Embed Size (px)

Citation preview

1

National Forum on Educational Loans

College Board Forum2006

2

Idea and Purpose

Need for a better option for students and families to finance college

Growing concern about borrowing from multiple sources

Current system has served us well for many years but may not serve the needs of students in the future

3

Idea and Purpose

How did the NFEL come about? Event organizers believe that the current

system of educational loans is: Confusing Inefficient

Many believe the current system is broken; others believe that it should be improved

Presented NASFAA Board with a proposal for a national forum on educational loans

4

Idea and Purpose

Confusing loan system Some require a FAFSA and some do not Federal loan limits are insufficient PLUS/Private loans not available to all School certifies some but not all loans Repayment start dates vary widely Often few qualify for advertised benefits Consolidation can change the rules

5

Idea and Purpose

Confusing loan system Private loans have answered a real call

for help, but at a cost Schools increasingly need time and

expertise to evaluate private loans Helping students and parents

understand advantages and disadvantages of private loans or specific private loans is time consuming

6

Idea and Purpose

Inefficient loan system Multiple loans required from multiple

lenders to get required funds at lowest cost

Federal Stafford Federal Perkins Private loan

Students/parents must sort out best option from among unknown loan sources

Processing and fund delivery methods vary

7

Idea and Purpose

Organizers wondered if aid administrators could create a better system A more integrated system A less time consuming system A more flexible system An easier to understand system A Better Option for Families

8

The Plan Invite participants from a cross-section of

school aid administrators from all sectors to engage in a dialogue about educational financing.

Identify speakers to facilitate discussions Develop a position paper following the forum

that articulates a new plan for educational loans

Present plan to constituent associations Work toward implementation

9

Speaker Panel – Day 1 Ken Redd, Director of Research and Policy Analysis,

National Association of Student Financial Aid Administrators

Who is Going to College and Who is Not, Including Socioeconomic and other Demographic Profiles

Sandy Baum, Economics Professor, Skidmore College and Senior Policy Analyst, The College Board

What Does College Really Cost and What are Reasonable Debt Levels

Jackie King, Director, Center for Policy Analysis, American Council on Education

Who is Borrowing and How Much, It’s affect on Life Styles and Pursuit of Advanced Degrees

10

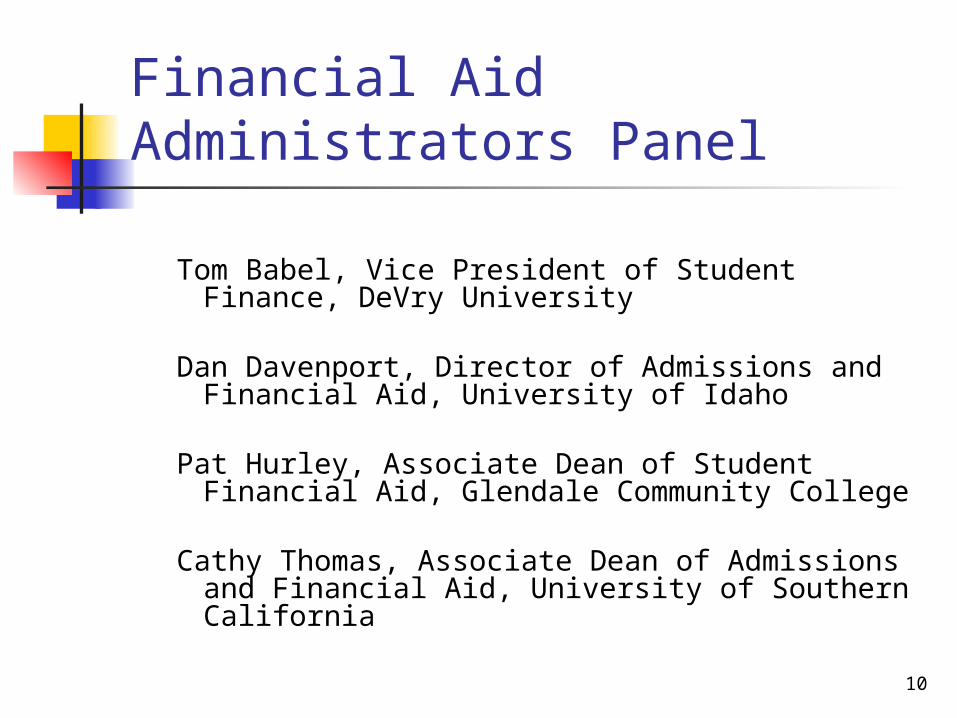

Financial Aid Administrators Panel

Tom Babel, Vice President of Student Finance, DeVry University

Dan Davenport, Director of Admissions and Financial Aid, University of Idaho

Pat Hurley, Associate Dean of Student Financial Aid, Glendale Community College

Cathy Thomas, Associate Dean of Admissions and Financial Aid, University of Southern California

