Embed Size (px)

Citation preview

1

Personal InvestmentsPersonal Investments

Unit 1Introduction – Your financial

life

2

Activity: Financial dreams/Financial nightmares

• List all your financial dreams

• List all your financial nightmares

3

Your (financial) Life

4Age (years)

10 20 30 40 50 60 70 80

Childhood

High School

and College Starting a

family

Growing your career and managing

life’s ups and downs

Retirement

Your Financial Life

-$10,000

$20,000

$40,000

$60,000

You begin by being a financial

drain to your middle-class parents at

$10,000 a year or $184,000

until you leave the roost—and

that doesn’t include college

tuition.

Income

You’re starting to earn money

(not much) and getting the

education (expensive) to

earn more. This is when you start with credit cards and student

loans.

Your earnings start to take off and you settle down to start a family. With that comes your first

house (down payment of about

$30,000), mortgage, and the kids who now drain

you $10,000 a year. You need an emergency fund of

six months. You protect your assets

with insurance.

You move towards your peak earning years and use this time to grow your

wealth. You upgrade your

house and save for your kids’ education

($100,000) and your retirement ($1 million). You may be unemployed

(by choice or not) at times. You may divorce. You may have to care for your parents. All these could set

you back.

Your income could fall well before you

reach retirement age. You continue to accumulate for

retirement and plan how your nest egg will last for the rest of your

life. Health issues start to crop up and you look to protect

your health and assets. You may work longer because you need to or because

you want to.

If you’ve been good about saving, you will enter retirement debt-free and comfortable

for the rest of your life. If you haven’t, the only option is to

continue working if you can. Healthcare

becomes a big expense.

Expect to be self-employed,under-employed or unemployed sometimes.

People change jobs on average every two years.

5

DRAFT 3/6/2007 6

Typical income

DRAFT 3/6/2007 7

Your financial life - income

2005 Median Household Income by Age

-20000

-10000

0

10000

20000

30000

40000

50000

60000

70000U

nd

er

5

5 t

o 1

4

15

to

24

25

to

29

30

to

34

35

to

39

40

to

44

45

to

49

50

to

54

55

to

59

60

to

64

65

to

69

70

to

74

Ov

er

75

Age in years

Inc

om

e in

20

05

do

llars

Source: US Census Current Population Survey 2006

DRAFT 3/6/2007 8

Based on gender?

DRAFT 3/6/2007 9

Based on education

Salaries are leveling off.

You can still improve your earnings with education.

Washington

2006 Median Income

Total: 63,705

2-person families 58,5843-person families 66,2524-person families 75,1405-person families 68,5626-person families 62,4847-or-more-person families 61,212

10

DRAFT 3/6/2007 11

Income is not rising but debt is

0

500000

1000000

1500000

2000000

2500000

3000000

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Consumer debt has doubled in the past 10 years(Consumer credit $ millions - does not include mortgages)

DRAFT 3/6/2007 12

People are raiding the piggy bank

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1950-9 1960-9 1970-9 1980-9 1990-9 2000-6

Homeowner equity is falling as more debt is assumed(Homeowner's equity/Value of Household Real Estate)

Source: Mortgage Bankers Association

DRAFT 3/6/2007 13

Spending power?

0

2,000

4,000

6,000

8,000

10,000

12,000

1979 1984 1989 1994 1999 2004

Personal Disposable Income

Outstanding Household Debt

Personal Disposable Income and Outstanding Household Debt$ Billions

DRAFT 3/6/2007 14

How are we doing at savings?

DRAFT 3/6/2007 15

Could we save more?

Summary

• Consider your entire financial life and be aware of all the twists and turns

• Choose a good career and educate yourself

• Don’t borrow to spend

• Save – even if you think you’ve saved all you can, save more

DRAFT 3/6/2007 16

DRAFT 3/6/2007 17

What we will do in this course

• Focus on financial goals• Save and let Uncle Sam help• Learn about different investments• Asset allocation NOT investment selection• Evaluate funds• Learn when to buy and sell• Protect your wealth

Your financial goals(optional)

DRAFT 3/6/2007 18

Setting goals – start small

• What do you want to achieve this year?

• Over the next year, what ONE occurrence would have to happen for you to feel you’ve made significant financial progress?

• Write this occurrence as a goal. • Describe why it is important to you.• Describe how you will feel when you

have accomplished this goal.

