Embed Size (px)

Citation preview

1

WORKSHOP ON

ENABLING SERVICE TAX PRACTICE

ORGANISED BY.....INDIRECT TAXES COMMITEEE OF ICAI

HOSTED BY…….HYDERABAD BRANCH OF SOUTH INDIAN REGIONAL COUNCIL OF ICAI

COVERAGE

SERVICE..DECLARED SERVICE

A CANDLE LOSES NOTHING BY LIGHTING ANOTHER CANDLE

2

PRESENTED BY RAJIV LUTHIA

NEGATIVE LIST

EXEMPTIONS

26th October,2012 CA Rajiv Luthia

NEGATIVE LIST REGIME!!!!!!!! W.e.f. 1st July,12

• Section 65, 65A, 66 & 66A amended whereby the provisions of those sections would not apply with effect from 1st July,2012.

• Section 65B inserted interpreting various terms in view of introduction of comprehensive approach for taxation of services.

• Section 66B inserted to levy ST @12% on the value of all services other than those specified in the negative list provided or agreed to be provided in the taxable territory by one person to another.

• Section 66C inserted to grant power to Central Government to make rules for determination of place of provision of service.

• Section 66D inserted to provide negative list of services. (17 items) Eg… Service by RBI, by foreign diplomatic mission, trading of goods, betting lottery etc., Funeral etc.

• Section 66E inserted providing for declared list of Services (9 items)

• Section 66F inserted to provide for ..Principles of interpretation of specified description of services or bundled services26th October,2012

3CA Rajiv Luthia

DEFINITON OF “SERVICE”`

• Section 65B(44)…. Definition of “Service” … means– Any activity…. Excluding

• Transfer of title in goods or immovable property by way of sale, gift or in any other manner; or

• Such transfer, delivery or supply of any goods which is deemed to be a sale within the meaning of clause (29A) of article 366 of the constitution; or

• A transaction in money or actionable claim;• Provision of Service by an employee to employer in

course of employment• Fees taken in court or tribunal established any law

– For consideration– Carried out by person for another & – Includes declared Service

426th October,2012 4CA Rajiv Luthia

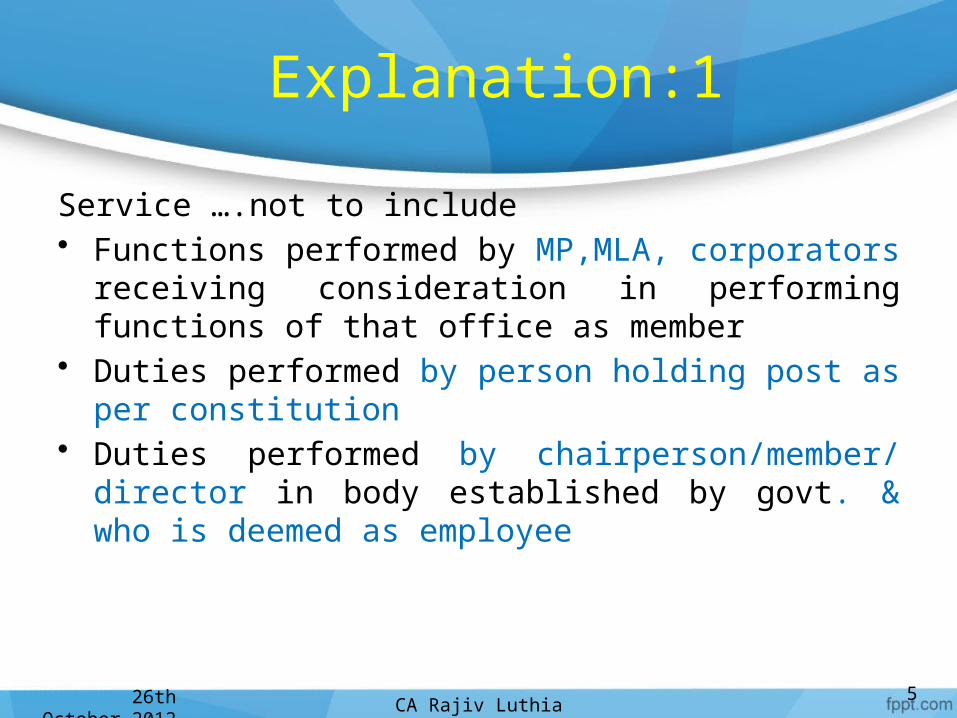

Explanation:1

Service ….not to include• Functions performed by MP,MLA, corporators receiving

consideration in performing functions of that office as member

• Duties performed by person holding post as per constitution

• Duties performed by chairperson/member/ director in body established by govt. & who is deemed as employee

26th October,2012 5CA Rajiv Luthia

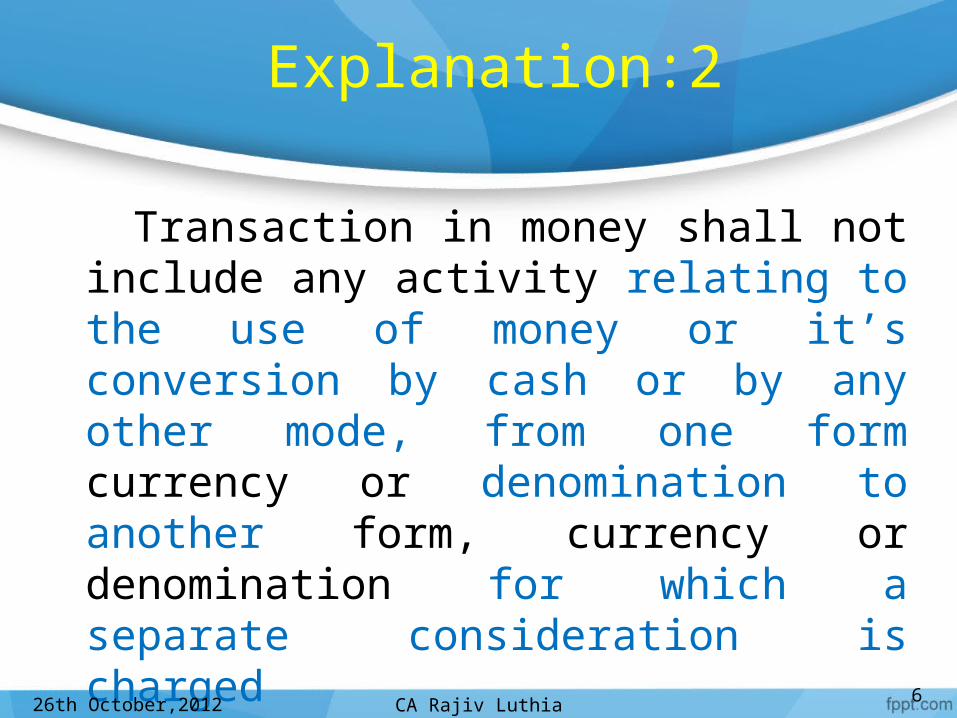

Explanation:2

Transaction in money shall not include any activity relating to the use of money or it’s conversion by cash or by any other mode, from one form currency or denomination to another form, currency or denomination for which a separate consideration is charged

26th October,2012 6CA Rajiv Luthia

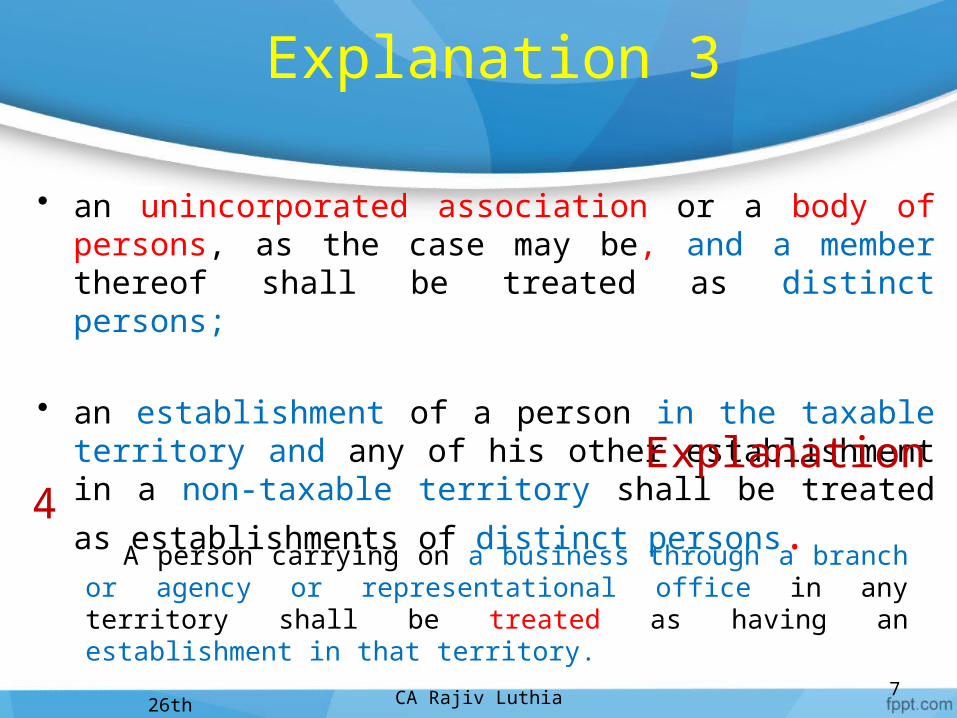

Explanation 3

• an unincorporated association or a body of persons, as the case may be, and a member thereof shall be treated as distinct persons;

• an establishment of a person in the taxable territory and any of his other establishment in a non-taxable territory shall be

treated as establishments of distinct persons.

26th October,20127

Explanation 4 A person carrying on a business through a branch or agency or

representational office in any territory shall be treated as having an establishment in that territory.

CA Rajiv Luthia

ACTIVITY

8

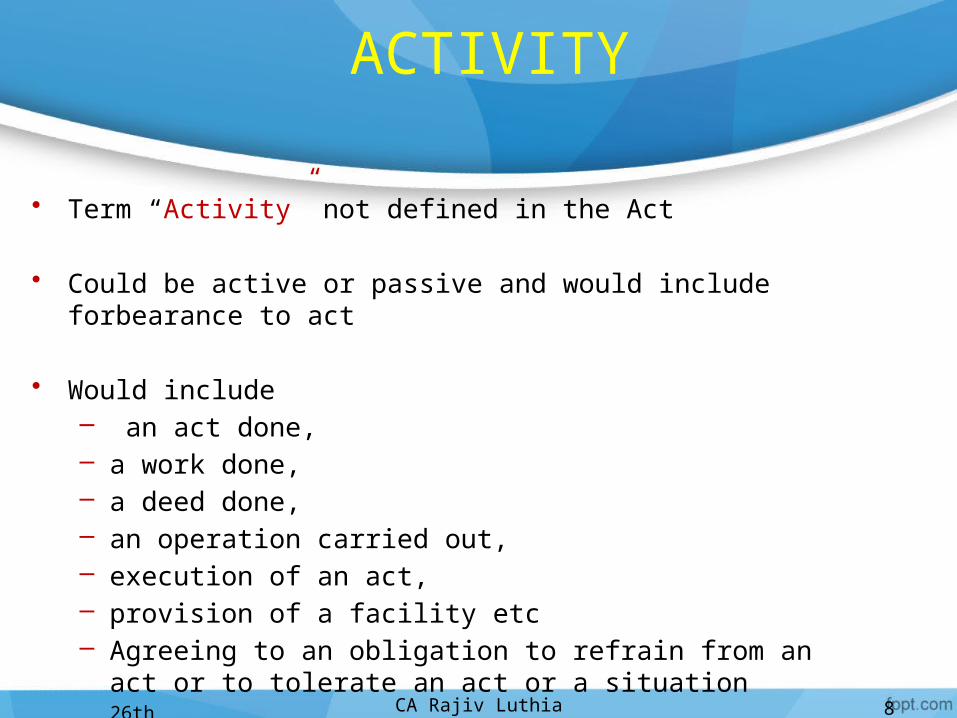

• Term “Activity” not defined in the Act

• Could be active or passive and would include forbearance to act

• Would include– an act done, – a work done, – a deed done, – an operation carried out, – execution of an act, – provision of a facility etc– Agreeing to an obligation to refrain from an act or to tolerate an

act or a situation

26th October,2012 CA Rajiv Luthia

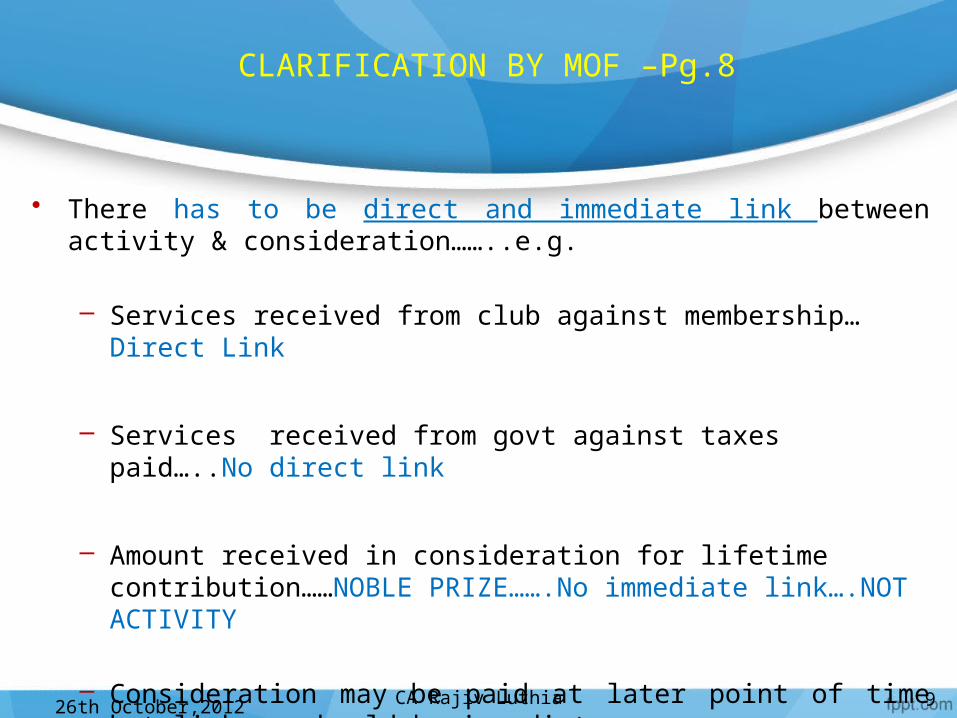

CLARIFICATION BY MOF –Pg.8

26th October,2012 9

• There has to be direct and immediate link between activity & consideration……..e.g.

– Services received from club against membership…Direct Link

– Services received from govt against taxes paid…..No direct link

– Amount received in consideration for lifetime contribution……NOBLE PRIZE…….No immediate link….NOT ACTIVITY

– Consideration may be paid at later point of time but linkage should be immediate

CA Rajiv Luthia

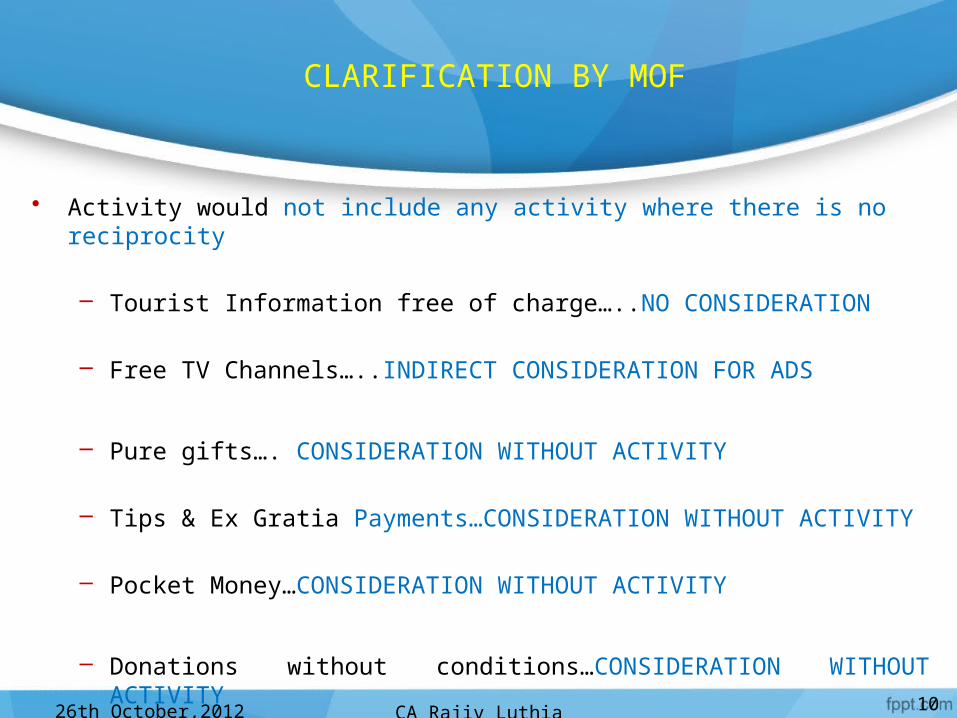

CLARIFICATION BY MOF

26th October,2012 10

• Activity would not include any activity where there is no reciprocity

– Tourist Information free of charge…..NO CONSIDERATION

– Free TV Channels…..INDIRECT CONSIDERATION FOR ADS

– Pure gifts…. CONSIDERATION WITHOUT ACTIVITY

– Tips & Ex Gratia Payments…CONSIDERATION WITHOUT ACTIVITY

– Pocket Money…CONSIDERATION WITHOUT ACTIVITY

– Donations without conditions…CONSIDERATION WITHOUT ACTIVITY

CA Rajiv Luthia

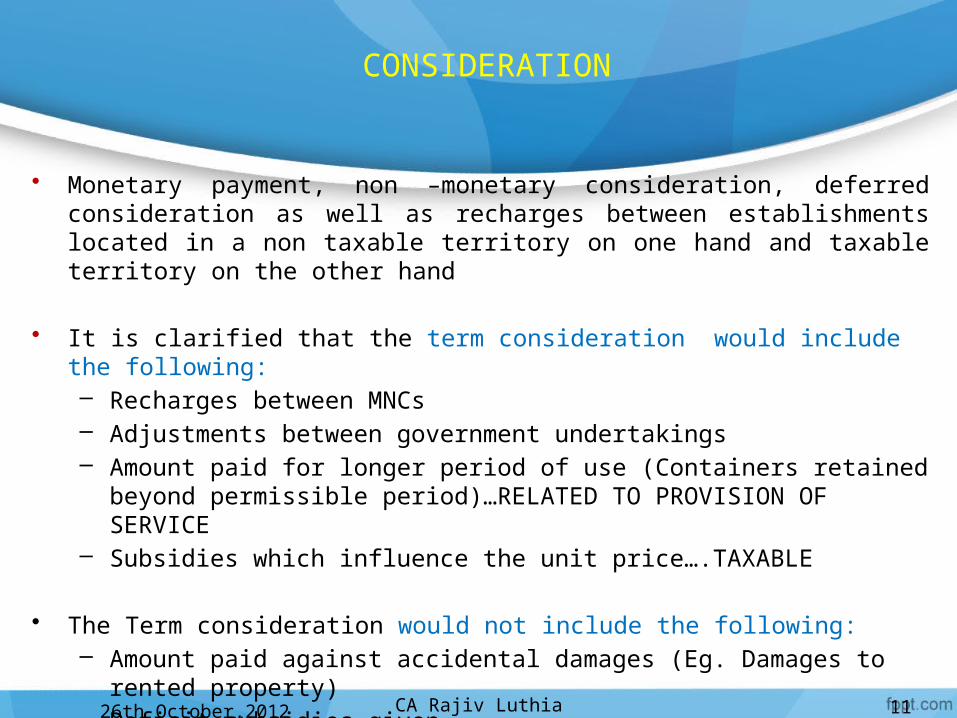

CONSIDERATION

26th October,2012 11

• Monetary payment, non –monetary consideration, deferred consideration as well as recharges between establishments located in a non taxable territory on one hand and taxable territory on the other hand

