Embed Size (px)

Citation preview

1

The presumed relationships between accountability processes and

performance in the UK’s private finance initiative (PFI)

Good Governance – Contributing to Better Performance, IPA/CIPFA, Croke Park Conference Centre

10 December 2006

Copyright I. Demirag Dec2007

Professor Istemi Demirag,Management School

Queen’s University Belfast

2

Purpose of the Paper

To explore and theorize the nature of the ‘problematic’ relationship between accountability and performance

To identify some of the mechanisms that may link accountability and performance in the case of Private Finance Initiative (PFI) in the UK

3

Conceptual Frameworks for Accountability

Accountability A complex, abstract and elusive concept

‘the giving and demanding of reasons for conduct‘

Management of Expectations

Internal (relating to organisational hierarchy) or external (relating to diverse interest groups)

5

Conceptual Frameworks for Accountability

Formal forms of accountability:

Discursive or communitarian accountability

Traditional or contractual accountability

Managerial accountability

Parliamentary accountability

6

M.Dubnick’s Cultures of Accountability

Answerability cultures reflect hierarchical and other forms of structured social settings where individuals perceive themselves as responsible for reporting, justifying or explaining their actions to others.

Liability cultures represent settings where the individuals regard themselves as subject to a system of rules and laws that carry the potential for sanctions (positive or negative).

Blameworthiness cultures stress the sense of responsibility within a moral community where expectations are generalized rather than specific to individuals or their roles in society.

Attributability cultures focus attention on the roles that individuals play and the expectations associated with those roles.

7

Hypothesized Relationships

Given these variations in accountability cultures, it is hypothesized that an effort to impact on the performance of an individual or any group of individuals would be most effective if the appropriate amounts and forms of accountability mechanisms were applied to that individual or group.

It follows that inappropriate amounts and a misfit of accountability mechanisms and accountability cultures will result in less success in achieving improved performance through accountability or, worse still, what O’Neill terms “counterproductive” performance.

8

*AT

*

1BT *

2BT

B

A

Accountability0

A

1B

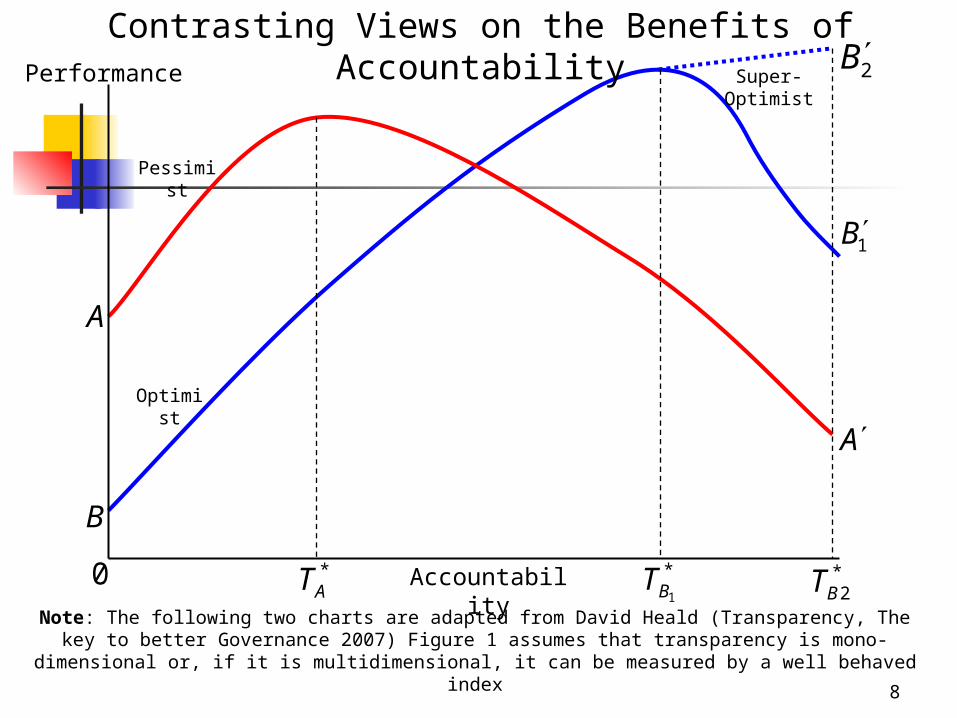

2BContrasting Views on the Benefits of Accountability

Performance

Pessimist

Optimist

Super-Optimist

Note: The following two charts are adapted from David Heald (Transparency, The key to better Governance 2007) Figure 1 assumes that transparency is mono-dimensional or, if it is multidimensional, it can be

