Embed Size (px)

Citation preview

1

Partnership Dissolution

2

Introduction A partnership may dissolve due to disagreement

among the partners, poor performance of the firm or being taken over by another business.

The assets of the partnership will be realized to pay off the liabilities.

The sales proceeds should be applied in the following order, as required by the Hong Kong Ordinance: Pay off creditors first, then the partners’ advances, and Finally the partners’ capital

3

Realization Account

In the partnership dissolution, an account named as ‘Realization Account’ will be opened to compute the profit or loss from realization which should be shared among the partners according to the profit or loss sharing ratio

4

Nature of partnership dissolution

Dissolution where the assets are sold separately

Dissolution where partnership is sold as a whole

5

Dissolution where Assets are sold

separately

6

Procedures of Dissolution

1. All assets will be sold to other persons or taken over by partners

2. Settle the liabilities of the partnership to outsider or partners

3. Transfer any ‘profit or loss on realization’ to each partner’s capital accounts in profit/loss sharing ratio

4. Merge the balances in the partners’ current accounts to their capital accounts

7

5. Any credit balance in each partner’s capital account represents the amount which can be withdrawn from the partnership to each partner; any debit balance in a partner’s capital account represents additional cash to be injected by that partners

8

Transactions Accounting entries

Close all asset accounts with net book value to the realization account (except cash and bank because these assets need not be disposed of)

Dr Realization

Cr Assets

Cost of dissolution or any losses or expenses incurred on realization

Dr Realization

Cr Bank

Proceeds from the disposal of assets

Dr Bank

Cr Realization

Assets taken over by a partner without payment

Dr Capital

Cr Realization

9

Transactions Accounting entries

Asset taken over by partners as a gift

No entries required

Creditors taken over by a partner

Dr Creditors

Cr Capitals

Payment to creditors with discounts received

Dr Creditors

Cr Realization – discount

Cr Bank

Profit or loss on realization to be shared among the partners according to the profit-sharing ratio

Dr Realization – profit

Cr Capitals

or

Dr Capital

Cr Realization - loss

10

Transactions Accounting entries

Repayment of loan to an partner

Dr Loan from partner

Cr Bank

Repayment of loan to an outsider ( creditors)

Dr Loan from outsider

Cr Bank

Transfer any balances in partners’ current accounts

Dr Current (for credit balance)

Cr Capitals

Or

Dr Capital

Cr Current (for debit balance)