• It is clarified that the term consideration would include the following:– Recharges between MNCs– Adjustments between government undertakings– Amount paid for longer period of use (Containers retained beyond

permissible period)…RELATED TO PROVISION OF SERVICE– Subsidies which influence the unit price….TAXABLE

• The Term consideration would not include the following: – Amount paid against accidental damages (Eg. Damages to rented property)– Deficit subsidies given

CA Rajiv Luthia

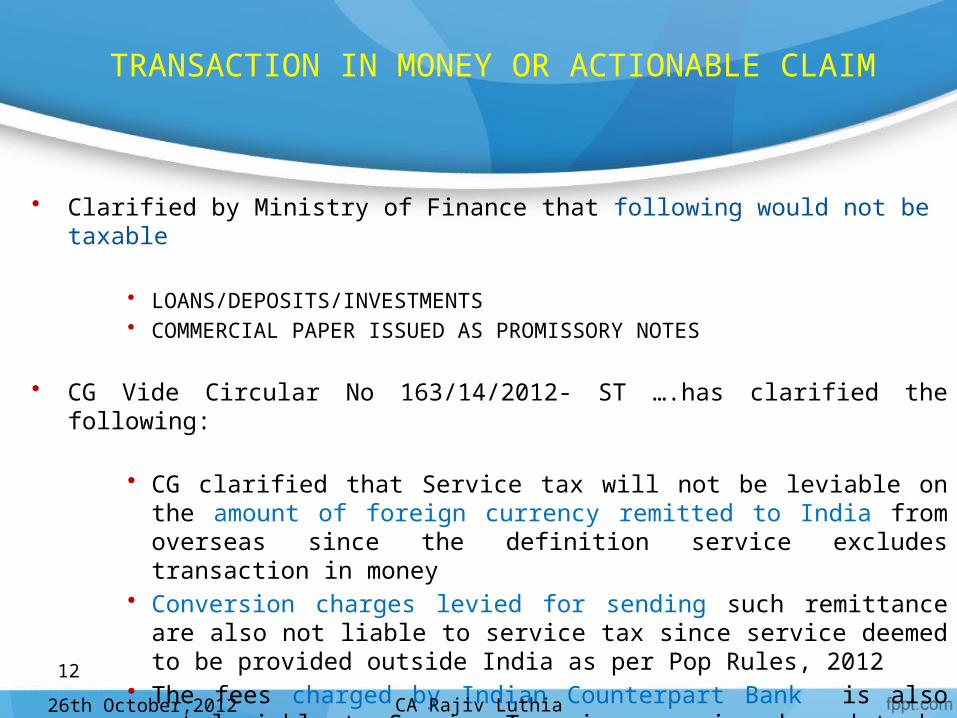

TRANSACTION IN MONEY OR ACTIONABLE CLAIM

26th October,2012

12

• Clarified by Ministry of Finance that following would not be taxable

• LOANS/DEPOSITS/INVESTMENTS• COMMERCIAL PAPER ISSUED AS PROMISSORY NOTES

• CG Vide Circular No 163/14/2012- ST ….has clarified the following:

• CG clarified that Service tax will not be leviable on the amount of foreign currency remitted to India from overseas since the definition service excludes transaction in money

• Conversion charges levied for sending such remittance are also not liable to service tax since service deemed to be provided outside India as per Pop Rules, 2012

• The fees charged by Indian Counterpart Bank is also not leviable to Service Tax since service deemed to be provided outside India

CA Rajiv Luthia

SERVICES BY EMPLOYEE TO EMPLOYER

26th October,2012 13

• Services provided beyond the course of employment is taxable…

Eg…Pvt. Coaching by teacher beyond school hours when under no obligation under the contract would be taxable

• Expenses recovered form employees for private use of company’s facilities is taxable unless otherwise exempt…canteen etc.

• Directors Fees, Commission, Bonus, Travel Reimbursements etc paid to directors would also become taxable

CA Rajiv Luthia

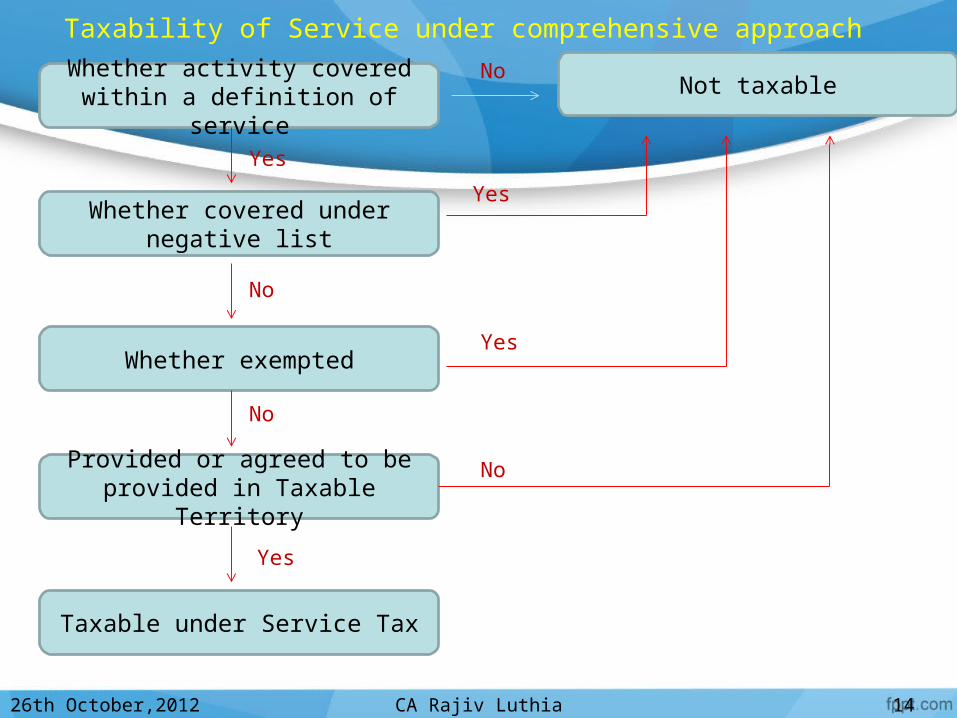

Taxability of Service under comprehensive approach

Whether activity covered within a definition of service

Not taxableNo

Yes

Whether covered under negative list

Yes

No

Whether exemptedYes

No

Provided or agreed to be provided in Taxable Territory

No

Yes

Taxable under Service Tax

26th October,2012 14CA Rajiv Luthia

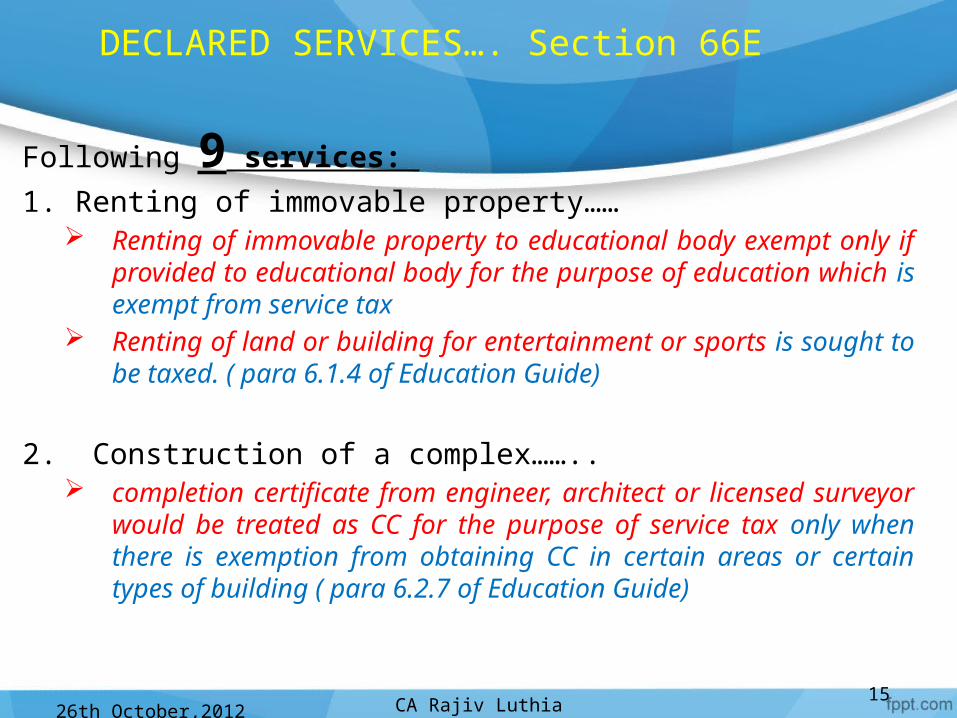

DECLARED SERVICES…. Section 66E

Following 9 services:

1. Renting of immovable property…… Renting of immovable property to educational body exempt only if

provided to educational body for the purpose of education which is exempt from service tax

Renting of land or building for entertainment or sports is sought to be taxed. ( para 6.1.4 of Education Guide)

2. Construction of a complex…….. completion certificate from engineer, architect or licensed surveyor

would be treated as CC for the purpose of service tax only when there is exemption from obtaining CC in certain areas or certain types of building ( para 6.2.7 of Education Guide)

26th October,201215

CA Rajiv Luthia

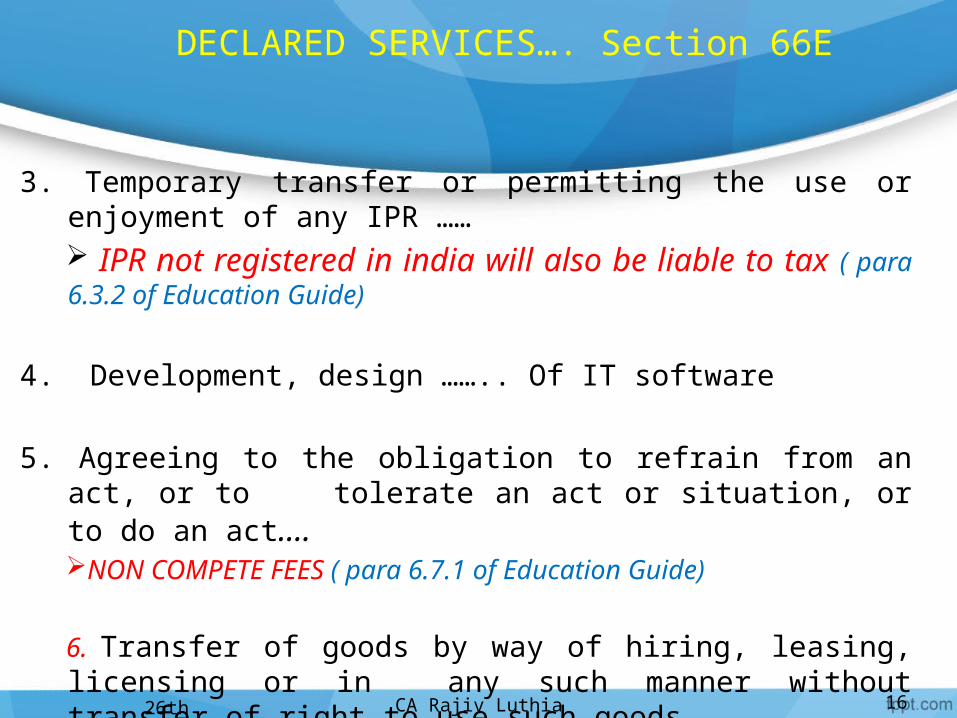

DECLARED SERVICES…. Section 66E

3. Temporary transfer or permitting the use or enjoyment of any IPR …… IPR not registered in india will also be liable to tax ( para 6.3.2 of Education Guide)

4. Development, design …….. Of IT software

5. Agreeing to the obligation to refrain from an act, or to tolerate an act or situation, or to do an act….NON COMPETE FEES ( para 6.7.1 of Education Guide)

6. Transfer of goods by way of hiring, leasing, licensing or in any such manner without transfer of right to use such goods.

26th October,2012 16CA Rajiv Luthia

DECLARED SERVICES…. Section 66E

7. Activities in relation to delivery of goods on hire purchase or any system of payment by installments Mere delivery of good on hire purchase or any system of payment

by installments not leviable to Service tax ( para 6.5.1 of Education Guide)

8. Service portion in execution of a works contract

9. Service portion in an activity wherein goods being food or any other article of human consumption or any drink (whether or not intoxicating) is supplied in any manner as a part of the activity.

26th October,201217

CA Rajiv Luthia

NEGATIVE LIST

1. Services provided by government/local authority except:

a. Service by departmental post by way of speed post, express parcel post, Life insurance & other agencies service provided to a person other than govt.. Postal services such as post card, inland, book post, registered post, money orders, postal orders provided exclusively by department of post are not liable…Services of speed post, express parcel service provided by postal department is already taxable under “courier service” w.e.f. 1st May,2006..

b. Service in relation to vessel/aircraft, inside or outside

precincts of port/airport

c. Transport of goods or passengers

26th October,2012 18CA Rajiv Luthia

NEGATIVE LIST

1. Services provided by government/local authority except:

d.Support Services (Defined in sec 65B(49) other than above 3, provided to business entities (Defined in sec 65B(17).. Services provided by Government in terms of their sovereign right to business entities which are not substitutable in any manner by any private entity, are not support services for e.g. grant of mining or licensing rights or audit by CAG…

Corporations formed under central/state act, government companies or autonomous institutions set up under special act are not covered in the definition of government.

Services provided by police/security agency to corporate entities or sports events held by a private entity are taxable

26th October,2012 19CA Rajiv Luthia

NEGATIVE LIST

2. Services by RBI………Prior to 1st July., 2012 also exempt

Services provided to RBI are not in negative list and would be taxable unless otherwise exempted

3. Services by foreign diplomatic mission located in India……..Prior to 1st July,2012 not notified service

Prior to 1st July, 2012, services provided to foreign diplomatic mission were exempted………..Post 1st July, 2012 also made exempt vide notification no. 27/2012-ST dt. 20th June, 2012

26th October,2012 20CA Rajiv Luthia

21

NEGATIVE LIST

4. Service relating to agriculture (defined in Section 65B(3)) or agricultural produce( defined in Section 65B(5)) by way of :

• Agricultural operations directly related to production of agricultural produce including harvesting, threshing etc.

• Supply of farm labour….. Prior to 1st July,12, taxable under the category of “manpower supply services”

• Process such as drying, fumigating, grading, cooling etc….. Which do not alter essential characteristic of agricultural produce but make it marketable for primary market…….. Services of production or processing of agricultural goods was exempted under the category of “Business Auxiliary Services” vide Notification No.14/2004-ST dt. 10/09/2004.

• Renting, leasing of agriculture machine or vacant land with or without structure thereon ….. Prior to 1st July,12 taxable under the category of “Supply of Tangible Goods for Use” if renting or leasing is without possession & effective control..Vacant land used for agriculture is excluded from the definition of immovable property 21

26th October,2012 CA Rajiv Luthia

26th October,2012 22

• Loading/unloading, packing, storage warehousing of agricultural produce…Presently exempted under the category of “Cargo Handling” & “Storage & Warehousing”

• Agricultural Extension Services (defined in section 65B(4)…. Application of scientific research or knowledge through agricultural practice through farmer education.

• Service by APMC/board or service by commission agent for sale or purchase of produce….. Services of renting of shops or property by APMC is liable to service tax

NEGATIVE LIST

22CA Rajiv Luthia

NEGATIVE LIST

5. Trading of goods ….

Forward contract in commodities are covered under trading of goods Commodities futures are not covered under the definition of service Auxiliary Services relating to forward contract or future contract not

covered under negative list

6. Any process amounting to manufacture or production of goods…defined in Section 65B(40)

7. Selling of space or timeslot for advertisement other than advertisements broadcast by radio or television ……..

Sale of space for advertisement in billboard, public place, building, conveyances, cell phones, ATM, aerial advertisement..not taxable

Making & preparation of advertisement & commission received by advertising agencies from broadcasters/publishing companies continue to be taxable. 2326th October,2012 23CA Rajiv Luthia

NEGATIVE LIST

8. Service by way of access of road or a bridge on payment of toll charges User access fee for use of road was not taxable as clarified by Circular

No.152/3/2012 dt. 22/02/2012 Service charges paid to toll collecting agency is liable to service tax

9. Betting, gambling or lottery Organizing or promoting gambling or betting events is liable to service

tax

10. Admission to entertainment events (defined in Sec 65B(24)) or access to amusement facilities (defined in Sec 65B(9))

Standalone ride set up in mall would be covered under amusement facility & negative list

2426th October,2012 24CA Rajiv Luthia

NEGATIVE LIST

11. Transmission or distribution of electricity by an electricity transmission or distribution utility..(defined in Section 65B(23)..

