Embed Size (px)

Citation preview

1

Governance issues and measures toward sustainability in Paris / Ile-de-France

Mrs. Sophie MOUGARD

EMTA General Meeting15-16 April 2010 in Budapest (Hungary)

22

Administrative levels

The Ile-de-France region:

• 11.5 million inhabitants(18.13% of the French population)

• 5.3 million jobs• 29% of GNP• Area: 12,000 km²• Regional administrative levels:

– 1 Regional Council– 8 ‘Départements’ (counties) of which the

City of Paris– 110 intermunicipalities– 1 280 municipalities

French administrative levels:

• State• Regions• ‘Départements’ (counties)• Intermunicipalities• Municiplaities

33

Metro: 14 lines, including 1 fully automated 214 km / 300 stations 1,472.5 million journeys in 2008

Railway network: 1,411 km / 444 stations 1,296.1 million journeys in 2008

Bus: 1,312 lines / 22,670 km28,950 stops / 8,000 buses 1,287 million journeys in 2008

Tramway & TVM: 3 tram lines / 31.5 km and TVM 12.5 km(TVM: express bus in exclusive lane) 6 stops total

107.6 million journeys in 2008

Tram-train: 1 line / 8 km / 11 stops

Main characteristics of the area covered by STIF

Networks & figures

44

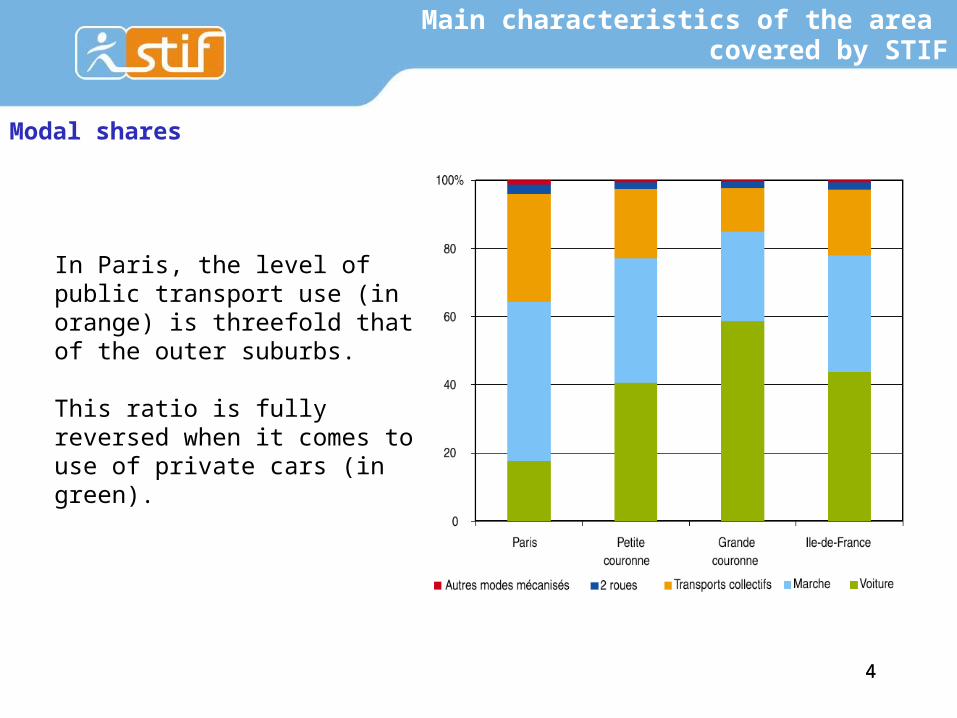

Main characteristics of the area covered by STIF

In Paris, the level of public transport use (in orange) is threefold that of the outer suburbs.

This ratio is fully reversed when it comes to use of private cars (in green).

