Embed Size (px)

Citation preview

1

Using the Financial Calculator

Copyright by Diane Scott Docking 2015

Learning Objectives

To learn how to use the Financial Calculator

Copyright by Diane Scott Docking 2015 2

3

TI BA II+ Calculator Setup—Follow This!!

Use one period per year: P/Y = 1

[P/Y] 1

Set decimal to 6 places: Format DEC=6

[FORMAT] 6

Set BGN register to “END”

Copyright by Diane Scott Docking 2015

2ND ENTER

2ND ENTER

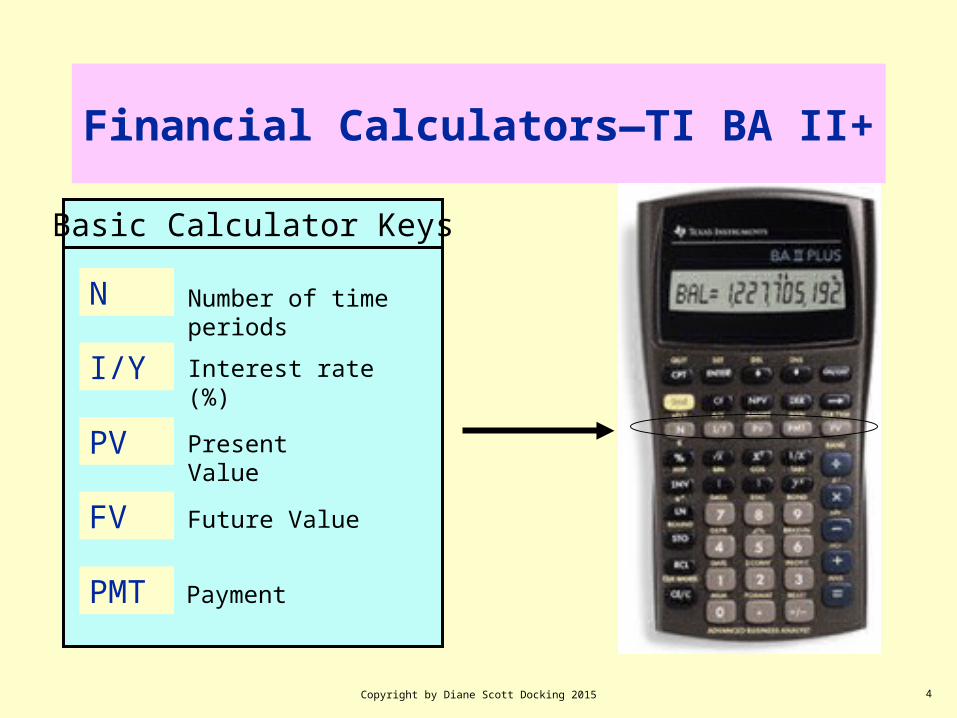

4

Financial Calculators—TI BA II+

N

I/Y

PMT

FV

PV

Number of time periods

Interest rate (%)

