Embed Size (px)

Citation preview

1

Risk management in agricultural financing

Crédit Agricole: a leading partner to an ever-changing world

Jean Luc PERRONManaging Director

Grameen Crédit Agricole Microfinance FoundationApril 2009 – Johannesburg

2

1. Introduction to Crédit Agricole Group2. Key features and figures of France’s farming

sector3. The risk approach of Crédit Agricole4. An accelerated and integrated solution for the

financing of farm machinery: the AGILOR solution5. Crédit Agricole’s agricultural insurance services:

crop insurance6. Crédit Agricole’s soft commodities hedging

services7. Crédit Agricole’s risk policy and monitoring

methodology

Risk management in agricultural financing

Crédit Agricole: a leading partner to an ever-changing world

3

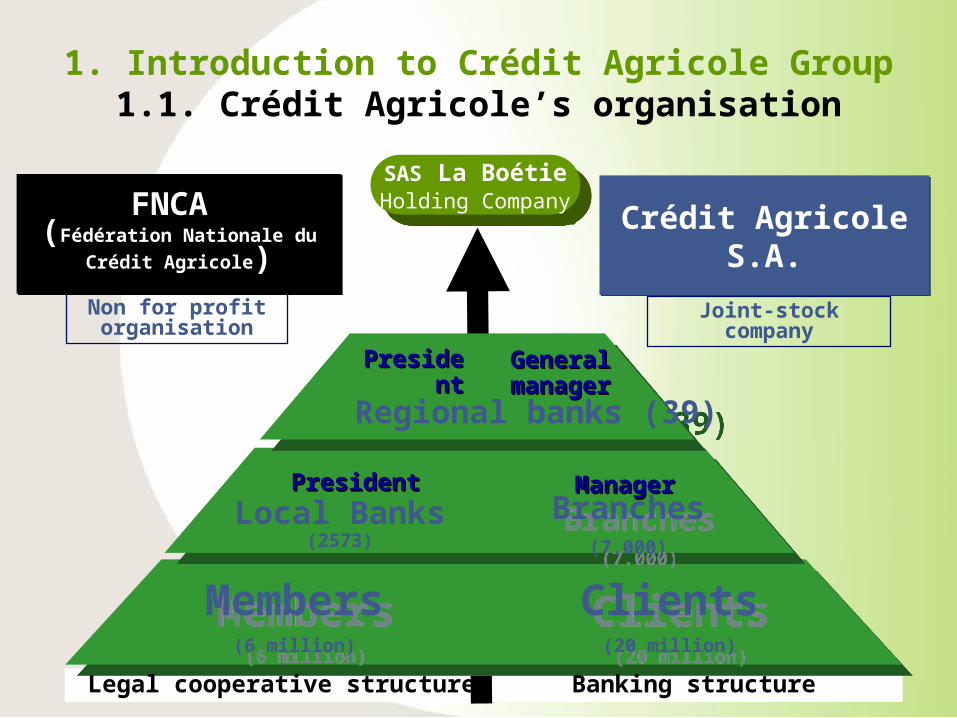

1. Introduction to Crédit Agricole Group1.1. Crédit Agricole’s organisation

Joint-stock companyNon for profit organisation

Regional banks (39)Regional banks (39)

Legal cooperative structure

PresidentPresident

Local Banks (2573)

General General managermanager

Branches(7.000)

Branches(7.000)

Members(6 million)

Members(6 million)

Clients(20 million)

Clients(20 million)

FNCA (Fédération Nationale du Crédit

Agricole)

FNCA (Fédération Nationale du Crédit

Agricole)Crédit Agricole S.A.Crédit Agricole S.A.

Banking structure

PresidentPresident ManagerManager

SAS La BoétieHolding Company

SAS La BoétieHolding Company

4

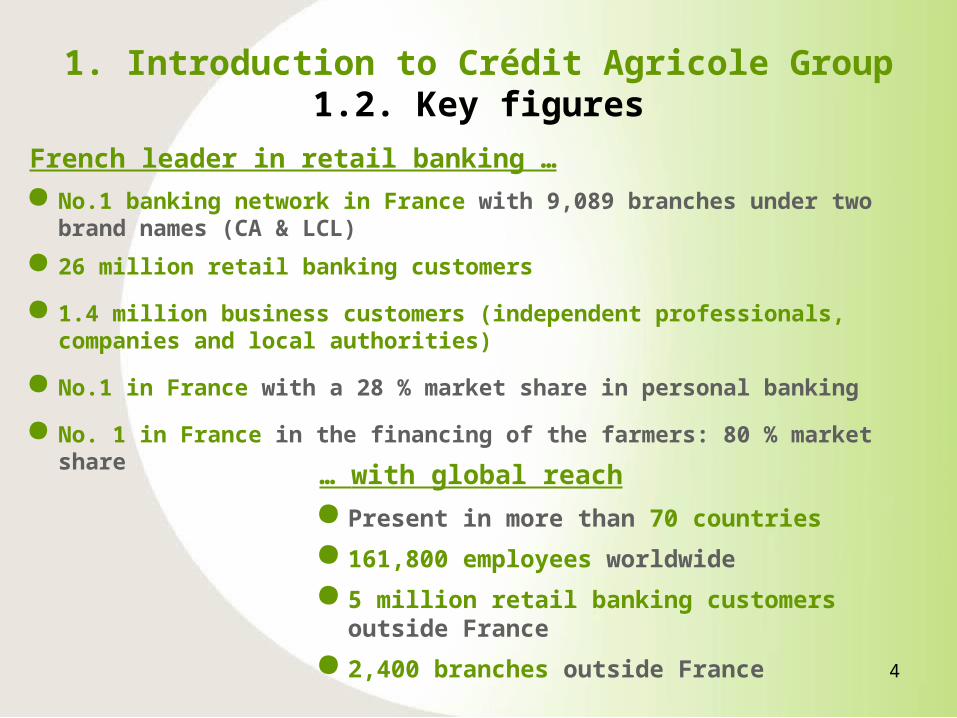

1. Introduction to Crédit Agricole Group1.2. Key figures

French leader in retail banking … No.1 banking network in France with 9,089 branches under two

brand names (CA & LCL)

26 million retail banking customers

1.4 million business customers (independent professionals, companies and local authorities)