Repayment of remaining capital to partners

Dr Capital

Cr Bank

11

Example 1

12

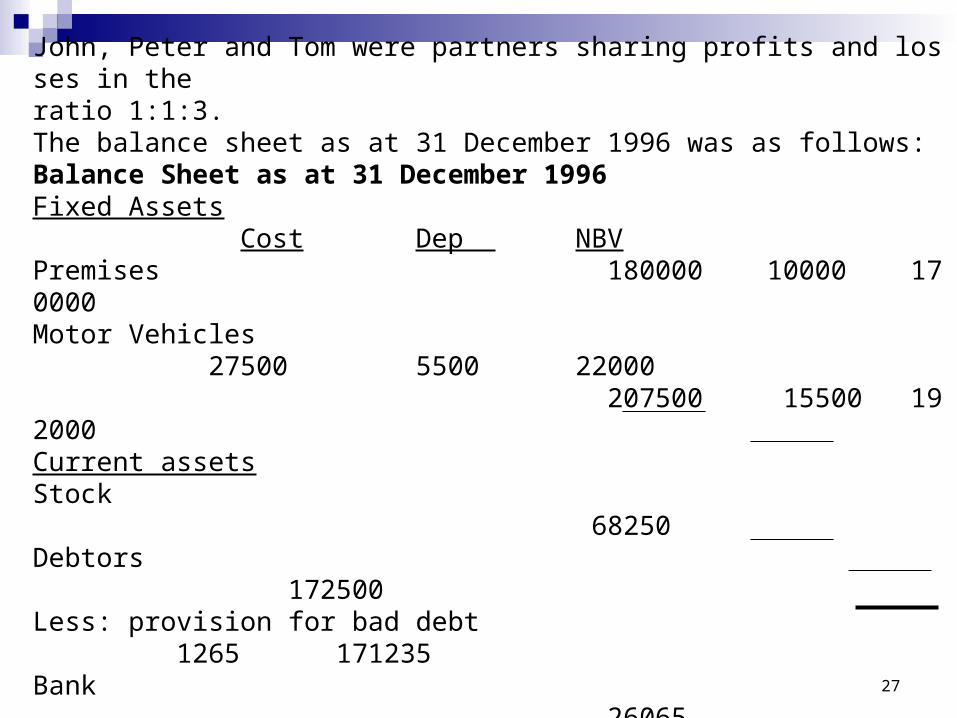

John, Peter and Tom were partners sharing profits and losses in the ratio 1:1:3. The balance sheet as at 31 December 1996 was as follows:Balance Sheet as at 31 December 1996 Fixed Assets Cost Dep NBVPremises 180000 10000 170000Motor Vehicles 27500 5500 22000

207500 15500 192000Current assetsStock 68250Debtors 172500Less: provision for bad debt 1265 171235Bank 26065 265550Less: Current LiabilitiesCreditors 60000Working Capital 205550 397550

13

Capital: John 100000 Peter 40000 Tom 160000 300000Current: John 30000 Peter (10000) Tom 70000 90000Long – term liabilitiesLoan from Tom 7550 397550

Assets and liabilities were disposed of as follows:1. The premises were sold at $ 200000 and legal charges from the

sale amount to $100002. Tom took over the stock and motor vehicles at book value3. Except for $2500, all debts were collected4. The creditors were discharged for $560005. Realization expenses of $10000 were paid

Required:Prepare the realization, Bank, Capital and Current account for the dissolution of partnership