Electricity charges recovered by developer or housing society not covered under the negative list

Service provided by way of installation of genset or similar equipment is taxable

12. Services by way of-

• Pre-school education and education up to higher secondary school or equivalent • Education as a part of curriculum for obtaining a qualification recognized by any

law for time being in force..(Qualification recognised by law of foreign country is not covered in negative list)

• Education as a part of an approved vocational education course

– Pvt Tutions are taxable (Para 4.12.8 of EG)– Placement Services provided by colleges are taxable..– Will commercial coaching classes be covered under limb 1 ????..– Doesn’t one need to differentiate between coaching & education?26th October,2012 25CA Rajiv Luthia

NEGATIVE LIST

13. Services by way of renting (defined in Section 65B (41) of residential dwelling for use as residence

Residential dwelling does not include hotel, motel, inn, guest house, campsite, lodge, house boat or like places for temporary stay

The rent received from a building which is used as a hotel or lodge by the lessee will not be covered in negative list

Prior to 1st July, 2012, the same was excluded from the definition of “immovable property” and hence was not taxable

26th October,2012 26CA Rajiv Luthia

NEGATIVE LIST

14. Services by way of-• Extending deposits, loans or advances in so far as the

consideration is represented by way of interest or discount…. Interest on FD, OD, Term Loan, Corporate deposit etc.

would fall under negative list Loan processing charges are not covered under negative

list Inter se sale or purchase of foreign currency amongst

banks or authorised dealers of foreign exchange or amongst banks and such dealers… Prior to 1st July, 2012, vide notification no. 19/2009-ST

dated 7th July, 2009 interbank transaction of purchase & sale of foreign currency between banks were exempt

26th October,201227 CA Rajiv Luthia

NEGATIVE LIST

15. Service of transportation of passenger with or without accompanied belongings by-

• A stage carriage… Presently excluded from definition of “Tour Operator”

• Railways in a class other than-– First class; or . EXEMPTED FROM 2nd July,12 – An air conditioned coach till 30th September,2012 vide

Notification No 43/2012..ST

• Metro, mono rail or tramway• Inland waterways • Public transport other than predominantly for tourism purpose in

a vessel in a vessel, between places located in india; and• Metered cabs, radio taxis or auto rickshaws.

26th October,2012 28CA Rajiv Luthia

NEGATIVE LIST

16. Services by way of transportation of goods- • By road except the services of-

– A goods transportation agency; or … Transportation of goods by road in 3-wheeler is made liable to tax

– A courier agency….. Presently Transport of goods by 3-wheeler not liable

• By an aircraft or a vessel from a place outside India upto the customs station of clearance in India; or…

Express cargo service is not covered under the negative list… Transport of goods by railway, air & by vessel in coastal waters are not

covered under negative list.

• By inland waterways

17.Funeral, burial, crematorium or mortuary services including transportation of the deceased.26th October,2012 29CA Rajiv Luthia

Lets have break

WHO SPEAKS SOWS

BUT

WHO LISTENS REAPS

26th October,2012 31

EXEMPTIONS

Presently there are more than 100 exemption notifications-

general or specific under different category of services

With the introduction of Negative List w.e.f. 1st july,2012,

government has introduced……

1 single mega exemption notification ;

&

Other 9 exemption notifications ….refer Guidance note no.6

CA Rajiv Luthia

26th October,2012 32

EXEMPTIONS UNDER MEGA NOTIFICATION

PRESENTLY POST AMENDMENT SCENARIO

Services provided to United Nations or International Organisation declared by Central Government in pursuance of Section 3 of United Nations (Privileges &Immunities) Act, 1947 is made exempt vide Notification No 16/2002 St dated 2nd August, 2002

•Exemption to UN/Specified IO•List of specified 23 specified IO stated in guidance note no. 6 ( refer page 60)

1. Services provided to United Nations or specified International Organisations

CA Rajiv Luthia

26th October,2012 33

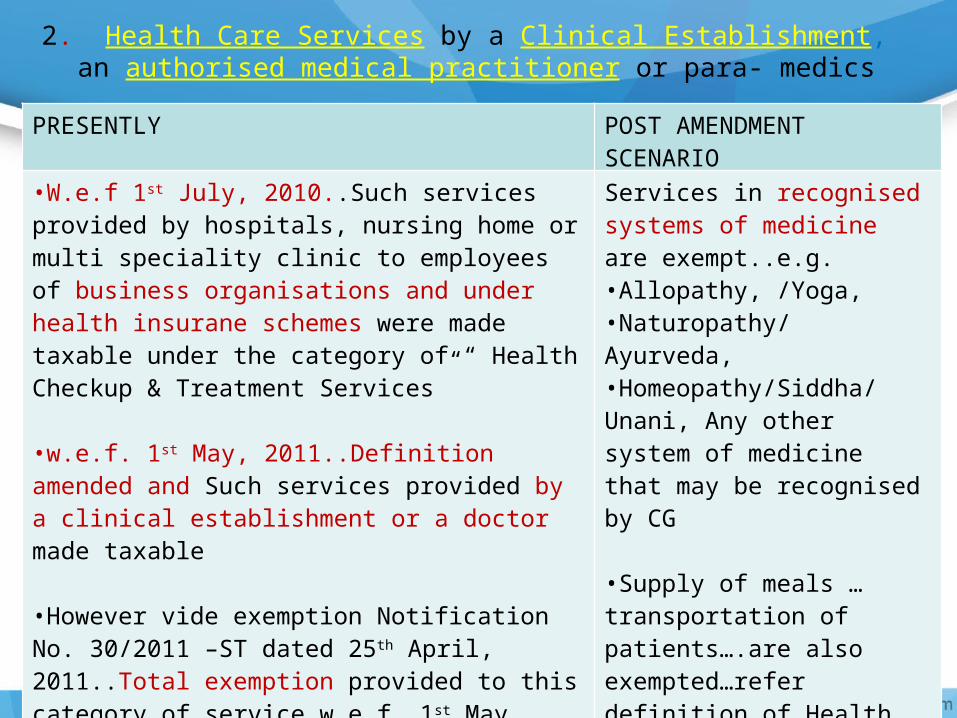

2. Health Care Services by a Clinical Establishment, an authorised medical practitioner or para- medics

PRESENTLY POST AMENDMENT SCENARIO

•W.e.f 1st July, 2010..Such services provided by hospitals, nursing home or multi speciality clinic to employees of business organisations and under health insurane schemes were made taxable under the category of “ Health Checkup & Treatment Services”

•w.e.f. 1st May, 2011..Definition amended and Such services provided by a clinical establishment or a doctor made taxable

•However vide exemption Notification No. 30/2011 –ST dated 25th April, 2011..Total exemption provided to this category of service w.e.f. 1st May, 2011

Services in recognised systems of medicine are exempt..e.g. •Allopathy, /Yoga, •Naturopathy/ Ayurveda, •Homeopathy/Siddha/ Unani, Any other system of medicine that may be recognised by CG

•Supply of meals … transportation of patients….are also exempted…refer definition of Health care service•Hair transplant or cosmetic/plastic surgery not exempted unless medically required.

26th October,2012 34

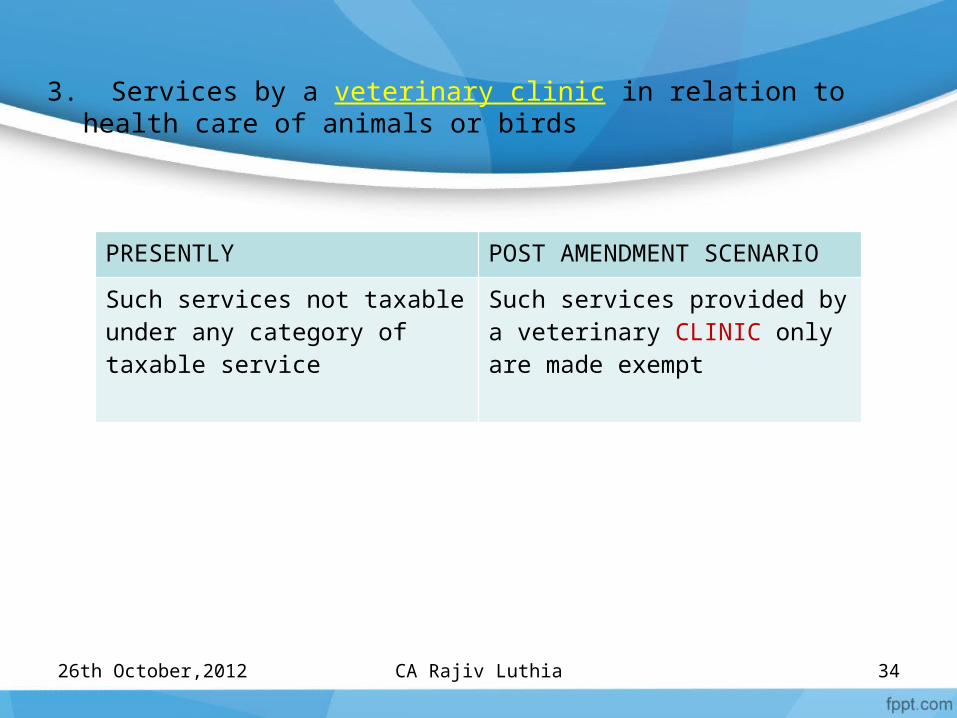

3. Services by a veterinary clinic in relation to health care of animals or birds

PRESENTLY POST AMENDMENT SCENARIO

Such services not taxable under any category of taxable service

Such services provided by a veterinary CLINIC only are made exempt

CA Rajiv Luthia

26th October,2012 35

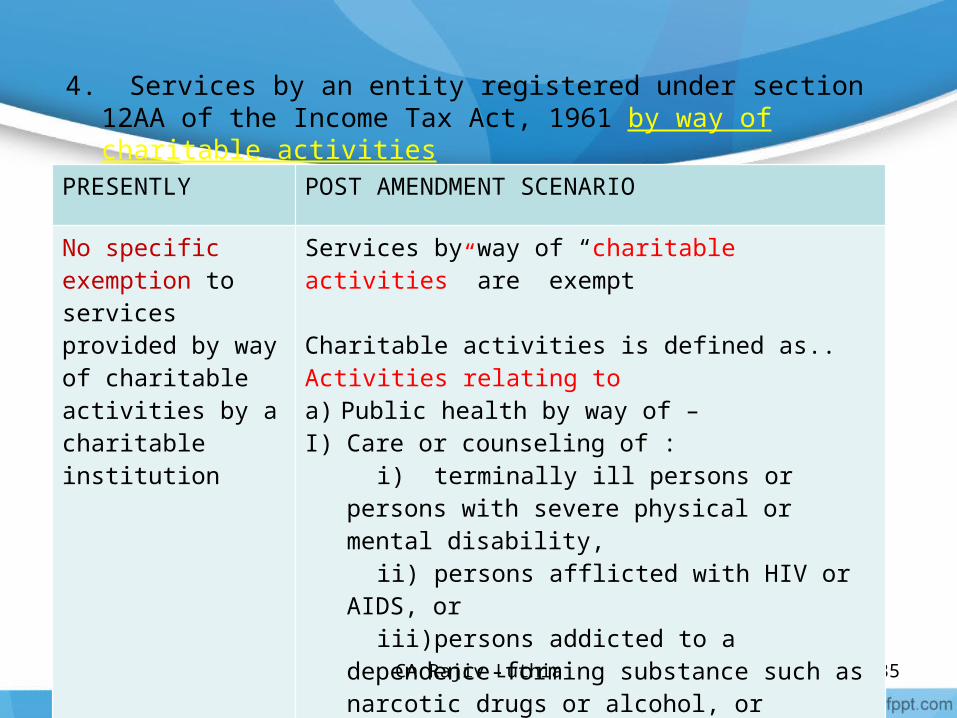

4. Services by an entity registered under section 12AA of the Income Tax Act, 1961 by way of charitable activities

PRESENTLY POST AMENDMENT SCENARIO

No specific exemption to services provided by way of charitable activities by a charitable institution

Services by way of “charitable activities” are exempt

Charitable activities is defined as..Activities relating toa) Public health by way of –I) Care or counseling of : i) terminally ill persons or persons with severe

physical or mental disability, ii) persons afflicted with HIV or AIDS, or iii)persons addicted to a dependence-forming

substance such as narcotic drugs or alcohol, or

II) Public awareness of preventive health, family planning or prevention of IV infection

CA Rajiv Luthia

26th October,2012 36

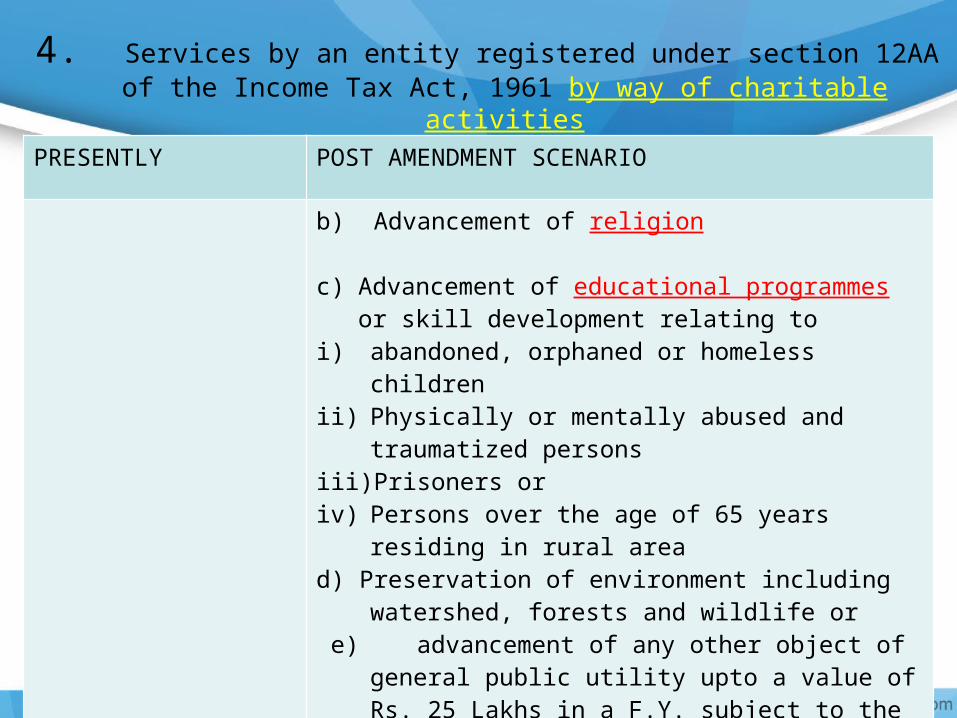

4. Services by an entity registered under section 12AA of the Income Tax Act, 1961 by way of charitable activities

PRESENTLY POST AMENDMENT SCENARIO

b) Advancement of religion

c) Advancement of educational programmes or skill development relating to

i) abandoned, orphaned or homeless childrenii) Physically or mentally abused and traumatized

personsiii) Prisoners oriv) Persons over the age of 65 years residing in rural

aread) Preservation of environment including watershed,

forests and wildlife or e) advancement of any other object of general public

utility upto a value of Rs. 25 Lakhs in a F.Y. subject to the condition that total value of such activities had not exceeded 25 Lakh Rs. In the preceding F.Y

26th October,2012 37

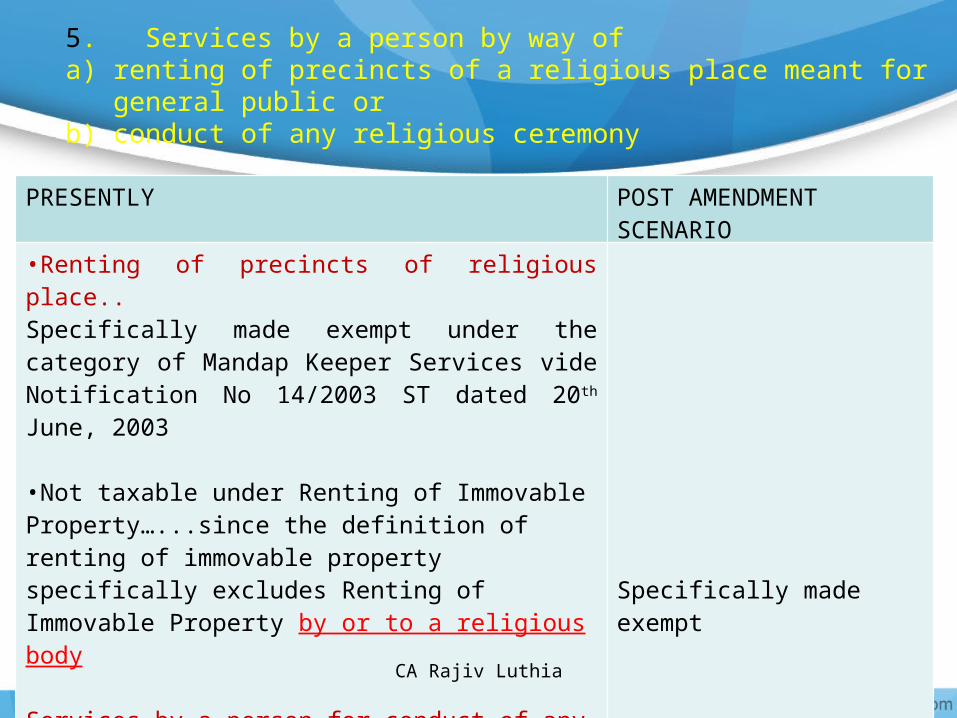

5. Services by a person by way of a) renting of precincts of a religious place meant for general public orb) conduct of any religious ceremony

PRESENTLY POST AMENDMENT SCENARIO

•Renting of precincts of religious place..Specifically made exempt under the category of Mandap Keeper Services vide Notification No 14/2003 ST dated 20th June, 2003

•Not taxable under Renting of Immovable Property…...since the definition of renting of immovable property specifically excludes Renting of Immovable Property by or to a religious body

Services by a person for conduct of any religious ceremony presently not taxable under any category of service

Specifically made exempt

CA Rajiv Luthia

38

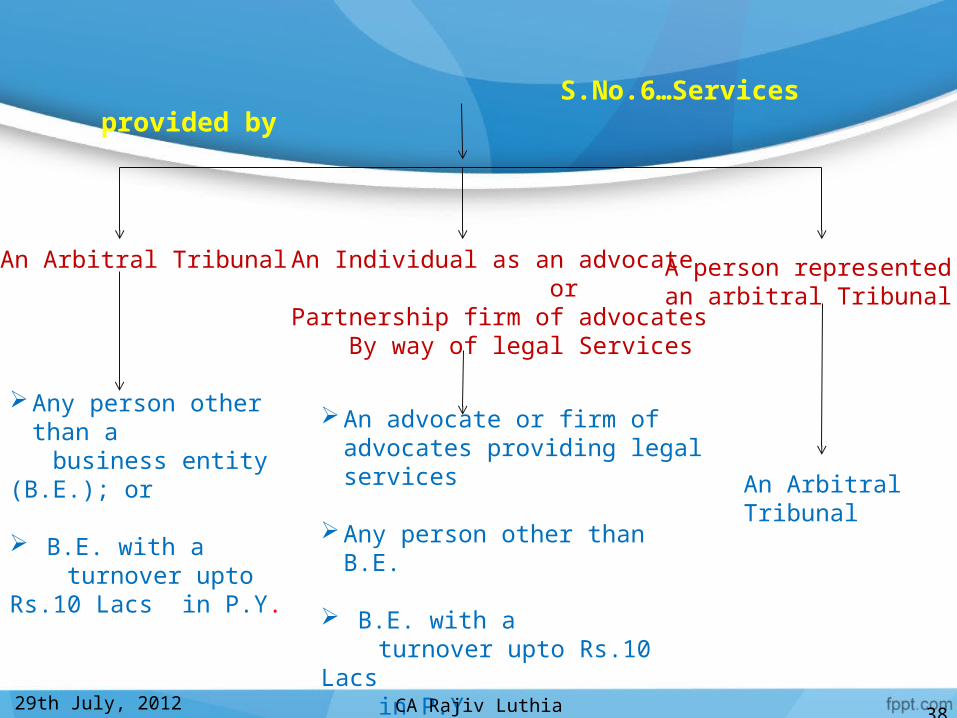

S.No.6…Services provided by

An Arbitral Tribunal

Any person other than a business entity (B.E.); or

B.E. with a turnover upto Rs.10 Lacs in P.Y.

