Embed Size (px)

Citation preview

1

Overview and Mandate

of

The Standing Committee on Appropriations

Musa Zamisa

Phelelani Dlomo

Zandi Hulley

Darrin Arends

Tshepo Masoeu

JULY 2014

PRESENTATION OUTLINE

Topic Presenter

• SCOA’S Main Focal Areas (Budget Approval & Budget Execution) Musa Zamisa

•Common Trends

• Constraints & Advantages

• Budget Cycle Darrin Arends &

• Budget Process Zandi Hulley

• Themes in Budgeting (Global) & (South Africa)

Tshepo Masoeu

• SONA

• Legal Framework- (Parliamentary Oversight & Fiscal Oversight)

• Money Bills Act (Mandate & Examples)

• What needs to happen now

• Important Stakeholders

• Parliamentary Budget Office2

3

UNIQUE FEATURES OF SCOA

Deals with the most important policy instrument

Has an overarching mandate

It is legislated

Has power to accept, reject or amend budgets

Has a coordinating role

SCOA’S MAIN FOCAL AREAS

4

Main focus for the

Committee

5

BUDGET APPROVAL

Sub-stages of Approval

Both in October

6

FOCAL AREAS ON BUDGET DAY

• NDP & MTSF= is the budget aligned to the long term goals?

• SONA= Are priorities, programmes & projects funded?

• ANNUAL REPORTS= does past performance justify current allocation?

• OVERSIGHT REPORTS= does allocation justify actual service delivery?

• PAST EXPENDITURE & PERFORMANCE REPORTS

• STRATEGIC & APP= is the budget linked to plans

7

MAIN INSTRUMENTS & GUIDING QUESTIONS

Is the revenue divided equitably?

