Embed Size (px)

Citation preview

1

Merrill Lynch Global Pharmaceutical, Biotechnology and Medical Device Conference 2008

Dr. John ClimaxExecutive Chairman

2

Certain statements contained herein including, without limitation, statements containing the words “believes,” “anticipates,” “intends,” “expects” and words of similar import, constitute forward-looking statements concerning the Company's operations, performance, financial condition and prospects. Because such statements involve known and unknown risks and uncertainties, actual results may differ materially from those expressed or implied by such forward-looking statements. Given these uncertainties, prospective investors are cautioned not to place undue reliance on such forward-looking statements. The Company undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

Forward Looking Statements

3

2006

• Revenues $456 million

• EPS $1.33

• Staff 4,300

1990

• Revenues $0.5 million

• Staff 5

The Journey So Far

2007 Guidance

• Revenues $615 - $625m

• EPS $1. 82 - $1.85

• Staff 5,500

2008 Guidance

• Revenues $750 - $770m

• EPS $2.27 - $2.36

• Staff 6,250

4

Global Full Service Clinical Development

US 53%

EU 41%

ROW 6%

Revenue by Region

5

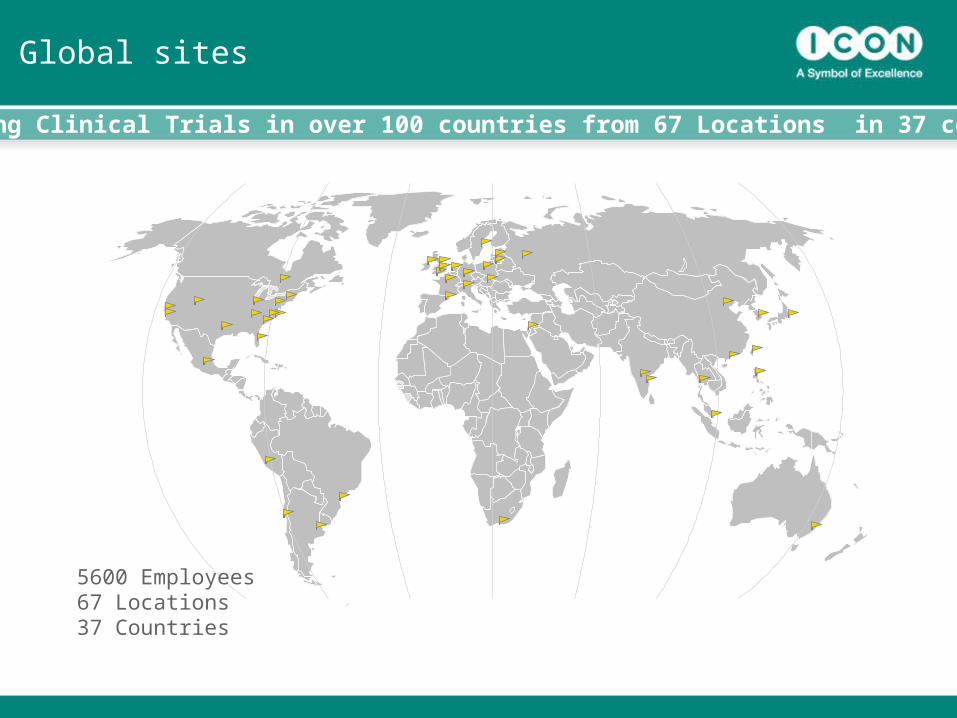

Global sites

5600 Employees67 Locations37 Countries

Conducting Clinical Trials in over 100 countries from 67 Locations in 37 countries

6

Market Environment

7

Strong Market Environment with...

• Fundamental R&D Spending Growth Trend 6%- 8% p.a.¯ Phase II / III pipelines strengthening

• Increased Outsourcing ¯ Being accelerated by activity & funding in Biotech / Speciality

¯ Globalisation of clinical research

¯ Cost containment pressures

¯ Evidence that projects, where CROs are engaged, complete faster than “internal only” studies*

¯ Growth c.15% p.a. since 2001*

• Increasing Regulation ¯ More patients/ more studies

¯ Post marketing surveillance

*Source: Tufts Centre for Study of Drug Development

8

$18.1

$22.4

$29.2

$33.1

$38.6

$0.0

$5.0

$10.0

$15.0

$20.0

$25.0

$30.0

$35.0

$40.0

$45.0

2003 2004 2005 2006 2007

$Bil

lio

n

Source: Burrill and Company

…US Biotech Funding Environment continuing to grow

Biotech fund raising ($billions)

9

956 9981,071

1,167 1,195

1,4811,599

1,720

1997 1998 1999 2000 2001 2002 2003 2004

Source: Informa Health

…significant growth in the number of companies with active clinical projects,….

