurial skills as well as technological skills. India is also

different in other way, that, indigenous private sector was actively supported by public

investments in R&D and Manufacturing. Government of India has taken on priority, public

health issue vis-à-vis development of Pharmaceutical Industry. Pharma associations, like IDMA

(Indian Drugs Manufacturers Association), OPPI (Organization of Pharmaceutical Producers of

India) represent Indian and MNCs respectively.

1.5 Indian Pharma Industry today!

Indian Pharma Industry is on threshold of becoming a major global market. There are more than

3000 companies and over 10500 manufacturing units. It is very much intensely competitive

market. Many dynamic changing trends can be seen, such as Mergers, large acquisitions,

increased trends of investments of Indian companies as well as MNCs. Penetration into rural

markets, growth factors all round, availability of healthcare facilities, different hospital chains

etc.

Indian Pharma Market is today driven by OTC products, patented products, Generic generics and

Branded generics. There is a great potential for Indian Pharma Industry to grow. It is one of the

fastest growing industries, not only in domestic market but in global market too. There are

emerging sectors too, such as, Bio-Pharmaceuticals, Bio-generics, Bio-similar. Pharma

packaging is also going to contribute significantly too.

1.6 Public Sector in Pharmaceutical Industry:

In the development of pharmaceutical industry in India, a major noticing event is setting up of

two public sector companies- Indian Drugs and Pharmaceuticals Ltd. (IDPL) in 1961 and

Hindustan Antibiotics Ltd. (HAL) in 1954. However, the origin of these two companies can be

traced to the work done at Haffkine Institute which was established in 1899, by the then

provincial Government of Bombay. HAL started manufacturing Penicillin, under the technical

assistance provided by WHO (World Health Organization). IDPL started manufacturing Folic

Acid, Vitamin B1, Streptomycin, Tetracycline, Isoniazid etc. Eventually, IDPL made foreign

collaboration with Farmafin of Italy and HAL made with Merck of USA. Both these two

companies gave boost to indigenous products and enhanced confidence amongst Indian

manufacturers.

Currently both these companies are not operative. Earlier they were declared sick and finally

went under BIFR (Board for Industrial & Financial Reconstruction).

1.7 Contributions of Research Laboratories

After independence many research laboratories were set up under CSIR (Council of Scientific &

Industrial Research). Mainly, CDRI (Central Drug Research Institute), Lucknow and IICT

(Indian Institute Of Chemical Technology), Hyderabad developed new drugs; however these

were commercially never launched. CSIR played major role in developing drugs and also

technology for manufacturing. There are six CSIR laboratories involved for manufacturing bulk

drugs.

1. CDRI (Central Drug Research Institute, Lucknow).

2. IICT (Indian Institute of Chemical Technology, Hyderabad).

3. CIMAP (Central Institute of Medicinal & Aromatic Plants, Lucknow).

4. NCL (National Chemical Laboratory, Pune)

5. RRL (Regional Research Laboratory, Jammu)

6. RRL (Regional Research Laboratory, Jorhat)

Almost all top Indian Pharma companies –Sun Pharma, Wockhardt, CIPLA, Ranbaxy,Torrent

etc. have used the services of CSIR. Lupin was benefited for vitamin B6 technology from NCL.

CIPLA used IICT mainly for anti-cancer drugs, and anti-asthma drugs.

1.8 Patents and Pharma industry.

The Patents are basically granted for : (a) It is expensive to generate knowledge which is

economically useful (b) Patents will stimulate innovations and research.(c) Innovator should be

able to recoup the invested costs (d) It will debar the other imitators for certain period of time

and in this period an innovator can recover the costs (e) the costs recovered by an innovator can

be re-invested in further research.(f) the cost of inventing new entity (NCE) is high whereas cost

of developing processes for manufacturing is low, hence imitation in Pharma industry is easy.

In the absence of patent , innovator cannot recoup the total costs.

If patent protection is not granted in Pharmaceutical Industry, an investment in R&D would be

reduced to a large extent. The empirical study done by M/s. Taylor & Silberstein in 1973 for the

UK industry and by M/s. Mansfield in 1986 for the US industry have reached the same

conclusions.

However, other argument is that, Patent once granted, it prohibits others to manufacture and

market the product, thereby innovator gets an opportunity to raise the price which is very

exorbitant and unaffordable. The classic case is that of CIPLA offering drugs for AIDS (acquired

immune-deficiency syndrome) at USD 350 as against USD 10,000 offered by Pfizer an

innovator. It has been possible for CIPLA to play such a role since no patent protection for

product was granted. The other countries who do not grant product patent are Brazil, China,

Cuba, Egypt, Korea, Mexico, Thailand, Uruguay, Vietnam etc.

1.9 Indian Patent act & Pharma industry.

The Pharmaceutical Industry is “Regulated” industry and hence being controlled by various laws

and regulations. “Patents” is one of the important aspects in the industry. Entire “market” of

drugs is controlled by various patents. The process of search of new entity (new drugs) till it is

launched in the market is very tedious and complicated. Obviously, this all adds to the cost of a

new drug. Higher price is one of the reasons of these costs. India is internationally known as a

country of having lower prices. The lower prices have given sleepless nights to most of the

MNCs. (Multi-National Companies) mainly from UK and USA. Their huge profits are getting

reduced day by day and year after year.

Patent is given to the innovator. Once the drug is successful in “animal test”, patent application is

filed. There are 3 distinct characteristics for getting a patent. (1)The research must be a “NEW”

one. The organic structure of a new drug must not have been the same as of existing drugs or

have not been made early. (2) The new drug must be distinct-innovative one (3) the process of

manufacturing must be such that it can be manufactured on large scale in the factory. Patent-

office of respective country checks the details on this basis.

Once patent is given, an imitation is barred. Imitation reduces the chances of recouping an

investment to an innovator. Imitated drug is sold at cheaper price and that makes a difference to

Innovator. Innovator cannot cover up its research expenses.

Patent’s life span is 20 years i.e. protection to innovator is 20 years. After 20 years any firm can

imitate and sell the drug called as Generic Drug. Due to intense competition, the retail prices of

these drugs get reduced. The price difference could be 80% less than the innovator price .The

Generic drug does not mean duplicate drug or with fewer efficacies. The manufacturer of such

drugs need to take permission from Drugs Controller Of India and needs to prove efficacy of

such drugs at par with that innovator, along with other details.

Today, India is recognized as a country making Quality drugs with least prices. India has more

US -FDA approved plants than USA itself. In fact US- FDA has opened its branch office in

Delhi, India. The export of “Generic Drugs” is mainly done by Dr. Reddy’s, CIPLA, Wockhardt,

Sun Pharma, Glenmark etc. India Pharma stands at no.3 in the Global competition.

Prior to Independence, the mortality rate in India was very high due to unhygienic conditions,

poverty, epidemic diseases. The drugs manufacturing in India was almost nil. Most of the drugs

were imported. The import price used to be so high, that, poor people in India could not afford.

To make availability of affordable drugs to the larger population in India, Govt. of India

appointed “Iyengar Committee”. One of the remedies recommended by the committee was to

change Patent Law. Committee studied other nations and concluded that less protection to patent

is the remedy to make available drugs at lower prices.

Iyengar committee suggested that medicines, chemicals, & foods—these are the areas where

only PROCESS PATENT should be given and not PRODUCT PATENT. On this basis, in 1970,

patent law was passed which gave boost to Indian Pharma to produce drugs at lower prices. Very

soon, India started exporting these drugs to other nations including US, UK, Australia, Canada,

South Africa etc.

India’s Pharma Industry progress became a deterrent to developed countries. The TRIPS was

brought in (Trade Related Agreement of Intellectual Property) 1996. The patent law of all the

nations should be the same and minimum protection years should be given to all patents of all

industries was the main agenda.

WTO forced to follow new laws of TRIPS after 2005. Hence India had to change its law. India

changed its patent act step by step in 1999, 2002 and 2005. India’s new patent act gives

protection to final product with clauses. By this time, Indian Industry was ready to face

challenges, taking benefits of old patent act of 1970- i.e. process patent.