Future Value

Present Value

Payment

Basic Calculator Keys

Copyright by Diane Scott Docking 2015

5

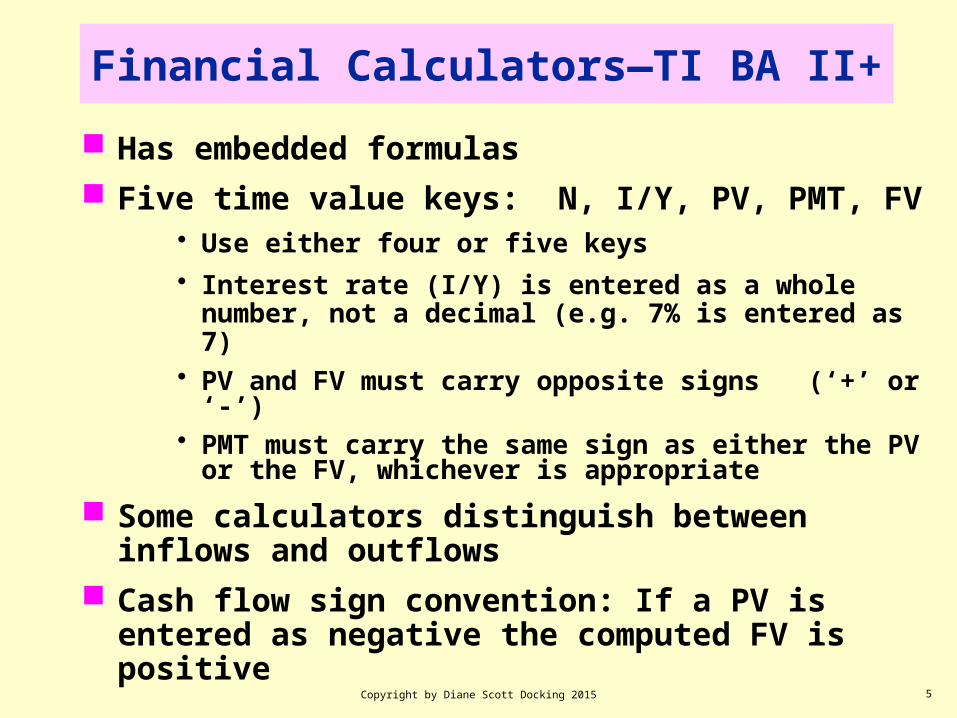

Financial Calculators—TI BA II+

Has embedded formulas

Five time value keys: N, I/Y, PV, PMT, FV• Use either four or five keys

• Interest rate (I/Y) is entered as a whole number, not a decimal (e.g. 7% is entered as 7)

• PV and FV must carry opposite signs (‘+’ or ‘-’)• PMT must carry the same sign as either the PV or the FV,

whichever is appropriate

Some calculators distinguish between inflows and outflows

Cash flow sign convention: If a PV is entered as negative the computed FV is positive

Copyright by Diane Scott Docking 2015

6

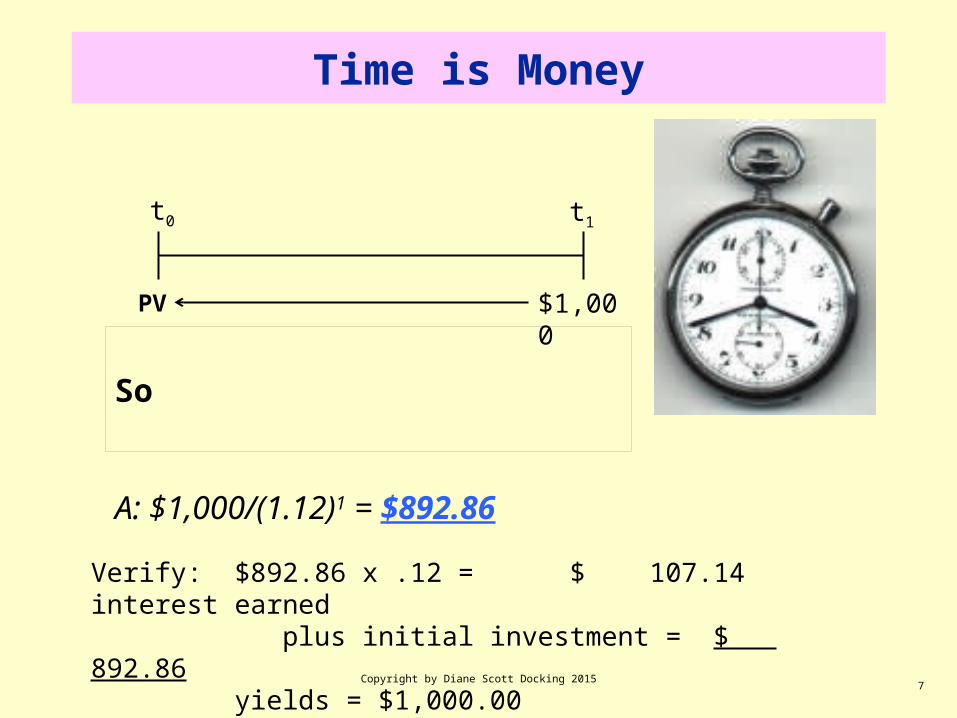

Time is Money

$100 in your hand today is worth more or less than $100 in one year?Money earns interest

• The higher the interest rate, the faster your money grows

Q: How much would $1,000 promised in one year be worth today if you could be earning 12% interest?