measured by a well behaved index

9

1t Time0t

Nominal versus Effective AccountabilityAccountability

Accountability

Illusion

2t 3t

NT3

NE TT 00 ,

ET3

10

Conceptual framework for Performance

NPM reforms Assume that these will improve performance of public services

(See critiques by, Hood 1991, 1995). Inculcate new performance measurement based accountability

systems in an attempt to improve the quality of public services.

Performance is a problematic concept because it is hard to,

Define performance. Set performance standards Measure performance (i.e. output and outcomes) of a

programme (Humphrey, Miller, Scapens, (1993)

11

Operationalising performance in PPP/PFI contracts

Performance is considered to be a concept synonymous to value for money (VFM) and has been broadly defined in terms of the 3Es, economy, efficiency and effectiveness (Glynn, 1985; Glynn and Murphy, 1996).

12

PFI

Private Finance Initiative (PFI) is a form of PPP where the needs for projects and objectives can be identified and related to a single project with identifiable cash inflows and outflows and expected responsibilities – usually 25-30 years.

Thus accountability is either non-existent or in the future

(Accountability after lifetime!).

13

Characteristics of PPPs? A new phenomena?

Reducing public sector entity - Public sector responsible for services but not delivery - Relationships managed at relatively low level within public

sector entity

Six stages of PPPs, proposal, negotiation, contract, construction, operation and termination

- Very long term contracts and few sanctions, unequal power relations

Multiple private sector partners which may change over time with different interests

- Subcontracting – costs and output measures diffused thru supply chain

information deficit due to commercial sensitivity

14

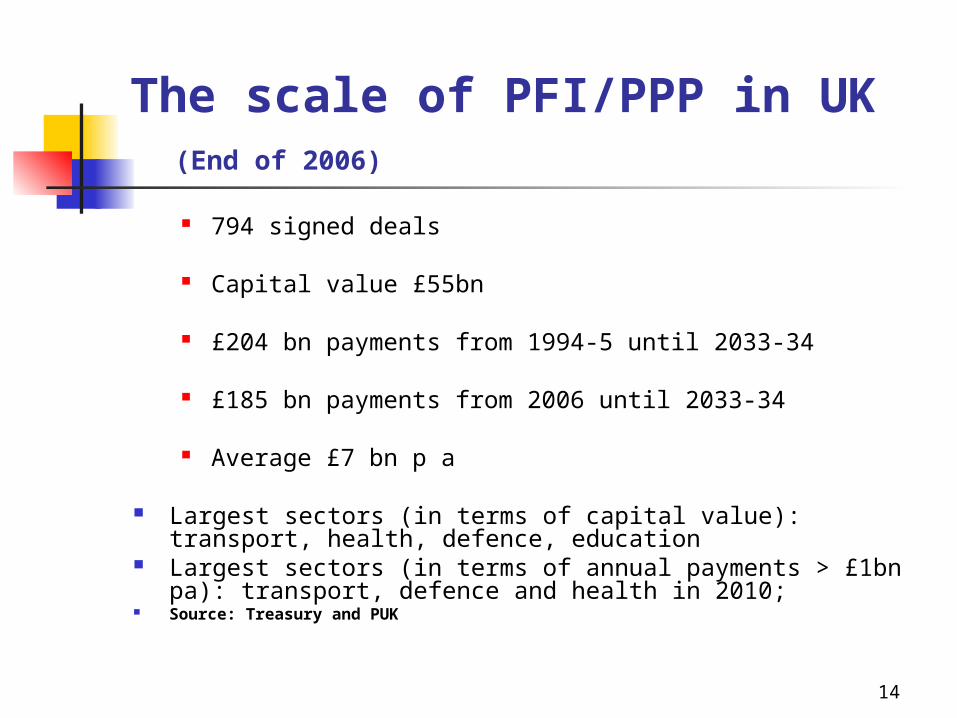

The scale of PFI/PPP in UK (End of 2006)