Does past performance justify allocation?Financial & service delivery

Are there any major changes in grants?Termination, merger, redesign

FFC is the most important stakeholder by law

8

FOCUS AREAS IN THE DORB

9

BUDGET EXECUTION

TRACK EXPENDITURE

PERFORMANCE

TRACK SERVICE DELIVERY

PERFORMANCE

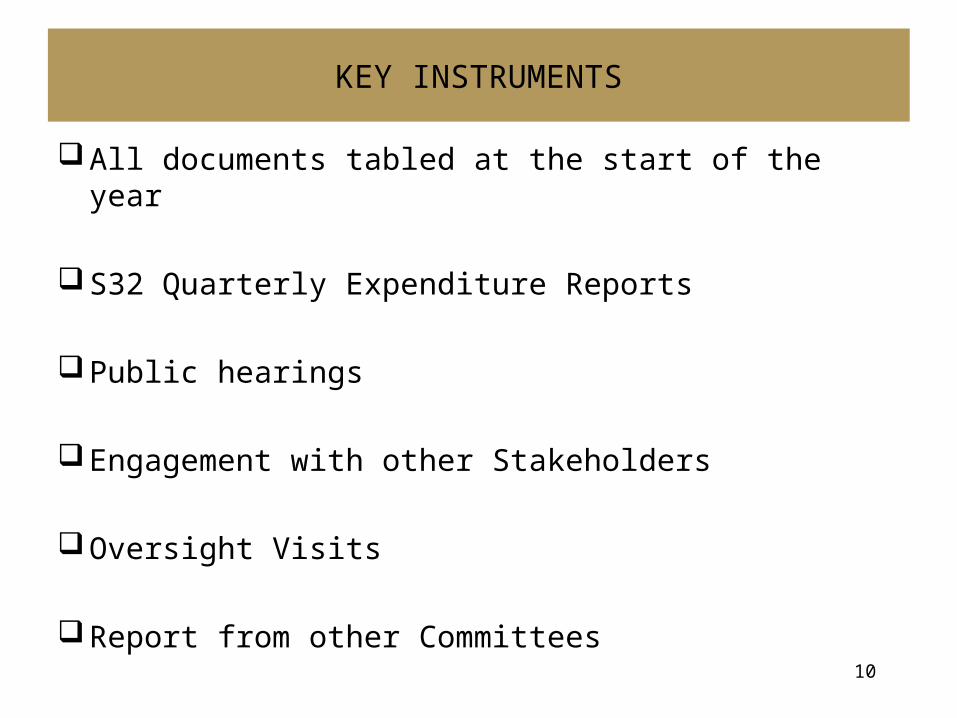

All documents tabled at the start of the year

S32 Quarterly Expenditure Reports

Public hearings

Engagement with other Stakeholders

Oversight Visits

Report from other Committees10

KEY INSTRUMENTS

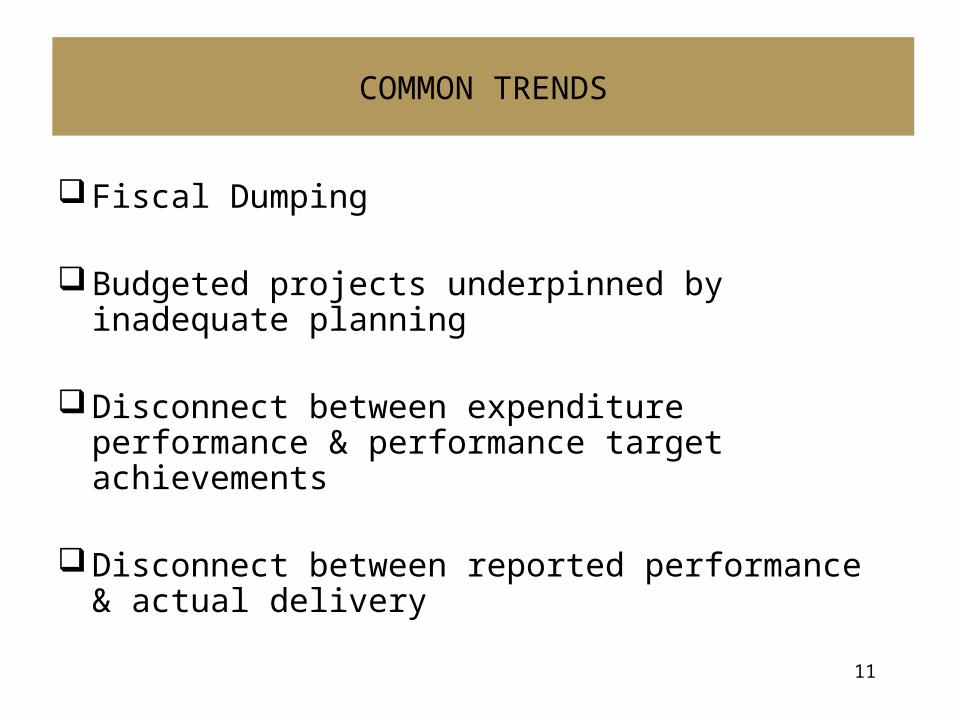

Fiscal Dumping

Budgeted projects underpinned by inadequate planning

Disconnect between expenditure performance & performance target achievements

Disconnect between reported performance & actual delivery

11

COMMON TRENDS

Late receipt of information from departments

Difficulties in Collaboration

Misalignment of financial year

Municipal vs. National & Provincial

Very tight frames in the Act

12

PRACTICAL CONSTRAINTS

No dual mandate any more (FOCUSED)

