Embed Size (px)

Citation preview

1 I. INTRODUCTION

2 Q. PLEASE STATE YOUR NAME, POSITION AND BUSINESS ADDRESS.

3 A. My name is Leigh Anne Strahler. I am currently Vice President — Regulatory &

4 Finance for AEP Texas Inc. (AEP Texas or Company). My business address is 539 N.

5 Carancahua, Corpus Christi, Texas 78478.

6 Q. WOULD YOU PLEASE REVIEW YOUR EDUCATIONAL AND BUSINESS

7 BACKGROUND?

8 A. I received a Bachelor of Arts degree with a major in economics from Bethany College,

9 Bethany, West Virginia, in May 1995 and a Master's in Business Administration from

10 The Ohio State University, Columbus, Ohio, in 2004. I am a certified Project

11 Management Professional. My early experience, before joining American Electric

12 Power Company, Inc. (AEP), focused on accounting, finance and process-related roles

13 within two large corporations.

14 In 2006, AEP hired me as a Senior Cost Control Analyst working with AEP

15 Generation's Major Projects organization. In 2009, I was promoted to Business

16 Operations Manager focusing on strategic planning, financial reporting, project

17 management and special projects. In 2013, I moved to the AEP Operations and

18 Performance Transformation team as a Project Manager and focused on implementing

19 continuous improvement methodologies in Information Technology and Distribution.

20 In 2015, I was promoted to Director, Business Operations Support, at AEP Appalachian

21 Power Company where I was responsible for review, reporting and analysis of

22 operating company financial results, short-term and long-term financial plans and

23 prioritization of capital and operations and maintenance expenditures. In 2018, I

DIRECT TESTIMONY 1 LEIGH ANNE STRAHLER

100

1 moved to AEP Texas and into my current role of Vice President of Regulatory &

2 Finance.

3 Q. WHAT ARE YOUR RESPONSIBILITIES IN YOUR CURRENT POSITION?

4 A. As Vice President, Regulatory & Finance, I am responsible for the Company's financial

5 and regulatory plans and coordinating and executing those plans in conjunction with

6 the relevant AEP centralized business units. I facilitate the prioritization of operations

7 and maintenance (O&M) and capital expenditures, and am responsible for the recovery

8 of those costs through the regulatory process. I also am responsible for establishing

9 and maintaining metrics in support of financial reporting and developing short- and

10 long-term financial plans for the Company. My current position gives me responsibility

11 over Texas Regulatory Services, Business Operations Support and Continuous

12 Improvement groups for AEP Texas. I supervise a staff of 21 employees.

13 Q. HAVE YOU PREVIOUSLY FILED TESTIMONY?

14 A. Yes. I previously filed testimony before the Public Utility Commission of Texas in

15 Docket No. 49402, Joint Report and Application of Oncor Electric Delivery Company

16 and AEP Texas Inc. for Approval of Transfer of Facilities, Transfer of Rights Under

17 and Amendment of Certificates of Convenience and Necessity, and for Other

18 Approvals.

DIRECT TESTIMONY 2 LEIGH ANNE STRAHLER

101

1 II. PURPOSE OF TESTIMONY

2 Q. WHAT IS THE PURPOSE OF YOUR DIRECT TESTIMONY?

3 A. My testimony has several purposes. Specifically, my testimony:

4

• provides a summary of AEP Texas rate filing;

5 • introduces AEP Texas' proposals to 1) expand and recover the costs of the

6 catastrophe reserve currently in place for the Central division and 2) eliminate the

7 AMS surcharge and roll AMS expenditures into base rates;

8 • describes AEP Texas' Regulatory & Finance organization and the services it

9 provides in support of the delivery of safe and reliable electricity to AEP Texas'

10 customers;

11 • describes American Electric Power Service Corporation's (AEPSC) Regulatory

12 Services organization and the services it provides to AEP Texas, including a

13 demonstration that the affiliate charges billed to AEP Texas for its services are

14 reasonable and necessary;

15 • describes AEPSC's Legal Services organization and the services provided to AEP

16 Texas, including a demonstration that the affiliate charges billed to AEP Texas for

17 its services are reasonable and necessary;

18 • describes the AEPSC Environmental Services organization's provision of services

19 to support AEP Texas' transmission and distribution planning and operations,

20 including a demonstration that the charges are reasonable and necessary; and

21 • supports AEP Texas' requested recovery of rate case expenses.

22 Q. WHAT SCHEDULES IN THE RATE FILING PACKAGE DO YOU SPONSOR OR

23 CO-SPONSOR?

24 A. I co-sponsor Schedule II-E-4.5, Rate Case Expenses.

25 III. DESCRIPTION OF AEP TEXAS' RATE FILING

26 Q. WHAT IS THE TEST YEAR UPON WHICH AEP TEXAS' RATE FILING IS

27 BASED?

28 A. AEP Texas' rate filing is based on a test year ending December 31, 2018. AEP Texas

29 has made certain post-test year adjustments that are further discussed by AEP Texas

30 witness Randall W. Hamlett.

DIRECT TESTIMONY 3 LEIGH ANNE STRAHLER

102

1 Q. WHAT ARE THE GENERAL COMMISSION RATE SETTING STANDARDS

2 UPON WHICH AEP TEXAS RELIED IN PREPARING THIS FILING?

3 A. AEP Texas has adhered to the rate setting standards set out in Chapter 36 of PURA and

4 the Commission's "Cost of Service" rule, 16 Tex. Admin. Code § 25.231 (TAC), which

5 requires that rates be set based on historical test year costs, adjusted for known and

6 measurable changes. Rates established consistent with AEP Texas request should

7 allow the Company the opportunity to recover a reasonable return on its used and useful

8 invested capital, in excess of its reasonable and necessary operating expenses,

9 consistent with the requirements of PURA § 36.051. Various AEP Texas witnesses

10 address the requirements of PURA and the Commission's Substantive Rules as those

11 requirements apply to the costs they sponsor.

12 Q. HAS AEP l'EXAS PROVIDED ALL THE SCHEDULES AND WORKPAPERS TO

13 COMPLY WITH THE COMMISSION'S REQUIREMENTS FOR TRANSMISSION

14 AND DISTRIBUTION (T&D) BASE RATE PROCEEDINGS?

15 A. Yes. AEP Texas has made its filing consistent with the Commission's rate filing

16 package (RFP) and the requirements of 16 TAC § 22.243. AEP Texas has also pre-

17 filed its supporting direct testimony, consistent with 16 TAC § 22.225(a)(6).

18 Q. DID AEP TEXAS INFORM THE OWNERS OF THE SOUTH TEXAS PROJECT

19 ELECTRIC GENERATING STATION OF ITS INTENT TO FILE THIS RATE

20 PROCEEDING?

21 A. Yes. The Company's former ownership share of the South Texas Project Electric

22 Generating Station (STP) Units 1 and 2 is now owned by NRG South Texas LP (NRG)

23 and the San Antonio City Public Service Board (CPS Energy). Under 16 TAC

DIRECT TESTIMONY 4 LEIGH ANNE STRAHLER

103

1 §25.303(g)(4), the owners may elect to request a change in the decommissioning

2 funding level during the Company's rate case. AEP Texas must give the owners:

3 ...at least 90 days notice of an anticipated rate application for its general

4 rates to allow the Transferee Company to prepare a funding analysis to be

5 filed jointly with the Collecting Utility's application. 6

7 AEP Texas mailed and emailed notice to the owners of its former share of STP

8 on January 28, 2019, more than 90 days prior to the filing of this case.

9 Q. DO EITHER OF THE OWNERS INTEND TO ELECT TO REQUEST A CHANGE

10 IN THE DECOMMISSIONING FUNDING LEVEL?

11 A. Both owners have indicated that they are not electing to request a change in the

12 decommissioning funding level at this time. The owners recently sought changes to

13 the funding levels in Docket Nos. 48447 and 48556, which AEP Texas implemented

14 through Docket No. 49163.

15 Q. PLEASE SUMMARIZE THE COMMISSION RULINGS REQUESTED BY AEP

16 TEXAS IN THIS FILING.

17 A. AEP Texas is requesting the Commission to:

18 • Approve AEP Texas' revenue requirement

19 • Approve AEP Texas' capital additions since its previous rate reviews

20 • Approve the cost allocation methodology

21 • Approve combined rates and discretionary charges for AEP Texas

22 • Approve the capital structure and Return on Equity (ROE) for AEP Texas

23 • Reset baselines for distribution and transmission

24 • Remove energy efficiency costs from base rates and recover through the AEP

25 Texas Energy Efficiency Cost Recovery Factors (EECRFs)

26 • Approve AEP Texas' proposed transmission, distribution and general plant

27 depreciation rates

DIRECT TESTIMONY 5 LEIGH ANNE STRAHLER

104

1 • Approve recovery of all transmission expenses through the Transmission Cost

2 Recovery Factor (TCRF)

3 • Approve the reconciliation of the cost expended and investments made in the

4 deployment of AEP Texas Advanced Metering System (AMS) through

5 December 31, 2018

6 • Authorize deferral of rate case expenses incurred for this case and find

7 reasonable the unrecovered legal and consultant rate case expenses associated

8 with prior dockets

9 • Approve AEP Texas' proposed funding and scope of coverage for its

10 catastrophe reserve account

11 • Approve AEP Texas' proposed Income Tax Refund Rider associated with the

12 Tax Cuts and Jobs Act of 2017

13

14 IV. PROPOSALS FOR REGULATORY PROGRAMS

15 A. Catastrophe Reserve

16 Q. DOES AEP TEXAS HAVE A COMMISSION-APPROVED CATASTROPHE

17 RESERVE?

18 A. As approved in Docket No. 33309, AEP Texas Central Division has a Commission-

19 approved catastrophe reserve, which allows it to collect $1.3 million for ten years, with

20 authority to continue the collection until the catastrophe reserve reaches $13 million.

