Embed Size (px)

Citation preview

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 1/64

Company

LOGO

TAXATION

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 2/64

…nothing is certain, but

death and taxes.B. Franklin

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 3/64

– What difference is there between taxesand theft?

– What justifies any taxation?

– What right does the government have totake some of our money?

– What right does the government have to

tax at all? – Why should the government get any part

of the profit from selling something I own?

– What's the best tax scheme?

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 4/64

History• During the reign of Egyptian

Pharaohs• Scribes as tax collectors

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 5/64

• The first known system of taxation was in Ancient Egypt around 3000 BC - 2800 BC inthe first dynasty of the Old Kingdom.

• The earliest and most widespread form oftaxation was the corvée and tithe.

• The corvée was forced labour provided to

the state by peasants too poor to pay otherforms of taxation (labour in ancient Egyptianis a synonym for taxes).

• .

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 6/64

• Records from the time document thatthe pharaoh would conduct a biennialtour of the kingdom, collecting tithesfrom the people.

• Other records are granary receipts on

limestone flakes and papyrus.

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 7/64

• During one period the scribes imposed atax on cooking oil.

• To insure that citizens were not avoiding

the cooking oil tax scribes would audithouseholds to insure that appropriateamounts of cooking oil were consumed

and that citizens were not using leavingsgenerated by other cooking processes asa substitute for the taxed oil.

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 8/64

• Early taxation is also described inthe Bible. In Genesis (chapter 47, verse24 - the New International Version),

• it states "But when the crop comes in,give a fifth of it to Pharaoh. The otherfour-fifths you may keep as seed for the

fields and as food for yourselves andyour households and your children".

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 9/64

• In the Quran

• People are merely entrusted with wealthfor their livelihood in this world. They are

allowed to hold property and enjoy thebenefits so long as they understand thatthey are holding the property in trust and

they must follow the God’s rule.

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 10/64

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 11/64

History

• In Greece• A tax referred to as Eisphora was

imposed only in times of war. No one was

exempt from the tax which was used topay for special wartime expenditures.

• However, rescinded the tax once the

emergency was over. When additionalresources were gained by the war effortthe resources were used to refund the tax

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 12/64

History

• In Athens• A monthly tax called Metoikon wascollected to foreigners . poll tax on

foreigners, people who did not haveboth an Athenian Mother and Father,of one drachma for men and a half

drachma for women.

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 13/64

• Earliest taxes in Rome• Taxes known as Portoria were customs

duties on imports and exports

• Caesar Augustus was consider by many tobe the most brilliant tax strategist of theRoman Empire. During this period cities

were given the responsibility for collectingtaxes. Caesar Augustus instituted aninheritance tax to provide retirement funds

for the military. The tax was 5 percent on allinheritances exce t ifts to children and s ouses.

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 14/64

• During the time of Julius Caesar a 1percent sales tax was imposed. Duringthe time of Caesar Augustus the sales tax

was 4 percent for slaves and 1 percent foreverything else.1

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 15/64

• In England• The first tax assessed in England was during

occupation by the Roman Empire

• Taxes were first used as an emergencymeasure

• When Rome fell, the Saxon kings imposedtaxes, referred to as Danegeld , on land andproperty. The kings also imposed substantialcustoms duties.

• Taxes on income or capital were a recent

development as a result of increasing

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 16/64

• In India, Islamic rulersimposed jizya (a poll tax on non-Muslims) starting in the 11th century.It was abolished by Akbar .

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 17/64

TAX REVOLT

• Because taxation is often perceived asoppressive, governments have alwaysstruggled with tax noncompliance and

resistance. Indeed, it has been suggestedthat tax resistance played a significant rolein the collapse of several empires,

including the Egyptian, Roman, Spanish,and Aztec.

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 18/64

• One of the most famous events in American Colonial history was the BostonTea Party, an incident where colonists

dressed up like Indians and threw barrelsof tea off ships into Boston harbor toprotest levies imposed on the popular

commodity.

