Embed Size (px)

Citation preview

1

REFORM OF ARTICLE 82 EC

BIICL, 24 February 2006

Treatment of Rebates

Johanne Peyre

2

N. KROES, Sept. 2005

“First, it is competition, and not competitors,

that is to be protected”

3

Competition vs. Competitors (1)

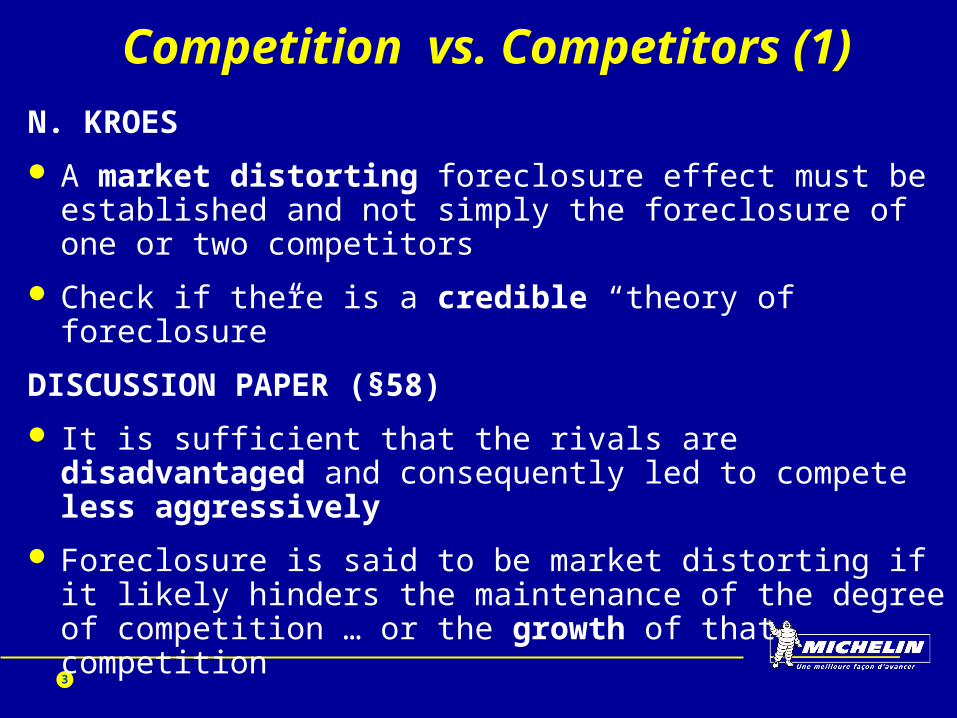

N. KROES

A market distorting foreclosure effect must be established and not simply the foreclosure of one or two competitors

Check if there is a credible “theory of foreclosure”

DISCUSSION PAPER (§58)

It is sufficient that the rivals are disadvantaged and consequently led to compete less aggressively

Foreclosure is said to be market distorting if it likely hinders the maintenance of the degree of competition … or the growth of that competition

4

Competition vs. Competitors (2)

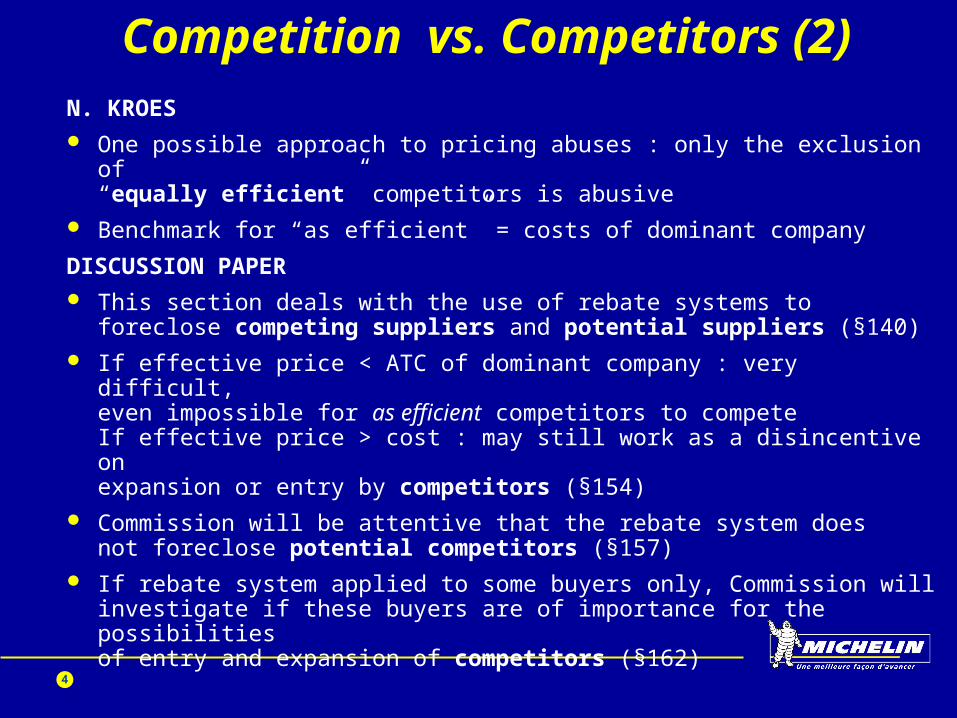

N. KROES One possible approach to pricing abuses : only the exclusion of

“equally efficient” competitors is abusive Benchmark for “as efficient” = costs of dominant company

DISCUSSION PAPER This section deals with the use of rebate systems to foreclose

competing suppliers and potential suppliers (§140) If effective price < ATC of dominant company : very difficult,

even impossible for as efficient competitors to competeIf effective price > cost : may still work as a disincentive on expansion or entry by competitors (§154)

Commission will be attentive that the rebate system does not foreclose potential competitors (§157)

If rebate system applied to some buyers only, Commission will investigate if these buyers are of importance for the possibilities of entry and expansion of competitors (§162)