Modal shares

55

Main characteristics of the area covered by STIF

Motorisation level (cars vs public transport)

Car share in motorized mobility

Average yearly evolution of both road traffic and PT traffic

6

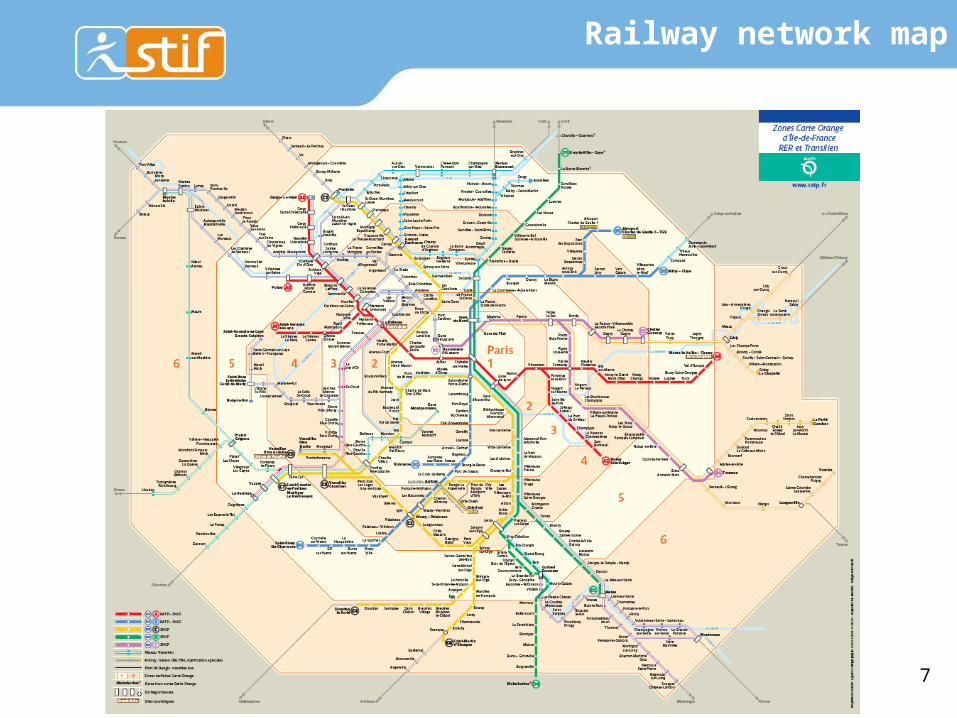

Railway network in Ile-de-France

7

Railway network map

88

Metro network map

99

Bus network and ‘Mobilien’ mapMobilien: regional bus network

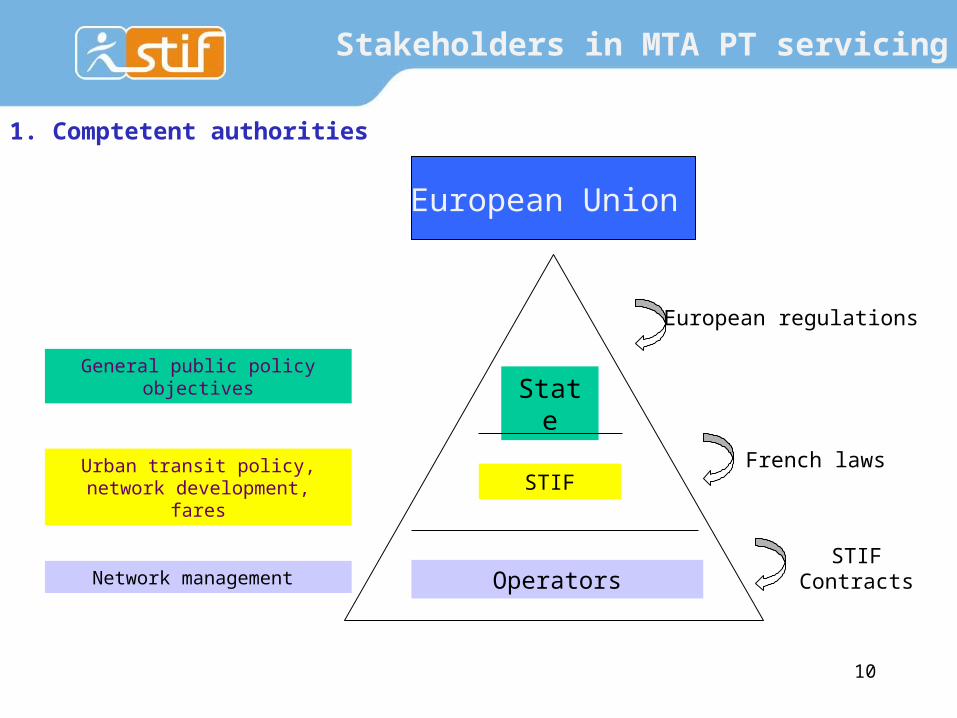

Stakeholders in MTA PT servicing

European Union

General public policy objectives

Urban transit policy, network development, fares

Network management

European regulations

French laws

STIF Contracts

State

STIF

Operators

10

1. Comptetent authorities

1111

• STIF is the public transport authority for the Île-de-France Region and is competent for all modes of transport. Its missions are as follows:

– definition and organisation of public transport services (definition of services - road, light rail, heavy rail - and quality, fare policy, contractual relation with operators, financial balance of the system)

– extension of the network and projection,– planning and monitoring activity.

Since 1st July 2005:

• The Regional Council holds a majority of the seats on the STIF Board as well as the chairmanship

• The French government no longer has representation on the STIF Board

• 2 new representatives have joined the Board:– 1 representative from the economic sector

appointed by the CRCI– 1 representative from the intermunicipalities in

Ile-de-France, elected by the college of EPCI chairmen

