Embed Size (px)

Citation preview

1

Financial OptionsFinancial Options

Ch 9

What is a financial option?What is a financial option?

An option is a contract which gives its holder the right, but not the obligation, to buy (or sell) an asset at some predetermined price within a specified period of time.

2

3

Financial Options: Call and Put OptionsFinancial Options: Call and Put Options

Call options gives the holder the right, but not the obligation, to buy a given quantity of some asset at some time in the future, at prices agreed upon today. When exercising a call option, you “call in” the asset.

Put options gives the holder the right, but not the obligation, to sell a given quantity of an asset at some time in the future, at prices agreed upon today. When exercising a put, you “put” the asset to someone.

4

Exercise (or strike) price: The price stated in the option contract at which the security can be bought or sold.

Option price: The market price of the option contract.

Expiration date: The date the option matures. Exercise value: The value of a call or put

option if it were exercised today EV of Call = Max (ST ─ X, 0)

EV of Put = Max (X ─ ST, 0)

Option VocabularyOption Vocabulary

5

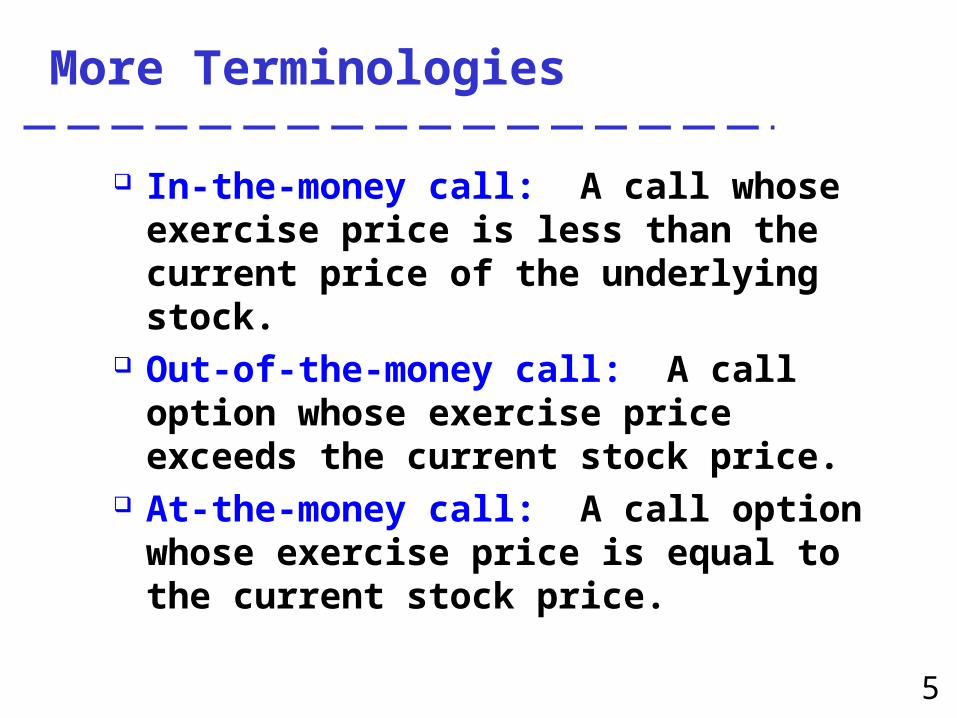

In-the-money call: A call whose exercise price is less than the current price of the underlying stock.

Out-of-the-money call: A call option whose exercise price exceeds the current stock price.

At-the-money call: A call option whose exercise price is equal to the current stock price.

More Terminologies

6

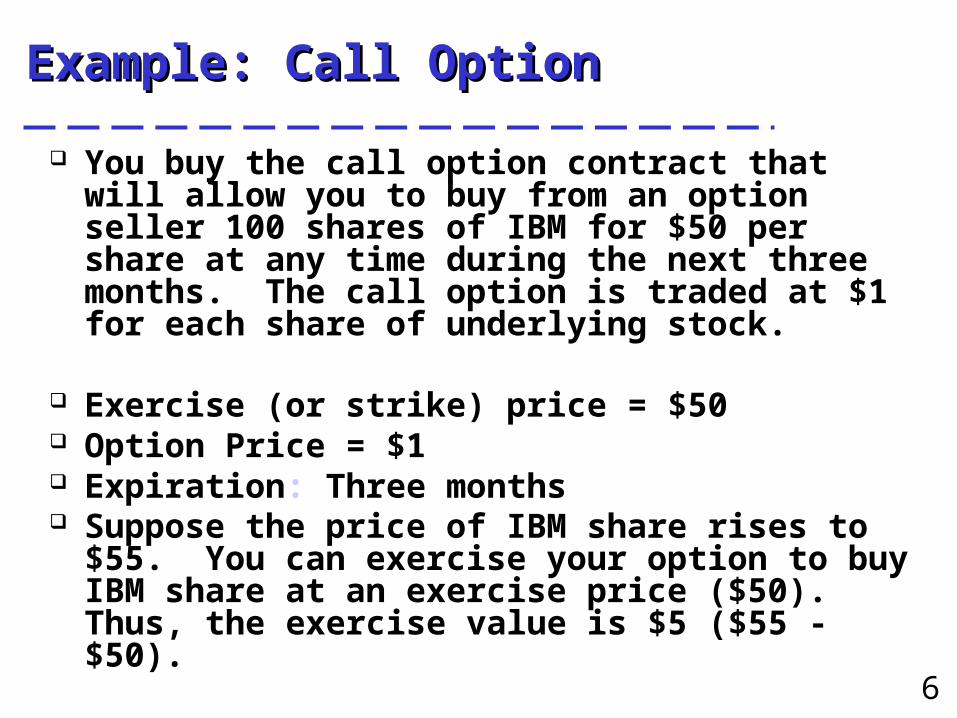

Example: Call OptionExample: Call Option

You buy the call option contract that will allow you to buy from an option seller 100 shares of IBM for $50 per share at any time during the next three months. The call option is traded at $1 for each share of underlying stock.

Exercise (or strike) price = $50 Option Price = $1 Expiration: Three months Suppose the price of IBM share rises to $55. You

can exercise your option to buy IBM share at an exercise price ($50). Thus, the exercise value is $5 ($55 - $50).

7

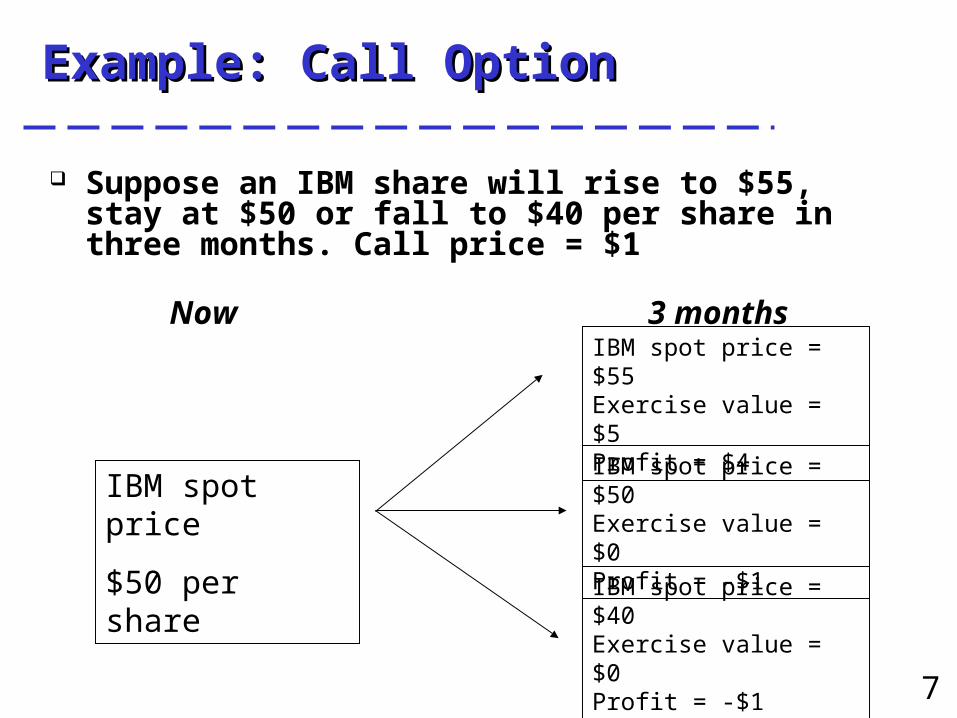

Example: Call OptionExample: Call Option

Suppose an IBM share will rise to $55, stay at $50 or fall to $40 per share in three months. Call price = $1