Copyright by Diane Scott Docking 2015

7

Time is Money

A: $1,000/(1.12)1 = $892.86

Copyright by Diane Scott Docking 2015

t0 t1

$1,000PV

So

Verify: $892.86 x .12 = $ 107.14 interest earned plus initial investment = $ 892.86

yields = $1,000.00

Financial Calculators & Cash Flow Sign Convention

Input $1,000 FV Input 12 I/Y Input 1 N Input 0 PMT Calculate PV (Cpt PV)

Is PV positive or negative? Why? What’s the deal?

Here are the key strokes:

1000 12 1 0

PV will be NEGATIVE. A -$892.86. But answer is $892.82.

By convention we put PV in as a negative number, so that FV will be positive.

Ignore the negative sign. The negative sign simply means you invested (had a cash outflow).

Copyright by Diane Scott Docking 2015 8

FV

I/Y

N

PMT

CPT PV

9

1. FV of a Lump Sum: What’s the FV of an initial $100 investment after 3 years if i = 10%?

FV = ?

0 1 2 310%

100

Copyright by Diane Scott Docking 2015

$100 x .10 = Interest $ 10 Principal $100 Balance $110 x .10 = interest $11

balance $110 Balance $121 x .10 = interest $ 12.10

balance $121.00 FV = $133.10

$100 x .10 = $10 x 3 yrs. = $30 in interest if withdraw interest each year.

Financial Calculator Input: FV of a Lump Sum

Input -$100 PV Input 10 I/Y Input 3 N Input 0 PMT Calculate FV (Cpt FV)

Is FV positive or negative? Why? What’s the deal?

Here are the key strokes:

100 10 3 0

FV will be a POSITIVE $133.10.

By convention we put PV in as a negative number, so that FV will be positive.

Copyright by Diane Scott Docking 2015 10

PV

I/Y

N

PMT

CPT FV

+│─

11

Another Example: FV of a Lump Sum

Mary invests $1,000 today for 20 years @ 8%. How much will she have in 20 years?

FVn = PV(1+i) n FV20 = $1,000 (1.08)20 = $4,660.96

Copyright by Diane Scott Docking 2015

Here are the key strokes: 1000 8 20 0

FV will be a POSITIVE $4,660.96

By convention we put PV in as a negative number, so that FV will be positive.

Input -$1000 PV Input 8 I/Y Input 20 N Input 0 PMT Calculate FV (Cpt FV)

+│─ PV

I/Y

N

PMT

CPT FV

12

2. PV of a Lump Sum: What’s the PV if i = 10% to end up with FV = $100 after 3 years?

FV = 100

0 1 2 310%

75.13

Copyright by Diane Scott Docking 2015

Verify:$75.13 x .10 = Interest $ 7.51

Principal $75.13 Balance $82.64 x .10 = interest $ 8.26

balance $82.64 Balance $90.90 x .10 = interest $ 9.09

balance $90.90 FV = $99.99 = $100

$100 /(1.10)3 = $75.13

Financial Calculator Input: PV of a Lump Sum

Input $100 FV Input 10 I/Y Input 3 N Input 0 PMT Calculate PV (Cpt PV)

Here are the key strokes:

100 10 3 0

PV will be a NEGATIVE $75.13.

Ignore negative sign. Answer is $75.13.

Copyright by Diane Scott Docking 2015 13

FV

I/Y

N

PMT

CPT PV

14

3. FV of an annuityExample 1: What is the FV of a 3-year

ordinary annuity of $100 at 10%?

$100 100100

0 1 2 310%

FV =

10% 10%

Copyright by Diane Scott Docking 2015

110121

100(1.10)=

100(1.10)2=

$331

Input $0 PV Input 10 I/Y Input 3 N Input $100 PMT Calculate FV (Cpt FV)

Here are the key strokes:

0 10 3 100

FV will be a NEGATIVE $331. Ignore negative sign. Answer: $331.

Cannot put 0 in as a negative.

Copyright by Diane Scott Docking 2015 15

PV

I/Y

N

PMT

CPT FV

Financial Calculator Input: FV of an ordinary annuity

16

Example 2: What’s the FV of a 3-year annuity due of $100 at 10%?

100$100 100

0 1 2 310%

FV = Copyright by Diane Scott Docking 2015

100(1.10)= 110100(1.10)2= 121

133.10100(1.10)3=

$364.10

Set calculator to BGN mode

Input $0 PV Input 10 I/Y Input 3 N Input $100 PMT Calculate FV (Cpt FV)

Here are the key strokes:

[BGN] [SET]

0 10 3 100

FV will be a NEGATIVE $364.10. Ignore negative sign. Answer: $364.10.