Benefit of the Parliamentary Budget Office

Evaluation Reports from DPME

Dedicated Support Staff

13

ADVANTAGES GOING FORWARD

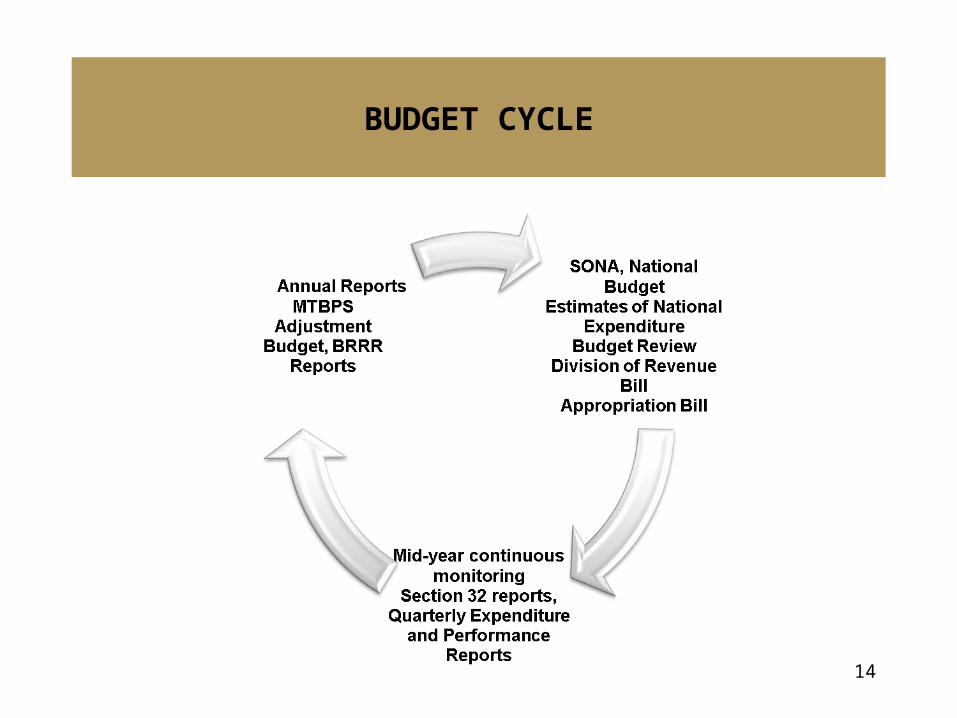

BUDGET CYCLE

14

BUDGET PROCESS

15

THEMES IN BUDGETING (GLOBAL) (1 OF 2)

• Fiscal vulnerabilities are rising in the developing economies. Fiscal positions of many emerging markets may worsen as growth in emerging market economies may be muted in the medium term

• There has been an increase in fiscal spending since the 1990s as a result of the need to expand social services and public investment.

• Three main areas critical for efficient, effective and sustainable government expenditure (IMF Fiscal Report June 2014):

– Ensure sustainability in the largest spending items, public wage bill and social expenditure– Attaining spending efficiencies whilst maintaining an effective service delivery programme– Enhancing the institutional capacity of those state bodies tasked with maintaining spending controls (i.e.

Parliaments, Audit institutions, finance and performance monitoring institutions, etc)

16

THEMES IN BUDGETING (GLOBAL) (2 OF 2)

• Research indicates that efficiency is an increasingly core component of government reforms (OECD Survey 2011)

• IMF surveyed identified 71 cases of fiscal consolidation programs in the last 30 years aimed at reducing budgets, the key finding was that large scale fiscal consolidations are painful, very difficult to innovate while under extreme cost pressure, governments needs to be proactive and improve the efficiency

• Studies suggests four key drivers to systematic efficiency in government :

– Innovate: There needs to be a constant process of innovation. Leading practices need to be identified, adapted and implemented.

– Scale: There needs to be an ability to mandate or provide clear direction for scaling up innovations. Need a governance structure that is responsive to innovation and leading practices.

– Measure: There needs to be a clear focus on performance measurement and analysis. Otherwise efficient practices are less likely to be scaled appropriately.

– Incentives: Governments need tighter sanctions and clearer incentives to drive efficiency at the highest levels.

