Embed Size (px)

Citation preview

1

Part IV

The 12 Key Elements of Practical Personal Finance!

2

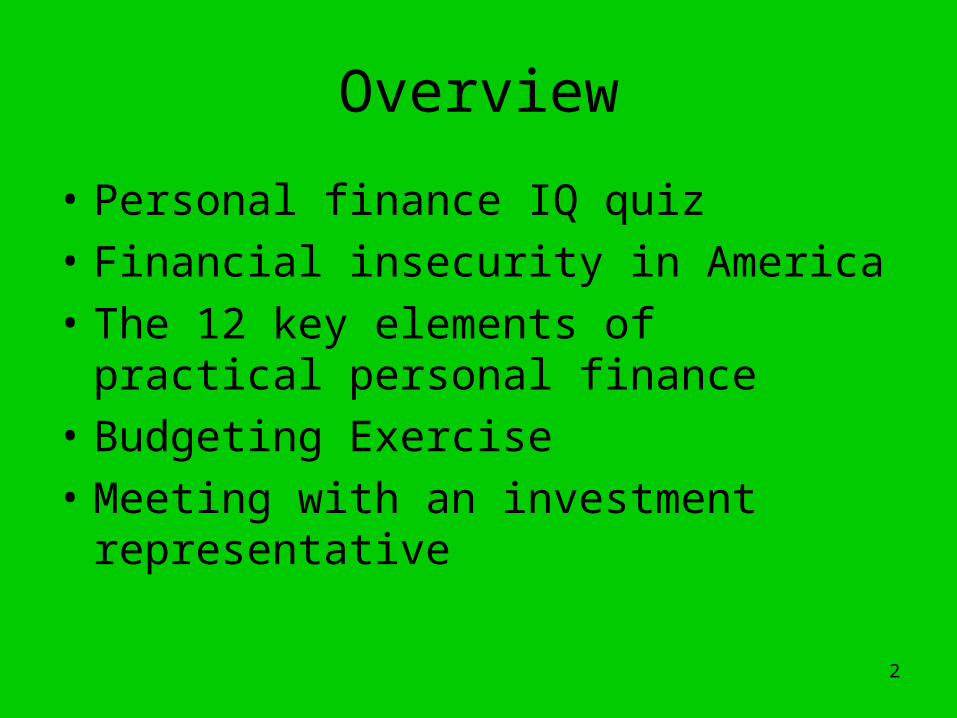

Overview

• Personal finance IQ quiz

• Financial insecurity in America

• The 12 key elements of practical personal finance

• Budgeting Exercise

• Meeting with an investment representative

3

Personal Finance IQ Quiz!

What do you know about personal finance?

4

Financial Insecurity in America

Why is there so much financial insecurity in America?

Is it because our income is so low?

5

Not Really!Real Disposable Income Per Capita

0

5000

10000

15000

20000

25000

30000

35000

1970 1975 1980 1985 1990 1995 2000 2005

Bil

lio

ns o

f 2000 C

hain

ed

Do

llars

6

Consumption per person has also been growing!

Real Disposible and Consumption Per Capita

0

5000

10000

15000

20000

25000

30000

1970 1975 1980 1985 1990 1995 2000 2005

Year

Billio

ns o

f 2000 C

hain

ed

Do

llars

Real Personal Disposible Income Per Capita (2000 Dollars) Real Personal Consumption Per Capita (2000 dollars)