5

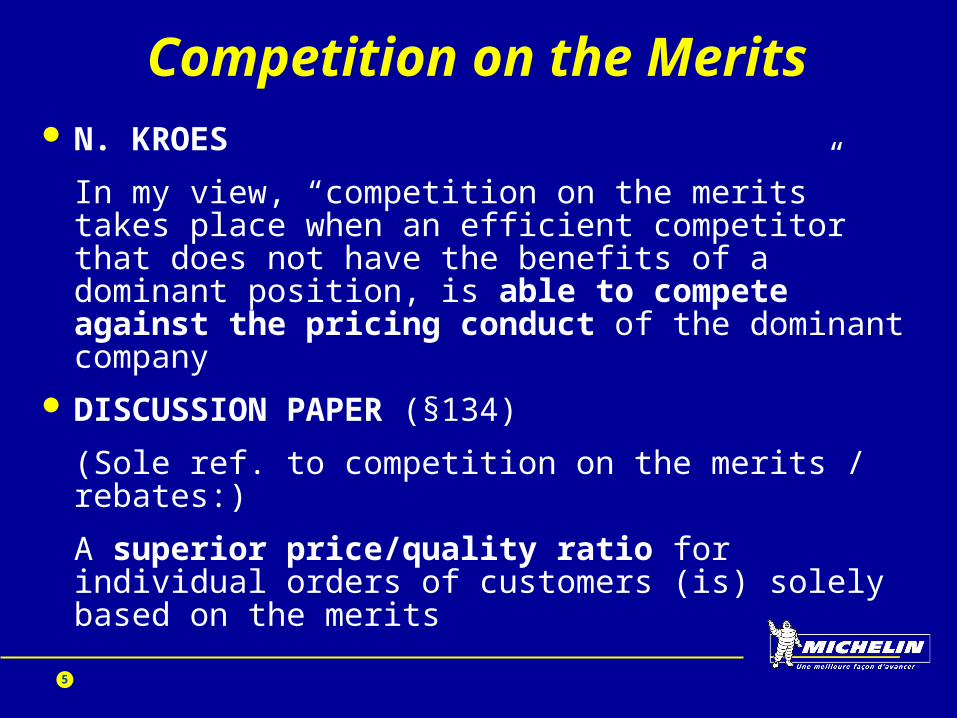

Competition on the Merits N. KROES

In my view, “competition on the merits” takes place when an efficient competitor that does not have the benefits of a dominant position, is able to compete against the pricing conduct of the dominant company

DISCUSSION PAPER (§134)

(Sole ref. to competition on the merits / rebates:)

A superior price/quality ratio for individual orders of customers (is) solely based on the merits

6

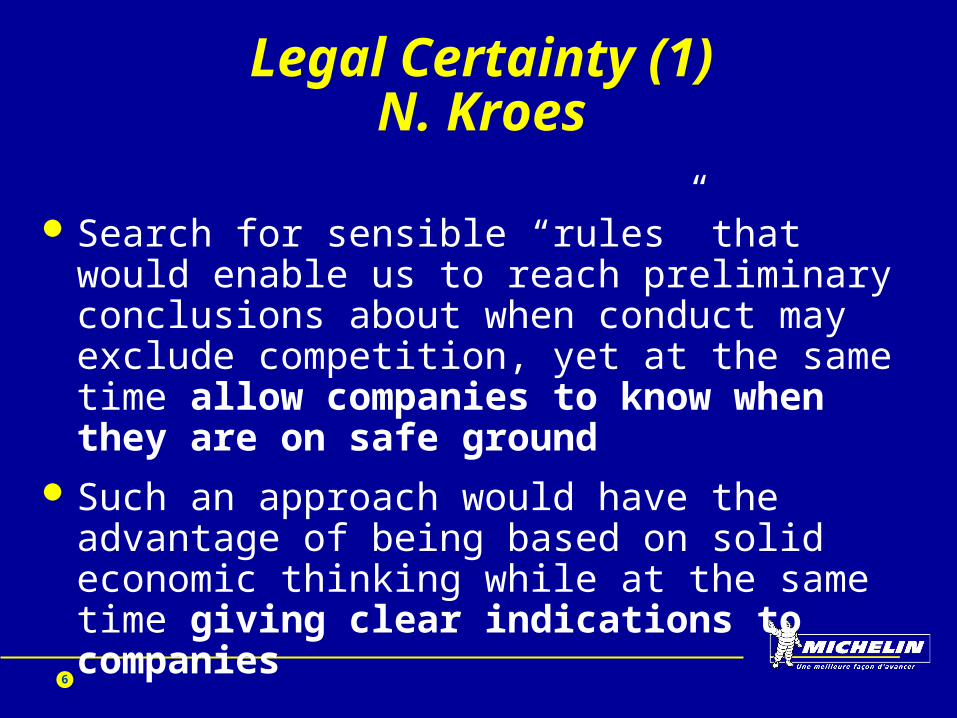

Legal Certainty (1)N. Kroes

Search for sensible “rules” that would enable us to reach preliminary conclusions about when conduct may exclude competition, yet at the same time allow companies to know when they are on safe ground

Such an approach would have the advantage of being based on solid economic thinking while at the same time giving clear indications to companies

