Embed Size (px)

Citation preview

1

V 1.0

Consumer financial empowerment and financial systems that work for the poor: the South African

pictureAstrid Ludin

FinMark Trust

2

V 1.0

FinMark Trust

Independent trust formed in April 2002 Initial funding from the UK’s Department for

International Development Mission: “Making Financial Markets Work for the

Poor” Facilitating and catalysing the next generation of

development around access to financial services

3

V 1.0

Overview

Consumer financial empowerment: the context

What is financial literacy? State of access to financial services State of financial literacy Some conclusions

4

V 1.0

Consumer Financial Empowerment: the context

5

V 1.0

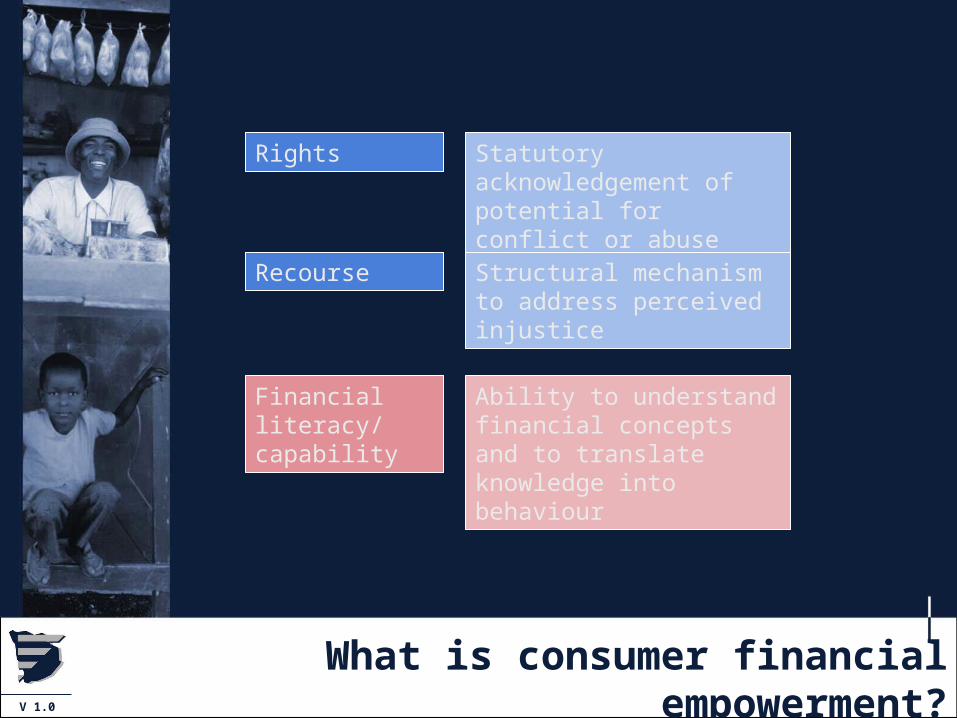

What is consumer financial empowerment?

Rights

Recourse

Financial literacy/ capability

Statutory acknowledgement of potential for conflict or abuseStructural mechanism to address perceived injustice

Ability to understand financial concepts and to translate knowledge into behaviour

6

V 1.0

Consumer empowerment : the debates

Consumer empowerment vs consumer protection– Philosophical difference; levels of financial

literacy may impact

Regulation vs access/financial inclusion (regulator’s dilemma)– Innovation drives lower-cost delivery, esp. to

the poor/financially excluded – Inappropriate regulation can limit competition

and innovation– But innovation and competition can also

destabilise

Rights without recourse or awareness of rights/recourse has little meaning

Too little or too much – how will we know?

