Embed Size (px)

Citation preview

1

The related literature on foreign banks

• The proponents of foreign bank entry argue that foreign banks enhance competition in domestic banking markets, improve the efficiency of domestic bank operations, provide financial services with lower costs, and play a positive role in economic growth by boosting the efficiency of resource allocation.

• Foreign banks play a favorable role in enhancing the host banking market stability.

– (e.g., Clasessens et al. (2001), Crystal et al. (2002), Clasessens and Laven (2005), Claessens and van Horen (2009), Wu et al. (2010), and Jeon et al. (2011)).

The related Literature (2)• The opponents of the growing role of foreign banks are

concerned that:– foreign banks lack hard information on the creditworthiness of smaller-

size borrowers in local markets,

– tend to have higher interest margins and profitability than domestic banks in developing countries, and

– lead domestic banking markets to lower competition.

– They are also concerned about a sudden stop or reversal of capital and credits during difficult times, especially when the parent banks in home countries suffer from the credit crunch or capital loss.

– They present evidence that foreign banks are a major channel of the financial shock transmission or contagion, and pose a significant challenge to the effectiveness of monetary policy in host economies (see, for example, Jeon et al. (2012) and Cetorelli and Goldberg (2012a, 2012b)).

2

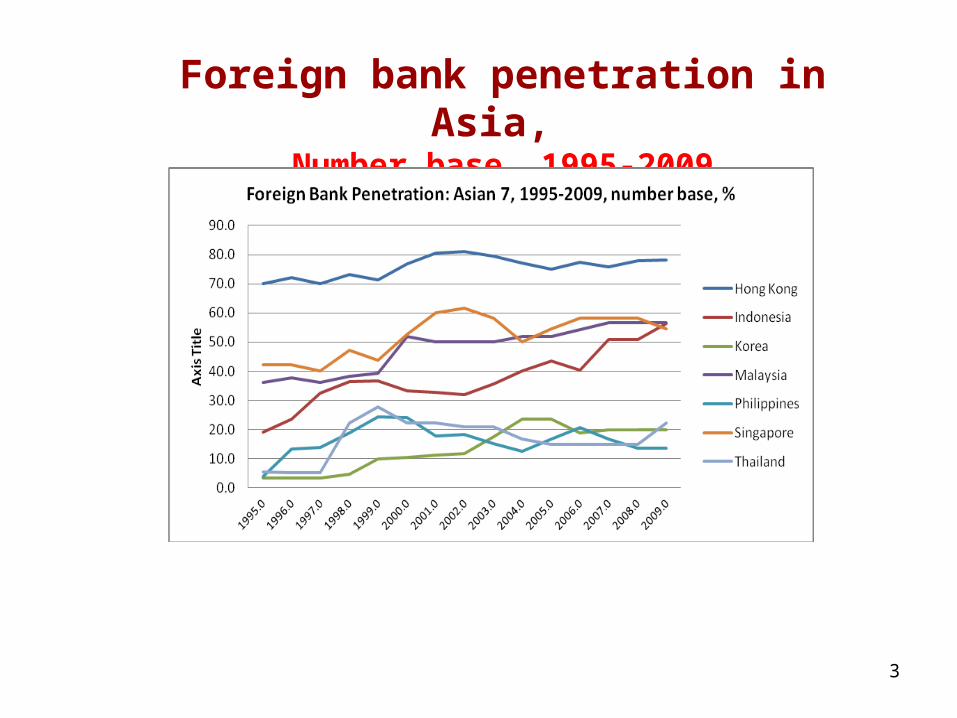

Foreign bank penetration in Asia, Number base, 1995-2009

3

Topic 6B: Global banking in emerging economiesForeign Banks in China Rev Profits

[9/26/2012, WSJ]

4

33 foreign banks (2% of the market share with $150 bil. assets) enjoyed more than doubled profit in 2011 from 2010 (note: 39% increase in profit for the sector in China).

Foreign banks in China: Challenges

• Banks last year, 2011, benefited from China's efforts to tighten lending to curb inflation and surging property prices. With loans harder to get, banks were able to charge more.

• This year, 2012, banks have posted declines in their net interest margins as authorities have cut benchmark interest rates for easy money, funding costs have risen and demand for credit has cooled.

• Major Chinese banks also are increasingly competing for the same pool of wealthy savers that foreign banks have targeted.

– "The real challenge is what to do next.…Many of the foreign banks realize that they don't have the brand recognition to compete in a bigger mass market,“

5

Foreign banks in China: Challenges (2)

• In 2010, the nation's banking regulator began pressing foreign banks to publicly disclose the information.

– No one foreign bank can own more than 20% of a state-owned bank;

– A group foreign banks can not own more than 25% of a state-owned bank.

– Various restrictions: e.g., no renminbi lending to corporates except a part of syndicated loan with Chinese banks

6

Banking in China• The China banking sector missed the recent financial crisis.

• Heavily controlled by the state, many state-owned banks—nationalization vs. Privatization

• 4 biggest Chinese banks have total assets of $4.6 tril.

– All state owned: ICBC ($1.4 tril., 24,000 branches), CCB ($1.1 tril.), ABC (1.0 tril.), BOC (1.0 tril.)

