Embed Size (px)

Citation preview

1

How to Reap the Benefits of a Strong Post-

License Monitoring

System

Live WebinarNovember 29, 2011 1-2pm ET

Technology Transfer Tactics Presents

2

Scott D. Marty,J.D., Ph.D.

AssociateBallard Spahr LLP

Judy Ann Byrd, CPA, CFF, CIRA

DirectorInvotex Group

Presenters

Jeffrey M. Sears,

Ph.D., J.D. Associate General

CounselColumbia University

3

It’s about responsibility

(and the money)

4

License Contracts Create Obligations

▼ Internal: Directors, Trustees, Presidents, Deans, Inventors▼ Maximize revenue negotiated▼ Project revenues for budget▼ Fiduciary duty to ensure compliance to terms

▼ External: Economic development offices, partners, licensees, future licensees▼ Maintain relationships for current/future

projects ▼ Clarify ambiguity in Agreement▼ Message of intent to protect rights /proactive

philosophy

5

Agenda

▼ How to set-up the post-license monitoring system

▼ Threshold questions for moving forward on post-license actions

▼ How to build a "team" for carrying forward post-license actions

▼ Categories of post-license actions (audits, licensing opportunities, infringement)

▼ Best practices to increase your likelihood of success in post-license actions

▼ Examples/Case Studies of post-license actions

6

How to Set-up the Post License Monitoring System ▼ Information Needed

▼ Agreement summary ▼ Correspondence▼ Status reports (financial statements,

progress reports)▼ Financial analysis

▼ Columbia’s Program▼ Other tools

▼ Program announcement letter▼ Annual update letter

7

Threshold questions for moving forward on post-license actions ▼ Columbia’s process for review and action

▼ Involvement of finance, business, and legal▼ Annual review of all royalty-bearing licenses

▼ revenue projections and trend analysis▼ deductions▼ milestones or expiration▼ interpretation mistakes▼ internal consistency

▼ Business statements▼ Product releases

8

Threshold questions for moving forward : Red Flagsthere may be errors in reporting if…▼ CHANGES OCCURRED

▼ The person preparing the royalty report is new or not familiar with the license agreement

▼ New products were launched▼ Selling licensed product in new territories▼ New manufacturing facility opened▼ Licensee was acquired or merged with another

company▼ Licensee changed its accounting system▼ Licensee is having financial difficulty▼ Royalty reports are late or arriving later each

period▼ Licensee’s sales of the covered product are not

keeping track with the industry

9

How to build a "team" for carrying forward post-license actions

▼ Know your institution - consider internal constituencies, philosophy and answer to ‘how far are you willing to take this?’▼ university-specific issues

▼ Analyze financial and legal resources▼ Consider external consultants

▼ Manpower▼ Expertise▼ Independence

10

How to build a “team”

• When do I act?

- Must be mindful of contractual rights

- Beware of Statues of Limitations, Estoppel, or Laches issues

- Do you have an internal procedure or policy?

11

Categories of post-license actions

▼ Financial▼ Compile, analyze, communicate▼ Desk audit, communicate▼ Site audit, communicate

12

Decide who to target

▼ Audit rule of thumb is to consider if license is generating over $100,000 in running royalties/year