794 signed deals

Capital value £55bn

£204 bn payments from 1994-5 until 2033-34

£185 bn payments from 2006 until 2033-34

Average £7 bn p a

Largest sectors (in terms of capital value): transport, health, defence, education

Largest sectors (in terms of annual payments > £1bn pa): transport, defence and health in 2010;

Source: Treasury and PUK

15

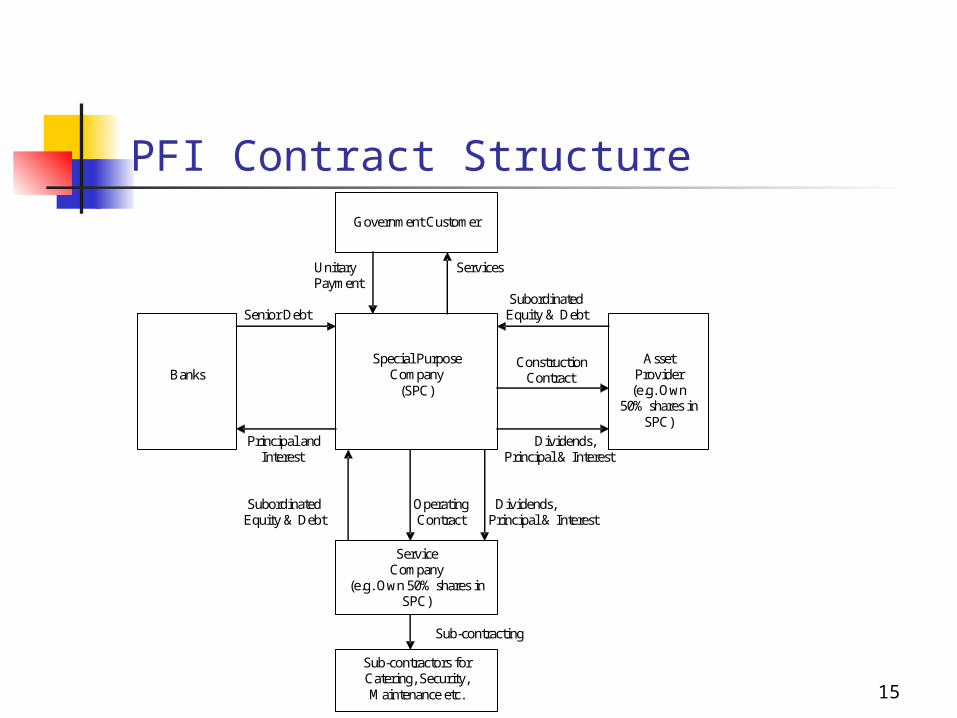

PFI Contract Structure Unitary Services Payment Subordinated Senior Debt Equity & Debt Construction Contract

Principal and Dividends,

Interest Principal & Interest Subordinated Operating Dividends, Equity & Debt Contract Principal & Interest

Sub-contracting

Government Customer

Banks

Special Purpose Company

(SPC)

Asset Provider

(e.g. Own 50% shares in

SPC)

Service Company

(e.g. Own 50% shares in SPC)

Sub-contractors for Catering, Security, Maintenance etc.