19

DRAFT 3/6/2007 20

Cost out your goals

• Down payment on house (The more you put down the less risk to default and less monthly payments)

• Wedding (yours or your kids)• Car (Budget or goal?)• College tuition (you/your kids/your grandkids)(http://cgi.money.cnn.com/tools/collegecost/collegecost.html)

• Starting your own business• Retirement (Rule of thumb – annual income divided by

4%) (http://sites.stockpoint.com/aarp_rc/wm/Retirement/Retirement.asp?act=LOGIN)

• Estate (Inheritance or charity)

Your net worth

What you own (home, car, bank accounts, etc.)

Less

What you owe (mortgage, car loans, student loans, credit card balance, etc.)

Keep track of it and grow it every year.

DRAFT 3/6/2007 21

DRAFT 3/6/2007 22

Your financial life – net worth Household Wealth - Survey of Income and Program Participation 2000

0

20000

40000

60000

80000

100000

120000

140000

Less than 35years

35 to 44years

45 to 54years

55 to 64years

65 to 69years

70 to 74years

75 years andolder

Median Net Worth

Excluding Home

Source: US Census

Summary

• Set goals – start small and keep at it

• Make your goals specific and cost them out

• Calculate your net worth

• Grow your net worth

DRAFT 3/6/2007 23

Unit 2 -Tax-advantaged saving -

Saving with help from Uncle Sam.

24

DRAFT 3/6/2007 25

The importance of saving early

Which is more?1. Saving $4000 a year

from 25 to 45 years old and then no more savings but you leave it in your account (at 8% per year)

2. Saving $8000 (double) a year from 45 to 65 years old

DRAFT 3/6/2007 26

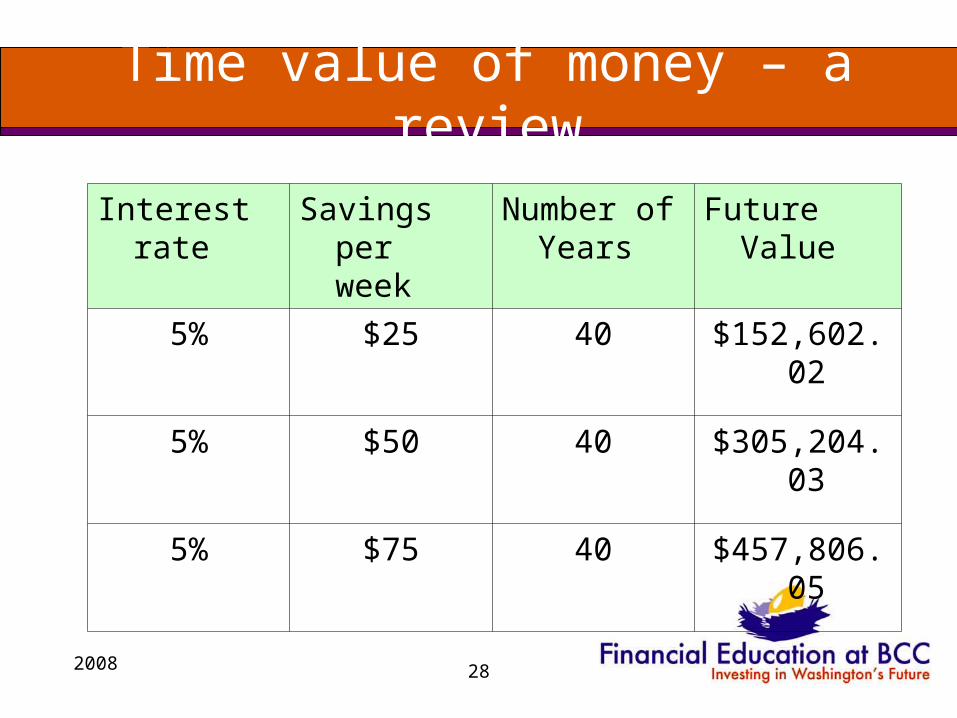

Finding money to invest – time value of money (a review)

27

3. The effect of saving every year

• You cut out candy and soda for savings of $25 every week.

• What will you have in 40 years?

2008 28

Time value of money – a review

Interest rate Savings per week

Number of Years

Future Value

5% $25 40 $152,602.02

5% $50 40 $305,204.03

5% $75 40 $457,806.05

29

The effect of a better return

Interest rate Savings per week

Number of Years

Future Value

8% $25 40 $349,100.78

8% $50 40 $698,201.57

8% $75 40 $1,047,302.35

Start early and let your money work for you

30

Number of

yearsSavings per year

Total contributions Earnings Total

25-65 years 40 4000 160000 $798,540 $958,54030-65 years 35 4000 140000 $552,947 $692,94735-65 years 30 4000 120000 $377,843 $497,84340-65 years 25 4000 100000 $252,996 $352,996.

