Embed Size (px)

Citation preview

LEGISLATIVE TRAIN 10.20164C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENEDINDUSTRIAL BASE / FINANCIAL SERVICES / UP TO €82BN

INSURANCE GUARANTEESCHEMES

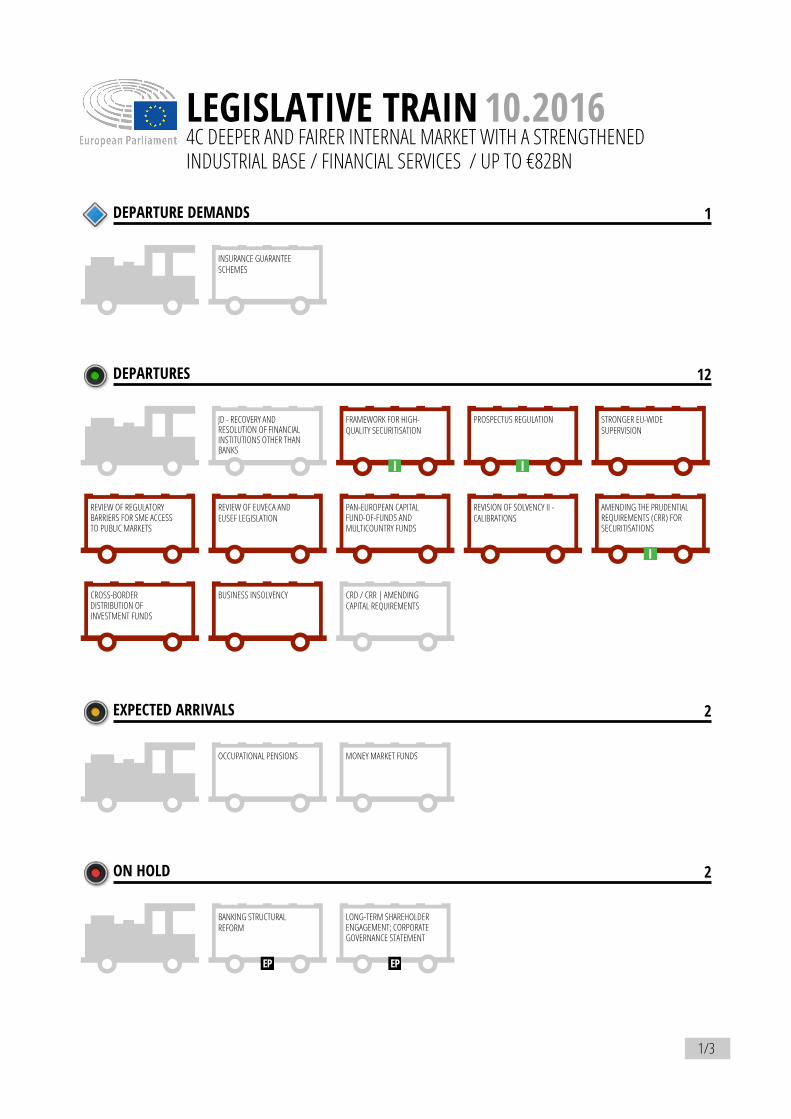

DEPARTURE DEMANDS 1

JD - RECOVERY ANDRESOLUTION OF FINANCIALINSTITUTIONS OTHER THANBANKS

FRAMEWORK FOR HIGH-QUALITY SECURITISATION

PROSPECTUS REGULATION STRONGER EU-WIDESUPERVISION

REVIEW OF REGULATORYBARRIERS FOR SME ACCESSTO PUBLIC MARKETS

REVIEW OF EUVECA ANDEUSEF LEGISLATION

PAN-EUROPEAN CAPITALFUND-OF-FUNDS ANDMULTICOUNTRY FUNDS

REVISION OF SOLVENCY II -CALIBRATIONS

AMENDING THE PRUDENTIALREQUIREMENTS (CRR) FORSECURITISATIONS

CROSS-BORDERDISTRIBUTION OFINVESTMENT FUNDS

BUSINESS INSOLVENCY CRD / CRR | AMENDINGCAPITAL REQUIREMENTS

DEPARTURES 12

OCCUPATIONAL PENSIONS MONEY MARKET FUNDS

EXPECTED ARRIVALS 2

BANKING STRUCTURALREFORM

LONG-TERM SHAREHOLDERENGAGEMENT; CORPORATEGOVERNANCE STATEMENT

ON HOLD 2

1/3

INTERCHANGE FEES FORCARD-BASED TRANSACTIONS -PAYMENTS LEGISLATIVEPACKAGE

SINGLE RULEBOOK FORBANKS

PAYMENT SERVICES IN THEINTERNAL MARKET

REPORTING AND FINANCINGOF SECURITIES TRANSACTIONS

INDICES AND BENCHMARKSIN FINANCIAL INSTRUMENTSAND FINANCIAL CONTRACTS

MARKETS IN FINANCIALINSTRUMENTS(MIFID2/MIFIR)

EUROPEAN LONG-TERMINVESTMENT FUNDS

INFORMATIONACCOMPANYING TRANSFERSOF FUNDS

ARRIVED 8

INVESTOR COMPENSATIONSCHEMES

DERAILED 1

LEGEND

ACTION PLAN FOR CAPITAL MARKETS UNION DEPARTED

EUROPARL

EUROPEAN COURT OF JUSTICE

COUNCIL

COMMISSION

JOINT DECLARATION ON THE EU'S

LEGISLATIVE PRIORITIES FOR 2018-19

MULTIANNUAL FINANCIAL FRAMEWORK

2021-2027

GLOSSARY

DEPARTURE DEMANDS

European Parliament legislative initiative reports in the fields covered by the Ten-Point Juncker Agenda

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 2/3

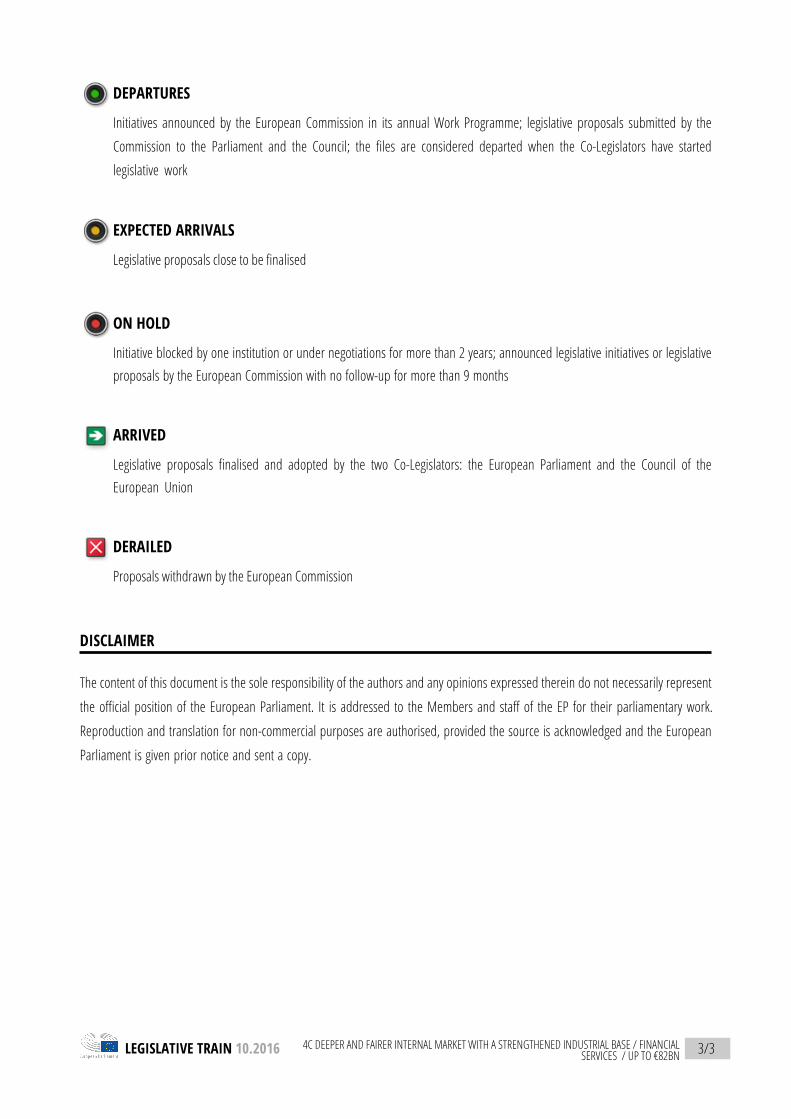

DEPARTURES

Initiatives announced by the European Commission in its annual Work Programme; legislative proposals submitted by the

Commission to the Parliament and the Council; the files are considered departed when the Co-Legislators have started

legislative work

EXPECTED ARRIVALS

Legislative proposals close to be finalised

ON HOLD

Initiative blocked by one institution or under negotiations for more than 2 years; announced legislative initiatives or legislativeproposals by the European Commission with no follow-up for more than 9 months

ARRIVED

Legislative proposals finalised and adopted by the two Co-Legislators: the European Parliament and the Council of theEuropean Union

DERAILED

Proposals withdrawn by the European Commission

DISCLAIMER

The content of this document is the sole responsibility of the authors and any opinions expressed therein do not necessarily represent

the official position of the European Parliament. It is addressed to the Members and staff of the EP for their parliamentary work.