CRCI: Regional Chamber of Commerce and IndustryEPCI: Inter-municipalities

2. Organisers

Stakeholders in MTA PT servicing

STIF Board

RATP – National public company (Monopoly)Metro systemTramway systems2 RER lines (rapid transit railway)4,300 buses – 266 lines in central zone

SNCF – National public company (Monopoly)5 RER lines (2 shared with the RATP)

Transilien railway network (trans-regional)

RFF – French Railway NetworkAs owner of the railway infrastructure, this a public body

administers the corridors and is funded through fares.

OPTILE – Association of 76 private bus operators(of which 3 main companies such as VEOLIA, KEOLIS and TRANSDEV)

4,181 buses daily – 1,079 regular lines in the outskirts of Paris284 million journeys in 2008Own exclusive rights to their routes 12

3. Service providers

Stakeholders in MTA PT servicing

1313

Contribution to PT financing (2008)

Direct revenue(passengers)

€ 2,979 m

38.3%

Transport tax€ 2,971 m

38.2%

Public subsidies € 1,522 m

19.6%

(Incl. € 1.075 bn statutory contributions and € 74 m fare subsidies from the

Regional Council)

RATPPublic corporation

(Metro + Bus + Tramways + RER)

€ 4,275 m

55%

SNCF Public corporationRailway networks

€ 2,642 m(incl. € 600 m in tolls to RFF)

34%

OPTILEBus network

€ 777.2 m

10%

Other

€ 300 m

3.9%

Operating expenses

€ 7,772 m

Other

€ 77.72 m

1%

1414

REGION DEPARTEMENTS

STIF

Local governments or groups of them

Employers

SNCF RATP OPTILE

TT

HOUSEHOLDS

Contracts

Grants for extra services in

specific areas

season transport

passreimb.

