Embed Size (px)

Citation preview

1

Konceptudvikling til interaktivt digitalt tv og Konceptudvikling til interaktivt digitalt tv og bredbåndbredbånd

Modul 1 28. august 2001Modul 1 28. august 2001

Peter Olaf LoomsPeter Olaf Looms

2

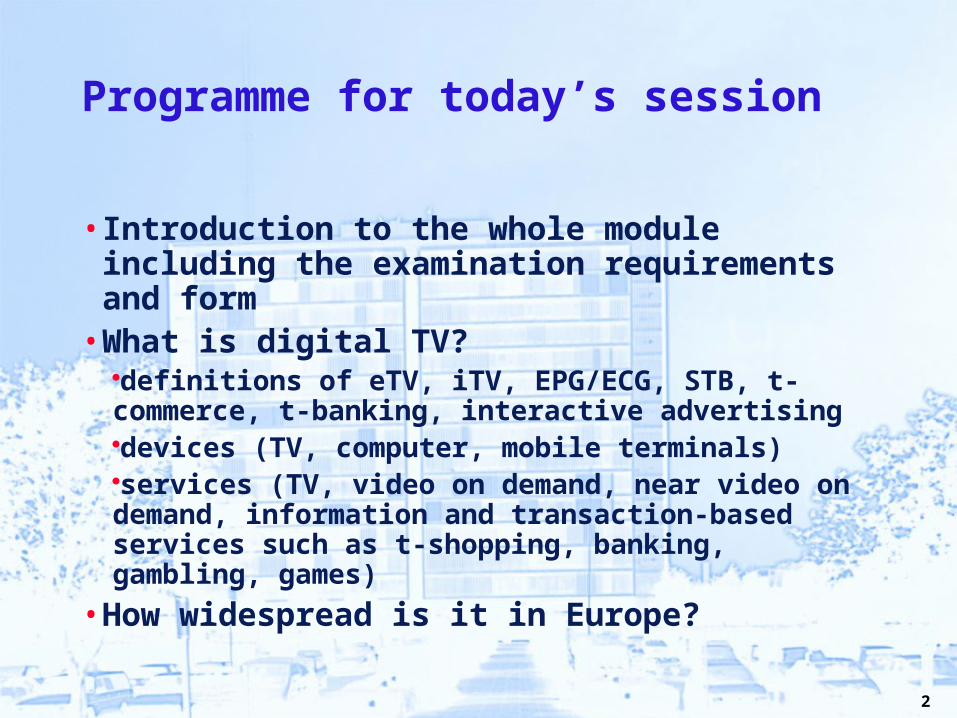

Programme for today’s session

• Introduction to the whole module including the examination requirements and form

• What is digital TV?definitions of eTV, iTV, EPG/ECG, STB, t-commerce, t-banking, interactive advertising devices (TV, computer, mobile terminals)services (TV, video on demand, near video on demand, information and transaction-based services such as t-shopping, banking, gambling, games)

• How widespread is it in Europe?

3

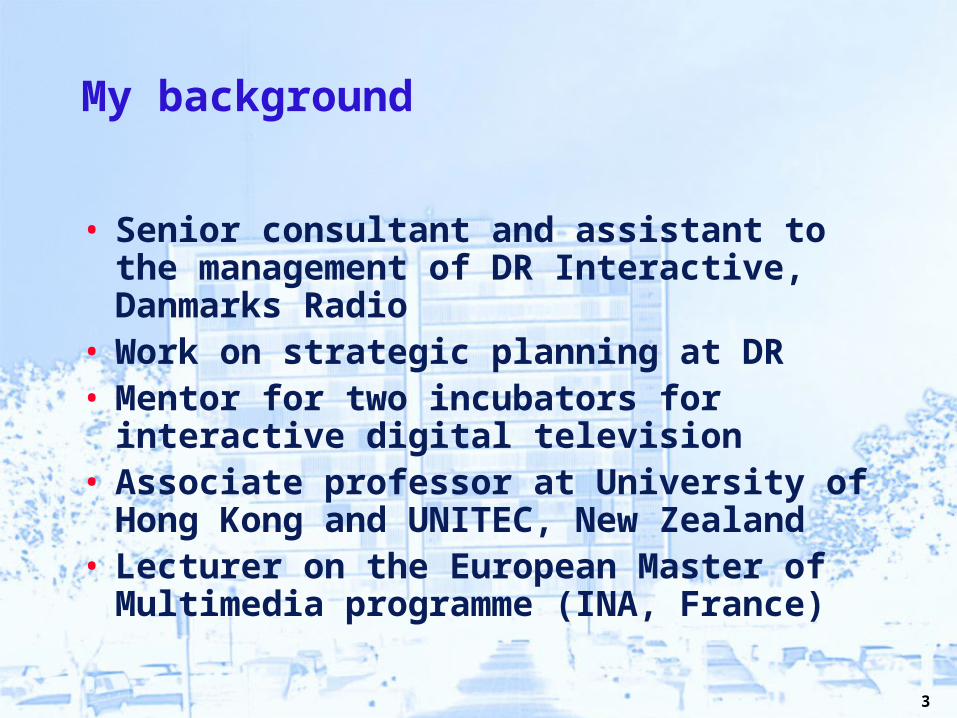

My background

• Senior consultant and assistant to the management of DR Interactive, Danmarks Radio

• Work on strategic planning at DR• Mentor for two incubators for interactive digital

television• Associate professor at University of Hong Kong and

UNITEC, New Zealand• Lecturer on the European Master of Multimedia

programme (INA, France)

4

1. What is digital television?

Depends on whether you are• A viewer• A broadcaster• An operator• A politician

• Handout in Danish

5

1. What is digital television?

• MoreMore programmes (also RADIO programmes) programmes (also RADIO programmes)

6

1. What is digital television?

• More programmes (also RADIO programmes)• Better technical quality• New ways of finding programmes...