Reproduction and translation for non-commercial purposes are authorised, provided the source is acknowledged and the European

Parliament is given prior notice and sent a copy.

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 3/3

LEGISLATIVE TRAIN 10.20164C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENEDINDUSTRIAL BASE / FINANCIAL SERVICES / UP TO €82BN

CONTENT

The untapped potential of the EU Single market is estimated at a possible increase of the EU GDP by 4.4% per year which is equivalent

of €615 billion per year. It is still incomplete due to the fragmentation and barriers, implementation of existing legislation lagging

behind or the ineffectiveness of policy instruments in some sectors.

As for transport, despite its key role in the EU economy as a common EU policy and important source of jobs, it remains incomplete

and vulnerable to external shocks. The potential gains coming from solving remaining problems and addressing existing barriers are

estimated by the EP at €8 billion per year. To achieve this main toolbox is the Single European Transport Area with technical, social and

legal aspects addressed.

The reform of the cross-border mobility of company seats could also contribute to completing the freedom of services. The EP

estimates that the potential benefits would amount to €440 million per year if 11% of firms were to move within the Single Market.

The potential benefits from a fully integrated and actively regulated EU-wide financial services sector could, on the basis of research

conducted by the European Parliament, be of the order of €82 billion per year. Completing and implementing financial regulatory

framework would bring up to €63 billion a year of gain and the implementation of measures on derivatives trade would add to this

figure €19 billion. Further phasing in of the EP resolution 2012/029(COD) on Financial markets: improving securities settlement in the EU;

central securities depositories (CSDs) adopted in July 2014 is already to bring in part of the above evaluation.

Source for the financial potential evaluation: The economic potential of the ten-point Juncker Plan for growth without debt,

European Parliament, DG EPRS study (PE543.844), Brussels 2014 and Mapping the Cost of Non-Europe 2014-19, European

Parliament, DG EPRS study (PE536.364), Brussels 2015.

References:

• European Parliament, Financial markets: improving securities settlement in the EU; central securities depositories (CSDs), Legislative

Observatory, COD/2012/029

1/1

LEGISLATIVE TRAIN 10.20164C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENEDINDUSTRIAL BASE / FINANCIAL SERVICES / UP TO €82BN

INSURANCE GUARANTEE SCHEMES [ DEPARTURE DEMANDS ]

CONTENT

Insurance Guarantee Schemes (IGS) provide last-resort protection to consumers when insurance companies are unable to fulfil their

contractual commitments. They protect against the risk that claims will not be met if an insurer becomes insolvent.

Only a few EU countries have insurance guarantee schemes in place, although there are specific EU directives for the banking and

securities sectors, such as Directive 2014/49/EU for deposit-guarantee schemes and EU directive 97/9/EC for investor-compensation

schemes.

To address the regulatory loopholes and inconsistencies, the Commission has carried out a thorough review (in 2009) of the adequacy

of existing insurance guarantee schemes in order to make appropriate legislative proposals, and produced a White Paper on this

issue.

In its resolution 2013/2658(RSP) adopted on 13 June 2013 (7th EP legislature) on Financial services: lack of progress in CCouncil and

Commission's delay in the adoption of certain proposals the European Parliament called on the Commission to come forward with

proposals for a cross-border standardisation directive establishing a coherent and consistent cross-border framework for IGS across

Member States, as some of them experienced extreme difficulties when facing serious stress.

The EP also asked to put forward the proposal for a directive on Insurance Guarantee Schemes to complement the existing Deposit

Guarantee Schemes, Investor Compensation Schemes and Solvency II, applying to the banking sector. So far no legislative proposal

was made as far as the Insurance Guarantee Schemes demand is concerned.

References:

• Legislative act, Directive 2014/49/EU of the European Parliament and of the Council of 16 April 2014 on deposit guarantee schemes

• Legislative act, Directive 97/9/EC of the European Parliament and of the Council of 3 March 1997 on investor-compensation schemes

• EP Legislative Observatory, Procedure file on a Resolution on financial services: lack of progress in Council and Commission's delay in the

adoption of certain proposals, 2013/2658(RSP)

1/46

For further information: Andrej Stuchlik, [email protected]

HYPERLINK REFERENCES

• http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=celex:32014L0049

• http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:31997L0009

• http://www.oeil.ep.parl.union.eu/oeil/popups/ficheprocedure.do?reference=2013/2658(RSP)&l=en

• mailto:[email protected]

JD - RECOVERY AND RESOLUTION OF FINANCIAL INSTITUTIONS OTHER THAN BANKS/ CENTRAL COUNTERPARTIES / BEFORE 2016 [ DEPARTURES ]

CONTENT

Expected potential gains after full phasing in of a large number of different initiatives: €63 billion

Financial institutions other than banks - which include clearing and settlement, asset management, insurance and trading of various

financial instruments - offer a range of essential services which constitute vital components for the orderly functioning of the financial

system. The financial crisis has shown that the sources and channels of contagion of systemic risk can vary.

As a result, the Commission promised in a 2010 Communication to investigate ‘what crisis management and resolution arrangements,

if any, are necessary and appropriate for (...) financial institutions’ other than banks. Following that Communication, the European

Commission launched in 2012 a consultation on the possible framework for the recovery and resolution of nonbank financial

institutions.

The European Parliament picked up and, in a 2013 owwn initiative report, called on the Commission to prioritise the recovery and

resolution of CCPs (central counterparties) and of those CSDs (central securities depositories) which are exposed to credit risk, and to

consider whether it is appropriate to develop similar legislation for other financial institutions - in the areas of insurance undertakings,

asset management and payment systems.

In this context, the Commission is expected to publish in the 3rd quarter of 2016 a proposal for a Regulation on the recovery and

resolution of central counterparties.

References:

• European Commission, Consultation on a possible recovery and resolution framework for financial institutions other than banks,

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 2/46

consultation website

• European Commission, Communication on An EU Framework for Crisis Management in the Financial Sector, COM(2010)0579

• European Parliament, Resolution of 10 December 2013 on recovery and resolution framework for non-bank institutions,

2013/2047(INI)

• EP Legislative Observatory, Procedure file on Recovery and resolution framework for non-bank institutions, 2013/2047(INI)

For further information: Angelos Delivorias, [email protected]

HYPERLINK REFERENCES

• http://ec.europa.eu/finance/consultations/2012/nonbanks/docs/consultation-document_en.pdf

• http://ec.europa.eu/internal_market/bank/docs/crisis-management/framework/com2010_579_en.pdf

• http://www.europarl.europa.eu/sides/getDoc.do?type=TA&language=EN&reference=P7-TA-2013-0533

• http://www.europarl.europa.eu/oeil/popups/ficheprocedure.do?reference=2013/2047(INI)&l=en

• mailto:[email protected]

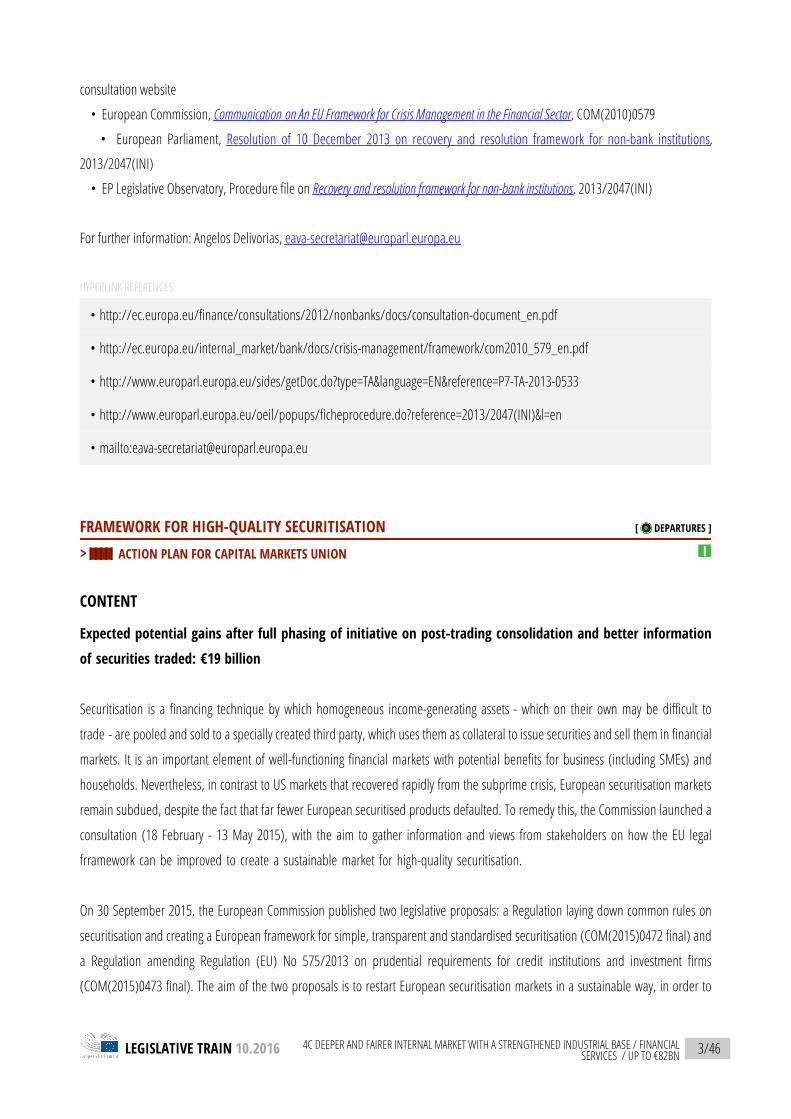

FRAMEWORK FOR HIGH-QUALITY SECURITISATION [ DEPARTURES ]