11

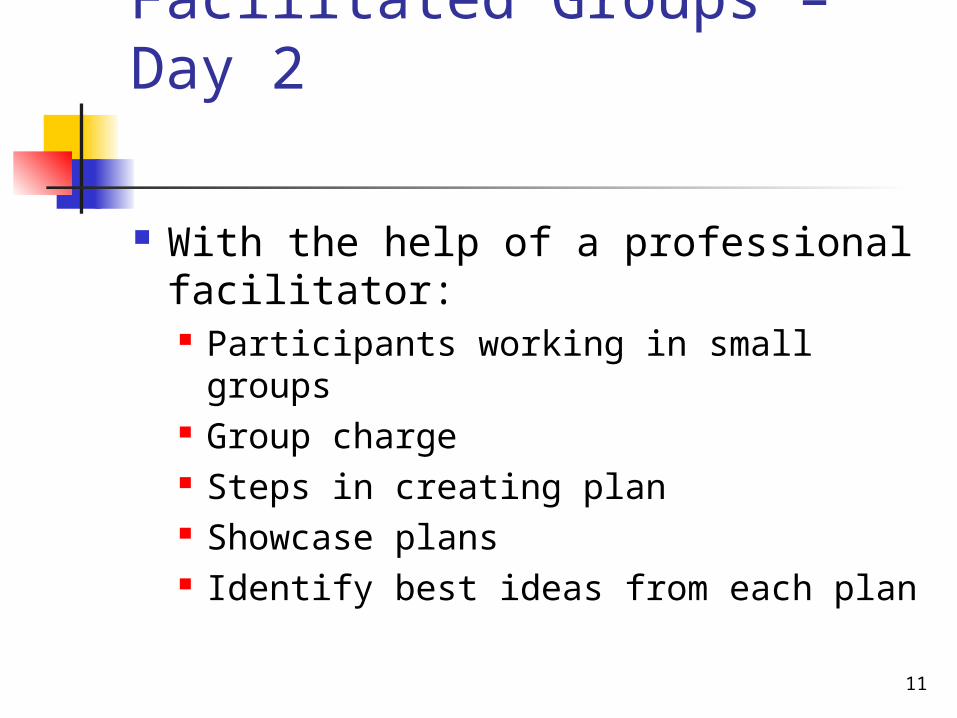

Facilitated Groups – Day 2

With the help of a professional facilitator: Participants working in small groups Group charge Steps in creating plan Showcase plans Identify best ideas from each plan

12

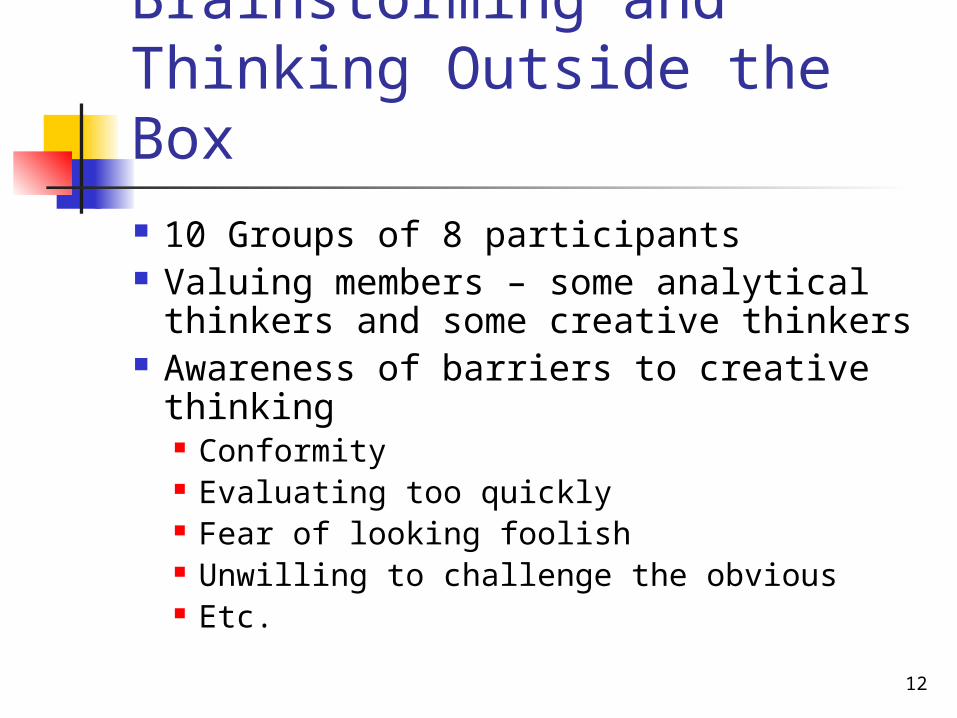

Brainstorming and Thinking Outside the Box 10 Groups of 8 participants Valuing members – some analytical

thinkers and some creative thinkers Awareness of barriers to creative

thinking Conformity Evaluating too quickly Fear of looking foolish Unwilling to challenge the obvious Etc.