IBM spot price

$50 per share

IBM spot price = $55 Exercise value = $5Profit = $4

Now 3 months

IBM spot price = $50 Exercise value = $0Profit = -$1

IBM spot price = $40 Exercise value = $0Profit = -$1

8

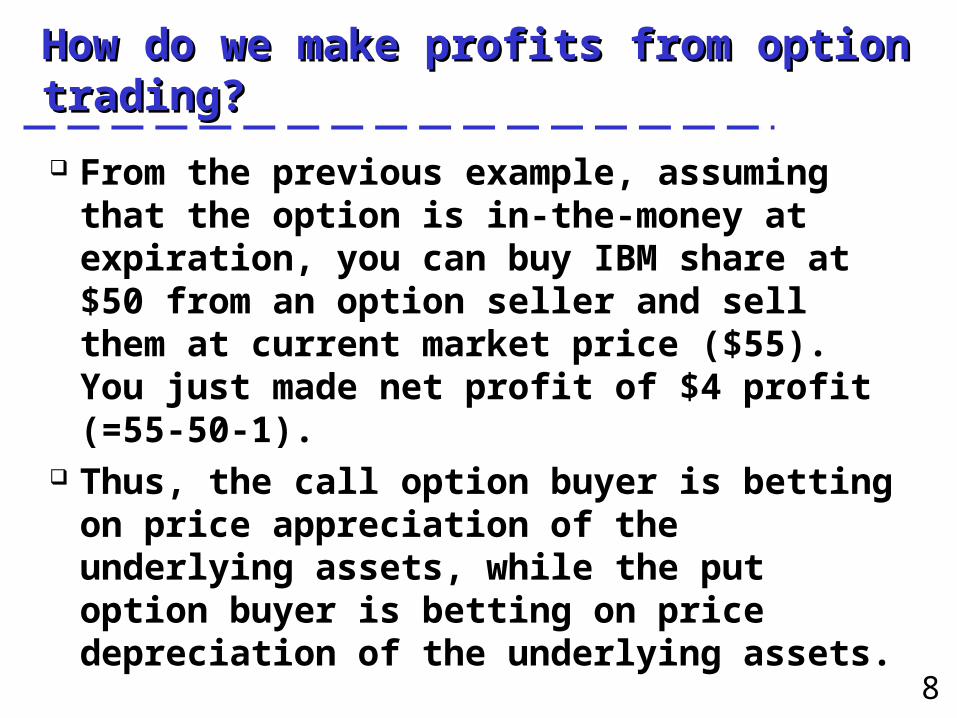

How do we make profits from option How do we make profits from option trading?trading?

From the previous example, assuming that the option is in-the-money at expiration, you can buy IBM share at $50 from an option seller and sell them at current market price ($55). You just made net profit of $4 profit (=55-50-1).

Thus, the call option buyer is betting on price appreciation of the underlying assets, while the put option buyer is betting on price depreciation of the underlying assets.

9

How do we lose money from option trading?How do we lose money from option trading?

From the previous example, suppose IBM shares never rises above $50. Then your option expires worthless, so you lose an entire option price ($1).

10

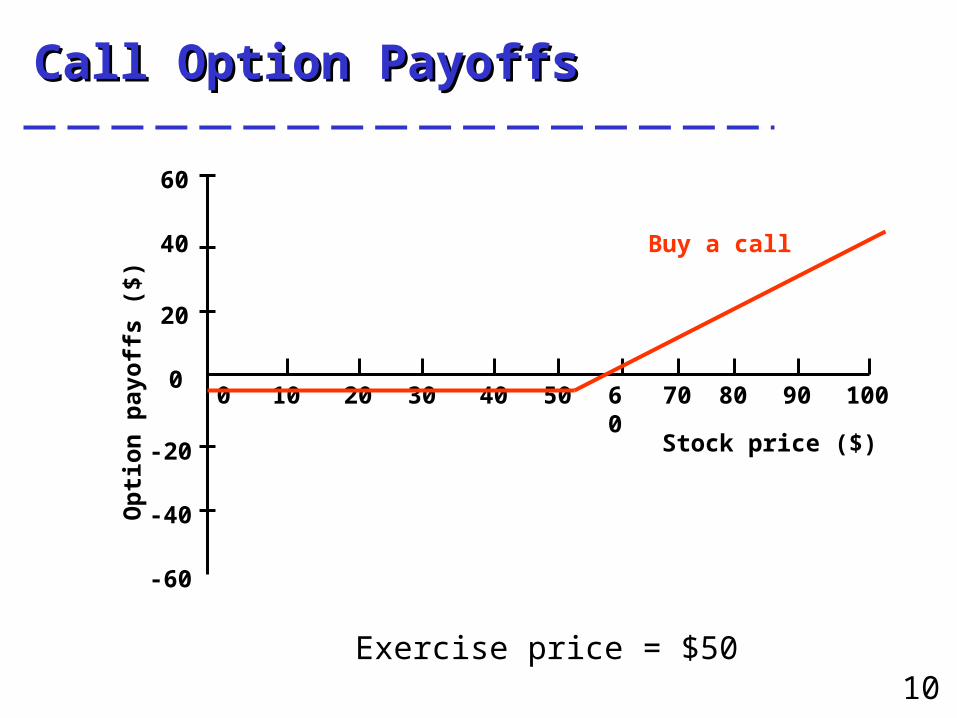

Call Option PayoffsCall Option Payoffs

-20

100908070600 10 20 30 40 50

-40

20

0

-60

40

60

Stock price ($)

Op

tio

n p

ayo

ffs

($)

Buy a call

Exercise price = $50

11

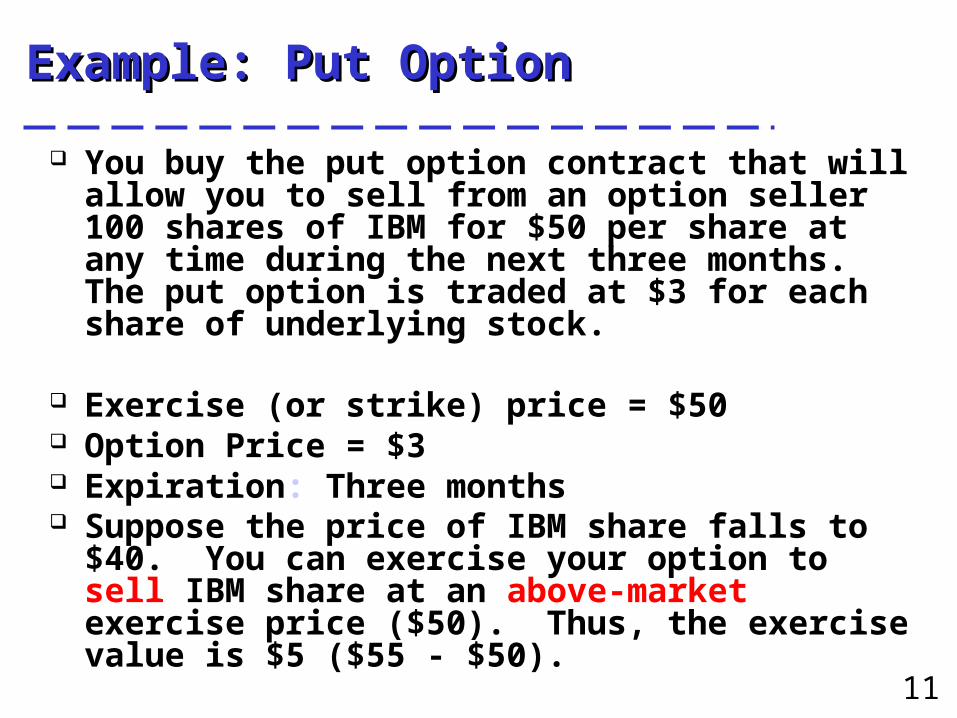

Example: Put OptionExample: Put Option

You buy the put option contract that will allow you to sell from an option seller 100 shares of IBM for $50 per share at any time during the next three months. The put option is traded at $3 for each share of underlying stock.