> ACTION PLAN FOR CAPITAL MARKETS UNION

CONTENT

Expected potential gains after full phasing of initiative on post-trading consolidation and better information

of securities traded: €19 billion

Securitisation is a financing technique by which homogeneous income-generating assets - which on their own may be difficult to

trade - are pooled and sold to a specially created third party, which uses them as collateral to issue securities and sell them in financial

markets. It is an important element of well-functioning financial markets with potential benefits for business (including SMEs) and

households. Nevertheless, in contrast to US markets that recovered rapidly from the subprime crisis, European securitisation markets

remain subdued, despite the fact that far fewer European securitised products defaulted. To remedy this, the Commission launched a

consultation (18 February - 13 May 2015), with the aim to gather information and views from stakeholders on how the EU legal

frramework can be improved to create a sustainable market for high-quality securitisation.

On 30 September 2015, the European Commission published two legislative proposals: a Regulation laying down common rules on

securitisation and creating a European framework for simple, transparent and standardised securitisation (COM(2015)0472 final) and

a Regulation amending Regulation (EU) No 575/2013 on prudential requirements for credit institutions and investment firms

(COM(2015)0473 final). The aim of the two proposals is to restart European securitisation markets in a sustainable way, in order to

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 3/46

the financing of the EU economy, while ensuring financial stability and investor protection, and to revise accordingly the regulatory

framework on capital charges for exposures to securitisations.

On 30 November 2015, the Council has published its compromise proposals for the Commission proposals (framework for STS and

prudential requirements).

On 6 June 2016, the European Parliament has published its draft reports on the Commission proposals (framework for STS and

prudential requirements). It plans to vote on them in plenary on 13 December 2016.

The rapporteur proposes to insert, among other things:

• the obligation for investors to be institutional investors, and for originators and original lenders to be regulated entities;

• the prohibition for SSPEs to be established in some 3rd countries with particular characteristics (e.g. off-shore financial centres);

• a 20% risk retention requirement;

• the extension of article 5 transparency requirements to investors;

• the change of the necessary information, from a specific list to all underlying documentation, essential to understand the

transaction;

• the addition to the information to be made available of information about the credit granting process for the underlying

assets/about the investors in the securitisation, the size of their investment and the securitisation tranche;

• the obligation for originator, sponsor and SSPE of a securitisation to provide the information of the aforementioned list to ESMA;

• the establishment by ESMA of a dedicated webpage, the 'European Securitisation Data Repository', where information on

underlying loans will be stored;

• the prohibition of arbitrage synthetic transactions to qualify as STS;

• the obligation of the originator, sponsor and SSPE to publish information on the long-term sustainable nature of the securitisation

for investors;

• the obligation of the originator or the original lender to disclose and publish an explanation of how the capital relief attained

through STS securitisation helped to fund new lending; and finally,

• with regards to Asset Backed Commercial Paper (ABCP) STS securitisation, the addition of requirements relating to the sponsor of

an ABCP Programme.

Reference:

• European Commission, Public consultation on securitisation, consultation website

• European Commission, Proposal for a Regulation laying down common rules on securitisation and creating a European framework for STS

securitisation, COM(2015)0472

• European Commission, Proposal for a Regulation amending Regulation (EU) No 575/2013 on prudential requirements for credit

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 4/46

institutions and investment firms, COM(2015)0473

• Council, Presidency compromise proposals for framework for STS, 30 November 2015

• Council, Presidency compromise proposals for prudential requirements, 30 November 2015

• European Parliament, Committee on Economic and Monetary Affairs draft report on simple, transparent and standardised securitisaion,

2015/0226(COD)

• European Parliament, Committee on Economic and Monetary Affairs draft report on prudential requirements for credit institutions and

investment firms, 2015/0225(COD)

• EP Legislative Observatory, Procedure file on Prudential requirements, 2015/0225(COD)

• EP Legislative Observatory, Procedure file on Common rules and European framework for STS, 2015/0226(COD)

Further reading:

• European Parliament, EPRS, Understanding securitisation background − benefits − risks, In-depth Analysis, October 2015

For further information: Angelos Delivorias, [email protected]

RAPPORTEURPaul TANG

HYPERLINK REFERENCES

• http://ec.europa.eu/finance/consultations/2015/securitisation/index_en.htm

• http://eur-lex.europa.eu/legal-content/EN/TXT/?qid=&uri=CELEX:52015PC0472R(01)

• http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52015PC0473

• http://data.consilium.europa.eu/doc/document/ST-14537-2015-INIT/en/pdf

• http://data.consilium.europa.eu/doc/document/ST-14536-2015-INIT/en/pdf

• http://www.europarl.europa.eu/sides/getDoc.do?pubRef=-//EP//NONSGML COMPARL PE-583.961 01 DOC PDFV0//EN&language=EN

• http://www.europarl.europa.eu/sides/getDoc.do?pubRef=-//EP//NONSGML COMPARL PE-583.904 01 DOC PDFV0//EN&language=EN

• http://www.oeil.ep.parl.union.eu/oeil/popups/ficheprocedure.do?reference=2015/0225(COD)&l=en

• http://www.oeil.ep.parl.union.eu/oeil/popups/ficheprocedure.do?reference=2015/0226(COD)&l=en

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 5/46

• http://www.europarl.europa.eu/RegData/etudes/IDAN/2015/569017/EPRS_IDA(2015)569017_EN.pdf

• mailto:[email protected]

REGULATION ON THE PROSPECTUS TO BE PUBLISHED WHEN SECURITIES AREOFFERED TO THE PUBLIC OR ADMITTED TO TRADING / 2015 [ DEPARTURES ]

> ACTION PLAN FOR CAPITAL MARKETS UNION

CONTENT

Prospectuses are legally required documents presenting the information necessary to enable investors to make an informed

assessment of the assets and liabilities, financial position, profits and losses, and prospects of the issuer and of any guarantor of

investment products, as well as the rights attached to them.

Directive 2003/71/EC, as amended in 2010, together with its Implementing Regulation No 809/2004 make up the current EU

prospectus regime. While this regime functions well, it was thought that certain of its requirements could still be improved to alleviate

administrative burden for companies (especially SMEs) and to make it a better information tool for investors. That is why the

Commission launched a consultation on the Prospectus Directive (18 February - 13 May 2015) asking for stakeholders’ views on issues

such as the scope of the prospectus requirement, the appropriate level of investor protection, possible ways to reduce administrative

burdden and costs, and the possibility to tailor the regime to the needs of SMEs.

Following the consultation, the Commission proposed on 30 November 2015 a Regulation (COM(2015)0583), which focuses among

other things on creating a lighter prospectus for smaller companies, shortening the length of the document and focusing on

information that is more pertinent to investors, simplifying secondary issuance for listed firms, fast-tracking the regime for frequent

issuers and providing, through ESMA, a single access point for all EU prospectuses.

On 8 June 2016, the Council agreed its most recent compromise proposal on new rules on prospectuses. On 16 March 2016, the

European Parliament published its draft report on the Commission’s proposal.

In his draft report, the rapporteur suggests the following amendments:

• to allow issuers located in the EU to choose their home Member State for both equity and non-equity securities in order to create

a level playing field and further promote cross-border activities;

• to increase the 'fewer than 150-person' limit exemption to the requirement to publish a prospectus, to 'fewer than 500' natural or

legal persons, excluding existing shareholders and employees;

• to delete the 'EUR 100 000 total consideration' exemption;

• to increase the monetary amount calculated over 12 months in the 'total consideration of the offer' exemption from €10 million to

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 6/46

€20 million;

• to define 'mid-cap enterprises' as companies that had an average market capitalisation of between €200 million and €1 billion on

the basis of end-year quotes for the previous three calendar years;

• to provide an exemption from the summary obligation, whenever the prospectus relates to non-equity securities offered solely to

qualified investors;

• to delete the obligation for third-country issuers to designate a representative established in its home Member State.

On 3 May, the rapporteur, Philippe De Backer (ALDE), left the European Parliament to join the Belgian government and was replaced,

in this file, by MEP Petr Je�ek (ALDE).

