Embed Size (px)

Citation preview

1

Review of Youth Training – Background Evidence Presentation

October 2014

2

• This slide pack set outs the economic and social context within which the review of youth training is taking place. It includes:

a summary of key messages;

the economic and labour market context;

the economic context for young people in particular;

the social context;

Northern Ireland’s skills profile and education statistics; and

national and international evidence of benefits of investment in vocational training especially for young people.

Objectives

3

Summary of key messages

• While the global downturn had a major impact on the NI economy in relation to falling output and rising unemployment a number of economic indicators have recently shown that the economy is moving back in a positive direction.

• The recent economic growth data in NI has largely seen a positive upward trend in output; more jobs are being created and this has lead to lower rates of unemployment.

• Longer term economic challenges remain: Northern Ireland continues to have low levels of output per head, a weak private sector.

• In terms of salary NI has the lowest salary of all UK regions however there is strong evidence that higher skills are associated with higher earnings.

• Northern Ireland is less well developed than the rest of the UK in a number of sectors that are likely to drive future growth such as ICT, Finance and Professional and Technical Activities. In addition youth unemployment rates are particularly high in Northern Ireland compared to the rest of the UK and many European countries.

4

Summary of key messages

• Skill levels in Northern Ireland have improved steadily over recent years. With the proportion of working aged adults qualified to level 2+, 3+ and 4+ all increasing from 2006 levels.

• However despite these figures NI skills profile is still weaker than other UK countries and the ROI.

• Almost 70% of pupils are now staying at school beyond year 12 and more school leavers are now entering HE and FE institutions.

• While there is an improving trend in the proportion of school leavers achieving at least 5 GCSE’s A*-C, by 2012/13, 21.5% of school leavers are still not achieving 5 GCSEs A*-C and 37.8% of pupils leave school without 5 GCSEs A*-C including English and Maths.

5

Summary of key messages (Cont’d)

• Literacy rates play an important role in the probability of not being in Education Employment or Training (NEET). In NI the literacy rates of school children (15 years old) are similar to the OECD average, however those aged 16-18 have literacy levels that are below the OECD average.

• Skills will be an important driver for growth and as the NI economy develops its demand for higher level skills will increase.

• Current skills deficiencies in NI include; employers noting difficulties recruiting people with the skills they need across a range of sectors from trade occupations to software development. Issues also relate to improving skill provision, sector attractiveness and stakeholder engagement.

• In NI employer investment in training per employee is relatively low by UK standards with 77% of NI firms providing training for staff compared to a UK average of 86% (NI Employer Skill Survey 2013)

6

Summary of key messages (Cont’d)

• Domestically Northern Ireland is making progress in terms of upskilling the workforce, However there is still a significant percentage of our workforce still that have no or low qualifications.

• There is a need to increase higher level skills (qualifications level 4 and above) with 50% of jobs in 2020 likely to require skills at that level including higher professional and technical skills; There is also a need for additional and improved technical skills across a range of sectors; Northern Ireland requires more individuals achieving STEM qualifications; and Vocational Training will have a critical role to play in addressing these needs and developing the skills required both now and in the future. Also there is a need for increasing literacy and numeracy skills as well as managerial and leadership skills.

• vocational qualifications deliver substantial wage and employment benefits over the learner’s lifetime, On average, individuals with an intermediate apprenticeship earn £48,000 to £74,000 more than similar individuals with Level 1 qualifications.

• Evidence from the Employer Skills Survey show that 70% of employers in Northern Ireland consider skills to have a positive impact on the performance of their employees, the highest of all UK countries. Yet a lower proportion of employers in Northern Ireland have taken steps to address the skills gaps of their staff - the lowest in the UK.

7

Summary of key messages (Cont’d)

8

The Economic and Labour Market Context

Source: NISRA, ONS

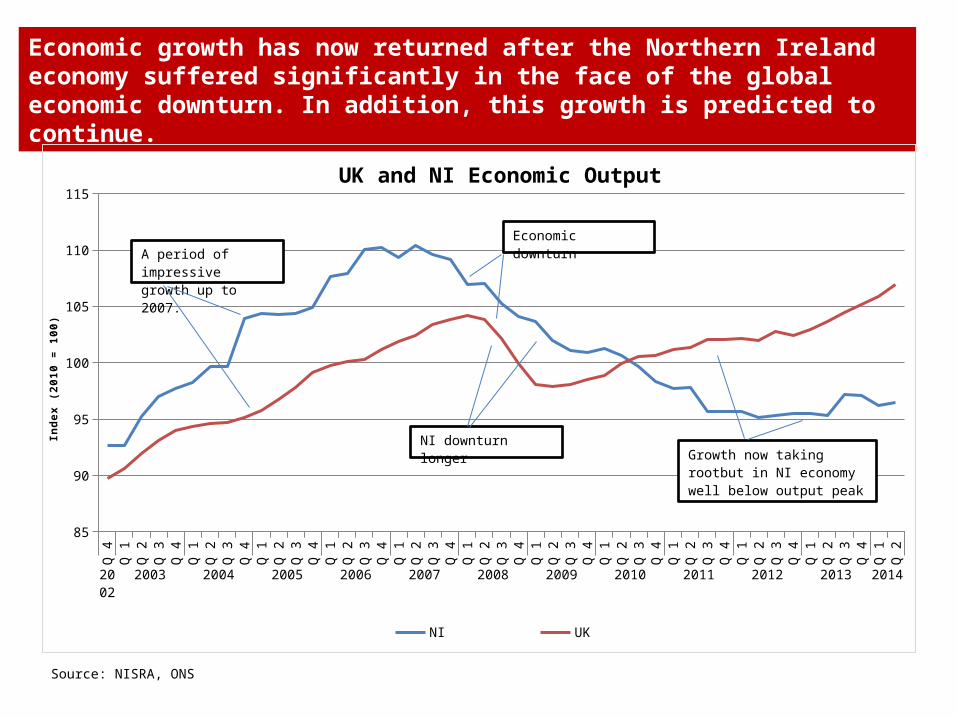

Economic growth has now returned after the Northern Ireland economy suffered significantly in the face of the global economic downturn. In addition, this growth is predicted to continue.

Q 4

Q 1

Q 2

Q 3

Q 4

Q 1

Q 2

Q 3

Q 4

Q 1

Q 2

Q 3

Q 4

Q 1

Q 2

Q 3

Q 4

Q 1

Q 2

Q 3

Q 4

Q 1

Q 2

Q 3

Q 4

Q 1

Q 2

Q 3

Q 4

Q 1

Q 2

Q 3

Q 4

Q 1

Q 2

Q 3

Q 4

Q 1

Q 2

Q 3

Q 4

Q 1

Q 2

Q 3

Q 4

Q 1

Q 2

2002

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

85

90

95

100

105

110

115UK and NI Economic Output

NI UK

Ind

ex

(2

01

0 =

10

0)

A period of impressive growth up to 2007.

Economic downturn

NI downturn longerGrowth now taking rootbut in NI economy well below output peak

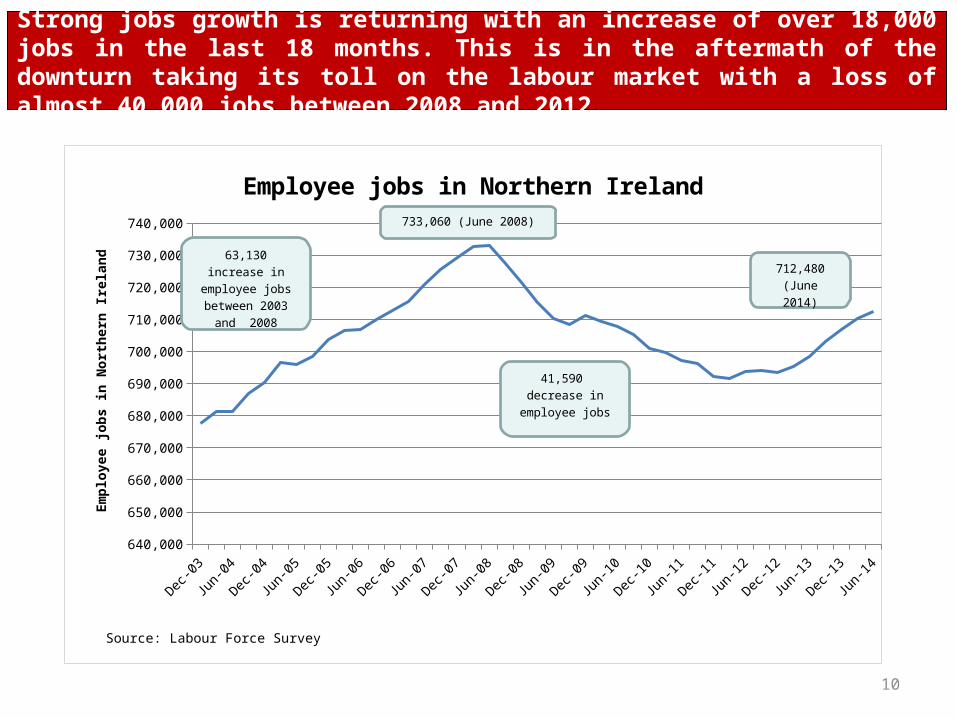

Strong jobs growth is returning with an increase of over 18,000 jobs in the last 18 months. This is in the aftermath of the downturn taking its toll on the labour market with a loss of almost 40,000 jobs between 2008 and 2012.

10

Dec-03

Jun-04

Dec-04

Jun-05

Dec-05

Jun-06

Dec-06

Jun-07

Dec-07

Jun-08

Dec-08

Jun-09

Dec-09

Jun-10

Dec-10

Jun-11

Dec-11

Jun-12

Dec-12

Jun-13

Dec-13

Jun-14640,000

650,000

660,000

670,000

680,000

690,000

700,000

710,000

720,000

730,000

740,000

Employee jobs in Northern Ireland

Source: Labour Force Survey

Empl

oyee

jobs

in N

orth

ern

Irela

nd

733,060 (June 2008)

41,590 decrease in em-

ployee jobs

63,130 increase in employee jobs be-tween 2003 and

2008

712,480(June 2014)

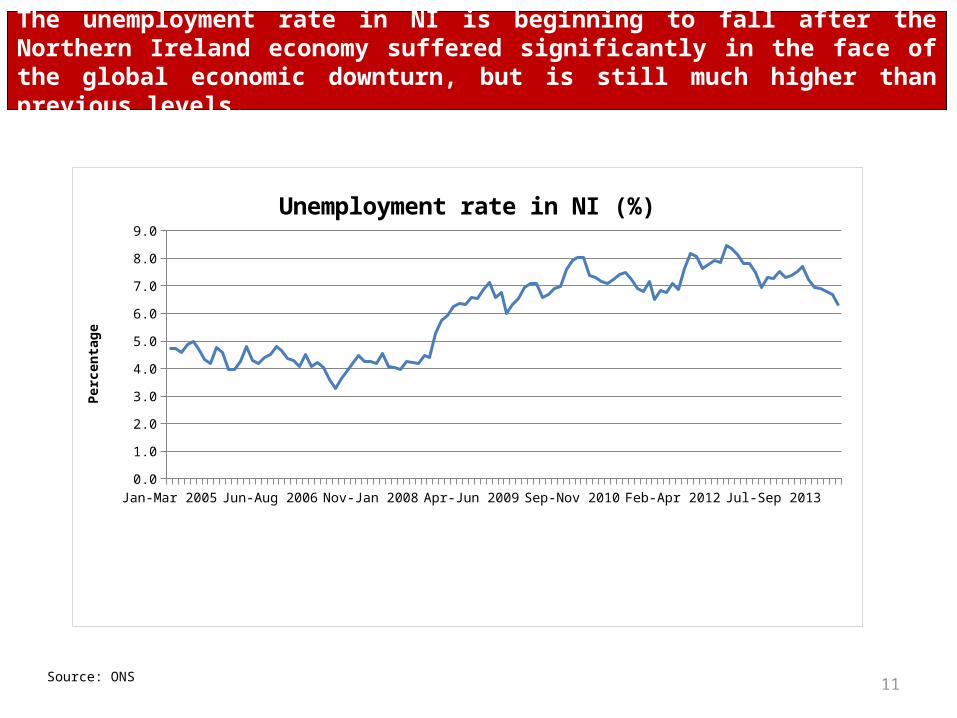

The unemployment rate in NI is beginning to fall after the Northern Ireland economy suffered significantly in the face of the global economic downturn, but is still much higher than previous levels.

Source: ONS 11

Jan-Mar 2005 Feb-Apr 2006Mar-May 2007Apr-Jun 2008 May-Jul 2009 Jun-Aug 2010 Jul-Sep 2011 Aug-Oct 2012 Sep-Nov 20130.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Unemployment rate in NI (%)

Perc

enta

ge

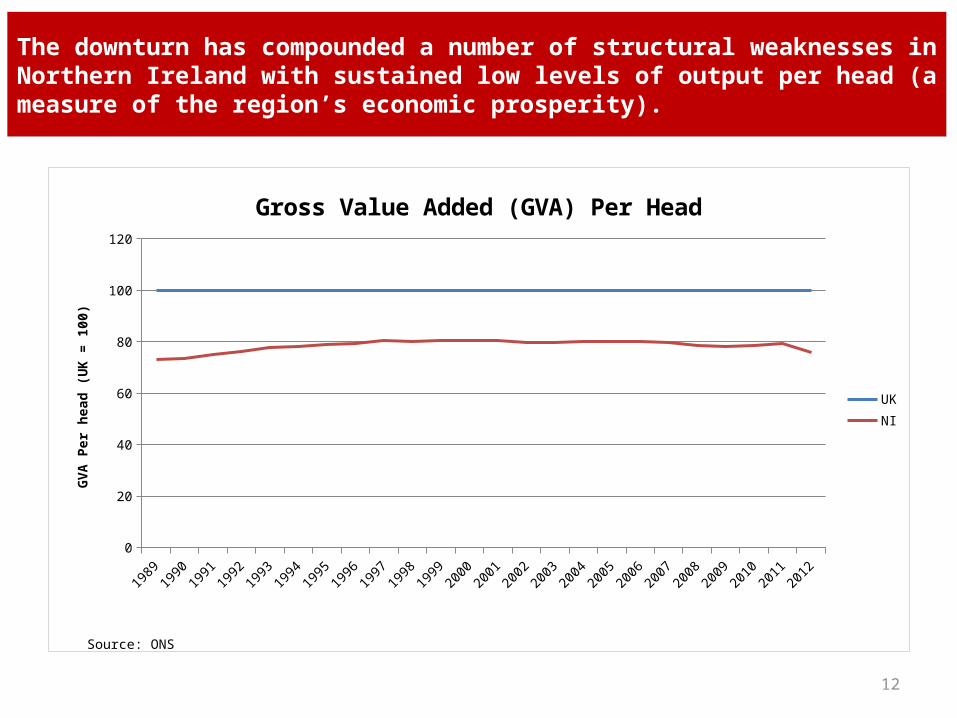

The downturn has compounded a number of structural weaknesses in Northern Ireland with sustained low levels of output per head (a measure of the region’s economic prosperity).

12

1989199019911992199319941995199619971998199920002001200220032004200520062007200820092010201120120

20

40

60

80

100

120

Gross Value Added (GVA) Per Head

UKNI

Source: ONS

GVA

Per h

ead

(UK

= 10

0)

13

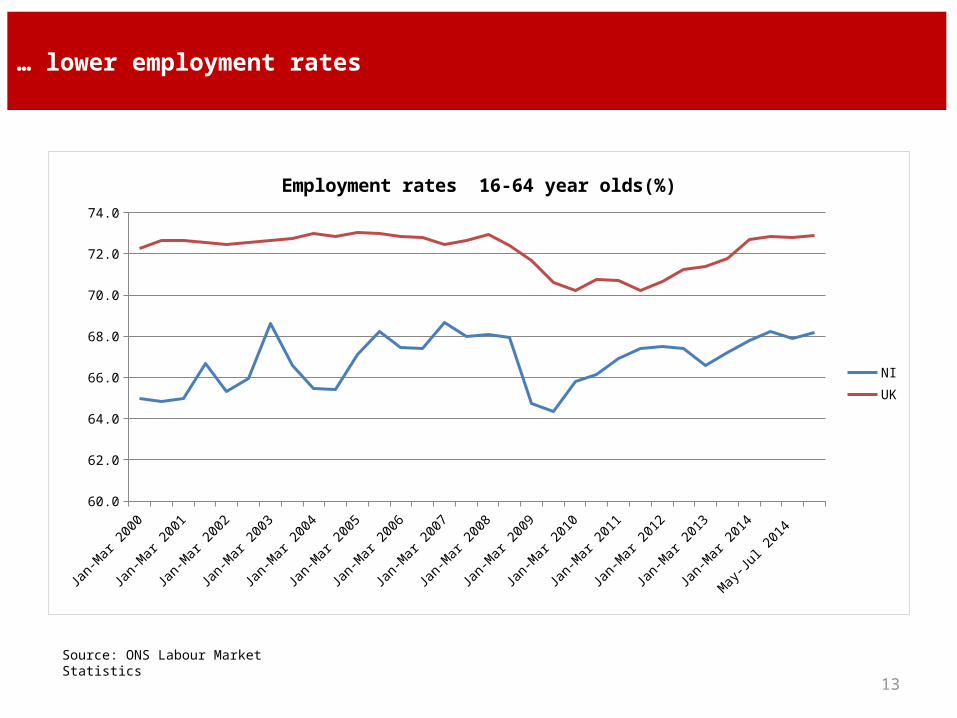

… lower employment rates

Source: ONS Labour Market Statistics

Jan-M

ar 2000

Jul-Sep

2000

Jan-M

ar 2001

Jul-Sep

2001

Jan-M

ar 2002

Jul-Sep

2002

Jan-M

ar 2003

Jul-Sep

2003

Jan-M

ar 2004

Jul-Sep

2004

Jan-M

ar 2005

Jul-Sep

2005

Jan-M

ar 2006

Jul-Sep

2006

Jan-M

ar 2007

Jul-Sep

2007

Jan-M

ar 2008

Jul-Sep

2008

Jan-M

ar 2009

Jul-Sep

2009

Jan-M

ar 2010

Jul-Sep

2010

Jan-M

ar 2011

Jul-Sep

2011

Jan-M

ar 2012

Jul-Sep

2012

Jan-M

ar 2013

Jul-Sep

2013

Jan-M

ar 2014

Apr-Jun 2014

May-Ju

l 2014

Jun-Aug 2

01460.0

62.0

64.0

66.0

68.0

70.0

72.0

74.0

Employment rates 16-64 year olds(%)

NIUK

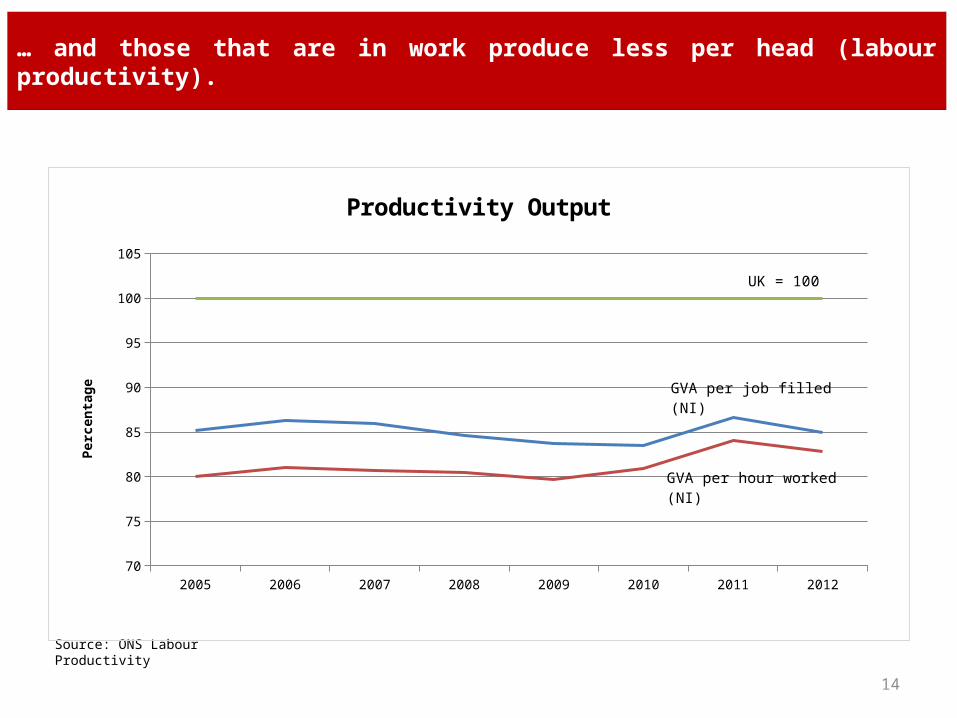

… and those that are in work produce less per head (labour productivity).

