Embed Size (px)

Citation preview

1

Minimizing Risk Through Company Restructuring Garth D. Stevens, Snell & Wilmer L.L.P.

Joshua P. Hayes, Eide Bailly LLP

2©2010 Snell & Wilmer L.L.P.

Objectives of Reorganization

1. Protect specific classes of assets (e.g., real estate, IP)

2. Create firewalls between different businesses

3. Insulate higher risk business from lower risk business

3

Limited Liability and Piercing the Corporate Veil

4©2010 Snell & Wilmer L.L.P.

Limited Liability

• A fundamental tenet of corporation and LLC formation:

• Ordinarily, a company’s shareholders will not be liable for the company’s debts or other liabilities beyond the shareholders’ equity investment in the company.

5©2010 Snell & Wilmer L.L.P.

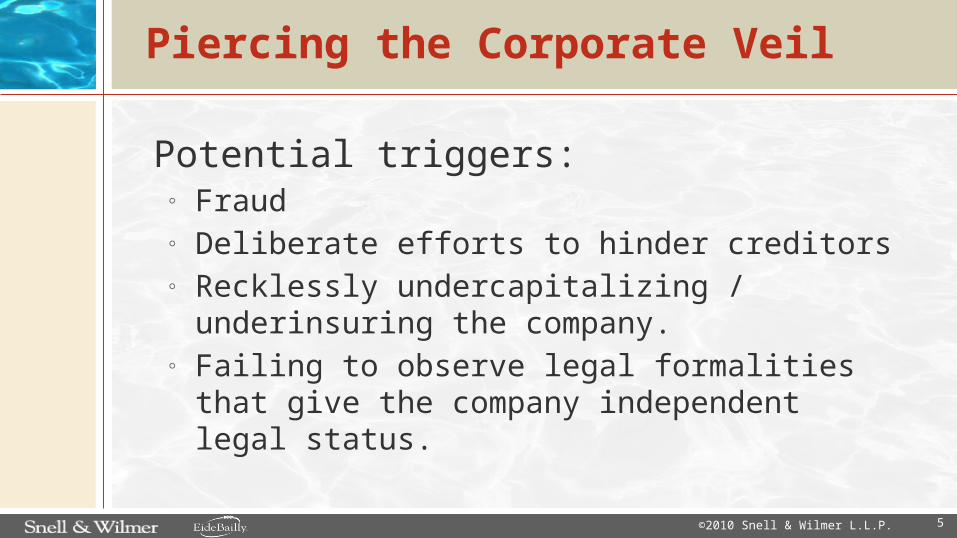

Piercing the Corporate Veil

Potential triggers:◦ Fraud◦ Deliberate efforts to hinder creditors◦ Recklessly undercapitalizing / underinsuring the

company.◦ Failing to observe legal formalities that give the

company independent legal status.

6©2010 Snell & Wilmer L.L.P.

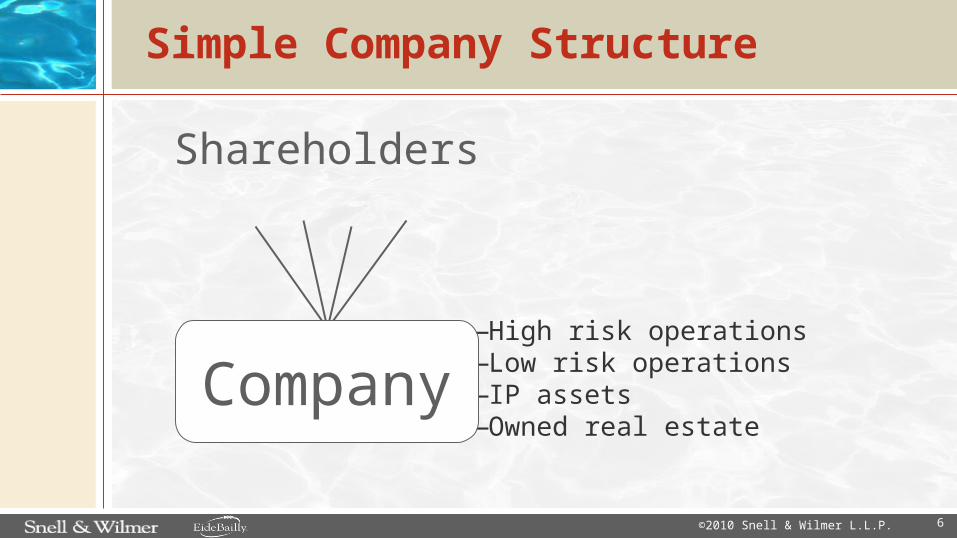

—High risk operations—Low risk operations—IP assets—Owned real estate

Shareholders

Company

Simple Company Structure

7©2010 Snell & Wilmer L.L.P.