No.1 in France with a 28 % market share in personal banking

No. 1 in France in the financing of the farmers: 80 % market share

… with global reach Present in more than 70 countries

161,800 employees worldwide

5 million retail banking customers outside France

2,400 branches outside France

5

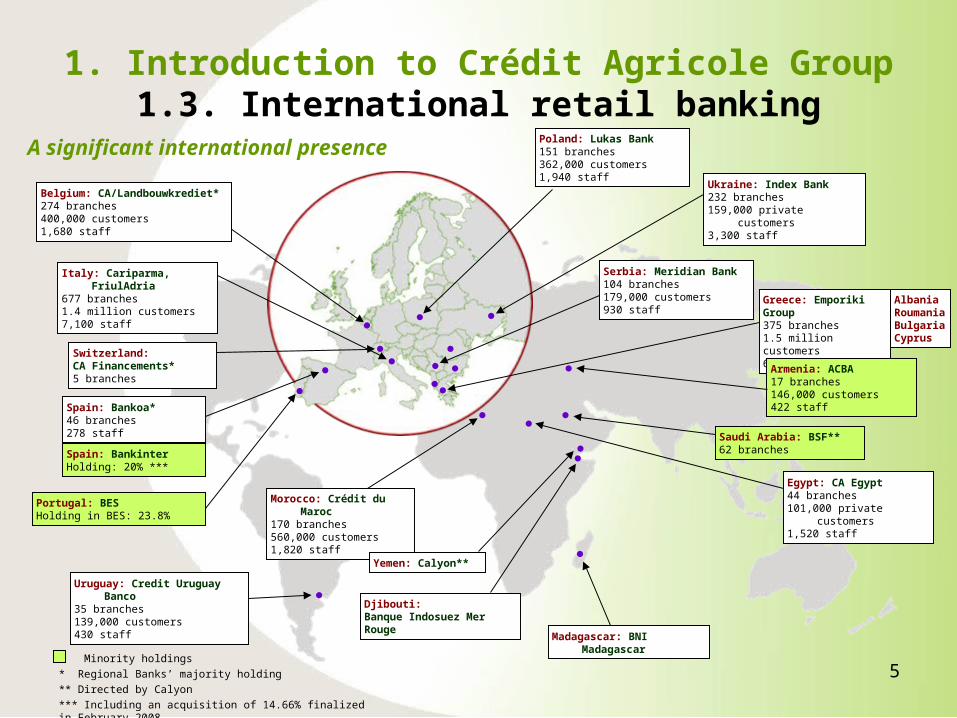

1. Introduction to Crédit Agricole Group1.3. International retail banking

Minority holdings

* Regional Banks’ majority holding

** Directed by Calyon

*** Including an acquisition of 14.66% finalized in February 2008

A significant international presence

Ukraine: Index Bank232 branches159,000 private customers3,300 staff

Serbia: Meridian Bank104 branches179,000 customers930 staff

Greece: Emporiki Group375 branches1.5 million customers6,700 staff

Saudi Arabia: BSF**62 branches

Poland: Lukas Bank151 branches362,000 customers1,940 staff

Switzerland: CA Financements*5 branches

Uruguay: Credit Uruguay Banco35 branches139,000 customers430 staff

Belgium: CA/Landbouwkrediet* 274 branches400,000 customers1,680 staff

Morocco: Crédit du Maroc170 branches560,000 customers1,820 staff

Italy: Cariparma, FriulAdria677 branches1.4 million customers7,100 staff

Spain: Bankoa*46 branches278 staff

Djibouti: Banque Indosuez Mer Rouge

Armenia: ACBA17 branches146,000 customers422 staff

Egypt: CA Egypt44 branches101,000 private customers1,520 staff

Yemen: Calyon**

Portugal: BESHolding in BES: 23.8%

AlbaniaRoumaniaBulgariaCyprus

Spain: BankinterHolding: 20% ***

Madagascar: BNI Madagascar

6

1. Introduction to Crédit Agricole Group1.4. Corporate & investment banking

Western Europe

Australia

Eastern and Central Europe

Africa / Middle-East

N & S. America Asia/Pacific

** offshore branches

France

UK

The Capital Markets and Syndicated loans teams work from a dual London-Paris platforms

Austria

Belgium

Finland

Germany

Greece

Italy

Luxembourg

Monaco

Nertherlands

Norway

Portugal

Spain

Sweden

Switzerland

United States:

• New York

• Chicago

• Dallas

• Houston

• Los Angeles

Canada

Chile

Brazil

Mexico

Venezuela

Uruguay

Argentina

Japan :

• Tokyo

• Osaka

China:• Beijing• Shanghai• Guangzhou• Tianjin• Xiamen• Shenzhen

Hong Kong

India:• Mumbai• Delhi• Chennai• Ahmedabad• Pune• Bengalore

Indonesia

Korea

Malaysia**

Philippines**

Singapore

Taiwan

Thailand

Vietnam :• Hanoi• Ho Chi Minh City

Managed by the International Retail Banking divisions of Crédit Agricole S.A. and Calyon

Czech Republic

Hungary

Poland

Russia:• Moscow• St Petersburg

Slovakia

Ukraine

Serbia

Algeria

Tunisia

Lybia

Morocco

Cameroon

Djibouti

Gabon

Ivory Coast

Madagascar

Republic of Congo

Senegal

South Africa

Bahrain

Egypt

Iran

Israel

Kazakhstan

Saudi Arabia: BSF

Turkey

United Arab Emirates

Yemen

Branches or banking subsidiaries

Representation offices

Other affiliates (brokerage, etc.)

Managed by the International Retail Banking divisions of Crédit Agricole S.A. and Calyon

7

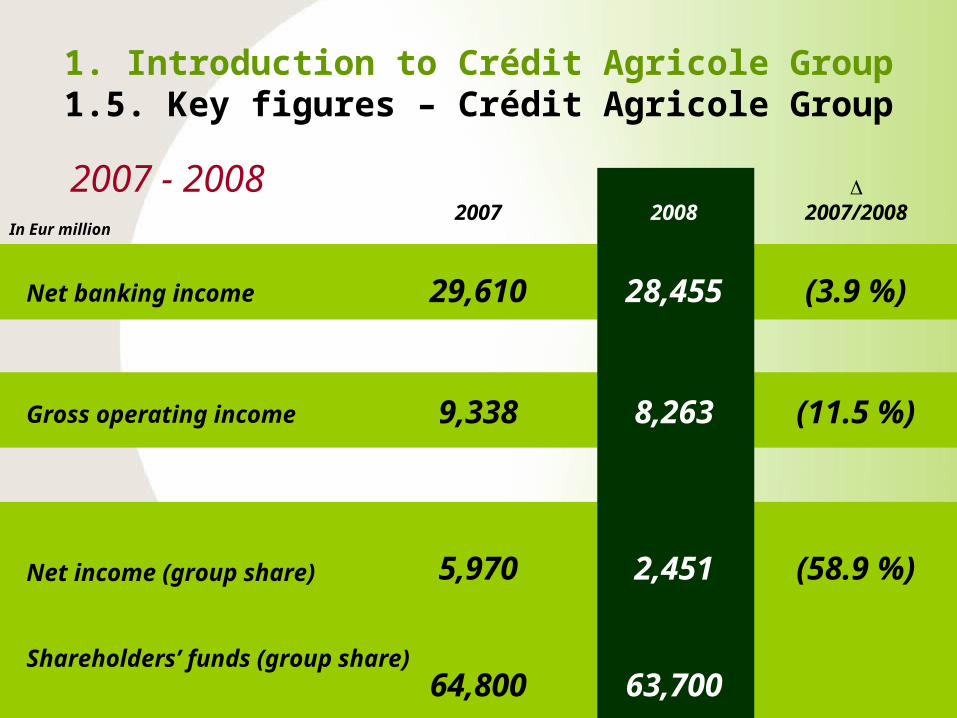

1. Introduction to Crédit Agricole Group1.5. Key figures – Crédit Agricole Group

In Eur million

Net banking income

Gross operating income

Net income (group share)

Shareholders’ funds (group share)

2007/200820082007

29,610

9,338

5,970

64,800

28,455

8,263

2,451

63,700

(3.9 %)

(11.5 %)

(58.9 %)

2007 - 2008

8

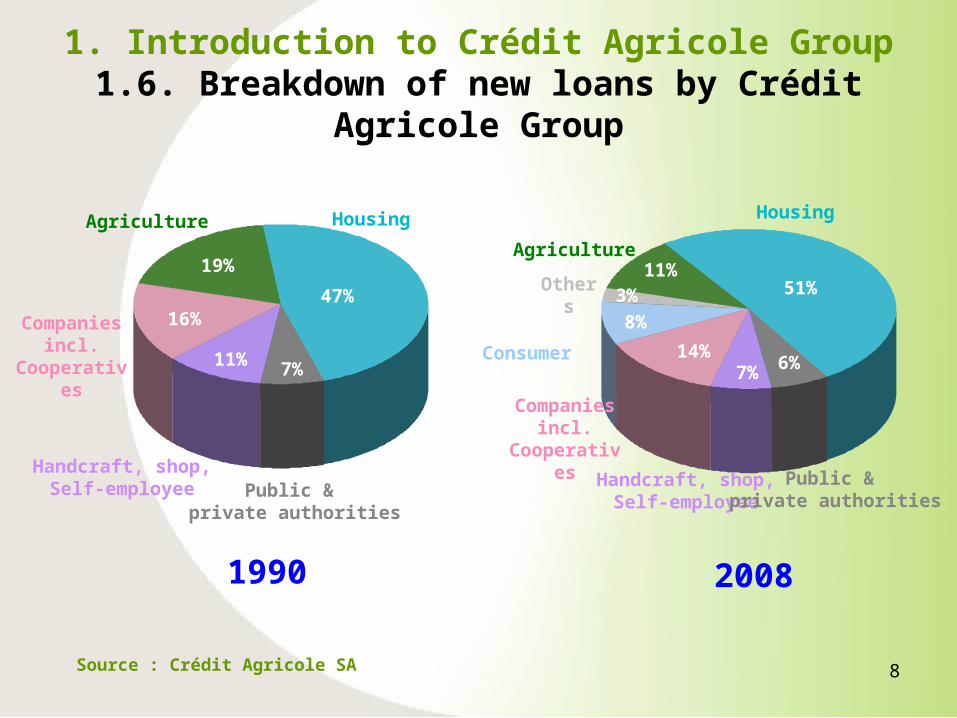

1. Introduction to Crédit Agricole Group1.6. Breakdown of new loans by Crédit Agricole

Group

Source : Crédit Agricole SA

Agriculture

Companies incl.

Cooperatives

Public & private authorities

Handcraft, shop,Self-employee

Housing

47%

19%

16%

11% 7%

1990 2008

Housing

Agriculture

Consumer

Others 51%11%

8%

14%6%7%

3%

Companies incl.