14

Source: ONS Labour Productivity

2005 2006 2007 2008 2009 2010 2011 201270

75

80

85

90

95

100

105

Productivity Output

Perc

enta

ge

GVA per job filled (NI)

GVA per hour worked (NI)

UK = 100

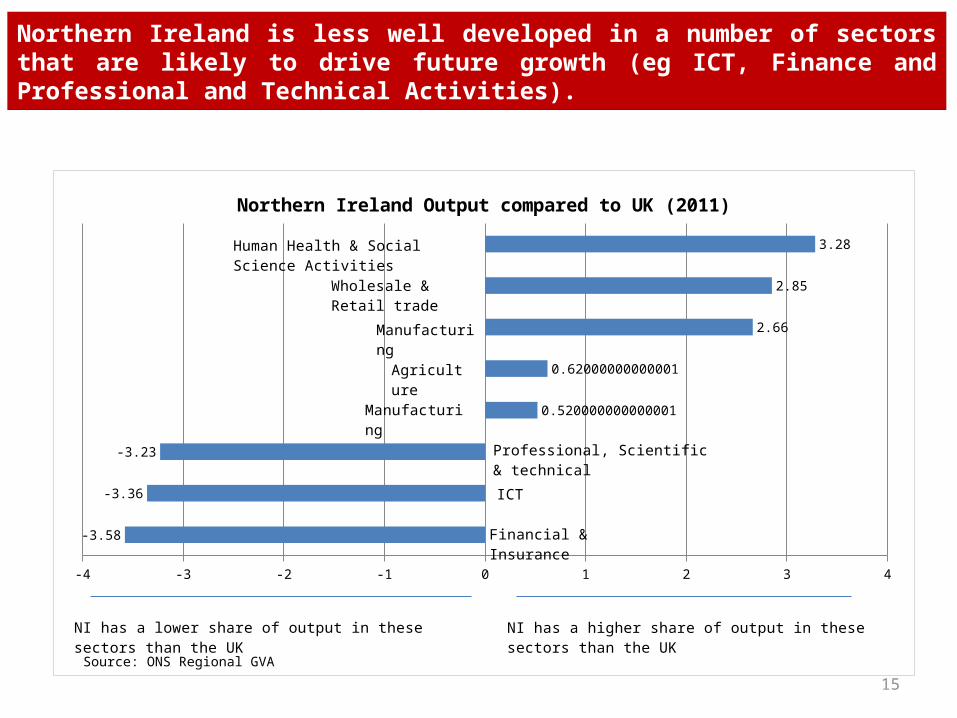

Northern Ireland is less well developed in a number of sectors that are likely to drive future growth (eg ICT, Finance and Professional and Technical Activities).

15

-4 -3 -2 -1 0 1 2 3 4

-3.58

-3.36

-3.23

0.520000000000001

0.62000000000001

2.66

2.85

3.28

Northern Ireland Output compared to UK (2011)

Human Health & Social Science Activ-ities

Wholesale & Retail trade

Manufacturing

Agriculture

Manufacturing

Professional, Scientific & technical

ICT

Financial & Insurance

Source: ONS Regional GVA

NI has a higher share of output in these sectors than the UK

NI has a lower share of output in these sectors than the UK

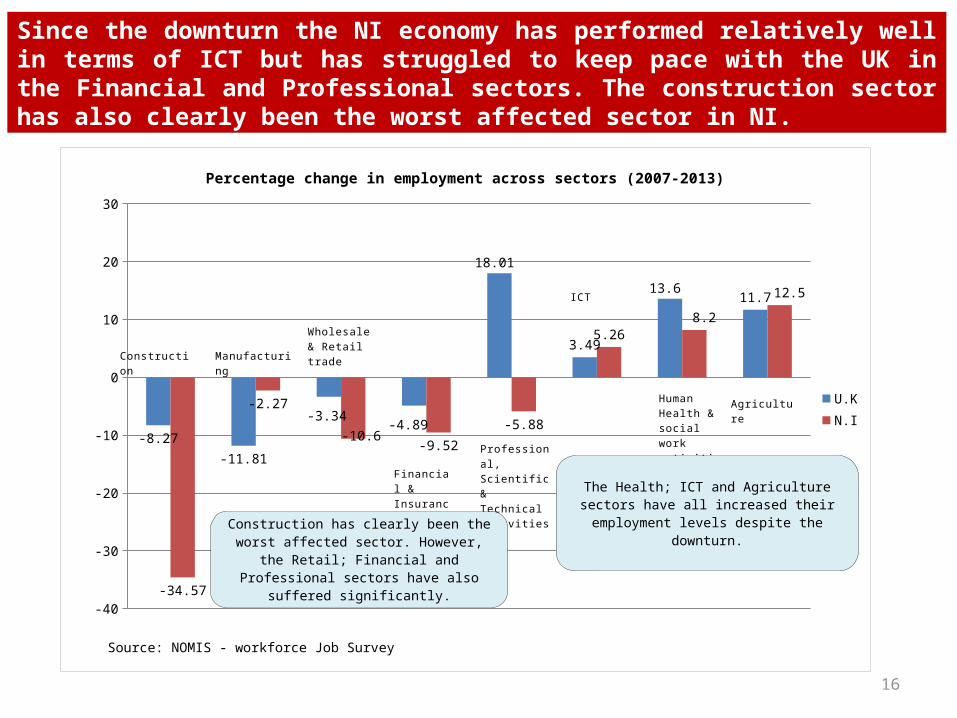

Since the downturn the NI economy has performed relatively well in terms of ICT but has struggled to keep pace with the UK in the Financial and Professional sectors. The construction sector has also clearly been the worst affected sector in NI.

16

-40

-30

-20

-10

0

10

20

30

-8.27

-11.81

-3.34-4.89

18.01

3.49

13.611.7

-34.57

-2.27

-10.6-9.52

-5.88

5.268.2

12.5

Percentage change in employment across sectors (2007-2013)

U.KN.I

Source: NOMIS - workforce Job Survey

Construction Manufacturing

Wholesale & Retail trade

Financial & Insurance

Professional, Scientific & Technical activities

ICT

Human Health & social work activities

Agriculture

Construction has clearly been the worst af-fected sector. However, the Retail; Financial and Professional sectors have also suffered

significantly.

The Health; ICT and Agriculture sectors have all increased their employment levels despite

the downturn.

17

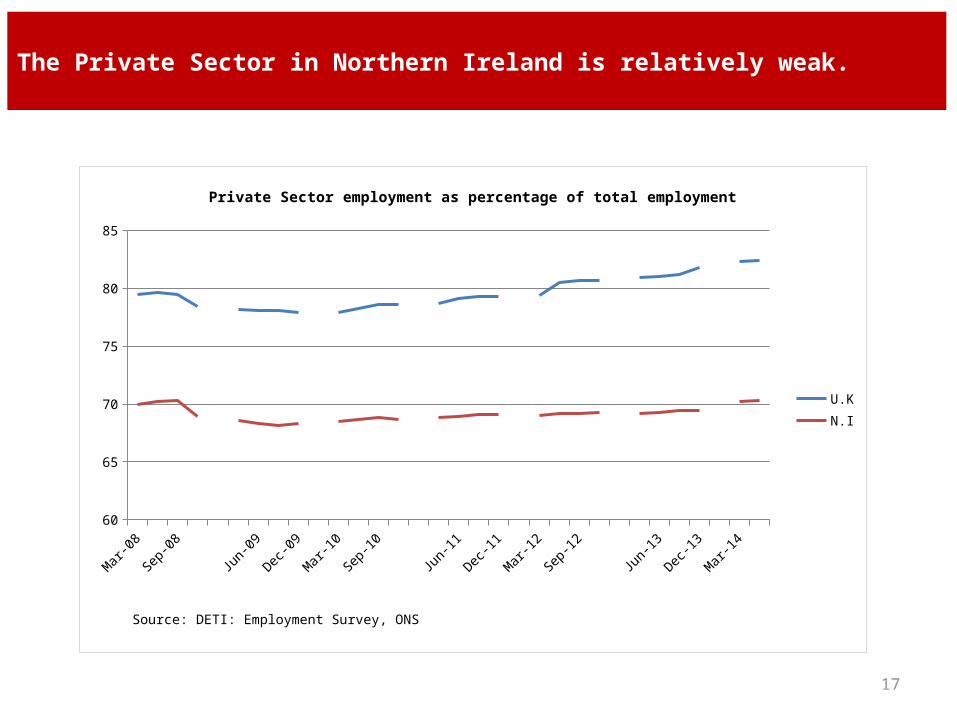

The Private Sector in Northern Ireland is relatively weak.

Mar-08

Jun-08

Sep-08

Dec-08

Mar-09

Jun-09

Sep-09

Dec-09

Mar-10

Jun-10

Sep-10

Dec-10

Mar-11

Jun-11

Sep-11

Dec-11

Mar-12

Jun-12

Sep-12

Dec-12

Mar-13

Jun-13

Sep-13

Dec-13

Mar-14

Jun-1460

65

70

75

80

85

Private Sector employment as percentage of total employment

U.KN.I

Source: DETI: Employment Survey, ONS

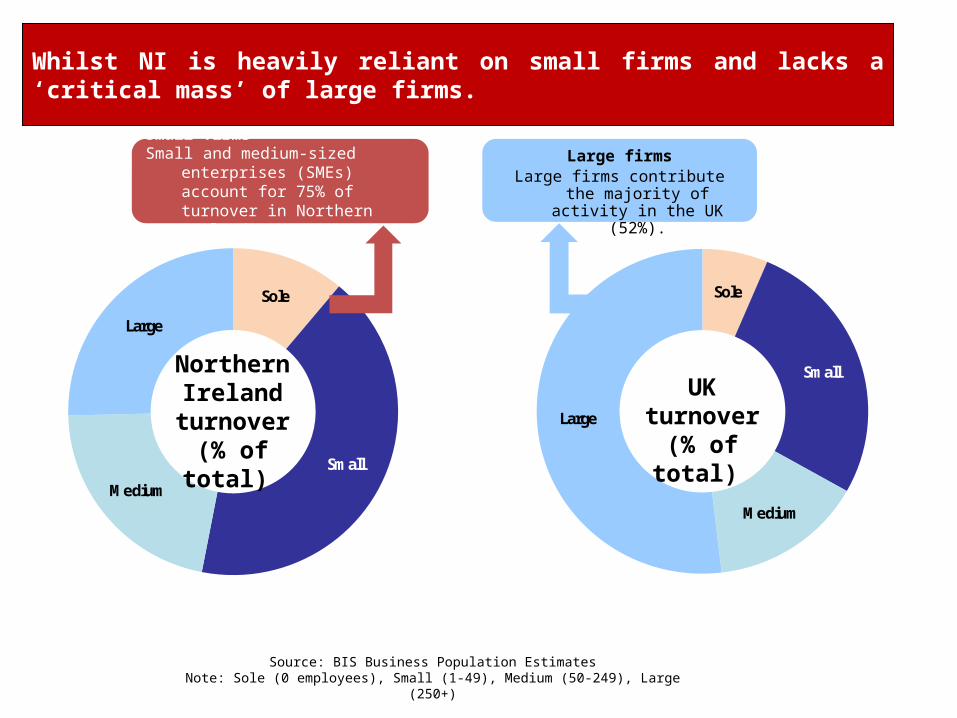

Sole

Small

Medium

Large

Sole

Small

Medium

Large

Small firmsSmall and medium-sized enterprises

(SMEs) account for 75% of turnover in Northern Ireland.

Large firmsLarge firms contribute the majority

of activity in the UK (52%).

Northern Ireland

turnover(% of total)

UKturnover

(% of total)

Source: BIS Business Population EstimatesNote: Sole (0 employees), Small (1-49), Medium (50-249), Large (250+)

Whilst NI is heavily reliant on small firms and lacks a ‘critical mass’ of large firms.

19

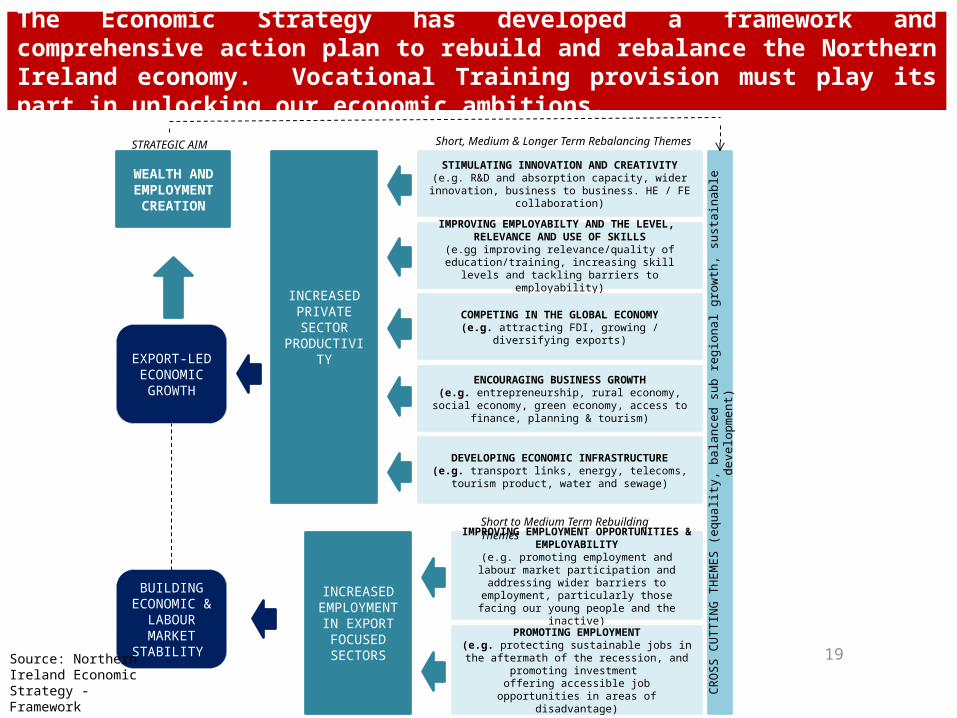

The Economic Strategy has developed a framework and comprehensive action plan to rebuild and rebalance the Northern Ireland economy. Vocational Training provision must play its part in unlocking our economic ambitions.

STIMULATING INNOVATION AND CREATIVITY(e.g. R&D and absorption capacity, wider innovation,

business to business. HE / FE collaboration)

IMPROVING EMPLOYABILTY AND THE LEVEL, RELEVANCE AND USE OF SKILLS

(e.gg improving relevance/quality of education/training, increasing skill levels and tackling barriers to employability)

COMPETING IN THE GLOBAL ECONOMY(e.g. attracting FDI, growing / diversifying exports)

ENCOURAGING BUSINESS GROWTH(e.g. entrepreneurship, rural economy, social economy, green economy, access to finance, planning & tourism)

DEVELOPING ECONOMIC INFRASTRUCTURE(e.g. transport links, energy, telecoms, tourism product,

water and sewage)

IMPROVING EMPLOYMENT OPPORTUNITIES & EMPLOYABILITY

(e.g. promoting employment and labour market participation and addressing wider barriers to

employment, particularly those facing our young people and the inactive)

PROMOTING EMPLOYMENT(e.g. protecting sustainable jobs in the aftermath of

the recession, and promoting investment offering accessible job opportunities in areas of

disadvantage)

CRO

SS C

UTT

ING

TH

EMES

(equ

ality

, bal

ance

d su

b re

gion

al g

row

th, s

usta

inab

le d

evel

opm

ent)

INCREASEDPRIVATESECTOR

PRODUCTIVITY

INCREASEDEMPLOYMENT

IN EXPORT FOCUSED SECTORS

BUILDINGECONOMIC &

LABOURMARKET

STABILITY

EXPORT-LED ECONOMIC GROWTH

WEALTH AND EMPLOYMENT

CREATION

Short to Medium Term Rebuilding Themes

Short, Medium & Longer Term Rebalancing ThemesSTRATEGIC AIM

Source: Northern Ireland Economic Strategy - Framework

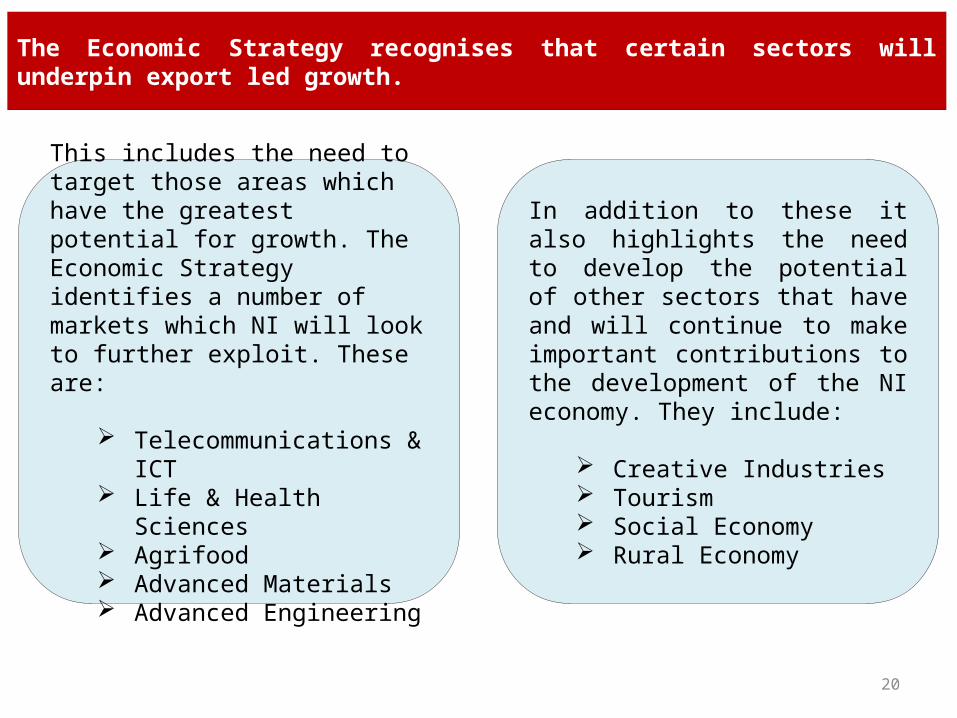

The Economic Strategy recognises that certain sectors will underpin export led growth.

20

In addition to these it also highlights the need to develop the potential of other sectors that have and will continue to make important contributions to the development of the NI economy. They include:

Creative Industries Tourism Social Economy Rural Economy

This includes the need to target those areas which have the greatest potential for growth. The Economic Strategy identifies a number of markets which NI will look to further exploit. These are:

Telecommunications & ICT Life & Health Sciences Agrifood Advanced Materials Advanced Engineering

• The global downturn has had a major impact on the NI economy: However, economic growth has returned with consistent increases in output; more jobs being created and lower levels of unemployment.

• Longer term economic challenges remain: Northern Ireland continues to have low levels of output per head, lower private sector activity and productivity particularly in key growth sectors.

• The challenge is to successfully rebuild and rebalance the local economy: skills will be critical to unlocking the region’s economic aspirations and youth and vocational training provision will be an essential ingredient.

The Northern Ireland Economy: Key Messages

21

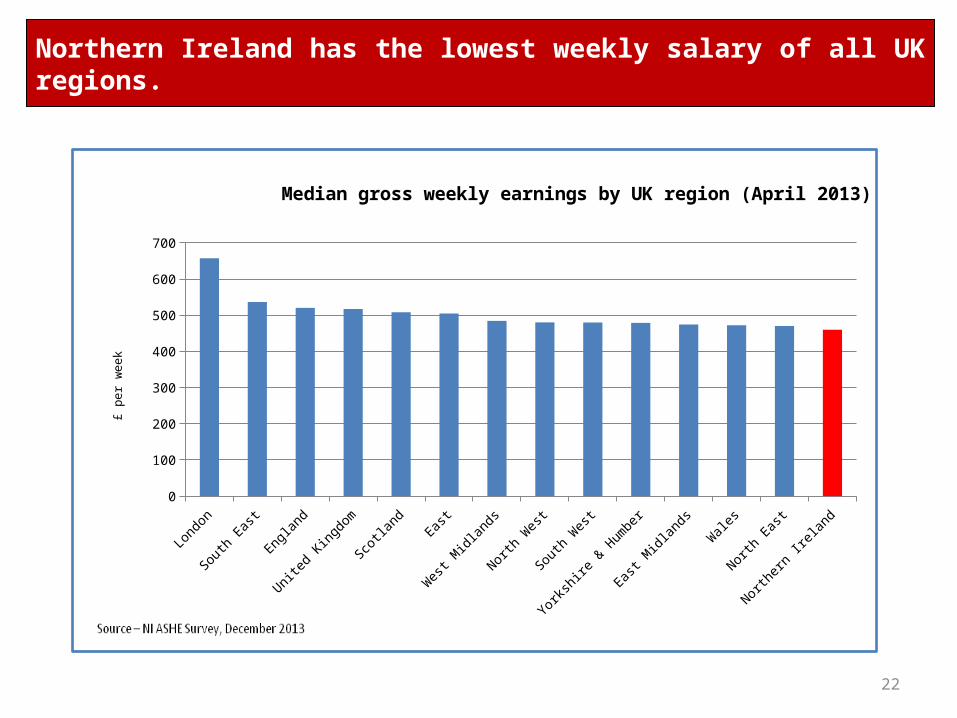

Northern Ireland has the lowest weekly salary of all UK regions.