TRIPS act says, that, Invention in any industry should be given patent. However invention is not

defined. This gives flexibility to interpret.

Developing countries decided to take advantage of such flaws. For public interest and security

purpose, India decided to keep prices of drugs low. This was expressly stated in 2001, in DOHA

and also in Indian Patent Act, 2005.

Companies like Pfizer, Novartis GSK, Bayer, Glaxo all these giant MNCs reduced the inventions

and new drugs discovery. Their monopoly almost vanished. These companies came out with new

solution i.e. “PATENT-REJUVINATION”. To make little change in the existing patent and call

it new-rejuvenation, to take further 20 years. This may suit the lifestyle of Developed countries,

since; sickness and medical expenses are insured. However in developing countries, the poor

person has to bear all the expenses. Indian patent act 2005, does not recognize rejuvenation of

patent.

Another highlighting point of the act is “COMPULSORY LICENCE”. Whenever patent is given

in India, certain conditions need to be fulfilled by the innovator.(1) will be manufactured in

India, (2) shall be available in Indian Market (3) price should be affordable by common man. If

one of the conditions is not fulfilled by the patented firm,(innovator) Government Of India can

issue “compulsory License” to any other manufacturing firm, which is capable of fulfilling

conditions even though patent was granted earlier e.g. Naxaver a cancer drug for kidney was

Rs.150,000 as against Rs.8000 per month of Indian firm. A huge difference !

Indian patent act 2005, allows to oppose Pre-patent or Post-patent. Patent is published prior to

granting. Anyone can oppose on the basis of unsuitability, inappropriateness or not being new

invention. Patent is not granted if one of the aforesaid grounds is applicable. In other countries,

opposition is possible only after granting, whereas, in India it is possible twice and hence better

control to avoid unnecessary patents.

All the aforesaid 3 clauses of Indian Patent Act are against interest of MNCs. MNCs cannot file

the suit or demand remedies from WTO, since, they are all as per TRIPS. For MNCs it is a

catch 22 condition. If they do not take Patent, generic manufacturer will grab an opportunity and

at the same time MNCs cannot avoid large market of Indian Population of 130 crs.!

US is putting pressure, that, India should remove these clauses. Govt. Of India has agreed to

form a committee to look into Intellectual Property Act and also agreed to take American

Officials on the board of the committee.

Prof. Carlos Korea is an expert on patents in drugs and medicines and an advisor to WTO.

According to him, Indian Patent Act has been crafted so intelligently, keeping in mind the

“patients’ rights”, that, all developing countries would follow them. Hopefully, India would not

come under pressure and would protect an interest of common Indian man.

1.10 US & Indian Patent act.

India’s intellectual property (IP) law has been hailed as one of the most progressive for

safeguarding public interest. Many countries are following it, especially, Brazil, Argentina, and

Philippines.

US Government is under pressure from corporates to take action against India over its IP laws.

Indian patent act is complying 100% with that TRIPS agreements of WTO. Hence if US takes

up with WTO, US will lose 100%. That is why US is taking up directly with Indian Government.

TRIPS allows flexibility to interpret what is NEW or INNOVATIVE. Pharma lobby that heavily

funds US government is too strong for the Government to bring the necessary changes in Patent

Laws.

In US majority of drugs being patented are just new forms of existing drugs with no change in

efficacy. In order to prevent this type of tweaking, Indian patent act has section 3 (d). US- FDA’s

own data says that 76% of patents in the US are only new forms of existing drugs. Thus, new

molecules discovery is grinding to a halt. In fact, US has been advised to follow Indian Patent

Act to prevent such tweaking.

In India, some lobby is pushing Government to change Patent Act. CII (Confederation Of Indian

Industries ) and FICCI (Federation Of Indian Chambers Of Commerce and Industry) want law

to be changed. In fact both these organizations are more or less part of MNC conglomerate.

All depends upon Government Of India, and hopefully it will not buckle to any pressure.

1.11 Drugs price control order (DPCO)

DPCO aim is to put regulatory framework for pricing of drugs, all over India, so as to ensure to

ensure (a) availability of drugs, (essential medicines) (b) availability at reasonable prices, which

are affordable to the poorer people.

The various drug policies, all these years, were broadly based on the principle of putting a ceiling

on prices of most popular drugs on a “lowest common denominator” basis. The Government Of

India finally realized that keeping prices under strict control and artificially very low will neither

benefit the patients, nor the industry.

The National Pharma Pricing Policy (NPPP) 2012, envisaged 3 major principles; (1) Essentiality

of drugs (2) Control on formulations and (3) Market based pricing. The paradigm shift from cost-

based pricing to market- based pricing, has been long overdue, as it has been stunting the

Industry’s growth and forcing manufacturers to discontinue production of some price controlled

drugs, since they are not viable.

The Department of Pharmaceuticals has now notified the DPCO 2013, and recommended that a

simple average of all the products in a therapeutic category with at least 1% market share is to be

considered based on IMS data.

An adverse impact of DPCO 2013 will be on both Sales and Margins, especially to MNCs.

New DPCO made drugs cheaper. --- MAY 2014 (Table No. 1.T1- Source:

AIOCD/AWACS, May2014 report)

DRUG Highest

Price

MRP

(Rs.)

Ceiling

Price

as per

new

DPCO

%

Reduc

tion

Category Leading Brands

Paracetamol

500 mg

Tablet

1.55 0.95 39 Fever/Pain Calpol,Crocin,Metac

in

Azthromyci

n 500 mg

Tablet

33.31 19.86 40 Anti-infective Azithral,

Azee,Azibact

Ceftazidime

200 mg inj.

132.1 63.4 52 Anti-infective Fortum, Tazid,

Megazid

Doxorubicin

50 mg inj.

2,074 1145.2 45 Oncology/

Anticancer

Adriamycin,Adrosal,

Duxocin

Losartan 25

mg tablet

4.51 2.50 45 Cardiac Losar, Repace,

Losacar

Atorvastatin

5mg tablet

6.88 3.82 44 Cardiac Atorva, Strovas,

Aztor

The new drug pricing policy includes price regulation of 652 packs of 348 essential

medicines.

Average price cut by ‘therapeutic segment’. (DPCO 2013)

(Table No.1.T2- Source: Business Standard dated 17th

June, 2014)

Therapeutic Category Average price reduction

1. ANTIBIOTICS 15-50%

2. ANTICANCER 10-30%

3.ANTITUBERCULOSIS 20-40%

4.CARDIOVASCULAR 20-30%

5.ANTI –HYPERTENSION 15-30%

However, there are critiques to this. The Government merely lifted the entire National List Of

Essential Medicines (NLEM),2011, comprising 348 medicines and placed it under price control.

The literal translation of the NLEM into DPCO 2013 has been done without a thought of its

implications. Price control to include all dosages and combinations, as was the case in the

previous DPCO of 1995. The combinations not included under NLEM account for 45% almost

of the total Pharma Market.

Secondly, the normative costs to determine production cost ignored standards of Quality, GMP

(Good manufacturing norms), age of plant, workers’ wages, R&D expenses etc. Consequently all

the expenses could not be recovered. This leads to non-availability of certain drugs.

Further tightening of prices

At present, medicines prices are regulated under the Drug Price Control Act (DPCO) 2013,

emerging out of the National Pharmaceutical Pricing Policy. The Government is planning to

bring legislation that would take into consideration pricing models across the US, EU (European

Union) China, and OECD (Organization for Economic Cooperation and Development) countries.

The proposal also would provide NPPA to penalize companies flouting the law or overcharging

the consumers. Currently only 30% of the total Rs.83,000 crs. Indian pharmaceutical market is

under regulation.

Since the announcement of NLEM and the Ceiling Prices, the growths have become a challenge

in the industry. Almost, 17.5% of the market is under the DPCO, which has started to indicate

growth of 0.7% on MAT basis and Non-NLEM is showing the growth of 12.5%. The overall

growth of Pharma industry is 10.25% on MAT basis.