7

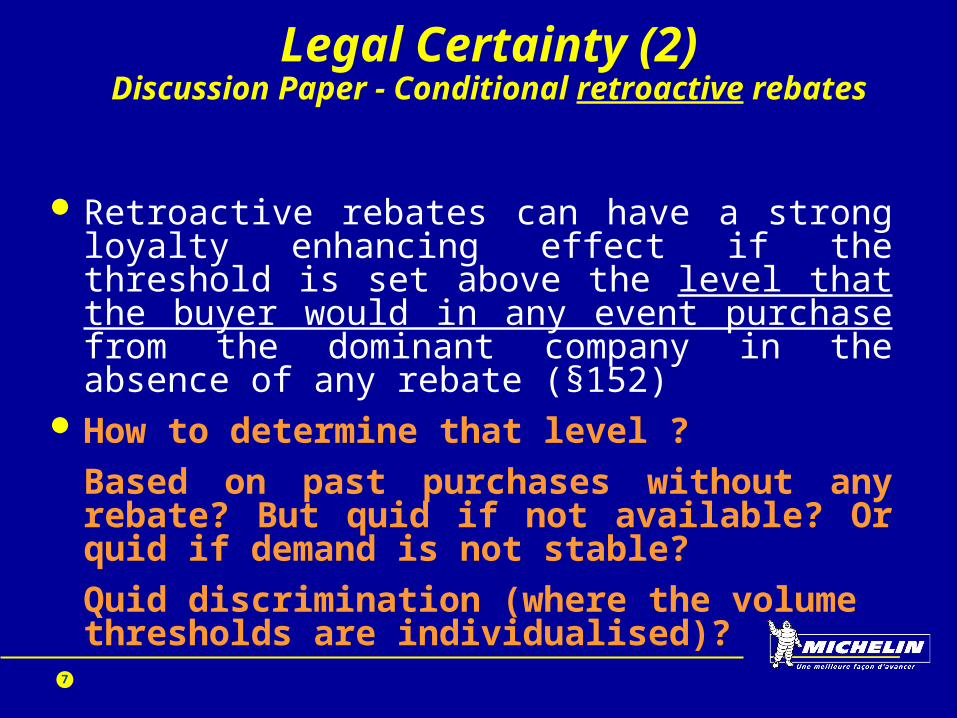

Legal Certainty (2)Discussion Paper - Conditional retroactive rebates

Retroactive rebates can have a strong loyalty enhancing effect if the threshold is set above the level that the buyer would in any event purchase from the dominant company in the absence of any rebate (§152)

How to determine that level ?

Based on past purchases without any rebate? But quid if not available? Or quid if demand is not stable?

Quid discrimination (where the volume thresholds are individualised)?

8

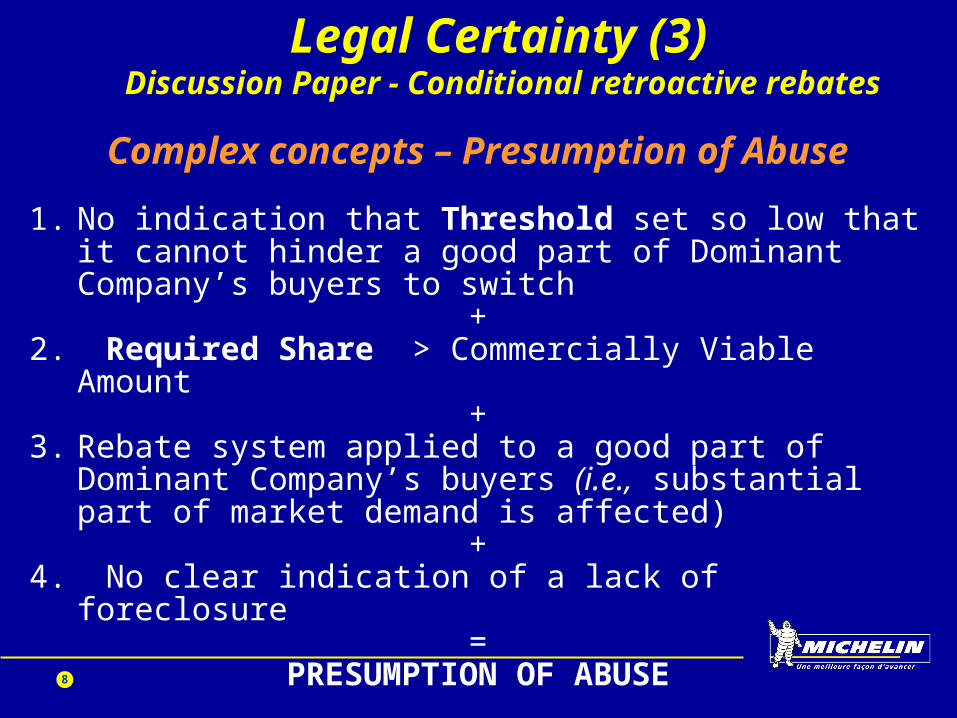

Legal Certainty (3) Discussion Paper - Conditional retroactive

rebatesComplex concepts – Presumption of Abuse

1. No indication that Threshold set so low that it cannot hinder a good part of Dominant Company’s buyers to switch

+2. Required Share > Commercially Viable Amount

+3. Rebate system applied to a good part of Dominant

Company’s buyers (i.e., substantial part of market demand is affected)