13

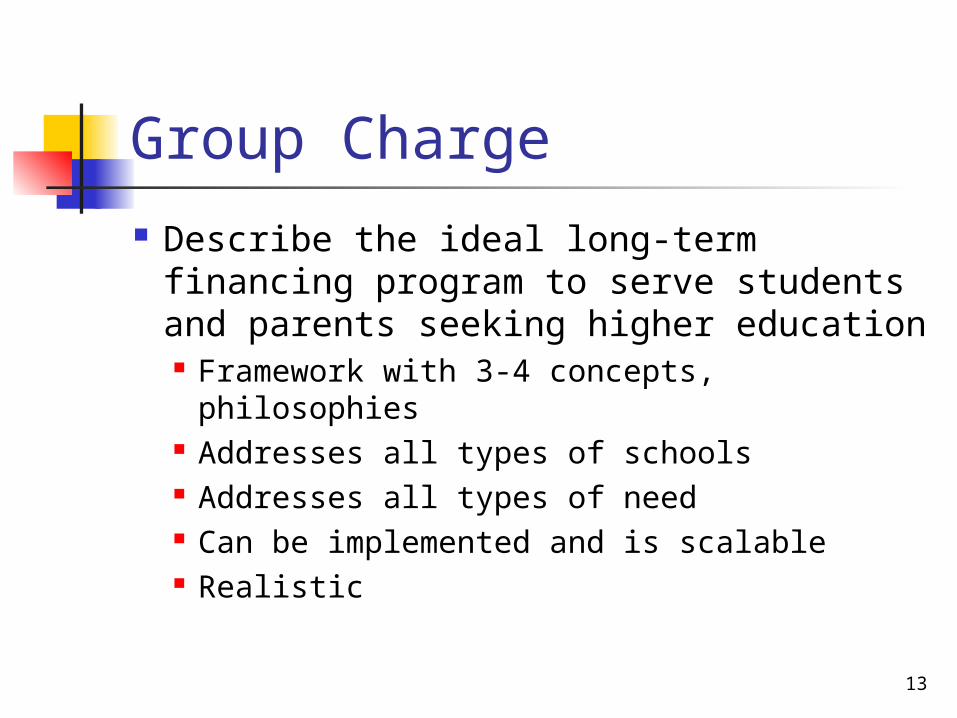

Group Charge

Describe the ideal long-term financing program to serve students and parents seeking higher education Framework with 3-4 concepts,

philosophies Addresses all types of schools Addresses all types of need Can be implemented and is scalable Realistic

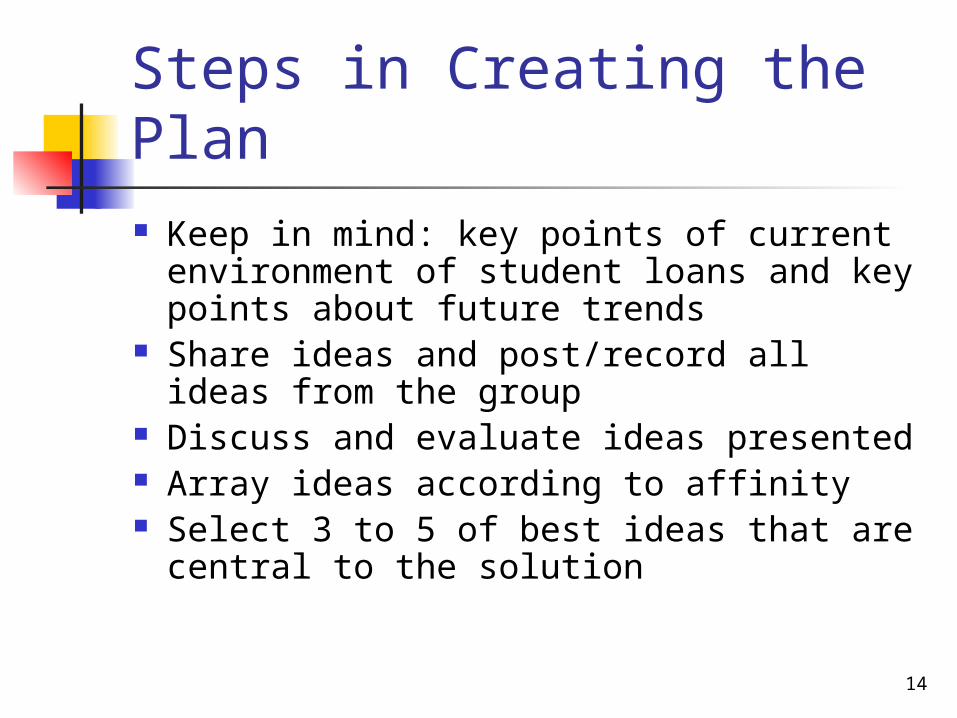

14

Steps in Creating the Plan Keep in mind: key points of current

environment of student loans and key points about future trends

Share ideas and post/record all ideas from the group

Discuss and evaluate ideas presented Array ideas according to affinity Select 3 to 5 of best ideas that are

