Embed Size (px)

Citation preview

1

The Art and Science of Valuation

Prepared for Faegre & Benson April 19, 2006

2

Overall Agenda Part 1: Capturing the Attention of the

Venture Capitalist Part 2: Understanding the state of the

Venture Capital Industry Part 3: Valuation Overview

3

Part 1 Agenda Part 1: Capturing the Attention of the

Venture Capitalist Finding the right VC Courting the right VC Management Team Market Characteristics How hard can it be?

Part 2: Understanding the state of the Venture Capital Industry

Part 3: Valuation Overview

4

Finding the Right VC

Do Your Homework

Buying Criteria Just Like a

Customer

5

Courting the Right VC

Online Dating Anonymous Highly

Competitive 1 Chance

6

“As a founder, think hardest about the team. Are these the people I want to be in trouble with for the next 5, 10, 15 years of my life? Because as you build a new business, one thing’s for sure: you will get into trouble.”

John Doerr, Kleiner Perkins Caufield & Byers

Management Team

7

Investing In TalentFactors considered most important by investment professionals(Weighted importance out of 100*)

Management Team

Market Sector

Business Model

Proprietary Product/Service

37

24

20

19

Source: Spencer Stuart/NVCA VC-backed Leadership survey

8

Market Characteristics Worth Winning

$250 million Sustainable

Drivers Y2k

Well Defined Sub-segment

9

How Hard can it Be?

10

A Rapidly Evolving World

Yahoo raises $2 million Amazon goes live Netscape goes public 45% heard of www AltaVista 16 million

pages

1995

11

Technology is only the Ante

12

Sustaining vs. Disruptive Technologies Sustaining Technology

Foster improved product performance Disruptive Technology

Bring to the market a very different value proposition

The Innovator’s Dilemma – Clayton Christensen

13

Sustaining vs. Disruptive Technologies

Sustaining Technology Improves

performance along an existing utility curve

A

BSustaining Technology

Cost

Performance

14

Sustaining vs. Disruptive Technologies

Disruptive Technology Moves the market

to new utility curveA

Disruptive Technology

B

Cost

Performance

15

Explicit Need / Compelling ROI

IT Budgets and ROI:“Purse strings are loosening ever so slightly, but that won’t slow the quest for better metrics”

16

Part 2 Agenda Part 1: Capturing the Attention of the

Venture Capitalist Part 2: Understanding the state of the

Venture Capital Industry Locations: East Coast / West Coast and everywhere else State of Emerging Market Funding US Market Trend Minnesota Market Trend Pre-Bubble Normal

Part 3: Valuation Overview

17

Locations: CA, MA and then the Rest

18

State of Emerging Company Funding(Hint: Small VC Funds are Disappearing )