16

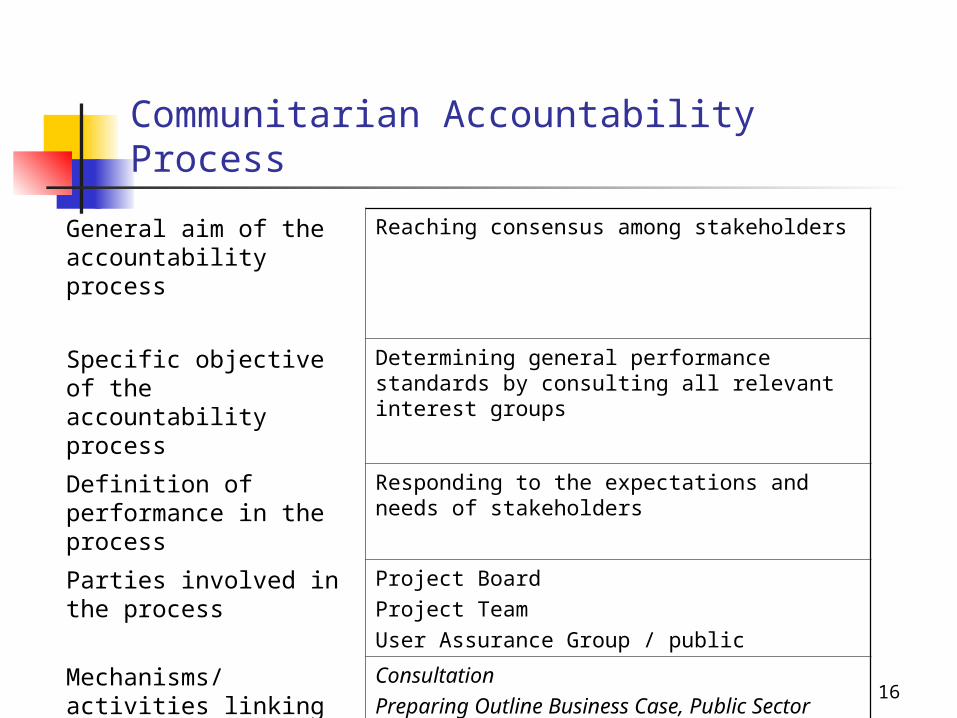

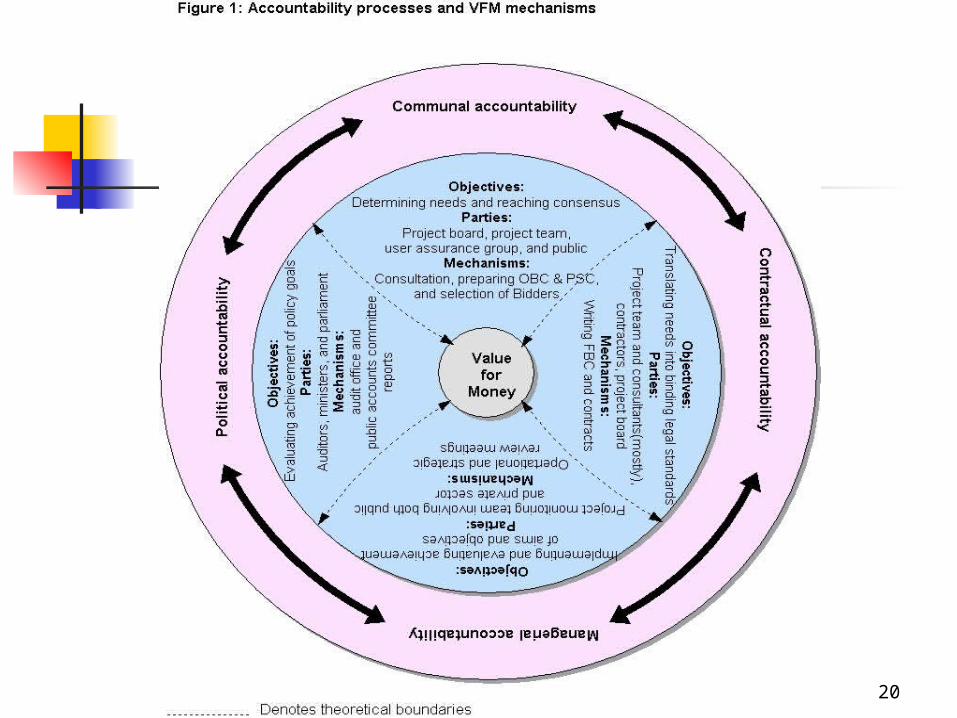

Communitarian Accountability Process

General aim of the accountability process

Reaching consensus among stakeholders

Specific objective of the accountability process

Determining general performance standards by consulting all relevant interest groups