Third-party payersSocial fares

Tickets

Contribution to PT financing

15

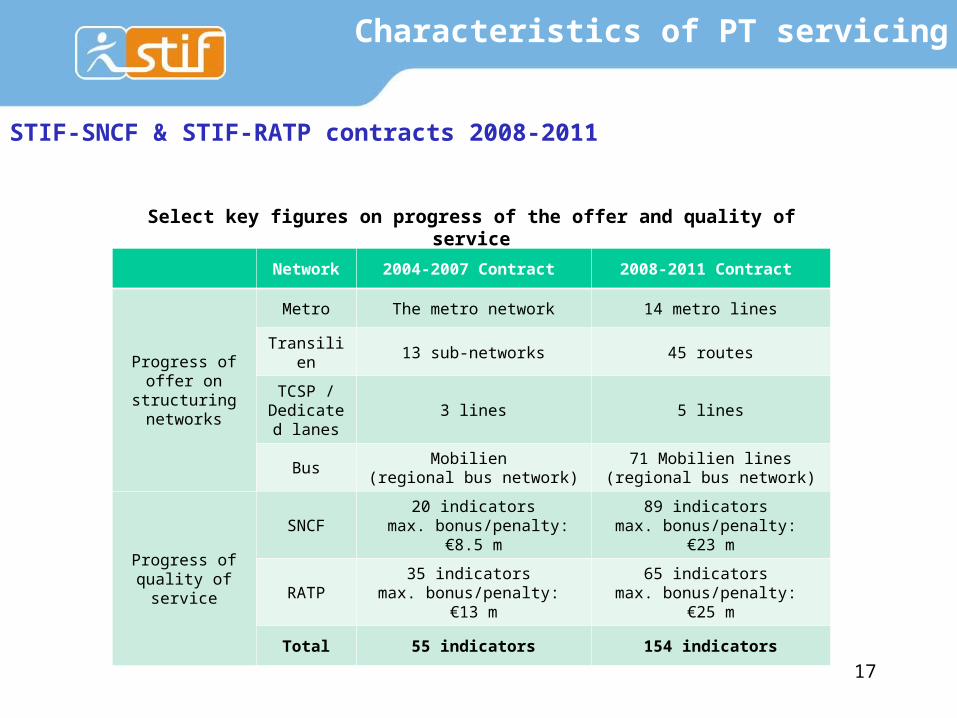

Characteristics of PT servicing

• STIF-SNCF and STIF-RATP contracts signed in February 2008

• OPTILE contracts:• ‘Type I’ contracts (1st generation) were signed in 2007• ‘Type II’ contract negotiations (2nd generation) are underway

• RFF contract (railway infrastructure) signed in July 2009

Contractual relationships

16

Characteristics of PT servicing

• Better service for passengers in Ile de France

• Implementing tools for an ambitious policy on public transport development

• New partnership relation between STIF and operators

• Service standards: description of supply, regularity, accessibility, ticket distribution, station services, information, equipment reliability...

• Measuring, inspection methods and profit-sharing levels in relation to objectives (bonus / penalty)

• Stricter requirements: different rules apply according to line, type of day and time of day

• Clearer and more motivating methods of compensation that separate reserves for investment costs from reserves for operating expenses

• Ambitious multi-year investment programmes to modernise the networks(€ 7 billion for RATP and SNCF over four years)

STIF-SNCF & STIF-RATP contracts 2008-2011

17

Network 2004-2007 Contract 2008-2011 Contract

Progress of offer on

structuring networks

Metro The metro network 14 metro lines

Transilien 13 sub-networks 45 routes

TCSP / Dedicated

lanes3 lines 5 lines

BusMobilien

(regional bus network)71 Mobilien lines

(regional bus network)

Progress of quality of service

SNCF20 indicators

max. bonus/penalty: €8.5 m

89 indicators max. bonus/penalty:

€23 m

RATP35 indicators

max. bonus/penalty: €13 m

65 indicators max. bonus/penalty:

€25 m

Total 55 indicators 154 indicators

Select key figures on progress of the offer and quality of service

Characteristics of PT servicing

STIF-SNCF & STIF-RATP contracts 2008-2011

18

These contracts are advancing the previous funding agreement towards an actual contractual system

The ‘Type I’ contract (1st generation) signed on 1st January 2007 for a maximum of four years is an initial step:

• Monitor and improve the offer and quality of service• Use a uniform pay scale• Produce multi-year business plans

The stakes of the ‘Type II’ contracts (2nd generation):• Cohesion/basin network (catchment area)• A public service contract• Stricter requirements for both the offer and the quality of service• Compensation in line with public service obligations

‘Type II’ contracts would include a partnership agreement involving the local governments affected, the STIF and the operator