14

Realization

Premises

Provision for depreciation

Bal b/f 180000 Prov. for depreciation 10000Realization 170000

180000 180000

Bal b/f 10000Premises 10000

Premises 170000

15

Realization

Motor Vehicles

Provision for depreciation

Bal b/f 27500 Prov. for depreciation 5500Realization 22000

27500 27500

Bal b/f 5500Motor Vehicles 5500

Premises 170000Motor Vehicles 22000

16

Realization

Debtors

Provision for Bad Debts

Bal b/f 172500 Prov. for bad debts 1265Realization 171235

172500 172500

Bal b/f 1265Motor Vehicles 1265

Premises 170000Motor Vehicles 22000Debtors 171235

17

Realization

StockBal b/f 68250 Realization 68250

Premises 170000Motor Vehicles 22000Debtors 171235Stock 68250

18

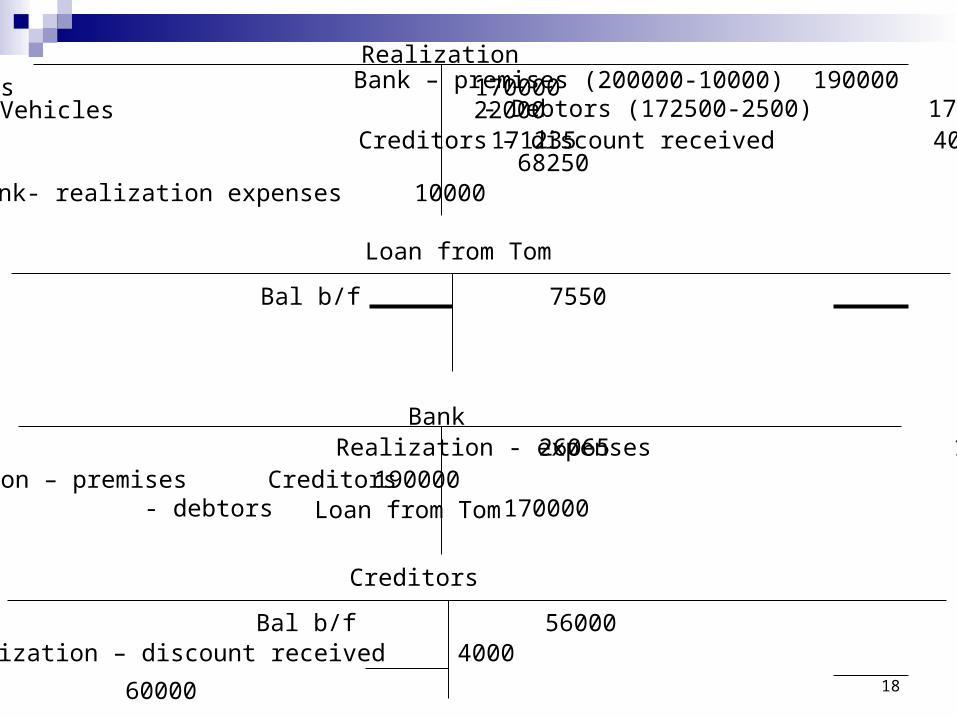

Realization

BankBal b/f 26065 Realization - expenses 10000

Premises 170000Motor Vehicles 22000Debtors 171235Stock 68250Bank- realization expenses 10000

Bank – premises (200000-10000) 190000 - Debtors (172500-2500) 170000

Realization – premises 190000 - debtors 170000

Creditors

Bal b/f 60000Bank 56000Realization – discount received 4000

60000 60000

Creditors – discount received 4000

Creditors 56000

Loan from Tom

Bal b/f 7550Bank 7550

Loan from Tom 7550

19

RealizationPremises 170000Motor Vehicles 22000Debtors 171235Stock 68250Bank- realization expenses 10000

Bank – premises (200000-10000) 190000 - Debtors (172500-2500) 170000Creditors – discount received 4000

CapitalJohn Peter Tom John Peter Tom

Bal b/f 100000 40000 160000Realization: Stock 68250 MV 22000

Tom – stock 68250 - MV 22000

Gain on realization: John 1/5 2553 Peter 1/5 2553 Tom 3/5 7659 12765

454250 454250

Gain on realizaiton 2553 2553 7659

20

CapitalJohn Peter Tom John Peter Tom

Bal b/f 100000 40000 160000Realization: Stock 68250 MV 22000

Gain on realizaiton 2553 2553 7659

CurrentJohn Peter Tom John Peter Tom

Bal b/f 30000 - 70000Bal b/f 10000Capital 10000Capital 30000 70000

30000 10000 70000 30000 10000 70000

BankBal b/f 26065 Realization - expenses 10000Realization – premises 190000 - debtors 170000

