Embed Size (px)

Citation preview

1

WHAT REGULATORS WANT

November 13, 2007

2

Disclaimer

The opinions expressed in this presentation are the opinions of the presenters and should not be construed to represent all situations or options and required actions may vary substantially depending on the domicile. Contact your regulator for additional information.

3

Panel of Regulators

Craig Watanabe, Hawaii

Shanna Lespere, Bermuda

Dean Wickens, Cayman Islands

Jeff Kehler, South Carolina

4

Before You Come To The Regulator

Presented by

Craig Watanabe

5

a. Identify objective of meeting with the regulator

(1) Cordial “Meet & Greet”

(2) General inquiry and consultation

(3) Obtain consensus from Regulator to proceed with formal application process

6

b. Do your homework

(1) Be prepared to talk about the organizers. Proficient understanding and knowledge of parent company / organizers.

(a) Nature and scope of operations, financial position, ownership structure & corporate philosophy

7

(2) Be prepared to talk about proposed captive. Proficient understanding of proposed captive program

(a) Objectives of captive program (short and long term)(b) Organizational structure (c) Operational requirements (including major service providers)(d) Funding approach(e) Insurance/reinsurance program design/structure(f) Timing requirements for implementation

8

c. Retain appropriate professional to coordinate & attend meeting (recommended)

d. Prepare any relevant questions for the regulator

9

Presented by

Shanna Lespere

Getting Your Captive Approved

10

Getting your Captive Approved• Regulating bodies recognize the importance in

ensuring the efficiency and stability in the insurance market -strict conditions governing the formal approval of insurance companies are necessary to protect policy holders

• Review of the insurance application, acceptability of proposed business and ongoing operations are considered

11

Reviewing Process

• Bermuda's Assessment and Licensing Committee -Recommends to SOI eligibility to register

• Determines conditions of Registration

12

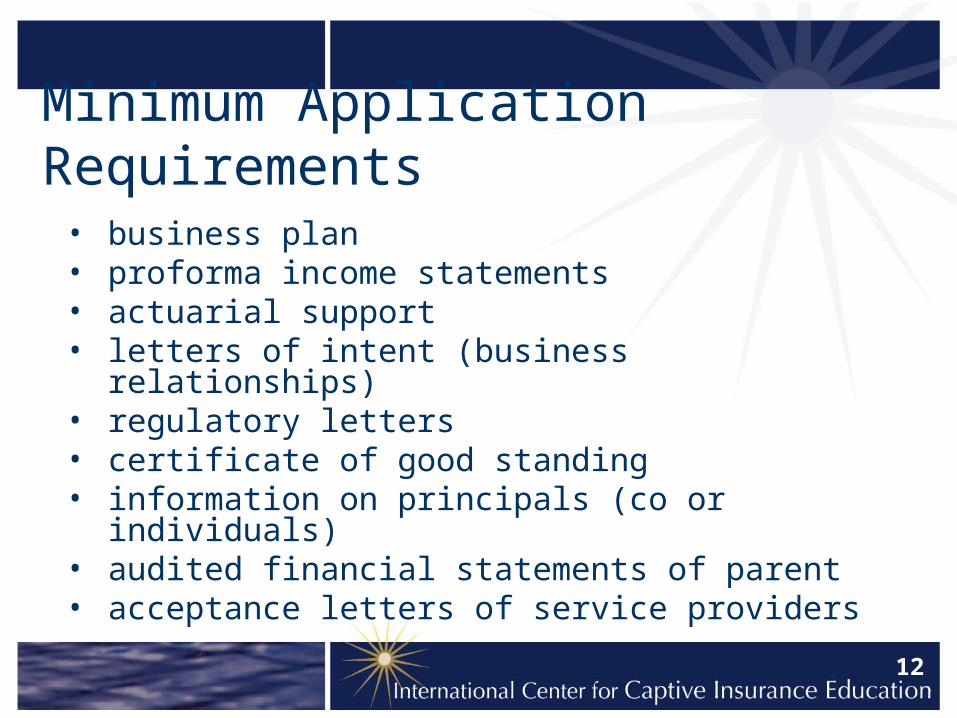

Minimum Application Requirements

• business plan • proforma income statements • actuarial support • letters of intent (business relationships)• regulatory letters • certificate of good standing • information on principals (co or individuals)• audited financial statements of parent• acceptance letters of service providers