▼ Review royalty bearing licenses for red flags

▼ Known problems

13

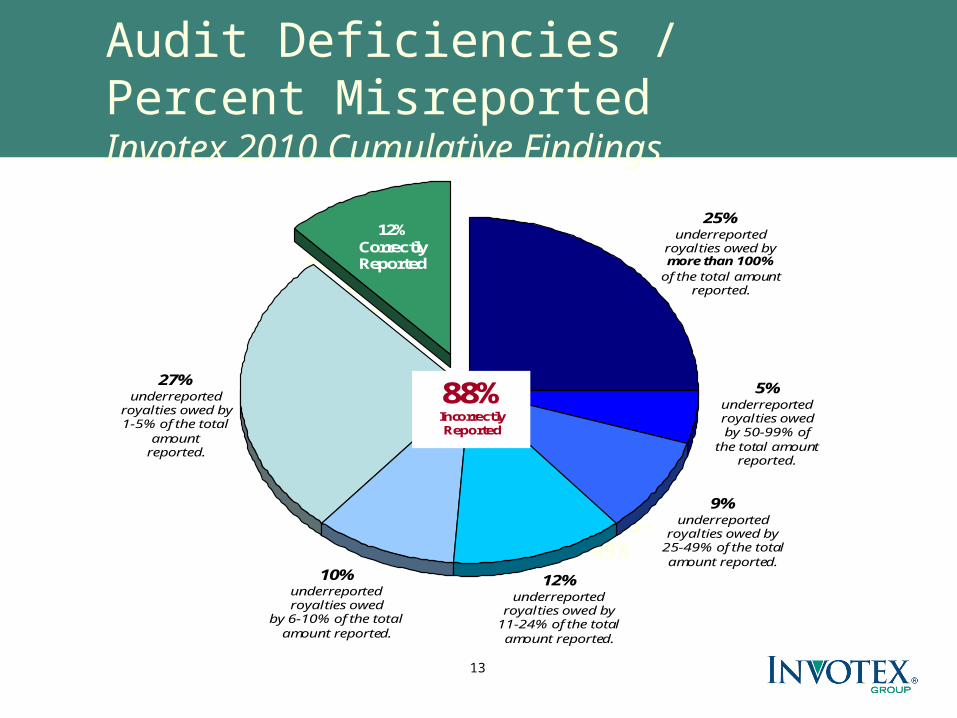

Audit Deficiencies / Percent Misreported Invotex 2010 Cumulative Findings

18 %Properly Reported

27% fell in Over 100%

Underreported!

10% in the 25-49%

27% underreported

royalties owed by 1-5% of the total

amount reported.

10% underreported royalties owed

by 6-10% of the total amount reported.

12% underreported

royalties owed by 11-24% of the total amount reported.

9% underreported

royalties owed by 25-49% of the total amount reported.

5% underreported royalties owed by 50-99% of

the total amount reported.

25% underreported

royalties owed by more than 100%

of the total amount reported.