Cooperatives

Handcraft, shop,Self-employee

Public & private authorities

9

1. Introduction to Crédit Agricole Group2. Key features and figures of France’s farming

sector3. The risk approach of Crédit Agricole4. An accelerated and integrated solution for the

financing of farm machinery: the AGILOR solution5. Crédit Agricole’s agricultural insurance services:

crop insurance6. Crédit Agricole’s soft commodities hedging

services7. Crédit Agricole’s risk policy and monitoring

methodology

Risk management in agricultural financing

Crédit Agricole: a leading partner to an ever-changing world

10

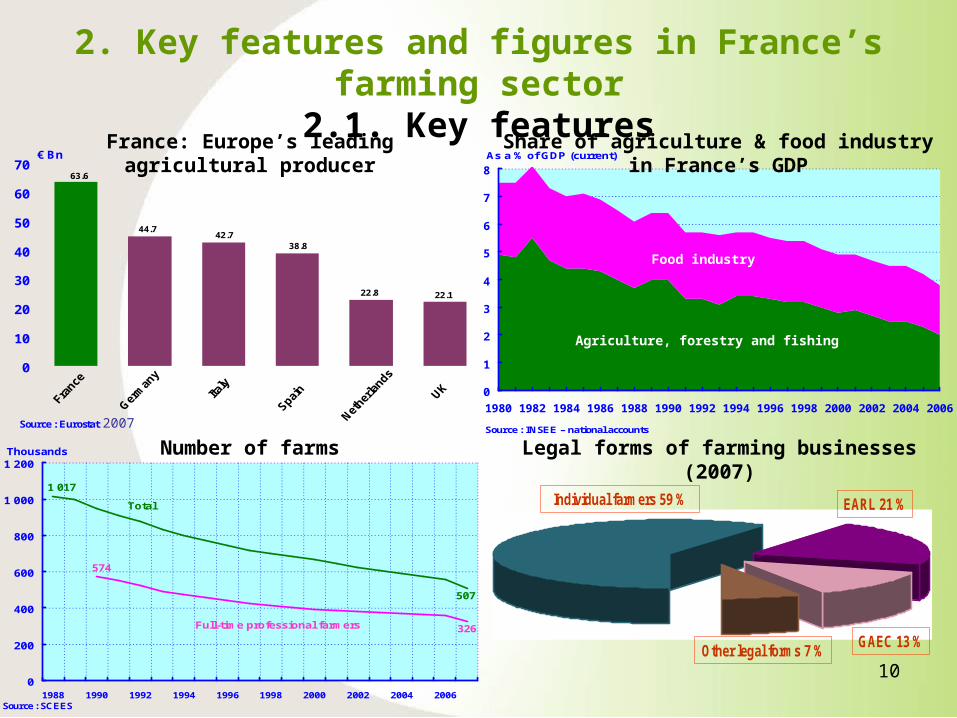

2. Key features and figures in France’s farming sector

2.1. Key features63.6

22.1

44.742.7

38.8

22.8

0

10

20

30

40

50

60

70

Source : Eurostat

€ BnFrance: Europe’s leading agricultural

producer

0

1

2

3

4

5

6

7

8

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006

Source : INSEE – national accounts

As a % of GDP (current)Share of agriculture & food industry in

France’s GDP

Agriculture, forestry and fishing

Food industry

2007

Number of farms

0

200

400

600

800

1 000

1 200

1988 1990 1992 1994 1996 1998 2000 2002 2004 2006Source : SCEES

Thousands

1 017

507

574

326

Total

Full-time professional farmers

Individual farmers 59 %

Other legal forms 7 %

EARL 21 %

GAEC 13 %

Legal forms of farming businesses (2007)

11

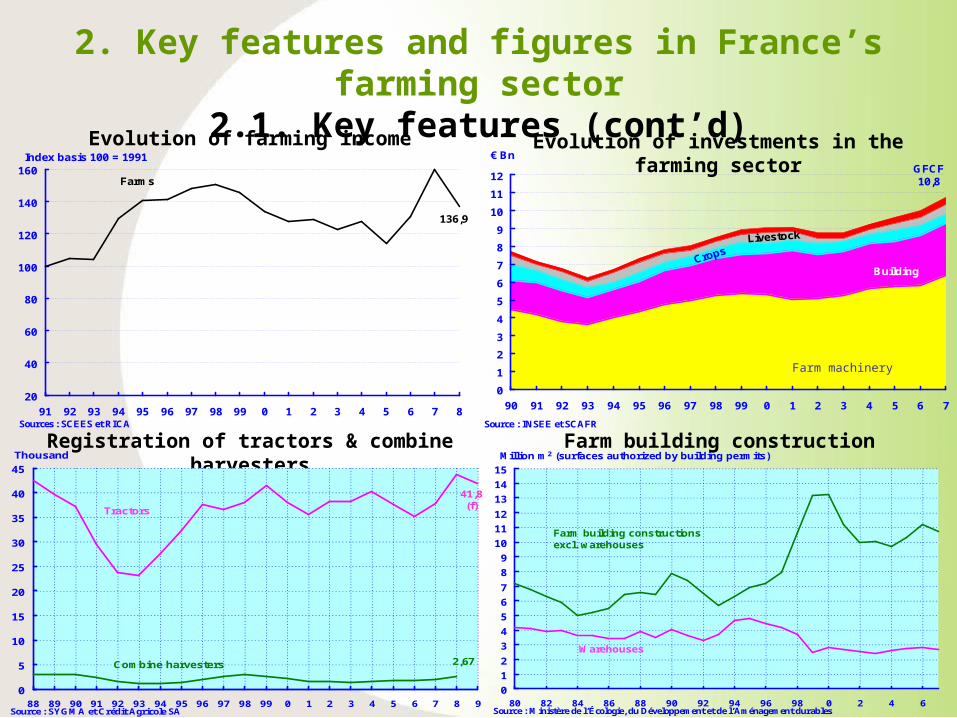

2. Key features and figures in France’s farming sector

2.1. Key features (cont’d)Evolution of farming income Evolution of investments in the farming sector

Registration of tractors & combine harvesters

Farm building construction

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

80 82 84 86 88 90 92 94 96 98 0 2 4 6

Million m2 (surfaces authorized by building permits)

Source : Ministère de l’Écologie, du Développement et de l’Aménagement durables

Warehouses

Farm building constructions excl. warehouses

0

5

10

15

20

25

30

35

40

45

88 89 90 91 92 93 94 95 96 97 98 99 0 1 2 3 4 5 6 7 8 9

Thousand

Source : SYGMA et Crédit Agricole SA

2,67

41,8(f)Tractors

Combine harvesters

Source : INSEE et SCAFR

€ Bn

0

1

2

3

4

5

6

7

8

9

10

11

12

90 91 92 93 94 95 96 97 98 99 0 1 2 3 4 5 6 7

GFCF10,8

Agricultural equipment

Building

Farm machinery

20

40

60

80

100

120

140

160

91 92 93 94 95 96 97 98 99 0 1 2 3 4 5 6 7 8

Farms

136,9

Index basis 100 = 1991

Sources : SCEES et RICA

12

2. Key features and figures in France’s farming sector

2.2. The financing of French farming sector by Crédit AgricoleBreakdown by sub-sector

Evolution of investments in the French farming sector & new MLT loans (subsidized

vs. non-sub.)Evolution of outstanding loan portfolio

Source : Crédit Agricole SA

Forestry, fishing, hunting

side services

Porcines,poultry

Other productions

Cereals, legumesand oleaginous

Vineyards

3%

34%

20%1%22%

1%

11%1%

2%2%

Bovines

Fruits

Cultivation,livestock farming

Other sectors

Vegetables, melons,

roots, tubers

3%

Ovines,goats

Source : Crédit Agricole SA

0

5

10

15

20

25

30

35

65 67 69 71 73 75 77 79 81 83 85 87 89 91 93 95 97 99 1 3 5 7

€ Bn

32,8

1,7

Total outstanding loan portfolio

Subsidized outstanding loan portfolio

New serie since 1994 incorporating in arrears and in advance interests

€ bn

Source : Crédit Agricole SA

0

1

2

3

4

5

6

7

8

9

10

11

90 91 92 93 94 95 96 97 98 99 0 1 2 3 4 5 6 7 8

4,94,6

4,2

3,13,4

3,94,3

4,7 4,85,4

4,74,9 5,3

5,65,9 5,7

5,5

6,3

7,1

Subsidised

Non-subsidized

FGCF

10.8

In 2008, Crédit Agricole’s lending activity in the farming sector amounted to:

€ 7.1 bn of new MLT loans € 38.1 bn in outstanding loan portfolio(including home loans for farmers)

Crédit Agricole provides banking services to 9 out of 10 farmers in France.