7

1. What is digital television?

• More programmes (also RADIO programmes)• Better technical quality• New ways of finding programmes...• New services (2nd Generation TTV, digital text channels

which enhance programmes)

8

1. What is digital television?

• More programmes (also RADIO programmes)• Better technical quality• New ways of finding programmes...• New services (2nd Generation TTV, digital text channels

which enhance programmes)

9

1. What is digital television?

• More programmes (also RADIO programmes)• Better technical quality• New ways of finding programmes...• New services (2nd Generation TTV, digital text channels which enhance

programmes)• Enhanced programmes (i.e. interactivity with no back channel to the

broadcaster)...

10

1. What is digital television?

• More programmes (also RADIO programmes)• Better technical quality• New ways of finding programmes...• New services (2nd Generation TTV, digital text channels which enhance

programmes)• Enhanced programmes (i.e. interactivity with no back channel to the

broadcaster)...• Interactive programmer such as ROFL (with back channel )

11

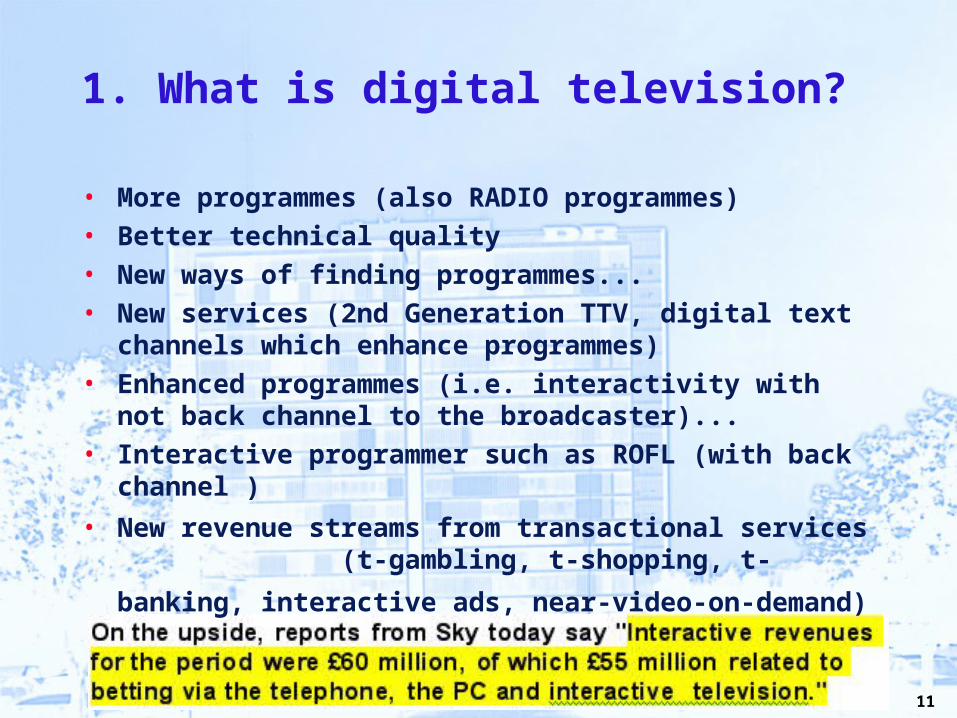

1. What is digital television?

• More programmes (also RADIO programmes)• Better technical quality• New ways of finding programmes...• New services (2nd Generation TTV, digital text channels which enhance

programmes)• Enhanced programmes (i.e. interactivity with not back channel to the

broadcaster)...• Interactive programmer such as ROFL (with back channel )• New revenue streams from transactional services (t-gambling, t-

shopping, t-banking, interactive ads, near-video-on-demand)