Case study: Cost of cashing out

• About 57% of people who leave companies cash out their retirement benefits of $8445. If you left this money in a retirement plan for 40 years at a return of 8%, calculate what it contributes to your retirement.

31

Cost of cashing out

• You lose about $183,500 for your retirement fund. If you cash out, you pay taxes on your withdrawal plus a 10% penalty on top of that. That would leave you with $6000 now versus $183,500 when you retire.

32

DRAFT 3/6/2007 33

Maximizing retirement saving

• 54% have access to employer-sponsored plans and 43% participate• 53% of white-collar occupations• 40% of blue-collar occupations• 20% of service occupations

• Employees make contributions to retirement savings plan• Employers may match contributions up to a certain amount• When employee leaves company, the money goes with him or

her (portable)• Retirement income depends on how much employee

contributes and the returns on the money

DRAFT 3/6/2007 34

Employer Plans

• Most common defined contribution plan is 401K– 43 million participants– 457,830 plans– $2.1 Trillion in assets

DRAFT 3/6/2007 35

401K – How does it work?

• Jill is single and makes $30,000 a year gross salary and she wants to put $1800 away for retirement in 30 years.

• She is considering three options:– 401K contribution– Traditional IRA contribution– Roth IRA contribution

DRAFT 3/6/2007 36

401K – How it works• Salary is typically contributed pretax – will reduce your

salary for tax purposes • Maximum contribution $15,500 (2008) with an

additional catch-up of $5000 for those over 50 years old

• 82% of employees contribute • On average participants put in 6.8% of salary• 91% of employers match your contributions up to on

average 3.3% of your salary• There is a 10% penalty for withdrawing before age 59

½ and you have to pay taxes on your withdrawal• When you leave your company, you may rollover your

401K to a Individual Retirement Account (IRA)

DRAFT 3/6/2007 37

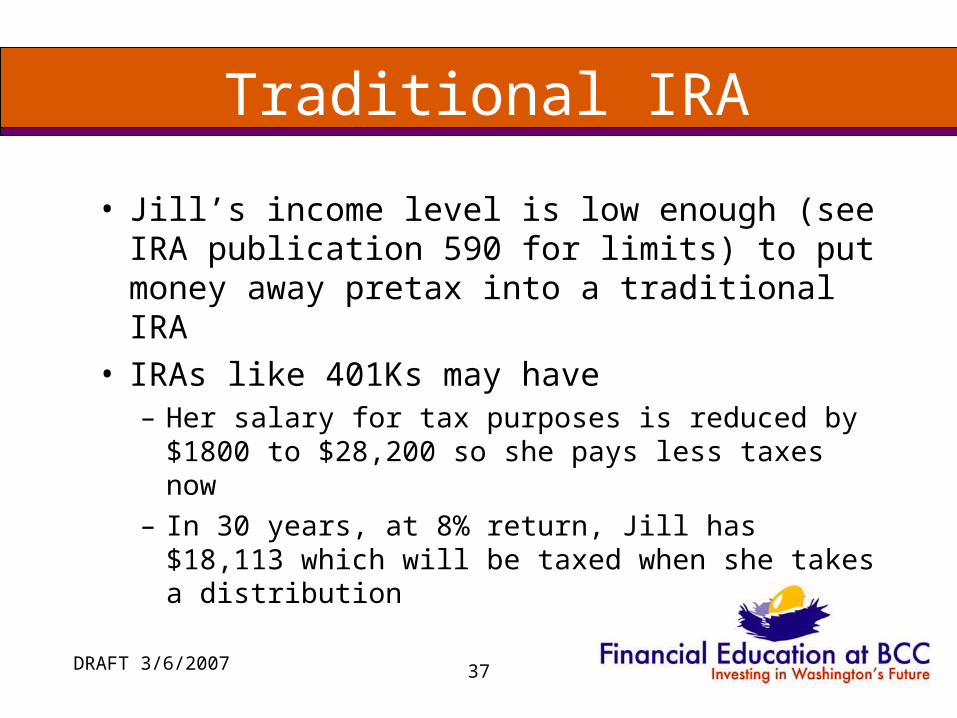

Traditional IRA

• Jill’s income level is low enough (see IRA publication 590 for limits) to put money away pretax into a traditional IRA

• IRAs like 401Ks may have – Her salary for tax purposes is reduced by $1800 to

$28,200 so she pays less taxes now– In 30 years, at 8% return, Jill has $18,113 which

will be taxed when she takes a distribution

DRAFT 3/6/2007 38

Roth IRA

• Jill’s income level is low enough to put money into a Roth IRA (see IRS publication 590 for limits)– Her salary is not reduced so she has no

tax savings now– In 30 years, at 8% return, Jill has $18,113

which will be NOT be taxed when she takes a distribution

DRAFT 3/6/2007 39

401K

• Jill puts 6% ($1800) in a 401K. Her company matches up to 50 cents for every dollar the employee contributes up to 6%.