central to the solution

15

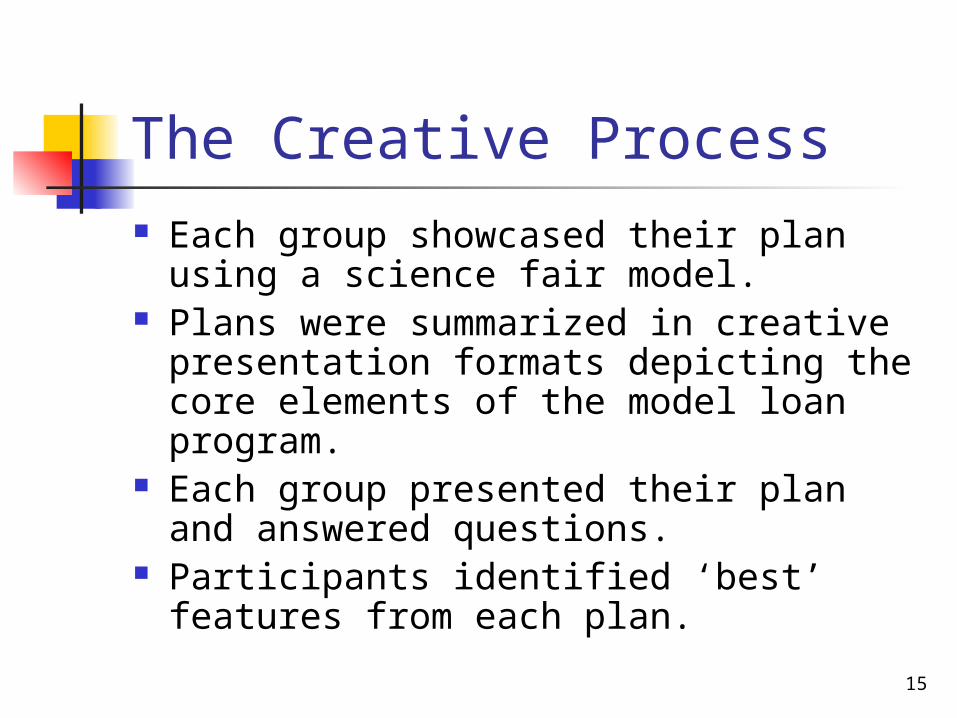

The Creative Process Each group showcased their plan using

a science fair model. Plans were summarized in creative

presentation formats depicting the core elements of the model loan program.

Each group presented their plan and answered questions.

Participants identified ‘best’ features from each plan.

16

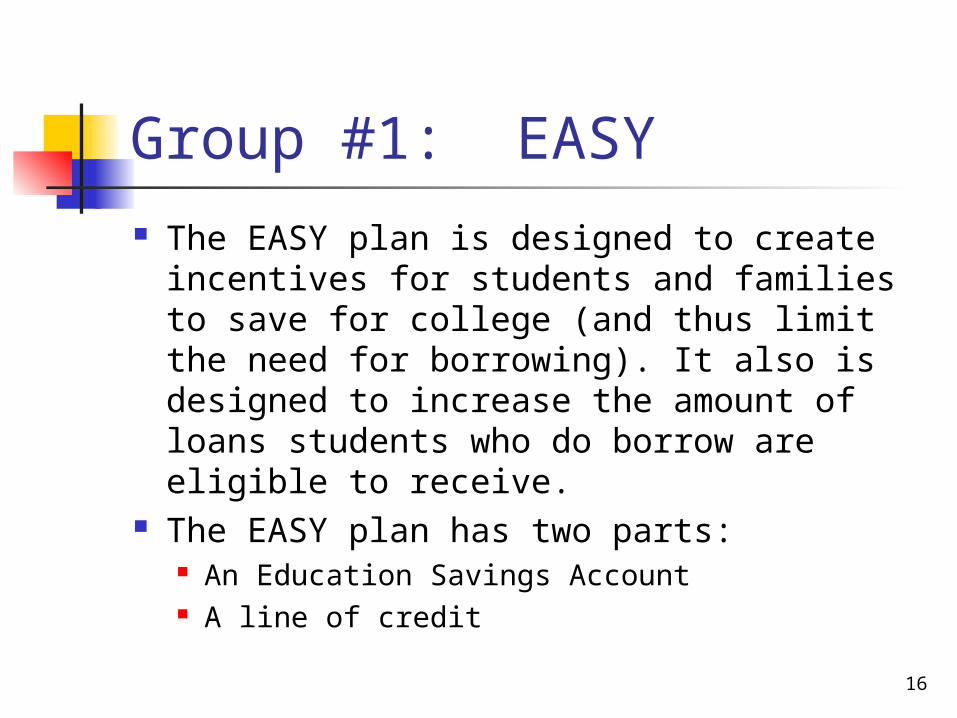

Group #1: EASY The EASY plan is designed to create

incentives for students and families to save for college (and thus limit the need for borrowing). It also is designed to increase the amount of loans students who do borrow are eligible to receive.