+4. No clear indication of a lack of foreclosure

=PRESUMPTION OF ABUSE

9

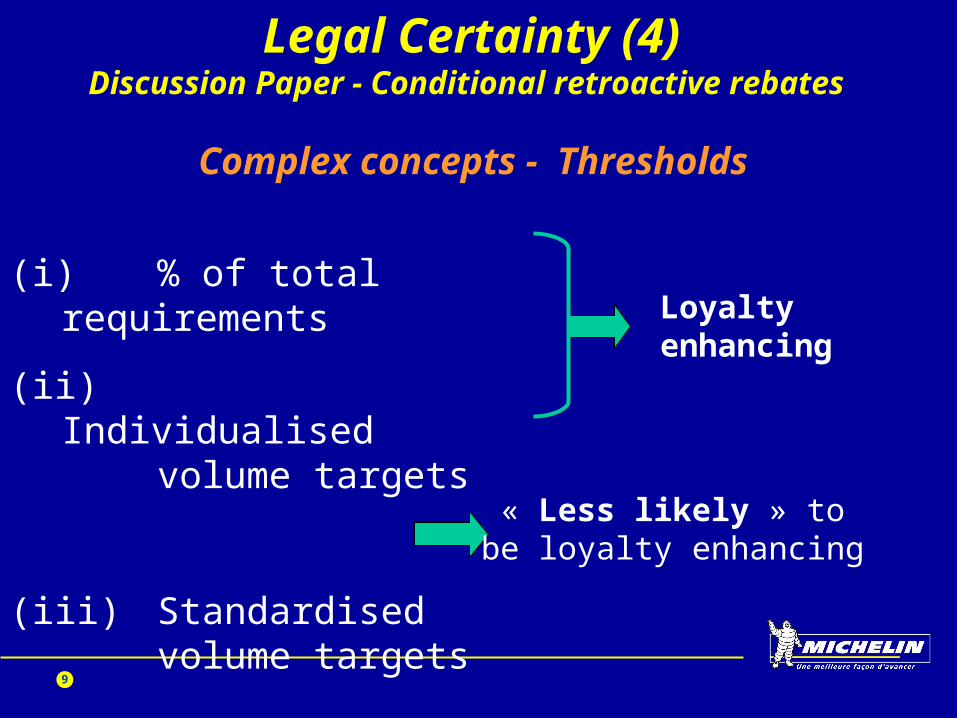

Legal Certainty (4) Discussion Paper - Conditional retroactive

rebates

(i) % of total requirements

(ii) Individualised volume targets

(iii) Standardised volume targets

Loyalty enhancing

« Less likely » to be loyalty enhancing

Complex concepts -

Thresholds

10

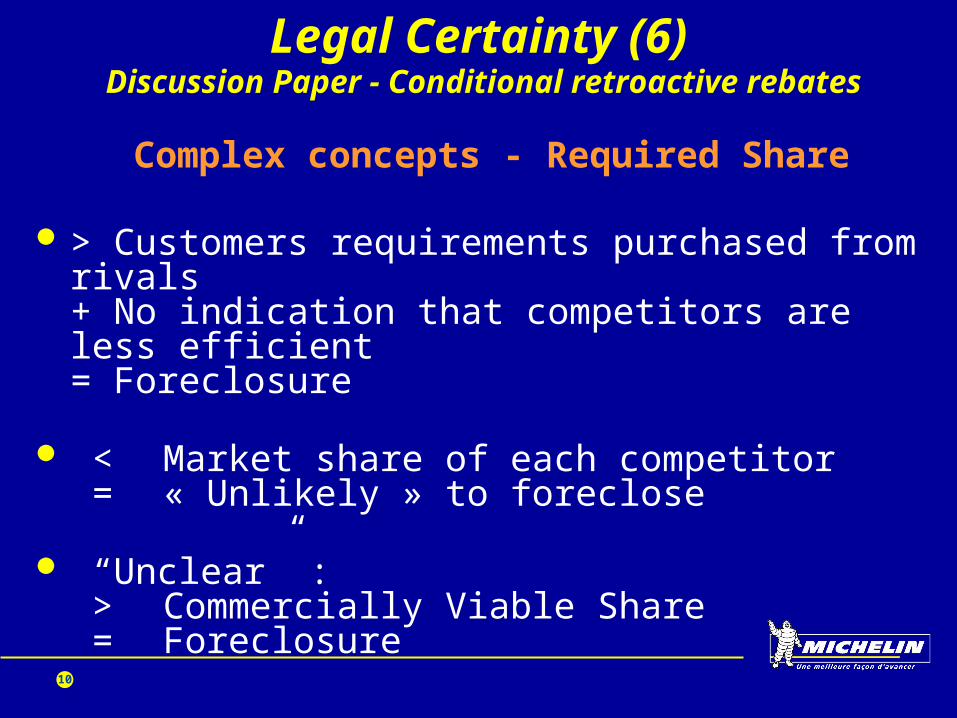

Legal Certainty (6) Discussion Paper - Conditional retroactive

rebates

Complex concepts - Required Share

> Customers requirements purchased from rivals + No indication that competitors are less efficient= Foreclosure

< Market share of each competitor = « Unlikely » to foreclose

“Unclear” : > Commercially Viable Share = Foreclosure

11

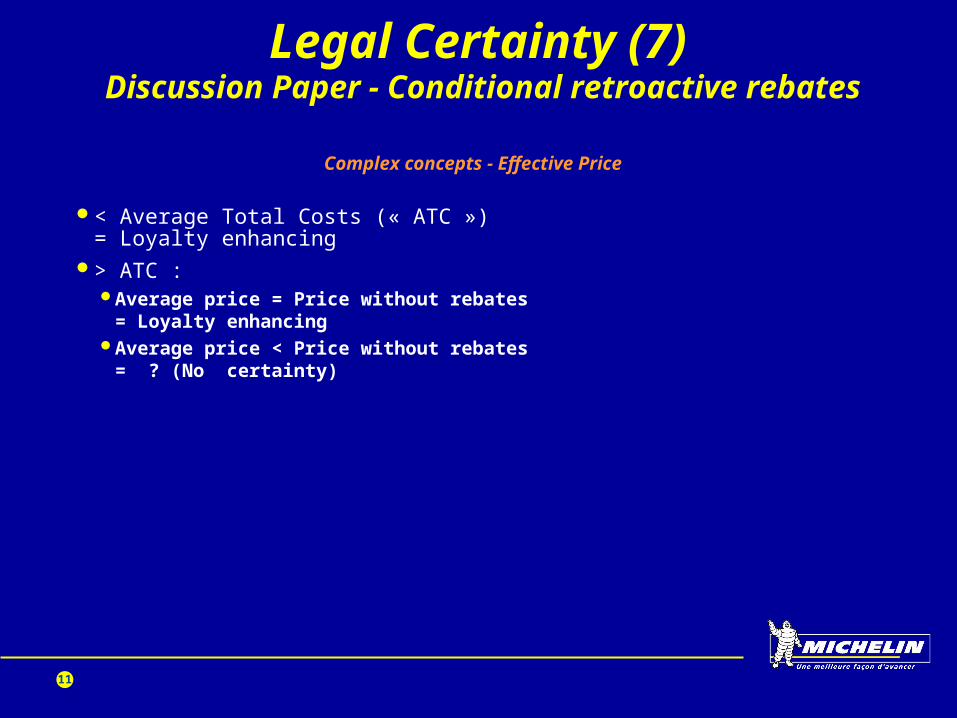

Legal Certainty (7) Discussion Paper - Conditional retroactive

rebates

Complex concepts - Effective Price

< Average Total Costs (« ATC »)= Loyalty enhancing

> ATC :Average price = Price without rebates

= Loyalty enhancingAverage price < Price without rebates

= ? (No certainty)