References:

• Legislative act, European Parliament and Council Directive 2003/71/EC of 4 November 2003 on the prospectus to be published when

securities are offered to the public or admitted to trading

• Legislative act, Commission regulation (EC) No 809/2004 of 29 April 2004 implementing Directive 2003/71/EC

• Legislative act, European Parliament and Council Directive 2010/73/EU of 24 November 2010 amending Directives 2003/71/EC and

2004/109/EC

• European Commission, Consultation on the Review of the Prospectus Directive, dedicated website

• European Commission, Proposal for a Regulation on the prospectus to be published when securities are offered to the public or admitted to

trading - Prospectus Regulation, COM(2015)583

• Council, Proposal for a general approach on the Commission Prospectus proposal, 3 June 2016

• EP Legislative Observatory, Procedure file on Prospectus Regulation - Prospectus to be published when securities are offered to the public

or admitted to trading, 2015/0268(COD)

Further reading:

• European Parliament, EPRS, Prospectuses for investors, Briefing, May 2016

For further information: Angelos Delivorias, [email protected]

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 7/46

RAPPORTEURPetr JEŽEK

HYPERLINK REFERENCES

• http://eur-lex.europa.eu/legal-content/EN/TXT/?qid=&uri=CELEX:32003L0071

• http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:02004R0809-20130828

• http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32010L0073

• http://ec.europa.eu/finance/consultations/2015/prospectus-directive/index_en.htm

• http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52015PC0583

• http://data.consilium.europa.eu/doc/document/ST-9801-2016-INIT/en/pdf

• http://www.europarl.europa.eu/oeil/popups/ficheprocedure.do?reference=2015/0268(COD)&l=en

• http://www.europarl.europa.eu/RegData/etudes/BRIE/2016/582019/EPRS_BRI(2016)582019_EN.pdf

• mailto:[email protected]

STRONGER EU-WIDE SUPERVISION / BEFORE 2016 [ DEPARTURES ]

> ACTION PLAN FOR CAPITAL MARKETS UNION

CONTENT

The European Commission in its Work Programme 2015 announced its willingness to strengthen banking supervision in its EU-wide

dimension. The completion and implementation of the significant overhaul of the financial regulatory framework in response to the

financial crisis, including the implementation of the new banking supervisory and resolution rules, remains a major area of the

Commission's work. On 30 September 2015, the Commission presented its Capital Markets Union (CMU) action plan

(COM(2015)0468) and, among others, announced to promote financial stability and increase supervisory convergence. To increase

financial stability, the Commission is currently preparing an impact assessment to prepare the review of the EU macroprudential

framework, scheduled for 2017. This will include an assessment of possible risks to financial stability arising from market-based

finance, the enhanced monitoring of such risks and expanding the macro-prudential toolkit accordingly. Supervisory convvergence is

expected to be addressed in a White Paper on funding and governance of the European Supervisory Agencies (ESAs). The document

was originally expected for Q2/2016. The Commission states that first preparatory work is underway.

In its resolution 2015/2634(RSP) on building a Capital Markets Union of 9 July 2015, the European Parliament emphasises that the

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 8/46

legal and supervisory frameworks will play a fundamental role to avoid excessive risk taking and excessive activism in financial markets;

it underlines that a strong Capital Markets Union project needs to be accompanied by a strong EU-wide and national supervision,

including adequate macro-prudential instruments. The EP believes that among possible options, a stronger role could be attributed to

ESMA for improving supervisory convergence.

References:

• European Commission, Action Plan on building a Capital Markets Union, dedicated website

• European Commission, Communication on an Action Plan on Building a Capital Markets Union, COM(2015)0468

• EP Legislative Observatory, Procedure file on a Resolution on Building a Capital Markets Union, 2015/2634(RPS)

Further reading:

• European Parliament, EPRS, The Capital Markets Union package, Plenary at a glance, October 2015

For further information: Andrej Stuchlik, [email protected]

HYPERLINK REFERENCES

• http://ec.europa.eu/finance/capital-markets-union/index_en.htm#action-plan

• http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52015DC0468

• http://www.oeil.ep.parl.union.eu/oeil/popups/ficheprocedure.do?reference=2015/2634(RSP)&l=en

• http://www.europarl.europa.eu/RegData/etudes/ATAG/2015/568353/EPRS_ATA(2015)568353_EN.pdf

• mailto:[email protected]

REVIEW OF REGULATORY BARRIERS FOR SME ACCESS TO PUBLIC MARKETS / 2017 /2017 [ DEPARTURES ]

> ACTION PLAN FOR CAPITAL MARKETS UNION

CONTENT

According to the Action Plan on building a Capital Markets Union (COM(2015)0468) the Commission will review the regulatory barriers

to small firms for their admission to trading on public markets in a number of pieces of EU legislation. The Commission will make use

of the new SME Growth Markets to ensure that the revised regulatory environment for SMEs will be taken into account in other pieces

of legislation.

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 9/46

SME Growth Markets were introduced by MiFID II. They are a new sub-category of the Multilateral Trading Facility (MFT) tailored to

the specific needs of SMEs. From 2017 on they will provide the opportunity for new companies to ready themselves for a listing on a

larger exchange. Administrative burdens will be reduced. SMEs will have the opportunity to more easily access capital markets.

Still according to the Action Plan, the Commission will explore together with the International Accounting Standards Board (IASB) the

possibility of developing a voluuntary tailor-made accounting solution, which could be used for companies admitted to trading on SME

Growth Markets.

References:

• European Commission, Communication from the Commission on an Action Plan on Building a Capital Marktes Union, COM(2015)0468

• European Commission, Updated rules for markets in financial instruments: MiFID II, decicated website

• International Standards Board (IASB) homepage

Further reading:

• European Parliament, EPRS, Barriers to SME growth in Europe, Briefing, May 2016

For further information: Christian Scheinert, [email protected]

HYPERLINK REFERENCES

• http://ec.europa.eu/finance/capital-markets-union/docs/building-cmu-action-plan_en.pdf

• http://ec.europa.eu/finance/securities/isd/mifid2/index_en.htm

• http://www.ifrs.org/Pages/default.aspx

• http://www.europarl.europa.eu/RegData/etudes/BRIE/2016/583788/EPRS_BRI(2016)583788_EN.pdf

• mailto:[email protected]

REVIEW OF EUVECA AND EUSEF LEGISLATION / BEFORE 2016-7 [ DEPARTURES ]

> ACTION PLAN FOR CAPITAL MARKETS UNION

CONTENT

Venture capital relates to the taking of ownership interest in a company, which is at an early stage (‘start-up’). While venture capital

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 10/46

can be supplied in a number of ways, the majority of such investments in Europe come from independent investors, usually funds.

Social businesses are companies that have a positive social impact and aim to address social objectives, while making a profit (i.e. they

are not charities). Funds dedicated to investing in such businesses suffered from two main hurdles: they could be costly and difficult to

set up and gather investments, and they were not always easy to identify or distinguish from other funds.

As a result, in 2013, two Regulations were published (Regulation (EU) No 345/2013 on European venture capital funds and Regulation

(EU) No 346/2013 on European social entrepreneurship funds), which set two ‘brands’ and laid down uniform requirements and

conditions for managers of collective investment undertakinggs that wished to use the designation ‘EuVECA’ or ‘EuSEF’ in relation to the

marketing of such funds in the EU. The rules relate to the marketing of EuVECA/EuSEF to investors across the EU, the portfolio

composition of these funds, the eligible investment instruments and techniques to be used by them, as well as organisation, conduct

and transparency rules for managers that market these funds across the EU.

While the review of the Regulations was only planned for 2017, the Commission decided to bring it forward, to increase their take-up

(only a small number EuVECa and EuSEF have so far been launched), while guaranteeing an adequate level of investor protection. As a

result, it launched a consultation on the review of the regulations on 30 September 2015. The consultation closed on 6 January 2016.

On 14 July 2016, the Commission published a proposal for a Regulation amending Regulations (EU) No 345/2013 and (EU) No

346/2013. The proposed amendments aim to allow managers authorised under the Alternative Investment Fund Managers Directive

(2011/61/EU) to use the ‘EuVECA’ and ‘EuSEF’ designations respectively in relation to the marketing of those funds in the Union; to

increase the size of SMEs accepted as qualifying undertakings; and to reduce the costs those funds incur, by ensuring that competent

authorities cannot impose fees and other charges on them and by ensuring that they cannot interpret ‘sufficient own funds’ in different

ways.

References:

• Legislative act, European Parliament and Council Regulation (EU) No 345/2013 of 17 April 2013 on European venture capital funds

• Legislative act, European Parliament and Council Regulation (EU) No 346/2013 of 17 April 2013 on European social entrepreneurship funds

• European Commission, Proposal for a Regulation amending Regulation (EU) No 345/2013 on European venture capital funds and

Regulation (EU) No 346/2013 on European social entrepreneurship funds, COM(2016)0461

• EP Legislative Observatory, Procedural file on European venture capital funds and European social entrepreneurship funds,

2016/0221(COD)

For further information: Angelos Delivorias, [email protected]

HYPERLINK REFERENCES

• http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32013R0345

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 11/46

• http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32013R0346

• http://www.europarl.europa.eu/RegData/docs_autres_institutions/commission_europeenne/com/2016/0461/COM_COM(2016)0461_EN.pdf

• http://www.europarl.europa.eu/oeil/popups/ficheprocedure.do?reference=2016/0221(COD)&l=en

• mailto:[email protected]

PAN-EUROPEAN CAPITAL FUND-OF-FUNDS AND MULTICOUNTRY FUNDS / 2016 [ DEPARTURES ]

> ACTION PLAN FOR CAPITAL MARKETS UNION

CONTENT

EU venture capital funds are half the size (average ≈ €60 million) of the ones operating in the US. This limits their ability to make larger

investments, so that they can follow companies, as they scale-up. Furthermore, an important part of the financing of the sector is done

by the public sector, instead of institutional investors (€5 billion market in the EU compared to €26 billion in the US). Finally, European

VC funds still face many trans-national barriers.