7

V 1.0

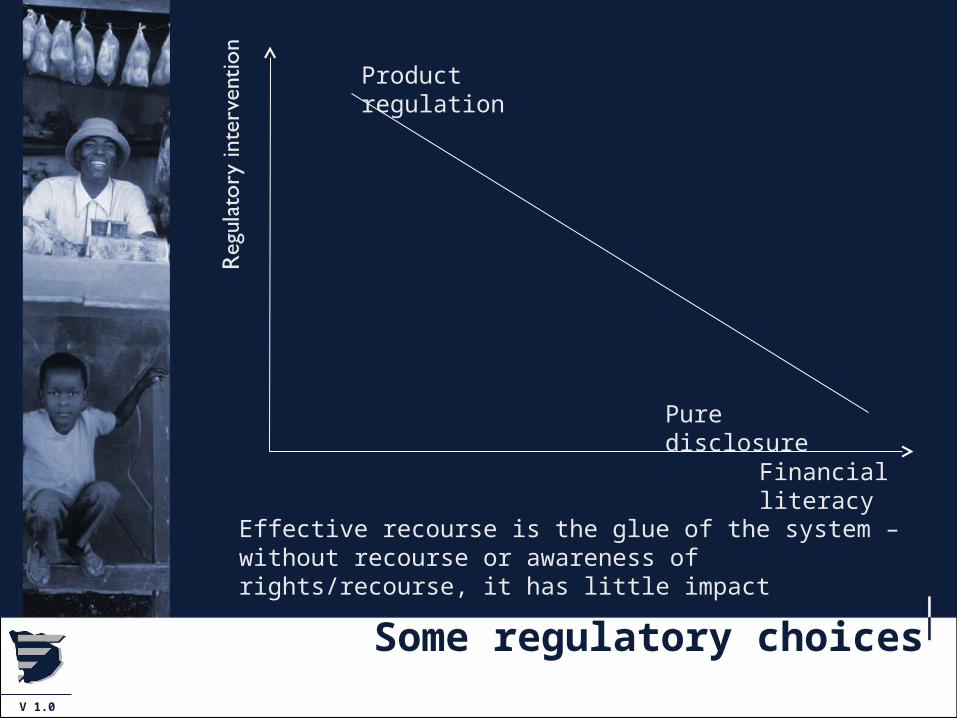

Some regulatory choices

Pure disclosure

Product regulation

Financial literacy

Effective recourse is the glue of the system – without recourse or awareness of rights/recourse, it has little impact

8

V 1.0

Financial Literacy

9

V 1.0

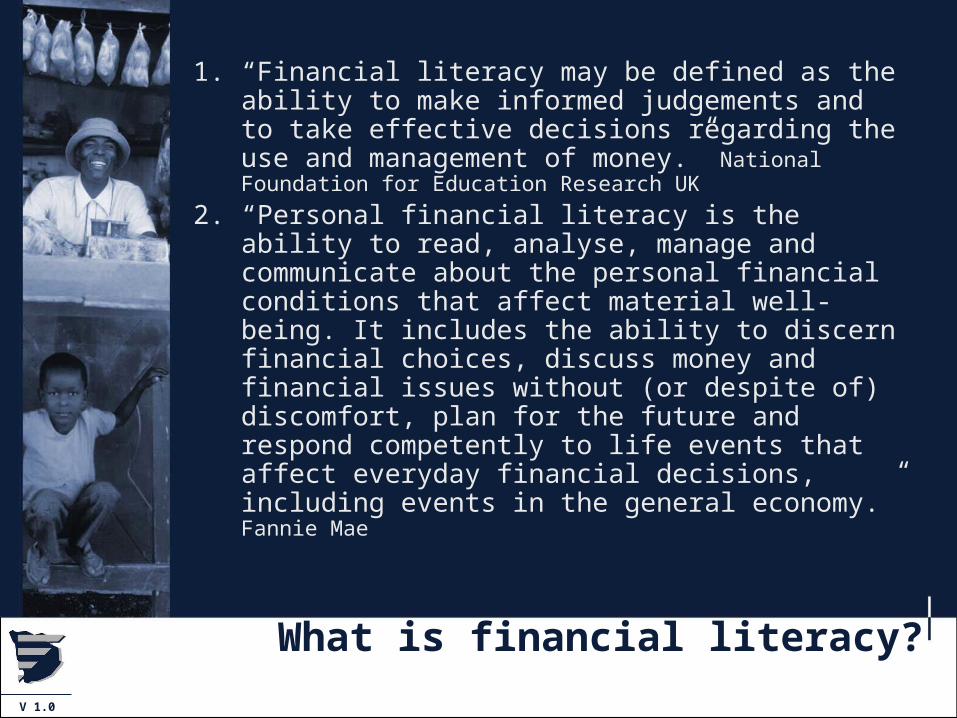

What is financial literacy?