Cannot put 0 in as a negative.

Copyright by Diane Scott Docking 2015 17

PV

I/Y

N

PMT

CPT FV

Financial Calculator Input: FV of an annuity due

2ND 2ND

18

4. PV of an annuityExample 1: What’s the PV of an 3-year

ordinary annuity of $100 per year at 10%?

100 100100

0 1 2 310%

= PVCopyright by Diane Scott Docking 2015

=100/(1.10)1

90.91=100/(1.10)2

82.64

75.13

$248.68

=100/(1.10)3

Reset calculator to END mode

Input $0 FV Input 10 I/Y Input 3 N Input $100 PMT Calculate PV (Cpt PV)

Here are the key strokes:

[BGN] [SET]

0 10 3 100

PV will be a NEGATIVE $248.68. Ignore negative sign. Answer: $248.68.

Cannot put 0 in as a negative.

Copyright by Diane Scott Docking 2015 19

FV

I/Y

N

PMT

CPT PV

2ND 2ND

Financial Calculator Input: PV of an ordinary annuity

20

Example 2: What’s the PV of an 3-year annuity due of $100 per year at 10%?

100 100

0 1 2 3

10%

100

= PV

Copyright by Diane Scott Docking 2015

90.91=100/(1.10)

82.64=100/(1.10)2

273.55

Reset calculator back to BGN mode

Input $0 FV Input 10 I/Y Input 3 N Input $100 PMT Calculate PV (Cpt PV)

Here are the key strokes:

[BGN] [SET]

0 10 3 100

PV will be a NEGATIVE $273.55 Ignore negative sign. Answer: $273.55

Cannot put 0 in as a negative.

Copyright by Diane Scott Docking 2015 21

FV

I/Y

N

PMT

CPT PV

2ND 2ND

Financial Calculator Input: PV of an annuity due

22

Example: What is the FV of this uneven cash flow stream if rates are 10% and payment is made at end of the year?

0

100

1

300

2

300

310%

-50

4

Copyright by Diane Scott Docking 2015

300 x (1.10) =

300 x (1.10)2 =

100 x (1.10)3=

330363133.10

FV = $776.10

Using Calculator for Uneven CFs

Reset calculator to END mode

Input $0 CF0

Input $100 CF1

Input $300 CF2

Input $300 CF3

Input -$50 CF4

Input 10% interest Calculate FV

Here are the key strokes: [BGN] [SET]

0 , C01 appears,

100 ,F01 appears,1 ,C02 appears

300 ,F02 appears,1 ,C03 appears

300 ,F03 appears,1 ,C04 appears

50 ,F04 appears, 1 , C05 appears

, I= appears, 10 , NPV= appears,

NPV = 530.09 appears. This is the PV of the CFs.

Continued>>>>>>>>>>>

Copyright by Diane Scott Docking 2015

23

CF

CPT

NPV

2ND

ENTER ↓

2ND

ENTER ↓ ENTER ↓

ENTER ↓ ENTER ↓

+│─ ↓

ENTER ↓

ENTER ↓

ENTER ↓

↓ENTERENTER

Financial Calculator Input:FV of uneven cash flows

Input $530.09 PV Input 10 I/Y Input 4 N Input $0 PMT Calculate FV (Cpt FV)

Here are the key strokes:

530.09 10 4 0

FV will be a $776.10.

Copyright by Diane Scott Docking 2015 24

PV

I/Y

N

PMT

CPT FV

Financial Calculator Input:FV of uneven cash flows (continued)

+│─

25

Example: What is the PV of this uneven cash flow stream if rates are 10% and payment is made at the end of the year?

0

100

1

300

2

300

310%

-50

4

90.91

______

$530.08 = PVCopyright by Diane Scott Docking 2015

=100/(1.10)

=300/(1.10)2

=300/(1.10)3

=-50/(1.10)4

247.93

225.39

-34.15

Reset calculator to END mode

Input $0 CF0

Input $100 CF1

Input $300 CF2

Input $300 CF3

Input -$50 CF4

Input 10% interest Calculate PV

Here are the key strokes: [BGN] [SET]

0 , C01 appears,

100 ,F01 appears,1 ,C02 appears

300 ,F02 appears,1 ,C03 appears

300 ,F03 appears,1 ,C04 appears

50 ,F04 appears, 1 , C05 appears

, I= appears, 10 , NPV= appears,

NPV = 530.09 appears. This is the PV of the CFs.