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 19/64

• In 60 A.D. Boadicea, queen of East Anglialed a revolt that can be attributed tocorrupt tax collectors in the BritishIsles. Her revolt allegedly killed all Romansoldiers within 100 miles; seized London;and it is said that over 80,000 people werekilled during the revolt. The Queen was

able to raise an army of 230,000. Therevolt was crushed by Emperor Nero andresulted in the appointment of new

administrators for the British Isles.1

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 20/64

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 21/64

• The 100 years War (the conflict betweenEngland and France) began in 1337 andended in 1453. One of the key factors that

renewed fighting in 1369 was the rebellionof the nobles of Aquitaine over theoppressive tax policies of Edward, The

Black Prince.

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 22/64

• In Modern Industrial Nations• The government designates a taxbase (such as income, propertyholdings, or a given commodity)

• A Tax Law is a body of rules passedby the legislature by which thegovernment acquires a claim on taxpayers to convey, transfer and pay tothe public authority

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 23/64

Effects of Taxation

• Personal Income Tax which is presumed to fallentirely on the legal taxpayers influencesdecisions to work, save, and invest. Thesedecisions affect other people.

• Corporate Income Tax may simply result tolower corporate profits and dividends. It mayreduce their income of all owners of property

and businesses. The company may movetoward raising the prices of their products

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 24/64

• The system of compulsorycontributions levied by a governmentor other qualified body on people,

corporations and property in order tofund public expenditures.

• An inherent power of the state toraise income and to demand enforcedcontributions for public purposes.

Definition

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 25/64

• the process by which thesovereign country, through its law – making body, raises revenue todefray the necessary expenses of thegovernment

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 26/64

ESSENTIAL CHARACTERISTICS

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 27/64

ESSENTIAL CHARACTERISTICS

OF TAX

It is an enforced contribution – Tax is not a voluntary payment or

donation

– Its imposition is no way dependent uponthe will or assent of the persons tax

It is generally payable in money

– It is an exaction to be discharged alonein money which must be in legal tender

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 28/64

It is proportionate in character – It is ordinarily based on the ability to pay

It is levied on persons or property

– Tax may be imposed on acts ortransactions or contracts

It is levied by the state which has

jurisdiction over the person orproperty

– The persons or property must be subjectto the urisdiction of the taxin state

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 29/64

It is levied by the law – making body ofthe state

– The power to tax is a legislative power

which only the legislative body canexercise through the enactment ofstatutes or ordinances

It is levied for public purposes – Taxation and tax involves a charge or

burden imposed to provide income for

public purposes

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 30/64

It is inherent in sovereignty – The power of taxation is inherent to

sovereignty by being essential to the

existence of every governmentIt is legislative in character

– Under the Constitution only legislative

body can impose taxes – Power to tax is also granted to local

government subject to limitations

y o governments

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 31/64

y o governments

impose taxes?

–Rais ing money for governmentspending. The most obvious reason is toraise money for all the expenditure that is

required so that persons can live in acivilized society. Hospitals, schools, thedefense system, the welfare state; thesethings do not come cheaply. Local taxes

also have to be levied to help pay forlibraries, cleaning the roads, local parksand the local council administration to

name just a few items.