12

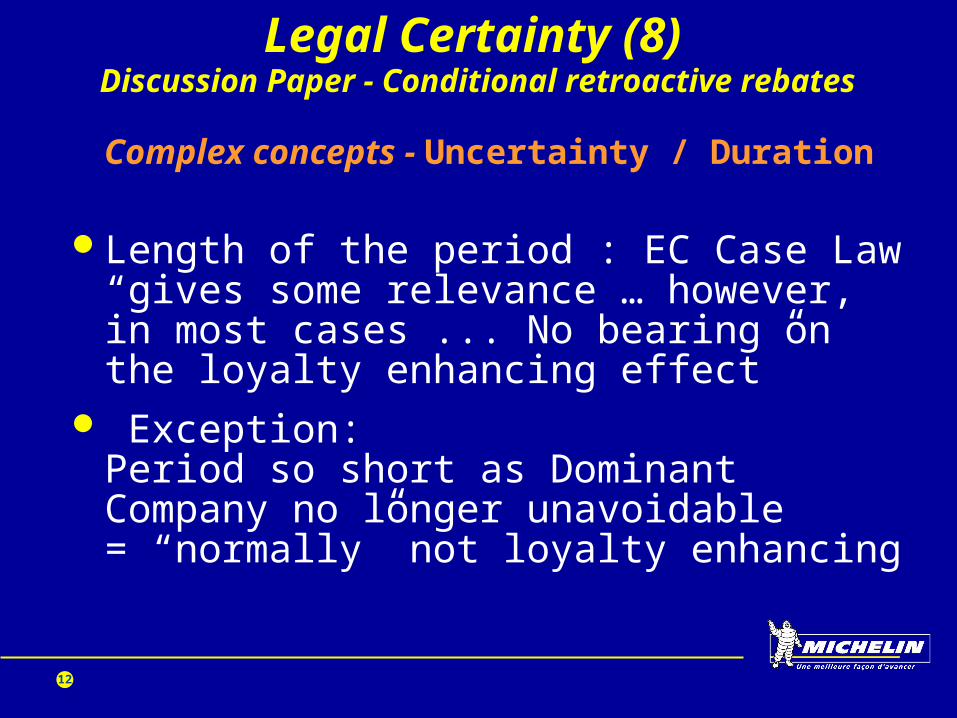

Legal Certainty (8) Discussion Paper - Conditional retroactive

rebates

Complex concepts - Uncertainty / Duration

Length of the period : EC Case Law “gives some relevance … however, in most cases ... No bearing on the loyalty enhancing effect”

Exception: Period so short as Dominant Company no longer unavoidable= “normally” not loyalty enhancing

13

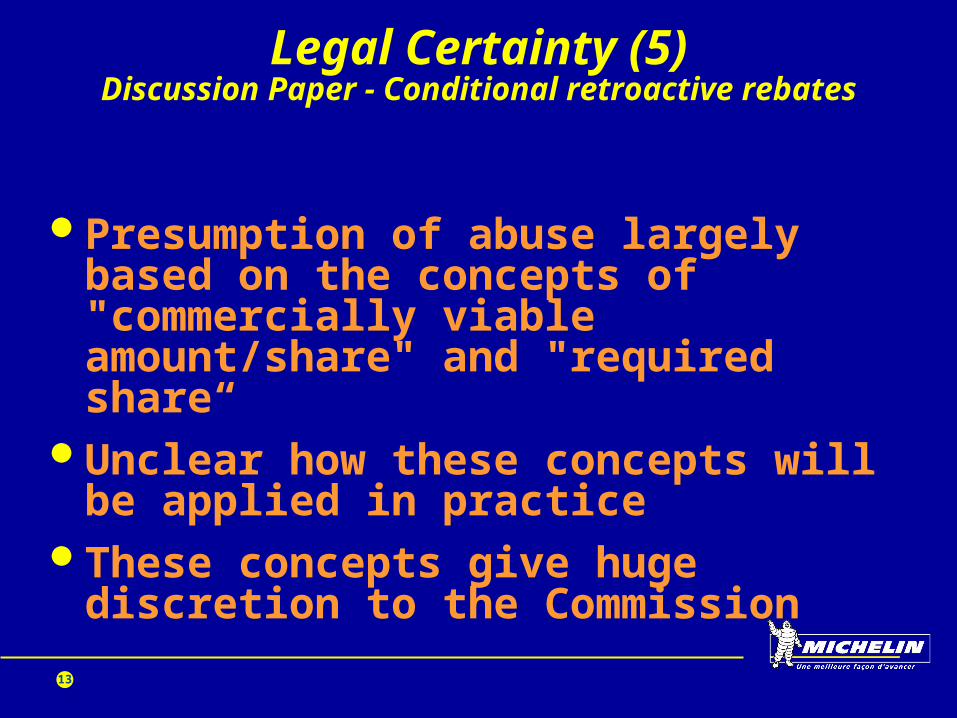

Legal Certainty (5) Discussion Paper - Conditional retroactive

rebates

Presumption of abuse largely based on the concepts of "commercially viable amount/share" and "required share“

Unclear how these concepts will be applied in practice

These concepts give huge discretion to the Commission

14

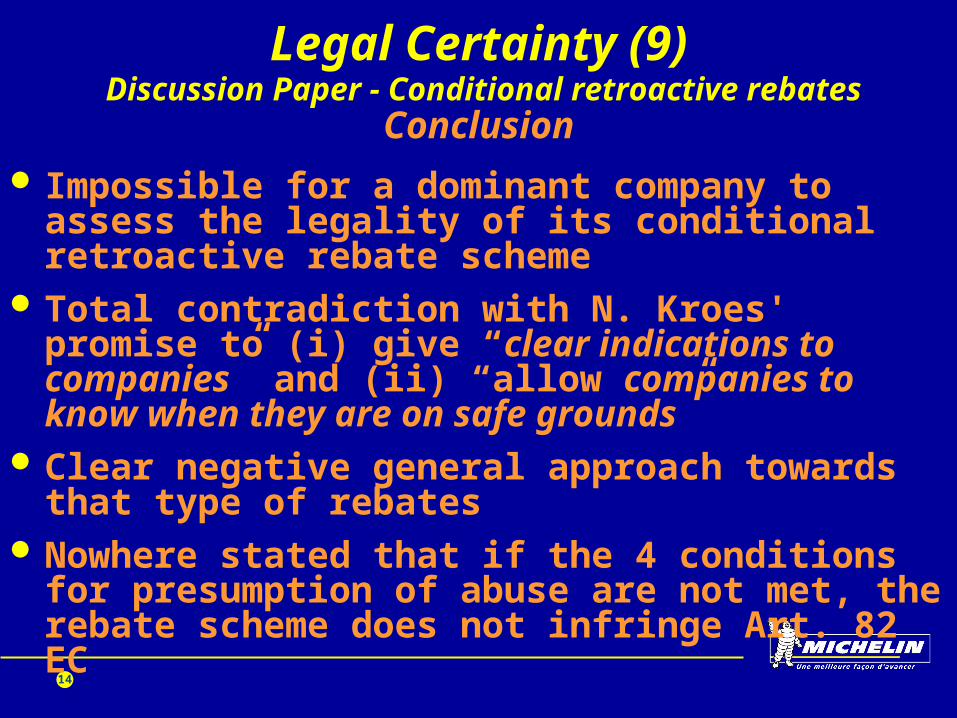

Legal Certainty (9) Discussion Paper - Conditional retroactive

rebatesConclusion

Impossible for a dominant company to assess the legality of its conditional retroactive rebate scheme