17

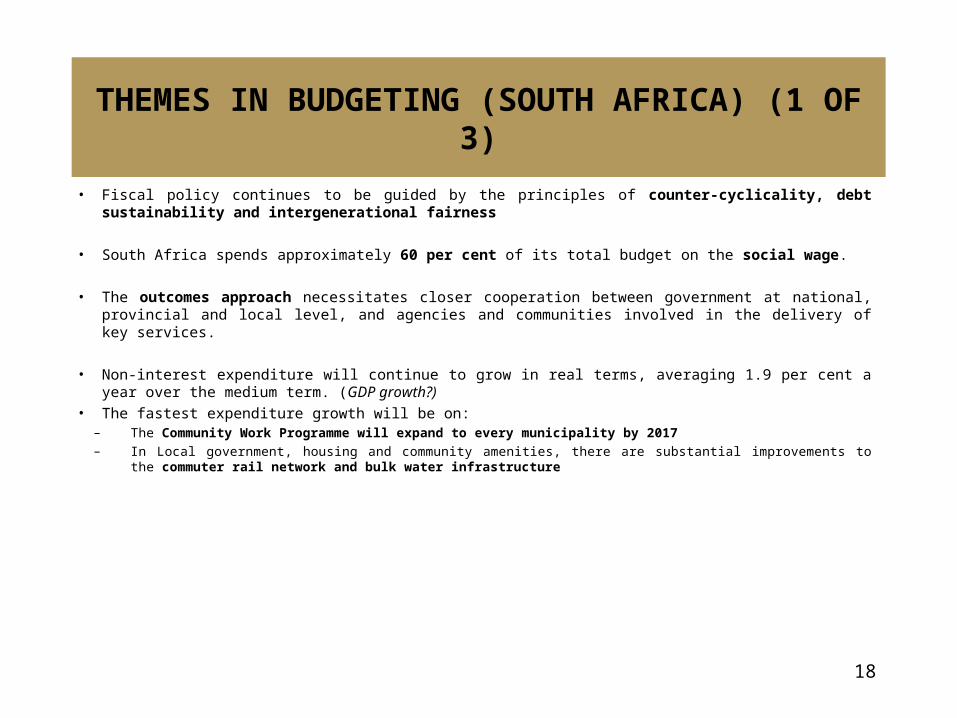

THEMES IN BUDGETING (SOUTH AFRICA) (1 OF 3)

• Fiscal policy continues to be guided by the principles of counter-cyclicality, debt sustainability and intergenerational fairness

• South Africa spends approximately 60 per cent of its total budget on the social wage.

• The outcomes approach necessitates closer cooperation between government at national, provincial and local level, and agencies and communities involved in the delivery of key services.

• Non-interest expenditure will continue to grow in real terms, averaging 1.9 per cent a year over the medium term. (GDP growth?)

• The fastest expenditure growth will be on: – The Community Work Programme will expand to every municipality by 2017– In Local government, housing and community amenities, there are substantial improvements to the commuter rail

network and bulk water infrastructure

18

THEMES IN BUDGETING (SOUTH AFRICA) (2 OF 3)

• The allocation of resources over the next government term years will be informed by government’s strategic priorities as guided by the National Development Plan (NDP).

• Cost-containment measures announced to limit expenditure on non-essential items. The measures were issued through a National Treasury instruction note in January 2014.

• National Treasury and the DPME to undertake a series of expenditure reviews; initial findings to be released in 2014/15

• The Chief Procurement Officer is building a national system for the purchase of high-value goods and services commonly used across government

• A key strategy for spending sustainability is through shifting the composition of spending away from consumption and towards productive investment.

19

THEMES IN BUDGETING (SOUTH AFRICA)(3 OF 3)

• Despite significant increases in the budget allocated to human settlements and the delivery of over three million houses, housing backlogs remain at levels similar to those in 1994.

– with an estimated R300 billion required to address the current 2.1 million backlog in housing units.

• Spending on infrastructure is short of the 10% objective set out by the NDP. South Africa's infrastructure spending levels are currently is closer to 8% of GDP.

• Budgeting has become more difficult: – Additional funds made available for allocation to government institutions have gradually decreased as a

proportion of the total budget, from 7.4 per cent in the 2009 Budget to 1.2 per cent in the 2014 Budget. This is due to the decreased quantum of additional funding made available in terms of the fiscal framework.