1. “Financial literacy may be defined as the ability to make informed judgements and to take effective decisions regarding the use and management of money.” National Foundation for Education Research UK

2. “Personal financial literacy is the ability to read, analyse, manage and communicate about the personal financial conditions that affect material well-being. It includes the ability to discern financial choices, discuss money and financial issues without (or despite of) discomfort, plan for the future and respond competently to life events that affect everyday financial decisions, including events in the general economy.” Fannie Mae

10

V 1.0

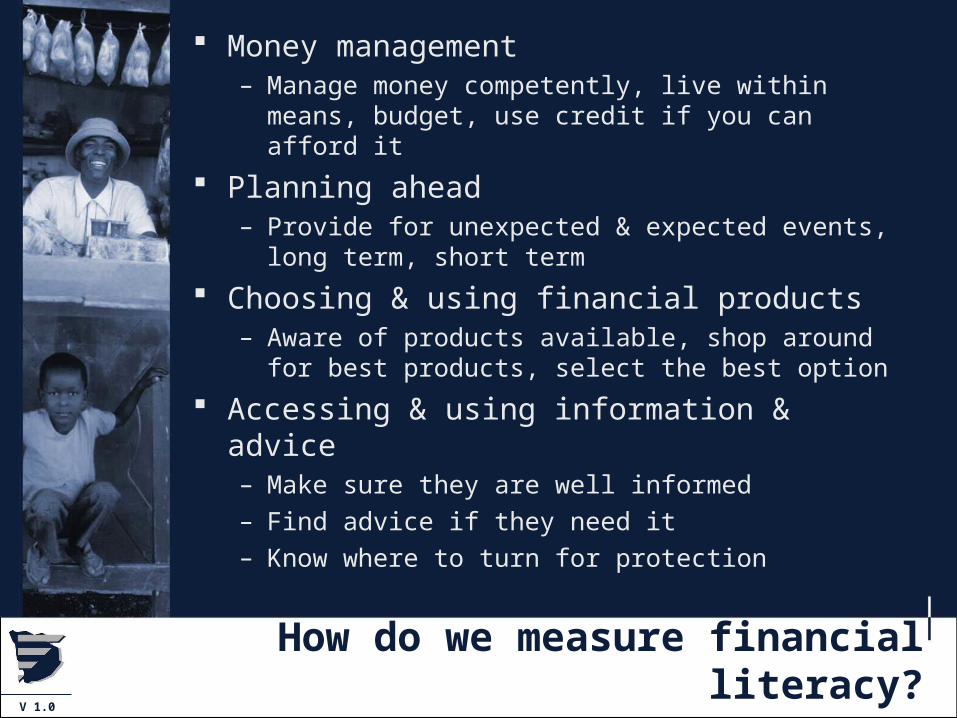

How do we measure financial literacy?

Money management– Manage money competently, live within

means, budget, use credit if you can afford it

Planning ahead– Provide for unexpected & expected events,

long term, short term

Choosing & using financial products– Aware of products available, shop around for

best products, select the best option

Accessing & using information & advice– Make sure they are well informed– Find advice if they need it– Know where to turn for protection