Exercise (or strike) price = $50 Option Price = $3 Expiration: Three months Suppose the price of IBM share falls to $40. You

can exercise your option to sell IBM share at an above-market exercise price ($50). Thus, the exercise value is $5 ($55 - $50).

12

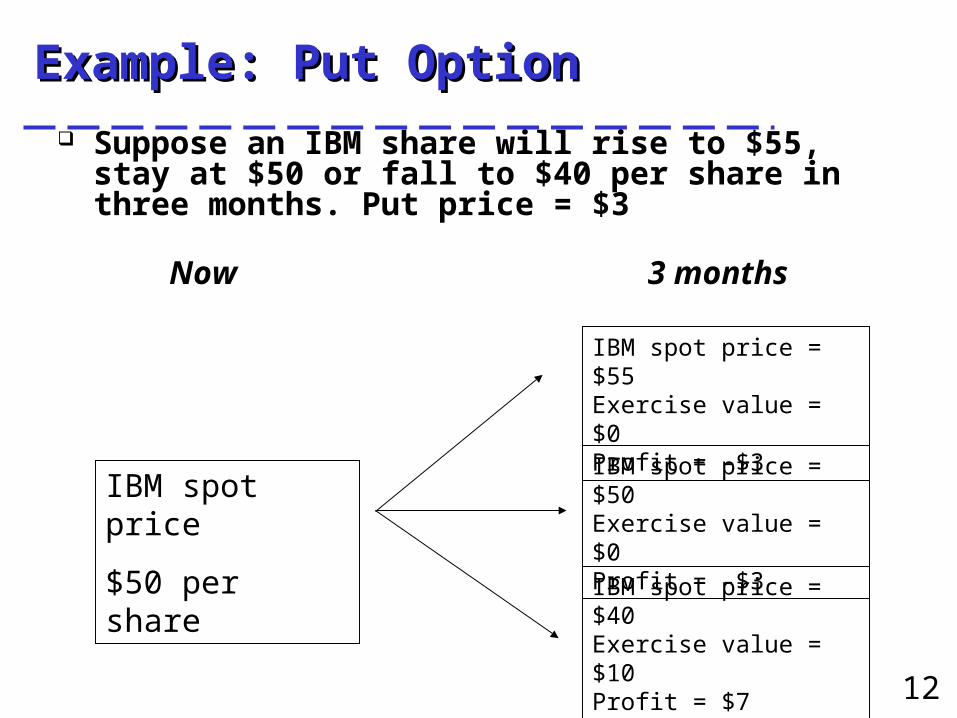

Example: Put OptionExample: Put Option

Suppose an IBM share will rise to $55, stay at $50 or fall to $40 per share in three months. Put price = $3

Now 3 months

IBM spot price

$50 per share

IBM spot price = $55 Exercise value = $0Profit = -$3

IBM spot price = $50 Exercise value = $0Profit = -$3

IBM spot price = $40 Exercise value = $10Profit = $7

13

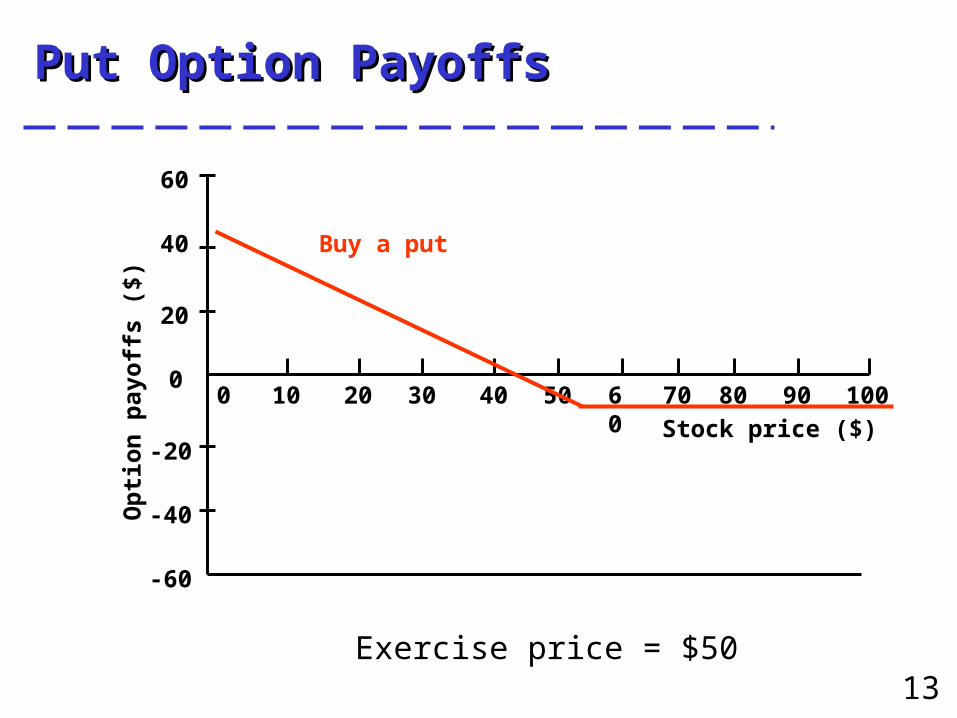

Put Option PayoffsPut Option Payoffs

-20

100908070600 10 20 30 40 50

-40

20

0

-60

40

60

Stock price ($)

Op

tio

n p

ayo

ffs

($)

Buy a put

Exercise price = $50

14

Reading Reading The Wall Street JournalThe Wall Street Journal

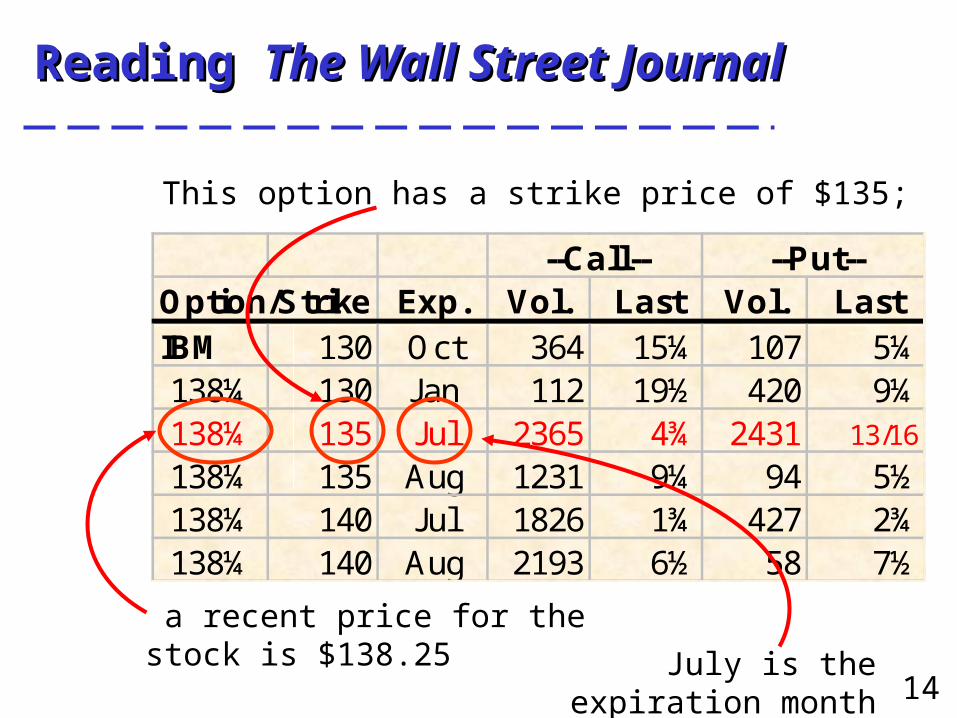

Option/Strike Exp. Vol. Last Vol. LastIBM 130 Oct 364 15¼ 107 5¼138¼ 130 Jan 112 19½ 420 9¼138¼ 135 Jul 2365 4¾ 2431 13/16