• The People’s Bank of China (1948) – China’s central bank

– The governor is Zhou Xiaochuan, 2003-

• Policy banks (4), 2nd-tier banks, joint-stock banks (10), China Minseng Bank (private), small regional commercial banks (100), postal offices (76,000)

• And foreign banks, foreign investment banks (JVs)– Goldman Sachs + Fang Fenglei (2004), UBS + Beijing Securities

7

8

Monetary policy instruments in China

9

China: Regulated interest rates

10

China: Net liquidity injection and interbank interest rates

11

The Role of Foreign Banks inMonetary Policy Transmission:

Evidence from Asia during the crisis of 2008-9

Bang Nam Jeona,*

Ji Wub

a Department of Economics & International Business, Bennett S. LeBow College of Business,

Drexel University, Philadelphia PA, U.S.A.b School of Business Administration, Penn State Harrisburg,

Middletown, PA, U.S.A.

*Corresponding author and presenter. [email protected] (B.Jeon)

The 2012 KDI - KAEA Conference June 22, 2012, Seoul, Korea

13

Objective:

This paper examines the impact of increased foreign bank penetration on the monetary policy transmission mechanism, a la bank lending channel, in emerging Asian economies during the period from 2000 to 2009, with a specific focus on the recent global financial crisis of 2008-9.

specifically focus on the bank lending channel

Using bank-level data from 2000 to 2009, covering 136 foreign bank subsidiaries, of 74 multinational banks, located in 7 emerging Asian economies,

Hong Kong SAR, Indonesia, Korea, Malaysia, Philippines, Singapore, and Thailand

14

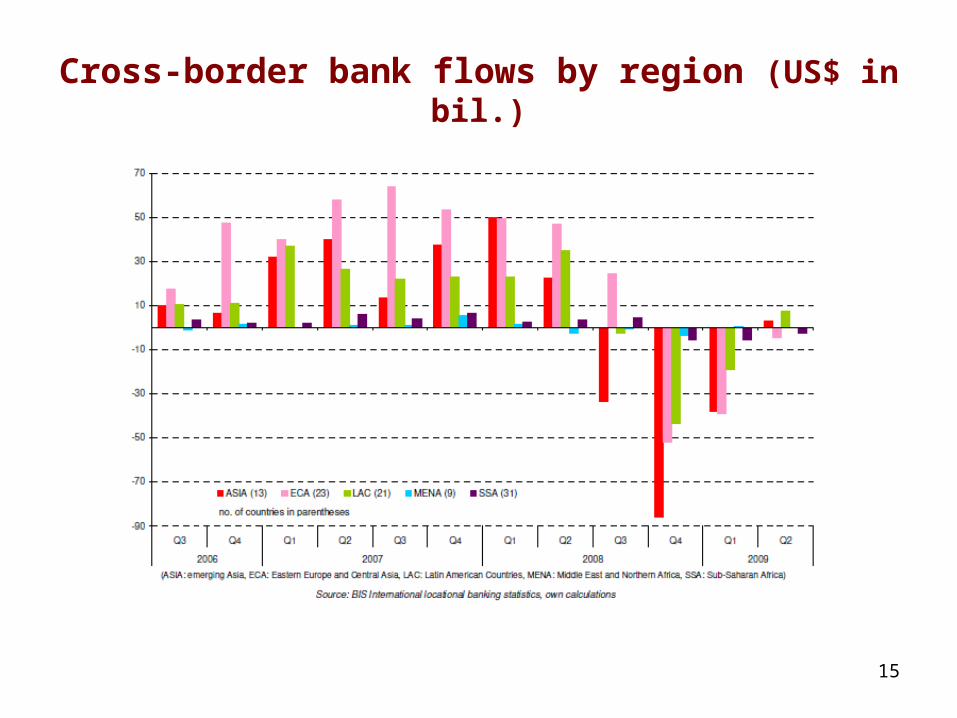

Source: BIS Locational Banking Statistics and Cetorelli and Goldberg (2010)

Cross-border bank flows by region (US$ in bil.)

15

Foreign banks’ cross-border lending to the Asian economies (in $billion), 2000-2009

16

International Capital flows via multinational banking

17

Foreign subsidiaries

Parent banks

Domestic banks

Cross-border lending

Internal capital markets

[The host country] [The home country]