Copyright by Diane Scott Docking 2015

26

CF

CPT

NPV

2ND

Financial Calculator Input:PV of uneven cash flows

ENTER ↓

2ND

ENTER ↓ ENTER ↓

ENTER ↓ ENTER ↓

+│─ ↓

ENTER ↓

ENTER ↓

ENTER ↓

↓ENTERENTER

27

Agree to make “step payments” on a contract as follows:

$1,000 per month for the first year

$1,300 per month for the second year

$2,000 per month for the third year

At 10% annual rate, what is the PV of these payments?

Example: PV of Monthly Uneven Cash Flow Stream

Copyright by Diane Scott Docking 2015

Make sure calculator is set to END mode

Input $0 CF0

Input $1000 CF1-12

Input $1300 CF13-24

Input $2000 CF25-36

Input 10%/12 =0.83333% interest

Calculate PV

Here are the key strokes: [CLR WORK] 0 , C01 appears,

1000 ,F01 appears, 12 ,C02 appears

1300 ,F02 appears,12 ,C03 appears

2000 ,F03 appears,12 ,C04 appears

, I= appears, 10 12 , I=0.833333 appears

, NPV= appears,

NPV = 43,400.52 appears. This is the PV of the CFs.

Copyright by Diane Scott Docking 2015

28

CF

CPT

NPV

ENTER ↓

ENTER ↓ ENTER ↓

ENTER ↓ ENTER ↓

ENTER ↓

ENTER ↓

ENTER ↓

Financial Calculator Input: PV of Monthly Uneven Cash Flow Stream

=

2ND CF 2ND

÷

29

Recall the formula:

We can use the Financial Calculator to solve for EAR.

Calculating Effective Annual Rates with a Calculator

Copyright by Diane Scott Docking 2015

11

m

Nom

m

iEAR

Where: m is number of compounding periods per year.

30

Example: EAR% for a nominal rate of 8%, compounded quarterly? Daily?

Copyright by Diane Scott Docking 2015

TO PRESS DisplaySelect Interest Conversion [ICONV] NOM = 0

Enter nominal interest rate 8 NOM = 8.00

Enter # of compounding periods per year

4 C/Y = 4.00

Compute EAR EFF = 8.243%

Enter # of compounding periods per year

365 C/Y = 365.00

Compute EAR EFF = 8.3278%

2ND

ENTER

↓ ↓ ENTER

CPT↑

↑ ↑

↑ CPT

ENTER

31

Example: EAR% for a nominal rate of 10%, compounded semi-annually, quarterly, monthly, and daily?

Copyright by Diane Scott Docking 2015

TO PRESS DisplaySelect Interest Conversion [ICONV] NOM = 0

Enter nominal interest rate 10 NOM = 10.00

Enter # of compounding periods per year

2 C/Y = 2.00

Compute EAR EFF = 10.25%

Enter # of compounding periods per year

4 C/Y = 4.00

Compute EAR EFF = 10.381%

Enter # of compounding periods per year

12 C/Y = 12.00

Compute EAR EFF = 10.471%

Enter # of compounding periods per year

365 C/Y = 365.00

Compute EAR EFF = 10.516%

2ND

ENTER

↓ ↓ ENTER

CPT↑

↑ ↑

↑ CPT

↑ ↑

↑

↑ ↑

↑

CPT

CPT

ENTER

ENTER

ENTER

Finding “n” and “i” of a Lump Sum

It is EASY to find “n” and “i” using a Financial Calculator

FV & PV of a lump sum: Example 1: At what interest rate would you have to

invest $100 today to end up with $133.10 in 3 years?

Copyright by Diane Scott Docking 201532

Input - $100 PV Input $133.10 FV Input 3 N Input $0 PMT Calculate I/Y (Cpt I/Y)

Here are the key strokes:

100 133.10 3 0

I/Y = 10%

FV

I/Y

N

PMT

CPT

PV+│─

Finding “n” and “i” of a Lump Sum

FV & PV of a lump sum: Example 2: If you invest $100 today at 10%, how long

will it take to grow to $133.10?