21 Q. FOR WHAT PURPOSES CAN THE CATASTROPHE RESERVE BE USED?

22 A. AEP Texas Central Division's incremental Transmission and Distribution operation

23 and maintenance costs can be charged against the catastrophe reserve if the total

24 incremental O&M costs for a storm exceeds $500,000 (capital related costs are

25 capitalized and recovered through Transmission Cost of Service (TCOS), Distribution

26 Cost Recovery Factor (DCRF) or base rate proceedings).

DIRECT TESTIMONY 6

LEIGH ANNE STRARLER 105

1 Q. IS AEP TEXAS REQUESTING ANY CHANGES TO THE CATASTROPHE

2 RESERVE?

3 A. Yes. AEP Texas requests that the Commission approve an expansion of the current

4 catastrophe reserve to include the AEP Texas North Division in addition to the Central

5 Division territory for a total reserve of $13.3M. Applying the catastrophe reserve

6 across the entire AEP Texas territory is consistent with AEP Texas request to merge

7 the rates for the two divisions of AEP Texas, as explained by AEP Texas witnesses

8 Judith E. Talavera and Jennifer L. Jackson. In addition, AEP Texas witnesses Gregory

9 S. Wilson and Randall W. Hamlett provide a complete explanation of the requested

10 expansion of the catastrophe reserve.

11 B. Advanced Metering System

12 Q. WHAT REQUEST IS AEP TEXAS MAKING RELATED TO ITS AMS SYSTEM IN

13 THIS CASE?

14 A. As further addressed by AEP Texas witnesses Hamlett, Jeff S. Stracener, Heather M.

15 Whitney, and Gregory A. Filipkowski, AEP Texas is requesting to (1) implement new

16 base rates reflecting its ongoing costs to provide AMS and (2) reconcile AMS costs

17 with AMS surcharge revenues under 16 TAC § 25.130. At the conclusion of this

18 proceeding, with the implementation of new base rates, AEP Texas proposes to

19 eliminate the AMS surcharge and roll AMS capital expenditures and AMS operations

20 and maintenance costs into base rates.

DIRECT TESTIMONY 7 LEIGH ANNE STRAIMER

106

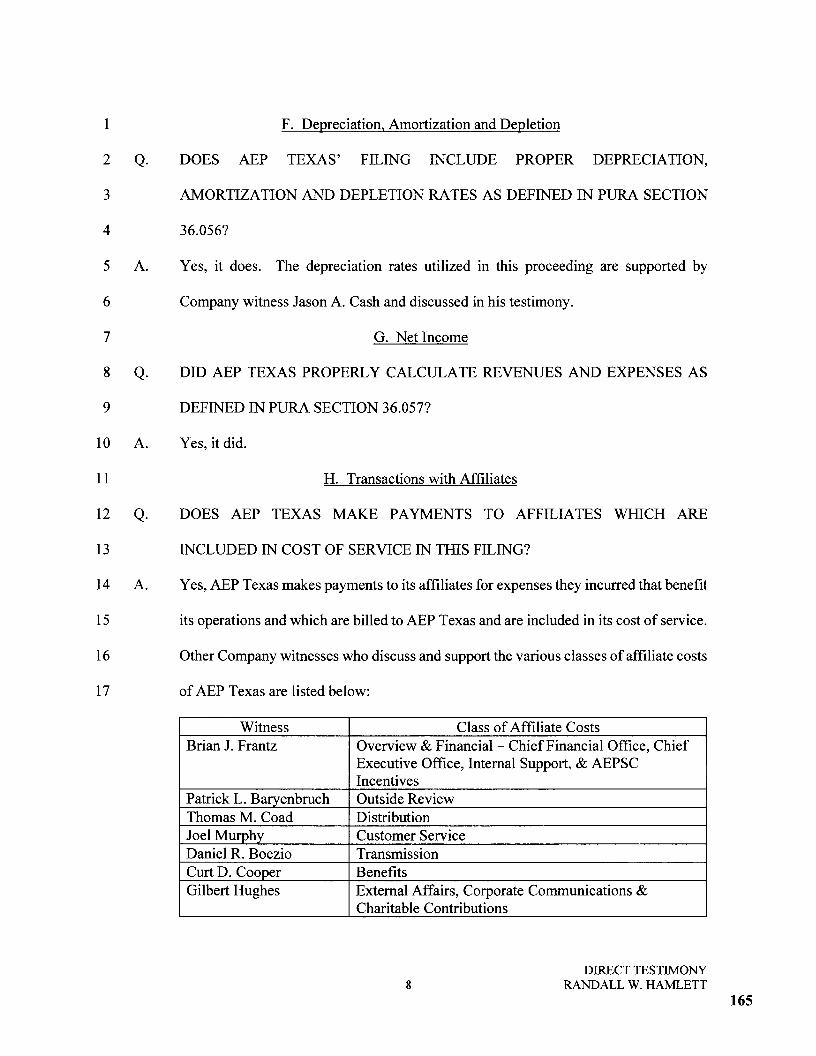

1 V. AEP TEXAS REGULATORY & FINANCE

2 Q. WHAT GROUPS ARE INCLUDED WITHIN AEP TEXAS REGULATORY &

3 FINANCE?

4 A. AEP Texas Regulatory & Finance includes the following groups: 1) Texas Regulatory

5 Services; 2) Business Operations Support; and 3) Continuous Improvement. As Vice

6 President of Regulatory & Finance, I am responsible for the oversight of these groups

7 and serve as a member of the AEP Texas leadership team. The AEP Texas Regulatory

8 & Finance organization is shown in EXHIBIT LAS-1.

9 Q. DO THE COSTS OF AEP TEXAS REGULATORY & FINANCE INCLUDE ANY

10 AFFILIATE CHARGES FROM AEPSC?

11 A. No.

12 A. Regulatory Services

13 Q. PLEASE DESCRIBE THE STAFFING OF THE AEP TEXAS REGULATORY

14 SERVICES GROUP.

15 A. The Texas Regulatory Services group has 11 employees, located in Austin, Texas and

16 the Company's office in Corpus Christi, Texas. In addition, the group is supplemented

17 by contract employees, as needed. The Regulatory Services team is led by a director

18 of regulatory services, located in Austin.

19 Q. PLEASE DESCRIBE THE SERVICES PROVIDED BY THE AEP TEXAS

20 REGULATORY SERVICES GROUP.

21 A. The Texas Regulatory Services group serves as the primary point of contact with the

22 Commission on regulatory issues. Specifically, the group is responsible for the

23 following activities:

DIRECT TESTIMONY 8 LEIGH ANNE STRABLER

107

1 • Preparing and filing rate change filings such as the DCRF, Interim TCOS,

2 TCRF, and Transition Charges;

3 • Maintaining regulatory relations with the Commission and participating in

4 regulatory proceedings;

5 • Coordinating the Company's engagement in Commission rulemaking and other

6 projects;

7 • Administering tariffs, including ensuring compliance with Commission-

8 approved tariffs and coordinating the implementation of rate changes;

9 • Preparing and filing numerous Commission required reports including outage

10 and monthly transmission construction reports;

11 • Investigating and resolving formal and informal customer complaints;

12 • Preparing and submitting applications for amendments to the Certificates of

13 Convenience and Necessity (CCNs);

14 • Coordinating with neighboring or dual-certified electric cooperatives and

15 municipally-owned utilities on regulatory-related issues;

16 • Maintaining the AEP Texas regulatory library and submitting filings to the

17 Commission;

18 • Participating with internal and external stakeholders on Electric Reliability

19 Council of Texas (ERCOT) and Texas Reliability Entity (TRE)-related issues;

20 • Acting as a liaison with the State Operations Center during major outages, such

21 as hurricanes; and

22 • Supporting legislative monitoring and analysis.

23 Q. WHY IS IT IMPORTANT FOR AEP TEXAS TO PLAY AN ACTIVE ROLE IN

24 REGULATORY MATTERS?

25 A. As a regulated transmission and distribution utility, AEP Texas is subject to a host of

26 state and federal regulatory requirements. The services provided by the AEP Texas

27 Regulatory Services organization during the test year were necessary to ensure that the

28 Company: 1) responded in a timely and effective manner to reporting obligations

29 imposed by applicable regulatory laws, rules and policies; 2) made its position known

30 in connection with the adoption of rules and regulatory policies affecting its T&D

31 service; 3) properly implemented the orders of state and federal regulators and properly

DIRECT TESTIMONY 9 LEIGH ANNE STRAHLER

108

1 administered its approved tariffs; and 4) effectively participated in regulatory

2 proceedings in which it was required to participate or in which its interests were

3 affected.

4 B. Business Operations Support

5 Q. PLEASE DESCRIBE THE STAFFING AND SERVICES OF THE AEP TEXAS

6 BUSINESS OPERATIONS SUPPORT GROUP.

7 A. The Business Operations Support group is composed of a director and two employees,

8 located in Corpus Christi, Texas. This group is responsible for the review, reporting

9 and analysis of AEP Texas fmancial results, and coordination of short and long term

10 financial plans. This includes assisting in the prioritization of capital expenditures and

11 operations and maintenance expenses. The Business Operations team interfaces with

12 various groups that impact AEP Texas' financial results, both within AEP Texas and

13 American Electric Power Service Corporation (AEPSC), a wholly owned subsidiary of

14 AEP that provides utility support services, at cost, for all operating units within the

15 AEP system. Key tasks performed are preparing monthly performance reports,

16 providing input into long range financial planning, assisting in routing and approval

17 processes for capital spend, ensuring that policies and procedures for expenditures are

18 followed, reviewing AEPSC services and billings; and developing capital and O&M

19 budgets. Other responsibilities include supporting regulatory activities and performing

20 ad hoc analysis as requested.