12% Correctly Reported

88%

Incorrectly Reported

14

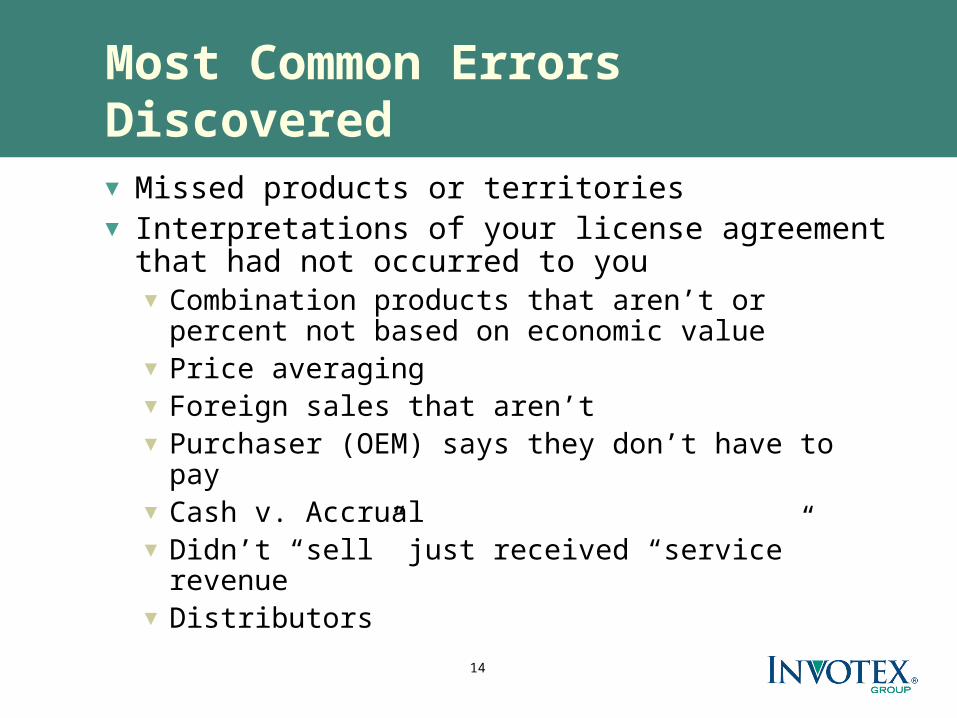

Most Common Errors Discovered▼ Missed products or territories▼ Interpretations of your license agreement

that had not occurred to you▼ Combination products that aren’t or percent

not based on economic value▼ Price averaging▼ Foreign sales that aren’t▼ Purchaser (OEM) says they don’t have to

pay▼ Cash v. Accrual▼ Didn’t “sell” just received “service” revenue▼ Distributors

15

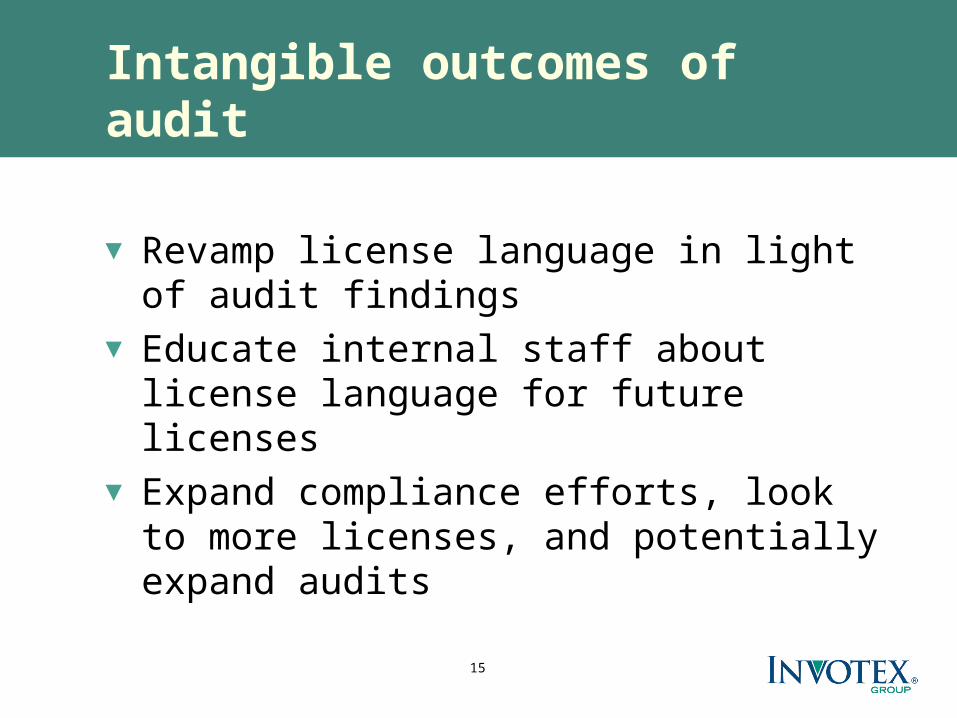

Intangible outcomes of audit

▼ Revamp license language in light of audit findings

▼ Educate internal staff about license language for future licenses

▼ Expand compliance efforts, look to more licenses, and potentially expand audits