An Individual as an advocate orPartnership firm of advocates By way of legal Services

An advocate or firm of advocates providing legal services

Any person other than B.E.

B.E. with a turnover upto Rs.10 Lacs in P.Y

A person represented on an arbitral Tribunal

An Arbitral Tribunal

29th July, 2012 CA Rajiv Luthia

26th October,2012 39

EXEMPTIONS UNDER MEGA NOTIFICATION

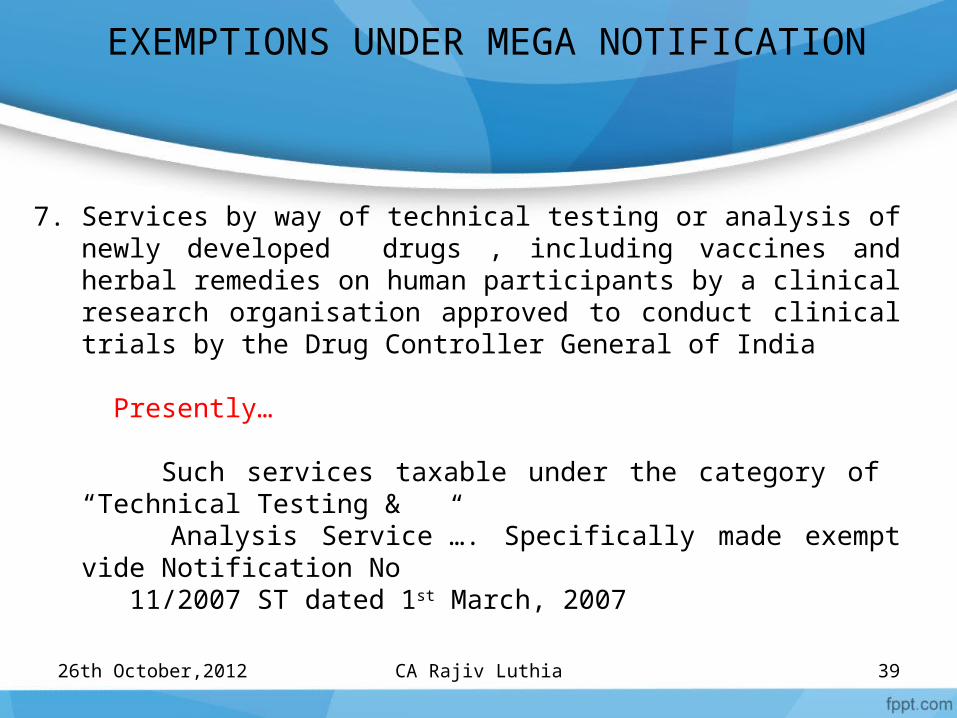

7. Services by way of technical testing or analysis of newly developed drugs , including vaccines and herbal remedies on human participants by a clinical research organisation approved to conduct clinical trials by the Drug Controller General of India

Presently…

Such services taxable under the category of “Technical Testing & Analysis Service”…. Specifically made exempt vide Notification No 11/2007 ST dated 1st March, 2007

CA Rajiv Luthia

26th October,2012 40

EXEMPTIONS UNDER MEGA NOTIFICATION

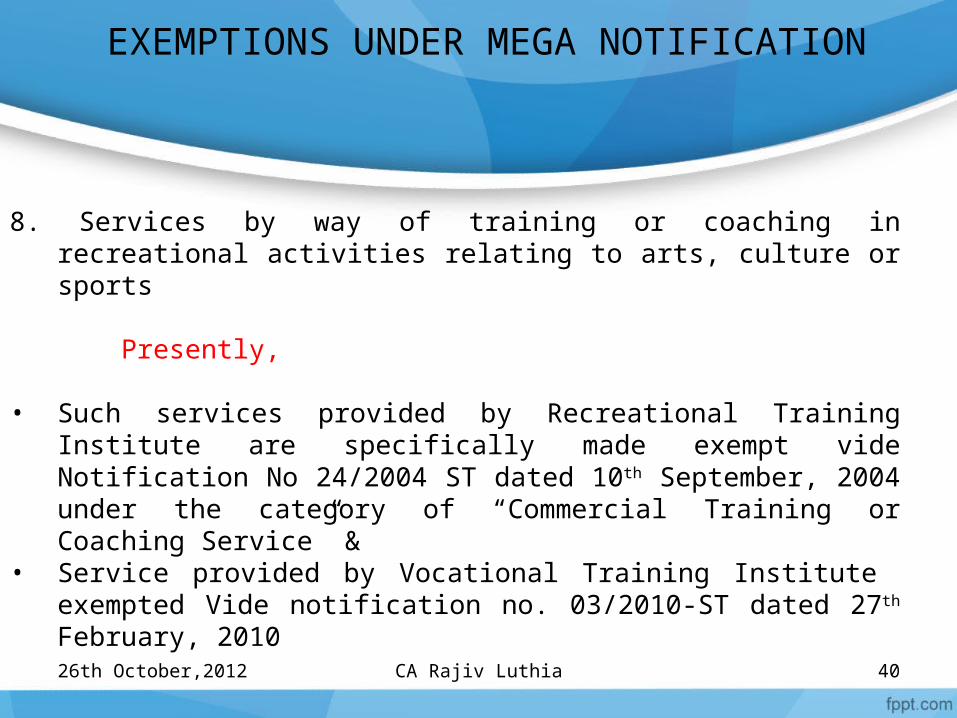

8. Services by way of training or coaching in recreational activities relating to arts, culture or sports

Presently,

• Such services provided by Recreational Training Institute are specifically made exempt vide Notification No 24/2004 ST dated 10th September, 2004 under the category of “Commercial Training or Coaching Service” &

• Service provided by Vocational Training Institute exempted Vide notification no. 03/2010-ST dated 27th February, 2010

CA Rajiv Luthia

26th October,2012 41

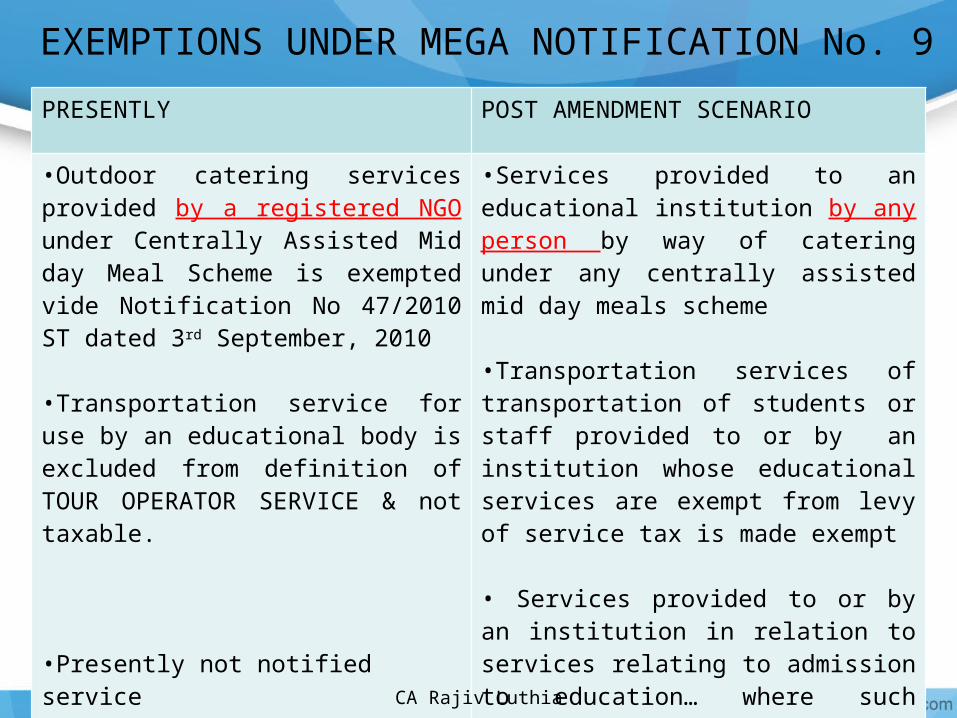

EXEMPTIONS UNDER MEGA NOTIFICATION No. 9

PRESENTLY POST AMENDMENT SCENARIO

•Outdoor catering services provided by a registered NGO under Centrally Assisted Mid day Meal Scheme is exempted vide Notification No 47/2010 ST dated 3rd September, 2010

•Transportation service for use by an educational body is excluded from definition of TOUR OPERATOR SERVICE & not taxable.

•Presently not notified service

•Services provided to an educational institution by any person by way of catering under any centrally assisted mid day meals scheme

•Transportation services of transportation of students or staff provided to or by an institution whose educational services are exempt from levy of service tax is made exempt

• Services provided to or by an institution in relation to services relating to admission to education… where such educational services are exempt from the levy of service tax

CA Rajiv Luthia

26th October,2012 42

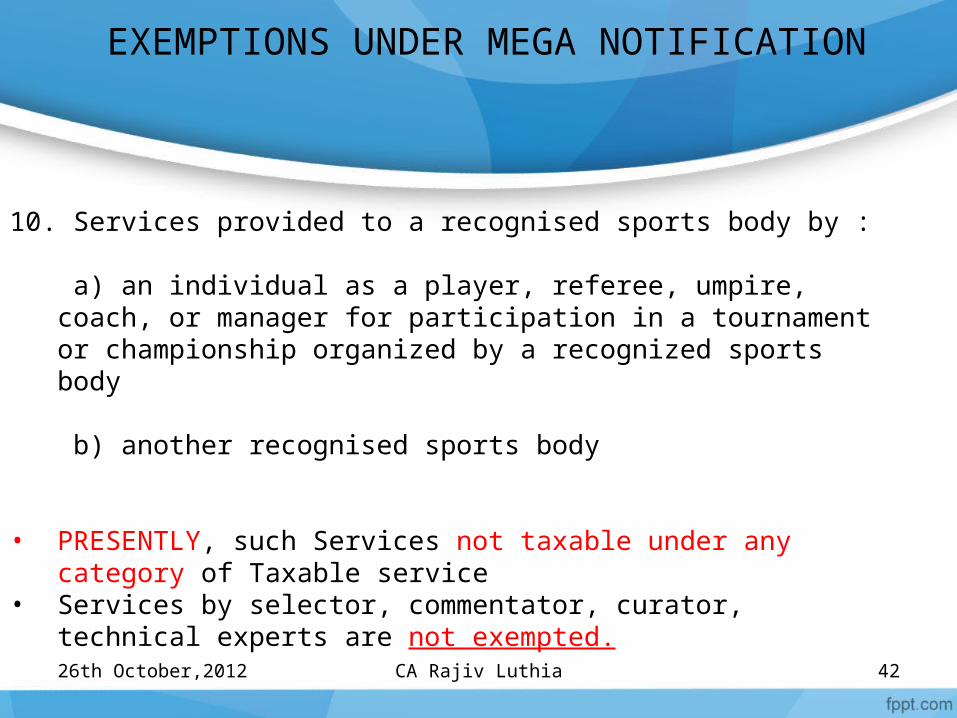

EXEMPTIONS UNDER MEGA NOTIFICATION

10. Services provided to a recognised sports body by :

a) an individual as a player, referee, umpire, coach, or manager for participation in a tournament or championship organized by a recognized sports body

b) another recognised sports body

• PRESENTLY, such Services not taxable under any category of Taxable service

• Services by selector, commentator, curator, technical experts are not exempted.

CA Rajiv Luthia

43

11. Services by way of sponsorship of tournaments or championships organized:

a) By a national sports federation or its affiliated federations where the participating teams or individuals represent any district, state, or zone

b) By association of Indian Universities, Inter University Sports Board, School Games Federation of India, All India Sports Council for the Deaf, Paralympic Committee of India, Special Olympics Bharat

c) By Central Civil Services Cultural and Sports Board

d) As part of National Games, By Indian Olympic Association or

e) Under Panchayat Yuva Kreeda aur Khel Abhiyaan Scheme

Presently, Services in relation to sponsorship of sports events are taxable under the

category of “Sponsorship services” w.e.f. 1st July, 2010

Sponsorship services provided for specified tournaments or championships as referred in the mega notificationAre presently also exempted vide Notification no 30/2010 ST dated 22nd June, 2010 w.e.f. 1st July, 2010

26th October,201244

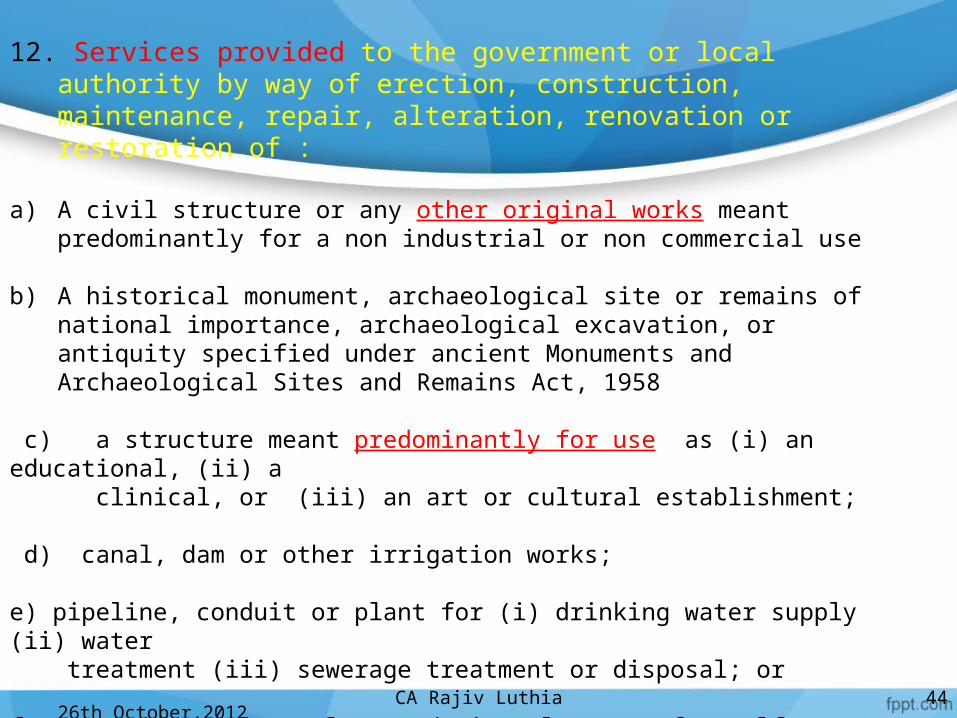

12. Services provided to the government or local authority by way of erection, construction, maintenance, repair, alteration, renovation or restoration of :

a) A civil structure or any other original works meant predominantly for a non industrial or non commercial use

b) A historical monument, archaeological site or remains of national importance, archaeological excavation, or antiquity specified under ancient Monuments and Archaeological Sites and Remains Act, 1958

c) a structure meant predominantly for use as (i) an educational, (ii) a clinical, or (iii) an art or cultural establishment; d) canal, dam or other irrigation works;

e) pipeline, conduit or plant for (i) drinking water supply (ii) water treatment (iii) sewerage treatment or disposal; or f) a residential complex predominantly meant for self-use or the use of their employees or other persons specified in the Explanation 1 to clause 44 of section 65 B of the said Finance Act

CA Rajiv Luthia

26th October,2012 45

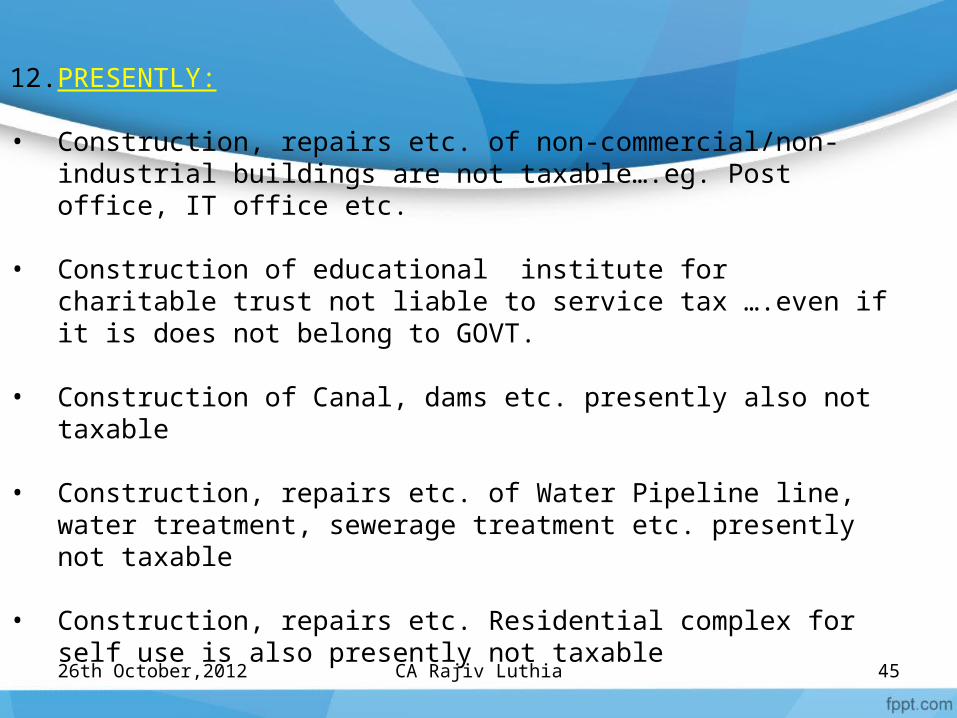

12.PRESENTLY:

• Construction, repairs etc. of non-commercial/non-industrial buildings are not taxable….eg. Post office, IT office etc.