13

1. Introduction to Crédit Agricole Group2. Key features and figures of France’s farming

sector3. The risk approach of Crédit Agricole4. An accelerated and integrated solution for the

financing of farm machinery: the AGILOR solution5. Crédit Agricole’s agricultural insurance services:

crop insurance6. Crédit Agricole’s soft commodities hedging

services7. Crédit Agricole’s risk policy and monitoring

methodology

Risk management in agricultural financing

Crédit Agricole: a leading partner to an ever-changing world

14

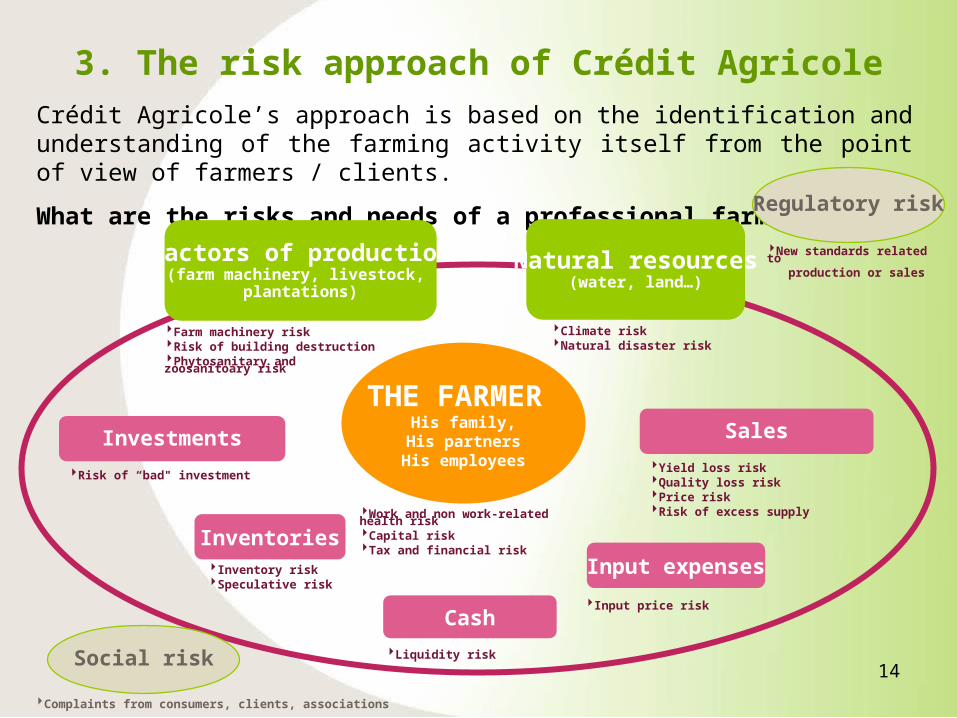

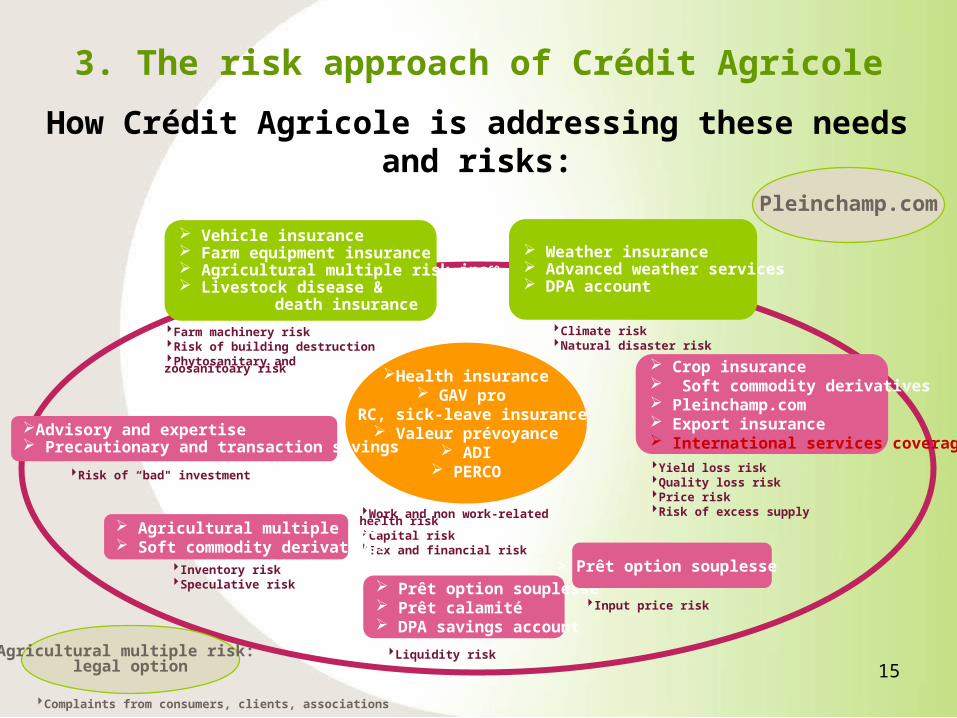

3. The risk approach of Crédit AgricoleCrédit Agricole’s approach is based on the identification and understanding of the farming activity itself from the point of view of farmers / clients.

What are the risks and needs of a professional farmer?

THE FARMER His family,

His partnersHis employees

Work and non work-related health riskCapital riskTax and financial risk

Farm machinery riskRisk of building destructionPhytosanitary and zoosanitoary risk

Liquidity risk

Yield loss riskQuality loss riskPrice riskRisk of excess supply

Risk of “bad" investment

Input price risk

Inventory riskSpeculative risk

Climate riskNatural disaster risk

Social risk

Complaints from consumers, clients, associations

Regulatory risk

Natural resources(water, land…)

Factors of production(farm machinery, livestock,

plantations)

Cash

SalesInvestments

Input expensesInventories

New standards related to production or sales

15

3. The risk approach of Crédit Agricole

How Crédit Agricole is addressing these needs and risks:

Health insurance GAV pro

RC, sick-leave insurance Valeur prévoyance

ADI PERCO

Work and non work-related health riskCapital riskTax and financial risk

Farm machinery riskRisk of building destructionPhytosanitary and zoosanitoary risk

Liquidity risk

Yield loss riskQuality loss riskPrice riskRisk of excess supply

Risk of “bad" investment

Input price risk

Inventory riskSpeculative risk

Climate riskNatural disaster risk

Agricultural multiple risk: legal option

Complaints from consumers, clients, associations

Pleinchamp.com

Weather insurance Advanced weather services DPA account

Vehicle insurance Farm equipment insurance Agricultural multiple risk insce

Livestock disease & death insurance

Prêt option souplesse Prêt calamité DPA savings account

Advisory and expertise Precautionary and transaction savings

> Prêt option souplesse

Agricultural multiple risk Soft commodity derivatives

Crop insurance Soft commodity derivatives Pleinchamp.com Export insurance International services coverage

16

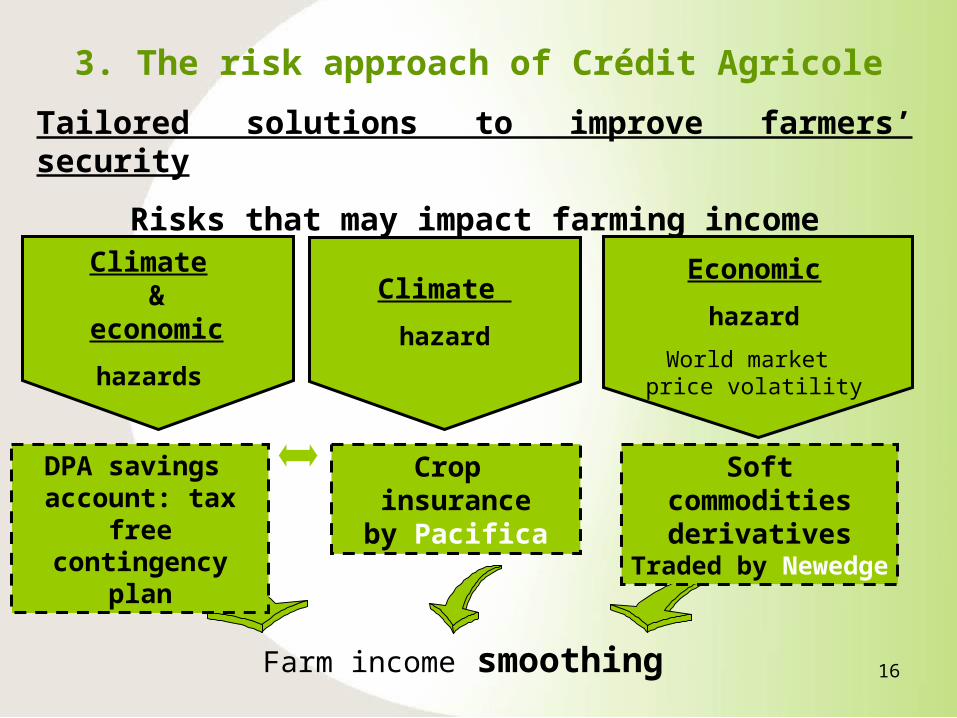

3. The risk approach of Crédit Agricole

Tailored solutions to improve farmers’ security

Risks that may impact farming income

Economic

hazard

World market price volatility

Farm income smoothing

Climate

hazard

Crop insuranceby Pacifica

Climate &

economic

hazards

DPA savings account: tax free contingency plan

Soft commodities derivatives

Traded by Newedge

17

1. Introduction to Crédit Agricole Group2. Key features and figures of France’s farming

sector3. The risk approach of Crédit Agricole4. An accelerated and integrated solution for the

financing of farm machinery: the AGILOR solution5. Crédit Agricole’s agricultural insurance services:

crop insurance6. Crédit Agricole’s soft commodities hedging

services7. Crédit Agricole’s risk policy and monitoring

methodology

Risk management in agricultural financing

Crédit Agricole: a leading partner to an ever-changing world

18

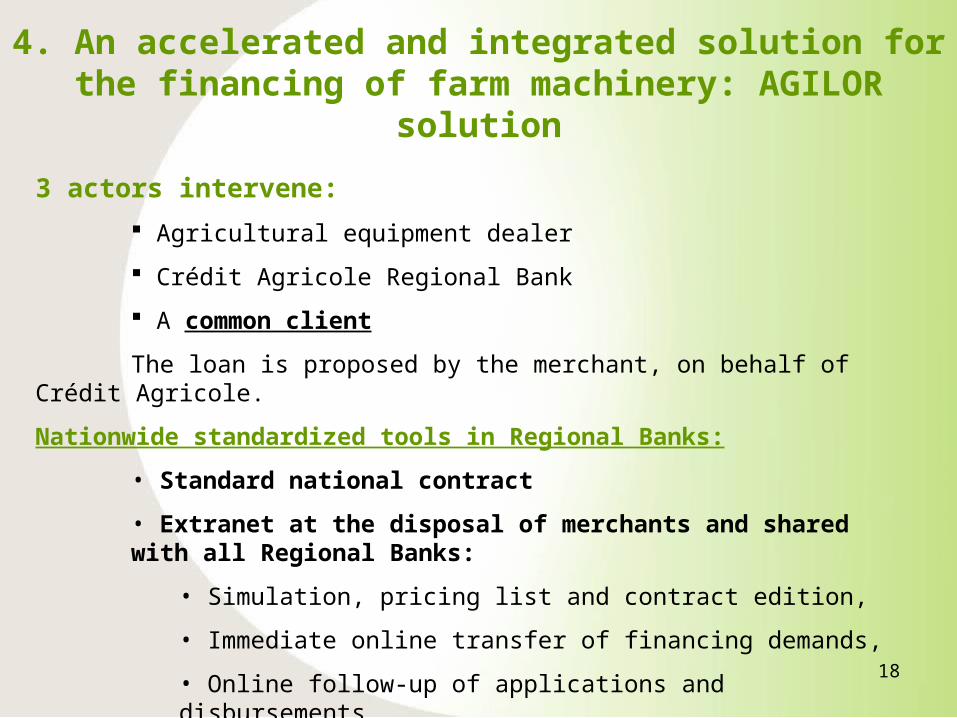

4. An accelerated and integrated solution for the financing of farm machinery: AGILOR

solution

3 actors intervene:

Agricultural equipment dealer

Crédit Agricole Regional Bank

A common client

The loan is proposed by the merchant, on behalf of Crédit Agricole.

Nationwide standardized tools in Regional Banks:

• Standard national contract

• Extranet at the disposal of merchants and shared with all Regional Banks:

• Simulation, pricing list and contract edition,

• Immediate online transfer of financing demands,

• Online follow-up of applications and disbursements

19

AGILOR solution advantages:

For farmers

• Simplified procedures: one single request at the merchant’s shop

• Attractiveness of the pricing

For dealers

• A single counterpart within the Regional Bank: the AGILOR unit

• Accelerated decision-making process: 48 hours max.

• Certainty of payment: direct payment to the merchant’s bank account

For Crédit Agricole

• Reinforcing partnerships with machinery merchants

• Strength to improve / maintain its market share in a more competitive world

• Competitive advantage due to its capacity to take anticipated decisions on the loan approval process

4. An accelerated and integrated solution for the financing of farm machinery: AGILOR

solution

20

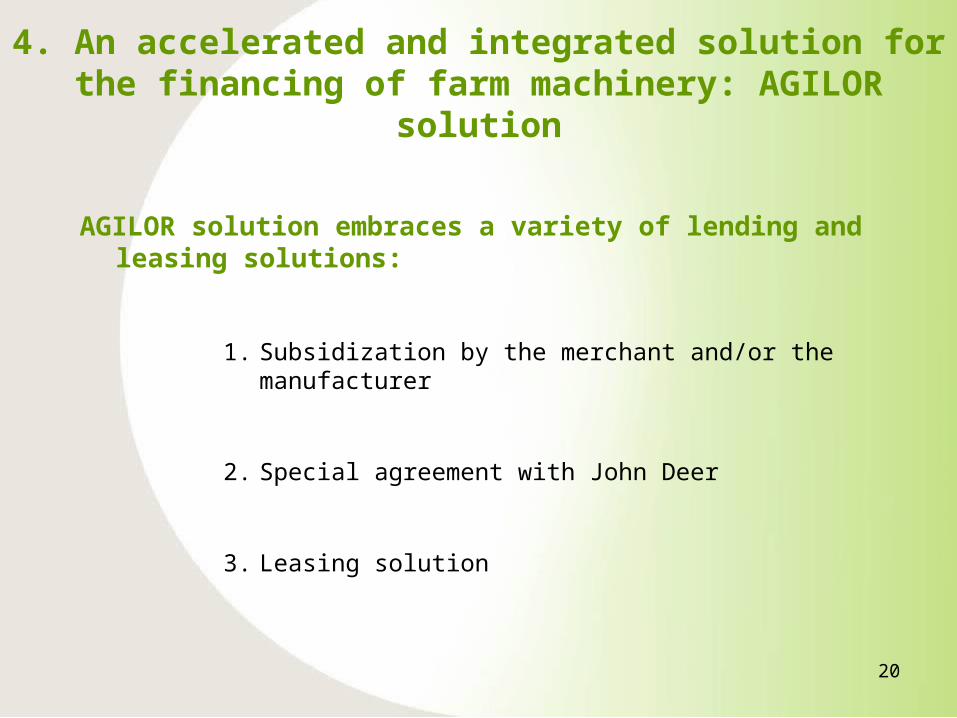

AGILOR solution embraces a variety of lending and leasing solutions:

1. Subsidization by the merchant and/or the manufacturer

2. Special agreement with John Deer

3. Leasing solution

4. An accelerated and integrated solution for the financing of farm machinery: AGILOR

solution

21

1. Introduction to Crédit Agricole Group2. Key features and figures of France’s farming

sector3. The risk approach of Crédit Agricole4. An accelerated and integrated solution for the

financing of farm machinery: the AGILOR solution5. Crédit Agricole’s agricultural insurance services:

crop insurance6. Crédit Agricole’s soft commodities hedging

services7. Crédit Agricole’s risk policy and monitoring

methodology

Risk management in agricultural financing

Crédit Agricole: a leading partner to an ever-changing world

22

5. Crédit Agricole’s agricultural insurance services: crop insurance

A climate multiple risk insurance which covers 11 events :

> For all crops except fruit : - Wind gust

- Sandstorm

- Storm rain

- Excess humidity

- Excess snow

> For all crops : - Hail

- Frost

- Storm

- Drought

- Flood and excess water

Risks not covered: Diseases not caused by a climate risk

Insects, animals damage

Weaknesses of farmers capacity

23

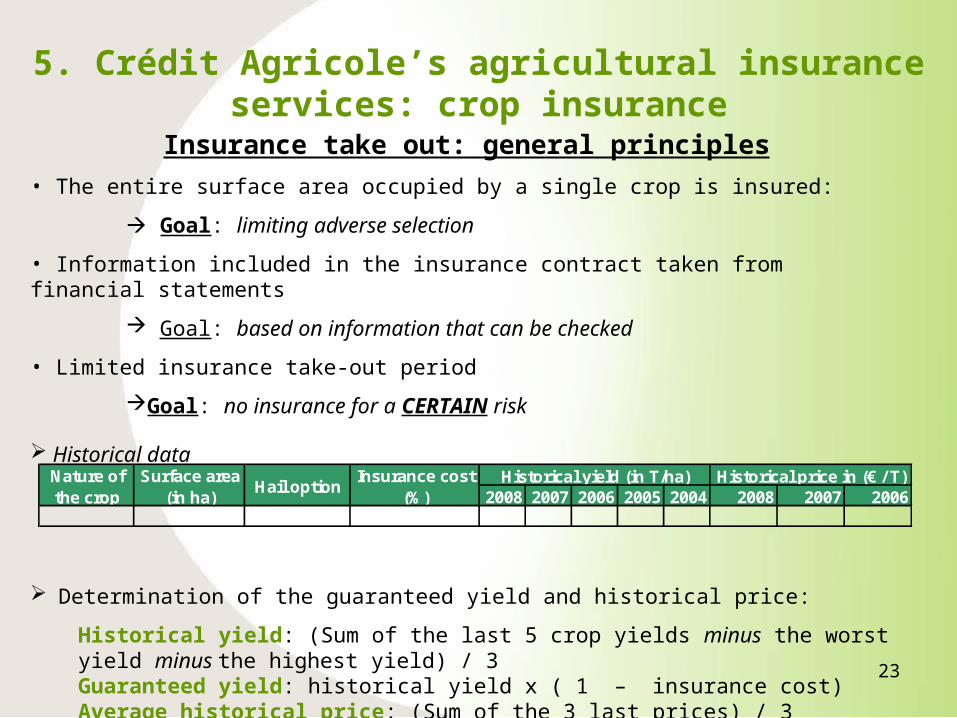

5. Crédit Agricole’s agricultural insurance services: crop insurance

Insurance take out: general principles• The entire surface area occupied by a single crop is insured:

Goal: limiting adverse selection

• Information included in the insurance contract taken from financial statements

Goal: based on information that can be checked

• Limited insurance take-out period

Goal: no insurance for a CERTAIN risk

Historical data

Determination of the guaranteed yield and historical price:

Historical yield: (Sum of the last 5 crop yields minus the worst yield minus the highest yield) / 3Guaranteed yield: historical yield x ( 1 – insurance cost)Average historical price: (Sum of the 3 last prices) / 3

2008 2007 2006 2005 2004 2008 2007 2006Historical yield (in T/ha) Historical price in (€ / T)Nature of

the cropSurface area

(in ha)Hail option

Insurance cost (%)

24

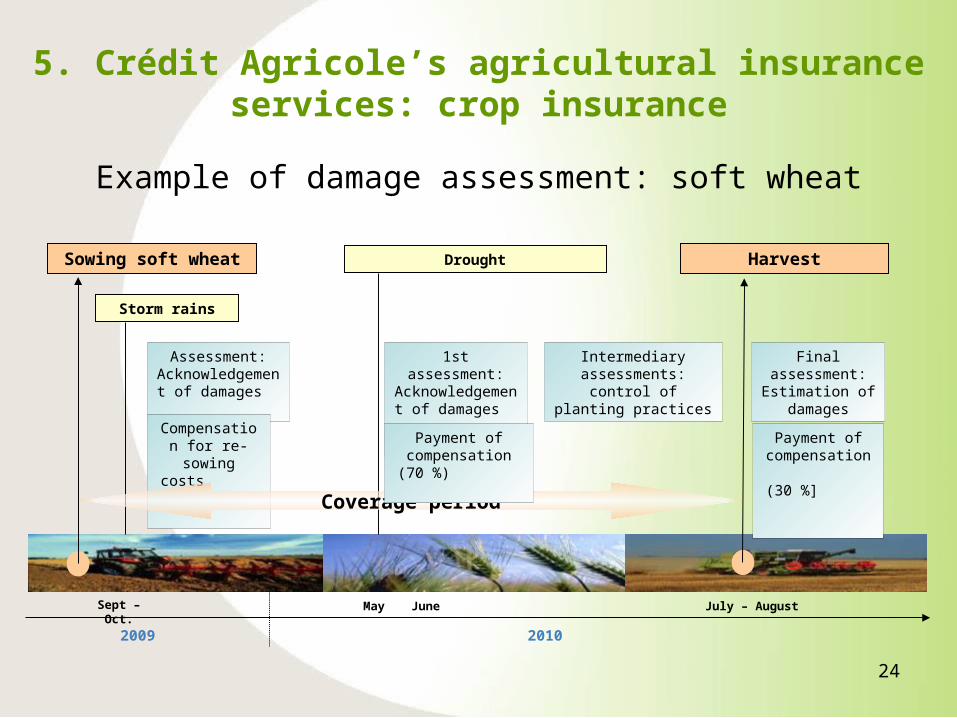

Sept – Oct.

2009 2010

Sowing soft wheat Harvest

July – AugustJune

Drought

1st assessment: Acknowledgement of damages

Intermediary assessments: control of planting practices

Final assessment: Estimation of

damages

Storm rains

Assessment: Acknowledgement of damages

Compensatio

n for re-sowing costs

Payment of compensation (30 %]

Example of damage assessment: soft wheat

May

Coverage period

5. Crédit Agricole’s agricultural insurance services: crop insurance

Payment of compensation

(70 %)

25

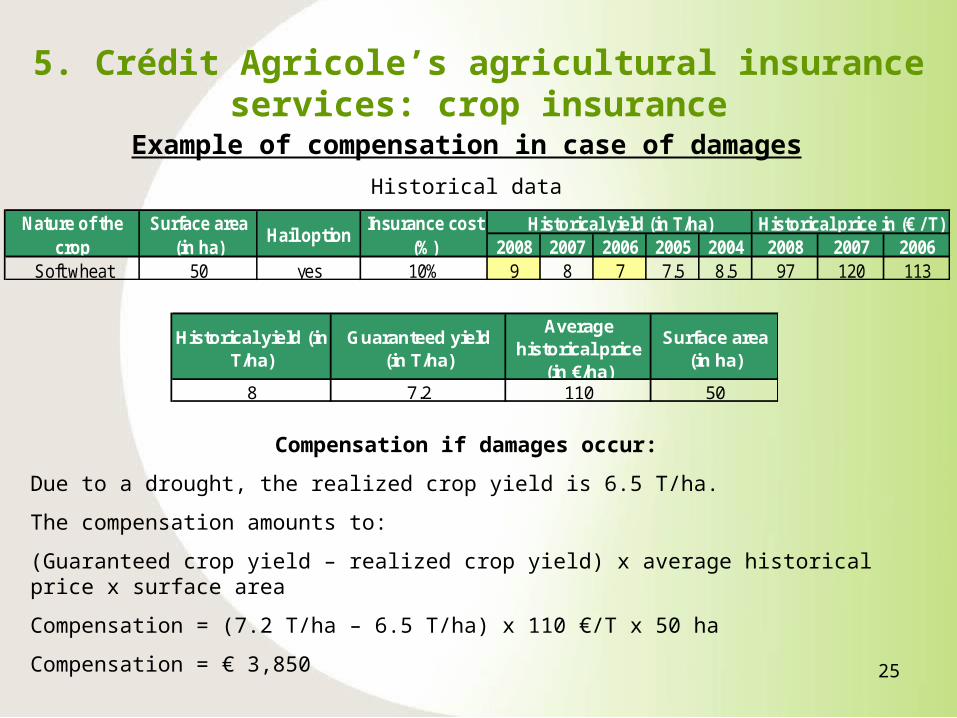

5. Crédit Agricole’s agricultural insurance services: crop insurance

Example of compensation in case of damages

Historical data

Compensation if damages occur:

Due to a drought, the realized crop yield is 6.5 T/ha.

The compensation amounts to:

(Guaranteed crop yield – realized crop yield) x average historical price x surface area

Compensation = (7.2 T/ha – 6.5 T/ha) x 110 €/T x 50 ha

Compensation = € 3,850

2008 2007 2006 2005 2004 2008 2007 2006Soft wheat 50 yes 10% 9 8 7 7.5 8.5 97 120 113

Historical yield (in T/ha) Historical price in (€ / T)Nature of the crop

Surface area (in ha)

Hail optionInsurance cost

(%)

Historical yield (in T/ha)

Guaranteed yield (in T/ha)

Average historical price

(in €/ha)

Surface area (in ha)

8 7.2 110 50

26

1. Introduction to Crédit Agricole Group2. Key features and figures of France’s farming

sector3. The risk approach of Crédit Agricole4. An accelerated and integrated solution for the

financing of farm machinery: the AGILOR solution5. Crédit Agricole’s agricultural insurance services:

crop insurance6. Crédit Agricole’s soft commodities hedging

services7. Crédit Agricole’s risk policy and monitoring

methodology

Risk management in agricultural financing

Crédit Agricole: a leading partner to an ever-changing world

27

6. Crédit Agricole’s soft commodities hedging services

Financial instruments available on soft commodity futures and options markets allow farmers to:

Hedge downward price risk through futures contractsBenefit from higher price or hedge downward risk thanks to options contracts

Why soft commodity futures and options markets are interesting for farmers:

Farmers can fix operating margins by determining selling price up to 16 months in advance.

Thus, accessing to soft commodity markets contributes to enhance the financial sustainability of the farm.

Correlation between soft commodity futures and options markets and physical markets permits an efficient hedging strategy in a downward or upward case.