Creditors 56000Loan from Tom 7550Capital: John 132553 Peter 32553 Tom 147409

386065 386065

Current 30000 70000Current 10000Bank 132553 32553 147409

132553 32553 147409 132553 32553 147409

21

Dissolution where partnership is sold as a whole

22

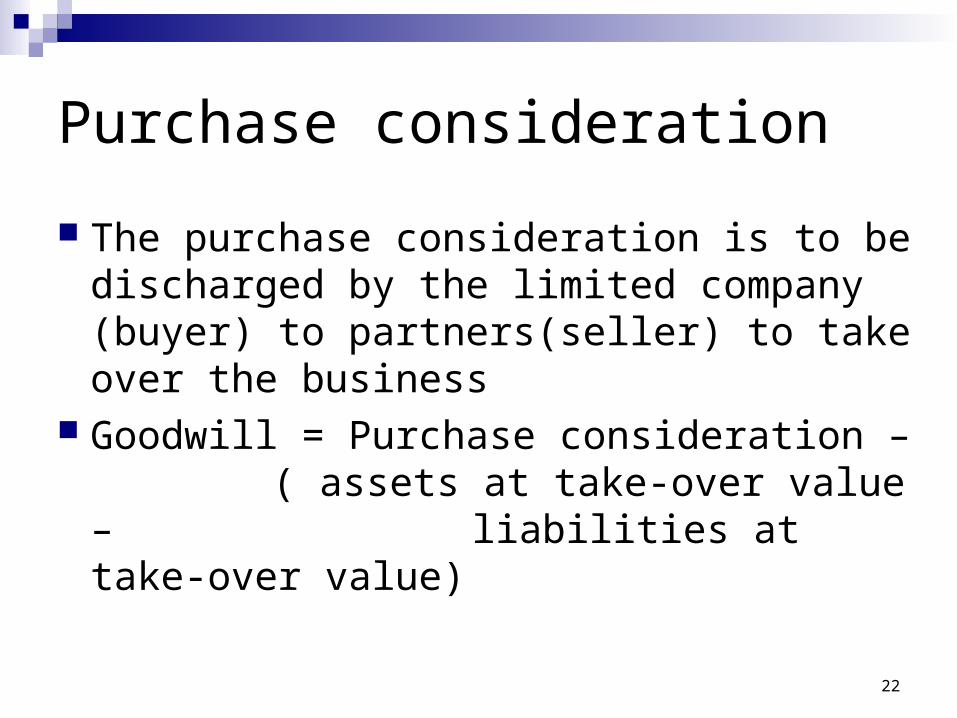

Purchase consideration

The purchase consideration is to be discharged by the limited company (buyer) to partners(seller) to take over the business

Goodwill = Purchase consideration – ( assets at take-over value – liabilities at take-over

value)

23

Transactions Accounting entries

For dissolution of Old partnership (seller)

Close all asset accounts with net book value to the realization account (Bank and cash may be taken over)

Dr Realization

Cr Assets

Cost of dissolution or any losses or expenses incurred on realization

Dr Realization

Cr Bank

Proceeds from sale of the business (purchase consideration)

Dr Vendee (buyer)

Cr Realization

24

Transactions Accounting entries

Liabilities taken over by the buyer

Dr Liabilities

Cr Realization

The purchase consideration settled by cheque, shares and debentures

Dr Bank/ Shares/ debentures in purchaser’s company

Cr Bank

Repayment of remaining capital to partners

Dr capital

Cr Bank/ shares/ debentures in purchaser’s company

25

Transactions Accounting entries

For opening entries of New Company (buyer)

Assets taken over Dr Assets

Cr Business Purchase

Liabilities taken over Dr Business Purchase

Cr Liabilities

The purchase consideration offered

Dr Business Purchase

Cr Vendor (seller)

The purchase consideration settled by cheques, shares and debentures

Dr Vendor (seller)

Cr Bank/Shares/Debentures

26

Example 2

27

John, Peter and Tom were partners sharing profits and losses in the ratio 1:1:3. The balance sheet as at 31 December 1996 was as follows:Balance Sheet as at 31 December 1996 Fixed Assets Cost Dep NBVPremises 180000 10000 170000Motor Vehicles 27500 5500 22000

207500 15500 192000Current assetsStock 68250Debtors 172500Less: provision for bad debt 1265 171235Bank 26065 265550Less: Current LiabilitiesCreditors 60000Working Capital 205550 397550

28

Capital: John 100000 Peter 40000 Tom 160000 300000Current: John 30000 Peter (10000) Tom 70000 90000Long – term liabilitiesLoan from Tom 7550 397550

On 31 December 1996, they incorporated a limited company, Fortune limited, to take over the partnership business. Fortune Limited had an authorized capital of $500000 ordinary shares of $1 each.