• Construction of educational institute for charitable trust not liable to

service tax ….even if it is does not belong to GOVT.

• Construction of Canal, dams etc. presently also not taxable

• Construction, repairs etc. of Water Pipeline line, water treatment, sewerage treatment etc. presently not taxable

• Construction, repairs etc. Residential complex for self use is also presently not taxable

CA Rajiv Luthia

26th October,2012 46

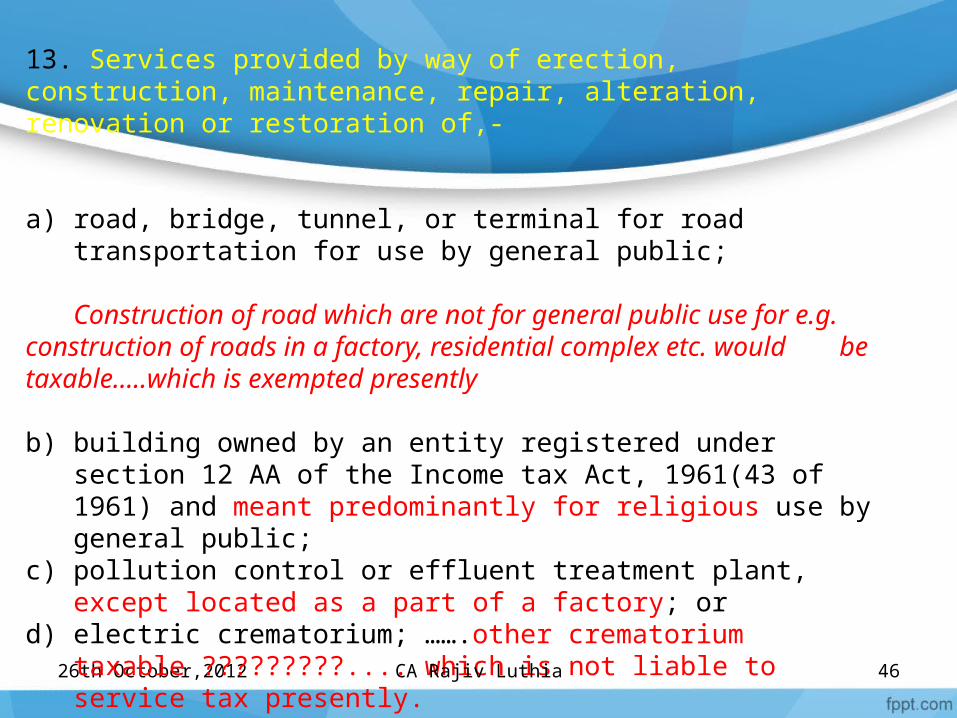

13. Services provided by way of erection, construction, maintenance, repair, alteration, renovation or restoration of,-

a) road, bridge, tunnel, or terminal for road transportation for use by general public;

Construction of road which are not for general public use for e.g. construction of roads in a factory, residential complex etc. would

be taxable…..which is exempted presently b) building owned by an entity registered under section 12 AA of the

Income tax Act, 1961(43 of 1961) and meant predominantly for religious use by general public;

c) pollution control or effluent treatment plant, except located as a part of a factory; or

d) electric crematorium; …….other crematorium taxable ?????????.... which is not liable to service tax presently.

CA Rajiv Luthia

26th October,2012 47

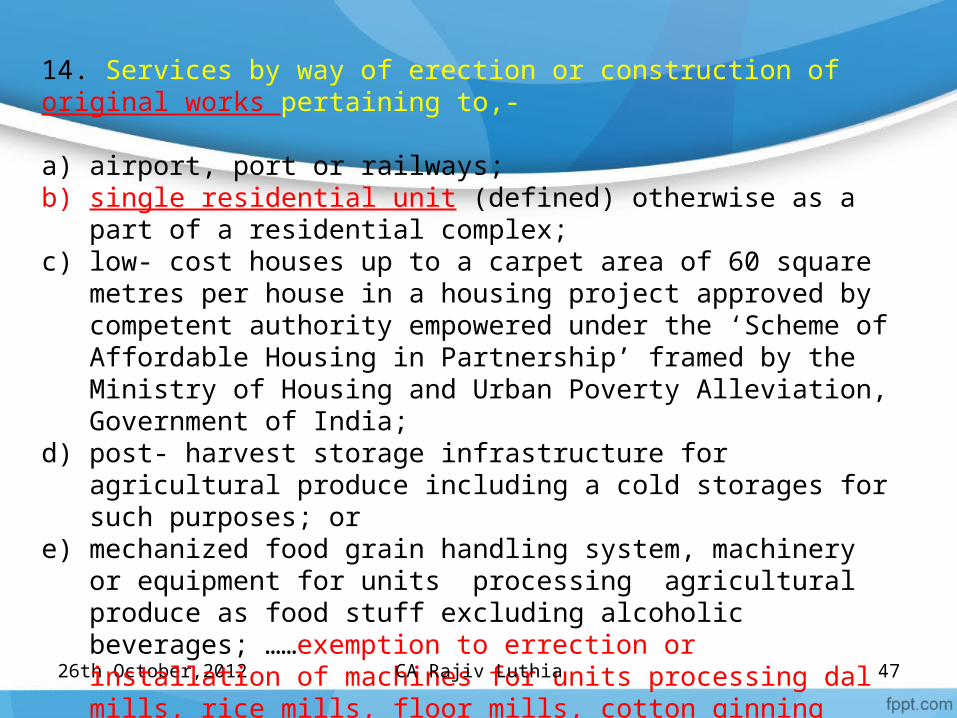

14. Services by way of erection or construction of original works pertaining to,- a) airport, port or railways; b) single residential unit (defined) otherwise as a part of a residential

complex;c) low- cost houses up to a carpet area of 60 square metres per house

in a housing project approved by competent authority empowered under the ‘Scheme of Affordable Housing in Partnership’ framed by the Ministry of Housing and Urban Poverty Alleviation, Government of India;

d) post- harvest storage infrastructure for agricultural produce including a cold storages for such purposes; or

e) mechanized food grain handling system, machinery or equipment for units processing agricultural produce as food stuff excluding alcoholic beverages; ……exemption to errection or installation of machines for units processing dal mills, rice mills, floor mills, cotton ginning mills……presently exempted under notification 12/2010

CA Rajiv Luthia

48

EXEMPTIONS UNDER MEGA NOTIFICATION

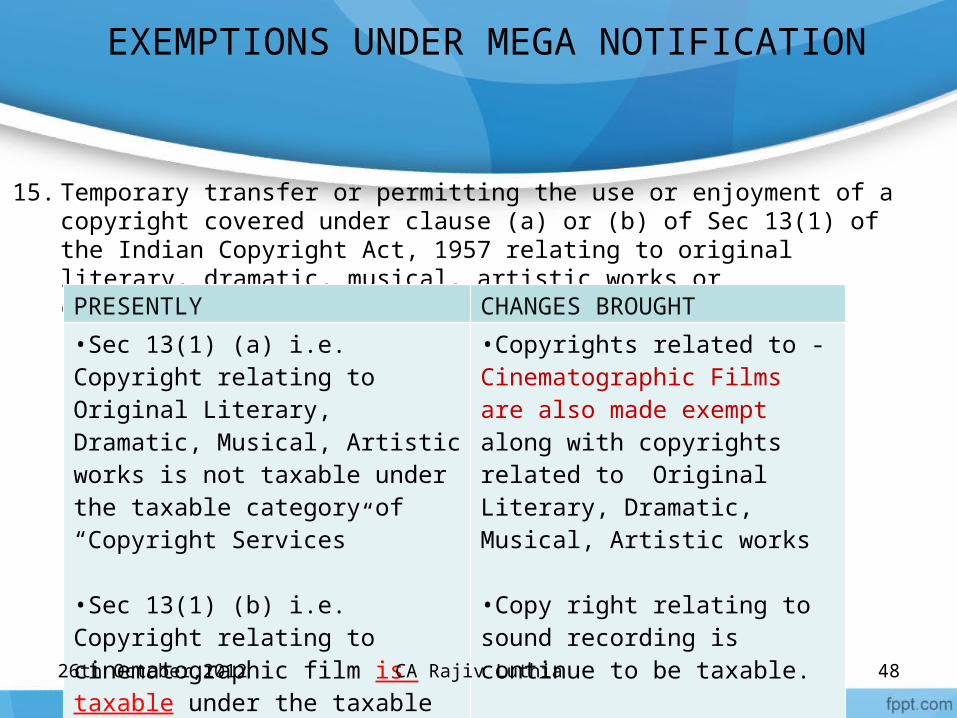

15. Temporary transfer or permitting the use or enjoyment of a copyright covered under clause (a) or (b) of Sec 13(1) of the Indian Copyright Act, 1957 relating to original literary, dramatic, musical, artistic works or cinematographic films

PRESENTLY CHANGES BROUGHT

•Sec 13(1) (a) i.e. Copyright relating to Original Literary, Dramatic, Musical, Artistic works is not taxable under the taxable category of “Copyright Services”

•Sec 13(1) (b) i.e. Copyright relating to cinematographic film is taxable under the taxable category of “Copyright Services”

•Copyrights related to -Cinematographic Films are also made exempt along with copyrights related to Original Literary, Dramatic, Musical, Artistic works

•Copy right relating to sound recording is continue to be taxable.

26th October,2012 CA Rajiv Luthia

26th October,2012 49

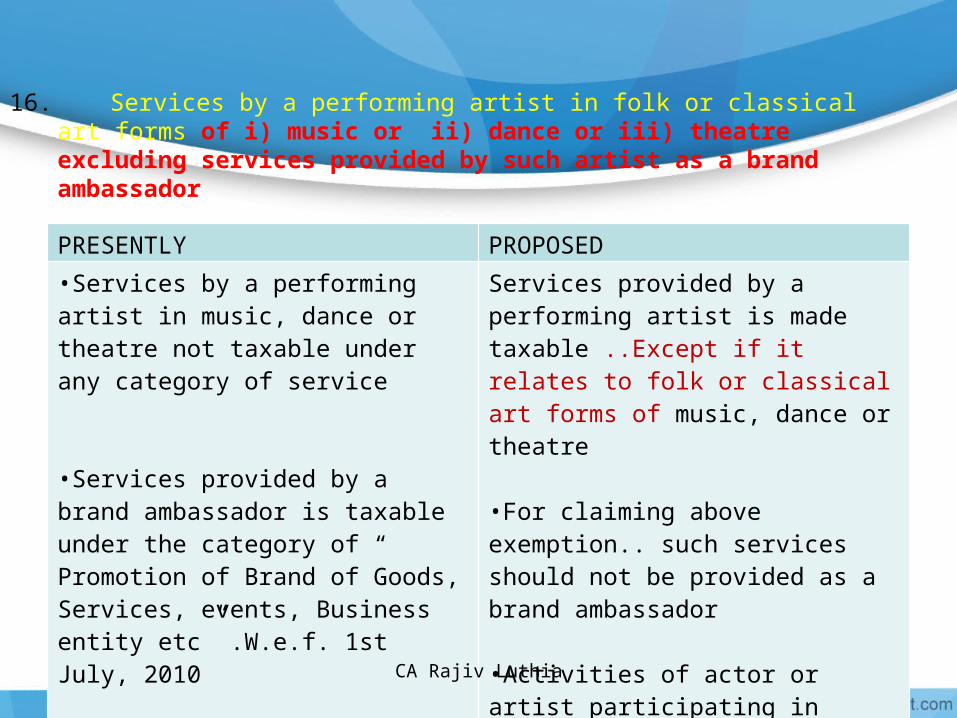

16. Services by a performing artist in folk or classical art forms of i) music or ii) dance or iii) theatre excluding services provided by such artist as a brand ambassador

PRESENTLY PROPOSED

•Services by a performing artist in music, dance or theatre not taxable under any category of service

•Services provided by a brand ambassador is taxable under the category of “ Promotion of Brand of Goods, Services, events, Business entity etc” .W.e.f. 1st July, 2010

Services provided by a performing artist is made taxable ..Except if it relates to folk or classical art forms of music, dance or theatre

•For claiming above exemption.. such services should not be provided as a brand ambassador

•Activities of actor or artist participating in magic show, mimicry, film, TV serial are proposed to be taxable .

CA Rajiv Luthia

26th October,2012 50

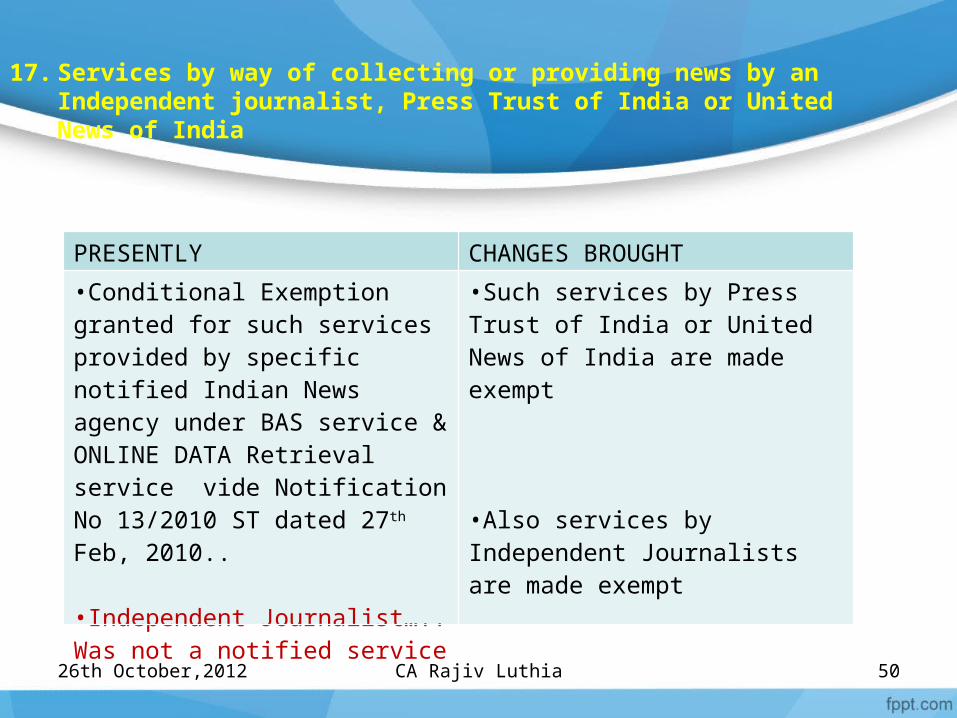

17. Services by way of collecting or providing news by an Independent journalist, Press Trust of India or United News of India

PRESENTLY CHANGES BROUGHT

•Conditional Exemption granted for such services provided by specific notified Indian News agency under BAS service & ONLINE DATA Retrieval service vide Notification No 13/2010 ST dated 27th Feb, 2010..

•Independent Journalist….. Was not a notified service

•Such services by Press Trust of India or United News of India are made exempt

•Also services by Independent Journalists are made exempt

CA Rajiv Luthia

26th October,2012 51

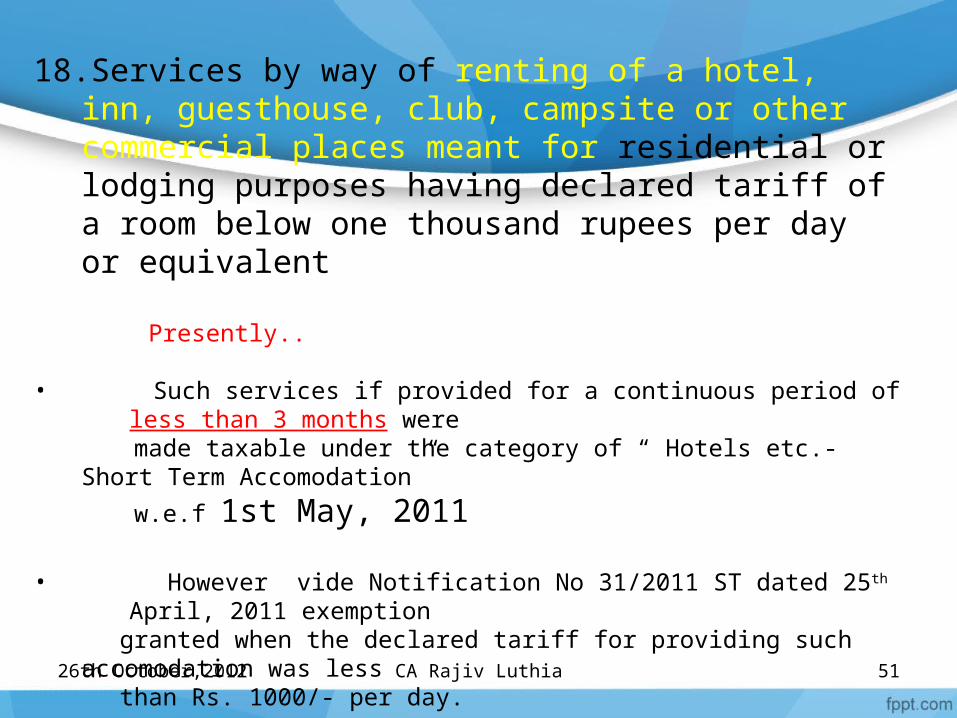

18.Services by way of renting of a hotel, inn, guesthouse, club, campsite or other commercial places meant for residential or lodging purposes having declared tariff of a room below one thousand rupees per day or equivalent

Presently.. • Such services if provided for a continuous period of less than 3 months

were made taxable under the category of “ Hotels etc.-Short Term Accomodation”

w.e.f 1st May, 2011

• However vide Notification No 31/2011 ST dated 25th April, 2011 exemption

granted when the declared tariff for providing such accomodation was less than Rs. 1000/- per day.