20

THEMES FROM SONA

21

Overview• Oversight is a Constitutional mandated function of the legislative organs of state, to

scrutinize and oversee Executive action and any organ of state.

• Section 92 provides that

(2) Members of the Cabinet are accountable collectively and individually to Parliament for the exercise of their powers and the performance of their functions.

(3) Members of Cabinet must … act in accordance with the Constitution; and provide Parliament with full and regular reports concerning matters under their control.

• Section 55 (2) provides as follows:The National Assembly must provide for mechanisms -(a) to ensure that all executive organs of state in the national sphere of

government are accountable to it; and(b) to maintain oversight of-(i) the exercise of national executive authority, including the implementation of legislation; and(ii) any organ of state.’

22

LEGAL FRAMEWORK – PARLIAMENTARY OVERSIGHT

Overview• South Africa has a legal fiscal oversight framework in place that enables parliamentary

oversight over the Executive which comprises of the Constitution, Public Finance Management Act (PFMA) and the Money Bills Amendment Procedure and Related Matters Act came into effect in April 2009. (Money Bills Act)

• Constitution Section 215 provides that – National, provincial and municipal budgets and budgetary processes must promote

transparency, accountability and the effective financial management of the economy, debt and the public sector.

• The PFMA- The main objective of this Act is to ensure transparency, accountability, and sound management of the revenue, expenditure, assets and liabilities of all public institutions. – PFMA Section 38(1)(b) states that accounting officers of departments and constitutional

institutions are responsible for the transparent, effective, efficient, and economical use of resources of the department or constitutional institution

– Section 32 states that within 30 days after the end of each month, National Treasury must publish in the Government Gazette a statement of actual revenue and expenditure....Section 40(4) states that the government institutions must submit explanations of variances and steps taken to ensure that these remain within the budget.

23

LEGAL FRAMEWORK – FISCAL OVERSIGHT

• Section 77 (3) of the Constitution: “All money Bills must be considered in accordance with the procedure established

by section 75. An Act of Parliament must provide for a procedure to amend money Bills before Parliament”.

• The Money Bills Amendment Procedure and Related Matters Act, 2009 (Money Bills Act) puts in place the procedure to amend money bills, as per Sec 77(3) of the Constitution. It defines the processes and procedures that will be undertaken to pass the Budget.

• The Money Bills Act enables Parliament to oversee budget expenditure by government departments, influence budget prioritisation, establish specific committee structures and a Parliamentary Budget Office.

• The Money Bills Act sets out statutory reporting requirements in relation to Medium Term Budget Policy Statement, Fiscal Framework, Annual and Adjusted Appropriations, Division of Revenue and the Budget Review and Recommendations Reports (BRRR)

24

MONEY BILLS ACT

25

MONEY BILLS COMMITTEES

• Section 4 of Money Bills Act establishes Parliamentary Committees for both Houses for consideration of Money Bills

• Committees on Finance

– Macro-economic and fiscal policy

– Fiscal framework and revenue proposals

– Reports on actual revenue published by NT

• Committees on Appropriations

– Spending issues

– Division of Revenue Bill, Appropriation Bill, Adjusted and Supplementary Appropriations

– FFC recommendations

– Reports on actual expenditure published by NT

Overview

26

SPENDING ISSUES

Transformation of i nputs into o utputs

Inputs Outputs Outcomes

Inputs should be purchased

E E E Outputs to entail

E E E

Inputs should be transformed into Outputs entail E E E

Assessing Value for Money

27

PUBLIC SERVICE INPUTS

• Inputs: all the resources that contribute to the production and delivery of outputs– Staffing resources (people)– Data (information)– Technology resources (ICT)– Other physical resources/furniture/office leases/ accomodation/hiring

equipment/medicines/– Consultants– Large scale procurement (coaches and locomotives, roads and rail

networks, water pipes) • Public Finance Management Act, Preferential Procurement Policy Framework