29

Assets and liabilities were disposed of as follows:1. John took over the stock at book value. Tom collected all the debts except

$25002. The company took over the premises at a valuation of $200000, motor vehicles at $25000, cash at bank and all the liabilities. Goodwill was

valued at $70000 for the purpose of the takeover 3. The purchase consideration was to be discharged by the issue to the

partners of 150000 ordinary shares at $1.2 each, according to the profit-sharing ratio, and the balance was to be in cash

4. The company also issued 50000 ordinary shares at $1.2 for cash to outsiders

Required:Prepare the realization, Capital and the opening balance sheet for the new company

30

Realization

Premises 170000MV 22000Stock 68250Debtors 171235Bank 26065

Bank be taken over Tom: debtors (172500-2500) 170000John: stock 68250

Creditors 60000Loan from Tom 7550

Liabilities taken over by Ltd. Co.

Fortune Ltd – purchase consideration[(200000+25000+26065-7550-60000)+70000] 253515

Purchase consideration=Asset-liabilities +goodwill

Capital: John 20353 Peter 20353 Tom 61059 101765

559315 559315

31

Capital

John Peter Tom John Peter Tom

Bal b/f 100000 40000 160000Current 30000 70000

Current 10000Realization Stock 68250 Debtors 170000

Shares in Fortune Ltd 36000 36000 108000

Realization -profit 20353 20353 61059

Bank 46103 14353 13059(Bal. fig.)

Shares in Fortune Ltd.150000*1.2 = 180000 John 1/5 36000 Peter 1/5 36000 Tom 3/5 108000 180000

150353 60353 291059 150353 60353 291059

32

Fortune LimitedBalance sheet as at 1 Jan 1996

Fixed AssetsGoodwill 70000Premises 200000MV 25000 295000

Current AssetsBank [26065 + (50000*1.2) –(46103+14353+13059)] 12550

Less: Current liabilities Creditors 60000

Working Capital (47450)247550

Share CapitalOrdinary Shares (150000*$1+50000*$1) 200000Share Premium (150000*$0.2+150000*$0.2) 40000

240000

Long-term liabilitiesLoan from Tom 7550

247550

33

Cash distribution among partners

34

Cash Distribution Among Partners

With the application of the Garner vs. Murray rule

When cash is to be distributed as soon as possible ( Piecemeal realization)

35

With the application of Garner vs. Murray rule

36

With the application of Garner vs. Murray rule Any CREDIT balance in each partner’s capital

account represents the amount which can be withdrawn from the partnership to each partner

Any DEBIT balance in a partner’s capital account represents additional cash to be injected by that partner. If he is insolvency to repay the amount, the solvency partners will be shared the amount in: Profit & loss sharing ratio Any agreed ratio given in the examination question GARNER vs. MURRAY rule may be applied

37

What is Garner vs. Murray rule?

38

Garner vs. Murray rule Under the rule, a partner is required to

contribute cash to eliminate the debit balance in his capital account

In the court case of Garner vs. Murray (1904), it was held that subject to any agreement to the contrary, such a debit balance deficiency was to be shared by the other partner not in their profit and loss sharing ratio but “ the ratio of their last agreed capitals”

39

If one partner is insolvent, his capital deficiency will be shared by other partners according to the ‘last agreed capital ratio’ (the ratio of the balances in the capital accounts before the dissolution, in the absence of any agreement to the contrary

40

Piecemeal Realization

41

Piecemeal realization

Cash is distributed as it becomes available, instead of waiting for all the assets to be realized first

Assets are sold piecemeal, and then outstanding debts are paid and the remaining cash is finally distributed to the partners as soon as possible

This situation occurs because some assets can be sold quickly, and some assets take longer time to be sold (i.e. less liquid)

42

Assumed Loss/Notional Loss Method This is possible loss by assuming that the

remaining assets do not have any scrap value

Any unsold assets will be assumed loss in each distribution

43

Steps on Piecemeal Dissolution

1. Find out the maximum possible loss Maximum possible loss

= NBV of assets to be realized - Total proceeds form disposal

OR Maximum possible loss

= Total capital balances - Total cash to be distributed to partners( i.e. cash available)