Number of companies running clinical projects

10

…which is enriching pipelines.

0

200

400

600

800

1000

1200

Phase I Phase II Phase III Registration

Dec-02 Dec-03 Dec-04 Dec-05 Dec-06

Source: IMS R&D Focus, Dec 2006 and previous year SMRs

2002 – 2006 46% Growth Phase I – II

11

4,157

4,5444,827

5,023

5,445

3,8833,6113,600 3,661

2,000

3,000

4,000

5,000

6,000

1998 1999 2000 2001 2002 2003 2004 2005 2006

Source: FDA

Number of Active INDs

… and significant growth in the number of active INDs,…

49% Increase since 2000

12

ICON in this Market Environment

13

Strong Gross Business wins has led to…

$127

$165

$186 $189 $193$207

$245$264

$246

Q3 05 Q4 05 Q1 06 Q2 06 Q3 06 Q4 06 Q1 07 Q2 07 Q3 07

ICON Gross Business Wins - Last 9 Quarters ($ millions)

14

.. excellent Net New Business wins and very strong book to bill ratios…

$122

$140

$171$166

$157

$171

$223$230$230

Q3 05 Q4 05 Q1 06 Q2 06 Q3 06 Q4 06 Q1 07 Q2 07 Q3 07

1.4

1.6

1.3

1.6

1.41.3

1.6

1.7

1.6

Net Business Wins Book to Bill Ratio

15

…leading to record Total Backlog levels. ($ millions)

$568

$633

$707

$772$815

$872

$963

$1,049

$1,125

Q3 05 Q4 05 Q1 06 Q2 06 Q3 06 Q406 Q1 07 Q2 07 Q3 07

16

From this backlog, coverage of next 4 quarters revenues is robust……..

$279$296 $307

$360

$395$415

$470$493

$542

Q3 '05 Q4 '05 Q1 '06 Q2 '06 Q3 '06 Q4 '06 Q1 '07 Q2 07 Q3 '07

71%

76% 76% 76%76%

77%76%

77%

76%

Value of backlog forecast to be earned in next 4 quarters

% coverage of next 4 quarters forecast revenues

17

…..and the customer base continues to diversify.