12

13

Kompendiet:Kan fås fra Annette på 2. sal

14

2. The development of broadband and digital television in selected national and European markets

Source: House DTV Penetration 2001 Jupiter Communications

15

Europe 9%Europe 9%UK 25%UK 25%USA 7.5%USA 7.5%

Source: House DTV Penetration 2001 Jupiter Communications

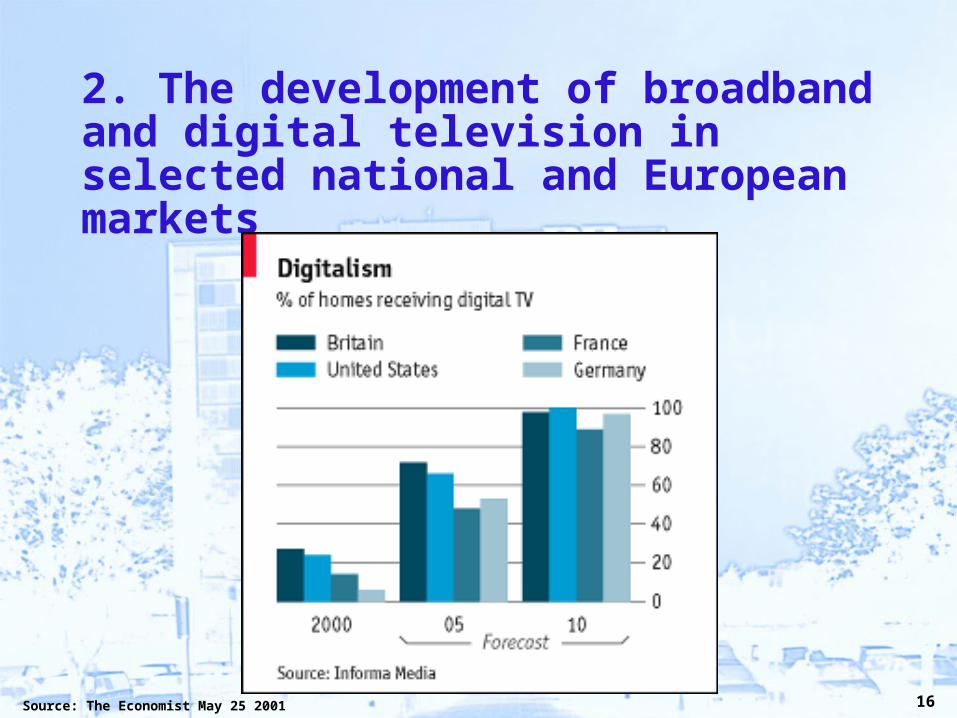

2. The development of broadband and digital television in selected national and European markets

16

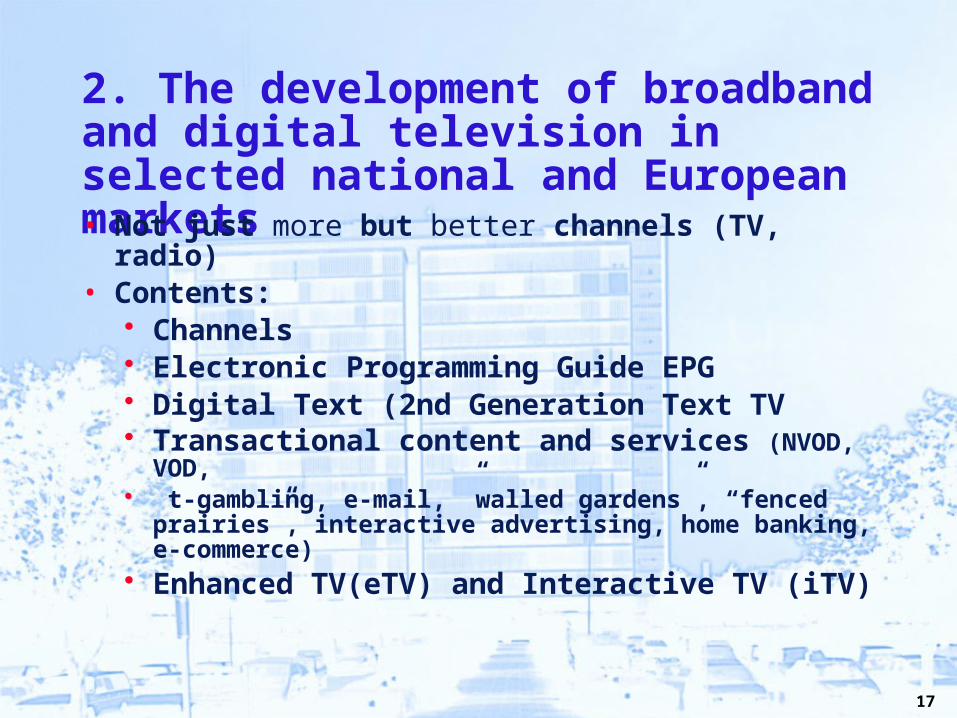

2. The development of broadband and digital television in selected national and European markets

Source: The Economist May 25 2001

17

2. The development of broadband and digital television in selected national and European markets• Not just more but better channels (TV, radio)• Contents:

Channels Electronic Programming Guide EPG Digital Text (2nd Generation Text TV Transactional content and services (NVOD, VOD, t-gambling, e-mail, ”walled gardens”, “fenced prairies”,

interactive advertising, home banking, e-commerce) Enhanced TV(eTV) and Interactive TV (iTV)

18

2. The development of broadband and digital television in selected national and European markets• Broadcaster no longer has direct relationship with viewer -

ménage a trois with digital TV operator• Serious legal and ethical implications about the transfer of

data between broadcaster and operator (legislation on personal data and public databases)

19

2. The development of broadband and digital television in selected national and European markets

20

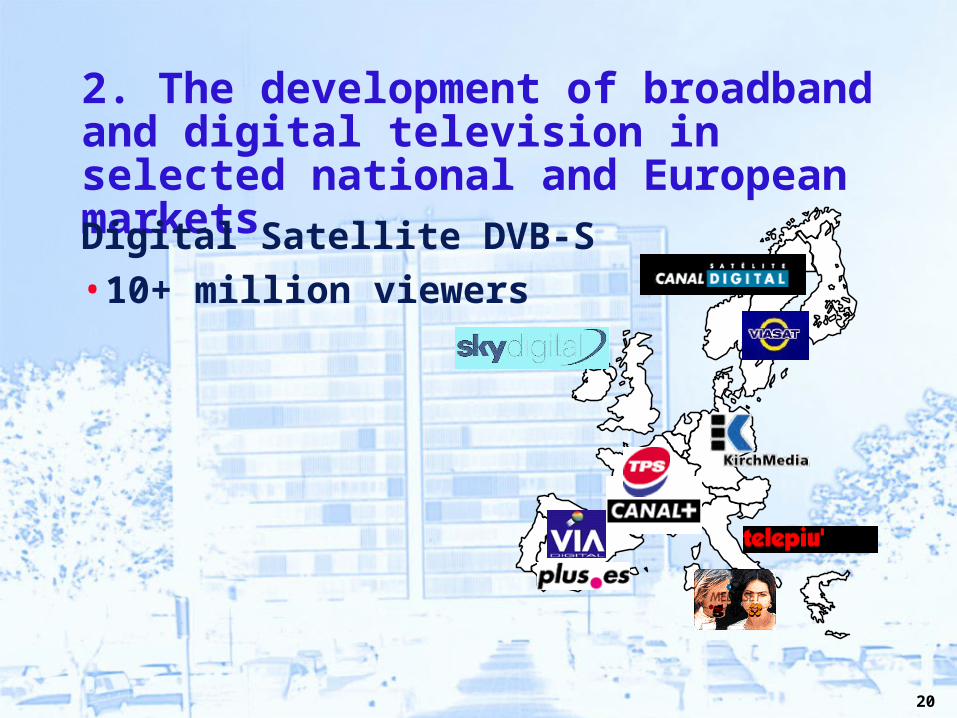

2. The development of broadband and digital television in selected national and European marketsDigital Satellite DVB-S• 10+ million viewers