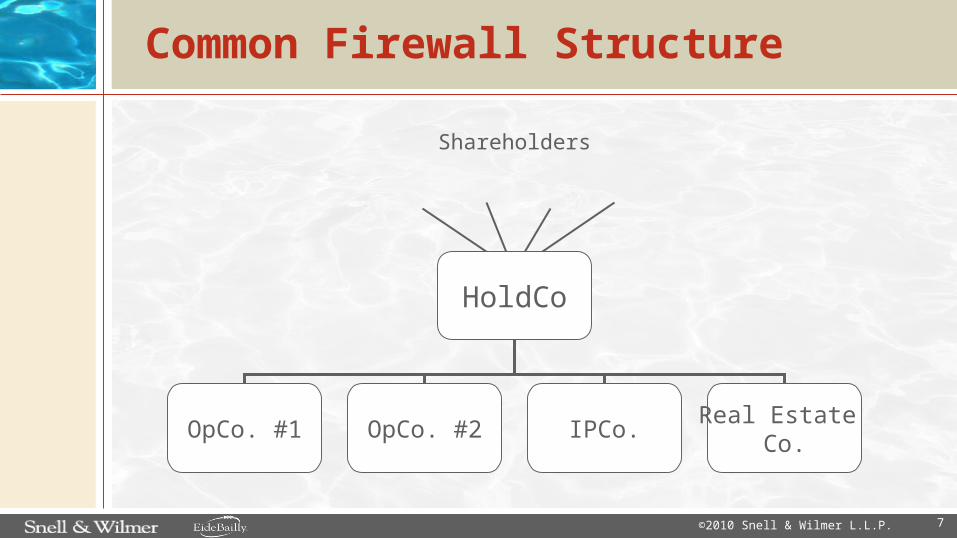

Common Firewall Structure

Shareholders

HoldCo

OpCo. #1 OpCo. #2 IPCo.Real Estate

Co.

8©2010 Snell & Wilmer L.L.P.

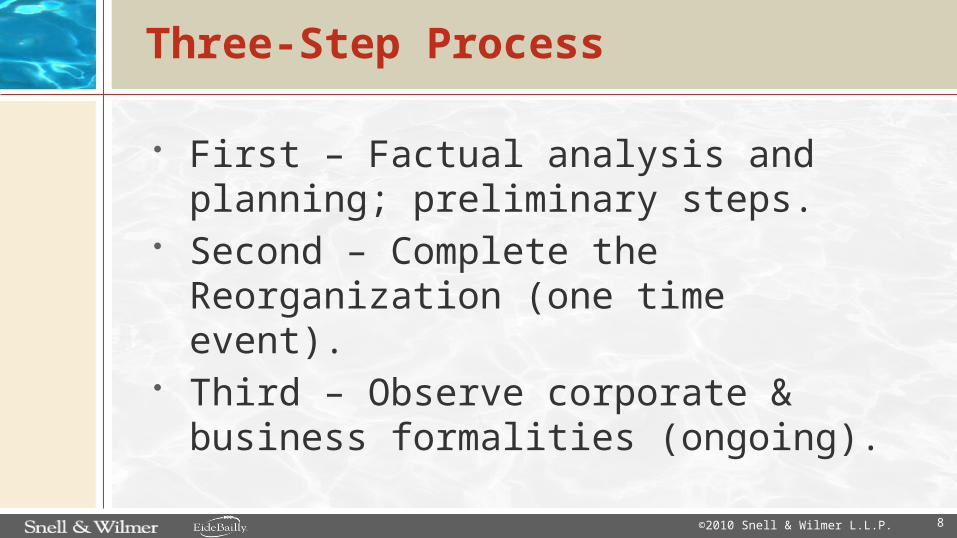

Three-Step Process

• First – Factual analysis and planning; preliminary steps.