21 C. Continuous Improvement

22 Q. PLEASE DESCRIBE THE STAFFING OF THE AEP TEXAS CONTINUOUS

23 IMPROVEMENT GROUP.

DIRECT TESTIMONY 10 LEIGH ANNE STRAHLER

109

1 A. The group is composed of seven employees and is led by a continuous improvement

2 manager. The group's members are located across the AEP service area, with

3 employees located in Corpus Christi, Abilene, San Angelo, Laredo and Pharr.

4 Q. PLEASE DESCRIBE THE SERVICES OF THE AEP TEXAS CONTINUOUS

5 IMPROVEMENT GROUP.

6 A. The Continuous Improvement group is responsible for 1) establishing and sustaining a

7 Continuous Improvement culture throughout AEP Texas and 2) implementing and

8 driving process improvements. The group conducts problem solving and process

9 improvement events across the AEP Texas organization, while training employees

10 throughout the organization on improvement skill sets. Sustaining a continuous

11 improvement culture provides opportunities for employees to identify new processes,

12 projects or tools that will enable operational efficiencies for AEP Texas customers.

13

14 VI. AFFILIATE EXPENSES

15 Q. WHAT CLASSES OF AFFILIATE EXPENSES DO YOU SUPPORT?

16 A. I support three classes of affiliate expenses: Regulatory Services, Legal Services, and

17 Environmental Services.

18 A. Description of AEPSC Regulatory Services

19 Q. DID AEP TEXAS RECEIVE AFFILIATE REGULATORY SERVICES DURING

20 THE TEST YEAR?

21 A. Yes.

22 Q PLEASE DESCRIBE THE AEPSC REGULATORY SERVICES ORGANIZATION.

DIRECT TESTIMONY 11 LEIGH ANNE STRARLER

110

1 A. During the test year, the AEPSC Regulatory Services organization was led by a Vice

2 President (VP) who reported directly to the Executive Vice President of External

3 Affairs. The AEPSC Regulatory Services organization provided support services

4 related to case management, pricing and analysis, state and federal regulatory strategy,

5 Regional Transmission Organizations (RTO), NERC compliance, and regulatory issue

6 management. These AEPSC employees were located in Dallas and Austin, Texas;

7 Tulsa, Oklahoma; and Columbus, Ohio.

8 Q. PLEASE DESCRIBE THE CASE MANAGEMENT SERVICES PROVIDED TO

9 AEP TEXAS.

10 A. AEPSC regulatory case management services include coordination and management

11 of major state and federal regulatory filings, under the direction of the AEP Texas

12 regulatory director. These employees facilitate overall development and management

13 of filings to state and federal regulatory agencies, collaborating with groups across the

14 AEP system, including testimony development and coordination of the discovery

15 process in regulatory proceedings. Five employees located in Austin, Texas, Dallas,

16 Texas, and Tulsa, Oklahoma focus their case management efforts on the AEP's West

17 operating companies cases.

18 Q. PLEASE DESCRIBE THE PRICING AND ANALYSIS SERVICES PROVIDED TO

19 AEP TEXAS.

20 A. The pricing and analysis group assists in the development of state regulatory filings,

21 working closely with case managers and state regulatory directors. The group performs

22 jurisdictional cost studies, class cost-of-service studies, rate design analysis and

23 provides supporting testimony.

DIRECT TESTIMONY 12 LEIGH ANNE STRAHLER

111

1 Q. PLEASE DESCRIBE THE STATE AND FEDERAL REGULATORY SERVICES

2 PROVIDED TO AEP TEXAS.

3 A. AEPSC Regulatory Services researches and recommends regulatory strategies to

4 AEP's operating companies and business units, monitors emerging regulatory issues

5 inside and outside of AEP's footprint and participates in the development of regulatory

6 policies. In addition to state regulatory matters, AEPSC Regulatory Services provides

7 regulatory support to the operating companies and business units that interface with

8 FERC for wholesale rates, operating agreements and open access transmission tariffs.

9 Q. PLEASE DESCRIBE THE RTO SERVICES PROVIDED TO AEP TEXAS.

10 A. The RTO group monitors and engages in activities of the regional transmission

11 organizations (RTO) in which AEP operates, including ERCOT. In addition to the

12 overall support provided by the West RTO group, one employee is located in Austin,

13 Texas, and is dedicated to engaging in ERCOT activities. The RTO group facilitates

14 analysis of issues in ERCOT and the other RTOs and coordinates the development of

15 company-wide positions on those issues affecting AEP.

16 Q. PLEASE DESCRIBE THE NERC COMPLIANCE SERVICES PROVIDED TO AEP

17 TEXAS.

18 A. The Enterprise NERC Compliance group provides centralized leadership and oversight

19 of AEP's compliance with applicable NERC Reliability and Critical Infrastructure

20 Protection (CIP) standards. The group serves as the primary compliance contact; tracks

21 and reports compliance deliverables; coordinates potential violation disposition;

22 manages AEP's NERC registration process; coordinates NERC and Regional Entity

23 audits; coordinates design of mitigation plans; and manages the system-wide review,

DIRECT TESTIMONY 13 LEIGH ANNE STRAHLER

112

1 comments, and balloting on NERC and regional proposals for new and revised NERC

2 standards.

3 Q. WERE AEPSC REGULATORY SERVICES NECESSARY TO SUPPORT THE

4 PROVISION OF RELIABLE UTILITY SERVICE?

5 A. Yes, they were. As a regulated utility, AEP Texas is subject to a host of state and

6 federal regulatory requirements. The services provided to AEP Texas during the test

7 year by the AEPSC Regulatory Services Department were a necessary complement to

8 the AEP Texas Regulatory team's efforts to ensure that AEP Texas complied with

9 applicable regulatory laws, rules and policies.

10 Q. IS THERE ANY DUPLICATION OF SERVICES PROVIDED BY AEPSC

11 REGULATORY SERVICES AND THE AEP I EXAS REGULATORY SERVICES

12 DEPARTMENT TO AEP TEXAS.

13 A. No, there is not. Regulatory services are provided to AEP Texas through the

14 complementary efforts of AEPSC's centralized Regulatory Services and the AEP

15 Texas Regulatory Services departments. No other service company or operating

16 company department provides such services.

17 B. Reasonableness of AEPSC Regulatory Services

18 Costs Charged to AEP Texas

19 Q. WHAT ARE THE TOTAL TEST YEAR CHARGES TO AEP TEXAS FOR THE

20 REGULATORY SERVICES CLASS OF AFFILIATE COSTS?

21 A. During the adjusted test year, $1,858,373 of affiliate charges for AEPSC Regulatory

22 Services were billed to AEP Texas. As shown in Table 1 below, approximately 77

23 percent of these Regulatory Services costs allocated to AEP Texas are directly related

DIRECT TESTIMONY 14 LEIGH ANNE STRAHLER

113

1

to labor and fringe benefits for the employees in the group. The reasonableness of the

2

compensation and benefits paid to the Regulatory Services staff is supported by the

3

testimony of Company witnesses Andrew R. Carlin and Curt D. Cooper. AEP Texas

4

witness Brian J. Frantz addresses the allocation of these costs as part of his testimony.

5

Table 1 6 Com onents of Reu1atorv Services Class bv Cost Cate o

Labor Outside Services

Other Grand Total

Amount $1,423,929 $372,744 $61,700 $1,858,373 % of Total 77% 20% 3% 100%

7

8 Q. WHAT APPROACH DOES YOUR TESTIMONY TAKE TO DEMONSTRATE THE

9 REASONABLENESS OF AEPSC'S CHARGES TO AEP 1EXAS FOR

10 REGULATORY SERVICES?

11 A. My testimony utilizes a combination of indicators to demonstrate the reasonableness

12 of AEPSC's charges to AEP Texas: cost trends, budget performance, staffing trends

13 and outsourcing.

14 1. Cost Trends

15 Q. PLEASE DISCUSS THE TRENDS IN AEPSC REGULATORY SERVICES

16 CHARGES TO AEP TEXAS LEADING UP TO THE TEST YEAR.

17 A. The following table depicts the trends in AEP Texas actual affiliate charges for

18 AEPSC Regulatory Services for the calendar years 2015 to 2018.

DIRECT TESTIMONY 15

LEIGH ANNE STRAHLER 114

Table 2 AEPSC Regulatory Services Charges to AEP Texas

Adjusted 2015 2016 2017 Test Year

$1,704,779 $1,748,778 $1,372,982 $1,858,373 1

2

AEPSC charges to AEP Texas have been stable since 2015 with less charges to AEP

3

Texas in 2017 for both labor and outside services. Variations in the charges from year

4

to year can be associated with the levels and types of projects that are undertaken in

5

any given year.

6 2. Budget Performance

7 Q. PLEASE DESCRIBE HOW THE BUDGETING PROCESS IS USED BY AEPSC

8 REGULATORY SERVICES TO MONITOR COSTS?

9 A. AEPSC Regulatory Services employs standardized budgeting tools to ensure that costs

10 are controlled within the individual sections of the department. AEPSC Regulatory

11 Services has its own budget to which it must adhere. Budgets are set annually and

12 compliance is monitored by the use of monthly variance reports.