44

2. The maximum possible loss is shared by the partners according to the profit-sharing ratio

3. Apply the Garner vs. Murray rule if there is any capital deficiency

4. Distribute any available cash to the partners according to their remaining capital balances

5. Repeat the process until all assets have been realized

45

Example 3

46

Au, Chow and Lee were partners sharing profits and losses in the ratio 2:2:1. The balance sheet as at 31 December 1996 was as follows:Balance Sheet as at 31 December 1996 Fixed Assets Cost Dep NBVGoodwill 100000 100000Land 150000 150000Plant & Machinery 133000 55800 77200Fixture & Fittings 30000 13000 17000Motor Vehicles 32000 24000 8000

445000 92800 352200Current assetsStock 64000Debtors 65000Less: provision for bad debt 6000 59000Cash 160 123160Less: Current LiabilitiesCreditors 57000Bank Overdraft 128360Working Capital 62200 290000

47

Capital: Au 120000 Chow 80000 Lee 30000 230000Current: Au 20000 Chow 20000 40000Long – term liabilitiesBank loan 20000 290000

On 31 December 1996 the partners agreed to dissolve the partnership due to a disagreement between the partners. Assets were to be realized, outstanding debts to be paid and the remainder to be shared by the partners in an equitable manner.Distributions of cash were to be made as soon as possible.

January• Provision was made for dissolution expenses of $2400• Land was sold for $200000• The cash available was utilized to settle in full the bank overdraft, the

bank overdraft, the bank loan and all creditors after receiving discounts

48

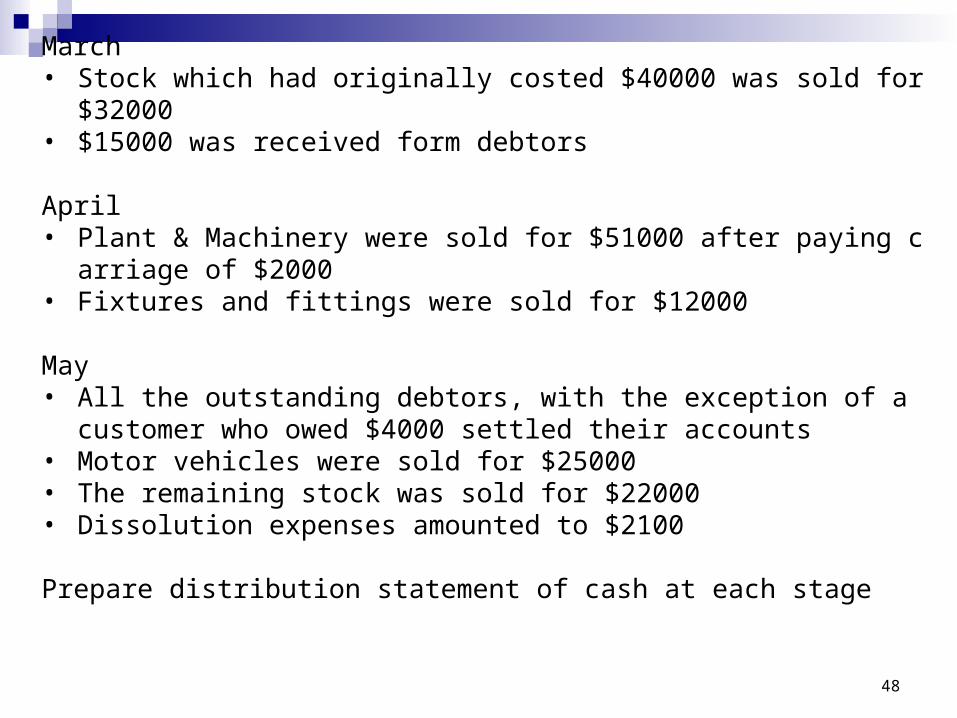

March• Stock which had originally costed $40000 was sold for $32000• $15000 was received form debtors

April• Plant & Machinery were sold for $51000 after paying carriage of $2000• Fixtures and fittings were sold for $12000