Total contradiction with N. Kroes' promise to (i) give “clear indications to companies” and (ii) “allow companies to know when they are on safe grounds”

Clear negative general approach towards that type of rebates

Nowhere stated that if the 4 conditions for presumption of abuse are not met, the rebate scheme does not infringe Art. 82 EC

15

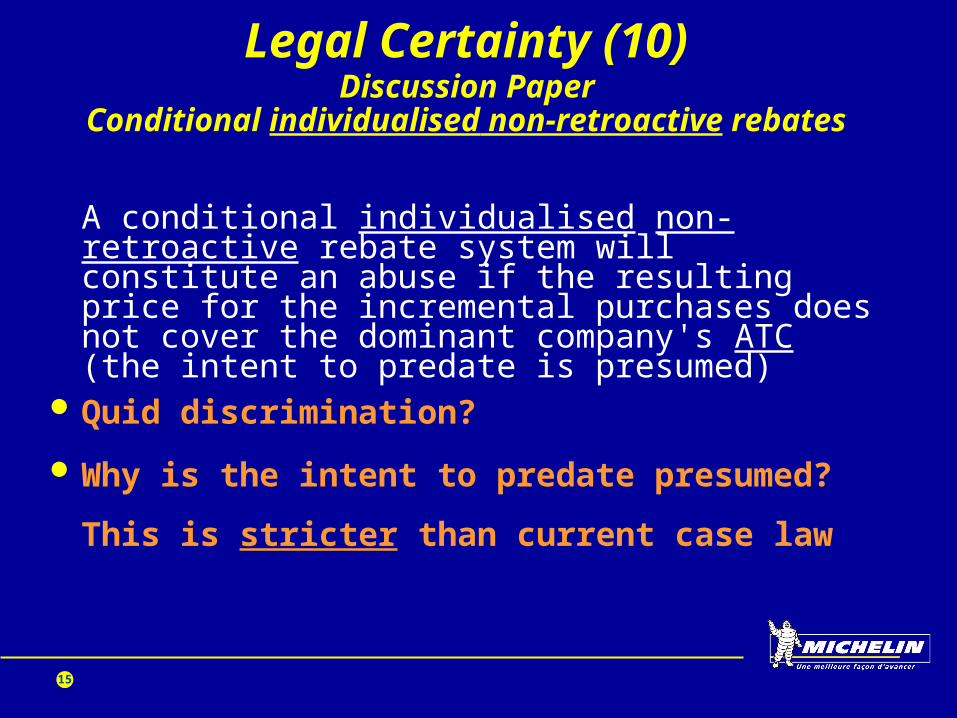

Legal Certainty (10) Discussion Paper

Conditional individualised non-retroactive rebates

A conditional individualised non-retroactive rebate system will constitute an abuse if the resulting price for the incremental purchases does not cover the dominant company's ATC (the intent to predate is presumed)

Quid discrimination?

Why is the intent to predate presumed?

This is stricter than current case law

16

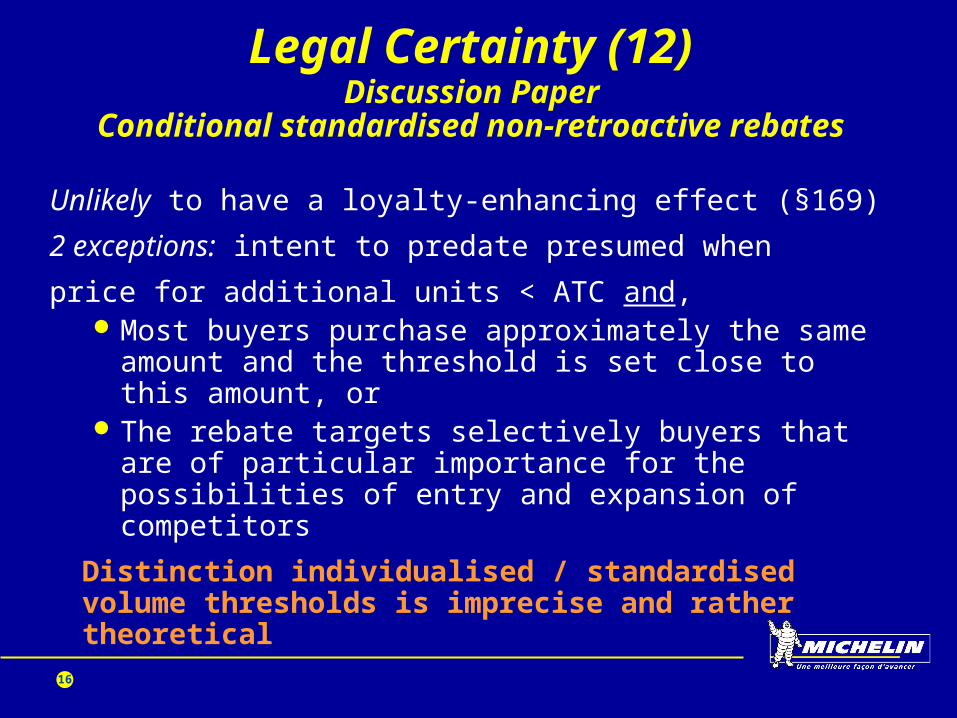

Legal Certainty (12) Discussion Paper

Conditional standardised non-retroactive rebates

Unlikely to have a loyalty-enhancing effect (§169)

2 exceptions: intent to predate presumed when

price for additional units < ATC and,Most buyers purchase approximately the same

amount and the threshold is set close to this amount, or

The rebate targets selectively buyers that are of particular importance for the possibilities of entry and expansion of competitors

Distinction individualised / standardised volume thresholds is imprecise and rather theoretical