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 32/64

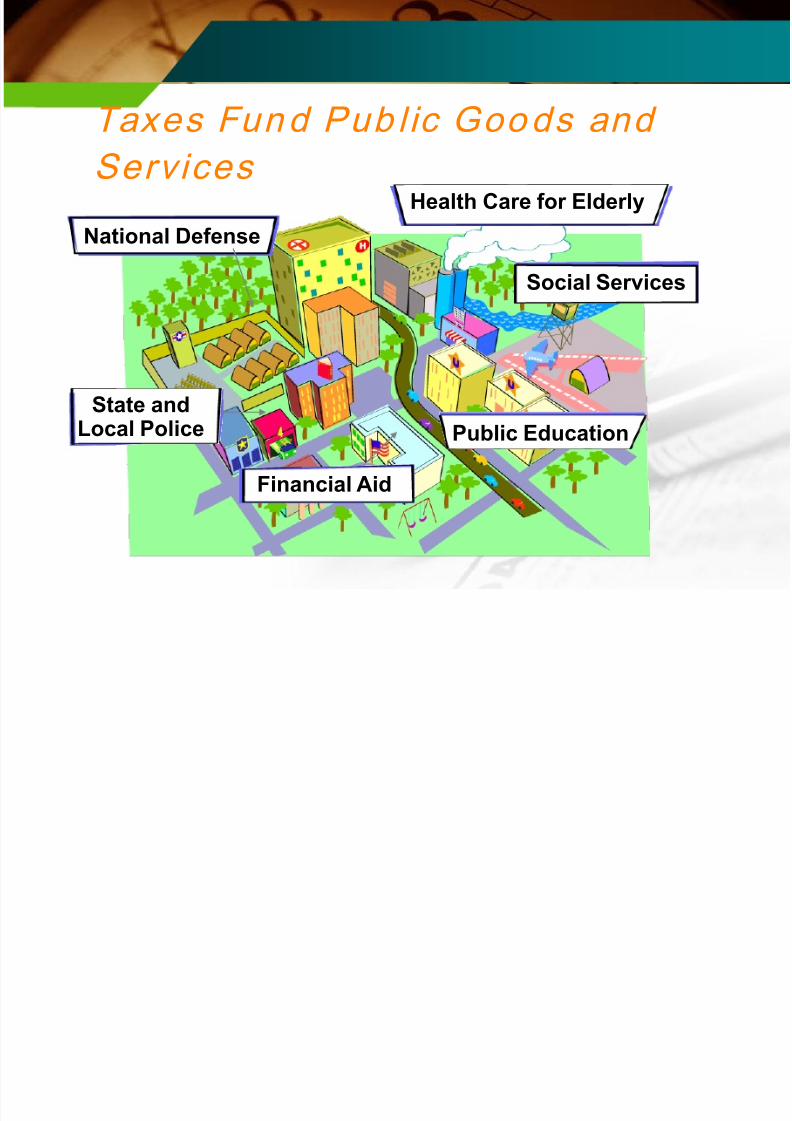

Taxes Fund Pub l ic Goods and

Services

National Defense

State andLocal Police

Financial Aid

Health Care for Elderly

Public Education

Social Services

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 33/64

The Economics of Taxation

• taxes also impact the economy in the followingways:• Resource allocation - if taxes are too high, supply will

decrease and /or prices will increase causing a shiftin the allocation of land, labor and capital.

• Behavior adjustment - sin taxes, such as thoseplaced on cigarettes attempt to change a person’sbehavior

• Productivity and Growth - if taxes are too high, there

is less incentive for people or businesses to continueto grow. Why earn more if most of it is taken away inhigher taxes?

• Correct negative externalities

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 34/64

BASIC PRINCIPLES OF

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 35/64

BASIC PRINCIPLES OF

SOUND TAX SYSTEM

Fiscal adequacy – The sources of revenue should be

sufficient to meet the demands of public

expenditureEquality or theoretical justice

– The tax burden should be proportionate to

the taxpayer’s ability to pay Administrative feasibility

– Tax laws should be capable of convenient

, just, and effective administration

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 36/64

Characteristics of a sound Tax system

• Fairness

• Clarity and Certainty• Convenience

• Efficiency

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 37/64

• Fairness. A tax should alwaysconsider the taxpayers' 'ability to pay'. and equity (concerned with the

distribution of income) • Certainty. The timing, method and

amount due should be absolutely

clear. There should be no excuses fortax evaders

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 38/64

–Convenience. It should be as easy aspossible for the taxpayer to pay the tax(in terms of means and timing of

payment). Note that the Pay As YouEarn (PAYE) method of tax collectionon most peoples' income is very good

here. –eff ic iency (concerned with the

allocation of resources)

Princ iples o f Tax and

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 39/64

Princ iples o f Tax and

Pol ic ies

– Other principles relate to the cost of operationof the tax system

– Cost. The cost of collection (for thegovernment) should not be too high. Inparticular, the cost should be a relatively smallproportion of the tax yield.

– The costs of operation are divided into two

types - administrative costs and compliancecosts.

Princ iples o f Tax and

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 40/64

Princ iples o f Tax and

Pol ic ies

– Administrative costs are the costs to thegovernment (and ultimately to the taxpayer) ofcollecting tax revenue. Thus they include thecosts of enforcing tax rules and attempting to

catch and to prosecute people breaking tax rules. – The more complex a tax system is, the more

easily can experts find their way around the rules.The more difficult it then becomes for the taxauthorities to tighten the rules to try to ensurethat people cannot avoid making the taxpayments which the government thinks they

should.