May• All the outstanding debtors, with the exception of a customer who owed

$4000 settled their accounts• Motor vehicles were sold for $25000• The remaining stock was sold for $22000• Dissolution expenses amounted to $2100

Prepare distribution statement of cash at each stage

49

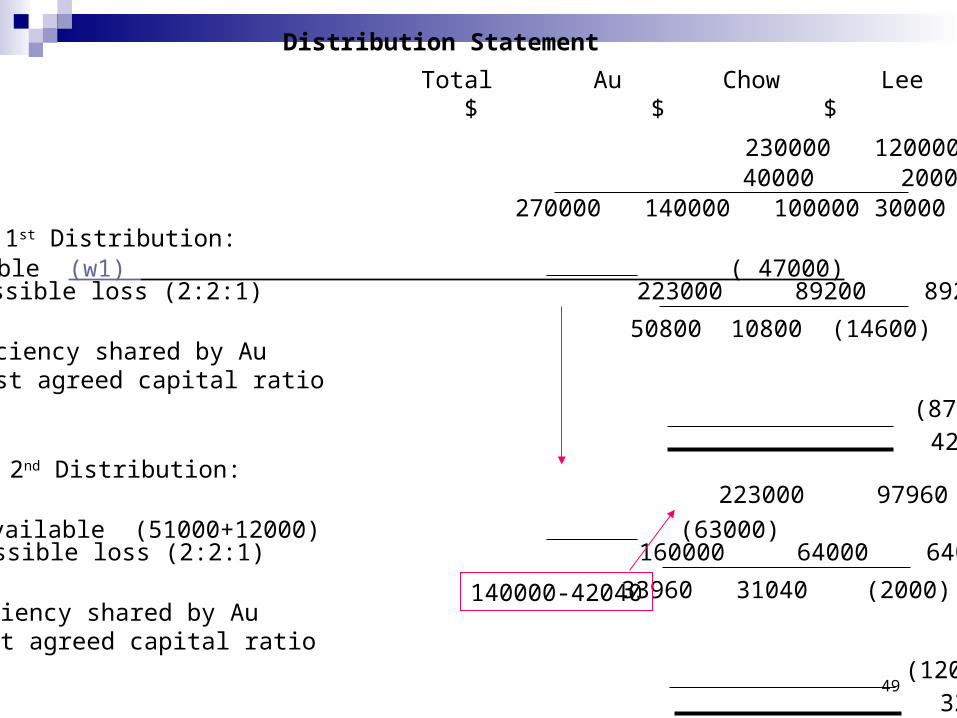

Distribution Statement

Total Au Chow Lee $ $ $ $

Capital accounts 230000 120000 80000 30000Current accounts 40000 20000 20000

270000 140000 100000 300001st Distribution:Cash available (w1) ( 47000)Maximum possible loss (2:2:1) 223000 89200 89200 44600

50800 10800 (14600)Lee’s capital deficiency shared by AuAnd Chow in the last agreed capital ratio(120000:80000) (8760) (5840) 14600

Cash distributed 42040 4960 02nd Distribution:

Cash available (51000+12000) (63000)Maximum possible loss (2:2:1) 160000 64000 64000 32000

33960 31040 (2000)Lee’s capital deficiency shared by AuAnd Chow in the last agreed capital ratio(120000:80000) (1200) (800) 2000

Cash distributed 32760 30240 0

Capital balance 223000 97960 95040 30000

140000-42040

50

3rd Distribution:

Cash available (W2) (93300)Maximum possible loss (2:2:1) 66700 26680 26680 13340

Cash distributed 38520 38120 16660

Capital balance 160000 65200 64800 30000

97960-32760

51

W1 Cash available for 1st distribution: January Opening balance 160

Receipt from land 200000200160

Less: Payment Assumed dissolution expenses 2400

(i.e. not actual expenses) Bank overdraft 128360 Bank loan 20000 Creditors (Bal. Fig.) 49400 200160

0

=> no cash distribution to partners on January

March Receipts: Stock 32000 Debtors 15000

First cash distributed to partners 47000

‘Settle in full’ means no more payment will bepaid. => the difference between 57000 and 49400 is discount received

Back

52

•Very often no cash is distributed to partners at first or second month since outstanding debts must be repaid first and then the remaining cash can then be distributed to partners.