13 Q. HOW HAS THE AEPSC REGULATORY SERVICES ORGANIZATION

14 PERFORMED IN COMPARISON TO ITS BUDGETS?

15 A. Table 3 below compares AEPSC Regulatory Services total, actual expenditures to

16 budget targets for which it is accountable, for calendar years 2015 to 2017, and the Test

17 Year. These expenses are allocated to AEP's operating companies, including AEP

18 Texas, based on allocation formulas. These amounts reflect what centralized

19 Regulatory Services budgeted and spent for the entire AEP System, not simply AEP

20 Texas.

DIRECT TESTIMONY 16 LEIGH ANNE STRAHLER

115

1 Table 3

2 AEPSC Regulatory Services

2015 2016 2017 Test Year ACTUAL $15,040,170 $15,044,058 $14,426,675 $17,082,708 BUDGET $14,961,423 $15,238,684 $16,037,741 $18,358,596

VARIANCE (Over)/Under ($78,747) $194,626 $1,611,066 $1,275,889

3

4 Q. HOW DOES THIS COMPARISON OF BUDGETED VERSUS ACTUAL AEPSC

5

REGULATORY SERVICES COSTS DEMONSTRATE THAT THESE COSTS ARE

6

REASONABLE?

7 A. As described above, AEPSC Regulatory Services actual costs were below the

8

department's control budget from 2016 through 2018, demonstrating its ability to

9 manage costs and budgets through a variety of budget and cost control mechanisms.

10 The AEPSC Regulatory Services budget variances provide support for the fact that the

11 department's managers are effectively managing expenses and making reasonable and

12 prudent decisions regarding staffing and major spending initiatives.

13 3. Staffing Trends

14 Q. WHAT HAS BEEN THE TREND IN STAFFING LEVELS FOR THE AEPSC

15 REGULATORY SERVICES ORGANIZATION?

16 A. As shown in Table 4, the AEPSC Regulatory Services organization's staffing level

17 increased slightly to 95 positions in the Test Year, from 90 positions in 2015. The net

18 gain in positions is attributable to continuous improvement efforts relating to NERC

19 reliability compliance and program oversight and the resulting addition of five FTEs to

20 address NERC compliance matters.

DIRECT TESTIMONY 17 LEIGH ANNE STRAHLER

116

1 Table 4

2 AEPSC Re2u1atorv Services FTEs

2015 2016 2017 Test Year FTEs 90 87 90 95

3

4

4. Outsourcing

5 Q. DOES AEPSC REGULATORY SERVICES USE OUTSOURCING AND/OR

6

CONTRACT SERVICES?

7 A. Yes. Outsourcing and contract services are used as necessary to provide specialized

8

services that AEPSC Regulatory Services is not staffed to provide and to supplement

9

the services they provide. Outside services and contractors are used in lieu of hiring

10 additional permanent staff or to perform specialized, overflow work activities when the

11 demands for regulatory services exceeds the department's ability to satisfy those needs

12 with existing in-house resources.

13 Q: WHAT IS YOUR CONCLUSION REGARDING THE REASONABLENESS OF

14 THE AEPSC REGULATORY COSTS?

15 Together, the cost trends of AEPSC charges to AEP Texas along with AEPSC staffing

16 trends, budget performance and effective use of outsourcing show that the AEPSC

17 Regulatory Services affiliate costs are reasonable and necessary.

18 C. Description of AEPSC Legal Services

19 Q. DOES AEPSC PROVIDE LEGAL SERVICES FOR AEP TEXAS?

20 A. Yes, the AEPSC Legal Services provides all internal legal services to AEP Texas. AEP

21 Texas does not have employees providing legal services.

DIRECT TESTIMONY 18

LEIGH ANNE STRAHLER 117

1 Q. HOW IS AEPSC LEGAL SERVICES ORGANIZED?

2 A. The department is led by an Executive Vice President, who is AEP's General Counsel

3 and Corporate Secretary. The attorneys in Legal Services are organized into practice

4 groups.

5 Q. CAN YOU PROVIDE A MORE DETAILED DESCRIPTION OF THE SERVICES

6 PROVIDED BY THE VARIOUS PRACTICE GROUPS IN AEPSC LEGAL

7 SERVICES?

8 A. Yes. The following is an overview of the services provided by the practice groups:

9 • Regulatory/Nuclear — AEPSC's regulatory lawyers handle all types of contested

10 case proceedings, rulemakings and projects ongoing before the Commission, other

11 state regulatory authorities and FERC. They also ensure that AEP Texas'

12 operations and activities are consistent with state and federal legal requirements

13 and policies applicable to regulated utilities. This practice group also provides

14 services related to AEP's nuclear generation.

15 • Real Estate —Legal Service's real estate attorneys are responsible for overseeing

16 negotiations and documentation required in connection with a variety of real estate

17 transactions entered into by AEP Texas, such as transmission and distribution

18 easements, real estate leases and condemnation-related matters.

19 • Litigation — These attorneys initiate and defend various types of lawsuits involving

20 AEP Texas, such as personal injury claims, disputes with contractors, right of way

21 disputes, injuries resulting from contact with energized facilities and employment-

22 related arbitrations and litigation.

23 • Environmental, Safety & Health — The attorneys in this group are responsible for

24 the provision of legal services to AEP Texas related to environmental, safety and

25 health issues. They help ensure that AEP Texas remains in compliance with

26 applicable federal and state environmental, safety and health laws.

27 • Finance and Compliance —Legal Service's finance and compliance attorneys handle

28 virtually all corporate financings, oversee the preparation of Securities and

29 Exchange Commission reports required by federal law and regulations, such as

30 Forms 10-K, 10-Q and 8-K, and ensure that AEP Texas financial activities are in

31 compliance with its corporate charger, by-laws and state corporate laws.

32 • Tax and Corporate Services — These Legal Services attorneys advise AEP Texas

33 and the other AEP Operating Companies on all aspects of state, local and federal

34 taxation. They also do pension-related Employee Retirement Income Security Act

DIRECT TESTIMONY 19 LEIGH ANNE STRAHLER

118

1

and compliance work, and handle legal matters related to the drafting and

2

administration of employee health, welfare and benefit plans.

3 • Transactions, Commercial Operations and Logistics — AEPSC's transactional

4 lawyers draft, negotiate and interpret many different types of contracts that AEP

5 Texas must enter into in the ordinary course of its business, including software

6 licenses, vendor contracts, and purchase and sale agreements related to facilities.

7 Energy, commercial operations and fuel matters also are handled by this group.

8

• Energy — The attorneys in this group are responsible for providing legal services to

9

AEP Energy.

10 Q. ARE THERE ANY OTHER WORK GROUPS THAT REPORT TO AEPSC LEGAL

11 SERVICES THAT RENDER SERVICES THAT ARE NOT CHARACTERIZED AS

12 LEGAL PRACTICE SERVICES?

13 A. Yes. During the test year, the Ethics and Compliance program and the Operations and

14 Performance Transformation (OPT) teams were housed within Legal Services. The

15 Ethics and Compliance program promotes ethical behavior and ensure compliance with

16 all laws and regulations that affect AEP's business activities. The OPT group has

17 overall responsibility for enabling continuous improvement principles, practices, tools

18 and behaviors through education, coaching/consulting, capturing best practices, and

19 facilitating workshops throughout the AEP system.

20 Q. IS THERE ANY DUPLICATION OF SERVICES PROVIDED TO AEP TEXAS BY

21 LEGAL SERVICES?

22 A. No. No other department in AEPSC provides legal services to AEP Texas; thus, there

23 is no duplication of these services within AEPSC and AEP Texas.

24 Q. WHO ARE THE CLIENTS OF THE VARIOUS PRACTICE GROUPS IN LEGAL

25 SERVICES?

DIRECT TESTIMONY 20 LEIGH ANNE STRAHLER

119

1 A. Legal Services provides services to all companies in the AEP System. The use of

2 practice groups allows AEPSC to centralize expertise in areas of legal services critical

3 to the support of various utility activities. At the same time, because all of the practice

4 groups are integrated in a single department, each practice group is able to provide

5 support to the activities of another group as the needs of a particular legal matter may

6 dictate. For example, while the Finance and Compliance group would be in charge of

7 doing the due diligence work and document preparation for an AEP Texas bond

8 financing, that practice group could turn to the Regulatory group if the need arose for

9 guidance regarding the state and federal regulatory requirements pertaining to the

10 proposed transaction.

11 Q. DOES AEPSC LEGAL SERVICES DEDICATE STAFF TO AEP TEXAS?

12 A. No, it does not.

13 Q. WFIERE ARE AEPSC LEGAL SERVICES PERSONNEL LOCATED?

14 A. Most of the Legal Services staff are based in the AEP headquarters in Columbus, Ohio,

15 while some are located regionally, such as in AEP's Austin, Dallas and Oklahoma City

16 offices. Certain legal services require a degree of localized expertise to interact face-

17 to-face with the parties, officials and decision makers involved in a particular lawsuit,

18 real estate transaction, or other legal matter. AEPSC's regulatory attorneys in Texas

19 are a good example of how AEP utilizes regionally-located counsel. Texas regulatory

20 matters require daily interaction between the Company's counsel, various staff

21 members of the Commission, and other parties involved in numerous contested case

22 proceedings, rulemakings, workshops and other projects that directly affect AEP

23 Texas.

DIRECT TESTIMONY 21 LEIGH ANNE STRAHLER

120

1 AEPSC has five attorneys located in Austin, Texas, three of whom are

2 regulatory attorneys with extensive backgrounds in Texas utility law and regulation.

3 They provide some of the legal support necessary for AEP Texas interests to be

4 properly represented in these proceedings. These attorneys, however, perform work

5 for all of AEP's Operating Companies to gain the efficiencies and economies of scale

6 associated with the provision of centralized legal services.

7 Q. ARE LEGAL SERVICES PROVIDED TO AEP TEXAS THROUGH OUTSIDE

8 COUNSEL AS WELL AS AEPSC LEGAL SERVICES EMPLOYEES?

9 A. Yes. AEP Texas utilizes the services of outside counsel to keep up with the legal work

10 as needed to support a regulated company as large and complex as AEP Texas.