138¼ 135 Aug 1231 9¼ 94 5½138¼ 140 Jul 1826 1¾ 427 2¾138¼ 140 Aug 2193 6½ 58 7½

--Put----Call--

This option has a strike price of $135;

a recent price for the stock is $138.25

July is the expiration month

15

Reading Reading The Wall Street JournalThe Wall Street Journal

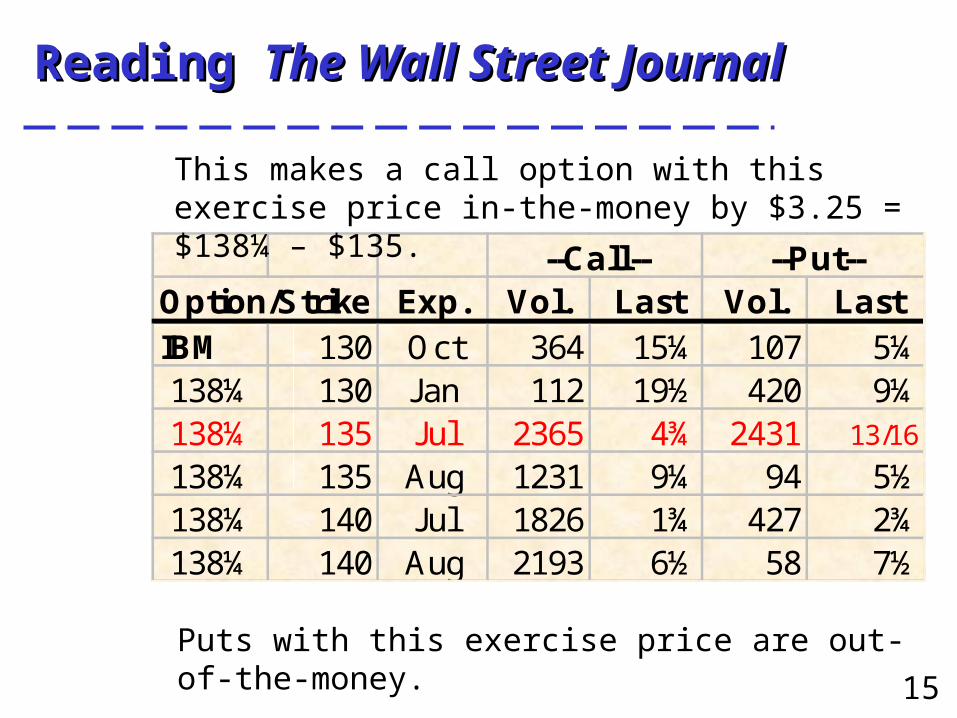

Option/Strike Exp. Vol. Last Vol. LastIBM 130 Oct 364 15¼ 107 5¼138¼ 130 Jan 112 19½ 420 9¼138¼ 135 Jul 2365 4¾ 2431 13/16

138¼ 135 Aug 1231 9¼ 94 5½138¼ 140 Jul 1826 1¾ 427 2¾138¼ 140 Aug 2193 6½ 58 7½

--Put----Call--

This makes a call option with this exercise price in-the-money by $3.25 = $138¼ – $135.

Puts with this exercise price are out-of-the-money.

16

Reading Reading The Wall Street JournalThe Wall Street Journal

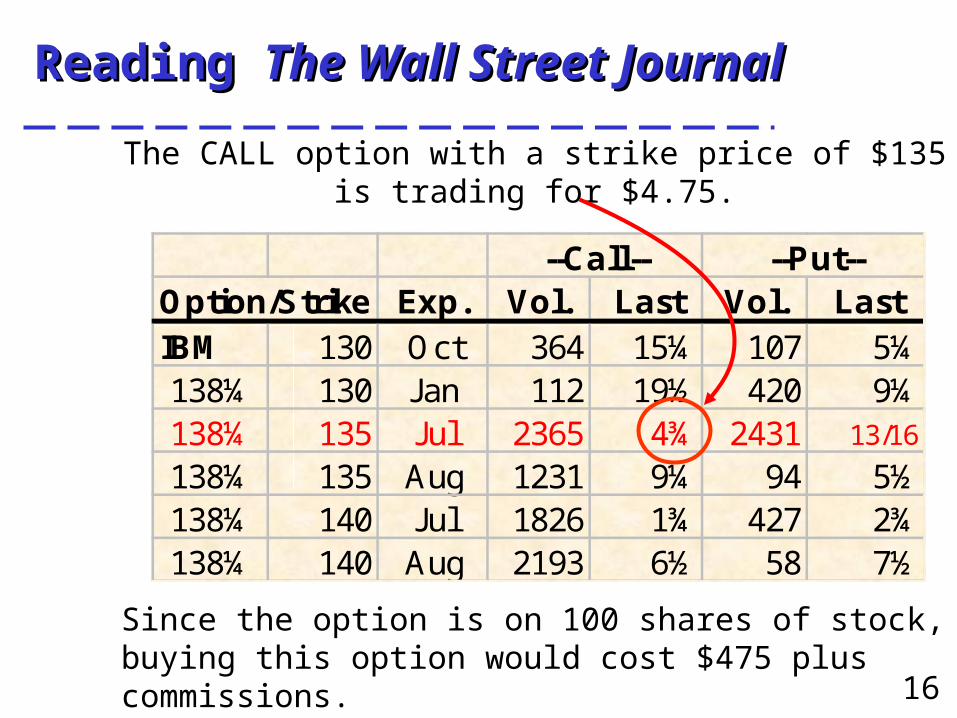

Option/Strike Exp. Vol. Last Vol. LastIBM 130 Oct 364 15¼ 107 5¼138¼ 130 Jan 112 19½ 420 9¼138¼ 135 Jul 2365 4¾ 2431 13/16

138¼ 135 Aug 1231 9¼ 94 5½138¼ 140 Jul 1826 1¾ 427 2¾138¼ 140 Aug 2193 6½ 58 7½

--Put----Call--

The CALL option with a strike price of $135 is trading for $4.75.

Since the option is on 100 shares of stock, buying this option would cost $475 plus commissions.

17

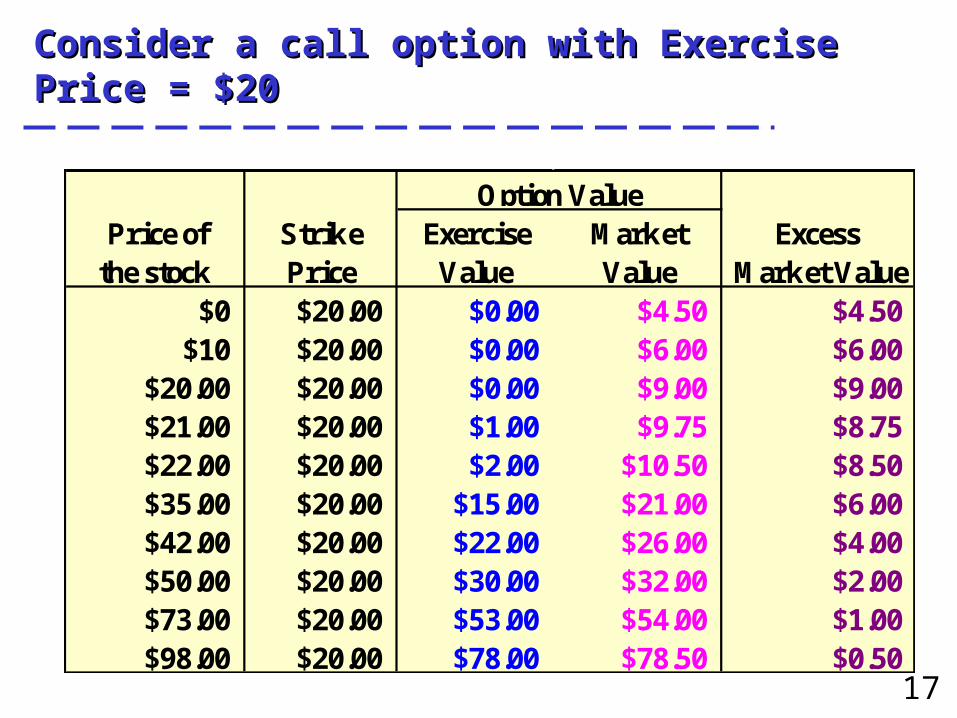

Consider a call option with Exercise Price = $20Consider a call option with Exercise Price = $20