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 41/64

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 42/64

AICPA No 1

– Basic concept by which a government is meant to beguided in designing and implementingan equitable taxation regime.

– (1) Adequacy: taxes should be just-enough to generaterevenue required for provision of essential publicservices.

– (2) Broad Basing: taxes should be spread over as wideas possible section of the population,or sectors of economy, to minimize the individual tax

burden.

– (3) Compatibility: taxes should be coordinated toensure tax neutrality and overall objectives ofgood governance.

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 43/64

– (4) Convenience: taxes should be enforced in amanner that facilitates voluntary compliance tothe maximum extent possible.

– (5) Earmarking: tax revenue from a

specific source should be dedicated to a specificpurpose only when there is a direct cost-and-benefit link between the tax source andthe expenditure, such as use of motor fuel tax forroad maintenance.

– (6) Efficiency: tax collection efforts shouldnot cost an inordinately high percentage of

tax revenues

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 44/64

– (7) Equity: taxes should equally burdenall individuals or entities in similar economiccircumstances.

– (8) Neutrality: taxes should not favor any

one group or sector over another, and should notbe designed to interfere-withor influence individual decisions-making.

– (9) Predictability: collection of taxes shouldreinforce their inevitability and regularity.

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 45/64

– (10) Restricted exemptions: tax exemptions mustonly be for specific purposes (such as toencourage investment) and for a limited period.

– (11) Simplicity: tax assessment and

determination should be easy to understand byan average taxpayer.

T E i

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 46/64

Tax Evasion

• When there is fraud through pretensionand the use of other illegal devices tolessen one’s taxes, there is tax evasion

– Under-declaration of income – Non-declaration of income and other items

subject to tax

– Under-appraisal of goods subject to tariff – Over-declaration of deductions

T A id

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 47/64

Tax Avoidance• Is the legal utilization of the tax regime to one's ownadvantage, to reduce the amount of tax that is payable

by means that are within the law.

• The term tax mitigation is a synonym for tax avoidance.

• Its original use was by tax advisors as an alternative tothe pejorative term tax avoidance.

• Latterly the term has also been used in the taxregulations of some jurisdictions to distinguish tax

avoidance foreseen by the legislators from tax avoidancewhich exploits loopholes in the law.

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 48/64

Direct and indirect taxes

• A direct tax is one that is paid directlyby the individual worker or firm. Incometax is the best example, usually being

paid directly through PAYE. Firms paycorporation tax on their profits, which isa bit like an income tax for business.

Others include Capital Gains tax,Inheritance tax, Stamp duty (paid whenbuying a house)

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 49/64

Direct and indirect taxes

• An indirect tax is one that is only paidindirectly through a third party. Consumerspay Value Added Tax (VAT), for example,

but only if they actually buy the good orservice in question. The retailer officiallypays the tax, although it is likely that theprice is raised to reflect the tax, so,effectively, the consumer ends up paying.Others include tobacco and alcohol duties,fuel duties (on petrol).

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 50/64

IslamicTax and Policies

– what are the Islamic taxes? – What philosophy they subscribe to?

– What aims and policies do they pursue?

What outcome do they seek? – What are their impacts?

– What are their institutional requirements?Can they be integrated into modern tax policy

and systems?

– Are they subject to changes and revisions?

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 51/64

CLASSIFICATION OF TAXES

AS TO SUBJECT MATTERPersonal, poll or capitation

– Tax of a fixed amount imposed onindividuals, residing within specifiedterritory, whether citizens or not, withoutregard to their property or the

occupation in which they may beengaged.

– Example: community tax

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 52/64

Property

– Tax imposed on property, whether realor personal, in proportion either to itsvalue or in accordance with some other

reasonable method of apportionment – Example: real estate tax

Excise

– Any tax which does not fall within theclassification of a poll tax or propertytax.