17

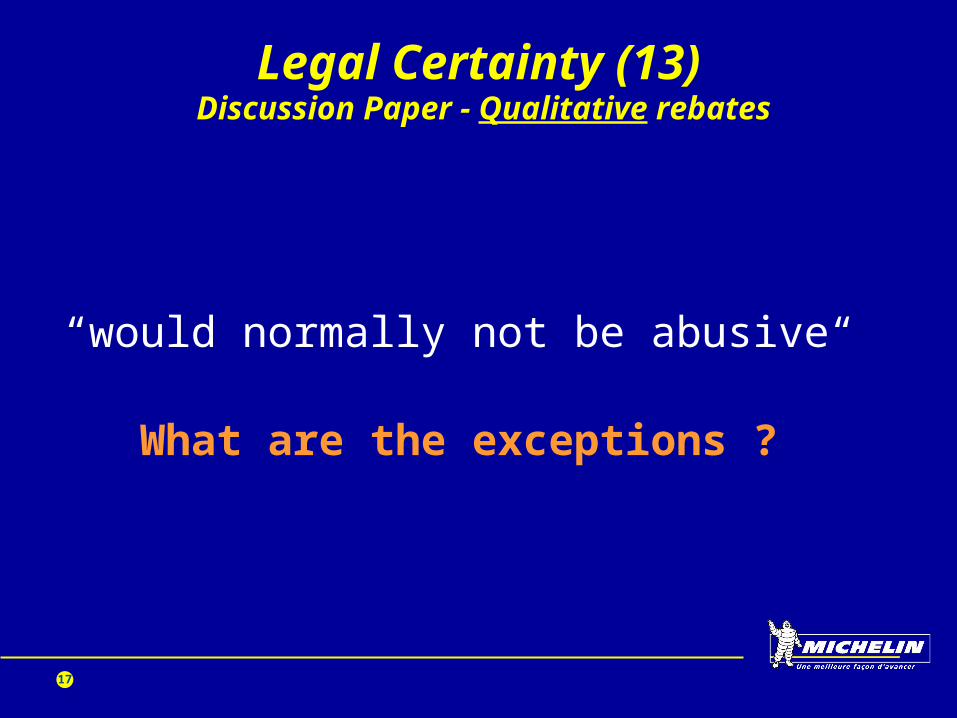

Legal Certainty (13) Discussion Paper - Qualitative rebates

“would normally not be abusive“

What are the exceptions ?

18

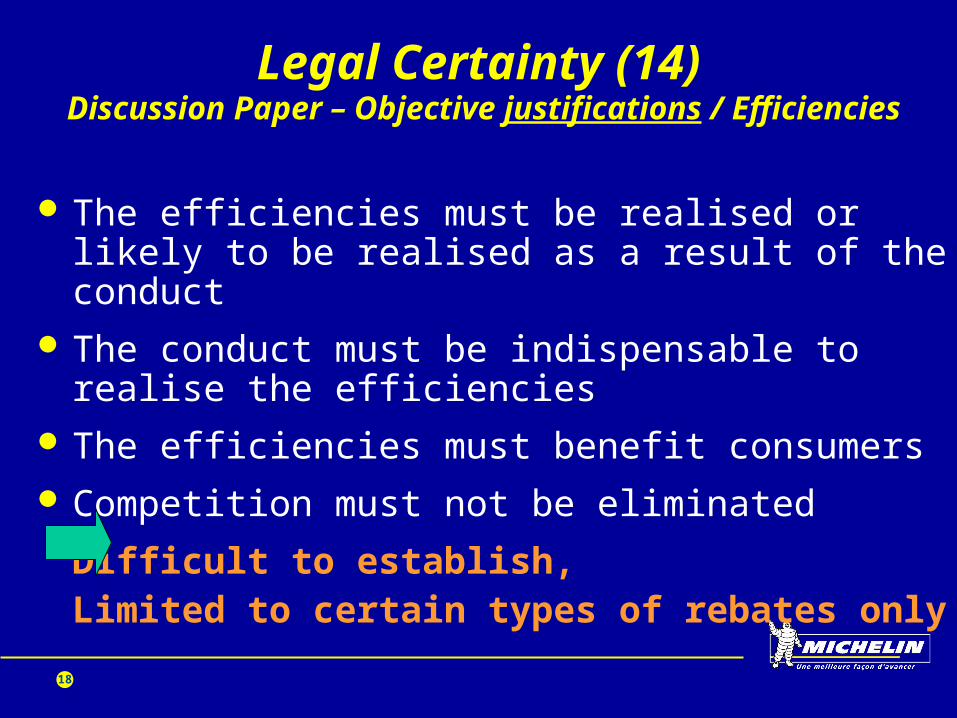

Legal Certainty (14) Discussion Paper – Objective justifications /

Efficiencies

The efficiencies must be realised or likely to be realised as a result of the conduct

The conduct must be indispensable to realise the efficiencies

The efficiencies must benefit consumers Competition must not be eliminated

Difficult to establish, Limited to certain types of rebates

only

19

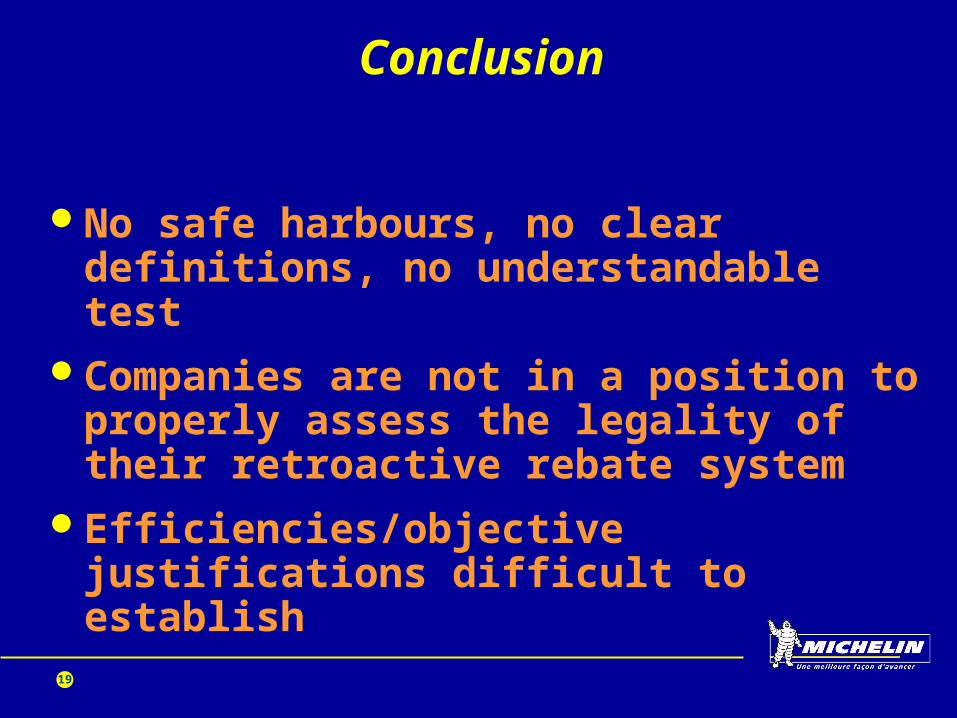

Conclusion

No safe harbours, no clear definitions, no understandable test

Companies are not in a position to properly assess the legality of their retroactive rebate system