Other global banks

Contagion links: funding shock, liquidity shock, cash flow shock,…

Loan

s to local firm

s

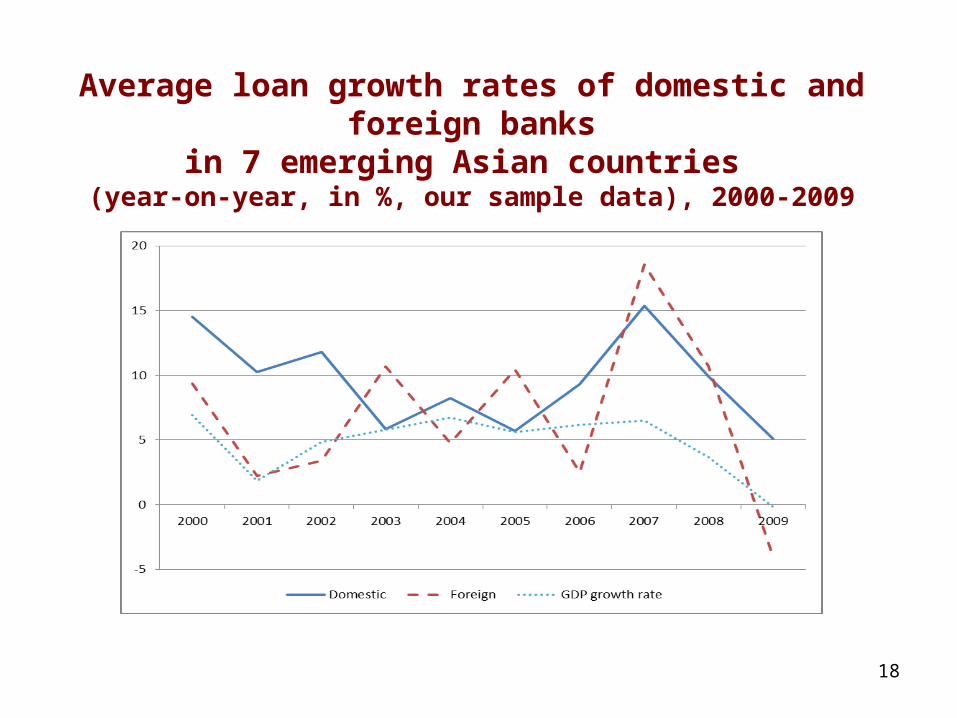

Average loan growth rates of domestic and foreign banksin 7 emerging Asian countries

(year-on-year, in %, our sample data), 2000-2009

18

19

Main findings/contributions:

– We present consistent evidence on the buffering impact of foreign banks on the effectiveness of monetary policy in emerging Asian economies during the period of global financial crisis.

– We identify specific conditions and environments under which that impact works more fully in the host banking markets,

• including the type of monetary policy shocks,

• the severity of shocks upon parent banks during global crisis,

• the dependence of parent banks on wholesale funding,

• the country origin of foreign banks, and

• their entry modes.

Main findings/contributions (2):

• The main findings of this paper will have useful policy implications for monetary authorities and bank regulators to minimize the adverse effects of the increasing presence of foreign banks on the stability and effectiveness of monetary policy in the region.

20

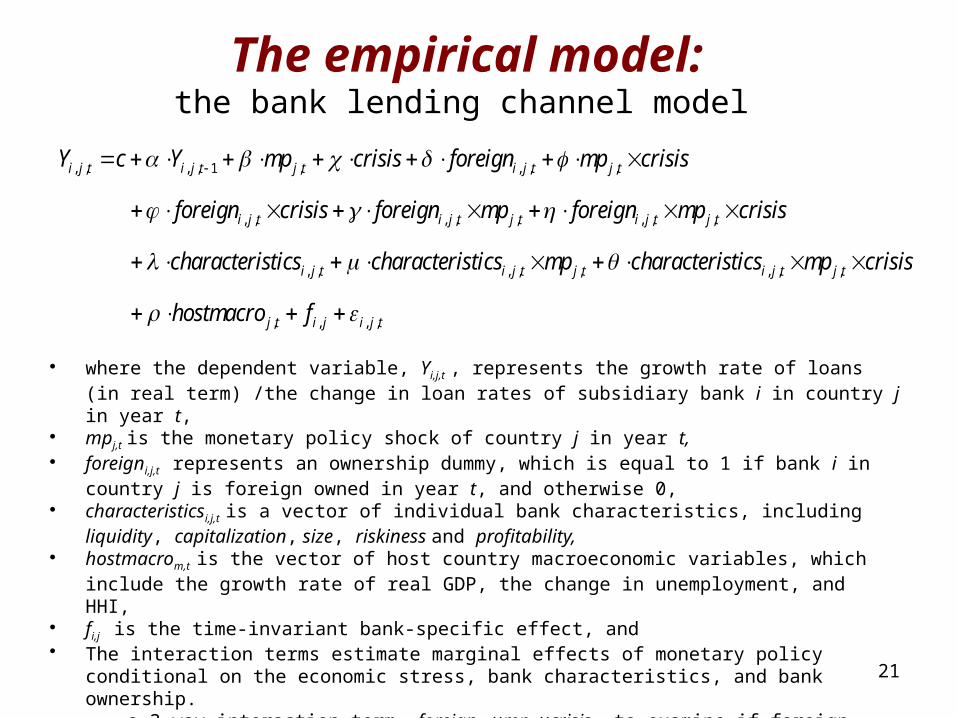

The empirical model: the bank lending channel model

• where the dependent variable, Yi,j,t , represents the growth rate of loans (in real term) /the change in loan rates of subsidiary bank i in country j in year t,