21

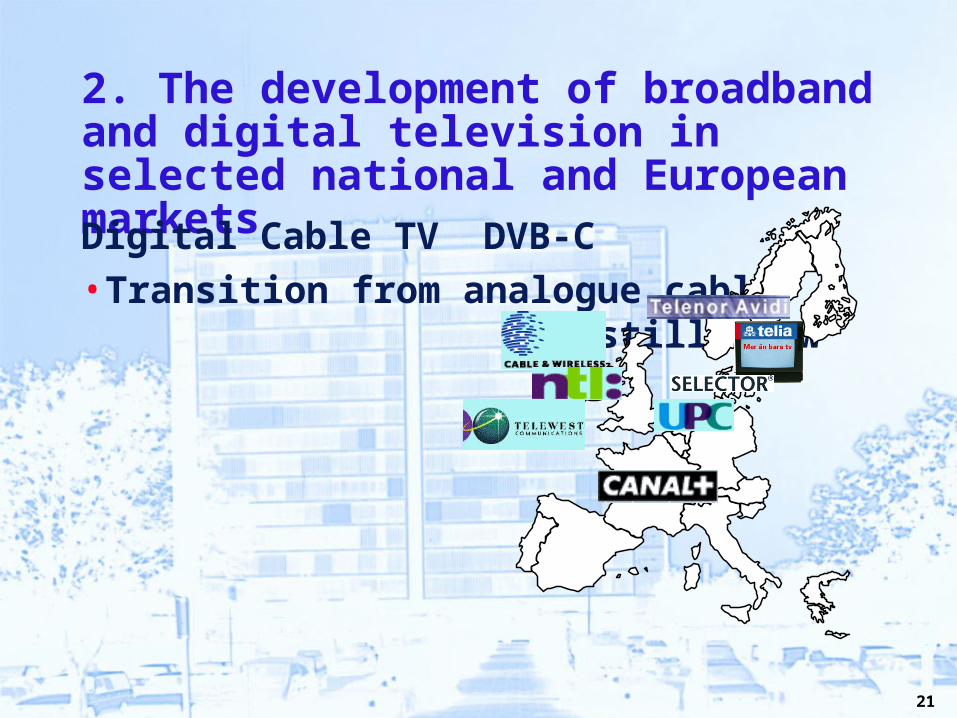

2. The development of broadband and digital television in selected national and European marketsDigital Cable TV DVB-C• Transition from analogue cable still

slow

22

2. The development of broadband and digital television in selected national and European marketsDigital Terrestrial TV DVB-T• 2002 will be ”make or break” year for

DVB-T in Europe

• DVB-T goes into service in 2002

New name:New name:

ITV.digitalITV.digitalPlatcoPlatco

23

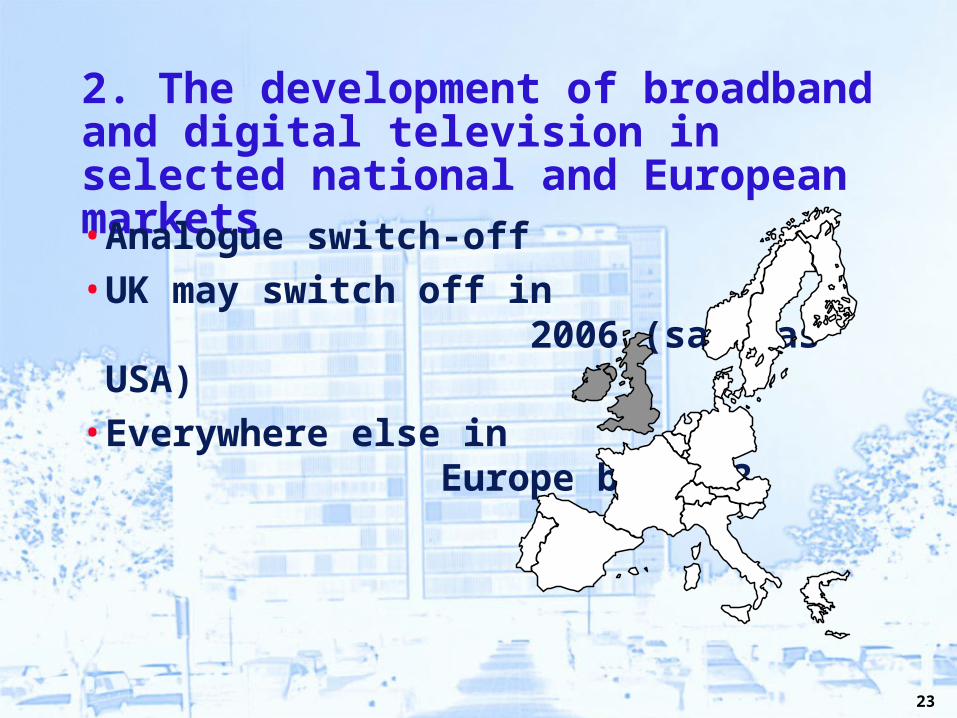

2. The development of broadband and digital television in selected national and European markets• Analogue switch-off• UK may switch off in 2006 (same