13

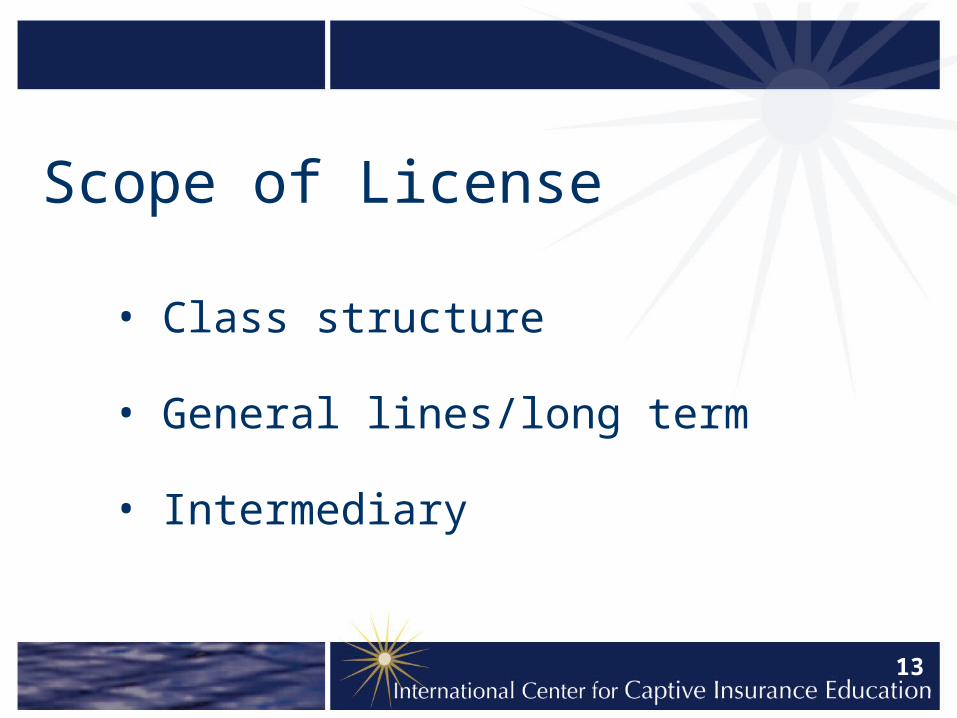

Scope of License

• Class structure

• General lines/long term

• Intermediary

14

Minimum Capital

• Capital requirements (quality)