The EASY plan has two parts: An Education Savings Account A line of credit

17

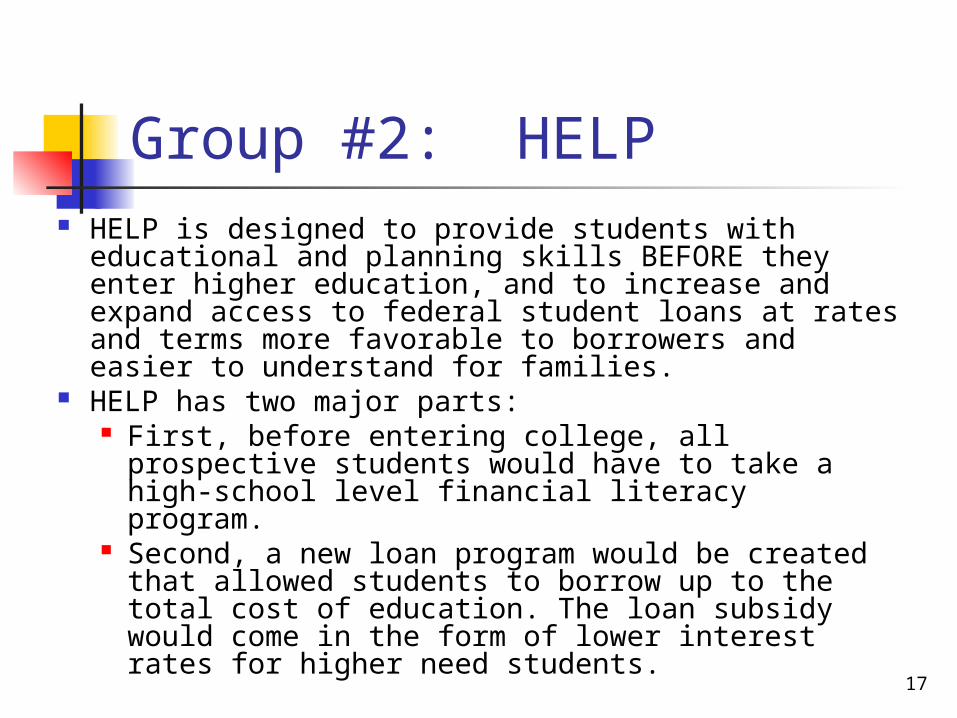

Group #2: HELP HELP is designed to provide students with

educational and planning skills BEFORE they enter higher education, and to increase and expand access to federal student loans at rates and terms more favorable to borrowers and easier to understand for families.

HELP has two major parts: First, before entering college, all prospective

students would have to take a high-school level financial literacy program.

Second, a new loan program would be created that allowed students to borrow up to the total cost of education. The loan subsidy would come in the form of lower interest rates for higher need students.

18

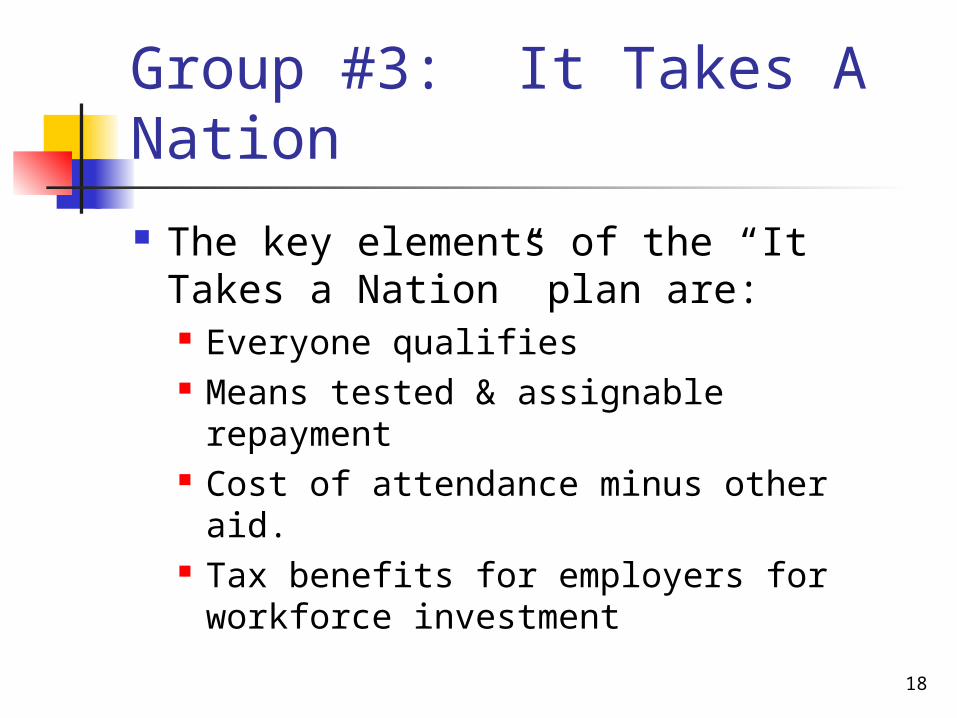

Group #3: It Takes A Nation

The key elements of the “It Takes a Nation” plan are: Everyone qualifies Means tested & assignable repayment Cost of attendance minus other aid. Tax benefits for employers for