CA Rajiv Luthia

26th October,2012 52

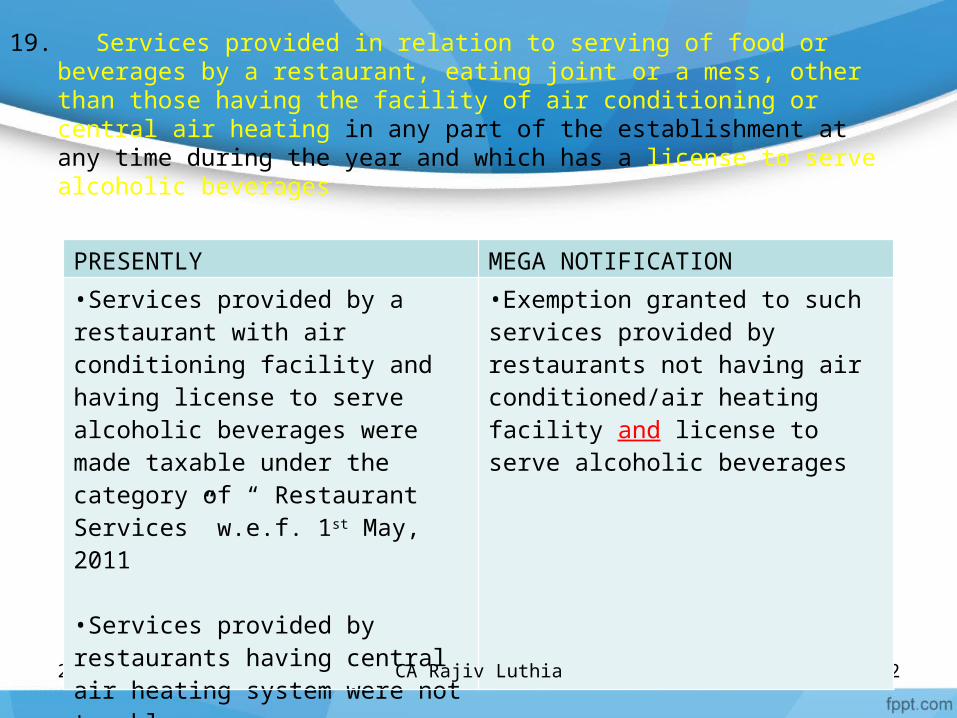

19. Services provided in relation to serving of food or beverages by a restaurant, eating joint or a mess, other than those having the facility of air conditioning or central air heating in any part of the establishment at any time during the year and which has a license to serve alcoholic beverages

PRESENTLY MEGA NOTIFICATION

•Services provided by a restaurant with air conditioning facility and having license to serve alcoholic beverages were made taxable under the category of “ Restaurant Services” w.e.f. 1st May, 2011 •Services provided by restaurants having central air heating system were not taxable

•Exemption granted to such services provided by restaurants not having air conditioned/air heating facility and license to serve alcoholic beverages

CA Rajiv Luthia

26th October,2012 53

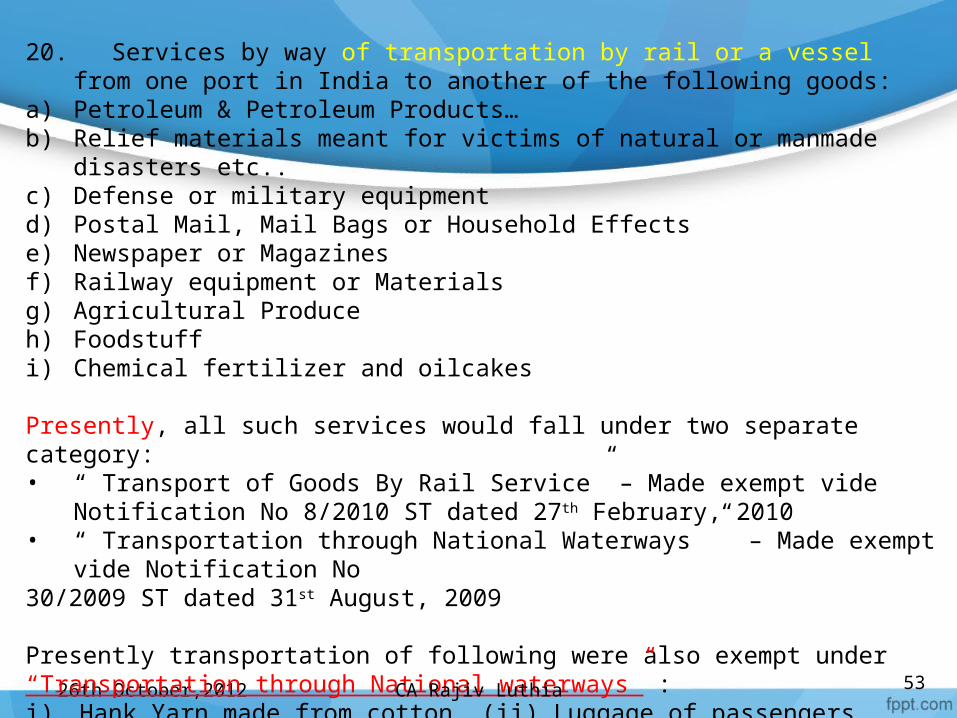

20. Services by way of transportation by rail or a vessel from one port in India to another of the following goods:

a) Petroleum & Petroleum Products…b) Relief materials meant for victims of natural or manmade disasters etc..c) Defense or military equipmentd) Postal Mail, Mail Bags or Household Effectse) Newspaper or Magazines f) Railway equipment or Materialsg) Agricultural Produceh) Foodstuffi) Chemical fertilizer and oilcakes

Presently, all such services would fall under two separate category: • “ Transport of Goods By Rail Service” – Made exempt vide Notification No 8/2010

ST dated 27th February, 2010• “ Transportation through National Waterways ” – Made exempt vide Notification

No30/2009 ST dated 31st August, 2009

Presently transportation of following were also exempt under “Transportation through National waterways” :i) Hank Yarn made from cotton, (ii) Luggage of passengers (iii) Raw Jute & Jute

Textiles CA Rajiv Luthia

26th October,2012 54

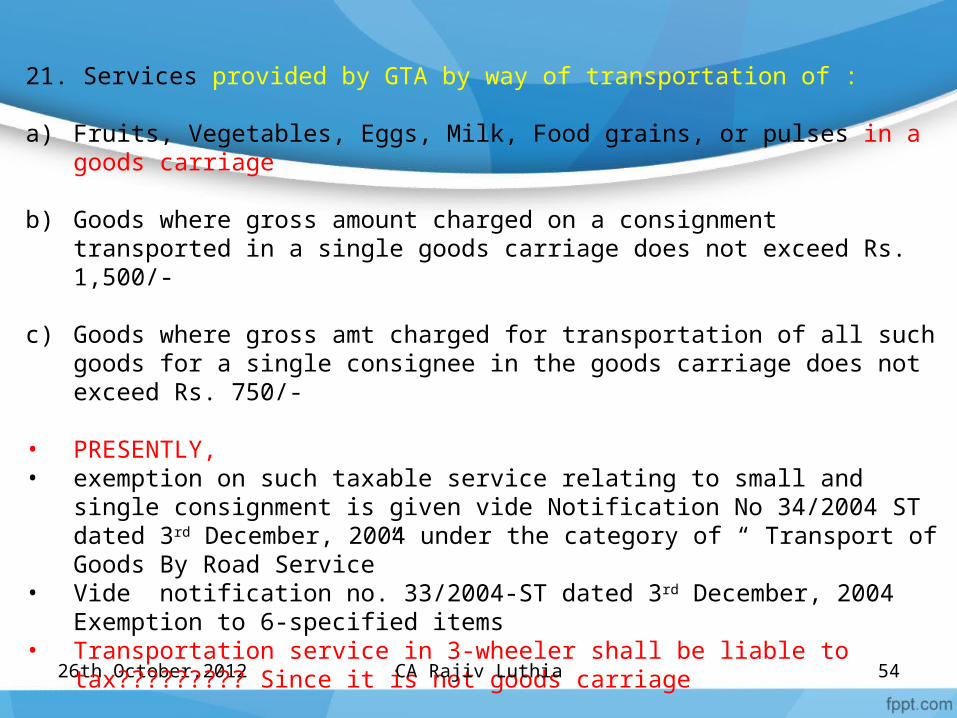

21. Services provided by GTA by way of transportation of :

a) Fruits, Vegetables, Eggs, Milk, Food grains, or pulses in a goods carriage

b) Goods where gross amount charged on a consignment transported in a single goods carriage does not exceed Rs. 1,500/-

c) Goods where gross amt charged for transportation of all such goods for a single consignee in the goods carriage does not exceed Rs. 750/-

• PRESENTLY, • exemption on such taxable service relating to small and single consignment is

given vide Notification No 34/2004 ST dated 3rd December, 2004 under the category of “ Transport of Goods By Road Service”

• Vide notification no. 33/2004-ST dated 3rd December, 2004 Exemption to 6-specified items

• Transportation service in 3-wheeler shall be liable to tax????????? Since it is not goods carriage

CA Rajiv Luthia

26th October,2012 55

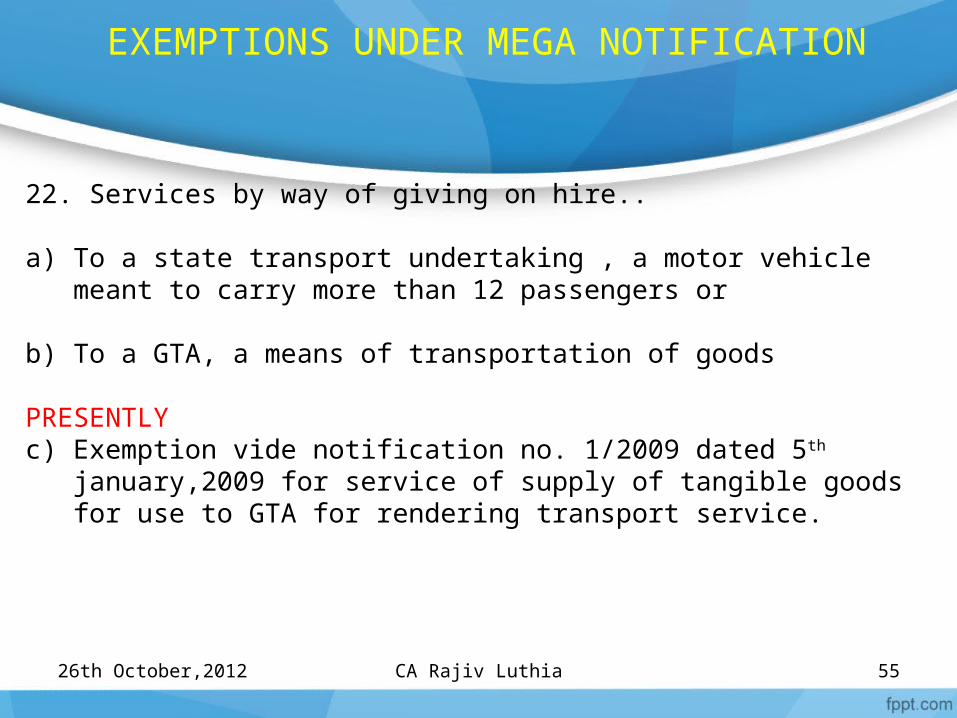

EXEMPTIONS UNDER MEGA NOTIFICATION

22. Services by way of giving on hire..

a) To a state transport undertaking , a motor vehicle meant to carry more than 12 passengers or

b) To a GTA, a means of transportation of goods

PRESENTLYc) Exemption vide notification no. 1/2009 dated 5th january,2009 for service

of supply of tangible goods for use to GTA for rendering transport service.

CA Rajiv Luthia

26th October,2012 56

EXEMPTIONS UNDER MEGA NOTIFICATION

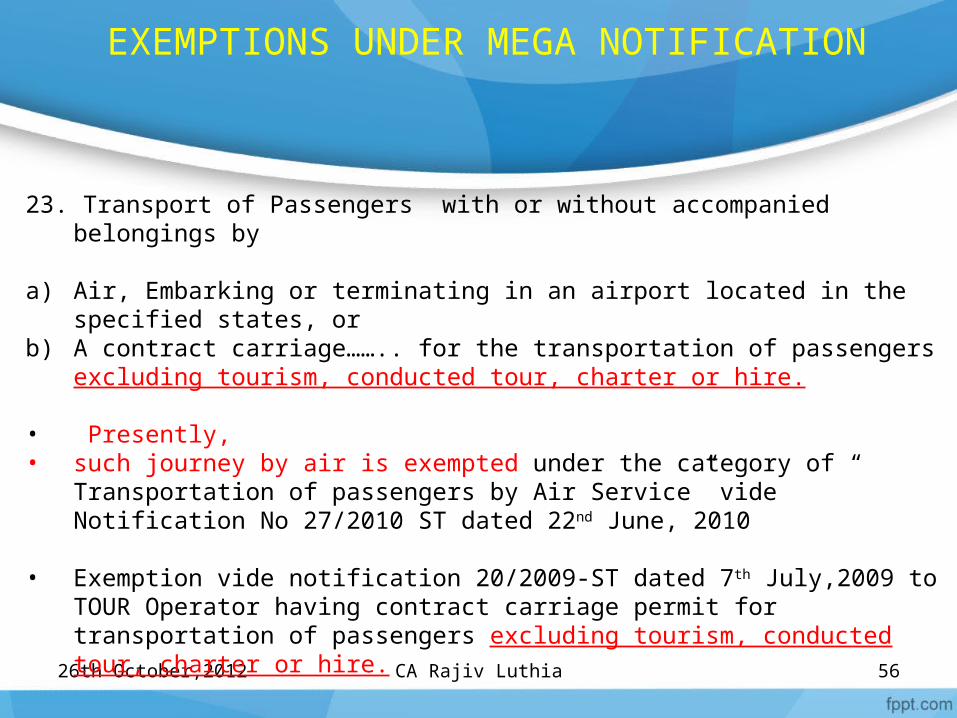

23. Transport of Passengers with or without accompanied belongings by

a) Air, Embarking or terminating in an airport located in the specified states, orb) A contract carriage…….. for the transportation of passengers excluding tourism,

conducted tour, charter or hire.

• Presently, • such journey by air is exempted under the category of “ Transportation of

passengers by Air Service” vide Notification No 27/2010 ST dated 22nd June, 2010

• Exemption vide notification 20/2009-ST dated 7th July,2009 to TOUR Operator having contract carriage permit for transportation of passengers excluding tourism, conducted tour, charter or hire.

CA Rajiv Luthia

26th October,2012 57

EXEMPTIONS UNDER MEGA NOTIFICATION

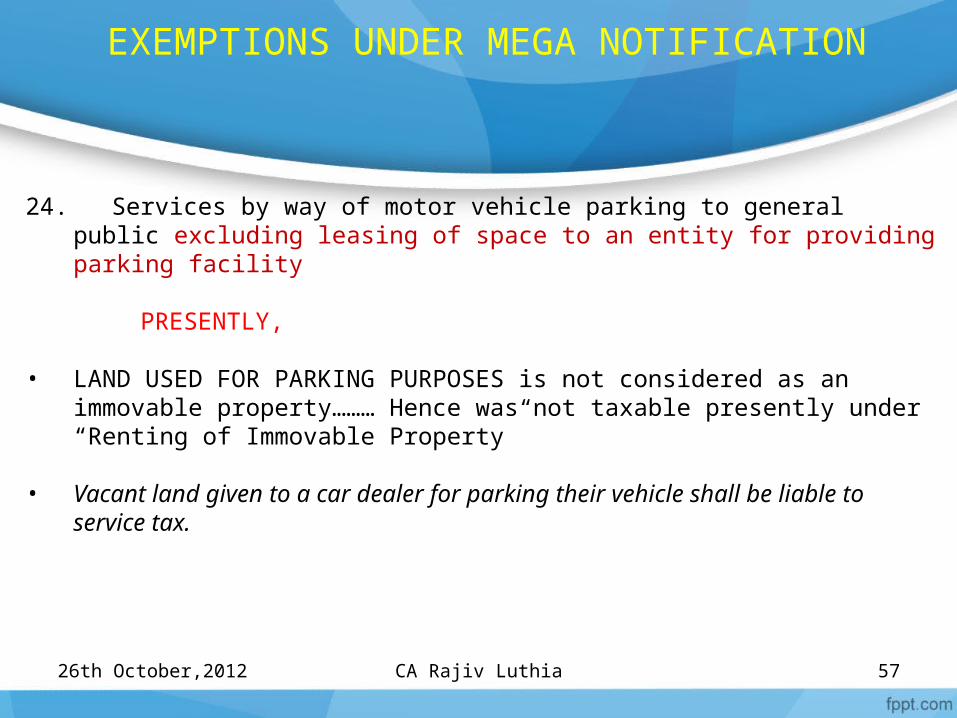

24. Services by way of motor vehicle parking to general public excluding leasing of space to an entity for providing parking facility

PRESENTLY,

• LAND USED FOR PARKING PURPOSES is not considered as an immovable property……… Hence was not taxable presently under “Renting of Immovable Property”

• Vacant land given to a car dealer for parking their vehicle shall be liable to service tax.