• Limits and risk coverage

• Future development

15

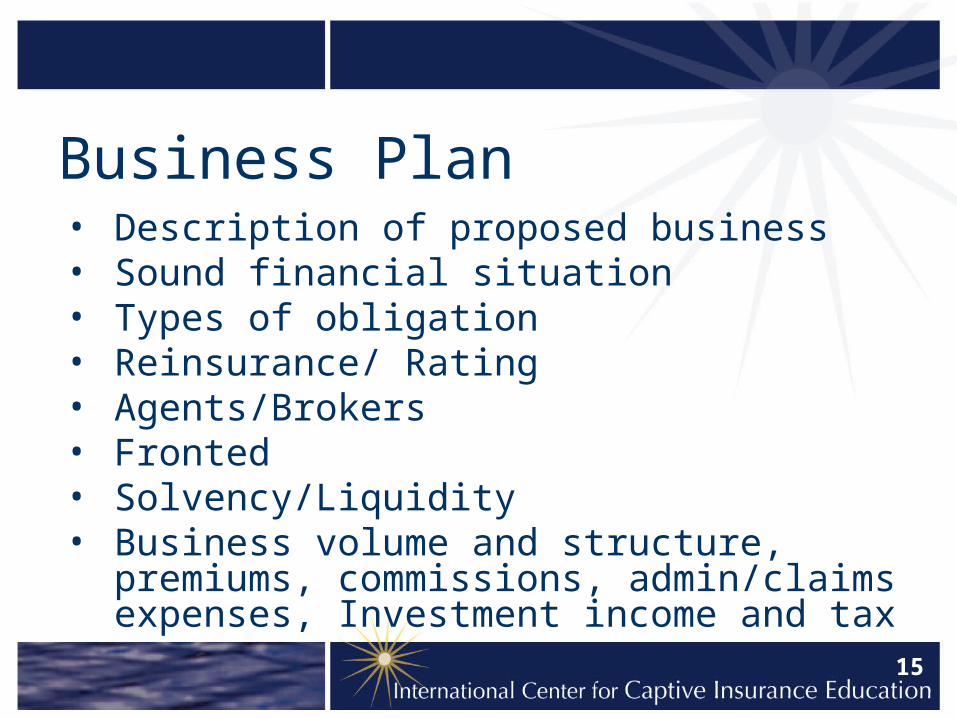

Business Plan• Description of proposed business• Sound financial situation• Types of obligation• Reinsurance/ Rating• Agents/Brokers• Fronted• Solvency/Liquidity• Business volume and structure, premiums,