•Even though the questions have not mentioned to repay outstanding debts, you should make sure to keep some cash to prepare to repay debts and could not be distributed it to partners

Notes:

53

W3 Cash available for 3rd distribution: May Receipts

Surplus in dissolution expenses(2400-2100) 300Collection remaining debtors balance (65000-15000-400) 46000Receipts from MV 25000Receipts from remaining stock 22000

93300

Back

54

Realization

Goodwill 100000Land 150000Plant & Machinery 77200Fixtures & fittings 17000Motor Vehicles 8000Stock 64000Debtors 59000

Cash: Land 200000 Stock (32000+22000) 54000 Debtors (15000+46000) 61000 Plant & machinery 51000 Fixture & fittings 12000 Motor vehicles 25000 Creditors – discount rececived (57000-49400) 7600

Capital: Au (2/5) 26680 Chow (2/5) 26680 Lee (1/5) 13340 66700

477300 477300

Cash - dissolution expenses 2100

55

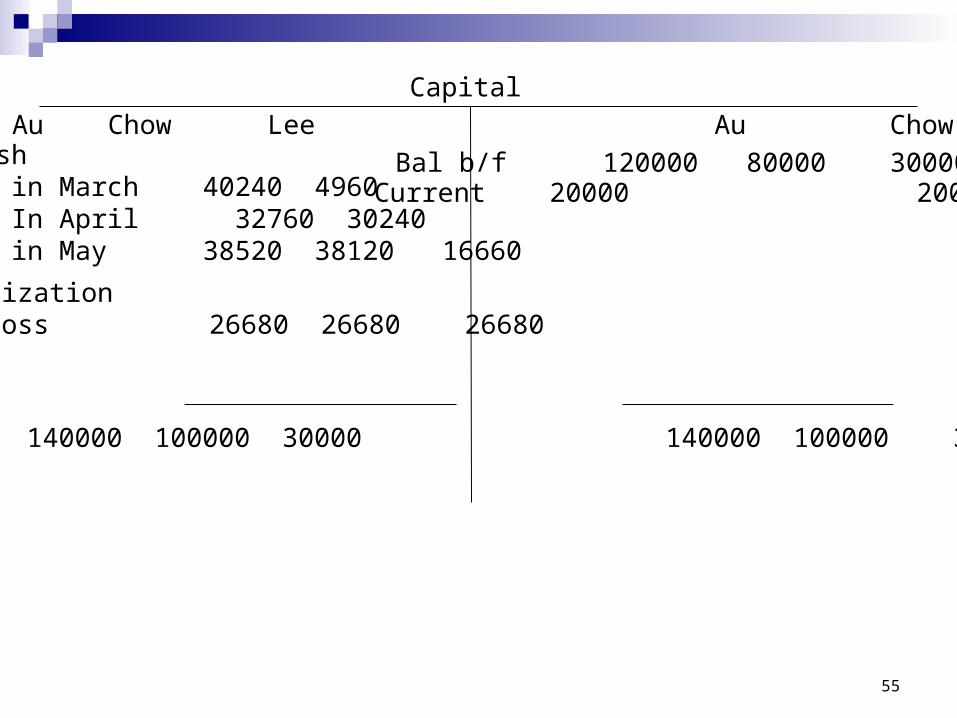

Capital

Au Chow Lee Au Chow Lee

Bal b/f 120000 80000 30000Current 20000 20000

Cash in March 40240 4960 In April 32760 30240 in May 38520 38120 16660

Realization -loss 26680 26680 26680

140000 100000 30000 140000 100000 30000