Effect of New ‘DPCO’ prices on Indian Pharma Market’s Growth.

(Table No. 1.T3- Source: AIOCD, Market Intelligence Report 2014)

MOVING ANNUAL TOTAL (MAT- December 2014)

MAT DEC

2014

VALUE in Rs.

Crs.

GROWTH % UNIT in 000’s GROWTH %

IPM 83,009 10.2 189,42,470 1.5

NLEM 14,546 00.7 39,20,142 2.3

NON NLEM 68,463 12.5 150,22,328 1.3

IPM= Indian Pharma Market. NLEM= National List of essential medicines.

1.12 Bulk Drug Policy

The Government is keen to revive API (Active Pharmaceutical Ingredient) or popularly called

Bulk Drug by formulating a separate policy, which will promote the industry globally, just like

formulations.

DoP is holding discussions with many stakeholders to prepare a white paper. The proposed

policy will address various concerned areas of Infrastructure, Incentives, Anti-dumping duties,

Environmental clearances, Special Zones etc. Earlier India was known for low-cost and Quality

API. This place was taken over by CHINA, in last few years. Today China is competing with

India in prices. China’s prices are less than India to the extent of 15-20%. The concerned areas

are:

• Currently API accounts for around 10% of India’s Rs.83,000 crs. Pharma market.

• API sales of most domestic drug manufacturers have dropped significantly over the past

10 years.

• Most of the API’s are imported from China, which are cheaper than India to the extent of

15-20%.

• Low margins than formulations have shifted many manufacturers focus .

• Environmental obstacles and lack of Infrastructure are hurdles.

• Assistance required in adequate power, water supply, logistics and capacity building.

• Currently many manufacturers are largely limited to captive usage.

1.13 Quality & Pharma Industry.

US FDA (United States Food and Drugs Administration) barred many facilities of Indian Pharma

Industry from supplying medicines to the World’s largest pharmaceutical market. The companies

facilities barred are Ranbaxy, Ipca Laboratories, Wockhardt, RPG life sciences, Strides Arcolab,

Fresenius Kabi AG, Sunpharma, etc.

India accounts for nearly 60% of Generic Drugs and OTC products & 10% of finished dosages

(medicines) used in US market. India is the largest exporter of medicines to US. Almost, 200

manufacturing facilities in India are US-FDA approved, which include MNCs.

Indian Pharma Industry cannot ignore the huge Export Market, earning foreign currency only

due to major factor of QUALITY ! It is expected from the industry to rise up to the

expectations and even beyond to re-earn reputation, respect, reliability in the world market. The

disturbing trend is very much evident in numbers as indicated in the given table.

Number of Indian Factories barred by US FDA.

(Table No.1.T4- Source: Business Standard, Sept.2013)

Sr. No. YEAR No. of companies

barred

% of barred facilities

to approved facilities.

1 2011 7 3.5%

2 2012 2 1.0%

3 2013 19 9.5%

Quality has different dimensions. However for Pharma company, important and related

dimensions could be :

(1) Performance: Primary Product Characteristics.

(2) Conformance: Meeting specifications or industry standards.

(3) Reliability : Consistency in performance

Lapses in Indian Pharma Industry Observed by US-FDA :

• suspected contamination.

• Embedded hair.

• Oil spots on tablets

• Lack of hot and cold water

• Inadequate written instructions to employees for proper Quality checks.

• Torn files found in a waste heap & urinals that emptied into an open drain in a bathroom

six meters from the entrance to a sterile manufacturing area.

• Unlabeled test tubes

• Unlabeled vials in the glass –ware washing area.

• Unlabeled batches of drugs.

While time and cost are very crucial to the generic drug business, industry sources suggest that

companies often tend to bypass or take a casual approach towards various processes and

procedures leading to systematic lapses. Companies are in a rush to apply for first to files. They

need to be cost competitive so as to gain a larger share in the market. In this process entire

compliance is compromised and the total quality aspects result in failure. Here the Indian

companies required to change their attitude and approach.

Quality Assurance and GMP

It would be worthwhile if we keep our ideas clear on Quality Assurance and GMP while

discussing about Pharmaceutical Industry.

Quality Assurance: This is sum total of organized arrangements made with an object that

products will be of quality that is intended for the use. It is involved right from an idea is

conceived, thru’ its design, development, manufacturing, storage, distribution till the time it is

consumed by the patient. At every stage of product, there is quality assurance.

Good Manufacturing Practices (GMP): This is a part of Quality Assurance ensuring that

product is manufactured with appropriate quality for the intended use. GMP is concerned with

manufacturing as well as quality control procedures. GMP is two-thronged. It protects an

interest of consumer and also, benefits manufacturer for improving efficiency and facilitating

audit part.

Quality Control: This is concerned with testing , specifications,& documentations and

ensuring relevant tests are carried out, prior to dispatching goods for sale/consumption to the

market.

1.14 Indian Pharma Domestic Market

The domestic market has reported Rs. 83,000 crs. approx. sales for the year 2014, & expected

to grow with compound growth of 14 %. The following information can throw light on growth

pattern and trends in the market.

• 10,500 players & 3000 manufacturers in IPM.

• Local players enjoy dominant position driven by formulations.

• Intensive competition.

• Price levels are low.

• Compounded annual growth is expected to be 14% mainly due to (a) enhanced medical

infrastructure (b) treatment of chronic diseases (c) greater health insurance coverage (d)

launch of new patented products (e) new market creation.

• IPM will grow to USD 55 billion by 2020.(Rs.330,000 Crores approx..) This will be

comparable to all developed markets like US, Japan, China etc.

• In terms of volume, it will be close to US, and second to only US market.

• Mix of therapies will gradually and continuously move in favor of Specialty & Super-

specialty therapies.

• Metro & Tier I markets will make significant contribution to growth driven by rapid

urbanization & greater economic development.

• Hospital segment will increase its share & influence growing market in 2020.

• There is not going to be any difference between Local & MNCs in terms of playing in the

market. The difference will be blurred.

• Human resource requirement will be more by 2020.

• Patented products, consumer healthcare, biologics, vaccines, public health & initiation

from Government appear to be emerging as trend in IPM and would cause further

growth.

• OTC products will also play major role. Rx to OTC like, CROCIN or VOLINI and non

Rx to OTC like, PAIN BALM, ENO, PUDIN HARA , SLIM-FAST etc. Some of the

Pharma companies have already focused their marketing efforts in this direction.

1.15 PHARMA EXPORTS

Imports & Exports of Pharmaceuticals from 2005-2006 to 2013-2014

(Table No.1.T5- Source IDMA Data Bank, Publication 2014)

Year Total Imports

(rupees in crores)

Total Exports

(rupees in

crores)

Export to

Import ratio

In Times

2005-2006 4515.22 21230 4.702

2006-2007 5866.37 25666 4.375

2007-2008 6734.31 29354 4.359

2008-2009 8648.90 39821 4.604

2009-2010 9959.00 42455.66 4.263

2010-2011 11113.86 48810.26 4.392

2011-2012 14384.88 63347.32 4.404

2012-2013 17981.10 79184.15 4.404

2013-2014 20714.22 90649.90 4.376

The export market can be broadly classified between regulated markets and unregulated

markets. In the former, there are regulatory barriers exporters are required to follow-- an

elaborate registration, inspection procedure to satisfy the drug control authorities about the

quality of the medicines. These type of requirements are not necessary in unregulated markets.

The stricter the regulation, the tougher are the entry barriers and accordingly higher are the price

realizations. The regulated markets comprise of countries in USA, Western Europe, Japan,

Australia, and New Zealand. The strictest regulated market is USA.

Some of the Indian Pharma Companies, who are major players in domestic market are also

exporters for both, Bulk Drugs and Formulations. They export to both the markets- regulated and

unregulated. The larger exporters are – Ranbaxy, Dr. Reddys, Cipla, Sun Pharma, Lupin and

Wockhardt.