workforce investment

19

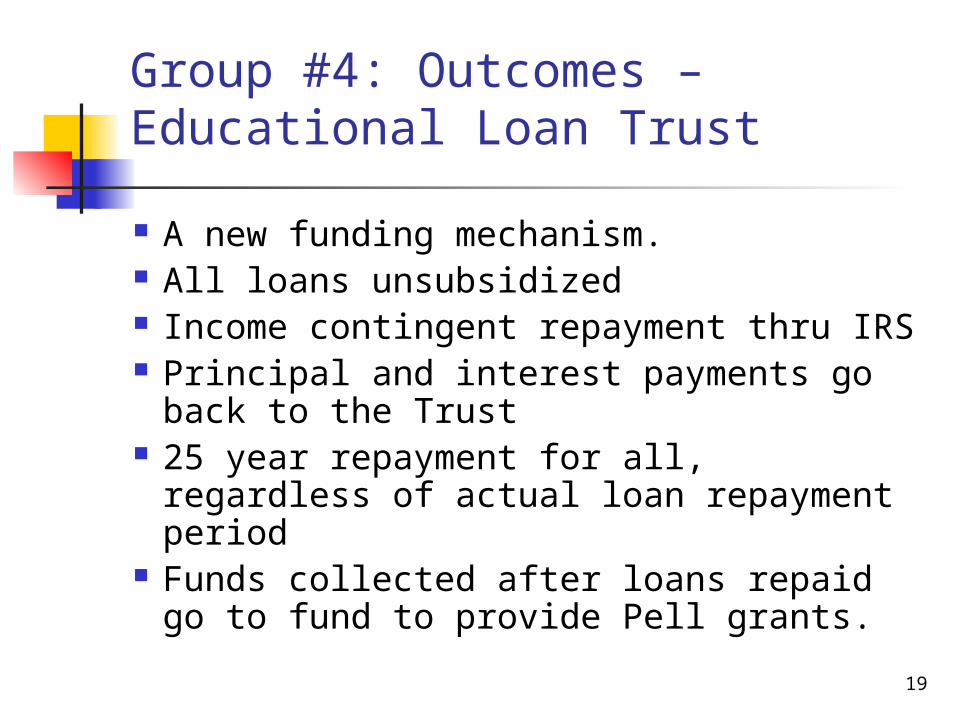

Group #4: Outcomes – Educational Loan Trust

A new funding mechanism. All loans unsubsidized Income contingent repayment thru IRS Principal and interest payments go

back to the Trust 25 year repayment for all, regardless

of actual loan repayment period Funds collected after loans repaid go

to fund to provide Pell grants.

20

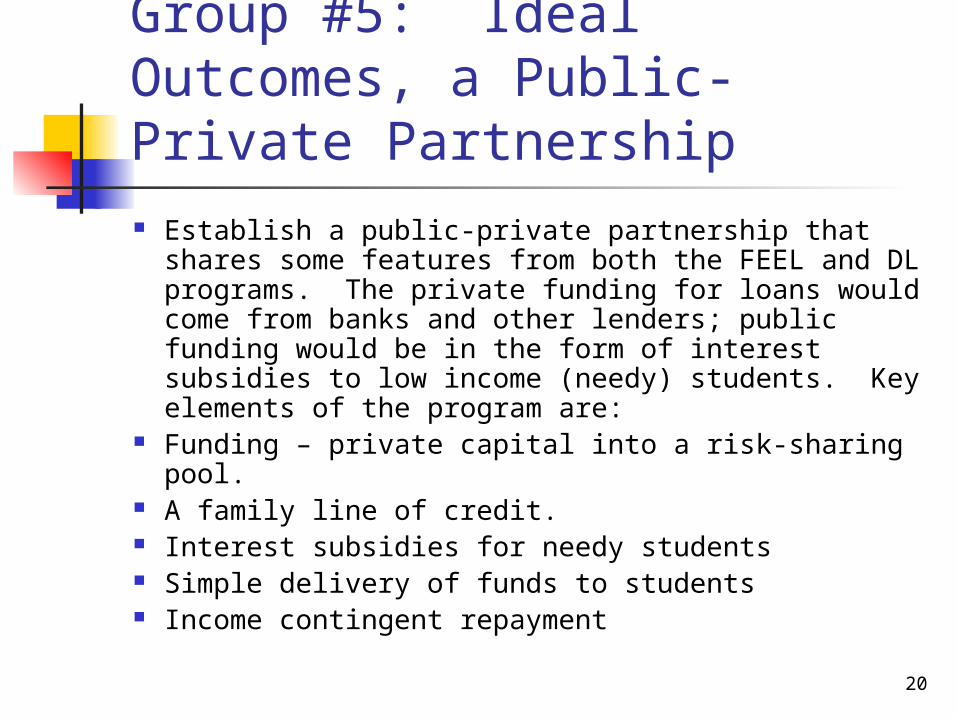

Group #5: Ideal Outcomes, a Public-Private Partnership Establish a public-private partnership that shares