11

V 1.0

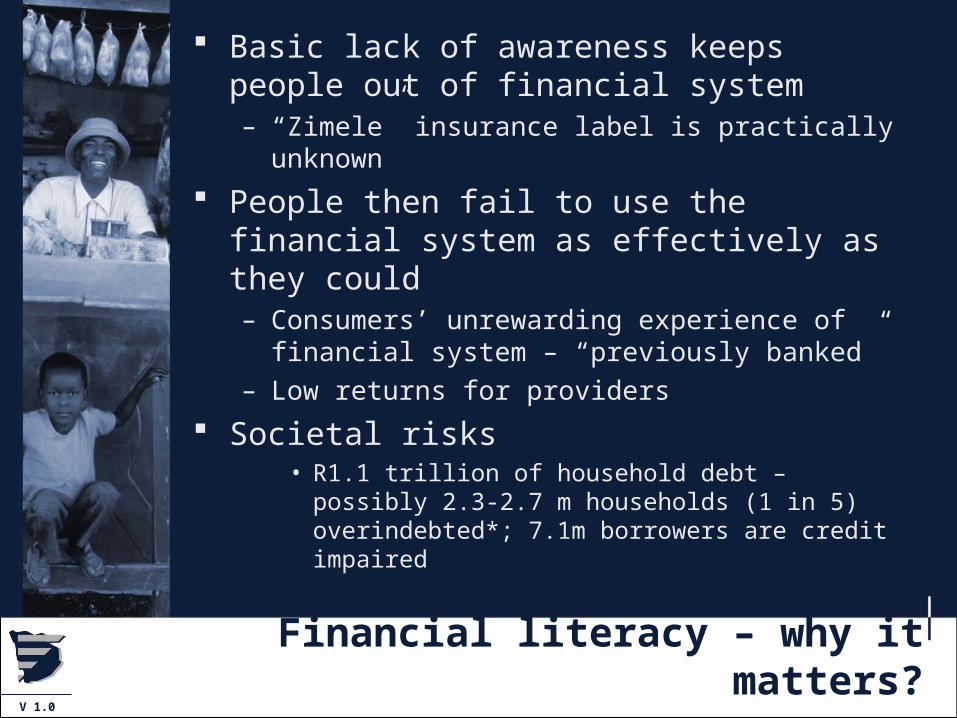

Financial literacy – why it matters?

Basic lack of awareness keeps people out of financial system– “Zimele” insurance label is practically

unknown

People then fail to use the financial system as effectively as they could– Consumers’ unrewarding experience of

financial system – “previously banked”– Low returns for providers

Societal risks• R1.1 trillion of household debt – possibly 2.3-2.7

m households (1 in 5) overindebted*; 7.1m borrowers are credit impaired

12

V 1.0

Access to financial services

13

V 1.0

South Africa’s access strand

Formal other: Other products supplied by financial institution e.g. funeral policy or store account;

Informal: effectively unregulated products e.g. burial society, stokvel

14

V 1.0

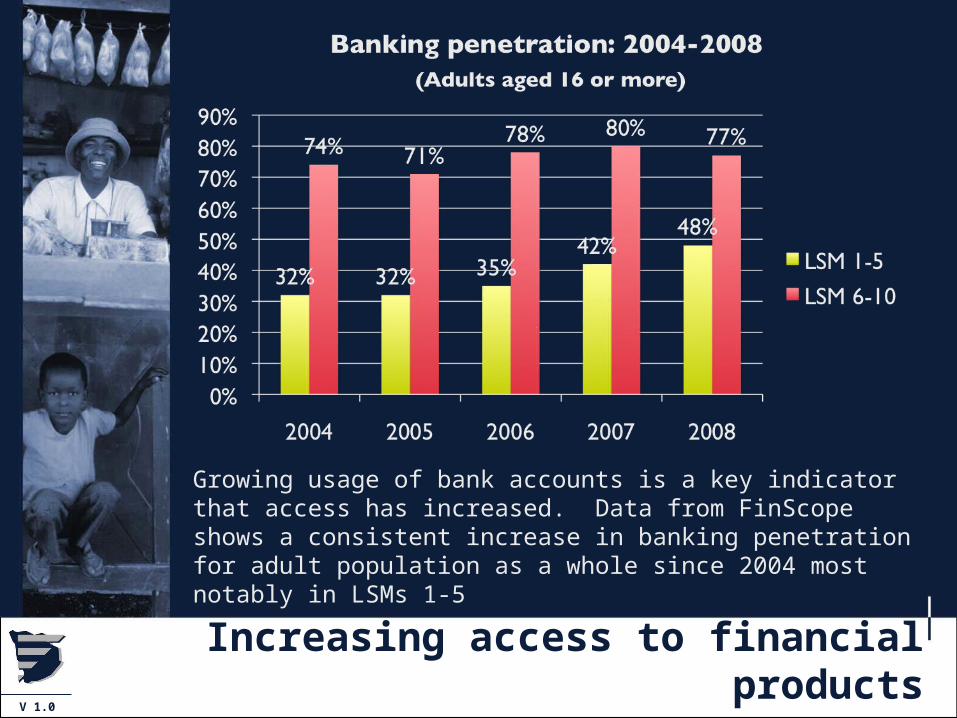

Increasing access to financial products

Growing usage of bank accounts is a key indicator that access has increased. Data from FinScope shows a consistent increase in banking penetration for adult population as a whole since 2004 most notably in LSMs 1-5