Price of Strike Exercise Market Excess the stock Price Value Value Market Value

$0 $20.00 $0.00 $4.50 $4.50$10 $20.00 $0.00 $6.00 $6.00

$20.00 $20.00 $0.00 $9.00 $9.00$21.00 $20.00 $1.00 $9.75 $8.75$22.00 $20.00 $2.00 $10.50 $8.50$35.00 $20.00 $15.00 $21.00 $6.00$42.00 $20.00 $22.00 $26.00 $4.00$50.00 $20.00 $30.00 $32.00 $2.00$73.00 $20.00 $53.00 $54.00 $1.00$98.00 $20.00 $78.00 $78.50 $0.50

Option Value

18

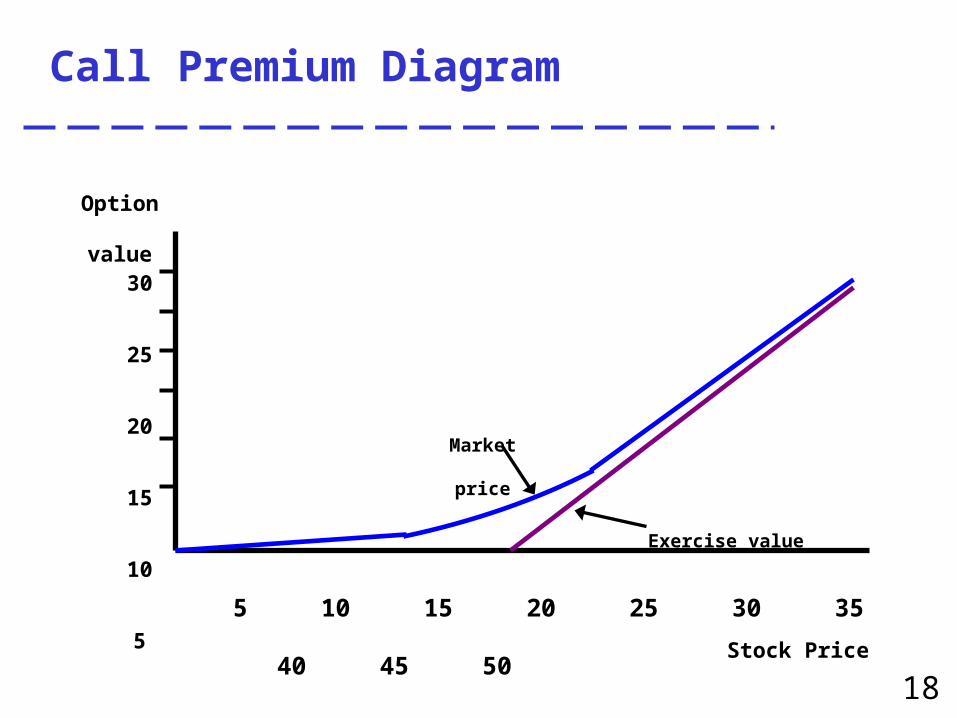

Call Premium Diagram

5 10 15 20 25 30 35 40 45 50

Stock Price

Option value

30

25

20

15

10

5

Market price

Exercise value

19

Why buying financial options is very risky Why buying financial options is very risky way to invest for individual investors?way to invest for individual investors?

Shorter-term investment, although LEAPs are introduced recently.LEAPs: Long-term Equity AnticiPation securities

that are similar to conventional options except that they are long-term options with maturities of up to 2 1/2 years.

High commission rate High level of volatility

20

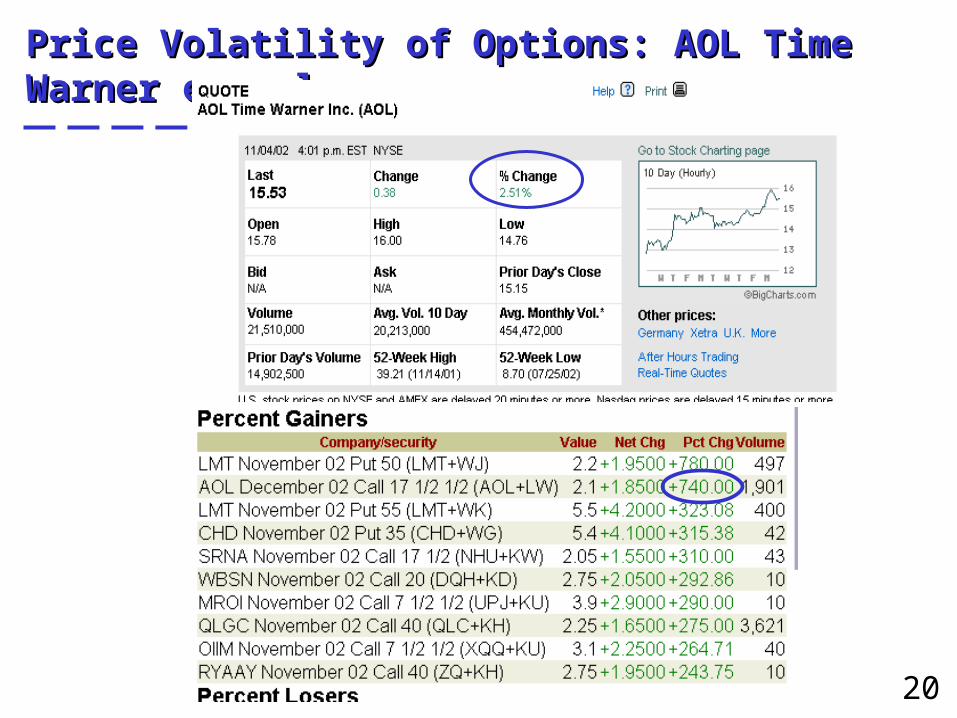

Price Volatility of Options: AOL Time Warner Price Volatility of Options: AOL Time Warner exampleexample

21

Is there any scientific way to derive the price Is there any scientific way to derive the price of options?of options?

Yes. The Black-Scholes Option Pricing Model.