Indian companies export formulations in their own brands (branded generics) to many

unregulated markets. Almost 50% companies export formulations in unregulated markets with

their own marketing set up- i.e. own distribution, medical representatives etc.

Another category of exporters is the specialized bulk drugs manufacturers, exporting to both

regulated as well as unregulated markets. The companies like Aurobindo Pharma, Shashun ,

Orchid Pharma, Hetero Drugs, Neuland Pharma, Divis , Ind-swift etc.

After the introduction of 1970 Indian Patent Act, the growth of the Pharmaceutical industry in

India has followed following sequence:

• Production for the domestic market.

• Exports to unregulated market.

• Exports to regulated market other than USA

• Exports to USA.

The strategic movement behind this is larger markets and higher price realizations. The top 25

Indian domestic players have been successful to undergo full transition to exports to USA.

However majority of vast exporters are stuck at first stage only.

• Pharmaceutical Export Promotion Council Of India was established in 2014. This was set

up by Ministry Of Commerce and Industries , Government Of India.)

• India is one of the fastest growing pharmaceutical market in the world and has

established itself as a global manufacturing & research hub. A large Raw Material base &

skilled workforce gives an industry a definite competitive advantage.

• In 2025, estimated exports is USD 100 billion. (Rs.6 Lacs crores)

• India exports to 200 countries.

• Pharma exports grew at compounded annual growth of 22%, between 2007-2008 and

2012-2013.

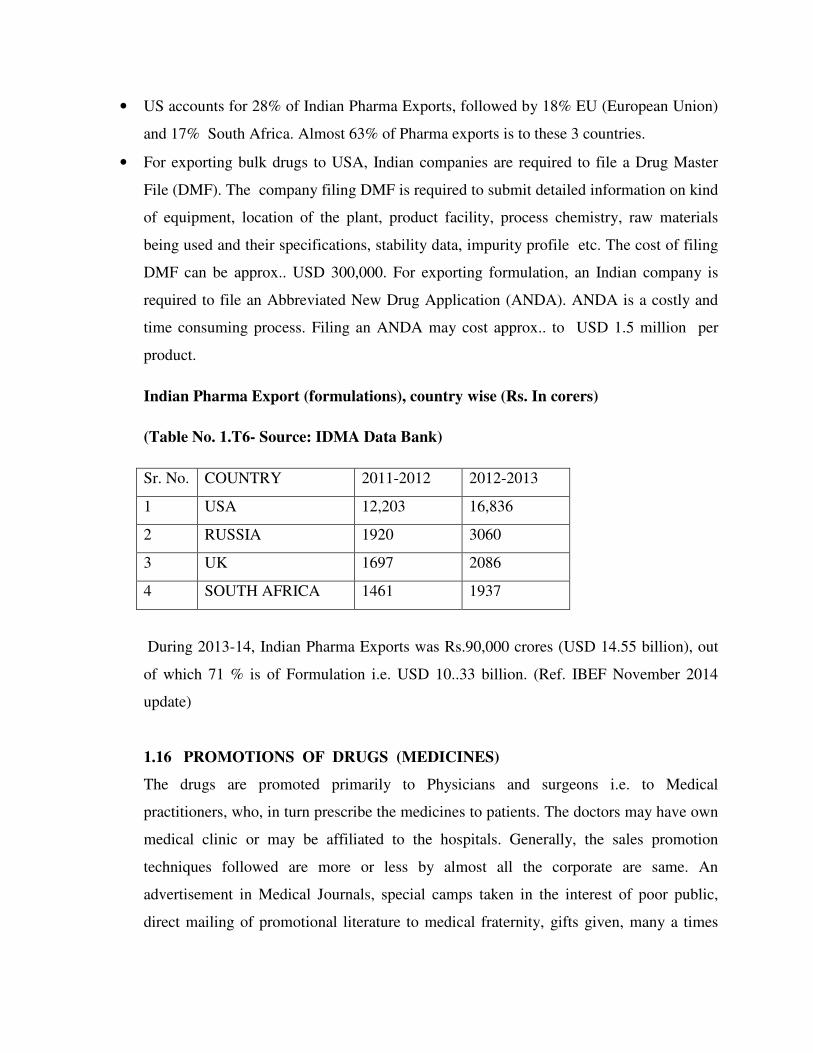

• US accounts for 28% of Indian Pharma Exports, followed by 18% EU (European Union)

and 17% South Africa. Almost 63% of Pharma exports is to these 3 countries.

• For exporting bulk drugs to USA, Indian companies are required to file a Drug Master

File (DMF). The company filing DMF is required to submit detailed information on kind

of equipment, location of the plant, product facility, process chemistry, raw materials

being used and their specifications, stability data, impurity profile etc. The cost of filing

DMF can be approx.. USD 300,000. For exporting formulation, an Indian company is

required to file an Abbreviated New Drug Application (ANDA). ANDA is a costly and

time consuming process. Filing an ANDA may cost approx.. to USD 1.5 million per

product.

Indian Pharma Export (formulations), country wise (Rs. In corers)

(Table No. 1.T6- Source: IDMA Data Bank)

Sr. No. COUNTRY 2011-2012 2012-2013

1 USA 12,203 16,836

2 RUSSIA 1920 3060

3 UK 1697 2086

4 SOUTH AFRICA 1461 1937

During 2013-14, Indian Pharma Exports was Rs.90,000 crores (USD 14.55 billion), out

of which 71 % is of Formulation i.e. USD 10..33 billion. (Ref. IBEF November 2014

update)

1.16 PROMOTIONS OF DRUGS (MEDICINES)

The drugs are promoted primarily to Physicians and surgeons i.e. to Medical

practitioners, who, in turn prescribe the medicines to patients. The doctors may have own

medical clinic or may be affiliated to the hospitals. Generally, the sales promotion

techniques followed are more or less by almost all the corporate are same. An

advertisement in Medical Journals, special camps taken in the interest of poor public,

direct mailing of promotional literature to medical fraternity, gifts given, many a times

free samples are given & finally sales/field staff or Medical Representatives are

appointed who do the detailing of products to Doctors. They bring awareness among the

medical practitioners about products, efficacy of products etc. They create habit of

prescribing products of their company.

1.17 Pharmaceutical Ancillaries

This covers wide range of products like, ampoules , vials, glass bottles, PET bottles, capsules,

collapsible tubes, corrugated boxes, syringes, hemoglobin counters, aluminum foil, printed

packaging, plastic items, pilfer proof caps (PP Caps), rubber stoppers etc.

Pharma ancillaries includes disparate producers with a varying intensity of pharmaceutical

interest. For instance the aluminum foil manufacturers’ sales revenue generated from Pharma

industry will not exceed more than 20%. That is not the case for ampoules or vials. It is largely

pharmaceutical market based, may be to an extent of 90 percent of Pharma market and rest for

others.

Ancillaries’ Characteristics-

Generally, an ancillary industry is far more power intensive than pharmaceuticals. Aluminum,

Glass industry are found to be highly energy consuming. The cost of power in these industry

could account for 25%. However certain packing materials as paper conversion products or

capsules for that matter are not power intensive. Pharmaceutical growth in general, is linear. The

ancillary industry’s growth pattern is with peaks and troughs .Over a period of time, the supply-

demand of Pharmaceutical & it’s ancillary is quite stable.

Currently, ancillary industry is matching demands as well as quality expectations of

Pharmaceutical Industry. The Pharma industry is more relying upon indigenous suppliers than

on imports. Even the exports have started picking up from ancillary industry. This speaks about

the growth and maturity stage industry reached. No doubt, exports of ancillary are not much as

compared to developed countries. However over the period, the ancillary industry will be world

class!

1.18 Packaging in Pharma Industry

In India, Pharmaceutical Packaging occupies a significant portion of the overall drugs market.

Earlier the Pharmaceutical Packaging Industry’s focus was on preserving quality of enclosed

medications. Later on , this was extended to preserving the product from counterfeiting &

tampering, assurance of product dispensing accuracy, promotion of patient compliance with

product dosage schedules. Packaging should be SIMPLE, SAFE and SUSTAINABLE. In US the

counterfeit drugs are to an extent 10%, in India it could be in the range of 20-25%. This

endangers not only public health but also damage to global Pharma industry. To counteract, the

new devised technologies like holograms, inks, dyes, tags, watermarks, and track & trace

technology- that use barcoding & RFID , Industry hopes to keep the cost of counterfeiting low.