– Her salary for tax purposes is reduced by $1800 to $28,200 so she pays less taxes now

– Her company matches 3% of $900 so the total contribution is $2700

– In 30 years, she will have $27,169 which will be taxed when she takes it out

DRAFT 3/6/2007 40

401K, IRA or Roth IRA for Jill?

• If a company matches, 401K is best up to the maximum of the match

• If your tax rate is low now and higher when you retire or you want more flexibility on your distribution, the Roth IRA is the next best

DRAFT 3/6/2007 41

Risks with 401K

• 18% to 25% of employees don’t participate or contribute

• About half of those under 25 contribute

• Participants don’t know how to allocate assets (100% company stock is a risk)

• When people leave company they cash out their 401Ks instead of rolling it over

DRAFT 3/6/2007 42

401K Checklist

• Max out employer contribution

• Monitor asset allocation

• Ask about fees

• Always roll over when leaving a company

IRA

• You can contribute up to what you earn for the year

• Roth IRAs are best if your tax rate is low

• When you leave a company, make sure that you roll over your savings to a IRA – keep it separate

DRAFT 3/6/2007 43

DRAFT 3/6/2007 44

Issues in retirement planning

• It’s up to you and not your employer – save in a tax-advantaged way

• How much should you save? Lots of opinions but 10% to 15% a year will be a good safety net

• Don’t cash out retirement savings – it costs you a lot

• Don’t borrow on your 401k—it costs you too

45

401K Roth IRA Traditional IRA

Who is eligible Determined by employer. Anyone who had income from working and his or her nonworking spouse.

There are income limits.

Anyone up with age 70 ½ with income from working and his or her nonworking spouse. There are no income limits.

Maximum you can contribute

$15,500 (2008 with cost of living after that) or maximum set by employer. $5000 catch-up contribution for those 50 and over.

Your employer may contribute a match which makes this attractive.

$5000 (2008) each with $1000 catch-up contributions for those over 50.

$5000 (2008) each with $1000 catch-up contributions for those over 50.

Tax status of contributions Contributions are pretax. Contributions must be after-tax. Contributions may be pretax up to certain income limits.

Tax status of earnings Earnings are tax deferred. You pay ordinary income tax when you take the money out therefore missing out on lower capital gains tax.

Earnings are tax free. Earnings are tax deferred. You pay ordinary income tax when you take the money out therefore missing out on lower capital gains tax.

Withdrawals Withdrawals made before age 59 ½ will be subject to a penalty of 10% in addition to tax.

Contributions may be withdrawn without penalty.

Earnings can be withdrawn without penalty for some expenses.

Withdrawals made before age 59 ½ will be subject to a penalty of 10% in addition to tax.

Mandatory age for withdrawals

70 1/2 None 70 1/2

http://www.irs.gov/publications/p590/ar01.html#d0e124 for the latest limits.

Unit 3: Investments

DRAFT 3/6/2007 46

DRAFT 3/6/2007 47

Understanding Returns

DRAFT 3/6/2007 48

A real life example

• You will get your paycheck next week but you need $100 now. You arrange for a payday loan paying a fee of $15 for the use of $100. The payday loan company will collect the $100 electronically from your bank account when your pay check is deposited next week. What is the rate charged?

Income investments

• Invest only in instruments you understand

• Most investors start off with income investments such as certificates of deposit or bonds

49

Certificate of Deposits• Invest a fixed amount of money (principal) in a CD.

Your principal is guaranteed plus a fixed amount of interest:– Receive interest monthly, quarterly or at maturity.– You will incur penalty fees for withdrawing your money early before

the term expires (before it reaches the maturity date).

• CDs can be purchased through banks, credit unions or brokerages. CD considerations are:– Time period (maturity date)– Interest yield includes the effect of compounding interest rate and is

usually higher than the interest rate of statement savings accounts.– Interest payments may be withdrawn as they are paid by the bank– CDs are insured by the FDIC or NCUA up to $100,000 ($250,000 on

retirement accounts)

50

Bond Primer

• Similar to CDs in that interest (yield) is paid usually semiannually

• Has a maturity, however may be redeemed before maturity.

• May be sold before maturity.

DRAFT 3/6/2007 51

Primer on bonds

52

Capital gain or loss on bonds

53

Stocks

• When you own a share of common stock, you own a share of the company.