some features from both the FEEL and DL programs. The private funding for loans would come from banks and other lenders; public funding would be in the form of interest subsidies to low income (needy) students. Key elements of the program are:

Funding – private capital into a risk-sharing pool. A family line of credit. Interest subsidies for needy students Simple delivery of funds to students Income contingent repayment

21

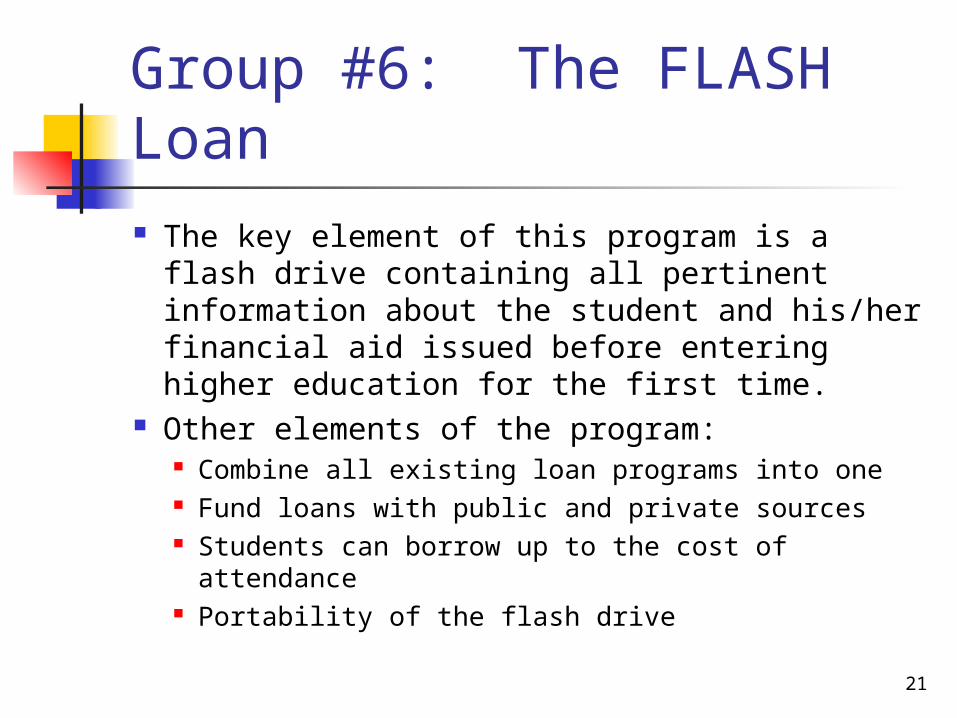

Group #6: The FLASH Loan The key element of this program is a flash

drive containing all pertinent information about the student and his/her financial aid issued before entering higher education for the first time.

Other elements of the program: Combine all existing loan programs into one Fund loans with public and private sources Students can borrow up to the cost of attendance Portability of the flash drive

22

Group #7: Lifetime Family Savings Account (LFSA) The LFSA is an account that could be used for

multiple purposes, not just college expenses. Multiple funding sources. Under this plan,

families and employers could make tax-advantaged contributions into a recipients’ account.

A Variety of Uses. After they reach college age, children could use the LSFA funds for a variety of purposes—such as paying postsecondary costs, buying a home, getting married, long-term health insurance, etc.

23

Group #8: KISS Create a portable line of credit that students

could use at any accredited postsecondary institution. The key elements of the program are:

The loans would be financed by the government but loan consolidation would be financed by a secondary market.

The student could borrow up to cost of attendance minus other aid.

To encourage students to stay in school and complete their degree programs, interest rates and loan repayment terms would improve for borrowers for each year of attendance, such that completers would get the best rates and terms.

Also, to reduce post-college loan repayment burdens, tax credits would be available to offset the cost of some portion of repayment. Otherwise, loan consolidation and income-contingent plans would be made available.

24

Group #9: Education Line of Credit This plan includes a financial literacy component and

increased access to college loans. All students would be required to take some form of

financial literacy training before entering school. Government database that includes the schools costs’

of attendance and the students’ expected income after graduation on which repayment is determined.

To help further with loan repayments, the borrowers’ interest rate would be based on their field of study, recognizing the different incomes and financial situations of students in certain low-wage occupations; benefits for making accelerated or on-time loan repayments

Employers would have some tax or other incentives for adding a loan repayment benefit plan.