11 Moreover, AEP Texas and AEPSC believe that use of outside counsel, when warranted

12 by the volume of work or when the nature of work requires expertise not otherwise

13 available internally, maintains the quality of the Company's legal services. If AEP

14 Texas had to staff a legal department sufficient to cover the entire range of legal

15 services it requires, it would lead to over-staffing and under-utilization of staff.

16 Q. WHAT IS THE APPROACH USED BY THE LEGAL SERVICES TO DETERMINE

17 WHETHER TO RETAIN OUTSIDE COUNSEL?

18 A. AEP prefers to use in-house counsel whenever possible. In-house employees are

19 generally less expensive than external counsel. A number of factors are weighed on a

20 case-by-case basis in the decision to retain outside counsel for any particular legal

21 matter. For example, outside counsel may be retained when internal workload is such

22 that the legal services cannot be provided by service company attorneys alone, or when

23 counsel with specialized expertise is not otherwise available internally. The legal

DIRECT TESTIMONY 22 LEIGH ANNE STRAHLER

121

1 staffing for this rate case is a good example of AEP' s approach to using outside counsel.

2 This case is too large to be handled only by in-house counsel, given the limited number

3 of available in-house counsel possessing the necessary experience and expertise.

4 Accordingly, AEP Texas has staffed the case with both internal and outside counsel

5 working cooperatively to ensure that all legal services necessary to support AEP Texas'

6 interests are covered without undue overlap.

7 Q. HOW DO AEPSC AND AEP TEXAS GO ABOUT SELECTING OUTSIDE

8 COUNSEL?

9 A. AEPSC and AEP Texas select outside counsel who possess the requisite experience

10 and demonstrated expertise in the areas of legal services required by AEP Texas, and

11 who have a substantial base of knowledge concerning the Company's organization and

12 business operations. For the most part, these attorneys have gained their experience

13 and demonstrated their expertise through prior relationships with AEP Texas and with

14 AEP, during which time they have demonstrated the ability to deliver high-quality legal

15 services in a timely fashion. The legal department employs a number of policies to

16 ensure an appropriate level of control over outside counsel's activities, fees and

17 expenses, such as utilizing standardized billing procedures and reviewing each invoice

18 from outside counsel to ensure the charges and scope of work are consistent with AEP's

19 policies and requirements.

20 Q. WERE THE SERVICES PROVIDED DURING THE TEST YEAR BY AEPSC

21 LEGAL SERVICES NECESSARY IN ORDER FOR AEP TEXAS TO PROVIDE

22 RELIABLE UTILITY SERVICE?

DIRECT TESTIMONY 23 LEIGH ANNE STRAHLER

122

1 A. Yes. Like any large company, AEP Texas business activities are governed by a host

2 of legal requirements and generate a number of legal issues. Some of these are the

3 product of statute, some are the product of government agency rules and regulations,

4 some of them are the product of lawsuits, and some are the product of AEP Texas' need

5 to protect its legal interests when it does business with investors, financial institutions,

6 service providers, vendors, and other contracting parties. The services provided to AEP

7 Texas by Legal Services during the test year were necessary to ensure that the Company

8 operated its utility business consistent with applicable legislative and regulatory

9

requirements, and that its legal interests were protected as it transacted business or

10 engaged in litigation with third parties.

11

D. Reasonableness of AEPSC Legal Services

12

Costs Charged to AEP Texas

13 Q. WHAT ARE THE AEPSC ADJUSTED TEST YEAR CHARGES TO AEP TEXAS

14 BY AEPSC LEGAL SERVICES?

15 A. The total amount of adjusted test year billings to AEP Texas from AEPSC for Legal

16 Services is $2,001,175. Approximately 89 percent of the AEPSC Legal Services costs

17 allocated to AEP Texas are directly related to labor and fringe benefits of the group's

18 employees. The reasonableness of the compensation and benefits paid for AEPSC

19 Legal Services is supported by the testimony of Company witnesses Carlin and Cooper,

20 respectively. AEP Texas witness Frantz addresses the allocation of these costs as part

21 of his testimony.

DIRECT TESTIMONY 24

LEIGH ANNE STRAHLER 123

1 Q. WHAT APPROACH DOES YOUR TESTIMONY TAKE TO DEMONSTRATE THE

2 REASONABLENESS OF AEPSC'S CHARGES TO AEP TEXAS FOR LEGAL

3 SERVICES?

4 A. I used a variety of forms of proof. These include: Legal Services budgeting processes

5 and budget performance; trends in actual costs incurred by Legal Services as a whole,

6 and in costs billed to AEP Texas; Staffing trends; benchmarking information; and

7 initiatives employed by Legal Services to control its costs. Viewed in combination,

8 this information supports the conclusion that Legal Services charges to AEP Texas for

9 legal services are reasonable and necessary.

10 1. Budget Performance

11 Q. WHAT PROCESSES DOES THE AEPSC LEGAL SERVICES ORGANIZATION

12 USE TO ENSURE COST EFFECTIVE PROVISION OF SERVICES?

13 A. Budget targets for the upcoming year are based on prior-year budget inputs plus or

14 minus any items that are identified and approved for inclusion or omission. Labor

15 expense is budgeted by hours. Materials, supplies, outside services, and other expenses

16 are budgeted based on prior activity and any anticipated changes. Once the budget is

17 established, ongoing actual expenditures are compared to budget targets. Budget

18 variances are analyzed monthly and anticipated costs and activities are reviewed to

19 address variances.

20 Q. HOW HAS AEPSC LEGAL SERVICES PERFORMED IN COMPARISON TO ITS

21 BUDGETS?

22 A. The table below compares the AEPSC Legal Services allocated actual expenditures to

23 budget targets for which it is accountable, for calendar years 2015 to 2017, and the Test

DIRECT TESTIMONY 25

LEIGH ANNE STRAHLER 124

1

Year. These expenses are directly assigned or allocated to AEP's operating companies,

2

including AEP Texas, based on allocation formulas as described in the testimony of

3

Brian Frantz.

4

The AEPSC Legal Services costs for outside services vary depending on the

5

number and nature of the legal issues confronting AEP at a given time, the workloads

6

and consequent availability of internal counsel to handle these issues, and the expertise

7

needed for a particular issue. The number and nature of legal issues that may arise and

8

the consequent costs to address them often are not predictable and not entirely within

9

AEP's control. The figures indicate that AEPSC Legal Services has generally been

10

able to spend less than its budgeted amounts, keeping the AEPSC Legal Services

11

overall actual expenses relatively flat since 2015.

12

Table 5

13

AEPSC Legal Services Bud2et vs. Actual

2015 2016 2017 2018 Test Year ACTUAL $20,033,382 $22,717,654 $21,052,557 $21,968,443

BUDGET VARIANCE (Over)/Under

$20,838,358 $20,206,731 $24,249,432 $23,650,490

$804,976 $(2,510,923) $3,196,875 $1,682,047

14 Q. HOW DOES THIS COMPARISON OF BUDGETED VERSUS ACTUAL AEPSC

15 LEGAL SERVICES COSTS DEMONSTRATE THAT THESE COSTS ARE

16 REASONABLE?

17 A. AEPSC Legal Services actual costs have been under budget in recent years, with the

18 exception of 2016 when additional outside services were required to address legal

19 matters. The AEPSC Legal Services budget variances provide support that the

DIRECT TESTIMONY 26

LEIGH ANNE STRABLER 125

1 department's managers are effectively managing expenses and making reasonable and

2 prudent decisions, balancing appropriate staffing levels and the use of outside services

3 to perform necessary legal work.

4 2. Cost Trends

5 Q. PLEASE DISCUSS THE TRENDS IN AEPSC LEGAL SERVICES CHARGES TO

6 AEP TEXAS LEADING UP TO THE TEST YEAR.

7 A. Table 6 depicts the trends in AEP Texas actual affiliate charge for AEPSC Legal

8 Services for the calendar years 2015 — 2018. The Legal Services charges to AEP

9 Texas have remained stable over this time period and reflects the organization's

10 continuing efforts to control costs.

11 Table 6

AEPSC Legal Services Charges to AEP Texas

2015 2016 2017

2018 Adjusted Test Year

$1,925,517 $1,803,268 $1,717,093 $2,001,175

12 3. Staffing Trends

13 Q. PLEASE DISCUSS STAFFING CHANGES WITHIN THE AEPSC LEGAL

14 SERVICES ORGANIZATION.

15 A. As shown in the table below, the Legal Services staff increased by eight employees in

16 the Test Year over the 2015 staffing level. These increases were primarily due to the

17 addition of in house legal personnel to handle more legal matters in house in a cost

18 effective manner and reflect the workload performed by in-house counsel over each of

19 these years.

DIRECT TESTIMONY 27 LEIGH ANNE STRAHLER

126

1 Table 7

AEPSC Legal Services FTEs

2015 2016 2017 2018 Test Year

FTEs 102 106 107 110

2 4. Benchmarking

3 Q. HOW DOES THE HOURLY RATE FOR AEP IN-HOUSE COUNSEL COMPARE

4 TO THE HOURLY RATES OF OUTSIDE LAW FIRMS?

5 A. Company witness Baryenbruch determined the AEPSC in house attorney cost per hour

6 to be $161 in 2018, which is less than the average hourly rate for outside counsel.

7 5. Process Improvements and Cost Savings Initiatives

8 Q. WHAT COST SAVINGS INITIATIVES AND/OR PROCESS IMPROVEMENTS

9 DOES AEP LEGAL SERVICES ENGAGE IN TO CONTROL COSTS AND

10 IMPROVE SERVICE?

11 A. I have already mentioned the Legal Service's efforts to control outside counsel costs.

12 Legal Services reviews all outside legal bills and approves the reasonableness of the

13 charges. In addition, Legal Services has an automated billing system in place to

14 streamline and monitor the outside billing process. The billing system includes

15 automated processes for enforcing billing guidelines as invoices come in and includes

16 automated provisions to identify potential billing issues, such duplicative billings.