• Owning stock is also referred to as owning equity or having a shareholder stake since you are a shareholder in the company.

• Stocks are historically much more volatile than bonds in that their prices can go up and down much more.

DRAFT 3/6/2007 54

Annual Stock Price Changes from 1900 to 2006(Percent change year to year in S&P 500)

-55%

-35%

-15%

5%

25%

45%

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000

Other investments• Real Estate - can be broken down into residential (places where people live)

and commercial (office buildings, shopping centers, hotels, warehouses, manufacturing facilities, and such). Estimates of worldwide value of commercial real estate is $14 trillion with the US having about $4.7 trillion.

• International -The 51 stock exchanges in the World Federation of Exchanges accounted for companies with $61 trillion in market value at the end of 2007. Over the past ten years, US exchanges and those of developed countries in Europe and the rest of the world accounted for less growth than markets in emerging economies such as China, India, and Latin America.

• Commodities - Commodities are raw materials such as oil, agricultural products such as wheat, cocoa or pork bellies, metals such as silver, gold, or copper. Commodities also include currencies, Treasury securities, and stock indexes. Speculators typically buy and sell commodities with options and futures contracts on an exchange.

DRAFT 3/6/2007 55

DRAFT 3/6/2007 56

Investment Risk

DRAFT 3/6/2007 57

Major asset classes: Risk & Return

Index Funds (2007) Average Return %

Risk %

Emerging markets are international stocks of developing countries

42 18

European large stocks 25 10

International stocks of developed countries 23 9

Real estate 22 17

Small cap stock - Small US companies $300 M to $2 B

15 12

Mid cap stock - companies $1.5B to $5 B 16 10

S&P 500 - Largest US stocks 13 8

Bonds 4 3

DRAFT 3/6/2007 58

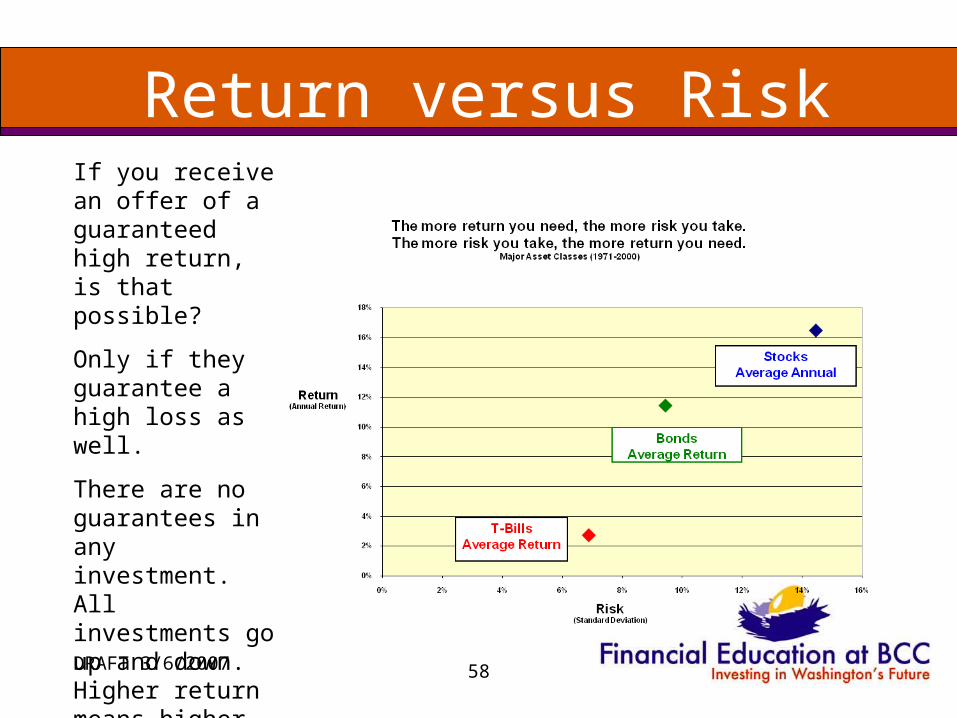

If you receive an offer of a guaranteed high return, is that possible?

Only if they guarantee a high loss as well.

There are no guarantees in any investment. All investments go up and down. Higher return means higher risk.

Return versus Risk

DRAFT 3/6/2007 59

Given the same return, the investment with less risk is better

DRAFT 3/6/2007 60

The Northwest is the best.