– Example: value-added tax, income tax

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 53/64

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 54/64

Specific

– Tax of a fixed amount imposed by the head ornumber, or by some standard of weight ormeasurement

– Example: excise taxes on wines, cigars,gasoline

Ad valorem

– Tax of a fixed proportion of the value of theproperty with respect to which the tax isassesed

– Example: real estate tax, value-added tax

T f T

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 55/64

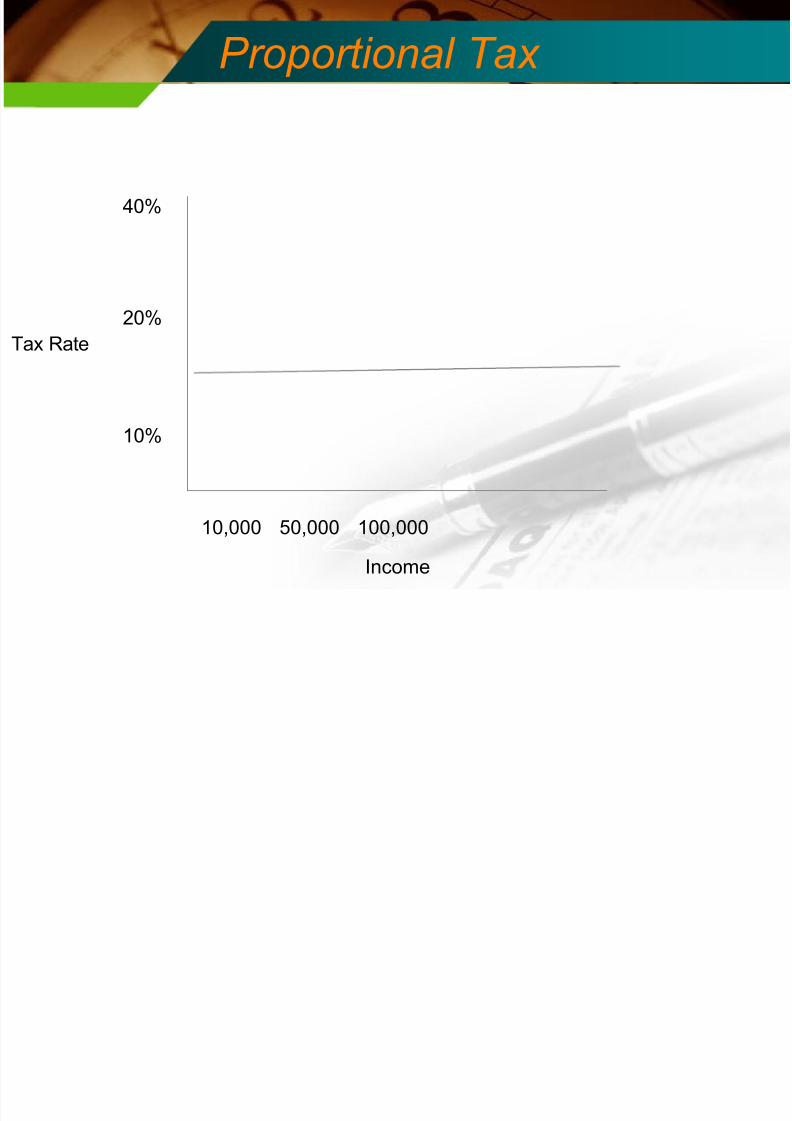

Types of Taxes

• Taxes are classified according to thepay in which the tax burden changesas income changes.