Copyright by Diane Scott Docking 2015 33

Input - $100 PV Input $133.10 FV Input 10 1/Y Input $0 PMT Calculate N (Cpt N)

Here are the key strokes:

100 133.10 10 0

N = 3 years

FV

N

I/Y

PMT

CPT

PV+│─

Finding “n”, “i”, and “payment” of Annuities

It is EASY to find “n”, “i”, and “payments” using a financial calculator.

FV & PV of an ordinary annuity: Example 1: At what interest rate would you have to

invest $100 payments made annually (at end of year) to end up with $331 in 3 years?

Example 2: If you invest $100 annually (at end of year) at 10%, for how many years must you invest before your future value equals $331?

Example 3: How much must you invest annually (at end of year) at 10%, for 3 years to accumulate a future value of $331 at the end of 3 years?

Copyright by Diane Scott Docking 2015 34

Finding “n”, “i”, and “payment” of Annuities

Finding “i”

FV & PV of an ordinary annuity: Example 1: At what interest rate would you have to

invest $100 payments made annually (at end of year) to end up with $331 in 3 years?

Copyright by Diane Scott Docking 2015 35

Input $0 PV Input - $331 FV Input 3 N Input $100 PMT Calculate I/Y (Cpt I/Y) Need to make FV or payments negative.

Here are the key strokes:

0 331 3 100

I/Y = 10%

FV

I/Y

N

PMT

CPT

PV

+│─

Finding “n”, “i”, and “payment” of Annuities

Finding “n”

FV & PV of an ordinary annuity: Example 2: If you invest $100 annually (at end of year)

at 10%, for how many years must you invest before your future value equals $331?

Copyright by Diane Scott Docking 2015 36

Input $0 PV Input $331 FV Input 10 1/Y Input -$100 PMT Calculate N (Cpt N)

Here are the key strokes:

0 331 10 100

N = 3 years

FV

N

I/Y

PMT

CPT

PV

+│─

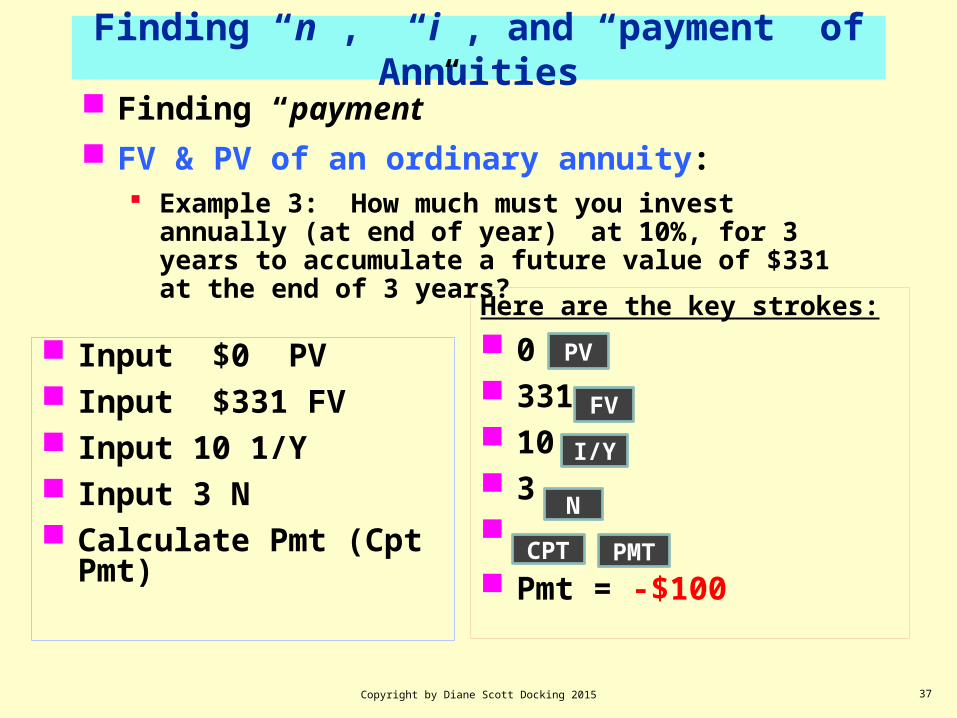

Finding “n”, “i”, and “payment” of Annuities

Finding “payment”

FV & PV of an ordinary annuity: Example 3: How much must you invest annually (at end

of year) at 10%, for 3 years to accumulate a future value of $331 at the end of 3 years?