17 Legal Services also uses the Sky Analytics database to ensure that it is paying

18 appropriate rates for outside legal services.

DIRECT TESTIMONY 28 LEIGH ANNE STRAHLER

127

1 E. Description of AEPSC Environmental Services

2 Q. HOW DOES AEP TEXAS RECEWE ENVIRONMENTAL SERVICES?

3 A. The AEPSC Environmental Services group provides environmental services to AEP

4 Texas. Although this group reports organizationally to AEP's Generation organization,

5 the AEPSC Environmental Services group provides services to Distribution and

6 Transmission organizations as well.

7 Q. PLEASE DESCRIBE THE AEPSC ENVIRONMENTAL SERVICES

8 DEPARTMENT AND THE SERVICES IT PROVIDES TO AEP TEXAS?

9 A. The Environmental Services Department is led by a Senior Vice President who

10 oversees four functional groups, including two that provide services to AEP Texas.

11 These two groups, Water & Ecological Resource Services and Land Environment &

12 Remediation Services, provide day-to-day environmental permitting for transmission

13 projects and environmental compliance support for transmission and distribution

14 facilities. These services are provided mainly to Distribution, Workplace Services, and

15 Transmission functions for AEP Texas.

16 Q. WERE THE SERVICES PROVIDED DURING THE TEST YEAR BY THE

17 ENVIRONMENTAL SERVICES DEPARTMENT NECESSARY IN ORDER FOR

18 AEP TEXAS TO PROVIDE RELIABLE UTILITY SERVICE?

19 A. Yes. The services are necessary to undertake and complete environmental compliance

20 requirements under various federal and state regulatory programs. The services also

21 include training on those environmental requirements, as well as analytical laboratory

22 services related to environmental samples (e.g., for oil spill remediation) as well as

23 operational samples (e.g., testing of physical and chemical properties of insulating oil

DIRECT TESTIMONY 29 LEIGH ANNE STRAHLER

128

1 for operational purposes). No other department in AEPSC or AEP Texas provides

2 environmental services to AEP Texas so there is no duplication of services.

3

F. Reasonableness of AEPSC Environmental Services

4

Costs Charged to AEP Texas

5 Q. WHAT ARE THE AEPSC TEST YEAR CHARGES TO AEP TEXAS FOR THE

6 ENVIRONMENTAL SERVICES CLASS OF AFFILIATE COSTS?

7 A. The total amount of adjusted test year billings to AEP Texas from AEPSC for

8 environmental services is $497,993. Approximately 78 percent of the AEPSC

9 Environmental Services costs allocated to AEP Texas are directly related to labor and

10 fringe benefits of the group's employees. The reasonableness of the compensation and

11 benefits paid for AEPSC Environmental Services is supported by the testimony of

12 Company witnesses Carlin and Cooper, respectively. AEP Texas witness Frantz

13 addresses the allocation of these costs as part of his testimony. The remaining 22

14 percent of the charges to AEP Texas were for outside services and other materials and

15 supplies.

16

Table 8

17 Com onents of Environmental Services Class bv Cost Cate o Labor Outside

Services Other Grand Total

Amount $388,692 $61,875 $47,426 $497,993 % of Total 78% 12% 10% 100%

18 Q. WHAT APPROACH DOES YOUR TESTIMONY TAKE TO DEMONSTRATE THE

19 REASONABLENESS OF AEPSC'S CHARGES TO AEP TEXAS FOR

20 ENVIRONMENTAL SERVICES?

DIRECT TESTIMONY 30 LEIGH ANNE STRAHLER

129

1 A. My testimony utilizes a combination of indicators: cost trends, budget performance,

2 and staff trends.

3 1. Cost Trends

4 Q. PLEASE DISCUSS THE TRENDS IN AEPSC ENVIRONMENTAL SERVICES

5 CHARGES TO AEP TEXAS.

6 A. The Table 9 depicts the trends in AEP Texas actual affiliate charges for AEPSC

7 Environmental Services for the calendar years 2015 to 2017, and the Adjusted Test

8 Year costs for which AEP Texas is seeking recovery. AEPSC Environmental Services

9 charges to AEP Texas have remained stable from 2015 through the Test Year.

10 Table 9

AEPSC Environmental Services Charges to AEP Texas

2015 2016 2017 Adjusted Test Year

$451,764 $469,076 $500,845 $497,993

11 2. Budget Performance

12 Q. WHAT PROCESSES DOES THE AEPSC ENVIRONMENTAL AFFAIRS

13 ORGANIZATION USE TO ENSURE COST EFFECTIVE PROVISION OF

14 SERVICES?

15 A. AEPSC Environmental Services employs standardized budgeting tools to ensure that

16 costs are controlled within the individual sections of the department. AEPSC

17 Environmental Services has its own budget to which it must adhere. Budgets are set

18 annually and compliance is monitored by the use of monthly variance reports.

19 Q. HOW HAS THE AEPSC ENVIRONMENTAL SERVICES ORGANIZATION

20 PERFORMED IN COMPARISON TO ITS BUDGETS?

DIRECT TESTIMONY 31 LEIGH ANNE STRAHLER

130

1 A. Table 10 below compares AEPSC Environmental Services total, actual expenditures

2 to budget targets for which it is accountable, for calendar years 2015 to 2018. These

3 expenses are allocated to AEP's operating companies, including AEP Texas, based on

4 allocation formulas. These amounts reflect what centralized Environmental Services

5 budgeted and spent for the entire AEP System, not simply AEP Texas.

6 Table 10

7 AEPSC Environmental Services Budget vs. Actual

2015 2016 2017 2018 Test Year ACTUAL 12,870,949 13,612,999 13,878,008 13,631,871 BUDGET 12,752,612 13,055,232 13,477,239 13,482,247

VARIANCE (Over)/Under (118,337) (557,767) (400,769) (149,623)

8 Q. HOW DOES THIS COMPARISON OF BUDGETED VERSUS ACTUAL AEPSC

9

ENVIRONMENTAL SERVICES COSTS DEMONSTRATE THAT THESE COSTS

10

ARE REASONABLE?

11 A. AEPSC Environmental Services' had slight variances during this time period, due

12

mainly to increased expenses of outside services. AEPSC Environmental Services'

13 budget variances provide support for the conclusion that the department's managers are

14 effectively managing expenses and making reasonable and prudent decisions regarding

15 major spending initiatives.

16 3. Staffing Trends

17 Q. PLEASE DISCUSS STAFFING CHANGES WITHIN THE AEPSC

18 ENVIRONMENTAL SERVICES ORGANIZATION.

19 A. As shown in Table 11, the AEPSC Environmental Services organization has added nine

20 FTEs since 2015. Most of the new FTEs are in the Water & Ecological Resource

DIRECT TESTIMONY 32

LEIGH ANNE STRAHLER 131

1 Services group, and were necessary to address ongoing environmental compliance

2 requirements.

3 Table 11

4 AEPSC Environmental Services FTEs

2018 Test 2015 2016 2017 Year

FTEs 103 107 109 112

5 Q. WHAT IS YOUR CONCLUSION REGARDING THE REASONABLENESS OF

6 THE AEPSC ENVIRONMENTAL SERVICES COSTS?

7 A. Together the cost and staffing trends along with and budget performance, viewed in

8 light of the array of essential services provided by centralized Environmental Services,

9 show that these affiliate costs are reasonable and necessary.

10

11 VII. RATE CASE EXPENSES

12 A. Rate Case Expenses Associated with this Proceeding

13 Q. WHAT PROCESS DOES AEP TEXAS PROPOSE FOR REVIEW AND

14 RECOVERY OF RATE CASE EXPENSES ASSOCIATED WITH THIS

15 PROCEEDING?

16 A. AEP Texas proposes that the review of the reasonableness of the rate case expenses

17 incurred in connection with this proceeding and the determination of the mechanism

18 for their recovery be severed to a separate proceeding to be convened at the conclusion

19 of this case. Rate case expenses incurred in this proceeding by the Company and cities

20 should be updated at that time to allow review of actual rate case expenses already

21 incurred. This approach is consistent with procedures followed in recent rate cases. In

DIRECT TESTIMONY 33 LEIGH ANNE STRAHLER

132

1 that separate severed proceeding, AEP Texas will also request approval of the recovery

2 mechanism for the rate case expenses associated with prior dockets that I address in

3 Section VII(B) below.

4 Q. HAS AEP TEXAS PREPARED AN ESTIMATE OF THE COST OF PREPARING

5 AND LITIGATING THIS RATE CASE FILING?

6 A. Yes. I estimate that the cost for processing this case is approximately $6.335 million.

7 Schedule II-E-4.5 is a schedule detailing the estimated expenses for preparing and

8 litigating this proceeding. Only costs of outside consultants, legal counsel and

9 incremental expenses such as publication of notice, printing, travel, temporary

10 employees and miscellaneous expenses is included in the estimate. No separate payroll

11 costs are being requested for AEPSC or AEP Texas personnel who have prepared and

12 support the filing.

13 Q. PLEASE DESCRIBE THE PROCESS EMPLOYED TO PREPARE THIS

14 APPLICATION.

15 A. AEP Texas and the AEPSC centralized Case Management group are responsible for

16 coordinating the preparation and litigation of the rate case filings for AEP Texas. Many

17 departments throughout AEPSC and AEP Texas participated in the preparation of this

18 rate case, including regulatory accounting, pricing and costing, distribution,

19 transmission, construction management, customer services and other departments. In

20 addition, the AEP Legal Department, in conjunction with AEP Texas and the Case

21 Management group, is responsible for coordinating the activities of outside consultants

22 and legal counsel.