Characteristics of PT servicing

Contracts with OPTILE companies

1. Single tickets: 5% (of the total of sales)

2. Ticket books: 15%

3. Season passes: 80%

• ‘Navigo’ : Weekly passesMonthly passes (3 million units)Yearly passes ‘Intégrale’ (1 million units)

• ‘Imagine’R’: Student pass (up to 26 years old)

Reduced Transit Fares:

Free for those receiving unemployment benefit (RMI), single-parent allowance (API), Specific Solidarity benefit (ASS), Supp. Universal Healthcare Coverage recipients (CMU) (RSA (job support income) benefits taken into account)

‘Carte Solidarité Transport’ (for recipients of State benefits): 75% discount

‘Améthyste’: yearly season pass distributed by the ’Départements’ (French counties) to 300,000 seniors and disabled

Tourist Passes:

‘Mobilis’ (valid during 1 day only) ‘Paris Visite’ (valid during 1,2,3 or 5 days) 19

Characteristics of PT servicing

Fares (incl. discounts)

20

Responsibilities regarding other transport modes in the MTA area

• Different actors are responsible for planning, at different levels:

– State, Region, ‘Département’ (Counties), Built-up (metropolitan) Area, Towns

• Plans are linked to legal compatibility requirements

State‘Départements’ (counties)

Region Municipalities

Public transport RoadsDelivery of goodsPublic parking

STIF

Sharing of responsibilities

21

Quality of service and passenger rights

Assessing quality delivered and quality perceived It is important that contracts include a dual quality assessment. • The quality of the service provided by the operator: this can be assessed using a set of indicators established by common agreement between the Organising Authority and the company. This measure enables the company’s performance in a certain number of areas to be assessed. • The quality of service as perceived by passengers: this is more often assessed through surveys conducted with passengers on the various networks, by asking them questions on the different points that are assessed in the contract. The important thing is to have this dual quality perspective, in order to check that what is being assessed in the contract with the operator is actually what passengers on the ground are experiencing. This enables us to ensure that the survey findings are consistent. Example: conducting a passenger survey enabled the STIF to realise that the RATP and the SNCF were receiving a bonus based on station and train cleanliness indicators, while passengers viewed the situation as unsatisfactory . La phrase n’est pas terminée dans la version FR. Voici donc ma suggestion.

Quality of service in general

22

Quality of service in the contracts 2008-2011

General principles and indicators within the contract

More detailed and complete description of the commitments regarding each

component of the quality of service (information, reception desks, selling, accessibility,

safety...)

Specifying regularity follow-up (objectives unchanged) as a replacement for the

global approach

Specifying the follow-up of network access indicators (information, reception in

station, functioning of the escalators) as a replacement for the global approach

New commitments coupled with penalties on services relevant for mobility reliability

(help desk to passengers in station, repairing of the lifts and escalators, information

about their reactivation lead time)

Quality of service and passenger rights

23

Better recognition of passenger’s feeling: setting up of a yearly survey in order to

assess the evolution of passenger’s perception regarding the quality of service

rendered, which results in bonus / malus

Widespread quality of service measuring device: threefold of the number of

indicators followed with bonus / malus (154 in total), doubling of the financial incentives

budget (€ 48 m), possible bonus decrease in case of aid and repairing delays

‘Technical’ measure completed by a yearly passenger's perception survey (resulting

in bonus / malus)

A strengthened control of the measures received by the operators: yearly audits and

penalties in case of significant gaps compared to the objectives

Quality of service and passenger rights

Quality of service in the contracts 2008-2011

24

Relationships with passengers

Communication: setting up of common principles with operators • consistent and readable communication• building up the image of an integrated network (fare policy, information, branding…)

Setting up local consultation process: • main rail lines committees• local collection of complaints from disabled passengers (provisioned in French law)• regular passenger’s perception measure

Linking the commitments of the operators into a sustainable development perspective

Quality of service and passenger rights

Quality of service in the contracts 2008-2011

25

• The PDUIF: a framework document on public transport in Ile-de-France that breaks down into short-term and medium-term operational actions