7

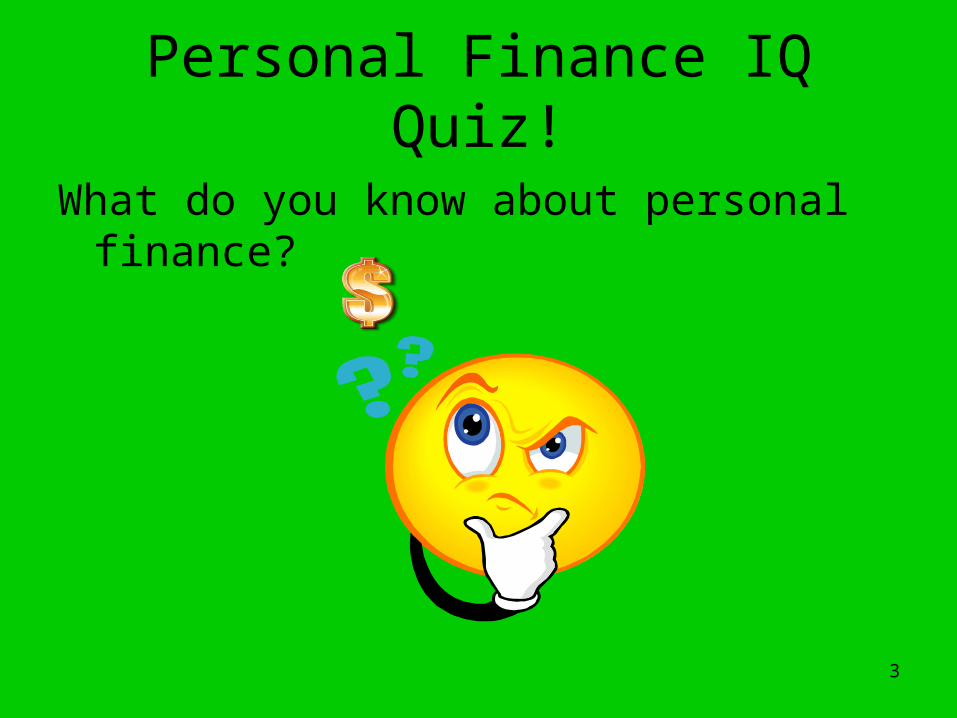

More Consuming + Less Saving = More Debt

As a Percentage of Real Disposable Income

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1970 1975 1980 1985 1990 1995 2000 2005

Savings Rate Consumption Rates

8

Debt Per Household

9

Who needs money when we have credit!

Real Unpaid Credit Card Balance Per U.S. Household (2007 Dollars)

$0

$2,000

$4,000

$6,000

$8,000

$10,000

1970 1975 1980 1985 1990 1995 2000 2005

10

Credit Card Debt!

11

Interest on household debt as a percentage of income

12

Is America in Trouble?

Real income per person is rising, but:

• Savings rate is falling

• Debt is increasing

What can we do?

Is there any escape?

13

Planning for Financial Success!

The bad news:

• Failure to save regularly, conserve wisely, invest strategically, and use credit cards prudently is the major cause of financial insecurity in America

The good news:

• Every one of these things is fixable!

14

The importance of financial security

Financial security leads to:

• Less conflict in marriage

• Better health

• Retirement

• A greater ability to achieve personal goals

15

The Millionaire Mind!

16

The 12 Key Elements of Personal Finance

The following is a list of fundamental steps that are necessary for achieving wealth and financial security into the future

17

#1 Discover your Comparative Advantage

• Discover what you can produce at a lower opportunity cost than other people.

• Don’t just think about money, your opportunity cost includes your personal satisfaction as well!

18

#1 Discover your Comparative Advantage

19

#1 Discover your Comparative Advantage

Start looking for your comparative advantage now!

20

#2 Be Entrepreneurial

• Remember, in market economy, people get rich by helping others and discovering better ways of doing things

21

#2 Be Entrepreneurial

Entrepreneurial talent involves the ability to discover:

a. New products that are highly valued relative to their costs.

The possibilities are endless!

22

#2 Be Entrepreneurial

Entrepreneurial talent involves the ability to discover:

b. Cost-reducing production methods

23

#2 Be Entrepreneurial

24

#2 Be Entrepreneurial

Entrepreneurial talent involves the ability to discover:

c. Profitable opportunities that others over look

Its hard to know what will work….