22

Lond

on

South

Eas

t

Englan

d

United

King

dom

Scotla

ndEas

t

Wes

t Midl

ands

North

Wes

t

South

Wes

t

Yorks

hire

& Hum

ber

East M

idlan

ds

Wale

s

North

Eas

t

North

ern

Irelan

d0

100

200

300

400

500

600

700

Median gross weekly earnings by UK region (April 2013)

£ pe

r w

eek

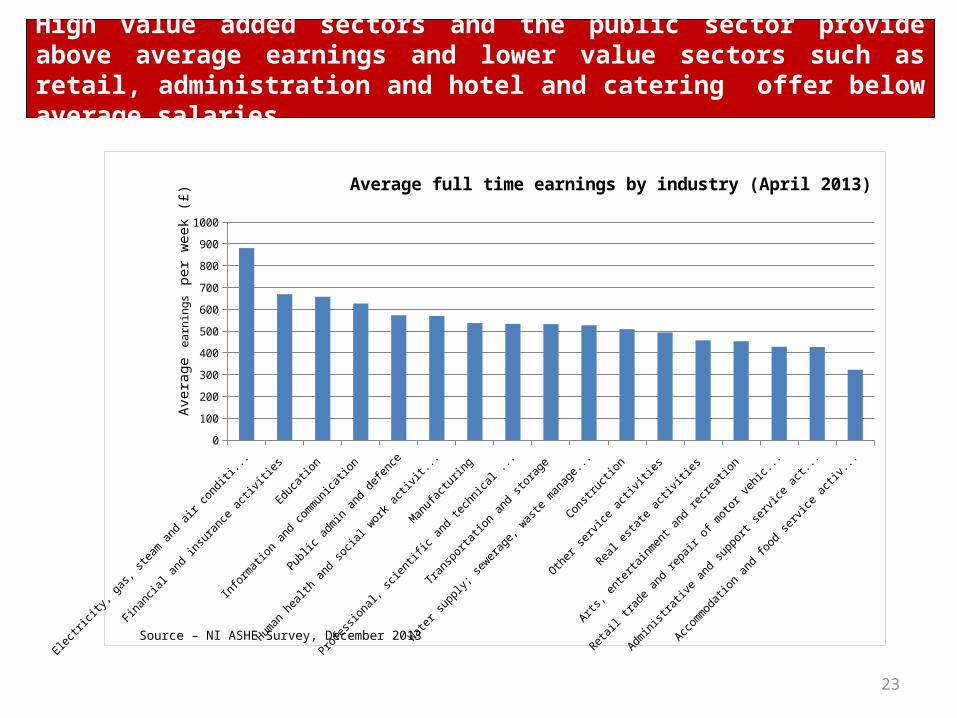

High value added sectors and the public sector provide above average earnings and lower value sectors such as retail, administration and hotel and catering offer below average salaries.

23

Electrici

ty, gas,

steam and air c

onditioning

Financial a

nd insu

rance acti

vities

Education

Information and co

mmunication

Public admin and defence

Human health and so

cial w

ork acti

vities

Manufactu

ring

Professi

onal, scie

ntific and te

chnica

l acti

vities

Transp

ortation and st

orage

Water s

upply; se

werage, waste

management

Constr

uction

Other s

ervice

activiti

es

Real e

state acti

vities

Arts

, enterta

inment and re

creation

Retail trade and re

pair of m

otor vehicl

es

Administ

rative and su

pport se

rvice

activiti

es

Acco

mmodation and food se

rvice

activiti

es 0

100

200

300

400

500

600

700

800

900

1000

Average full time earnings by industry (April 2013)

Ave

rage

ear

ning

s pe

r w

eek

(£)

Source – NI ASHE Survey, December 2013

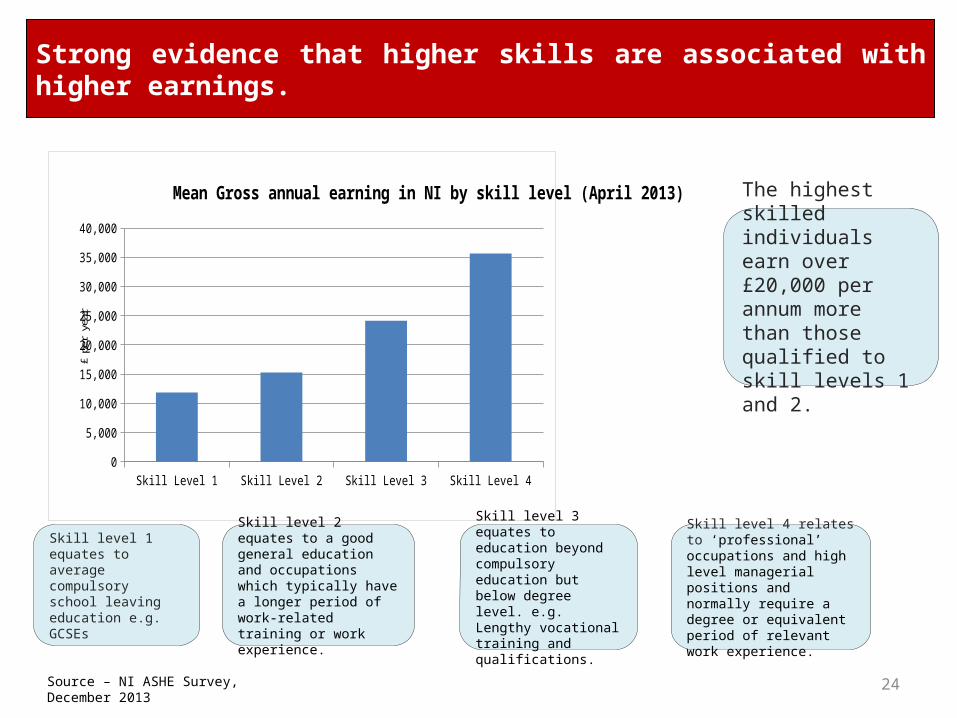

Strong evidence that higher skills are associated with higher earnings.

24

Skill Level 1 Skill Level 2 Skill Level 3 Skill Level 40

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Mean Gross annual earning in NI by skill level (April 2013)

£ pe

r ye

ar

The highest skilled individuals earn over £20,000 per annum more than those qualified to skill levels 1 and 2.

Skill level 1 equates to average compulsory school leaving education e.g. GCSEs

Skill level 4 relates to ‘professional’ occupations and high level managerial positions and normally require a degree or equivalent period of relevant work experience.

Skill level 2 equates to a good general education and occupations which typically have a longer period of work-related training or work experience.

Skill level 3 equates to education beyond compulsory education but below degree level. e.g. Lengthy vocational training and qualifications.

Source – NI ASHE Survey, December 2013

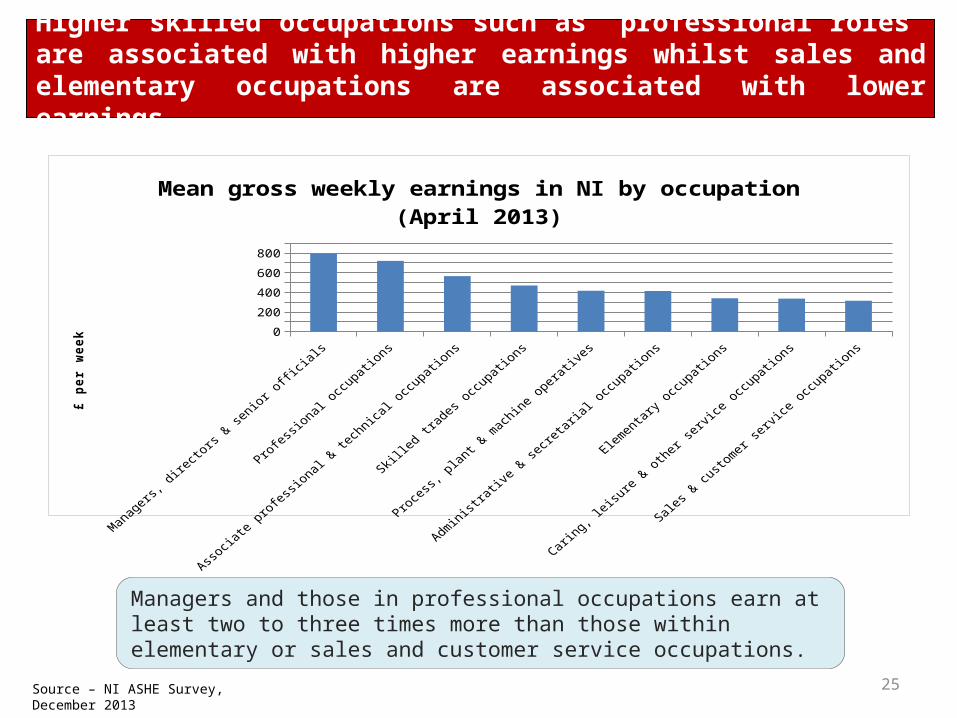

Higher skilled occupations such as ‘professional roles’ are associated with higher earnings whilst sales and elementary occupations are associated with lower earnings.

25

Managers and those in professional occupations earn at least two to three times more than those within elementary or sales and customer service occupations.

Source – NI ASHE Survey, December 2013

Manag

ers, d

irecto

rs & se

nior officia

ls

Profes

sional

occupati

ons

Associa

te pro

fessio

nal & te

chnica

l occu

pations

Skille

d trad

es occu

pations

Proces

s, plan

t & m

achine o

perative

s

Administrati

ve &

secre

tarial

occupati

ons

Elemen

tary o

ccupati

ons

Caring,

leisu

re & other

servic

e occu

pations

Sales

& cu

stomer

servic

e occu

pations

0100200300400500600700800900

Mean gross weekly earnings in NI by occupation (April 2013)

£ pe

r wee

k

26

The Economic Context for Young People

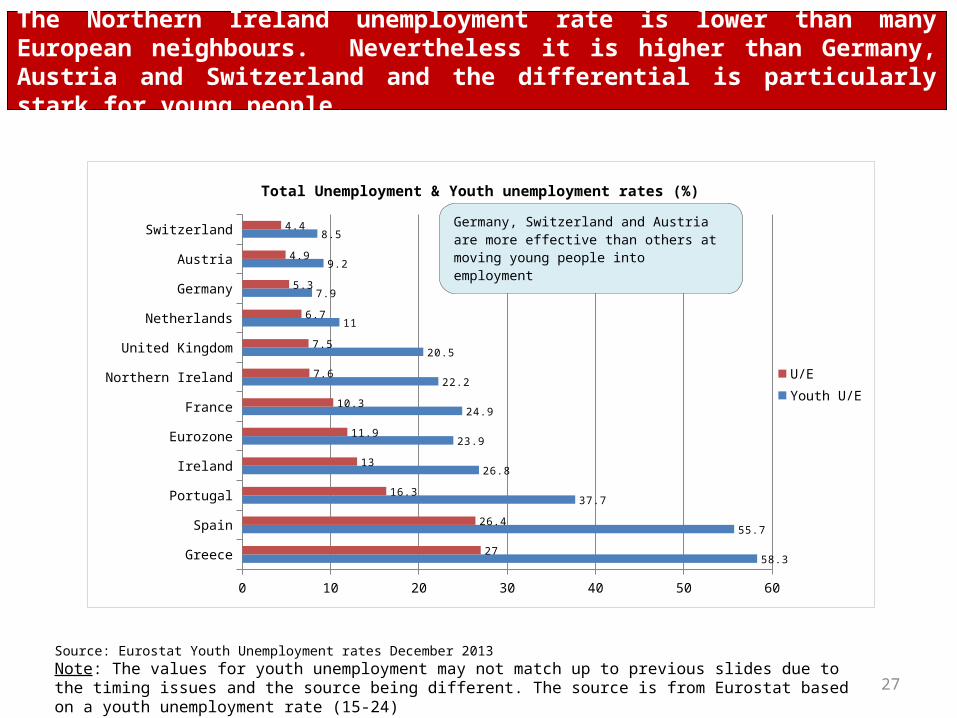

The Northern Ireland unemployment rate is lower than many European neighbours. Nevertheless it is higher than Germany, Austria and Switzerland and the differential is particularly stark for young people.

27

Source: Eurostat Youth Unemployment rates December 2013

Note: The values for youth unemployment may not match up to previous slides due to the timing issues and the source being different. The source is from Eurostat based on a youth unemployment rate (15-24)

Greece

Spain

Portugal

Ireland

Eurozone

France

Northern Ireland

United Kingdom

Netherlands

Germany

Austria

Switzerland

0 10 20 30 40 50 60

58.3

55.7

37.7

26.8

23.9

24.9

22.2

20.5

11

7.9

9.2

8.5

27

26.4

16.3

13

11.9

10.3

7.6

7.5

6.7

5.3

4.9

4.4

Total Unemployment & Youth unemployment rates (%)

U/EYouth U/E

Germany, Switzerland and Austria are more ef-fective than others at moving young people into employment

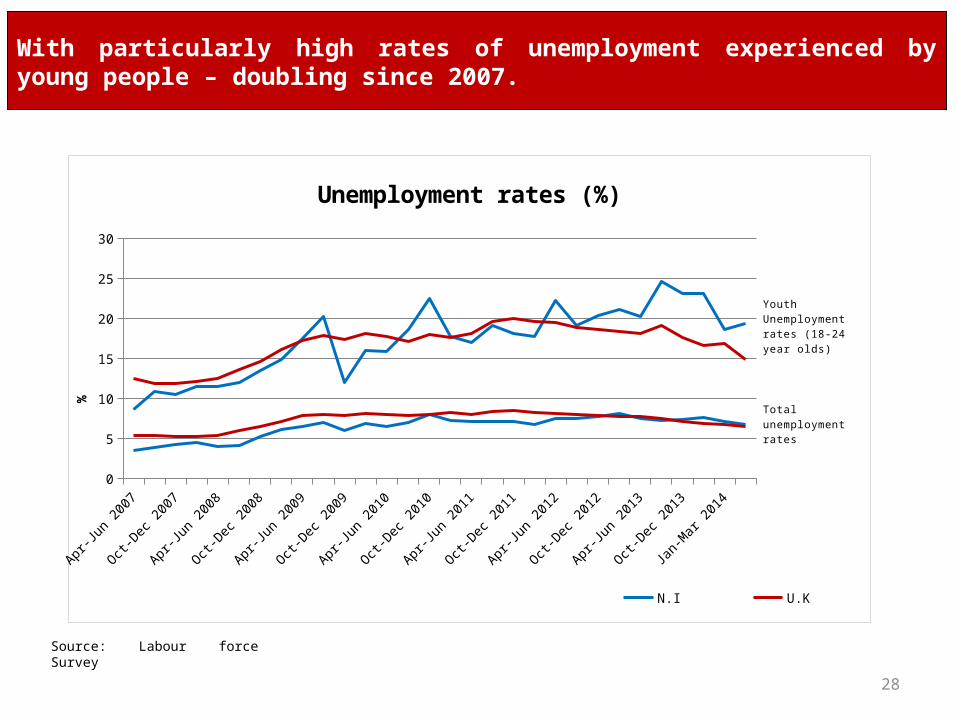

With particularly high rates of unemployment experienced by young people – doubling since 2007.

Source: Labour force Survey

28

Apr-Jun 2007

Jul-Sep

2007

Oct-Dec

2007

Jan-M

ar 2008

Apr-Jun 2008

Jul-Sep

2008

Oct-Dec

2008

Jan-M

ar 2009

Apr-Jun 2009

Jul-Sep

2009

Oct-Dec

2009

Jan-M

ar 2010

Apr-Jun 2010

Jul-Sep

2010

Oct-Dec

2010

Jan-M

ar 2011

Apr-Jun 2011

Jul-Sep

2011

Oct-Dec

2011

Jan-M

ar 2012

Apr-Jun 2012

Jul-Sep

2012

Oct-Dec

2012

Jan-M

ar 2013

Apr-Jun 2013

July-sep

t 2013

Oct-Dec

2013

Dec-Fe

b 2014

Jan-M

ar 2014

Apr-Jun 2014

0

5

10

15

20

25

30

Unemployment rates (%)

N.I U.K

%

Youth Unemploy-ment rates (18-24 year olds)

Total unemploy-ment rates

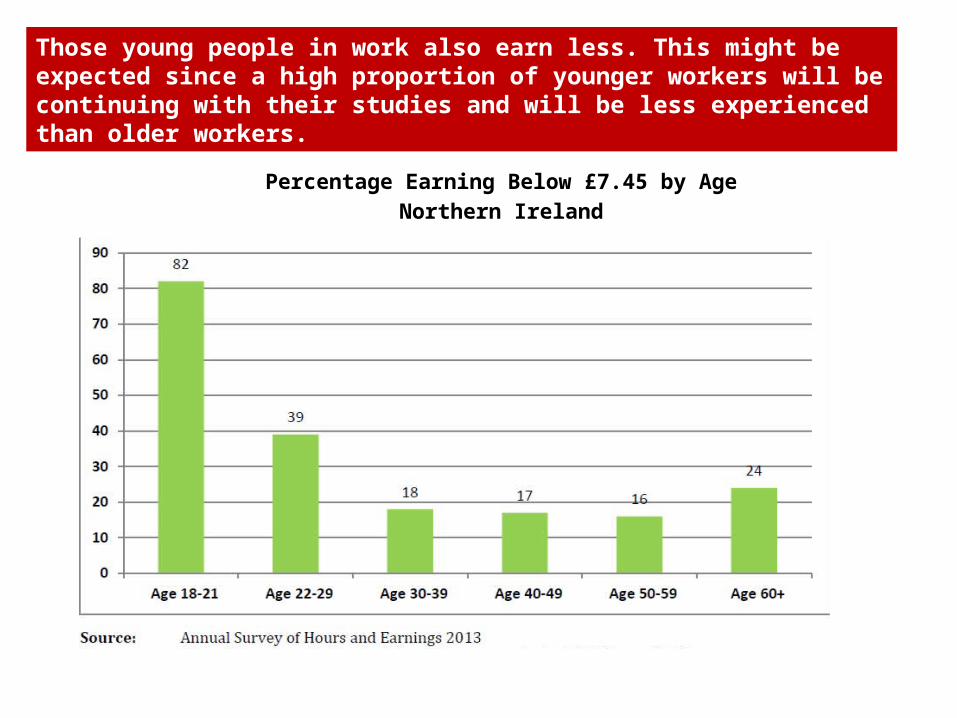

Percentage Earning Below £7.45 by AgeNorthern Ireland

Those young people in work also earn less. This might be expected since a high proportion of younger workers will be continuing with their studies and will be less experienced than older workers.

30

other

ICT

Administration

Accomadation & Food

Construction

Wholesale & Retail

Manufacturing

Agriculture

0 10 20 30 40 50 60 70

11

19

40

10

19

28

10

32

65

14

34

13

28

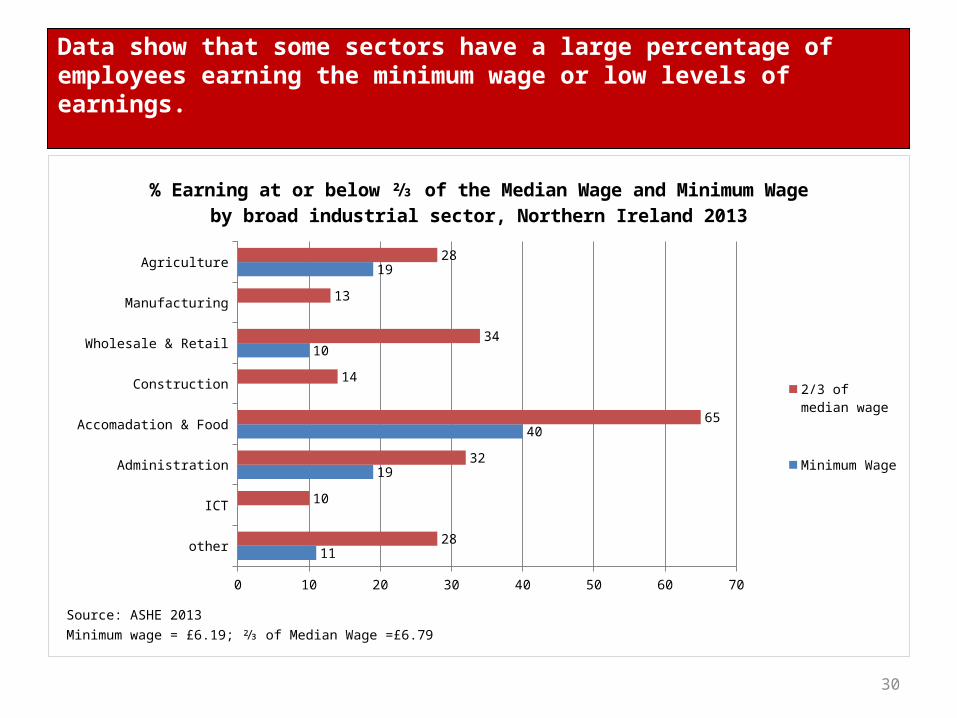

% Earning at or below ⅔ of the Median Wage and Minimum Wage by broad industrial sector, Northern Ireland 2013

2/3 of median wage

Minimum Wage

Source: ASHE 2013Minimum wage = £6.19; ⅔ of Median Wage =£6.79

Data show that some sectors have a large percentage of employees earning the minimum wage or low levels of earnings.

• As jobs become more specialised and skills intensive - the transition between education and the labour market has become increasingly complex.

• This is not just an issue related to the downturn but has been emphasised as a result of it.

• Research shows that periods of unemployment when young leave labour market scars for life (in terms of future earnings and future employment prospects).

Young people entering the economy are worthy of a particular focus.