This is why the Commission intends to accompany the review of the EuVECA Regulation with a call to create a Pan-European venture

capital fund-of-funds. This fund-of-funds, with a size of at least €500 million, will combine public finance with greater volumes of

private capital, to bring additional scale and stimulus for the support of the most promising new enterprises. Specifically, the fund will

invest in a combination of early-stage, later stage and expansion stage venture capital funds; tthus it will be attractive to major

investors and will attract more private investment to the European venture capital market.

The Commission currently works with the European Investment Fund and intends to launch a call this summer for the creation of this

fund-of-funds. Both the European Commission and the European Investment Fund have not published any proposal so far. The role of

the European Parliament is non-existent at this stage.

References:

• European Commission, Financing ideas from Europe, speech by Commissioner Moedas, 31 March 2016

For further information: Angelos Delivorias, [email protected]

HYPERLINK REFERENCES

• https://ec.europa.eu/commission/2014-2019/moedas/announcements/financing-ideas-europe_en

• mailto:[email protected]

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 12/46

REVISION OF SOLVENCY II - CALIBRATIONS / BEFORE 2018 [ DEPARTURES ]

> ACTION PLAN FOR CAPITAL MARKETS UNION

CONTENT

Solvency II (Directive 2009/138/EC - as amended by Directive 2014/51/EU known as 'Omnibus II') is the EU level regime regulating

insurance and reinsurance. It replaces the previous regime (Solvency I) which consisted of 14 Directives.

Solvency II applied from 1 January 2016 and according to the EC, introduced for the first time ‘a harmonised sound and robust

prudential framework for insurance firms in the EU.’ It seeks to promote comparability, transparency and competitiveness whilst

providing an individual risk profile for each insurance company. Very broadly, the Solvency II rules cover requirements in three areas:

(1) quantitative rules (i.e. solvency capital requirements - the amount of capital insurers must hold so they can pay claims); (2)

governance, risk management and supervision of insurers; and (3) disclosure and transparency rules.

The EC’s Capital Markets Union (CMU) action plan published on 30 September 2015 noted that, whilst life insurrance companies are

natural long-term investors, they have been retreating from investments in long term projects and companies. Clearly the way different

types of investments are treated under Solvency II capital requirements rules influences insurance companies’ investment decisions.

Hence, alongside the plan, the EC made immediate amendments to the Solvency II delegated regulation to introduce more risk

sensitive calibrations for infrastructure and European long term investment funds (ELTIFs). These changes facilitate the funding of

infrastructure and sustainable long term investment in Europe.

The CMU plan also committed to new prudential calibrations in solvency II (through amendment to the Delegated Act) for simple,

transparent and standardised (STS) securitisation products, once the STS securitisation products framework is in place. Also, noting

consultation feedback that prudential treatment of private equity and privately placed debt in Solvency II was considered an

impediment to investing in these asset classes, the EC will consider what changes are necessary here. These could then be taken

forward in the context of the review of Solvency II.

References:

• Legislative act, European Parliament and Council Directive 2009/138/EC of 25 November 2009 on Insurance and Reinsurance (Solvency II)

• Legislative act, European Parliament and Council Directive 2014/51/EU of 16 April 2014 on Insurance and Reinsurance (Omnibus II)

• European Commission, Communication on the Capital Markets Union, COM(2015)0468

• European Commission, Solvency II and Omnibus II, dedicated website

• European Commission, European long term investment funds, dedicated website

• European Commission, Fact sheet on securitisation, dedicated website

• EP Legislative Observatory, Procedure file on Common rules on securitisation, 2015/0226(COD)

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 13/46

For further information: David Eatock, [email protected]

HYPERLINK REFERENCES

• http://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX:32009L0138&from=EN

• http://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX:32014L0051&from=EN

• http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52015DC0468&from=EN

• http://ec.europa.eu/finance/insurance/solvency/

• http://ec.europa.eu/finance/investment/index_en.htm

• http://europa.eu/rapid/press-release_MEMO-15-5733_en.htm

• http://www.europarl.europa.eu/oeil/popups/ficheprocedure.do?reference=2015/0226(COD)&l=en

• mailto:[email protected]

AMENDING THE PRUDENTIAL REQUIREMENTS (CRR) FOR SECURITISATIONS [ DEPARTURES ]

> ACTION PLAN FOR CAPITAL MARKETS UNION

CONTENT

As part of its ambition to create a Capital Markets Union, the European Commission wants to revive the securitisation market in the EU,

in order to offer new financing tools and ease credit provision, especially for small and medium-sized enterprises. Its 'securitisation

initiative', set out in a proposed regulation on 30 September 2015, would establish a new framework for 'simple, transparent, and

standardised' (STS) securitisations.

This new initiative also has implications for the overall prudential framework for credit institutions and investment firms, therefore the

Commission proposed (COM(2015)0473) to amend the Capital Requirements Regulation (CRR) (EU) No 575/2013 accordingly. The

proposed amendments would adjust risk retention profiles to reflect properly the specific features of STS securitisations. The overall

aim of amending the CRR provisions, as a consequence of the securitisation proposal, is to recalibrate the prudential requirements for

credit institutions aand investment firms either issuing or purchasing securitisations. The Commission provided an impact assessment

(SWD(2015)0185) for both proposals.

The most significant changes are: a new hierarchy of risk calculation methods and lower capital requirements for STS in order to lower

costs for credit provision and unlock additional sources for long-term finance, especially to SMEs. The Council agreed on a general

approach on 7 December 2015.

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 14/46

On 6 June 2016, the rapporteur Pablo Zalba Bidegain (EPP, Spain) presented his draft report to the Parliamentary Committee of

Economic and Monetary Affairs (ECON). In his draft report, the rapporteur addresses two main points: (i) to amend the hierarchy of

approaches and (ii) to ease access to securitisation instruments for SMEs. In his view, ‘even after rescaling for STS securitisations’,

using external ratings ‘can lead to substantially higher capital requirements than the approaches SEC-IRBA or SEC-SA. ... Therefore the

External Ratings-Based approach (SEC-ERBA) should be eliminated from the hierarchy of approaches for STS securitisation’. As to

SMEs, the rapporteur supports the use, for certain senior tranches of synthetic securitisations of SMEs loans, of the same reduced

capital charges as STS securitisations. A first debate in the Committee took place on 21 June 2016 with an expected Committee vote in

November. The vote in plenary is scheduled for January 2017.

References:

• EP Legislative Observatory, Procedural file on Prudential requirements for credit institutions and investment firms, 2015/0225(COD)

• European Commission, Proposal for a Regulation laying down common rules on securitisation and creating a European framework for

simple, transparent and standardised securitisation and amending Directives 2009/65/EC, 2009/138/EC, 2011/61/EU and Regulations (EC) No

1060/2009 and (EU) No 648/2012, COM(2015)0472

• European Commission, Proposal for a Regulation amending Regulation (EU) No 575/2013 on prudential requirements for credit institutions

and investment firms, COM(2015)0473

• Legislative act, European Parliament and Council Regulation (EU) No 575/2013 of 27 June 2016 on prudential requirements for credit

institutions and investment firms and amending Regulation (EU) No 648/2012

• European Commission, Impact Assessment accompanying the documents COM(2015)0472 and COM(2015)0473, SWD(2015)0185

• Council, General approach, ST 14701 2015 REV 1 - 2015/0225 (OLP), 7 December 2015

• European Parliament, Draft Economic and Monetary Affairs Committee report on the proposal for a regulation amending Regulation (EU)

No 575/2013 on prudential requirements for credit institutions and investment firms, 2016/0225(COD)

For further information: Andrej Stuchlik, [email protected]

RAPPORTEURPablo ZALBA BIDEGAIN

HYPERLINK REFERENCES

• http://www.europarl.europa.eu/oeil/popups/ficheprocedure.do?lang=&reference=2015/0225(COD)

• http://eur-lex.europa.eu/legal-content/EN/TXT/?qid=1452173966407&uri=CELEX:52015PC0472

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 15/46

• http://www.europarl.europa.eu/RegData/docs_autres_institutions/commission_europeenne/com/2015/0473/COM_COM(2015)0473_EN.pdf

• http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32013R0575

• http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=SWD:2015:0185:FIN:EN:PDF

• http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=consil:ST_14701_2015_REV_1

• http://www.europarl.europa.eu/sides/getDoc.do?type=COMPARL&mode=XML&language=EN&reference=PE583.904

• mailto:[email protected]

CROSS-BORDER DISTRIBUTION OF INVESTMENT FUNDS / 2017 [ DEPARTURES ]

> ACTION PLAN FOR CAPITAL MARKETS UNION

CONTENT

Cross-border investment funds have an important role to play in achieving the Capital Markets Union: if funds can do business

more easily cross-border, they can grow and become more efficient, allocate capital efficiently across the EU, and compete within

national markets to deliver better value and greater innovation for consumers.