Definition of performance in the process

Responding to the expectations and needs of stakeholders

Parties involved in the process

Project BoardProject Team User Assurance Group / public

Mechanisms/ activities linking accountability and performance

Consultation Preparing Outline Business Case, Public Sector ComparatorSelection of Bidders

17

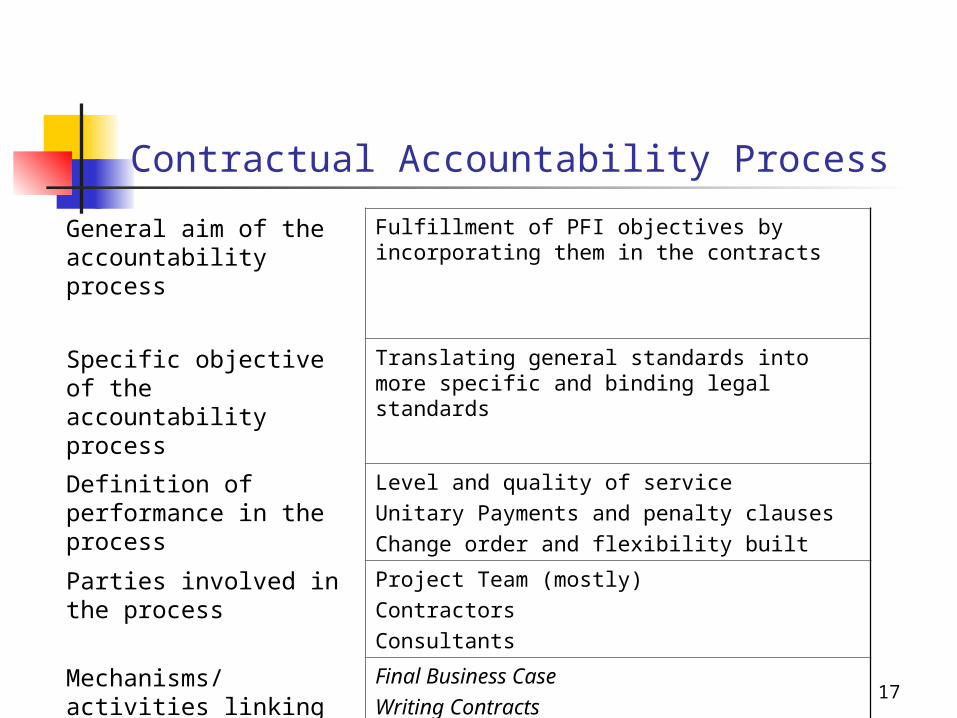

Contractual Accountability Process

General aim of the accountability process

Fulfillment of PFI objectives by incorporating them in the contracts

Specific objective of the accountability process

Translating general standards into more specific and binding legal standards

Definition of performance in the process

Level and quality of serviceUnitary Payments and penalty clausesChange order and flexibility built