32

Social Context

Changing incomes in Northern Ireland and the UK

33

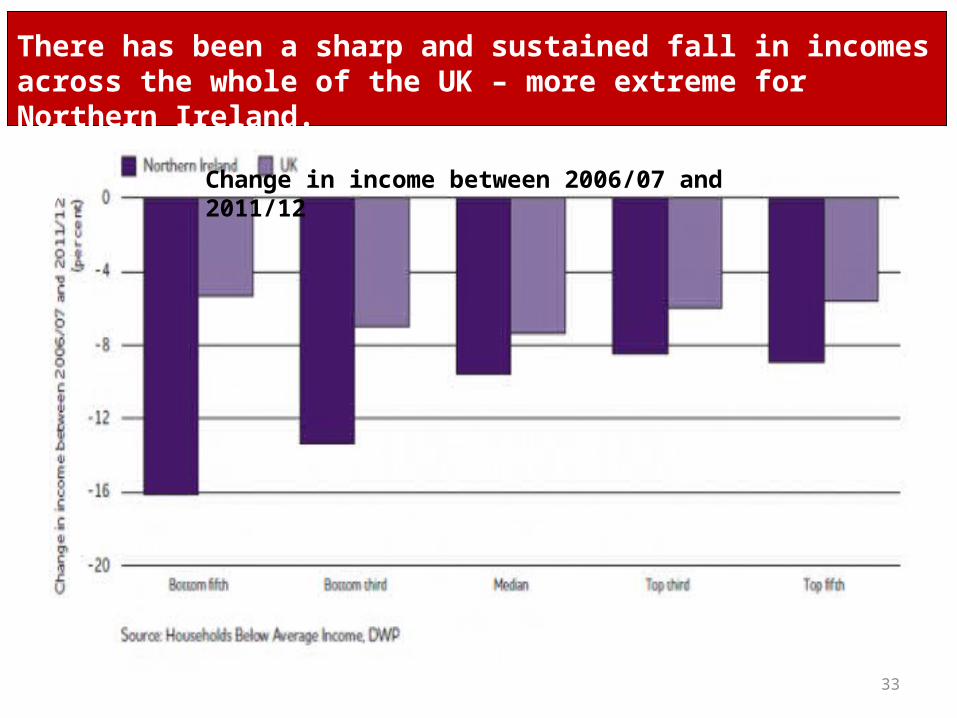

There has been a sharp and sustained fall in incomes across the whole of the UK – more extreme for Northern Ireland.

Change in income between 2006/07 and 2011/12

34

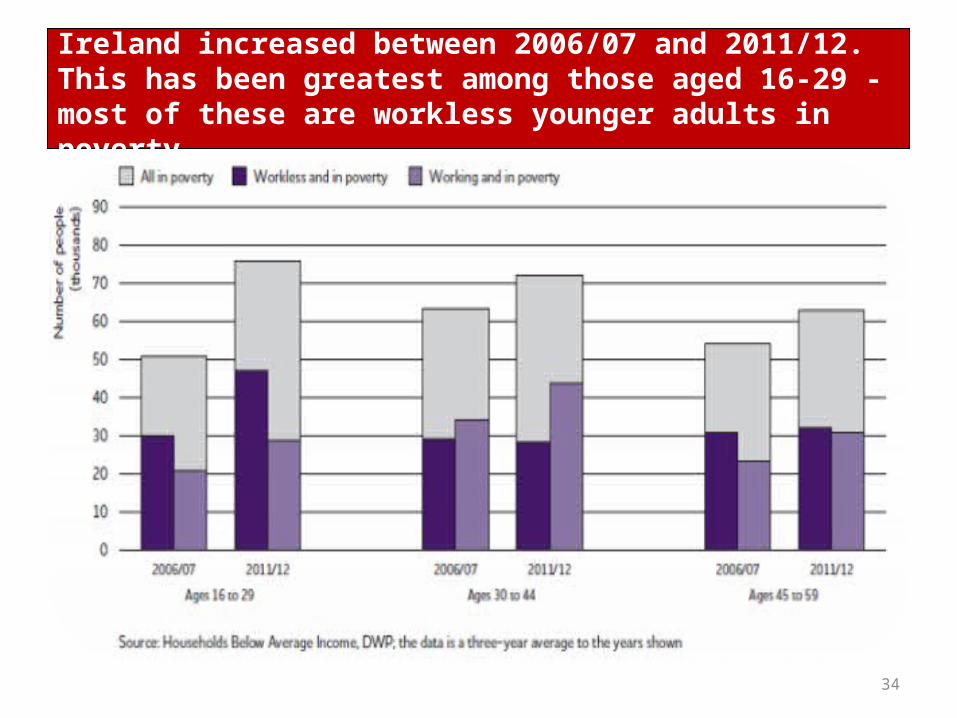

The number of people in poverty in Northern Ireland increased between 2006/07 and 2011/12. This has been greatest among those aged 16-29 - most of these are workless younger adults in poverty.

35

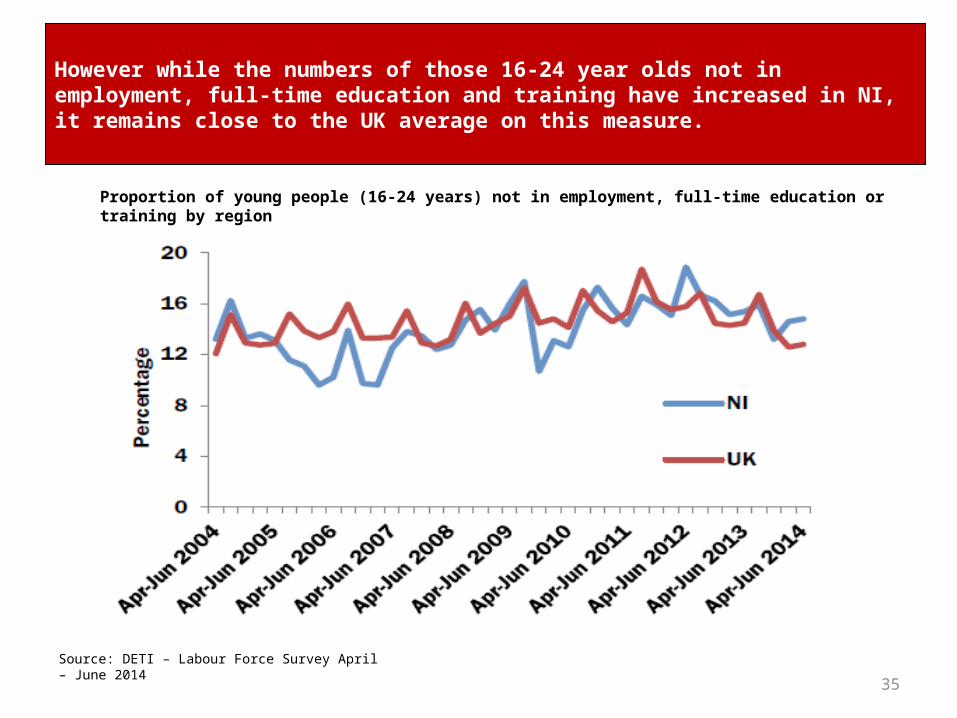

However while the numbers of those 16-24 year olds not in employment, full-time education and training have increased in NI, it remains close to the UK average on this measure.

Proportion of young people (16-24 years) not in employment, full-time education or training by region

Source: DETI – Labour Force Survey April – June 2014

36

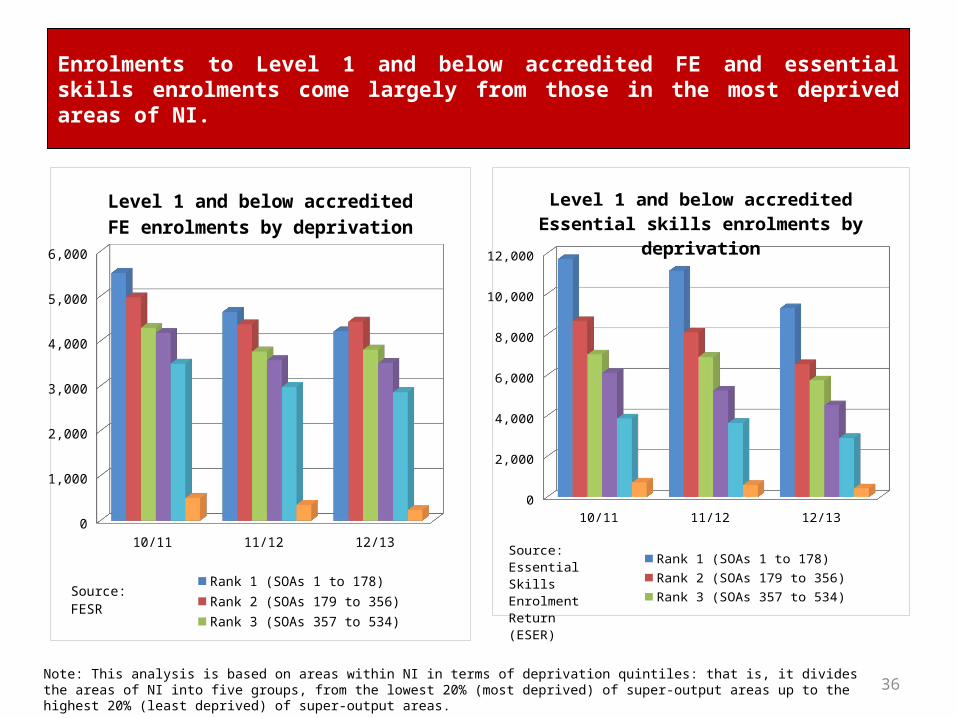

10/11 11/12 12/130

1,000

2,000

3,000

4,000

5,000

6,000

Level 1 and below accredited FE en-rolments by deprivation

Rank 1 (SOAs 1 to 178) Rank 2 (SOAs 179 to 356)Rank 3 (SOAs 357 to 534) Rank 4 (SOAs 535 to 712)Rank 5 (SOAs 713 to 890) Unknown Postcode

Source: FESR

10/11 11/12 12/130

2,000

4,000

6,000

8,000

10,000

12,000

Level 1 and below accredited Essential skills enrolments by deprivation

Rank 1 (SOAs 1 to 178) Rank 2 (SOAs 179 to 356)Rank 3 (SOAs 357 to 534) Rank 4 (SOAs 535 to 712)Rank 5 (SOAs 713 to 890) Unknown Postcode

Source: Essen-tial Skills En-rolment Return (ESER)

Enrolments to Level 1 and below accredited FE and essential skills enrolments come largely from those in the most deprived areas of NI.

Note: This analysis is based on areas within NI in terms of deprivation quintiles: that is, it divides the areas of NI into five groups, from the lowest 20% (most deprived) of super-output areas up to the highest 20% (least deprived) of super-output areas.

37

Northern Ireland’s Skills Profile and Education Statistics

• Widespread consensus on value of skills to individual, employers and economy.

• Positive correlation between skills and GDP per capita.

• Important driver for economic growth.

• Skills help people move into work, stay in work and progress in work.

• Strong association with wages – higher skilled individuals earn higher wages.

38

Skills are the most important offering that we have to attract inward investment and enable local companies to grow." Minister Farry (Hansard 27/2/2012)

“Skills are, without doubt, a critical factor in economic development ….” Minister Foster, (25/1/2010)

Skills Matter for the individual, for employers and for the economy

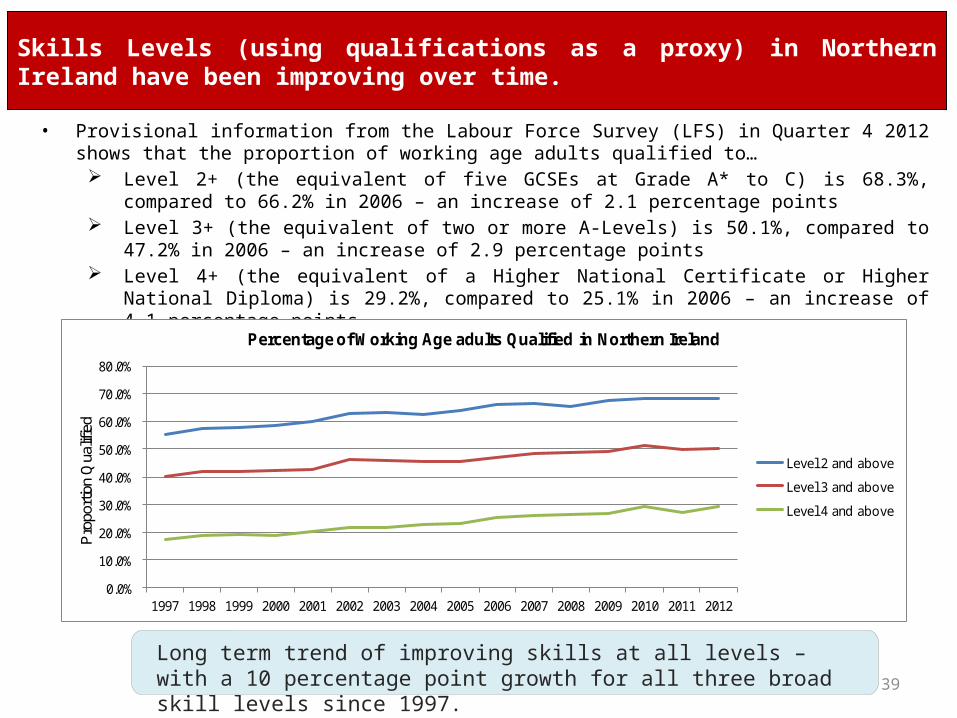

• Provisional information from the Labour Force Survey (LFS) in Quarter 4 2012 shows that the proportion of working age adults qualified to… Level 2+ (the equivalent of five GCSEs at Grade A* to C) is 68.3%, compared to 66.2% in 2006 – an increase

of 2.1 percentage points Level 3+ (the equivalent of two or more A-Levels) is 50.1%, compared to 47.2% in 2006 – an increase of 2.9

percentage points Level 4+ (the equivalent of a Higher National Certificate or Higher National Diploma) is 29.2%, compared

to 25.1% in 2006 – an increase of 4.1 percentage points

39

Skills Levels (using qualifications as a proxy) in Northern Ireland have been improving over time.

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Pro

port

ion

Qua

lifie

d

Percentage of Working Age adults Qualified in Northern Ireland

Level 2 and above

Level 3 and above

Level 4 and above

Long term trend of improving skills at all levels – with a 10 percentage point growth for all three broad skill levels since 1997.

40

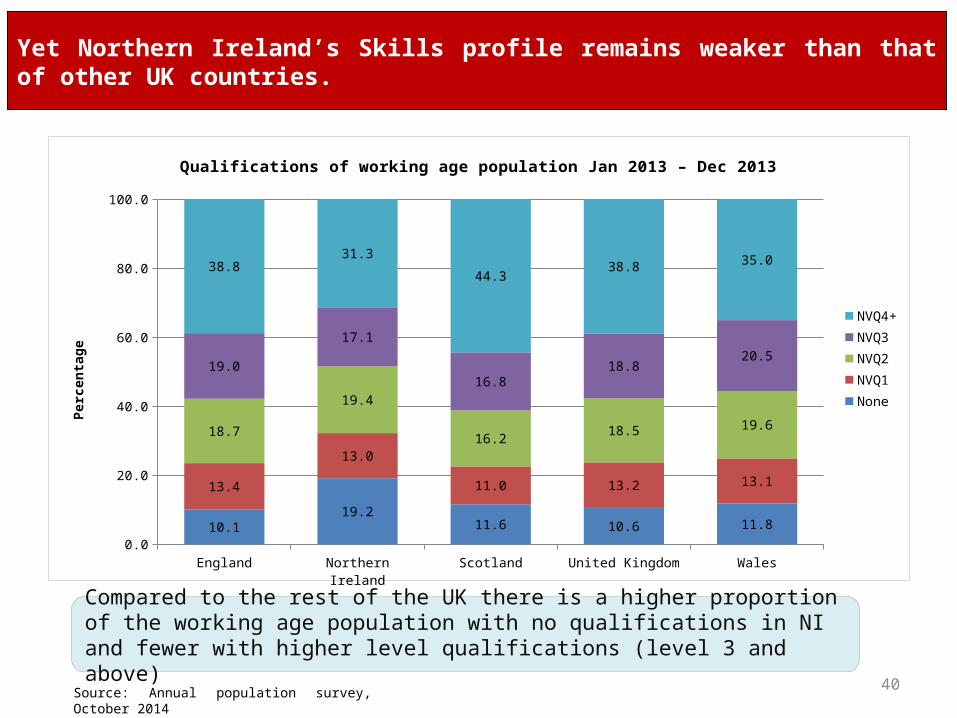

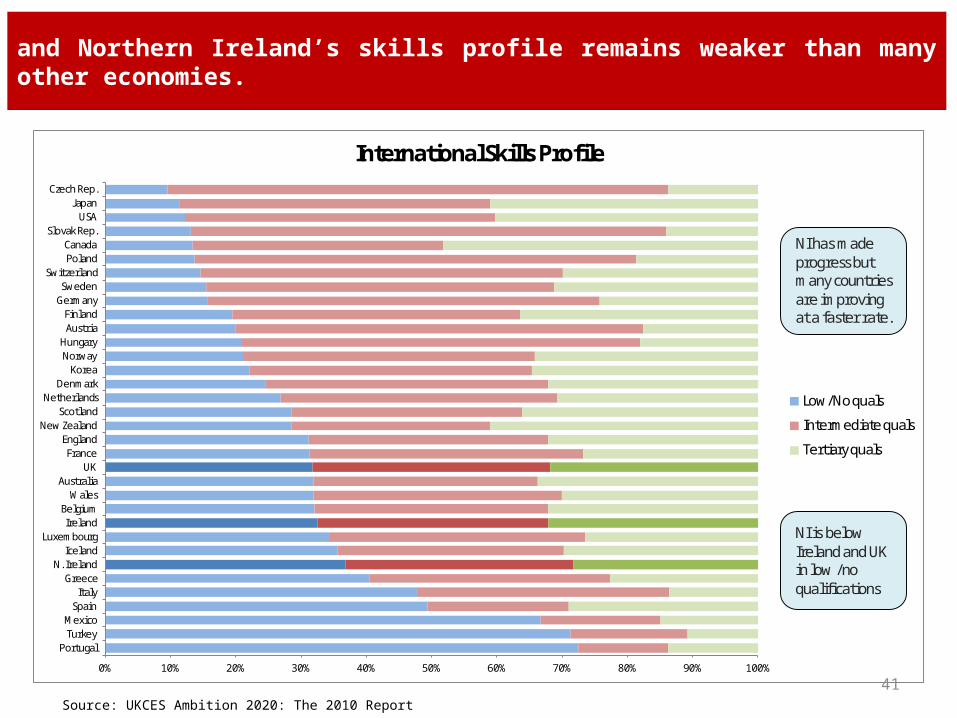

Yet Northern Ireland’s Skills profile remains weaker than that of other UK countries.

Compared to the rest of the UK there is a higher proportion of the working age population with no qualifications in NI and fewer with higher level qualifications (level 3 and above)

Source: Annual population survey, October 2014

England Northern Ireland Scotland United Kingdom Wales0.0

20.0

40.0

60.0

80.0

100.0

10.119.2

11.6 10.6 11.8

13.4

13.0

11.0 13.2 13.1

18.7

19.4

16.218.5 19.6

19.0

17.1

16.818.8

20.5

38.831.3

44.338.8 35.0

Qualifications of working age population Jan 2013 – Dec 2013

NVQ4+NVQ3NVQ2NVQ1None

Perc

enta

ge

and Northern Ireland’s skills profile remains weaker than many other economies.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

PortugalTurkeyMexico

SpainItaly

GreeceN. Ireland

IcelandLuxembourg

IrelandBelgium

WalesAustralia

UKFrance

EnglandNew Zealand

ScotlandNetherlands

DenmarkKorea

NorwayHungary

AustriaFinland

GermanySweden

SwitzerlandPolandCanada

Slovak Rep.USA

JapanCzech Rep.

International Skills Profile

Low/No quals

Intermediate quals

Tertiary quals

NI has made progress but many countries are improving at a faster rate.

NI is below Ireland and UK in low /no qualifications

41Source: UKCES Ambition 2020: The 2010 Report

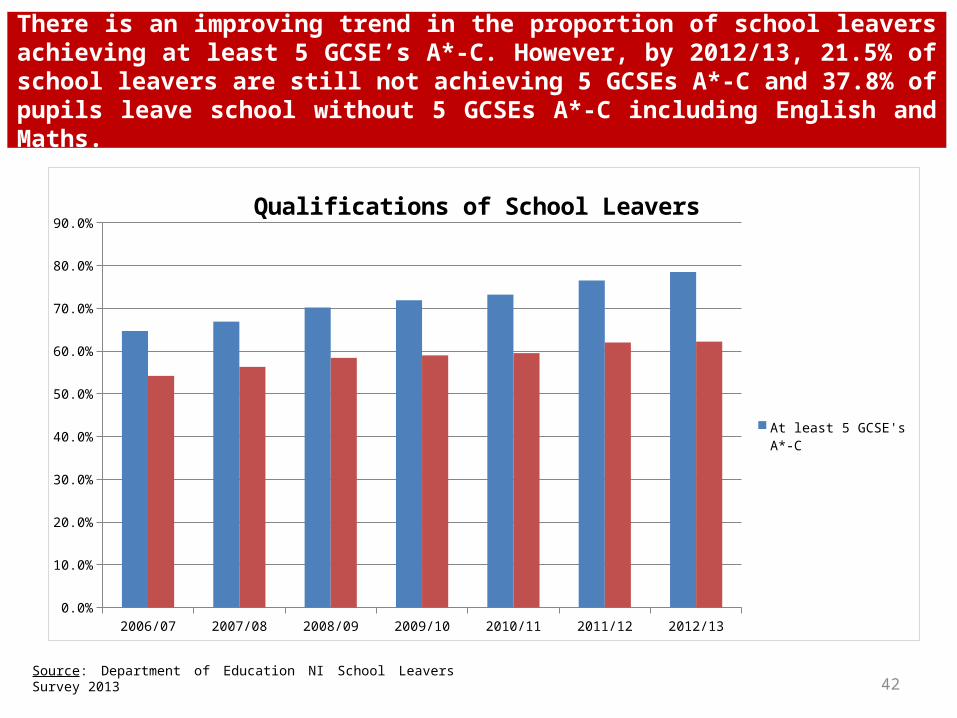

There is an improving trend in the proportion of school leavers achieving at least 5 GCSE’s A*-C. However, by 2012/13, 21.5% of school leavers are still not achieving 5 GCSEs A*-C and 37.8% of pupils leave school without 5 GCSEs A*-C including English and Maths.