• Proportional Tax

• Progressive Tax

• Regressive Tax

T f T

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 56/64

Types of Taxes

Proportional –Tax based on fixed percentage of

the amount of property, income orother basis to be taxed

–Example: real property tax

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 57/64

P ti l T

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 58/64

Proportional Tax

Income

10,000 50,000 100,000

Tax Rate

40%

20%

10%

T f T

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 59/64

Types of Taxes

Progressive or graduated –Tax based on the rate of which

increases as the tax base orbracket increases

–Example: income tax

P i T

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 60/64

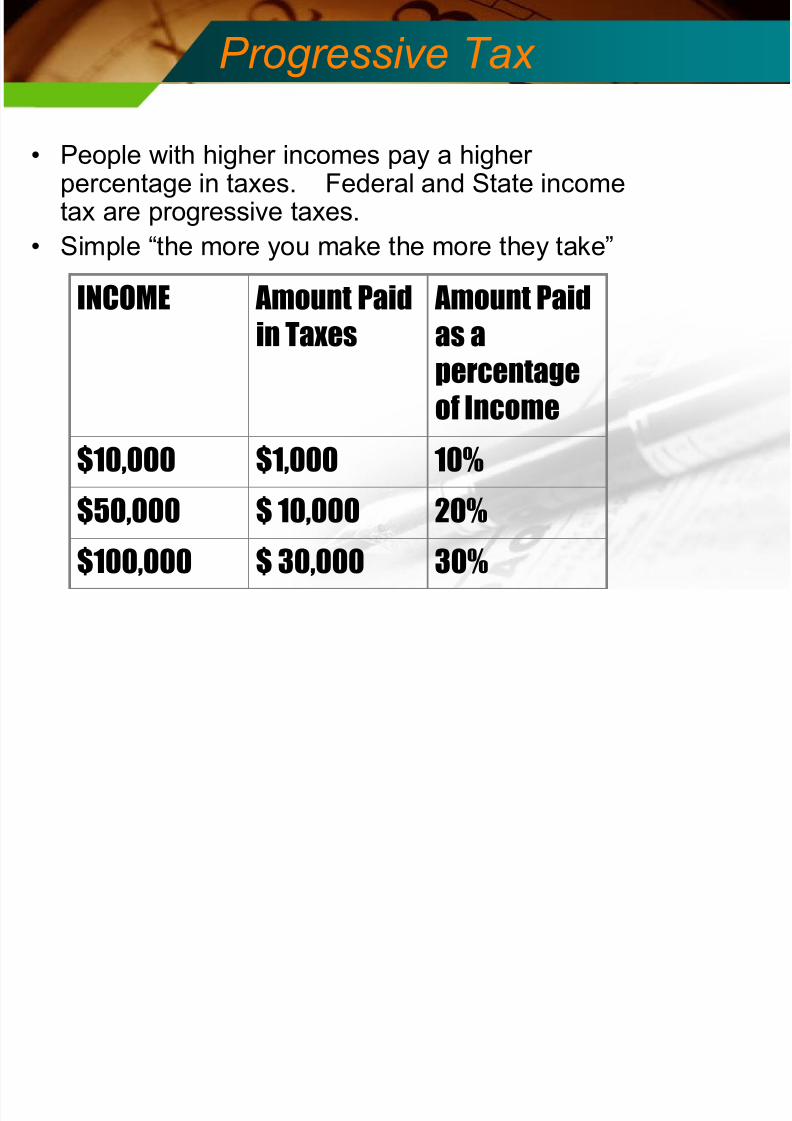

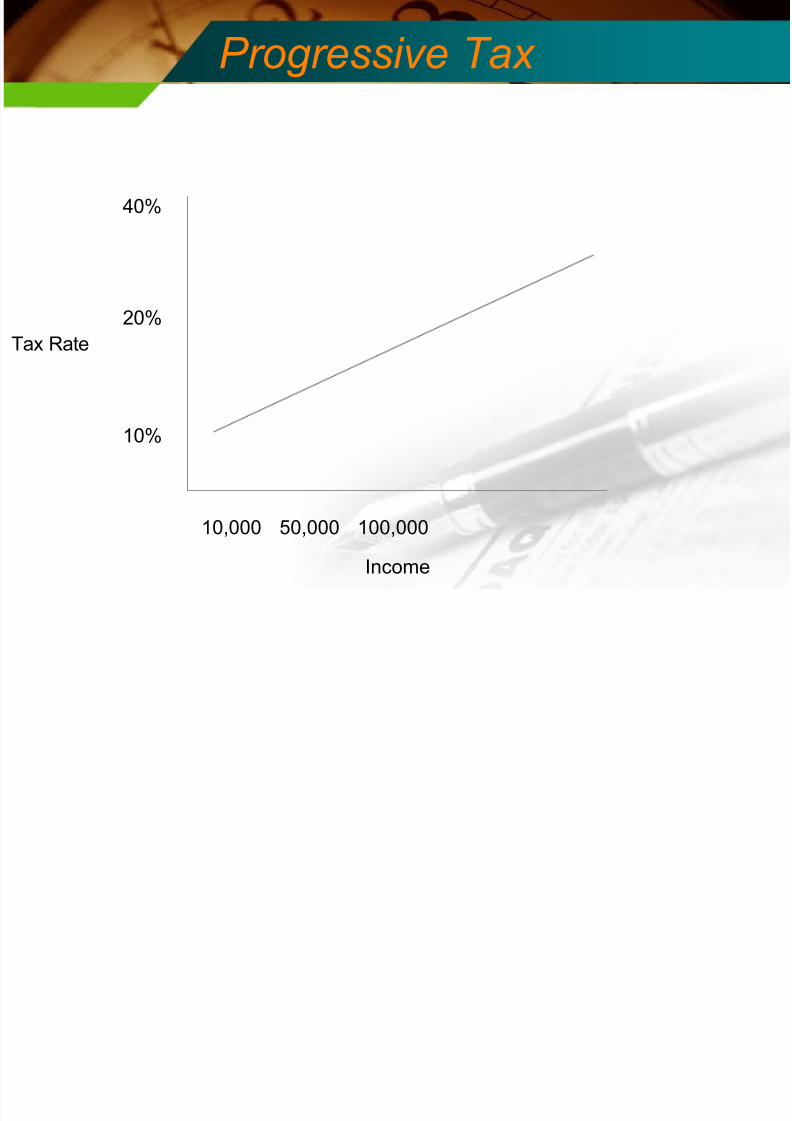

Progressive Tax

• People with higher incomes pay a higherpercentage in taxes. Federal and State incometax are progressive taxes.

• Simple “the more you make the more they take”