15

V 1.0

State of financial literacy

16

V 1.0

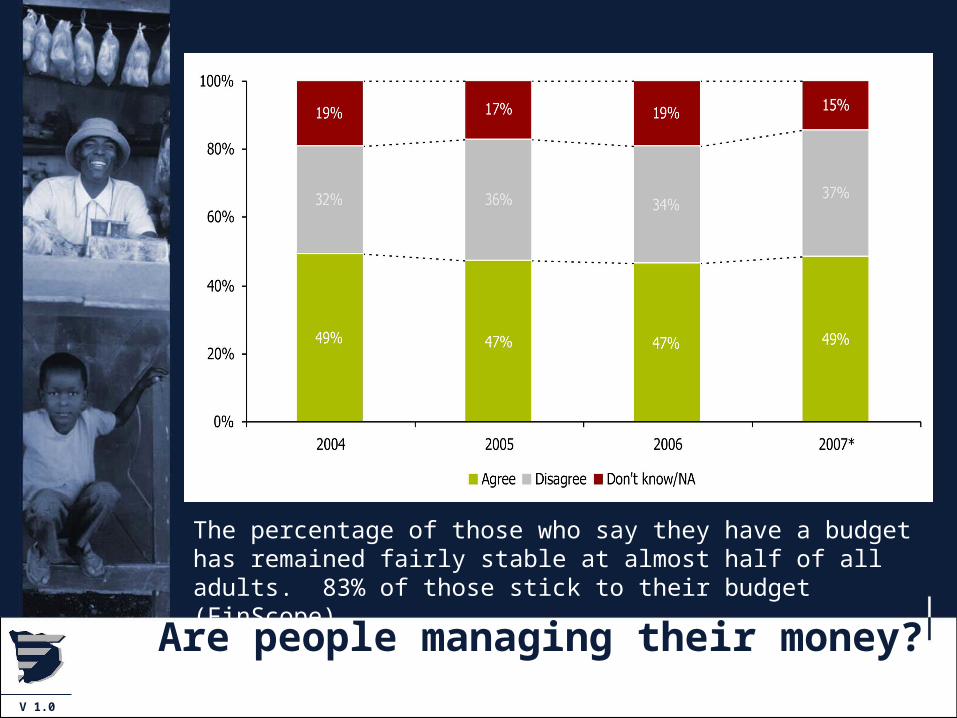

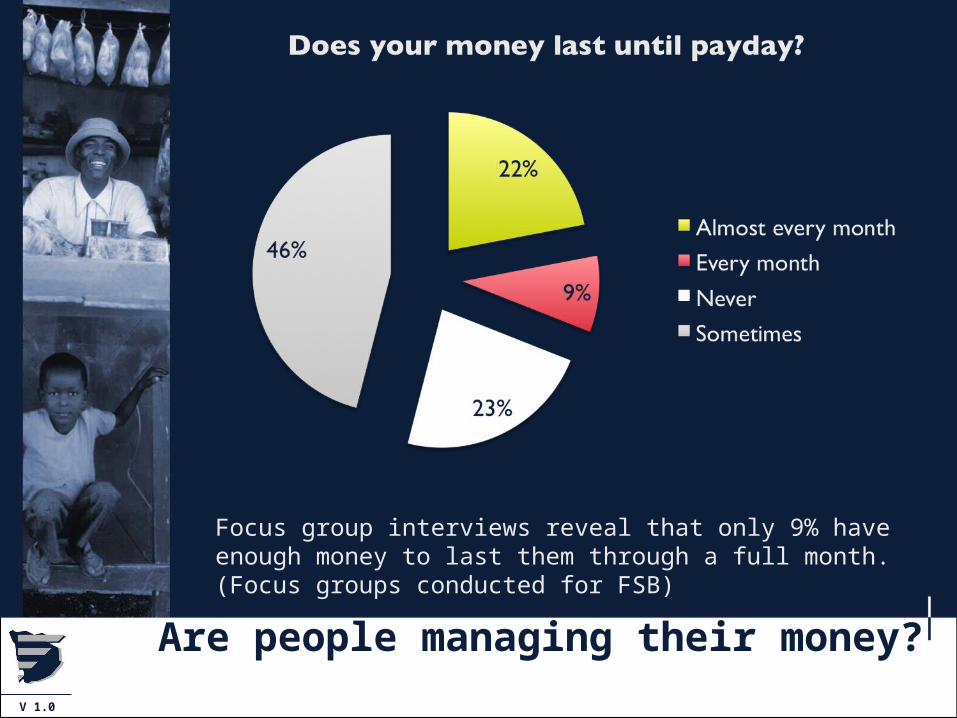

Are people managing their money?

The percentage of those who say they have a budget has remained fairly stable at almost half of all adults. 83% of those stick to their budget (FinScope)

17

V 1.0

Are people managing their money?

Focus group interviews reveal that only 9% have enough money to last them through a full month. (Focus groups conducted for FSB)

18

V 1.0

Are people planning for the future?