The EU has been promoting the cross-border distribution of funds for at least 30 years (since directive 85/611/CEE). The main

legislative tools have been the UCITS Directives and the Alternative Investment Fund Managers Directive. On 2 June 2016, in the context

of the CMU, it has launched a consultation on cross-border distribution of funds (UCITS, AIF, ELTIF, EuVECA and EuSEF) across the EU

to get stakeholders’ opinions on where and how the cross-border distribution of funds could be improved. The consultation

specifically focuses on the following possible impediments: marketing restrictions, distribution costs and regulatoory fees,

administrative arrangements, distribution networks, notification processes and taxation. The consultation will close on 9 October 2016.

References:

• European Commission, Consultation on cross-border distribution of funds across the EU, consultation website

For further information: Angelos Delivorias, [email protected]

HYPERLINK REFERENCES

• http://ec.europa.eu/finance/consultations/2016/cross-borders-investment-funds/docs/consultation-document_en.pdf

• mailto:[email protected]

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 16/46

BUSINESS INSOLVENCY / 2016 [ DEPARTURES ]

> ACTION PLAN FOR CAPITAL MARKETS UNION

CONTENT

In 2014 the Commission published a Recommendation COM(2014)1500 on a new approach to business failure and insolvency which

encourages Member States to implement early restructuring procedures and gives a "second chance" to entrepreneurs. The

Recommendation sets out common principles for national insolvency procedures for businesses as well as measures aimed at

reducing the lengths and costs of proceedings for SMEs. While it is clear that the Recommendation has provided a useful focus for

those Member States undertaking reforms in the area of insolvency, an assessment undertaken by the Commission shows that it has

only been implemented partially, including in those Member States that have launched some reforms.

In parallel, the Commission proposed, back in 2012, a reform of the Insolvency Regulation (dating from 2000) which addresses the

cross-border aspects of insolvency in the EU (but does not seek to harmonise national insolvency laws). The proposal was enacted into

law in May 2015 as a recast regulation. In line with the ‘second-chance approach’, the Regulation now covers not only bankruptcy

proceedings, but hybrid and pre-insolvency proceedings, as well as debt discharges and debt adjustments for natural persons

(consumers and sole traders). Further modifications include greater legal certainty regarding the determination of the business’s

‘centre of main interests’ in order to prevent abusive forum-shopping practices. Courts must now be proactive in checking whether

they really have jurisdiction to open insolvency proceedings for a given company, taking into account the actual perception of creditors

as to where the business is administered from. In order to promote transparency, all Member States will be obliged to establish

insolvency registers that will be interconnected via the e-Justice portal. There are also new rules on group insolvency and rules allowing

for the coordination of proceedings regarding the companies within the group.

As follow-up to the 2014 recommendation, the Commission is currently working on an “insolvency initiative” aimed at providing new

legal tools for viable businesses in distress and honest but bankrupt individuals. A legislative proposal – presumably addressing not

only cross-border issues (as per the Insolvency Regulation), but also seeking to harmonise national laws – is due to be presented by

the end of 2016. A public consultation on the insolvency initiative lasted from March until mid-June 2016.

The Commission’s insolvency initiative should be seen in the context of an earlier own-initiative resolution of the Parliament from 2011

where it pointed out that:

• disparities between national insolvency laws create competitive advantages or disadvantages and difficulties for companies with

cross-border activities and favour forum-shopping

• steps must be taken to prevent forum shopping

• even if the creation of a body of substantive insolvency law at EU level is not possible, there are certain areas of insolvency law

where harmonisation is worthwhile and achievable;

• insolvency law should be a tool for the rescue of companies at Union level

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 17/46

• insolvency proceedings should not be used abusively by a creditor

• Member States should ensure that their insolvency laws include adequate provisions allowing special arrangements at EU level

for separation of insolvent cross-border conglomerates into viable units

• the issue of insolvency needs to be considered from an employment-law perspective, as differing definitions of ‘employment’ and

‘employee’ in Member States should not undermine the rights of employees in the event of insolvency;

• lack of harmonisation with regard to the ranking of creditors reduces predictability of outcomes of judicial proceedings;

• it is necessary to increase the priority of employees' claims relative to other creditors' claims.

References:

• European Commission, Commission Recommendation of 12 March 2014 on a new approach to business failure and insolvency,

COM(2014)1500

• Legislative act, European Parliament and Council Regulation (EU) 2015/848 of 20 May 2015 on insolvency proceedings

• EP Legislative Observatory, Procedural file on Insolvency proceedings, 2012/0360(COD)

Further reading:

• European Parliament, Policy Department C, Harmonisation of Insolvency Law at EU Level, Note, 2010

• European Parliament, EP Library, Cross-border insolvency law in the EU, Briefing, February 2013

• European Parliament, EPRS, Reform of the EU Insolvency Regulation, Briefing, January 2014

• European Parliament, EPRS, Finalising reform of cross-border insolvency rules, At a glance, May 2015

• European Parliament, DG IPOL, Harmonizing insolvency laws in the Euro area: rationale, stock taking and challenges. What role for the

Euro group?, Study, July 2016

• European Commission, DG JUST, Study on a new approach to business failure and insolvency: Comparative legal analysis of the Member

States’ relevant provisions and practices, January 2016

•

For further information: Rafal Manko, [email protected]

HYPERLINK REFERENCES

• http://ec.europa.eu/justice/civil/files/c_2014_1500_en.pdf

• http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:32015R0848

• http://www.europarl.europa.eu/oeil/popups/ficheprocedure.do?lang=en&reference=2012/0360(COD)

• http://www.europarl.europa.eu/meetdocs/2009_2014/documents/empl/dv/empl_study_insolvencyproceedings_/empl_study_insolvencyproceedings_en.pdf

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 18/46

• http://www.europarl.europa.eu/RegData/bibliotheque/briefing/2013/130476/LDM_BRI(2013)130476_REV1_EN.pdf

• http://www.europarl.europa.eu/RegData/bibliotheque/briefing/2014/140736/LDM_BRI(2014)140736_REV1_EN.pdf

• http://www.europarl.europa.eu/RegData/etudes/ATAG/2015/556989/EPRS_ATA(2015)556989_EN.pdf

• http://www.europarl.europa.eu/RegData/etudes/STUD/2016/574428/IPOL_STU(2016)574428_EN.pdf

• http://ec.europa.eu/justice/civil/files/insolvency/insolvency_study_2016_final_en.pdf

• mailto:[email protected]

AMENDMENTS OF THE CAPITAL REQUIREMENTS DIRECTIVE/CAPITALREQUIREMENTS REGULATION / 2016 [ DEPARTURES ]

CONTENT

The completion and implementation of the significant overhaul of the financial regulatory framework in response to the financial crisis,

including the revision the prudential requirements for financial institutions and investment firms, remains a major area of the

Commission's work.

The Commission is currently preparing its review of capital requirements (CR) provisions, and should publish proposals before the

end of 2016. This review will explore lowering the risk weights for infrastructure projects for banks as well as the possibility for all

Member States to authorise credit unions outside the EU's capital requirements rules for banks. An impact assessment on the revision

of the capital requirement legislation is in preparation.

In addition, the Commission announced to collect evidence on the cumulative impact of the current regulatory framework. A call for

evidence on the impact on financial services was concluded in January 2016.

The European Parlliament addressed the topic of capital requirements in its annual report on the Banking Union in March 2016: The

report notes that CR 'beyond a certain threshold may in the short term create unintended consequences, limiting banks’ lending

capacity'. For financing of SMEs, the European supervisory authorities should 'conduct a comprehensive assessment of CR embedded

in current and future legislation' as well as take into account 'the balance between short-term and long-term impact of CR'. Since the

EU's prudential requirements framework (CRD-IV/CRR) already existed, the report 'encourages' the Commission to align it with the

Banking Union framework. It calls for flexibility on the Maximum Distributable Amount (MDA), to avoid being 'too rigid' and 'negatively

affect[ing] the Additional Tier 1 bond market and the level playing field'. The report pushes for regulations rather than directives.

References:

• European Parliament, Resolution of 10 March 2016 on the Banking Union – Annual Report 2015, 2015/2221(INI)

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 19/46

• EP Legislative Observatory, Procedural file on Banking Union - 2015 Annual Report, 2015/2221(INI)

• European Commission, Capital requirements regulation and directive – CRR/CRD IV, dedicated website

Further reading:

• European Commission, Call for evidence: regulatory framework for financial services, consultation website

For further information: Andrej Stuchlik, [email protected]

HYPERLINK REFERENCES

• http://www.europarl.europa.eu/sides/getDoc.do?pubRef=-//EP//TEXT TA P8-TA-2016-0093 0 DOC XML V0//EN

• http://www.europarl.europa.eu/oeil/popups/ficheprocedure.do?lang=en&reference=2015/2221(INI)

• http://ec.europa.eu/finance/bank/regcapital/legislation-in-force/index_en.htm

• http://ec.europa.eu/finance/consultations/2015/financial-regulatory-framework-review/index_en.htm

• mailto:[email protected]

OCCUPATIONAL PENSIONS [ EXPECTED ARRIVALS ]

CONTENT

Europe’s population is ageing, and we are moving from having around four people of working age (15-64) for every person aged over

65 years, to just two by 2060. This has put increased pressure on pension systems and led to reforms to make them more sustainable

for the future. As a result, pay-as-you-go public pensions are, in general, expected to become less generous in future. To support

retirement incomes, the EC’s 2012 pensions White Paper called for more opportunities for citizens to be able to save in safe and good

value funded pensions. In response to the White Paper, the EP’s 2013 resolution Adequate, safe and sustainable pensions: ‘stresses the

urgent need to promote efforts to build up [...] complementary occupational pension systems.’