22

Originally developed in the early 1970s By Black and Scholes and later refined

by Merton. Equity option, index option, foreign

currency option, interest rate option, etc

Five inputs: current stock price, exercise price, risk-free rate, maturity, volatility of the underlying asset

Visit Chicago Board of Options Exchange (www.cboe.com)

Black-Scholes Option Pricing Model

23

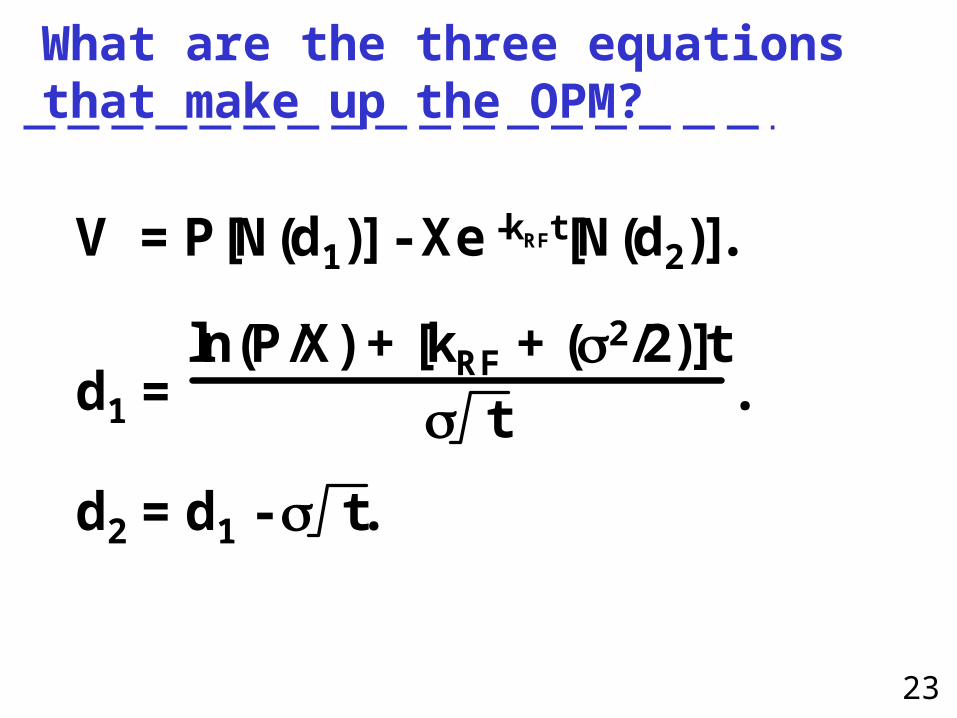

What are the three equations that make up the OPM?

V = P[N(d1)] - Xe -kRFt[N(d2)].

d1 = . t

d2 = d1 - t.

ln(P/X) + [kRF + (2/2)]t

24

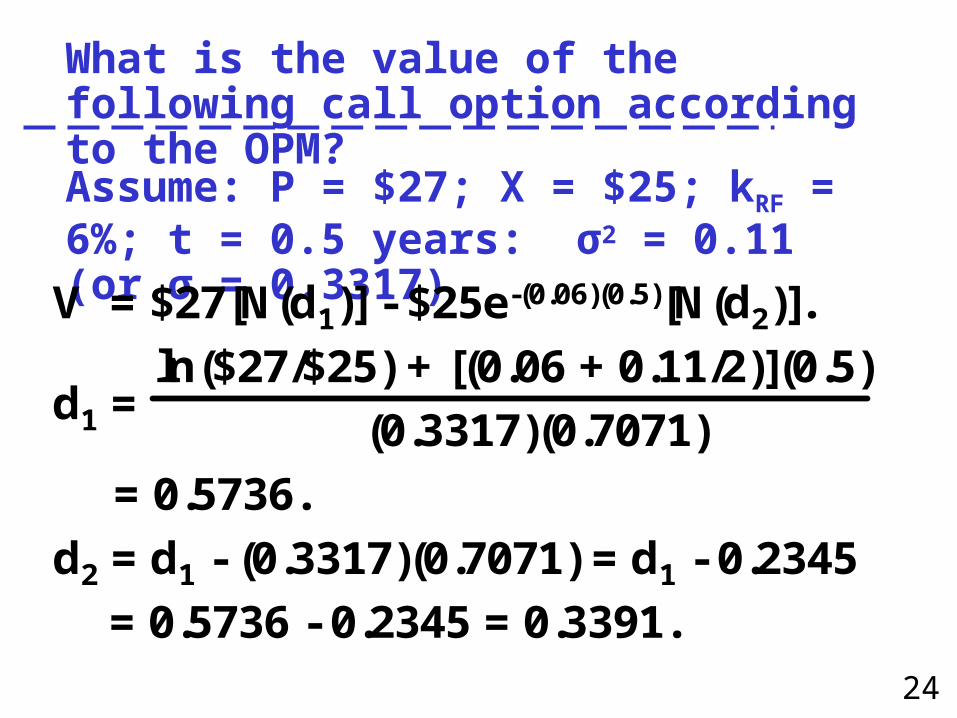

What is the value of the following call option according to the OPM?Assume: P = $27; X = $25; kRF = 6%; t = 0.5 years: σ2 = 0.11 (or σ = 0.3317)

V = $27[N(d1)] - $25e-(0.06)(0.5)[N(d2)].

ln($27/$25) + [(0.06 + 0.11/2)](0.5)

(0.3317)(0.7071)

= 0.5736.

d2 = d1 - (0.3317)(0.7071) = d1 - 0.2345

= 0.5736 - 0.2345 = 0.3391.

d1 =

25

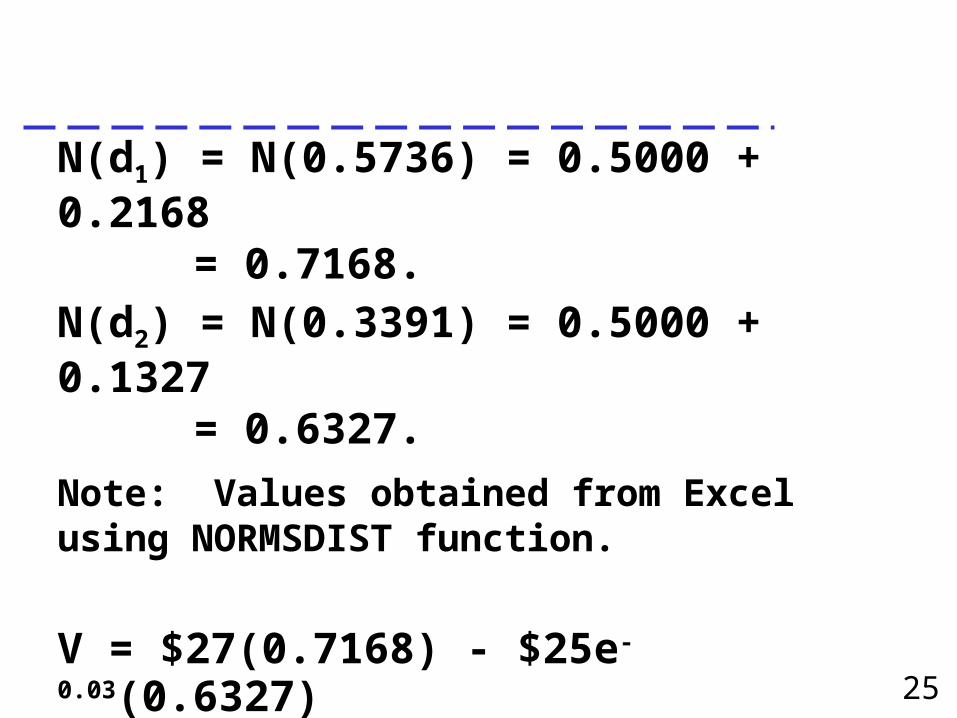

N(d1) = N(0.5736) = 0.5000 + 0.2168 = 0.7168.

N(d2) = N(0.3391) = 0.5000 + 0.1327 = 0.6327.

Note: Values obtained from Excel using NORMSDIST function.

V = $27(0.7168) - $25e-0.03(0.6327) = $19.3536 - $25(0.97045)(0.6327) = $4.0036.