DRAFT 3/6/2007 61

Combined – Risk Return

DRAFT 3/6/2007 62

Year-to-year stock returnsAnnual Stock Price Changes from 1900 to 2006

(Percent change year to year in S&P 500)

-55%

-35%

-15%

5%

25%

45%

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000

DRAFT 3/6/2007 63

Risk gets lower with time

Average Previous Five Years S&P 500 Gains

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000

DRAFT 3/6/2007 64

Lowest risk over ten yearsAverage Previous Ten Years S&P 500 Gains

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000

DRAFT 3/6/2007 65

Summary

• All investments have risk• Buy and hold market index funds

(doesn’t work for individual stocks)• Have an emergency fund (3 to 6 months)

to tide you over• Have other sources of income so you

don’t have to cash out during down markets

DRAFT 3/6/2007 66

Asset Allocation

DRAFT 3/6/2007 67

All eggs in one basket?

• 34.6 percent of families had stock in only one company

• 59.5 percent had stock in three or fewer companies

• 9.5 percent had stock in fifteen or more companies

Source: 2004 Consumer Finance Survey

DRAFT 3/6/2007 68

Why asset allocate?

• It has to do with return and risk

DRAFT 3/6/2007 69

Can you predict the best return?

DRAFT 3/6/2007 70

Does the risk double with two investments?

The key is having two

investments which aren’t correlated.

DRAFT 3/6/2007 71

Adding a riskier investment to your portfolio decreases overall risk.

DRAFT 3/6/2007 72

If you allocate the right amount you reduce risk and increase return!

DRAFT 3/6/2007 73

Pension Fund Asset Allocation

DRAFT 3/6/2007 74

“Millionaires” Portfolio

75

David Swensen suggests a portfolio

Summary

• Don’t put all your eggs in one basket.

• Rebalance every year to keep your portfolio on track.

DRAFT 3/6/2007 76

Funds

DRAFT 3/6/2007 77

Unit 5: Selecting funds

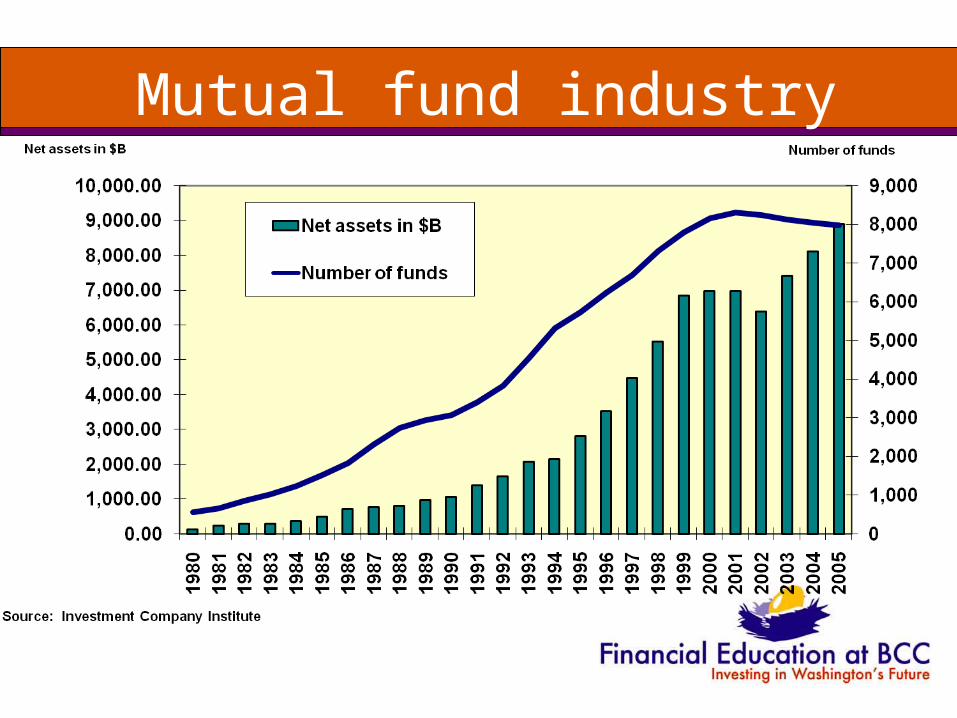

Types of funds

• Mutual funds

• Closed-end funds

• Exchange-traded funds (ETFs)

Mutual fund industry

Closed-end funds

ETFs

Evaluating funds

9/12/07 82

Objective Relates to your asset allocation goals Check the portfolio to be sure

Fees The lower the better – check against index funds

Performance How does it do against the index? How does it do against other

funds?Risk

Is it lower risk than other funds?Management

If you are choosing an actively-managed fund – how experienced is the manager?