19

U.S. Venture Capital Market Trend Info

% of U.S. VC

0%

10%

20%

30%

40%

50%

60%

70%

1995

-1

1996

-1

1997

-1

1998

-1

1999

-1

2000

-1

2001

-1

2002

-1

2003

-1

2004

-1

2005

-1

Expansion Later StageEarly Stage Seed Stage

Group Median Expansion – 53% Later Stage –

18% Early Stage –

22% Seed Stage – 4%

Source: PWC MoneyTree

20

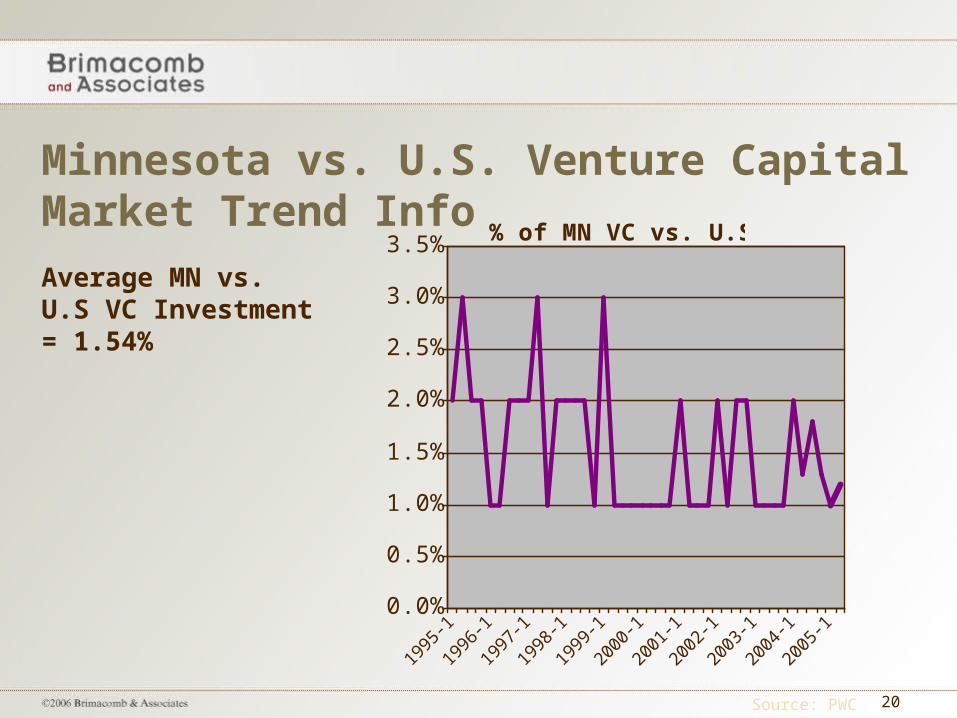

Minnesota vs. U.S. Venture Capital Market Trend Info

Source: PWC MoneyTree

% of MN VC vs. U.S. VC

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

1995

-1

1996

-1

1997

-1

1998

-1

1999

-1

2000

-1

2001

-1

2002

-1

2003

-1

2004

-1

2005

-1

Average MN vs. U.S VC Investment = 1.54%

21

A Pre-Bubble NormalValution Trends

0

20

40

60

80

100

120

140

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

$ i

n M

illi

on

s Seed

Early

Expansion

Later

BuyOut

22

Part 3 Agenda Part 1: Capturing the Attention of the

Venture Capitalist Part 2: Understanding the state of the

Venture Capital Industry Part 3: Valuation Overview

Valuation Start-Up Stages Equity Financing Food Chain Sherpa Guide to Success Valuation Methodology A Lesson from Charles Darwin

23

Valuation is Chess Not Checkers

24

Stages of a Startup

Definition and Validation

Prove Solution is Repeatable

Grow the Channel to Capture Opportunity

25

Seed Stage

100% – 30% IRR

Early Stage – (Sherpa)

50% - 20% IRR

Expansion Stage

25% - 15% IRR

Late Stage

20% - 12% IRR

Early Adopter Customers

Early Majority Customers

Late Majority Customers

Innovation Customers

Friends/Family

Angels Institutional - VCs Public Market

Equity Financing Food ChainReturn Expectations

26

Return Expectations

27

Return Expectations

5-10x your investment

or30%+ IRR

28

Sherpa Pocket Guide to Success

Quick Go vs. No Go Decision

(4x in 5 Years = 32% IRR)

29

Valuation Methodology1. Determine valuation

in an out year

Revenue in year 5 is $20 million

Use a multiplier (i.e., revenue, operating income, earnings, subscribers, locations, etc.) to determine value

A revenue multiple of 2x would make the company value $40 million in year 5

2. Compare future value with current value

Divide the future value ($40 million) by the post-money valuation

Post-money value of $10 million means this investment increased in value by 4x ($40 million / $10 million)

4x in 5 years equals a 32% IRR

30

“It is not the strongest of the species that survives, nor the most intelligent; it is the one that is most adaptable to change.”

- Charles Darwin, British Naturalist

31

Recap Part 1: Capturing the Attention of the

Venture Capitalist Part 2: Understanding the state of the

Venture Capital Industry Part 3: Valuation Overview

32

Rick BrimacombFounder, Brimacomb & AssociatesGeneral Partner, Sherpa PartnersBoard Member, Minnesota Venture Capital

Association

Jason VoiovichPrincipal, Ecra Creative [email protected]

![Benson Lecture Inpla[1] Phil Benson](https://img.pdfslide.us/doc/110x75/5549e849b4c90518488b4ca4/benson-lecture-inpla1-phil-benson.jpg)

![George Benson - The Best of George Benson[1]](https://img.pdfslide.us/doc/110x75/5695cf541a28ab9b028d9c4a/george-benson-the-best-of-george-benson1.jpg)