as USA)• Everywhere else in Europe by 2013

24

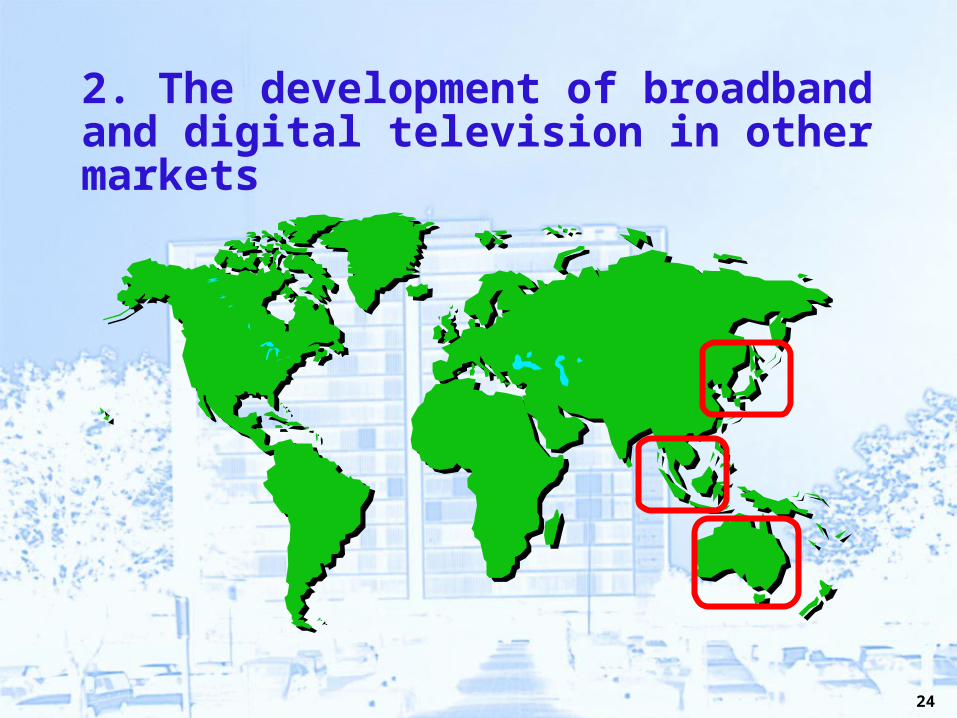

2. The development of broadband and digital television in other markets

25

26

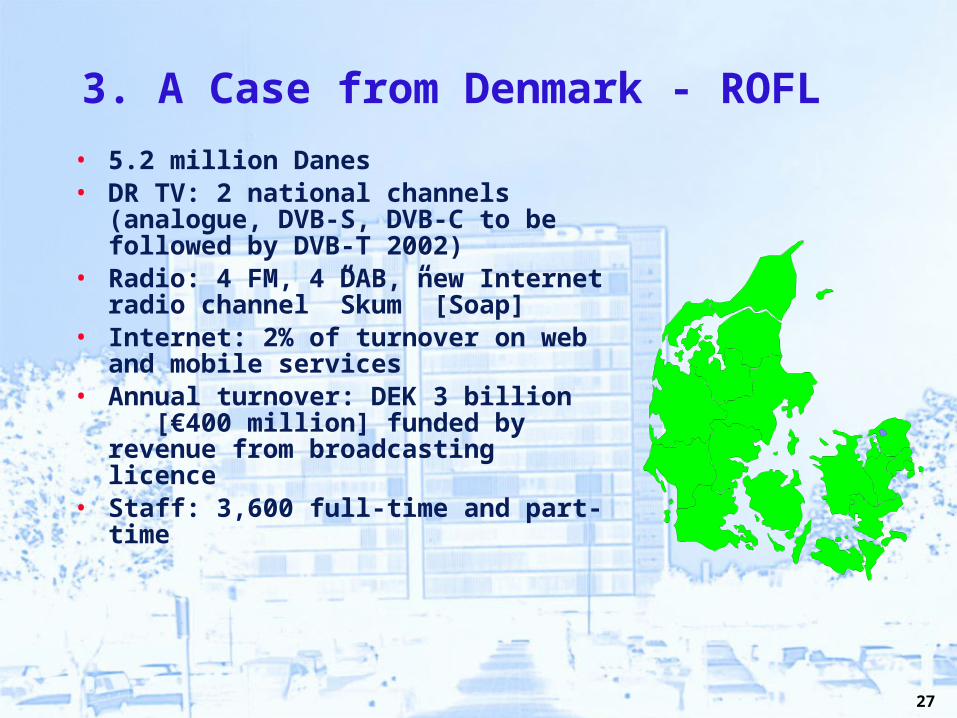

3. A Case from Denmark - ROFL

27

3. A Case from Denmark - ROFL

• 5.2 million Danes • DR TV: 2 national channels (analogue, DVB-S,

DVB-C to be followed by DVB-T 2002)• Radio: 4 FM, 4 DAB, new Internet radio channel

”Skum” [Soap]• Internet: 2% of turnover on web and mobile

services• Annual turnover: DEK 3 billion [€400 million]

funded by revenue from broadcasting licence• Staff: 3,600 full-time and part-time

28

ROFL - Original Aims

• June 1998: need to clarify the added value of enhanced and interactive television for our viewers

• ”The Digital Kitty”: Internal competition for a kitty of DEK 8 million [€ 1 million] - the winner takes it all

• November 1998: BetaLab wins the kitty but additional funding found for ”Digital Children” i.e. 2 projects instead of 1