42.6%

34.6%30.8%

62.7%

51.1%

45.0%

81.4%

72.0%

66.7%

8.1%9.6%12.3%

FY To May 2005 FY 2006 2007 YTD

Largest Client

Top 5

Top 10

Top 25

Client Concentration 2005, 2006, YTD 2007

18

YTD ‘07 Revenue Breakdown

Revenue by Customer Segment Revenue by Therapeutic Area

Estimate 2007 Revenue $620m*

* Mid Point of Calendar year Guidance issued October 2007

19

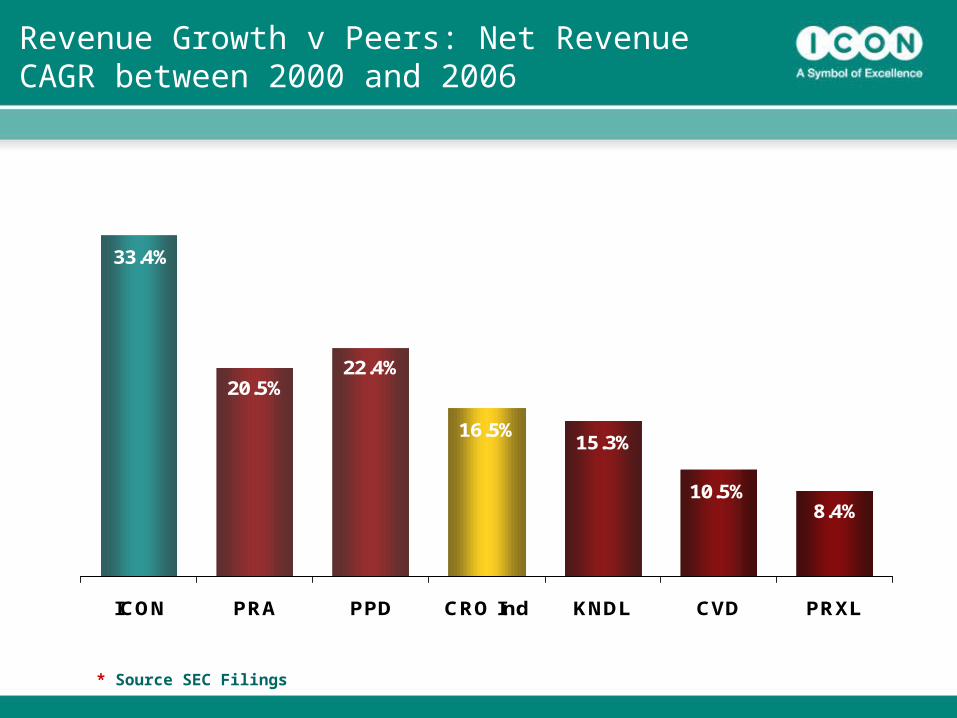

Revenue Growth v Peers: Net Revenue CAGR between 2000 and 2006

8.4%10.5%

15.3%16.5%

22.4%20.5%

33.4%

ICON PRA PPD CRO Ind KNDL CVD PRXL

* Source SEC Filings

20

Strategy

21

Core Strategy is Organic Growth, with acquisitions adding new services or scale.

Capitalise on market fundamentals to drive organic growth in all business units.

Expand geographic footprint to exploit globalisation.

Pursue acquisitions to enhance depth and scale of current operations and to add additional complementary services e.g.

Phase I

Bioanalytical / Biomarkers

Therapeutic specialists

Safety / Phase IV

Patient Recruitment

Staffing

Cross-sell services to grow sales and margin

22

Financial Performance

23

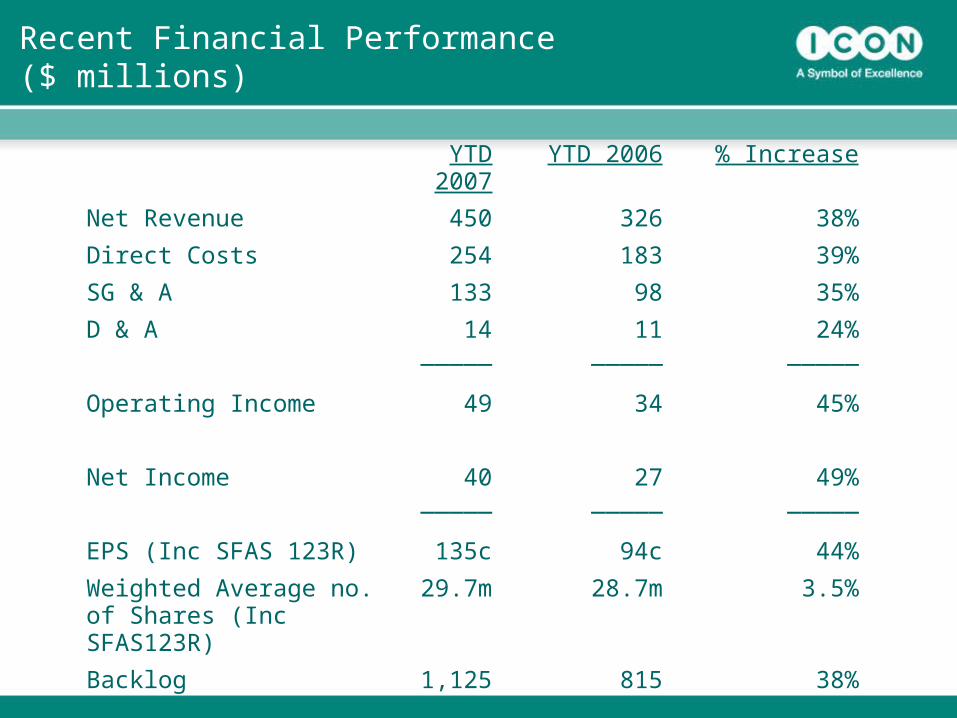

Recent Financial Performance ($ millions, except EPS; includes stock option expense)

Q3 ’07 Q3 ’06 % Increase

Net Revenue 167.0 120.7 38.3%

Direct Costs 91.7 68.4 34.1%

SG & A 51.5 35.8 43.9%

D & A 5 3.9 28%_____ _____ _____

Operating Income 18.7 12.6 48.3%

Net Income 14.5 10.1 43.7%_____ _____ _____

EPS (Inc SFAS123R) 49c 35c 40%

Weighted Average no. of Shares (Inc SFAS123R)

29.8m 29.1m 2.4%

Backlog 1125 815 38%

24

Recent Financial Performance ($ millions)

YTD 2007

YTD 2006 % Increase

Net Revenue 450 326 38%

Direct Costs 254 183 39%

SG & A 133 98 35%

D & A 14 11 24%_____ _____ _____

Operating Income 49 34 45%

Net Income 40 27 49%_____ _____ _____

EPS (Inc SFAS 123R) 135c 94c 44%

Weighted Average no. of Shares (Inc SFAS123R)