Parties involved in the process

Project Team (mostly)ContractorsConsultants

Mechanisms/ activities linking accountability and performance

Final Business CaseWriting Contracts

18

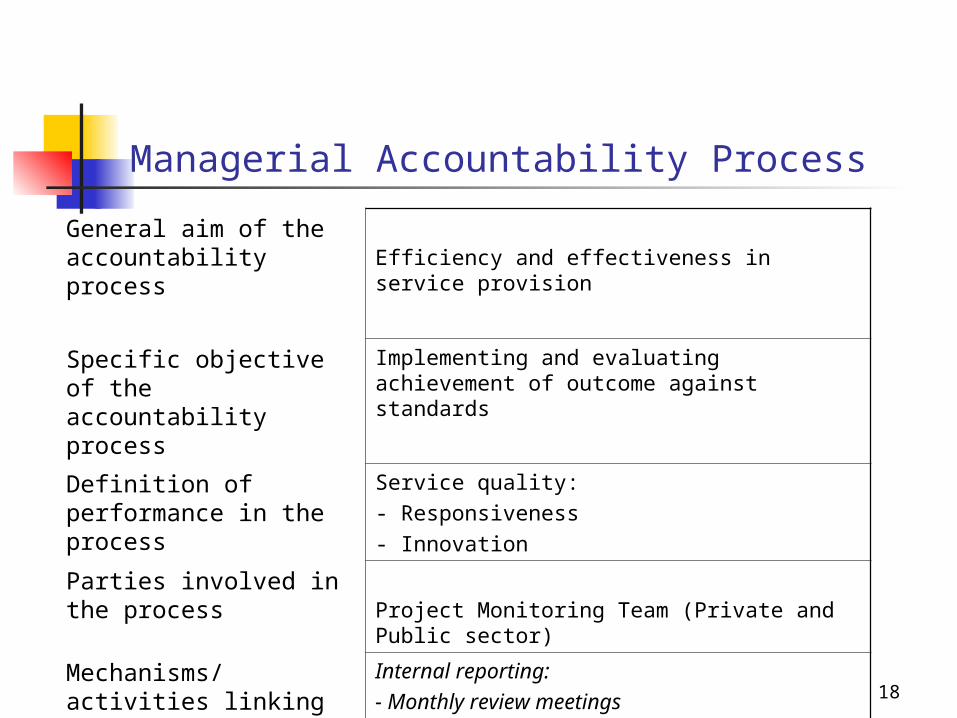

Managerial Accountability Process

General aim of the accountability process Efficiency and effectiveness in service

provision

Specific objective of the accountability process

Implementing and evaluating achievement of outcome against standards

Definition of performance in the process

Service quality: - Responsiveness- Innovation

Parties involved in the process Project Monitoring Team (Private and Public

sector)

Mechanisms/ activities linking accountability and performance

Internal reporting:- Monthly review meetings- Quarterly review meetings

19

Parliamentary Accountability Process

General aim of the accountability process Achievement of policy goals

Specific objective of the accountability process

Reporting to Parliament on the legitimate use of public funds

Definition of performance in the process

EconomyEfficiencyOutcome

Parties involved in the process

Public sector auditorsMinisters (representing public)

Mechanisms/ activities linking accountability and performance

External reporting to Parliament and public

20

21

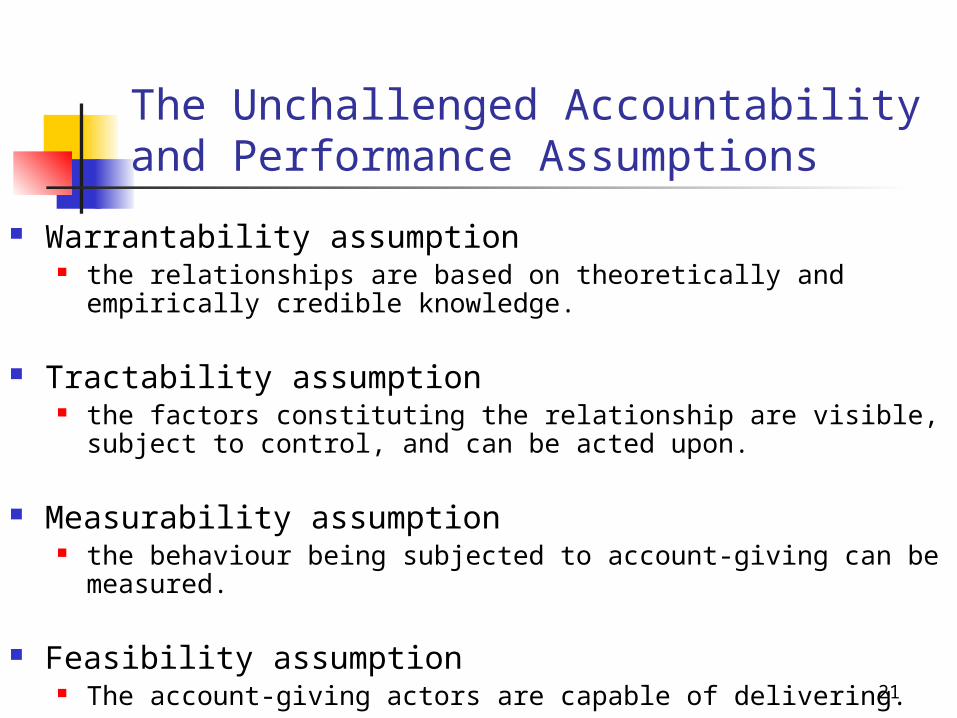

The Unchallenged Accountability and Performance Assumptions

Warrantability assumption the relationships are based on theoretically and empirically

credible knowledge.