29

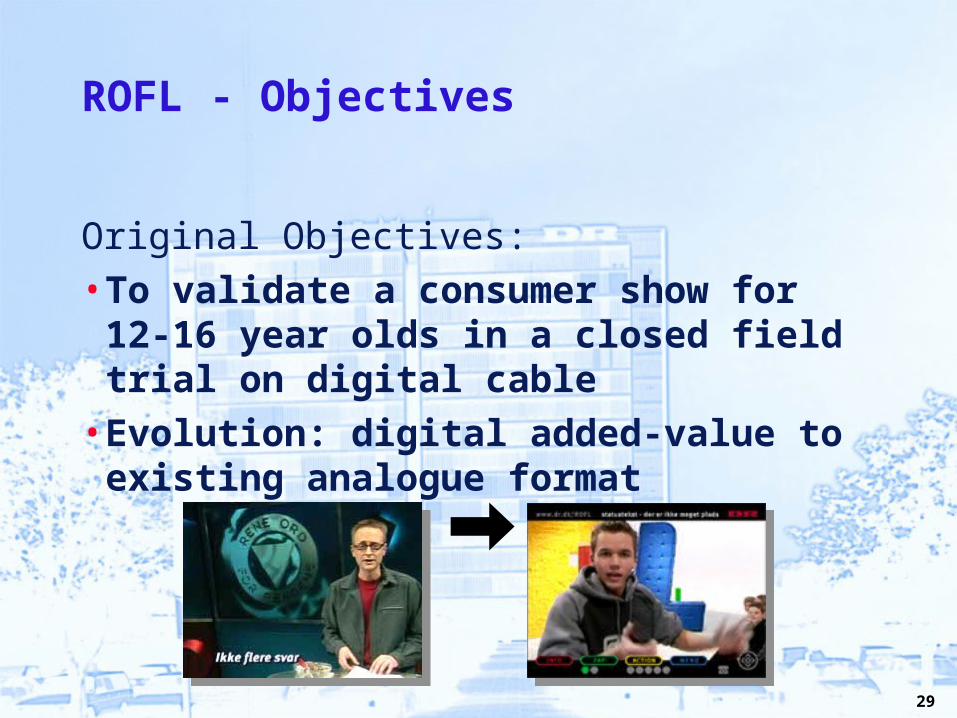

ROFL - Objectives

Original Objectives: • To validate a consumer show for 12-16 year olds in a

closed field trial on digital cable• Evolution: digital added-value to existing analogue

format

30

ROFL - Method

Method: • Production of a simulated format on a television set• Focus group tests• Production of a dummy tested

in November 1999

31

ROFL - theory and Murphy

• Format developed and simulator validated on time but…

• Delays negotiating details of fiield trial - 14 months!

Change of tactics: • Field trial replaced by full-scale launch on digital cable and

satellite• Tele Danmark Cable, NSAB and Viasat as partners• Initial scheduling of show with 20 programmes started January 23

2001

32

Video demo

33

34

ROFL and digital TV strategy

• ”Digital added-value” from the viewpoint of viewer• Added value currently perceived to be more choice and better technical

quality• No felt need for interactivity, therefore need to

raise awareness…

”Interactive Lighthouse or Beacon”

35

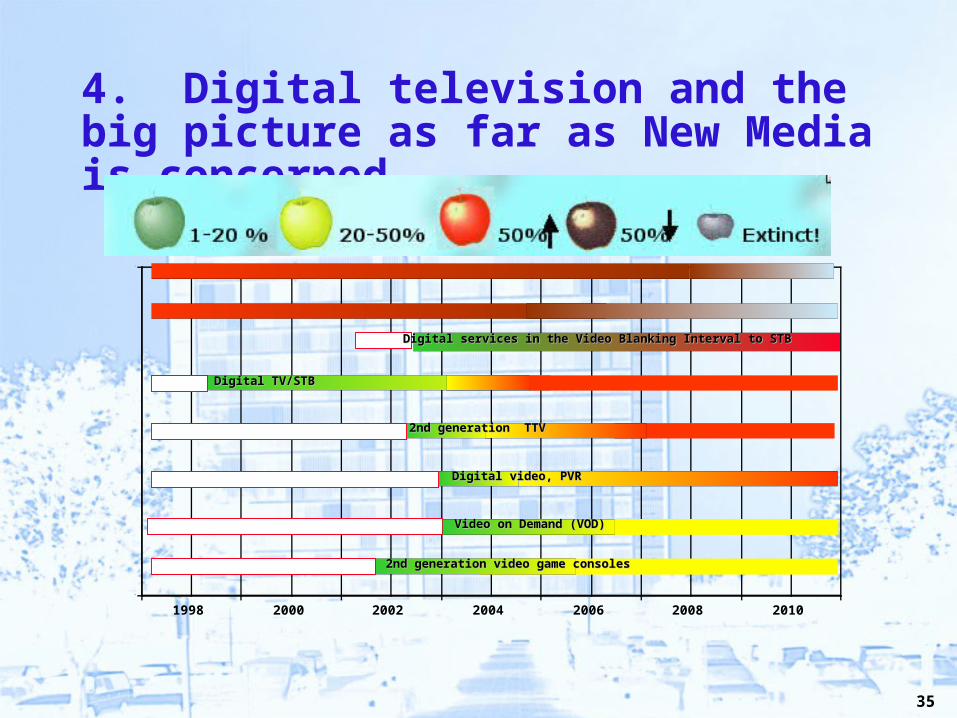

4. Digital television and the big picture as far as New Media is concerned

0

1

1998 2000 2002 2004 2006 2008 2010

1-20 % 20-50% 50% 50% Død!

Digital TV/STBDigital TV/STB

2nd generation TTV2nd generation TTV

Digital video, PVRDigital video, PVR

2nd generation video game consoles2nd generation video game consoles

Video on Demand (VOD) Video on Demand (VOD)

Digital services in the Video Blanking Interval to STBDigital services in the Video Blanking Interval to STB

36

4. Digital television and the big picture as far as New Media is concerned

• Multiple channel universe• Mutiple digital channel universe seems to be

different from analogue• As the competition increases, the share is likely to

drop• Commercial broadcasters still depend on advertising• Drop in share = less money for programme making

37

Some of the competition for media and services on television screens....