29.7m 28.7m 3.5%

Backlog 1,125 815 38%

25

Net Revenue CAGR in excess of 30% over 6 Years

$157

$226

$296$327

$456

$620(E)*

$0

$100

$200

$300

$400

$500

$600

$700

FY2002 FY2003 FY2004 FY2005 FY2006 FY2007

Mill

ions

CAGR 31.6%

* Mid Point of Calendar year Guidance issued October 2007

** Mid Point of Calendar year Guidance issued December, 2007

$760(E)**

FY2008(E)(E)

26

Earnings Per Share Growth

$0.58

$0.75

$0.94$0.85

$1.84(E)*

$1.35

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

$1.80

$2.00

FY2002 FY2003 FY2004 FY2005 FY2006 FY2007

CAGR 25.9%

(E)

** Mid Point of Guidance issued December 2007* Mid Point of Guidance issued October 2007

$2.32(E)**

FY2008(E)

27

Summary Balance Sheet and Cash Flow ($ millions)

May 31, 05(Year)

Dec 31, 05(7 mths)

Dec 31, 06(Year)

Sept 30, 07 (YTD)

Net Cash $78.4 $82.3 $98 $27.7

Total assets $347.6 $349.1 $476.3 $631.8

Shareholder’s equity $233.1 $241.6 $302.7 $631.8

Cashflow from operations

$23.8 $11.7 $51.5 $0.6

Capital expenditures $15.6 $7.8 $12.3 $19.3

Shares outstanding 27.8 28.0 28.5 29.8

28

Improving Margins

29

Quarterly Operating margins have beenimproving and ….

10.8%

11.20%

10.7%10.4%

10.6%

10.2%

9.2%

8.7%

7.6%

10.9%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

Q2 2005 Q32005*

Q42005*

Q12006*

Q2 2006 Q3 2006 Q4 2006 Q1 2007 Q2 2007 Q3 2007

* Includes an estimated SFAS 123 non cash stock compensation charge for the 2005 figures

Turnaround in Lab

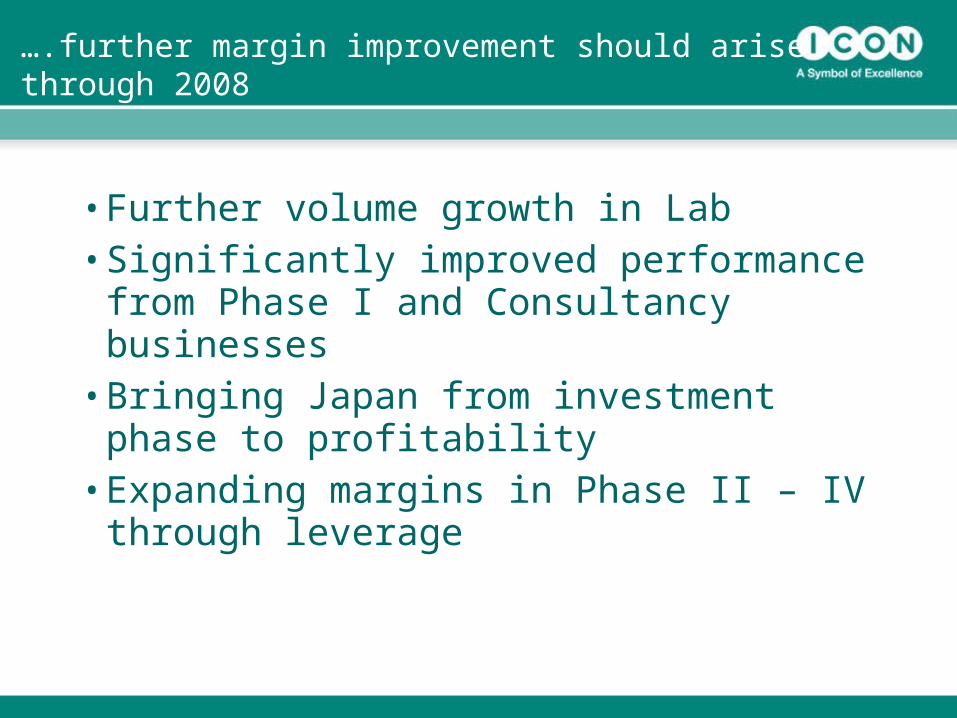

30

• Further volume growth in Lab • Significantly improved performance from Phase

I and Consultancy businesses • Bringing Japan from investment phase to

profitability • Expanding margins in Phase II – IV through

leverage

….further margin improvement should arisethrough 2008

31

• Top Global Clinical CRO - #4• Outstanding record of growth • Strong market fundamentals • Excellent strategic position• Strong balance sheet• Margin expansion opportunity

Investment Case Summary