• mpj,t is the monetary policy shock of country j in year t,• foreigni,j,t represents an ownership dummy, which is equal to 1 if bank i in country j is foreign owned in year

t, and otherwise 0,• characteristicsi,j,t is a vector of individual bank characteristics, including liquidity, capitalization, size,

riskiness and profitability,• hostmacrom,t is the vector of host country macroeconomic variables, which include the growth rate of real

GDP, the change in unemployment, and HHI,• fi,j is the time-invariant bank-specific effect, and• The interaction terms estimate marginal effects of monetary policy conditional on the economic stress, bank

characteristics, and bank ownership.– a 3-way interaction term, foreigni,j,t×mpj,t×crisis, to examine if foreign banks respond

differently to changes in monetary policy during the 2008-09 crisis period. 21

, , , , 1 , , , ,

, , , , , , , ,

, ,

i j t i j t j t i j t j t

i j t i j t j t i j t j t

i j t

Y c Y mp crisis foreign mp crisis

foreign crisis foreign mp foreign mp crisis

characteristics characteristi

, , , , , ,

, , , ,

i j t j t i j t j t

j t i j i j t

cs mp characteristics mp crisis

hostmacro f

Interpretation of the estimated coefficients• β: the loan (loan rate)-monetary policy coefficient on mp

– domestic bank’s loan response to changes in monetary policy– its expected sign is “-”

• γ: the 2-way interaction coefficient on foreign×mp– ”the marginal effect of monetary policy on foreign subsidiary’s lending

during tranquil periods”

• η: the 3-way interaction coefficient on foreign×mp×crisis– ”the marginal effect of monetary policy on foreign subsidiary’s lending

during crisis periods” – a buffering effect when its sign is “+”

• β + γ + η– ”overall effects”– foreign bank subsidiary’s responses to host monetary policy during

crisis periods 22

List of multinational banks and the distribution of foreign bank subsidiaries in emerging and developing economies

23

Multinational bank Home country Host countries U.S. and Canada 1 Bank of America US HK(2), MY 2 Bank of New York Mellon US HK 3 Bank of Nova Scotia (The) - SCOTIABANK CA HK, MY 4 Canadian Imperial Bank of Commerce CA HK, SG 5 Citigroup US HK(3), KR, MY, PH, SG 6 JP Morgan Chase US HK(2), MY 7 Lone Star Fund US KR 8 Newbridge Capital US KR 9 Royal Bank of Canada CA SG 10 Toronto Dominion Bank CA SG Europe 11 ABN Amro NL MY, PH, TH 12 Banco Santander ES PH 13 Bayerische Landesbank DE SG 14 BNP Paribas FR ID 15 Commerzbank AG DE ID 16 Credit Agricole S.A. FR ID 17 Credit Lyonnais FR ID 18 Deutsche Bank AG DE MY 19 Fortis BE HK 20 HSBC GB HK(2), ID, MY 21 ICB Financial Group Holdings AG CH ID 22 ING Bank NL ID, SG 23 Rabobank Group NL ID(2), SG 24 Royal Bank of Scotland Group GB ID, MY 25 Societe Generale FR ID, KR, TH 26 Standard Chartered GB HK(3), ID, KR, MY, TH 27 WestLB AG DE SG

24

Japan 28 Bank of Tokyo - Mitsubishi UFJ JP ID, MY, PH 29 Dai-Ichi Kangyo Bank Ltd DKB JP HK 30 Fuji Bank JP ID 31 Mizuho Financial Group JP HK, ID 32 Resona Bank JP ID 33 Sumitomo Mitsui Banking Corporation JP ID, SG 34 UFJ Bank JP ID Other Asian economies 35 Allied Banking Corporation PH HK 36 Banco Delta Asia S.A.R.L. MO HK 37 Bangkok Bank Public Company Limited TH MY 38 Bank of Baroda IN HK 39 Bank of China CN HK(4), MY 40 Bank of India IN ID 41 Bank Internasional Indonesia ID HK 42 China Construction Bank CN HK(2) 43 China Merchants Bank Co Ltd CN HK 44 Chinatrust Financial Holding Company TW HK, ID, PH 45 Chohung Bank KR HK 46 CIMB Bank Berhad MY ID, TH 47 CITIC Industrial Bank CN HK 48 DBS Group SG HK(2), ID(2), PH, TH 49 Fubon Financial Holding Co Ltd TW HK 50 Grand Commercial Bank TW HK 51 Hana Bank KR ID 52 Hong Leong Bank Berhad MY HK(2), PH, SG 53 Industrial & Commercial Bank of China (The) -

ICBC CN HK(2), ID

54 Khazanah Nasional Bhd MY ID 55 Kookmin Bank KR HK 56 Korea Exchange Bank KR ID 57 Malayan Banking Berhad (Maybank) MY ID(2), PH 58 Mega International Commercial Bank TW TH 59 Oversea-Chinese Banking Corporation Limited

OCBC SG ID(2), MY

25

60 Overseas Union Bank SG MY 61 Public Bank Berhad MY HK 62 RHB Capital Bhd MY ID 63 Shanghai Commercial & Savings Bank TW HK 64 Shinhan Bank KR HK 65 Southern Bank Berhad MY SG 66 United Overseas Bank SG ID(2), MY, PH, TH(2) 67 Woori Bank KR ID Other 68 Absa Group ZA HK 69 Australia and New Zealand Banking Group AU ID 70 Commonwealth Bank of Australia AU ID 71 Islamic Development Bank SA ID 72 LGT Bank in Liechtenstein LI SG 73 National Australia Bank AU SG 74 Standard Bank Group ZA HK