25

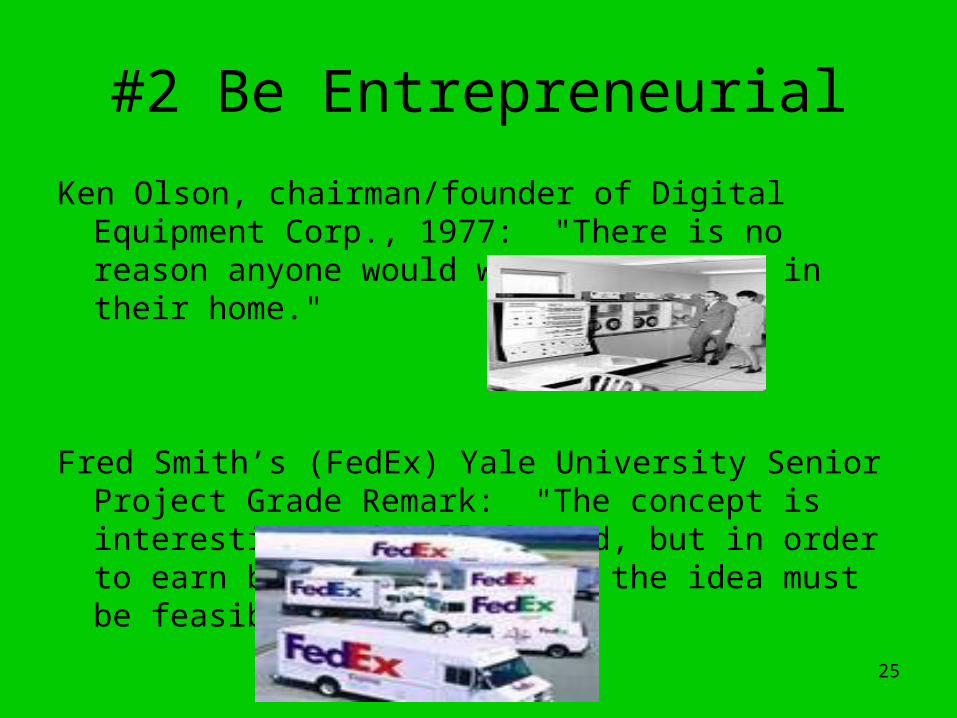

#2 Be Entrepreneurial

Ken Olson, chairman/founder of Digital Equipment Corp., 1977: "There is no reason anyone would want a computer in their home."

Fred Smith’s (FedEx) Yale University Senior Project Grade Remark: "The concept is interesting and well-formed, but in order to earn better than a 'C,' the idea must be feasible."

26

#2 Be Entrepreneurial

Would you have invested?

27

#2 Be Entrepreneurial

Who would have thought….

28

#2 Be Entrepreneurial

Requires the tolerance for risk:• Entrepreneurial activity and self-

employment are riskier than being employed by someone else

• This greater risk can translate into higher income and wealth

29

#2 Be Entrepreneurial

Entrepreneurs tend to:

a. Have high savings rates: they are often reinvesting in their businesses

b. Work long hours and work more strategically

A free market economy tends to promote entrepreneurship….

30

#2 Be Entrepreneurial

31

#3 Spend less than you earn

Savings and Investment is the most likely way that you will become rich

32

#3 Spend less than you earn

Start Saving Now!

1. If you don’t exert the willpower to save now, it is unlikely that you will start later.

33

#3 Spend less than you earn

Start Saving Now!

2. The longer you wait to start saving, the more potential wealth you give up!

You only have to save a little!

34

#3 Spend less than you earn

Start out saving small amounts and then build up to larger amounts:

“A journey of a thousand miles begins with a single step” – Chinese proverb, most commonly attributed to Lao Tzu

35

#3 Spend less than you earn

Save Automatically:• You can have money automatically deducted

from your paycheck or bank account for savings• Include a plan to save in your budget

Save Strategically: Tax Deferred Savings• 401 (k)• Traditional IRA’s• Roth IRA’s

36

#4 Don’t Finance Anything Longer Than Its Useful Life

You don’t want to be paying for things long after your done consuming them.

Three things worth financing:• House

• Education

• Automobiles (in some cases)

37

#4 Don’t Finance Anything Longer Than Its Useful Life

38

#4 Don’t Finance Anything Longer Than Its Useful Life

Things you don’t want to finance:

• Food

• Clothing

• Entertainment

• Vacations

39

#5 Get More Out of Your Money

A. Avoid credit card debt!

a. Interest rates on credit cards are very high (usually higher than savings and investment return rates).

b. Always pay your credit card in full and on time

40

#5 Get More Out of Your Money

B. Consider purchasing used items

a. New cars lose substantial value as soon as they are driven off of the lot.

b. Used cars have higher maintenance costs, but depreciation costs are much lower

41

#5 Get More Out of Your Money

42

#6 Begin paying into a real-world savings account every month

• Things are going to go wrong, its just a matter of when!

• Make contributions to an emergency savings account a regular part of your budget.

43

#7 Harness the Power of Compound Interest

“Mr. Einstein, what is the most powerful force in the Universe?”

“Compound Interest!”

44

#7 Harness the Power of Compound Interest

The Rule of 70: Divide 70 by the expected rate of return and you will see how long it takes for your investment to double

Again, its all about saving early!