Source: Department of Education NI School Leavers Survey 2013 42

2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/130.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%Qualifications of School Leavers

At least 5 GCSE's A*-C

At Least 5 GCSEs A*-C inc English and maths

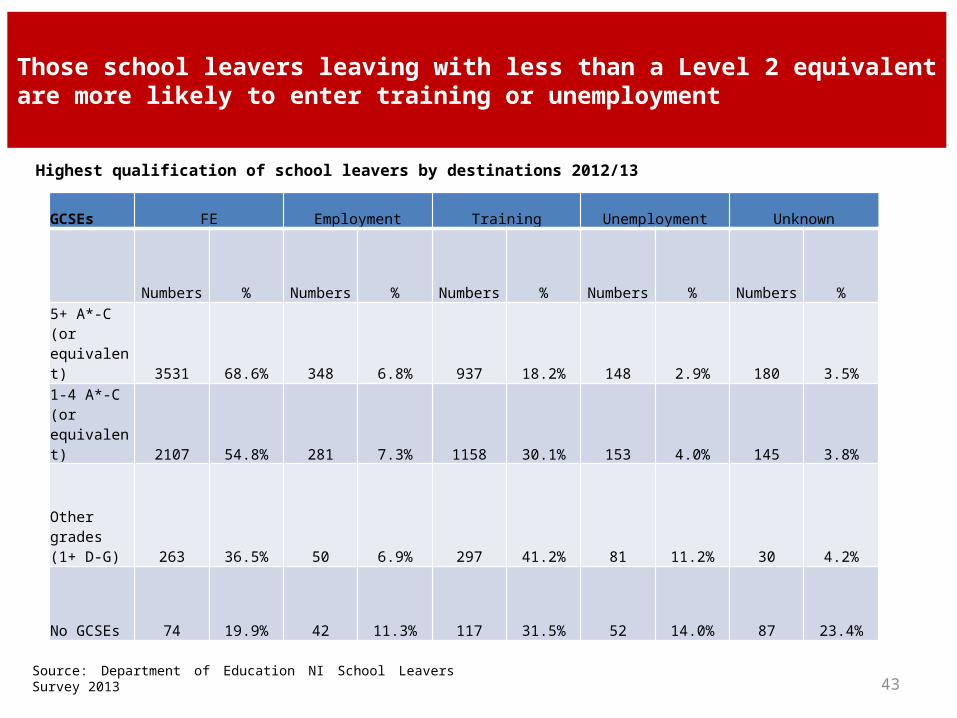

Those school leavers leaving with less than a Level 2 equivalent are more likely to enter training or unemployment

Source: Department of Education NI School Leavers Survey 2013 43

GCSEs FE Employment Training Unemployment Unknown

Numbers % Numbers % Numbers % Numbers % Numbers %

5+ A*-C (or equivalent) 3531 68.6% 348 6.8% 937 18.2% 148 2.9% 180 3.5%

1-4 A*-C (or equivalent) 2107 54.8% 281 7.3% 1158 30.1% 153 4.0% 145 3.8%

Other grades (1+ D-G) 263 36.5% 50 6.9% 297 41.2% 81 11.2% 30 4.2%

No GCSEs 74 19.9% 42 11.3% 117 31.5% 52 14.0% 87 23.4%

Highest qualification of school leavers by destinations 2012/13

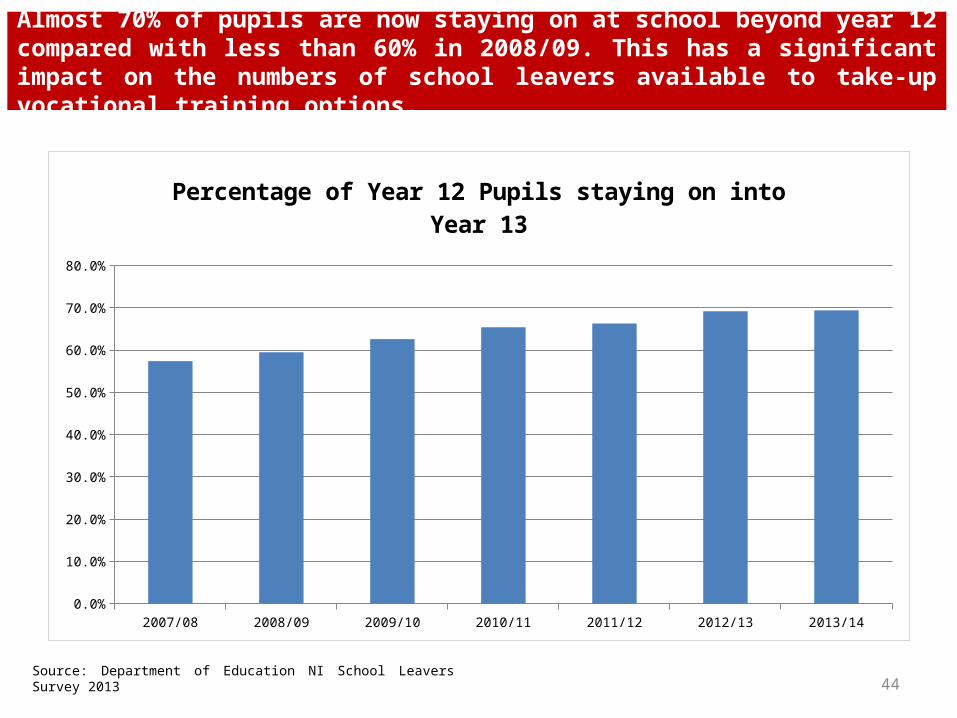

Almost 70% of pupils are now staying on at school beyond year 12 compared with less than 60% in 2008/09. This has a significant impact on the numbers of school leavers available to take-up vocational training options.

Source: Department of Education NI School Leavers Survey 2013 44

2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/140.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Percentage of Year 12 Pupils staying on into Year 13

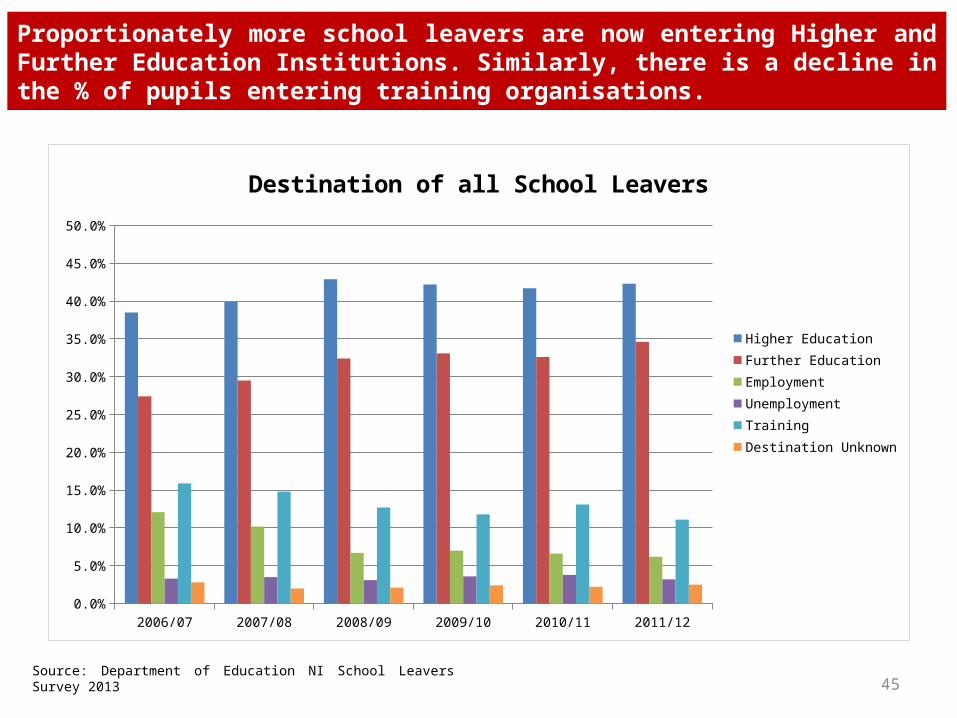

Proportionately more school leavers are now entering Higher and Further Education Institutions. Similarly, there is a decline in the % of pupils entering training organisations.

Source: Department of Education NI School Leavers Survey 2013 45

2006/07 2007/08 2008/09 2009/10 2010/11 2011/120.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

Destination of all School Leavers

Higher EducationFurther EducationEmploymentUnemploymentTrainingDestination Unknown

Total numbers achieving level 2 and Level 3

46

2007/08 2008/09 2009/10 2010/11 2011/12 2012/130

1000

2000

3000

4000

5000

6000

Level 2 and Level 3 Qualifications Achieved on TfS, PLA and AppsNI

Total level 2Total level 3

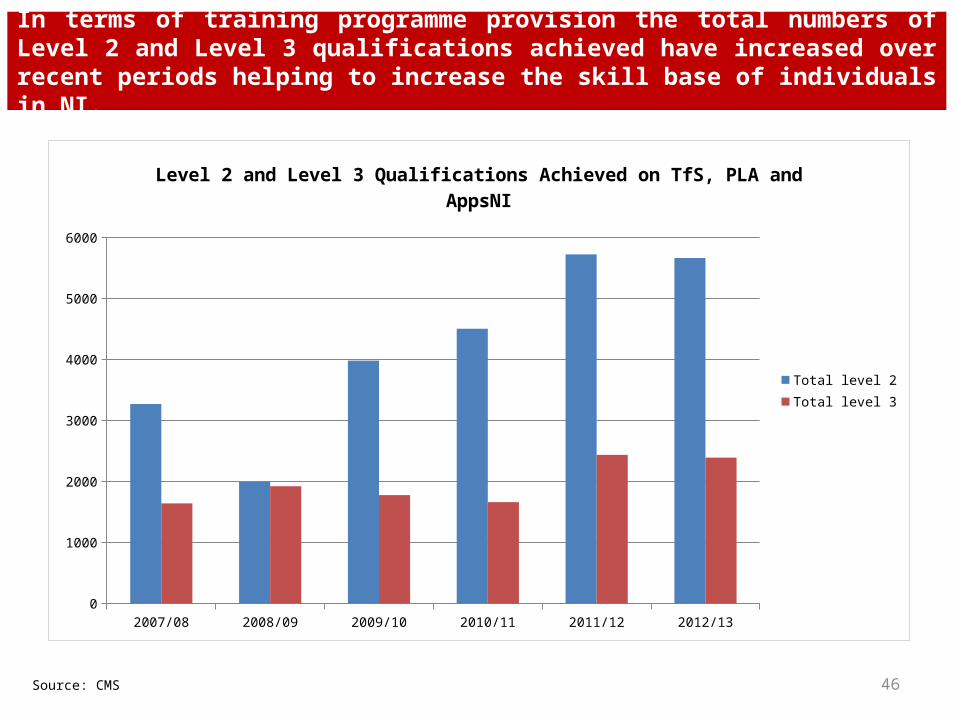

In terms of training programme provision the total numbers of Level 2 and Level 3 qualifications achieved have increased over recent periods helping to increase the skill base of individuals in NI.

Source: CMS

Source: OECD Survey of Adult Skills 2012 (PIAAC)

Leve

l 1

Leve

l 2

Leve

l 3

Leve

l 4 a

nd 5

Leve

l 1

Leve

l 2

Leve

l 3

Leve

l 4 a

nd 5

Leve

l 1

Leve

l 2

Leve

l 3

Leve

l 4 a

nd 5

16-29 30-49 50-65

-30%

-25%

-20%

-15%

-10%

-5%

0%

-0.032-0.051-0.096-0.068-0.003-0.047-0.094-0.088-0.096-0.136-0.215-0.243

Chart Title

Uppe

r sec

onda

ry

Post

-sec

onda

ry, n

on-te

rtiar

y

Terti

ary

Uppe

r sec

onda

ry

Post

-sec

onda

ry, n

on-te

rtiar

y

Terti

ary

Uppe

r sec

onda

ry

Post

-sec

onda

ry, n

on-te

rtiar

y

Terti

ary

16-29 30-49 50-65

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%-0.006

-0.028 -0.033-0.039 -0.039 -0.086 -0.053 -0.061 -0.134Chart Title

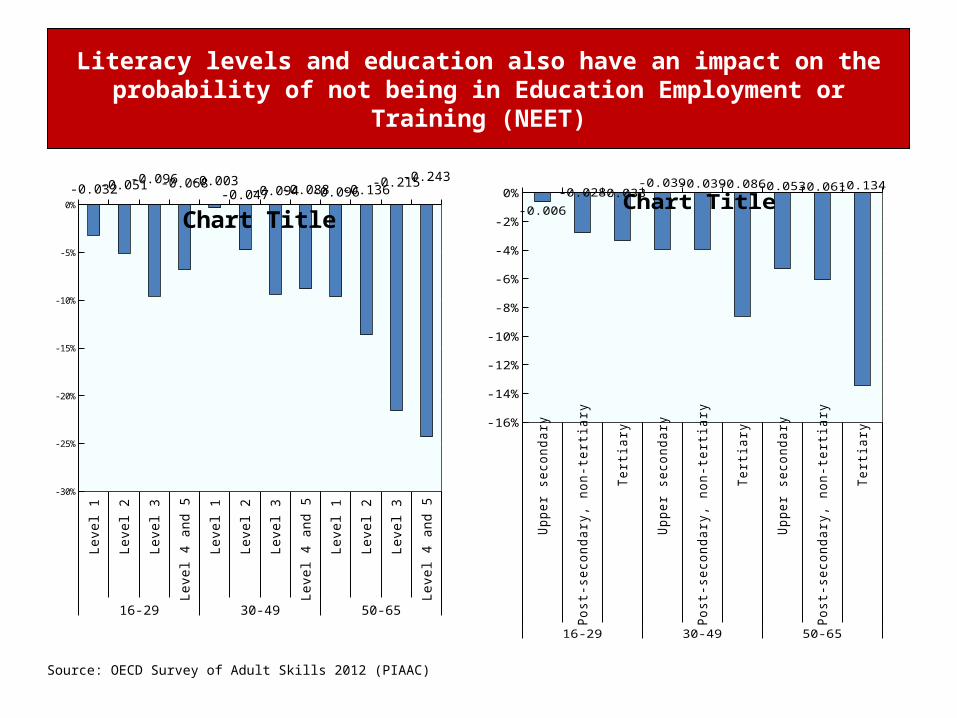

Literacy levels and education also have an impact on the probability of not being in Education Employment or Training (NEET)

Source: OECD Survey of Adult Skills 2012 (PIAAC)

Leve

l 1

Leve

l 2

Leve

l 3

Leve

l 4 a

nd 5

Leve

l 1

Leve

l 2

Leve

l 3

Leve

l 4 a

nd 5

Leve

l 1

Leve

l 2

Leve

l 3

Leve

l 4 a

nd 5

16-29 30-49 50-65

-5%

0%

5%

10%

15%

20%

25%

30%

-0.0132283

0.0214568

0.0504373

0.0808664000000002

0.0370062000000003

0.0799176000000009

0.1416734

0.2205027

0.03223380000000050.0544923000000007

0.0861287

0.242617200000001

Uppe

r sec

onda

ry

Post

-sec

onda

ry, n

on-te

rtiar

y

Terti

ary

Uppe

r sec

onda

ry

Post

-sec

onda

ry, n

on-te

rtiar

y

Terti

ary

Uppe

r sec

onda

ry

Post

-sec

onda

ry, n

on-te

rtiar

y

Terti

ary

16-29 30-49 50-65

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

0.030

-0.017

0.130

-0.007-0.045

0.105

0.006

0.029

0.085

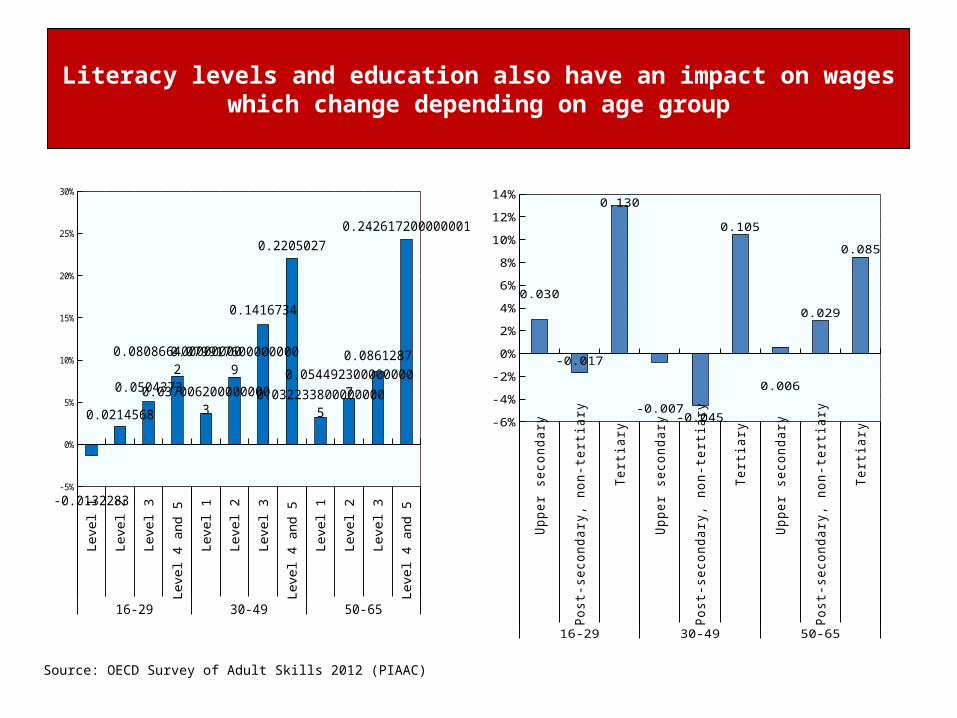

Literacy levels and education also have an impact on wages which change depending on age group

-20

-15

-10

-5

0

5

10

15

HK

SIN

GJA

PKO

RRO

ISW

IG

ER FRA UK NI

US

SPA

LUX

SWE

GRE CH

IM

EX

NI hasSimilar performance as OECD average

Source: OECD PISA Study 2012 Note: Measures literacy of 15 year olds

-20-15-10

-505

101520

SIN

G HK

KOR

JAP

SWI

GER RO

IFR

A UK

LUX NI

SPA US

SWE

GRE CH

IM

EX

-20

-15

-10

-5

0

5

10

15

HK

SIN

GJA

PKO

RRO

ISW

IG

ER FRA UK NI

US

SPA

LUX

SWE

GRE CH

IM

EX

OECD Comparison of Reading skills

OECD Comparison of Maths skills

OECD Comparison of Science skills

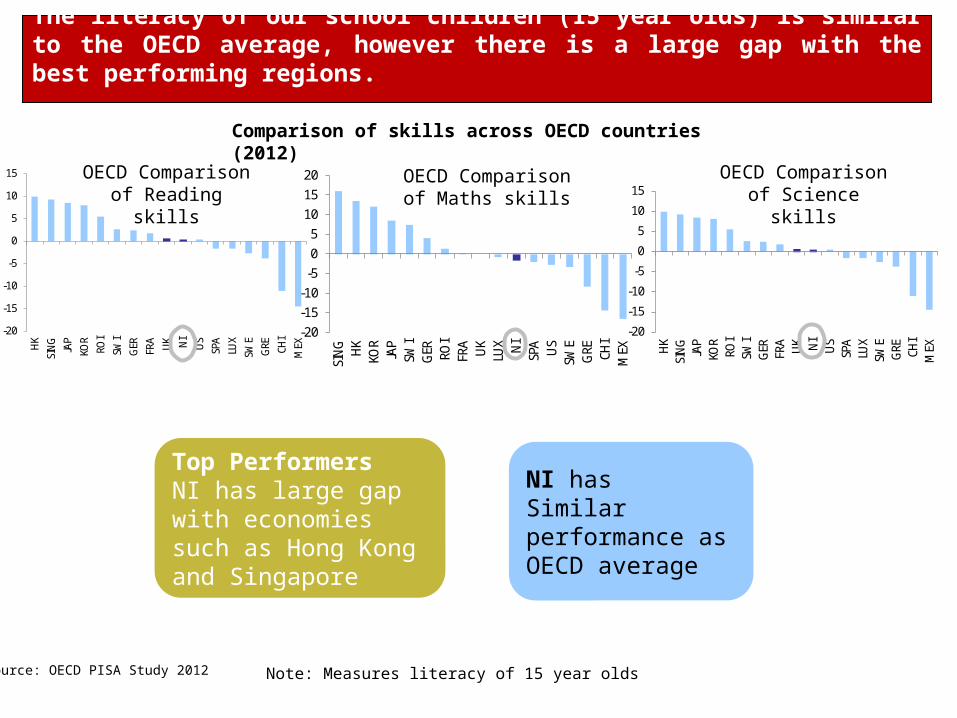

Top PerformersNI has large gap with economies such as Hong Kong and Singapore

The literacy of our school children (15 year olds) is similar to the OECD average, however there is a large gap with the best performing regions.