• A longer period than the current PDUIF so the actions are implemented effectively deadline 2020

• A scope covering all the transit policies (infrastructures, operation, quality of service) in observance of the authorities of the various players

• Strategic objectives that are broken down into region-specific operational actions

• Actions should be evaluated in relation to the planned objectives

• Ongoing monitoring

Selected tools and measures to promote sustainable mobility

The Regional Urban Mobility Plan (PDUIF)

26

• Urban challenges in Ile-de-France – 60,000 housing units built every year– fight against urban sprawl by encouraging urban density in city

centres or population centres in existing urban hubs.• Changes in the energy field

– decreasing supply of fossil fuel,– rising energy prices, – commitments to reduce greenhouse gas emissions

• Changing social expectations– increased awareness of sustainable development– changes in how cars are being used, which is becoming apparent

in Ile-de-France as well as the rest of France• Changes in society and lifestyles

– ageing of the population– patterns and times of transport are changing

Selected tools and measures to promote sustainable mobility

The objectives of the PDUIF: managing the changing context of the transit policy in Ile-de-France

27

Selected tools and measures to promote sustainable mobility

The PDUIF: a technical elaboration process to identify pertinent actions through thematic work groups

Which mobility by 2020 ?

Public Transport: Provision of transportation services

Public Transport: intermodality

Fare scheme

Multimodal passengers information

Car and two-wheel motorized vehicles parking

Operating of the road networks

Road safety

Pedestrians, cycling and sharing of the public space

Living and mobility areas

Link between urban planning and transport

Mobility of the people with disabilities

Mobility management

Taxis and on demand transport

Transport and delivery of goods

Financal needs, new modes of financing, urban toll

Environment

Governance, local implementation, Local Mobility Plans

28

Selected tools and measures to promote sustainable mobility

What is at stake in the PDUIF?

Ensuring the mobility needs of people and goods: According to the different scales of mobility For various motives For all

Reducing environmental nuisances (pollution, greenhouse gases, noise) Improving road safety Improving the quality of life Controlling energy consumption and reducing the dependence on fossil fuels

MOBILITYENVIRONMENT, HEALTH,

QUALITY OF LIFE

In order to ensure this balance today and moreover in the future, we have to: Change the mobility conditions Change our behaviour

The PDUIF must ensure a sustainable balance between the needs of mobility, the protection of environment and health and the financial needs.

This balance shall facilitate the attractiveness of the French region ‘Ile-de-France’ and guarantee the social cohesion.

Ensuring the financial sustainability Identifying the sources of financing for all the actions of the Regional Urban Mobility Plan (RUMP) whatever the scope Looking for efficient measures