commissions, admin/claims expenses, Investment income and tax

16

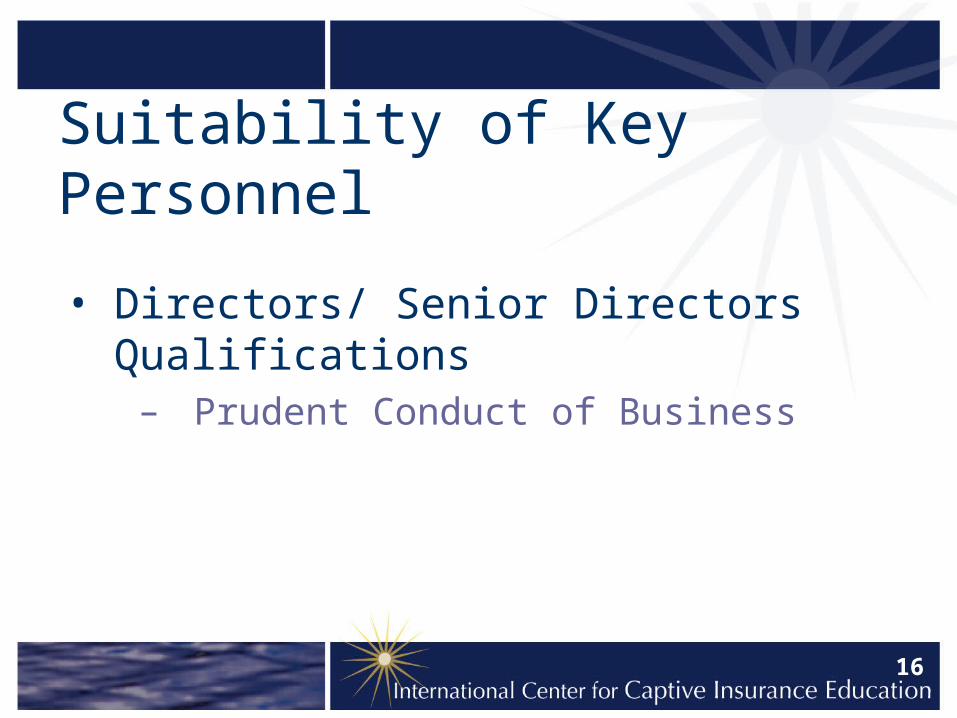

Suitability of Key Personnel

• Directors/ Senior Directors Qualifications– Prudent Conduct of Business

17

Suitability of Owners

• Ability for Sound and Prudent Management

• Professionally Qualified

• Reliable/ Good Repute

• Transparent Structure

18

Other Considerations

• Affiliation contracts and outsourcing

• Product control and General Policy Conditions

• Actuaries, Auditors, Loss Reserve Specialists, Principal Representative

19

The Ongoing Relationship

The Seven Habits of Highly Effective People Captives

Presented by

Dean Wickens

20

• Insurance licence confers responsibilities.• Captive's relationship with its regulator is

different...• A good on-going relationship with your

regulator is essential / fundamental / integral (delete as applicable).

21

Habit Number 1

• Understand your regulator’s role– Current and future policyholders– Jurisdiction's reputation

22

Habit Number 2• Maintain open dialogue

– Take advantage of opportunities to meet with your regulator.

– Advantages of open dialogue:• Reports to the main board• Allay regulator’s suspicions• Kept advised of developments

23

Habit Number 3

• Know the legislation in your captive's jurisdiction.– Identify issues relevant to the parent– Notification or approval?

24

Habit Number 4

• Ensure the captive complies with legislative requirements

25

Habit Number 5

• Run off / exit plans

26

Habit Number 6

• When problems do occur...

27

Habit Number 7

• Think Win/Win

28

What To Do When Things Go Wrong

Presented by

Jeff Kehler

29

Inform your regulator immediately

• Sooner rather than later

• Phone to initiate discussion

• Formal follow-up with letter or e-mail

30

Provide factual details

• When did you discover it?

• Precise details as you know them

• Why and how did it happen?

• What is being done about right now?

• Make arrangements to meet with regulator

31

Meeting with regulators

• Depending on severity of situation– Teleconference with captive manager and

captive owners– Face to face meeting with all parties

• Provide details of the situation

• Discuss options and work-out plan

• Consider future viability

32

Prepare Detailed Work-out Plan• Summary of current situation

– How it happened and time frame– Be as precise as possible

• Explain immediate actions taken to remediate the situation

• Provide detailed action plan– Actionable items– Milestones– Timeframe

33

Prepare for regulatory action• Depending on the severity of the situation• Whack on the knuckles• Cease & Desist

– Voluntary or mandatory• Supervision

– Confidential or public• Rehabilitation• Liquidation

34

Cooperate fully with regulator

• Prompt replies to all requests– Phone calls, e-mails, letters, documents

• Make available– Books, records, and accounts

• Do not:– Obstruct– Interfere– Otherwise delay or sidetrack

35

Examples of things gone wrong• Minor

– Failure or late notification of non-material changes to plan of operation

• Change of service provider• Change of captive director or officer• Incidental change to investment policy• Change of location

36

Examples of things gone wrong• Material

– Unauthorized payment of dividend– Unauthorized loan to parent or affiliate– Loss of front company– Cancellation of reinsurance– Increased exposure to captive, e.g., higher

retentions, change in policy terms

37

Examples of things gone wrong• Major

– Financial impairment– Illegal dealings– Evidence of embezzlement– Operation hazardous to policyholders

38

Summary

• When things go wrong– Contact your regulator immediately– Work closely with them to resolve the

situation– Learn from it– What can be done to avoid it in the future?

39

Questions for the Panel Members?

40

Thank you

panel members for your participation today.

41

This program fulfills 1/3rd of the teleconference requirement for the completion of the Associate in

Captive Insurance (ACI) designation. It also counts as 100 minutes of continuing education (2 CPE

credits) for CPAs via ICCIE’s certification through the National Association of State Boards of

Accountancy (NASBA), as well as 2 continuing education credits for ACI designation recipients. It

also counts as 2 contact hours through the American Society for Healthcare Risk Management for the FASRHM and DFASHRM designations, as

well as for CPHRM renewal.