16

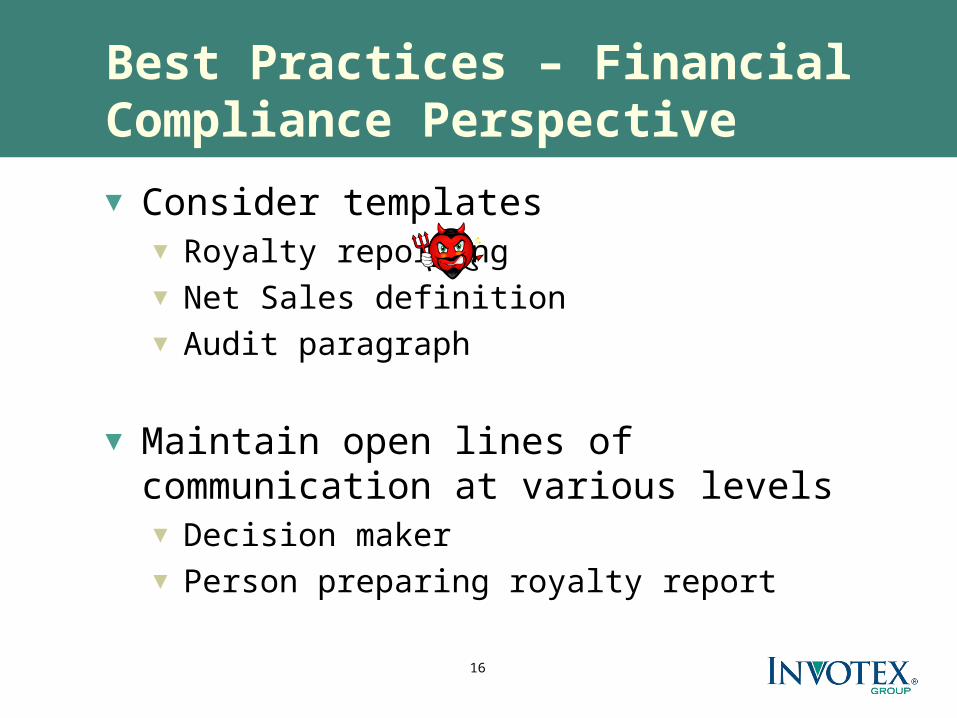

Best Practices – Financial Compliance Perspective

▼ Consider templates▼ Royalty reporting▼ Net Sales definition▼ Audit paragraph

▼ Maintain open lines of communication at various levels▼ Decision maker▼ Person preparing royalty report