DIRECT TESTIMONY 34 LEIGH ANNE STRAHLER

133

1 Q. PLEASE DESCRIBE THE COSTS AEP TEXAS IS SEEKING TO RECOVER

2 RELATED TO THIS APPLICATION.

3 A. AEP Texas is seeking recovery of four categories of costs: outside consultants, outside

4 legal counsel, cities expenses and miscellaneous expenses. Internal employee time

5 associated with legal and regulatory requirements is not included in the rate case

6 expenses.

7 Q. PLEASE DESCRIBE THE OUTSIDE CONSULTING EXPENSES.

8 A. Outside consultants were employed to develop and/or support various requests in this

9 filing including return on equity, cash working capital, catastrophe reserve, capital

10 structure, AMS and affiliate costs.

11 Robert B. Hevert and his firm, Scott Madden, is filing testimony supporting the

12 recommended return on equity for AEP Texas.

13 Jay Joyce of Expergy, prepared a lead-lag study to determine the appropriate

14 amount of cash working capital to be included in cost of service.

15 Greg Wilson of Lewis & Ellis, is providing testimony supporting AEP Texas'

16 propdsed catastrophe reserve treatment.

17 Steve Fetter, of Regulation Unfettered, is providing testimony regarding capital

18 structure and factoring.

19 Pat Baryenbruch, of Baryenbruch & Company, LLC, conducted a

20 comprehensive review of AEPSC's affiliate services and prepared testimony regarding

21 AEPSC's affiliate services, budgeting processes, use of allocation factors, cost trends,

22 and benchmarking of AEPSC costs.

23 Brent Heidebrecht, of Financo, provided modeling support for the AMS

24 reconciliation.

25 AEP Texas negotiated rates with each of the outside consultants discussed

26 above based upon the scope of the requested engagement and customary fees paid to

27 consultants with the required level of experience in their respective disciplines.

DIRECT TESTIMONY 35 LEIGH ANNE STRARLER

134

1 Estimated expenses of outside consultants were developed through discussions with

2 the consultants on the scope of the engagement and based upon expenses incurred in

3 prior rate cases.

4 Q. PLEASE DESCRIBE THE EXPENSES FOR OUTSIDE LEGAL COUNSEL.

5 A. AEP Texas has employed outside legal counsel from Duggins Wren Mann & Romero,

6 LLP, as regulatory counsel for AEP Texas, along with in-house counsel. This outside

7 firm has worked with AEP Texas previously and has extensive experience in Texas

8 regulatory matters. Fees have been negotiated based upon the scope of the engagement

9 and the customary fees for regulatory attorneys.

10 Q. PLEASE DESCRIBE THE CITIES EXPENSES.

11 A. PURA § 33.023 requires AEP Texas to reimburse cities in its service territory for their

12 reasonable and necessary expenses of participating in proceedings for the review of

13 rates. The PUC will determine what costs are reasonable and necessary expenses for

14 future recovery.

15 Q. PLEASE DESCRIBE THE MISCELLANEOUS EXPENSES.

16 A. Miscellaneous expenses incurred by AEP Texas include expenses for printing,

17 temporary employees, travel, lodging and other miscellaneous items. Printing

18 expenses include costs of printing the rate filing package, testimony, discovery and

19 costs of copying other documents associated with the filing. Printing costs have been

20 estimated based upon the expected volume of the rate filing package and costs of

21 responding to discovery in prior cases. Temporary employees may be utilized to assist

22 in printing and assembling the rate filing package and other documents, word

23 processing and other support activities. Travel and lodging expenses include expenses

DIRECT TESTIMONY 36 LEIGH ANNE STRABLER

135

1 of employees incurred in traveling from their work locations to locations required to

2 prepare and participate in the filing. In addition to the travel required to prepare the

3 filing, AEPSC and AEP Texas personnel will incur expenses to participate in the

4 hearings in Austin. Miscellaneous expenses also include other expenses of preparing

5 and litigating the filing.

6 B. Rate Case Expenses Associated with Prior Dockets

7 Q. WHAT IS AEP TEXAS SEEKING IN THIS PROCEEDING RELATING TO RA IE

8 CASE EXPENSES ASSOCIATED WITH PRIOR PROCEEDINGS?

9 A. AEP Texas is seeking a reasonableness finding in this proceeding for rate case expenses

10 incurred in prior dockets that have yet to be recovered. Those dockets and associated

11 expenses for which AEP Texas seeks recovery are as follows:

12 • Docket No. 28840, Application of AEP Texas Central Company for Authority

13 to Change Rates,

14 • Docket No. 33309, Application of AEP Texas Central Company for Authority

15 to Change Rates,

16 • Docket No. 33310, Application of AEP Texas North Company for Authority to

17 Change Rates

18 • Docket No. 34301, Proceeding to Consider Rate Case Expenses Severed from

19 Docket No. 33310 (Application of AEP Texas North Company for Authority to

20 Change Rates) and Docket No. 33309 (Application of AEP Texas Central

21 Company for Authority to Change Rates)

22 • Docket No. 40261, Application of AEP Texas Central Company and AEP Texas

23 North Company for Approval of Advanced Metering System Reconciliation

24 Pursuant to PUC Subst. R. §25.130(k)(6)

25 • Docket No. 47015, Application of AEP Texas, Inc. to Amend Its Distribution

26 Cost Recovery Factors

27 • Docket No. 48222, Application of AEP Texas Inc. to Amend Its Distribution

28 Cost Recovery Factors

29 • Docket No. 48577, Application of AEP Texas Inc. for Determination of System

30 Restoration Costs

DIRECT TESTIMONY 37 LEIGH ANNE STRAITIER

136

1 The rate case expenses associated with these dockets total $1,000,027.12

2 through February 2019. However, as shown on EXHIBIT LAS-2, AEP Texas is

3 proposing to offset this amount by the #302,051 over-recovered by AEP Texas for

4 Docket No. 34301. Therefore, AEP Texas seeks a finding that the $1,000,027.12 was

5 reasonable, but will only seek recovery of $697,975.99 in the severed docket.

6 Q. PLEASE DESCRIBE THE COSTS AEP TEXAS IS SEEKING TO RECOVER IN

7 CONNECTION WITH THESE PRIOR PROCEEDINGS.

8 A. AEP Texas is seeking recovery of three categories of costs: outside legal counsel,

9 cities expenses, and miscellaneous expenses and has not included internal employee

10 time associated with legal and regulatory requirements in the requested rate case

11 expenses.

12 Q. PLEASE EXPLAIN EXHIBIT LAS-2

13 A. EXHIBIT LAS-2 reflects the rate case expenses AEP Texas seeks to recover in

14 connection with each of the prior dockets described above. EXHIBIT LAS-2 also

15 contains a summary of the items that make up AEP Texas' rate case expenses for each

16 prior docket. The summary includes a description of: 1) the particular services

17 provided by each law firm; and 2) a description of miscellaneous expenses including

18 printing, delivery, travel and lodging, temporary services and other expenses.

19 Q. DO THE LEGAL INVOICES CONTAIN SUFFICIENT INFORMATION TO

20 IDENTIFY THE AMOUNT OF EXPENSES ASSOCIATED WITH THE ISSUES

21 INVOLVED IN EACH CASE?

22 A. Yes. Information that details and itemizes expenses by issue, proceeding stage, and

23 litigation activity is provided in the invoices.

DIRECT TESTIMONY 38 LEIGH ANNE STRAHLER

137

1 Q. WHAT PROCESS DOES AEP TEXAS PROPOSE FOR REVIEW OF RATE CASE

2 EXPENSES ASSOCIATED WITH THESE PRIOR PROCEEDINGS?

3 A. AEP Texas proposes the review of the reasonableness of rate case expenses incurred in

4 connection with these prior proceedings in this docket; however, AEP Texas is not

5 requesting approval of the mechanism for their recovery in this docket. To recover

6 these prior expenses, AEP Texas will request recovery through the mechanism

7 requested in the severed docket that is opened to address the recovery of expenses

8 associated with this case.

9 Q. WHY DOES AEP TEXAS PROPOSE THAT THE FEES ASSOCIATED WITH

10 THESE PRIOR CASES BE REVIEWED IN THE CURRENT PROCEEDING?

11 A. The litigation in these cases has concluded. Therefore, review of these fees incurred

12 are well-timed for review in this proceeding.

13 Q. WHAT WAS YOUR RESPONSIBILITY RELATED TO THE ABOVE DOCKETS?

14 A. Although some of the dockets occurred before I assumed my current role as Vice

15 President, Regulatory & Finance of AEP Texas, I was directly involved in the other

16 two dockets (Docket Nos. 48222 and 48557). As Vice President, Regulatory &

17 Finance, my team is responsible for the preparation, filing, and litigation of all

18 regulatory cases such as these dockets. In supervising the teams prosecuting these

19 proceedings, I was in frequent contact with the persons primarily responsible for

20 reviewing the reasonableness and necessity of the invoices submitted to AEP Texas in

21 association with these proceedings. Due to this responsibility, I have gained familiarity

22 with the prevailing hourly rates associated with individuals and the firms that provide

23 consulting and legal services in connection with utility general rate cases, distribution

DIRECT TESTIMONY 39 LEIGH ANNE STRAHLER

138

1 cost recovery factor proceedings, and other regulatory proceedings. I am also familiar

2 with the range of services provided by outside attorneys in connection with such cases,

3 and the amount of time and effort expended in performing such engagements. The

4 factual matters addressed in my testimony are based on my personal knowledge gained

5 from prior experience, my participation and management of recent AEP Texas

6 proceedings before the Commission, over 13 years of experience working for AEP in

7 various capacities, and from records maintained by AEP Texas in the ordinary course

8 of business, including the books and records that are addressed by AEP Texas witness

9 Hamlett.

10 Q. WHAT OTHER WITNESSES ARE SUBMITTING TESTIMONY IN SUPPORT OF

11 AEP TEXAS APPLICATION TO RECOVER RATE CASE EXPENSES?

12 A. As noted above, AEP Texas witness Hamlett also provides testimony related to AEP

13 Texas' requested recovery of rate case expenses. Specifically, in his direct testimony,

14 Mr. Hamlett explains: that the source of the expenses are the Company's books and

15 records and that the rate case expenses AEP Texas seeks to recover represent

16 incremental expense that, absent the regulatory proceedings, would not have been

17 incurred by AEP Texas; confirms that AEP Texas is not currently recovering these

18 expenses via base rates or any other recovery mechanism; explains that the

19 documentation provided by AEP Texas is consistent with past rate case expense

20 proceedings and employee expense account support follows Internal Revenue Service

21 guidelines; and discusses adjustments that were made to the actually incurred expenses

22 to be consistent with prevailing PUC guidelines for recovery of rate case expenses.