Tractability assumption the factors constituting the relationship are visible, subject to

control, and can be acted upon.

Measurability assumption the behaviour being subjected to account-giving can be

measured.

Feasibility assumption The account-giving actors are capable of delivering.

22

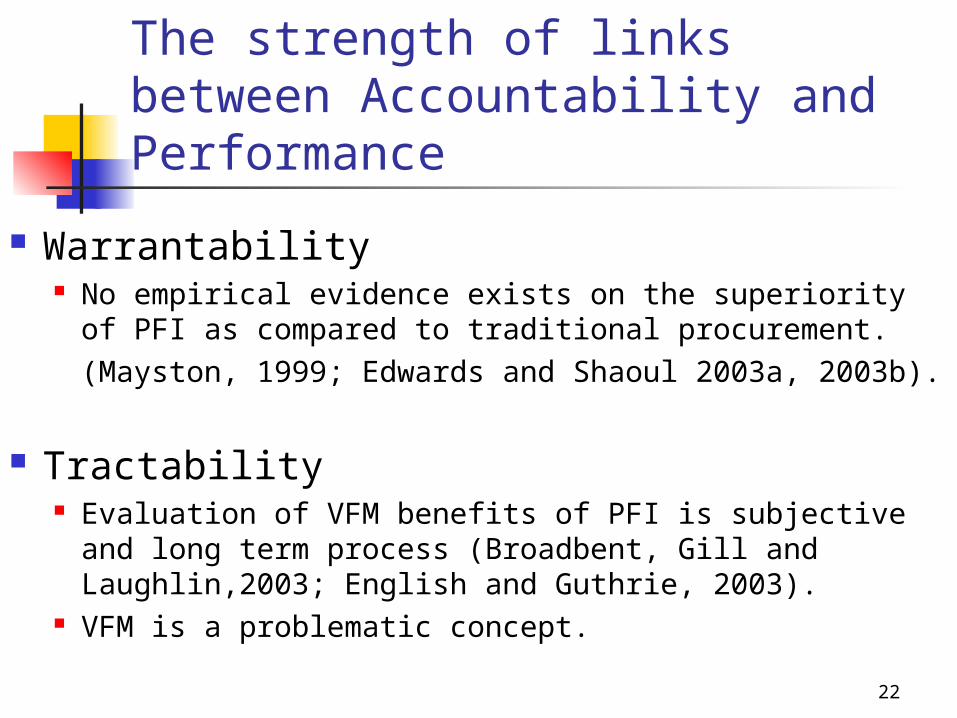

The strength of links between Accountability and Performance

Warrantability No empirical evidence exists on the superiority of PFI

as compared to traditional procurement.(Mayston, 1999; Edwards and Shaoul 2003a, 2003b).

Tractability Evaluation of VFM benefits of PFI is subjective and

long term process (Broadbent, Gill and Laughlin,2003; English and Guthrie, 2003).

VFM is a problematic concept.

23

Measurability VFM involves the preparation of a Public Sector Comparator to

benchmark the PFI option is a subjective process.

Selection of performance measures and measuring efficiency and effectiveness of PFI programmes are subjective.

Feasibility PFI accountability processes are difficult to implement. Risks may revert back to the public sector when the private

sector fails to deliver (See, Royal Armouries, Channel Tunnel Rail Link, the National Insurance and Passport Office PFIs).

24

Conclusions

Accountability is a buzz word but it is difficult concept to define to the satisfaction of all the interested groups.

Accountability is a continuous and dynamic concept often emerging in different forms and may be overlapping and influencing each other at any time.

Information available on value for money is limited.

Risk transfer thus becomes crucial.

25

Conclusions Cont… Performance relating to accountability may not

be immediate.

Therefore it may not be warrantable, traceable, measurable and feasible.

Further empirical work is required to ground accountability concepts and theories and their assumed performance relationships.

The best that can be expected is to explain each case on its own merit and try to explain the possible links.