With effect from October 2011, Government Of India has made sport barcode on the outermost

(TERTIARY PACKAGING) on exporter an obligatory.

Currently packaging trend is changing. It is more focused on Eco friendly and patient-

convenience.

Product Trends influence Pack Trends.

Packaging Materials—Changes in trend.

Packaging Process--- Changes in trend.

Few examples can be quoted---

LOZENGES are now available in “HANDY TUBE”- convenient and protection from

humidity.

MOOV--- Earlier it was available in collapsible tube, now it is also available in ‘ Aerosol Spray’

---- convenient and easy to apply.

1.19 Changing Dynamics in Indian Pharma Industry:

• Largest selling is Antibiotics (Anti-infective) brands, however, Anti-diabetic and Cardiac

are two segments showing fastest growth.

• MNCs are moving from launching only patented to generic products.

• Outsourcing is increased to a large extent. Many MNCs do not have their factories or

having limitations, but products are manufactured either on loan license basis or on the

third party manufacturing basis.

• Industry is moving from Cost cutting to Cost efficiency.

• Indian companies are becoming Global players hence the approach and attitudes are

changing .

• Moving from low value chain to high value chain.

• Moving from traditional market to newer market.

• Efforts put to make affordable and Quality healthcare to a large public.

1.20 Challenges in Indian Pharma Domestic market:

• Number of players is more.

• Competition in the market is very intense. Many brands are available for one molecule

itself. e.g. 100 brands available only for Atorvastatin and 200 brands of Cefixime.

• OTC products are made available without prescription from qualified medical

practitioners.

• DPCO is creating still unhappiness among the manufacturers.

• Large investment is expected if one has to enter Rural market, where, the returns cannot

be guaranteed and the time is long enough.

• Employees cost is going up. Attrition rate is very high. HR needs to play a vital role in

keeping educated staff and maintaining them.

1.21 Overall Future Strategies & Challenges for Pharma Industry

Most of the Indian Pharma companies came into existence post-independence. Very

exceptionally few are pretty old, may be more than 100 years like, ALEMBIC, BENGAL

CHEMICALS etc. As against this, some of the Pharma companies in US, EUROPE are 300

years old. Indian population was dependent on Imported Medicines, till 1970. The introduction

of Indian Patent Law, 1970, was a historical brick, turned the corner, in spite of pressures from

developed countries

India became a leader of manufacturing of Bulk Drugs like Streptomycin, Tetracycline,

Penicillin, Erythromycin, and all sulpha drugs, anti- malarial, antibiotics, anti-helminthic, anti-

TB, etc. In fact, by 1990, India became one of the largest producers of all these Bulk Drugs.

Even though some of the plants manufacturing are closed due to unviability, those could be

revived with the help of Government of India. There is lot of opportunities for Indian Pharma to

emerge as number one in the Global Market.

Accessibility:

India needs to focus on ensuring accessibility of medicines at affordable prices with good quality

for mass consumption. Health-Insurance, Medical Insurance required to be encouraged. The

special focus should be on rural India.

API :

Indian industry and Government should focus to produce Bulk Drugs at reasonable prices. Not

only Bulk Drugs but even Intermediates required to be produced. Currently, India depends more

on CHINA for imports of intermediates and some of basic bulk-drugs. China competes

internationally. The more reliance on China, creates significant danger for Indian Domestic

market and hazardous to India’s self-sufficiency. Land, Electricity, steam, transaction cost,

infrastructure, subsidies, and fermentation technology, in all these areas China scores over India.

Brand building of India.

Brand India Pharma- events &/or shows for various countries for target audience, exhibitions,

seminars, presentations, press conferences, road shows, advertisements, conferences for

promoting Indian Generics Industry globally required to be done.

Clinical Research Organization.

Indian clinical research market is estimated to reach $ 1 billion by 2016.More studies in varied

therapeutic area; cost competitiveness has attracted Indian Market for CRO. The approved

protocols, transparency in clinical trials, time efficiency, regulations in clinical trials areas can

bring ultimate benefits to Pharmaceutical Industry.

Chemical Industry Cluster

Chemical industry cluster could work more effectively, as it would cater all requirements of

Pharmaceutical Industry. Especially, effluent treatment plant, power supply, water requirement,

subsidies, world class laboratories are common denominator & can provide primary support

to industry.

Formulations

In Formulations, even though, India is self-sufficient, India can dominate World Market,

provided, strategic road-map is drawn by the Industry and Government of India by working

together and in tandem.

DPCO is a major hindrance & can work better as long as market based price control continue to

exist. NDDS (new drug delivery system) need an encouragement through proper fiscal measures.

New plants with high-tech and critical areas should be on fast track.

Human Resource

Every year thousands of pharmacy graduates are churning out without proper training in various

disciplines like Quality Control, Manufacturing, Analytical and Regulatory etc. In true sense,

they are not employable. There is an acute shortage of employees, who are well versed . National

Skill Development Council (NSDC) is promoting skill development and specifically for

Pharma sector. There is a need to focus on skill development and training of personnel for

Pharma.

In spite of several advantages enlisted earlier, Indian Pharma sector requires to

encounter challenges faced by certain unavoidable facts and consequently emerge out

as number one in the Global Market.

� Obsolescence- Many drugs available today were not in existence couple of decades ago.

New research has created better/newer products, due to innovativeness of the industry.

Current products would disappear in time to come and they would be replaced by newer

ones. This implies for basic research and innovation from the industry.

� Demographic change- The hike in life expectancy is enhancing the age factor. More

population is of ageing and thus, acute diseases are reducing and chronic and

degenerating diseases are creeping in.

� R&D cost- For developing new molecule, there is enormous cost incurred in R&D.

Again, the risk is high and success rate is extremely low. Not only that, the new drug

needs to be cost effective and thus, pressure on profitability. Selection of the drug and

returns on investment is a tricky issue.

� Competition with Global Giants- As compare to Indian organizations MNCs are giants

with strong base and enormous experience in the field. MNCs can invest much more than

Indian companies due to their intrinsic strength.

� New Patent Era- Developed countries are having less population as against India’s

population. Over and above that, population below poverty line is much rampant in India

than developed countries. Indian Pharma faces more challenges of newly borne diseases

like HIV/AIDS, BIRD-FLU etc. Hence, role of Pharma industry needs to be newly

defined in the context of new challenges.

� OTC (over the counter) products- The regulation of OTC products needs to be more

detailed, self-explanatory & consumer friendly.

� Direct to consumer (DTC)- Pharma companies directly sell the product to consumer like

confectionaries. In US this trend has already been well taken off. May be, due to high

literacy & awareness.

� Aggregate Cost- DPCO in India is going to be permanent hurdle. For the patient, the

cost of medicine is very low as compare to the total health care cost- diagnostic cost,

Physicians fees, hospitalization, pathology fees etc. are going to be higher than today’s

costs. In order to monitor the aggregate cost of total health care, Pharma industry requires

taking economical call on this matter.

To conclude, Indian Pharma Industry, with Government support can-

(a) Create a strong global brand as cost effective supplier of quality products in Pharmaceutical

field.

(b) Capture significant market share in global market.

(c) Achieve world class manufacturing facilities and quality

1.22 COST REDUCTION ---SUSTAINING FOR A LONG TERM:

To summarize, Indian Pharma Industry has strengths, weaknesses at the same time can avail of

opportunities and overcome the threats. One of the most important strategy to avail of

opportunities, is to focus on cost reduction. The seriousness of this should be at the top

management level and a proper target with proper accountability is required to be assigned by

the top management. “Cost reduction” could be achieved by using different tools and

techniques. Almost all the departments and processes can be involved in the cost reduction

process and ultimately it should become culture of the organization.