CA Rajiv Luthia

26th October,2012 58

EXEMPTIONS UNDER MEGA NOTIFICATION

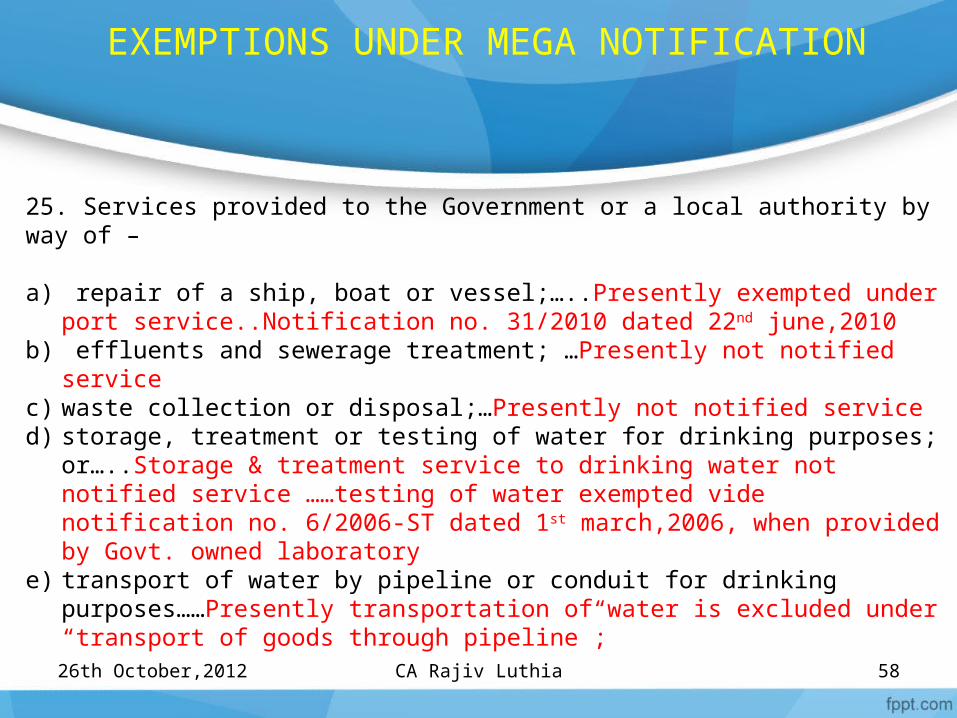

25. Services provided to the Government or a local authority by way of – a) repair of a ship, boat or vessel;…..Presently exempted under port

service..Notification no. 31/2010 dated 22nd june,2010b) effluents and sewerage treatment; …Presently not notified servicec) waste collection or disposal;…Presently not notified service d) storage, treatment or testing of water for drinking purposes; or…..Storage &

treatment service to drinking water not notified service ……testing of water exempted vide notification no. 6/2006-ST dated 1st march,2006, when provided by Govt. owned laboratory

e) transport of water by pipeline or conduit for drinking purposes……Presently transportation of water is excluded under “transport of goods through pipeline”;

CA Rajiv Luthia

26th October,2012 59

EXEMPTIONS UNDER MEGA NOTIFICATION

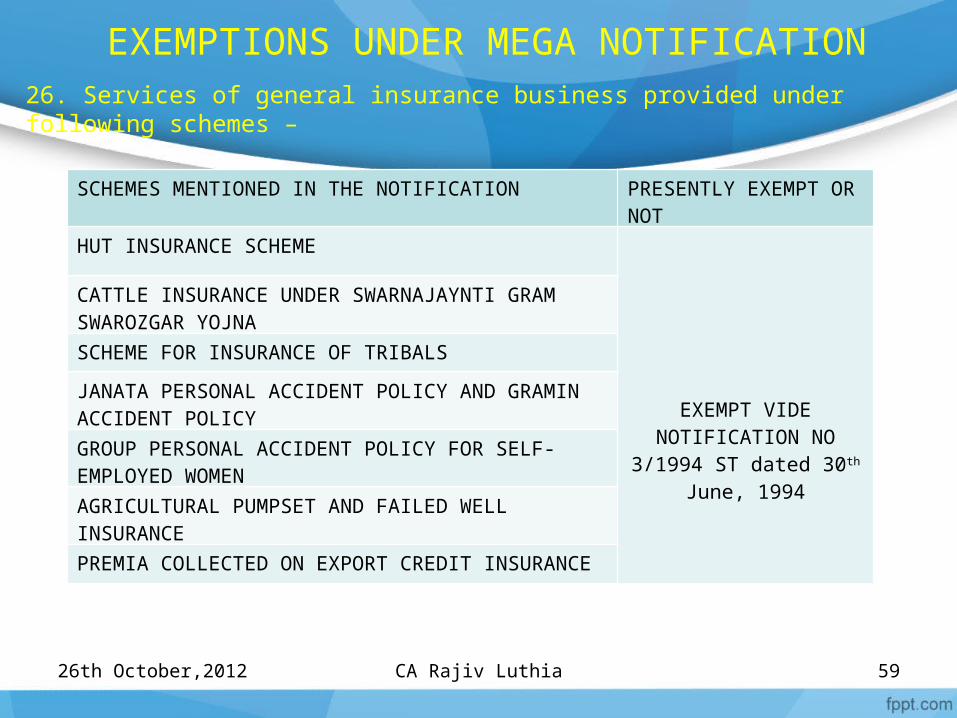

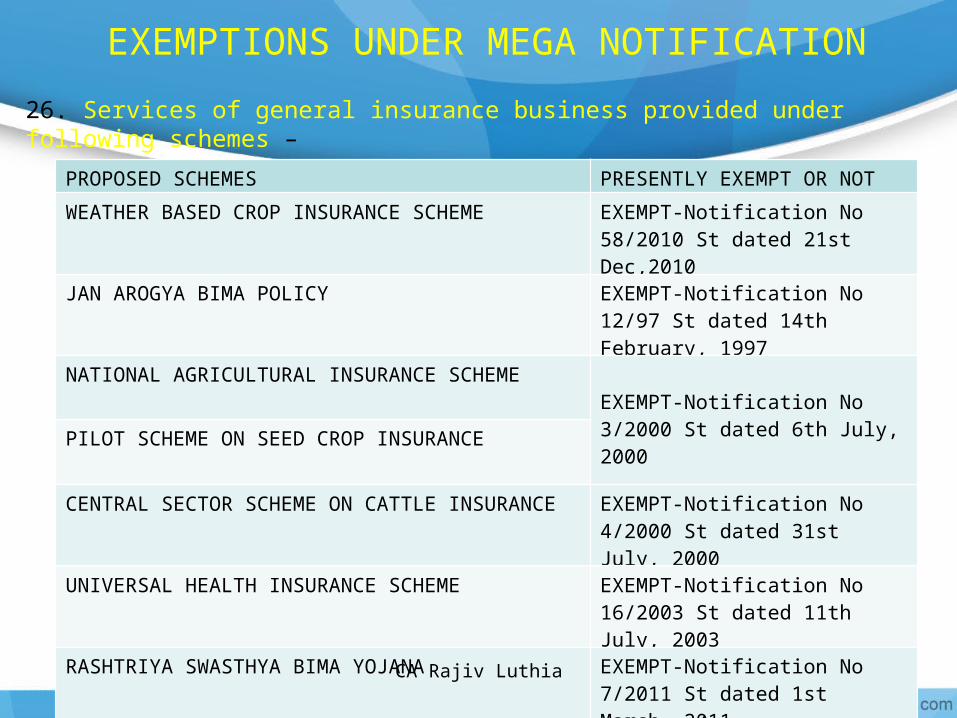

26. Services of general insurance business provided under following schemes –

SCHEMES MENTIONED IN THE NOTIFICATION PRESENTLY EXEMPT OR NOT

HUT INSURANCE SCHEME

EXEMPT VIDE NOTIFICATION NO 3/1994 ST dated 30th

June, 1994

CATTLE INSURANCE UNDER SWARNAJAYNTI GRAM SWAROZGAR YOJNA

SCHEME FOR INSURANCE OF TRIBALS

JANATA PERSONAL ACCIDENT POLICY AND GRAMIN ACCIDENT POLICY

GROUP PERSONAL ACCIDENT POLICY FOR SELF-EMPLOYED WOMEN

AGRICULTURAL PUMPSET AND FAILED WELL INSURANCE

PREMIA COLLECTED ON EXPORT CREDIT INSURANCE

CA Rajiv Luthia

26th October,2012 60

EXEMPTIONS UNDER MEGA NOTIFICATION

26. Services of general insurance business provided under following schemes –

PROPOSED SCHEMES PRESENTLY EXEMPT OR NOT

WEATHER BASED CROP INSURANCE SCHEME EXEMPT-Notification No 58/2010 St dated 21st Dec,2010

JAN AROGYA BIMA POLICY EXEMPT-Notification No 12/97 St dated 14th February, 1997

NATIONAL AGRICULTURAL INSURANCE SCHEME EXEMPT-Notification No 3/2000 St dated 6th July, 2000

PILOT SCHEME ON SEED CROP INSURANCE

CENTRAL SECTOR SCHEME ON CATTLE INSURANCE EXEMPT-Notification No 4/2000 St dated 31st July, 2000

UNIVERSAL HEALTH INSURANCE SCHEME EXEMPT-Notification No 16/2003 St dated 11th July, 2003

RASHTRIYA SWASTHYA BIMA YOJANA EXEMPT-Notification No 7/2011 St dated 1st March, 2011

COCONUT PALM INSURANCE SCHEME NOT EXEMPT

CA Rajiv Luthia

26th October,2012 61

EXEMPTIONS UNDER MEGA NOTIFICATION

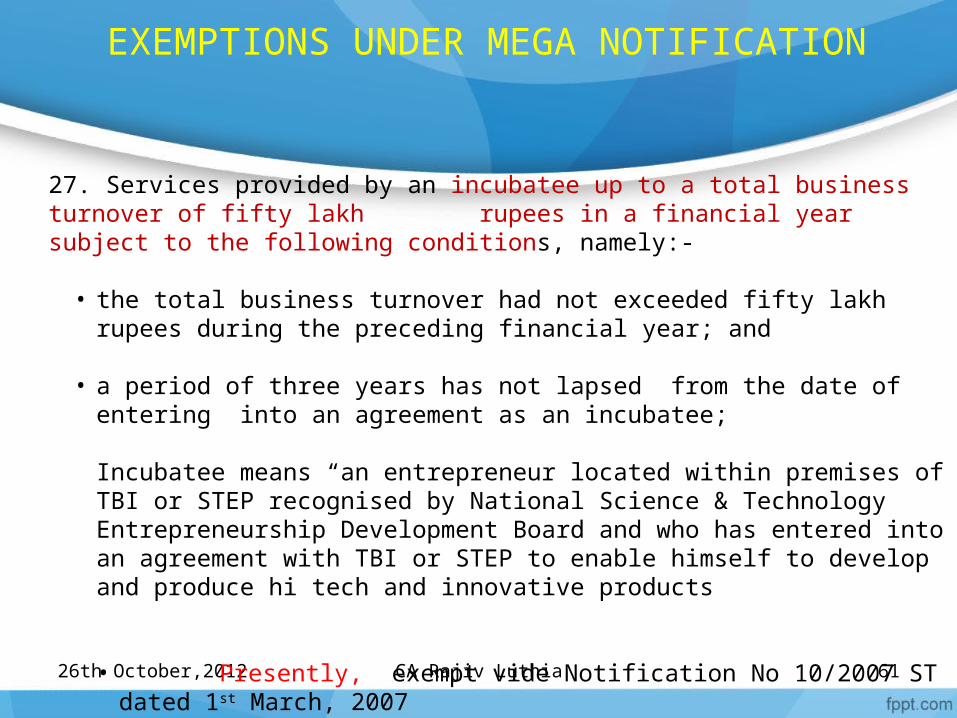

27. Services provided by an incubatee up to a total business turnover of fifty lakh rupees in a financial year subject to the following conditions, namely:-

• the total business turnover had not exceeded fifty lakh rupees during the preceding financial year; and

• a period of three years has not lapsed from the date of entering into an agreement as an incubatee;

Incubatee means “an entrepreneur located within premises of TBI or STEP recognised by National Science & Technology Entrepreneurship Development Board and who has entered into an agreement with TBI or STEP to enable himself to develop and produce hi tech and innovative products

• Presently, exempt vide Notification No 10/2007 ST dated 1st March, 2007

CA Rajiv Luthia

26th October,2012 62

EXEMPTIONS UNDER MEGA NOTIFICATION

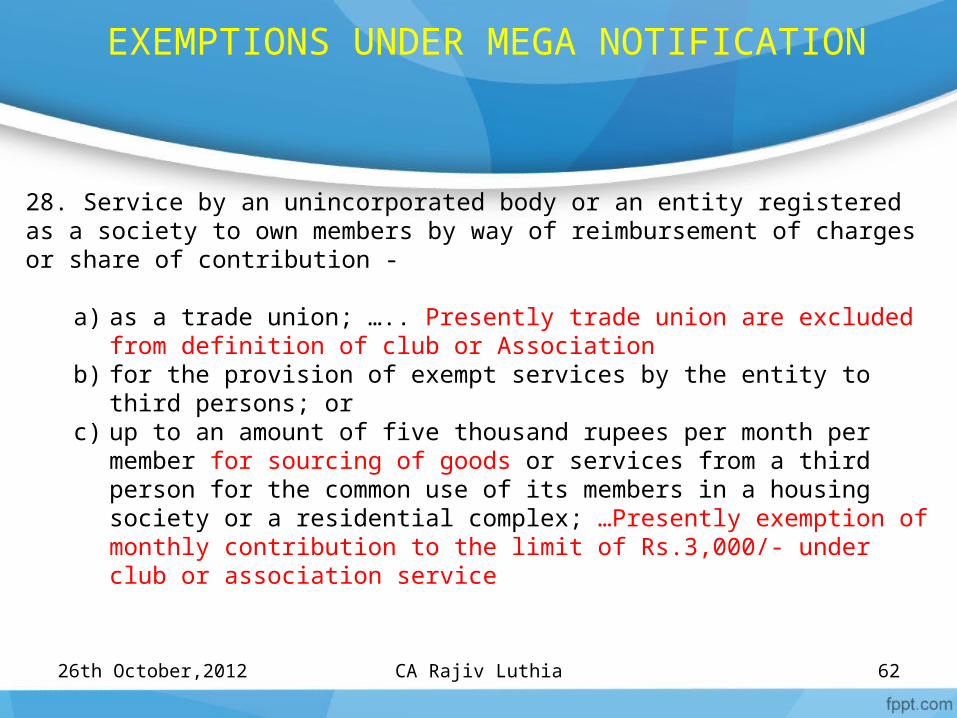

28. Service by an unincorporated body or an entity registered as a society to own members by way of reimbursement of charges or share of contribution -

a) as a trade union; ….. Presently trade union are excluded from definition of club or Association

b) for the provision of exempt services by the entity to third persons; or c) up to an amount of five thousand rupees per month per member for sourcing

of goods or services from a third person for the common use of its members in a housing society or a residential complex; …Presently exemption of monthly contribution to the limit of Rs.3,000/- under club or association service