Note: The number of subsidiaries in parenthesis. AU=Australia, BE=Belgium, CA=Canada, CN=China, DE=Germany, ES=Spain, FR=France, GB=U.K., HK=Hong Kong SAR, ID=Indonesia, IN=India, JP=Japan, KR=Korea, LI= Liechtenstein, MO=Macau, MY=Malaysia, NL=Netherlands, PH=Philippines, SA=Saudi Arabia, SG=Singapore, TH=Thailand, TW=Taiwan, US=U.S.A., ZA=South Africa.

U.S. Europe Japan Other Asian

Countries Other Total

Hong Kong 8 6 2 28 4 48

Indonesia 0 12 6 17 3 38

Korea 3 2 0 0 0 5

Malaysia 3 5 1 5 1 15

Philippines 1 2 1 5 0 9

Singapore 1 5 1 2 4 13

Thailand 0 3 0 5 0 8

Total 16 35 11 62 12 136

26

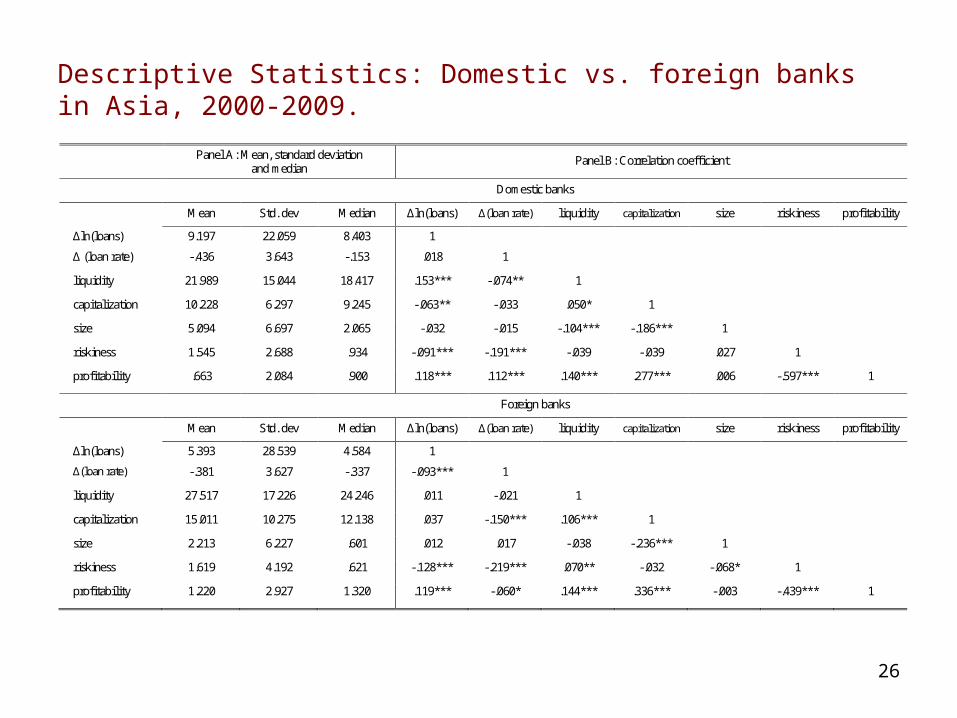

Descriptive Statistics: Domestic vs. foreign banks in Asia, 2000-2009.

Panel A: Mean, standard deviation and median

Panel B: Correlation coefficient

Domestic banks

Mean Std. dev Median ∆ln(loans) ∆(loan rate) liquidity capitalization size riskiness profitability

∆ln(loans) 9.197 22.059 8.403 1

∆ (loan rate) -.436 3.643 -.153 .018 1

liquidity 21.989 15.044 18.417 .153*** -.074** 1

capitalization 10.228 6.297 9.245 -.063** -.033 .050* 1

size 5.094 6.697 2.065 -.032 -.015 -.104*** -.186*** 1

riskiness 1.545 2.688 .934 -.091*** -.191*** -.039 -.039 .027 1

profitability .663 2.084 .900 .118*** .112*** .140*** .277*** .006 -.597*** 1

Foreign banks

Mean Std. dev Median ∆ln(loans) ∆(loan rate) liquidity capitalization size riskiness profitability

∆ln(loans) 5.393 28.539 4.584 1

∆(loan rate) -.381 3.627 -.337 -.093*** 1

liquidity 27.517 17.226 24.246 .011 -.021 1

capitalization 15.011 10.275 12.138 .037 -.150*** .106*** 1

size 2.213 6.227 .601 .012 .017 -.038 -.236*** 1

riskiness 1.619 4.192 .621 -.128*** -.219*** .070** -.032 -.068* 1

profitability 1.220 2.927 1.320 .119*** -.060* .144*** .336*** -.003 -.439*** 1

Empirical results

• Baseline estimation

– Fixed effects estimator and system GMM estimator

– Bank characteristics are shown to play important roles in determining

a bank’s loan growth, in particular, its liquidity and capitalization.