FINANCING

Sustainable balance

29

Selected tools and measures to promote sustainable mobility

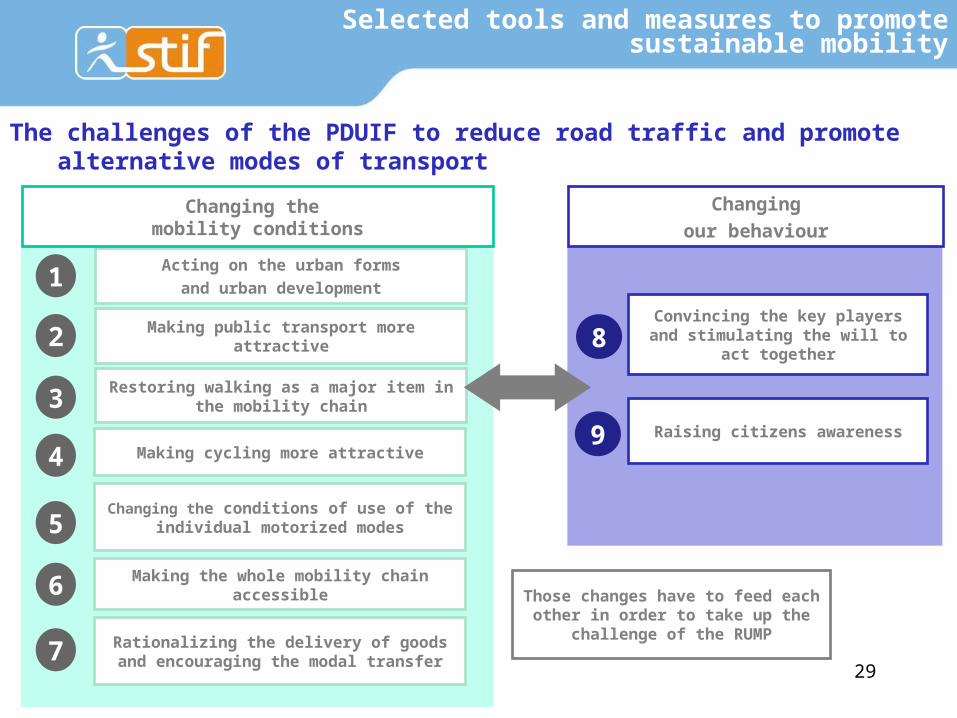

The challenges of the PDUIF to reduce road traffic and promote alternative modes of transport

1Acting on the urban formsand urban development

2 Making public transport more attractive

3 Restoring walking as a major item in the mobility chain

4 Making cycling more attractive

8Convincing the key players

and stimulating the will to act together

9 Raising citizens awareness

5Changing the conditions of use of the

individual motorized modes

Changing the mobility conditions

Changingour behaviour

Those changes have to feed each other in order to take up

the challenge of the RUMP

Making the whole mobility chain accessible6

Rationalizing the delivery of goods and encouraging the modal transfer7

• Increasing the supply and the quality on the existing railway network: Example of time-phasing implemented by STIF since 2007

(€75 Mn/year). There are more trains during off-hours, evenings, week-ends as well as a better regularity

RER (Regional Express Network) Master Plans: upgraded infrastructure and rolling stock, enhancement of the supply (€650 Mn to RER A line; €500 Mn to RER B line; €440 Mn to RER C line; €190 Mn to RER D line)

Reinforcement of the metro supply (peak-hours, off-hours, evenings)

• Offering more performing road services: ‘TZEN’ (new High Level of Service Bus) is a specifically designed

vehicle running on a dedicated lane with real stops; 60 express lines between big urban and economic areas; ‘Mobilien’ regional network of buses (100 lines). Interurban

services and connection with railway network.

30

Actions implemented in favour of a sustainable mobility: improving the supply and the services to passengers

Opinions about different possible measures and their barriers to promote PT

attractiveness

31

Opinions about different possible measures and their barriers to promote PT

attractiveness

Francilien

Tzen

• Enhancement of the hubs within the first PDUIF (Urban Master Plan): Implementation of 100 Committees of intermodal transport hubs

since 2001, 15 projects carried out, 35 underway 50% of the investments are funded by STIF

• Working-out of Master Plans since 2006: Park & Ride (P&R) areas, road stations, passengers information as well as accessibility Sets the levels of service to be reached as well as the Organising

Authority’s financial contribution (200 road stations; 500 P&R areas) Accessibility Master Plan: an investment programme is to be achieved

by 2015 on both railway and bus networks. Budget: €1.8 Bn, of which 50% are funded by STIF

• The new PDUIF (Urban Master Plan): experiencing and encouraging the development of new services Access to P&R areas using the ‘Navigo Pass’ and through carpool;

information about all operators; confirmed correspondence between train and bus; secure bike areas; map of the time needed to go by foot to the stations and stops

32

Actions implemented in favour of a sustainable mobility: intermodality policies

Opinions about different possible measures and their barriers to promote PT

attractiveness

33

Sources and proportions of PT financing

The Regional Urban Mobility Plan (PDUIF) and the sources of funding

• Heavy trucks taxes

• City tolls

• Increase of parking fines (of which 50% go to STIF)

• Fare increases

• Land value capture

34

Thank you for your attention !

EMTA General Meeting15-16 April 2010 in Budapest (Hungary)