Act, Broad-based Black Economic Empowerment Act, etc

• Economy - right quality, right quantity, right time, lowest price (Payment of Suppliers within 30 days, needs assessment, appoint non-performing contractor)

• Efficiency – minimal resources for maximum outputs (Additional costs incurred to due to substandard work by contractor, consultants, employees)

• Effectiveness - achievement of policy objectives (70% local content in solar heater panels, fair and transparent procurement)

28

TRANSFORMATION OF INPUTS INTO OUTPUTS

• Weak administration is a recurring theme and is leading to poor service delivery (DPME 2013)

• The effective and efficient translation of inputs into outputs through good management practices is important for improving service delivery.

• Economy - right quality, right quantity, right time, lowest price (Weak operational planning impacts negatively on the quality of procurement planning. 31 per cent of departments did not meet the prescribed requirements for planning (MPAT Report 2012))

• Efficiency – minimal resources for maximum outputs ( costs on travel, accommodation, use of consultants whilst there is internal capacity (R76 million spend on addressing audit findings (AG Consultancy Report 2012))

• Effectiveness - achievement of policy objectives (under-expenditure, HR-related standards are particularly important for achieving results in terms of the meeting performance targets in the APP, with able staff can enhance contract management (MPAT Report 2012))

29

PUBLIC SERVICE OUTPUTS

• Budget Review 2012 – “Despite consistent growth in public spending over the past decade, rising budget allocations have not been matched by a commensurate improvement in service-delivery outcomes”

– Social services– Infrastructure (schools, hospitals, rail and roads networks, water and

sanitation, houses, etc)– General government services (Home Affairs, regulation,etc)

• Economy - right quality, right quantity, right time, lowest price (High technology water services infrastructure – sludge plants/water treatment)

• Efficiency – minimal resources for maximum outputs (Additional costs incurred to due to substandard work by contractor, consultants, employees)

• Effectiveness - achievement of policy objectives (Completed projects were not always used for their intended purposes. Facilities were also unused long after construction is complete or not fully operational as they were unsafe due to construction defects (AG Infrastructure Report 2011), Informal Settlements Upgrading – “....apartheid geography exacerbated”- NDP 2030)

30

Division of Revenue Act (DoRA)• Section 9 of the Money Bills Act• After adoption of the Fiscal Framework, DoRA is referred to Committees on

Appropriations.

• The Bill provides for the equitable division of revenue raised nationally among the national, provincial and local spheres of government ........and the responsibilities of all three spheres pursuant to such division and allocations; and to provide for matters connected therewith.

• Parliament (NA & NCOP) should consider & report within 35 days after adoption of Fiscal Framework

• Any amendment must be consistent with the adopted fiscal framework and Section 214 of the Constitution

• The Committees on Appropriations must consult with the FFC and allow the Minister 3 days to respond to any proposed amendments prior to submission to the relevant house

31

32

Appropriation Act

• Section 10 of the Money Bills Act• After the adoption of Fiscal Framework, the Appropriation Bill

must be referred to the ST on Appropriations

• Should be passed by Parliament within four months after the start of the new financial year. This means by the end of July it should be passed by Parliament.

• Committees should facilitate public participation.

• Ministers should be given 10 days to respond to proposed amendments

• Amendments may only be considered after the DoRA Bill is

passed

33

Important issues for consideration• Section 10 (10) provides that when amending the Appropriation Bill,

the report from the Committee on Appropriations: – Indicate reasons for such an amendment;– Demonstrate how the proposed amendments take into account the broad

strategic priorities and allocations of the relevant budget;– Demonstrate the implications for each amendment on affected vote and

main divisions within the vote;– Demonstrate the impact of any proposed amendment on the balance

between transfer payments, capital payments and recurrent spending;– Set out how the report relates to the prevailing departmental strategic

plans, reports of the Auditor General, committee reports of the house and section 32 reports.

• If a Committee amends, the report proposing the amendments must include the responses of the Minister or Cabinet member affected.