• Second – Complete the Reorganization (one time event).

• Third – Observe corporate & business formalities (ongoing).

9©2010 Snell & Wilmer L.L.P.

Factual Analysis & Planning; Preliminary Steps

• Determine appropriate tax structure. • Identify contractual restrictions (e.g., bank loan

documents; shareholder agreements).• Identify permit and licensing issues, including

transferability.• Identify notices/registrations that will need to be

made (e.g., IP transfers; notices to customers).• Obtain applicable shareholder/director approvals.

10©2010 Snell & Wilmer L.L.P.

Tax Analysis and Considerations

• Tax considerations – e.g., preservation of NOLs and tax credits.

• Valid business purpose.• Shareholders receive stock in exchange

for stock.• Investment position is equivalent after

transaction is complete.

11©2010 Snell & Wilmer L.L.P.

How Do We Get There?

1. Form new HoldCo.2. Shareholders of current OpCo

assign their shares of OpCo to new HoldCo (Code § 351)

3. In exchange, HoldCo issues shares to OpCo shareholders

4. The result – Shareholders now hold the same % ownership of HoldCo and HoldCo owns OpCo

Step One – Formation of New Parent Holding Company

Shareholders

HoldCo

OpCo.

12©2010 Snell & Wilmer L.L.P.

Shareholders

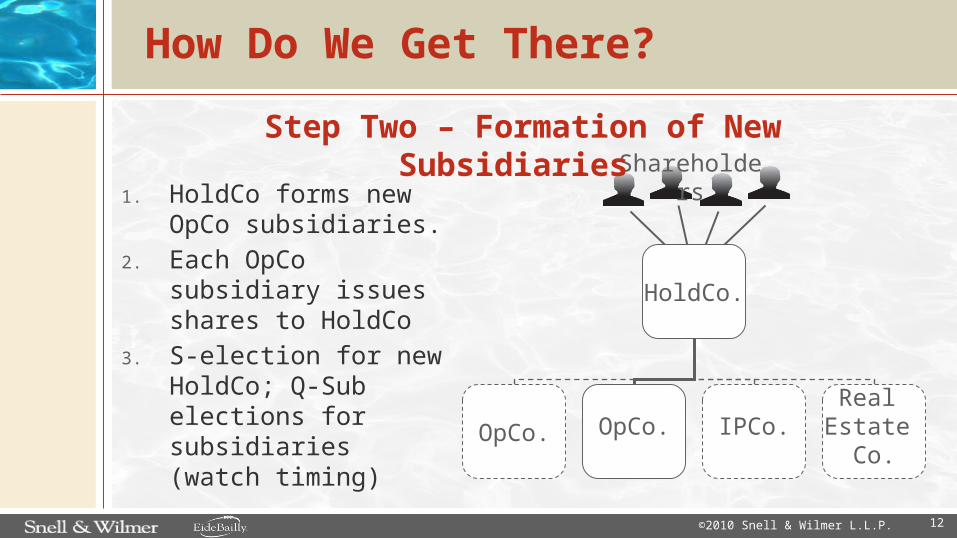

How Do We Get There?

1. HoldCo forms new OpCo subsidiaries.

2. Each OpCo subsidiary issues shares to HoldCo

3. S-election for new HoldCo; Q-Sub elections for subsidiaries (watch timing)

Step Two – Formation of New Subsidiaries

HoldCo.

OpCo. OpCo. IPCo.Real

Estate Co.

13©2010 Snell & Wilmer L.L.P.