DIRECT TESTIMONY 40 LEIGH ANNE STRAHLER

139

1 Q. WHAT PROCEDURE DOES AEP TEXAS EMPLOY TO ENSURE THE

2 REASONABLENESS OF RATE CASE EXPENSES?

3 A. EXHIBIT LAS-3 provides a detailed description of the practices and procedures

4 employed by AEP Texas to control and manage rate case expenses and to ensure that

5 the requested rate case expenses are reasonable and necessary.

6 Q. WHAT WAS AEP TEXAS APPROACH TO OUTSIDE CONSULTANT AND

7 LEGAL STAFFING FOR THE DOCKETS ADDRESSED IN YOUR TESTIMONY?

8 A. AEP Texas staffed these prior cases listed above with a reasonable number of outside

9 lawyers consistent with the procedures outlined earlier in my testimony with regard to

10 the use of external counsel. AEP Texas is a sizeable and complex business, and the

11 amount of information, analysis, and attorney support required in the prior proceedings

12 listed above reflects this fact. The number of outside attorneys AEP Texas used, and

13 the amount of work they performed (as documented in monthly invoices) was

14 reasonable and justified given the nature of these cases, each of which are described

15 above.

16 Considering the scope and complexity of the matters involved, the time and

17 labor required, the value of property at stake, the number and complexity of the legal,

18 procedural and evidentiary issues, and the scope of responsibilities assumed by the

19 outside attorneys, the amount of rate case expenses incurred by AEP Texas is

20 reasonable and necessary. AEP Texas manages the work of its outside counsel so as

21 to avoid duplication of effort, through the oversight of the case manager and the in-

22 house counsel assigned to the case.

DIRECT TESTIMONY 41 LEIGH ANNE STRAHLER

140

1 Q. PLEASE DESCRIBE THE PROCESS THAT AEP TEXAS USES TO SELECT

2 OUTSIDE LEGAL COUNSEL.

3 A. AEP Texas selects its outside attorneys primarily based on their specialized expertise

4 in the area of their particular engagement, the quality of their prior work, and their

5 experience with and knowledge of the AEP Texas operations and/or regulatory

6 matters. AEP Texas is aware of the range of hourly rates for consultants and attorneys

7 in the field of utility regulation because it contracts with such professionals on a routine

8 basis. AEP Texas applies this knowledge in determining the reasonableness of the

9 hourly rates and charges for services in its regulatory proceedings. Based on my

10 experience, the hourly rates charged by these professionals are reasonable, and

11 compared with those of other firms and individuals providing similar services. Further,

12 the hourly rates charged by these professionals are their normal rates.

13 Q. DESCRIBE HOW INVOICES AND OTHER DOCUMENTATION AREA

14 REVIEWED PRIOR TO APPROVAL AND PAYMENT.

15 A. AEP Texas and/or AEPSC personnel have scrutinized all invoices of outside lawyers

16 to ensure that: a) invoice terms are consistent with the terms of the engagement; b)

17 adequate documentation has been provided for time expended for travel and

18 miscellaneous expenses; and c) invoices are accurate and include no duplicate billing.

19 The invoices supporting the rate case expenses sought in connection with the prior

20 dockets listed above are in good order and the amounts requested are supported by

21 appropriate descriptions of the work performed. The hourly fees paid are reasonable

22 and consistent with contract, prevailing standards, and the hours bill by such lawyers

DIRECT TESTIMONY 42 LEIGH ANNE STRAHLER

141

1 are reasonable for the activities that needed to be performed in connection with these

2 dockets.

3 Q. HOW WERE BILLINGS AND EMPLOYEE EXPENSES HANDLED IN THIS

4 REQUES T?

5 A. For purposes of this request, billings were adjusted as necessary to ensure that the items

6 requested were consistent with prevailing PUC guidelines for recovery of rate case

7 expenses, as discussed further in Mr. Hamlett's testimony. Additionally, AEPSC

8 personnel have scrutinized all the employee expense reports of AEP Texas and AEPSC

9 personnel who have charged reimbursable employee expenses to these dockets, and

10 have adjusted accordingly.

11 Q. WHAT DO YOU CONCLUDE REGARDING THE RATE CASE EXPENSES

12 REQUESTED BY THE COMPANY IN CONNECTION WITH PRIOR

13 PROCEEDINGS?

14 A. The supporting rate case expense detail and information provided in EXHIBIT LAS-2

15 and supporting workpapers comes from the books and records maintained by AEPSC

16 for AEP Texas and are true and correct as supported by Mr. Hamlett. The adjustments

17 and explanatory notes contained within such information, the summary of the requested

18 updated rate case expenses, and the description of practices and procedures contained

19 in EXHIBIT LAS-3 and discussed above are accurate and fair representations of the

20 matters addressed, based on my supervision of those responsible for reviewing the

21 requested rate case expenses. For all the reasons discussed above and in the direct

22 testimony of Mr. Hamlett and based on the voluminous supporting detail and

23 information provided, the rate case expenses incurred by AEP Texas for these dockets

DIRECT TESTIMONY 43

LEIGH ANNE STRAHLER 142

I have been reasonably and necessarily incurred. Retention of each of the professionals

2 whose fees and expenses are reflected in those rate case expenses was necessary in

3 order for the Company to properly and fully present its case and to meet Commission

4 requirements for cases of that nature. The amounts billed by outside professionals, out-

5 of-pocket costs incurred by AEPSC personnel, and other miscellaneous expenses are

6 proper and reasonable in amount.

7

8 VIII. CONCLUSION

9 Q. DOES THIS CONCLUDE YOUR DIRECT TESTIMONY?

I 0 A. Yes, it does.

DIRECT TESTIMONY 44 LEIGH ANNE STRAHLER

143

AEP TEXAS REGULATORY & FINANCE ORGANIZATION

Regulatory & Finance

Regulatory Services

Business Operations

Support

Continuous Improvement

EXHIBIT LAS-2

Page 1. of 5

AEP TEXAS INC SUMMARY OF RATE CASE EXPENSES

PUC DOCKET NOS. 33309, 33310, 34301, 40261, 47015, 48222 and 48577

AEP Texas Total Expenses

PUC Docket No. 33309/33310/34301 Legal Expenses - Central Legal Expenses - North

211,749.86 1,827.20

Total Requested Company Expenses Docket No. 33309/33310/34301 $ 213,577.06

PUC Docket No. 40261 Legal Expenses Employee Expenses

82,047.58

55.48

Total Company Expenses Docket No. 40261 $ 82,103.06

PUC Docket No. 47015 Other Expenses Employee Expenses

4,314.05

4,005.91

Total Company Expenses Docket No. 47015 $ 8,319.96

PUC Docket No. 48222 Other Expenses Employee Expenses

372.25 23,414.13

PUC Docket No. 48577

Total Company Expenses Docket No. 48222 $ 23,786.38

Consuttant Expenses Legal Expenses Other Expenses Employee Expenses

2,400.00 366,397.52 26,383.77

3,994.81 Total Company Expenses Docket No. 48577 $ 399,176.10

ota Company Expenses Docke Nos. 33309, 333 0, 3430 , 4026 , 470 5, 482 2 and 48577 726,962.56 Less: Over-Recovery on 34301 Rate Case Amortization- Allocable to Cities (143,175.95)

Tota Company Expenses o be co ec ed or Docke Nos. 3309, 0, 3430 4026 4 0 5, 48222 and 48577 583,786.61

145

Municipal Expenses Reimbursed by AEP Texas Inc City of Abilene City of McAllen

or Docke ota Nos. 33 Municipa , 4026 0, 3430 09,333 Expenses Reimbursed

1,094.64 271,969.92 273 064.56 48222 and 48577

EXHIBIT LAS-2

Page 2 of 5

AEP TEXAS INC SUMMARY OF RATE CASE EXPENSES

PUC DOCKET NOS. 33309, 33310, 34301, 40261, 47015, 48222 and 48577

Municipal Expenses Reimbursed by AEP Texas Total Expenses

PUC Docket No. 33309/33310/34301 City of Abilene City of McAllen

1,094.64 234,968.20

Total Expenses Requested for Reimbursment Associated with Docket Nos. 33309/33310/34301 $

236,062.84

PUC Docket No. 47015 City of McAllen

Financo City of McAllen

12,680 27 Total Expenses Reimbursed Docket No. 48222 $ 12,680.27

24,321.45 Total Expenses Reimbursed Docket No. 48222 $ 24,321.45

Less: Over-Recovery on 34301 Rate Case Amortization- Allocable to Legal

(158,875.18) Total Municipal Expenses to be collected for Docket Nos. 33309, 33310, 34301, 40261, 48222 and 48577

114,189.38