25

Group #10: CHEF The CHEF program would be a flexible, reliable

source of funding that encourages early preparedness, identifies a role for private industry to play due to their vested interest in a well-educated workforce, promotes important service-based contributions to society, and maintains a Federal presence and priority for funding higher education.

Multiple Funding Sources: family, employer Collaborative, flexible and easily manageable

means of repayment.

26

27

Most Supported Ideas Comprehensive single loan program

This concept provides simplicity in processing and eliminates confusion for students in repayment

A student account Savings program Line of Credit Add to account by community service Tax incentives for contributors

28

Most Supported Ideas

Loan limits increased to total cost of education minus other aid

Financial literacy programs Loan repayment programs

Incentives and loan benefits based on needs test during repayment

Employer tax benefits for assisting employees in loan repayment

29

Most Supported Ideas

Not intended to replace grant programs which should be the major source of funding for low income students

30

Conceptual Model

One source of funding for a single loan program Could include part of the loan

repayment be directed at parents Need analysis still used for

students but allows for only student data when parents refuse to complete the information

31

Conceptual Model

Funds delivered through the school to the student

Loan amount up to cost of attendance minus other aid Schools can determine lower

borrowing limits for their students

32

Conceptual Model

Repayment Based on financial circumstances during

repayment Subsidies provided during repayment

rather than during attendance time-period Payment can be part of income tax process

Tax benefits for others helping with repayment of loans

33

Conceptual Model Financial literacy provided by those

administering the program Provided prior to attending college

Conclusion Current programs fall short of family needs Must keep higher education accessible and

affordable Concepts intended to stimulate thinking of

new ideas and solutions

34

Next Steps Feedback sessions from presentations to

groups Draft white paper out this fall

Feedback to refine basic concepts and ideas Present second draft white paper of the model

program to other constituents: Aid Community and other professional post-

secondary associations Presidential Associations Interested Loan Associations Congressional Advisory Committee National Student Associations Other constituent groups

35

Next Steps

Convene meeting with key stakeholders to further refine the model

Further develop the model to ensure all perspectives have been adequately addressed

36

Next Steps Present final white paper with new

loan concepts for further action in the political process House and Senate Committees Committee on Education Funding (CEF) Federal funding agencies (OMB, CBO, etc)

Encourage support from associations involved in student financial aid programs

37

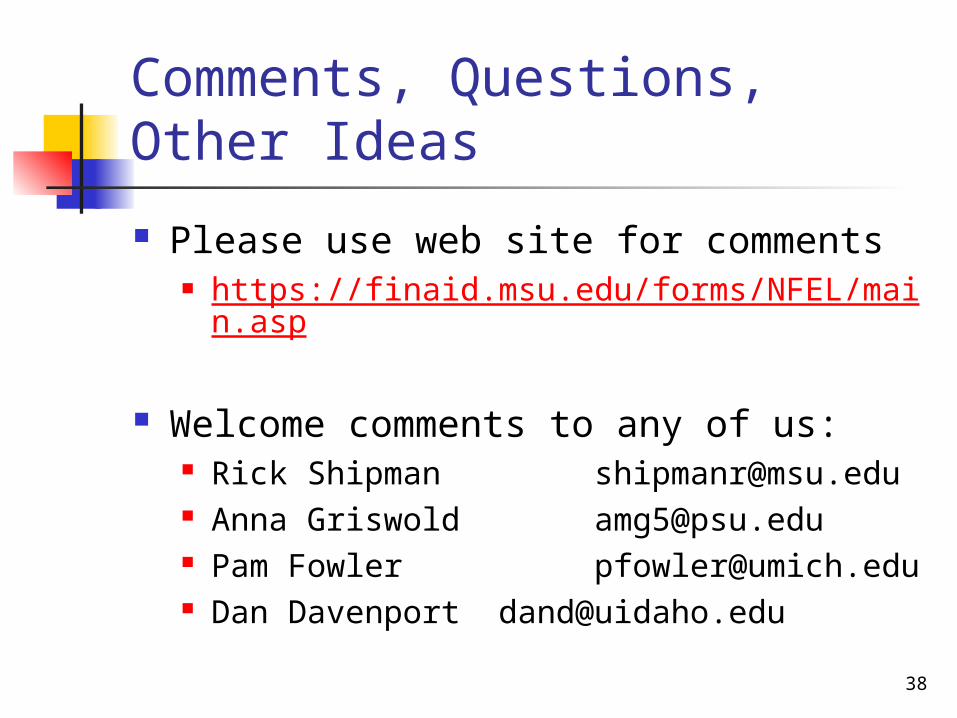

38

Comments, Questions, Other Ideas

Please use web site for comments https://finaid.msu.edu/forms/NFEL/main.asp

Welcome comments to any of us: Rick Shipman [email protected] Anna Griswold [email protected] Pam Fowler [email protected] Dan Davenport [email protected]