60% of people who claim to earn R4,000 – R7,999 are not saving for their retirement– 89% are formally employed– 30% of those in this income bracket are not

saving “have never thought about it” – 440,000 people

Only the most basic concepts about retirement issues are well-known– Only 31% of people understand the term

“retirement planning”– Only 26% understand “retirement annuities or

income”– Only 43% understand “retirement age”

2 in 3 people in LSM 1-5 have no knowledge of any of the above terms

19

V 1.0

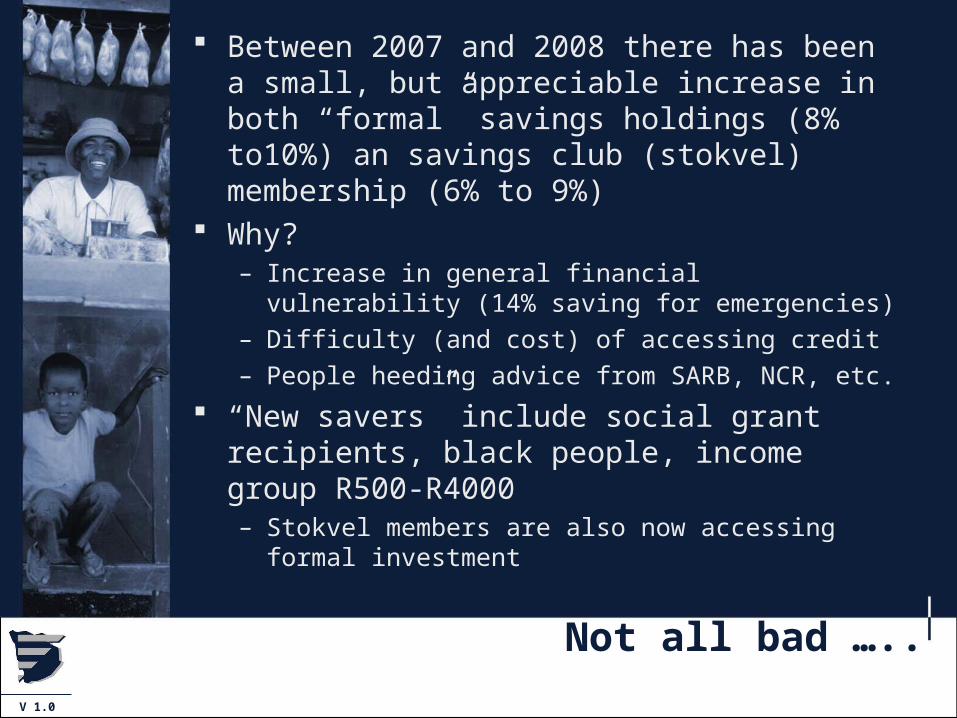

Not all bad …..