WHY COST REDUCTION?

• Cost Reduction is for a sustainable competitive advantage, not only for GROWTH

but also for SURVIVAL.

• Today’s killing competition is compelling corporations to review business process ,

to deliver the products & services to the customers who are more demanding &

looking for the value for money spent by them.

• Organizations which enjoyed the benefits of protection are discovering that it is no

longer possible to pass on the costs of inefficiency to customers by way of increase in

prices. Profits can be sustained & improved only when serious attention is paid

towards the ‘COST’ side of the profit equation.

• To gain competitive advantage over competitors. Competitive advantage is gained

by offering consumers greater value, either by means of lower prices or by

providing greater benefits and services that justifies higher prices.

• Cost reduction results in ‘Profit’ improvisation of an organization. The more profits

can make organization more stable. It enhances share value, improves investment

opportunities.

• Pharmaceutical organizations can think of investments in ‘Research &

Development’.

• By and large society will be benefited by reduced prices which may be possible by

savings from cost reduction programs.

• The country also stands immensely by cost reduction programs. Pharma industry

will be able to maintain the international parity in prices of exportable drugs and

medicines & consequential increase in exports. This will result in increase of foreign

exchange.

1.23 MATERIALS MANAGEMENT:

Materials management department is selected for the research paper ,since, lots of

tools/techniques can be used by this department very intensively rather than other departments of

the organization. Moreover, the researcher has spent his entire career of 40 years in the field of

Materials Management in the early years and then in the Supply chain, in the Pharmaceutical

Industry experiencing MNCs and Indian Pharma companies’ working and culture.

“Purchasing” is one of the main functions of an organization that is responsible for acquisition of

required materials, services and equipment. Whereas “Procurement” is broader--- an

“organizational” function that includes specifications development, value analysis, supplier

market research, negotiation, buying activities, contract administration, inventory control, traffic,

receiving and stores.

“Materials Management” is broader still because it extends beyond the actual purchase and is

defined as “a managerial and organizational approach used to integrate the supply management

functions in an organization. It involves the planning, acquisition, flow and distribution of

production materials from the raw material state to the finished product state. Activities include

procurement, inventory management, receiving, stores and warehousing, in-plant materials

handling, production planning and control, traffic and surplus and salvage”.

During world war I and II, the status of purchasing increased due to effectively buying the

materials and services needed to run the factories was essential for the success of the

organization . In 1970-1980,organisations started outsourcing materials and parts from countries

with lower cost structures to gain a competitive advantage. After 1980, “Purchasing” was found

to be best positioned within an organization to take over the responsibility based on its expertise

in cost reduction.

Early 1990, purchasing became more integrated into corporate strategy as organizations faced

domestic and global competition. Many organizations changed the functional name to Materials

Management, and now recently to Supply management or Supply-chain management. This is to

reflect a more process-oriented, strategic-focus.

The objective of materials management is to contribute to enhance the profitability of the

organization, by coordinated achievement of least materials cost. This is done through

optimizing capital investment, capacity & personnel, consistent with the appropriate customer

service level.

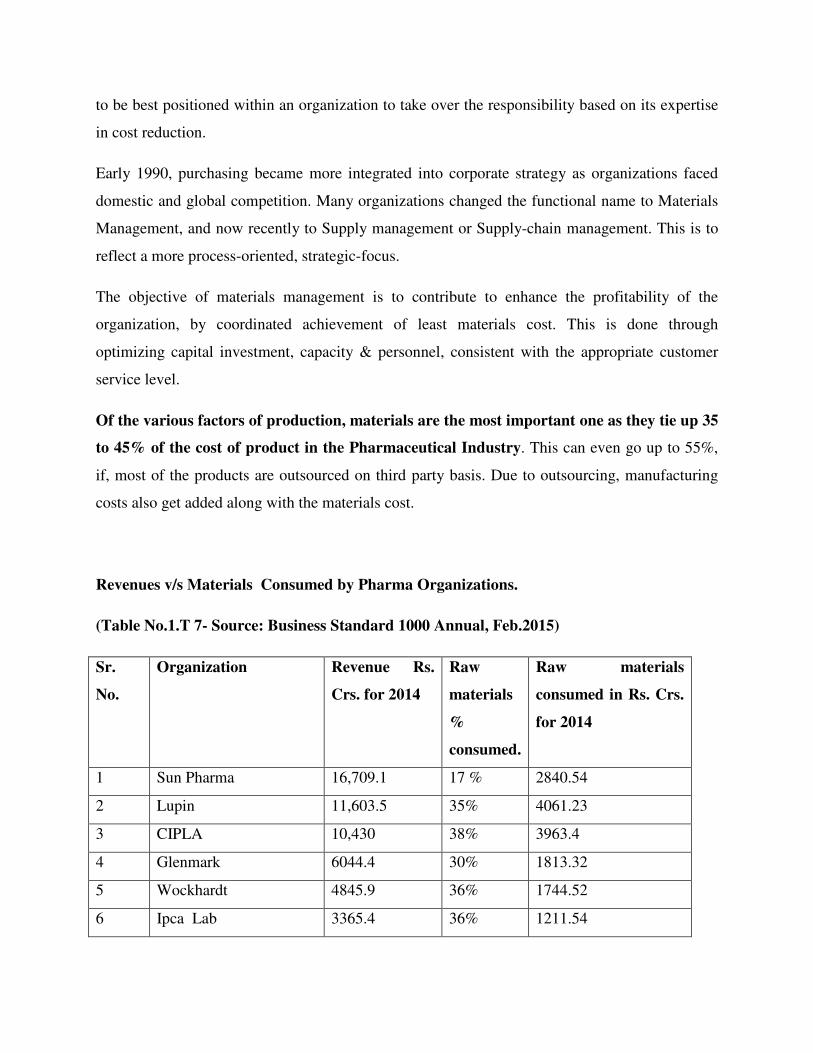

Of the various factors of production, materials are the most important one as they tie up 35

to 45% of the cost of product in the Pharmaceutical Industry. This can even go up to 55%,

if, most of the products are outsourced on third party basis. Due to outsourcing, manufacturing

costs also get added along with the materials cost.

Revenues v/s Materials Consumed by Pharma Organizations.

(Table No.1.T 7- Source: Business Standard 1000 Annual, Feb.2015)

Sr.

No.

Organization Revenue Rs.

Crs. for 2014

Raw

materials

%

consumed.

Raw materials

consumed in Rs. Crs.

for 2014

1 Sun Pharma 16,709.1 17 % 2840.54

2 Lupin 11,603.5 35% 4061.23

3 CIPLA 10,430 38% 3963.4

4 Glenmark 6044.4 30% 1813.32

5 Wockhardt 4845.9 36% 1744.52

6 Ipca Lab 3365.4 36% 1211.54

7 Glaxo Smith Kline 2819.1 43% 1212.21

8 Abbott India 1939.4 58% 1124.85

9 Alembic 1907.1 40% 762.84

10 Sanofi 1901.6 44% 836.70

11 Unichem Lab 1249.1 34% 424.69

12 Pfizer 1218.4 31% 377.70

13 Novartis 951.0 41% 389.91

14 Alkem # 2620.5 32.33% 847.21

� The above table clearly indicates that cost of materials, on an average ranges

from 35 to 45 %.

� This does not include ‘TRADED PRODUCTS’ cost.

� Cost of materials would depend upon, product-mix and the various businesses of

an organization.

� The last column of the table indicate in figures, cost of materials.

� A small saving on materials can significantly change the bottom line.