Comparison of skills across OECD countries (2012)

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

Proportion of 25-29 year olds with very low skills: less than upper secondary education and numeracy at level 1 or be-

low

%

Source: OECD Survey of Adult Skills 2012 (PIAAC)

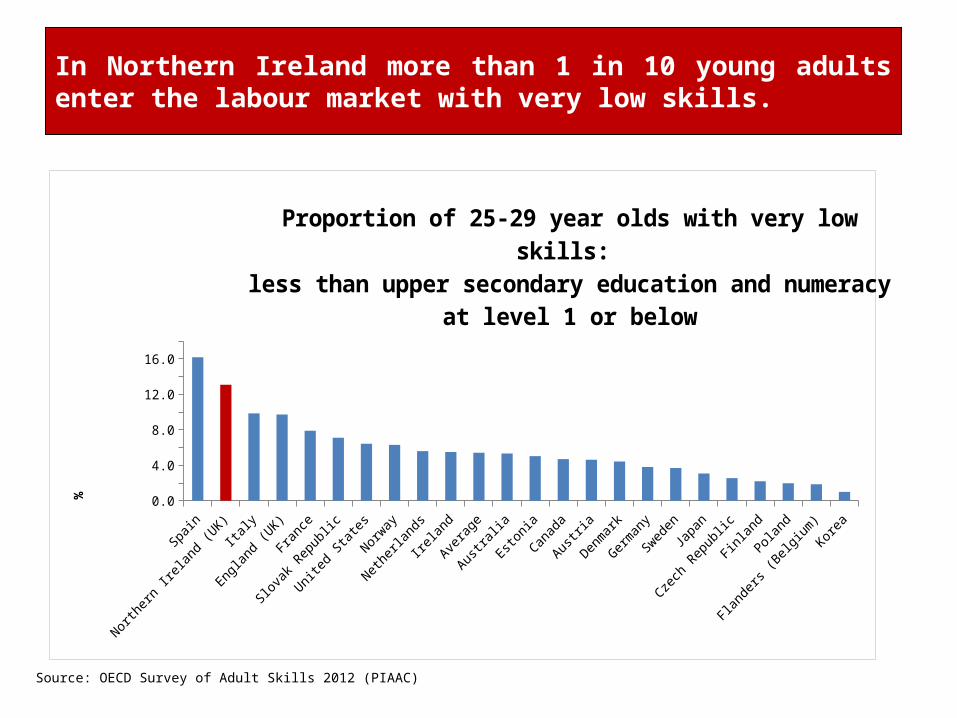

In Northern Ireland more than 1 in 10 young adults enter the labour market with very low skills.

Aged 16-18 Aged 19-24 Aged 25-34 Aged 35-44 Aged 45-54 Aged 55-65 Aged 16-65240

245

250

255

260

265

270

275

280

285

290

263

277 278

274

262

255

269

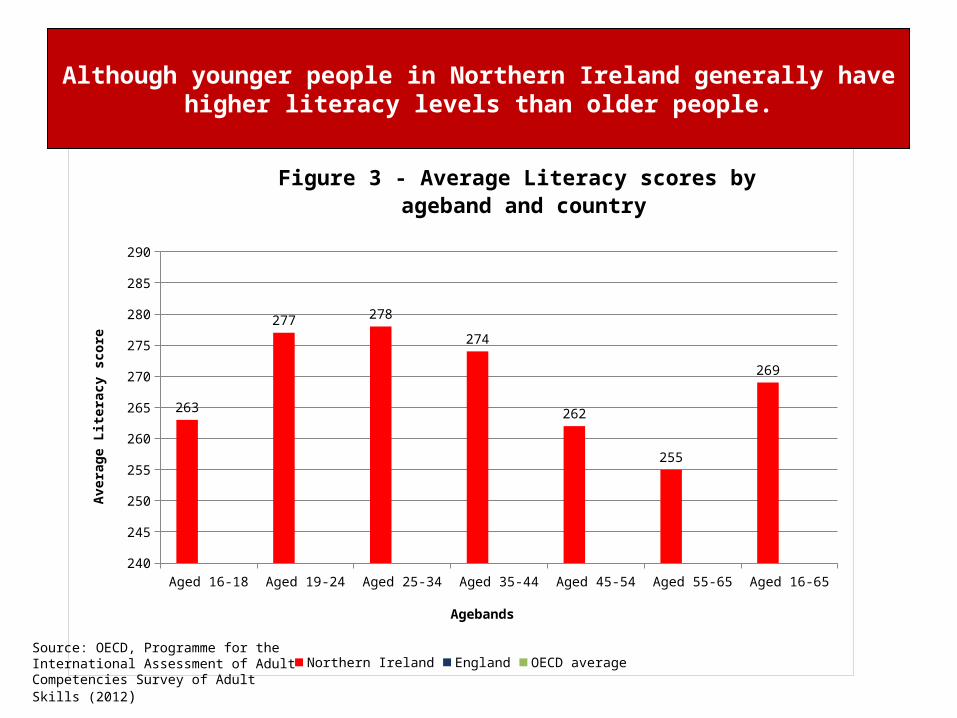

Figure 3 - Average Literacy scores by ageband and country

Northern Ireland England OECD average

Agebands

Aver

age

Liter

acy

scor

eAlthough younger people in Northern Ireland generally have higher literacy levels

than older people.

Source: OECD, Programme for the International Assessment of Adult Competencies Survey of Adult Skills (2012)

Aged 16-18 Aged 19-24 Aged 25-34 Aged 35-44 Aged 45-54 Aged 55-65 Aged 16-65240

245

250

255

260

265

270

275

280

285

290

263

277 278

274

262

255

269

259

269

280 279

271

265

273274

281

284

278

267

255

273

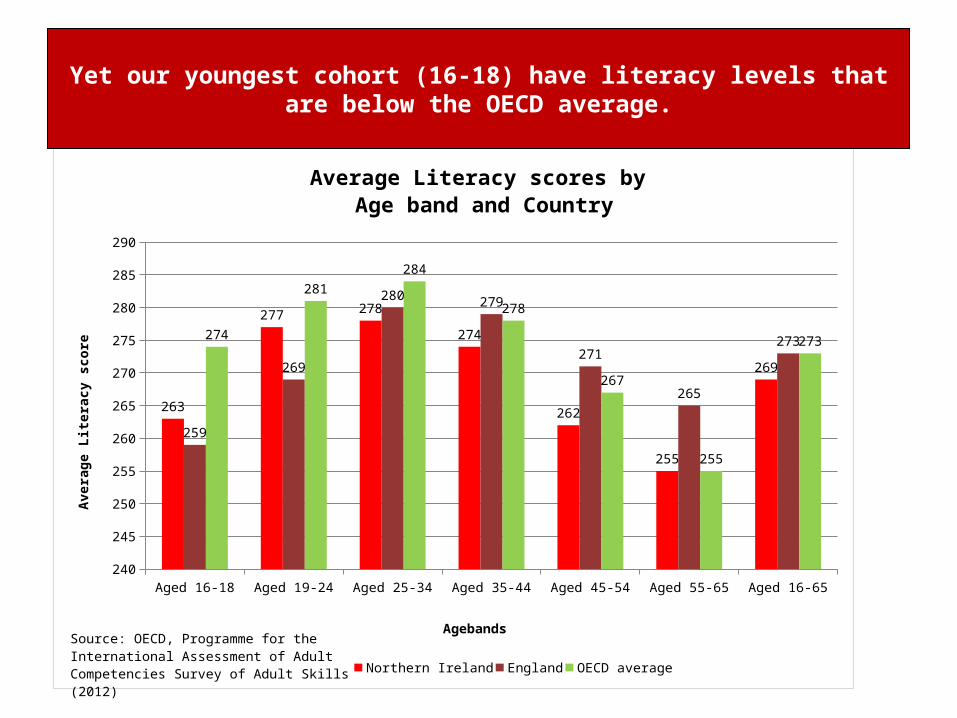

Average Literacy scores by Age band and Country

Northern Ireland England OECD average

Agebands

Aver

age

Liter

acy

scor

e

Source: OECD, Programme for the International Assessment of Adult Competencies Survey of Adult Skills (2012)

Yet our youngest cohort (16-18) have literacy levels that are below the OECD average.

Skills will continue to be an important driver of growth here and certain skills will be particularly important

• The ‘Forecasting Future Skills Needs in NI’ report, which underpins the Northern Ireland Skills Strategy, Success through Skills – Transforming Futures, identified the likely 2020 skills profile that employers will need if productivity is to improve.

• Key areas identified are:

– need for Higher Level Skills;

– need for appropriate Up-skilling of the workforce;

– developing literacy and numeracy skills

– need for improved management and leadership;

– addressing subject imbalances;

– need for qualifications in STEM; and

– need to attract skilled labour

53

54

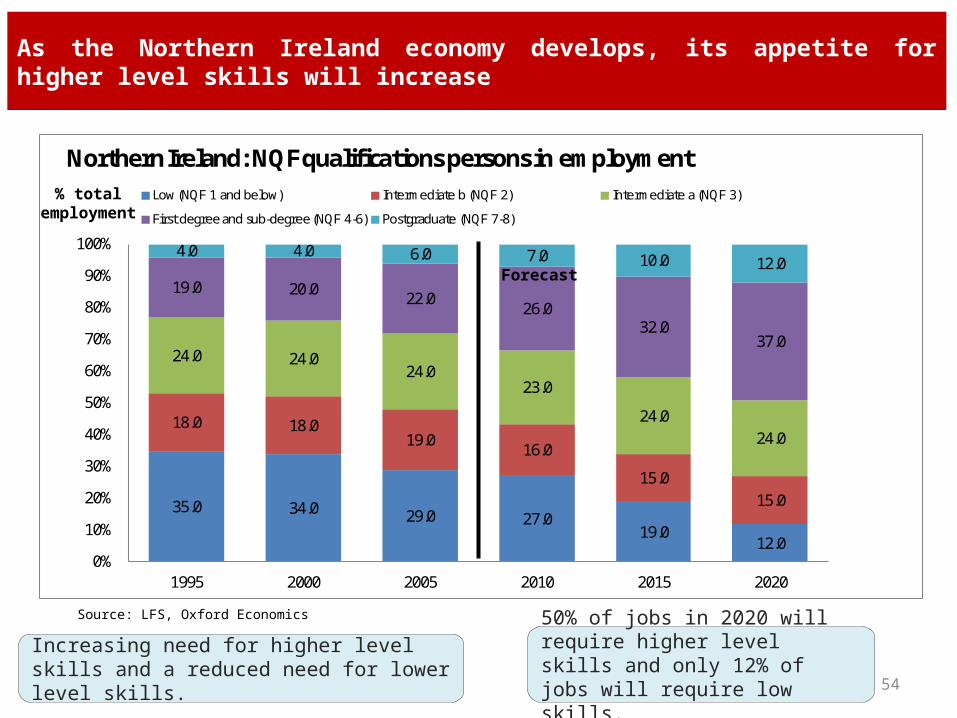

Increasing need for higher level skills and a reduced need for lower level skills.

50% of jobs in 2020 will require higher level skills and only 12% of jobs will require low skills.

As the Northern Ireland economy develops, its appetite for higher level skills will increase

35.0 34.0 29.0 27.019.0

12.0

18.0 18.019.0

16.0

15.015.0

24.0 24.024.0

23.0

24.024.0

19.0 20.0 22.026.0

32.037.0

4.0 4.0 6.0 7.0 10.0 12.0

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1995 2000 2005 2010 2015 2020

Northern Ireland: NQF qualifications persons in employmentLow (NQF 1 and below) Intermediate b (NQF 2) Intermediate a (NQF 3)

First degree and sub-degree (NQF 4-6) Postgraduate (NQF 7-8)

Source: LFS, Oxford Economics

% total employment

Forecast

55

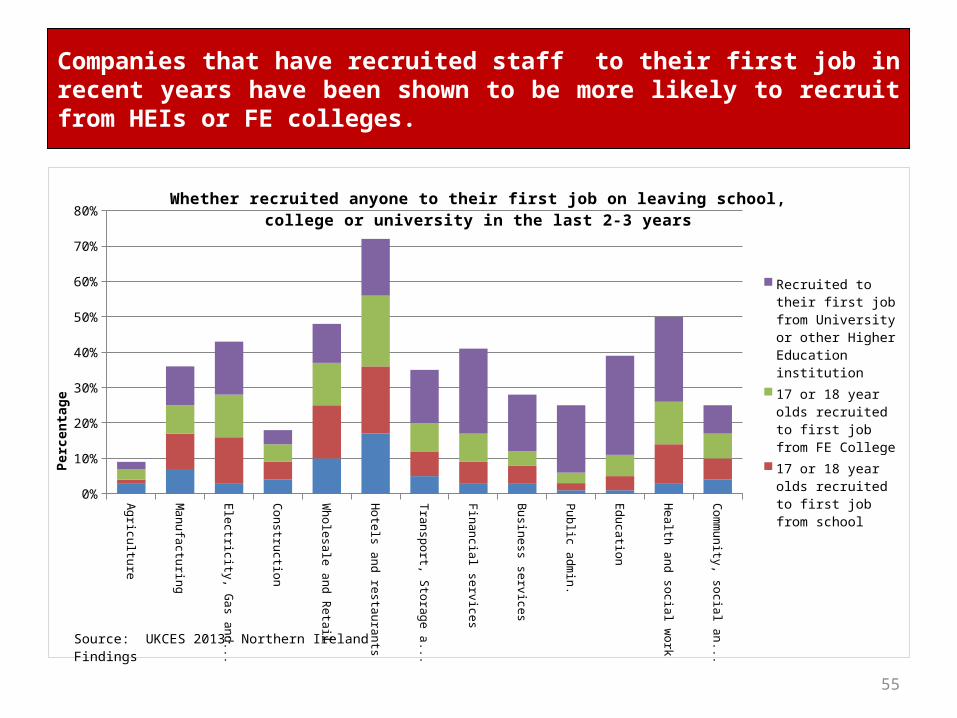

Companies that have recruited staff to their first job in recent years have been shown to be more likely to recruit from HEIs or FE colleges.

Agriculture

Manufacturing

Electricity, Gas and W

ater

Construction

Wholesale and Retail

Hotels and restaurants

Transport, Storage and Comm

s

Financial services

Business services

Public admin.

Education

Health and social work

Comm

unity, social and other ac...

0%

10%

20%

30%

40%

50%

60%

70%

80%Whether recruited anyone to their first job on leaving school, college or university in the last 2-3

years

Recruited to their first job from University or other Higher Education institution

17 or 18 year olds re-cruited to first job from FE College

17 or 18 year olds re-cruited to first job from school

16 year olds recruited to first job from school

Perc

enta

ge

Source: UKCES 2013: Northern Ireland Findings

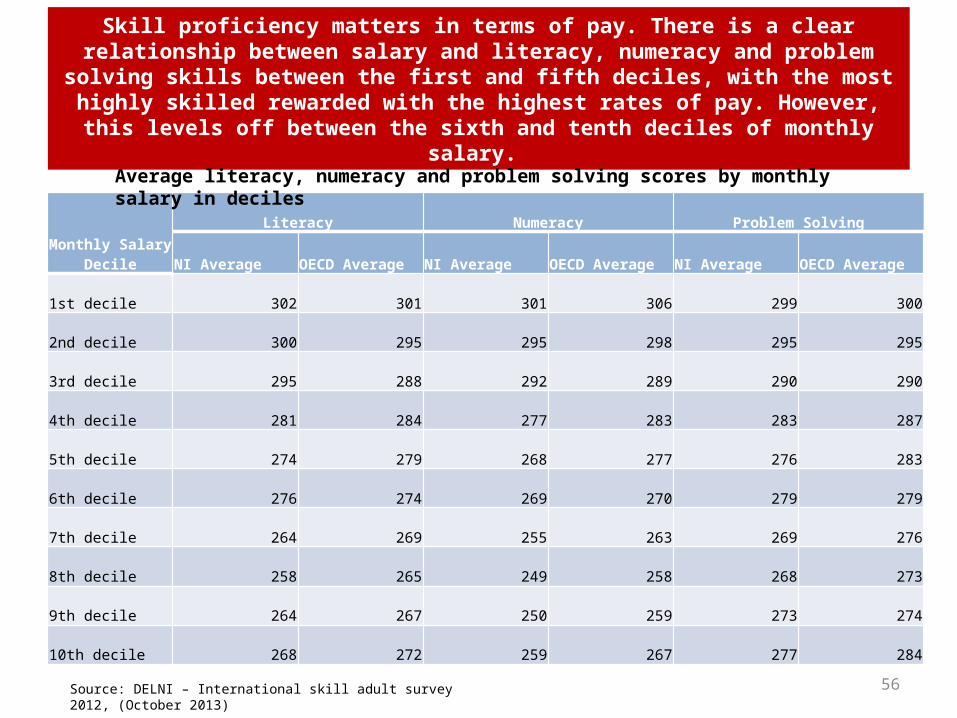

Monthly Salary Decile

Literacy Numeracy Problem Solving

NI Average OECD Average NI Average OECD Average NI Average OECD Average

1st decile 302 301 301 306 299 300

2nd decile 300 295 295 298 295 295

3rd decile 295 288 292 289 290 290

4th decile 281 284 277 283 283 287

5th decile 274 279 268 277 276 283

6th decile 276 274 269 270 279 279

7th decile 264 269 255 263 269 276

8th decile 258 265 249 258 268 273

9th decile 264 267 250 259 273 274

10th decile 268 272 259 267 277 284

56

Skill proficiency matters in terms of pay. There is a clear relationship between salary and literacy, numeracy and problem solving skills between the first and fifth deciles, with the most highly skilled rewarded with the highest rates of pay. However, this levels off between the sixth

and tenth deciles of monthly salary.

Source: DELNI – International skill adult survey 2012, (October 2013)

Average literacy, numeracy and problem solving scores by monthly salary in deciles

While recognising the future skill needs there is also a need to be aware of current skills gaps and shortages.

• NI’s Employer Skills Survey (2013) found concentrations of employers reporting difficulties recruiting people with the skills they need (skill shortages) in skilled trade occupations and professional occupations.

• Skills deficiencies have been reported across several sectors in NI e.g. Software development/testing and engineering sector.

• Skill needs have been well articulated by business to the Minister.

• This has led to the establishment of three sectoral Working Groups – ICT, Advanced Manufacturing and Engineering Services and Food and Drink.

• Action Plans have been developed to address key issues.

57

Further evidence of skills deficiencies

58

• Issues relate to improving skills provision, sector attractiveness and stakeholder communication and engagement.

• At sectoral level – skill shortages and gaps exist in hotel & catering, business services and retail sectors.

• Evidence of skill gaps amongst existing employees – particularly in elementary and sales / customer service occupations.

• Similar evidence reported by NI Skills Adviser who previously (2011) found skill needs in business services, retail, financial services and manufacturing.

In response to current and future skill needs, a number of Northern Ireland Priority Skill areas have been identified.

• Northern Ireland’s Priority Skill Areas:

Business services (specifically ICT).

Financial services.

Retail.

Manufacturing (including food and drink/agri-food, advanced

manufacturing and advanced engineering).

Hotels and Catering (in support of tourism).

Life and health sciences.

Creative Industries.

59

Northern Ireland’s Skills Profile – Key Messages

• Skills are fundamental to employment, productivity and economic growth.

• Domestically Northern Ireland is making progress in terms of upskilling the workforce.

• However, Northern Ireland still has much ground to catch up on the world leaders.

• A significant percentage of our workforce still have no or low qualifications.

• There is a need to increase higher level skills (qualifications level 4 and above) with 50% of jobs in 2020 likely to require skills at that level including higher professional and technical skills.

• There is also a need for additional and improved technical skills across a range of sectors.

• Northern Ireland requires more individuals achieving STEM qualifications.

• Vocational Training will have a critical role to play in addressing these needs and developing the skills required both now and in the future.

60

61

Evidence on Employer Engagement with Skills

62

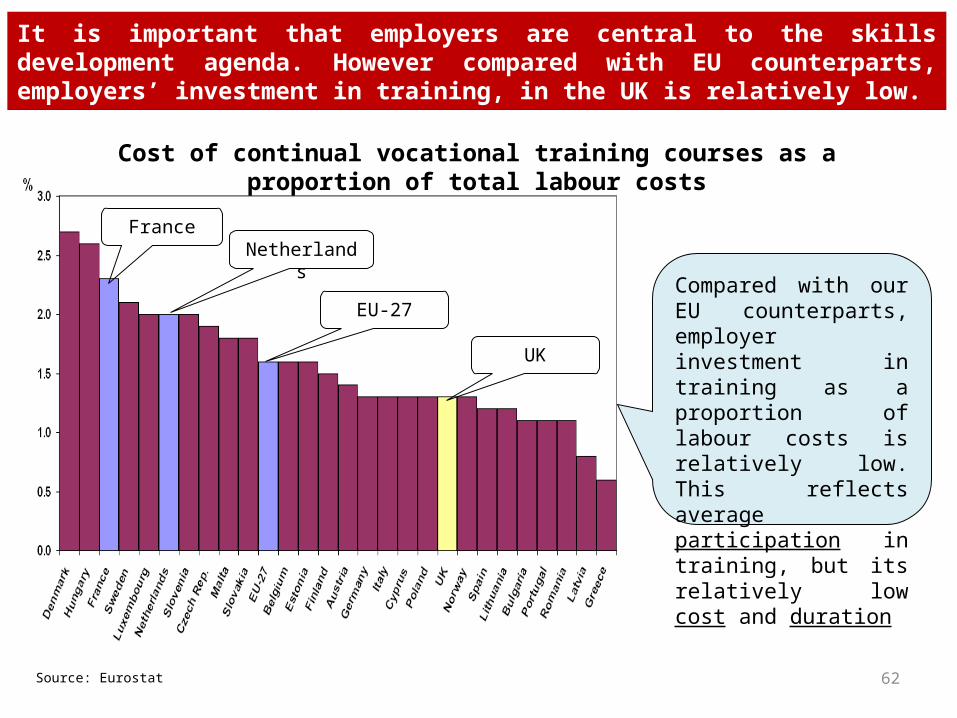

UK

EU-27

NetherlandsFrance

Cost of continual vocational training courses as a proportion of total labour costs

Compared with our EU counterparts, employer investment in training as a proportion of labour costs is relatively low. This reflects average participation in training, but its relatively low cost and duration

It is important that employers are central to the skills development agenda. However compared with EU counterparts, employers’ investment in training, in the UK is relatively low.