Between 2007 and 2008 there has been a small, but appreciable increase in both “formal” savings holdings (8% to10%) an savings club (stokvel) membership (6% to 9%)

Why?– Increase in general financial vulnerability

(14% saving for emergencies)– Difficulty (and cost) of accessing credit– People heeding advice from SARB, NCR, etc.

“New savers” include social grant recipients, black people, income group R500-R4000– Stokvel members are also now accessing

formal investment

20

V 1.0

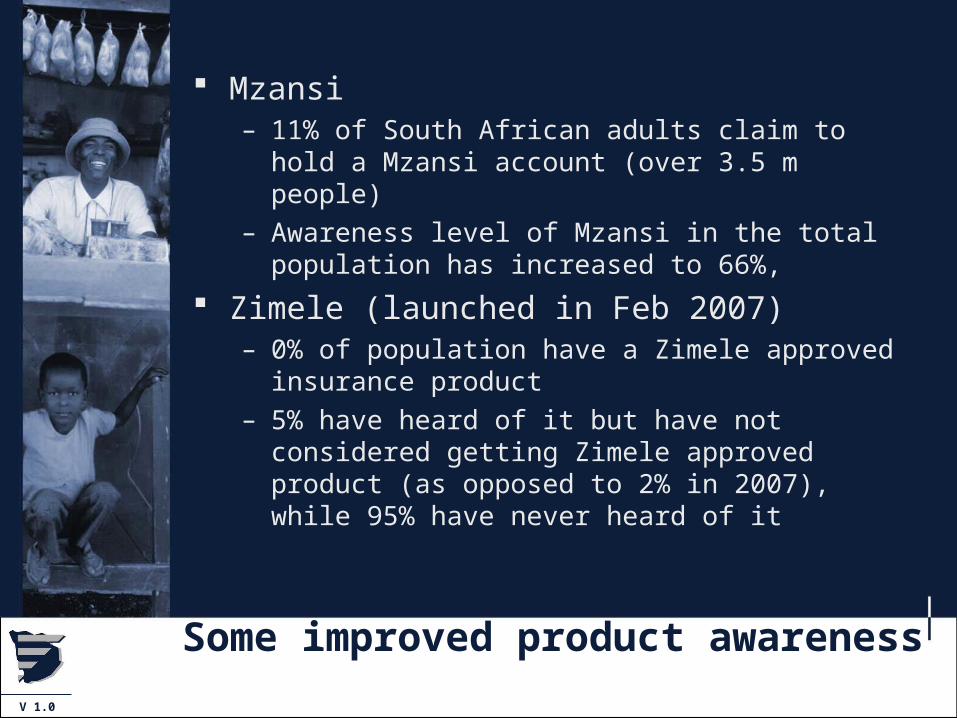

Some improved product awareness

Mzansi – 11% of South African adults claim to hold a

Mzansi account (over 3.5 m people)– Awareness level of Mzansi in the total

population has increased to 66%,

Zimele (launched in Feb 2007)– 0% of population have a Zimele approved

insurance product– 5% have heard of it but have not considered

getting Zimele approved product (as opposed to 2% in 2007), while 95% have never heard of it