Copyright by Diane Scott Docking 2015 37

Input $0 PV Input $331 FV Input 10 1/Y Input 3 N Calculate Pmt (Cpt Pmt)

Here are the key strokes:

0 331 10 3

Pmt = -$100

FV

N

I/Y

PMTCPT

PV

Finding “n”, “i”, and “payment” of Annuities

It is EASY to find “n”, “i”, and “payments” using a financial calculator.

FV & PV of an annuity due: Example 1: At what interest rate would you have to

invest $100 payments made annually (at beginning of year) to end up with $364.10 in 3 years?

Example 2: If you invest $100 annually (at beginning of year) at 10%, for how many years must you invest before your future value equals $364.10?

Example 3: How much must you invest annually (at beginning of year) at 10%, for 3 years to accumulate a future value of $364.10 at the end of 3 years?

Copyright by Diane Scott Docking 2015 38

Finding “n”, “i”, and “payment” of Annuities

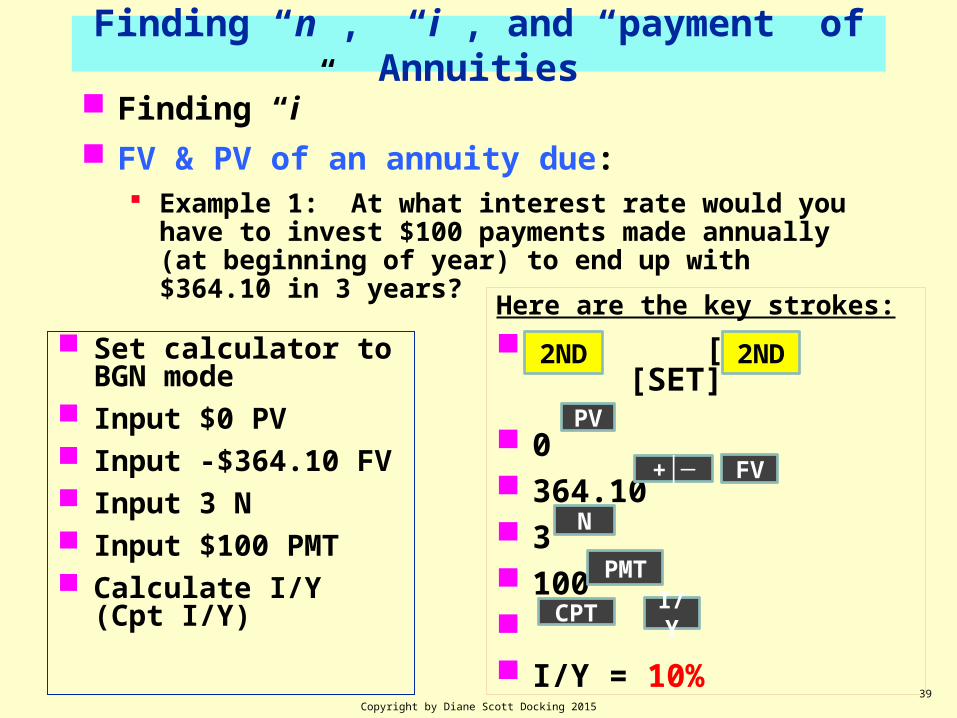

Finding “i”

FV & PV of an annuity due: Example 1: At what interest rate would you have to

invest $100 payments made annually (at beginning of year) to end up with $364.10 in 3 years?

Copyright by Diane Scott Docking 201539

Set calculator to BGN mode

Input $0 PV Input -$364.10 FV Input 3 N Input $100 PMT Calculate I/Y (Cpt I/Y)

Here are the key strokes:

[BGN] [SET]

0 364.10 3 100 I/Y = 10%

PV

I/Y

N

PMT

CPT

FV

2ND 2ND

+│─

Finding “n”, “i”, and “payment” of Annuities

Finding “n”

FV & PV of an annuity due: Example 2: If you invest $100 annually (at beginning of

year) at 10%, for how many years must you invest before your future value equals $364.10?

Copyright by Diane Scott Docking 201540

Set calculator to BGN mode

Input $0 PV Input -$364.10 FV Input 10 I/Y Input $100 PMT Calculate N (Cpt N)

Here are the key strokes: Already at BGN

0 364.10 10 100 N = 3

PV

I/Y

N

PMT

CPT

FV+│─

Finding “n”, “i”, and “payment” of Annuities

Finding “payment”

FV & PV of an annuity due: Example 3: How much must you invest annually (at

beginning of year) at 10%, for 3 years to accumulate a future value of $364.10 at the end of 3 years?