INCOME Amount Paidin Taxes

Amount Paidas apercentageof Income

$10,000 $1,000 10%

$50,000 $ 10,000 20%

$100,000 $ 30,000 30%

P i T

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 61/64

Progressive Tax

Income

10,000 50,000 100,000

Tax Rate

40%

20%

10%

T f T

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 62/64

Types of Taxes

Regressive –Tax base on the rate of which

decreases as the tax base orbracket increases

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 63/64

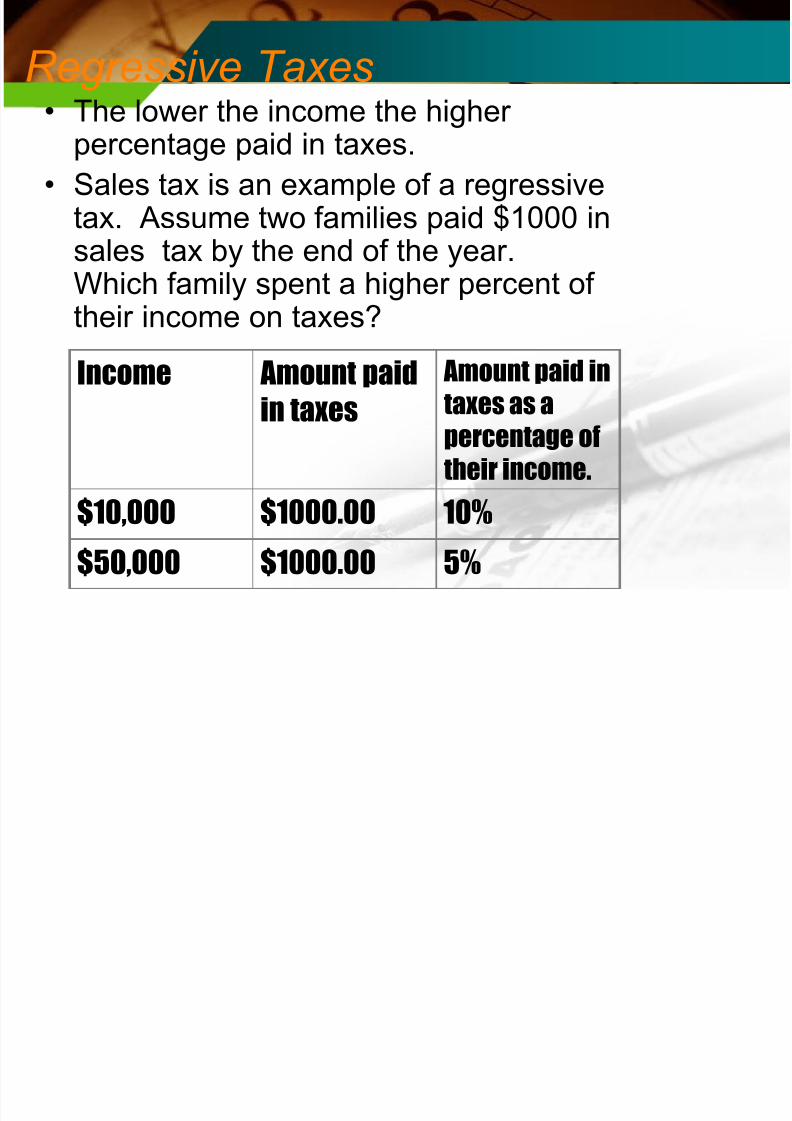

Regressive Taxes• The lower the income the higher