21

V 1.0

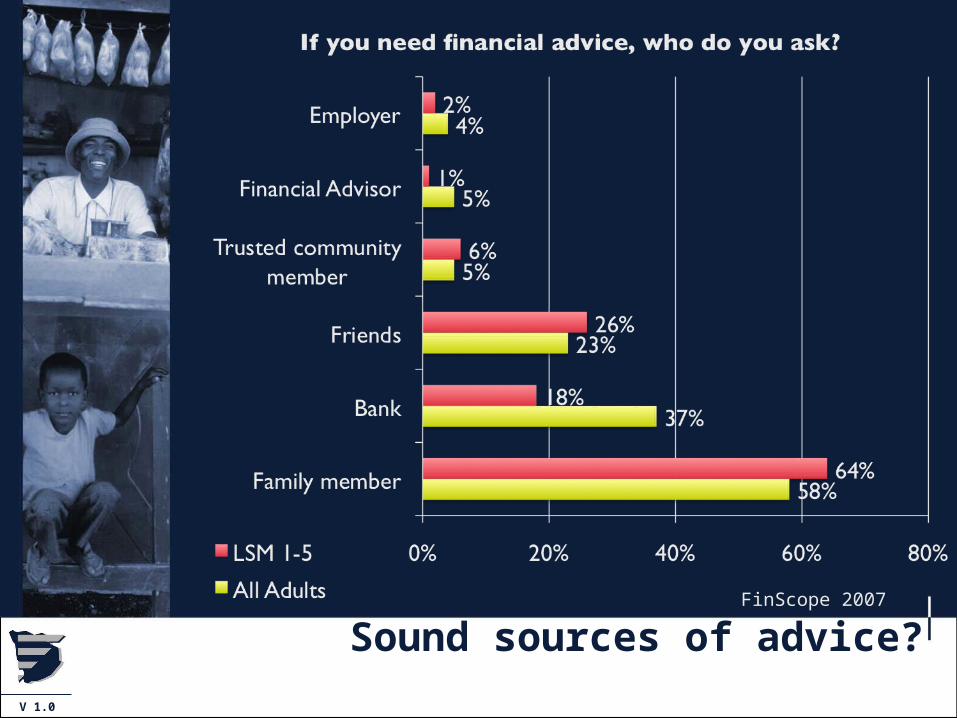

Sound sources of advice?FinScope 2007

22

V 1.0

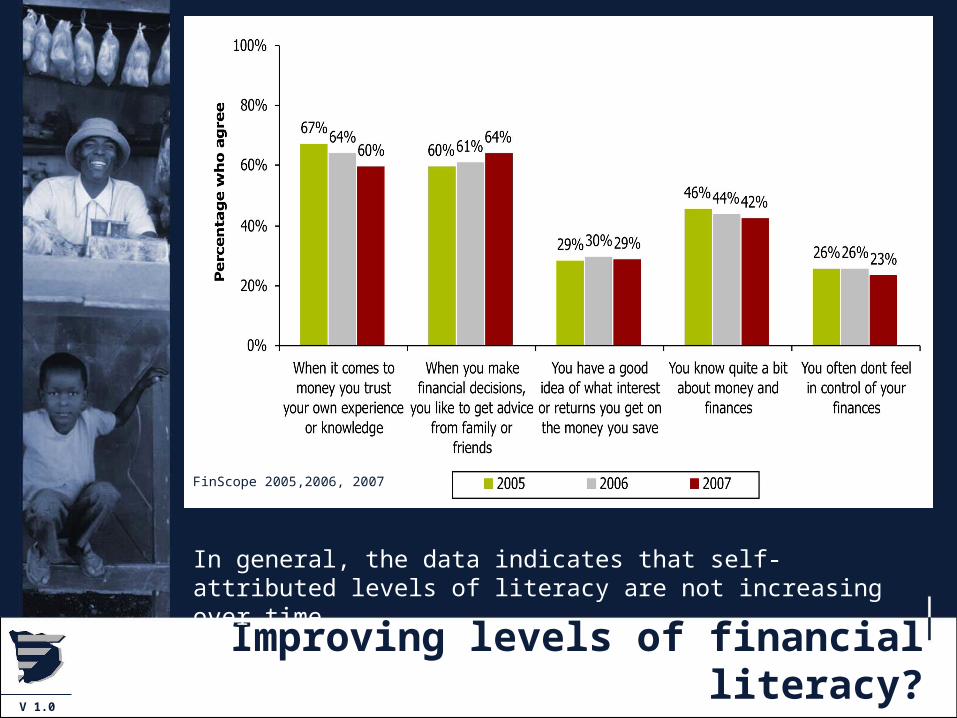

Improving levels of financial literacy?

In general, the data indicates that self-attributed levels of literacy are not increasing over time

FinScope 2005,2006, 2007

23

V 1.0

Conclusions

Financial product penetration is increasing, but not accompanied by greatly improved financial literacy

Multiple initiatives to improve levels of financial literacy/awareness– Financial Sector Charter – R81 million in last

financial year– Various other stakeholder initiatives (regulators,

civil society, government, donors)

But no overarching strategy to focus and prioritise, little collaboration, no measurement of impact, no sharing of learning

Uncertainty of charter future means industry spending will reduce (probably) – who/what will fill the void?

www.finmarktrust.org.za