26

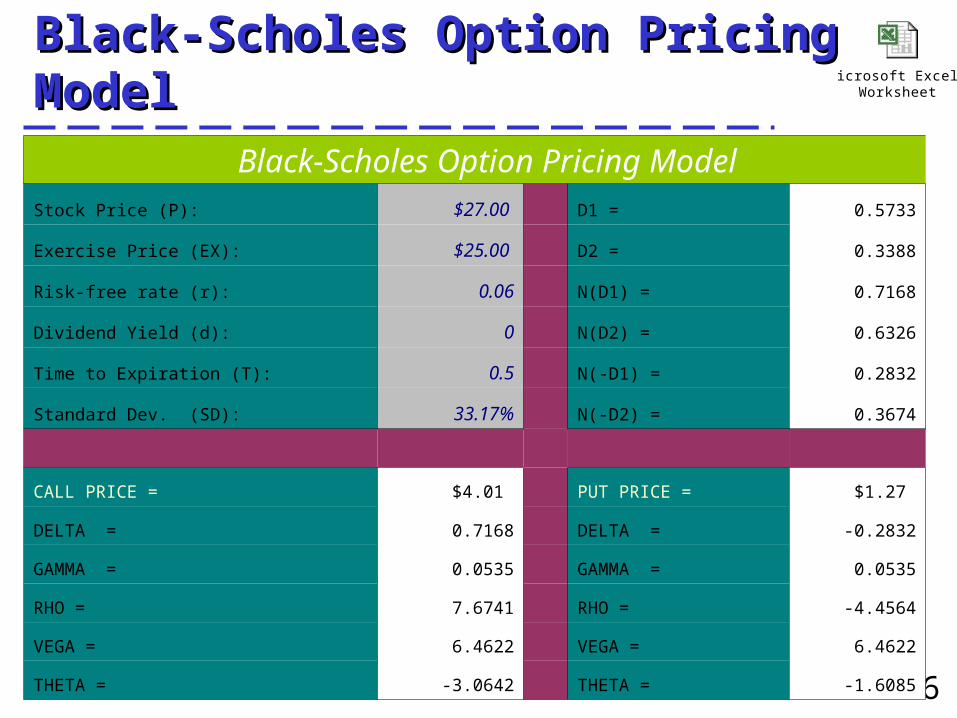

Black-Scholes Option Pricing ModelBlack-Scholes Option Pricing Model

Black-Scholes Option Pricing ModelStock Price (P): $27.00 D1 = 0.5733

Exercise Price (EX): $25.00 D2 = 0.3388

Risk-free rate (r): 0.06 N(D1) = 0.7168

Dividend Yield (d): 0 N(D2) = 0.6326

Time to Expiration (T): 0.5 N(-D1) = 0.2832

Standard Dev. (SD): 33.17% N(-D2) = 0.3674

CALL PRICE = $4.01 PUT PRICE = $1.27

DELTA = 0.7168 DELTA = -0.2832

GAMMA = 0.0535 GAMMA = 0.0535

RHO = 7.6741 RHO = -4.4564

VEGA = 6.4622 VEGA = 6.4622

THETA = -3.0642 THETA = -1.6085

Microsoft Excel Worksheet

27

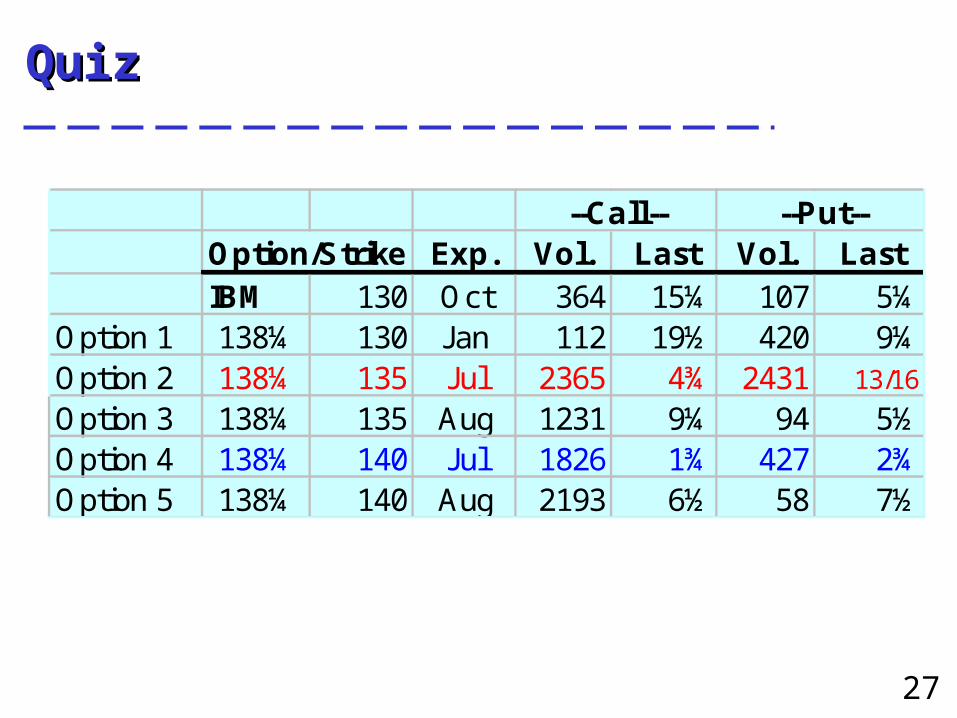

QuizQuiz

Option/Strike Exp. Vol. Last Vol. LastIBM 130 Oct 364 15¼ 107 5¼

Option 1 138¼ 130 Jan 112 19½ 420 9¼Option 2 138¼ 135 Jul 2365 4¾ 2431 13/16

Option 3 138¼ 135 Aug 1231 9¼ 94 5½Option 4 138¼ 140 Jul 1826 1¾ 427 2¾Option 5 138¼ 140 Aug 2193 6½ 58 7½

--Put----Call--

28

QuizQuiz

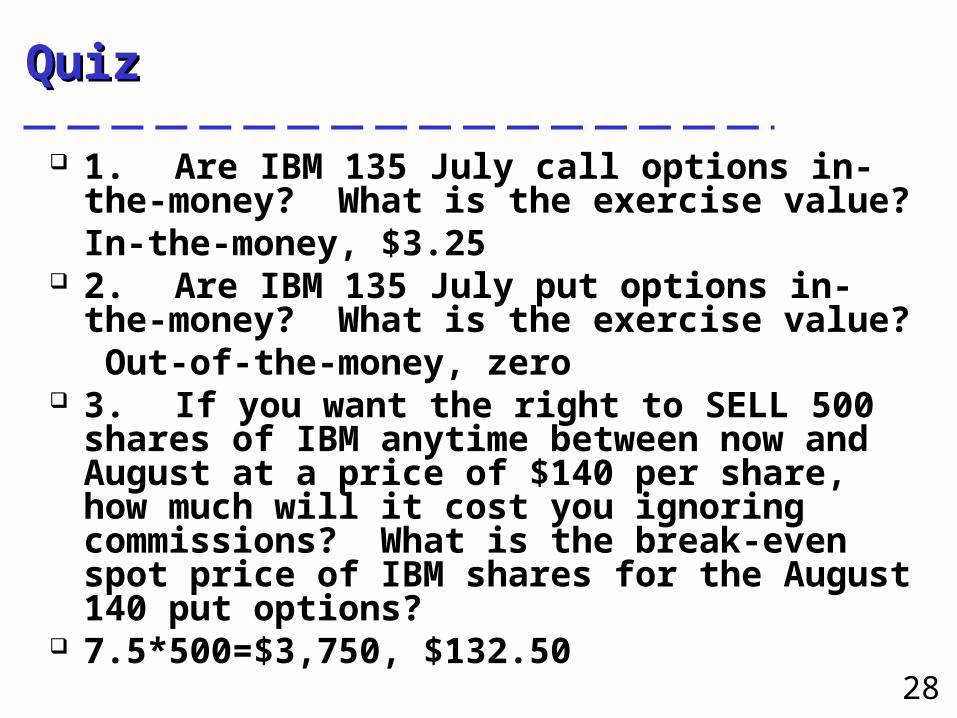

1. Are IBM 135 July call options in-the-money? What is the exercise value?

In-the-money, $3.25 2. Are IBM 135 July put options in-the-

money? What is the exercise value? Out-of-the-money, zero

3. If you want the right to SELL 500 shares of IBM anytime between now and August at a price of $140 per share, how much will it cost you ignoring commissions? What is the break-even spot price of IBM shares for the August 140 put options?

7.5*500=$3,750, $132.50

29

4. Suppose you buy one August 140 IBM put option? What is the maximum gain? What is the net gain if a share of IBM stocks is selling at 132 ½ on the expiration date? What is the net gain or loss if IBM is selling at 140 on the expiration date?