Why should farmers adopt a hedging strategy:

High price volatility+

Decreasing operating margin=

Operating risk

28

6. Crédit Agricole’s soft commodities hedging services

3 actors are involved in Crédit Agricole’s soft commodity hedging services :

> Crédit Agricole Regional Banks

> Newedge Group

Crédit Agricole Group – Société Générale joint venture A world leader giving clients the opportunity to access more than 80 global exchanges

Functions: Direct transfer of orders through phone to the trading floor in charge of execution Same access for farmers and major actors Assistance and advisory from Newedge experts Daily balance reporting

> Agritel

Training

29

6. Crédit Agricole’s soft commodities hedging services

Opening of a “MAT” bank account

1. Bank account opening with 3 products: Opening of a bank account exclusively dedicated to futures and

options markets Issuance of a compulsory bank guarantee as required by the financial

market regulator Loan granting in order to post regulatory collateral and daily margin

call

2. Process Meeting with the farmer and his banker Determination of the maximum number of lots that the farmer can

subscribe and of the required credit amount and guarantee according crop rotation and yield

2 weeks = delay between the first meeting and the opening of the dedicated bank account

30

1. Introduction to Crédit Agricole Group2. Key features and figures of France’s farming

sector3. The risk approach of Crédit Agricole4. An accelerated and integrated solution for the

financing of farm machinery: the AGILOR solution5. Crédit Agricole’s agricultural insurance services:

crop insurance6. Crédit Agricole’s soft commodities hedging

services7. Crédit Agricole’s risk policy and monitoring

methodology

Risk management in agricultural financing

Crédit Agricole: a leading partner to an ever-changing world

31

7. Crédit Agricole’s risk policy and monitoring methodology

7.1. Guarantee policy

The best guarantee:

The perfect knowledge of the farmer, his business and his environment

For long term loans and large loan amounts:Such as: acquisition of a farm, of land or real estate, hydroponics setup

Additional requirements: Either a personal guarantee Or a mortgage/a pledge on farm machinery as a collateral for all or part of the loan.

For short term loans: A crop or livestock warrant From time to time, direct payment from buyers (cooperative or trader) or from the proceeds of the Single Farm System (CAP)

32

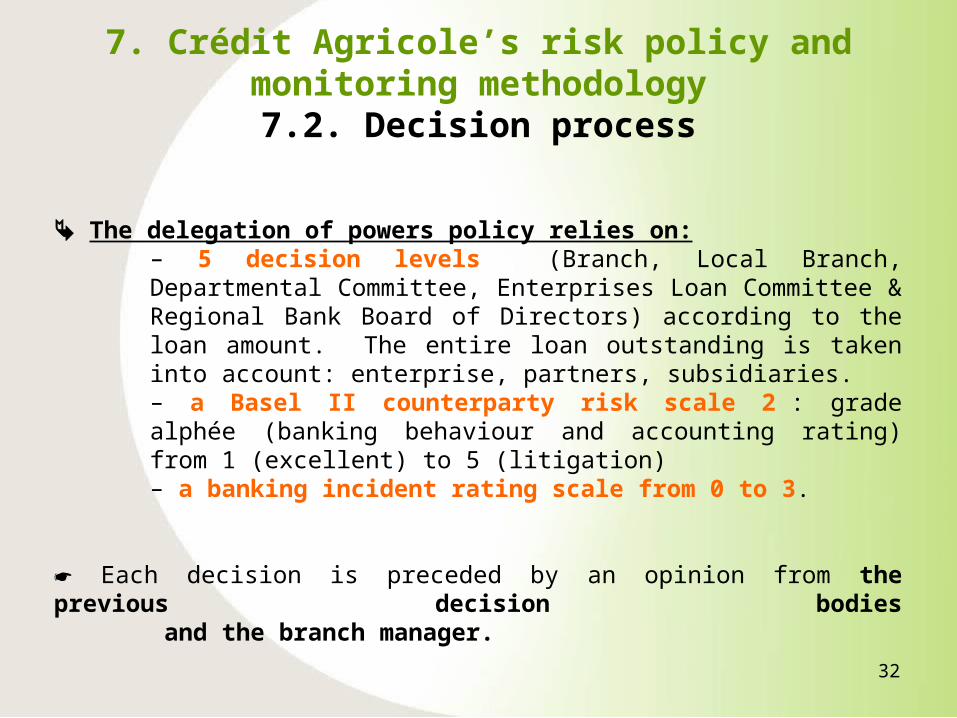

7. Crédit Agricole’s risk policy and monitoring methodology

7.2. Decision process

The delegation of powers policy relies on:– 5 decision levels (Branch, Local Branch, Departmental Committee, Enterprises Loan Committee & Regional Bank Board of Directors) according to the loan amount. The entire loan outstanding is taken into account: enterprise, partners, subsidiaries.– a Basel II counterparty risk scale 2 : grade alphée (banking behaviour and accounting rating) from 1 (excellent) to 5 (litigation) – a banking incident rating scale from 0 to 3.

Each decision is preceded by an opinion from the previous decision bodies

and the branch manager.

33

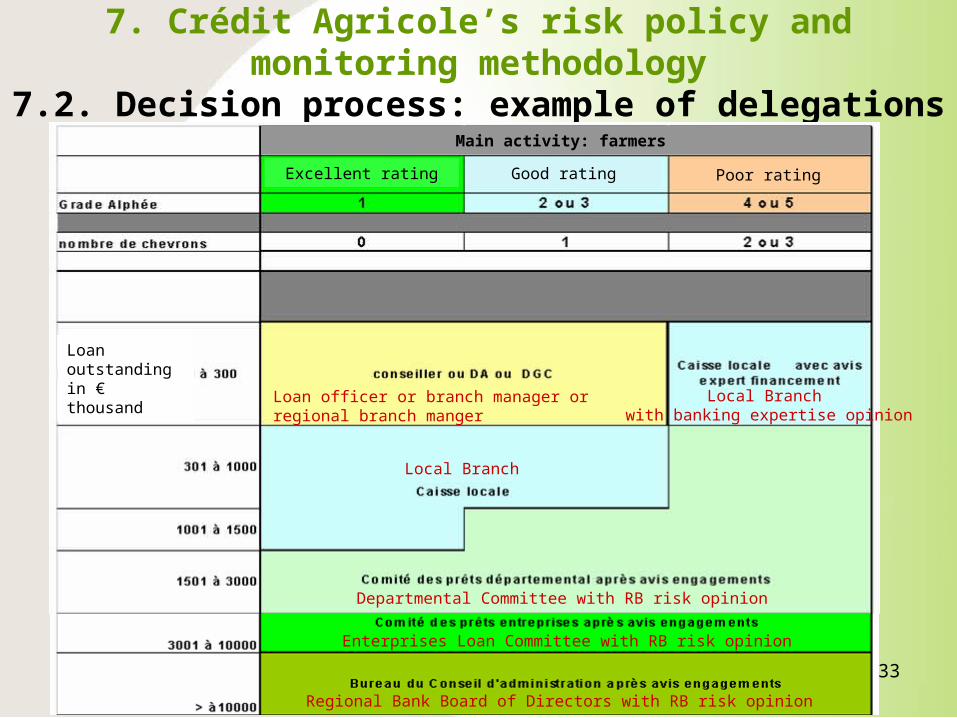

7. Crédit Agricole’s risk policy and monitoring methodology

7.2. Decision process: example of delegations of powerMain activity: farmers

Loan outstandingin € thousand Loan officer or branch manager or regional

branch manger

Departmental Committee with RB risk opinion

Enterprises Loan Committee with RB risk opinion

Local Branch

Regional Bank Board of Directors with RB risk opinion

Local Branch with banking expertise opinion

Excellent rating Good rating Poor rating

34

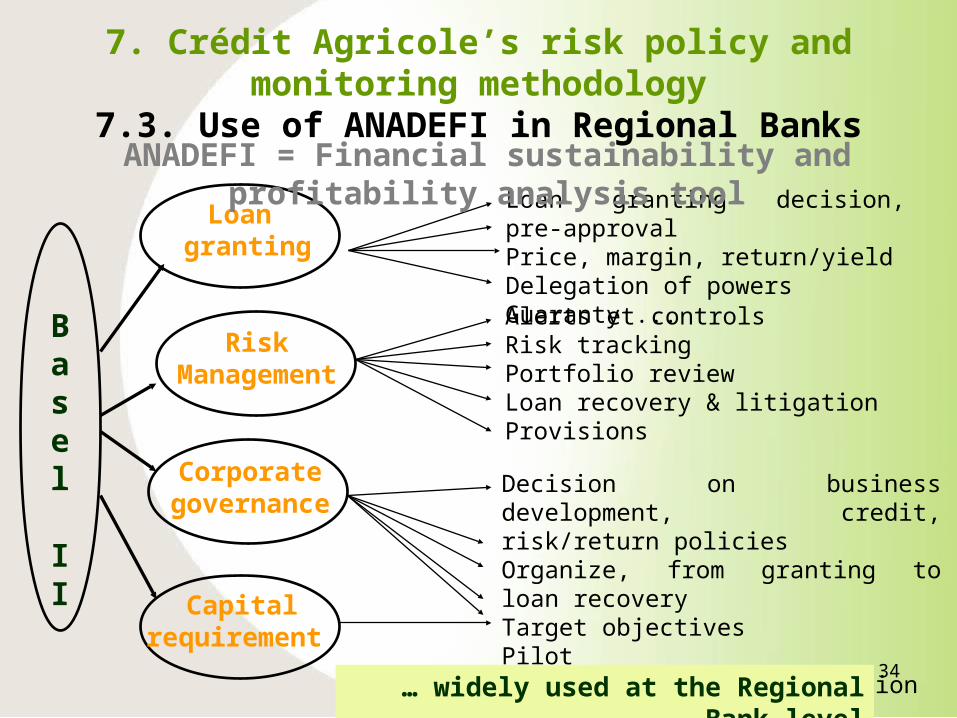

7. Crédit Agricole’s risk policy and monitoring methodology

7.3. Use of ANADEFI in Regional Banks

Loan granting decision, pre-approval Price, margin, return/yieldDelegation of powersGuaranty ...