Shareholders

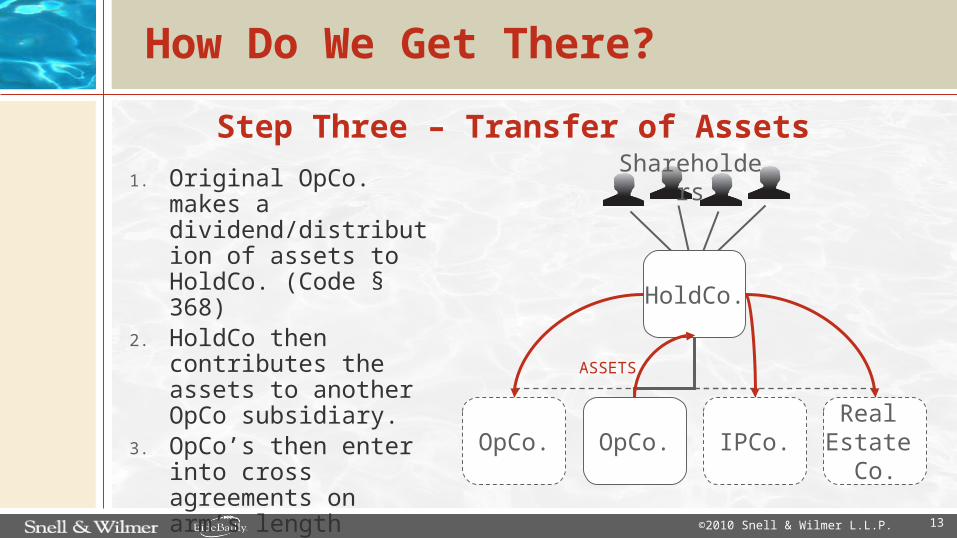

How Do We Get There?

1. Original OpCo. makes a dividend/distribution of assets to HoldCo. (Code § 368)

2. HoldCo then contributes the assets to another OpCo subsidiary.

3. OpCo’s then enter into cross agreements on arm’s length terms.

Step Three – Transfer of Assets

HoldCo.

OpCo. OpCo. IPCo.Real

Estate Co.

ASSETS

14©2010 Snell & Wilmer L.L.P.

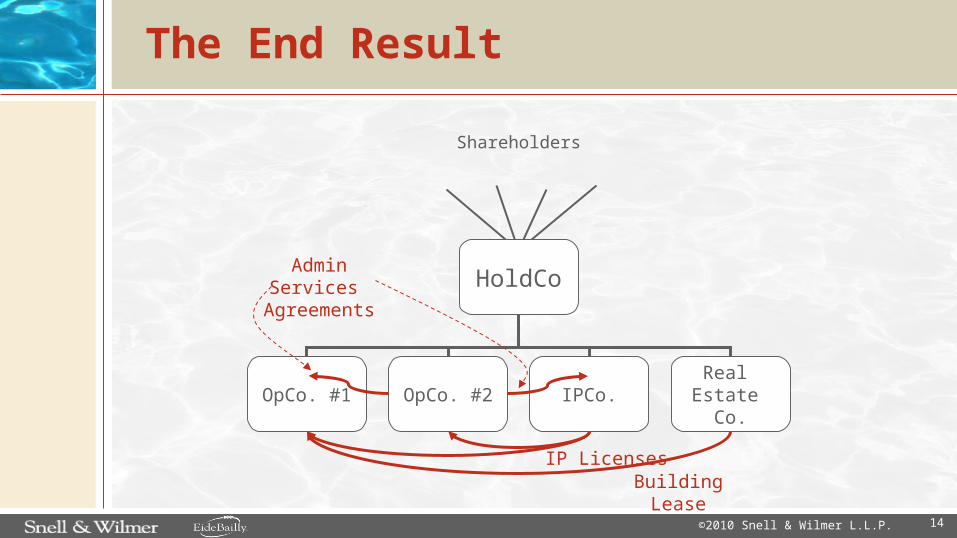

The End Result

Shareholders

HoldCo

OpCo. #1 OpCo. #2 IPCo.Real

Estate Co.

Building LeaseIP Licenses

Admin Services Agreements

15©2010 Snell & Wilmer L.L.P.