CA Rajiv Luthia

26th October,2012 63

EXEMPTIONS UNDER MEGA NOTIFICATION

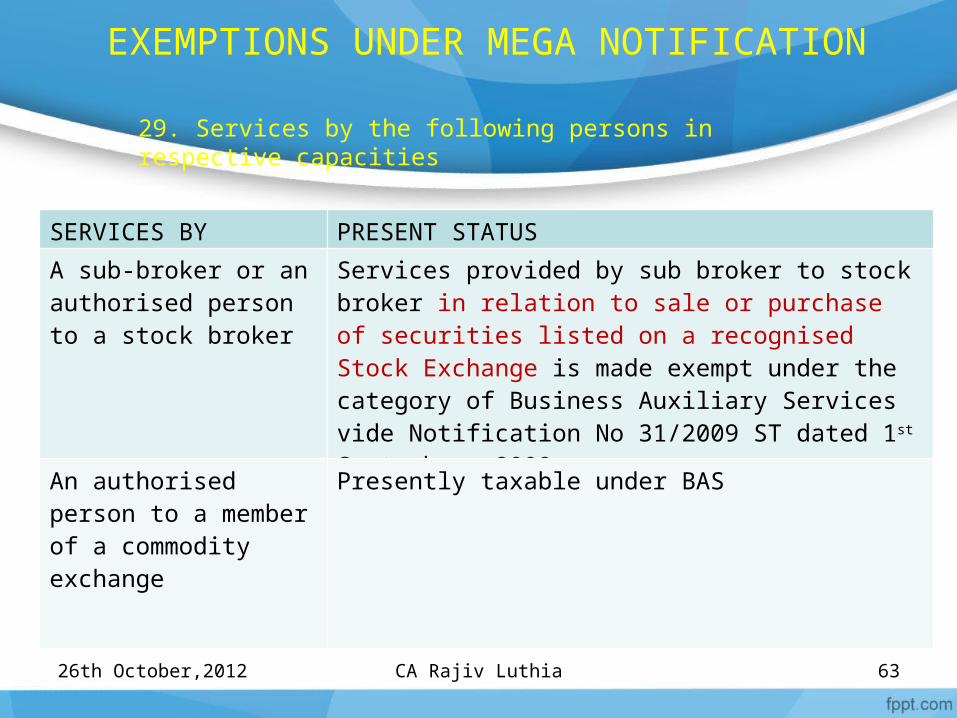

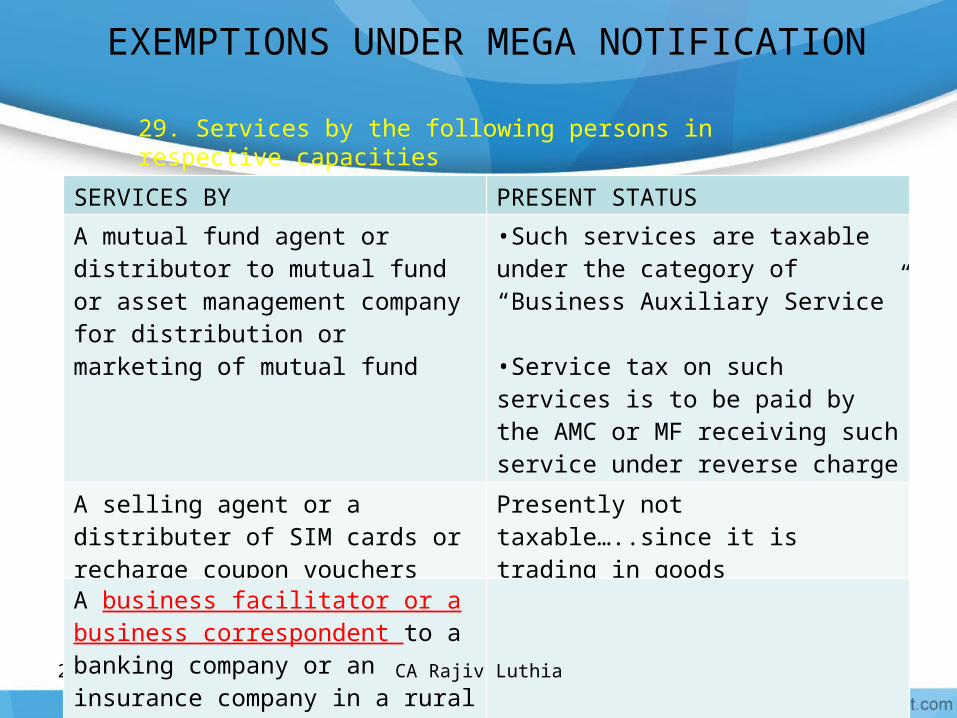

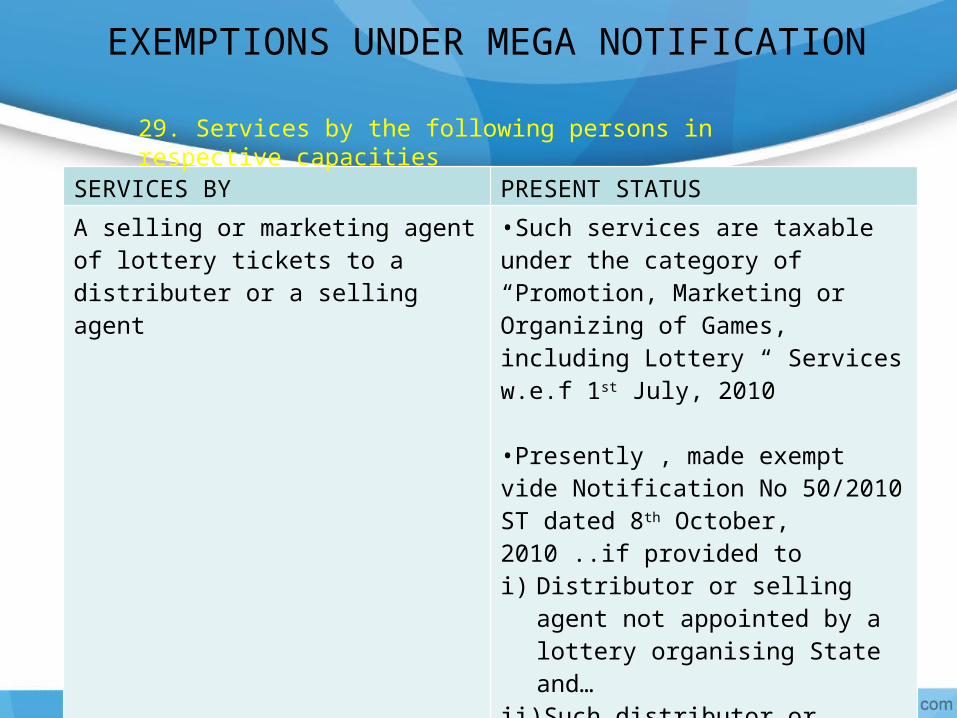

29. Services by the following persons in respective capacities

SERVICES BY PRESENT STATUS

A sub-broker or an authorised person to a stock broker

Services provided by sub broker to stock broker in relation to sale or purchase of securities listed on a recognised Stock Exchange is made exempt under the category of Business Auxiliary Services vide Notification No 31/2009 ST dated 1st September, 2009

An authorised person to a member of a commodity exchange

Presently taxable under BAS

CA Rajiv Luthia

26th October,2012 64

EXEMPTIONS UNDER MEGA NOTIFICATION

SERVICES BY PRESENT STATUS

A mutual fund agent or distributor to mutual fund or asset management company for distribution or marketing of mutual fund

•Such services are taxable under the category of “Business Auxiliary Service”

•Service tax on such services is to be paid by the AMC or MF receiving such service under reverse charge mechanism

A selling agent or a distributer of SIM cards or recharge coupon vouchers

Presently not taxable…..since it is trading in goods

A business facilitator or a business correspondent to a banking company or an insurance company in a rural area

29. Services by the following persons in respective capacities

CA Rajiv Luthia

65

EXEMPTIONS UNDER MEGA NOTIFICATION

SERVICES BY PRESENT STATUS

A selling or marketing agent of lottery tickets to a distributer or a selling agent

•Such services are taxable under the category of “Promotion, Marketing or Organizing of Games, including Lottery “ Services w.e.f 1st July, 2010

•Presently , made exempt vide Notification No 50/2010 ST dated 8th October, 2010 ..if provided to i) Distributor or selling agent not

appointed by a lottery organising State and…

ii) Such distributor or selling agent has availed benefit of optional composition scheme as provided in Rule 6 (7C) of the Service tax Rules

29. Services by the following persons in respective capacities

EXEMPTIONS UNDER MEGA NOTIFICATION

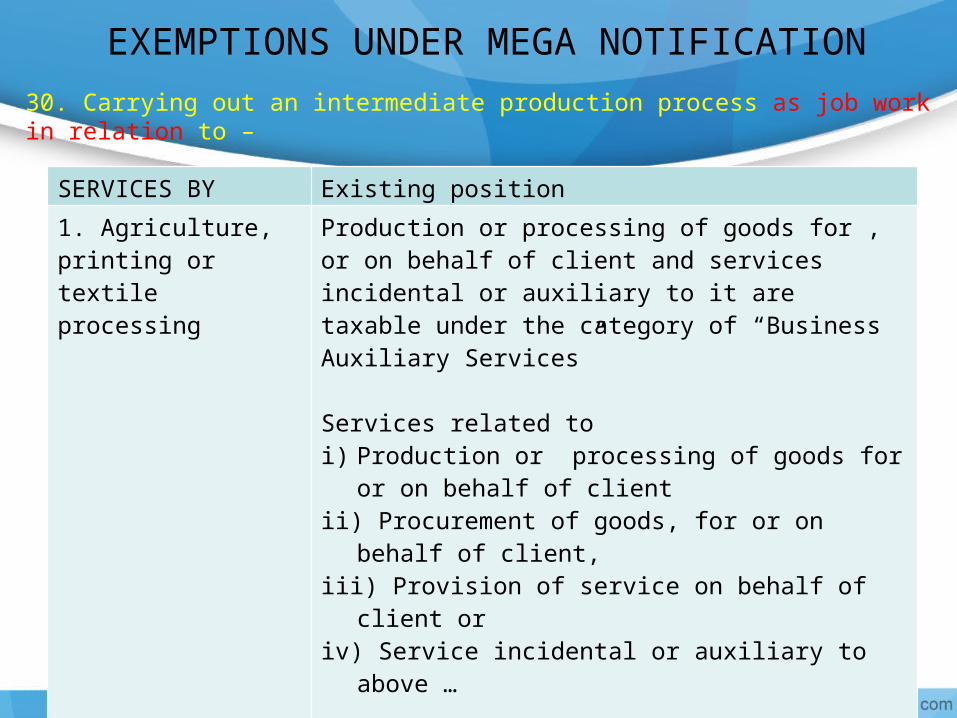

30. Carrying out an intermediate production process as job work in relation to –

SERVICES BY Existing position

1. Agriculture, printing or textile processing

Production or processing of goods for , or on behalf of client and services incidental or auxiliary to it are taxable under the category of “Business Auxiliary Services”

Services related to i) Production or processing of goods for or on behalf

of clientii) Procurement of goods, for or on behalf of client, iii) Provision of service on behalf of client or iv) Service incidental or auxiliary to above … if provided in relation to agriculture, printing, textile

processing or education made exempt under the category of BAS vide Notification No 14/2004 ST dated 10th September, 2004

26th October,2012 67

EXEMPTIONS UNDER MEGA NOTIFICATION

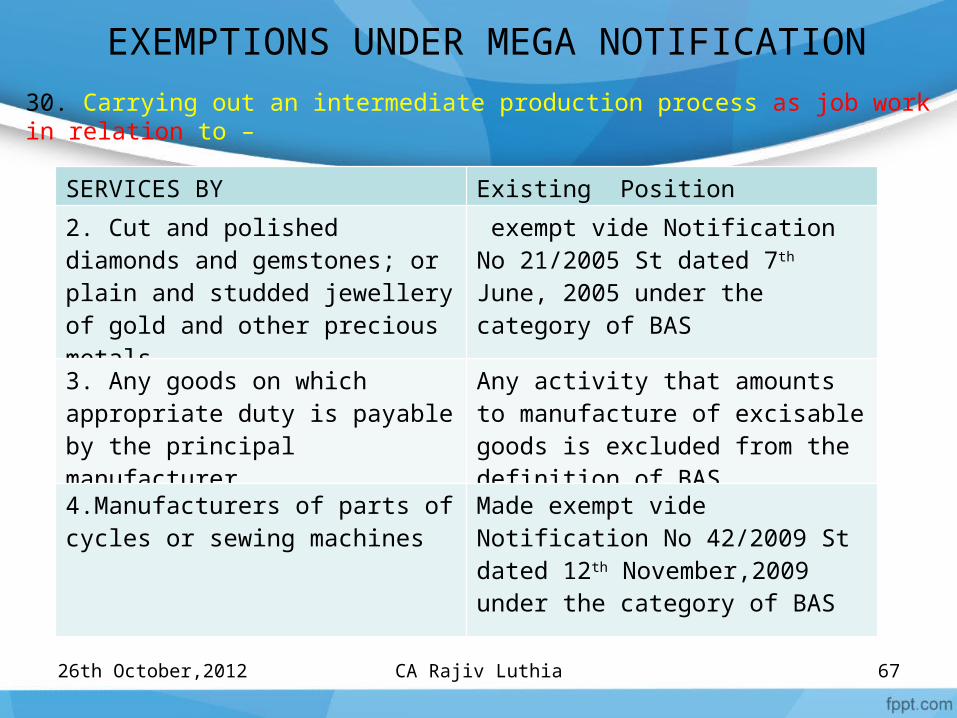

30. Carrying out an intermediate production process as job work in relation to –

SERVICES BY Existing Position

2. Cut and polished diamonds and gemstones; or plain and studded jewellery of gold and other precious metals

exempt vide Notification No 21/2005 St dated 7th June, 2005 under the category of BAS

3. Any goods on which appropriate duty is payable by the principal manufacturer

Any activity that amounts to manufacture of excisable goods is excluded from the definition of BAS

4.Manufacturers of parts of cycles or sewing machines

Made exempt vide Notification No 42/2009 St dated 12th November,2009 under the category of BAS

CA Rajiv Luthia

26th October,2012 68

EXEMPTIONS UNDER MEGA NOTIFICATION

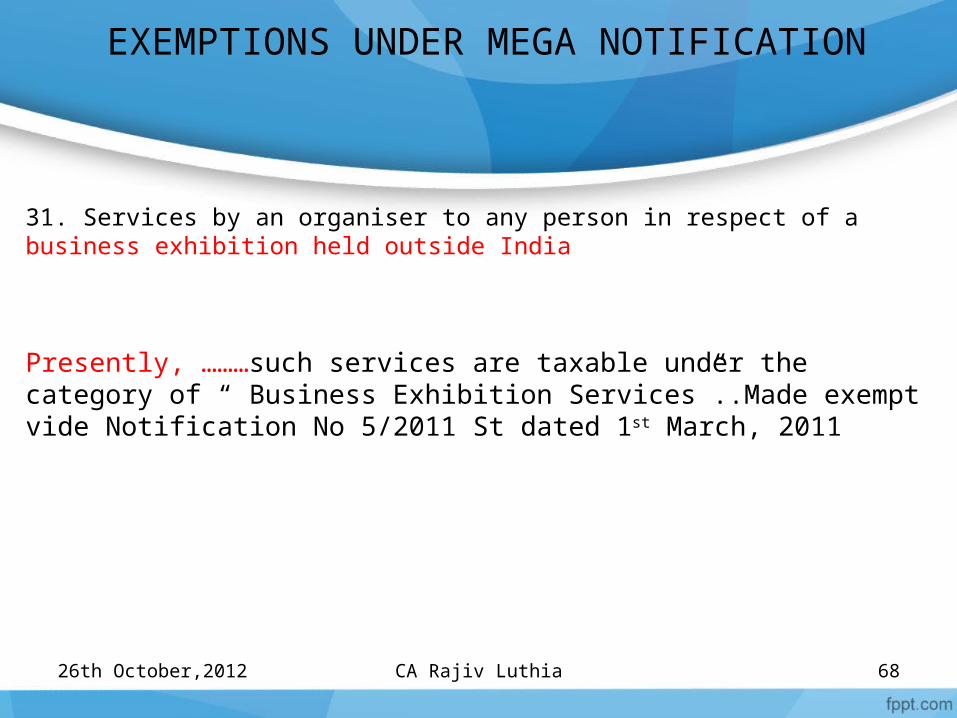

31. Services by an organiser to any person in respect of a business exhibition held outside India

Presently, ………such services are taxable under the category of “ Business Exhibition Services”..Made exempt vide Notification No 5/2011 St dated 1st March, 2011

CA Rajiv Luthia

26th October,2012 69

EXEMPTIONS UNDER MEGA NOTIFICATION

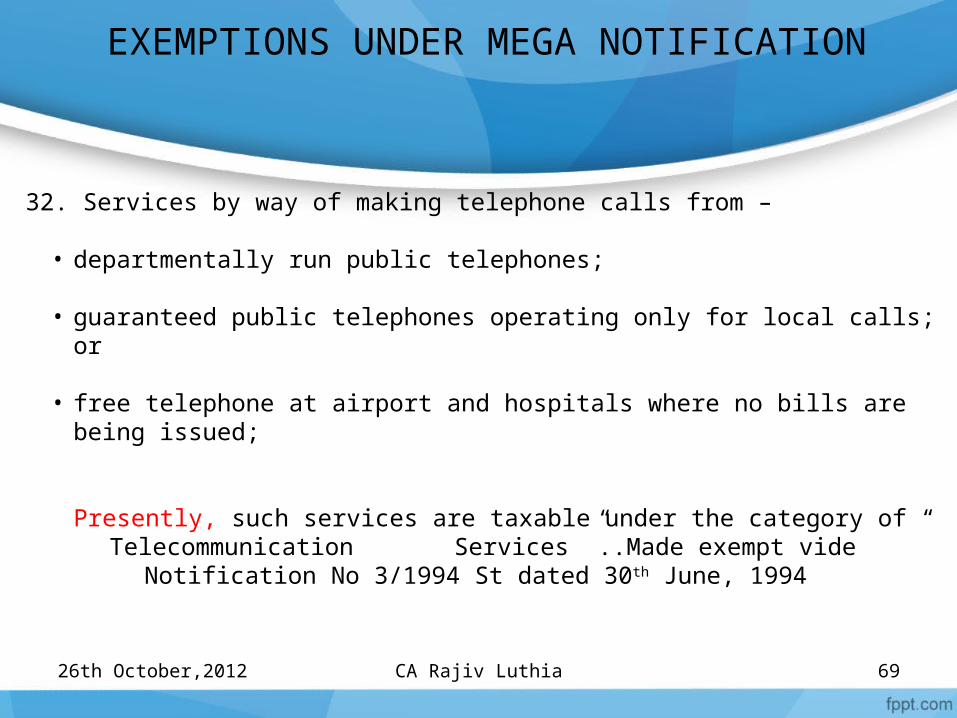

32. Services by way of making telephone calls from –

• departmentally run public telephones;

• guaranteed public telephones operating only for local calls; or

• free telephone at airport and hospitals where no bills are being issued;

Presently, such services are taxable under the category of “ Telecommunication Services ”..Made exempt vide Notification No 3/1994 St dated 30th June, 1994

CA Rajiv Luthia

26th October,2012 70

EXEMPTIONS UNDER MEGA NOTIFICATION

33. Services by way of slaughtering of animals

Were made taxable w.e.f. 16th October, 1998 under the category of “Mechanised Slaughter House”

Exemption provided to taxable service provided by a mechanised slaughter house from so much of the service tax leviable on such slaughter house as is in excess of Rs. 100/- per bovine animal vide Notification No 58/1998 ST dated 7th October, 1998

Exemption to slaughter house from the whole of service tax vide Notification No 2/2000- St dated 1st March,2000

CA Rajiv Luthia

26th October,2012 71

EXEMPTIONS UNDER MEGA NOTIFICATION

34. Services received from a service provider located in a non- taxable territory by -

• the Government, a local authority or an individual in relation to any purpose other than industry, business or commerce; or

• an entity registered under section 12AA of the Income tax Act, 1961 (43 of 1961) for the purposes of providing charitable activities….. …..Presently service tax is payable u/s 66A if services are provided from outside india & received by charitable trust in india.

CA Rajiv Luthia

26th October,2012 72

EXEMPTIONS UNDER MEGA NOTIFICATION

35. Services of Public Libraries by way of lending of books, publications or any other knowledge enhancing content or material

36. Services by Employee State Insurance Corporations to persons governed under the Employees Insurance Act, 1948

37. Services by way of transfer of going concern, as a whole or independent part thereof

38. Services by way of public conveniences such as provision of facilities of bathroom, washrooms, lavoratories, urinals or toilets

39. Services by a governmental authority by way of any activity in relation to any function entrusted to a municipality under Article 243W of the Constitiution

CA Rajiv Luthia

Any questions ???????

73

CA. Rajiv LuthiaR.J.Luthia & Associates,

Chartered Accountants610/611, Parmeshwari Centre, Above Galaxy Motors, Dalmia Estate,

Off. LBS Marg, Mulund (West), Mumbai-400 090.

Ph : 2564 1553/2569 4989Email: [email protected]

7426th October,2012 CA Rajiv Luthia