45

#8 Diversify

Don’t put all of your eggs in one basket:

Investment involves risk, especially in the short run. Mitigate this risk by building a diversified portfolio.

46

#8 Diversify

Historically, long term returns on stocks have been really good. Just make sure you:

• Hold a large number of unrelated stocks

• Hold stocks for a lengthy period of time.

47

#8 Diversify

The Law of Large Numbers: The tendency, over an increasing number of observations, for the sample average to approach the population average (the expected value).

If you hold a diversified set of stocks, some will do poorly while others will do well so that the rate of return will converge toward the historic average of the stock market

48

#8 Diversify

Avoid Double Jeopardy:

If your company offers you a stock-based retirement program then you may want sell your company’s shares as soon as you are permitted

If you don’t, and the company goes under, then you have lost your job and your investment!

49

#8 Diversify

50

#9 Indexed Equity Funds Can Help You Beat the Experts Without Taking Excessive Risk

Random Walk Theory: Current stock prices reflect all known information about the company, so unforeseeable events is what drives changes in stock prices.

No one person, group of people, or company can predict changes in the stock market.

51

#9 Indexed Equity Funds Can Help You Beat the Experts Without Taking Excessive Risk

Mutual Funds: a professionally managed collective investment scheme that pools money from many investors and channels this money into alternative investments

Many types: money market, equity funds, bonds, etc.

52

#9 Indexed Equity Funds Can Help You Beat the Experts Without Taking Excessive Risk

• Managed equity funds are administered by professionals who research and select stocks in an effort to maximize your return

• Indexed equity funds reflect the holdings of broad indexes such as the Dow Jones and the S&P 500

53

#9 Indexed Equity Funds Can Help You Beat the Experts Without Taking Excessive Risk

Go with indexed funds:

1. The administrative costs of indexed funds are lower than managed funds

2. Historically, the average long-term yield of indexed equity funds has been higher than managed funds

54

#10 For the long-run, invest in stocks; for the

short-run, switch to bonds

Historically, the real return from stocks has been higher than that for bonds.

• Over the long-run, your investment in stocks will be able to ride out the bad times in the market.

55

#10 For the long-run, invest in stocks; for the short-run, switch to bonds

• However, over short time horizons, stocks are risky. As you get older, you should switch a higher proportion of your investment over to bonds which is less risky.

56

#10 For the long-run, invest in stocks; for the short-run, switch to bonds

Bonds do carry some risk:

1. Inflation Risk: Unexpected inflation erodes the purchasing power of the face value of the bond and interest earned

2. Interest Rate Risk: Unexpected increases in interest rates reduce the value of outstanding bonds

57

#10 For the long-run, invest in stocks; for the short-run, switch to bonds

As your time horizon gets shorter, switch to bonds that will mature as you need the money

58

#11 Beware of Investment Schemes Promising High Returns with Little or No Risk

• Remember, there is no such thing as a free lunch!

Principle-Agent Problem:

The incentive problem that occurs when the buyer of services (investor) lacks full information about the circumstances faced by the seller of circumstances (investee).

59

#11 Beware of Investment Schemes Promising High Returns with Little or No Risk

Tips for avoiding investment fraud:

1. Only deal with reputable parties2. Never purchase an investment by phone or email3. Do not allow yourself to be forced into a quick (or any)

decision.4. Do not allow friendship to influence an investment

decision5. Avoid investments that use high pressured marketing

techniques.6. If it looks too good to be true than it probably is

60

#12 Teach Your Children About Money

• Teach your children the value of a dollar

• Help your children develop a good work ethic and savings habit (teach them to save early)

61

#12 Teach Your Children About Money

• Save for your retirement over your children’s education

• Children make bad retirement investments

62

Review

• Understand the causes of the financial insecurity in America

• Know how to effectively budget your money and the importance of saving now for your future.

• Know the 12 Key Elements of Personal Finance:1. Discover your comparative advantage2. Be entrepreneurial3. Spend less than you earn (Save Now!)

63

ReviewKnow the 12 Key Elements of Personal Finance (continued):

4. Don’t finance anything for longer than its useful life.5. Get more out of your money (avoid credit card debt

and buy used)6. Establish a real-world savings account7. Harness the power of compound interest8. Diversify9. Indexed equity funds can help you beat the market10. Invest in stocks for the long run and bonds for the

short run11. Beware of investment schemes promising high returns

and little to no risk12. Teach your children about money (earning and saving)