percentage paid in taxes.• Sales tax is an example of a regressive

tax. Assume two families paid $1000 insales tax by the end of the year.

Which family spent a higher percent oftheir income on taxes?

Income Amount paid

in taxes

Amount paid intaxes as a

percentage oftheir income.

$10,000 $1000.00 10%

$50,000 $1000.00 5%

Regressi e Ta

8/12/2019 1. Introduction to Tax Ideology and Policy

http://slidepdf.com/reader/full/1-introduction-to-tax-ideology-and-policy 64/64

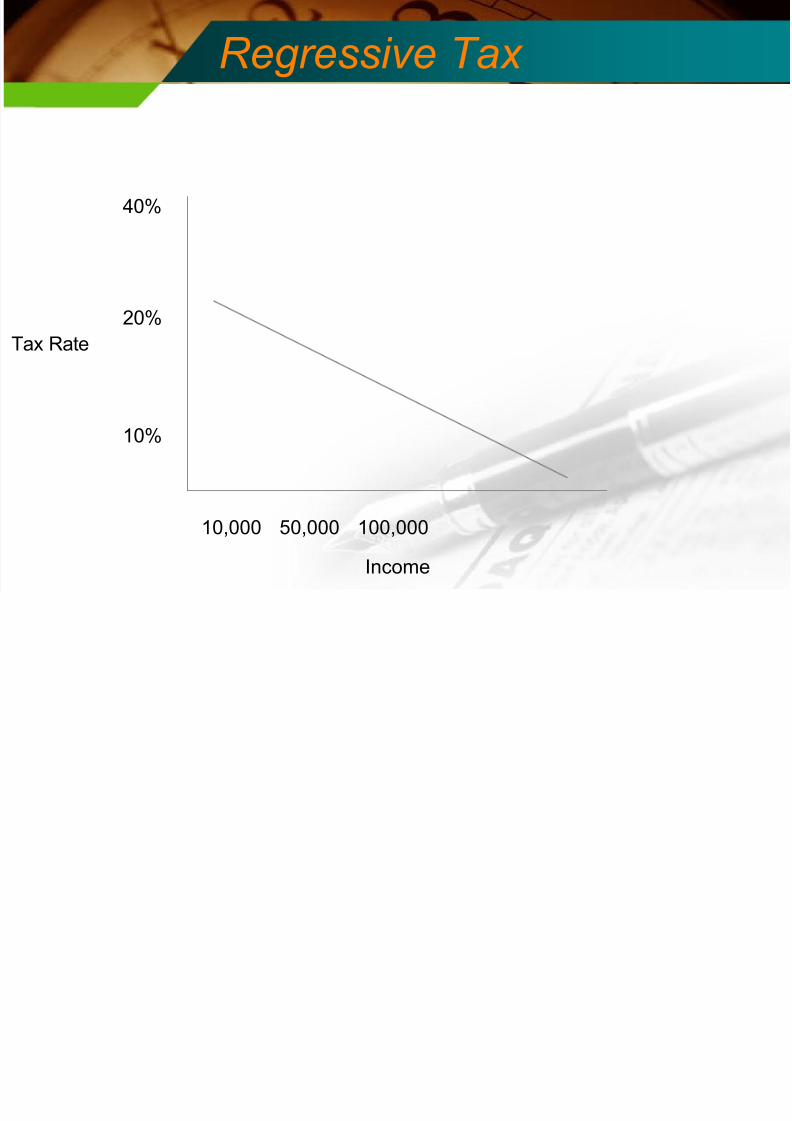

Regressive Tax

10,000 50,000 100,000

Tax Rate

40%

20%

10%