In 27th March 2014, the European Commission proposed a revision (‘IORP II’) of the existing Institutions for Occupational Retirement

Provisionn (IORP) Directive of 2003, which covers certain occupational pension savings. Currently, these are overwhelmingly in the

United Kingdom (55.9% of IORP assets) and the Netherlands (30.7%). The proposed revision aims to improve the governance, risk

management, transparency and information provision of IORPs and help increase cross-border (broadly, IORPs with a sponsoring

employer in another Member State) IORP activity, strengthening the single market. The proposal did not include new capital

requirements for IORPs following a long and controversial debate.

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 20/46

The EP's ECON Committee considered the matter and voted on its report and mandate for negotiations on 25 January 2016. Trilogue

discussions began on 29th February 2016 with the Council and European Commission and concluded in late June.

The compromise text contains a number of aspects proposed by the EP, including: recognition of the need for intergenerational

balance of risks and benefits in IORPs; the need for IORPs to take account of environmental, social, governance and ethical factors

(often called ‘ESG’ for short) when IORPs make and review investment decisions and set investment policies; and changes to rules

governing IORPs operating across borders to encourage their development.

A plenary vote in the EP is provisionally scheduled for November 2016.

References:

• European Commission, White Paper on pensions, dedicated website

• European Parliament, Resolution of 21 May 2013 on an Agenda for Adequate, Safe and Sustainable Pensions, 2012/2234(INI)

• European Commission, Proposal for a Directive on the activities and supervision of institutions for occupational retirement provision

(recast), COM(2014)0167

• European Parliament, Economic and Monetary Affairs Committee report of 25 January 2016 on occupation retirement, 2014/0091(COD)

• EP Legislative Observatory, Procedure file on Activities and supervision of institutions for occupational retirement

provision, 2014/0091(COD)

• Legislative act, European Parliament and Council Directive 2003/41/EC of 3 June 2003 on the activities and supervision of institutions for

occupational retirement provision

Further reading:

• European Parliament, EPRS, Occupational pensions - Revision of the Institutions for Occupational Retirement Provisions Directive (IORP II),

Legislative briefing, September 2016

• European Insurance and Occupational Pensions Authority (EIOPA), EIOPA 2014 report on IORPs

For further information: David Eatock, [email protected]

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 21/46

RAPPORTEURBrian HAYES

HYPERLINK REFERENCES

• http://ec.europa.eu/social/main.jsp?langId=en&catId=89&newsId=1194&furtherNews=yes

• http://www.europarl.europa.eu/sides/getDoc.do?type=TA&language=EN&reference=P7-TA-2013-204

• http://eur-lex.europa.eu/legal-content/EN/TXT/?qid=&uri=CELEX:52014PC0167

• http://www.europarl.europa.eu/sides/getDoc.do?pubRef=-//EP//NONSGML REPORT A8-2016-0011 0 DOC PDF V0//EN

• http://www.europarl.europa.eu/oeil/popups/ficheprocedure.do?reference=2014/0091(COD)&l=en

• http://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX:32003L0041&from=EN

• http://www.europarl.europa.eu/RegData/etudes/BRIE/2016/589800/EPRS_BRI(2016)589800_EN.pdf

• https://eiopa.europa.eu/Publications/Reports/EIOPA-BoS-14-083-Market-Development-Report-2014-deff.pdf

• mailto:[email protected]

MONEY MARKET FUNDS [ EXPECTED ARRIVALS ]

CONTENT

The aim of the regulation on Money Market Funds 2013/0306(COD) is to ensure uniform prudential requirements that apply to money

market funds throughout the Union.

A money market fund (MMF) is a mutual fund that purchases short-term assets such as money-market instruments issued by banks,

governments or corporations (e.g. treasury bills, commercial papers and certificates of deposit). These instruments qualify as an MMF

only if their residual maturity does not surpass 397 days (short-term MMF) or two years (standard MMF). MMFs are a considerable

source of short-term financing for financial institutions, corporations and governments. The MMFs in issue in the EU have systemic

relevance as they are worth approximately €1 trillion and constitute around 15% of the Union's funds industry. The crisis highlighted

possible problems with instantaneous redemption and value preservation when the prices of assets in which MMFs are invested start

to decline.. This could potentially lead to runs as investors withdraw from MMFs.

On 4 September 2013, the European Commission adopted a proposal for new rules on MMFs. The proposed regulation aims to

improve the ability of MMFs to weather possible redemption pressure by boosting their liquidity profile as well as stability, to be

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 22/46

achieved through five initiatives: (i) introducing mandatory conditions on portfolio structure – MFFs would need to hold at least 10%

of assets that mature (i.e. have to be repaid by the issuer) within a day, and another 20% that mature within a week; (ii) establishing a

capital buffer for 'constant net asset value' (CNAV) MMFs, which seek to maintain a stable share/unit price (unlike variable NAV

MMFs) – this buffer will be used to help ensure stable redemption prices; (iii) clear labelling of MMFs, differentiating between short-

term and standard kinds; (iv) customer profiling to help predict substantial redemptions; and (v) internal credit risk assessment by

MMF managers, to prevent excessive dependence on external ratings.

The taking up of activities as fund manager is regulated either by the UCITS Directive or by the AIFM Directive. The activities of the

managers will continue to be subject to AIFMD and UCITS Directive but the product rules contained under UCITS framework will be

supplemented by the product rules contained in this proposed Regulation.

The European Parliament voted its amendments on the proposal for the MMF regulation in plenary on 29 April 2015. In its

amendments the European Parliament recognised that MMFs need to be more resilient to crises. MEPs proposed to remove the

obligation to hold a 3% capital buffer for CNAV MMFs and to limit CNAV MMFs to:

• Retail CNAV MMFs, available only for selected investors such as charities, public authorities, and foundations and non-profit

organisations;

• Public Debt CNAV MMFs (investing 99.5% of their assets in public debt instruments, and, by 2020, at least 80% of their assets in

EU public debt instruments) – a new type of Low Volatility Net Asset Value MMFs (LVNAV MMFs may show a constant NAV under strict

conditions). This type of fund would be authorised for a maximum period of five years, but the Commission would review the

regulation after four years, specifically including examination of the possibility of extending this authorisation indefinitely (this

provision is called by many stakeholders a 'sunset clause' and means that a law will expire on a particular date, unless it is

reauthorised by the legislature).

All MMFs should have in place liquidity fees and redemption gates to help prevent sudden outflows. Public Debt CNAV MMFs and

Retail CNAV MMFs should cease to be CNAV MMFs if they fail to meet the minimum amount of weekly liquidity requirements within 30

days of having utilised the liquidity fees or redemption gates. In such instances, they should automatically convert to a VNAV MMF or

be liquidated. The Parliament also underlined that it is not appropriate to ban MMFs from soliciting or financing an external credit

rating and added financial derivative instruments (fulfilling certain conditions) and high-quality asset backed securities (e.g. car loans)

to instruments eligible for investment by MMFs. MMFs will also be required to diversify their asset portfolios, respect strict liquidity

and concentration standards, have sound stress-testing processes and increase their reporting and transparency towards investors.

Importantly, the assets of an MMF are to be valued every day and this value published daily on its website. MMFs are also to report

weekly to their investors the following: the liquidity profile; the credit profile and portfolio composition; weighted average maturity

(WAM) of the portfolio; weighted average life (WAL) of the portfolio; and concentration of the top five investors in the MMF.

The plenary did not conclude Parliament's first reading, instead referring the proposal back to the ECON Committee with a view to

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 23/46

starting trilogue negotiations as soon as possible, pending the Council agreeing on its general approach.

While the Council strived to advance the dossier, no further progress on general position was reported until June 2016 when the

Economic and Financial Affairs Council agreed draft rules to be negotiated with the EP. The draft regulation lays down rules for MMFs,

in particular the composition of their portfolios and the valuation of their assets, introduces common standards to boost their liquidity

when market conditions are stressed. In addition, the text provides for common rules to ensure that the fund manager has a good

understanding of his/her investors, and provides investors and supervisors with adequate and transparent information. The new rules

introduce a permanent category of LVNAV MMFs which are to replace most of the existing CNAV MMFs within 2 years of entry into

force of the regulation. LNAV MMFs would be allowed - although to a limited extent and under strict conditions - to offer a constant

net asset value. The CNAV MMFs would be limited to those that invest 99.5% of their assets in public debt instruments and those with

an investor base solely outside the EU.

Two trilogue meetings on MMF regulation took place so far (in July and September 2016), with a third one scheduled for 4 October

2016.