www.morningstar.com or www.marketwatch.com for Lipper

9/12/07 83

www.morningstar.com

9/12/07 84

9/12/07 85

9/12/07 86

9/12/07 87

9/12/07 88

9/12/07 89

9/12/07 90

9/12/07 91

9/12/07 92

9/12/07 93

9/12/07 94

9/12/07 95

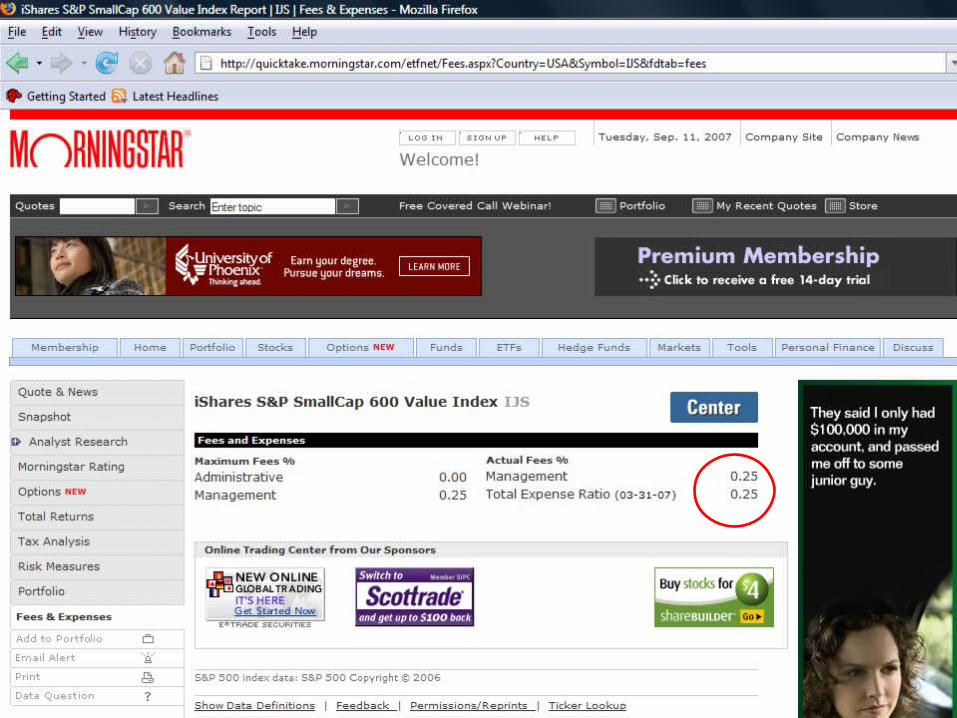

Fund Fees True or False?

96

• All fund fees are charged when you buy.• All fund fees have the same effect.• A no-load fund has no fees.• All funds should have the same level of

fees and expense ratios.• Expense ratios are such a small part of

your investment you shouldn’t worry about them.

Index Funds

• Index funds are funds that represent certain categories of assets

• There are index funds for large, medium and small stocks, international stock, bonds, industries, real estate, commodities, and more.

• They are not actively managed. Their investments don’t change.

DRAFT 3/6/2007 97

Beating the indices -- negatively

9/12/07 98

Source: Statement of John C. Bogle to the United States Senate Governmental Affairs Subcommittee, November 3, 2003

How fees (negatively) impact your return

9/12/07 99

Source: Statement of John C. Bogle to the United States Senate Governmental Affairs Subcommittee, November 3, 2003

DRAFT 3/6/2007 100

Evaluate your fund performance/fees against index funds performance/fees

9/12/07 101

Mutual Fund Category

Index FundExpense Ratio %

All Funds Expense Ratio

%

Emerging markets are international stocks of developing countries 0.77 1.77

European large stocks 0.6 1.64International stocks of developed countries 0.35 1.65

Real estate 0.35 1.46Small cap stock - Small US companies $300 M to $2

B 0.2 1.41

Mid cap stock - Medium-sized US companies $1.5B to $5 B 0.2 1.39

S&P 500 - Largest US stocks 0.09 1.25

Bonds 0.2 1.05

9/12/07 102

Unit 6: When to buy and sell

Bond/CD Laddering

Bond laddering is buying income investments over many periods rather than just at one time.

The advantages of a bond ladder (or CD ladder) are:

• You will have a mixed yield portfolio of bonds coming due in the short and long term, which will give you a better current bond yield.

• If interest rates go up, you will have a bond maturing shortly that you can reinvest at a higher interest rate for another five year term.

• If interest rates drop, only a small portion of your portfolio (the one-year bond maturing) would be reinvested at the lower rate.

• You can match your cash needs with how long you make the bond ladder by deciding the type of bond for the ladder.