– Macroeconomic conditions are shown to play a role in affecting a

bank’s loan growth in Asia.

– δ (foreign bank) < 0, φ (foreign bank × crisis) < 0.

27

The loan growth equation: The impact of monetary policy on loan growth for domestic vs. foreign banks

• β (mp) < 0• γ (foreign×mp) ? 0• η (foreign×mp×crisis) > 0

– implying that foreign banks are less sensitive to monetary policy in adjusting the growth rate of their lending during crisis periods.

– also indicating that there exists a buffering / dampening effect of foreign banks on the potency of monetary policy during the 2008-09 global financial crisis period.

28

The loan growth equation: The impact of monetary policy on loan growth on domestic vs. foreign banks (2)

• As an effort to bail out from a recessionary economy and credit-crunch stricken banks during the 2008-9 global financial crisis period, most monetary authorities in Asia adopted expansionary monetary policy in 2008 and 2009. – which led to an effect of increase in loans by domestic banks (reflected by

negative numbers for the sum of the coefficients on mp and mp×crisis).

• β + γ + η > 0 for foreign banks during the crisis period

– However, in contrast to the behavior of domestic banks, foreign banks have been observed only to cut down their lending (reflected by the sum of the coefficients on mp, mp×foreign and foreign×mp×crisis), resulting in less pronounced impacts of eased monetary policy on foreign banks’ lending.

– This provides evidence that foreign banks in Asia weakened the effectiveness of the monetary policy transmission mechanism during the 2008-9 global financial crisis period.

29

Why?• Bank lending channel – supply side and bank characteristics

• Demand factors• Internal capital markets

– Multinational banks manage their liquidity on a global base, such that the liquidity constraints and capital inadequacy in multinational banks during the global financial turmoil cause a “reversed” capital flow, via internal capital markets, from foreign subsidiaries in host countries to their headquarters in home countries.

– When host central banks relax their monetary policy, subsidiaries in the host country have more deposits available to lend and these resources can be reallocated toward the liquidity-seeking and capital-needing headquarters in the home country. As a result, subsidiaries reduce, rather than increase, their loans within the boundary of host countries in reaction to the expansionary monetary policy.

• Cetorelli and Goldberg (2011, 2012), Jeon, Olivero and Wu (2012)

30

31

Source: Cetorelli and Goldberg (2011)

The asymmetric effects of changes in monetary policy on loan growth and loan rates of domestic and foreign banks in Asia, 2000-9:

Expansionary vs. contractionary monetary policy

32

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Hong Kong SAR + − − − + + − − − −

Indonesia − + − − − + + − + −

Korea + − − − − − + + + −

Malaysia − + − + − + + + − −

Philippines + − − − + + + − − −

Singapore + − − − + + + − − −

Thailand + + − − − + + − − −

Note: “+” represents contractionary monetary policy, and “-” denotes expansionary monetary policy.

The asymmetric effects of changes in monetary policy on loan growth and loan rates of domestic and foreign banks in Asia, 2000-9:

Expansionary vs. contractionary monetary policy

33

Panel A: Dependent variable: ∆ln(loans)i,j,t Panel B: Dependent variable: ∆loan ratei,j,t Fixed effects System GMM Fixed effects System GMM (1) (2) (3) (4) (5) (6) (7) (8)

Expansionary policy

mp -1.074**

(.029)

-1.940*

(.082)

-.159

(.822)

-3.064*

(.080)

.533***

(.000)

.550***

(.000)

.386***

(.000)

.354*

(.053)

foreign × mp -1.163 (.294)

-2.110** (.022)

.687 (.549)

.256 (.844)

-.057 (.481)

-.154** (.029)

-.047 (.710)

.042 (.729)

foreign × mp × crisis 7.680** (.014)

7.432** (.017)

7.305** (.018)

6.029* (.096)

-.334 (.205)

-.332 (.175)

-.653** (.018)

-.669* (.073)

observations (banks)

874

(202)

874

(202)

874

(202)

874

(202)

872

(202)

872

(202)

872

(202)

872

(202)

R2 .231 .261 .382 .416

AR(1)/AR(2) .000/ .780 .000/ .526 .000/.920 .000/.639

Hansen J test .449 .516 .464 .543

Contractionary policy

mp 2.086

(.247)

2.562

(.325)

-2.151***

(.007)

-5.380*

(.063)

.679***

(.000)

1.031***

(.000)

.609***

(.000)

.811***

(.000)

foreign × mp -6.601*** (.000)

-7.183*** (.000)

.823 (.534)

2.190 (.420)

-.331** (.011)

-.219* (.067)

-.027 (.815)

-.065 (.739)

foreign × mp × crisis .849 (.794)

-.893 (.822)

19.700* (.099)

11.175 (.563)

.355 (.250)

-.149 (.660)

.638 (.303)

.552 (.508)

observations (banks)

589

(197)

589

(197)

589

(197)

589

(197)

588

(197)

588

(197)