17

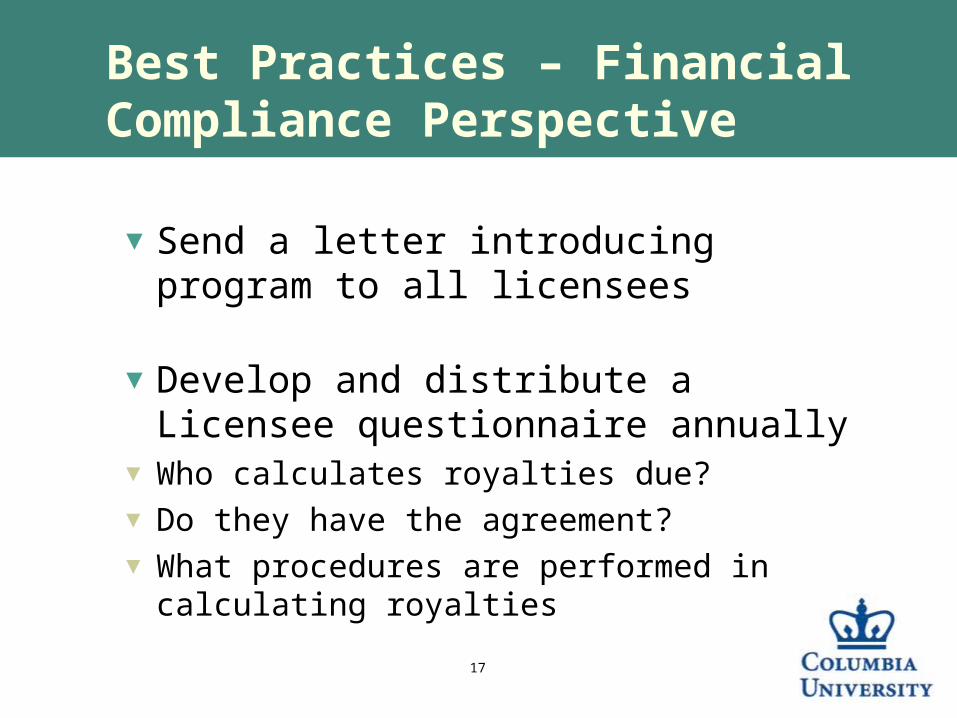

Best Practices – Financial Compliance Perspective

▼ Send a letter introducing program to all licensees

▼ Develop and distribute a Licensee questionnaire annually

▼ Who calculates royalties due?▼ Do they have the agreement?▼ What procedures are performed in

calculating royalties

18

Categories of post-license actions-Legal

• Infringement

• Inventorship/Ownership

• Filing new IP

• Renegotiations

• Breach and Termination

19

Best Practices

• Stay Informed

- Require Reporting (Licensee, Sublicensees, Affiliates)

- Require Copies (Sublicenses, Sponsored Research, Joint Research Projects)

- Require Quarterly Meetings or Access to Licensee Meetings

- Set-up Internal Watches (Google Alerts)

- Beware of Estoppel Issues

20

Best Practices

Inventorship/Ownership

• Be clear about preexisting rights to IP

• Be clear about future IP developed

- Example: "Foreground Intellectual Property" signifies all Intellectual Property conceived, developed or reduced to practice during the course of the Project in the performance of the Work detailed in Appendix XXX.”

- “Foreground Intellectual Property" signifies all Intellectual Property conceived, developed or reduced to practice solely by Licensee/Licensor without the inventive contribution, as defined by United States Patent laws, of the other party, during the course of the Project in the performance of the Work detailed in Appendix XXX. Licensee/Licensor will own all rights title and interest to Licensee Foreground Intellectual Property.

• Make sure you address Joint IP and who has rights

21

Best Practices

Inventorship/Ownership

• Who has the right/duty to control:

- Prosecution

- Commercialization

- Enforcement

22

Best Practices

• Protect what is yours

- Be mindful of the post-Medimmune world

• Covenants not to sue

• Grounds for termination

• Royalty step ups

• Attorneys fees

• Venue

• Milestones

23

Best Practices

Audit Language• “Licensee’s books and the supporting data shall be open to inspection by

Licensor or its agents, upon reasonable prior notice to Licensee, its Affiliates or Sublicensees, as applicable, at all reasonable times for a term of XXX (XXX) years following the end of the calendar year to which they pertain, for the purpose of verifying Licensee’s royalty statement or compliance in other respects with this Agreement.”

• “… once a year for three (3) years after the expiration or termination of this Agreement.”

• “Should such inspection lead to the discovery of at least a five percent (5%) or five thousand dollar ($5,000) discrepancy in reporting to Licensor’s detriment (whichever is greater), Licensee agrees to pay the full cost of such inspection.”

• You may also want to include language regarding the ability to Audit after the expiration of the License.

24

Best Practices – Net Sales

▼ Gross Sales (invoice price) of Licensed Product less the following (only as they pertain to the making, using or selling of Licensed Products and if billed to customer and separately stated on the invoice):▼ Import, export, excise and sales taxes▼ Cost of insurance, installation and shipping to

customer▼ Credits, returns, allowances given and actually taken

▼ If Licensed Product is transferred at below market price, then Gross Sales will be the average price charged to independent third party customers in the same reporting period.

25

Case Study

• Research Tool

- Post-expiration royalties

- Audit rights

- Record keeping

- Pre-expiration manufacturing/post-expiration sales

- End product vs. process payments

26

Scott D. Marty,J.D., Ph.D.

AssociateBallard Spahr LLP

Judy Ann Byrd, CPA, CFF, CIRA

DirectorInvotex Group

Questions?

Jeffrey M. Sears,

Ph.D., J.D.Associate General

CounselColumbia University