Be careful how you build your bond ladder. Here are some suggestions to keep in mind:

• The longer the maturity, the higher your yield but the risk will be greater.

• For your bond ladder, the more rungs on your ladder, the more diversified your investment portfolio will be.

DRAFT 3/6/2007 103

Bond Ladder

DRAFT 3/6/2007 104

The effect – not always better

Lump sum

Ladder

1980 10.7% 100000 200001981 12.8% 200001982 14.7% 200001983 10.0% 200001984 11.4% 200001985 10.9% 20000At maturity 153700 190490

DRAFT 3/6/2007 105

Rebalancing

DRAFT 3/6/2007 106

Do we buy at the right time?

DRAFT 3/6/2007 107

Rebalancing

• Adjusting portfolio based on asset allocation goals

DRAFT 3/6/2007 108

No rebalancing

DRAFT 3/6/2007 109

Year Bond Stock1992 40% 60%1993 40% 60%1994 39% 61%1995 35% 65%1996 32% 68%1997 27% 73%1998 24% 76%1999 21% 79%2000 24% 76%2001 28% 72%2002 36% 64%2003 31% 69%2004 30% 70%2005 29% 71%2006 27% 73%

Rebalancing

DRAFT 3/6/2007 110

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

No action

Rebalanced

Final Value - No Action Portfolio $376,353Final Value Rebalance Portfolio - $381,608

DRAFT 3/6/2007 111

Advice from the prosDavid Swensen who manages the Yale University endowment, and who is

considered one of the best investment managers, has sobering advice to give to individual investors:

• Individuals shouldn’t pick stocks themselves. The markets are competitive and they don’t have the information to compete nor the clout to negotiate.

• Beware of actively-managed mutual funds. They allow popular funds to grow too big so they can’t beat the market. They also tend to promote the wrong fund at the wrong time. The vast majority of actively-managed funds underperform the market.

• Mutual fund monitoring companies don’t help you either. They downgrade funds after the damage has been done.

• Individuals are best served by index funds with the lowest fees.

• Have a diversified portfolio and rebalance.

Investor FraudUnit 6: Protect your wealth

113

Choosing a financial advisor

• Comparison shop - talk to people at several firms. Meet with them face to face at their offices. Make a list of questions to ask. Get a copy of their Form ADV.

• Qualifications - What is the advisor’s education? What certification does he or she have? Does it relate to financial knowledge? Ask about their clients. How many clients do they have? How long do clients stay with them? What are the total assets they are advising on? What is the average portfolio of their clients? Make sure you fit the profile.

• Style: Ask if the advisor or an assistant will handle your portfolio. Ask for at least three references. Do you feel comfortable with the advisor? Investing is a very personal activity. Does the advisor’s investing style match yours? You need to feel that the advisor is working in your best interest.

• Disclosure - Make sure that you have complete disclosure of any fees and the commission schedule. Ask if there is any potential conflict of interest. Get this all in writing.

Investment Fraud

• Investment fraud criminals use a wide array of influence tactics.

• Research done by the National Association of Securities Dealers on transcripts from phone calls of these con artists found 1,100 separate uses of the influence tactics in 128 transcripts.

• First the con artist identifies victims and then cases out the potential victim. They establish that the victim has money. Then they create the “ether” or the state where the victim is susceptible to the fraud.

Commonly Used Influence Tactics

• Phantom Fixation – The con puts something that is completely unavailable before the victim. Often it appeals to health issues, wealth, popularity or avoiding death. The amount of money that they claim you can earn is astronomic. For example, earn $30,000 a month.

• Commitment – “You can vote to stop drilling, but if you do, all the rest of what you have invested will be lost.”

• Authority – “I have been in the oil business for over 30 years and I have seen it all.”

• Social Proof – Everyone is getting in on the offer• Scarcity including product scarcity (only three left) and time

scarcity (offer good only today)

Other influence tactics

• Comparison – Inflated “regular” price• Profiling – Probe for information and then customizes

pitch• Friendship – Changes the relationship from con to

victim to friend to friend• Reciprocity – Does favor so you will return favor

(gifts, free lunch, etc.- with gift response rate goes from 17% to 36%)

• Landscaping – changes social interaction so it lead to where the con wants to go by setting the agenda, limiting choices or controlling information.

www.dfi.wa.gov

• If it sound too good to be true, it is.

• Don’t invest in anything you don’t understand.

• Check out your investment advisor and your investments at www.dfi.wa.gov

• Report any suspicious activity right away.

Activity

• Similar to a will that outlines your wishes for your children, what are the most important financial lessons you want to pass onto your children? When would you start teaching them these concepts?

DRAFT 3/6/2007 118