$13,250, Zero -$750

30

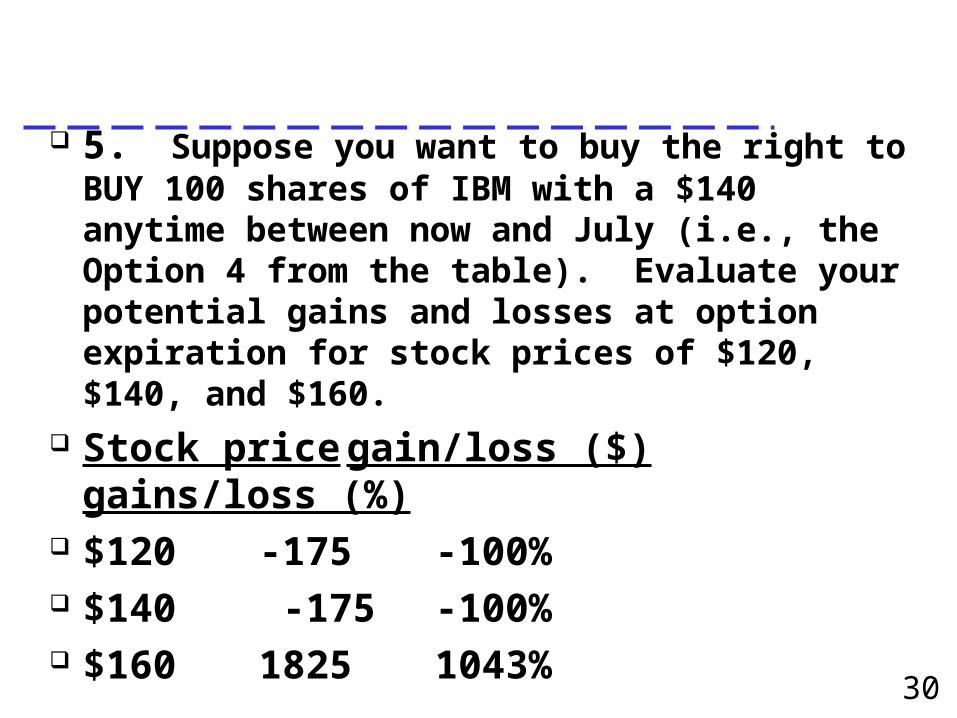

5. Suppose you want to buy the right to BUY 100 shares of IBM with a $140 anytime between now and July (i.e., the Option 4 from the table). Evaluate your potential gains and losses at option expiration for stock prices of $120, $140, and $160.

Stock price gain/loss ($) gains/loss (%)

$120 -175 -100% $140 -175 -100% $160 1825 1043%

31

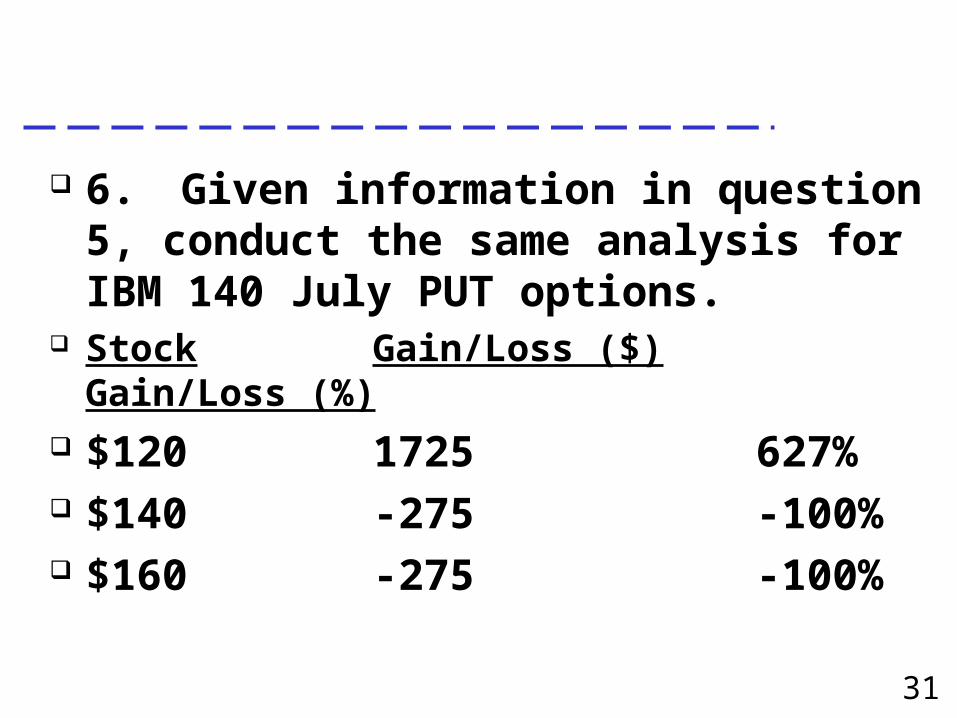

6. Given information in question 5, conduct the same analysis for IBM 140 July PUT options.

Stock Gain/Loss ($) Gain/Loss (%) $120 1725 627% $140 -275 -100% $160 -275 -100%

32

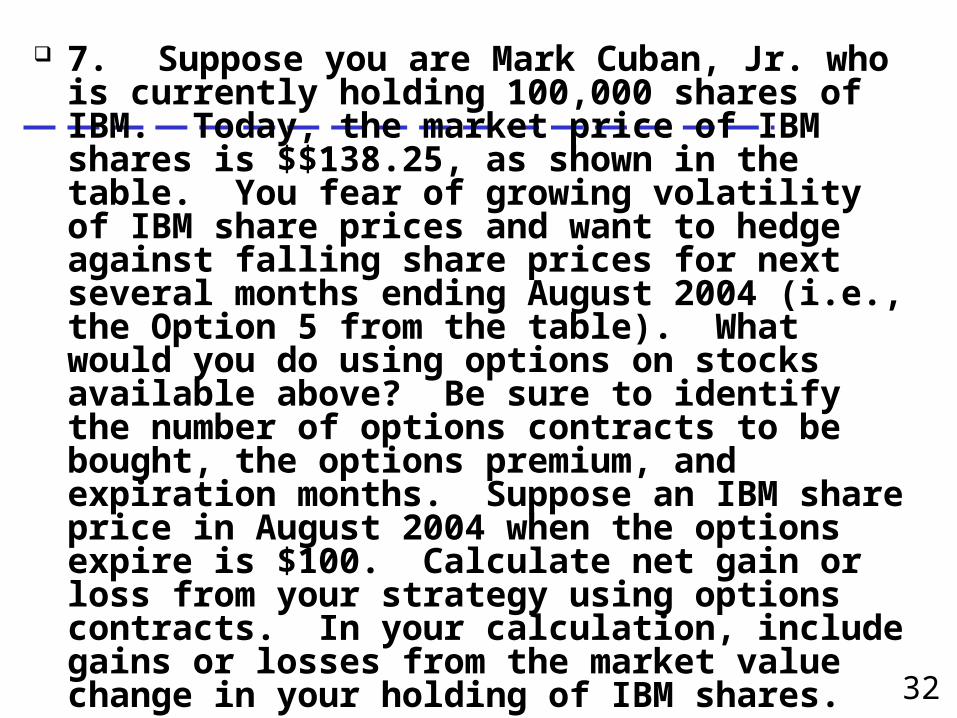

7. Suppose you are Mark Cuban, Jr. who is currently holding 100,000 shares of IBM. Today, the market price of IBM shares is $$138.25, as shown in the table. You fear of growing volatility of IBM share prices and want to hedge against falling share prices for next several months ending August 2004 (i.e., the Option 5 from the table). What would you do using options on stocks available above? Be sure to identify the number of options contracts to be bought, the options premium, and expiration months. Suppose an IBM share price in August 2004 when the options expire is $100. Calculate net gain or loss from your strategy using options contracts. In your calculation, include gains or losses from the market value change in your holding of IBM shares.