� Alkem # is unlisted company as on date (Feb. 2015)

COMPONENTS OF MATERIALS MANAGEMENT:

1. Strategic sourcing 7. Quality

2. Procurement. 8. Production.

3. Inventory control 9. Packaging

4. Vendor development/vendor audit 10. Distribution.

5. Product/service development. 11. Transport/Shipping

6. Receiving & warehousing. 12. Disposition.

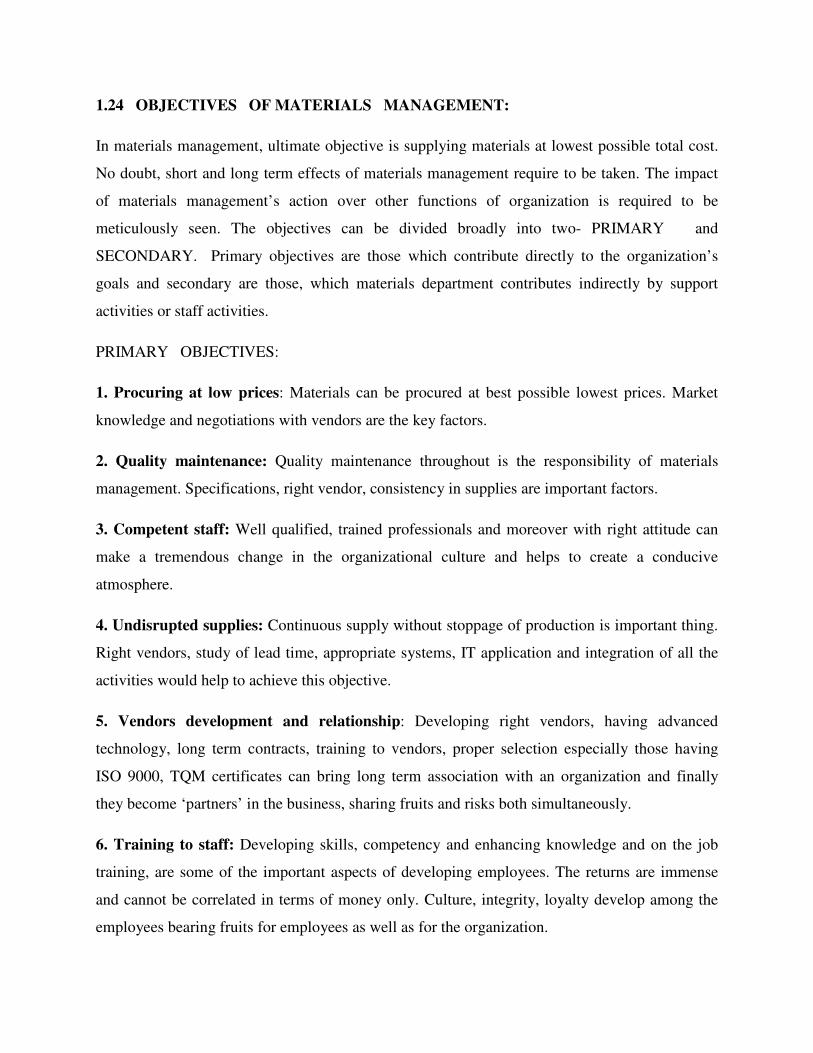

1.24 OBJECTIVES OF MATERIALS MANAGEMENT:

In materials management, ultimate objective is supplying materials at lowest possible total cost.

No doubt, short and long term effects of materials management require to be taken. The impact

of materials management’s action over other functions of organization is required to be

meticulously seen. The objectives can be divided broadly into two- PRIMARY and

SECONDARY. Primary objectives are those which contribute directly to the organization’s

goals and secondary are those, which materials department contributes indirectly by support

activities or staff activities.

PRIMARY OBJECTIVES:

1. Procuring at low prices: Materials can be procured at best possible lowest prices. Market

knowledge and negotiations with vendors are the key factors.

2. Quality maintenance: Quality maintenance throughout is the responsibility of materials

management. Specifications, right vendor, consistency in supplies are important factors.

3. Competent staff: Well qualified, trained professionals and moreover with right attitude can

make a tremendous change in the organizational culture and helps to create a conducive

atmosphere.

4. Undisrupted supplies: Continuous supply without stoppage of production is important thing.

Right vendors, study of lead time, appropriate systems, IT application and integration of all the

activities would help to achieve this objective.

5. Vendors development and relationship: Developing right vendors, having advanced

technology, long term contracts, training to vendors, proper selection especially those having

ISO 9000, TQM certificates can bring long term association with an organization and finally

they become ‘partners’ in the business, sharing fruits and risks both simultaneously.

6. Training to staff: Developing skills, competency and enhancing knowledge and on the job

training, are some of the important aspects of developing employees. The returns are immense

and cannot be correlated in terms of money only. Culture, integrity, loyalty develop among the

employees bearing fruits for employees as well as for the organization.

7. Good records maintenance: Proper maintenance of good records, automation, use of IT,

quick retrieval would help the organization.

SECONDARY OBJECTIVES:

There are many secondary objectives and do not limit their scope as primary. These can be

extended and can vary from industry to industry & organization to organization.

1. Market research for new products/ new materials/new vendors.

2. Reciprocity.

3. Make or buy &/or outsourcing.

4. Standardization.

5. Interdepartmental harmony.

6. Updating knowledge in terms of advanced technology, skills and market.

7. Exposure to Global market etc.

1.25 MATERIALS MANAGEMENT COSTS:

(a) Costs Of Materials- Total purchase price, Packing, Freight, Insurance charges, Taxes and

duties.

(b) Cost of Acquiring Materials- Expenses of the Purchasing department, including salaries and

wages of Purchasing professional, market research, rent paid, market research, negotiations,

following up, expediting, stationery, office-overheads.

(c) Inventory carrying cost- This includes investments done in inventories, rent paid for stores,

insurance charges paid, materials handling, transportation costs (within organization), overheads

of stores, losses due to pilferage, evaporation, spillage, deterioration, obsolescence, disposal etc.

In India, this cost is very high to the extent of 25-30%.

(d) General overheads- This covers the cost of testing of item, finance and accounting, record-

keeping, and general administration.

(e) Opportunity Costs- This is mainly due to losses through idle capacity, idle manpower or fixed

overheads, caused by materials not being available, loss of business, loss of good-will etc.

1.26 COST CONTROL V/S COST REDUCTION:

Many a times, cost reduction is confused with cost control. Cost control is maintaining costs

within pre-determined, prescribed or planned costs. It means cost control is conforming actual to

predetermined costs. Generally, “Budgetary and Standard costing” are most popular techniques

which are used.

Cost reduction is elimination of unnecessary costs permanently. It is an achievement of real and

permanent reduction in the unit costs of goods manufactured or service rendered, without

impairing the quality or suitability. In cost reduction, retaining Quality is of prime importance

while reducing the costs permanently. As the Japanese professional says, “We must have

constructive discontent of everything”. We need to develop a positive attitude for making a

change then is viable to achieve cost reduction.