• The role and expertise of Parliamentary Budget Office critical

34

Medium Term Budget Policy Statement

• Section 6 of the Money Bills Act

• The MTBPS contains, broadly, the revised and proposed fiscal framework and outlines the spending priorities of government for the medium term

• Matters dealing with the fiscal framework, macro economic and fiscal policy estimates are referred to the Committees on Finance

• Matters dealing with revised actual spending projections and adjusted grant allocations, proposed spending priorities and proposed division of revenue to be referred to the Committees on Appropriations

• The Committee is required to consider and report on the following issues:

– the spending priorities of national government for the next three years;– the proposed division of revenue between the spheres of government and

between arms of government within a sphere for the next three years; and – the proposed substantial adjustments to conditional grants to provinces and

local government, if any.

35

Important issues for consideration

• Recommendations from the Committees on Finance may include proposals to amend the fiscal framework

• Recommendations from the Committees on Appropriations may include proposals to amend the division of revenue

• Section 7(4) provides that the Minister of Finance must report to both Houses at the time of tabling the budget how the budget responds to the recommendations of all four Committees

– i.e. When the Finance Minister tables the Budget he must table a report indicating how the Division of Revenue and the Budget gives effect to the Committee recommendations

– If the Minister’s explanation does not address Parliament’s concerns, Parliament can amend the Budget in order to give effect to its proposals

36

Examples• Recommendations of SCoA in 2013 MTBPS and National Treasury

Responses• The Ministers of Finance and Human Settlements develop and implement a

capacity enhancement and support initiative specifically aimed at the successful devolvement of the human settlements function to the six metropolitan municipalities.

– The 2014 Budget includes a new conditional grant to fund the development of capacity to administer housing programmes in the six metropolitan municipalities assigned this function. The municipal human settlements capacity grant has an allocation of R900 million over the 2014 medium-term expenditure framework (MTEF) period and will be administered by the Department of Human Settlements.

• The National Treasury should develop and implement mechanisms to ensure that baseline funding requirements are in place for the successful transfer of the further education and training colleges function to the Department of Higher Education and Training.

– A special committee, including provincial treasuries, will be established in 2014 to work with the heads of the Education Committee and the Council of Education Ministers to provide executive stewardship of the full funding shift of further education and training colleges on 1 April 2015 and adult education and training functions on 1 April 2016.

37

What Happens Now?• 2014 Appropriation Bill was tabled in Parliament at the time of the Budget – 26

February 2014• The Bill provides for the appropriation of money from the National Revenue

Fund in terms of section 213 of the Constitution, 1996 and section 15 of the Public Finance Management Act (PFMA), 1999

• Spending is subject to the PFMA and the provisions of the Appropriation Bill itself

• Parliament needs to pass the Bill so that the Act can be promulgated before the end of July

• Section 10 (7) states that Parliament must pass, with or without amendments, or reject the Appropriation Bill within four months after the start of the financial year.

– Briefings by National Treasury– Hold Public hearings– Invite Departments and Stakeholders

IMPORTANT STAKEHOLDERS

• Legislatures (Portfolio Committees, Finance and Appropriations Committees, SCOPA)

• Cabinet (National and Provincial Departments, National Treasury)

• Auditor-General• Public Entities• Constitutional entities• Financial and Fiscal Commission (FFC)• South African Local Government Association• Civil Society• Parliamentary Budget Office

38

39

Parliamentary Budget Office• Established in terms of the Money Bills Act. • Section 15 (2) provides that the core function of PBO is to

support the Finance and Appropriations Committees through:– Annually review and analysis of relevant budget documents.– Provide advice and analysis on proposed amendments to

the fiscal framework, DORB, money bills, policy proposals with budgetary implications, etc.

– Monitor and synthesise matters and relevant reports with budgetary implications adopted in the House with particular emphasis on reports by other committees.

– Keep abreast of policy debates and developments on expenditure and revenue.

– Monitor and report on potential unfunded mandates

Ndza Nkhensa

40