Copyright by Diane Scott Docking 201541

Set calculator to BGN mode

Input $0 PV Input -$364.10 FV Input 10 I/Y Input 3 N Calculate Pmt (Cpt Pmt)

Here are the key strokes: Already at BGN

0 364.10 10 3 PMT = $100

PV

I/Y

N

PMTCPT

FV+│─

42

Constructing Amortization Schedules using the Financial Calculator

Construct an amortization schedulefor a $1,000, 10% annual rate loanwith 3 equal payments in arrears (paid at end of year).

Copyright by Diane Scott Docking 2015

43

Step 1: Find the required payments.

PMT PMTPMT

0 1 2 310%

-1,000

3 10 -1000 0

INPUTS

OUTPUT

N I/Y PV FVPMT

402.11

Amortization Schedule Using Calculator

Copyright by Diane Scott Docking 2015

44

2nd AMORT:

Amortization Schedule using Calculator

Copyright by Diane Scott Docking 2015

P1 = ___ P2 = ___

BAL = _______ PRN =______ INT =______

P1 = ___ P2 = ___

BAL = _______ PRN =______ INT =______

P1 = ___ P2 = ___

BAL = _______ PRN =______ INT =______

-697.89 302.11 100.00

enter

enter 1 1

2

Ignore negative sign

2

3 3

enter

enter

enter

enter

-365.56 332.33 69.79

365.56 0 36.56

45

BEG PRN ENDYR BAL PMT INT PMT BAL

1 $1,000 $402.11 $100 $302.11$697.89

2 697.89 402.11 69.79 332.33 365.56

3 365.56 402.12 36.56 365.56 0

TOT 1,206.34 206.35 1,000

Copyright by Diane Scott Docking 2015

Amortization Schedule using Calculator

46

Example: Amortization of a Real-World Mortgage (and why to stay home with mom and dad)

Buy a $300,000 house with 20% down Finance $240,000 at 6% over 30 years Questions:

What are your monthly mortgage payments?For the first year, how much did you pay in interest and

principal?What is the loan balance at the end of year 5?For the 12th monthly payment, how much did you pay in

interest and principal?How much total interest did you pay in years 1 through 5?

Copyright by Diane Scott Docking 2015

47

Example: Amortization of a Real-World Mortgage

Questions:What are your monthly mortgage payments?

Copyright by Diane Scott Docking 2015

N = 30 yrs x 12 = 360 paymentsI/Y = 6%/12 = 0.50%

INPUTS

OUTPUT 1,438.92

360 .50 -240,000 0

N PMTI/Y PV FV

48

Questions:For the first year, how much did you pay in interest and

principal? Keep payment information in calculator.

2nd AMORT:

Copyright by Diane Scott Docking 2015

P1 = ___ P2 = ___

BAL = ___________

PRN =___________

INT =____________

-237,052.77

2,947.23

14,319.83

enter

enter 1 12

Ignore negative sign

Example: Amortization of a Real-World Mortgage

49

Questions:What is the loan balance at the end of year 5?

Keeping everything the same in the calculator

Bring back up to P1 by hitting the ↑ two times.

Copyright by Diane Scott Docking 2015

P1 = ___ P2 = ___

BAL = ___________ -223,330.46

enter

enter 60 60

Ignore negative sign

Example: Amortization of a Real-World Mortgage

50

Questions:For the 12th monthly payment, how much did you pay in interest

and principal? Keeping everything the same in the calculator

Bring back up to P1 by hitting the ↑ four times.:

Copyright by Diane Scott Docking 2015

P1 = ___ P2 = ___

BAL = ___________

PRN =___________

INT =____________

-237,052.77

252.40

1,186.53

enter

enter 12 12

Ignore negative sign

Example: Amortization of a Real-World Mortgage

51

Questions:How much total interest did you pay in years 1 through 5?

Keeping everything the same in the calculator

Bring back up to P1 by hitting the ↑ four times.:

Copyright by Diane Scott Docking 2015

P1 = ___ P2 = ___

BAL = ___________

PRN =___________

INT = ____________

-223,330.46

16,669.54

enter

enter 1 60

Ignore negative sign

Example: Amortization of a Real-World Mortgage

69,665.73