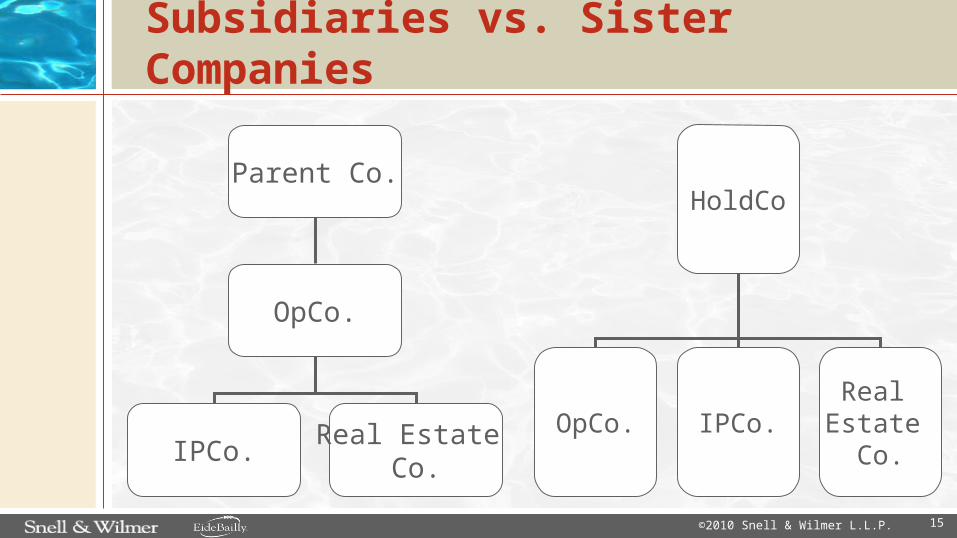

Subsidiaries vs. Sister Companies

Parent Co.

OpCo.

IPCo.Real Estate

Co.

HoldCo

OpCo. IPCo.Real

Estate Co.

16©2010 Snell & Wilmer L.L.P.

Subsidiaries vs. Sister Companies

• Consolidated tax election?• Combined filing?

Tax Filing Considerations:

17©2010 Snell & Wilmer L.L.P.

Preserving Limited Liability

TWO KEYS:

1. Maintenance of independent existence and operation.

2. REASONABLE capitalization and/or insurance for each company.

18©2010 Snell & Wilmer L.L.P.

Independent Existence

• Think of (and treat) each company as if it was truly independent of each other company.

• If you don’t treat each company as a separate legal entity, there is a good chance that a court won’t either.

19©2010 Snell & Wilmer L.L.P.

Maintaining The Firewalls

• Avoid co-mingling funds; each company with its own bank account.

• Document inter-company transactions with written agreements on arm’s length terms.

• Intercompany loans should be under written, interest-bearing notes or loan agreements (not just GL entry).

• Each company should follow proper corporate formalities.• Where appropriate, each company should have its own

employees.• If possible, avoid cross guaranties and cross-default terms

in contracts.• If possible, physical segregation of businesses.

20©2010 Snell & Wilmer L.L.P.

Capitalization and Insurance

• The best way to avoid a creditor’s attempt to “pierce the veil” is to give the creditor no need to do so.

• Take a REASONABLE approach to capitalizing and/or insuring each company.

7 Tax Mistakes that will cost you

• Payroll Taxes◦ It’s a VERY easy and tempting loan to make◦ It isn’t the employer’s money, it is trust fund money on

behalf of employees.

• Independent Contractors◦ Employees are expensive and healthcare reform is

complicated.◦ 20 part test IRS uses to determine status of worker

21©2010 Snell & Wilmer L.L.P.

7 Tax Mistakes that will cost you

• Owner compensation strategies◦ Reasonable compensation for services◦ C-corp vs. S-Corp vs. LLC

• Hire your Children?◦ Reasonable compensation for services◦ Must be real work performed or services performed◦ College planning with low tax cost and potential

credits

22©2010 Snell & Wilmer L.L.P.

7 Tax Mistakes that will cost you

• Keeping Receipts◦ Must keep an accurate diary or business log in

addition to receipts◦ Documentation of Who? Why? When? Where?

• Purchasing equipment at the end of the year◦ Mid quarter convention might limit deduction◦ Uncertainty of bonus depreciation and Sec. 179

23©2010 Snell & Wilmer L.L.P.

7 Tax Mistakes that will cost you

• Embezzlement◦ Separation of duties

- Ordering vs. receiving- Check writing/signing vs. A/P input

◦ Monthly oversight by owner is a must!

24©2010 Snell & Wilmer L.L.P.

25

Thank You

Garth StevensSnell & Wilmer

Joshua P. HayesEide Bailly LLP

602.264.8663 [email protected]