38

Set-top boxes (digital TV)

Kilde: Nokia (2000)

39

Video On Demand (VOD)

Kilde: Logos fra Egmont, TV2, Tele Danmark, boks fra Nokia

40

Personal Video Recorders (PVR)

Kilde: Logo fra TiVO (1999)

Take a look at the emerging standard for PVRs in Take a look at the emerging standard for PVRs in Europe based on DVB and MHP called TV-Anytime Europe based on DVB and MHP called TV-Anytime from the TV-Anytime Forumfrom the TV-Anytime Forum

41

Video game consoles

Kilde: Logos fra Sony, Microsoft, Nintendo (2001)

42

All in one devicesbased on televisions

Kilde:)

43

44

45

46

4. Digital television and the big picture as far as New Media is concerned

• Awake 1,000 minutes daily• Max. 250 mins. of this “to do our own thing” incl.

watching TV

47

4. Digital television and the big picture as far as New Media is concerned

-

500

1,000

1,500

2,000

2,500

3,000

Kl.6-7

Kl.7-8

Kl.8-9

Kl.9-10

Kl.10-11

Kl.11-12

Kl.12-13

Kl.13-14

Kl.14-15

Kl.15-16

Kl.16-17

Kl.17-18

Kl.18-19

Kl.19-20

Kl.20-21

Kl.21-22

Kl.22-23

Kl.23-24

Kl.24-01

TV el video Radio Internet/60%60%

40%40%

20%20%

0%0%

48

-10

-5

0

5

10

15

20

25

30

35

12-19/20 år TV+R 97 12-20 år TV+R 00 12-20 år TV+RA 2000 minus 1997

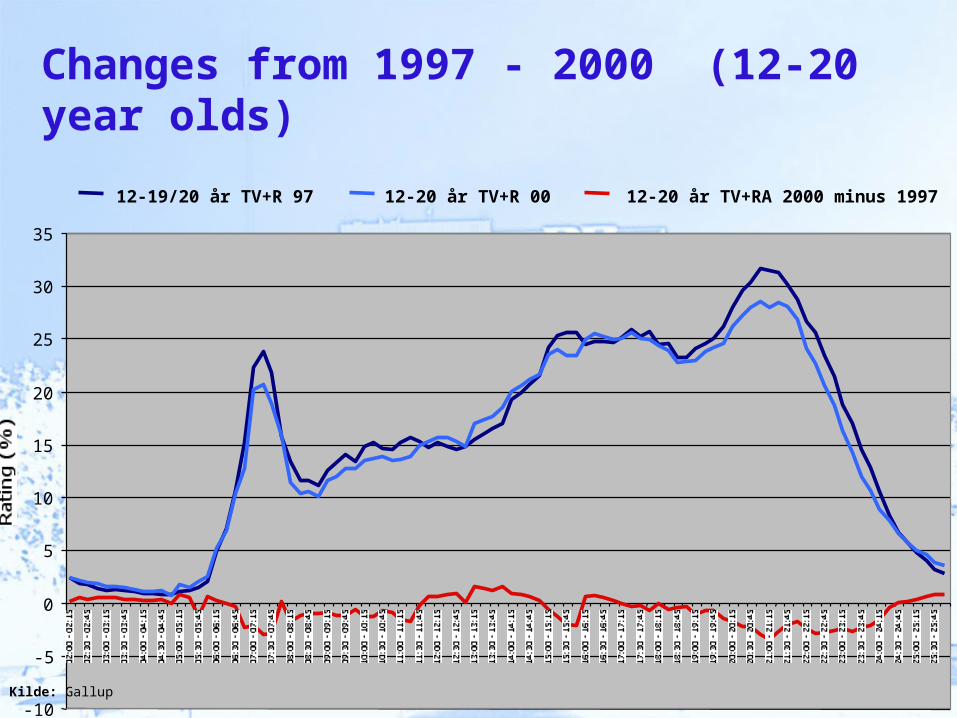

Changes from 1997 - 2000 (12-20 year olds)

Kilde: Gallup

49

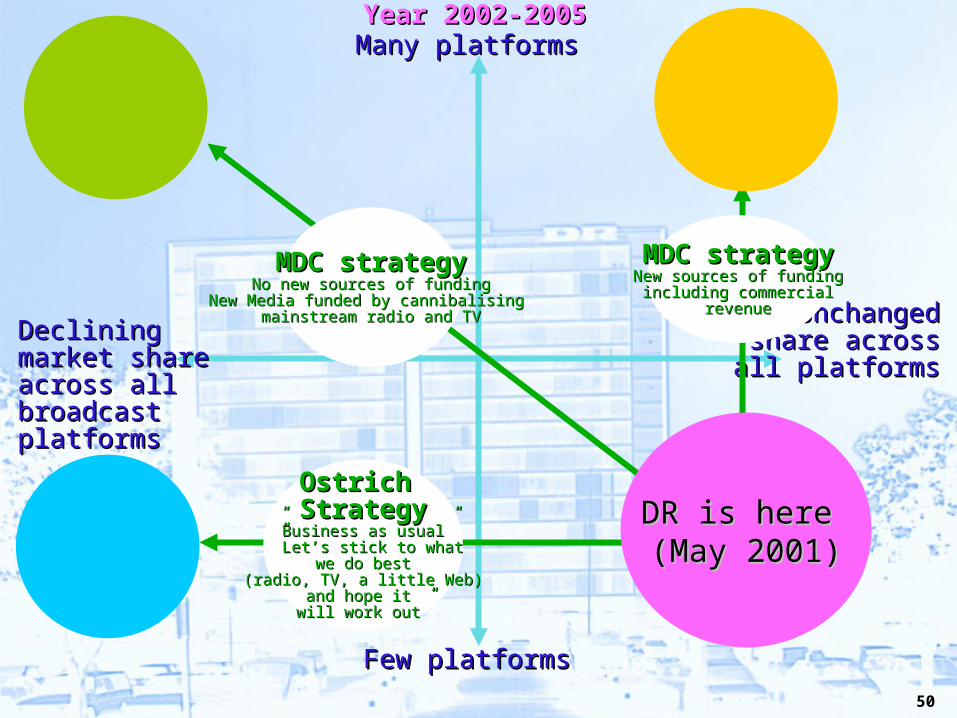

Year 2002-2005Year 2002-2005Many platformsMany platforms

Declining market share Declining market share across all broadcast across all broadcast platformsplatforms

Few platformsFew platforms

Unchanged share Unchanged share across all platformsacross all platforms

DR is here DR is here (May 2001)(May 2001)

50

Year 2002-2005Year 2002-2005Many platformsMany platforms

Declining market share Declining market share across all broadcast across all broadcast platformsplatforms