Source: Eurostat

63

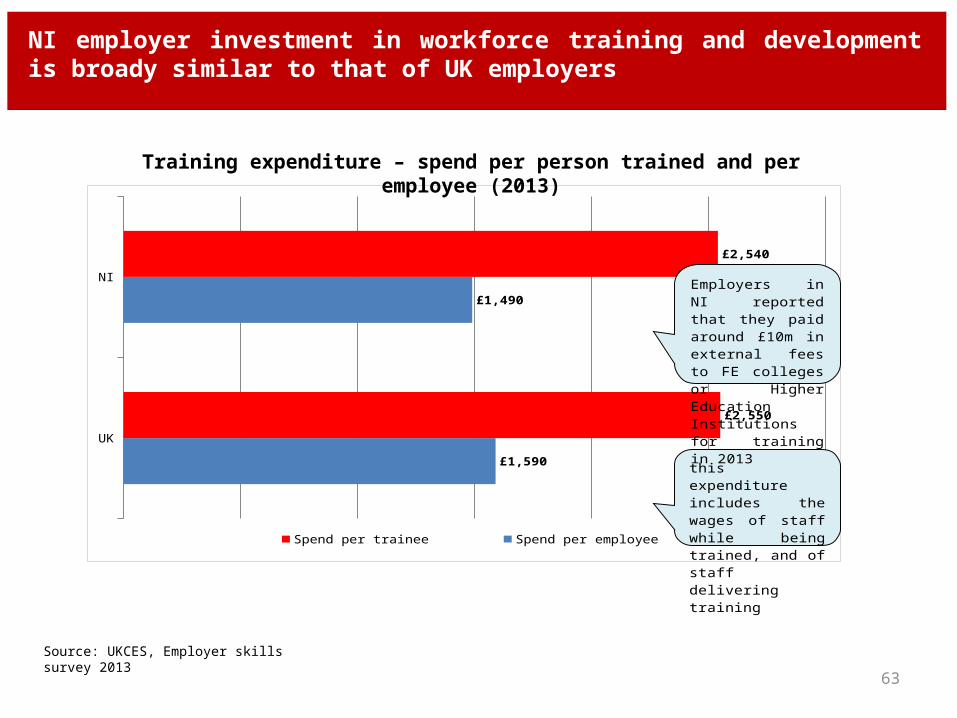

UK

NI

£1,590

£1,490

£2,550

£2,540

Spend per trainee Spend per employee

this expenditure in-cludes the wages of staff while being trained, and of staff delivering training

Employers in NI re-ported that they paid around £10m in ex-ternal fees to FE col-leges or Higher Educa-tion Institutions for training in 2013

Training expenditure – spend per person trained and per employee (2013)

NI employer investment in workforce training and development is broady similar to that of UK employers

Source: UKCES, Employer skills survey 2013

Northern Ireland Employer Skills Survey 2013

• 77% of NI firms provided training for their staff in previous 12 months compared with a UK average of 86%.

• Employers in NI are also considerably less likely to have increased training-related activities more specifically (58% in contrast with the UK average of 68%.

• Similarly, in terms of training per employee NI lags other UK countries with 3.7 days training per employee against the UK average of 4.2 days per employee.

• Incidence of training increased between 2011 and 2013 but at a slower rate than other UK countries.

64

Those trained in Northern Ireland also receive the fewest days training per annum in the UK.

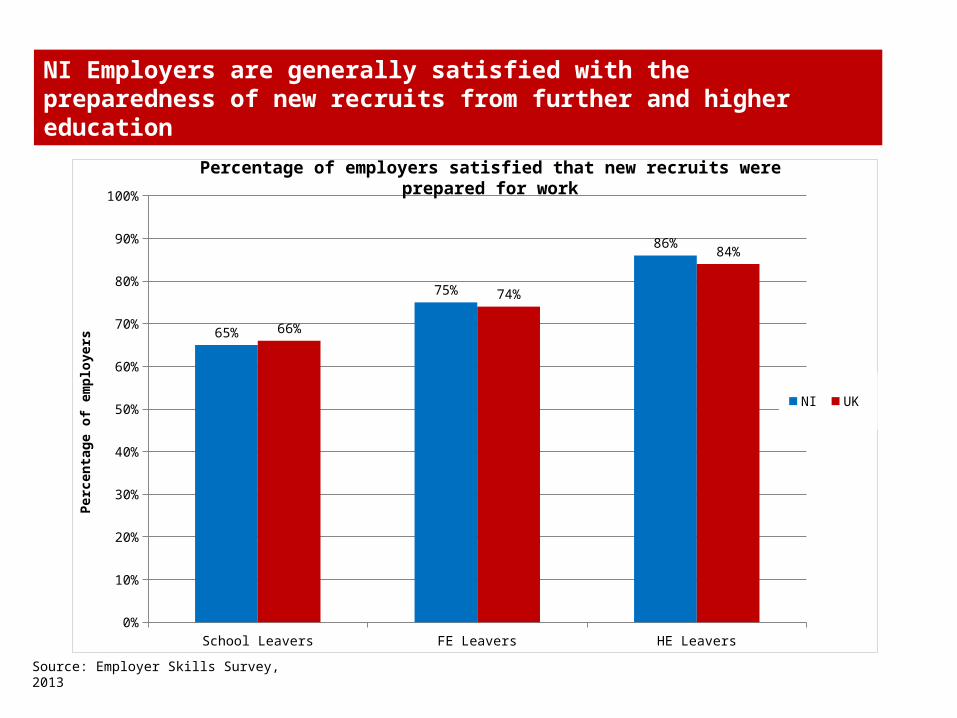

NI Employers are generally satisfied with the preparedness of new recruits from further and higher education

School Leavers FE Leavers HE Leavers0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

65%

75%

86%

66%

74%

84%

NI UK

Perc

enta

ge o

f em

ploy

ers

Source: Employer Skills Survey, 2013

Percentage of employers satisfied that new recruits were prepared for work

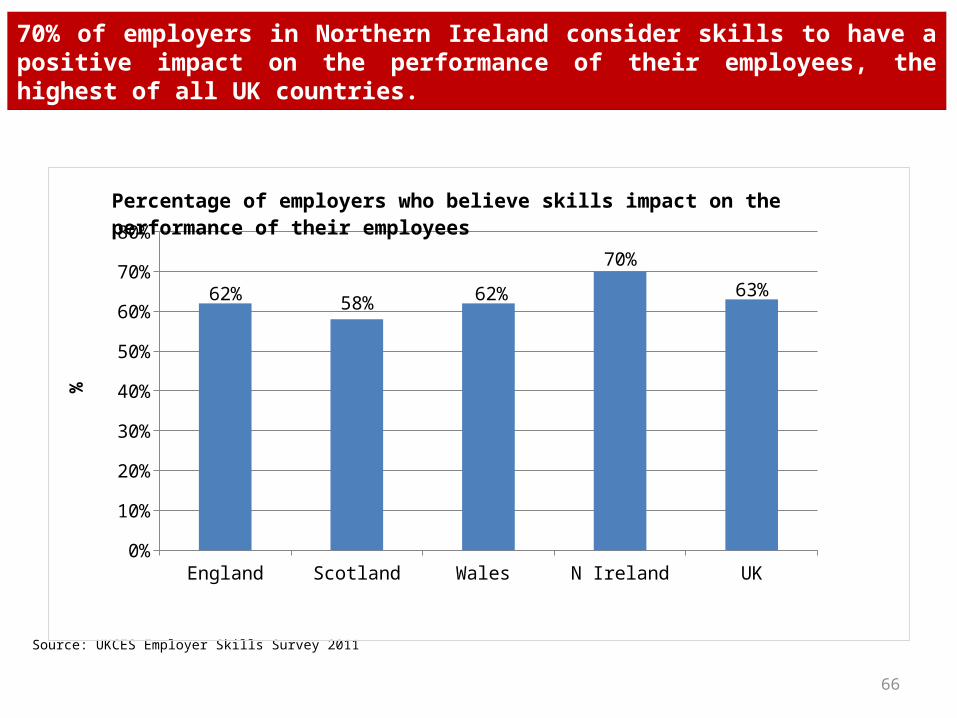

70% of employers in Northern Ireland consider skills to have a positive impact on the performance of their employees, the highest of all UK countries.

Source: UKCES Employer Skills Survey 2011

66

England Scotland Wales N Ireland UK0%

10%

20%

30%

40%

50%

60%

70%

80%

62% 58% 62%

70%

63%

%

Percentage of employers who believe skills impact on the performance of their employees

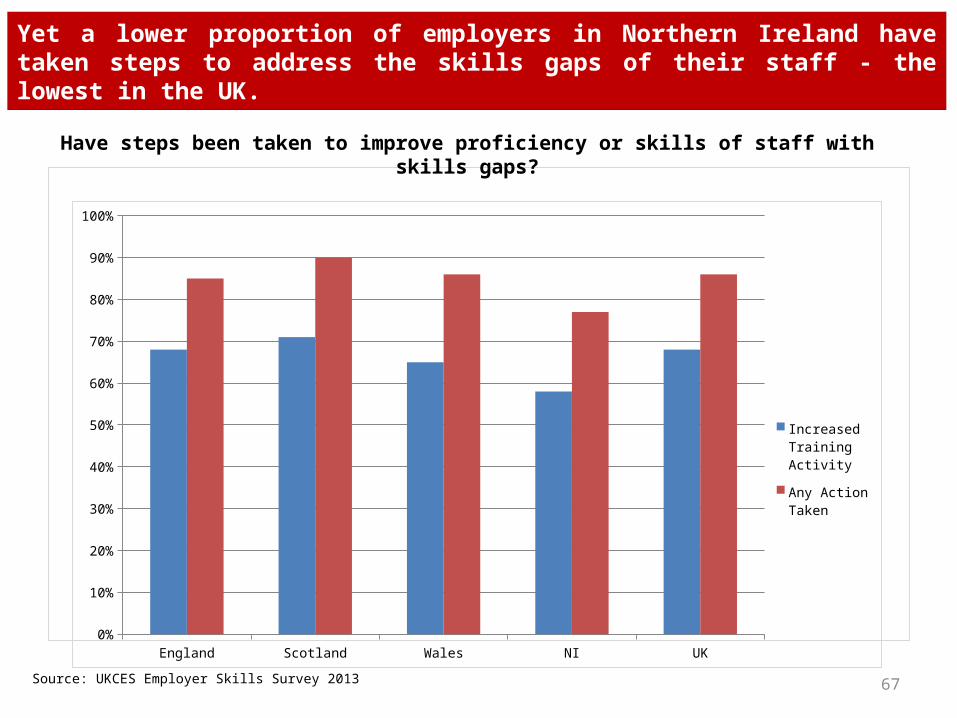

Yet a lower proportion of employers in Northern Ireland have taken steps to address the skills gaps of their staff - the lowest in the UK.

Source: UKCES Employer Skills Survey 2013 67

Have steps been taken to improve proficiency or skills of staff with skills gaps?

England Scotland Wales NI UK0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Increased Train-ing Activity

Any Action Taken

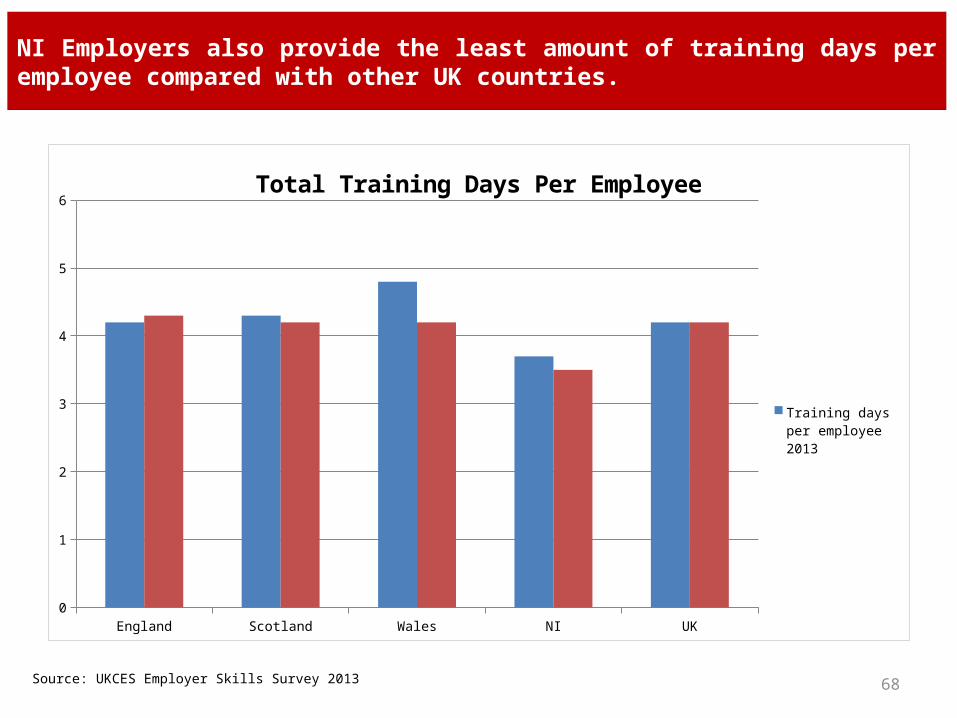

NI Employers also provide the least amount of training days per employee compared with other UK countries.

Source: UKCES Employer Skills Survey 2013 68

England Scotland Wales NI UK0

1

2

3

4

5

6Total Training Days Per Employee

Training days per employee 2013

Training days per employee 2011

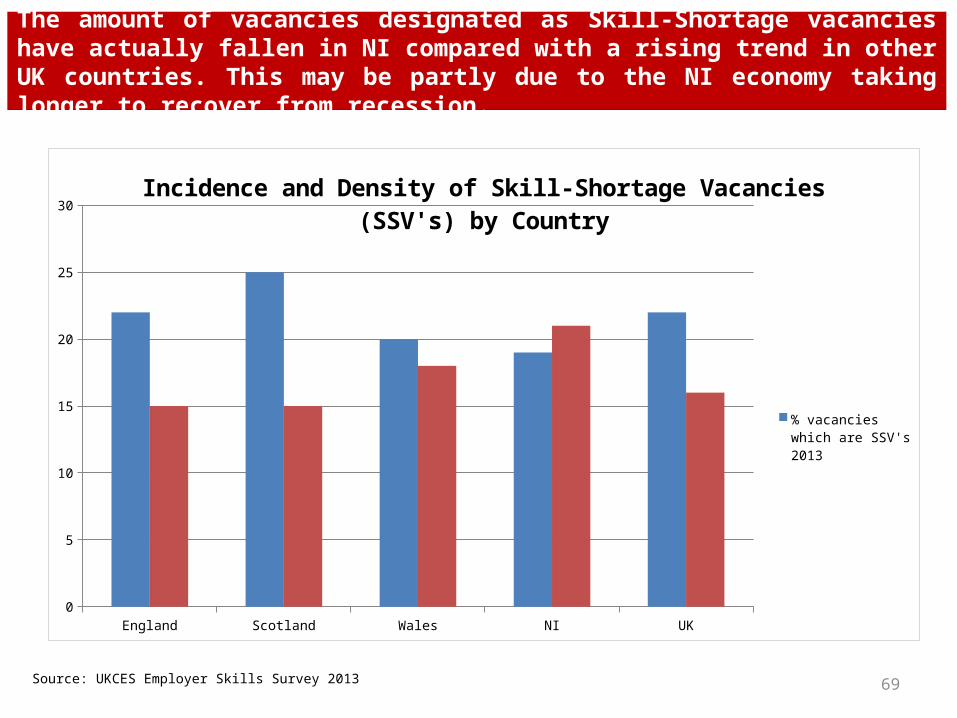

The amount of vacancies designated as Skill-Shortage vacancies have actually fallen in NI compared with a rising trend in other UK countries. This may be partly due to the NI economy taking longer to recover from recession.

Source: UKCES Employer Skills Survey 2013 69

England Scotland Wales NI UK0

5

10

15

20

25

30

Incidence and Density of Skill-Shortage Vacancies (SSV's) by Country

% vacancies which are SSV's 2013

% vacancies which are SSV's 2011

70Source: NI Employer Skills Survey 2013

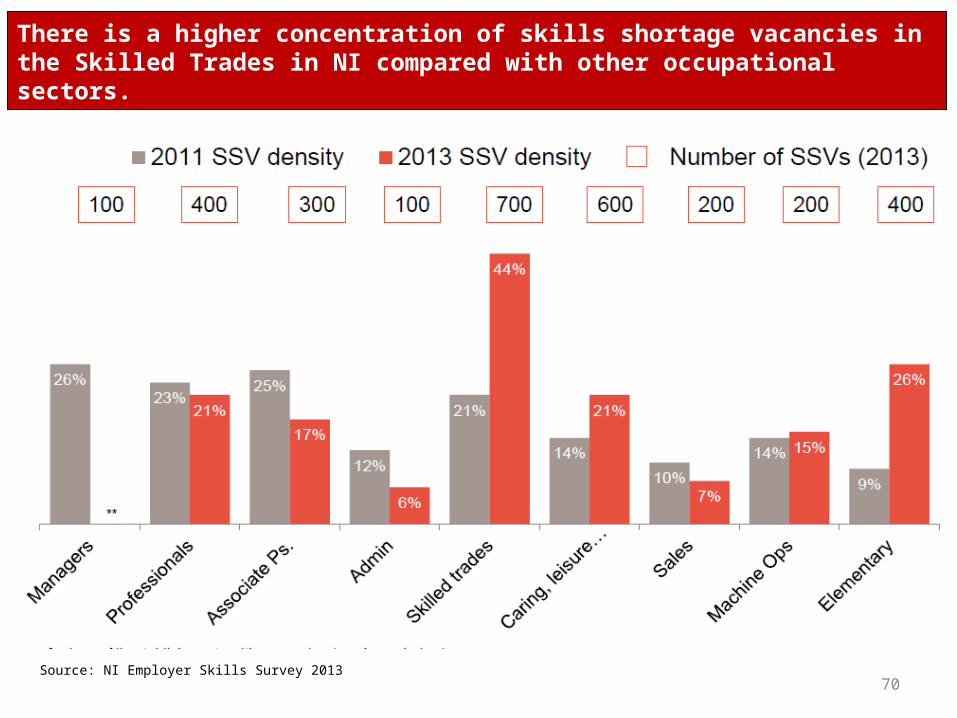

There is a higher concentration of skills shortage vacancies in the Skilled Trades in NI compared with other occupational sectors.

71Source: NI Employer Skills Survey 2013

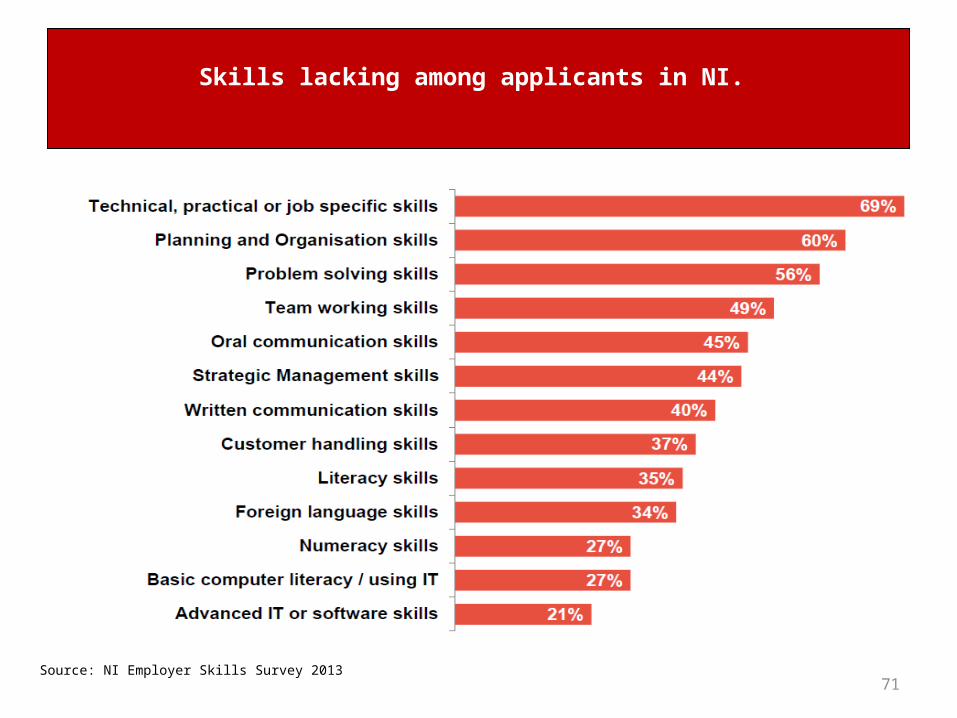

Skills lacking among applicants in NI.