Basel II

RiskManagement

Corporategovernance

Alerts et controls Risk trackingPortfolio reviewLoan recovery & litigationProvisions

Loan granting

Capitalrequirement

Decision on business development, credit, risk/return policies Organize, from granting to loan recoveryTarget objectives PilotFinancial management decision

… widely used at the Regional Bank level

ANADEFI = Financial sustainability and profitability analysis tool

35

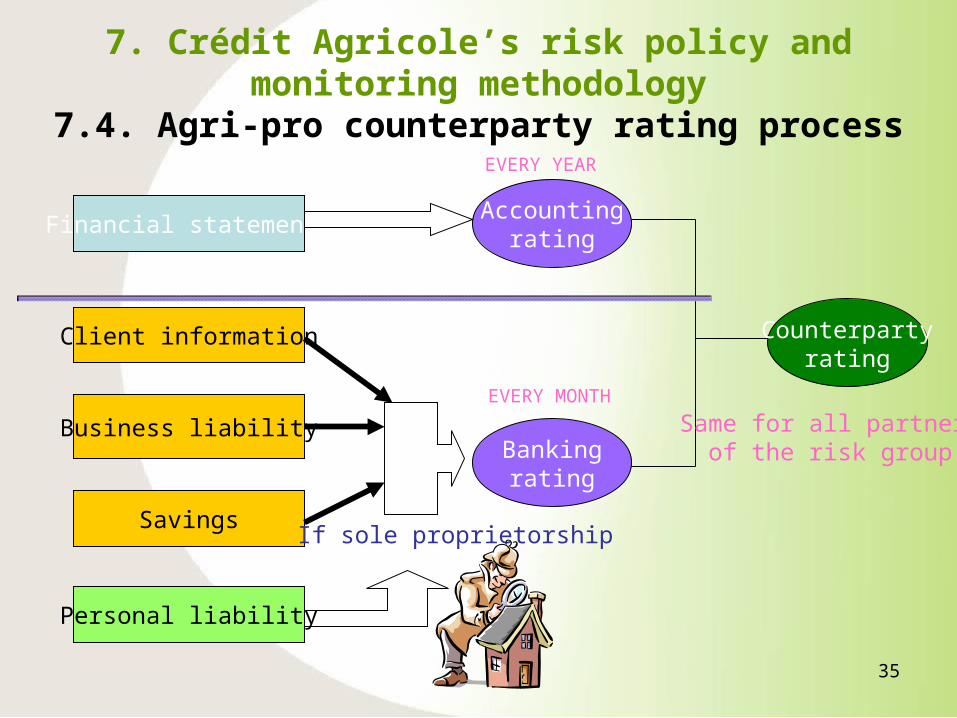

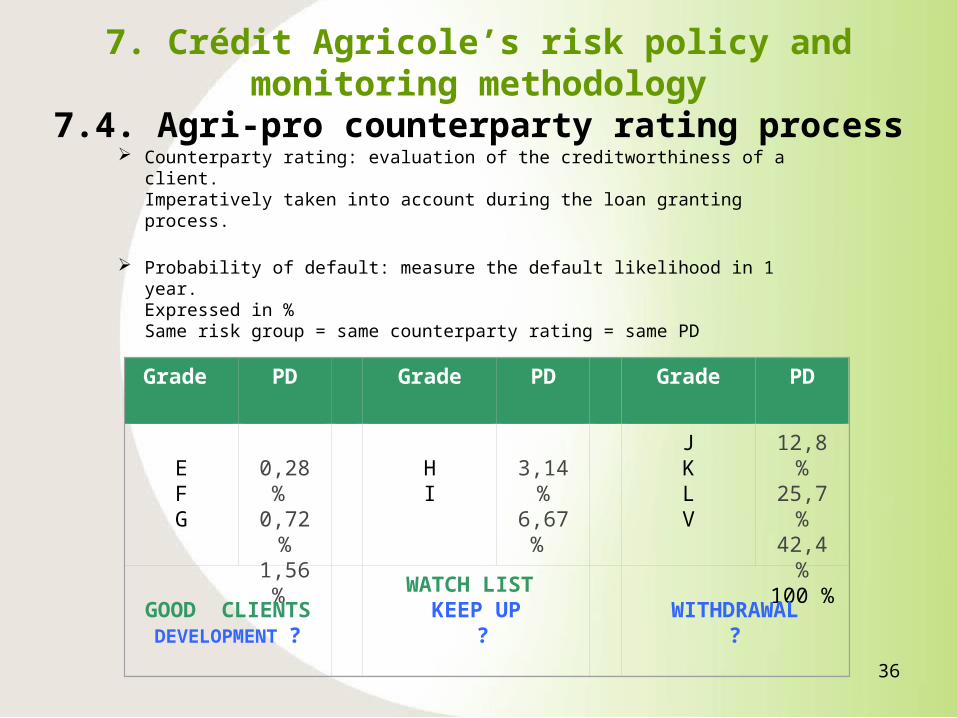

7. Crédit Agricole’s risk policy and monitoring methodology

7.4. Agri-pro counterparty rating process

Financial statementsAccounting

rating

Client information

Business liability

Savings

Personal liability

If sole proprietorship

Bankingrating

Counterpartyrating

EVERY YEAR

EVERY MONTH

Same for all partnersof the risk group

36

7. Crédit Agricole’s risk policy and monitoring methodology

7.4. Agri-pro counterparty rating process Counterparty rating: evaluation of the creditworthiness of a client.

Imperatively taken into account during the loan granting process.

Probability of default: measure the default likelihood in 1 year.Expressed in %Same risk group = same counterparty rating = same PD

Grade PD Grade PD Grade PD

EFG

0,28 % 0,72 %1,56 %

HI

3,14 %6,67 %

JKLV

12,8 %25,7 %42,4 %100 %

GOOD CLIENTS

DEVELOPMENT ?

WATCH LIST KEEP UP

?

WITHDRAWAL

?

37

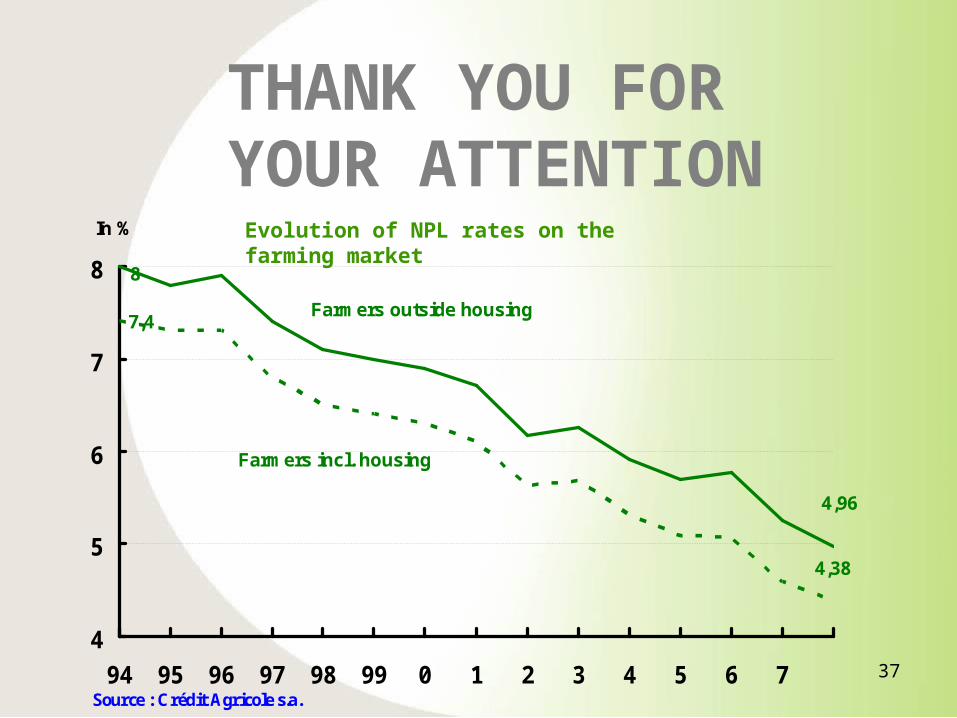

Source : Crédit Agricole s.a.

In %

4

5

6

7

8

94 95 96 97 98 99 0 1 2 3 4 5 6 7

Farmers outside housing7,4

4,38

Farmers incl. housing

8

4,96

Evolution of NPL rates on the farming market

THANK YOU FOR YOUR ATTENTION