588

(197)

588

(197)

R2 .163 .194 .183 .223

AR(1)/AR(2) .013/ .430 .042/.879 .005/.841 .012/.825

Hansen J test .469 .708 .150 .189

The asymmetric effects of changes in monetary policy on loan growth and loan rates of domestic and foreign banks in Asia, 2000-9: Foreign bank subsidiaries whose parent banks are more adversely affected vs.

less affected

34

Panel A: Dependent variable: ∆ln(loans)i,j,t Panel B: Dependent variable: ∆loan ratei,j,t Fixed effects System GMM Fixed effects System GMM (1) (2) (3) (4) (5) (6) (7) (8)

mp -.671**

(.030)

-1.142*

(.096)

-1.000*

(.093)

-2.795

(.115)

.445***

(.000)

.359***

(.000)

.460***

(.000)

.421*

(.080)

foreign (parent more affected)× mp

.764 (.321)

.553 (.427)

1.023 (.413)

-.736 (.597)

-.034 (.440)

-.090 (.136)

-.187 (.307)

.007 (.967)

foreign (parent less affected) × mp

-1.277* (.068)

-1.622*** (.006)

-.131 (.913)

-1.500 (.240)

-.060 (.283)

-.101* (.086)

.106 (.574)

.170 (.334)

foreign (parent more affected)× mp × crisis

8.944*** (.001)

7.938*** (.003)

10.903** (.023)

10.374* (.088)

-.691** (.020)

-.743** (.028)

-1.103* (.092)

-1.314* (.087)

foreign (parent less affected) × mp × crisis

1.412 (.443)

1.128 (.528)

2.751 (.400)

4.095 (.251)

-.222* (.093)

-.268* (.063)

-.614* (.078)

-.588 (.139)

observations (banks)

1463

(216)

1463

(216)

1463

(216)

1463

(216)

1460

(216)

1460

(216)

1460

(216)

1460

(216)

R2 .168 .186 .362 .369

AR(1)/AR(2) .000/.419 .000/.125 .000/.570 .000/.174

Hansen J test .697 .736 .303 .281

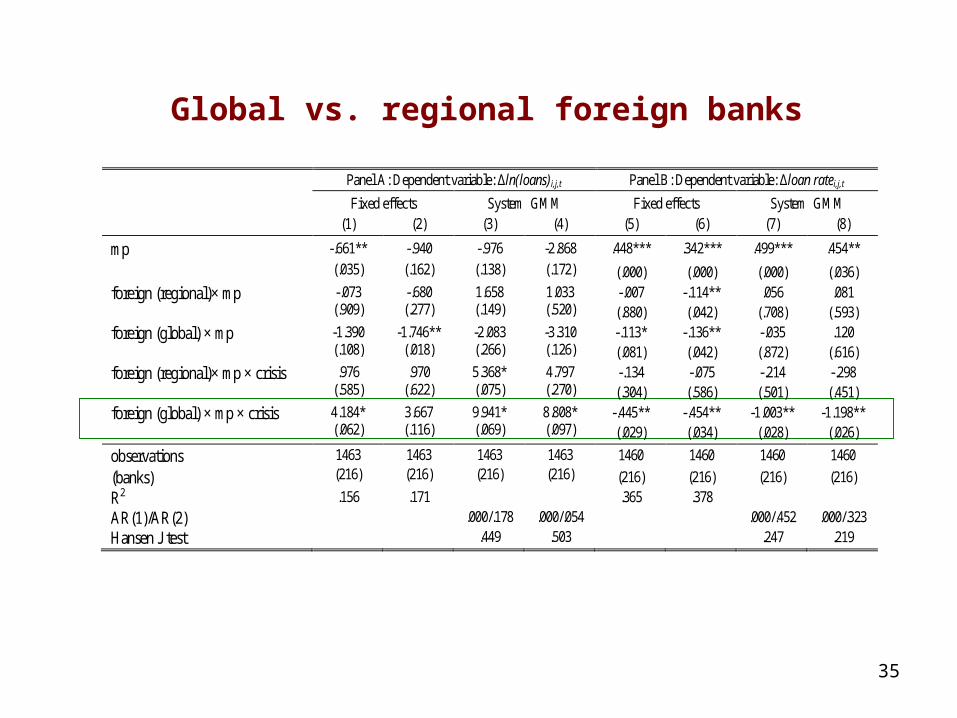

Global vs. regional foreign banks

35

Panel A: Dependent variable: ∆ln(loans)i,j,t Panel B: Dependent variable: ∆loan ratei,j,t Fixed effects System GMM Fixed effects System GMM (1) (2) (3) (4) (5) (6) (7) (8)

mp -.661**

(.035)

-.940

(.162)

-.976

(.138)

-2.868

(.172)

.448***

(.000)

.342***

(.000)

.499***

(.000)

.454**

(.036)

foreign (regional)× mp -.073 (.909)

-.680 (.277)

1.658 (.149)

1.033 (.520)

-.007 (.880)

-.114** (.042)

.056 (.708)

.081 (.593)

foreign (global) × mp -1.390 (.108)

-1.746** (.018)

-2.083 (.266)