Employer Engagement – Key Messages

• Employers in Northern Ireland value skills more highly than other parts of the UK.

• Although employers in Northern Ireland are less likely to take steps to address the skills gaps of their staff when compared to the rest of the UK.

• Employers in NI have identified that skills shortage vacancies (SSV’s) have doubled in the Skilled Trades sector between 2011 and 2013. However, it should be noted that only 3% of firms reported having a SSV and that SSV’s accounted for 19% of all vacancies in NI in 2013. Both of these figures are lower than the UK average which was 4% and 22% respectively.

• A number of planning, strategic, problem solving and team working skills were reported to be lacking in NI applicants.

72

73

Wider National and International Evidence on the Benefits of Investment

in Vocational Training

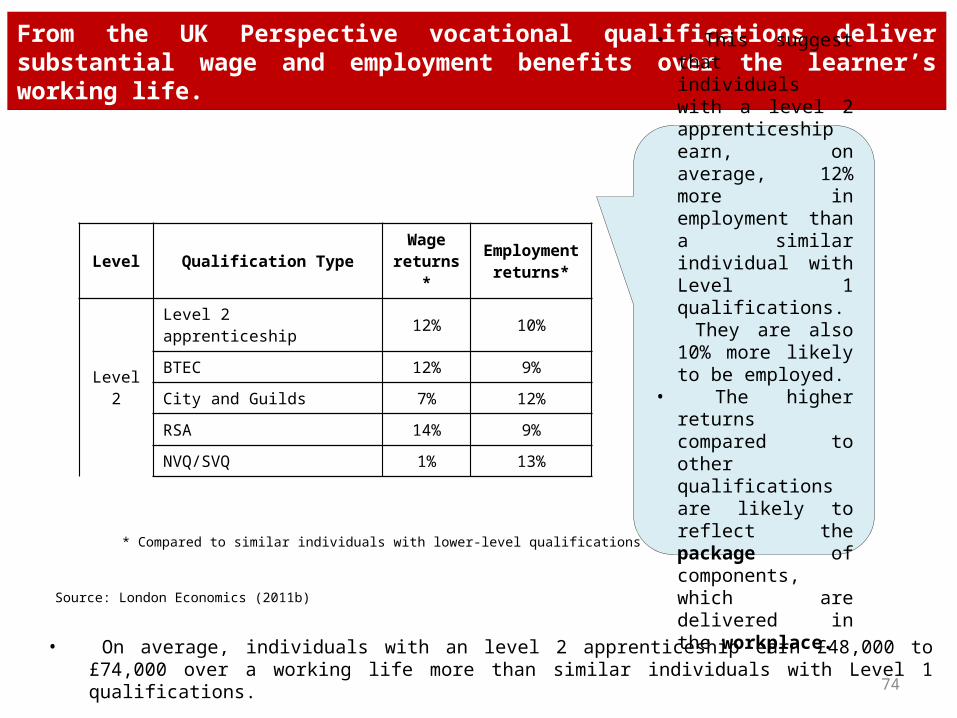

From the UK Perspective vocational qualifications deliver substantial wage and employment benefits over the learner’s working life.

Level Qualification TypeWage

returns*Employment

returns*

Level 2

Level 2 apprenticeship 12% 10%

BTEC 12% 9%

City and Guilds 7% 12%

RSA 14% 9%

NVQ/SVQ 1% 13%

• This suggest that individuals with a level 2 apprenticeship earn, on average, 12% more in employment than a similar individual with Level 1 qualifications. They are also 10% more likely to be employed.

• The higher returns compared to other qualifications are likely to reflect the package of components, which are delivered in the workplace.

* Compared to similar individuals with lower-level qualifications

Source: London Economics (2011b)

• On average, individuals with an level 2 apprenticeship earn £48,000 to £74,000 over a working life more than similar individuals with Level 1 qualifications.

74

75Source: BIS Research Paper Number 53

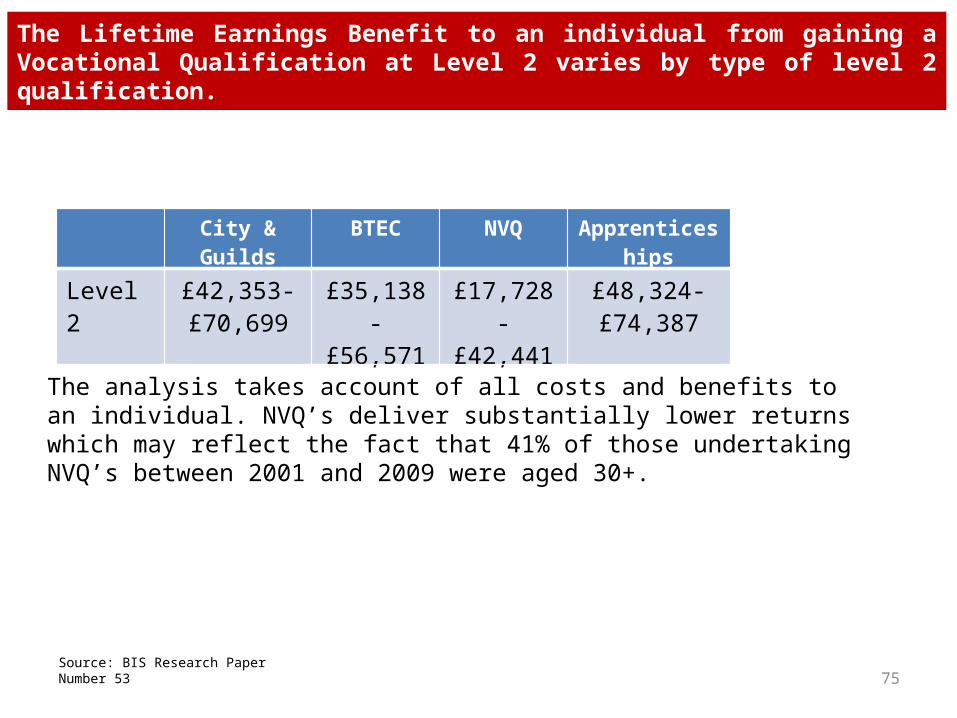

The Lifetime Earnings Benefit to an individual from gaining a Vocational Qualification at Level 2 varies by type of level 2 qualification.

City & Guilds BTEC NVQ Apprenticeships

Level 2 £42,353-£70,699

£35,138-£56,571

£17,728-£42,441

£48,324-£74,387

The analysis takes account of all costs and benefits to an individual. NVQ’s deliver substantially lower returns which may reflect the fact that 41% of those undertaking NVQ’s between 2001 and 2009 were aged 30+.

76Source: BIS Research Paper Number 53

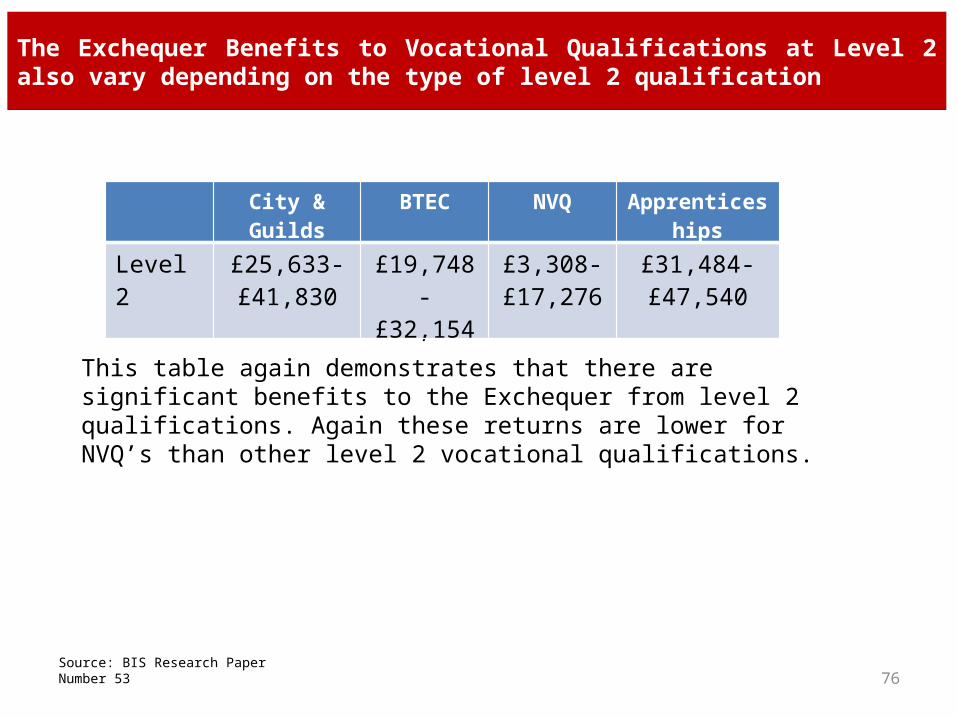

The Exchequer Benefits to Vocational Qualifications at Level 2 also vary depending on the type of level 2 qualification

City & Guilds BTEC NVQ Apprenticeships

Level 2 £25,633-£41,830

£19,748-£32,154

£3,308-£17,276

£31,484-£47,540

This table again demonstrates that there are significant benefits to the Exchequer from level 2 qualifications. Again these returns are lower for NVQ’s than other level 2 vocational qualifications.

77Source: BIS Research Paper Number 53

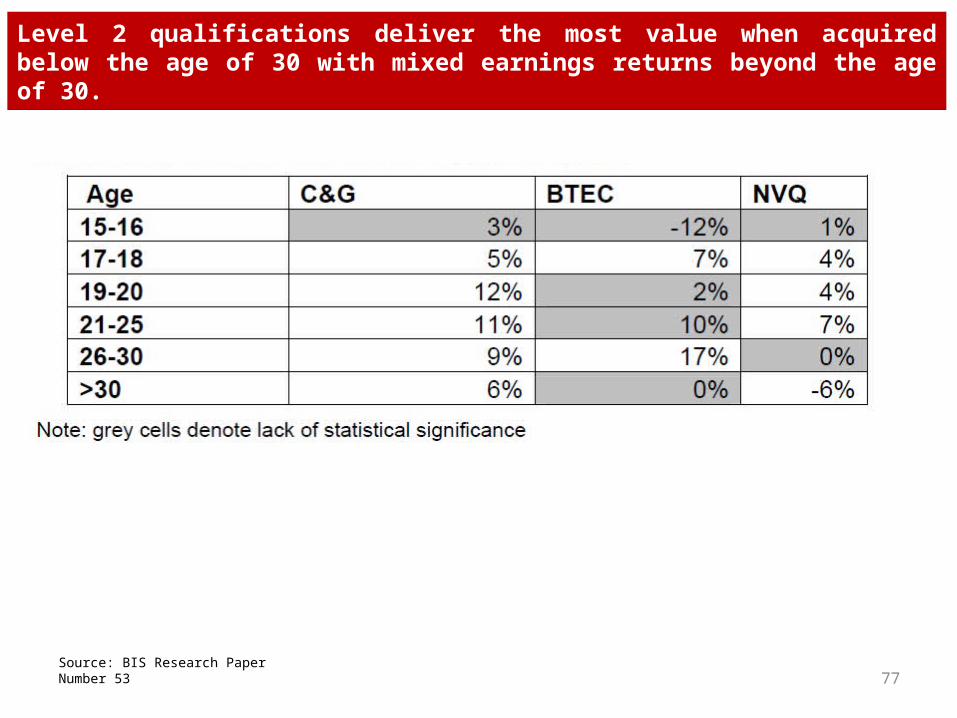

Level 2 qualifications deliver the most value when acquired below the age of 30 with mixed earnings returns beyond the age of 30.

78

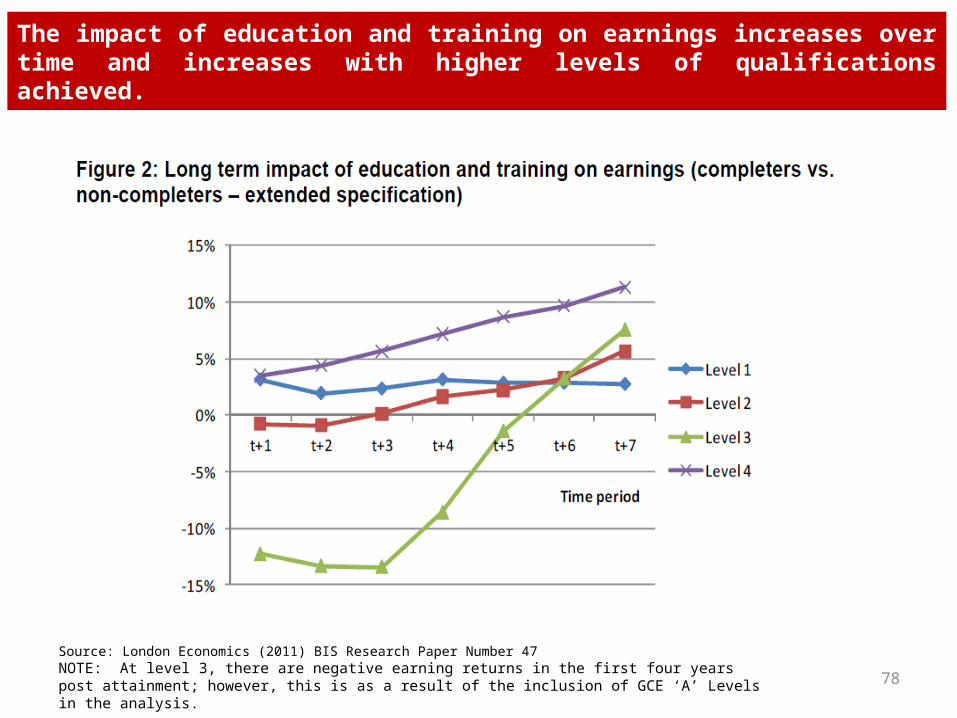

Source: London Economics (2011) BIS Research Paper Number 47NOTE: At level 3, there are negative earning returns in the first four years post attainment; however, this is as a result of the inclusion of GCE ‘A’ Levels in the analysis.

The impact of education and training on earnings increases over time and increases with higher levels of qualifications achieved.

79

Source: London Economics (2011) BIS Research Paper Number 47

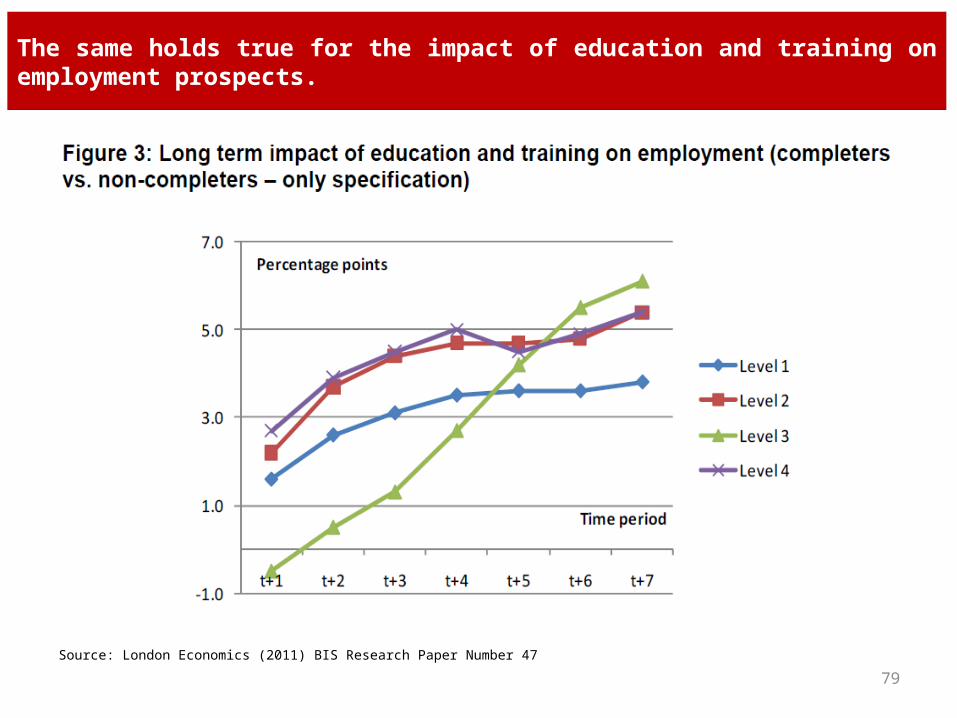

The same holds true for the impact of education and training on employment prospects.

80Source: London Economics (2011) BIS Research Paper Number 47

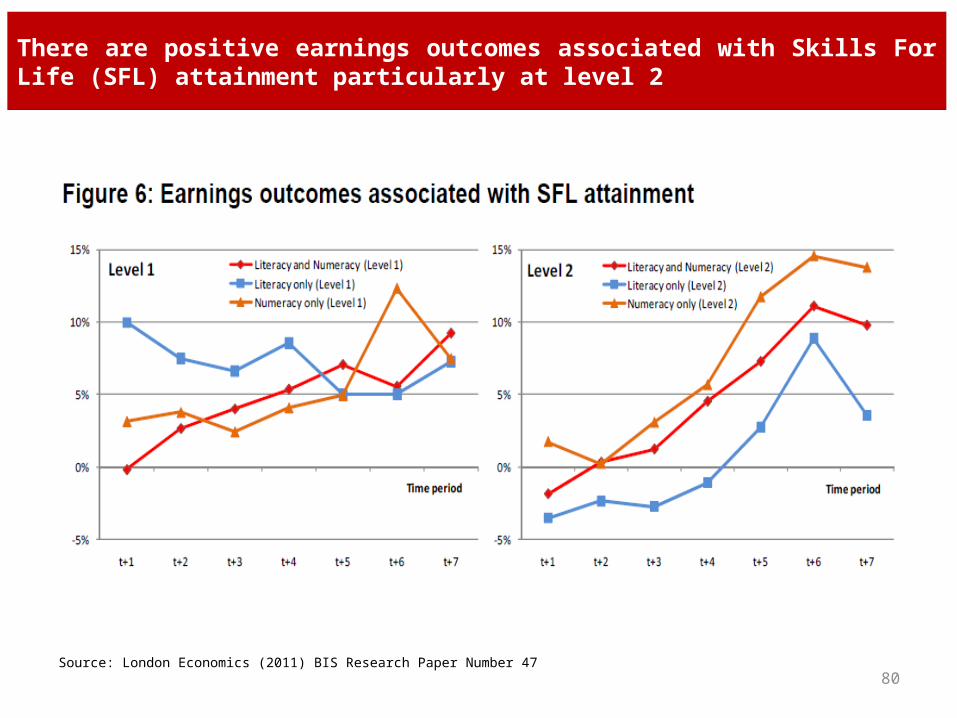

There are positive earnings outcomes associated with Skills For Life (SFL) attainment particularly at level 2

81Source: London Economics (2011) BIS Research Paper Number 47

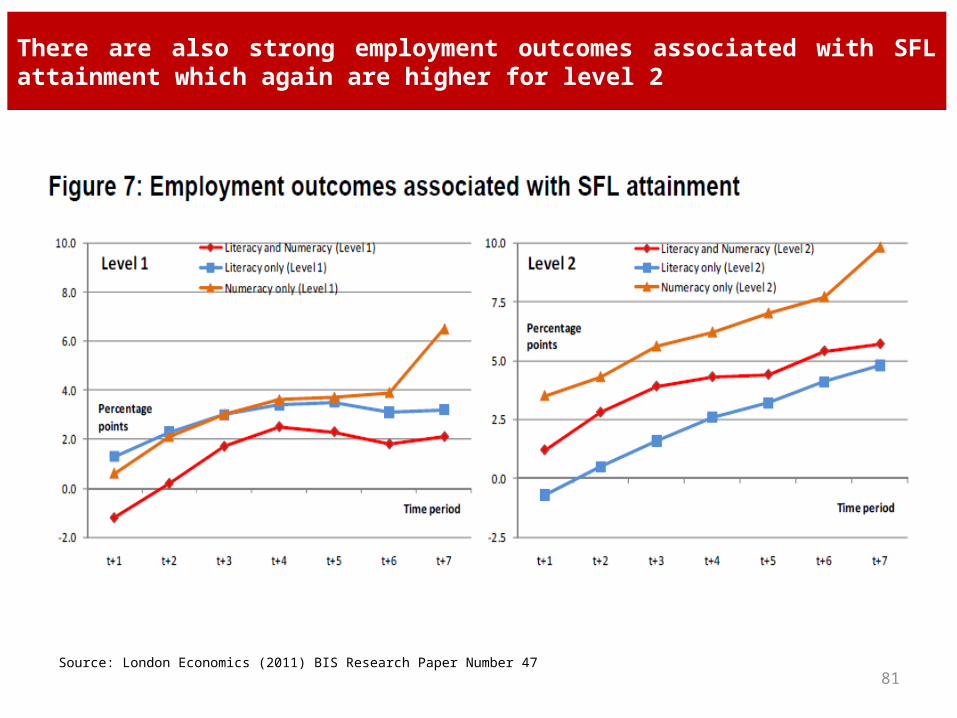

There are also strong employment outcomes associated with SFL attainment which again are higher for level 2