Efficiencies/objective justifications difficult to establish

20

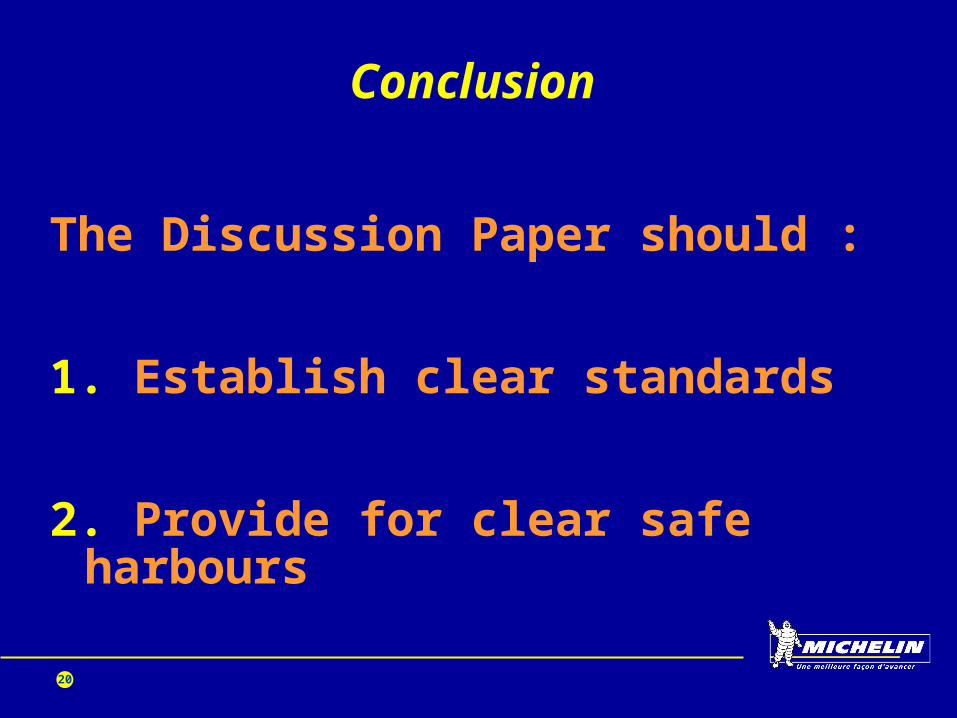

Conclusion

The Discussion Paper should :

1. Establish clear standards

2. Provide for clear safe harbours

21

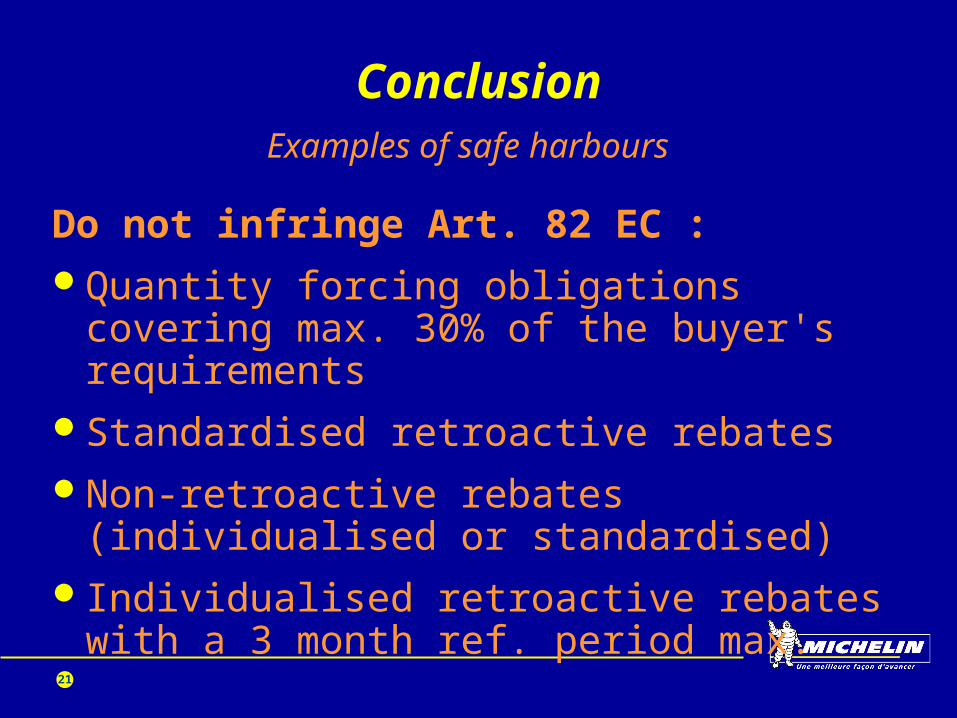

ConclusionExamples of safe harbours

Do not infringe Art. 82 EC :Quantity forcing obligations covering

max. 30% of the buyer's requirementsStandardised retroactive rebates Non-retroactive rebates

(individualised or standardised)Individualised retroactive rebates with

a 3 month ref. period max.

22

Conclusion

3. Provide for appropriate presumptions of illegality that

could be rebutted(e.g. individualised annual target rebate presumed illegal unless it can establish that it has no anticompetitive effect for example because the target does not prevent the buyer from purchasing substantial amounts from other suppliers)

23

Conclusion

4. Explain clearly how the Discussion Paper is compatible or can be distinguished from existing European Courts case law

24

Thank you for

your attention