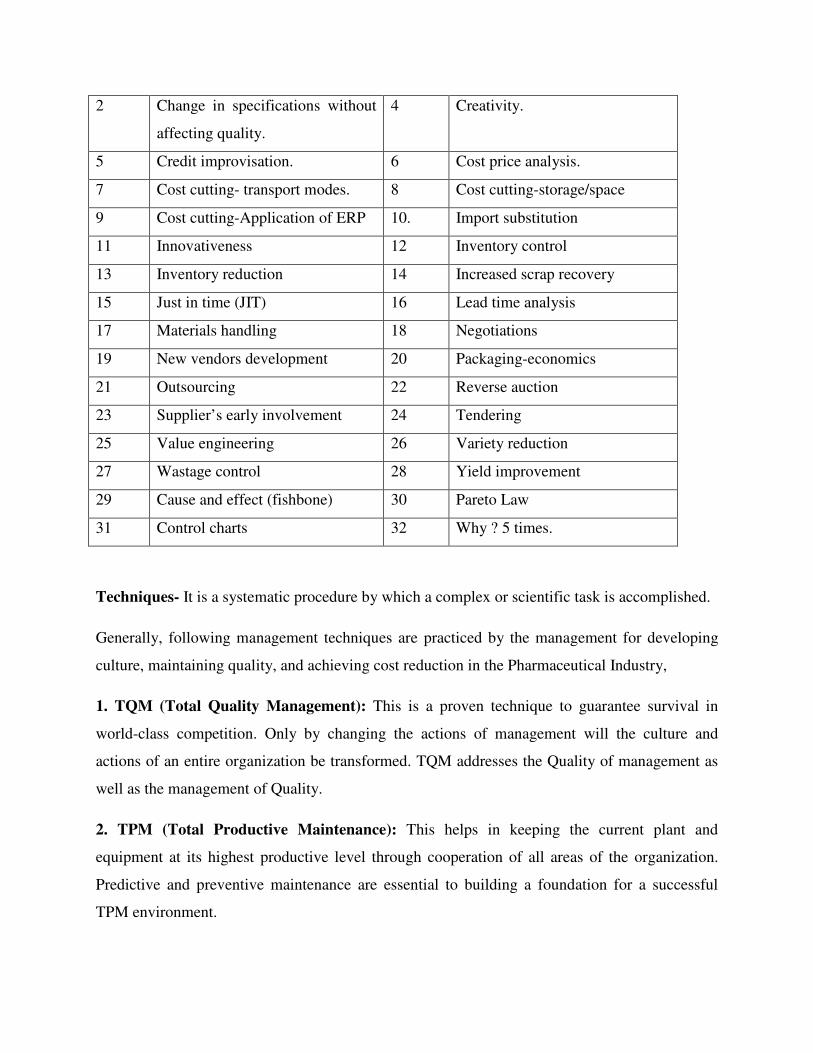

1.27 TOOLS AND TECHNIQUES USED FOR COST REDUCTION:

Tools- To carry out one’s occupation or the profession, different tools are used, such as,

Brainstorming, Cause and Effect, Check sheet, Control charts, Five Whys, Flow chart,

Histogram, Pareto chart etc.

The management tools which are generally used in Pharmaceutical Industry are as follow. These

techniques were furnished in the ‘Questionnaire’ for the respondents to response on their

organizations practicing these for cost reduction. However, the list cannot be claimed as

‘Exclusive List’ of tools being used for cost reduction.

(Table No.1.T8- Tools used for cost reduction.)

Sr. No. Tools used for cost reduction. Sr. No. Tools used for cost reduction.

1 Alternate Materials. 3 Brainstorming.

2 Change in specifications without

affecting quality.

4 Creativity.

5 Credit improvisation. 6 Cost price analysis.

7 Cost cutting- transport modes. 8 Cost cutting-storage/space

9 Cost cutting-Application of ERP 10. Import substitution

11 Innovativeness 12 Inventory control

13 Inventory reduction 14 Increased scrap recovery

15 Just in time (JIT) 16 Lead time analysis

17 Materials handling 18 Negotiations

19 New vendors development 20 Packaging-economics

21 Outsourcing 22 Reverse auction

23 Supplier’s early involvement 24 Tendering

25 Value engineering 26 Variety reduction

27 Wastage control 28 Yield improvement

29 Cause and effect (fishbone) 30 Pareto Law

31 Control charts 32 Why ? 5 times.

Techniques- It is a systematic procedure by which a complex or scientific task is accomplished.

Generally, following management techniques are practiced by the management for developing

culture, maintaining quality, and achieving cost reduction in the Pharmaceutical Industry,

1. TQM (Total Quality Management): This is a proven technique to guarantee survival in

world-class competition. Only by changing the actions of management will the culture and

actions of an entire organization be transformed. TQM addresses the Quality of management as

well as the management of Quality.

2. TPM (Total Productive Maintenance): This helps in keeping the current plant and

equipment at its highest productive level through cooperation of all areas of the organization.

Predictive and preventive maintenance are essential to building a foundation for a successful

TPM environment.

3. Six Sigma: It is simply a TQM process that uses process capability analysis as away of

measuring progress. Sigma, σ, is the Greek symbol for the statistical measurement of dispersion

called standard deviation. It is the best measurement of process variability, because the smaller

the deviation values, the less variability in the process.

4. P-D-S-A. (Plan-Do-Study-Act):The cycle was first developed by Shewhart and then

modified by Deming. This is an effective improvement technique.

5. KAIZEN: It is a Japanese word for the philosophy that defines management’s role in

continuously encouraging and implementing small improvements involving everyone. It is a

process of continuous improvement in small increments that make the process more efficient,

effective, under control and adaptable. Improvements are generally accomplished at little or no

expense, without sophisticated techniques or expensive equipment.

6. BENCHMARKING: It is a systematic study by which organizations can measure themselves

against the best industry practices. It promotes superior performance by providing details of

superior performance to the ‘learning organization’. How ‘best in class’ differs from the one’s

organization can be learnt and accordingly change can takes place to close the gap.

.

1.28 Cost Reduction in Materials Management in Pharmaceutical

Industry: Business transactions are characterized by two factors:

(a) Reward or Revenue

(b) Sacrifice or cost

Revenue minus cost is profit. It is obvious therefore, that, the sacrifice (the cost we incur) must

be minimal, in order to sustain our profitability at the optimum level.

In Pharma industry, especially a developing country like India, many “Life Saving Drugs” are

under DPCO (Drugs Price Control Order). In short, the maximum retail price is fixed by the

Central Government.

It is therefore obvious that firm needs to control costs to remain competitive. Even in Export

market there is a cut-throat competition. Not only that, the profit generated needs to be re-

invested in R&D in order to invent new products &/or innovate processes or products.

However, one has limitations to control all the costs which are incurred. Only cost of materials

should not be focused but also, cost on materials, which are incurred after we have paid price

for it. These are mostly hidden costs & unfortunately in accounting, these do not go under the

heading of materials but are booked under various heads of account like wages, salaries, rentals,

communication expenses, overheads, production costs etc.

Manager’s focus should be on costs & should aim at not only controlling them to pre-determined

levels but eliminating them altogether. It is possible, only by eliminating wastes & unnecessary

expenditure.

CONTROL: These are predetermined levels and manager performs to maintain these levels.

There is a plan & results are manipulated to be in line with planned standards or norms or levels.

REDUCTION: The unnecessary costs are attacked and eliminated altogether, instead of trying to

merely control them.

Cost Reduction is a real & permanent reduction in the unit cost of goods manufactured or service

rendered without impairing their suitability for the intended use. The retention of QUALITY of

product or service is of PRIME IMPORTANCE.

Cost control starts by fixing standards, whereas in cost reduction these standards are constantly

challenged for improvement. There is no phase of business which is exempted from cost

reduction. All inputs are subject to continuous scrutiny to see where & how they can be reduced

in cost. In cost reduction the potential savings are buried in the standards and can be dug out only

by continuous & planned research.

As the Japanese say, “We must have a constructive discontent of everything”. One needs to

develop a positive attitude for change & it is only then the cost reduction can result.

Many techniques such as value analysis , brainstorming, Pareto’s law etc. can be used .

However, manager with high integrity, openness to new ideas play a major role.

In Pharma industry, the material costs incurred is between 40 to 55%, depending upon products-

mix, size of company, formulations sales revenue and other factors.

Hence, the focus would be on “Materials Management” for cost reduction in Pharma

industry.

I am tempted to quote “Rudyaird Kipling’s famous poem-

“ I keep six honest serving men

They taught me all I knew

Their names are What and Why and

When and How and Where and Who”

1.29 SCOPE OF PROJECT:

In order to study the tools and techniques being used, different management approaches, cost

reduction planned and actual achieved, review systems, awards system, motivation to employees,

employees view towards management, etc. a research region was selected as Mumbai, since, it

was comparatively easy to collect data as most of the top Pharmaceutical Organizations’ are

having theirs’ Materials/Commercial departments located in MUMBAI city. The survey was

done primarily through Questionnaire and then thru’ personal interactions formally and

sometimes informally in person or on cell-phone. Many things were revealed during informal

discussions, which threw more light on the study-topic.

Of course there is a limitation to the study. At the outset, the study was limited to top companies

in Pharma field, generally these being big companies and well known in Domestic as well as

Global market and located in one city of India i.e. MUMBAI region. Almost all these

organizations, are well organized as far as ‘Materials Management’ function is concerned. The

small or medium type of organizations is not in the scope.