References:

• European Commission, Money Market Funds, dedicated website

• European Commission, UCITS – Undertakings for the collective investment in transferable securities, dedicated website

• Legislative act, European Parliament and Council Directive 2011/61/EU of 8 June 2011 on Alternative Investment Fund Managers (AIFM)

• EP Legislative Observatory, Procedure file on Money Markets Funds, 2013/0306(COD)

• EP Press release: Making money market funds more resilient to financial crises, 26 February 2015

Further reading:

• European Parliament, EPRS, Money Market Funds. Measures to improve stability and liquidity, Legislative briefing, February 2016

• Council, Money market funds: Council agrees its negotiating stance, press release, 15 June 2016

For further information: Marcin Szczepanski, [email protected]

RAPPORTEURNeena GILL

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 24/46

HYPERLINK REFERENCES

• http://ec.europa.eu/finance/investment/money-market-funds/index_en.htm

• http://ec.europa.eu/finance/investment/ucits-directive/index_en.htm

• http://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX:32011L0061&from=EN

• http://www.oeil.ep.parl.union.eu/oeil/popups/ficheprocedure.do?reference=2013/0306(COD)&l=en

• http://www.europarl.europa.eu/news/nl/news-room/20150224IPR25114/making-money-market-funds-more-resilient-to-financial-crises

• http://www.europarl.europa.eu/RegData/etudes/BRIE/2016/577956/EPRS_BRI(2016)577956_EN.pdf

• http://www.consilium.europa.eu/en/press/press-releases/2016/06/15-money-market-funds/

• mailto:[email protected]

BANKING STRUCTURAL REFORM [ ON HOLD ]

CONTENT

Over the last five years, the EU has undertaken a large number of reforms to establish a safer, more resilient, transparent and

responsible financial system serving the economy and society as a whole. However, the size and complexity of a number of banks

remain an issue of concern. The balance sheet of some of these banks is larger than the GDP of their home countries. These banks still

remain ‘too big to fail’ and, as a result, take advantage of the presumption that the sovereign will bail them out with taxpayers’ money

in case of substantial trouble, instead of letting them fail.

That is why, on 29 January 2014, the Commission submitted a proposal for a regulation on structural measures improving the resilience of

EU credit institutions, which aims at strengthening the stability of the EU banking system and protecting the deposit-taking business of

the biggest and most complex EU banks from potentially risky trading activities. The new rules wouldd apply to banks that are either

deemed of global systemic importance or exceed certain thresholds in terms of trading activity or absolute size. The two key elements

of the regulation are the prohibition of proprietary trading and the potential separation of a bank's high-risk activities (market-making,

investment in/sponsoring of securitization and trading of certain derivatives) from its 'core' business, such as deposit-taking or retail

payment services. It would also empower supervisory authorities to systematically review banking activities including compulsory

‘separations plans’. Note that the proposed Regulation builds on the recommendations made by the High Level Expert Group chaired

by the Governor of the Bank of Finland, Mr Erkki Liikanen (‘Liikanen Group’).

The Council reached a common approach for negotiations with the Parliament on structural measures to improve the resilience of EU

credit institutions on 19 June 2015.

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 25/46

The issue is currently on hold within the European Parliament's Committee on Economic and Monetary Affairs (ECON) after the draft

report was rejected in late May 2015 (29 in favour, 30 against, 0 abstentions). Among the most controversial issues discussed was

whether mandatory structural separation could be avoided if banks would add capital. The key proposals for amendments of the draft

report indicate a less strict approach than the Commission proposal: For instance, the rapporteur suggests to alter in Article 2b (subject

matter) the original wording 'separation of certain trading activities' into 'measures to reduce excessive risk taking'. Accordingly, Article

3 (scope) should read 'trading related risk exposures' instead of 'trading activities' as proposed by the Commission. Article 6.2 on

'prohibition of certain trading activities' should be slightly eased regarding the use of Alternative Investment Funds (AIF). The title of

Chapter 3 'Separation of certain trading activities' should instead read 'Measures regarding...' with subsequent further alterations to

Article 8 (scope of activities).

In the rapporteur's explanatory statement, he stresses that since systemic risk has less to do with the respective banking model or a

particular size of institution, regulation needs instead to focus on 'interdependence and the risk exposure'. Put differently, as trading

per se is 'not more systemically risky than lending', using a risk-based approach seems more appropriate than focussing on structures

or activities.

Further progress would require a second vote but no decision for this purpose has been taken yet. It was reported that the major

political groups reached an informal compromise in October 2015.

The 2015 Banking Union annual report adopted by Parliament on 10 March 2016 noted that 'Banking Structural Reform, which was

conceived to reduce systemic risk and address the issue of ‘too big to fail’ institutions, has yet to be implemented' and, as a result,

called for ‘a swift legislative agreement’.

References:

• European Commission, Proposal for a Regulation on structural measures improving the resillience of the EU credit

institutions, COM(2014)0043

• High-level Expert Group on reforming the structure of the EU banking sector, Final report, 2 October 2012

• Council, Restructuring risky banks: Council agrees its negotiating stance, Press release, 19 June 2015

• Committee on Economic and Monetary Affairs, Minutes of the meeting of 26 May 2015

• European Parliament, Resolution of 10 March 2016 on the Banking Union - Annual Report 2015, 2015/2221(INI)

• EP Legislative observatory, Procedure file on Structural measures improving the resillience of EU credit institutions, 2014/0020(COD)

For further information: Andrej Stuchlik, [email protected]

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 26/46

RAPPORTEURGunnar HÖKMARK

HYPERLINK REFERENCES

• http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52014PC0043&from=EN

• http://ec.europa.eu/finance/bank/docs/high-level_expert_group/report_en.pdf

• http://www.consilium.europa.eu/en/press/press-releases/2015/06/19-restructuring-risky-banks-council-agrees-negotiating-stances/

• http://www.europarl.europa.eu/sides/getDoc.do?type=COMPARL&reference=PE-560.570&format=PDF&language=EN&secondRef=02

• http://www.europarl.europa.eu/sides/getDoc.do?type=TA&language=EN&reference=P8-TA-2016-0093

• http://www.europarl.europa.eu/oeil/popups/ficheprocedure.do?reference=2014/0020(COD)&l=en

• mailto:[email protected]

CORPORATE GOVERNANCE: LONG-TERM SHAREHOLDER ENGAGEMENT - CORPORATEGOVERNANCE STATEMENT [ ON HOLD ]

CONTENT

Corporate governance and company law are essential to ensure that companies are well-governed and sustainable in the long

term. For this reason, they are important in the context of the long-term financing of the European economy. European areas of

interest in corporate governance include directors’ duties and liability, shareholders’ right, remuneration policies, country-by-country

reporting provisions for financial institutions or transparency requirements.

In the context of the 2012 Action Plan on European company law and corporate governance and the Communication on the long-term

financing of the European economy, the Commission published on 9 April 2014 a proposal for a directive. The proposal focuses on

amending two other directives: one, which regards the encouragement of long-term shareholder engagement (2007/36/EC), and one,

which regards certain elements of the corporate governance statement (2013/34/EU).

On 08 July 2015 the rappoorteur proposed that the vote on the draft legislative resolution should be postponed in accordance with

Rule 61(2)). Parliament approved the proposal. The matter was thus deemed to have been referred back to the committee

responsible for reconsideration.

LEGISLATIVE TRAIN 10.2016 4C DEEPER AND FAIRER INTERNAL MARKET WITH A STRENGTHENED INDUSTRIAL BASE / FINANCIALSERVICES / UP TO €82BN 27/46

References:

• Legislative act, European Parliament and Council Directive 2007/36/EC of 11 July 2007 on the exercise of certain rights of shareholders in

listed companies

• Legislative act, European Parliament and Council Directive 2013/34/EU of 26 June 2013 on the annual financial statements, consolidated

financial statements and related reports of certain types of undertakings

• European Commission, Proposal for a Directive amending Directive 2007/36/EC and Directive 2013/34/EU, COM(2014)0213

• European Commission, Commission Communication - Action Plan: European company law and corporate governance - a modern legal

framework for more engaged shareholders and sustainable companies, COM(2012)0740

• European Parliament, Long-term shareholder engagement and corporate governance statement, amendments adopted by EP, 8 July

2015

• EP Legislative Observatory, Procedure file on Corporate governance: long-term shareholder engagement; corporate governance

statement, 2014/0121(COD)

Further reading:

• European Commission, Commission roadmap to meet the long-term financing needs of the European economy, press release, 27 March

2014

For further information: Angelos Delivorias, [email protected]

RAPPORTEURSergio Gaetano COFFERATI

HYPERLINK REFERENCES

• http://eur-lex.europa.eu/legal-content/EN/TXT/?qid=1397142478478&uri=CELEX:32007L0036

• http://eur-lex.europa.eu/legal-content/EN/TXT/?qid=1397142682708&uri=CELEX:32013L0034

• http://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52014PC0213

• http://eur-lex.europa.eu/legal-content/EN/TXT/?qid=1453891145338&uri=CELEX:52012DC0740

• http://www.europarl.europa.eu/sides/getDoc.do?type=TA&language=EN&reference=P8-TA-2015-0257

• http://www.oeil.ep.parl.union.eu/oeil/popups/ficheprocedure.do?reference=2014/0121(COD)&l=en