Few platformsFew platforms

Unchanged share Unchanged share across all platformsacross all platforms

Ostrich Ostrich StrategyStrategy

””Business as usual”Business as usual” ” ”Let’s stick to whatLet’s stick to what

we do bestwe do best(radio, TV, a little Web)(radio, TV, a little Web)

and hope it and hope it will work out”will work out”

MDC strategyMDC strategyNo new sources of fundingNo new sources of funding

New Media funded by cannibalising New Media funded by cannibalising mainstream radio and TVmainstream radio and TV

MDC strategyMDC strategyNew sources of fundingNew sources of funding

including commercialincluding commercialrevenuerevenue

DR is here DR is here (May 2001)(May 2001)

51

Many platformsMany platforms

Declining market share Declining market share across all broadcast across all broadcast platformsplatforms

Few platformsFew platforms

UnchangedUnchanged share share across all platformsacross all platforms

Year 2002-2005Year 2002-2005

Ostrich Ostrich StrategyStrategy

””Business as usual”Business as usual” ” ”Let’s stick to whatLet’s stick to what

we do bestwe do best(radio, TV, a little Web)(radio, TV, a little Web)

and hope it and hope it will work out”will work out”

MDC strategyMDC strategyNo new sources of fundingNo new sources of funding

New Media funded by cannibalising New Media funded by cannibalising mainstream radio and TVmainstream radio and TV

MDC strategyMDC strategyNew sources of fundingNew sources of funding

including commercialincluding commercialrevenuerevenue

DR maintains its DR maintains its cross platform reach at cross platform reach at

91% of Danes 91% of Danes across all platforms and across all platforms and

continues to be socially inclusive, continues to be socially inclusive, to promote democracy to promote democracy in a fragmented worldin a fragmented world

DR maintains its DR maintains its share of younger viewers share of younger viewers

but risks alienatingbut risks alienating mature audiencesmature audiences

DR is here DR is here (May 2001)(May 2001)

DR maintains its share DR maintains its share of radio and TV of radio and TV

but its reach drops but its reach drops

52

5. The exam itself...

• E Day minus 2 weeks... 8 existing TV shows to choose from - an eTV or iTV

version has to be the result A week to familiarise yourself with the show

• E Day minus 1 week… Demographic data (audience research) CLICK A week to familiarise yourself with it CLICK

• E day 09:00 The task itself and 6 hours to handle it

53

Task 1 of 3

• Task• Using one of the eight shows listed below, prepare a

pitching document for use when meeting with a broadcaster or production company.

54

Task 2 of 3

• The submission must include• An illustrated document outlining the proposed

enhancements to the show selected• An estimate of the budget required to produce a dummy and

simulator (e.g.. MacroMedia Director /QT) and for focus group tests. Remember to include your own time in the budget

55

Task 3 of 3

The 8 options were:

1. DEN STORE MISSION2. EN NATURLIG FORKLARING3. LÆGENS BORD4. SØNDAGSSPORTEN5. STATION 26. VOXTOP OG VOXPOP7. ÅNDERNES MAGT8. T-commerce on Viasat (CD’s)

56

Outcomes

• Cathrine Catharine's slides

57

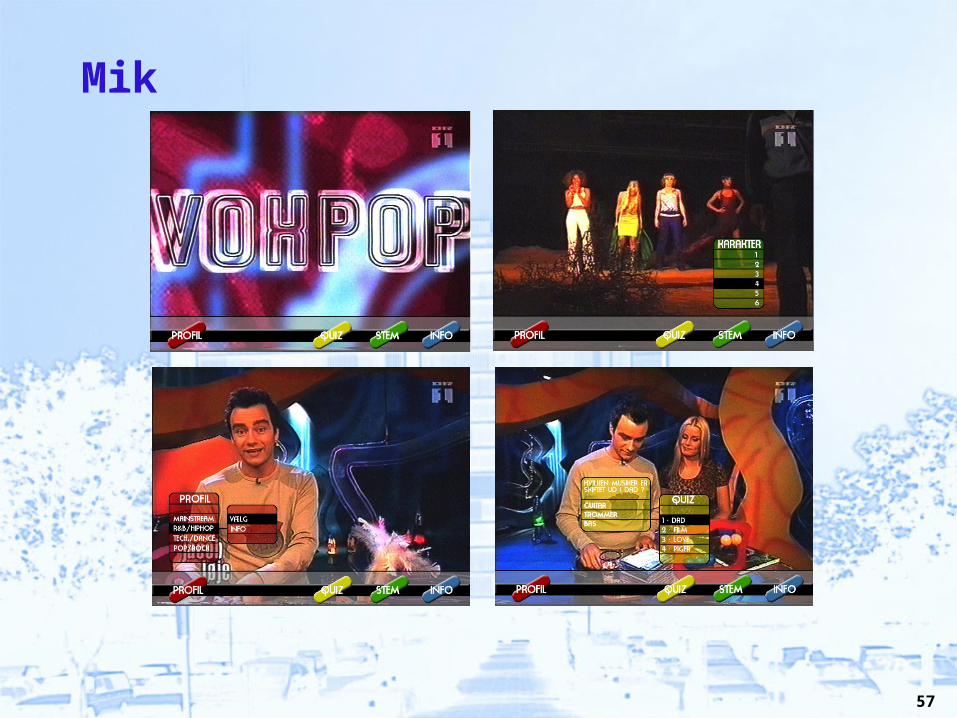

Mik

58

Outcomes

• A commissioning editor and a technologist as external examiners

• 13 of the 15 students passed• Feedback on individual submissions• Suggestions to form new groups• 4 groups pitched to broadcasters and production

companies• Dummy production of 1 (2)

59

Contact Details:

Peter Olaf LoomsDanmarks RadioDR InteraktivTV-ByenDK-2860 SøborgDENMARK

[email protected] eller [email protected]: 40 71 43 50