-3.310 (.126)

-.113* (.081)

-.136** (.042)

-.035 (.872)

.120 (.616)

foreign (regional)× mp × crisis .976 (.585)

.970 (.622)

5.368* (.075)

4.797 (.270)

-.134 (.304)

-.075 (.586)

-.214 (.501)

-.298 (.451)

foreign (global) × mp × crisis 4.184* (.062)

3.667 (.116)

9.941* (.069)

8.808* (.097)

-.445** (.029)

-.454** (.034)

-1.003** (.028)

-1.198** (.026)

observations (banks)

1463 (216)

1463 (216)

1463 (216)

1463 (216)

1460

(216)

1460

(216)

1460

(216)

1460

(216)

R2 .156 .171 .365 .378

AR(1)/AR(2) .000/.178 .000/.054 .000/.452 .000/.323

Hansen J test .449 .503 .247 .219

De novo vs. M&A foreign bank subsidiaries

36

Panel A: Dependent variable: ∆ln(loans)i,j,t Panel B: Dependent variable: ∆loan ratei,j,t

Fixed effects System GMM Fixed effects System GMM (1) (2) (3) (4) (5) (6) (7) (8)

mp -.652**

(.037)

-1.310**

(.039)

-1.039

(.181)

-1.799

(.446)

.444***

(.000)

.322***

(.000)

.434***

(.000)

.379*

(.100)

foreign (de novo)× mp -1.155* (.090)

-1.799*** (.002)

1.090 (.466)

-3.016** (.042)

-.071 (.209)

-.154*** (.004)

.088 (.536)

.165 (.434)

foreign (M&A) × mp .306 (.668)

.077 (.910)

-.526 (.683)

-1.547 (.275)

-.028 (.564)

-.070 (.240)

-.094 (.680)

-.050 (.833)

foreign (de novo)× mp × crisis 5.038** (.043)

4.631* (.076)

9.235* (.087)

8.330* (.073)

-.314* (.099)

-.368 (.132)

-.802* (.072)

-.993* (.094)

foreign (M&A) × mp × crisis .085 (.956)

-.674 (.671)

6.804 (.272)

2.058 (.558)

-.287* (.064)

-.232 (.136)

.085 (.892)

.019 (.976)

observations (banks)

1463

(216)

1463

(216)

1463

(216)

1463

(216)

1460

(216)

1460

(216)

1460

(216)

1460

(216)

R2 .156 .179 .366 .382

AR(1)/AR(2) .000/.727 .000/.070 .000/.368 .000/.315

Hansen J test .157 .316 .252 .221

Robustness tests

• Robustness test 1: alternative measure of monetary policy

• Robustness test 2: without Hong Kong SAR and Singapore

• Robustness test 3: the extended crisis period of 2007-09

• Robustness test 4: to add foreign × real GDP growth × crisis and foreign × unemployment × crisis

37

38

Conclusions and policy implications This paper presents consistent evidence that there exist heterogeneous

responses on loan growth and loan interest rates between domestic banks and foreign-owned banks in response to changes in monetary policy in the host emerging Asian economies during the recent global financial crisis of 2008-9.

We find that first, foreign banks overall do not show distinctive behavior from domestic banks in adjusting loan growth and loan interest rates in host Asian banking markets during non-crisis, tranquil periods, and

second, during crisis periods, however, foreign banks play a buffering or even hampering role in affecting the monetary policy transmission mechanism by adjusting loan growth and loan interest rates in a way opposite to domestic banks.

This finding is consistent with the proposition that, when global banks encounter liquidity shocks in their home countries, they conduct a global reallocation of liquidity from foreign subsidiaries in host countries to the parent banks in home countries using internal capital markets (Cetorelli and Goldberg (2011), Jeon et al. (2012))

Conclusions and policy implications (2)

• We present empirical evidence that the buffering effects of foreign banks in the Asian banking markets on the efficiency of monetary policy transmission during crisis periods become more conspicuous under conditions,

– (1) when an expansionary monetary policy, instead of a contractionary monetary policy, is conducted in the host countries;

– (2) for foreign banks whose parent banks in home countries are more adversely affected;

– (3) for foreign banks whose parent banks are more dependent on non-deposits, wholesale markets funding;

– (4) for global foreign banks more than Asia-regional foreign banks; and

– (5) for foreign banks entered the host banking markets via a greenfield entry mode rather than an M&A entry mode.

39

Conclusions and policy implications (3)

• An important policy implication for both policy makers and banking regulators:

• When monetary authorities in host countries conduct monetary policies—expansionary or contractionary--during crisis periods to bail them out from the credit crunch and spillover effects of financial shocks from abroad,

• Monetary policy authority must take into account the buffering or hampering effects of foreign banks on the effectiveness of the monetary policy transmission mechanism in the host countries.

• The magnitude of the offsetting effects by foreign banks varies according to different factors originated from various bank-specific, host banking-market specific, and policy-specific conditions, as identified in this paper.

• This challenge facing monetary authorities in emerging Asian economies is expected to remain significant and become even larger as the level of foreign bank penetration in the Asian banking markets continues rising in the near future.

40